AUDIT OF: Richmond Pubic Schools PAYROLL

|

|

|

- Angelina Sims

- 5 years ago

- Views:

Transcription

1 AUDIT OF: Richmond Pubic Schools PAYROLL Report Issued: Report Number:

2 TABLE OF CONTENTS Executive Summary... ii Comprehensive List of Recommendations...v Introduction and Scope...1 Methodology...2 Background...3 Management Responses... Appendix A

3 Executive Summary October 25, 2013 The Honorable Members of the Richmond Public School Board Subject: Richmond Public Schools Payroll Audit function. The auditors conducted this performance audit in accordance with generally accepted government auditing standards. RPS paid a total of $277,273,056 to their employees over the course of the 18-month audit period. Payroll is the most significant expenditure in the RPS annual budget. Although the processing of payroll is centralized within the Department of Finance, tracking and submission of time worked and leave taken is decentralized throughout the more than 60 schools and departments. Proper oversight and controls over Payroll expenditures are critical. This report examines the oversight and management of the payroll function. Salient Findings The auditors identified that transparency in reporting payroll expenditures to the School Board needs improvement. RPS staff was not able to provide basic information such as the total number of RPS employees. RPS has employment contracts with a majority of its employees. There is a mix of contractual and non-contractual employees doing the same jobs. The School Board is requested to approve contracted positions. - not fully disclosed to the Board. The records indicate that on average 1,037 non-contracted employees may have been paid by RPS during FY12. ii

4 The authority to hire non-contracted employees is often assumed by individual departments and schools. Risks that are associated with this hiring authority are as followed: o Favoritism and Cronyism o Nepotism o Fraud and Waste Any abuse of this authority will not be apparent, as no other control exists to manage expenditures on non-contracted employees. At times, normal hiring process is circumvented by the Principals and Directors. This situation has the potential for risks, such as: o Favoritism and Cronyism o Nepotism o Hiring individuals with questionable criminal histories o Hiring individuals that are not eligible for rehire Currently, the time and leave documentation process is inconsistently handled at each of the more than 60 schools and departments. Several discrepancies were noticed, including inaccurate payments, missing supervisory approvals, lack of employee validation and hours worked. auditors noticed two instances where an employee received pay for overtime hours not worked. Additionally, there were five instances where there was no supervisory approval of timesheets, in which overtime was earned. In these cases, if an inappropriate amount of overtime is paid, it will not be detected through normal procedures. The Finance Department does not keep properly detailed records of compensatory time earned and used. Staff was unable to provide the history of compensatory time earned and used during the audit period. This discrepancy creates the risk of employees utilizing leave that is not earned, which could result in financial loss to the Division. iii

5 RPS needs to develop a formal comprehensive policies and procedures manual. Incomplete written policies and procedures, and failure to effectively communicate them to staff, may lead to unclear job duties and responsibilities, and inconsistent job performance by employees. Richmond Public staff. Please contact me for questions and comments on this report. Sincerely, Umesh Dalal Umesh Dalal, CPA, CIA, CIG City Auditor ce: Dr. Jonathan Lewis, Interim Superintendant iv

6 COMPREHENSIVE LIST OF RECOMMENDATIONS # PAGE 1 Improve transparency in reporting payroll costs by: 7 a. Separately budgeting and presenting to the School Board the cost of non-contracted employees in each function and in the budget summary. b. Periodically report to the School Board the total number of noncontracted employees and related payroll costs. 2 Establish a policy that ensures Principals/Directors are held accountable for 10 not complying with the established hiring process and termination procedures. 3 Implement an automated timekeeping system, such as electronic time clocks 13 or a computerized time entry system for the hourly employees, that includes timely review and approval of time worked. 4 Establish a system for recording and tracking compensatory time earned and 13 used, which provides a documented history of activity. 5 Develop a written policy for submitting unclaimed property to the State that 15 includes a compliance review by the CFO. 6 Develop a formal, comprehensive policies and procedures manual, which should be readily available to all staff. 15 v

7 Overview Introduction and Scope the Richmond Public Schools (RPS) Payroll function. This audit covers the 18-month period that ended December 31, The objectives of this audit were to: Evaluate the efficiency and effectiveness of operations Determine the existence and effectiveness of internal controls Verify compliance with laws, regulations, and policies The auditors conducted this performance audit in accordance with generally accepted government auditing standards. Those standards require that the auditors plan and perform the audit to obtain sufficient, appropriate evidence to provide a reasonable basis for their findings and conclusions based on the audit objectives. The auditors believe that the evidence obtained provides a reasonable basis for their findings and conclusions based on the audit objectives. Methodology The auditors employed the following procedures to complete this audit: Compared time sheets to time entered and paid Reviewed relevant records, policies, and regulations Reviewed manual checks issued to personnel Reviewed payroll and personnel files to determine whether there were any ghost employees Observed the payroll distribution process Recalculated final pay for accuracy Reviewed overtime earned Performed other audit procedures, as deemed necessary 1

8 Management Responsibility Background The Management of RPS is responsible for ensuring resources are managed properly and used in compliance with laws and regulations; RPS programs are achieving their objectives; and services are being provided efficiently, effectively, and economically. Background RPS paid a total of $277,273,056 to their employees over the course of the 18-month audit period. Payroll is the most significant expenditure in the RPS annual budget. The following pie-chart depicts the magnitude of this expenditure for FY12: 2% 2%1% 2% Payroll is the largest expenditure for RPS 7% 21% 4% 61% Salaries and Wages Employee Benefits Purchased Services Other Charges Materials & Supplies Other Operating Expenses Capital Outlay Other Uses of Funds Sour ce: FY12 Approved Budget Proper oversight and controls over Payroll expenditures are critical. This report examines the oversight and management of the payroll function. The RPS payroll function relies on several interdependent relationships between the payroll, human resources, and budget functions; consequently, it was necessary to review certain processes and procedures outside of payroll ties during this audit. 2

9 Decentralized Operations Although the processing of payroll is centralized within the Department of Finance, tracking and submission of time worked and leave taken is decentralized throughout the more than 60 schools and departments. Below is an overview of the process: Over 60 Schools and Departments: Maintains timesheets Submits hours worked in the system Tracks and submits absences in the system Submits compensatory time earned Payroll: Receives memorandums for compensatory time earned Runs semi- monthly payroll based on data entered into the system 3

10 Observations and Recommendations What Works Well? As part of the audit process, the auditors reviewed many facets of the payroll function. While this report includes recommendations for improving the payroll process, the auditors identified processes that are functioning adequately. Those include the following: RPS conducts several payroll tasks well Automated access to personnel data was acceptable FICA payroll tax deductions were calculated correctly Medical and dental benefit deductions were appropriately entered and accurately deducted There were no duplicate social security numbers or employee identification numbers within the system, minimizing the existence of ghost employees Any duplicate names, addresses, and bank account numbers identified and reviewed were acceptable In addition, the following improvements are currently in progress: RPS is in the process of implementing a web portal for staff to retrieve their direct deposit pay remittances and tax documentation RPS is working to implement the use of payroll debit cards to eliminate the necessity to print paper checks. This development will address the currently inconsistent payroll check distribution. Also, it may reduce the number of manual checks written by RPS 4

11 What Needs Improvement? Transparency The auditors identified that transparency in reporting payroll expenditures to the School Board needs improvement. RPS staff was not able to provide basic information such as the total number of RPS employees. Transparency in reporting payroll information to the School Board needs improvement RPS has employment contracts with a majority of its employees. These include teachers, bus drivers, custodians, food and nutrition staff, and administrative staff, etc. However, there is a mix of contractual and non-contractual employees doing the same jobs. Non-contractual employees are typically considered to be temporary employees, and they do not receive benefits offered by RPS to its contracted employees. Both contracted and non-contracted employees work throughout the schools and departments. Non-contracted employees are paid on a per hour basis. The School Board is requested to approve contracted positions. -contracted not fully disclosed to the Board. The following table illustrates the variance between the approved number of contracted positions and the actual number of paid employees for FY12. 5

12 RPS has employed many non-contracted personnel, without specific approval by the School Board Month FY12 Total Employees Paid by Month FY12 Approved FTE Count Excess Number of Employees Over Approved July 5,236 3,888 1,348 August 4,527 3, September 4,450 3, October 4,739 3, November 4,999 3,888 1,111 December 5,008 3,888 1,120 January 5,013 3,888 1,125 February 5,067 3,888 1,179 March 5,050 3,888 1,162 April 5,040 3,888 1,152 May 5,037 3,888 1,149 June 4,933 3,888 1,045 Average: 4,925 3,888 1,037 RPS has consistently budgeted contracted positions at a level less than its actual labor needs Auditors learned, as illustrated above, some departments have consistently budgeted for contracted positions at a level less than their actual labor needs. As a result, RPS has consistently hired noncontracted employees to perform duties similar or identical to contracted workers, without providing health or other benefits normally received by contracted employees. This may be causing unequal treatment of employees performing identical duties. RPS neither assigns position numbers to the non-contracted positions, nor do they have a specific budget allocated to the positions in this category. As a result, the School Board does not have the knowledge or opportunity to critically evaluate expenditures incurred for noncontracted positions. 6

