Why Bulgaria Investment Atlas

|

|

|

- Beryl Farmer

- 6 years ago

- Views:

Transcription

1 Why Bulgaria Investment Atlas 2017

2 Forton is a premium commercial real estate advisory company. We are a subsidiary of AG Capital, the largest real estate company in Bulgaria, and Member of the Cushman & Wakefield Alliance in Bulgaria and Macedonia. Our alliance with Cushman & Wakefield, the world s largest privately owned real estate advisory firm, contributes to the successful blend of local real estate insight and experience with international expertise. So is Cushman & Wakefield our gateway to investors in more than 60 countries all over the world. We employ this hands-on experience to add value to our clients real estate projects and developments. We offer the following advantages: Strict application of Cushman & Wakefield s methodology and professional quality standards. Full compliance with the Royal Institution of Chartered Surveyors (RICS) ethical standards (Red Book 2014) and the International Valuation Standards Among the biggest real estate consultancy companies in Bulgaria Forton is the only RICS regulated firm and the only company that has 3 certified RICS members. At present Forton has 2 Registered Valuers by RICS. Complete coverage of the Bulgarian commercial real estate market. Access to knowledge and data within Bulgaria s leading real estate service group, involved in all important markets and all property types.

, NATO Member (2004) Political and business stability - EU Member; Currency board; Low budget deficit and")

3 Bulgaria Key Facts Area: 110,910 sq. km Population: 7.1 million (2016) Capital City: Sofia Currency: Lev (BGN). Fixed exchange rate pegged to Euro Government type: parliamentary republic EU Member (2007), NATO Member (2004) Political and business stability - EU Member; Currency board; Low budget deficit and government debt Low cost of doing business - 10% corporate tax rate (0% in high unemployment areas); 10% personal income tax; Lowest cost of labor within EU; Favorable office rents and low cost of utilities Educated and skilled workforce Government incentives

4

5 Optional Section Divider Economy

6 Economy Economic Growth Projected to Remain on a Sustainable Path The Labour Market Has Seen Marked Improvements Public Investment Gets Strong Support from EU Funds Bulgaria is a member of the European Union since 2007 and benefits significantly from the trade with EU countries (exports to EU members grew by 7.2% in 2016), as well as from the investment support of the European Structural and Investment Funds. Over the Bulgarian economy has been growing at a faster pace than EU-28 and this trend is expected to continue over the forecast period Bulgarian GDP is estimated at ca. EUR 42.7 billion in 2016, increasing by 3.4% in real terms, which was above the estimates of the international financial institutions. The better-than-expected results were mainly driven by the higher domestic consumption stemming from the increased income and falling unemployment. Based on the improved macroeconomic indicators, IMF raised its GDP growth forecast to 2.9% for 2017 and 2.7% for Going forward, the positive effect of growing net exports is expected to diminish, with oil prices rising and uncertainty in the EU, while consumption and investment will have greater contribution to GDP growth. Economic growth is expected to be further supported by EU funds, with a total budget of EUR 11.7 billion secured for the period and directed at creating jobs, developing infrastructure, providing an innovation-friendly business environment, etc Inflation Real GDP growth, % Bulgaria EU-28 Consumer price inflation, % The introduction of a Currency Board in 1997 helped stabilise the country following a period of hyperinflation. Since the second half of 2013, the economy entered a deflationary period that continued until Falling consumer prices were mainly driven by supply-side factors including decreasing food and energy prices. In the coming years, inflation is expected to increase gradually,

7 converging to the overall EU level of around 2% in the long term. Labour market After the unemployment rate peaked at 13% in 2013, the labour market improved continuously in the next three years. Following the positive recent developments, IMF lowered its forecast for Bulgaria s unemployment and expects the rate to stabilise at around 6.6% in the long term. The decrease will be driven by both new jobs creation and expected increase in the labour participation rate as a result of the ongoing pension reform (increasing the age and length of service needed for retirement). Yet, important challenges in the labour market relate to the shrinking population due to emigration and declining fertility rates. Fiscal stability The authorities are targeting to gradually decrease fiscal deficit to zero by 2020, which will also help reduce government debt to below 25% of GDP. Currently Bulgaria benefits from a relatively low government debt, which provides a substantial buffer against unexpected economic volatilities. IMF forecasts a slight downward trend in the general government gross debt as a percentage of GDP in the next few years. Bulgaria has enjoyed favourable financing conditions in recent years, both in terms of access and yields. In March 2017, the secondary market yield on Bulgaria s government bonds Unemployment rate, % Government gross debt (2016) as % of GDP with maturities close to ten years was 1.73% (compared to 0.35% on the German bonds of similar maturity). The yields for short-term bonds are also at historically low levels. The country s current long-term credit rating is BB+ with a stable outlook according to Standard&Poor s (last update in December 2016) and Baa2 according to Moody s (last update in June 2015). The economic overview is prepared by

