FRAUD DETERRENCE AND DETECTION

|

|

|

- Joan Bridges

- 5 years ago

- Views:

Transcription

1 FRAUD DETERRENCE AND DETECTION

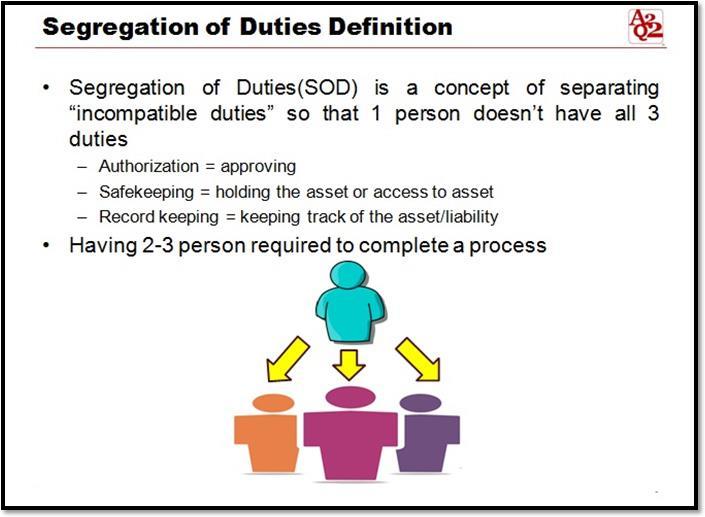

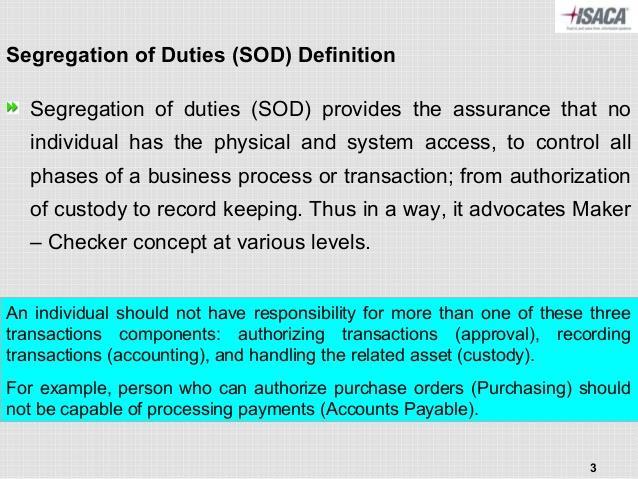

2 Segregation of Duties

3 Corruption Scheme Red Flags Unchecked authority to approve No formal documented procedures Circumventing normal policies and procedures Employees receiving gifts or things of value from customers Falsified or altered documents Customers only asking for certain employees

4 Skimming Scheme Red Flags Inadequate separation of duties Employees who do not take vacations, work a lot of overtime, don t like for others to perform their duties or have access to their desk Missing register tapes or other records Consistent differences in register receipts to cash on hand (i.e. longs and shorts)

5 The case of the Examples of Internal Controls to prevent Skimming Schemes: Separate duties over cash handling functions $100,000 Surprise cash counts Motivate customers to ask for receipts Use pre-numbered receipts and account for all receipts Brownies daily Account for the numerical sequence of cash register transactions Reconcile cash drawers to cash register receipts Use surveillance equipment and periodically review the tapes Enforce mandatory vacations for all employees who handle cash Deposit cash receipts daily

6 Increase in services performed Falsified or altered documents Vendors with PO box addresses Billing Scheme Red Flags Delivery address other than departmental or company address Payments to unapproved vendors Excessive returns to vendors

7 Examples of Internal Controls to prevent Billing Schemes: Separate duties over purchasing, receipt, and vendor The payments Case Require appropriate documentation on all transactions Compare information on the purchase orders, receiving of the reports, and vendor invoices before making payments Shopaholic Verify the legitimacy of vendors Review cancelled checks, purchase orders, requisitions, receiving reports, etc. for alterations Mark invoices and supporting documentation paid so they cannot be used again Reconcile accounts payable ledger to recorded liabilities

8 Lack of separation of duties Missing employee information No voluntary deductions No evidence of work performed Payroll Scheme Red Flags No physical address or phone number for the employee Bypassing normal hiring procedures

9 Examples of Internal Controls over Payroll: Separate the duties of hiring, timekeeping functions, processing, authorizing, and distributing payroll, and reconciling payroll bank accounts Stringent access controls over the payroll database should be in place to restrict unauthorized changes Analyze employee deductions and withholdings Review payroll records (i.e. timesheets or timecards) for hours worked, management authorizations, overtime, etc. Compare the number of paychecks to the number of authorized workers

10 Non-Cash Scheme Red Flags Shrinkage in inventory Employees who frequently visit the office after normal business hours Missing tools, equipment, office supplies, etc. Missing, altered, or unmatched supporting documents to inventory records Employees borrowing office supplies, tools or equipment

11 Examples of Internal Controls over Non-Cash Items: Restrict physical access to inventory Monitor employees who have access to non-cash items Use surveillance devices, such as video cameras Separate the duties over the inventory process Take frequent inventory counts and hold employees responsible for any shortages Require proper documentation to support inventory items (i.e. requisitions, receiving documents, inventory records, etc.) Implement and strictly follow a policy which prohibits the borrowing of non-cash assets

12 Check Tampering Scheme Red Flags One employee performs reconciliations without any independent checks Altered bank statements Voided checks do not match physical copies of the checks Altered check register, check disbursement journal, or cancelled checks Checks endorsed by an employee or dual endorsements

13 Examples of Internal Controls over Check Tampering: Separation of duties over disbursement process Bank reconciliations should be performed timely and reviewed by someone other than the preparer Supporting documentation required for all check disbursements Blank checks or check stock should be kept in a secure location where physical access is limited Checks should be mailed or delivered as soon as possible after being prepared Access to and changes made to the accounts payable database should be restricted

14 Behavioral Red Flags Living Beyond Means Financial difficulties Unusually close association w/ vendor Wheeler-dealer attitude Control issues, unwilling to share duties Divorce / family problems Irritability, suspiciousness, or defensiveness Addiction problems Complaining about inadequate pay No Behavioral Red Flags Refusal to take vacations Excessive pressure from within organization Past employment-related problems Past legal problems Excessive family / peer pressure for success Complaining about lack of authority Instability in life circumstances 2016 ACFE Report to the Nations on Occupational Fraud and Abuse

SMALL BUSINESS FRAUD ASSESSMENT INTERNAL CONTROL QUESTIONNAIRE Download your risk assessment form at

SMALL BUSINESS FRAUD ASSESSMENT INTERNAL CONTROL QUESTIONNAIRE Download your risk assessment form at www.businessfraudprevention.org/forms.html Owner: Date: Discussed with: Question Yes No N/A Comments

SMALL BUSINESS FRAUD ASSESSMENT INTERNAL CONTROL QUESTIONNAIRE Download your risk assessment form at www.businessfraudprevention.org/forms.html Owner: Date: Discussed with: Question Yes No N/A Comments

Review and Implementation. Of Practice Internal Controls

Review and Implementation Of Practice Internal Controls Is there a fraudster in your practice? An embezzler or other workplace fraud perpetrator will often display certain telltale red flags. One of the