13 Lack of transparency could result in abuse Risks Associated with the Lack of Transparency The authority to hire non-contracted employees is often assumed by individual departments and schools. The following risks are associated with this hiring authority: Favoritism and cronyism Nepotism Fraud and waste Any abuse of this authority will not be apparent, as no other control exists to manage expenditures on non-contracted employees. Recommendation: 1. Improve transparency in reporting payroll costs by: a. Separately budgeting and presenting to the School Board the cost of non-contracted employees in each function and in the budget summary. b. Periodically report to the School Board the total number of non-contracted employees and related payroll costs. Internal Controls According to Government Auditing Standards, internal control, in the broadest sense, s, policies, procedures, methods, and processes adopted by management to meet its mission, goals, and objectives. Internal control includes the processes for planning, organizing, directing, and controlling program operations. It also includes systems for measuring, reporting, and monitoring program performance. Based on the results and findings of the audit methodology employed, the auditors concluded that controls and procedures need to be improved for effective management of RPS payroll processing, as discussed in the next section. 7

14 Human Resources (HR) Hiring Processes are Circumvented: RPS has an established process for the hiring of personnel within the school system. This process is depicted below: Some RPS managers circumvented established hiring process Position Posted Hired Upon Acceptable Background Checks HR Receives and Reviews Applications Background Checks Interviews Offer Contingent on Background Checks The above procedures, however, are not consistently followed creating potential for abuse. Principals/Directors have hired hourly personnel without following HR established hiring processes. The auditors reviewed a sample of 64 terminated employees and, in the process, identified the following two instances where the normal hiring process was circumvented: 1. A retiree was rehired prior to satisfying the Virginia Retirement System (VRS) required break in service. VRS allows retirees to return to work, under certain circumstances, and continue to receive retirement benefits, if there is a bona fide break in service of at least one full calendar month from retirement date. This individual retired in June 2012 and was rehired and subsequently paid wages of $1, by RPS in July After inquiring about the discrepancy, the auditor was provided an undated memo, addressed to the RPS Education Foundation, requesting this individual be paid as a consultant for the period 8

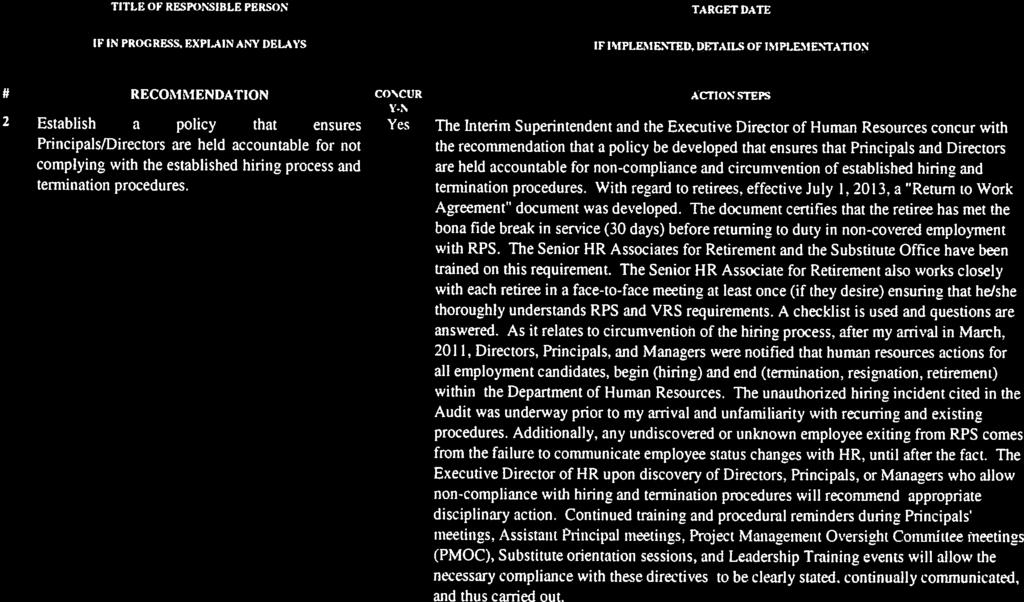

15 worked. The Foundation reimbursed RPS in June 2013 after the auditor brought this matter to the attention of the Finance Department staff. In at least one instance, circumvention of the hiring process could have placed summer school students in harms way 2. The auditors also identified an individual, terminated for taking indecent liberties with a minor and ineligible for rehire, who was rehired on an hourly basis without going through the established hiring process. Upon learning of the hiring, due to the individual not receiving a paycheck, HR immediately contacted the Principal, and subsequently the individual was terminated. Hiring by circumventing the established process is infrequent, but not isolated The above examples do not appear to be isolated incidents. Through a review of manual payroll checks issued, the auditor identified 95 employees that could have been hired outside the established process. In these cases, manual checks were issued because (1) new employee paperwork was not turned into HR timely; (2) employees were not set up by HR prior to the first payroll date; and/or (3) the employees did not initially receive a paycheck for hours worked. Any abuse occurring in these hiring situations may not be detected in a timely manner. There is a potential for abuse in the current practices It appears RPS management needs to take the necessary steps to effectively discipline Principals/Directors who circumvent the established process. When established hiring processes are circumvented, the individuals are not subjected to the pre-employment 9

16 background and employment eligibility checks. This results in the potential for: Nepotism Favoritism Hiring individuals with questionable criminal histories Hiring individuals that are not eligible for rehire Untimely Notification of Terminated Employees When an employee resigns or is terminated, the relevant principal or manager must notify HR in a timely manner for further action and system update. During the review of the sample of 64 terminated employees, the auditor observed that one contracted employee was overpaid $1, This individual resigned on September 28, 2011, but the notice of personnel change was not entered until October 31, RPS collection efforts have not been successful in recovering the overpayment from the former employee. Recommendation: 2. Establish a policy that ensures Principals/Directors are held accountable for not complying with the established hiring process and termination procedures. Incomplete or Unauthorized Timesheets Inconsistent timesheet records may not allow for accurate time keeping The Finance Department has not established a uniform method to document time and attendance at all locations. Currently, the time and leave documentation process is inconsistently handled at each of the more than 60 schools and departments. These methods ranged from the timekeeper simply observing staff presence to having daily, formal 10

17 sign-in sheets. Generally, time and attendance tracking was accomplished using one of the following methods: Visual observation not supported by documentation Sign-in and sign-out logs for all hourly employees in the building Individualized time sheets for hourly employees Auditors observed time and attendance tracking for a sample of 55 individuals over 6 pay periods at 15 RPS locations. The auditors were unable to validate hours worked for all employees reviewed. Of the sample selected, 283 of 330 potential time tracking documents were available. Auditors made the following observations: Several timesheets were missing, and errors were identified in the timesheets available The 64 documents reviewed did not agree with the hours paid within the system: Documented hours were less than hours paid in 45 cases Documented hours were more than hours paid in 19 cases No documentation was available to validate hours worked in 47 cases. In reviewing available documentation, it was noted that often documents were missing supervisory approval, employee validation, and hours worked. Without complete and authorized time and attendance records, RPS could be over or under compensating its hourly employees. Additionally, employees may not be reporting leave taken. These discrepancies have a financial impact on RPS that could not be quantified. 11

18 Unsupproted Overtime Before any employee can receive overtime pay, the individual must work 40 hours within the pay week, not including any sick or vacation time utilized. The auditor reviewed a sample of 65 employees from RPS departments. The Transportation, Maintenance, and Security departments incurred the most overtime hours and experienced higher overtime costs. Department Overtime Hours Transportation 34, Maintenance 4, Security 4, When reviewing the documentation available in the Transportation Department (46 of the 65 items sampled) the auditor noted 2 instances where an employee received pay for overtime hours not worked. The documentation available for these instances did not support the hours paid. After discussion with Transportation Management, it appears these are isolated incidents and the employees involved have since resigned from their positions. Accuracy of all overtime hours could not be verified in the selected sample Additionally, there were five instances where there was no supervisory approval of timesheets, in which overtime was earned. In these cases, if an inappropriate amount of overtime is paid, it will not be detected through normal procedures. For the remaining 19 employees in the sample selection from other departments, the auditor could not confirm if the overtime was earned. The Security, Plant Services, and Food and Nutrition functions assign their employees to locations throughout the school system; however, the time worked is documented and approved at the respective central 12