8

9 Optional Section Divider Office Market

10 Office Market Office Market is Going Full Steam Ahead New Office Zones Emerge alongside Main Roads and in the Central Part of Sofia Along with Sofia, Secondary Cities Draw IT and BPO Industries Attention Overview Bulgarian office market is on the way of sustainable growth based on strong leasing and development activity. The last several years were marked by stable rent increase and rising demand for quality space which stimulate developers to start or to resume office projects that have been put on hold. In the middle term the new supply is forecasted to slightly push vacancy up while at present the shortage of prime space remains a challenge. As in the previous years, the IT and BPO industries are key demand drivers alongside more traditional customers from the financial and pharma industries. Sofia is the most active leasing market but with the expansion of the outsourcing industry secondary cities as Plovdiv, Varna and Burgas also demonstrate growth potential. Hot spots Sofia With 1.6 million square meters class A and B stock, Sofia is the most developed and well diversified office market in the country and highly competitive location within South Eastern SQM, THOUSANDS SQM, THOUSANDS Completions (f) 2018 (f) Q1 Q2-Q (f) 2018 (f) STOCK Stock & Pipeline PIPELINE Europe. The city is appealing office location, thanks to the high-quality supply, affordable rents and low operational costs. Well educated workforce with good knowledge of foreign languages is another competitive advantage. The inquiries of IT and BPO companies have had the most positive impact on the office market over the last few years. These tenants accounted for more than 60 per cent of the leasing volume in 2016 and are expected to remain key market

by the outsourcing company Telus International.")

