RDC Risk Management & FFIEC Compliance May 2010 Update

|

|

|

- Susan Isabel Reed

- 6 years ago

- Views:

Transcription

1 RDC Risk Management & FFIEC Compliance May 2010 Update Presented By: John Leekley, CEO and Co-Founder Ed McLaughlin, Executive Director RemoteDepositCapture.com May 2010

872-7882 email: victoria.lant@fiserv.")

2 Today s Webinar is Brought to you in part by Source Capture Optimization An industry leading, web-based approach to Remote Deposit Capture from any point of check presentment: consumer, small business, merchant, corporate, branch, teller and ATM. Visit to learn more. call (800) victoria.lant@fiserv.com FIS is the world's top-ranked technology provider to the banking industry. With more than 24,000 experts in 100 countries, FIS delivers the most comprehensive range of check processing solutions, including outsourced and turnkey enterprise platform solutions for the broadest range of financial markets, all with a singular focus: helping you succeed. Our breadth of distributed capture solutions include branch capture, teller capture, vault capture, business remote deposit and consumer remote deposit. Every FIS solution has the strength you need for profitability today, and the power to help you manage whatever comes next. For more information about FIS visit 2

3 Discussion Objectives FFIEC Update Examiner Handbook (February 2010) BSA / AML (April 29, 2010) Confusion & Clarification Site Visits: Required or not? KYC: What does this mean? Pricing, Underwriting & Reserves are they really necessary? Fact vs. Fiction: What are the Real Risks? Discussion of Actual Fraud Risk Mitigation RDC Risk Management Best Practices RDC Risk Management Evolution Legal Disclaimer: This is not legal advice. RemoteDepositCapture.com is reporting on observations and experiences while working directly with solution providers, financial institutions and the various regulatory agencies. For legal advice / guidance, please work with a competent and qualified legal representative. 3

4 Regulatory Guidance Overview 1. FFIEC RDC Risk Management Guidance released January 14, 2009 RDC risk management process in an electronic environment Focusing on RDC deployed at a customer location Principles of RDC risk management discussed are applicable to: FI s Internal deployment ATM, Branch, Cash Vault Other forms of electronic deposit delivery systems (e.g., mobile banking and automated clearing house [ACH] check conversions). 2. Retail Payment Systems Booklet (N), (M) February 10, Version of the Bank Secrecy Act/Anti-Money Laundering Examination Manual Updated April 29,

5 Three Pillars of the FFIEC Guidance Responsibility Senior Management Board Risk Identification & Assessment Internal External Process Mitigation & Controls Planning Measure Monitor Report Risk Identification 5

6 RDC is a Delivery System RDC is a Payments & Data Processing & Delivery System Scope of implementation and exposure Should be incorporated into existing risk management process Governance, Oversight & Tactics will, and should, vary by institution Non-Public Personal Information Complexity of Risk Identification will vary Internal IT systems, Third-Party Solution Providers Involve relevant stakeholders FFIEC Guidance Mitigate Monitor Measure Actionability & Sustainability 6

7 Risk Environment Identification Identify Key elements of the RDC environment Internal Third-Party Customer Identify Responsible staff members and risk management team Internal Staff: Product Manager, Risk, Treasury, Sales, etc External: Technology Provider, Processor, etc. Review: Volume reports ($ s and Transactions) Network design at the FI, Service provider and customer Dataflow maps and logical system diagrams The risk management process Report review process Establish Relevant Contracts & Agreements 7

Product Management Cash Management Sales IT - Application Development IT -")

8 Which Resources are Required? Remote Deposit Capture Implementation Stakeholders Area Senior Management Project Management Office (PMO) Product Management Cash Management Sales IT - Application Development IT - Infrastructure/Operations IT Security Audit HR/Training Procurement/Vendor Management Operations (ACH, Day1, Day 2, Lockbox) Risk / Compliance Finance & Treasury Deposits are the lifeblood of any financial institution. RDC impacts almost all areas within an FI. Source; Catalyst Consulting, RemoteDepositCapture.com 8

9 Internal Risk Assessment Scope Clients / Channels: Merchant, Business, Consumer, Branch, ATM, Correspondent, etc. Devices: MICR, TWAIN, Mobile, etc. Locations domestic and international ICL (Image Cash Letter) use and location of originators Risks & Responsibilities as BOFD or Correspondent, etc. Customer Documentation: Roles & Responsibilities Non-Public Information Customer reports what is included and if NPI (Non Public information) is it highlighted as such Technology and service providers Clearing and settlement channels (ACH, Image, IRD) Integration into BCP, AML/BSA, OFAC, Enterprise Information Security, Customer Support (help desk) 9

10 Key Information: Understand Business Know Your Customer Finances, Customers, Processes Understand Deposits Obtain History Volumes & Values of Items, deposits, returns, Velocity Use this data to custom-fit RDC Thresholds, Limits, Holds & Availability Schedules Separation of Duties, Approvals Functional Capabilities Pricing, Balances, monitor deposit & data trends. RDC Should be customized to each individual client. 10

IQA and IUA MICR & CAR/LAR Controls Clearing")

IT")

11 System Capabilities & Integration System Functionality Duplicate item detection Scanner options Data Integration & Usability Audit logs and event logs (MIS reporting) IQA and IUA MICR & CAR/LAR Controls Clearing options LCR (lowest cost routing) Includes rules for ACH vs.. Image and IRD ABA Validation routines Integration of BSA/AML systems and processes OFAC BCP (Enterprise) IT Security Infrastructure (SSO, rights and privileges, etc.) 11

12 Risk Management Duplicate Detection Duplicate Detection should ideally be done across all levels & accounts, channels and products. Levels & Accounts User, Location, Account Channels RDC Location, Lockbox, ATM, Branch, Mail Drop, Kiosk & Inclearings, etc. Products Check and ACH (for converted items) Network All banks using a specific service provider Industry i3g / Fed Initiative 12

13 Risk Parameter Settings Use KYC to Customize Risk Management Daily Limits Value Limits Volume Limits Item Limits Source: FIS 13

14 Validation Rules and Work Types Define Systemic Rules & Thresholds Image Quality Field Validation Item type acceptance Balancing Rules Target Functionality by Client Group Excellent Customers New Customers Risky Customers Source: Fiserv 14

15 Risk Management Process Supervision, Monitoring and Reporting Review strategic planning documents and implementation procedures Board approval minutes and date Review key objectives in installing RDC Offensive or defensive maintain customer deposits attract new customer deposits, geographic Merchant Commercial customers, Consumer customers Mobile as a capture device Implementation model and service or technology supplier model Records management and customer compliance with established guidelines Physical and logical security Accountability separation of duties 15

16 Oversight and Monitoring Locations Financial institution Vendor Customer Operational benchmarks Key risk metrics Performance metrics Management Review Who and how Frequency &Timeliness Accurate Point-in-time Trend RDC Product Individual customer Aggregate customers Type of Reports 16

17 Vendor Management Selecting the Right Solution Provider Deployment Options In-House ASP / Hosted View Webinar: Hosted vs. In-House Solutions Is vendor included in the Vendor Management Program Is RDC a Core Capability? Financial Stability Systemic Capabilities Strategic Fit for your organization Service Level Agreements Processing Timeliness, Bandwidth, Uptime Cutoffs, Reviews, Data Entry Help Desk Roles & Responsibilities Liabilities / Indemnity & Insurance Any customers using a 3 rd party RDC processor Security, Accessibility & Reliability SAS 70 Type II Certification Issue Resolution, Reporting Process / System Monitoring & Confirmations 17

18 Physical and Logical Access Customer location Physical Building security RDC System security Check storage Equipment security computers, scanners and software Offsite storage security and transportation if used Logical Encryption of local area networks, transmission and data storage Multifactor or strong authentication Access level controls Password security procedures strong passwords Equipment enrollment scanner management (SN), Software (Unique ID), Mobile device registration etc.) 18

and send deposits or for review of reports of deposits sent and for reconciliation.")

19 Separation of Duties Split responsibilities and procedures for: Account set up and Deposit review, approvals and reconciliation at the FI System security review procedures At the customer location separation of duties Capture (scan) and send deposits or for review of reports of deposits sent and for reconciliation. Other controls 19

20 BSA / AML & OFAC New (April / May 2010) update to the Bank Secrecy Act/ Anti-Money Laundering Examination Manual New RDC Highlights 1. Senior management should identify BSA/AML, operational, information security, compliance, legal, and reputation risks. 2. Conducting appropriate customer CDD and EDD. 3. Obtaining expected account activity. Case Studies: Wachovia: $160MM Fine Dallas Community Bank, T-Bank: $5.1MM RDC must be integrated into a bank s AML / BSA risk management and reporting activities. 20

21 Systemic & Targeted Risk Management Systemic Risk Management Enterprise Risk Management AML / BSA / Payment Validation & Reporting System-Wide Risk Management Duplicate Detection, Image Quality / Usability Reporting & Audit Functionality Legal Agreements Targeted Risk Management Trend Analysis & Patterning Item / User Limits & Thresholds Holds, Availability, Balance Requirements, Customer Selection, etc. Optimal RDC Risk Management should be tailored to each end-user, location and device, yet leverage system and enterprise risk management capabilities. 21