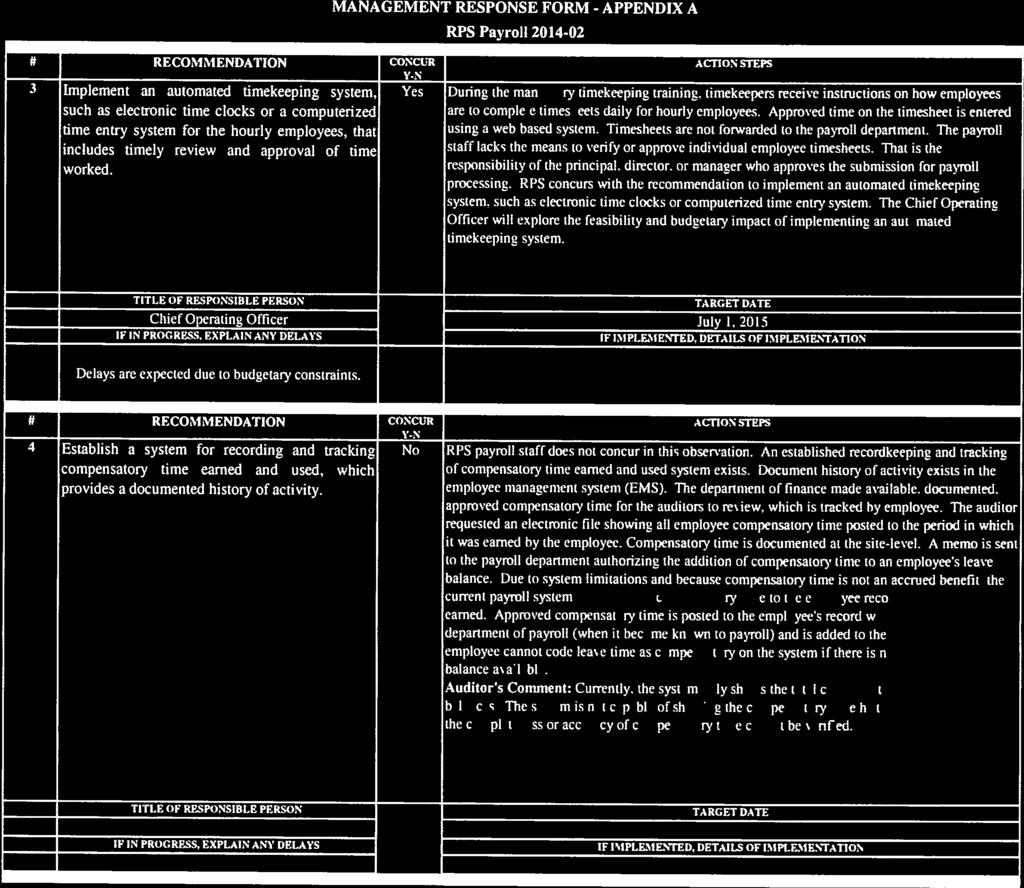

19 locations. Therefore, the timekeeper does not have the ability to verify the time actually worked by the employees. At the individual locations where the work is performed, no one is consistently validating the hours worked and overtime earned by the individuals. Therefore, it is not possible to validate the appropriateness of the overtime paid. Detailed records of compensatory time earned and used are not available Compensatory Time is Not Being Tracked Properly Auditors attempted to verify whether compensatory time earned during the audit period was properly authorized and used. The auditors were not able to perform this testing, as the Finance Department does not keep properly detailed records of compensatory time earned and used. Staff was unable to provide the history of compensatory time earned and used during the audit period. This discrepancy creates the risk of employees utilizing leave that is not earned, which could result in financial loss to the Division. Recommendation: 3. Implement an automated timekeeping system, such as electronic time clocks or a computerized time entry system for the hourly employees, that includes timely review and approval of time worked. 4. Establish a system for recording and tracking compensatory time earned and used, which provides a documented history of activity. Outstanding Payroll Checks The auditor s review identified 104 outstanding payroll checks, ranging in age from 30 days to more than 1 year. Most of these checks were issued to correct a tax calculation error that resulted in underpayments 13

20 to employees. All of the outstanding checks belong to currently active employees. Seven employees on the list had more than one check outstanding as follows: Employee Number of Checks Total Dollars A 2 $ B 3 $2, C 2 $ D 3 $ E 2 $ F 3 $2, G 2 $1, According to the State of Virginia Code , unpaid wages, including wages that have remained unclaimed by the owner for more than one year after becoming payable, are presumed to be abandoned. Through review of the outstanding checks, the auditor determined five checks should have been reported to the Unclaimed Property Division in October It is the responsibility of RPS to attempt to contact the payee no less than 60 days prior to the submission of the report. Once due diligence has been performed and the check is more than one year old, the check should be turned over to the State Department of Treasury Unclaimed Property Division by November 1 of each year. Although RPS does not have a documented policy to dictate how to handle outstanding payroll checks, the Finance Department had complied with the State policy and sent due diligence letters to the payees of these checks. According to Departmental staff, the checks were not forwarded to the State because the individual payees contacted the Department indicating they would retrieve their checks. 14

21 Recommendation: 5. Develop a written policy for submitting unclaimed property to the State that includes a compliance review by the CFO. Policies and Procedures A formal, comprehensive policies and procedures manual needs to be developed Lack of Complete and Updated Payroll Policies and Procedures The auditor requested a copy of the written payroll policies and procedures. A set of documents was provided that did not include any formal manual. These appeared to be training documents, rather than a formal policies and procedures manual. The set of documents provided lacked the following elements of a formal policies and procedures manual: Authority by which the document was issued Consistent organization and structure of policies and procedures Effective date of policies and procedures Number and titling of policies and procedures Distribution to employees and/or electronic access A formal comprehensive policies and procedures manual must be developed. Incomplete written policies and procedures, and failure to effectively communicate them to staff, may lead to unclear job duties and responsibilities, and inconsistent job performance by employees. Also, written policies and procedures are important to ensure the continuity of operations during employee turnover. Recommendation: 6. Develop a formal, comprehensive policies and procedures manual, which should be readily available to all staff. 15

22

23

24

Citywide Payroll

2019-07 City of Richmond, VA City Auditor s Office January 04, 2019 Executive Summary... i Background, Objectives, Scope, Methodology... 1 Findings and Recommendations... 4 Management Response...Appendix

2019-07 City of Richmond, VA City Auditor s Office January 04, 2019 Executive Summary... i Background, Objectives, Scope, Methodology... 1 Findings and Recommendations... 4 Management Response...Appendix

Assistance. and Guidance Report. Administration and Processing of Leave and Attendance Report #1219 September 5, 2012

Assistance and Guidance Report Sam M. McCall, Ph.D., CPA, CGFM, CIA, CGAP City Auditor Administration and Processing of Leave and Attendance Report #1219 September 5, 2012 Introduction This guidance is

Assistance and Guidance Report Sam M. McCall, Ph.D., CPA, CGFM, CIA, CGAP City Auditor Administration and Processing of Leave and Attendance Report #1219 September 5, 2012 Introduction This guidance is

The Honorable Members of the School Board of the City of Richmond, Virginia

School Board of the City of Richmond, Virginia Richmond Public Schools Internal Audit Services Review of the Payroll Process July 1, 2006 May 31, 2009 Audit Assignment No.: A 3101 09 001 June 22, 2009

School Board of the City of Richmond, Virginia Richmond Public Schools Internal Audit Services Review of the Payroll Process July 1, 2006 May 31, 2009 Audit Assignment No.: A 3101 09 001 June 22, 2009

March 22, Internal Audit Report Municipal Payroll Review Finance Department

Internal Audit Report 2005-3 Introduction. The Municipality of Anchorage has a complex payroll system that includes nine unions, a wide variety of work schedules and leave plans, and serves about 2,900

Internal Audit Report 2005-3 Introduction. The Municipality of Anchorage has a complex payroll system that includes nine unions, a wide variety of work schedules and leave plans, and serves about 2,900

Office of the City Auditor. Committed to increasing government efficiency, effectiveness, accountability and transparency

Office of the City Auditor Committed to increasing government efficiency, effectiveness, accountability and transparency Issue Date: TABLE OF CONTENTS Executive Summary... ii Recommendation... iv Background...1

Office of the City Auditor Committed to increasing government efficiency, effectiveness, accountability and transparency Issue Date: TABLE OF CONTENTS Executive Summary... ii Recommendation... iv Background...1

PERSONNEL POLICY MANUAL

POLICY C-1 Page 1 of 2 SUBJECT: PAYMENT OF WAGES Notes: Replaces Policy 3.0, Payment of Wages, Policy 3.3, Pay Advance and Policy 6.8, Direct Deposit PURPOSE: To establish processes required for payment

POLICY C-1 Page 1 of 2 SUBJECT: PAYMENT OF WAGES Notes: Replaces Policy 3.0, Payment of Wages, Policy 3.3, Pay Advance and Policy 6.8, Direct Deposit PURPOSE: To establish processes required for payment

Edmonton Police Service Payroll Audit April 4, 2012

Edmonton Police Service Payroll Audit April 4, 2012 The Office of the City Auditor conducted this project in accordance with the International Standards for the Professional Practice of Internal Auditing

Edmonton Police Service Payroll Audit April 4, 2012 The Office of the City Auditor conducted this project in accordance with the International Standards for the Professional Practice of Internal Auditing

Section Contents Page # What s New? General Information Board Policy Federal Law Payroll Staff...

SECTION 13: PAYROLL Section Contents Page # What s New?...13-2 General Information...13-2 Board Policy...13-2 Federal Law...13-2 Payroll Staff...13-3 TEAMS Employee Service Center...13-3 Timekeeping for

SECTION 13: PAYROLL Section Contents Page # What s New?...13-2 General Information...13-2 Board Policy...13-2 Federal Law...13-2 Payroll Staff...13-3 TEAMS Employee Service Center...13-3 Timekeeping for

Montgomery I.S.D Payroll Procedures Manual

Montgomery I.S.D. 2017-2018 Payroll Procedures Manual Table of Contents SECTION A GENERAL INFORMATION 01. INTRODUCTION... 2 02. LOCATION........ 2 03. PAYROLL CONTACT INFORMATION... 2 04. PAY DATES & PAYROLL

Montgomery I.S.D. 2017-2018 Payroll Procedures Manual Table of Contents SECTION A GENERAL INFORMATION 01. INTRODUCTION... 2 02. LOCATION........ 2 03. PAYROLL CONTACT INFORMATION... 2 04. PAY DATES & PAYROLL

NORTH CAROLINA SCHOOL OF SCIENCE AND MATHEMATICS TEMPORARY APPOINTMENT POLICY AND PROCEDURES

NORTH CAROLINA SCHOOL OF SCIENCE AND MATHEMATICS TEMPORARY APPOINTMENT POLICY AND PROCEDURES Departments employ temporary staff due to vacancies in permanent positions or for additional, short-term labor.

NORTH CAROLINA SCHOOL OF SCIENCE AND MATHEMATICS TEMPORARY APPOINTMENT POLICY AND PROCEDURES Departments employ temporary staff due to vacancies in permanent positions or for additional, short-term labor.

