Office of the City Auditor. Committed to increasing government efficiency, effectiveness, accountability and transparency

|

|

|

- Marilynn Fields

- 6 years ago

- Views:

Transcription

1 Office of the City Auditor Committed to increasing government efficiency, effectiveness, accountability and transparency Issue Date:

2 TABLE OF CONTENTS Executive Summary... ii Recommendation... iv Background...1 Findings & Recommendations...3 Objectives, Scope, and Methodology... Appendix A Management Response... Appendix B

3

4

5 Comprehensive List of Recommendations # PAGE 1 Director of Procurement Services needs to revise the existing contract administration policies and procedures to specifically include administration of citywide contracts Director of Procurement Services needs to provide training to applicable employees in City Departments for the revised contract administration policies and procedures CAO needs to establish and implement a standard citywide process for verifying and maintaining background checks for temporary services personnel Director of Public Works needs to discontinue using the signature stamp for the approval of temporary service invoices. 10 iv

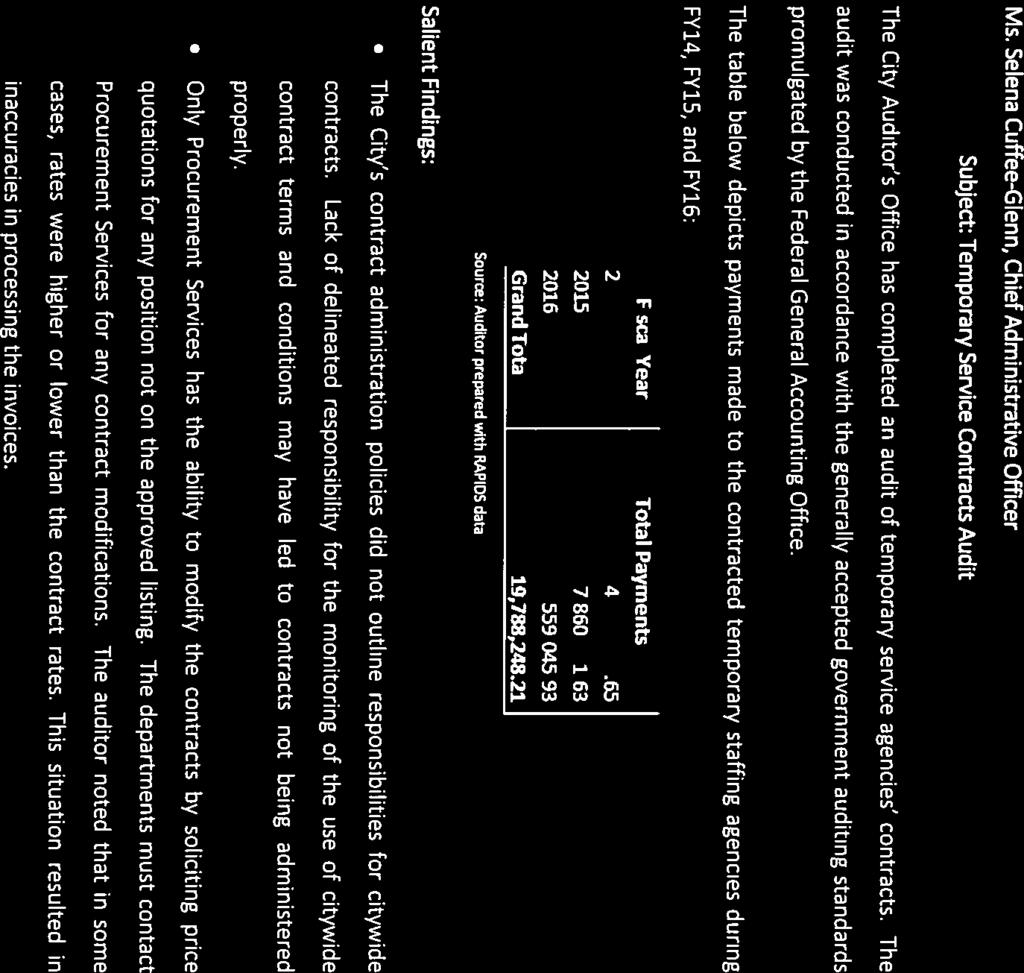

6 BACKGROUND The City of Richmond contracted with several temporary services agencies in October 2013 to provide temporary staffing. These agencies allow the City to select from a large pool of candidates to fill a diverse range of needs. Each temporary services agency has different rates and terms and conditions, as outlined in each proposal accepted by the City. The temporary services contract allows City departments to fill positions quickly to meet their required ongoing service demands. During the audit scope, the City used temporary staffing for services such as refuse collection, financial services, and customer service. The positions filled with temporary staff may be short-term or long-term depending on the needs of the City, the assigned tasks, or funding availability. Funding As a part of the annual budgeting process, the City departments are responsible for requesting funds needed for temporary services. The table below depicts payments made to the contracted temporary staffing agencies during FY14, FY15, and FY16: Source: Auditor prepared with RAPIDS data Invoice Processing The payment process differed slightly among the temporary services agencies as some used either an automated or manual process. Below is a flowchart of the overall invoice processing: Page 1 of 11

7 Source: Auditor prepared Page 2 of 11

8 FINDINGS & RECOMMENDATIONS INTERNAL CONTROLS Internal Controls Over the Temporary Services Contract Need Improvement According to the Government Auditing Standards, internal control, in the broadest sense, encompasses the agency s plan, policies, procedures, methods, and processes adopted by management to meet its mission, goals, and objectives. Internal control includes the processes for planning, organizing, directing, and controlling program operations. It also includes systems for measuring, reporting, and monitoring program performance. An effective control structure is one that provides reasonable assurance regarding: Efficiency and effectiveness of operations; Accurate financial reporting; and Compliance with laws and regulations. Based on the audit test work discussed below, the auditor concluded that internal controls over the temporary services contract need improvement: Temporary Services Contract Monitoring Needs Improvement Summary Policies and procedures were not in place for administering the Temporary Services contract. Lack of delineated responsibility for the monitoring of the use of citywide contract terms and conditions may have led to contracts not being administered properly. Departments directly negotiated with agencies to procure positions not included in the contract. The contract was not modified as Procurement was not aware of the needed change. Departments circumvented the procurement process by using the existing, approved position rates for the unapproved position. Procurement Services did not update the approved contract rates in RAPIDS, which resulted in the departments using improper rates. A temporary employee was authorized to use the supervisor s signature stamp for approving his agency s billing hours, which can be abused. Page 3 of 11

9 Contract Administration Policies The City s contract administration policies did not outline responsibilities for citywide contracts. According to the contract listing for temporary services, the Department of Procurement Services was responsible for monitoring deliverables. However, the Department of Procurement Services indicated that City departments are responsible for the contract deliverables for citywide contracts. This situation may have created confusion and resulted in inconsistent practices and lack of appropriate guidance to the City departments for ensuring compliance with the terms and conditions of these contracts. As a result, the contract administration process was ineffective. Contract Modifications According to the Request for Proposal for Temporary Services, only Procurement Services has the ability to modify the contracts by soliciting price quotations for any positions not on the approved listing. The departments must contact Procurement Services for any contract modifications. The auditor reviewed 108 invoices, which represented 132 separate temporary positions. The auditor identified nine positions that were not aligned with the approved contracts as follows: Four positions were not included on the approved contract price listing. For the other five positions, the rate charged was not in agreement with the contract price. The unapproved invoice rates resulted in inconsistent charges to the City. According to Procurement Services, the departments were responsible for negotiating rates for the positions not included in the approved listings. During the audit period, the auditor observed that the departments independently negotiated these rates with the temporary agencies. In both cases, the departments were required to approach Procurement Services to make contract modifications. However, based on the above observations, these modifications were not made to the respective contracts indicating a breakdown in the process. The auditor also noted that in some cases, rates were higher or lower than the contract rates. All approved contract rates were not in RAPIDS, which resulted in inaccuracies in processing the invoices. Page 4 of 11

10 The auditor found an example which represents a breakdown in the existing process as follows: The Budget Department rehired the former Budget Manager as a provisional employee for four days after his retirement at a rate of $60.79 an hour. Immediately after this period, the Budget Manager joined a temporary agency that charged a much higher rate for the position. The table below depicts this situation: Type Rate per hour Included in Contract Approved by Procurement Provisional $60.79 n/a n/a Temporary $ No No The auditor found the following two issues with the payments for this employee: Budget Department created a purchase requisition using an approved contract rate of $26.40 for 598 hours. This action misrepresents the actual payment rate of $119. However, payments were not processed against the resulting purchase order. Instead, the department circumvented the established procurement procedure and paid for this employee s services via an Invoice Payment Form, which is not an approved payment method. The accounts payable function acts as the City s control to prevent using unacceptable payment methods. In this case, these payments should have been rejected and returned to the Budget Department for proper processing. The temporary services invoice rate was 96% higher than the employee s provisional pay rate. During the audit period, the Budget Manager worked a total of 131 hours resulting in total payments of $15, to the temporary agency. This cost exceeds the employee s provisional salary rate for the same hours by $7, The above example represents a significant cost implication for the City. The auditor did not receive an explanation for moving the former employee from provisional employment to a temporary services vendor. Page 5 of 11

