Internal Control Fundamentals and Introduction to Fraud - Spring Brenda M. Shannon, CPA, CIA Chief Audit Executive New Mexico State University

|

|

|

- Edward Horn

- 6 years ago

- Views:

Transcription

1 Internal Control Fundamentals and Introduction to Fraud - Spring Brenda M. Shannon, CPA, CIA Chief Audit Executive New Mexico State University

2 Objectives To give participants a high-level overview of internal control fundamentals and to raise awareness levels with regard to fraud in the workplace.

3 Outline Video on Internal Controls Internal Control Fundamentals Introduction to Fraud

4 VIDEO - Internal Controls for Colleges & Universities (20 minutes) Association of College & University Auditors

5 Internal Control Fundamentals under the COSO Model (COSO is a voluntary, private sector organization dedicated to improving the quality of financial reporting through business ethics, effective internal controls, and corporate governance.)

6 COSO (Committee of Sponsoring Organizations) Sponsoring organizations AICPA, AAA, FEI, IIA, IMA History several business failures in the 1980 s prompted creation of a committee in 1985 to examine causes of fraudulent financial reporting. Committee charged with creating a control model. Result: Report titled Internal Control Integrated Framework, published in 1992.

7 COSO (Committee of Sponsoring Organizations) COSO model was considered to be best practices, but had no teeth. Renewed interest more recently because of accounting scandals and Sarbanes-Oxley Act of 2002 (SOX). The COSO model is still considered by many to be the best internal control guidance available.

8 Sarbanes-Oxley Act of 2002 (Corporate Governance & Accounting Reform Legislation) Applies to SEC companies (but relevant to us) Reforms aimed at companies, auditors, board members and lawyers Section 404 provision requires companies to adopt and evaluate internal controls.

9 COSO Definition of Internal Control Internal control is a process designed to provide reasonable assurance regarding the achievement of objectives in the following categories: Effectiveness and efficiency of operations (including protection of assets) Reliability of financial reporting Compliance with applicable laws and regulations

10 Types of Controls Internal controls may be: Preventive - designed to keep errors or irregularities from occurring. Detective - designed to detect errors or irregularities that have already occurred. Corrective - designed to correct errors or irregularities that have been detected.

11 Examples of Controls Personal Installing locks/alarm systems on homes and vehicles. Reviewing bills and credit card statements before payment Reconciling bank statements. Securing valuables such as jewelry, blank checks, credit cards and cash. Establishing rules and curfews for our children. Purchasing insurance.

12 Society Laws and Regulations Examples of Controls Minimum age limits for legally driving a car or drinking alcohol Traffic regulations Court hearings and trials Zoning ordinances Religious doctrine

13 Examples of Controls University NMSU Policy Manual; Business Procedures Manual; Student Code of Conduct Required use of computer passwords, anti-virus software Locking offices, buildings, state vehicles Securing laptops, procurement cards and petty cash funds Reconciling financial and P-card reports against receipts Requiring authorization from Purchasing for large purchases Requiring approvals for travel, timesheets and leave reports Running background checks, credit checks, motor vehicle checks I.D. cards Degree requirement audits

14 Who is Responsible for Internal Control? The organization s leadership is responsible for establishing the control environment. Everyone in an organization plays some role in effecting control. All personnel are responsible for communicating problems in operations, deviations from established standards, and violations of policy or law. Auditors evaluate whether appropriate controls have been implemented and are functioning as intended, but they are not responsible to establish or maintain them.

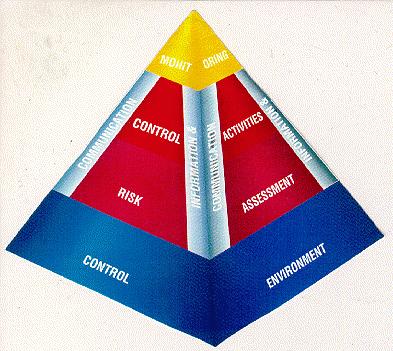

15 Five Components of an Integrated System of Internal Controls Control Environment Risk Assessment Control Activities Information & Communication Monitoring

16 Control Environment (1) ethical tone established by management; tone at the top, control consciousness (soft controls) Factors include: Integrity & Ethical Values must be clearly communicated, in writing and by example. Commitment to Competence Management Philosophy & Operating Style Organizational Structure Human Resource Policies & Procedures practices related to hiring, training, evaluation, promoting, compensating, etc.

17 How do you Evaluate Soft Controls? Subjective - the only valid measure of their effectiveness may be employees perceptions. Most internal control evaluation practices have a strong element of self-assessment Control Self-Assessment (CSA)

18 Risk Assessment (2) mechanism to identify, analyze and manage risks relevant to meeting our objectives. Factors: External Factors - economic changes, changing needs & expectations of clients, legislation & regulations, technological developments, natural disasters. Internal Factors - new personnel, new computer systems/processes, low morale.

19 Risk Assessment continued After risks have been identified, they must be analyzed as to likelihood of occurrence and impact, and then we must consider how to manage the risk. We cannot anticipate every potential risk Risk assessment should be an integral part of the strategic planning and budgeting process.

20 Control Activities (3) - policies (what should be done) and procedures (how it should be done) designed to help ensure that objectives are achieved. (Hard controls) Types of control activities: Transaction Approvals, Authorizations, Verifications (limits to authority) Reconciliations (explain differences between two sets of data), Verifications Performance reviews (programs, people, departments), benchmarking, trend analysis

21 Control Activities continued Physical controls - restrict access to equipment, conduct inventories, secure/count cash, etc. Segregation of Duties - different people should ideally be responsible for: authorizing transactions recording transactions (accounting) handling the related assets (custody) monitoring transactions (reconciling, verifying).

22 Information System Control Activities General controls: Segregation of duties within IT environment Backup and recovery policies & procedures Program development & documentation controls Hardware / access controls (i.e. passwords) Virus detection software Firewalls

23 Information System Control Activities Application controls: Input controls (authorization, validation, error notification i.e. field checks, limit checks, sequence checks) Processing controls batch totals, audit trails Output controls listing of master file changes, error listings

24 Controls What Kind and How Many do you Need? Enough to ensure that you are managing your significant risks, as determined by the risk assessment process.

25 Information & Communication (4)- how we identify/capture/communicate information in a way that allows employees to carry out their responsibilities. To be effective, the information system must have adequate resources and be able to provide data that is: Relevant to established objectives (operational, financial, compliance-related) Accurate and in sufficient detail Understandable and in usable form Provided to the appropriate people in a timely manner

26 Monitoring (5) assessing the quality of the system of internal controls over time. Activities include: Management review of financial reports for propriety and trends. Review and analysis of tips and complaints from external sources. Comparison of recorded data with physical assets. Self assessments, internal audits, external reviews Established means to report and correct deficiencies

27

28 Internal Control Components

29 Limitations of Internal Controls Judgment - decisions are made by people, often under pressure and time constraints, based on information at hand. Breakdowns - Employees may not understand instructions or may simply make mistakes. Errors may result from new systems and processes. Controls may be Outdated Waste of time and money.

30 Limitations of Internal Controls continued Management Override - high level personnel may be able to override prescribed policies and procedures. Collusion - two or more individuals, working together, may be able to circumvent controls. It is one thing to establish controls and quite another to ensure that they are operating as intended.

31 Perhaps the lesson to be learned from the 1980 s Savings & Loan scandals; the 1990 s corporate governance failures of Enron, WorldCom, Tyco and the like; and the more recent subprime mortgage debacle, is that you cannot legislate ethics or morality, and an Internal Control System is only as good as the people who administer it.

32 Balancing Risks and Controls Risks Controls Cost vs. Benefit - The risk of failure and the potential effects must be weighed against the cost of establishing controls.

33 Balancing Risk and Controls not having an effective balance may cause: Excessive Risks - Loss of Assets, Donors, Grants & Contracts, State funding - Poor Business Decisions - Noncompliance with laws & regulations - Increased Regulations - Public Scandals

34 Balancing Risk and Controls not having an effective balance may cause: Excessive Controls - Increased Bureaucracy - Increased Complexity - Increased Cycle Time - Increase in Non-Value Added Activities - Reduced Productivity

35 Integrated System of Internal Controls An effective system of internal controls requires: All 5 components working together Control Environment Risk Assessment Control Activities Information & Communication Monitoring Everyone in the organization playing an active role Internal Controls are Everyone s Business!

36 QUESTIONS? (Internal Control Training Supplement on Segregation of Duties)

37 Introduction to Fraud

38 What is Fraud? Occupational Fraud The use of one s occupation for personal enrichment through the deliberate misuse or misapplication of the employing organization s resources or assets. (Generally referred to as white-collar crime.) (Source: Association of Certified Fraud Examiners 2008 Report to the Nation on Occupational Fraud and Abuse)

39 Association of Certified Fraud Examiners 2008 Report to the Nation on Occupational Fraud & Abuse The study was based on data compiled from 959 cases of occupational fraud that were investigated between January 2006 and February All information was provided by the Certified Fraud Examiners (CFEs) who investigated those cases. The 2008 report is the fourth of its kind, with other reports produced in 2002, 2004 and 2006.