Office of the City Auditor. Committed to increasing government efficiency, effectiveness, accountability and transparency

Office of the City Auditor Committed to increasing government efficiency, effectiveness, accountability and transparency Issue Date: January 10, 2017 Table of Contents Executive Summary... ii Comprehensive

Office of the City Auditor Committed to increasing government efficiency, effectiveness, accountability and transparency Issue Date: January 10, 2017 Table of Contents Executive Summary... ii Comprehensive

Audit Follow Up. Citywide Disbursements (Report #0410, Issued April 15, 2004) As of September 30, Summary

As of September 30, Summary") Audit Follow Up As of September 30, 2004 Sam M. McCall, CPA, CGFM, CIA, CGAP City Auditor Citywide Disbursements - 2003 (Report #0410, Issued April 15, 2004) Report #0521 March 28, 2005 Summary City departments

Audit Follow Up As of September 30, 2004 Sam M. McCall, CPA, CGFM, CIA, CGAP City Auditor Citywide Disbursements - 2003 (Report #0410, Issued April 15, 2004) Report #0521 March 28, 2005 Summary City departments

Village of Waterville

DIVISION OF LOCAL GOVERNMENT AND SCHOOL ACCOUNTABILITY REPORT OF EXAMINATION 2017M-281 Village of Waterville Payroll and Time and Attendance Records APRIL 2018 Contents Report Highlights.............................

DIVISION OF LOCAL GOVERNMENT AND SCHOOL ACCOUNTABILITY REPORT OF EXAMINATION 2017M-281 Village of Waterville Payroll and Time and Attendance Records APRIL 2018 Contents Report Highlights.............................

Administration & Finance

Issuing Office: Policy Number: FY16-HRS-009-00 Policy Name: Time & Attendance Policy and Guidelines Original Date Issued: June 24, 2016 Revised: Purpose of Policy: The purpose of this policy is to: Confirm

Issuing Office: Policy Number: FY16-HRS-009-00 Policy Name: Time & Attendance Policy and Guidelines Original Date Issued: June 24, 2016 Revised: Purpose of Policy: The purpose of this policy is to: Confirm

Timekeeping Procedures

Timekeeping Procedures San Angelo ISD s electronic timekeeping program, TimeClock Plus, is the official system for recording hours worked by all non exempt employees. Initial Set up The Human Resources

Timekeeping Procedures San Angelo ISD s electronic timekeeping program, TimeClock Plus, is the official system for recording hours worked by all non exempt employees. Initial Set up The Human Resources

Prince William County, Virginia Internal Audit Report Timekeeping Cycle Audit. August 31, 2018

Prince William County, Virginia Internal Audit Report Timekeeping Cycle Audit August 31, 2018 TABLE OF CONTENTS Transmittal Letter... 1 Executive Summary... 2 Background... 4 Objectives and Approach...

Prince William County, Virginia Internal Audit Report Timekeeping Cycle Audit August 31, 2018 TABLE OF CONTENTS Transmittal Letter... 1 Executive Summary... 2 Background... 4 Objectives and Approach...

PAYROLL-PROCEDURE

207-01 PAYROLL-PROCEDURE 1. PURPOSE The purpose of the Payroll Procedure is to establish criteria for the proper control and handling of payments to employees. 2. PROCEDURES 1. Budget Manager Responsibilities

207-01 PAYROLL-PROCEDURE 1. PURPOSE The purpose of the Payroll Procedure is to establish criteria for the proper control and handling of payments to employees. 2. PROCEDURES 1. Budget Manager Responsibilities

Richmond Ambulance Authority

REPORT # 2012-06 AUDIT Of the TABLE OF CONTENTS Executive Summary..... i Comprehensive List of Recommendations. iii Introduction........... 1 Background 2 Observations and Recommendations..... 3 Management

REPORT # 2012-06 AUDIT Of the TABLE OF CONTENTS Executive Summary..... i Comprehensive List of Recommendations. iii Introduction........... 1 Background 2 Observations and Recommendations..... 3 Management

INDEPENDENT ACCOUNTANT'S REPORT ON APPLYING AGREED-UPON PROCEDURES BACKGROUND

INDEPENDENT ACCOUNTANT'S REPORT ON APPLYING AGREED-UPON PROCEDURES Board of County Commissioners and Department Heads Ramsey County BACKGROUND In October 1996, a newspaper article reported that the now

INDEPENDENT ACCOUNTANT'S REPORT ON APPLYING AGREED-UPON PROCEDURES Board of County Commissioners and Department Heads Ramsey County BACKGROUND In October 1996, a newspaper article reported that the now

TEXAS SOUTHERN UNIVERSITY MANUAL OF ADMINISTRATIVE POLICIES AND PROCEDURES. SECTION: Fiscal Affairs NUMBER:

TEXAS SOUTHERN UNIVERSITY MANUAL OF ADMINISTRATIVE POLICIES AND PROCEDURES SECTION: Fiscal Affairs NUMBER: 03.04.05 AREA: SUBJECT: Payroll Employee Time and Effort Reporting I. PURPOSE AND SCOPE This document

TEXAS SOUTHERN UNIVERSITY MANUAL OF ADMINISTRATIVE POLICIES AND PROCEDURES SECTION: Fiscal Affairs NUMBER: 03.04.05 AREA: SUBJECT: Payroll Employee Time and Effort Reporting I. PURPOSE AND SCOPE This document

(2) Be incorporated into official district records.

Be incorporated into official district records.") Business and Noninstuctional Operations AR 3235(a) FEDERAL RESOURCE COMPENSATION I. Overview. All employees who are paid in full or in part with federal funds must keep specific documents to demonstrate

Business and Noninstuctional Operations AR 3235(a) FEDERAL RESOURCE COMPENSATION I. Overview. All employees who are paid in full or in part with federal funds must keep specific documents to demonstrate

EXAMINATION OF CERTAIN FINANCIAL PROCESSES AND INTERNAL CONTROLS OF THE KENTUCKY CORRECTIONAL INDUSTRIES

EXAMINATION OF CERTAIN FINANCIAL PROCESSES AND INTERNAL CONTROLS OF THE KENTUCKY CORRECTIONAL INDUSTRIES CRIT LUALLEN AUDITOR OF PUBLIC ACCOUNTS www.auditor.ky.gov 105 SEA HERO ROAD, SUITE 2 FRANKFORT,

EXAMINATION OF CERTAIN FINANCIAL PROCESSES AND INTERNAL CONTROLS OF THE KENTUCKY CORRECTIONAL INDUSTRIES CRIT LUALLEN AUDITOR OF PUBLIC ACCOUNTS www.auditor.ky.gov 105 SEA HERO ROAD, SUITE 2 FRANKFORT,

Ms. Jeanine Rufo, President, Board of Education

Date: August 31, 2016 To: From: Cc: Subject: Ms. Jeanine Rufo, President, Board of Education David Moran, Director of Education Practice Audit Committee Natalie Doherty, Assistant Superintendent Jill Figarella,

Date: August 31, 2016 To: From: Cc: Subject: Ms. Jeanine Rufo, President, Board of Education David Moran, Director of Education Practice Audit Committee Natalie Doherty, Assistant Superintendent Jill Figarella,

Audit of Public Works Overtime

T. Bert Fletcher, CPA, CGMA City Auditor HIGHLIGHTS Highlights of City Auditor Report #1618, a report to the City Commission and City management WHY THIS AUDIT WAS DONE From October 1, 2011, through September

T. Bert Fletcher, CPA, CGMA City Auditor HIGHLIGHTS Highlights of City Auditor Report #1618, a report to the City Commission and City management WHY THIS AUDIT WAS DONE From October 1, 2011, through September

Title: Timekeeping Standards

Title: Timekeeping Standards POLICY Owner: Human Resources Keywords: timekeeping, KRONOS, payroll # HR.309 Issued: 4/9/03 I. Statement of Purpose Kaleida Health requires that each employee report accurate

Title: Timekeeping Standards POLICY Owner: Human Resources Keywords: timekeeping, KRONOS, payroll # HR.309 Issued: 4/9/03 I. Statement of Purpose Kaleida Health requires that each employee report accurate

EGYPTIAN AREA AGENCY ON AGING Fiscal Monitoring Program

EGYPTIAN AREA AGENCY ON AGING Fiscal Monitoring Program Fiscal Year: Name of Project/Site: (TIN #) Address: (city) (state) (zip code) Project Director/Site Manager: Geographic Area Served: (county) Project/Site

EGYPTIAN AREA AGENCY ON AGING Fiscal Monitoring Program Fiscal Year: Name of Project/Site: (TIN #) Address: (city) (state) (zip code) Project Director/Site Manager: Geographic Area Served: (county) Project/Site

Section II Payroll. Kennard ISD Page 1

Section II Payroll Kennard ISD Page 1 This page left blank intentionally. Kennard ISD Page 2 Table of Contents Timekeeping Procedures... 4 A. Reporting Absences... 4 B. Supplemental Pay Procedure... 5

Section II Payroll Kennard ISD Page 1 This page left blank intentionally. Kennard ISD Page 2 Table of Contents Timekeeping Procedures... 4 A. Reporting Absences... 4 B. Supplemental Pay Procedure... 5

Ambulance Contract Billing Report October 12, 2016 KEY CONTROL FINDING RECOMMENDATION STATUS The City should:

Ambulance Contract Billing Report October 12, 2016 The City should: General Recordkeeping Inconsistencies exist in the basic recordkeeping related to ambulance calls. Continue with the implementation of

Ambulance Contract Billing Report October 12, 2016 The City should: General Recordkeeping Inconsistencies exist in the basic recordkeeping related to ambulance calls. Continue with the implementation of