22 Education & Training Education & Training FI associates and customers Most customers will want to protect themselves System Operation & Process Safekeeping & Destruction of original items Risks & the role of the customer and the FI Duplicate Presentment Information & Data Problem Resolution Periodic s or letters to customers to remind them of their responsibilities for: training, security, process, check retention, endorsements, adequate safeguards for storage of checks and account information 22

23 Business Continuity Planning (BCP) Enterprise-wide BCP Consider Service Provider Customer service Contractual requirements Periodic testing With customers With service providers Customer contingency plans Plan for Change & Continuous Compliance Change Management Records Management 23

24 RDC Deposit Fraud Prevalent RDC Losses Definition: Process by which criminal is able to deposit the same legitimate or fraudulent item at several FIs, then withdraws the funds before items are returned. Criminals Look For Minimal KYC No Balance Requirement No Holds Immediate Availability No / High $$$ Limits Risk Management Beware of Customers who don t keep balances. Require Balances! Holds on New Customers, High $$$ Availability Schedules $$$ Thresholds 24

25 Testing Risk Management Risk Control / Risk Type Operational Error Check Kiting Duplicate Error Duplicate Fraud Value Fraud Volume Fraud Return Items Value / Volume Thresholds - RDC System DD* *Duplicate Detection Cross-Channel DD* *Duplicate Detection IQA / IQU / CAR / LAR Patterning Holds Availability Schedules Balances Level of Risk Management Adequacy: ¼ Circle = Minimal ½ Circle = Fair ¾ Circle = Moderate Full Circle = Good FIs should have at least 1.5 Total Circles per risk type, 2+ for Fraud Risk Types. 25

26 Recourse is Essential In the worst-case scenario, how can the FI retrieve funds? Availability Schedules Key: Provide availability to account for potential returns based upon Client Risk Profile. Required Balances Key: Can enable FI to actually earn more revenues while also providing a reserve against returns. Adds to Deposits, Capital, Liquidity, Loan Capabilities. Credit Relationship? Interesting concept, but does not enable FI to have access to funds. Customer already owes FI $$$. Insurance & Indemnity 26

27 Optimal Risk Management 10 Steps to Minimize RDC Risk: 1. Client Selection / KYC - Use Information to setup parameters. 2. User / Location / Account Parameters - Identify & Prevent Fraud & Mistakes, manage exceptions 3. Education & Training - Most customers will want to protect themselves. 4. Functionality Restrictions Minimize Fraud Opportunities. 5. Availability Schedules & Holds - Don t make short-term loans, allow for returns, effective way to deal with questionable items. 6. Positive / Negative Databases The data is out there! 7. Integration & Reporting Monitor client deposit trends, integrate into bank-wide risk management systems (AML / BSA for example). 8. Real-time Systems Manage systems, Mitigate Risk before / as it happens 9. Balances Competitive advantage, strengthens balance sheet, maximizes revenues and minimizes losses. 10. Insurance & Indemnification when all else fails. 27

28 Today s Webinar was Brought to you by FIS is the world's top-ranked technology provider to the banking industry. With more than 24,000 experts in 100 countries, FIS delivers the most comprehensive range of check processing solutions, including outsourced and turnkey enterprise platform solutions for the broadest range of financial markets, all with a singular focus: helping you succeed. Our breadth of distributed capture solutions include branch capture, teller capture, vault capture, business remote deposit and consumer remote deposit. Every FIS solution has the strength you need for profitability today, and the power to help you manage whatever comes next. For more information about FIS visit Source Capture Optimization An industry leading, web-based approach to Remote Deposit Capture from any point of check presentment: consumer, small business, merchant, corporate, branch, teller and ATM. Visit to learn more. call (800) victoria.lant@fiserv.com 28

29 A Unique Perspective RemoteDepositCapture.com is an independent information & services resource for the Payments Industry. We are NOT a reseller, solution provider, etc. We ARE experts in, and an open resource for the industry. We work with the vast majority of leading solution providers, FIs, processors. Thousands of FIs, corporations, businesses and consumers visit the site each month. We were directly involved in the formulation of the guidance and training of over 1,200 Regulators, Examiners & Auditors. Services News & Research RDC Marketplace Solution Provider Directories RDC Overviews White Paper Central FREE Webinars, Community Forums, and more. Contacts: Ed.McLaughlin@RemoteDepositCapture.com John.Leekley@RemoteDepositCapture.com 29

30 KYC is Critical Customer selection and KYC Review process at the FI who is involved and what level of management Risk rating system Elements included in decision criteria User / Location / Account Parameters - Identify & Prevent Fraud & Mistakes. Client Deposit Trends Ensure metrics, safeguards are relevant. Availability Schedules & Holds - Don t make short-term loans, allow for returns, effective way to deal with questionable items. Balances Competitive advantage, strengthens balance sheet, maximizes revenues and minimizes losses. 30

31 Change Management Change Management Ensure system, process and personnel changes do not negatively impact RDC Risk Management Compatibility of software and hardware components Defined Software Update Procedures Internal (System, Branch, etc.) External (Clients) Records Management Assess the Process for verification by customer for compliance with contract requirements : Secure retention, storage, & destruction of physical deposit items Electronic File Handling How? Legal Agreements, Training, Confirmation, Systemic Capabilities & Monitoring 31

limits Random review of deposits Timeliness in processing of received deposits Monitoring and review of accounts for duplicates, rejected and returned items Monitor")

32 Risk Reporting Policies and Procedures for RDC that include metrics for reporting and risk tolerances for accounts: Daily batch totals and account rules and limits report Account Selection Deposit limits and amounts Item amount ($) limits Random review of deposits Timeliness in processing of received deposits Monitoring and review of accounts for duplicates, rejected and returned items Monitor internal processes for separation of responsibilities: Regular reporting of deposits and history to identify patterns Transaction velocity exception ($ and transactions) levels and trends Integration with other Risk systems for complete account risk Report should be structured for the various levels of management Actionability of exceptions and Sustainability Customer reconciliation reports 32

33 Fraud Monitoring & Prevention Monitoring Process to identify potential fraudulent items Real-time Systems Mitigate Risk before / as it happens Functionality duplicate detection, deposit limits, pattern identification, safeguarding check Restrict Functional Capabilities by location Minimize Fraud Opportunities. Foreign location identification and monitoring Positive / Negative Databases The data is out there! 33

34 Contracts and Agreements Roles and responsibilities Document handling and record retention requirements Transmittable items Customer processes and procedures Periodic customer audits Mandating customer internal controls (maintenance & admin) Performance standards High risk customer limits and exclusions BCP and back up requirements Governing laws regulations and or rules Authority of FI to mandate specific controls Information Security Incident Reporting Allocating: Liability Warranties Indemnification Dispute resolution Deposit limits, availability etc. Cut-off times Deposit acknowledgement Service termination 34

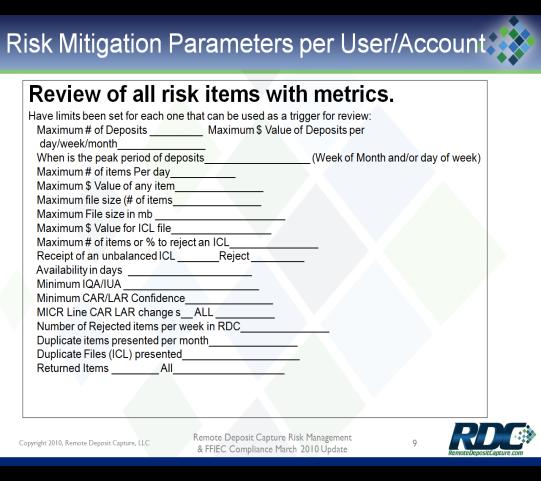

35 Risk Mitigation Parameters per User/Account Review of all risk items with metrics. Have limits been set for each one that can be used as a trigger for review: Maximum # of Deposits Maximum $ Value of Deposits per day/week/month When is the peak period of deposits (Week of Month and/or day of week) Maximum # of items Per day Maximum $ Value of any item Maximum file size (# of items Maximum File size in mb Maximum $ Value for ICL file Maximum # of items or % to reject an ICL Receipt of an unbalanced ICL Reject Availability in days Minimum IQA/IUA Minimum CAR/LAR Confidence MICR Line CAR LAR change s ALL Number of Rejected items per week in RDC Duplicate items presented per month Duplicate Files (ICL) presented Returned Items All 35

36 Customer Risk Rating Risk Category: Type of Business (based on scale of 1 to 10 for example with 10 being the highest risk - adult entertainment, check cashers,etc.) New Customer (based on a scale of 1 to 10 where transaction history has been reviewed, credit reports, $ value exposure daily or monthly, time in business) Existing Customer (based on a scale of 1 to 10 where transaction history has been reviewed, daily balances established, $ value exposure daily or monthly, time in business) Consumer (established criteria to qualify for service - balances, length of time with bank, transaction history) Daily $ volume exposure by item and total $ amount (Rate on a scale of 1 to 10 with 10 being for large dollar items and/or for large volume of checks) Is the customer a processor for other customers (10 point scale should rate this type of customer very high unless other proof is provided) Type of items being processed (IF RCCs are to be processed then customer should score a 10 on the ten point scale) # and locations of capture sites (Review OFAC list for denied countries and persons - reject if listed, understand the nature of the relationship - subsidiary or their customer. The scale again would be based on a combination of type of business, volume, and relationship) Has the site been visited and an onsite checklist been completed (Same 10 point scale with the results of the check list determining score) Assign a Risk # or Grouping based on a weighted average of the above risk categories (The weighting is important to offset any unintentional bias) 36