11 Rate Variance Amongst Temporary Agencies Due to the City having several temporary services agreements, similar positions were offered by multiple agencies at different rates. In some cases, the rates varied significantly. The variances between the high and low costs for the temporary agencies ranged from a difference of less than a dollar to as much as a $14 per hour. The below table demonstrates some of the identified positions and salary differences: Position Agency A Agency B % Difference Accountant I $20.25 $ % Accounting Specialist $15.88 $ % General Office Clerk $11.76 $ % Customer Service Representative II $15.88 $ % Source: Auditor Prepared from contract rates Guidance was not available for the departments to choose an agency that would have provided the best suited candidate for the least cost. Invoice Processing From the same invoice sample above, the auditor tested for: compliance with the contracted rates; accuracy of calculation; proper support (timecards to support invoiced hours); and approval of the hours worked. The auditor found: Most of the Invoices were properly authorized and supported The auditor found that work hours for 106 out of 132 temporary staff were properly supported with timesheets. Similar documentation was not found for the remaining 26 positions. This occurrence can result in the City paying for services not received or authorized. In addition, the City may pay excessive rates for services. Page 6 of 11

12 Invoices were mathematically accurate The auditor recalculated the agency invoices based on the rates and hours. From the 132 sample items, all invoices were properly calculated. Controls over invoice approval could be improved A Department of Public Works (DPW) employee supervising the temporary employees sometimes used a signature stamp to approve their hours. The auditor noted that an employee working for the temporary services agency performed the conflicting administrative duties of compiling, reconciling, and submitting timesheets for fellow employees, including himself. He also had access to the supervisor s signature stamp and was authorized to use it for approving hours for the fellow temporary agency employees for billing purposes. DPW indicated that City personnel oversee the work completed by the temporary employee and use of the stamp was only done with their approval when City supervisors were not available. Although the temporary employee was supervised, the conflicting duties can result in the City being overcharged or charged for hours not worked. In addition, allowing a temporary employee to approve his own hours and overtime can lead to abuse. Background Checks The auditor reviewed 41 background checks for temporary staff from three City departments. For the selected 41 background checks, seven showed various misdemeanors and the remaining 34 did not show any negative information. The City departments did not obtain the background checks from the temporary agencies. However, the auditor independently obtained all background checks from the respective temporary agencies. The departments provided communications with the temporary agencies for seven of the 41 background checks. Overall, the City does not have a standard criteria for conducting background checks for temporary employees. Each temporary agency identified the type of background check they would conduct in their proposals. According to various proposals, the background check types were inconsistent. The City accepts background checks conducted by the temporary agencies. Page 7 of 11

13 The City departments did not seek verification of any of the completed background checks. Verification of background checks is critical for positions that have access to sensitive information. Inadequate background checks conducted for these positions could expose the City to the risk of compromising the systems and data. The auditor found that temporary staff are allowed identical access to the City systems and data as would be provided to a permanent employee in that position. Cost Benefit of Hiring Temporary Services During FY16, the City had approximately 470 vacancies citywide. The total requested funding for these positions was $14,245,531. Only $5,041,760 was funded, which is 65% underfunded. Due to underfunding, the City departments had to fill their vacancies with temporary staffing to provide citizen services using their operating funds. The below chart demonstrates the City departments with significant use of temporary services for FY14 FY16: Source: Auditor Prepared from RAPIDS data The temporary services costs are analyzed as long term versus short term needs as follows: Long Term Needs Certain departments, such as DPW, relied heavily on temporary workers to ensure that services were properly provided. DPW has relied on temporary workers to deliver the refuse collection service for more than 10 years, due to the availability of workers when needed. Subsequent to the audit period, the Page 8 of 11

14 temporary services agency that DPW had relied upon for some time could no longer provide the refuse collector positions. Recently, DPW hired 34 refuse collectors as provisional employees. The City s Policy allows hiring a provisional employee for 90 days without benefits. After 90 days, the City has an option to complete the formal recruitment process for these positions and pay them benefits. For the refuse collector position, the auditor compared the annualized compensation paid to the vendor for these positions of $30,576 each to the cost of provisional employees of $24,253. However, if hired after 90 days, the cost of the employees with estimated cost of benefits will be $33,226. Although DPW has added the positions to the City, they still must use a temporary services agency for refuse collection. According to the Chief of Risk Management, hiring of the additional refuse collectors will increase the City s risk of workman s compensation claims. This cost will not be known until incurred. Based on the above discussion, the following conclusions can be drawn: The use of the temporary services agency provided DPW with adequate staffing every day. For an extended period, DPW was able to provide refuse collection services effectively with temporary staff. The hiring of permanent employees will not eliminate the need for temporary employees. To appropriately evaluate the cost effectiveness of staffing options for refuse collection or similar operations, additional analysis must be completed to determine long term costs of temporary versus permanent labor. Short Term Needs Departments such as the Department of Public Utilities, Finance, and Economic Development relied on temporary services agencies for short term needs either due to temporary vacancies or lack of funding. From time to time, the City needs to hire temporary employees to fill vacancies caused by retirement, terminations, extended sick leave, etc. In these situations, the City intends to hire permanent employees or use temporary staffing until the permanent employee returns. Page 9 of 11

15 Analysis Overall, the City s cost depends on the agency and the position, which may result in higher or lower fees paid. The auditor identified 10 temporary services job descriptions corresponding to permanent City positions. For long term use of temporary positions, the rate was up to 26% lower and for short term use, the rate was up to 50% higher than corresponding City rates for permanent positions. Overall, the City s use of temporary services is reliant on the needs of each department. They must evaluate which staffing options are more cost effective in the long run, minimize liability, and are most reliable. Therefore, a universal policy related to use of temporary services may not be possible. Recommendations: 1. Director of Procurement Services needs to revise the existing contract administration policies and procedures to specifically include administration of citywide contracts. 2. Director of Procurement Services needs to provide training to applicable employees in City Departments for the revised contract administration policies and procedures. 3. CAO needs to establish and implement a standard citywide process for verifying and maintaining background checks for temporary services personnel. 4. Director of Public Works needs to discontinue using the signature stamp for the approval of temporary service invoices. Page 10 of 11

16 Appendix A: Objectives, Scope, & Methodology The audit was conducted in accordance with the Generally Accepted Government Auditing Standards promulgated by the Comptroller General of the United States. Those Standards require that the auditor plan and perform the audit to obtain sufficient, appropriate evidence to provide a reasonable basis for their findings and conclusions based on the audit objectives. The auditor believe that the evidence obtained provides a reasonable basis for their findings and conclusions based on the audit objectives. SCOPE The City Auditor s Office has completed an audit of the Temporary Services Contract. This audit covers temporary service activities during the 12-month period that ended June 30, OBJECTIVES AND METHODOLOGY Overall objectives of the audit were to: To determine the adequacy of using temporary labor. Evaluate compliance with deliverables, and the terms and conditions of the contracts. The auditor performed the following procedures to complete this audit: Interviewed staff and management; Reviewed policies and procedures; Conducted a walkthrough of the Temporary Services process; Reviewed and reconciled invoices; Analyzed costs of temporary versus permanent labor; and Performed other tests, as deemed necessary. MANAGEMENT RESPONSIBILITY City management is responsible for ensuring resources are managed properly and used in compliance with laws and regulations; programs are achieving their objectives; and services are being provided efficiently, effectively, and economically. Page 11 of 11

17 MANAGEMENT RESPONSE FORM APPENDIX B # RECOMMENDATION CONCUR Y/N ACTION STEPS Director of Procurement Services needs to revise the Procurement is currently updating all existing contract 1 existing contract administration policies and administration polices and procedures. The Y procedures to specifically include administration of new/revised forms will be located on the Procurement citywide contracts. website as well as StarNet. #REF! TITLE OF RESPONSIBLE PERSON TARGET DATE #REF! Director of Procurement Services 31-Mar-18 #REF! IF IN PROGRESS, EXPLAIN ANY DELAYS IF IMPLEMENTED, DETAILS OF IMPLEMENTATION #REF! # RECOMMENDATION 2 Director of Procurement Services needs to provide training to applicable employees in City Departments for the revised contract administration policies and procedures. CONCUR Y/N Y ACTION STEPS A citywide training on how to use forms and a relaunching of all procurement policies & procedures citywide will begin April 2, 2018 #REF! TITLE OF RESPONSIBLE PERSON TARGET DATE #REF! Director of Procurement Services 30-Jun-18 #REF! IF IN PROGRESS, EXPLAIN ANY DELAYS IF IMPLEMENTED, DETAILS OF IMPLEMENTATION #REF! # RECOMMENDATION CONCUR Y/N ACTION STEPS 3 CAO needs to establish and implement a standard citywide process for verifying and maintaining background checks for temporary services personnel. Y The CAO will inform the Interim Director of Procurement Services to contact all temporary service vendors of the City's requirement to secure and provide documentation of background checks for all temporary staff assigned to the City of Richmond. #REF! TITLE OF RESPONSIBLE PERSON TARGET DATE #REF! CAO 11-Sep-17 #REF! IF IN PROGRESS, EXPLAIN ANY DELAYS IF IMPLEMENTED, DETAILS OF IMPLEMENTATION #REF! # RECOMMENDATION CONCUR Y/N ACTION STEPS 4 Director of Public Works needs to discontinue using the signature stamp for the approval of temporary service invoices. Y The Director of Public Works sent a directive to his senior staff to discontinue utilizing the signature stamp for approval of temporary services invoices. #REF! TITLE OF RESPONSIBLE PERSON TARGET DATE #REF! Director of Public Works 7-Sep-17 #REF! IF IN PROGRESS, EXPLAIN ANY DELAYS IF IMPLEMENTED, DETAILS OF IMPLEMENTATION #REF!

