Pre-Engagement Activities and Audit Planning By: Tariq Mahmood FCA, ACMA

|

|

|

- Sharon Peters

- 6 years ago

- Views:

Transcription

1 Model Audit Practice Manual Pre-Engagement Activities and Audit Planning By: Tariq Mahmood FCA, ACMA

2 Today s Learnings Pre-Engagement Activities Audit Planning Procedures Completion of Sample Forms (Annexures)

3 Objective of the Manual To provide guidance to the practicing members through all the stages of an audit (financial as well as cost audit) i.e. Planning of audit; Assessment of risk and determination of materiality; Analytical reviews; Execution and detailed audit programs; and Reporting.

4 Pre-Engagement Activities

5 Pre-Engagement Activities Client Acceptance / Continuance Communication with Predecessor Auditors (NOC) New Client (Associated Risks) Compliance with Independence and Ethical Requirements Engagement Letters Handling with Changes in Terms of Engagement Lack of Knowledge of Business No Previous Experience with Management Transactions and Associated Risks affecting the statements

6 Client Acceptance / Continuance Consider Nature and Purpose of Engagement Do We Want This Client? Can We Effectively Perform This Audit? Research the Client Assess Client Reputation, Integrity and Competence Sources of such information are: Entity Website Third parties i.e. bankers, advisors, industry peers etc. Background searchers of relevant pears Identity and business reputation of principal owners and key management Nature of operations Attitude of principal owners and key management towards accounting standards, internal control environment Client s concern with maintaining the fee as low as possible Indication of scope limitations Reasons for change of auditors Identity and business reputation of related parties

7 Client Acceptance / Continuance Assess the Firm s Resources and Competence Knowledge of relevant industries or subject matter Experience with relevant regulatory or reporting requirements Sufficient personal with competence or ability to gain the necessary skills and knowledge effectively Experts are available Ability to complete engagement within reporting time Other Risk Concerns (Form 001 & 002 at Appendices)

8 Communication with Predecessor Auditors Process Initiated by the Successor Auditor Client Permission is Required to Initiate the Contact as well as for the Predecessor to respond to the inquiry Conduct Interview with the Partner and Manager In-charge Discuss Risk Areas Obtain Copies of some or all of audit documentation Predecessor auditor may be able to provide information that will assist the successor auditor in determining whether to accept the engagement. The successor auditor should bear in mind that, among other things the predecessor auditor and the client may have disagreed about : accounting principles, auditing procedures, or similarly significant matters.

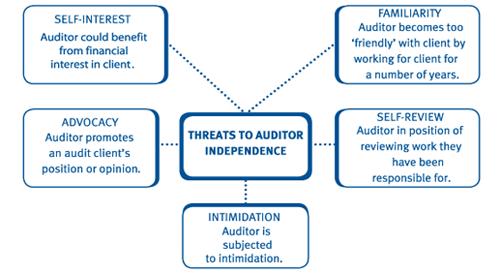

9 Compliance with Independence / Ethical Requirements Integrity; Objectivity; Professional Competence and Due Care; Confidentiality; and The Fundamental Principles are reinforced by: The Leadership of the Firm; Education and Training; Monitoring; and A process of dealing with non-compliance Professional Behavior;

10

11 Engagement Letter Formal Contract (ISA 210) Objective and Scope of Audit Responsibilities of Auditor Responsibilities of Management Applicable Reporting Framework Expected Deliverables Timeline and Fee Management Acknowledgement for Preparation of Statements Management Acknowledgement for Internal Controls Access to Records Consider not accepting engagement in case of limitation on scope

12 Handling with Changes in Terms of Engagement Change Request by Client or by Auditor Evaluate the Changes for Acceptance / Rejection Bring in Writing Due to Circumstance Affecting the Entity s Environment Due to Misunderstanding Concerning the Nature of Service Originally Requested Not Justified if relating to Information being Incorrect / Unsatisfactory Withdraw from audit engagement where possible under applicable laws; and Determine whether there is any obligation to report the circumstances to stakeholders, such as regulators or executive management.

13 Audit Planning Procedures

14 Audit Planning Importance Successful Execution and Completion of Engagement Proper Organization and Management of Engagement Selection of Team Members with Required Capabilities Efficient and Complete Delivery of Professional Responsibilities

15 Audit Planning Purpose Understanding of Entity s Business, Industry & Environment Understanding of Accounting Policies and Practices / Financial Performance Assessment of Risk of Material Misstatement Formulate Overall Audit Strategy Planned Audit Approach for Significant Account Balances and Disclosures Determine Materiality Plan Staff

16 Overall Audit Strategy Kick of Meeting with Client Management Define and Agree Scope of Engagement Ascertain Reporting Objectives and Decide Timing of Activities Assess Nature and Timing of Communication Required with Client Select Team, Team Meetings and Communication Apply Risk Assessment Procedures Use Knowledge from Preliminary Assessment Determine Involvement on Other Other Significant Matters

17 Risk Assessment Procedures Inquiries about the entity s business and control environment from: Those Charged with Governance and Management Internal Audit Key Staff Involved in Transaction Initiating and Processing In-house Legal Council, if any Internal Tax Staff Analytical Procedures to Identify Unusual Transactions / Events Observations of Entity Environment Inspection of Documents and Management Reports Information from Prior Period Audits - Corrections / Adjustments Discussion among Team Members Use SWOT and PEST Analysis (Form 003 at Appendices)

18 Key Information About Client Nature of Business and History Product and Services Client Profile Major Customer Major Suppliers Corporate Structure and Conduct of Operations Objectives of Business Entity s Industrial Environment Legal and Regulatory Environment Employees Investments Financing Related Parties Litigations and Claims

19 Business Control Environment Legal and Operating Structure Culture of the Client s Entity Ethics Adapted by Entity Corporate Governance Environment Remuneration of Management Personal Profile of Management

20 Computer Information System Level of Dependence on CIS CIS Personnel Structure and Skills Security and Access Controls Back-ups and Recovery Procedures Reliability of CIS Data Integrity Data Processing and Reporting Controls (Form 007 of Appendices)

21 Reporting Environment Applicable Reporting Framework Approved Management Reporting Guidelines Selection and Application of Accounting Policies Critical Accounting Policies Impact of Policies on Specific Aspects of Statements Reconciliation with Financial Records Key Issues: New Accounting Pronouncements Going Concern Legal and Regulatory Changes Financial / Cost Analysis and Results

22 Critical Areas and Expert Involvement Identify Critical Areas Significant Estimates Decommissioning etc. Property Valuations Employee Benefits Actuaries Nature of Inventory Investment Valuations (Form 004 at Appendices for Critical Areas )

23 Control Overview (Form 005 at Appendices)

24

25 Determine Audit Materiality ISA 320 Use Professional Judgment Consider Both Qualitative and Quantitative Aspects Calculate using Quantitative Approach (%) Example are: Financial Statement Level Account Balance Level Transaction Level Performance Based

26

27 Fraud Risk Assessment - ISA 240, 315 and 330 Professional Skepticism Identify Risk of Material Misstatement Use Analytical Procedures for Risk Assessment Obtain Appropriate Audit Evidence Discussion among Engagement Partner and Team Discussion with Management Obtain Written Representations for: Responsibility for design and implementation of internal controls Disclosure to Auditor of result of their assessments Disclosure about their knowledge of fraud Disclosure about their knowledge of any allegations for fraud (Form 006 and 008 in Appendices)

28 Example of Financial Statement Level Fraud Risk Factors Incentives and Pressures Excessive Pressure to Meet Third Party Expectations Unrealistic profitability expectations Critical need for funding to stay competitive or to repay debt Transactions without economic justifications Potential to adversely impact pending transactions Overly optimistic press releases Threats to Financial Stability of Profitability Competition / market saturation Bankruptcy / take over threat Cash / funding gap, Declining industry New accounting, regulatory or statutory requirements

29 Example of Financial Statement Level Fraud Risk Factors Incentives and Pressures Threats to Personal Financial Position Compensation contingent on achieving aggressive targets Significant financial interest / personal guarantees Pressures to Meet Financial Targets Excessive pressure to meet targets through sales or profitability incentives Inappropriate accounting estimates Aggressive forecasts

30 Example of Financial Statement Level Fraud Risk Factors Opportunities Ineffective Monitoring of Management Dominance / aggressive management style Ineffective oversight by the Board Internal Control Components are Deficient Ineffective systems and controls Inadequate monitoring / ineffective application of controls History of significant adjustments Ineffective staff