37 Customer Selection Checklist Customer selection checklist. The following should be included: Customer Name Customer Address and locations of additional RDC sites Names of Principals Names of RDC Operators_(# of staff) Name of Person completing checklist Type of Business (SIC Code) - Assign a Risk Category based on SIC code; Is it a processor for other customers? What types of businesses does it process for and establish a process for evaluating each of its customers Is this a high risk business (this could include: parties include online payment processors, certain credit-repair services, certain mail order and telephone order companies, online gambling operations, businesses located offshore, and adult entertainment businesses) Years in Business Consumer - How long with bank, other bank products, transaction history, average daily balance Existing Business Customer - How long, transaction history, balances, existing bank products (loans, credit cards, payroll account etc,) New Business or Consumer Customer - Name of previous bank, 3 months of transaction history, average daily balances, other bank products being included Customer location evaluation - Internal IT structure (include out sourced and none where appropriate), Risk management policies (specify and include none for small businesses) All non domestic locations must be specified and relationship to the domestic account included Credit Report - has one been obtained? All new customers and large depositors should be reviewed Expected daily, weekly and monthly value of deposits and $ size of the items to be deposited; will there be any peak periods during the week or month What type of clearing channels will be used - Check and ACH PCI compliance report if applicable VISA/MasterCard terminated merchant report or ChexSystems reports if appropriate Has the customer location been visited by an Officer or a Treasury sales person 37

38 Customer Self Assessment Checklist Develop a customer self assessment checklist. The following should be included Customer Name Customer Address and locations of additional RDC sites Names of Principals Names of RDC Operators Name of Person completing checklist Title of Person completing the checklist Type of Business (SIC Code) - Assign SIC code; Do you process RDC for your customers? What types of businesses Do you process for and establish a process for evaluating the risk for each of your customers Existing Business Customer - How long have you been with the bank, Your transaction history, balances, other existing bank products (loans, credit cards, payroll account etc,) Have you signed the banks deposit agreement New Business Customer - Name of previous bank, 3 months of transaction history, average daily balances, other bank products being included Annual Revenue of Business How long in business Customer location evaluation - Internal IT structure (include if it is out sourced and none where appropriate), Risk management policies (specify and include none if you do not have one) All non domestic locations must be specified and relationship to the domestic account included Number of Staff How will the staff be trained on RDC Credit Report - Do you have one you can supply? Review any available audits (SAS 70, IT, ISO etc) that are relevant What is the expected daily, weekly and monthly value of deposits $ size of the items and deposits to be deposited; # of items and deposits will there be any peak periods during the week or month What type of clearing channels will be used - Check and ACH What Controls can the customer exercise over the RDC system (Access, Security) Does the customer do background checks on employees Does the customer have a risk management policy in place, if so describe Have you been visited by an Officer or a Treasury salesperson? If yes, When 38

39 Report Contents Established Risk Criteria, measurements, monitoring frequency, report content and review procedures. Items to be included include: Reports by account that include: Date and times of deposits Location and operator Total number of deposits Total $ deposits Total # of items Number of files Number of items sent for review Number of items/files rejected and why Number of times deposit $ levels were exceeded; Number of items that exceeded max $ value Number of IQA issues Established hold and availability schedules Clearing channels used and results(5 of each channel used) Number of returned items (from return systems) Ability to aggregate up or dive down for item information 39

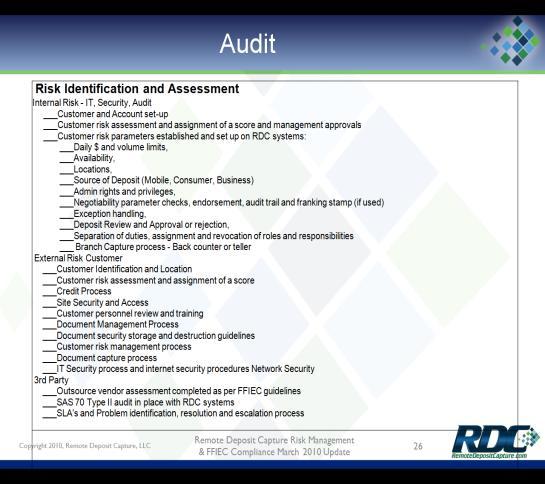

40 Audit Risk Identification and Assessment Internal Risk - IT, Security, Audit Customer and Account set-up Customer risk assessment and assignment of a score and management approvals Customer risk parameters established and set up on RDC systems: Daily $ and volume limits, Availability, Locations, Source of Deposit (Mobile, Consumer, Business) Admin rights and privileges, Negotiability parameter checks, endorsement, audit trail and franking stamp (if used) Exception handling, Deposit Review and Approval or rejection, Separation of duties, assignment and revocation of roles and responsibilities Branch Capture process - Back counter or teller External Risk Customer Customer Identification and Location Customer risk assessment and assignment of a score Credit Process Site Security and Access Customer personnel review and training Document Management Process Document security storage and destruction guidelines Customer risk management process Document capture process IT Security process and internet security procedures Network Security 3rd Party Outsource vendor assessment completed as per FFIEC guidelines SAS 70 Type II audit in place with RDC systems SLA's and Problem identification, resolution and escalation process 40

41 41

RDC Risk Management in 2013

RDC Risk Management in 2013 Paul Carrubba, Partner Adams and Reese, LLP John Leekley, Founder & CEO RemoteDepositCapture.com Legal and Regulatory Issues No Mobile Banking Law Federal Laws and Regulations

RDC Risk Management in 2013 Paul Carrubba, Partner Adams and Reese, LLP John Leekley, Founder & CEO RemoteDepositCapture.com Legal and Regulatory Issues No Mobile Banking Law Federal Laws and Regulations

RDC Risk Management in 2015

RDC Risk Management in 2015 John Leekley, Founder & CEO RemoteDepositCapture.com Be sure to tweet about the #RDCSummit and mention @RDCTweet Setting the Stage Discussion Objectives Definition of RDC Risk

RDC Risk Management in 2015 John Leekley, Founder & CEO RemoteDepositCapture.com Be sure to tweet about the #RDCSummit and mention @RDCTweet Setting the Stage Discussion Objectives Definition of RDC Risk

RDC Risk Management Update 2011

RDC Risk Management Update 2011 Heather Holliway, Product Manager Synovus Financial Corp. Ed McLaughlin, Executive Director RemoteDepositCapture.com September 30, 2011 Regulatory Guidance Overview 1. FFIEC

RDC Risk Management Update 2011 Heather Holliway, Product Manager Synovus Financial Corp. Ed McLaughlin, Executive Director RemoteDepositCapture.com September 30, 2011 Regulatory Guidance Overview 1. FFIEC

RDC Audit & Compliance: Lessons from the Battlefield

RDC Audit & Compliance: Lessons from the Battlefield Kevin Olsen, AAP, NCP Payments Space Advisors September / October 2, 2014 Be sure to tweet about the #RDCSummit and mention @RDCTweet Disclaimer This

RDC Audit & Compliance: Lessons from the Battlefield Kevin Olsen, AAP, NCP Payments Space Advisors September / October 2, 2014 Be sure to tweet about the #RDCSummit and mention @RDCTweet Disclaimer This

Risk Management Technologies The Latest & Greatest from Throughout the Industry

Risk Management Technologies The Latest & Greatest from Throughout the Industry John Leekley, Founder & CEO RemoteDepositCapture.com Be sure to tweet about the #RDCSummit and mention @RDCTweet Perspective

Risk Management Technologies The Latest & Greatest from Throughout the Industry John Leekley, Founder & CEO RemoteDepositCapture.com Be sure to tweet about the #RDCSummit and mention @RDCTweet Perspective

Consumer & Small Business RDC Opportunity & Case Study

Consumer & Small Business RDC Opportunity & Brought to you by: Presented By: Gary Brand, Fiserv Mike Williams, PenFed Q3 2010 Moderator: John Leekley, RemoteDepositCapture.com Today s webinar is brought

Consumer & Small Business RDC Opportunity & Brought to you by: Presented By: Gary Brand, Fiserv Mike Williams, PenFed Q3 2010 Moderator: John Leekley, RemoteDepositCapture.com Today s webinar is brought

Remote Deposit Capture An Overview of how Technology and Legislation changed core banking

Remote Deposit Capture An Overview of how Technology and Legislation changed core banking John M. Curtis, AAP/NCP Vice President and Director Education and Communications Western Payments Alliance September

Remote Deposit Capture An Overview of how Technology and Legislation changed core banking John M. Curtis, AAP/NCP Vice President and Director Education and Communications Western Payments Alliance September

Expand Remote Deposit & Mitigate Risk:

IMAGING & PAYMENTS PROCESSING : How Smart Financial Institutions Can Apply the FFIEC Guidelines to Remote Deposit sales@profitstars.com 877.827.7101 How Smart Financial Institutions Can Apply the FFIEC

IMAGING & PAYMENTS PROCESSING : How Smart Financial Institutions Can Apply the FFIEC Guidelines to Remote Deposit sales@profitstars.com 877.827.7101 How Smart Financial Institutions Can Apply the FFIEC

Retail Payment Systems Internal Control Questionnaire

Retail Payment Systems Internal Control Questionnaire Completed by: Date Completed: POLICIES AND PROCEDURES 1. Has the board of directors, consistent with its duties and responsibilities, adopted formal