40 Measuring the Cost of Fraud (Source: Association of Certified Fraud Examiners 2008 Report to the Nation on Occupational Fraud and Abuse) Fraud, by its very nature, does not lend itself to being scientifically observed or measured in an accurate manner. One of the primary characteristics of fraud is that it is clandestine, or hidden, and almost all fraud involves the attempted concealment of the crime.

41 Types of Occupational Fraud and Abuse (Source: Association of Certified Fraud Examiners 2008 Report to the Nation on Occupational Fraud and Abuse) Asset Misappropriation theft or misuse of an organization s resources. (i.e., theft of cash, equipment or supply inventory; submitting false invoices, timesheets, or expense reports; abuse of leave) Corruption an employee wrongfully uses his/her influence in business transactions in a way that violates their duty to their employers in order to obtain a benefit for themselves or someone else. (i.e., engaging in conflicts of interest; receiving or offering bribes; extorting funds from third parties) Financial Statement Fraud making a company appear more/less profitable (i.e., booking fictitious sales or inventories, recording income/expense in wrong period)

42 Occupational Fraud by Category (Source: Association of Certified Fraud Examiners 2008 Report to the Nation on Occupational Fraud and Abuse)

43 Occupational Fraud by Category Median Losses (Source: Association of Certified Fraud Examiners 2008 Report to the Nation on Occupational Fraud and Abuse)

44 Occupational Fraud Schemes in Government and Public Administration (Source: Association of Certified Fraud Examiners 2008 Report to the Nation on Occupational Fraud & Abuse)

45 Occupational Fraud Schemes in the Education Industry (Source: Association of Certified Fraud Examiners 2008 Report to the Nation on Occupational Fraud & Abuse)

46 Fraud Statistics (Source: Association of Certified Fraud Examiners 2008 Report to the Nation on Occupational Fraud and Abuse) It is estimated that the average organization loses: about 7% of annual revenues to fraudulent activity This translates into ~$994 billion in annual fraud losses applied to the estimated 2008 U.S. Gross Domestic Product NMSU had operating revenues of over $500 million in FY08. 7% of that would be over $35 million.

47 Fraud Statistics continued Who commits more fraud men or women? Men are the perpetrators in 60% of all fraud cases Median $ losses caused by men are twice those caused by women.

48 Gender of Perpetrator Frequency Gender of Perpetrator Median Loss Source: Association of Certified Fraud Examiners 2008 Report to the Nation on Occupational Fraud and Abuse

49 Fraud Statistics continued Who commits more fraud employees, managers or owner/executives? While employees (40%) and managers (37%) account for the majority of offenses, median losses caused by owners/executives were 5 times more than those caused by managers, and 11 times more than those caused by rank and file employees.

50 Position of Perpetrator Frequency Position of Perpetrator Median Loss

51 Fraud Statistics continued Who commits more fraud younger people (<40) or older people? More than half of cases studied involved a fraudster over the age of 40, and over one-third were individuals between 41 and 50 The older they were, the greater the median losses incurred

52 Age of Perpetrator Frequency Source: Association of Certified Fraud Examiners 2008 Report to the Nation on Occupational Fraud and Abuse Age of Perpetrator Median Loss

53 Fraud Statistics continued Who commits more fraud those with more education or less education? While slightly more than half of all frauds were committed by people with no college degree, median $ losses caused by perpetrators with college degrees were up to 5 times greater than losses caused by those without college degrees.

54 Education of Perpetrator Frequency Education of Perpetrator Median Loss

55 Fraud Statistics continued Who commits more fraud those with more money or those with less money? While the number of frauds decreased as income brackets rose, the median loss increased directly with the annual income of the perpetrator. The schemes perpetrated by individuals who earned over $500,000 were associated with a median loss of $50 million dollars 50 times that of any other income bracket.

56 Median Loss Based on Perpetrator s Annual Income Source: Association of Certified Fraud Examiners 2008 Report to the Nation on Occupational Fraud and Abuse

57 Why? Older, more educated males tend to occupy more positions of authority and trust, and have a greater degree of control over company assets.

58 Profile of a Typical Fraudster White Male College educated Over the age of 40 Occupies position of authority and trust Often married, well respected in the community, etc. Under stress As women and minorities move into more positions of authority, this profile is changing. In our industry, the typical fraudster does not necessarily fit this profile it could be anybody, and it is often the person you would least expect.

59 Fraud Statistics continued The typical perpetrator is a first-time offender. The average fraud scheme lasts approximately 24 months before detection. Small businesses (and small departments) are the most vulnerable to fraud and abuse. Cash is the asset most frequently targeted by dishonest employees.

60 Fraud Statistics continued What is the most common method for detecting fraud? Internal controls? Internal audit? By accident? Tip from employee, vendor, customer, other? External audit? The most common method for detecting fraud is a tip from an employee, customer, vendor or anonymous source. The next most common method is by internal controls, followed by accident or from an internal audit.

Initial Detection of Occupational")

61 Fraud Detection (Source: Association of Certified Fraud Examiners 2008 Report to the Nation on Occupational Fraud & Abuse) Initial Detection of Occupational Fraud

62 Percent of Tips by Source (Source: Association of Certified Fraud Examiners 2008 Report to the Nation on Occupational Fraud & Abuse)

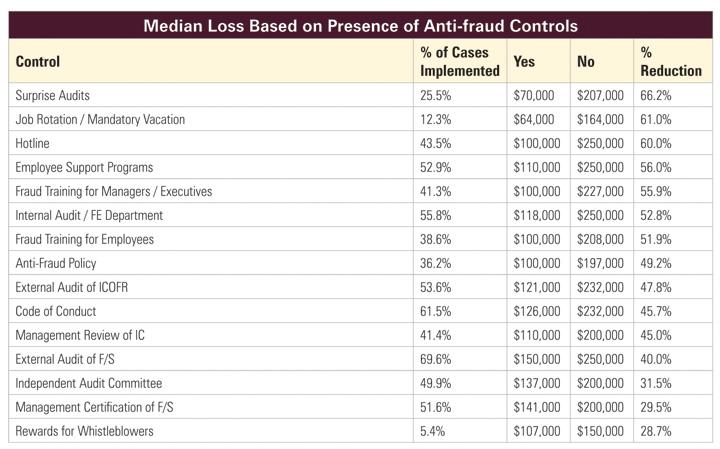

63 Fraud Statistics continued Which measures are most helpful in preventing fraud? Audits internal or external? Background checks? Internal Controls? Hotlines? Fraud Awareness/Ethics training? Strong internal controls are the best deterrent to fraud; however, organizations without fraud hotlines suffered fraud losses that were 2.5 times greater than those with hotlines. Organizations without internal audit functions suffered median losses more than twice those with an internal audit function. Organizations without fraud training had twice the median losses of those that did not have such training. Background checks are valuable, but almost 90% of fraudsters have no previous charges or convictions.

64

65 Credit Checks Financial pressures are one of the key motivating factors of occupational fraud, and the two most commonly cited behavioral red flags among fraudsters were financial difficulties and living beyond one s means. Given that financial difficulties are often associated with fraudulent behavior, it would seem advisable for organizations to devote more efforts to conducting credit background checks on new applicants.

66 Control Weaknesses that Contributed to Fraud (Source: Association of Certified Fraud Examiners 2008 Report to the Nation on Occupational Fraud & Abuse) Lack of controls, absence of management review, and override of existing controls were the three most commonly cited factors by survey participants, that allowed fraud schemes to succeed.

67 Necessary Components of Fraud Motive Opportunity Rationalization

68 Components of Fraud Motive - some kind of pressure or perceived pressure, typically financial, such as the need to pay for: Hospital bills Child support or alimony Gambling debts or other addictions Extramarital affairs An expensive lifestyle Motive could also be greed, revenge, thrill seeking, etc.

69 Components of Fraud Opportunity or perceived opportunity typically caused by circumventing internal controls or by internal controls weaknesses. Examples: Nobody counts supply inventory or checks deviations from specifications, so losses are not known. Equipment is checked on the inventory list without being physically located. The petty cash box is left unattended. Laptops and digital cameras are left out in the open in unlocked offices. People are given authority, but their work is not reviewed. Too much trust and responsibility placed in one employee - improper separation of duties. Employees that are caught stealing get fired, but aren t prosecuted.

70 Opportunity continued More Examples: Supervisors set a bad example by using university equipment for personal use, padding travel expense reimbursements, not paying for personal long distance calls or copies, not reporting leave, etc. Supervisors set a bad example by not dealing with problem employees, showing favoritism, allowing employees to abuse privileges, etc. Monthly financial reports are not reviewed by managers. There are not expectations with regard to ethical behavior, no hotline, no internal audit function, no training on internal controls and fraud. The perception of detection is the biggest deterrent to fraud.

71 Components of Fraud Rationalization some excuse or validation for actions, such as: I m just borrowing the money and will pay it back; it s only temporary until I get over this financial difficulty. I need it more than they do, and they will never miss it. Everybody else is doing it. No one will get hurt. It s for a good purpose. I deserve it because I ve been treated unfairly the organization owes me.