Review and Implementation Of Practice Internal Controls Is there a fraudster in your practice? An embezzler or other workplace fraud perpetrator will often display certain telltale red flags. One of the

Laurie Beets. PDG 27 th National College & University Bursars & SFS Conference

Foiling Fraudsters Laurie Beets Oklahoma State University Acknowledgements 2006 Fraud Examiners Manual, Association of Certified Fraud Examiners (ACFE) 2012 Report to the Nation on Occupational Fraud &

Foiling Fraudsters Laurie Beets Oklahoma State University Acknowledgements 2006 Fraud Examiners Manual, Association of Certified Fraud Examiners (ACFE) 2012 Report to the Nation on Occupational Fraud &

Fraud Risk Management

Fraud Risk Management Specific Anti-Fraud Controls (Process or Transaction Level) 2017 Association of Certified Fraud Examiners, Inc. Discussion Questions 1. Does your organization have adequate staffing

Fraud Risk Management Specific Anti-Fraud Controls (Process or Transaction Level) 2017 Association of Certified Fraud Examiners, Inc. Discussion Questions 1. Does your organization have adequate staffing

Fraud Prevention, Detection, and Internal Controls

Fraud Prevention, Detection, and Internal Controls Budget, Accounting and Reporting Council May 28, 2015 Sherrie Ard, CPA, CFE Financial Management Specialist Local Government Performance Center Local

Fraud Prevention, Detection, and Internal Controls Budget, Accounting and Reporting Council May 28, 2015 Sherrie Ard, CPA, CFE Financial Management Specialist Local Government Performance Center Local

Can You Spot Fraudsters?

Can You Spot Fraudsters? CACUBO Workshop March 22, 2018 Eric Conforti, CPA, CFE 1 Who Are We? A One-Firm Firm: Over 2,200 industry experts to partner with when specific industry knowledge is needed during

Can You Spot Fraudsters? CACUBO Workshop March 22, 2018 Eric Conforti, CPA, CFE 1 Who Are We? A One-Firm Firm: Over 2,200 industry experts to partner with when specific industry knowledge is needed during

Petty Cash and Change Funds. Inventories (Equipment and Supplies)

") UCLA Policy 360 Page 1 of 8 ATTACHMENT A Guidelines for Application of Internal Control Principles The following are control activities, as described in section III.B.3. of Policy 360, for applying the

UCLA Policy 360 Page 1 of 8 ATTACHMENT A Guidelines for Application of Internal Control Principles The following are control activities, as described in section III.B.3. of Policy 360, for applying the

- Excessive gambling or investment habits - Strong challenge to beat the system - Undue family pressure such as divorce - Overwhelming desire for pers

RED FLAGS OF INTERNAL FRAUD PROFILE OF THE PERPETRATOR: - Most frequently it is the person you trust the most - Has the technical skills to pull off the theft secretly - The activity is clandestine - The

RED FLAGS OF INTERNAL FRAUD PROFILE OF THE PERPETRATOR: - Most frequently it is the person you trust the most - Has the technical skills to pull off the theft secretly - The activity is clandestine - The

Ten Payment Fraud Protections

Ten Payment Fraud Protections 1. Payee Positive Pay a. Provided by banks b. Banks match check serial numbers and dollar amounts against a company provided list of checks issued and only pays those checks

Ten Payment Fraud Protections 1. Payee Positive Pay a. Provided by banks b. Banks match check serial numbers and dollar amounts against a company provided list of checks issued and only pays those checks

APPENDIX 2 COMMUNITY DEVELOPMENT COMMISSION FINANCIAL CHECKLIST REQUIRED FOR ALL APPLICANTS (A SITE VISIT MAY BE CONDUCTED LATER)

") REQUIRED FOR ALL APPLICANTS (A SITE VISIT MAY BE CONDUCTED LATER) AGENCY NAME: AGENCY ADDRESS AGENCY PHONE: DATE PREPARED: PREPARED BY: TITLE: EMAIL: AGENCY GENERAL INFORMATION EXECUTIVE DIRECTOR /CITY

REQUIRED FOR ALL APPLICANTS (A SITE VISIT MAY BE CONDUCTED LATER) AGENCY NAME: AGENCY ADDRESS AGENCY PHONE: DATE PREPARED: PREPARED BY: TITLE: EMAIL: AGENCY GENERAL INFORMATION EXECUTIVE DIRECTOR /CITY

EGYPTIAN AREA AGENCY ON AGING Fiscal Monitoring Program

EGYPTIAN AREA AGENCY ON AGING Fiscal Monitoring Program Fiscal Year: Name of Project/Site: (TIN #) Address: (city) (state) (zip code) Project Director/Site Manager: Geographic Area Served: (county) Project/Site

EGYPTIAN AREA AGENCY ON AGING Fiscal Monitoring Program Fiscal Year: Name of Project/Site: (TIN #) Address: (city) (state) (zip code) Project Director/Site Manager: Geographic Area Served: (county) Project/Site

Effective Internal Control Strategies

Effective Internal Control Strategies 1. The unique nonprofit environment A. Reliance on contributed services of volunteers B. Many volunteers have a limited nonprofit financial background C. Revenue often

Effective Internal Control Strategies 1. The unique nonprofit environment A. Reliance on contributed services of volunteers B. Many volunteers have a limited nonprofit financial background C. Revenue often

How to Prevent Financial Fraud at Your Church VONNA LAUE

How to Prevent Financial Fraud at Your Church VONNA LAUE Agenda Why churches fall victim to fraud Financial control best practices Recognize and respond to financial fraud Why Churches Fall Victim to Fraud

How to Prevent Financial Fraud at Your Church VONNA LAUE Agenda Why churches fall victim to fraud Financial control best practices Recognize and respond to financial fraud Why Churches Fall Victim to Fraud

Karen L. Mosteller, CPA, CHBC

Karen L. Mosteller, CPA, CHBC Recognize the Red Flags of Fraud and areas of vulnerability Examine checks and balances that should be implemented Establish processes and procedures needed for fraud protection

Karen L. Mosteller, CPA, CHBC Recognize the Red Flags of Fraud and areas of vulnerability Examine checks and balances that should be implemented Establish processes and procedures needed for fraud protection

EMPLOYEE FRAUD OPPORTUNITIES CHECKLIST

Page 128 of 174 EMPLOYEE FRAUD OPPORTUNITIES CHECKLIST Recognizing Warning Signs and Preventing Problem Situations Why are consistent internal controls important? Management decisions, financial reports,

Page 128 of 174 EMPLOYEE FRAUD OPPORTUNITIES CHECKLIST Recognizing Warning Signs and Preventing Problem Situations Why are consistent internal controls important? Management decisions, financial reports,

Financial Controls Checklist

Financial Controls Checklist Board of Health: Board of Health for the Leeds, Grenville & Lanark District Health Unit Period ended: Dec. 31/17 Objective: The objective of the Financial Controls Checklist

Financial Controls Checklist Board of Health: Board of Health for the Leeds, Grenville & Lanark District Health Unit Period ended: Dec. 31/17 Objective: The objective of the Financial Controls Checklist

This Questionnaire/Guide is intended to assist you in decision making, as well as in day-to-day operations. Best Regards,