Citywide Payroll

2019-07 City of Richmond, VA City Auditor s Office January 04, 2019 Executive Summary... i Background, Objectives, Scope, Methodology... 1 Findings and Recommendations... 4 Management Response...Appendix

2019-07 City of Richmond, VA City Auditor s Office January 04, 2019 Executive Summary... i Background, Objectives, Scope, Methodology... 1 Findings and Recommendations... 4 Management Response...Appendix

Office of the City Auditor. Committed to increasing government efficiency, effectiveness, accountability and transparency

Office of the City Auditor Committed to increasing government efficiency, effectiveness, accountability and transparency Issue Date: November 15, 2016 TABLE OF CONTENTS Executive Summary... ii Comprehensive

Office of the City Auditor Committed to increasing government efficiency, effectiveness, accountability and transparency Issue Date: November 15, 2016 TABLE OF CONTENTS Executive Summary... ii Comprehensive

AUDIT OF: Richmond Pubic Schools PAYROLL

AUDIT OF: Richmond Pubic Schools PAYROLL Report Issued: Report Number: 2014-02 TABLE OF CONTENTS Executive Summary... ii Comprehensive List of Recommendations...v Introduction and Scope...1 Methodology...2

AUDIT OF: Richmond Pubic Schools PAYROLL Report Issued: Report Number: 2014-02 TABLE OF CONTENTS Executive Summary... ii Comprehensive List of Recommendations...v Introduction and Scope...1 Methodology...2

City Property Damage Claims Processing and Collection

City Property Damage Claims Processing and Collection March 30, 2016 Report 201602 City Auditor: Jed Johnson, CIA, CGAP Major Contributor: Marla Hamilton Staff Auditor Jonna Murphy Staff Auditor Contents

City Property Damage Claims Processing and Collection March 30, 2016 Report 201602 City Auditor: Jed Johnson, CIA, CGAP Major Contributor: Marla Hamilton Staff Auditor Jonna Murphy Staff Auditor Contents

Office of the City Auditor. Committed to increasing government efficiency, effectiveness, accountability and transparency

Office of the City Auditor Committed to increasing government efficiency, effectiveness, accountability and transparency Issue Date: January 10, 2017 Table of Contents Executive Summary... ii Comprehensive

Office of the City Auditor Committed to increasing government efficiency, effectiveness, accountability and transparency Issue Date: January 10, 2017 Table of Contents Executive Summary... ii Comprehensive

Office of the City Auditor. Committed to increasing government efficiency, effectiveness, accountability and transparency

Office of the City Auditor Committed to increasing government efficiency, effectiveness, accountability and transparency Issue Date: TABLE OF CONTENTS Executive Summary... ii Recommendation... iv Background...1

Office of the City Auditor Committed to increasing government efficiency, effectiveness, accountability and transparency Issue Date: TABLE OF CONTENTS Executive Summary... ii Recommendation... iv Background...1

Richmond Ambulance Authority

REPORT # 2012-06 AUDIT Of the TABLE OF CONTENTS Executive Summary..... i Comprehensive List of Recommendations. iii Introduction........... 1 Background 2 Observations and Recommendations..... 3 Management

REPORT # 2012-06 AUDIT Of the TABLE OF CONTENTS Executive Summary..... i Comprehensive List of Recommendations. iii Introduction........... 1 Background 2 Observations and Recommendations..... 3 Management

2011 CFS Salary Guide

2011 CFS Salary Guide Creative Financial Staffing www.cfstaffing.com Welcome to the 2011 CFS Salary Guide The 2011 CFS Salary Guide consists of the following sections: National Salary Data Local Market

2011 CFS Salary Guide Creative Financial Staffing www.cfstaffing.com Welcome to the 2011 CFS Salary Guide The 2011 CFS Salary Guide consists of the following sections: National Salary Data Local Market

Long Beach City Auditor s Office

Long Beach City Auditor s Office Contract Administration Audit Limited Scope Review Report 7 of 10 Utiliworks Consulting, LLC July 1, 2016 Laura L. Doud City Auditor Audit Team: Deborah K. Ellis Assistant

Long Beach City Auditor s Office Contract Administration Audit Limited Scope Review Report 7 of 10 Utiliworks Consulting, LLC July 1, 2016 Laura L. Doud City Auditor Audit Team: Deborah K. Ellis Assistant

Internal Audit Report - Contract Compliance Cycle Audit Department of Technology Services: SHI International Corporation Contract Number

Internal Audit Report - Contract Compliance Cycle Audit Department of Technology Services: SHI International Corporation Contract Number- 582-14 TABLE OF CONTENTS Transmittal Letter... 1 Executive Summary

Internal Audit Report - Contract Compliance Cycle Audit Department of Technology Services: SHI International Corporation Contract Number- 582-14 TABLE OF CONTENTS Transmittal Letter... 1 Executive Summary

Edmonton Police Service Payroll Audit April 4, 2012

Edmonton Police Service Payroll Audit April 4, 2012 The Office of the City Auditor conducted this project in accordance with the International Standards for the Professional Practice of Internal Auditing

Edmonton Police Service Payroll Audit April 4, 2012 The Office of the City Auditor conducted this project in accordance with the International Standards for the Professional Practice of Internal Auditing

Review of City's Bank Reconciliation and Deposit Procedures

Review of City's Bank Reconciliation and Deposit Procedures The Audit Committee recommends the adoption of the following report (September 13, 2000) from the City Auditor. The Audit Committee reports,

Review of City's Bank Reconciliation and Deposit Procedures The Audit Committee recommends the adoption of the following report (September 13, 2000) from the City Auditor. The Audit Committee reports,

REPORT 2016/001 INTERNAL AUDIT DIVISION

INTERNAL AUDIT DIVISION REPORT 2016/001 Audit of the recruitment and use of consultants and individual contractors by the Departments of Peacekeeping Operations and Field Support Overall results relating

INTERNAL AUDIT DIVISION REPORT 2016/001 Audit of the recruitment and use of consultants and individual contractors by the Departments of Peacekeeping Operations and Field Support Overall results relating

Prince William County, Virginia Internal Audit Report Timekeeping Cycle Audit. August 31, 2018

Prince William County, Virginia Internal Audit Report Timekeeping Cycle Audit August 31, 2018 TABLE OF CONTENTS Transmittal Letter... 1 Executive Summary... 2 Background... 4 Objectives and Approach...

Prince William County, Virginia Internal Audit Report Timekeeping Cycle Audit August 31, 2018 TABLE OF CONTENTS Transmittal Letter... 1 Executive Summary... 2 Background... 4 Objectives and Approach...