72 Fraud Detection Symptoms or indications that fraud may exist in an organization (Organizational Red Flags ): Internal Control Weaknesses lack of: segregation of duties, physical safeguards, independent checks, proper authorizations, proper documents and records, overriding of existing controls. Analytical Anomalies unexplained inventory shortages, deviations from specifications, increased scrap, purchases in excess of needs, too many voided transactions and returns, unusual cash shortages.

73 Fraud Detection continued More possible indications (Employee Red Flags ): Lifestyle changes/extravagant lifestyles Significant personal debt and credit problems Unusual behavior most perpetrators are under stress caused by feelings of guilt and the fear of being caught. Stress causes behavioral changes such as insomnia, addictions, irritability. Missing or altered documents, denial of access to records, refusal to take vacations or sick leave.

74 Fraud Prevention Create a culture of honesty - Set a good example and do not tolerate dishonest or unethical behavior in others Have a written code of ethics and make sure everyone is aware of it (NMSU Policy Manual Section 3.19) Check employee references, conduct background checks (NMSU Policy Manual Section ) Train employees in fraud awareness Create a positive work environment Provide employee assistance programs (

75 Fraud Prevention continued Limit Opportunities for Fraud Implement a strong system of internal controls and monitoring Make sure all employees are aware of and have access to policies and procedures Alert vendors and contractors to company policies Establish a hotline Create an expectation of punishment Proactively audit for fraud

76 How to Encourage Fraud (Source: Fraud Examination for Managers & Auditors by Jack C. Robertson, PhD, CPA, CFE) Practice autocratic management Manage by power with little trust in people Manage by crisis Centralize authority in top management Measure performance on a short-term basis Make rewards punitive, stingy and political Give feedback that is always critical and negative Create a highly hostile, competitive workplace

77 More Ways to Encourage Fraud Let your secretary, accounting tech, audit/budget tech, records tech, administrative assistant do everything. While you re at it, give them your passwords and approval access codes. Never look at or verify your monthly financial reports. Openly criticize and disregard institutional policies and procedures.

78 What to Do if You Suspect Fraud Contact Audit Services by phone, fax, or in person File a report through the NMSU Confidential Reporting Line at: or by calling: ETHICSP ( ) For additional information, refer to Section 7.15 of the Business Procedures Manual

79 Office of Audit Services Phone: 575/ Fax: 575/ MSC 3AU (Hadley Hall, Rm. 134) New Mexico State University P.O. Box Las Cruces, NM Website:

80 Sources of Additional Information COSO - Internal Control Integrated Framework AICPA Summary of Sarbanes-Oxley (Type Sarbanes-Oxley into Search box & scroll down to item 5) Association of Certified Fraud Examiners, 2008 Report to the Nation:

81 QUESTIONS OR COMMENTS? THANK YOU FOR COMING!

82 Training Addendum COSO issued a new framework in September 2004 titled: Enterprise Risk Management Integrated Framework This is a more robust framework for an organization s management to identify, assess and manage risk. Commonly referred to as ERM. Does not replace the Internal Control Framework issued in 1992, but does incorporate it into a broader risk management process.

83 Enterprise Risk Management Defined Enterprise risk management is a process, effected by an entity s board of directors, management and other personnel, applied in strategy setting and across the enterprise, designed to identify potential events that may affect the entity, and manage risk to be within its risk appetite, to provide reasonable assurance regarding the achievement of entity objectives.

84 The ERM Framework Entity objectives can be viewed in the context of four categories: Strategic Compliance Operations Reporting

85 Objectives Strategic high-level goals, aligned with and supporting the mission Operations effective and efficient use of resources Reporting reliability of reporting Compliance compliance with applicable laws and regulations

86 For more information:

Fraud Prevention Training

Fraud Prevention Training The Massachusetts Collectors and Treasurers Association Sixty-Sixth Annual Education Conference June 15, 2015 Presented By: Eric Demas, CFE Melanson Heath edemas@melansonheath.com

Fraud Prevention Training The Massachusetts Collectors and Treasurers Association Sixty-Sixth Annual Education Conference June 15, 2015 Presented By: Eric Demas, CFE Melanson Heath edemas@melansonheath.com

STUDY UNIT TEN INTERNAL AUDIT RESPONSIBILITIES FOR FRAUD

STUDY UNIT TEN INTERNAL AUDIT RESPONSIBILITIES FOR FRAUD 1 10.1 Fraud -- Nature, Prevention, and Detection..................................... 1 10.2 Fraud -- Indicators........................................................

STUDY UNIT TEN INTERNAL AUDIT RESPONSIBILITIES FOR FRAUD 1 10.1 Fraud -- Nature, Prevention, and Detection..................................... 1 10.2 Fraud -- Indicators........................................................

FRAUD SCHEMES. South Carolina HFMA Finance & Reimbursement Forum. November 13, 2012 WITH RELATED INTERNAL CONTROLS

FRAUD SCHEMES WITH RELATED INTERNAL CONTROLS South Carolina HFMA Finance & Reimbursement Forum November 13, 2012 2 Fraud Facts: Estimated loss of 5% of annual revenues to occupational fraud Financial statement

FRAUD SCHEMES WITH RELATED INTERNAL CONTROLS South Carolina HFMA Finance & Reimbursement Forum November 13, 2012 2 Fraud Facts: Estimated loss of 5% of annual revenues to occupational fraud Financial statement

Fraud Prevention and Detection Michael Schulstad, CPA/CFF/CGMA/FBI (ret)

") WEALTH ADVISORY OUTSOURCING AUDIT, TAX, AND CONSULTING Investment advisory services are offered through CliftonLarsonAllen Wealth Advisors, LLC, an SEC-registered investment advisor Fraud Prevention and

WEALTH ADVISORY OUTSOURCING AUDIT, TAX, AND CONSULTING Investment advisory services are offered through CliftonLarsonAllen Wealth Advisors, LLC, an SEC-registered investment advisor Fraud Prevention and

Eric Kinsherf, CPA MMAAA Conference June 12, 2018

Eric Kinsherf, CPA MMAAA Conference June 12, 2018 Agenda Overview What is Fraud? How does Fraud happen? How to Detect and Prevent Fraud Summarize Objectives Gain better Understanding of Fraud Risk Illustrate

Eric Kinsherf, CPA MMAAA Conference June 12, 2018 Agenda Overview What is Fraud? How does Fraud happen? How to Detect and Prevent Fraud Summarize Objectives Gain better Understanding of Fraud Risk Illustrate

2/27/2017. Segregation of Duties/ Internal Controls. Objectives. Agenda

Segregation of Duties/ Internal Controls 2017 WASBO Accounting Conference David Maccoux, Shareholder Objectives Discuss failures of internal controls to detect or prevent fraud and learn how to implement

Segregation of Duties/ Internal Controls 2017 WASBO Accounting Conference David Maccoux, Shareholder Objectives Discuss failures of internal controls to detect or prevent fraud and learn how to implement

OVERVIEW. Common Personality Traits of Fraudsters. Common Sources of Pressure. Changes in Behavior

Red Flags of Fraud OVERVIEW Red Flags of Fraud are warning signs that may indicate a higher fraud risk. They are NOT evidence that fraud is actually occurring. Many employees demonstrate one or more of

Red Flags of Fraud OVERVIEW Red Flags of Fraud are warning signs that may indicate a higher fraud risk. They are NOT evidence that fraud is actually occurring. Many employees demonstrate one or more of

Fraud Prevention, Detection and Control. Elizabeth Coles, CPA Aldrich CPAs + Advisors LLP

Fraud Prevention, Detection and Control Elizabeth Coles, CPA Aldrich CPAs + Advisors LLP 1 Agenda Who and Why? Fraud Schemes and Risks Fraud Prevention what can you do? 3 Who Commits Fraud? Long time,

Fraud Prevention, Detection and Control Elizabeth Coles, CPA Aldrich CPAs + Advisors LLP 1 Agenda Who and Why? Fraud Schemes and Risks Fraud Prevention what can you do? 3 Who Commits Fraud? Long time,

Internal Controls. They Are Everyone s Business. Valdosta State University Office of Internal Audits June 2016

Internal Controls They Are Everyone s Business Valdosta State University Office of Internal Audits June 2016 1 Presentation Overview Understand Internal Controls Identify Control Weaknesses Fraud Best

Internal Controls They Are Everyone s Business Valdosta State University Office of Internal Audits June 2016 1 Presentation Overview Understand Internal Controls Identify Control Weaknesses Fraud Best

Fraud Prevention, Detection, and Internal Controls

Fraud Prevention, Detection, and Internal Controls Budget, Accounting and Reporting Council May 28, 2015 Sherrie Ard, CPA, CFE Financial Management Specialist Local Government Performance Center Local

Fraud Prevention, Detection, and Internal Controls Budget, Accounting and Reporting Council May 28, 2015 Sherrie Ard, CPA, CFE Financial Management Specialist Local Government Performance Center Local

Information and and training provid v ed by Smith Elliott Elliott Kearns & Compan

Nuts and Bolts of Avoiding Fraud in Your Organization Information and training provided by Smith Elliott Kearns & Company, LLC as part of this Fraud Avoidance presentation is intended for reference only.