31 Example of Financial Statement Level Fraud Risk Factors Opportunities Nature of Industry or Entity s Operations Significant unusual or highly complex transactions Estimates involving significant judgment or uncertainties difficult to corroborate Overly complex banking arrangements Significant related party transactions Use of intermediaries Complex or Unstable Organization Structure Unexplained turn over of senior management Controlling interest unclear Overly complex corporate structure

32 Example of Assertion Level Fraud Risk Factors Revenue False sales and customers Advancing or delaying revenue Manipulation of rebates and discounts Misrepresentation of credit status Under / over provisioning for bad debts Expenses Under / over accruals Delaying or advancing expenses Manipulation of rebates and discounts Misrecording of capital items Hidden contract terms

33 Example of Assertion Level Fraud Risk Factors Cash False cash entries Hidden pledges of cash deposits Teaming and lading or lapping Inventory Standard cost manipulations False ownership status False quantity False quality False valuation

34 Example of Assertion Level Fraud Risk Factors Others Misuse of merger reserves Manipulation of transfer pricing Manipulation of joint ventures Improper valuation of assets Misuse of inter-company and suspense accounts

(Use Form 011) (Use Form 012) (Use Form")

35 Other Considerations Evaluate Internal Audit Function Review Points Brought Forward Plan Staff and Allocate Time Group Audit (Use Form 009) (Use Form 011) (Use Form 012) (Use Form 010)

Related Party Transactions (Use Form 042) Subsequent Events (Use")

36 Specific Topics Compliance with Laws and Regulations (Use Form 037) Going Concern Assumption (Use Form 038) Related Party Transactions (Use Form 042) Subsequent Events (Use Form 048)

37

FRAUD RISK FACTORS CHECKLIST (Source: New AU Section 240, Appendix A)

") Page 136 of 174 FRAUD RISK FACTORS CHECKLIST (Source: New AU Section 240, Appendix A) RECOGNIZING RISK FACTORS THAT SHOULD GET YOUR ATTENTION How to use the checklist: 1. Review this checklist towards

Page 136 of 174 FRAUD RISK FACTORS CHECKLIST (Source: New AU Section 240, Appendix A) RECOGNIZING RISK FACTORS THAT SHOULD GET YOUR ATTENTION How to use the checklist: 1. Review this checklist towards

Chapter 06. Audit Planning, Understanding the Client, Assessing Risks, and Responding. McGraw-Hill/Irwin

Chapter 06 Audit Planning, Understanding the Client, Assessing Risks, and Responding McGraw-Hill/Irwin Copyright 2012 by The McGraw-Hill Companies, Inc. All rights reserved. Obtaining Clients Submit a

Chapter 06 Audit Planning, Understanding the Client, Assessing Risks, and Responding McGraw-Hill/Irwin Copyright 2012 by The McGraw-Hill Companies, Inc. All rights reserved. Obtaining Clients Submit a

INTERNATIONAL STANDARD ON AUDITING 260 COMMUNICATION WITH THOSE CHARGED WITH GOVERNANCE CONTENTS

Introduction INTERNATIONAL STANDARD ON AUDITING 260 COMMUNICATION WITH THOSE CHARGED WITH GOVERNANCE (Effective for audits of financial statements for periods beginning on or after December 15, 2009) +

Introduction INTERNATIONAL STANDARD ON AUDITING 260 COMMUNICATION WITH THOSE CHARGED WITH GOVERNANCE (Effective for audits of financial statements for periods beginning on or after December 15, 2009) +

CPA REVIEW SCHOOL OF THE PHILIPPINES M a n i l a AUDITING THEORY AUDIT PLANNING

CPA REVIEW SCHOOL OF THE PHILIPPINES M a n i l a Related PSAs: PSA 300, 310, 320, 520 and 570 Appointment of the Independent Auditor AUDITING THEORY AUDIT PLANNING Page 1 of 9 Early appointment of the

CPA REVIEW SCHOOL OF THE PHILIPPINES M a n i l a Related PSAs: PSA 300, 310, 320, 520 and 570 Appointment of the Independent Auditor AUDITING THEORY AUDIT PLANNING Page 1 of 9 Early appointment of the

REGISTERED CANDIDATE AUDITOR (RCA) TECHNICAL COMPETENCE REQUIREMENTS

TECHNICAL COMPETENCE REQUIREMENTS") REGISTERED CANDIDATE AUDITOR (RCA) TECHNICAL COMPETENCE REQUIREMENTS 1. Context After completion of the recognised training contract, a period of specialisation is required, appropriate to the level required

REGISTERED CANDIDATE AUDITOR (RCA) TECHNICAL COMPETENCE REQUIREMENTS 1. Context After completion of the recognised training contract, a period of specialisation is required, appropriate to the level required

International Standard on Auditing (Ireland) 315

315") International Standard on Auditing (Ireland) 315 Identifying and Assessing the Risks of Material Misstatement Through Understanding the Entity and its Environment MISSION To contribute to Ireland having

International Standard on Auditing (Ireland) 315 Identifying and Assessing the Risks of Material Misstatement Through Understanding the Entity and its Environment MISSION To contribute to Ireland having

(Effective for audits of financial statements for periods ending on or after December 15, 2013) CONTENTS

CONTENTS") INTERNATIONAL STANDARD ON AUDITING 315 (REVISED) IDENTIFYING AND ASSESSING THE RISKS OF MATERIAL MISSTATEMENT THROUGH UNDERSTANDING THE ENTITY AND ITS ENVIRONMENT Introduction (Effective for audits of

INTERNATIONAL STANDARD ON AUDITING 315 (REVISED) IDENTIFYING AND ASSESSING THE RISKS OF MATERIAL MISSTATEMENT THROUGH UNDERSTANDING THE ENTITY AND ITS ENVIRONMENT Introduction (Effective for audits of

Identifying and Assessing the Risks of Material Misstatement through Understanding the Entity and Its Environment

ISA 315 (Revised) Issued September 2012; updated February 2018 International Standard on Auditing Identifying and Assessing the Risks of Material Misstatement through Understanding the Entity and Its Environment

ISA 315 (Revised) Issued September 2012; updated February 2018 International Standard on Auditing Identifying and Assessing the Risks of Material Misstatement through Understanding the Entity and Its Environment

IAASB CAG Public Session (March 2018) CONFORMING AND CONSEQUENTIAL AMENDMENTS ARISING FROM DRAFT PROPOSED ISA 540 (REVISED) 1

CONFORMING AND CONSEQUENTIAL AMENDMENTS ARISING FROM DRAFT PROPOSED ISA 540 (REVISED) 1") Agenda Item B.4 CONFORMING AND CONSEQUENTIAL AMENDMENTS ARISING FROM DRAFT PROPOSED ISA 540 (REVISED) 1 ISA 200, Overall Objectives of the Independent Auditor and the Conduct of an Audit in Accordance

Agenda Item B.4 CONFORMING AND CONSEQUENTIAL AMENDMENTS ARISING FROM DRAFT PROPOSED ISA 540 (REVISED) 1 ISA 200, Overall Objectives of the Independent Auditor and the Conduct of an Audit in Accordance

CPA REVIEW SCHOOL OF THE PHILIPPINES M a n i l a. AUDITING THEORY Risk Assessment and Response to Assessed Risks

Page 1 of 7 CPA REVIEW SCHOOL OF THE PHILIPPINES M a n i l a Related PSAs: PSA 400, 315 and 330 AUDITING THEORY Risk Assessment and Response to Assessed Risks 1. Which of the following is correct statement?

Page 1 of 7 CPA REVIEW SCHOOL OF THE PHILIPPINES M a n i l a Related PSAs: PSA 400, 315 and 330 AUDITING THEORY Risk Assessment and Response to Assessed Risks 1. Which of the following is correct statement?

SRI LANKA AUDITING STANDARD 260 COMMUNICATION WITH THOSE CHARGED WITH GOVERNANCE CONTENTS

SRI LANKA AUDITING STANDARD 260 COMMUNICATION WITH THOSE CHARGED WITH GOVERNANCE Introduction (Effective for audits of financial statements for periods beginning on or after 01 January 2012) CONTENTS Paragraph

SRI LANKA AUDITING STANDARD 260 COMMUNICATION WITH THOSE CHARGED WITH GOVERNANCE Introduction (Effective for audits of financial statements for periods beginning on or after 01 January 2012) CONTENTS Paragraph

VERSION #1 WRITE ON YOUR SCANTRON!!!