Payroll and Business Services

1) Roles and Responsibilities As a Kronos Manager you will be responsible for reviewing and approving your employee's timecards assigned to your school or department. Supervisor Level: Compliance with

1) Roles and Responsibilities As a Kronos Manager you will be responsible for reviewing and approving your employee's timecards assigned to your school or department. Supervisor Level: Compliance with

CITY OF CARROLLTON ADMINISTRATIVE DIRECTIVES. SECTION: Workforce Services REFERENCE NO: CATEGORY: Compensation EFFECTIVE DATE:

CITY OF CARROLLTON ADMINISTRATIVE DIRECTIVES SECTION: Workforce Services REFERENCE NO: 1.7.12 CATEGORY: Compensation EFFECTIVE DATE: 04-25-94 TOPIC: Payroll/Time Keeping/Direct Deposit APPROVED REVISION

CITY OF CARROLLTON ADMINISTRATIVE DIRECTIVES SECTION: Workforce Services REFERENCE NO: 1.7.12 CATEGORY: Compensation EFFECTIVE DATE: 04-25-94 TOPIC: Payroll/Time Keeping/Direct Deposit APPROVED REVISION

A. Dual employment only applies to those employees who hold full-time equivalent (FTE) positions within the University

positions within the University") Policy Title: Dual and Outside Employment Policy Number: FAST-HREO 217 Created: May 2015 Policy(ies) Superseded: 1232; HREO- 132 Revised: July 2012, September 2014, May 2015, August 2016 Policy Management

Policy Title: Dual and Outside Employment Policy Number: FAST-HREO 217 Created: May 2015 Policy(ies) Superseded: 1232; HREO- 132 Revised: July 2012, September 2014, May 2015, August 2016 Policy Management

General Government and Gainesville Regional Utilities Vendor Master File Audit

FINAL AUDIT REPORT A Report to the City Commission General Government and Gainesville Regional Utilities Vendor Master File Audit Mayor Lauren Poe Mayor Pro-Tem Adrian Hayes-Santos Commission Members David

FINAL AUDIT REPORT A Report to the City Commission General Government and Gainesville Regional Utilities Vendor Master File Audit Mayor Lauren Poe Mayor Pro-Tem Adrian Hayes-Santos Commission Members David

STATE OF NORTH CAROLINA

STATE OF NORTH CAROLINA DEPARTMENT OF PUBLIC SAFETY DIVISION OF ADULT CORRECTION AND JUVENILE JUSTICE SHIFT PREMIUM PAY FINANCIAL RELATED AUDIT NOVEMBER 2013 OFFICE OF THE STATE AUDITOR BETH A. WOOD, CPA

STATE OF NORTH CAROLINA DEPARTMENT OF PUBLIC SAFETY DIVISION OF ADULT CORRECTION AND JUVENILE JUSTICE SHIFT PREMIUM PAY FINANCIAL RELATED AUDIT NOVEMBER 2013 OFFICE OF THE STATE AUDITOR BETH A. WOOD, CPA

Time of Hours per Pay Hours per Employment Period Accrued Year Accrued. 0-6 yrs yrs 1 day 14 yrs yrs 1 day + 6.

ARTICLE 17 - LEAVES OF ABSENCE Section 1. Requesting Leaves of Absence All requests for leaves of absence with or without pay shall be made to the employee s Director for approval on forms approved by

ARTICLE 17 - LEAVES OF ABSENCE Section 1. Requesting Leaves of Absence All requests for leaves of absence with or without pay shall be made to the employee s Director for approval on forms approved by

EMPLOYMENT AUDIT CHECKLIST

EMPLOYMENT AUDIT CHECKLIST I. Classification of Staff Employee Exempt (from minimum wage and overtime) 1. Must be Salaried (Same rate of pay each pay period regardless of the number of hours worked); and

EMPLOYMENT AUDIT CHECKLIST I. Classification of Staff Employee Exempt (from minimum wage and overtime) 1. Must be Salaried (Same rate of pay each pay period regardless of the number of hours worked); and

Internal Audit Report. Jackson County Payroll Testing Special Pay Codes June 13, 2011

Internal Audit Report Jackson County Payroll Testing Special Pay Codes 2010-11 June 13, 2011 Presented To The Jackson County Board of Commissioners By The Internal Audit Program Audit Team Debbie Taylor,

Internal Audit Report Jackson County Payroll Testing Special Pay Codes 2010-11 June 13, 2011 Presented To The Jackson County Board of Commissioners By The Internal Audit Program Audit Team Debbie Taylor,

DEPARTMENT OF BIOLOGY AUDIT OF ALLEGATIONS OF MISREPORTING PAYROLL HOURS

DEPARTMENT OF BIOLOGY AUDIT OF ALLEGATIONS OF MISREPORTING PAYROLL HOURS THE UNIVERSITY OF NEW MEXICO Report 2006-05 July 5, 2006 Raymond Sanchez, Chair Don Chalmers, Vice Chair John M. "Mel" Eaves Audit

DEPARTMENT OF BIOLOGY AUDIT OF ALLEGATIONS OF MISREPORTING PAYROLL HOURS THE UNIVERSITY OF NEW MEXICO Report 2006-05 July 5, 2006 Raymond Sanchez, Chair Don Chalmers, Vice Chair John M. "Mel" Eaves Audit

INTERNAL CONTROLS MANUAL DICKSON COUNTY SCHOOLS DANNY L. WEEKS, ED.D. DIRECTOR OF SCHOOLS LINDA FRAZIER BUSINESS MANAGER JUNE 2016

1 INTERNAL CONTROLS MANUAL DICKSON COUNTY SCHOOLS DANNY L. WEEKS, ED.D. DIRECTOR OF SCHOOLS LINDA FRAZIER BUSINESS MANAGER JUNE 2016 2 Table of Contents Introduction...3 Internal Controls Questionnaire...4

1 INTERNAL CONTROLS MANUAL DICKSON COUNTY SCHOOLS DANNY L. WEEKS, ED.D. DIRECTOR OF SCHOOLS LINDA FRAZIER BUSINESS MANAGER JUNE 2016 2 Table of Contents Introduction...3 Internal Controls Questionnaire...4

All A&M System employees will access Workday through Single Sign On (SSO). Workday Home Page

. Workday Home Page") Workday Basics & FAQ What Is Workday? Workday is a cloud-based system that The Texas A&M University System uses to manage the Human Resources, Benefits and Payroll functions for all employees. Workday

Workday Basics & FAQ What Is Workday? Workday is a cloud-based system that The Texas A&M University System uses to manage the Human Resources, Benefits and Payroll functions for all employees. Workday

Mountain Song Community School Recruitment and Hiring Policy

Mountain Song Community School Recruitment and Hiring Policy Policy/Procedure This policy provides an overview of MSCS s hiring process. Hiring Personnel Hiring Official: When hiring for a position on

Mountain Song Community School Recruitment and Hiring Policy Policy/Procedure This policy provides an overview of MSCS s hiring process. Hiring Personnel Hiring Official: When hiring for a position on

KRONOS Workforce Central Suite

Denver Public Schools KRONOS Workforce Central Suite Principals / Department Managers Guide for Kronos Version 6.3 Roles and Responsibilities As a Kronos Manager you will be responsible for reviewing and

Denver Public Schools KRONOS Workforce Central Suite Principals / Department Managers Guide for Kronos Version 6.3 Roles and Responsibilities As a Kronos Manager you will be responsible for reviewing and

STATE OF NORTH CAROLINA

STATE OF NORTH CAROLINA WINSTON-SALEM STATE UNIVERSITY FISCAL CONTROL AUDIT OFFICE OF THE STATE AUDITOR BETH A. WOOD, CPA STATE AUDITOR WINSTON-SALEM STATE UNIVERSITY FISCAL CONTROL AUDIT Beth A. Wood,

STATE OF NORTH CAROLINA WINSTON-SALEM STATE UNIVERSITY FISCAL CONTROL AUDIT OFFICE OF THE STATE AUDITOR BETH A. WOOD, CPA STATE AUDITOR WINSTON-SALEM STATE UNIVERSITY FISCAL CONTROL AUDIT Beth A. Wood,

Richmond City Department of Justice Services Truancy and Diversion

REPORT # 2012-05 AUDIT Of the Richmond City Department of Justice Services Truancy and Diversion TABLE OF CONTENTS Executive Summary..... i Comprehensive List of Recommendations iii Introduction...........

REPORT # 2012-05 AUDIT Of the Richmond City Department of Justice Services Truancy and Diversion TABLE OF CONTENTS Executive Summary..... i Comprehensive List of Recommendations iii Introduction...........