Nuts and Bolts of Avoiding Fraud in Your Organization Information and training provided by Smith Elliott Kearns & Company, LLC as part of this Fraud Avoidance presentation is intended for reference only.

Presented by Ed Williamson and Erica Bailey

Presented by Ed Williamson and Erica Bailey Internal Controls & Fraud Detection Objectives Background on internal controls Review of organizational and functional level controls Fraud prevention and risk

Presented by Ed Williamson and Erica Bailey Internal Controls & Fraud Detection Objectives Background on internal controls Review of organizational and functional level controls Fraud prevention and risk

FRAUD AWARENESS UPDATE

Tammy Michaud, CPA, Principal Sarah Belliveau, CPA, Senior Manager FRAUD AWARENESS UPDATE berrydunn.com CATEGORIES OF FRAUD Asset misappropriations (stealing) Theft or misuse of assets Corruption Inappropriate

Tammy Michaud, CPA, Principal Sarah Belliveau, CPA, Senior Manager FRAUD AWARENESS UPDATE berrydunn.com CATEGORIES OF FRAUD Asset misappropriations (stealing) Theft or misuse of assets Corruption Inappropriate

Karen L. Mosteller, CPA, CHBC

Karen L. Mosteller, CPA, CHBC Recognize the Red Flags of Fraud and areas of vulnerability Examine checks and balances that should be implemented Establish processes and procedures needed for fraud protection

Karen L. Mosteller, CPA, CHBC Recognize the Red Flags of Fraud and areas of vulnerability Examine checks and balances that should be implemented Establish processes and procedures needed for fraud protection

My experiences with Employee Fraud

My experiences with Employee Fraud - Capt Percy Jokhi March 18, 2008 Introduction The present industry scenario is most prone to losses due to Fraud not only associated with external agencies, but more

My experiences with Employee Fraud - Capt Percy Jokhi March 18, 2008 Introduction The present industry scenario is most prone to losses due to Fraud not only associated with external agencies, but more

Virginia Association of School Business Officers Getting Reacquainted with Internal Controls Presented by John S. Aldridge, CPA

Virginia Association of School Business Officers Getting Reacquainted with Internal Controls Presented by John S. Aldridge, CPA Introduction What are internal controls? Simple Definition Internal control

Virginia Association of School Business Officers Getting Reacquainted with Internal Controls Presented by John S. Aldridge, CPA Introduction What are internal controls? Simple Definition Internal control

Can You Spot Fraudsters?

Can You Spot Fraudsters? CACUBO Workshop March 22, 2018 Eric Conforti, CPA, CFE 1 Who Are We? A One-Firm Firm: Over 2,200 industry experts to partner with when specific industry knowledge is needed during

Can You Spot Fraudsters? CACUBO Workshop March 22, 2018 Eric Conforti, CPA, CFE 1 Who Are We? A One-Firm Firm: Over 2,200 industry experts to partner with when specific industry knowledge is needed during

Internal Control 2015 Training

Internal Control 2015 Training Internal Control Training is a mandate under the New York State Internal Control Act, which states that NYS agencies implement education and training efforts to ensure all

Internal Control 2015 Training Internal Control Training is a mandate under the New York State Internal Control Act, which states that NYS agencies implement education and training efforts to ensure all

Moving the Needle: Fighting Fraud from the Inside Through Audit. Mary Breslin, CFE, CIA President Empower Audit Training and Consulting

Moving the Needle: Fighting Fraud from the Inside Through Audit Mary Breslin, CFE, CIA President Empower Audit Training and Consulting Moving the Needle Fighting Fraud from the Inside Through Audit Mary

Moving the Needle: Fighting Fraud from the Inside Through Audit Mary Breslin, CFE, CIA President Empower Audit Training and Consulting Moving the Needle Fighting Fraud from the Inside Through Audit Mary

Fraud in the Insurance Industry How it Can Impact Your Agency

A MarshBerry Publication Volume XXIX, Issue 4 APRIL 2013 Authored by Molly McCarthy, Senior Consultant 440.392.6584 email: Molly.McCarthy@MarshBerry.com Fraud in the Insurance Industry How it Can Impact

A MarshBerry Publication Volume XXIX, Issue 4 APRIL 2013 Authored by Molly McCarthy, Senior Consultant 440.392.6584 email: Molly.McCarthy@MarshBerry.com Fraud in the Insurance Industry How it Can Impact

Internal Controls for Deans, Directors and Chairs

Internal Controls for Deans, Directors and Chairs Presented by: Laura Howat, CPA Controller/Director Financial Management Financial and Business Services Phone: 801-581-5077 Email: laura.howat@admin.utah.edu

Internal Controls for Deans, Directors and Chairs Presented by: Laura Howat, CPA Controller/Director Financial Management Financial and Business Services Phone: 801-581-5077 Email: laura.howat@admin.utah.edu

INTERNAL AUDIT EFFECTIVENESS. Conducting Fraud Investigations Conducting Internal Audit

INTERNAL AUDIT EFFECTIVENESS Conducting Fraud Investigations Conducting Internal Audit Conducting Fraud Investigations Why Fraud? Fraud is the product of three factors: Supply of motivated offenders; The

INTERNAL AUDIT EFFECTIVENESS Conducting Fraud Investigations Conducting Internal Audit Conducting Fraud Investigations Why Fraud? Fraud is the product of three factors: Supply of motivated offenders; The

PREVENTING FRAUD BEFORE IT IS TOO LATE Presented to LeadingAge Michigan Annual Conference and Trade Show May 19, 2015

Arlen S. Lasinsky Frost, Ruttenberg & Rothblatt, P.C. alasinsky@frrcpas.com 847/282-6352 Phone and Fax www.frrcpas.com PREVENTING FRAUD BEFORE IT IS TOO LATE Presented to LeadingAge Michigan Annual Conference

Arlen S. Lasinsky Frost, Ruttenberg & Rothblatt, P.C. alasinsky@frrcpas.com 847/282-6352 Phone and Fax www.frrcpas.com PREVENTING FRAUD BEFORE IT IS TOO LATE Presented to LeadingAge Michigan Annual Conference

Guide to Internal Controls

Guide to Internal Controls Table of Contents Introduction to Internal Controls...3 Roles...4 Components....5 Control Environment...5 Risk assessment...6 Control Activities...7 Information & Communication...9

Guide to Internal Controls Table of Contents Introduction to Internal Controls...3 Roles...4 Components....5 Control Environment...5 Risk assessment...6 Control Activities...7 Information & Communication...9

OCCUPATIONAL FRAUD IN GOVERNMENT AND STEPS TO PREVENT AND DETECT IT

OCCUPATIONAL FRAUD IN GOVERNMENT AND STEPS TO PREVENT AND DETECT IT This session will explore government fraud risks as well as common areas of abuse and corresponding red flags. It will also provide ideas

OCCUPATIONAL FRAUD IN GOVERNMENT AND STEPS TO PREVENT AND DETECT IT This session will explore government fraud risks as well as common areas of abuse and corresponding red flags. It will also provide ideas

Fraud and the Small Business Owner

Fraud and the Small Business Owner Can you recognize it when you see it? National Society of Accountants Annual Meeting August 15, 2009 Erik H. Lindquist, CFE Presenter Definition The use of one s occupation

Fraud and the Small Business Owner Can you recognize it when you see it? National Society of Accountants Annual Meeting August 15, 2009 Erik H. Lindquist, CFE Presenter Definition The use of one s occupation

MANAGING FRAUD RISK. Teresa D. Thamer, CPA, CFE Brenau University

MANAGING FRAUD RISK Teresa D. Thamer, CPA, CFE Brenau University Overview I. Understanding what Fraud is and is not II. Identifying and assessing key fraud risk areas III. Developing a Comprehensive Fraud

MANAGING FRAUD RISK Teresa D. Thamer, CPA, CFE Brenau University Overview I. Understanding what Fraud is and is not II. Identifying and assessing key fraud risk areas III. Developing a Comprehensive Fraud

Laurie Beets. PDG 27 th National College & University Bursars & SFS Conference

Foiling Fraudsters Laurie Beets Oklahoma State University Acknowledgements 2006 Fraud Examiners Manual, Association of Certified Fraud Examiners (ACFE) 2012 Report to the Nation on Occupational Fraud &

Foiling Fraudsters Laurie Beets Oklahoma State University Acknowledgements 2006 Fraud Examiners Manual, Association of Certified Fraud Examiners (ACFE) 2012 Report to the Nation on Occupational Fraud &

Employee Dishonesty: Prevention and Detection

Employee Dishonesty: Prevention and Detection Frontline Risk Management Series Welcome to this session on Employee Dishonesty, a risk management module presented by CUMIS General Insurance s Risk Solutions

Employee Dishonesty: Prevention and Detection Frontline Risk Management Series Welcome to this session on Employee Dishonesty, a risk management module presented by CUMIS General Insurance s Risk Solutions

- Excessive gambling or investment habits - Strong challenge to beat the system - Undue family pressure such as divorce - Overwhelming desire for pers