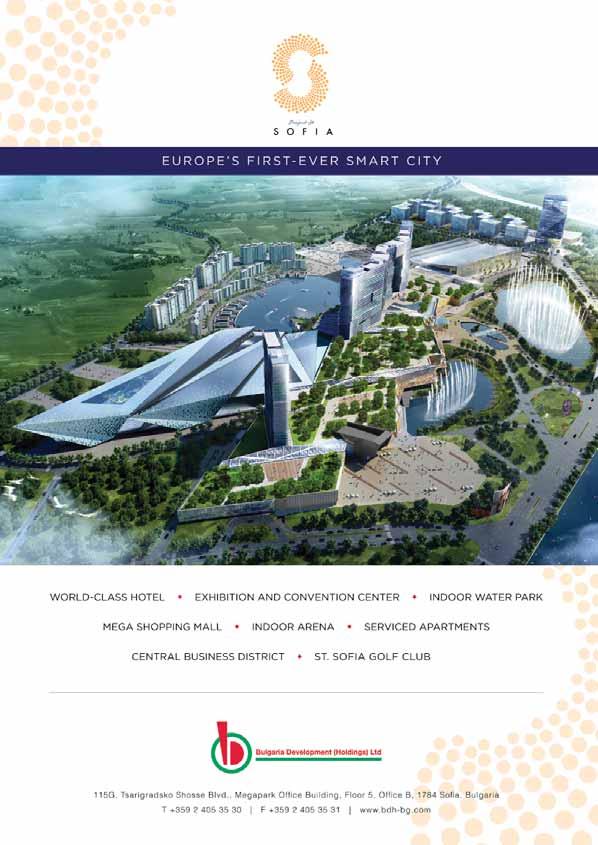

11 driver. Part of these companies expand their operations, while others consolidate their business as a result of mergers and acquisitions and need more office space. The most notable example is the prelease of 20,000 square meters in City Tower (34,000 sqm GLA) by the outsourcing company Telus International. This is the biggest deal for the last few years and consolidates part of the company s offices in one building. With the prelease of 10,000 sqm the IT services and solutions provider Bulpros is the largest tenant in Building 15 of Business Park Sofia, which is currently under construction. The company will relocate after the completion of the building with 20,800 square meters GLA in H In general, the IT and BPO s inquiries are for prime offices with easy access, enough parking places and flexible working space. Locations alongside main roads and near metro stations are preferred and attract developers attention. As a result, new business zones emerge on the Sofia s map together with the established areas. The combination of emblematic office projects, main road location and metro station makes the area around Capital Fort on Tsarigradsko Shose Blvd. prominent business location. Currently about 100,000 sqm new offices are under construction or in planning phase in close vicinity, including Sky Fort (202 m) the new tallest office building in Sofia. The area between Nikola Vaptsarov Blvd. and the shopping center Paradise in the south part of Sofia is also rapidly developing with potential for construction of 90,000 sqm new office space. Another 100,000 sqm offices are expected to be completed over the next few years in the Business Park Sofia area. Garitage Park, Richhill Business Center, Advance Business Center and the second building of the investor in Adora Office Center are among the notable projects. SQM, THOUSANDS SQM, THOUSANDS Take up (f) Q1 Q2-Q OCCUPIED Occupancy rate VACANT The Central Business Zone with 55,000 sqm under development and the area alongside Todor Alexandrov Blvd. are other emerging office locations. As a whole, the abovementioned locations represent about 70 per cent of the total office pipeline in Sofia by As of H more than 340,000 sqm are under construction and another 170,000 sqm in planning phase. The delivery of this space is forecasted to slightly increase the vacancy rate, which currently stands at 9.6 per cent. With ,000 sqm annual take-up and about per cent net absorption, this supply is expected to be absorbed in the next four years. For the time being, the market suffers from a shortage of prime space with a large share

12 Office Market Office Market is Going Full Steam Ahead of preleases in the total volume. Even so, the developers have to be careful, bearing in mind the demand fluctuations. In a long run, some developers are looking for opportunities outside Sofia borders. Such is the case with the multifunctional project Saint Sofia in Musachevo village area which will comprise 785,000 square meters offices. The investor Bulgaria Development Holdings Limited intends to establish a business hub with the newest technology and modern design from Asia, efficient area distribution and high-tech capabilities. Secondary cities Along with Sofia, the second largest city Plovdiv gains popularity as outsourcing destination and a number of IT and shared services firms are looking to establish operations there. Fast growing companies such as Telus, Speedflow, Scale Focus, Sofica Group, SB Tech and 60K already have offices in Plovdiv, some of them announcing plans for further expansion. Outside Sofia, Plovdiv is the most developed office location with class A stock of about 50,000 sqm and 36,000 sqm under construction, as of H Other locations with potential for BPO operations are Burgas and Varna. These cities are large economic and university centres with high proportion of young, well-educated people. IT and shared services companies as Bulpros, Adecco, Sitel are presented in Varna, while Sutherland has chosen Burgas to open second Bulgarian office. Rents /SQM/MONTH 13,50 13,00 12,50 12, (f) 2018 (f) RENT Rents & Yields YIELD 9,50% 9,00% 8,50% 8,00% 7,50% 7,00% The headline rents for Class A office space in Sofia range between 13 and 13.5 per square meter. Highest levels are registered in the central business area and alongside the main boulevards. In the last two years, the prices have steadily increased, fueled by the scarcity of prime office space and increasing demand. Now, the growing supply stabilizes the rents. Rental levels for class B space are stable in the range of 6-8/sqm/month. The rates outside Sofia range from 6 to 9/sqm/ month, in particular for Varna and Plovdiv. Rents in Burgas are stable at 6 per square meters.