EXAMINATION OF CERTAIN FINANCIAL PROCESSES AND INTERNAL CONTROLS OF THE KENTUCKY CORRECTIONAL INDUSTRIES

EXAMINATION OF CERTAIN FINANCIAL PROCESSES AND INTERNAL CONTROLS OF THE KENTUCKY CORRECTIONAL INDUSTRIES CRIT LUALLEN AUDITOR OF PUBLIC ACCOUNTS www.auditor.ky.gov 105 SEA HERO ROAD, SUITE 2 FRANKFORT,

EXAMINATION OF CERTAIN FINANCIAL PROCESSES AND INTERNAL CONTROLS OF THE KENTUCKY CORRECTIONAL INDUSTRIES CRIT LUALLEN AUDITOR OF PUBLIC ACCOUNTS www.auditor.ky.gov 105 SEA HERO ROAD, SUITE 2 FRANKFORT,

Contract Management Internal Audit Report August 17, 2018

Contract Management August 17, 2018 Linda J. Lindsey, CPA, CGAP, Senior Director Vince Roberts, CIA, Internal Auditor Jarai Ings, Internal Auditor Table of Contents Page Number EXECUTIVE SUMMARY 1 BACKGROUND

Contract Management August 17, 2018 Linda J. Lindsey, CPA, CGAP, Senior Director Vince Roberts, CIA, Internal Auditor Jarai Ings, Internal Auditor Table of Contents Page Number EXECUTIVE SUMMARY 1 BACKGROUND

Fire Department Inventory Management Audit

Fire Department Inventory Management Audit With over $3 million spent annually on inventory, the Fire Department needs stronger inventory management practices and controls Independence you can rely on

Fire Department Inventory Management Audit With over $3 million spent annually on inventory, the Fire Department needs stronger inventory management practices and controls Independence you can rely on

All American Asphalt Annual Street Improvement Contract Audit

All American Asphalt Annual Street Improvement Contract Audit The contractor was paid $2.5 million for projects outside of set contract pricing in a nine- month period. Not all of these projects adhered

All American Asphalt Annual Street Improvement Contract Audit The contractor was paid $2.5 million for projects outside of set contract pricing in a nine- month period. Not all of these projects adhered

A. General Information

Management Systems Questionnaire for Standard Cost Reimbursement Grants (Jan 2016) 1. Legal name of applicant organization: 2. Name and title of individual completing this questionnaire: 3. Signature of

Management Systems Questionnaire for Standard Cost Reimbursement Grants (Jan 2016) 1. Legal name of applicant organization: 2. Name and title of individual completing this questionnaire: 3. Signature of

Senior Accounting Specialist Class Specification

Senior Accounting Specialist Class Specification FLSA Designation: Non-Exempt Effective: 03/2004 Revised: N/A DEFINITION Under general supervision, to perform a variety of specialized, technical, and complex

Senior Accounting Specialist Class Specification FLSA Designation: Non-Exempt Effective: 03/2004 Revised: N/A DEFINITION Under general supervision, to perform a variety of specialized, technical, and complex

MARK J.F. SCHROEDER COMPTROLLER

C I T Y O F B U F F A L O D E P A R T M E N T O F A U D I T A N D C O N T R O L FOLLOW UP To the Audit Report ON the PAYROLL PROCEDURES AT THE FIRE DEPARTMENT MARK J.F. SCHROEDER COMPTROLLER A N N E F

C I T Y O F B U F F A L O D E P A R T M E N T O F A U D I T A N D C O N T R O L FOLLOW UP To the Audit Report ON the PAYROLL PROCEDURES AT THE FIRE DEPARTMENT MARK J.F. SCHROEDER COMPTROLLER A N N E F

HFTP Hospitality Financial and Technology Professionals

About our Sample Accounting Jobs Descriptions for Clubs: The HFTP Americas Research Center, with guidance from members of the HFTP Club Advisory Council, has developed example job descriptions for accounting

About our Sample Accounting Jobs Descriptions for Clubs: The HFTP Americas Research Center, with guidance from members of the HFTP Club Advisory Council, has developed example job descriptions for accounting

ATLANTA PUBLIC SCHOOLS COMPENSATION GUIDELINES. Human Resources HR Services

ATLANTA PUBLIC SCHOOLS COMPENSATION GUIDELINES Human Resources HR Services ATLANTA PUBLIC SCHOOLS COMPENSATION GUIDELINES Human Resources HR Services Compensation Philosophy The purpose of the Atlanta

ATLANTA PUBLIC SCHOOLS COMPENSATION GUIDELINES Human Resources HR Services ATLANTA PUBLIC SCHOOLS COMPENSATION GUIDELINES Human Resources HR Services Compensation Philosophy The purpose of the Atlanta

Ms. Jeanine Rufo, President, Board of Education

Date: August 31, 2016 To: From: Cc: Subject: Ms. Jeanine Rufo, President, Board of Education David Moran, Director of Education Practice Audit Committee Natalie Doherty, Assistant Superintendent Jill Figarella,

Date: August 31, 2016 To: From: Cc: Subject: Ms. Jeanine Rufo, President, Board of Education David Moran, Director of Education Practice Audit Committee Natalie Doherty, Assistant Superintendent Jill Figarella,

Honorable Mayor, City Council President, and members of the City Council:

AMANDA NOBLE City Auditor anoble@atlantaga.gov STEPHANIE JACKSON Deputy City Auditor sjackson@atlantaga.gov C I T Y O F A T L A N T A CITY AUDITOR S OFFICE 68 MITCHELL STREET SW, SUITE 12100 ATLANTA, GEORGIA

AMANDA NOBLE City Auditor anoble@atlantaga.gov STEPHANIE JACKSON Deputy City Auditor sjackson@atlantaga.gov C I T Y O F A T L A N T A CITY AUDITOR S OFFICE 68 MITCHELL STREET SW, SUITE 12100 ATLANTA, GEORGIA

SUMMARY. 1,278 regular budget positions and 148 resolution authorities. Page i

SUMMARY The Department of Transportation (DOT) is responsible for the development of plans to meet the ground transportation needs of the traveling public and commerce in the City of Los Angeles. It has

SUMMARY The Department of Transportation (DOT) is responsible for the development of plans to meet the ground transportation needs of the traveling public and commerce in the City of Los Angeles. It has

REQUEST FOR PROPOSALS

REQUEST FOR PROPOSALS FOR COMPENSATION STUDY Proposals Due: November 3, 2016, 4:00 PM 1.0 OBJECTIVE SECTION 1 SUBMITTAL PROCEDURES & DEADLINE The City of Signal Hill is seeking proposals from qualified

REQUEST FOR PROPOSALS FOR COMPENSATION STUDY Proposals Due: November 3, 2016, 4:00 PM 1.0 OBJECTIVE SECTION 1 SUBMITTAL PROCEDURES & DEADLINE The City of Signal Hill is seeking proposals from qualified

Audit of Human Resources Operations Report Number A-1617DJJ-004 June 28, The Office of the Inspector General Bureau of Internal Audit

Report Number A-1617DJJ-004 June 28, 2017 By The Office of the Inspector General Robert A. Munson Inspector General Michael Yu, CIA, CIG Director of Auditing Kelly Neel Auditor-in-Charge Karen Miller Auditor

Report Number A-1617DJJ-004 June 28, 2017 By The Office of the Inspector General Robert A. Munson Inspector General Michael Yu, CIA, CIG Director of Auditing Kelly Neel Auditor-in-Charge Karen Miller Auditor

HUMAN RESOURCES DEPARTMENT

City of San Mateo MISSION STATEMENT HUMAN RESOURCES DEPARTMENT To provide the City with effective human resource programs in the areas of diversity, personnel recruitment and selection, employee training

City of San Mateo MISSION STATEMENT HUMAN RESOURCES DEPARTMENT To provide the City with effective human resource programs in the areas of diversity, personnel recruitment and selection, employee training

Ambulance Contract Billing Report October 12, 2016 KEY CONTROL FINDING RECOMMENDATION STATUS The City should:

Ambulance Contract Billing Report October 12, 2016 The City should: General Recordkeeping Inconsistencies exist in the basic recordkeeping related to ambulance calls. Continue with the implementation of

Ambulance Contract Billing Report October 12, 2016 The City should: General Recordkeeping Inconsistencies exist in the basic recordkeeping related to ambulance calls. Continue with the implementation of

Final Audit Follow-Up As of May 31, 2015

Final Audit Follow-Up As of May 31, 2015 T. Bert Fletcher, CPA, CGMA City Auditor Audit of Selected Departments Performing Accounts Receivable Functions (Report #1204 issued February 15, 2012) Report #1512

Final Audit Follow-Up As of May 31, 2015 T. Bert Fletcher, CPA, CGMA City Auditor Audit of Selected Departments Performing Accounts Receivable Functions (Report #1204 issued February 15, 2012) Report #1512

University System of Maryland University of Baltimore

Audit Report University System of Maryland University of Baltimore January 2018 OFFICE OF LEGISLATIVE AUDITS DEPARTMENT OF LEGISLATIVE SERVICES MARYLAND GENERAL ASSEMBLY For further information concerning

Audit Report University System of Maryland University of Baltimore January 2018 OFFICE OF LEGISLATIVE AUDITS DEPARTMENT OF LEGISLATIVE SERVICES MARYLAND GENERAL ASSEMBLY For further information concerning

STATE OF NORTH CAROLINA

STATE OF NORTH CAROLINA DEPARTMENT OF ADMINISTRATION DIVISION OF PURCHASE AND CONTRACT FINANCIAL RELATED AUDIT OFFICE SUPPLIES TERM CONTRACT AUDIT FOLLOW-UP JUNE 2014 OFFICE OF THE STATE AUDITOR BETH A.