Total Rewards: Compensation & Hours of Work for Employees of the College

POLICY: 6Hx28:3C-01 Responsible Executive: Vice President, Organizational Development and Human Resources Policy Contacts: Director, Human Resources and Compliance Programs Specific Authority: 1001.64,

POLICY: 6Hx28:3C-01 Responsible Executive: Vice President, Organizational Development and Human Resources Policy Contacts: Director, Human Resources and Compliance Programs Specific Authority: 1001.64,

Consulting Services Floyd Curl Dr. MC#797 4 San Antonio, Texas Fax:

San Antonio Internal Audit & Consulting Services Internal Audit & Consulting Services 7703 Floyd Curl Dr. MC#797 4 San Antonio, Texas 78229-3900 210-567-2370 Fax: 210-567-2373 www.uthscsa.edu Date: July

San Antonio Internal Audit & Consulting Services Internal Audit & Consulting Services 7703 Floyd Curl Dr. MC#797 4 San Antonio, Texas 78229-3900 210-567-2370 Fax: 210-567-2373 www.uthscsa.edu Date: July

Process Owner: Dennis Cultice. Revision: 1 Effective Date: 01/01/2016 Title: Holiday, Vacation and PTO Policy Page 1 of 9

Title: Holiday, Vacation and PTO Policy Page 1 of 9 Scope: This policy applies to all Team Members in the U.S. other than Puerto Rico-based and Dover Union Team Members. Team Members regularly scheduled

Title: Holiday, Vacation and PTO Policy Page 1 of 9 Scope: This policy applies to all Team Members in the U.S. other than Puerto Rico-based and Dover Union Team Members. Team Members regularly scheduled

Hurricane Harvey Payroll

Hurricane Harvey Payroll Payroll Internal Audit Lyndsey Davis, Brooke Jacobson, Haley Moreno February 9, 2018 TABLE OF CONTENTS Executive Summary 2 Audit Scope and Procedures 2 Observations and Findings

Hurricane Harvey Payroll Payroll Internal Audit Lyndsey Davis, Brooke Jacobson, Haley Moreno February 9, 2018 TABLE OF CONTENTS Executive Summary 2 Audit Scope and Procedures 2 Observations and Findings

UNIVERSITY OF CALIFORNIA, SAN FRANCISCO AUDIT AND ADVISORY SERVICES

, SAN FRANCISCO AUDIT AND ADVISORY SERVICES UCSF Health Sterile Processing Department Time Reporting and Related Payroll Activities Project #16-046 September 2015 University of California San Francisco

, SAN FRANCISCO AUDIT AND ADVISORY SERVICES UCSF Health Sterile Processing Department Time Reporting and Related Payroll Activities Project #16-046 September 2015 University of California San Francisco

Prince William County, Virginia. Internal Audit of Fleet Management Division

Prince William County, Virginia Internal Audit of Fleet Management Division Table of Contents Transmittal Letter... 1 Executive Summary... 2-5 Background... 6-7 Objectives and Approach... 8 Issues Matrix...

Prince William County, Virginia Internal Audit of Fleet Management Division Table of Contents Transmittal Letter... 1 Executive Summary... 2-5 Background... 6-7 Objectives and Approach... 8 Issues Matrix...

Administering Labor Expenditures on Sponsored Projects

Administering Labor Expenditures on Sponsored Projects Office of Sponsored Programs 1 Overview 2 Position Types Permanent An employee hired to fill an authorized position on a full-time or part-time basis

Administering Labor Expenditures on Sponsored Projects Office of Sponsored Programs 1 Overview 2 Position Types Permanent An employee hired to fill an authorized position on a full-time or part-time basis

DOWNINGTOWN AREA SCHOOL DISTRICT SCHOOL BOARD POLICY SECTION: SUPPORT EMPLOYEES

0 ADMINISTRATIVE GUIDELINES FOR. TIME CLOCK I. INTRODUCTION The Downingtown Area School District (District) utilizes an electronic time tracking system. The electronic time tracking system will enable

0 ADMINISTRATIVE GUIDELINES FOR. TIME CLOCK I. INTRODUCTION The Downingtown Area School District (District) utilizes an electronic time tracking system. The electronic time tracking system will enable

Comptroller of the Treasury Central Payroll Bureau

Audit Report Comptroller of the Treasury Central Payroll Bureau June 2006 OFFICE OF LEGISLATIVE AUDITS DEPARTMENT OF LEGISLATIVE SERVICES MARYLAND GENERAL ASSEMBLY This report and any related follow-up

Audit Report Comptroller of the Treasury Central Payroll Bureau June 2006 OFFICE OF LEGISLATIVE AUDITS DEPARTMENT OF LEGISLATIVE SERVICES MARYLAND GENERAL ASSEMBLY This report and any related follow-up

Seattle Police Department Overtime Controls Audit

Office of City Auditor 700 Fifth Avenue, Suite 2410 Seattle WA 98124-4729 Ph: 206-233-3801 www.seattle.gov/cityauditor Seattle Police Department Overtime Controls Audit CC Image courtesy of donte on Flickr

Office of City Auditor 700 Fifth Avenue, Suite 2410 Seattle WA 98124-4729 Ph: 206-233-3801 www.seattle.gov/cityauditor Seattle Police Department Overtime Controls Audit CC Image courtesy of donte on Flickr

Montgomery I.S.D Payroll Procedures Manual

Montgomery I.S.D. 2016-2017 Payroll Procedures Manual Table of Contents SECTION A GENERAL INFORMATION 01. INTRODUCTION... 2 02. LOCATION........ 2 03. PAYROLL CONTACT INFORMATION... 2 04. PAY DATES...

Montgomery I.S.D. 2016-2017 Payroll Procedures Manual Table of Contents SECTION A GENERAL INFORMATION 01. INTRODUCTION... 2 02. LOCATION........ 2 03. PAYROLL CONTACT INFORMATION... 2 04. PAY DATES...

Northern Oklahoma College Tonkawa, Oklahoma

Northern Oklahoma College Tonkawa, Oklahoma Internal Audit Report INTERNAL AUDIT REPORT Table of Contents Section Page Executive Summary of Procedures Performed and Results Thereof... I 1 Expenditures...

Northern Oklahoma College Tonkawa, Oklahoma Internal Audit Report INTERNAL AUDIT REPORT Table of Contents Section Page Executive Summary of Procedures Performed and Results Thereof... I 1 Expenditures...

Department of Labor Unpaid Back Wages

Department of Labor Unpaid Back Wages Analysis January 2013 through December 2014 OPA Report No. 15-04 June 2015 Department of Labor Unpaid Back Wages Analysis January 2013 through December 2014 OPA Report

Department of Labor Unpaid Back Wages Analysis January 2013 through December 2014 OPA Report No. 15-04 June 2015 Department of Labor Unpaid Back Wages Analysis January 2013 through December 2014 OPA Report

HERNANDO COUNTY Board of County Commissioners

HERNANDO COUNTY Board of County Commissioners Policy Title: Effective Date: February 11, 2014 Pay Plan and Employee Compensation Policy Revision Date(s): March 12, 2013 October 16, 2013 Latest Review:

HERNANDO COUNTY Board of County Commissioners Policy Title: Effective Date: February 11, 2014 Pay Plan and Employee Compensation Policy Revision Date(s): March 12, 2013 October 16, 2013 Latest Review:

Angelo State University Operating Policy and Procedure

Angelo State University Operating Policy and Procedure OP 52.31: Multiple State Employment and Other Outside Employment DATE: January 23, 2017 PURPOSE: REVIEW: The purpose of this OP is to establish policy

Angelo State University Operating Policy and Procedure OP 52.31: Multiple State Employment and Other Outside Employment DATE: January 23, 2017 PURPOSE: REVIEW: The purpose of this OP is to establish policy

Christopher Newport University Policy and Procedures

Policy: Student Employment Policy Number: 5005 Last Review completed: Executive Oversight: Chief of Staff and Executive Vice President Contact Offices: Office of Human Resources (HR) classification and

Policy: Student Employment Policy Number: 5005 Last Review completed: Executive Oversight: Chief of Staff and Executive Vice President Contact Offices: Office of Human Resources (HR) classification and

For Self-Directed Services under the. Acquired Brain Injury Medicaid Waiver Program

For Self-Directed Services under the Acquired Brain Injury Medicaid Waiver Program Information provided to the Participant / Employer by the Financial Management Services Agent 2012 Copyright Allied Community

For Self-Directed Services under the Acquired Brain Injury Medicaid Waiver Program Information provided to the Participant / Employer by the Financial Management Services Agent 2012 Copyright Allied Community

Results in Brief. Audit of WMATA s Employee Separation Process. OIG January 18, 2019

All publicly available OIG reports ( Results in Brief OIG 19-07 January 18, 2019 Why We Did This Review The Department of Human Resources (HR) is organized to reflect six functional areas of responsibility:

All publicly available OIG reports ( Results in Brief OIG 19-07 January 18, 2019 Why We Did This Review The Department of Human Resources (HR) is organized to reflect six functional areas of responsibility:

PSAB SUPPLEMENT 14 PAYROLL

PSAB SUPPLEMENT 14 PAYROLL Claire Cieremans Chief Finance Officer Los Lunas Schools ccieremans@llschools.net 505-866-8242 Introduction and Payroll Highlights Los Lunas Schools Introduction of Supplement

PSAB SUPPLEMENT 14 PAYROLL Claire Cieremans Chief Finance Officer Los Lunas Schools ccieremans@llschools.net 505-866-8242 Introduction and Payroll Highlights Los Lunas Schools Introduction of Supplement

Payroll Services General Information

Payroll Services General Information Pay Day The Districts Annualized Non-Exempt and Exempt staff receives pay on a monthly basis. The Hourly and Substitute staff receives pay on a Semi-monthly basis.

Payroll Services General Information Pay Day The Districts Annualized Non-Exempt and Exempt staff receives pay on a monthly basis. The Hourly and Substitute staff receives pay on a Semi-monthly basis.