Retail Payment Systems Internal Control Questionnaire Completed by: Date Completed: POLICIES AND PROCEDURES 1. Has the board of directors, consistent with its duties and responsibilities, adopted formal

Mobile Remote Deposit Risks, Rewards, and Deposits Presented by Kevin Olsen, AAP NCP SVP, Payments Education

Mobile Remote Deposit Risks, Rewards, and Deposits 2017 Presented by Kevin Olsen, AAP NCP SVP, Payments Education 2017 Audio Handouts Questions MOBILE REMOTE DEPOSIT RISKS, REWARDS, AND DEPOSITS 2017 Kevin

Mobile Remote Deposit Risks, Rewards, and Deposits 2017 Presented by Kevin Olsen, AAP NCP SVP, Payments Education 2017 Audio Handouts Questions MOBILE REMOTE DEPOSIT RISKS, REWARDS, AND DEPOSITS 2017 Kevin

NCR Passport for Commercial. Part of NCR s enterprise hub for remote deposit capture

NCR Passport for Commercial Part of NCR s enterprise hub for remote deposit capture For more information on RDC, speak to your sales contact or go to ncr.com. Easy and secure deposits from where their

NCR Passport for Commercial Part of NCR s enterprise hub for remote deposit capture For more information on RDC, speak to your sales contact or go to ncr.com. Easy and secure deposits from where their

Image Exchange: Processes National Check Payments Certification. Image Exchange: Processes

NCP 2014 Exam ECCHO Training Series Session 5 March 13, 2014 2:00 pm ET (1:00 pm CT; 11:00 am PT) All sessions 90 min. Image Exchange: Processes Copyright 2013 by the Electronic Check Clearing House Organization

NCP 2014 Exam ECCHO Training Series Session 5 March 13, 2014 2:00 pm ET (1:00 pm CT; 11:00 am PT) All sessions 90 min. Image Exchange: Processes Copyright 2013 by the Electronic Check Clearing House Organization

Solutions. Cash & Logistics Intelligent and Integrated Solutions to Optimize Currency Levels, Reduce Expenses and Improve Control

Solutions Cash & Logistics Intelligent and Integrated Solutions to Optimize Currency Levels, Reduce Expenses and Improve Control Solutions The financial services industry faces a number of new challenges

Solutions Cash & Logistics Intelligent and Integrated Solutions to Optimize Currency Levels, Reduce Expenses and Improve Control Solutions The financial services industry faces a number of new challenges

Electronic Banking Remote Deposit Capture Third Party Payment Processors Automated Monitoring Systems Staffing & Resources

Electronic Banking Remote Deposit Capture Third Party Payment Processors Automated Monitoring Systems Staffing & Resources Examples of electronic banking systems: Automated teller machine transactions

Electronic Banking Remote Deposit Capture Third Party Payment Processors Automated Monitoring Systems Staffing & Resources Examples of electronic banking systems: Automated teller machine transactions

Ruth A. Harpool, AAP, CTP Director, Treasury Operations Indiana University

Ruth A. Harpool, AAP, CTP Director, Treasury Operations Indiana University 1 Remote deposit capture industry overview Regulatory/risk management update Benefits realized Market trends Indiana University

Ruth A. Harpool, AAP, CTP Director, Treasury Operations Indiana University 1 Remote deposit capture industry overview Regulatory/risk management update Benefits realized Market trends Indiana University

Treasury Management Guide

Treasury Management Guide Preparing your business for success You will continue to receive a high level of customer service from a team of experts committed to helping you meet your financial goals no

Treasury Management Guide Preparing your business for success You will continue to receive a high level of customer service from a team of experts committed to helping you meet your financial goals no

RDC Risk Management and Compliance: Expert Update & Case Study

RDC Risk Management and Compliance: Expert Update & Case Study David Rathke, Senior Vice President, Frost Bank Steve Vaglio Senior Vice President, EastPay Ed McLaughlin, RemoteDepositCapture.com September

RDC Risk Management and Compliance: Expert Update & Case Study David Rathke, Senior Vice President, Frost Bank Steve Vaglio Senior Vice President, EastPay Ed McLaughlin, RemoteDepositCapture.com September

VISION MANAGEMENT SOLUTION

VISION MANAGEMENT SOLUTION THE MOST ADVANCED MANAGEMENT SOLUTION ON THE MARKET TODAY, FUTURE-PROOFED TO SUPPORT CONTINUOUS GROWTH AND EVOLUTION IN THE RETAIL BANKING ENVIRONMENT. An NCR Buyer s Guide TAKE

VISION MANAGEMENT SOLUTION THE MOST ADVANCED MANAGEMENT SOLUTION ON THE MARKET TODAY, FUTURE-PROOFED TO SUPPORT CONTINUOUS GROWTH AND EVOLUTION IN THE RETAIL BANKING ENVIRONMENT. An NCR Buyer s Guide TAKE

User s Starter Kit. For Home or Small Office Use. fcbbanks.com

D E P O S I T User s Starter Kit For Home or Small Office Use fcbbanks.com Table of Contents 2 4 6 8 10 12 About Fast Track Deposit Frequently Asked Questions Scanner & Software Information Your Rights

D E P O S I T User s Starter Kit For Home or Small Office Use fcbbanks.com Table of Contents 2 4 6 8 10 12 About Fast Track Deposit Frequently Asked Questions Scanner & Software Information Your Rights

W H I T E PA P E R l The True Paperless Branch

W H I T E PA P E R l The True Paperless Branch Trudy Lotter Solution Market Manager, Financial Institutions Joe Pitzo ECM Product Manager Doug Turner Product Line Manager July 2009 2009 WAUSAU FINANCIAL

W H I T E PA P E R l The True Paperless Branch Trudy Lotter Solution Market Manager, Financial Institutions Joe Pitzo ECM Product Manager Doug Turner Product Line Manager July 2009 2009 WAUSAU FINANCIAL

RETHINKING WHAT RDC MEANS TO YOUR CUSTOMERS AND YOUR FINANCIAL INSTITUTION

RETHINKING WHAT RDC MEANS TO YOUR CUSTOMERS AND YOUR FINANCIAL INSTITUTION Thank you for joining! Please wait while others join the line. The Webinar will begin shortly. As a courtesy to others, please

RETHINKING WHAT RDC MEANS TO YOUR CUSTOMERS AND YOUR FINANCIAL INSTITUTION Thank you for joining! Please wait while others join the line. The Webinar will begin shortly. As a courtesy to others, please

TREASURY MANAGEMENT. Dynamic Solutions. Superior Results.

TREASURY MANAGEMENT Dynamic Solutions. Superior Results. HELP YOUR COMMERCIAL CLIENTS BY OFFERING TREASURY MANAGEMENT SERVICES ENHANCED FEE REVENUE CSI s Treasury Management solutions let your financial

TREASURY MANAGEMENT Dynamic Solutions. Superior Results. HELP YOUR COMMERCIAL CLIENTS BY OFFERING TREASURY MANAGEMENT SERVICES ENHANCED FEE REVENUE CSI s Treasury Management solutions let your financial

E-Debit International Inc. Introduction to Transaction Processing. Basic Overview of our Payment & Processing Systems 08/13

E-Debit International Inc. Introduction to Transaction Processing Basic Overview of our Payment & Processing Systems 08/13 Introducing E-Debit International Payment program and the Westsphere Systems Inc.

E-Debit International Inc. Introduction to Transaction Processing Basic Overview of our Payment & Processing Systems 08/13 Introducing E-Debit International Payment program and the Westsphere Systems Inc.

Payment Processor Buying Guide. How to prepare for sending out an RFP

Payment Processor Buying Guide How to prepare for sending out an RFP Payment Processor Buying Guide This document is meant to provide potential customers a framework to evaluate payment processors. PRELIMINARY

Payment Processor Buying Guide How to prepare for sending out an RFP Payment Processor Buying Guide This document is meant to provide potential customers a framework to evaluate payment processors. PRELIMINARY

Risk Management TRAINING AND EVENTS. aba.com/risktraining

Risk Management TRAINING AND EVENTS Stay ahead of the changing world of risks. Risk management is much more complex today and requires new approaches to talent management. Your bank needs comprehensive

Risk Management TRAINING AND EVENTS Stay ahead of the changing world of risks. Risk management is much more complex today and requires new approaches to talent management. Your bank needs comprehensive

Attachment 2: Merchant Card Services

Attachment 2: Merchant Card Services Overview The County s primary purpose in seeking proposals for merchant card services is to provide a variety of card payment options and services to County customers

Attachment 2: Merchant Card Services Overview The County s primary purpose in seeking proposals for merchant card services is to provide a variety of card payment options and services to County customers

Remote Deposit Capture Check Images or ACH?