In an effort to disseminate information and assure that we are in compliance with guidelines caused by the Sarbanes Oxley Act that proper internal controls are being adhered to, we have developed some

In an effort to disseminate information and assure that we are in compliance with guidelines caused by the Sarbanes Oxley Act that proper internal controls are being adhered to, we have developed some

The Episcopal Diocese of Kentucky

The Episcopal Diocese of Kentucky Internal Control Questionnaire Manual of Business Methods in Church Affairs (Spring 2012) Chapter II: Internal Controls, Section C The following Internal Control Questionnaire

The Episcopal Diocese of Kentucky Internal Control Questionnaire Manual of Business Methods in Church Affairs (Spring 2012) Chapter II: Internal Controls, Section C The following Internal Control Questionnaire

Eric Kinsherf, CPA MMAAA Conference June 12, 2018

Eric Kinsherf, CPA MMAAA Conference June 12, 2018 Agenda Overview What is Fraud? How does Fraud happen? How to Detect and Prevent Fraud Summarize Objectives Gain better Understanding of Fraud Risk Illustrate

Eric Kinsherf, CPA MMAAA Conference June 12, 2018 Agenda Overview What is Fraud? How does Fraud happen? How to Detect and Prevent Fraud Summarize Objectives Gain better Understanding of Fraud Risk Illustrate

Internal Controls Checklist

1. Are checks endorsed for deposit only immediately upon receipt? 2. Does someone prepare a daily list of all cash and checks immediately upon receipt? 3. Are duplicate deposit slips and copies of checks

1. Are checks endorsed for deposit only immediately upon receipt? 2. Does someone prepare a daily list of all cash and checks immediately upon receipt? 3. Are duplicate deposit slips and copies of checks

Information and and training provid v ed by Smith Elliott Elliott Kearns & Compan

Nuts and Bolts of Avoiding Fraud in Your Organization Information and training provided by Smith Elliott Kearns & Company, LLC as part of this Fraud Avoidance presentation is intended for reference only.

Nuts and Bolts of Avoiding Fraud in Your Organization Information and training provided by Smith Elliott Kearns & Company, LLC as part of this Fraud Avoidance presentation is intended for reference only.

FRAUD SCHEMES. South Carolina HFMA Finance & Reimbursement Forum. November 13, 2012 WITH RELATED INTERNAL CONTROLS

FRAUD SCHEMES WITH RELATED INTERNAL CONTROLS South Carolina HFMA Finance & Reimbursement Forum November 13, 2012 2 Fraud Facts: Estimated loss of 5% of annual revenues to occupational fraud Financial statement

FRAUD SCHEMES WITH RELATED INTERNAL CONTROLS South Carolina HFMA Finance & Reimbursement Forum November 13, 2012 2 Fraud Facts: Estimated loss of 5% of annual revenues to occupational fraud Financial statement

INTERNAL CONTROLS REVIEW PROGRESS REPORT Yellow highlighted items have been completed/validated since last report in August 2016

INTERNAL S REVIEW PROGRESS REPORT Yellow highlighted items have been completed/validated since last report in August 2016 RECOMMENDATIONS ADDRESSED THROUGH INTERNAL AUDIT WORK PLANS Monthly Reconciliation

INTERNAL S REVIEW PROGRESS REPORT Yellow highlighted items have been completed/validated since last report in August 2016 RECOMMENDATIONS ADDRESSED THROUGH INTERNAL AUDIT WORK PLANS Monthly Reconciliation

INTERNAL CONTROLS REVIEW PROGRESS REPORT Highlighted items have been completed since last report in January 2016

INTERNAL S REVIEW PROGRESS REPORT Highlighted items have been completed since last report in January 2016 RECOMMENDATIONS ADDRESSED THROUGH INTERNAL AUDIT WORK PLANS Internal Audit: prepare documentation

INTERNAL S REVIEW PROGRESS REPORT Highlighted items have been completed since last report in January 2016 RECOMMENDATIONS ADDRESSED THROUGH INTERNAL AUDIT WORK PLANS Internal Audit: prepare documentation

Diocese of Covington Policies & Procedures Manual Section: Compliance Accounting Policy: Internal Control & Segregation of Duties

Internal Control refers to the policies and procedures established to provide reasonable assurance that parish assets are safeguarded, that accountability is achieved, and that errors in financial records

Internal Control refers to the policies and procedures established to provide reasonable assurance that parish assets are safeguarded, that accountability is achieved, and that errors in financial records

INTERNAL CONTROLS REVIEW PROGRESS REPORT Yellow highlighted items have been updated since last report in October 2017

INTERNAL S REVIEW PROGRESS REPORT Yellow highlighted items have been updated since last report in October 2017 RECOMMENDATIONS ADDRESSED THROUGH INTERNAL AUDIT WORK PLANS Internal Audit: prepare documentation

INTERNAL S REVIEW PROGRESS REPORT Yellow highlighted items have been updated since last report in October 2017 RECOMMENDATIONS ADDRESSED THROUGH INTERNAL AUDIT WORK PLANS Internal Audit: prepare documentation

Internal Fraud Monitoring & Investigation Best Practices. By Tom Holland, CFE

Internal Fraud Monitoring & Investigation Best Practices By Tom Holland, CFE BSA Coalition Training BSA Event Coalition Anti-Money February Laundering 9, 2010 Conferencewww.bsacoalition.org The Threat

Internal Fraud Monitoring & Investigation Best Practices By Tom Holland, CFE BSA Coalition Training BSA Event Coalition Anti-Money February Laundering 9, 2010 Conferencewww.bsacoalition.org The Threat

Whether you take in a lot of money. or you collect pennies

Whether you take in a lot of money or you collect pennies ..it is important to maintain good cash handling procedures: Segregation of Duties Security Reconciliation Management Review Documentation It s

Whether you take in a lot of money or you collect pennies ..it is important to maintain good cash handling procedures: Segregation of Duties Security Reconciliation Management Review Documentation It s

Cash Reconciliations and Cash Handling

Cash Reconciliations and Cash Handling WASBO Accounting Conference March, 2016 Handling Cash Cash may be the most vulnerable asset in your LEA. How do you safeguard your cash? Timely reconciliation of

Cash Reconciliations and Cash Handling WASBO Accounting Conference March, 2016 Handling Cash Cash may be the most vulnerable asset in your LEA. How do you safeguard your cash? Timely reconciliation of

INTERNAL CONTROLS REVIEW PROGRESS REPORT Yellow highlighted items have been updated since last report in October 2016

INTERNAL S REVIEW PROGRESS REPORT Yellow highlighted items have been updated since last report in October 2016 RECOMMENDATIONS ADDRESSED THROUGH INTERNAL AUDIT WORK PLANS Internal Audit: prepare documentation

INTERNAL S REVIEW PROGRESS REPORT Yellow highlighted items have been updated since last report in October 2016 RECOMMENDATIONS ADDRESSED THROUGH INTERNAL AUDIT WORK PLANS Internal Audit: prepare documentation

SEGREGATION OF DUTIES for SAP

SEGREGATION OF DUTIES for SAP SEGREGATION-OF-DUTIES In todays modern, technology driven world, segregation-of-duties (SoD) is enforced through business applications and ERP s, but highlighting breakdowns