Payroll Services Internal Audit Report January 30, 2018

January 30, 2018 Linda J. Lindsey, CPA, CGAP, Senior Director Alpa H. Vyas, CIA, CRMA, Internal Auditor Table of Contents Page Number EXECUTIVE SUMMARY 1 BACKGROUND 2 OBJECTIVE, SCOPE, AND METHODOLOGY

January 30, 2018 Linda J. Lindsey, CPA, CGAP, Senior Director Alpa H. Vyas, CIA, CRMA, Internal Auditor Table of Contents Page Number EXECUTIVE SUMMARY 1 BACKGROUND 2 OBJECTIVE, SCOPE, AND METHODOLOGY

Introduction. June 12, Stacey Adler, Superintendent Mono County Office of Education 451 Sierra Park Rd. Mammoth Lakes, CA 93546

June 12, 2018 Stacey Adler, Superintendent Mono County Office of Education 451 Sierra Park Rd. Mammoth Lakes, CA 93546 Dear Superintendent Adler: The purpose of this management letter is to provide the

June 12, 2018 Stacey Adler, Superintendent Mono County Office of Education 451 Sierra Park Rd. Mammoth Lakes, CA 93546 Dear Superintendent Adler: The purpose of this management letter is to provide the

COMPENSATION AND BENEFITS SALARIES AND WAGES

The Chancellor shall recommend an annual compensation plan for all College District employees. The compensation plan may include wage and salary structures, stipends, benefits, and incentives. The recommended

The Chancellor shall recommend an annual compensation plan for all College District employees. The compensation plan may include wage and salary structures, stipends, benefits, and incentives. The recommended

9/13/2017 CHA-CHING! PAYROLL CONTROLS THAT PAY OFF PERSONAL INTRODUCTION. Personal Introduction. Melinda Stinnett, CPA, CIA Managing Director

CHA-CHING! PAYROLL CONTROLS THAT PAY OFF Melinda Stinnett, CPA, CIA Managing Director September 15, 2017 1 PERSONAL INTRODUCTION Professional Bachelor s Degree (Accounting) Oklahoma State University Public

CHA-CHING! PAYROLL CONTROLS THAT PAY OFF Melinda Stinnett, CPA, CIA Managing Director September 15, 2017 1 PERSONAL INTRODUCTION Professional Bachelor s Degree (Accounting) Oklahoma State University Public

Islip Union Free School District

DIVISION OF LOCAL GOVERNMENT AND SCHOOL ACCOUNTABILITY REPORT OF EXAMINATION 2017M-291 Islip Union Free School District Payroll FEBRUARY 2018 Contents Report Highlights............................. 1 Payroll...................................

DIVISION OF LOCAL GOVERNMENT AND SCHOOL ACCOUNTABILITY REPORT OF EXAMINATION 2017M-291 Islip Union Free School District Payroll FEBRUARY 2018 Contents Report Highlights............................. 1 Payroll...................................

PSAB Supplement 14 Payroll

PSAB Supplement 14 Payroll MANUAL OF PROCEDURES PSAB SUPPLEMENT 14 PAYROLL TABLE OF CONTENTS INTRODUCTION... 1 PURPOSE... 1 LOCAL POLICIES AND CONTROLS... 2 DIVISION OF DUTIES... 2 PAYROLL AND HUMAN RESOURCE

PSAB Supplement 14 Payroll MANUAL OF PROCEDURES PSAB SUPPLEMENT 14 PAYROLL TABLE OF CONTENTS INTRODUCTION... 1 PURPOSE... 1 LOCAL POLICIES AND CONTROLS... 2 DIVISION OF DUTIES... 2 PAYROLL AND HUMAN RESOURCE

SECTION 9. PAYROLL AND ONLINE TIMESHEETS

PAYROLL PREREQUISITE CHECKLIST THE FOLLOWING ITEMS/INFORMATION ARE REQUIRED PRIOR TO INPUTTING PAYROLL ON THE SYSTEM ITEM DESCRIPTION PI ROLE USER ROLE The RCUH Timesheet PI/Designee must templates are

PAYROLL PREREQUISITE CHECKLIST THE FOLLOWING ITEMS/INFORMATION ARE REQUIRED PRIOR TO INPUTTING PAYROLL ON THE SYSTEM ITEM DESCRIPTION PI ROLE USER ROLE The RCUH Timesheet PI/Designee must templates are

Department of Biology

THE UNIVERSITY OF TEXAS-PAN AMERICAN OFFICE OF AUDITS & CONSULTING SERVICES Department of Biology Report No. 14-10 OFFICE OF INTERNAL AUDITS THE UNIVERSITY OF TEXAS - PAN AMERICAN 1201 West University

THE UNIVERSITY OF TEXAS-PAN AMERICAN OFFICE OF AUDITS & CONSULTING SERVICES Department of Biology Report No. 14-10 OFFICE OF INTERNAL AUDITS THE UNIVERSITY OF TEXAS - PAN AMERICAN 1201 West University

Annual HR Department Calendar

Sample Annual Calendar It is important for an administrator to know when human resource responsibilities need to be performed in order to plan for the daily, weekly, monthly, or annual demands that will

Sample Annual Calendar It is important for an administrator to know when human resource responsibilities need to be performed in order to plan for the daily, weekly, monthly, or annual demands that will

Purpose To establish the proper classification of faculty and staff positions.

300.1 Position Classifications Purpose To establish the proper classification of faculty and staff positions. Definitions A Position Classification refers to the description of a position in terms of duties,

300.1 Position Classifications Purpose To establish the proper classification of faculty and staff positions. Definitions A Position Classification refers to the description of a position in terms of duties,

1.2. The School Board shall annually approve salaries for administrators and for certificated employees.

1. Professional Staff Salary Schedules 1.1. Generally, the Fauquier County School Board desires to adopt annually a Teacher Pay Plan that will attract outstanding teachers and will retain those teachers

1. Professional Staff Salary Schedules 1.1. Generally, the Fauquier County School Board desires to adopt annually a Teacher Pay Plan that will attract outstanding teachers and will retain those teachers

NSU FLSA Guidelines, Information and Tips for Supervisors

NSU FLSA Guidelines, Information and Tips for Supervisors As a supervisor, you should have received copies of the notification letters that were sent to those employees transitioning from exempt to non-exempt

NSU FLSA Guidelines, Information and Tips for Supervisors As a supervisor, you should have received copies of the notification letters that were sent to those employees transitioning from exempt to non-exempt

Schedules / Calendars

Payroll Session Secretary Training July 16, 2013 July 18, 2013 Schedules / Calendars Color copies will be provided to you today FY14 Calendars (July June) FY14 Semi-Monthly Payroll Schedule FY14 Pay Dates

Payroll Session Secretary Training July 16, 2013 July 18, 2013 Schedules / Calendars Color copies will be provided to you today FY14 Calendars (July June) FY14 Semi-Monthly Payroll Schedule FY14 Pay Dates

VI. Personnel. A. Supervisors Responsibilities in Personnel Management. B. Personnel Management Where to go for Help

VI. Personnel A. Supervisors Responsibilities in Personnel Management NOTE: Sample personnel policies are available on the SWCD Intranet (from the home page, click on Handbooks link, then Personnel Handbook).

VI. Personnel A. Supervisors Responsibilities in Personnel Management NOTE: Sample personnel policies are available on the SWCD Intranet (from the home page, click on Handbooks link, then Personnel Handbook).

PAYROLL CHECK-OFF AUDIT

PAYROLL CHECK-OFF AUDIT Prepared By: Craig Hametner, CPA, CIA, CMA, CFE City Auditor Randall Mahaffey, CIA, CGAP Senior Audit Analyst Steve Culpepper, CPA, CIA Audit Analyst Jed Johnson Audit Analyst Elizabeth

PAYROLL CHECK-OFF AUDIT Prepared By: Craig Hametner, CPA, CIA, CMA, CFE City Auditor Randall Mahaffey, CIA, CGAP Senior Audit Analyst Steve Culpepper, CPA, CIA Audit Analyst Jed Johnson Audit Analyst Elizabeth

OFFICE OF THE AUDITOR

OFFICE OF THE AUDITOR SELECT PAYROLL TRANSACTIONS PARKS AND RECREATION PERFORMANCE AUDIT NOVEMBER 2008 Dennis J. Gallagher Auditor Dennis J. Gallagher Auditor City and County of Denver 201 West Colfax

OFFICE OF THE AUDITOR SELECT PAYROLL TRANSACTIONS PARKS AND RECREATION PERFORMANCE AUDIT NOVEMBER 2008 Dennis J. Gallagher Auditor Dennis J. Gallagher Auditor City and County of Denver 201 West Colfax

Oklahoma State University Policy and Procedures

Oklahoma State University Policy and Procedures MONTHLY TIME & EFFORT CONFIRMATION In Compliance with OMB Circular A-21 3-0321 BUSINESS & EXTERNAL RELATIONS Personnel Services May 1998 INTRODUCTION AND

Oklahoma State University Policy and Procedures MONTHLY TIME & EFFORT CONFIRMATION In Compliance with OMB Circular A-21 3-0321 BUSINESS & EXTERNAL RELATIONS Personnel Services May 1998 INTRODUCTION AND

University Community (faculty, staff and students)

") University Community (faculty, staff and students) SUBJECT (R*) EFFECTIVE DATE (R*) POLICY NUMBER (O*) Effort Reporting and Certification February 11, 2004 2330.020 POLICY STATEMENT (R*) An after-the-fact

University Community (faculty, staff and students) SUBJECT (R*) EFFECTIVE DATE (R*) POLICY NUMBER (O*) Effort Reporting and Certification February 11, 2004 2330.020 POLICY STATEMENT (R*) An after-the-fact

March 1, Ms. Selena Cuffee-Glenn Chief Administrative Officer

March 1, 2016 Ms. Selena Cuffee-Glenn Chief Administrative Officer The Office of the Inspector General (OIG) has completed an investigation of travel, training, and education expenditures of an employee

March 1, 2016 Ms. Selena Cuffee-Glenn Chief Administrative Officer The Office of the Inspector General (OIG) has completed an investigation of travel, training, and education expenditures of an employee

Dayton ISD. Time Clock Policy and Guidelines

Dayton ISD Time Clock Policy and Guidelines Table of Contents 1. INTRODUCTION 2. OFFICIAL TIME OF RECORD 3. EMPLOYEE TIME REPORTS 4. DISD ID NUMBER 5. CLOCK LOCATIONS 6. DAILY CLOCK IN/OUT REQUIREMENTS

Dayton ISD Time Clock Policy and Guidelines Table of Contents 1. INTRODUCTION 2. OFFICIAL TIME OF RECORD 3. EMPLOYEE TIME REPORTS 4. DISD ID NUMBER 5. CLOCK LOCATIONS 6. DAILY CLOCK IN/OUT REQUIREMENTS

"Base Daily Hours" Average hours that an employee will work in a normal workday.