ECON 132A WINTER 2009 MIDTERM #2 Name: Date: ANSWER ALL MULTIPLE CHOICE QUESTIONS ON GREEN SCANTRON ANSWER QUESTIONS 29 & 30 IN THE SPACE PROVIDED ANSWER THE SIMULATION ASSIGNMENT IN YOUR BLUE-BOOK, PUT

ECON 132A WINTER 2009 MIDTERM #2 Name: Date: ANSWER ALL MULTIPLE CHOICE QUESTIONS ON GREEN SCANTRON ANSWER QUESTIONS 29 & 30 IN THE SPACE PROVIDED ANSWER THE SIMULATION ASSIGNMENT IN YOUR BLUE-BOOK, PUT

International Standard on Auditing (UK) 315 (Revised June 2016)

315 (Revised June 2016)") Standard Audit and Assurance Financial Reporting Council June 2016 International Standard on Auditing (UK) 315 (Revised June 2016) Identifying and Assessing the Risks of Material Misstatement Through Understanding

Standard Audit and Assurance Financial Reporting Council June 2016 International Standard on Auditing (UK) 315 (Revised June 2016) Identifying and Assessing the Risks of Material Misstatement Through Understanding

IAASB Main Agenda (March 2005) Page Agenda Item 12-C

Page Agenda Item 12-C") IAASB Main Agenda (March 2005) Page 2005 429 Agenda Item 12-C [ISA AND IAPS SPLIT] PROPOSED INTERNATIONAL AUDITING PRACTICE STATEMENT XXX THE APPLICATION OF INTERNATIONAL STANDARDS ON AUDITING IN AN AUDIT

IAASB Main Agenda (March 2005) Page 2005 429 Agenda Item 12-C [ISA AND IAPS SPLIT] PROPOSED INTERNATIONAL AUDITING PRACTICE STATEMENT XXX THE APPLICATION OF INTERNATIONAL STANDARDS ON AUDITING IN AN AUDIT

and Assessing the Risks of Material Misstatement through Understanding the Entity and Its Environment

IFACIAAS Board IAASB Main Agenda (April 2013) Agenda Iten 5-D Final Pronouncement March 2012 International Standard on Auditing ISA 315 (Revised), Identifying and Assessing the Risks of Material Misstatement

IFACIAAS Board IAASB Main Agenda (April 2013) Agenda Iten 5-D Final Pronouncement March 2012 International Standard on Auditing ISA 315 (Revised), Identifying and Assessing the Risks of Material Misstatement

SUGGESTED SOLUTIONS Audit and Assurance. Certificate in Accounting and Business II Examination March 2014

SUGGESTED SOLUTIONS 06204 - Audit and Assurance Certificate in Accounting and Business II Examination March 2014 THE INSTITUTE OF CHARTERED ACCOUNTANTS OF SRI LANKA All Rights Reserved Answer No. 01 (i)

SUGGESTED SOLUTIONS 06204 - Audit and Assurance Certificate in Accounting and Business II Examination March 2014 THE INSTITUTE OF CHARTERED ACCOUNTANTS OF SRI LANKA All Rights Reserved Answer No. 01 (i)

SRI LANKA AUDITING STANDARD 315 (REVISED)

") SRI LANKA AUDITING STANDARD 315 (REVISED) IDENTIFYING AND ASSESSING THE RISKS OF MATERIAL MISSTATEMENT THROUGH UNDERSTANDING THE ENTITY AND ITS ENVIRONMENT (Effective for audits of financial statements

SRI LANKA AUDITING STANDARD 315 (REVISED) IDENTIFYING AND ASSESSING THE RISKS OF MATERIAL MISSTATEMENT THROUGH UNDERSTANDING THE ENTITY AND ITS ENVIRONMENT (Effective for audits of financial statements

ISA 240 (Redrafted), The Auditor s Responsibilities Relating to Fraud in an Audit of Financial Statements

, The Auditor s Responsibilities Relating to Fraud in an Audit of Financial Statements") CONFORMING AMENDMENTS TO OTHER STANDARDS AS A RESULT OF ISA 265, COMMUNICATING DEFICIENCIES IN INTERNAL CONTROL TO THOSE CHANGED WITH GOVERNANCE AND MANAGEMENT ISA 240 (Redrafted), The Auditor s Responsibilities

CONFORMING AMENDMENTS TO OTHER STANDARDS AS A RESULT OF ISA 265, COMMUNICATING DEFICIENCIES IN INTERNAL CONTROL TO THOSE CHANGED WITH GOVERNANCE AND MANAGEMENT ISA 240 (Redrafted), The Auditor s Responsibilities

Understanding the Entity and Its Environment and Assessing the Risks of Material Misstatement

Issued December 2007 International Standard on Auditing Understanding the Entity and Its Environment and Assessing the Risks of Material Misstatement The Malaysian Institute of Certified Public Accountants

Issued December 2007 International Standard on Auditing Understanding the Entity and Its Environment and Assessing the Risks of Material Misstatement The Malaysian Institute of Certified Public Accountants

International Standard on Auditing (Ireland) 300. Planning an Audit of Financial Statements

300. Planning an Audit of Financial Statements") International Standard on Auditing (Ireland) 300 Planning an Audit of Financial Statements MISSION To contribute to Ireland having a strong regulatory environment in which to do business by supervising

International Standard on Auditing (Ireland) 300 Planning an Audit of Financial Statements MISSION To contribute to Ireland having a strong regulatory environment in which to do business by supervising

Audit Quality Assurance workshop Audit Planning by: CPA Steve Obock Associate Director- KPMG Kenya March 2017

Audit Quality Assurance workshop Audit Planning by: CPA Steve Obock Associate Director- KPMG Kenya March 2017 Uphold public interest Agenda Introduction Developing an audit strategy Setting audit materiality

Audit Quality Assurance workshop Audit Planning by: CPA Steve Obock Associate Director- KPMG Kenya March 2017 Uphold public interest Agenda Introduction Developing an audit strategy Setting audit materiality

Mapping of Original ISA 315 to New ISA 315 s Standards and Application Material (AM) Agenda Item 2-C

Agenda Item 2-C") Mapping of to 315 s and Application Material (AM) Agenda Item 2-C AM 1. The purpose of this International Standard on Auditing (ISA) is to establish standards and to provide guidance on obtaining an understanding

Mapping of to 315 s and Application Material (AM) Agenda Item 2-C AM 1. The purpose of this International Standard on Auditing (ISA) is to establish standards and to provide guidance on obtaining an understanding

INTERNATIONAL STANDARD ON AUDITING 315 UNDERSTANDING THE ENTITY AND ITS ENVIRONMENT AND ASSESSING THE RISKS OF MATERIAL MISSTATEMENT CONTENTS

INTERNATIONAL STANDARD ON AUDITING 315 UNDERSTANDING THE ENTITY AND ITS ENVIRONMENT AND ASSESSING THE RISKS OF MATERIAL MISSTATEMENT (Effective for audits of financial statements for periods beginning

INTERNATIONAL STANDARD ON AUDITING 315 UNDERSTANDING THE ENTITY AND ITS ENVIRONMENT AND ASSESSING THE RISKS OF MATERIAL MISSTATEMENT (Effective for audits of financial statements for periods beginning

International Standard on Auditing (Ireland) 500 Audit Evidence

500 Audit Evidence") International Standard on Auditing (Ireland) 500 Audit Evidence MISSION To contribute to Ireland having a strong regulatory environment in which to do business by supervising and promoting high quality

International Standard on Auditing (Ireland) 500 Audit Evidence MISSION To contribute to Ireland having a strong regulatory environment in which to do business by supervising and promoting high quality

Professional Competence for Engagement Partners Responsible for Audits of Financial Statements (Revised)

") IFAC Board Final Pronouncement December 2014 International Education Standard (IES ) 8 Professional Competence for Engagement Partners Responsible for Audits of Financial Statements (Revised) This document

IFAC Board Final Pronouncement December 2014 International Education Standard (IES ) 8 Professional Competence for Engagement Partners Responsible for Audits of Financial Statements (Revised) This document

McGraw-Hill/Irwin. Copyright 2013 by The McGraw-Hill Companies, Inc. All rights reserved.