Remote Deposit Capture Check Images or ACH? Prepared by: PAUL A. CARRUBBA Phone: (601) 292-0788 E-Mail: paul.carrubba@arlaw.com Remote Deposit Capture Bank and Customer Agreement Items Cleared as Images

Remote Deposit Capture Check Images or ACH? Prepared by: PAUL A. CARRUBBA Phone: (601) 292-0788 E-Mail: paul.carrubba@arlaw.com Remote Deposit Capture Bank and Customer Agreement Items Cleared as Images

NCR APTRA PASSPORT An enterprise hub for remote deposit capture

NCR APTRA PASSPORT An enterprise hub for remote deposit capture A better way for your customers to deposit checks Banks and financial institutions continue to face the challenges of managing new and evolving

NCR APTRA PASSPORT An enterprise hub for remote deposit capture A better way for your customers to deposit checks Banks and financial institutions continue to face the challenges of managing new and evolving

Defining and promoting excellence in the provision of mobile money services

SAFEGUARDING OF FUNDS DATA PRIVACY AML/CFT/FRAUD PREVENTION STAFF AND PARTNER MANAGEMENT CUSTOMER SERVICE TRANSPARENCY QUALITY OF OPERATIONS SECURITY OF SYSTEMS Defining and promoting excellence in the

SAFEGUARDING OF FUNDS DATA PRIVACY AML/CFT/FRAUD PREVENTION STAFF AND PARTNER MANAGEMENT CUSTOMER SERVICE TRANSPARENCY QUALITY OF OPERATIONS SECURITY OF SYSTEMS Defining and promoting excellence in the

Auditing for Effective Training

Maleka Ali M. Ali 2013 Director of Consulting & Education Page 0 Banker s Toolbox Auditing for Effective Training I. INTRODUCTION Banking organizations must develop, implement, and maintain effective AML

Maleka Ali M. Ali 2013 Director of Consulting & Education Page 0 Banker s Toolbox Auditing for Effective Training I. INTRODUCTION Banking organizations must develop, implement, and maintain effective AML

ACING YOUR REMOTE DEPOSIT CAPTURE AUDIT:

ACING YOUR REMOTE DEPOSIT CAPTURE AUDIT: LESSONS FROM BANKERS WHO HAVE BEEN THERE AND DONE THAT! COMPLIANCE STARTS AT THE TOP Many banks are becoming savvy about how to ace their audits after experiencing

ACING YOUR REMOTE DEPOSIT CAPTURE AUDIT: LESSONS FROM BANKERS WHO HAVE BEEN THERE AND DONE THAT! COMPLIANCE STARTS AT THE TOP Many banks are becoming savvy about how to ace their audits after experiencing

How Teller, ATM and Bank Vault reconciliations Can Help Track Physical Cash

How Teller, ATM and Bank Vault reconciliations Can Help Track Physical Cash Richard Chapman, Vice President, Business Development and Strategy, FIS Reconciliation Business Joseph Vesey, Global Pre-sales

How Teller, ATM and Bank Vault reconciliations Can Help Track Physical Cash Richard Chapman, Vice President, Business Development and Strategy, FIS Reconciliation Business Joseph Vesey, Global Pre-sales

X9 EXCEPTIONS MANAGER

X9 EXCEPTIONS MANAGER Working with the New Federal Reserve Bank Reg CC Time is Money X9 Exceptions Working with the New FRB Reg CC August 2017 Table of Contents Executive Summary... 1 Exception Processing

X9 EXCEPTIONS MANAGER Working with the New Federal Reserve Bank Reg CC Time is Money X9 Exceptions Working with the New FRB Reg CC August 2017 Table of Contents Executive Summary... 1 Exception Processing

Operational/Implementation Issues

Operational/Implementation Issues Version 1 January 2005 One of ECCHO s primary focuses relative to Check 21 was the identification and resolution of Operational and Implementation issues. Some of the

Operational/Implementation Issues Version 1 January 2005 One of ECCHO s primary focuses relative to Check 21 was the identification and resolution of Operational and Implementation issues. Some of the

CORE BANK PROCESSING NUPOINT. Dynamic Solutions. Superior Results.

CORE BANK PROCESSING NUPOINT Dynamic Solutions. Superior Results. NUPOINT FULL INTEGRATION OF CORE SERVICES AND MUCH MORE FULL INTEGRATION across banking platforms NuPoint provides your bank with a dynamic,

CORE BANK PROCESSING NUPOINT Dynamic Solutions. Superior Results. NUPOINT FULL INTEGRATION OF CORE SERVICES AND MUCH MORE FULL INTEGRATION across banking platforms NuPoint provides your bank with a dynamic,

IIB - INTERNATIONAL BANKING ANTI-MONEY LAUNDERING SEMINAR

IIB - INTERNATIONAL BANKING ANTI-MONEY LAUNDERING SEMINAR Practical Suggestions and Tips for an Effective BSA/AML Compliance Function - Risk Assessment and Transaction Monitoring May 15, 2012 Disclaimer

IIB - INTERNATIONAL BANKING ANTI-MONEY LAUNDERING SEMINAR Practical Suggestions and Tips for an Effective BSA/AML Compliance Function - Risk Assessment and Transaction Monitoring May 15, 2012 Disclaimer

Are You Sure You Have the Right RDC Solution

Are You Sure You Have the Right RDC Solution Denis Bergeron, SVP NCR Corporation Bill Phillips, President, Enterprise Payment Solutions ProfitStars/Jack Henry Mike Murphy, SVP RDM Corporation September

Are You Sure You Have the Right RDC Solution Denis Bergeron, SVP NCR Corporation Bill Phillips, President, Enterprise Payment Solutions ProfitStars/Jack Henry Mike Murphy, SVP RDM Corporation September

CORE BANK PROCESSING MERIDIAN.NET. Dynamic Solutions. Superior Results.

CORE BANK PROCESSING MERIDIAN.NET Dynamic Solutions. Superior Results. MERIDIAN.NET A POWERFUL SOLUTION TO MANAGE CORE PROCESSING FROM AN IN-HOUSE OR OUTSOURCED PLATFORM PRODUCTIVITY A highly flexible

CORE BANK PROCESSING MERIDIAN.NET Dynamic Solutions. Superior Results. MERIDIAN.NET A POWERFUL SOLUTION TO MANAGE CORE PROCESSING FROM AN IN-HOUSE OR OUTSOURCED PLATFORM PRODUCTIVITY A highly flexible

Source Capture Solutions

Resource Guide Source Capture Solutions A Resource Guide to Web-Based Deposit Capture Solutions from Fiserv October 2013, Version 1.0 Contents 3 ATM Source Capture 3 Branch Source Capture 4 Central Source

Resource Guide Source Capture Solutions A Resource Guide to Web-Based Deposit Capture Solutions from Fiserv October 2013, Version 1.0 Contents 3 ATM Source Capture 3 Branch Source Capture 4 Central Source

active:check active payment solutions

:check Modular solution providing total processing for check s within financial institutions (commercial banks, government banks and credit unions). Fully scalable architecture Fraud Prevention Parameter

:check Modular solution providing total processing for check s within financial institutions (commercial banks, government banks and credit unions). Fully scalable architecture Fraud Prevention Parameter

City of Los Angeles Office of the Treasurer. Responses to Requests for Proposal. General Banking Services

City of Los Angeles Office of the Treasurer Responses to Requests for Proposal General Banking Services On February 13, 2008, the City of Los Angeles held a Request for Proposal (RFP) Pre- Proposal Conference,

City of Los Angeles Office of the Treasurer Responses to Requests for Proposal General Banking Services On February 13, 2008, the City of Los Angeles held a Request for Proposal (RFP) Pre- Proposal Conference,

Enroll Today! Annual Member Package Price: $2, Founder s Message TERRI SANDS CAMS AUDIT, CFE, AAP, ACT SPECIALIST

Founder s Message TERRI SANDS CAMS AUDIT, CFE, AAP, ACT SPECIALIST Over the past year, there have been significant changes in the payments industry to move payments faster. Industry-wide, financial institutions

Founder s Message TERRI SANDS CAMS AUDIT, CFE, AAP, ACT SPECIALIST Over the past year, there have been significant changes in the payments industry to move payments faster. Industry-wide, financial institutions

Juan Carlos Ramirez, VP, AML/ATF & Sanctions Audit, Scotiabank. Compliance and Risk Management

Juan Carlos Ramirez, VP, AML/ATF & Sanctions Audit, Scotiabank Compliance and Risk Management Governance Service providers Operational Risk Fraud AML Sanctions Risk Management Compliance Assessment Financial

Juan Carlos Ramirez, VP, AML/ATF & Sanctions Audit, Scotiabank Compliance and Risk Management Governance Service providers Operational Risk Fraud AML Sanctions Risk Management Compliance Assessment Financial

Anti-Money Laundering

Anti-Money Laundering Risk Assessments as a Key to AML/BSA Compliance AIBA Quarterly Meeting March 2008 January 2006 About edelta Consulting edelta Consulting, Inc. is a full service consulting firm formed

Anti-Money Laundering Risk Assessments as a Key to AML/BSA Compliance AIBA Quarterly Meeting March 2008 January 2006 About edelta Consulting edelta Consulting, Inc. is a full service consulting firm formed

Jen Wasmund, AAP, NCP Compliance Services Director

Jen Wasmund, AAP, NCP Compliance Services Director Regional Payments Associations, through their Direct Membership in NACHA, are specially recognized and licensed providers of ACH education, publications

Jen Wasmund, AAP, NCP Compliance Services Director Regional Payments Associations, through their Direct Membership in NACHA, are specially recognized and licensed providers of ACH education, publications

Effective Vendor Risk Management. April 21, Mario A. Mosse. This Training is Brought to you by ComplianceOnline. Presenter:

This Training is Brought to you by ComplianceOnline. Effective Vendor Risk Management Presenter: Mario A. Mosse April 21, 2017 This training session is sponsored by 2014 ComplianceOnline www.complianceonlie.com

This Training is Brought to you by ComplianceOnline. Effective Vendor Risk Management Presenter: Mario A. Mosse April 21, 2017 This training session is sponsored by 2014 ComplianceOnline www.complianceonlie.com

Introducing an easier way to manage your business

Introducing an easier way to manage your business With our suite of easy-to-use treasury solutions, you can manage your payments and receipts, help protect against transactional fraud and receive robust

Introducing an easier way to manage your business With our suite of easy-to-use treasury solutions, you can manage your payments and receipts, help protect against transactional fraud and receive robust

ANTI-MONEY LAUNDERING SERVICES EXPERTS WITH IMPACT

ANTI-MONEY LAUNDERING SERVICES EXPERTS WITH IMPACT FTI Consulting Anti-Money Laundering Services F TI Consulting provides end-to-end Anti-Money Laundering consulting services to financial institutions.