2490 Payroll PURPOSE: To establish the College s payroll procedure regarding pay schedules, classification, absences and to comply with the requirements of the Fair Labor Standards Act. DEFINITIONS "Base

2490 Payroll PURPOSE: To establish the College s payroll procedure regarding pay schedules, classification, absences and to comply with the requirements of the Fair Labor Standards Act. DEFINITIONS "Base

Report No. D February 9, Controls Over Time and Attendance Reporting at the National Geospatial-Intelligence Agency

Report No. D-2009-051 February 9, 2009 Controls Over Time and Attendance Reporting at the National Geospatial-Intelligence Agency Report Documentation Page Form Approved OMB No. 0704-0188 Public reporting

Report No. D-2009-051 February 9, 2009 Controls Over Time and Attendance Reporting at the National Geospatial-Intelligence Agency Report Documentation Page Form Approved OMB No. 0704-0188 Public reporting

BORGER ISD FAIR LABOR STANDARDS ACT BULLETIN FLSA. Personnel Services. Excellence Begins Now Borger ISD

BORGER ISD FAIR LABOR STANDARDS ACT BULLETIN FLSA Personnel Services Excellence Begins Now Borger ISD www.borgerisd.net 1 DEFINITIONS BREAKS WAGE and HOUR GUIDLINES Breaks are not required by Federal,

BORGER ISD FAIR LABOR STANDARDS ACT BULLETIN FLSA Personnel Services Excellence Begins Now Borger ISD www.borgerisd.net 1 DEFINITIONS BREAKS WAGE and HOUR GUIDLINES Breaks are not required by Federal,

[HR / WORKFORCE ADMINISTRATION FACT SHEET]

![[HR / WORKFORCE ADMINISTRATION FACT SHEET]](/thumbs/72/66311039.jpg "[HR / WORKFORCE ADMINISTRATION FACT SHEET]") UCPath is a system-wide project launched by the University of California to modernize its current payroll system. UCPath introduces new, modern technology on the PeopleSoft platform that will align payroll,

UCPath is a system-wide project launched by the University of California to modernize its current payroll system. UCPath introduces new, modern technology on the PeopleSoft platform that will align payroll,

Sonoma County. Internal Audit Report. Auditor Controller Treasurer Tax Collector. Sonoma County Payroll Process

For the Period: July 1, 2011 to June 30, 2015 Sonoma County Auditor Controller Treasurer Tax Collector Internal Audit Report Engagement No: 4050 Report Date: May 31, 2016 Donna M. Dunk, CPA Auditor Controller

For the Period: July 1, 2011 to June 30, 2015 Sonoma County Auditor Controller Treasurer Tax Collector Internal Audit Report Engagement No: 4050 Report Date: May 31, 2016 Donna M. Dunk, CPA Auditor Controller

Review of Water and Wastewater Services Procurement Card Transactions

Exhibit 1 Review of Water and Wastewater Services Robert Melton, CPA, CIA, CFE, CIG County Auditor Audit Conducted by: Jed Shank, CPA, Audit Manager Dirk Hansen, CPA, Audit Supervisor Bryan Thabit, CPA,

Exhibit 1 Review of Water and Wastewater Services Robert Melton, CPA, CIA, CFE, CIG County Auditor Audit Conducted by: Jed Shank, CPA, Audit Manager Dirk Hansen, CPA, Audit Supervisor Bryan Thabit, CPA,

Guide to Internal Controls

Guide to Internal Controls Updated January 2017 The Guide to Internal Controls was developed to help you establish and maintain effective internal controls in your department/division. This guide summarizes

Guide to Internal Controls Updated January 2017 The Guide to Internal Controls was developed to help you establish and maintain effective internal controls in your department/division. This guide summarizes

Mecklenburg County Department of Internal Audit

Mecklenburg County Department of Internal Audit Department of Social Services Mecklenburg Transportation System Time Reporting Investigation Report 1288 July 18, 2012 Internal Audit s Mission Internal

Mecklenburg County Department of Internal Audit Department of Social Services Mecklenburg Transportation System Time Reporting Investigation Report 1288 July 18, 2012 Internal Audit s Mission Internal

Compensation Policy and Procedures for Grants and Contracts. Responsible Office Contact:

Policy Number and Title: Approval Authority: 200.203 Compensation Policy and President Date Effective: July 1, 2015 Responsible Office: Accounting Responsible Office Contact: Vice President for Business

Policy Number and Title: Approval Authority: 200.203 Compensation Policy and President Date Effective: July 1, 2015 Responsible Office: Accounting Responsible Office Contact: Vice President for Business

Fair Labor Standards Act (FLSA) Overtime Revisions. Supervisor Training

Overtime Revisions. Supervisor Training") Fair Labor Standards Act (FLSA) Overtime Revisions Supervisor Training Questions to Answer What is the FLSA? What are the changes and why are they occurring? When are the changes effective? Who is affected

Fair Labor Standards Act (FLSA) Overtime Revisions Supervisor Training Questions to Answer What is the FLSA? What are the changes and why are they occurring? When are the changes effective? Who is affected

City Property Damage Claims Processing and Collection

City Property Damage Claims Processing and Collection March 30, 2016 Report 201602 City Auditor: Jed Johnson, CIA, CGAP Major Contributor: Marla Hamilton Staff Auditor Jonna Murphy Staff Auditor Contents

City Property Damage Claims Processing and Collection March 30, 2016 Report 201602 City Auditor: Jed Johnson, CIA, CGAP Major Contributor: Marla Hamilton Staff Auditor Jonna Murphy Staff Auditor Contents

University Policy TERMINATION

University Policy 200.19 TERMINATION Responsible Administrator: Office of the President Responsible Office: Office of Human Resources Originally Issued: August 2006 Revision Date: Authority: Office of

University Policy 200.19 TERMINATION Responsible Administrator: Office of the President Responsible Office: Office of Human Resources Originally Issued: August 2006 Revision Date: Authority: Office of

THE LANGUAGE USED IN THIS DOCUMENT DOES NOT CREATE AN EMPLOYMENT CONTRACT BETWEEN THE EMPLOYEE AND COASTAL CAROLINA UNIVERSITY

Policy Title: Minimum Wage and Overtime Policy Number: FAST-HREO 216 Created: August 2011 Policies Superseded: 1229; HREO-129 Revised: July 2014, June 2015, December 2016, April 2018 Policy Management

Policy Title: Minimum Wage and Overtime Policy Number: FAST-HREO 216 Created: August 2011 Policies Superseded: 1229; HREO-129 Revised: July 2014, June 2015, December 2016, April 2018 Policy Management

The university shall pay employees on a scheduled basis for work performed as

Name of Policy: Payroll Policy Number: 3364-40-09 Approving Officer: Executive Vice President of Finance and Administration / CFO Responsible Agent: Controller Scope: All University of Toledo Campuses

Name of Policy: Payroll Policy Number: 3364-40-09 Approving Officer: Executive Vice President of Finance and Administration / CFO Responsible Agent: Controller Scope: All University of Toledo Campuses

Woodland Equipment Inc. Employee Vacation Policy

Woodland Equipment Inc. Employee Vacation Policy Policy Number: Vac0001.1 Revision Number: 2016-001 Replaces: Vac0001 Effective Date: January 1, 2016 Date Last Reviewed: December 2015 Next Review Date:

Woodland Equipment Inc. Employee Vacation Policy Policy Number: Vac0001.1 Revision Number: 2016-001 Replaces: Vac0001 Effective Date: January 1, 2016 Date Last Reviewed: December 2015 Next Review Date:

LOUISIANA COMMUNITY & TECHNICAL COLLEGE SYSTEM Policy # Title: Recoupment of Overpayments

LOUISIANA COMMUNITY & TECHNICAL COLLEGE SYSTEM Policy # 5.024 Title: Recoupment of Overpayments Authority: LCTCS Board Action Original Adoption: May 11, 2005 Effective Date: April 10, 2013 Last Revision:

LOUISIANA COMMUNITY & TECHNICAL COLLEGE SYSTEM Policy # 5.024 Title: Recoupment of Overpayments Authority: LCTCS Board Action Original Adoption: May 11, 2005 Effective Date: April 10, 2013 Last Revision:

Campus Overtime Audit

Campus Overtime Audit Internal Audit Report No. I2016-109b May 5, 2016 Prepared By Helen Templin, Senior Auditor Reviewed By Evans Owalla, Principal Auditor Approved By Mike Bathke, Director UNIVERSITY

Campus Overtime Audit Internal Audit Report No. I2016-109b May 5, 2016 Prepared By Helen Templin, Senior Auditor Reviewed By Evans Owalla, Principal Auditor Approved By Mike Bathke, Director UNIVERSITY