McGraw-Hill/Irwin Copyright 2013 by The McGraw-Hill Companies, Inc. All rights reserved. Chapter 03 Engagement Planning "Vision without action is a daydream. Action without vision is a nightmare. Japanese

McGraw-Hill/Irwin Copyright 2013 by The McGraw-Hill Companies, Inc. All rights reserved. Chapter 03 Engagement Planning "Vision without action is a daydream. Action without vision is a nightmare. Japanese

International Standard on Auditing (UK and Ireland) 500

500") Standard Audit and Assurance Financial Reporting Council October 2009 International Standard on Auditing (UK and Ireland) 500 Audit evidence The FRC is responsible for promoting high quality corporate

Standard Audit and Assurance Financial Reporting Council October 2009 International Standard on Auditing (UK and Ireland) 500 Audit evidence The FRC is responsible for promoting high quality corporate

TOPIC 11: PRE APPOINTMENT PROCEDURES - LETTER OF ENGAGEMENT

TOPIC 11: PRE APPOINTMENT PROCEDURES - LETTER OF ENGAGEMENT Acceptance of Audit and Review Assignments The Audit Appointment Process 1 The First Steps when offered a new Audit Project is sometimes referred

TOPIC 11: PRE APPOINTMENT PROCEDURES - LETTER OF ENGAGEMENT Acceptance of Audit and Review Assignments The Audit Appointment Process 1 The First Steps when offered a new Audit Project is sometimes referred

IAASB Main Agenda (March 2019) Agenda Item

Agenda Item") Agenda Item 8 B (For Reference) INTERNATIONAL STANDARD ON AUDTING (ISA) 500, AUDIT EVIDENCE (INCLUDING CONSEQUENTIAL AND CONFORMING AMENDMENTS FROM ISA 540 (REVISED) 1 ) Introduction Scope of this ISA

Agenda Item 8 B (For Reference) INTERNATIONAL STANDARD ON AUDTING (ISA) 500, AUDIT EVIDENCE (INCLUDING CONSEQUENTIAL AND CONFORMING AMENDMENTS FROM ISA 540 (REVISED) 1 ) Introduction Scope of this ISA

SRI LANKA AUDITING STANDARD 300 PLANNING AN AUDIT OF FINANCIAL STATEMENTS CONTENTS

SRI LANKA AUDITING STANDARD 300 PLANNING AN AUDIT OF FINANCIAL STATEMENTS (Effective for audits of financial statements for periods beginning on or after 01 January 2014) * CONTENTS Paragraph Introduction

SRI LANKA AUDITING STANDARD 300 PLANNING AN AUDIT OF FINANCIAL STATEMENTS (Effective for audits of financial statements for periods beginning on or after 01 January 2014) * CONTENTS Paragraph Introduction

PHILIPPINE STANDARD ON AUDITING 300 PLANNING AN AUDIT OF FINANCIAL STATEMENTS CONTENTS

PHILIPPINE STANDARD ON AUDITING 300 PLANNING AN AUDIT OF FINANCIAL STATEMENTS (Effective for audits of financial statements for periods beginning on or after December 15, 2009) CONTENTS Paragraph Introduction

PHILIPPINE STANDARD ON AUDITING 300 PLANNING AN AUDIT OF FINANCIAL STATEMENTS (Effective for audits of financial statements for periods beginning on or after December 15, 2009) CONTENTS Paragraph Introduction

Memo. Date: October 2018 INTRODUCTION

Memo To: All Public Accounting Firms From: Kathy Zaplitny, CPA, CA Senior Director, Stakeholder Services & Engagement Re: FOCUS ON PRACTICE INSPECTION REPORTABLE DEFICIENCIES 2017-18 Date: October 2018

Memo To: All Public Accounting Firms From: Kathy Zaplitny, CPA, CA Senior Director, Stakeholder Services & Engagement Re: FOCUS ON PRACTICE INSPECTION REPORTABLE DEFICIENCIES 2017-18 Date: October 2018

Planning an Audit of Financial Statements

ISA 300 Issued February 2008; updated February 2018 International Standard on Auditing Planning an Audit of Financial Statements INTERNATIONAL STANDARD ON AUDITING 300 PLANNING AN AUDIT OF FINANCIAL STATEMENTS

ISA 300 Issued February 2008; updated February 2018 International Standard on Auditing Planning an Audit of Financial Statements INTERNATIONAL STANDARD ON AUDITING 300 PLANNING AN AUDIT OF FINANCIAL STATEMENTS

SRI LANKA AUDITING STANDARD 300 PLANNING AN AUDIT OF FINANCIAL STATEMENTS CONTENTS

SRI LANKA AUDITING STANDARD 300 PLANNING AN AUDIT OF FINANCIAL STATEMENTS Introduction (Effective for audits of financial statements for periods beginning on or after 01 January 2012) CONTENTS Paragraph

SRI LANKA AUDITING STANDARD 300 PLANNING AN AUDIT OF FINANCIAL STATEMENTS Introduction (Effective for audits of financial statements for periods beginning on or after 01 January 2012) CONTENTS Paragraph

AUDIT QUALITY ASSURANCE WORKSHOP Tuesday 20 th March Presentation by: CPA Hesbon Omollo Bon&Drew Associates-CPA-K

AUDIT QUALITY ASSURANCE WORKSHOP Tuesday 20 th March 2018 Presentation by: CPA Hesbon Omollo Bon&Drew Associates-CPA-K Uphold public interest Contents Introduction Acceptance and Continuance of Client

AUDIT QUALITY ASSURANCE WORKSHOP Tuesday 20 th March 2018 Presentation by: CPA Hesbon Omollo Bon&Drew Associates-CPA-K Uphold public interest Contents Introduction Acceptance and Continuance of Client

Scope of this SA Effective Date Objective Definitions Sufficient Appropriate Audit Evidence... 6

SA 500* AUDIT EVIDENCE (Effective for audits of financial statements for periods beginning on or after April 1, 2009) Contents Introduction Paragraph(s) Scope of this SA...1-2 Effective Date... 3 Objective...

SA 500* AUDIT EVIDENCE (Effective for audits of financial statements for periods beginning on or after April 1, 2009) Contents Introduction Paragraph(s) Scope of this SA...1-2 Effective Date... 3 Objective...

Auditing Standards and Practices Council

Auditing Standards and Practices Council PHILIPPINE STANDARD ON AUDITING 315 UNDERSTANDING THE ENTITY AND ITS ENVIRONMENT AND ASSESSING THE RISKS OF MATERIAL MISSTATEMENT PHILIPPINE STANDARD ON AUDITING

Auditing Standards and Practices Council PHILIPPINE STANDARD ON AUDITING 315 UNDERSTANDING THE ENTITY AND ITS ENVIRONMENT AND ASSESSING THE RISKS OF MATERIAL MISSTATEMENT PHILIPPINE STANDARD ON AUDITING

PLANNING AN AUDIT OF FINANCIAL STATEMENTS

SINGAPORE STANDARD ON AUDITING SSA 300 PLANNING AN AUDIT OF FINANCIAL STATEMENTS This revised Singapore Standard on Auditing (SSA) 300 supersedes the SSA of the same title in May 2007. This SSA has been

SINGAPORE STANDARD ON AUDITING SSA 300 PLANNING AN AUDIT OF FINANCIAL STATEMENTS This revised Singapore Standard on Auditing (SSA) 300 supersedes the SSA of the same title in May 2007. This SSA has been

Identifying and Assessing the Risks of Material Misstatement through Understanding the Entity and Its Environment

ISA 315 February 2008 International Standard on Auditing Identifying and Assessing the Risks of Material Misstatement through Understanding the Entity and Its Environment INTERNATIONAL STANDARD ON AUDITING

ISA 315 February 2008 International Standard on Auditing Identifying and Assessing the Risks of Material Misstatement through Understanding the Entity and Its Environment INTERNATIONAL STANDARD ON AUDITING

SRI LANKA AUDITING STANDARD 300 PLANNING AN AUDIT OF FINANCIAL STATEMENTS CONTENTS

SRI LANKA AUDITING STANDARD 300 PLANNING AN AUDIT OF FINANCIAL STATEMENTS (Effective for all the audits carried out on or after ) CONTENTS Paragraph Introduction 1-5 Preliminary Engagement Activities 6-7