ANTI-MONEY LAUNDERING SERVICES EXPERTS WITH IMPACT FTI Consulting Anti-Money Laundering Services F TI Consulting provides end-to-end Anti-Money Laundering consulting services to financial institutions.

INTERNAL CONTROLS REVIEW PROGRESS REPORT Yellow highlighted items have been completed/validated since last report in August 2016

INTERNAL S REVIEW PROGRESS REPORT Yellow highlighted items have been completed/validated since last report in August 2016 RECOMMENDATIONS ADDRESSED THROUGH INTERNAL AUDIT WORK PLANS Monthly Reconciliation

INTERNAL S REVIEW PROGRESS REPORT Yellow highlighted items have been completed/validated since last report in August 2016 RECOMMENDATIONS ADDRESSED THROUGH INTERNAL AUDIT WORK PLANS Monthly Reconciliation

Non-Banking Financial Institution (NBFI) Third Party Payment Processor (TPPP) AMLQuestionnaire

Third Party Payment Processor (TPPP) AMLQuestionnaire") n-banking Financial Institution (NBFI) Third Party Payment Processor (TPPP) AMLQuestionnaire I. Overview This questionnaire is designed to provide HSBC with information about your organisation s financial

n-banking Financial Institution (NBFI) Third Party Payment Processor (TPPP) AMLQuestionnaire I. Overview This questionnaire is designed to provide HSBC with information about your organisation s financial

INTERNAL CONTROLS REVIEW PROGRESS REPORT Highlighted items have been completed since last report in January 2016

INTERNAL S REVIEW PROGRESS REPORT Highlighted items have been completed since last report in January 2016 RECOMMENDATIONS ADDRESSED THROUGH INTERNAL AUDIT WORK PLANS Internal Audit: prepare documentation

INTERNAL S REVIEW PROGRESS REPORT Highlighted items have been completed since last report in January 2016 RECOMMENDATIONS ADDRESSED THROUGH INTERNAL AUDIT WORK PLANS Internal Audit: prepare documentation

HOW INTEGRATED RECEIVABLES OVERCOMES THE FOUR BIGGEST CHALLENGES IN ORDER-TO-CASH

HOW INTEGRATED RECEIVABLES OVERCOMES THE FOUR BIGGEST CHALLENGES IN ORDER-TO-CASH EXECUTIVE SUMMARY Businesses are demanding more of their treasury departments. Treasury must become a strategic advisor,

HOW INTEGRATED RECEIVABLES OVERCOMES THE FOUR BIGGEST CHALLENGES IN ORDER-TO-CASH EXECUTIVE SUMMARY Businesses are demanding more of their treasury departments. Treasury must become a strategic advisor,

Advanced Finance for Governing Board Members. Charter Schools: Advancing the Promise!! 2015 Annual Conference

Advanced Finance for Governing Board Members Charter Schools: Advancing the Promise!! 2015 Annual Conference Governing Body Responsibilities with regard to finance Fiduciary responsibilities outlined in

Advanced Finance for Governing Board Members Charter Schools: Advancing the Promise!! 2015 Annual Conference Governing Body Responsibilities with regard to finance Fiduciary responsibilities outlined in

What Happens When Internal Controls Fail

What Happens When Internal Controls Fail 1 Your Presenters Brian Sanvidge Principal Baker Tilly Ellen Labita Partner Baker Tilly Danielle Callaci Manager Baker Tilly 2 Today s Agenda > What are Internal

What Happens When Internal Controls Fail 1 Your Presenters Brian Sanvidge Principal Baker Tilly Ellen Labita Partner Baker Tilly Danielle Callaci Manager Baker Tilly 2 Today s Agenda > What are Internal

September 2, 2016 ADDENDUM No. 5 SFMTA

September 2, 2016 ADDENDUM No. 5 SFMTA 2016-83 Request for Proposals Citation Processing, Permit Processing and Support Services To all prospective bidders: The following modifications are made to the

September 2, 2016 ADDENDUM No. 5 SFMTA 2016-83 Request for Proposals Citation Processing, Permit Processing and Support Services To all prospective bidders: The following modifications are made to the

REGULATORY COMPLIANCE. Dynamic Solutions. Superior Results.

REGULATORY COMPLIANCE Dynamic Solutions. Superior Results. STREAMLINE, STRENGTHEN AND SIMPLIFY YOUR COMPLIANCE EFFORTS CSI S AUTOMATED, DYNAMIC SOLUTIONS MITIGATE RISK, DECREASE COSTS AND IMPROVE COMPLIANCE

REGULATORY COMPLIANCE Dynamic Solutions. Superior Results. STREAMLINE, STRENGTHEN AND SIMPLIFY YOUR COMPLIANCE EFFORTS CSI S AUTOMATED, DYNAMIC SOLUTIONS MITIGATE RISK, DECREASE COSTS AND IMPROVE COMPLIANCE

You Don t Have to be Big to Get Operational Economies of Scale

You Don t Have to be Big to Get Operational Economies of Scale Richard Chapman, Vice President, Business Development and Strategy, FIS Reconciliation Business Joseph Vesey, Global Pre-sales Manager, FIS

You Don t Have to be Big to Get Operational Economies of Scale Richard Chapman, Vice President, Business Development and Strategy, FIS Reconciliation Business Joseph Vesey, Global Pre-sales Manager, FIS

Secure Payments Task Force Payment Use Cases Webinar

Secure Payments Task Force Payment Use Cases Webinar ACH, Wire, and Check Tammy Hornsby-Fink Vice President, Federal Reserve System Gloria Dugan Senior Industry Relations Representative, Federal Reserve

Secure Payments Task Force Payment Use Cases Webinar ACH, Wire, and Check Tammy Hornsby-Fink Vice President, Federal Reserve System Gloria Dugan Senior Industry Relations Representative, Federal Reserve

Product Frontier Reconciliation

Product Frontier Reconciliation Mitigate Risk, Improve Operational Efficiency and Enable Regulatory Compliance Product Frontier Reconciliation from Fiserv takes an enterprise approach to reconciliation

Product Frontier Reconciliation Mitigate Risk, Improve Operational Efficiency and Enable Regulatory Compliance Product Frontier Reconciliation from Fiserv takes an enterprise approach to reconciliation

ACTIVEVIEW ITEM PROCESSING IMAGE-BASED ITEM PROCESSING SOLUTION

ACTIVEVIEW ITEM PROCESSING IMAGE-BASED ITEM PROCESSING SOLUTION 2 FINASTRA Brochure INTRODUCTION The Powerful ActiveView Item Processing With ActiveView Item Processing, financial institutions of any size

ACTIVEVIEW ITEM PROCESSING IMAGE-BASED ITEM PROCESSING SOLUTION 2 FINASTRA Brochure INTRODUCTION The Powerful ActiveView Item Processing With ActiveView Item Processing, financial institutions of any size

Outline of the Discussion

IT Risk Supervision Outline of the Discussion Define IT Risk Identify Scope of an IT Examination Describe a Bank s Operating Environment Identify Risks Considered in IT Supervision Describe the IT Ratings

IT Risk Supervision Outline of the Discussion Define IT Risk Identify Scope of an IT Examination Describe a Bank s Operating Environment Identify Risks Considered in IT Supervision Describe the IT Ratings

Source Capture Solutions : New Year, New Capabilities. February 3, 2010

Source Capture Solutions : New Year, New Capabilities February 3, 2010 Agenda Welcome and introductions Victoria Lant, Product Marketing Director, Fiserv Overview and Industry Trends Gary Brand, Director

Source Capture Solutions : New Year, New Capabilities February 3, 2010 Agenda Welcome and introductions Victoria Lant, Product Marketing Director, Fiserv Overview and Industry Trends Gary Brand, Director

RSM ANTI-MONEY LAUNDERING SURVEY BEST PRACTICES AND BENCHMARKING FOR YOUR BSA/AML PROGRAM

RSM ANTI-MONEY LAUNDERING SURVEY BEST PRACTICES AND BENCHMARKING FOR YOUR BSA/AML PROGRAM Anti-money laundering (AML) regulations are at times challenging for banks. Emerging risks and increased scrutiny

RSM ANTI-MONEY LAUNDERING SURVEY BEST PRACTICES AND BENCHMARKING FOR YOUR BSA/AML PROGRAM Anti-money laundering (AML) regulations are at times challenging for banks. Emerging risks and increased scrutiny

Risk Assessment - Balancing Risk While Enhancing Controls

Risk Assessment - Balancing Risk While Enhancing Controls cliftonlarsonallen.com Session Objectives Define risk and risk assessment. Execution of assessment and approach Impact on controls and future state

Risk Assessment - Balancing Risk While Enhancing Controls cliftonlarsonallen.com Session Objectives Define risk and risk assessment. Execution of assessment and approach Impact on controls and future state

PAYMENTS PROCESSING ITEM CAPTURE & PROCESSING. Dynamic Solutions. Superior Results.