STATE OF NORTH CAROLINA DEPARTMENT OF ADMINISTRATION DIVISION OF PURCHASE AND CONTRACT FINANCIAL RELATED AUDIT OFFICE SUPPLIES TERM CONTRACT AUDIT FOLLOW-UP JUNE 2014 OFFICE OF THE STATE AUDITOR BETH A.

Internal recruitment. CH- 6 Presented by: Kamelia Gulam HUR-332

Internal recruitment CH- 6 Presented by: Kamelia Gulam HUR-332 1 Staffing Organizations Model Organization Mission Goals and Objectives Organization Strategy HR and Staffing Strategy Legal compliance Planning

Internal recruitment CH- 6 Presented by: Kamelia Gulam HUR-332 1 Staffing Organizations Model Organization Mission Goals and Objectives Organization Strategy HR and Staffing Strategy Legal compliance Planning

CITY OF CORPUS CHRISTI

CITY OF CORPUS CHRISTI CITY AUDITOR S OFFICE Audit of Purchasing Program Project No. AU12-004 September 20, 2012 City Auditor Celia Gaona, CIA CISA CFE Auditor Nora Lozano, CIA CISA Executive Summary In

CITY OF CORPUS CHRISTI CITY AUDITOR S OFFICE Audit of Purchasing Program Project No. AU12-004 September 20, 2012 City Auditor Celia Gaona, CIA CISA CFE Auditor Nora Lozano, CIA CISA Executive Summary In

COMMUNITY & ORGANIZATION RELATIONS

COMMUNITY & ORGANIZATION RELATIONS E-26 City of Mercer Island 2007-2008 Budget Department: Community & Organization Relations In November 2006, the Community & Organization Relations Department (CORe)

COMMUNITY & ORGANIZATION RELATIONS E-26 City of Mercer Island 2007-2008 Budget Department: Community & Organization Relations In November 2006, the Community & Organization Relations Department (CORe)

PRIVY COUNCIL OFFICE. Audit of PCO s Accounts Payable Function. Final Report

[*] An asterisk appears where sensitive information has been removed in accordance with the Access to Information Act and Privacy Act. PRIVY COUNCIL OFFICE Audit and Evaluation Division Final Report January

[*] An asterisk appears where sensitive information has been removed in accordance with the Access to Information Act and Privacy Act. PRIVY COUNCIL OFFICE Audit and Evaluation Division Final Report January

Transportation and Infrastructure Renewal: Mechanical Branch Management

4 Transportation and Infrastructure Renewal: Mechanical Branch Management Summary The Department of Transportation and Infrastructure Renewal s management of mechanical branch operations is deficient.

4 Transportation and Infrastructure Renewal: Mechanical Branch Management Summary The Department of Transportation and Infrastructure Renewal s management of mechanical branch operations is deficient.

Policy and Procedure on Engaging Externally Contracted Service Providers

Policy and Procedure on Engaging Externally Contracted Service Providers 1. Purpose of this Policy The purpose of this Policy is to set down clear guidelines for the appropriate engagement of externally

Policy and Procedure on Engaging Externally Contracted Service Providers 1. Purpose of this Policy The purpose of this Policy is to set down clear guidelines for the appropriate engagement of externally

Contract Administration Audit: Universal Protection Services, LP

Contract Administration Audit: Universal Protection Services, LP Limited Scope Review Report 9 of 10 Independence you can rely on October 17, 2016 Laura L. Doud City Auditor Deborah K. Ellis Assistant

Contract Administration Audit: Universal Protection Services, LP Limited Scope Review Report 9 of 10 Independence you can rely on October 17, 2016 Laura L. Doud City Auditor Deborah K. Ellis Assistant

Internal Audit Report Accounts Payable September 2017

Internal Audit Report 17-03 September 2017 City of Sioux Falls Internal Audit Department Carnegie Town Hall 235 W. 10 th Street Sioux Falls, SD 57117-7402 www.siouxfalls.org/council/internal-audit September

Internal Audit Report 17-03 September 2017 City of Sioux Falls Internal Audit Department Carnegie Town Hall 235 W. 10 th Street Sioux Falls, SD 57117-7402 www.siouxfalls.org/council/internal-audit September

Request for Proposal For: 2018 American Bar Association Temporary Services

Table of Contents Bid Timetable [2] 1.0 General Bid Information [3] 2.0 Proposal Requirements [5] 3.0 Criteria for Selection [7] 4.0 Specifications and Work Statement [7] Appendix A: Bidder Response Sheet

Table of Contents Bid Timetable [2] 1.0 General Bid Information [3] 2.0 Proposal Requirements [5] 3.0 Criteria for Selection [7] 4.0 Specifications and Work Statement [7] Appendix A: Bidder Response Sheet

Richmond City Department of Justice Services Truancy and Diversion

REPORT # 2012-05 AUDIT Of the Richmond City Department of Justice Services Truancy and Diversion TABLE OF CONTENTS Executive Summary..... i Comprehensive List of Recommendations iii Introduction...........

REPORT # 2012-05 AUDIT Of the Richmond City Department of Justice Services Truancy and Diversion TABLE OF CONTENTS Executive Summary..... i Comprehensive List of Recommendations iii Introduction...........

County Timekeeping Practices

Contra Costa County Grand Jury Report 1511 County Timekeeping Practices Contact: Sherry Rufini Foreperson 925-957-5638 Need for Accuracy in Reporting Time & Remedies for Inaccuracy TO: The Contra Costa

Contra Costa County Grand Jury Report 1511 County Timekeeping Practices Contact: Sherry Rufini Foreperson 925-957-5638 Need for Accuracy in Reporting Time & Remedies for Inaccuracy TO: The Contra Costa

Procurement May 2018

Procurement May 2018 May 16, 2018 Office of the Auditor General Halifax Regional Municipality The following audit of Procurement, completed under section 50(2) of the Halifax Regional Municipality Charter,

Procurement May 2018 May 16, 2018 Office of the Auditor General Halifax Regional Municipality The following audit of Procurement, completed under section 50(2) of the Halifax Regional Municipality Charter,

Executive Summary THE OFFICE OF THE INTERNAL AUDITOR. Internal Audit Update

1 Page THE OFFICE OF THE INTERNAL AUDITOR The Office of Internal Audit focuses its attention on areas where it can contribute the most by working with the organization to reduce risk and increase operational

1 Page THE OFFICE OF THE INTERNAL AUDITOR The Office of Internal Audit focuses its attention on areas where it can contribute the most by working with the organization to reduce risk and increase operational

Lawrence Berkeley National Lab. Observations from Audit Procedures October 17, 2005

Lawrence Berkeley National Lab Observations from Audit Procedures October 17, 2005 Table of Contents Page Your Needs and Expectations 3 Background 4 Risk Assessment 5 Audit Strategy 6 Details of Work Performed

Lawrence Berkeley National Lab Observations from Audit Procedures October 17, 2005 Table of Contents Page Your Needs and Expectations 3 Background 4 Risk Assessment 5 Audit Strategy 6 Details of Work Performed

Employee Relations Approved General Government Operating Budget ER - 1. Municipal Manager. Employee Relations

Municipal Manager Administration Benefits Central Payroll Employment, Classification & Records Labor Relations ER - 1 Description The Municipality of Anchorage Department provides employment services,

Municipal Manager Administration Benefits Central Payroll Employment, Classification & Records Labor Relations ER - 1 Description The Municipality of Anchorage Department provides employment services,

Seattle Public Schools The Office of Internal Audit

Seattle Public Schools The Office of Internal Audit Internal Audit Report September 1, 2014 through Current Issue Date: June 21, 2016 Executive Summary Background Information The function is centralized

Seattle Public Schools The Office of Internal Audit Internal Audit Report September 1, 2014 through Current Issue Date: June 21, 2016 Executive Summary Background Information The function is centralized

LA18-09 STATE OF NEVADA. Performance Audit. Department of Administration Hearings Division Legislative Auditor Carson City, Nevada

LA18-09 STATE OF NEVADA Performance Audit Department of Administration Hearings Division 2017 Legislative Auditor Carson City, Nevada Audit Highlights Highlights of performance audit report on the Hearings

LA18-09 STATE OF NEVADA Performance Audit Department of Administration Hearings Division 2017 Legislative Auditor Carson City, Nevada Audit Highlights Highlights of performance audit report on the Hearings

Administrative Services About Administrative Services

About The Department oversees and directs the operations of Finance, Human Resources, Sales Tax, Purchasing, Information Technology, Risk Management, Budget, the Public Information Office, Front Desk Reception,

About The Department oversees and directs the operations of Finance, Human Resources, Sales Tax, Purchasing, Information Technology, Risk Management, Budget, the Public Information Office, Front Desk Reception,

Internal Audit How the Internal Audit Function Facilitates Internal Controls. Office of the City Auditor City of Tallahassee

Internal Audit How the Internal Audit Function Facilitates Internal Controls Office of the City Auditor City of Tallahassee 1 Internal Audits and Internal Controls Session Purpose: How does an internal