SRI LANKA AUDITING STANDARD 300 PLANNING AN AUDIT OF FINANCIAL STATEMENTS (Effective for all the audits carried out on or after ) CONTENTS Paragraph Introduction 1-5 Preliminary Engagement Activities 6-7

Planning an Audit 259

Planning an Audit 259 AU-C Section 300 Planning an Audit Source: SAS No. 122; SAS No. 128. Effective for audits of financial statements for periods ending on or after December 15, 2012. Introduction Scope

Planning an Audit 259 AU-C Section 300 Planning an Audit Source: SAS No. 122; SAS No. 128. Effective for audits of financial statements for periods ending on or after December 15, 2012. Introduction Scope

CAAS 104 Cost Audit and Assurance Standard on Knowledge of Business, its Processes and the Business Environment

CAAS 104 Cost Audit and Assurance Standard on Knowledge of Business, its Processes and the Business Environment The following is the Cost Audit and Assurance Standard (CAAS 104) on Knowledge of Business,

CAAS 104 Cost Audit and Assurance Standard on Knowledge of Business, its Processes and the Business Environment The following is the Cost Audit and Assurance Standard (CAAS 104) on Knowledge of Business,

of Financial Statements

Issued November 2004 Effective for audits of financial statements for periods beginning on or after 15 December 2004 Hong Kong Standard on Auditing 300 Planning an Audit of Financial Statements HONG KONG

Issued November 2004 Effective for audits of financial statements for periods beginning on or after 15 December 2004 Hong Kong Standard on Auditing 300 Planning an Audit of Financial Statements HONG KONG

IAASB Main Agenda (September 2004) Page Agenda Item PROPOSED REVISED INTERNATIONAL STANDARD ON AUDITING 540

Page Agenda Item PROPOSED REVISED INTERNATIONAL STANDARD ON AUDITING 540") IAASB Main Agenda (September 2004) Page 2004 1651 Agenda Item 4-A PROPOSED REVISED INTERNATIONAL STANDARD ON AUDITING 540 AUDITING ACCOUNTING ESTIMATES AND RELATED DISCLOSURES (EXCLUDING THOSE INVOLVING

IAASB Main Agenda (September 2004) Page 2004 1651 Agenda Item 4-A PROPOSED REVISED INTERNATIONAL STANDARD ON AUDITING 540 AUDITING ACCOUNTING ESTIMATES AND RELATED DISCLOSURES (EXCLUDING THOSE INVOLVING

ISA 500. Issued March 2009; updated June International Standard on Auditing. Audit Evidence

ISA 500 Issued March 2009; updated June 2018 International Standard on Auditing Audit Evidence INTERNATIONAL STANDARD ON AUDITING 500 AUDIT EVIDENCE The Malaysian Institute of Accountants has approved

ISA 500 Issued March 2009; updated June 2018 International Standard on Auditing Audit Evidence INTERNATIONAL STANDARD ON AUDITING 500 AUDIT EVIDENCE The Malaysian Institute of Accountants has approved

Compilation Engagements

IFAC Board Final Pronouncement March 2012 International Standard on Related Services ISRS 4410 (Revised), Compilation Engagements The International Auditing and Assurance Standards Board (IAASB) develops

IFAC Board Final Pronouncement March 2012 International Standard on Related Services ISRS 4410 (Revised), Compilation Engagements The International Auditing and Assurance Standards Board (IAASB) develops

International Auditing and Assurance Standards Board ISA 500. April International Standard on Auditing. Audit Evidence

International Auditing and Assurance Standards Board ISA 500 April 2009 International Standard on Auditing Audit Evidence International Auditing and Assurance Standards Board International Federation of

International Auditing and Assurance Standards Board ISA 500 April 2009 International Standard on Auditing Audit Evidence International Auditing and Assurance Standards Board International Federation of

Audit Evidence. HKSA 500 Issued July 2009; revised July 2010, May 2013, February 2015, August 2015, June 2017

HKSA 500 Issued July 2009; revised July 2010, May 2013, February 2015, August 2015, June 2017 Effective for audits of financial statements for periods beginning on or after 15 December 2009 Hong Kong Standard

HKSA 500 Issued July 2009; revised July 2010, May 2013, February 2015, August 2015, June 2017 Effective for audits of financial statements for periods beginning on or after 15 December 2009 Hong Kong Standard

Statements. This Standard is effective for reviews of financial statements for periods ending on or after 31 December 2013.

SINGAPORE STANDARD ON REVIEW ENGAGEMENTS SSRE 2400 (Revised) Engagements to Review Historical Financial Statements This revised Singapore Standard on Review Engagements (SSRE) 2400 supersedes SSRE 2400

SINGAPORE STANDARD ON REVIEW ENGAGEMENTS SSRE 2400 (Revised) Engagements to Review Historical Financial Statements This revised Singapore Standard on Review Engagements (SSRE) 2400 supersedes SSRE 2400

Audit Evidence. SSA 500, Audit Evidence superseded the SSA of the same title in September 2009.

SINGAPORE STANDARD SSA 500 ON AUDITING Audit Evidence SSA 500, Audit Evidence superseded the SSA of the same title in September 2009. SSA 610 (Revised 2013), Using the Work of Internal Auditors gave rise

SINGAPORE STANDARD SSA 500 ON AUDITING Audit Evidence SSA 500, Audit Evidence superseded the SSA of the same title in September 2009. SSA 610 (Revised 2013), Using the Work of Internal Auditors gave rise

covered member immediate family impaired not a covered member close relative not impaired

BUS 425 Auditing Tad Miller May 22, 2017 Audit Planning, Analytical Procedures, Materiality & Risk, Internal Control Evaluation and Audit Plan 1. INDEPENDENCE All independence problems refer to a client

BUS 425 Auditing Tad Miller May 22, 2017 Audit Planning, Analytical Procedures, Materiality & Risk, Internal Control Evaluation and Audit Plan 1. INDEPENDENCE All independence problems refer to a client

Planning an Audit of Financial Statements

ISA 300 February 2008 International Standard on Auditing Planning an Audit of Financial Statements INTERNATIONAL STANDARD ON AUDITING 300 Planning an Audit of Financial Statements Explanatory Foreword

ISA 300 February 2008 International Standard on Auditing Planning an Audit of Financial Statements INTERNATIONAL STANDARD ON AUDITING 300 Planning an Audit of Financial Statements Explanatory Foreword

Cost Auditing Standard Cost Auditing Standard on Knowledge of Business, its Processes and the Business Environment

Cost Auditing Standard - 104 Cost Auditing Standard on Knowledge of Business, its Processes and the Business Environment The following is the Cost Auditing Standard (Cost Auditing Standard - 104) on Knowledge

Cost Auditing Standard - 104 Cost Auditing Standard on Knowledge of Business, its Processes and the Business Environment The following is the Cost Auditing Standard (Cost Auditing Standard - 104) on Knowledge

Compilation Engagements

SINGAPORE STANDARD ON RELATED SERVICES SSRS 4410 (REVISED) Compilation Engagements This revised Singapore Standard on Related Services (SSRS) 4410 supersedes SSRS 4410 Engagements to Compile Financial

SINGAPORE STANDARD ON RELATED SERVICES SSRS 4410 (REVISED) Compilation Engagements This revised Singapore Standard on Related Services (SSRS) 4410 supersedes SSRS 4410 Engagements to Compile Financial

INTERNATIONAL STANDARD ON AUDITING 701 COMMUNICATING KEY AUDIT MATTERS IN THE INDEPENDENT AUDITOR S REPORT

INTERNATIONAL STANDARD ON AUDITING 701 COMMUNICATING KEY AUDIT MATTERS IN THE INDEPENDENT AUDITOR S REPORT (Effective for audits of financial statements for periods ending on or after December 15, 2016)

INTERNATIONAL STANDARD ON AUDITING 701 COMMUNICATING KEY AUDIT MATTERS IN THE INDEPENDENT AUDITOR S REPORT (Effective for audits of financial statements for periods ending on or after December 15, 2016)

Utility Debt Securitization Authority

Utility Debt Securitization Authority Report to the Finance and Audit Committee Audit plan and strategy for the year ending December 31, 2018 December 12, 2018 This presentation to the Finance and Audit

Utility Debt Securitization Authority Report to the Finance and Audit Committee Audit plan and strategy for the year ending December 31, 2018 December 12, 2018 This presentation to the Finance and Audit