SEGREGATION OF DUTIES for SAP SEGREGATION-OF-DUTIES In todays modern, technology driven world, segregation-of-duties (SoD) is enforced through business applications and ERP s, but highlighting breakdowns

Fraud Prevention Training

Fraud Prevention Training The Massachusetts Collectors and Treasurers Association Sixty-Sixth Annual Education Conference June 15, 2015 Presented By: Eric Demas, CFE Melanson Heath edemas@melansonheath.com

Fraud Prevention Training The Massachusetts Collectors and Treasurers Association Sixty-Sixth Annual Education Conference June 15, 2015 Presented By: Eric Demas, CFE Melanson Heath edemas@melansonheath.com

Fraud Awareness February 27, 2015

Fraud Awareness February 27, 2015 Clara Ewing Megan Dix Fraud Defined The term fraud is defined in Black's Law Dictionary (Sixth Edition, 1990) as: An intentional perversion of truth for the purpose of

Fraud Awareness February 27, 2015 Clara Ewing Megan Dix Fraud Defined The term fraud is defined in Black's Law Dictionary (Sixth Edition, 1990) as: An intentional perversion of truth for the purpose of

Internal Control Evaluation

INTERNAL CONTROL EVALUATION Adapted from a checklist created by Jackie F. Breland, CPA (www.jackiebreland.com) Organization: Date Prepared or Updated: Prepared by: Introduction The purpose of this checklist

INTERNAL CONTROL EVALUATION Adapted from a checklist created by Jackie F. Breland, CPA (www.jackiebreland.com) Organization: Date Prepared or Updated: Prepared by: Introduction The purpose of this checklist

Chapter 7 Internal Controls

Chapter 7 Internal Controls Establishment of and adherence to internal controls is a major part of managing an organization. Internal controls serve as the first line of defense in safeguarding assets

Chapter 7 Internal Controls Establishment of and adherence to internal controls is a major part of managing an organization. Internal controls serve as the first line of defense in safeguarding assets

Internal Control Checklist

Instructions: The may be used to document a review of the existing procedures and activities that make up your internal control system, or serve as a guide in developing additional controls. The provides

Instructions: The may be used to document a review of the existing procedures and activities that make up your internal control system, or serve as a guide in developing additional controls. The provides

Fraud Awareness and Prevention

Awareness and Prevention Craig Bodette Awareness and Prevention Craig Bodette Senior Accountant & Member of Construction Team Weber O Brien This session is eligible for 1.5 Continuing Education Hours.

Awareness and Prevention Craig Bodette Awareness and Prevention Craig Bodette Senior Accountant & Member of Construction Team Weber O Brien This session is eligible for 1.5 Continuing Education Hours.

AICC 2017 ANNUALMEETING PRESENTED BY MITCHELL E. KLINGHER CPA PROTECTING YOUR COMPANY FROM EMPLOYEE THEFT

AICC 2017 ANNUALMEETING PRESENTED BY MITCHELL E. KLINGHER CPA PROTECTING YOUR COMPANY FROM EMPLOYEE THEFT WHY DO THEY DO IT?????? THE PSYCHOLOGY OF THEFT Vicarious thrill It doesn t matter Everyone does

AICC 2017 ANNUALMEETING PRESENTED BY MITCHELL E. KLINGHER CPA PROTECTING YOUR COMPANY FROM EMPLOYEE THEFT WHY DO THEY DO IT?????? THE PSYCHOLOGY OF THEFT Vicarious thrill It doesn t matter Everyone does

Contract and Procurement Fraud

Contract and Procurement Fraud Fraud in Procurement Without Competition 2018 Association of Certified Fraud Examiners, Inc. Sole-Source Awards The procurement process is noncompetitive through the solicitation

Contract and Procurement Fraud Fraud in Procurement Without Competition 2018 Association of Certified Fraud Examiners, Inc. Sole-Source Awards The procurement process is noncompetitive through the solicitation

STATE OF MINNESOTA OFFICE OF THE STATE AUDITOR

REBECCA OTTO STATE AUDITOR STATE OF MINNESOTA OFFICE OF THE STATE AUDITOR SUITE 500 525 PARK STREET SAINT PAUL, MN 55103-2139 (651) 296-2551 (Voice) (651) 296-4755 (Fax) state.auditor@osa.state.mn.us (E-mail)

REBECCA OTTO STATE AUDITOR STATE OF MINNESOTA OFFICE OF THE STATE AUDITOR SUITE 500 525 PARK STREET SAINT PAUL, MN 55103-2139 (651) 296-2551 (Voice) (651) 296-4755 (Fax) state.auditor@osa.state.mn.us (E-mail)

OVERVIEW 4/19/10. Internal Controls and the Audit Process May 4, 2010 OVERVIEW. Definition and historical perspective of internal auditing

and the Audit Process May 4, 2010 Presented by: Deborah A. Stevens CPA Wichita County Auditor 1 OVERVIEW Definition and historical perspective of internal auditing Role and responsibilities of the internal

and the Audit Process May 4, 2010 Presented by: Deborah A. Stevens CPA Wichita County Auditor 1 OVERVIEW Definition and historical perspective of internal auditing Role and responsibilities of the internal

Internal Control Questionnaire

Internal Control Questionnaire CASH RECEIPTS/SALE QUESTIONS: 1. Is there a designated cash receipt custodian? 2. Are all receipts recorded on pre-numbered cash receipts tickets, including those received

Internal Control Questionnaire CASH RECEIPTS/SALE QUESTIONS: 1. Is there a designated cash receipt custodian? 2. Are all receipts recorded on pre-numbered cash receipts tickets, including those received

INTERNAL CONTROL HANDBOOK

INTERNAL CONTROL HANDBOOK INTERNAL CONTROL HANDBOOK ILLINOIS STATE BOARD OF EDUCATION SCHOOL BUSINESS SERVICES DIVISION Revised July, 2017 Most Content remains the same as published in 1993 Prepared by

INTERNAL CONTROL HANDBOOK INTERNAL CONTROL HANDBOOK ILLINOIS STATE BOARD OF EDUCATION SCHOOL BUSINESS SERVICES DIVISION Revised July, 2017 Most Content remains the same as published in 1993 Prepared by

INTERNAL CONTROLS. Revision A

INTERNAL CONTROLS Internal Controls Approved. CHANGE HISTORY Sections Affected/Description of Change Section All: Consolidate original document and all changes approved Through ; standardize formatting

INTERNAL CONTROLS Internal Controls Approved. CHANGE HISTORY Sections Affected/Description of Change Section All: Consolidate original document and all changes approved Through ; standardize formatting

2/27/2017. Segregation of Duties/ Internal Controls. Objectives. Agenda

Segregation of Duties/ Internal Controls 2017 WASBO Accounting Conference David Maccoux, Shareholder Objectives Discuss failures of internal controls to detect or prevent fraud and learn how to implement

Segregation of Duties/ Internal Controls 2017 WASBO Accounting Conference David Maccoux, Shareholder Objectives Discuss failures of internal controls to detect or prevent fraud and learn how to implement

Central Florida Chapter Florida Government Finance Officers Association INTERNAL CONTROLS

Central Florida Chapter Florida Government Finance Officers Association INTERNAL CONTROLS 1 FRAUD Any intentional act or omission designed to deceive or mislead others and resulting in the victim suffering