13

14

15 Optional Section Divider Industrial Market

16 Industrial Market Industrial Property Market Continues on a Growth Path Bulgaria Remains in the Focus of Manufacturing Companies Sofia and Plovdiv are Logistics Hot-Spots OVERVIEW Bulgarian industrial property market has experienced sustainable development during the last few years, without significant fluctuations in prices and inquiries. Market performance is driven by the economic growth and the stable demand of warehouse and production space. Automotive parts suppliers, as well as expanding logistics and retail business are main source of growth countrywide. Thanks to overall stability, EU membership, low taxation and operating costs and attractive payroll to productivity ratio Bulgaria remains in the focus of manufacturing companies, aiming to outsource some of their operations. Locations with sufficient infrastructure and skilled labor force are preferred for development of new projects. HOT SPOTS Sofia Sofia is the largest real estate market countrywide and cross point of three European Transport Corridors. The combination of road and railway Sofia market - Annual Completions (f) Q1 Q2-Q4 infrastructure and international airport makes the capital city highly preferred location for logistic operations. Central storage facilities of major FMCG retailers and warehouses of international 3PL providers are mainly concentrated east of Sofia, in the area between the ring road and Elin Pelin Musachevo Novi Han industrial area. Among the notable projects under development in the area are both storage facilities and clean productions such as the Automotive Leather Company (ALC) Group, Nobel Solar Solutions, dm Drogeriemarkt, Maxima, Billa, Lidl and large industrial parks offering build-to-suit and speculative space, such as Logistic Park East Ring, Industrial Park Sofia East and Logistics Park Sofia Ring. West of Sofia, Danish based everything for home

17 retail chain JYSK acquired 30 ha for 92,300 sqm logistics and distribution center in the state-run Bozhurishte Economic Zone. The first phase of the storage facility is already under construction and will serve company s operations in the Balkans and Hungary. Behr-Hella Thermocontrol production facility and R&D center is yet another considerable project in the industrial zone. The new manufacturing facility of global supplier of climbing walls Walltopia is also being developed. In this corner of Sofia also facilitates the DB Schenker central warehouse, Coca-Cola production site and a number of logistics and industrial parks under development. As of H the industrial property stock in Sofia is totaling 911,000 sqm, mostly owner-occupied facilities. The shortage of modern supply in combination with the growing demand from retail and logistics business provides good ground for new build-to-suit and speculative developments. The new office and distribution center of DHL in Sofia Airport is among the marked build-tosuit projects under construction. Sofia airport also facilitates Lufthansa Technik premises - one of the most successful maintenance centers of the company across Europe and it s up to its successive expansion. Lufthansa Technik are present in Sofia since 2008, are investing EUR 30 mln in the new maintenance unit and administrative building. sqm, thousands Plovdiv Sofia Market - Stock & Pipeline STOCK ACTIVE PIPELINE The second largest Bulgarian city Plovdiv, is an important manufacturing and logistics center, thanks to the convenient location, easy access and availability of skilled workforce. The largest industrial project in the region is Trakia Economic Zone (TEZ) which spreads on more than 1000 ha. Currently, about 140 companies are operating within the zone mostly auto part suppliers and light industrial firms. Worth mentioning are the factories of ABB, Liebherr, Schneider Electric, Socotab, Sensata, Magna Powertrain, SMC Automation, Willy Elbe and Osram Lightings. The largest storage and distribution center (currently over sqm) in Bulgaria is also located here the German food retailer Kaufland

18 Industrial Market Industrial Property Market Continues on a Growth Path operates its country logistics from Plovidv. The 3PL operator DB Schenker, also maintain a 6,000 sqm warehouse facility after the second expansion in Sofia Market - Take up South/South-East The South-East region is highly attractive for new production developments due to the availability of workforce and location advantages. The Japanese automotive wire harness producer Yazaki is among the notable examples with two factories in Sliven and Yambol and a third one under construction in the Dimitrovgrad. Meanwhile the company started pilot factory operations in Stara Zagora after a former retail store was converted into production facility to meet the specific needs. The completion of Trakia and Maritsa Highways boosted the investments in the regional cities alongside, such as Haskovo, Kardzhali, Yambol and Sliven. For example, Haskovo region has been chosen by the Turkish supplier of plasticbased products Sa-Ba for the construction of a new factory in Bulgaria. Thanks to its strategic position on the road between Turkey and Europe, Stara Zagora hosts the first foreign factory of the automotive seals producer Standard Profile. The company doubled its production capacity in Bulgaria in the recent years. The largest city in South-Eastern Bulgaria and Black-Sea port Burgas, is also providing (f) Q1 opportunities for industrial development thanks to the combination of road and railway infrastructure, sea port and international airport. In general, the good transport connections make the South-East region suitable for logistics. The second Bulgarian distribution centre of German FMCG discounter Lidl in Yambol exemplifies the trend. The project has easy access to Trakia Highway and with 47,000 sqm built-up area is the largest logistics facility completed in North/North-East Q2-Q4 North-East part of Bulgaria provides benefits being the sea port in Varna, access to sufficient labor market and availability of production brownfields. While Sofia and Plovdiv are interesting for logistics because of their proximity to highways, smaller