PAYMENTS PROCESSING ITEM CAPTURE & PROCESSING Dynamic Solutions. Superior Results. KEEP PACE WITH RAPIDLY CHANGING ITEM CAPTURE AND PROCESSING TECHNOLOGIES WITH OUR INNOVATIVE SUITE OF SOLUTIONS IMPLEMENT

PAYMENTS PROCESSING ITEM CAPTURE & PROCESSING Dynamic Solutions. Superior Results. KEEP PACE WITH RAPIDLY CHANGING ITEM CAPTURE AND PROCESSING TECHNOLOGIES WITH OUR INNOVATIVE SUITE OF SOLUTIONS IMPLEMENT

STAR Network Overview

STAR Network Overview Presented by: Jeff Jakopec, Sr. Strategy Business Development September 26, 2017 What Differentiates STAR Network From the Rest STAR provides market leading fraud solutions that help

STAR Network Overview Presented by: Jeff Jakopec, Sr. Strategy Business Development September 26, 2017 What Differentiates STAR Network From the Rest STAR provides market leading fraud solutions that help

LI & FUNG LIMITED ANNUAL REPORT 2016

52 Our approach to risk management We maintain a sound and effective system of risk management and internal controls to support us in achieving high standards of corporate governance. Our approach to risk

52 Our approach to risk management We maintain a sound and effective system of risk management and internal controls to support us in achieving high standards of corporate governance. Our approach to risk

Dealing with Duplicates 3-Part Session Series -Session #2- Operational Considerations

ealing with uplicates 3-Part Session Series -Session #2- Operational Considerations Phyllis Meyerson, AAP, CCM Executive Vice President, ECCHO Ellen Heffner, NCP irector, Product Management, ECCHO John

ealing with uplicates 3-Part Session Series -Session #2- Operational Considerations Phyllis Meyerson, AAP, CCM Executive Vice President, ECCHO Ellen Heffner, NCP irector, Product Management, ECCHO John

VENDOR MANAGEMENT 101

VENDOR MANAGEMENT 101 Enterprise Risk Management Vendor Management Business Continuity IT GRC Internal Audit Regulatory Compliance Manager Introduction to Vendor Management About Your Presenter Andrea

VENDOR MANAGEMENT 101 Enterprise Risk Management Vendor Management Business Continuity IT GRC Internal Audit Regulatory Compliance Manager Introduction to Vendor Management About Your Presenter Andrea

Products. Commercial Banking Attract, Retain and Grow Profitable Business Relationships in a Highly Competitive Environment

Products Commercial Banking Attract, Retain and Grow Profitable Business Relationships in a Highly Competitive Environment Products Each year, U.S. financial institutions are devoting more of their IT

Products Commercial Banking Attract, Retain and Grow Profitable Business Relationships in a Highly Competitive Environment Products Each year, U.S. financial institutions are devoting more of their IT

Bank Secrecy Act Training: Who, What, When, How and Why? Presented by Lynn English Lafayette Federal Credit Union

Bank Secrecy Act Training: Who, What, When, How and Why? Presented by Lynn English Lafayette Federal Credit Union Key Takeaways After this webinar, participants should have an understanding of minimum

Bank Secrecy Act Training: Who, What, When, How and Why? Presented by Lynn English Lafayette Federal Credit Union Key Takeaways After this webinar, participants should have an understanding of minimum

RDC as a Receivables Platform

RDC as a Receivables Platform September 28, 2012 Blaine Carnprobst Managing Director, Receivables BNY Mellon Sam Golbach Senior Vice President WAUSAU Financial Systems Ed McLaughlin RemoteDepositCapture.com

RDC as a Receivables Platform September 28, 2012 Blaine Carnprobst Managing Director, Receivables BNY Mellon Sam Golbach Senior Vice President WAUSAU Financial Systems Ed McLaughlin RemoteDepositCapture.com

A Guide to IT Risk Assessment for Financial Institutions. March 2, 2011

A Guide to IT Risk Assessment for Financial Institutions March 2, 2011 Welcome! Housekeeping Control panel on the right side of your screen. Audio Telephone VoIP Submit Questions in the pane on the control

A Guide to IT Risk Assessment for Financial Institutions March 2, 2011 Welcome! Housekeeping Control panel on the right side of your screen. Audio Telephone VoIP Submit Questions in the pane on the control

Vendor Management Challenges and Expectations An Open Discussion April 13, 2017

1 Practical solutions driving tangible results Vendor Management Challenges and Expectations An Open Discussion April 13, 2017 Agenda Common Themes Discussion Expectations Overcoming Obstacles Common Comments

1 Practical solutions driving tangible results Vendor Management Challenges and Expectations An Open Discussion April 13, 2017 Agenda Common Themes Discussion Expectations Overcoming Obstacles Common Comments

Customer Due Diligence A Risk Based Approach. Dr Tony Wicks Director of AML Solutions NICE Actimize

Customer Due Diligence A Risk Based Approach Dr Tony Wicks Director of AML Solutions NICE Actimize tony.wicks@actimize.com PLEASE NOTE that, to the extent that Actimize provides, in this presentation or

Customer Due Diligence A Risk Based Approach Dr Tony Wicks Director of AML Solutions NICE Actimize tony.wicks@actimize.com PLEASE NOTE that, to the extent that Actimize provides, in this presentation or

Image-Based Item Processing Solution

Image-Based Item Processing Solution Image-Based Item Processing Solution The Powerful ActiveView Item Processing Improved efficiency Scalable configuration for any size institution Increased productivity

Image-Based Item Processing Solution Image-Based Item Processing Solution The Powerful ActiveView Item Processing Improved efficiency Scalable configuration for any size institution Increased productivity

Questions and Answers Request for Proposal for Banking Services

Questions and Answers Request for Proposal for Banking Services Date: March 14, 2018 Q: Can you provide a copy of the RFP in Word for the providers? Especially given the very quick turnaround time (3 weeks),

Questions and Answers Request for Proposal for Banking Services Date: March 14, 2018 Q: Can you provide a copy of the RFP in Word for the providers? Especially given the very quick turnaround time (3 weeks),

Check Products National Check Payments Certification. Check Products. Copyright 2016 by the Electronic Check Clearing House Organization

NCP 2017 Exam Cycle Core Training Series Session 9 Check Products Copyright 2016 by the Electronic Check Clearing House Organization NOTICES This training course may provide an introduction to or summary

NCP 2017 Exam Cycle Core Training Series Session 9 Check Products Copyright 2016 by the Electronic Check Clearing House Organization NOTICES This training course may provide an introduction to or summary

REGULATORY HOT TOPICS FOR INTERNAL AUDITORS: EVALUATING THE USE OF AML TECHNOLOGY

REGULATORY HOT TOPICS FOR INTERNAL AUDITORS: EVALUATING THE USE OF AML TECHNOLOGY Shaheen Dil MANAGING DIRECTOR, PROTIVITI John Atkinson DIRECTOR, PROTIVITI Carl Hatfield DIRECTOR, PROTIVITI Chetan Shah

REGULATORY HOT TOPICS FOR INTERNAL AUDITORS: EVALUATING THE USE OF AML TECHNOLOGY Shaheen Dil MANAGING DIRECTOR, PROTIVITI John Atkinson DIRECTOR, PROTIVITI Carl Hatfield DIRECTOR, PROTIVITI Chetan Shah

Treasury Management Solutions

Sales Support T3 Tech Support Team Live Chat @ www.texasbankandtrust.com 903-237-1881 1-800-263-7013 rev 20431 12/2017 Treasury Management Solutions THE TBT DIFFERENCE Established in 1958, Texas Bank and

Sales Support T3 Tech Support Team Live Chat @ www.texasbankandtrust.com 903-237-1881 1-800-263-7013 rev 20431 12/2017 Treasury Management Solutions THE TBT DIFFERENCE Established in 1958, Texas Bank and

Maximize your Investment in FIS Core Banking Solutions

Maximize your Investment in FIS Core Banking Solutions With Automated Reconciliation Richard Chapman, Vice President, Business Development and Strategy, FIS Reconciliation Business Joseph Vesey, Global

Maximize your Investment in FIS Core Banking Solutions With Automated Reconciliation Richard Chapman, Vice President, Business Development and Strategy, FIS Reconciliation Business Joseph Vesey, Global

Doc P-Card Services Provider RFP

1 of 9 2/29/2016 4:55 PM Go To Dashboard Help Keith Haran Doc706066747 - P-Card Services Provider RFP Prev Next Exit On this page you create the information that participants will read and respond to during

1 of 9 2/29/2016 4:55 PM Go To Dashboard Help Keith Haran Doc706066747 - P-Card Services Provider RFP Prev Next Exit On this page you create the information that participants will read and respond to during

Solutions. Card Risk Management Leverage Our Industry-Leading Solutions and Services to Fight the Rising Cost of Fraud

Solutions Card Risk Management Leverage Our Industry-Leading Solutions and Services to Fight the Rising Cost of Fraud 2 Solutions Debit and credit cards are the payment methods of choice for U.S. consumers.

Solutions Card Risk Management Leverage Our Industry-Leading Solutions and Services to Fight the Rising Cost of Fraud 2 Solutions Debit and credit cards are the payment methods of choice for U.S. consumers.