AUDIT RISK ASSESSMENT AND RESPONSES TO ASSESSED RISK BY Geoffrey Byamugisha Partner, Ernst & Young. Lessons on Audit Risk. Responding to fraud risk

AUDIT RISK ASSESSMENT AND RESPONSES TO ASSESSED RISK BY Geoffrey Byamugisha Partner, Ernst & Young ICPAU Page 1 COURSE CONTENT Lessons on Audit Risk Identification of audit risk and audit risk assessment

AUDIT RISK ASSESSMENT AND RESPONSES TO ASSESSED RISK BY Geoffrey Byamugisha Partner, Ernst & Young ICPAU Page 1 COURSE CONTENT Lessons on Audit Risk Identification of audit risk and audit risk assessment

SECTION A CASE QUESTIONS (Total: 50 marks)

") SECTION A CASE QUESTIONS (Total: 50 marks) Answer 1(a) Control activities that are relevant to an audit are: - Control activities that relate to significant risks or relate to risks for which substantive

SECTION A CASE QUESTIONS (Total: 50 marks) Answer 1(a) Control activities that are relevant to an audit are: - Control activities that relate to significant risks or relate to risks for which substantive

Case Report:Deficiencies in Audit Quality Control

Case Report:Deficiencies in Audit Quality Control July 2011 Certified Public Accountants and Auditing Oversight Board Introduction Since its establishment in April 2004, the Certified Public Accountants

Case Report:Deficiencies in Audit Quality Control July 2011 Certified Public Accountants and Auditing Oversight Board Introduction Since its establishment in April 2004, the Certified Public Accountants

CHAMBER OF TAX CONSULTANT S STUDENT COMMITTEE. Presentation on

CHAMBER OF TAX CONSULTANT S STUDENT COMMITTEE Presentation on AUDIT AROUND THE COMPUTER INCLUDING AUDIT DOCUMENTATION by CA MEHUL R. SHETH 08TH JUNE 2018 1 An audit is a systematic and independent examination

CHAMBER OF TAX CONSULTANT S STUDENT COMMITTEE Presentation on AUDIT AROUND THE COMPUTER INCLUDING AUDIT DOCUMENTATION by CA MEHUL R. SHETH 08TH JUNE 2018 1 An audit is a systematic and independent examination

Audit Practice Introduced by HKSA (HKSA 300, 315 and 330) 10 July 2008

10 July 2008") Audit Practice Introduced by HKSA (HKSA 300, 315 and 330) 10 July 2008 Nelson Lam 林智遠 MBA MSc BBA ACA ACS CFA CPA(Aust) CPA(US) FCCA FCPA(Practising) MSCA 2006-08 Nelson 1 Overview HK auditing standards

Audit Practice Introduced by HKSA (HKSA 300, 315 and 330) 10 July 2008 Nelson Lam 林智遠 MBA MSc BBA ACA ACS CFA CPA(Aust) CPA(US) FCCA FCPA(Practising) MSCA 2006-08 Nelson 1 Overview HK auditing standards

Your committee: Evaluates the "tone at the top" and the company's culture, understanding their relevance to financial reporting and compliance

Audit Committee Self-assessment Guide The following guide summarizes leading audit committee practices discussed in the "Audit Committee Effectiveness- What Works Best" report. You may use it to help assess

Audit Committee Self-assessment Guide The following guide summarizes leading audit committee practices discussed in the "Audit Committee Effectiveness- What Works Best" report. You may use it to help assess

Annual Assessment of the External Auditor

Annual Assessment of the External Auditor TOOL FOR AUDIT COMMITTEES January 2014 ENHANCING AUDIT QUALITY AUDIT COMMITTEES iii Table of Contents Introduction 1 1. Determine the scope, timing and process

Annual Assessment of the External Auditor TOOL FOR AUDIT COMMITTEES January 2014 ENHANCING AUDIT QUALITY AUDIT COMMITTEES iii Table of Contents Introduction 1 1. Determine the scope, timing and process

Comparison of the PCAOB s Auditing Standards No. 5 and No. 2 (Certain key differences are highlighted by underlining)

") Comparison of the PCAOB s Auditing Standards No. 5 and No. 2 (Certain key differences are highlighted by underlining) Topic AS No. 5 AS No. 2 Objective of ICFR Audit Planning the ICFR Audit Integration

Comparison of the PCAOB s Auditing Standards No. 5 and No. 2 (Certain key differences are highlighted by underlining) Topic AS No. 5 AS No. 2 Objective of ICFR Audit Planning the ICFR Audit Integration

INTERNATIONAL STANDARD ON AUDITING 210 TERMS OF AUDIT ENGAGEMENTS CONTENTS

INTERNATIONAL STANDARD ON AUDITING 210 TERMS OF AUDIT ENGAGEMENTS (Effective for audits of financial statements for periods beginning on or after December 15, 2006. Appendix 2 contains conforming amendments

INTERNATIONAL STANDARD ON AUDITING 210 TERMS OF AUDIT ENGAGEMENTS (Effective for audits of financial statements for periods beginning on or after December 15, 2006. Appendix 2 contains conforming amendments

Financial reporting: Reviewing financial information

0 0 Financial reporting: Reviewing financial information The PwC Audit Committee Guide is designed to help members of the audit committee work through their maze of responsibilities in a practical manner.

0 0 Financial reporting: Reviewing financial information The PwC Audit Committee Guide is designed to help members of the audit committee work through their maze of responsibilities in a practical manner.

INTERNATIONAL STANDARD ON AUDITING 620 USING THE WORK OF AN AUDITOR S EXPERT CONTENTS

INTERNATIONAL STANDARD ON 620 USING THE WORK OF AN AUDITOR S EXPERT (Effective for audits of financial statements for periods beginning on or after December 15, 2009) CONTENTS Paragraph Introduction Scope

INTERNATIONAL STANDARD ON 620 USING THE WORK OF AN AUDITOR S EXPERT (Effective for audits of financial statements for periods beginning on or after December 15, 2009) CONTENTS Paragraph Introduction Scope

Agreeing the Terms of Audit Engagements

ISA 210 Issued March 2009; updated February 2018 International Standard on Auditing Agreeing the Terms of Audit Engagements INTERNATIONAL STANDARD ON AUDITING 210 AGREEING THE TERMS OF AUDIT ENGAGEMENTS

ISA 210 Issued March 2009; updated February 2018 International Standard on Auditing Agreeing the Terms of Audit Engagements INTERNATIONAL STANDARD ON AUDITING 210 AGREEING THE TERMS OF AUDIT ENGAGEMENTS

REPORT WRITING & INDEPENDENT REVIEW

REPORT WRITING & INDEPENDENT REVIEW 1 PRESENTED BY FAITH NGWENYA TECHNICAL & STANDARDS SERVICES EXECUTIVE Professional Accountant 2 3 QUALITY CONTROL ISQC 1 Monitoring ISQC 1 Engagement performance Human

REPORT WRITING & INDEPENDENT REVIEW 1 PRESENTED BY FAITH NGWENYA TECHNICAL & STANDARDS SERVICES EXECUTIVE Professional Accountant 2 3 QUALITY CONTROL ISQC 1 Monitoring ISQC 1 Engagement performance Human

INTERNATIONAL STANDARD ON AUDITING (IRELAND) 210 AGREEING THE TERMS OF AUDIT ENGAGEMENTS

210 AGREEING THE TERMS OF AUDIT ENGAGEMENTS") INTERNATIONAL STANDARD ON AUDITING (IRELAND) 210 AGREEING THE TERMS OF AUDIT ENGAGEMENTS MISSION To contribute to Ireland having a strong regulatory environment in which to do business by supervising and

INTERNATIONAL STANDARD ON AUDITING (IRELAND) 210 AGREEING THE TERMS OF AUDIT ENGAGEMENTS MISSION To contribute to Ireland having a strong regulatory environment in which to do business by supervising and

INTERNATIONAL STANDARD ON AUDITING (NEW ZEALAND) 315 (Revised)

315 (Revised)") Issued 07/11 Revised 04/13 Compiled 10/15 INTERNATIONAL STANDARD ON AUDITING (NEW ZEALAND) 315 (Revised) Identifying and Assessing the Risks of Material Misstatement through Understanding the Entity and