19 regional cities in the northern part of the country are attractive for a variety of industries mainly aiming at low operating costs. Turkish glass maker Sisecam, Danish Carlsberg Group, the local manufacturers, such as Lavena and the Ficosota Holding are some of the largest industrial employers in Shumen Targovishte region. Last year, the region attracted another large investor - the German based Dr. Bock Industries plans to build a textile processing facility on 2.1 ha in Targovishte. The new ceramic factory of Akgun Seramik is yet another ongoing project in this part of the country. Ruse is also an industrial and logistics hub in that region. The city is the largest Danube river port in Bulgaria and a crossing point of two Pan European routes: Corridor 7 and Corridor 9. The city provides direct connection to Romania via the Danube bridge. For these reasons, auto part producers, such as French manufacturer of aluminum components Montupet and German Witte Automotive, choose Ruse to establish operations in Bulgaria. Textile industry is also largely presented in the region. West/North and West The northwestern part of Bulgaria has industrial traditions and potential for cost sensitive manufacturing although the local economy underperforms. The region benefits from the sqm, thousands Sofia Market - Vacancy Rate OCCUPIED VACANT proximity to the second Danube bridge Vidin Kalafat, the ferryboat connections to Romania and the Pan-European Corridor IV crossing the area. The North-West has strong traditions in the chemicals, textiles, food and beverage industry, as well as in the agriculture. In the last several years the automotive industry received a strong impetus with the opening of a number of factories producing cable harnesses for cars. The German manufacturer Nexans Autoelectric opened a production facility in Pleven in the fall of 2014, creating 600 new jobs. In Mezdra, German- Japanese SE Borndnetze produces wire harnesses for a variety of automobile platforms. Bulgarian car battery maker Monbat has a factory in Montana and expands with recycling facilities on neighbor markets.

20 Industrial Market Industrial Property Market Continues on a Growth Path In the west part of Bulgaria, Botevgrad and Pernik are the most active municipalities with industrial facilities. Both cities take advantage from the proximity to Pan-European Corridor IV as well as the good transport connection to Sofia. First Bulgarian plant of the US-based producer of sensors Sensata operates in Botevgrad, together with R&D center in Sofia and second factory recently opened in Plovdiv. Pernik is mostly known for the steel manufacturing and mining industry but the local authorities and private investors consider establishing a logistics and industrial park on a ha land plot at the intersection of Corridors IV and VIII. RENTS Sofia is the biggest and the most developed lease market in the country due to the large speculative projects developed in the region. After years of stagnation, 2015 and 2016 was marked by slight rental growth and now due to the raising demand of industrial space. Now the levels for prime logistic space are stable at 4.20 /sqm. Rents are higher for the prime logistics area near Sofia Airport, exceeding 5 /sqm. Since the annual supply of speculative space does not exceed 30,000 40,000 sqm, the market is balanced and rents are forecasted to remain stable. Land market is also active due to the strong 4,50 4,00 3,50 3,00 2,50 2,00 1,50 1,00 0,50 0,00 Sofia Market - Rents & Yields (f) Rent Yield 14,00% 12,00% 10,00% 8,00% 6,00% 4,00% 2,00% 0,00% development activity in the big cities and industrial zones. Prices for urbanized pre-developed plots of land are in the range of 15-20/sqm average countrywide. The restructuring of some real estate funds, in the possession of large pieces of land, opens the door to development of mid-size logistics and industrial projects (5,000 to 10,000 sqm GLA) across the country.