RED FLAGS OF INTERNAL FRAUD PROFILE OF THE PERPETRATOR: - Most frequently it is the person you trust the most - Has the technical skills to pull off the theft secretly - The activity is clandestine - The

RED FLAGS OF INTERNAL FRAUD PROFILE OF THE PERPETRATOR: - Most frequently it is the person you trust the most - Has the technical skills to pull off the theft secretly - The activity is clandestine - The

Internal Controls: Providing an Effective Control Environment. Why This Session Is Needed. Lesson Overview & Module Objectives

Internal Controls: Providing an Effective Control Environment Internal Controls 1 Why This Session Is Needed Uniform Guidance has expanded the requirements and increased the focus on internal controls

Internal Controls: Providing an Effective Control Environment Internal Controls 1 Why This Session Is Needed Uniform Guidance has expanded the requirements and increased the focus on internal controls

OUTSMART FRAUD. Strategic Internal Controls to Prevent Business Fraud

OUTSMART FRAUD Strategic Internal Controls to Prevent Business Fraud GrowthForce LLC 800 Rockmead Drive Suite 200 Phone 281.358.2007 Fax 281.358.4120 OUTSMART BUSINESS FRAUD Using statistical data from

OUTSMART FRAUD Strategic Internal Controls to Prevent Business Fraud GrowthForce LLC 800 Rockmead Drive Suite 200 Phone 281.358.2007 Fax 281.358.4120 OUTSMART BUSINESS FRAUD Using statistical data from

Module 1: Safeguarding District Resources: Roles & Responsibilities

Module 1: Safeguarding District Resources: Roles & Responsibilities Presenter: Jamie P. McPherson Leadership Development Manager New School Board Member Mandated Training Day Two: Fiscal Oversight Training

Module 1: Safeguarding District Resources: Roles & Responsibilities Presenter: Jamie P. McPherson Leadership Development Manager New School Board Member Mandated Training Day Two: Fiscal Oversight Training

Annual Audit and Other Financial Matters

Getting Ready for Your Annual Audit and Other Financial Matters by Donna M. Ingram, CPA, CFE, Cr.FA, CFF Donna M. Ingram, CPA, PC dingram@cablelynx.com Role of the Auditor The role of the independent auditor

Getting Ready for Your Annual Audit and Other Financial Matters by Donna M. Ingram, CPA, CFE, Cr.FA, CFF Donna M. Ingram, CPA, PC dingram@cablelynx.com Role of the Auditor The role of the independent auditor

Internal Controls. Presented by: Mark Payne, CPA Partner Rae Kerr, CPA Senior Manager. March 5, 2014

Internal Controls Presented by: Mark Payne, CPA Partner Rae Kerr, CPA Senior Manager March 5, 2014 What Are Internal Controls? Internal controls are a set of policies and procedures to prevent deliberate

Internal Controls Presented by: Mark Payne, CPA Partner Rae Kerr, CPA Senior Manager March 5, 2014 What Are Internal Controls? Internal controls are a set of policies and procedures to prevent deliberate

SMALL BUSINESS FRAUD ASSESSMENT INTERNAL CONTROL QUESTIONNAIRE Download your risk assessment form at

SMALL BUSINESS FRAUD ASSESSMENT INTERNAL CONTROL QUESTIONNAIRE Download your risk assessment form at www.businessfraudprevention.org/forms.html Owner: Date: Discussed with: Question Yes No N/A Comments

SMALL BUSINESS FRAUD ASSESSMENT INTERNAL CONTROL QUESTIONNAIRE Download your risk assessment form at www.businessfraudprevention.org/forms.html Owner: Date: Discussed with: Question Yes No N/A Comments

Fraud Awareness Jennifer Murtha Clara Ewing

Fraud Awareness Jennifer Murtha Clara Ewing The Monkey Business Illusion 2 Fraud Defined The term fraud is defined in Black's Law Dictionary (Sixth Edition, 1990) as: An intentional perversion of truth

Fraud Awareness Jennifer Murtha Clara Ewing The Monkey Business Illusion 2 Fraud Defined The term fraud is defined in Black's Law Dictionary (Sixth Edition, 1990) as: An intentional perversion of truth

Understanding Internal Controls Office of Internal Audit

Understanding Internal Controls Office of Internal Audit July 2015 Objectives for this manual Provide guidance to help management understand their responsibility to ensure that internal controls are established,

Understanding Internal Controls Office of Internal Audit July 2015 Objectives for this manual Provide guidance to help management understand their responsibility to ensure that internal controls are established,

This Questionnaire/Guide is intended to assist you in decision making, as well as in day-to-day operations. Best Regards,

In an effort to disseminate information and assure that we are in compliance with guidelines caused by the Sarbanes Oxley Act that proper internal controls are being adhered to, we have developed some

In an effort to disseminate information and assure that we are in compliance with guidelines caused by the Sarbanes Oxley Act that proper internal controls are being adhered to, we have developed some

ACCTG 533: Module 14: Asset Misappropriation Fraud. [Slide Content]: Asset Misappropriation Fraud. [Jeanne H. Yamamura]: Asset Misappropriation Fraud

![ACCTG 533: Module 14: Asset Misappropriation Fraud. [Slide Content]: Asset Misappropriation Fraud. [Jeanne H. Yamamura]: Asset Misappropriation Fraud](/thumbs/81/83190759.jpg "ACCTG 533: Module 14: Asset Misappropriation Fraud. [Slide Content]: Asset Misappropriation Fraud. [Jeanne H. Yamamura]: Asset Misappropriation Fraud") ACCTG 533: Module 14: Asset Misappropriation Fraud Asset Misappropriation Fraud Asset Misappropriation Fraud Asset Misappropriation Fraud Theft or misuse of company assets Most common type of fraud Every

ACCTG 533: Module 14: Asset Misappropriation Fraud Asset Misappropriation Fraud Asset Misappropriation Fraud Asset Misappropriation Fraud Theft or misuse of company assets Most common type of fraud Every

Protecting Your Organization Against Fraud

Protecting Your Organization Against Fraud Special Agent Jamila Davis/Region 4 May 2015 SECTION I HUDOIG - Mission and Purpose HUDOIG Mission As the Office of Inspector General (OIG) for the U.S. Department

Protecting Your Organization Against Fraud Special Agent Jamila Davis/Region 4 May 2015 SECTION I HUDOIG - Mission and Purpose HUDOIG Mission As the Office of Inspector General (OIG) for the U.S. Department

Agenda. Course Objectives. Internal Controls Workshop. Financial and Business Services Course Objectives Ethics

Internal Controls Workshop Financial and Business Services 2009 Agenda Course Objectives Ethics Introduction to internal control What happens when internal control is weak Fraud Internal control theory

Internal Controls Workshop Financial and Business Services 2009 Agenda Course Objectives Ethics Introduction to internal control What happens when internal control is weak Fraud Internal control theory

BFSv9 Internal Controls Guidance

presented by: Hans Gude, MBA, CIA Barbara VanCleave Smith, PhD, CPA Office of Ethics, Compliance, and Risk Management Presented May 10 and 17, 2010 LMS Course Number BECTR306 1 Today s Topics 1. Overview

presented by: Hans Gude, MBA, CIA Barbara VanCleave Smith, PhD, CPA Office of Ethics, Compliance, and Risk Management Presented May 10 and 17, 2010 LMS Course Number BECTR306 1 Today s Topics 1. Overview

Cash Receipting: Fraud Prevention and Internal Controls

Office of the Washington State Auditor Pat McCarthy Cash Receipting: Fraud Prevention and Internal Controls WACO Annual Conference October 3, 2018 Table of Contents Fraud Statistics and Overview... 2 Importance

Office of the Washington State Auditor Pat McCarthy Cash Receipting: Fraud Prevention and Internal Controls WACO Annual Conference October 3, 2018 Table of Contents Fraud Statistics and Overview... 2 Importance

Fraud Risk Management

Fraud Risk Management Introduction Bethmara Kessler, CFE, CISA Campbell Soup Company 2017 Association of Certified Fraud Examiners, Inc. CPE Information 2017 Association of Certified Fraud Examiners, Inc.

Fraud Risk Management Introduction Bethmara Kessler, CFE, CISA Campbell Soup Company 2017 Association of Certified Fraud Examiners, Inc. CPE Information 2017 Association of Certified Fraud Examiners, Inc.