Internal Audit How the Internal Audit Function Facilitates Internal Controls Office of the City Auditor City of Tallahassee 1 Internal Audits and Internal Controls Session Purpose: How does an internal

Seattle Public Schools The Office of Internal Audit

only Seattle Public Schools The Office of Internal Audit Internal Audit Report September 1, 2011 through April 30 2013 Issue Date: June 18, 2013 Executive Summary Background Information The District s

only Seattle Public Schools The Office of Internal Audit Internal Audit Report September 1, 2011 through April 30 2013 Issue Date: June 18, 2013 Executive Summary Background Information The District s

REPORT 2016/067 INTERNAL AUDIT DIVISION. Audit of management of national staff recruitment in the United Nations Assistance Mission for Iraq

INTERNAL AUDIT DIVISION REPORT 2016/067 Audit of management of national staff recruitment in the United Nations Assistance Mission for Iraq Overall results relating to the effective management of national

INTERNAL AUDIT DIVISION REPORT 2016/067 Audit of management of national staff recruitment in the United Nations Assistance Mission for Iraq Overall results relating to the effective management of national

Internal Controls. for County Recorders

Internal Controls for County Recorders Definition of Internal Controls State Board of Accounts (SBOA) defines internal control as follows: Internal control is a process executed by officials and employees

Internal Controls for County Recorders Definition of Internal Controls State Board of Accounts (SBOA) defines internal control as follows: Internal control is a process executed by officials and employees

INTERNAL AUDIT DIVISION REPORT 2016/131

INTERNAL AUDIT DIVISION REPORT 2016/131 Audit of movement control operations in the United Nations Multidimensional Integrated Stabilization Mission in the Central African Republic Control processes over

INTERNAL AUDIT DIVISION REPORT 2016/131 Audit of movement control operations in the United Nations Multidimensional Integrated Stabilization Mission in the Central African Republic Control processes over

Accounting Specialist I Accounting Specialist II Accounting Specialist III Class Specification

Accounting Specialist I Accounting Specialist II Accounting Specialist III Class Specification FLSA Designation: Non-Exempt Effective: 03/2004 Revised: N/A DEFINITION Under general supervision (Accounting

Accounting Specialist I Accounting Specialist II Accounting Specialist III Class Specification FLSA Designation: Non-Exempt Effective: 03/2004 Revised: N/A DEFINITION Under general supervision (Accounting

JOB RECRUITMENT: ACCOUNTANT TECHNICIAN

JOB RECRUITMENT: ACCOUNTANT TECHNICIAN FINAL FILING DATE: JUNE 30 TH 2015 Justice with Dignity and Respect Superior Court of California, County of Santa Cruz About the Position The Superior Court of Santa

JOB RECRUITMENT: ACCOUNTANT TECHNICIAN FINAL FILING DATE: JUNE 30 TH 2015 Justice with Dignity and Respect Superior Court of California, County of Santa Cruz About the Position The Superior Court of Santa

Guidelines for Using the Intra-agency Agreement or Approval Letter for Temporary Special Assignment of Personnel

Guidelines for Using the Intra-agency Agreement or Approval Letter for Temporary Special Assignment of Personnel INTRODUCTION Projects often require the special skills and knowledge of college or university

Guidelines for Using the Intra-agency Agreement or Approval Letter for Temporary Special Assignment of Personnel INTRODUCTION Projects often require the special skills and knowledge of college or university

CONVENT OF THE SACRED HEART SCHOOL FOUNDATION FINANCIAL REGULATIONS

CONVENT OF THE SACRED HEART SCHOOL FOUNDATION FINANCIAL REGULATIONS Approved by Convent of the Sacred Heart School Foundation, Board of Governors on 9 th October 2008 Policy Statement So that all officers

CONVENT OF THE SACRED HEART SCHOOL FOUNDATION FINANCIAL REGULATIONS Approved by Convent of the Sacred Heart School Foundation, Board of Governors on 9 th October 2008 Policy Statement So that all officers

A REPORT FROM THE OFFICE OF INTERNAL AUDIT

A REPORT FROM THE OFFICE OF INTERNAL AUDIT PRESENTED TO THE CITY COUNCIL CITY OF BOISE, IDAHO AUDIT / TASK: #18-06, P-Card Program Review AUDIT CLIENT: Purchasing / Cross-Functional REPORT DATE: September

A REPORT FROM THE OFFICE OF INTERNAL AUDIT PRESENTED TO THE CITY COUNCIL CITY OF BOISE, IDAHO AUDIT / TASK: #18-06, P-Card Program Review AUDIT CLIENT: Purchasing / Cross-Functional REPORT DATE: September

REPORT 2015/184 INTERNAL AUDIT DIVISION. Audit of rations management in the United Nations Support Office in Somalia

INTERNAL AUDIT DIVISION REPORT 2015/184 Audit of rations management in the United Nations Support Office in Somalia Overall results relating to the effective management of rations in the United Nations

INTERNAL AUDIT DIVISION REPORT 2015/184 Audit of rations management in the United Nations Support Office in Somalia Overall results relating to the effective management of rations in the United Nations

Office of Inspector General City of New Orleans

Office of Inspector General City of New Orleans A Performance Audit of the New Orleans Aviation Board Month-to-Month Contracts A&R12PAU001 E. R. Quatrevaux Inspector General Issued October 1, 2013 A Performance

Office of Inspector General City of New Orleans A Performance Audit of the New Orleans Aviation Board Month-to-Month Contracts A&R12PAU001 E. R. Quatrevaux Inspector General Issued October 1, 2013 A Performance

Effecting Change Through the Audit Process: Audit of the Orlando-Orange County Expressway Authority

Effecting Change Through the Audit Process: Audit of the Orlando-Orange County Expressway Authority Presented to the Florida Audit Forum February 8, 2008 Tampa, FL 1 Effecting Change Through the Audit

Effecting Change Through the Audit Process: Audit of the Orlando-Orange County Expressway Authority Presented to the Florida Audit Forum February 8, 2008 Tampa, FL 1 Effecting Change Through the Audit

TxDOT Internal Audit Letting Programming and Scheduling Function (1101-2) Department-wide Report

Department-wide Report") Introduction Letting Programming and Scheduling Function (1101-2) Department-wide Report This report has been prepared for the Transportation Commission, TxDOT Administration and Management. The report

Introduction Letting Programming and Scheduling Function (1101-2) Department-wide Report This report has been prepared for the Transportation Commission, TxDOT Administration and Management. The report

2010 Joint Chairmen s Report. UMB Progress to Address Audit Findings. (R30B/R75T), pages 133/ Release of Restricted Funds

, pages 133/ Release of Restricted Funds") 2010 Joint Chairmen s Report UMB Progress to Address Audit Findings (R30B/R75T), pages 133/145-146 Release of Restricted Funds 1 Subject: 2010 Joint Chairmen s Report - UMB Progress to Address Audit Findings

2010 Joint Chairmen s Report UMB Progress to Address Audit Findings (R30B/R75T), pages 133/145-146 Release of Restricted Funds 1 Subject: 2010 Joint Chairmen s Report - UMB Progress to Address Audit Findings

Reviewed by ADM(RS) in accordance with the Access to Information Act. Information UNCLASSIFIED.

in accordance with the Access to Information Act. Information UNCLASSIFIED.") Reviewed by ADM(RS) in accordance with the Access to Information Act. Information UNCLASSIFIED. Audit of the Financial Management Framework: Royal Canadian Air Force March 2015 7050-8-39 (CRS) Table of

Reviewed by ADM(RS) in accordance with the Access to Information Act. Information UNCLASSIFIED. Audit of the Financial Management Framework: Royal Canadian Air Force March 2015 7050-8-39 (CRS) Table of

General Government and Gainesville Regional Utilities Vendor Master File Audit

FINAL AUDIT REPORT A Report to the City Commission General Government and Gainesville Regional Utilities Vendor Master File Audit Mayor Lauren Poe Mayor Pro-Tem Adrian Hayes-Santos Commission Members David

FINAL AUDIT REPORT A Report to the City Commission General Government and Gainesville Regional Utilities Vendor Master File Audit Mayor Lauren Poe Mayor Pro-Tem Adrian Hayes-Santos Commission Members David

DEPARTMENT OF CORRECTIONS

DEPARTMENT OF CORRECTIONS REPORT ON AUDIT OF SELECT CYCLES FOR THE YEAR ENDED JUNE 30, 2018 Auditor of Public Accounts Martha S. Mavredes, CPA www.apa.virginia.gov (804) 225-3350 AUDIT SUMMARY Our audit

DEPARTMENT OF CORRECTIONS REPORT ON AUDIT OF SELECT CYCLES FOR THE YEAR ENDED JUNE 30, 2018 Auditor of Public Accounts Martha S. Mavredes, CPA www.apa.virginia.gov (804) 225-3350 AUDIT SUMMARY Our audit