Central Florida Chapter Florida Government Finance Officers Association INTERNAL CONTROLS 1 FRAUD Any intentional act or omission designed to deceive or mislead others and resulting in the victim suffering

9/13/2017 CHA-CHING! PAYROLL CONTROLS THAT PAY OFF PERSONAL INTRODUCTION. Personal Introduction. Melinda Stinnett, CPA, CIA Managing Director

CHA-CHING! PAYROLL CONTROLS THAT PAY OFF Melinda Stinnett, CPA, CIA Managing Director September 15, 2017 1 PERSONAL INTRODUCTION Professional Bachelor s Degree (Accounting) Oklahoma State University Public

CHA-CHING! PAYROLL CONTROLS THAT PAY OFF Melinda Stinnett, CPA, CIA Managing Director September 15, 2017 1 PERSONAL INTRODUCTION Professional Bachelor s Degree (Accounting) Oklahoma State University Public

Internal Controls Integrating COSO

Community Action Partnership 2016 Annual Convention August 30 September 2, 2016 Austin, TX J.W. Marriott Austin Internal Controls Integrating COSO Thursday, September 1, 2016 9:15 am 10:45 am Presented

Community Action Partnership 2016 Annual Convention August 30 September 2, 2016 Austin, TX J.W. Marriott Austin Internal Controls Integrating COSO Thursday, September 1, 2016 9:15 am 10:45 am Presented

CORP Appendix A CORPORATE POLICY. Attachments: Related Documents/Legislation: Revenue Administrative Policy

CORP2014-085 Appendix A CORPORATE POLICY Policy Title: Cash Handling Policy Policy Category: Financial Control Policy Policy No.: FC-016 Department: Corporate Services Approval Date: Revision Date: Author:

CORP2014-085 Appendix A CORPORATE POLICY Policy Title: Cash Handling Policy Policy Category: Financial Control Policy Policy No.: FC-016 Department: Corporate Services Approval Date: Revision Date: Author:

Finance Committee, Board of Health Elizabeth Bowden, Interim Director of Administrative Services FINANCIAL CONTROLS CHECKLIST

March 20, 2016 Report To: Submitted by: Subject: Finance Committee, Board of Health Elizabeth Bowden, Interim Director of Administrative Services FINANCIAL CONTROLS CHECKLIST RECOMMENDATION(S): (a) That

March 20, 2016 Report To: Submitted by: Subject: Finance Committee, Board of Health Elizabeth Bowden, Interim Director of Administrative Services FINANCIAL CONTROLS CHECKLIST RECOMMENDATION(S): (a) That

Division of Student Affairs Internal Control Questionnaire FY 2011

Control Environment Yes No N/A Notations Are the roles and responsibilities of financial and administrative staff (including the establishment of the unit Director as the appropriate signature authority)

Control Environment Yes No N/A Notations Are the roles and responsibilities of financial and administrative staff (including the establishment of the unit Director as the appropriate signature authority)

Contract and Procurement Fraud. Fraud in Procurement without Competition

Contract and Procurement Fraud Fraud in Procurement without Competition Sole-Source Awards Noncompetitive procurement process through the solicitation of only one source Procurement through sole-source

Contract and Procurement Fraud Fraud in Procurement without Competition Sole-Source Awards Noncompetitive procurement process through the solicitation of only one source Procurement through sole-source

Accounting Procedures

Accounting Procedures Steven M. Bragg Chapter 1 Overview of Accounting Procedures... 1 Learning Objectives... 1 Introduction... 1 The Nature of a Procedure... 1 The Need for Procedures... 1 The Number

Accounting Procedures Steven M. Bragg Chapter 1 Overview of Accounting Procedures... 1 Learning Objectives... 1 Introduction... 1 The Nature of a Procedure... 1 The Need for Procedures... 1 The Number

With Jodi Kippe, CPA & Partner Retail Dealer Practice at Crowe Horwath LLP. Moderated by Mike Bowers, Executive Editor at DealersEdge

How to Identify and Stop Internal Theft in the Dealership! Failing to be alert for employee schemes to embezzle or otherwise steal from the dealership can be not only costly - It's embarrassing! With Jodi

How to Identify and Stop Internal Theft in the Dealership! Failing to be alert for employee schemes to embezzle or otherwise steal from the dealership can be not only costly - It's embarrassing! With Jodi

INTERNAL CONTROLS REVIEW PROGRESS REPORT

INTERNAL S REVIEW PROGRESS REPORT RECOMMENDATIONS ADDRESSED THROUGH INTERNAL AUDIT WORK PLANS Monthly Reconciliation 1 High High Accounts Receivable Training 2, 8, 9 High Moderate 1 12, 13 High High 3

INTERNAL S REVIEW PROGRESS REPORT RECOMMENDATIONS ADDRESSED THROUGH INTERNAL AUDIT WORK PLANS Monthly Reconciliation 1 High High Accounts Receivable Training 2, 8, 9 High Moderate 1 12, 13 High High 3

SAN FRANCISCO COURT APPOINTED SPECIAL ADVOCATE PROGRAM

SAN FRANCISCO COURT APPOINTED SPECIAL ADVOCATE PROGRAM FINANCIAL PROCEDURES MANUAL Table of Contents GENERAL ACCOUNTING POLICY AND PROCEDURES... 3 OVERALL ACCOUNTING SYSTEM DESIGN... 3 CONTROL OBJECTIVE...

SAN FRANCISCO COURT APPOINTED SPECIAL ADVOCATE PROGRAM FINANCIAL PROCEDURES MANUAL Table of Contents GENERAL ACCOUNTING POLICY AND PROCEDURES... 3 OVERALL ACCOUNTING SYSTEM DESIGN... 3 CONTROL OBJECTIVE...

With Jodi Kippe, CPA & Partner Retail Dealer Practice at Crowe Horwath LLP. Moderated by Mike Bowers, Executive Editor at DealersEdge

How to Identify and Stop Internal Theft in the Dealership! Failing to be alert for employee schemes to embezzle or otherwise steal from the dealership can be not only costly - It's embarrassing! With Jodi

How to Identify and Stop Internal Theft in the Dealership! Failing to be alert for employee schemes to embezzle or otherwise steal from the dealership can be not only costly - It's embarrassing! With Jodi

Segregation of Duties Employee Compensation

Segregation of Duties Employee Compensation Internal Controls A process the provides reasonable assurance that the objectives of the institution will be achieved. Not one event, but a series of actions

Segregation of Duties Employee Compensation Internal Controls A process the provides reasonable assurance that the objectives of the institution will be achieved. Not one event, but a series of actions

OCCUPATIONAL FRAUD IN GOVERNMENT AND STEPS TO PREVENT AND DETECT IT

OCCUPATIONAL FRAUD IN GOVERNMENT AND STEPS TO PREVENT AND DETECT IT This session will explore government fraud risks as well as common areas of abuse and corresponding red flags. It will also provide ideas

OCCUPATIONAL FRAUD IN GOVERNMENT AND STEPS TO PREVENT AND DETECT IT This session will explore government fraud risks as well as common areas of abuse and corresponding red flags. It will also provide ideas

Accounting Procedures

Accounting Procedures 3 rd Edition Steven M. Bragg Chapter 1 Overview of Accounting Procedures... 1 Learning Objectives... 1 Introduction... 1 The Nature of a Procedure... 1 The Need for Procedures...