Integrated Deposit Origination

Integrated Deposit Origination New Functionality and Best Practices Bill Johnson, Development Supervisor Adi Rebronja, ido Implementation May 25th, 2017 Agenda New functionality Masking of TIN and ID Numbers

Integrated Deposit Origination New Functionality and Best Practices Bill Johnson, Development Supervisor Adi Rebronja, ido Implementation May 25th, 2017 Agenda New functionality Masking of TIN and ID Numbers

Sarbanes-Oxley Compliance Kit

Kit February 2018 This product is NOT FOR RESALE or REDISTRIBUTION in any physical or electronic format. The purchaser of this template has acquired the rights to use it for a SINGLE Disaster Recovery

Kit February 2018 This product is NOT FOR RESALE or REDISTRIBUTION in any physical or electronic format. The purchaser of this template has acquired the rights to use it for a SINGLE Disaster Recovery

AML model risk management and validation

AML model risk management and validation Who we are EY s Anti-Money Laundering (AML) and Regulatory Compliance Technology practice is a global team of client-serving, financial services professionals.

AML model risk management and validation Who we are EY s Anti-Money Laundering (AML) and Regulatory Compliance Technology practice is a global team of client-serving, financial services professionals.

Why Businesses Love Payables Lockbox

Why Businesses Love Payables Lockbox (And Yours Should, Too!) A whitepaper examining how businesses can streamline accounts payable processing, reduce payment processing time, and lower accounts payable

Why Businesses Love Payables Lockbox (And Yours Should, Too!) A whitepaper examining how businesses can streamline accounts payable processing, reduce payment processing time, and lower accounts payable

Product. DNA Improved Efficiency, Superior Relationship Management and Unparalleled Flexibility for Innovative Banks and Credit Unions

Product DNA Improved Efficiency, Superior Relationship Management and Unparalleled Flexibility for Innovative Banks and Credit Unions DNA More than ever before, financial services organizations need account

Product DNA Improved Efficiency, Superior Relationship Management and Unparalleled Flexibility for Innovative Banks and Credit Unions DNA More than ever before, financial services organizations need account

CONSULTATION DOCUMENT AML/CFT SUPERVISORY STRATEGY

CONSULTATION DOCUMENT AML/CFT SUPERVISORY STRATEGY Central Bank of The Bahamas Bank Supervision Department December 2017 1 Executive summary The Central Bank of the Bahamas ( the Bank ) regulates and supervises

CONSULTATION DOCUMENT AML/CFT SUPERVISORY STRATEGY Central Bank of The Bahamas Bank Supervision Department December 2017 1 Executive summary The Central Bank of the Bahamas ( the Bank ) regulates and supervises

The top five benefits of outsourcing B2B payments processing

fis integrated payables leave the check behind The top five benefits of outsourcing B2B payments processing Migrating away from checks to electronic payments can help companies reduce costs. However, many

fis integrated payables leave the check behind The top five benefits of outsourcing B2B payments processing Migrating away from checks to electronic payments can help companies reduce costs. However, many

Customer Due Diligence Risk-Based Approach. Dan Soto CCO Ally Financial

Welcome Customer Due Diligence Risk-Based Approach Megan Hodge CCO RBC Bank Dan Soto CCO Ally Financial Agenda Risk Based Approach Customer Risk Scoring Enhanced Due Diligence Case Studies Evolution of

Welcome Customer Due Diligence Risk-Based Approach Megan Hodge CCO RBC Bank Dan Soto CCO Ally Financial Agenda Risk Based Approach Customer Risk Scoring Enhanced Due Diligence Case Studies Evolution of

EMBEDDING THE PAYMENTS PROCESS: 3 STEPS FOR INTEGRATION AN EBOOK BY

EMBEDDING THE PAYMENTS PROCESS: 3 STEPS FOR INTEGRATION AN EBOOK BY TABLE OF CONTENTS Intended Audience... 3 Introduction... 4 Step 1: Choose an Onboarding Method... 10 Step 2: Determine Transaction Processing

EMBEDDING THE PAYMENTS PROCESS: 3 STEPS FOR INTEGRATION AN EBOOK BY TABLE OF CONTENTS Intended Audience... 3 Introduction... 4 Step 1: Choose an Onboarding Method... 10 Step 2: Determine Transaction Processing

REMOTE DEPOSIT CAPTURE (RDC) CHECK IMAGING AT THE ATM

CHECK IMAGING AT THE ATM") REMOTE DEPOSIT CAPTURE (RDC) CHECK IMAGING AT THE ATM Part of NCR s enterprise hub for remote deposit capture For more information visit ncr.com or contact us at financial@ncr.com Better check deposits

REMOTE DEPOSIT CAPTURE (RDC) CHECK IMAGING AT THE ATM Part of NCR s enterprise hub for remote deposit capture For more information visit ncr.com or contact us at financial@ncr.com Better check deposits

REMOTE DEPOSIT CAPTURE (RDC) CHEQUE IMAGING AT THE ATM PART OF NCR S ENTERPRISE HUB FOR REMOTE DEPOSIT CAPTURE

CHEQUE IMAGING AT THE ATM PART OF NCR S ENTERPRISE HUB FOR REMOTE DEPOSIT CAPTURE") REMOTE DEPOSIT CAPTURE (RDC) CHEQUE IMAGING AT THE ATM PART OF NCR S ENTERPRISE HUB FOR REMOTE DEPOSIT CAPTURE For more information, visit ncr.com, or email ncr.financial@ncr.com. BETTER CHEQUE DEPOSITS

REMOTE DEPOSIT CAPTURE (RDC) CHEQUE IMAGING AT THE ATM PART OF NCR S ENTERPRISE HUB FOR REMOTE DEPOSIT CAPTURE For more information, visit ncr.com, or email ncr.financial@ncr.com. BETTER CHEQUE DEPOSITS

BSA/AML Self-Assessment Tool. Overview and Instructions

BSA/AML Self-Assessment Tool Overview and Instructions February 2018 1129 20 th Street, N.W. Ninth Floor Washington, DC 20036 www.csbs.org 202-296-2840 FAX 202-296-1928 2 Introduction and Overview The

BSA/AML Self-Assessment Tool Overview and Instructions February 2018 1129 20 th Street, N.W. Ninth Floor Washington, DC 20036 www.csbs.org 202-296-2840 FAX 202-296-1928 2 Introduction and Overview The

Prince William County, Virginia

Prince William County, Virginia Internal Audit of Procurement Card Management Fiscal Year 2014/2015 Prepared By: Internal Auditors June 29, 2015 Table of Contents Transmittal Letter... 1 Executive Summary...

Prince William County, Virginia Internal Audit of Procurement Card Management Fiscal Year 2014/2015 Prepared By: Internal Auditors June 29, 2015 Table of Contents Transmittal Letter... 1 Executive Summary...

EXAMINATION OF CERTAIN FINANCIAL PROCESSES AND INTERNAL CONTROLS OF THE KENTUCKY CORRECTIONAL INDUSTRIES

EXAMINATION OF CERTAIN FINANCIAL PROCESSES AND INTERNAL CONTROLS OF THE KENTUCKY CORRECTIONAL INDUSTRIES CRIT LUALLEN AUDITOR OF PUBLIC ACCOUNTS www.auditor.ky.gov 105 SEA HERO ROAD, SUITE 2 FRANKFORT,

EXAMINATION OF CERTAIN FINANCIAL PROCESSES AND INTERNAL CONTROLS OF THE KENTUCKY CORRECTIONAL INDUSTRIES CRIT LUALLEN AUDITOR OF PUBLIC ACCOUNTS www.auditor.ky.gov 105 SEA HERO ROAD, SUITE 2 FRANKFORT,

Index of Tables. General Information. New Account Application Review. Customer Authentication

Index of Tables Table Number Page General Information 1 For which units in your banking organization are you reporting the information?... 79 2 Your total banking assets and deposits for the units included

Index of Tables Table Number Page General Information 1 For which units in your banking organization are you reporting the information?... 79 2 Your total banking assets and deposits for the units included

RISK MANAGEMENT IN ELECTRONIC PAYMENTS. Olutimilehin Oyesanya (Phillips Consulting) CISSP, CISA, COBIT 5 Assessor, PMP, ISO LA, ISO LI

CISSP, CISA, COBIT 5 Assessor, PMP, ISO LA, ISO LI") RISK MANAGEMENT IN ELECTRONIC PAYMENTS Olutimilehin Oyesanya (Phillips Consulting) CISSP, CISA, COBIT 5 Assessor, PMP, ISO 27001 LA, ISO 20000 LI Phillips Consulting Who we are Our Technology Division

RISK MANAGEMENT IN ELECTRONIC PAYMENTS Olutimilehin Oyesanya (Phillips Consulting) CISSP, CISA, COBIT 5 Assessor, PMP, ISO 27001 LA, ISO 20000 LI Phillips Consulting Who we are Our Technology Division

Fed Consultation Paper Association for Financial Professionals (AFP) Response

Response") Fed Consultation Paper Association for Financial Professionals (AFP) Response Q1: Are you in general agreement with the payment system gaps and opportunities identified? What other gaps or opportunities

Fed Consultation Paper Association for Financial Professionals (AFP) Response Q1: Are you in general agreement with the payment system gaps and opportunities identified? What other gaps or opportunities