Internal Control in Higher Education

Internal Control in Higher Education Daniel Adams Office of Audit Services Audit Services Mission To provide assurance and advisory services that are independent, objective and risk-based in order to protect

Internal Control in Higher Education Daniel Adams Office of Audit Services Audit Services Mission To provide assurance and advisory services that are independent, objective and risk-based in order to protect

Diving into the 2013 COSO Framework. Presented by: Ronald A. Conrad

Diving into the 2013 COSO Framework Presented by: Ronald A. Conrad 2 Objectives Obtain an understanding of why the COSO Framework has been updated Understand how the framework has changed Identify the

Diving into the 2013 COSO Framework Presented by: Ronald A. Conrad 2 Objectives Obtain an understanding of why the COSO Framework has been updated Understand how the framework has changed Identify the

Internal Control: The Human Risk Factor

Internal Control: The Human Risk Factor 1 P R E S E N T A T I O N F O R T H E S P D N E W C F O O R I E N T A T I O N P R O G R A M M A Y 1 5, 2 0 1 7 Ann Gibson, PhD, CPA Andrews University Purposes of

Internal Control: The Human Risk Factor 1 P R E S E N T A T I O N F O R T H E S P D N E W C F O O R I E N T A T I O N P R O G R A M M A Y 1 5, 2 0 1 7 Ann Gibson, PhD, CPA Andrews University Purposes of

Internal Control: The Human Risk Factor

Internal Control: The Human Risk Factor 1 E U D O R I E N T A T I O N F O R N E W U N I O N A N D C O N F E R E N C E O F F I C E R S A U G U S T 2 8 S E P T E M B E R 1, 2 0 1 7 Ann Gibson, PhD, CPA Andrews

Internal Control: The Human Risk Factor 1 E U D O R I E N T A T I O N F O R N E W U N I O N A N D C O N F E R E N C E O F F I C E R S A U G U S T 2 8 S E P T E M B E R 1, 2 0 1 7 Ann Gibson, PhD, CPA Andrews

Fraud Risk Management

Fraud Risk Management Specific Anti-Fraud Controls (Process or Transaction Level) 2017 Association of Certified Fraud Examiners, Inc. Discussion Questions 1. Does your organization have adequate staffing

Fraud Risk Management Specific Anti-Fraud Controls (Process or Transaction Level) 2017 Association of Certified Fraud Examiners, Inc. Discussion Questions 1. Does your organization have adequate staffing

FRAUD DETECTION. Early Detection = $ Saved. Red Flag = Danger. But a symptom = FRAUD. Accounting Anomalies. Accounting Anomalies

Proactive Fraud Auditing End of Chapter 4 in Albrecht FRAUD DETECTION Recognizing the Symptoms of Fraud Actg 537 Identify Risk Exposures 1 2 Identify Fraud Symptoms for Each Exposure Proactively Look for

Proactive Fraud Auditing End of Chapter 4 in Albrecht FRAUD DETECTION Recognizing the Symptoms of Fraud Actg 537 Identify Risk Exposures 1 2 Identify Fraud Symptoms for Each Exposure Proactively Look for

9. Internal control Internal control, as defined in accounting and auditing, is a process for assuring achievement of an organization's objectives in

9. Internal control Internal control, as defined in accounting and auditing, is a process for assuring achievement of an organization's objectives in operational effectiveness and efficiency, reliable

9. Internal control Internal control, as defined in accounting and auditing, is a process for assuring achievement of an organization's objectives in operational effectiveness and efficiency, reliable

FRAUD IN GOVERNMENT AN OPEN DISCUSSION. Presented By William Blend, CPA, CFE

FRAUD IN GOVERNMENT AN OPEN DISCUSSION Presented By William Blend, CPA, CFE AGENDA Fraud and Ethics Discussion Fraud Triangle and Beyond Data from 2016 ACFE Report to the Nations Recent Fraud Investigations

FRAUD IN GOVERNMENT AN OPEN DISCUSSION Presented By William Blend, CPA, CFE AGENDA Fraud and Ethics Discussion Fraud Triangle and Beyond Data from 2016 ACFE Report to the Nations Recent Fraud Investigations

FRAUD DETERRENCE AND DETECTION

FRAUD DETERRENCE AND DETECTION Segregation of Duties Corruption Scheme Red Flags Unchecked authority to approve No formal documented procedures Circumventing normal policies and procedures Employees receiving

FRAUD DETERRENCE AND DETECTION Segregation of Duties Corruption Scheme Red Flags Unchecked authority to approve No formal documented procedures Circumventing normal policies and procedures Employees receiving

Internal Control: The Human Risk Factor

Andrews University Digital Commons @ Andrews University Faculty Publications 5-15-2017 Internal Control: The Human Risk Factor Annetta M. Gibson Andrews University, gibson@andrews.edu Follow this and additional

Andrews University Digital Commons @ Andrews University Faculty Publications 5-15-2017 Internal Control: The Human Risk Factor Annetta M. Gibson Andrews University, gibson@andrews.edu Follow this and additional

Creating a Fraud Risk Assessment and Implementing a Continuous Monitoring Program. Christopher DiLorenzo, CFE, CPA, CIA, CRMA

Creating a Fraud Risk Assessment and Implementing a Continuous Monitoring Program Christopher DiLorenzo, CFE, CPA, CIA, CRMA 2015 Association of Certified Fraud Examiners, Inc. Creating a Robust Fraud

Creating a Fraud Risk Assessment and Implementing a Continuous Monitoring Program Christopher DiLorenzo, CFE, CPA, CIA, CRMA 2015 Association of Certified Fraud Examiners, Inc. Creating a Robust Fraud

2/20/15. Trevor Stewart, CPA Director of Business Services Source documentation includes CCIA and FCMAT

2/20/15 Trevor Stewart, CPA Director of Business Services Source documentation includes CCIA and FCMAT The Fraud Triangle factors that influence the commission of fraud The Fraud Tree occupational fraud

2/20/15 Trevor Stewart, CPA Director of Business Services Source documentation includes CCIA and FCMAT The Fraud Triangle factors that influence the commission of fraud The Fraud Tree occupational fraud

Cash Receipting: Fraud Prevention and Internal Controls

Cash Receipting: Fraud Prevention and Internal Controls Your government works hard to serve its residents with the resources available. This can mean that the internal processes you rely on to do your

Cash Receipting: Fraud Prevention and Internal Controls Your government works hard to serve its residents with the resources available. This can mean that the internal processes you rely on to do your

Changing Your Paradigm on Risks and Controls

Changing Your Paradigm on Risks and Controls Stacey Walker, CPA, CFE Director, Internal Auditing Office of Audit, Compliance & Privacy October 31, 2018 OBJECTIVE: PARADIGM CHANGE Paradigm A set of assumptions,

Changing Your Paradigm on Risks and Controls Stacey Walker, CPA, CFE Director, Internal Auditing Office of Audit, Compliance & Privacy October 31, 2018 OBJECTIVE: PARADIGM CHANGE Paradigm A set of assumptions,

Internal Controls and the Internal Auditor. Presented By: Richard Kudlik, CPA

Internal Controls and the Internal Auditor Presented By: Richard Kudlik, CPA Interrelated Components Control Environment Risk Assessment Control Activities Information and Communication Monitoring What

Internal Controls and the Internal Auditor Presented By: Richard Kudlik, CPA Interrelated Components Control Environment Risk Assessment Control Activities Information and Communication Monitoring What

Fraud in Construction Companies: Lessons From the Trenches

Fraud in Construction Companies: Lessons From the Trenches Presented by Angela Morelock, CPA, CFE, CFF, ABV, Certified Forensic Accountant www.bkdforensics.com Twitter: @AngelaMorelock Cost of Fraud &

Fraud in Construction Companies: Lessons From the Trenches Presented by Angela Morelock, CPA, CFE, CFF, ABV, Certified Forensic Accountant www.bkdforensics.com Twitter: @AngelaMorelock Cost of Fraud &

Common Frauds Found in Not-for- Profit Organizations

Common Frauds Found in Not-for- Profit Organizations NCACPA Not-for-Profit Conference May 19, 2015 Presented by Lynda M. Dennis CPA, CGFO, PhD Today s Session Overview 2014 Occupational Fraud Report Findings

Common Frauds Found in Not-for- Profit Organizations NCACPA Not-for-Profit Conference May 19, 2015 Presented by Lynda M. Dennis CPA, CGFO, PhD Today s Session Overview 2014 Occupational Fraud Report Findings

Internal Control Awareness: Tips for Improving Business Practices

Internal Control Awareness: Tips for Improving Business Practices S U S A N H A C K E R I N T E R N A L A U D I T O R Agenda Understand the value of internal controls. Learn some basic principles and best

Internal Control Awareness: Tips for Improving Business Practices S U S A N H A C K E R I N T E R N A L A U D I T O R Agenda Understand the value of internal controls. Learn some basic principles and best

Office of the Utah Legislative Auditor General. Fraud Prevention. Utah Government Finance Officers Association. Spring 2017 Conference

Office of the Utah Legislative Auditor General Fraud Prevention Utah Government Finance Officers Association Spring 2017 Conference Utah Legislative Auditor General Constitutional Charge and Authority

Office of the Utah Legislative Auditor General Fraud Prevention Utah Government Finance Officers Association Spring 2017 Conference Utah Legislative Auditor General Constitutional Charge and Authority

ACFE FRAUD PREVENTION CHECK-UP ASSOCIATION OF CERTIFIED FRAUD EXAMINERS

ACFE FRAUD PREVENTION ASSOCIATION OF CERTIFIED FRAUD EXAMINERS ACFE FRAUD PREVENTION One of the ACFE s most valuable fraud prevention resources, the ACFE Fraud Prevention Check-Up is a simple yet powerful