Accounting Procedures 3 rd Edition Steven M. Bragg Chapter 1 Overview of Accounting Procedures... 1 Learning Objectives... 1 Introduction... 1 The Nature of a Procedure... 1 The Need for Procedures...

Christopher Dawkins, CPA, CIA Director of County Audit Phil Diamond, CPA Orange County Comptroller s Office

Christopher Dawkins, CPA, CIA Director of County Audit Phil Diamond, CPA Orange County Comptroller s Office What Will I Talk About? Why we have auditors and the difference between external auditors and

Christopher Dawkins, CPA, CIA Director of County Audit Phil Diamond, CPA Orange County Comptroller s Office What Will I Talk About? Why we have auditors and the difference between external auditors and

INTERNAL CONTROLS MANUAL DICKSON COUNTY SCHOOLS DANNY L. WEEKS, ED.D. DIRECTOR OF SCHOOLS LINDA FRAZIER BUSINESS MANAGER JUNE 2016

1 INTERNAL CONTROLS MANUAL DICKSON COUNTY SCHOOLS DANNY L. WEEKS, ED.D. DIRECTOR OF SCHOOLS LINDA FRAZIER BUSINESS MANAGER JUNE 2016 2 Table of Contents Introduction...3 Internal Controls Questionnaire...4

1 INTERNAL CONTROLS MANUAL DICKSON COUNTY SCHOOLS DANNY L. WEEKS, ED.D. DIRECTOR OF SCHOOLS LINDA FRAZIER BUSINESS MANAGER JUNE 2016 2 Table of Contents Introduction...3 Internal Controls Questionnaire...4

Control Self Assessment Questionnaire

Control Self Assessment Questionnaire (31 Questions) 1. The department documents the monthly reconciliation of its Lynx finance accounts and reports. A yes answer indicates that the department has written

Control Self Assessment Questionnaire (31 Questions) 1. The department documents the monthly reconciliation of its Lynx finance accounts and reports. A yes answer indicates that the department has written

OVERVIEW. Common Personality Traits of Fraudsters. Common Sources of Pressure. Changes in Behavior

Red Flags of Fraud OVERVIEW Red Flags of Fraud are warning signs that may indicate a higher fraud risk. They are NOT evidence that fraud is actually occurring. Many employees demonstrate one or more of

Red Flags of Fraud OVERVIEW Red Flags of Fraud are warning signs that may indicate a higher fraud risk. They are NOT evidence that fraud is actually occurring. Many employees demonstrate one or more of

Sage MyAssistant - Construction Tasks

Sage MyAssistant - Construction Tasks Accounts Payable Invoice Management Banks with insufficient cash Commitments with unsigned change orders and are selected to be paid Invoices from the same vendor,

Sage MyAssistant - Construction Tasks Accounts Payable Invoice Management Banks with insufficient cash Commitments with unsigned change orders and are selected to be paid Invoices from the same vendor,

How to Keep Your Bookkeeper from Robbing Your Business Blind. Jen Deal CPA (252)

") How to Keep Your Bookkeeper from Robbing Your Business Blind Jen Deal CPA (252) 292-9138 Bio: Jen Deal, CPA (FL) (NC) Born & raised in Florida Empty-nester, moved to NC Jan. 2015 to be near family CPA

How to Keep Your Bookkeeper from Robbing Your Business Blind Jen Deal CPA (252) 292-9138 Bio: Jen Deal, CPA (FL) (NC) Born & raised in Florida Empty-nester, moved to NC Jan. 2015 to be near family CPA

ACCTG 533: Module 14: Asset Misappropriation Fraud. [Slide Content]: Asset Misappropriation Fraud. [Jeanne H. Yamamura]: Asset Misappropriation Fraud

![ACCTG 533: Module 14: Asset Misappropriation Fraud. [Slide Content]: Asset Misappropriation Fraud. [Jeanne H. Yamamura]: Asset Misappropriation Fraud](/thumbs/81/83190759.jpg "ACCTG 533: Module 14: Asset Misappropriation Fraud. [Slide Content]: Asset Misappropriation Fraud. [Jeanne H. Yamamura]: Asset Misappropriation Fraud") ACCTG 533: Module 14: Asset Misappropriation Fraud Asset Misappropriation Fraud Asset Misappropriation Fraud Asset Misappropriation Fraud Theft or misuse of company assets Most common type of fraud Every

ACCTG 533: Module 14: Asset Misappropriation Fraud Asset Misappropriation Fraud Asset Misappropriation Fraud Asset Misappropriation Fraud Theft or misuse of company assets Most common type of fraud Every

Safety In Numbers. Presented by Terry Shoebotham May 10 th and 18 th, 2010

Safety In Numbers Presented by Terry Shoebotham May 10 th and 18 th, 2010 Overview Financial Information: Secure and Accurate Prevent Unauthorized access Detect and Correct Processes that help And Avoid

Safety In Numbers Presented by Terry Shoebotham May 10 th and 18 th, 2010 Overview Financial Information: Secure and Accurate Prevent Unauthorized access Detect and Correct Processes that help And Avoid

FRAUD DETECTION. Early Detection = $ Saved. Red Flag = Danger. But a symptom = FRAUD. Accounting Anomalies. Accounting Anomalies

Proactive Fraud Auditing End of Chapter 4 in Albrecht FRAUD DETECTION Recognizing the Symptoms of Fraud Actg 537 Identify Risk Exposures 1 2 Identify Fraud Symptoms for Each Exposure Proactively Look for

Proactive Fraud Auditing End of Chapter 4 in Albrecht FRAUD DETECTION Recognizing the Symptoms of Fraud Actg 537 Identify Risk Exposures 1 2 Identify Fraud Symptoms for Each Exposure Proactively Look for

Financial Management. Self-Assessment Checklist: The Code identifies one key principle on financial management:

Self-Assessment Checklist: Financial Management The Code of Good Practice for NGOs Responding to HIV/AIDS (the Code ) states that in order to have effective financial management organisations should ensure:

Self-Assessment Checklist: Financial Management The Code of Good Practice for NGOs Responding to HIV/AIDS (the Code ) states that in order to have effective financial management organisations should ensure:

What Happens When Internal Controls Fail

What Happens When Internal Controls Fail 1 Your Presenters Brian Sanvidge Principal Baker Tilly Ellen Labita Partner Baker Tilly Danielle Callaci Manager Baker Tilly 2 Today s Agenda > What are Internal

What Happens When Internal Controls Fail 1 Your Presenters Brian Sanvidge Principal Baker Tilly Ellen Labita Partner Baker Tilly Danielle Callaci Manager Baker Tilly 2 Today s Agenda > What are Internal

Seminar Internal Control Identification and Filtering

Seminar Internal Control Identification and Filtering 4 March 2011 by Stephen Ho Definition The process designed, implemented and maintained by those charged with governance, management and other personnel

Seminar Internal Control Identification and Filtering 4 March 2011 by Stephen Ho Definition The process designed, implemented and maintained by those charged with governance, management and other personnel

716 West Ave Austin, TX USA

Fundamentals of Computer and Internet Fraud GLOBAL Headquarters the gregor building 716 West Ave Austin, TX 78701-2727 USA II. THE USE OF COMPUTERS IN OCCUPATIONAL FRAUD Occupational fraud refers to the