REPORT 2015/086 INTERNAL AUDIT DIVISION. Audit of the Kuwait Joint Support Office

INTERNAL AUDIT DIVISION REPORT 2015/086 Audit of the Kuwait Joint Support Office Overall results relating to the effective management of support functions performed by the Kuwait Joint Support Office were

INTERNAL AUDIT DIVISION REPORT 2015/086 Audit of the Kuwait Joint Support Office Overall results relating to the effective management of support functions performed by the Kuwait Joint Support Office were

Audit Recommendations Status Report as of December 31, 2018

SO U THWEST F LORIDA Internal Audit Report Audit Recommendations Report as of December 31, 2018 Date: March 15, 2019 To: The Honorable Linda Doggett, Lee County Clerk of the Circuit Court & Comptroller

SO U THWEST F LORIDA Internal Audit Report Audit Recommendations Report as of December 31, 2018 Date: March 15, 2019 To: The Honorable Linda Doggett, Lee County Clerk of the Circuit Court & Comptroller

City of Westby Clerk/Treasurer Job Description

City of Westby Clerk/Treasurer Job Description Job Title Clerk/Treasurer Department Office Description of Work Performs administrative work conducting the daily business of the City of Westby including

City of Westby Clerk/Treasurer Job Description Job Title Clerk/Treasurer Department Office Description of Work Performs administrative work conducting the daily business of the City of Westby including

Construction Auditing: UTILIZING INDUSTRY STANDARDS, BEST PRACTICES AND CHANGE ORDER AUDITING APRIL 4, 2017

Construction Auditing: UTILIZING INDUSTRY STANDARDS, BEST PRACTICES AND CHANGE ORDER AUDITING APRIL 4, 2017 OPENING REMARKS Kinney Poynter Moderator Executive Director NASACT Alan Pennington Speaker Vice

Construction Auditing: UTILIZING INDUSTRY STANDARDS, BEST PRACTICES AND CHANGE ORDER AUDITING APRIL 4, 2017 OPENING REMARKS Kinney Poynter Moderator Executive Director NASACT Alan Pennington Speaker Vice

CITY OF REEDLEY ACCOUNTING TECHNICIAN I ACCOUNTING TECHNICIAN II

CITY OF REEDLEY ACCOUNTING TECHNICIAN I ACCOUNTING TECHNICIAN II DEFINITION Under immediate supervision (Accounting Technician I) or general supervision (Accounting Technician II), to perform a variety

CITY OF REEDLEY ACCOUNTING TECHNICIAN I ACCOUNTING TECHNICIAN II DEFINITION Under immediate supervision (Accounting Technician I) or general supervision (Accounting Technician II), to perform a variety

Comprehensive List of Fraud Indicators

Comprehensive List of Fraud Indicators This document provides links to our contract audit resources. The scenarios are grouped by audit type, but the issues presented could be applicable to other audits

Comprehensive List of Fraud Indicators This document provides links to our contract audit resources. The scenarios are grouped by audit type, but the issues presented could be applicable to other audits

QUALITY CONTROL FOR AUDIT WORK CONTENTS

CONTENTS Paragraphs Introduction... 1-3 Audit Firm... 4-7 Individual Audits... 8-17 Appendix: Illustrative Examples of Quality Control Procedures for an Audit Firm 1 International Standards on Auditing

CONTENTS Paragraphs Introduction... 1-3 Audit Firm... 4-7 Individual Audits... 8-17 Appendix: Illustrative Examples of Quality Control Procedures for an Audit Firm 1 International Standards on Auditing

ONTARIO POWER GENERATION KEY ACTIONS UPDATE 2013 AUDITOR GENERAL S REPORT ON HUMAN RESOURCES

ONTARIO POWER GENERATION KEY UPDATE 2013 AUDITOR GENERAL S REPORT ON HUMAN RESOURCES OPG has made substantial progress in implementing the Auditor General s six recommendations at the first six month mark.

ONTARIO POWER GENERATION KEY UPDATE 2013 AUDITOR GENERAL S REPORT ON HUMAN RESOURCES OPG has made substantial progress in implementing the Auditor General s six recommendations at the first six month mark.

Dutchess County Department of Planning and Community Development Division of Mass Transit January 2007 December 2008

Dutchess County Department of Planning and Community Development Division of Mass Transit January 2007 December 2008 COMPTROLLER S SUMMARY... 2 Organization and Background... 2 Audit Scope, Objective and

Dutchess County Department of Planning and Community Development Division of Mass Transit January 2007 December 2008 COMPTROLLER S SUMMARY... 2 Organization and Background... 2 Audit Scope, Objective and

TEXAS BOARD OF NURSING CONTRACT PROCUREMENT AND MANAGEMENT HANDBOOK JULY 2018

TEXAS BOARD OF NURSING CONTRACT PROCUREMENT AND MANAGEMENT HANDBOOK JULY 2018 I. Introduction a. Purpose i. All staff involved with procuring goods and services for the agency must comply with proper purchasing

TEXAS BOARD OF NURSING CONTRACT PROCUREMENT AND MANAGEMENT HANDBOOK JULY 2018 I. Introduction a. Purpose i. All staff involved with procuring goods and services for the agency must comply with proper purchasing

INTERNAL CONTROLS MANUAL DICKSON COUNTY SCHOOLS DANNY L. WEEKS, ED.D. DIRECTOR OF SCHOOLS LINDA FRAZIER BUSINESS MANAGER JUNE 2016

1 INTERNAL CONTROLS MANUAL DICKSON COUNTY SCHOOLS DANNY L. WEEKS, ED.D. DIRECTOR OF SCHOOLS LINDA FRAZIER BUSINESS MANAGER JUNE 2016 2 Table of Contents Introduction...3 Internal Controls Questionnaire...4

1 INTERNAL CONTROLS MANUAL DICKSON COUNTY SCHOOLS DANNY L. WEEKS, ED.D. DIRECTOR OF SCHOOLS LINDA FRAZIER BUSINESS MANAGER JUNE 2016 2 Table of Contents Introduction...3 Internal Controls Questionnaire...4

REPORT OF INTERNAL AUDIT

REPORT OF INTERNAL AUDIT PRESENTED TO AUDIT/TASK: #09-07, City Hiring Practices AUDIT CLIENT: Human Resources AUDIT DATE: June 30, 2009 REPORT DATE: December 31, 2009 AUDITOR: Steven Rehn CIA, CFSA APPROVAL:

REPORT OF INTERNAL AUDIT PRESENTED TO AUDIT/TASK: #09-07, City Hiring Practices AUDIT CLIENT: Human Resources AUDIT DATE: June 30, 2009 REPORT DATE: December 31, 2009 AUDITOR: Steven Rehn CIA, CFSA APPROVAL:

Sonoma County. Internal Audit Report. Auditor Controller Treasurer Tax Collector. Sonoma County Payroll Process

For the Period: July 1, 2011 to June 30, 2015 Sonoma County Auditor Controller Treasurer Tax Collector Internal Audit Report Engagement No: 4050 Report Date: May 31, 2016 Donna M. Dunk, CPA Auditor Controller

For the Period: July 1, 2011 to June 30, 2015 Sonoma County Auditor Controller Treasurer Tax Collector Internal Audit Report Engagement No: 4050 Report Date: May 31, 2016 Donna M. Dunk, CPA Auditor Controller

Prince William County, Virginia

Prince William County, Virginia Internal Audit of Procurement Card Management Fiscal Year 2014/2015 Prepared By: Internal Auditors June 29, 2015 Table of Contents Transmittal Letter... 1 Executive Summary...

Prince William County, Virginia Internal Audit of Procurement Card Management Fiscal Year 2014/2015 Prepared By: Internal Auditors June 29, 2015 Table of Contents Transmittal Letter... 1 Executive Summary...

STATE OF NORTH CAROLINA

STATE OF NORTH CAROLINA PERFORMANCE AUDIT NORTH CAROLINA DEPARTMENT OF TRANSPORTATION FERRY DIVISION JULY 2011 OFFICE OF THE STATE AUDITOR BETH A. WOOD, CPA STATE AUDITOR PERFORMANCE AUDIT NORTH CAROLINA

STATE OF NORTH CAROLINA PERFORMANCE AUDIT NORTH CAROLINA DEPARTMENT OF TRANSPORTATION FERRY DIVISION JULY 2011 OFFICE OF THE STATE AUDITOR BETH A. WOOD, CPA STATE AUDITOR PERFORMANCE AUDIT NORTH CAROLINA

UNFPA. This policy applies to all UNFPA personnel, particularly those involved in the purchasing and payment of goods and services.