ACFE FRAUD PREVENTION ASSOCIATION OF CERTIFIED FRAUD EXAMINERS ACFE FRAUD PREVENTION One of the ACFE s most valuable fraud prevention resources, the ACFE Fraud Prevention Check-Up is a simple yet powerful

Week 3: Fraud, Procure to Pay Process Controls

Edward Beaver Edward.Beaver@temple.edu ff MIS 5121: Business Processes, ERP Systems & Controls Week 3: Fraud, Procure to Pay Process Controls Video: Record the Class Discussion v Something really new,

Edward Beaver Edward.Beaver@temple.edu ff MIS 5121: Business Processes, ERP Systems & Controls Week 3: Fraud, Procure to Pay Process Controls Video: Record the Class Discussion v Something really new,

In Control: Getting Familiar with the New COSO Guidelines. CSMFO Monterey, California February 18, 2015

In Control: Getting Familiar with the New COSO Guidelines CSMFO Monterey, California February 18, 2015 1 Background on COSO Part 1 2 Development of a comprehensive framework of internal control Internal

In Control: Getting Familiar with the New COSO Guidelines CSMFO Monterey, California February 18, 2015 1 Background on COSO Part 1 2 Development of a comprehensive framework of internal control Internal

Fraud Prevention: How to Identify and Protect Your Higher Ed Institution

Fraud Prevention: How to Identify and Protect Your Higher Ed Institution November 16, 2017 Investment advisory services are offered through CliftonLarsonAllen Wealth Advisors, LLC, an SEC-registered investment

Fraud Prevention: How to Identify and Protect Your Higher Ed Institution November 16, 2017 Investment advisory services are offered through CliftonLarsonAllen Wealth Advisors, LLC, an SEC-registered investment

CHAPTER 7. Internal Control. Review Questions

CHAPTER 7 Internal Control Review Questions 7 1 Internal control is a process, affected by the entity s board of directors, management and other personnel, designed to provide reasonable assurance regarding

CHAPTER 7 Internal Control Review Questions 7 1 Internal control is a process, affected by the entity s board of directors, management and other personnel, designed to provide reasonable assurance regarding

Fraud incident handling management. Meeting the challenges of fraud

Fraud incident handling management Meeting the challenges of fraud Recently, more companies are becoming more aware of the financial and reputational damage that fraud can cause to a company. Especially

Fraud incident handling management Meeting the challenges of fraud Recently, more companies are becoming more aware of the financial and reputational damage that fraud can cause to a company. Especially

Fraud Detection and Prevention

Fraud Detection and Prevention Presented by: Louise Hanson, Moss Adams LLP Emily Ogden, Moss Adams LLP April 24, 2014 1 DISCLOSURE STATEMENT The material appearing in this presentation is for informational

Fraud Detection and Prevention Presented by: Louise Hanson, Moss Adams LLP Emily Ogden, Moss Adams LLP April 24, 2014 1 DISCLOSURE STATEMENT The material appearing in this presentation is for informational

MSD Internal Control Policy 01/16/08. Metropolitan Sewerage District of Buncombe County Internal Control Policy

Metropolitan Sewerage District of Buncombe County Internal Control Policy Purpose: To document how the management of the Metropolitan Sewerage District of Buncombe County ( District ) has fulfilled their

Metropolitan Sewerage District of Buncombe County Internal Control Policy Purpose: To document how the management of the Metropolitan Sewerage District of Buncombe County ( District ) has fulfilled their

Chapter 7 Internal Controls

Chapter 7 Internal Controls Establishment of and adherence to internal controls is a major part of managing an organization. Internal controls serve as the first line of defense in safeguarding assets

Chapter 7 Internal Controls Establishment of and adherence to internal controls is a major part of managing an organization. Internal controls serve as the first line of defense in safeguarding assets

38 Years of Excellent Client Service New COSO Model and How Internal Controls Help to Reduce Opportunity for Fraud

38 Years of Excellent Client Service New COSO Model and How Internal Controls Help to Reduce Opportunity for Fraud Presented By William Blend, CPA, CFE Session Overview Review the new COSO model on internal

38 Years of Excellent Client Service New COSO Model and How Internal Controls Help to Reduce Opportunity for Fraud Presented By William Blend, CPA, CFE Session Overview Review the new COSO model on internal

The most commonly applied model for designing and auditing internal

Fair Value Accounting Fraud: New Global Risks and Detection Techniques By Gerard M. Zack Copyright 2009 by Gerard M. Zack Appendix C Internal Controls over Fair Value Accounting Applications The most commonly

Fair Value Accounting Fraud: New Global Risks and Detection Techniques By Gerard M. Zack Copyright 2009 by Gerard M. Zack Appendix C Internal Controls over Fair Value Accounting Applications The most commonly

FRAUD RISK FACTORS CHECKLIST (Source: New AU Section 240, Appendix A)

") Page 136 of 174 FRAUD RISK FACTORS CHECKLIST (Source: New AU Section 240, Appendix A) RECOGNIZING RISK FACTORS THAT SHOULD GET YOUR ATTENTION How to use the checklist: 1. Review this checklist towards

Page 136 of 174 FRAUD RISK FACTORS CHECKLIST (Source: New AU Section 240, Appendix A) RECOGNIZING RISK FACTORS THAT SHOULD GET YOUR ATTENTION How to use the checklist: 1. Review this checklist towards

AICC 2017 ANNUALMEETING PRESENTED BY MITCHELL E. KLINGHER CPA PROTECTING YOUR COMPANY FROM EMPLOYEE THEFT

AICC 2017 ANNUALMEETING PRESENTED BY MITCHELL E. KLINGHER CPA PROTECTING YOUR COMPANY FROM EMPLOYEE THEFT WHY DO THEY DO IT?????? THE PSYCHOLOGY OF THEFT Vicarious thrill It doesn t matter Everyone does

AICC 2017 ANNUALMEETING PRESENTED BY MITCHELL E. KLINGHER CPA PROTECTING YOUR COMPANY FROM EMPLOYEE THEFT WHY DO THEY DO IT?????? THE PSYCHOLOGY OF THEFT Vicarious thrill It doesn t matter Everyone does

Committee for Senior Business Administrators. Segregation of Duties

Committee for Senior Business Administrators Segregation of Duties Presented by: Tammy R. Hoskens and Margaret (Peggy) B. Zapalac University Risk and Compliance May 21, 2009 Segregation of Duties Segregation

Committee for Senior Business Administrators Segregation of Duties Presented by: Tammy R. Hoskens and Margaret (Peggy) B. Zapalac University Risk and Compliance May 21, 2009 Segregation of Duties Segregation

Kerkering, Barberio & Co. Certified Public Accountants

Kerkering, Barberio & Co. Certified Public Accountants 1990 Main Street, Suite 801, Sarasota, FL 34236 6320 Venture Drive, Suite 203, Lakewood Ranch, FL 34202 941 365 4617 461 www.kbgrp.com ESSENTIAL INTERNAL

Kerkering, Barberio & Co. Certified Public Accountants 1990 Main Street, Suite 801, Sarasota, FL 34236 6320 Venture Drive, Suite 203, Lakewood Ranch, FL 34202 941 365 4617 461 www.kbgrp.com ESSENTIAL INTERNAL

Ten Payment Fraud Protections

Ten Payment Fraud Protections 1. Payee Positive Pay a. Provided by banks b. Banks match check serial numbers and dollar amounts against a company provided list of checks issued and only pays those checks

Ten Payment Fraud Protections 1. Payee Positive Pay a. Provided by banks b. Banks match check serial numbers and dollar amounts against a company provided list of checks issued and only pays those checks

SAMPLE BEC SuperfastCPA Review Notes

BEC 2018 SuperfastCPA Review Notes Table of Contents Corporate Governance 1 Internal Control Frameworks 1 Enterprise Risk Management Frameworks 6 Other Regulatory Frameworks and Provisions 10 Economic

BEC 2018 SuperfastCPA Review Notes Table of Contents Corporate Governance 1 Internal Control Frameworks 1 Enterprise Risk Management Frameworks 6 Other Regulatory Frameworks and Provisions 10 Economic

716 West Ave Austin, TX USA

Fundamentals of Computer and Internet Fraud GLOBAL Headquarters the gregor building 716 West Ave Austin, TX 78701-2727 USA II. THE USE OF COMPUTERS IN OCCUPATIONAL FRAUD Occupational fraud refers to the

Fundamentals of Computer and Internet Fraud GLOBAL Headquarters the gregor building 716 West Ave Austin, TX 78701-2727 USA II. THE USE OF COMPUTERS IN OCCUPATIONAL FRAUD Occupational fraud refers to the

OVERVIEW 4/19/10. Internal Controls and the Audit Process May 4, 2010 OVERVIEW. Definition and historical perspective of internal auditing

and the Audit Process May 4, 2010 Presented by: Deborah A. Stevens CPA Wichita County Auditor 1 OVERVIEW Definition and historical perspective of internal auditing Role and responsibilities of the internal

and the Audit Process May 4, 2010 Presented by: Deborah A. Stevens CPA Wichita County Auditor 1 OVERVIEW Definition and historical perspective of internal auditing Role and responsibilities of the internal