Issued 07/11 Revised 04/13 Compiled 10/15 INTERNATIONAL STANDARD ON AUDITING (NEW ZEALAND) 315 (Revised) Identifying and Assessing the Risks of Material Misstatement through Understanding the Entity and

ILLUSTRATIVE RISKS OF MATERIAL MISSTATEMENT, RELATED CONTROL OBJECTIVES AND CONTROL ACTIVITIES. (Refer paragraphs 77 and 100)

") APPENDIX IV ILLUSTRATIVE RISKS OF MATERIAL MISSTATEMENT, RELATED CONTROL OBJECTIVES AND CONTROL ACTIVITIES (Refer paragraphs 77 and 100) Standards on Auditing ( SA ) 315 Identifying and Assessing the Risk

APPENDIX IV ILLUSTRATIVE RISKS OF MATERIAL MISSTATEMENT, RELATED CONTROL OBJECTIVES AND CONTROL ACTIVITIES (Refer paragraphs 77 and 100) Standards on Auditing ( SA ) 315 Identifying and Assessing the Risk

IAASB Main Agenda (June 2004) Page Agenda Item

Page Agenda Item") IAASB Main Agenda (June 2004) Page 2004 1009 Agenda Item 7-B INTERNATIONAL STANDARD ON AUDITING 300 (MARK-UP) PLANNING AN AUDIT OF FINANCIAL STATEMENTS CONTENTS Paragraphs Introduction... 1-5 Preliminary

IAASB Main Agenda (June 2004) Page 2004 1009 Agenda Item 7-B INTERNATIONAL STANDARD ON AUDITING 300 (MARK-UP) PLANNING AN AUDIT OF FINANCIAL STATEMENTS CONTENTS Paragraphs Introduction... 1-5 Preliminary

International Standard on Auditing (UK) 620 (Revised June 2016)

620 (Revised June 2016)") Standard Audit and Assurance Financial Reporting Council June 2016 International Standard on Auditing (UK) 620 (Revised June 2016) Using the Work of an Auditor s Expert The FRC s mission is to promote

Standard Audit and Assurance Financial Reporting Council June 2016 International Standard on Auditing (UK) 620 (Revised June 2016) Using the Work of an Auditor s Expert The FRC s mission is to promote

INTERNATIONAL STANDARD ON AUDITING 500 AUDIT EVIDENCE CONTENTS

INTERNATIONAL STANDARD ON 500 AUDIT EVIDENCE (Effective for audits of financial statements for periods beginning on or after December 15, 2004) CONTENTS Paragraph Introduction... 1-2 Concept of Audit Evidence...

INTERNATIONAL STANDARD ON 500 AUDIT EVIDENCE (Effective for audits of financial statements for periods beginning on or after December 15, 2004) CONTENTS Paragraph Introduction... 1-2 Concept of Audit Evidence...

Completion and review

chapter 11 Completion and review Chapter learning objectives Upon completion of this chapter you will be able to: Subsequent events explain the purpose of a subsequent events review discuss the procedures

chapter 11 Completion and review Chapter learning objectives Upon completion of this chapter you will be able to: Subsequent events explain the purpose of a subsequent events review discuss the procedures

CPA REVIEW SCHOOL OF THE PHILIPPINES Manila. AUDITING THEORY OTHER PSAs and PAPSs

Page 1 of 11 CPA REVIEW SCHOOL OF THE PHILIPPINES Manila AUDITING THEORY OTHER PSAs and PAPSs Related PSAs/PAPSs: PSA 501, 505, 510, 520, 540, 545, 550, 620, 560 and 580 PAPS 1000, 1005 and 1000Ph PSA

Page 1 of 11 CPA REVIEW SCHOOL OF THE PHILIPPINES Manila AUDITING THEORY OTHER PSAs and PAPSs Related PSAs/PAPSs: PSA 501, 505, 510, 520, 540, 545, 550, 620, 560 and 580 PAPS 1000, 1005 and 1000Ph PSA

Auditing and Attestation (AUD) - Content Outline Effective January 2014

- Content Outline Effective January 2014") Auditing and Attestation (AUD) - Content Outline Effective January 2014 The Auditing and Attestation section tests knowledge and understanding of the following professional standards: Auditing standards

Auditing and Attestation (AUD) - Content Outline Effective January 2014 The Auditing and Attestation section tests knowledge and understanding of the following professional standards: Auditing standards

ISA 701, Communicating Key Audit Matters in the Independent Auditor s Report

ISA 701 April 2015 International Standard on Auditing ISA 701, Communicating Key Audit Matters in the Independent Auditor s Report Explanatory Foreword INTERNATIONAL STANDARD ON AUDITING 701 Communicating

ISA 701 April 2015 International Standard on Auditing ISA 701, Communicating Key Audit Matters in the Independent Auditor s Report Explanatory Foreword INTERNATIONAL STANDARD ON AUDITING 701 Communicating

LIST OF SUBSTANTIVE CHANGES AND ADDITIONS. PPC's Guide to Dealerships. Twentieth Edition (August 2015)

") Route To: Partners Managers Staff File LIST OF SUBSTANTIVE CHANGES AND ADDITIONS PPC's Guide to Dealerships Twentieth Edition (August 2015) Highlights of This Edition The following are some of the important

Route To: Partners Managers Staff File LIST OF SUBSTANTIVE CHANGES AND ADDITIONS PPC's Guide to Dealerships Twentieth Edition (August 2015) Highlights of This Edition The following are some of the important

INTERNATIONAL STANDARD ON AUDITING (NEW ZEALAND) 500

500") Issued 07/11 Compiled 10/15 INTERNATIONAL STANDARD ON AUDITING (NEW ZEALAND) 500 Audit Evidence (ISA (NZ) 500) This compilation was prepared in October 2015 and incorporates amendments up to and including

Issued 07/11 Compiled 10/15 INTERNATIONAL STANDARD ON AUDITING (NEW ZEALAND) 500 Audit Evidence (ISA (NZ) 500) This compilation was prepared in October 2015 and incorporates amendments up to and including

CHARTER OF THE AUDIT, FINANCE AND RISK COMMITTEE OF THE BOARD OF DIRECTORS OF ACE AVIATION HOLDINGS INC.

CHARTER OF THE AUDIT, FINANCE AND RISK COMMITTEE OF THE BOARD OF DIRECTORS OF ACE AVIATION HOLDINGS INC. 1. Structure, Procedure, Qualifications The Audit, Finance and Risk Committee (the Audit Committee

CHARTER OF THE AUDIT, FINANCE AND RISK COMMITTEE OF THE BOARD OF DIRECTORS OF ACE AVIATION HOLDINGS INC. 1. Structure, Procedure, Qualifications The Audit, Finance and Risk Committee (the Audit Committee

Detailed competency map

Detailed competency map Additional competency requirements for entry to the Hong Kong Institute of CPAs qualification programme (Professional bridging examination) Fields of competency The items listed

Detailed competency map Additional competency requirements for entry to the Hong Kong Institute of CPAs qualification programme (Professional bridging examination) Fields of competency The items listed

Standard on Auditing (SA) 701, Communicating Key Audit Matters in the Independent Auditor s Report Contents Paragraph(s) Introduction Scope of this SA

701, Communicating Key Audit Matters in the Independent Auditor s Report Contents Paragraph(s) Introduction Scope of this SA") Standard on Auditing (SA) 701, Communicating Key Audit Matters in the Independent Auditor s Report Contents Paragraph(s) Introduction Scope of this SA... 1 5 Effective Date... 6 Objectives... 7 Definition...

Standard on Auditing (SA) 701, Communicating Key Audit Matters in the Independent Auditor s Report Contents Paragraph(s) Introduction Scope of this SA... 1 5 Effective Date... 6 Objectives... 7 Definition...

AUDITOR S RESPONSIBILITY UNDER AUDITING STANDARDS GENERALLY ACCEPTED IN THE UNITED STATES OF AMERICA

Crowe Horwath LLP Independent Member Crowe Horwath International Audit Committee Western Climate Initiative, Inc. Sacramento, California Professional standards require that we communicate certain matters

Crowe Horwath LLP Independent Member Crowe Horwath International Audit Committee Western Climate Initiative, Inc. Sacramento, California Professional standards require that we communicate certain matters

Due: Tuesday, May 1, 2007 by 5:45 p.m.