Fundamentals of Computer and Internet Fraud GLOBAL Headquarters the gregor building 716 West Ave Austin, TX 78701-2727 USA II. THE USE OF COMPUTERS IN OCCUPATIONAL FRAUD Occupational fraud refers to the

Week 3: Fraud, Procure to Pay Process Controls

Edward Beaver Edward.Beaver@temple.edu ff MIS 5121: Business Processes, ERP Systems & Controls Week 3: Fraud, Procure to Pay Process Controls Video: Record the Class Discussion v Something really new,

Edward Beaver Edward.Beaver@temple.edu ff MIS 5121: Business Processes, ERP Systems & Controls Week 3: Fraud, Procure to Pay Process Controls Video: Record the Class Discussion v Something really new,

Kua O Ka La s Financial/Accounting Policies & Procedures

Kua O Ka La New Century Public Charter School 14-5322 Kaimu-Kapoho Rd. Pahoa, HI 96778 Campus Site Telephone: (808) 965-2193 Fax: (808) 965-9618 E-mail: pualaa@ilhawaii.net Kua O Ka La s Financial/Accounting

Kua O Ka La New Century Public Charter School 14-5322 Kaimu-Kapoho Rd. Pahoa, HI 96778 Campus Site Telephone: (808) 965-2193 Fax: (808) 965-9618 E-mail: pualaa@ilhawaii.net Kua O Ka La s Financial/Accounting

SURPRISE CASH COUNTS O N T H E R O A D A R E A T R A I N I N G B U R N E T, T E X A S. P r e p a r e d B y : T i a n a L a f a e l e 0 1 / 2 5 / 1 8

SURPRISE CASH COUNTS O N T H E R O A D A R E A T R A I N I N G B U R N E T, T E X A S P r e p a r e d B y : T i a n a L a f a e l e 0 1 / 2 5 / 1 8 Why Are Cash Counts Performed? Satisfies Statutory Requirements

SURPRISE CASH COUNTS O N T H E R O A D A R E A T R A I N I N G B U R N E T, T E X A S P r e p a r e d B y : T i a n a L a f a e l e 0 1 / 2 5 / 1 8 Why Are Cash Counts Performed? Satisfies Statutory Requirements

Northern Oklahoma College Tonkawa, Oklahoma

Northern Oklahoma College Tonkawa, Oklahoma Internal Audit Report INTERNAL AUDIT REPORT Table of Contents Section Page Executive Summary of Procedures Performed and Results Thereof... I 1 Expenditures...

Northern Oklahoma College Tonkawa, Oklahoma Internal Audit Report INTERNAL AUDIT REPORT Table of Contents Section Page Executive Summary of Procedures Performed and Results Thereof... I 1 Expenditures...

Cash Receipting: Fraud Prevention and Internal Controls

Office of the Washington State Auditor Pat McCarthy Cash Receipting: Fraud Prevention and Internal Controls WACO Annual Conference October 3, 2018 Table of Contents Fraud Statistics and Overview... 2 Importance

Office of the Washington State Auditor Pat McCarthy Cash Receipting: Fraud Prevention and Internal Controls WACO Annual Conference October 3, 2018 Table of Contents Fraud Statistics and Overview... 2 Importance

LOYOLA MARYMOUNT UNIVERSITY POLICIES AND PROCEDURES

LOYOLA MARYMOUNT UNIVERSITY POLICIES AND PROCEDURES DEPARTMENT: CONTROLLER S OFFICE SUBJECT: UNIVERSITY CASH HANDLING POLICY Policy Number: BF021.01 Effective Date: June 1, 2013 Approvals: Business & Finance

LOYOLA MARYMOUNT UNIVERSITY POLICIES AND PROCEDURES DEPARTMENT: CONTROLLER S OFFICE SUBJECT: UNIVERSITY CASH HANDLING POLICY Policy Number: BF021.01 Effective Date: June 1, 2013 Approvals: Business & Finance

Guide to Internal Controls

Guide to Internal Controls Updated January 2017 The Guide to Internal Controls was developed to help you establish and maintain effective internal controls in your department/division. This guide summarizes

Guide to Internal Controls Updated January 2017 The Guide to Internal Controls was developed to help you establish and maintain effective internal controls in your department/division. This guide summarizes

Embezzlement & Fraud How You Can Protect Yourself. Pam Newman, CMA,CFM, MBA

Embezzlement & Fraud How You Can Protect Yourself Pam Newman, CMA,CFM, MBA Pam Newman BS and MBA from University of Nebraska CMA Certified Management Accountant CFM Certified Financial Manager President

Embezzlement & Fraud How You Can Protect Yourself Pam Newman, CMA,CFM, MBA Pam Newman BS and MBA from University of Nebraska CMA Certified Management Accountant CFM Certified Financial Manager President

DEPARTMENTAL CONTROL SELF-ASSESSMENT. Dept.: Date:

Dept.: Date: Performing a control self-assessment (CSA) in your department is a constructive approach to evaluating existing controls and to developing additional controls if needed. This worksheet was

Dept.: Date: Performing a control self-assessment (CSA) in your department is a constructive approach to evaluating existing controls and to developing additional controls if needed. This worksheet was

Internal Controls. for County Recorders

Internal Controls for County Recorders Definition of Internal Controls State Board of Accounts (SBOA) defines internal control as follows: Internal control is a process executed by officials and employees

Internal Controls for County Recorders Definition of Internal Controls State Board of Accounts (SBOA) defines internal control as follows: Internal control is a process executed by officials and employees

OTHER PEOPLE S MONEY: THE BASICS OF ASSET MISAPPROPRIATION

OTHER PEOPLE S MONEY: THE BASICS OF ASSET MISAPPROPRIATION World Headquarters the gregor building 716 West Ave Austin, TX 78701-2727 USA IV. PAYROLL SCHEMES Overview Payroll schemes occur when an employee

OTHER PEOPLE S MONEY: THE BASICS OF ASSET MISAPPROPRIATION World Headquarters the gregor building 716 West Ave Austin, TX 78701-2727 USA IV. PAYROLL SCHEMES Overview Payroll schemes occur when an employee

MIS 5208 Week 2 Fraud Detection & Prevention

MIS 5208 Week 2 Fraud Detection & Prevention Introductions, Course Outline, and Other Administration Issues Ed Ferrara, MSIA, CISSP eferrara@temple.edu Fraud Awareness & Internal Controls Awareness Internal

MIS 5208 Week 2 Fraud Detection & Prevention Introductions, Course Outline, and Other Administration Issues Ed Ferrara, MSIA, CISSP eferrara@temple.edu Fraud Awareness & Internal Controls Awareness Internal

INTERNAL AUDIT EFFECTIVENESS. Conducting Fraud Investigations Conducting Internal Audit

INTERNAL AUDIT EFFECTIVENESS Conducting Fraud Investigations Conducting Internal Audit Conducting Fraud Investigations Why Fraud? Fraud is the product of three factors: Supply of motivated offenders; The

INTERNAL AUDIT EFFECTIVENESS Conducting Fraud Investigations Conducting Internal Audit Conducting Fraud Investigations Why Fraud? Fraud is the product of three factors: Supply of motivated offenders; The