Policy Title Previous title (if any) Policy objective Target audience Risk Matrix Policy and Procedures for Accounts Payable n/a The Policy and Procedures for Accounts Payable policy establishes the procedures

Policy Title Previous title (if any) Policy objective Target audience Risk Matrix Policy and Procedures for Accounts Payable n/a The Policy and Procedures for Accounts Payable policy establishes the procedures

Quality Control Review of Air Force Audit Agency s Special Access Program Audits (Report No. D )

") August 26, 2005 Oversight Review Quality Control Review of Air Force Audit Agency s Special Access Program Audits (Report No. D-2005-6-009) Department of Defense Office of the Inspector General Quality

August 26, 2005 Oversight Review Quality Control Review of Air Force Audit Agency s Special Access Program Audits (Report No. D-2005-6-009) Department of Defense Office of the Inspector General Quality

Table of Contents. Temporary Custodian Services

Table of Contents Temporary Custodian Services July, 2012 Page Number BACKGROUND 2 OBJECTIVE 2 SCOPE AND METHODOLOGY 2 FINDINGS AND RECOMMENDATIONS 2-4 BACKGROUND The district has a contract with an agency

Table of Contents Temporary Custodian Services July, 2012 Page Number BACKGROUND 2 OBJECTIVE 2 SCOPE AND METHODOLOGY 2 FINDINGS AND RECOMMENDATIONS 2-4 BACKGROUND The district has a contract with an agency

Page 1 of VACANT EXISTING PERMANENT, TEMPORARY, OR PART TIME POSITIONS

Page 1 of 7 Hiring Policy PURPOSE This policy outlines the procedures for recruiting and hiring County personnel for all positions except the position of Chief Administrative Officer County Administrator.

Page 1 of 7 Hiring Policy PURPOSE This policy outlines the procedures for recruiting and hiring County personnel for all positions except the position of Chief Administrative Officer County Administrator.

Prairielands Groundwater Conservation District Accepting Applications for General Manager

Prairielands Groundwater Conservation District Accepting Applications for General Manager POSITION: IMMEDIATE SUPERVISOR: General Manager Board of Directors JOB SUMMARY: The Prairielands Groundwater Conservation

Prairielands Groundwater Conservation District Accepting Applications for General Manager POSITION: IMMEDIATE SUPERVISOR: General Manager Board of Directors JOB SUMMARY: The Prairielands Groundwater Conservation

Audit of Management Staff Reductions for Select Crown Corporations

Audit of Management Staff Reductions for Select Crown Corporations PREPARED BY: CONTACTS: MNP LLP 2500 201 Portage Ave. Winnipeg, MB R3B 3K6 Kathryn Graham 204.336.6243 REPORT November 9, 2018 TABLE OF

Audit of Management Staff Reductions for Select Crown Corporations PREPARED BY: CONTACTS: MNP LLP 2500 201 Portage Ave. Winnipeg, MB R3B 3K6 Kathryn Graham 204.336.6243 REPORT November 9, 2018 TABLE OF

Audit Follow Up. Citywide Disbursements (Report #0410, Issued April 15, 2004) As of September 30, Summary

As of September 30, Summary") Audit Follow Up As of September 30, 2004 Sam M. McCall, CPA, CGFM, CIA, CGAP City Auditor Citywide Disbursements - 2003 (Report #0410, Issued April 15, 2004) Report #0521 March 28, 2005 Summary City departments

Audit Follow Up As of September 30, 2004 Sam M. McCall, CPA, CGFM, CIA, CGAP City Auditor Citywide Disbursements - 2003 (Report #0410, Issued April 15, 2004) Report #0521 March 28, 2005 Summary City departments

APPENDIX 2 COMMUNITY DEVELOPMENT COMMISSION FINANCIAL CHECKLIST REQUIRED FOR ALL APPLICANTS (A SITE VISIT MAY BE CONDUCTED LATER)

") REQUIRED FOR ALL APPLICANTS (A SITE VISIT MAY BE CONDUCTED LATER) AGENCY NAME: AGENCY ADDRESS AGENCY PHONE: DATE PREPARED: PREPARED BY: TITLE: EMAIL: AGENCY GENERAL INFORMATION EXECUTIVE DIRECTOR /CITY

REQUIRED FOR ALL APPLICANTS (A SITE VISIT MAY BE CONDUCTED LATER) AGENCY NAME: AGENCY ADDRESS AGENCY PHONE: DATE PREPARED: PREPARED BY: TITLE: EMAIL: AGENCY GENERAL INFORMATION EXECUTIVE DIRECTOR /CITY

Department of Biology

THE UNIVERSITY OF TEXAS-PAN AMERICAN OFFICE OF AUDITS & CONSULTING SERVICES Department of Biology Report No. 14-10 OFFICE OF INTERNAL AUDITS THE UNIVERSITY OF TEXAS - PAN AMERICAN 1201 West University

THE UNIVERSITY OF TEXAS-PAN AMERICAN OFFICE OF AUDITS & CONSULTING SERVICES Department of Biology Report No. 14-10 OFFICE OF INTERNAL AUDITS THE UNIVERSITY OF TEXAS - PAN AMERICAN 1201 West University

PHYSICAL PLANT DEPARTMENT MAINTENANCE AND PLANNING DIVISION AUDIT OF ALLEGED CONFLICT OF INTEREST

PHYSICAL PLANT DEPARTMENT MAINTENANCE AND PLANNING DIVISION AUDIT OF ALLEGED CONFLICT OF INTEREST THE UNIVERSITY OF NEW MEXICO September 8, 2009 J.E. Gene Gallegos, Chair Carolyn Abeita, Vice Chair James

PHYSICAL PLANT DEPARTMENT MAINTENANCE AND PLANNING DIVISION AUDIT OF ALLEGED CONFLICT OF INTEREST THE UNIVERSITY OF NEW MEXICO September 8, 2009 J.E. Gene Gallegos, Chair Carolyn Abeita, Vice Chair James

PERSONNEL COMMISSION. Class Code: 5128 Salary Range: 34 (C1) PURCHASING AGENT JOB SUMMARY

PURCHASING AGENT JOB SUMMARY") PERSONNEL COMMISSION Class Code: 5128 Salary Range: 34 (C1) PURCHASING AGENT JOB SUMMARY Under general supervision, perform a variety of specialized duties related to the procurement, receipt, distribution

PERSONNEL COMMISSION Class Code: 5128 Salary Range: 34 (C1) PURCHASING AGENT JOB SUMMARY Under general supervision, perform a variety of specialized duties related to the procurement, receipt, distribution

UNIVERSITY OF NEVADA, LAS VEGAS HARRY REID CENTER FOR ENVIRONMENTAL STUDIES Internal Audit Report July 1, 2007 through June 30, 2008

UNIVERSITY OF NEVADA, LAS VEGAS HARRY REID CENTER FOR ENVIRONMENTAL STUDIES Internal Audit Report July 1, 2007 through June 30, 2008 GENERAL OVERVIEW The Harry Reid Center (HRC) at the University of Nevada,

UNIVERSITY OF NEVADA, LAS VEGAS HARRY REID CENTER FOR ENVIRONMENTAL STUDIES Internal Audit Report July 1, 2007 through June 30, 2008 GENERAL OVERVIEW The Harry Reid Center (HRC) at the University of Nevada,

Procurement and Contracting Operations Audit

D..1D Procurement and Contracting Operations Audit Office of the Chief Audit Executive February 016 Cette publication est également disponible en français. This publication is available in accessible PDF

D..1D Procurement and Contracting Operations Audit Office of the Chief Audit Executive February 016 Cette publication est également disponible en français. This publication is available in accessible PDF

APPENDIX A - CAO-A-1307

APPENDIX A - CAO-A-1307 INTERNAL AUDIT REPORT Procurement Controls and Compliance Final Report June 20, 2013 Prepared by: Katherine Gray, Supervisor, Service Performance and Development Loretta Alonzo,

APPENDIX A - CAO-A-1307 INTERNAL AUDIT REPORT Procurement Controls and Compliance Final Report June 20, 2013 Prepared by: Katherine Gray, Supervisor, Service Performance and Development Loretta Alonzo,

Audit of Public Works Overtime

T. Bert Fletcher, CPA, CGMA City Auditor HIGHLIGHTS Highlights of City Auditor Report #1618, a report to the City Commission and City management WHY THIS AUDIT WAS DONE From October 1, 2011, through September

T. Bert Fletcher, CPA, CGMA City Auditor HIGHLIGHTS Highlights of City Auditor Report #1618, a report to the City Commission and City management WHY THIS AUDIT WAS DONE From October 1, 2011, through September

Village of Farmingdale

DIVISION OF LOCAL GOVERNMENT AND SCHOOL ACCOUNTABILITY REPORT OF EXAMINATION 2018M-100 Village of Farmingdale Procurement, Claims Audit and Check Signing OCTOBER 2018 Contents Report Highlights.............................

DIVISION OF LOCAL GOVERNMENT AND SCHOOL ACCOUNTABILITY REPORT OF EXAMINATION 2018M-100 Village of Farmingdale Procurement, Claims Audit and Check Signing OCTOBER 2018 Contents Report Highlights.............................