A439: Advance Auditing 2007 Final exam Directions: The final exam consists of 30 multiple choice questions. Ground Rules. As a take-home exam you may use notes, the internet, auditing textbooks or other

A439: Advance Auditing 2007 Final exam Directions: The final exam consists of 30 multiple choice questions. Ground Rules. As a take-home exam you may use notes, the internet, auditing textbooks or other

Report on Inspection of KPMG AG Wirtschaftspruefungsgesellschaft (Headquartered in Berlin, Federal Republic of Germany)

") 1666 K Street, N.W. Washington, DC 20006 Telephone: (202) 207-9100 Facsimile: (202) 862-8433 www.pcaobus.org Report on 2016 (Headquartered in Berlin, Federal Republic of Germany) Issued by the Public Company

1666 K Street, N.W. Washington, DC 20006 Telephone: (202) 207-9100 Facsimile: (202) 862-8433 www.pcaobus.org Report on 2016 (Headquartered in Berlin, Federal Republic of Germany) Issued by the Public Company

PROFESSIONAL LEVEL PART-A: OVERVIEW OF AUDITING AND ASSURANCE

SYLLABS 2016 Part-D Weightage Part-E Part-C Part-A PROFESSIONAL LEVEL P2 - Audit & Assurance Part-B Part-A Overview of Auditing and Assurance 15% Part-B Audit Planning 20% Part-C Internal Controls 20%

SYLLABS 2016 Part-D Weightage Part-E Part-C Part-A PROFESSIONAL LEVEL P2 - Audit & Assurance Part-B Part-A Overview of Auditing and Assurance 15% Part-B Audit Planning 20% Part-C Internal Controls 20%

2013 PUBLIC ENTITIES OVERVIEW FOR KNOWLEDGE COACH USERS

2013 PUBLIC ETITIES OVERVIEW FOR KOWLEDGE COACH USERS PURPOSE This document is published for the purpose of communicating, to users of the toolset, updates and enhancements included in the current version.

2013 PUBLIC ETITIES OVERVIEW FOR KOWLEDGE COACH USERS PURPOSE This document is published for the purpose of communicating, to users of the toolset, updates and enhancements included in the current version.

Chapter 18. Integrated Audits of Public Companies. McGraw-Hill/Irwin. Copyright 2012 by The McGraw-Hill Companies, Inc. All rights reserved.

Chapter 18 Integrated Audits of Public Companies McGraw-Hill/Irwin Copyright 2012 by The McGraw-Hill Companies, Inc. All rights reserved. Nature of an Integrated Audit Auditors of public companies should

Chapter 18 Integrated Audits of Public Companies McGraw-Hill/Irwin Copyright 2012 by The McGraw-Hill Companies, Inc. All rights reserved. Nature of an Integrated Audit Auditors of public companies should

AUSTRALIAN GAAS 2007 AUDITING STANDARDS CHECKLISTS

AUSTRALIAN GAAS 2007 AUDITING STANDARDS CHECKLISTS COLIN PARKER B.Bus FCA MAICD Principal, GAAP Consulting www.gaap.com.au AUSTRALIAN GAAS* 2007 AUDITING STANDARDS CHECKLISTS AS AT 1 JANUARY 2007 COLIN

AUSTRALIAN GAAS 2007 AUDITING STANDARDS CHECKLISTS COLIN PARKER B.Bus FCA MAICD Principal, GAAP Consulting www.gaap.com.au AUSTRALIAN GAAS* 2007 AUDITING STANDARDS CHECKLISTS AS AT 1 JANUARY 2007 COLIN

IAASB Main Agenda (December 2008) Page Agenda Item

Page Agenda Item") IAASB Main Agenda (December 2008) Page 2008 2669 Agenda Item 2-C PROPOSED INTERNATIONAL STANDARD ON AUDITING 265 COMMUNICATING DEFICIENCIES IN INTERNAL CONTROL (Effective for audits of financial statements

IAASB Main Agenda (December 2008) Page 2008 2669 Agenda Item 2-C PROPOSED INTERNATIONAL STANDARD ON AUDITING 265 COMMUNICATING DEFICIENCIES IN INTERNAL CONTROL (Effective for audits of financial statements

Sample Audit Committee. of Auditors and Management

Sample Audit Committee Questions to Ask of Auditors and Management 2 Sample Audit Committee Questions to Ask of Auditors and Management u Sample Audit Committee Questions to Ask of Auditors and Management

Sample Audit Committee Questions to Ask of Auditors and Management 2 Sample Audit Committee Questions to Ask of Auditors and Management u Sample Audit Committee Questions to Ask of Auditors and Management

Audit and Risk Committee Charter

Audit and Risk Committee Charter Purpose The Audit and Risk Committee ( Committee ) has been established as a committee of the board of directors ( Board ) of Trustpower Limited (the Company ) to assist

Audit and Risk Committee Charter Purpose The Audit and Risk Committee ( Committee ) has been established as a committee of the board of directors ( Board ) of Trustpower Limited (the Company ) to assist

IAASB Main Agenda (June 2008) Page Agenda Item

Page Agenda Item") IAASB Main Agenda (June 2008) Page 2008 595 Agenda Item 2-A PROPOSED INTERNATIONAL STANDARD ON AUDITING 500 (REDRAFTED) OBTAINING SUFFICIENT APPROPRIATE AUDIT EVIDENCE (Mark-up Showing Changes from March

IAASB Main Agenda (June 2008) Page 2008 595 Agenda Item 2-A PROPOSED INTERNATIONAL STANDARD ON AUDITING 500 (REDRAFTED) OBTAINING SUFFICIENT APPROPRIATE AUDIT EVIDENCE (Mark-up Showing Changes from March

AUDIT COMMITTEE CHARTER

- 1 - AUDIT COMMITTEE CHARTER I. ROLE AND OBJECTIVES The Audit Committee is a committee of the Board of Directors (the "Board") of Pembina Pipeline Corporation (the "Corporation") to which the Board has

- 1 - AUDIT COMMITTEE CHARTER I. ROLE AND OBJECTIVES The Audit Committee is a committee of the Board of Directors (the "Board") of Pembina Pipeline Corporation (the "Corporation") to which the Board has

International Standard on Auditing (UK) 220 (Revised June 2016)

220 (Revised June 2016)") Standard Audit and Assurance Financial Reporting Council June 2016 International Standard on Auditing (UK) 220 (Revised June 2016) Quality Control for an Audit of Financial Statements The FRC is responsible

Standard Audit and Assurance Financial Reporting Council June 2016 International Standard on Auditing (UK) 220 (Revised June 2016) Quality Control for an Audit of Financial Statements The FRC is responsible

Audit Evidence. ISA 500 Issued December International Standard on Auditing

Issued December 2007 International Standard on Auditing Audit Evidence The Malaysian Institute of Certified Public Accountants (Institut Akauntan Awam Bertauliah Malaysia) INTERNATIONAL STANDARD ON AUDITING

Issued December 2007 International Standard on Auditing Audit Evidence The Malaysian Institute of Certified Public Accountants (Institut Akauntan Awam Bertauliah Malaysia) INTERNATIONAL STANDARD ON AUDITING

STATEMENT OF AUDITING STANDARDS 500 AUDIT EVIDENCE

STATEMENT OF AUDITING STANDARDS 500 AUDIT EVIDENCE (Issued January 2004) Contents Paragraphs Introduction 1-2 Concept of Audit Evidence 3-6 Sufficient Appropriate Audit Evidence 7-14 The Use of Assertions

STATEMENT OF AUDITING STANDARDS 500 AUDIT EVIDENCE (Issued January 2004) Contents Paragraphs Introduction 1-2 Concept of Audit Evidence 3-6 Sufficient Appropriate Audit Evidence 7-14 The Use of Assertions

Assurance Hand Note Professional Stage-Knowledge Level By: Shafique Ahmed-Sr. Officer (Internal Audit-BSRM) Assurance

Assurance") Assurance 1 CONTENTS OF ASSURANCE 01. Preliminary of Assurance: 1.01 Assurance Engagement: 1.02 Key elements of an assurance engagement: 1.03 Levels of assurance 1.04 Objective of an Audit: 1.05 True &

Assurance 1 CONTENTS OF ASSURANCE 01. Preliminary of Assurance: 1.01 Assurance Engagement: 1.02 Key elements of an assurance engagement: 1.03 Levels of assurance 1.04 Objective of an Audit: 1.05 True &