2018 Parking Services Cash Handling Review 8/3/2018. P.O. BOX 1027, SAVANNAH, GA

2018 Parking Services Cash Handling Review 8/3/2018 P.O. BOX 1027, SAVANNAH, GA 31402 www.savannahga.gov Table of Contents Executive Summary...3 Introduction and Background..4 Objective, Scope, and Methodology.5

2018 Parking Services Cash Handling Review 8/3/2018 P.O. BOX 1027, SAVANNAH, GA 31402 www.savannahga.gov Table of Contents Executive Summary...3 Introduction and Background..4 Objective, Scope, and Methodology.5

Accounting Specialist I Accounting Specialist II Accounting Specialist III Class Specification

Accounting Specialist I Accounting Specialist II Accounting Specialist III Class Specification FLSA Designation: Non-Exempt Effective: 03/2004 Revised: N/A DEFINITION Under general supervision (Accounting

Accounting Specialist I Accounting Specialist II Accounting Specialist III Class Specification FLSA Designation: Non-Exempt Effective: 03/2004 Revised: N/A DEFINITION Under general supervision (Accounting

Adopted by Naytahwaush Community Charter School Board: November 13, 2012

INTERNAL CONTROLS (MSBA/MASA Model Policy 703) Adopted by Naytahwaush Community Charter School Board: November 13, 2012 This policy is designed to be used in conjunction with current procedures, and to

INTERNAL CONTROLS (MSBA/MASA Model Policy 703) Adopted by Naytahwaush Community Charter School Board: November 13, 2012 This policy is designed to be used in conjunction with current procedures, and to

November In this Issue

Page 1 of 5 View this newsletter and archived copies online at www.businesswc.com November 2010 - In this Issue TRAVERSE & OSAS News Year End Assistance Accounts Payable Tips Emailing Invoices & Purchase

Page 1 of 5 View this newsletter and archived copies online at www.businesswc.com November 2010 - In this Issue TRAVERSE & OSAS News Year End Assistance Accounts Payable Tips Emailing Invoices & Purchase

10/6/2018. Frank Gorrell, MSA, CPA, CGMA. Payroll fraud happens! No organization is immune! We ll checks the stats We ll review controls

Frank Gorrell, MSA, CPA, CGMA Payroll fraud happens! No organization is immune! We ll checks the stats We ll review controls 1 Association of Certified Fraud Examiners (ACFE) Report to the Nations 2018

Frank Gorrell, MSA, CPA, CGMA Payroll fraud happens! No organization is immune! We ll checks the stats We ll review controls 1 Association of Certified Fraud Examiners (ACFE) Report to the Nations 2018

Nutrition & Food Services AHIA 2012

Internal Control Questionnaire (2) page 1 of 5 7/17/2012 General Information Control Questionnaire Objective: To gather departmental information and documentation as a part of the preliminary survey phase

Internal Control Questionnaire (2) page 1 of 5 7/17/2012 General Information Control Questionnaire Objective: To gather departmental information and documentation as a part of the preliminary survey phase

CITY OF REEDLEY ACCOUNTING TECHNICIAN I ACCOUNTING TECHNICIAN II

CITY OF REEDLEY ACCOUNTING TECHNICIAN I ACCOUNTING TECHNICIAN II DEFINITION Under immediate supervision (Accounting Technician I) or general supervision (Accounting Technician II), to perform a variety

CITY OF REEDLEY ACCOUNTING TECHNICIAN I ACCOUNTING TECHNICIAN II DEFINITION Under immediate supervision (Accounting Technician I) or general supervision (Accounting Technician II), to perform a variety

Going on the Offensive: Blocking and Tackling to Minimize Fraud

Going on the Offensive: Blocking and Tackling to Minimize Fraud Welcome and Introductions Linda Goldstein Director, Compliance & Privacy Associate General Counsel MARY SMITH CEO Jonathan Marks CPA, CFE

Going on the Offensive: Blocking and Tackling to Minimize Fraud Welcome and Introductions Linda Goldstein Director, Compliance & Privacy Associate General Counsel MARY SMITH CEO Jonathan Marks CPA, CFE

IIA Springfield IL Chapter

Adding Value with Data Analytics IIA Springfield IL Chapter October 14, 2010 0 Jan Beckmann, CPA, ACL Certified Trainer, ACDA jbeckmann@bswllc.com 314.983.1254 1050 N. Lindbergh Blvd. St. Louis, Missouri

Adding Value with Data Analytics IIA Springfield IL Chapter October 14, 2010 0 Jan Beckmann, CPA, ACL Certified Trainer, ACDA jbeckmann@bswllc.com 314.983.1254 1050 N. Lindbergh Blvd. St. Louis, Missouri

Committee for Senior Business Administrators. Segregation of Duties

Committee for Senior Business Administrators Segregation of Duties Presented by: Tammy R. Hoskens and Margaret (Peggy) B. Zapalac University Risk and Compliance May 21, 2009 Segregation of Duties Segregation

Committee for Senior Business Administrators Segregation of Duties Presented by: Tammy R. Hoskens and Margaret (Peggy) B. Zapalac University Risk and Compliance May 21, 2009 Segregation of Duties Segregation

Cash Receipting: Fraud Prevention and Internal Controls

Cash Receipting: Fraud Prevention and Internal Controls Your government works hard to serve its residents with the resources available. This can mean that the internal processes you rely on to do your

Cash Receipting: Fraud Prevention and Internal Controls Your government works hard to serve its residents with the resources available. This can mean that the internal processes you rely on to do your

CHAPTER 5 INFORMATION TECHNOLOGY SERVICES CONTROLS

5-1 CHAPTER 5 INFORMATION TECHNOLOGY SERVICES CONTROLS INTRODUCTION In accordance with Statements on Auditing Standards Numbers 78 and 94, issued by the American Institute of Certified Public Accountants

5-1 CHAPTER 5 INFORMATION TECHNOLOGY SERVICES CONTROLS INTRODUCTION In accordance with Statements on Auditing Standards Numbers 78 and 94, issued by the American Institute of Certified Public Accountants

DOCUMENT EDIT/VOID RULES (When Editing and/or Voiding documents once entered into the system) PURCHASING

PURCHASING") DOCUMENT EDIT/VOID RULES (When Editing and/or Voiding documents once entered into the system) PURCHASING Purchase Order Can be fully Edited up until Approval Can be Voided up until Approval Once Approved

DOCUMENT EDIT/VOID RULES (When Editing and/or Voiding documents once entered into the system) PURCHASING Purchase Order Can be fully Edited up until Approval Can be Voided up until Approval Once Approved

ADMINISTRATIVE RESPONSIBILITIES FOR UNIVERSITY AND COLLEGE ADMINISTRATORS, DEPARTMENT HEADS, AND DIRECTORS

ADMINISTRATIVE RESPONSIBILITIES FOR UNIVERSITY AND COLLEGE ADMINISTRATORS, DEPARTMENT HEADS, AND DIRECTORS Internal Controls & Your Role 1) Internal Accounting Controls - procedures that ensure compliance

ADMINISTRATIVE RESPONSIBILITIES FOR UNIVERSITY AND COLLEGE ADMINISTRATORS, DEPARTMENT HEADS, AND DIRECTORS Internal Controls & Your Role 1) Internal Accounting Controls - procedures that ensure compliance