Internal Control: It s More Than A Locked Safe

Internal Control: It s More Than A Locked Safe 1 P R E S E N T A T I O N F O R T H E N A D O R I E N T A T I O N F O R N E W T R E A S U R E R S M A R C H 3 0, 2 0 1 6 Ann Gibson, PhD, CPA Andrews University

Internal Control: It s More Than A Locked Safe 1 P R E S E N T A T I O N F O R T H E N A D O R I E N T A T I O N F O R N E W T R E A S U R E R S M A R C H 3 0, 2 0 1 6 Ann Gibson, PhD, CPA Andrews University

Keep Procure-to-Pay (P2P) Fraud at Bay with Fraud Detection Tools & Techniques

Fraud at Bay with Fraud Detection Tools & Techniques") Keep Procure-to-Pay (P2P) Fraud at Bay with Fraud Detection Tools & Techniques Chris Doxey, CAPP, CCSA, CICA, CPC President, Doxey, Inc. chris@chrisdoxey.com 571-267-9107 2 May 7-9, 2017 Chris Doxey, CAPP,

Keep Procure-to-Pay (P2P) Fraud at Bay with Fraud Detection Tools & Techniques Chris Doxey, CAPP, CCSA, CICA, CPC President, Doxey, Inc. chris@chrisdoxey.com 571-267-9107 2 May 7-9, 2017 Chris Doxey, CAPP,

Company LOGO C B T. An Educational Computer Based Training Program

C B T An Educational Computer Based Training Program The University of Texas at Dallas Compliance Training Effectively Controlling Risks Company Effectively Controlling Risks What is the purpose of this

C B T An Educational Computer Based Training Program The University of Texas at Dallas Compliance Training Effectively Controlling Risks Company Effectively Controlling Risks What is the purpose of this

Fraud Seminar. Fraud Seminar: Fraud Basics and Red Flags. Agenda 10/01/ McHard Accounting Consulting LLC

Fraud Seminar Beth A. Mohr, CFE, CAMS, PI, MPA NM-PI #2503; AZ-PI #1639940 Janet M. McHard, CPA, CFE, MAFF, CFF McHard Accounting Consulting LLC IIA El Paso Chapter October 1, 2013 Agenda Fraud Basics

Fraud Seminar Beth A. Mohr, CFE, CAMS, PI, MPA NM-PI #2503; AZ-PI #1639940 Janet M. McHard, CPA, CFE, MAFF, CFF McHard Accounting Consulting LLC IIA El Paso Chapter October 1, 2013 Agenda Fraud Basics

Cash and Internal Controls For SDA Organizations

Cash and Internal Controls For SDA Organizations 1 P R E S E N T A T I O N F O R T R E A S U R E R S E U R O - A S I A D I V I S I O N J U L Y 1 7, 2 0 1 3 Ann Gibson, PhD, CPA Andrews University Purpose

Cash and Internal Controls For SDA Organizations 1 P R E S E N T A T I O N F O R T R E A S U R E R S E U R O - A S I A D I V I S I O N J U L Y 1 7, 2 0 1 3 Ann Gibson, PhD, CPA Andrews University Purpose

INTERNAL CONTROLS AUDITOR JOHN BYRD, SENIOR AUDITOR TONYA CARRIGAN, SENIOR AUDITOR

1 INTERNAL CONTROLS FOR THE BEGINNING AUDITOR JOHN BYRD, SENIOR AUDITOR TONYA CARRIGAN, SENIOR AUDITOR UF HEALTH SHANDS HOSPITAL AHIA 32 nd Annual Conference August 25-28, 2013 Chicago, Illinois www.ahia.org

1 INTERNAL CONTROLS FOR THE BEGINNING AUDITOR JOHN BYRD, SENIOR AUDITOR TONYA CARRIGAN, SENIOR AUDITOR UF HEALTH SHANDS HOSPITAL AHIA 32 nd Annual Conference August 25-28, 2013 Chicago, Illinois www.ahia.org

Going on the Offensive: Blocking and Tackling to Minimize Fraud

Going on the Offensive: Blocking and Tackling to Minimize Fraud Welcome and Introductions Linda Goldstein Director, Compliance & Privacy Associate General Counsel MARY SMITH CEO Jonathan Marks CPA, CFE

Going on the Offensive: Blocking and Tackling to Minimize Fraud Welcome and Introductions Linda Goldstein Director, Compliance & Privacy Associate General Counsel MARY SMITH CEO Jonathan Marks CPA, CFE

Marine Bureau Cash Handling Operations Audit

Office of the City Auditor Marine Bureau Cash Handling Operations Audit October 2014 Audit Staff City Auditor: Laura L. Doud Assistant City Auditor: Deborah K. Ellis Deputy City Auditor: Joanna Munar Senior

Office of the City Auditor Marine Bureau Cash Handling Operations Audit October 2014 Audit Staff City Auditor: Laura L. Doud Assistant City Auditor: Deborah K. Ellis Deputy City Auditor: Joanna Munar Senior

EMPLOYEE FRAUD OPPORTUNITIES CHECKLIST

Page 128 of 174 EMPLOYEE FRAUD OPPORTUNITIES CHECKLIST Recognizing Warning Signs and Preventing Problem Situations Why are consistent internal controls important? Management decisions, financial reports,

Page 128 of 174 EMPLOYEE FRAUD OPPORTUNITIES CHECKLIST Recognizing Warning Signs and Preventing Problem Situations Why are consistent internal controls important? Management decisions, financial reports,

Internal Control Checklist

Instructions: The may be used to document a review of the existing procedures and activities that make up your internal control system, or serve as a guide in developing additional controls. The provides

Instructions: The may be used to document a review of the existing procedures and activities that make up your internal control system, or serve as a guide in developing additional controls. The provides

SELF ASSESSMENT OF BUSINESS OBJECTIVES. Kelly Dorin CPA, CA, CIA, CFE, CCSA, CRMA

SELF ASSESSMENT OF BUSINESS OBJECTIVES Kelly Dorin CPA, CA, CIA, CFE, CCSA, CRMA Overview What is Control Self-Assessment (CSA) Benefits obtained from using CSA How would you use CSA Enterprise-wide CSA

SELF ASSESSMENT OF BUSINESS OBJECTIVES Kelly Dorin CPA, CA, CIA, CFE, CCSA, CRMA Overview What is Control Self-Assessment (CSA) Benefits obtained from using CSA How would you use CSA Enterprise-wide CSA

Embezzlement & Fraud How You Can Protect Yourself. Pam Newman, CMA,CFM, MBA

Embezzlement & Fraud How You Can Protect Yourself Pam Newman, CMA,CFM, MBA Pam Newman BS and MBA from University of Nebraska CMA Certified Management Accountant CFM Certified Financial Manager President

Embezzlement & Fraud How You Can Protect Yourself Pam Newman, CMA,CFM, MBA Pam Newman BS and MBA from University of Nebraska CMA Certified Management Accountant CFM Certified Financial Manager President

Standards for Internal Control in New York State Government 2016 Update

Standards for Internal Control in New York State Government 2016 Update Presented to the New York State Internal Control Association John F. Buyce Audit Director April 28, 2016 1 Last Revised in 2007 A

Standards for Internal Control in New York State Government 2016 Update Presented to the New York State Internal Control Association John F. Buyce Audit Director April 28, 2016 1 Last Revised in 2007 A

Internal Controls Integrating COSO

Community Action Partnership 2016 Annual Convention August 30 September 2, 2016 Austin, TX J.W. Marriott Austin Internal Controls Integrating COSO Thursday, September 1, 2016 9:15 am 10:45 am Presented

Community Action Partnership 2016 Annual Convention August 30 September 2, 2016 Austin, TX J.W. Marriott Austin Internal Controls Integrating COSO Thursday, September 1, 2016 9:15 am 10:45 am Presented

Agenda 11/26/13. Updated COSO Framework

Updated COSO Framework Danny M. Goldberg, Founder Agenda COSO Update Overview History/Background Changes Overview Five Control Objectives 17 Control Principles Case Study: Developing a Checklist for Your

Updated COSO Framework Danny M. Goldberg, Founder Agenda COSO Update Overview History/Background Changes Overview Five Control Objectives 17 Control Principles Case Study: Developing a Checklist for Your

Segregation of Duties

Segregation of Duties The Basics of Accounting Controls Segregation of Duties The Basics of Accounting Controls 2014 SP Plus Corporation. All rights reserved. No part of this publication may be reproduced,

Segregation of Duties The Basics of Accounting Controls Segregation of Duties The Basics of Accounting Controls 2014 SP Plus Corporation. All rights reserved. No part of this publication may be reproduced,

INTERNAL CONTROLS 101

INTERNAL CONTROLS 101 Presented by: Christopher White, CPA Kristina Hoyng, CPA Northwest Region Overview of Topic Internal Controls - The Basics Components of Internal Controls Benefits of Internal Controls

INTERNAL CONTROLS 101 Presented by: Christopher White, CPA Kristina Hoyng, CPA Northwest Region Overview of Topic Internal Controls - The Basics Components of Internal Controls Benefits of Internal Controls