21 Industrial Revolution in Bulgaria 2017

22

23 Optional Section Divider Retail Market

24 Retail Market Retail Market: in the Mood to Expand Developers' Focus Shifts on Multifunctional Projects with Large Shopping Areas Prime Rents Slightly Increase Reflecting Consumption Growth and Tenant Appetite for Expansion OVERVIEW The stable growth of consumption and strong economic performance give a strong impetus to the Bulgarian retail market. Improving purchasing power stimulates the expansion of a number of shopping segments which results in active leasing market. Fashion, Health & Beauty and FMCG are the most rapidly growing categories. With almost 900,000 square meters stock the retail property market provides a variety of opportunities for penetration of new brands and for enlargement of the ones already presented. After the years of strong development activity, now the retail segment is entering more mature phase. The market is relatively saturated and now it is time for the existing shopping centers and retail parks to reposition. HOT SPOTS Shopping Centers As of H the total shopping centers stock reached 738,000 sqm with over half of this space situated in Sofia where 9 malls are operating. The capital city is the largest market with high proportion of young people and above-average incomes. For that reason, a prevailing part of retail projects is concentrated here. In the booming years, a number of shopping centers and retail parks were completed in the secondary cities, as well. Now, the market is well saturated and development activity is slowing down with only one scheme completed in the last couple of years. Markovo Tepe Mall (20,500 sqm GLA), which opened in Plovdiv,

in the fall of 2016, following full restructuring and tenant mix refreshment.")

25 was the sole new delivery for the period. In Sofia, it is worth mentioning the rebranding of City Center Sofia as Park Center (23,500 sqm GLA) in the fall of 2016, following full restructuring and tenant mix refreshment. Strong competition shifts the development focus on multifunctional projects where retailers could capitalize on the synergy between different types of space. Such is the case with Grand Kanyon which obtained building permit in the spring of The project of the Turkish developer Garanti Koza will have build-up area of 250,000 square meters, comprising residential and hotel parts along with 40,000 square meters retail zone. The second Sofia s project of the company Sofia Square, is also planned as mixed-use development with a large shopping area. The market countrywide is driven mostly by the expansion of middle to budget class fashion brands, while upscale tenants strengthen their presence mostly in Sofia. H&M, LC Waikiki, Polish shoes retailer CCC are rapidly growing with focus on secondary cities. Toys brands, drugstore chains, sport goods retailers are among the other active groups of tenants countrywide. Food & Beverage is another rapidly growing category. The increasing presence of international cuisines, such as Asian, Spanish, Serbian, American burgers and steak houses is evident in the streets and the large shopping centers. The entry of Asian fusion chain Wagamama in Sofia in H also supports the trend. In general, although a number of international fashion retailers entered Bulgaria in the last several years, there is still room for new brands. The limited variety in the different market segments remains a challenge.

26 Retail Market Retail Market: in the Mood to Expand DIY and FMCG The increasing purchasing power in Sofia and the big cities revived the home décor and Do It Yourself segments on the retail market. Large international brands are in expansion mode, aiming at strengthening their positions not only in Bulgaria, but in South-Eastern Europe as a whole. Such example is JYSK which announced plans for 35 stores countrywide and started construction of a huge regional distribution center west of Sofia at the beginning of Do It Yourself chains, such as Praktiker and Homemax (ex-baumax), are also active in the retail market. After the opening of the first Bulgarian store in 2011, IKEA aims to increase its presence across the country through smaller format stores. The furniture chain entered the largest Black Sea coast cities Varna and Burgas, with first order & collect points in Large shifts occur in the FMCG retail, as well. The withdrawal of Carrefour and the insolvency procedure of Piccadilly, a local chain of supermarkets, resulted in increasing vacancy rates in many shopping centers across the country. In some cases, the abovementioned retailers were replaced by Lidl and Billa, in others the vacated space opened room for big-box tenants, such as JYSK, IKEA and Jumbo Toys, to enter shopping Stara Zagora Burgas Gabrovo Sofia Varna Veliko Tarnovo Ruse Pleven Plovdiv Bulgaria Shopping Center GLA Density IN SQM PER 1000 OF THE POPULATION 0 0,1 0,2 0,3 0,4

27 centers. In general, after the years of rapid growth now the retailers are refining their market positions. Some of them take the opportunity also to diversify their sales channels. Rental levels Rents in Sofia rebounded, supported by the growing consumption and the reviving retailers interest. Prime levels in the shopping centers continue to slightly increase, reaching 31/sqm/ month in H with prospect for further growth. Since the market is back on the way of growth, landlords seize the momentum to raise revenues. Prime locations on main streets, such as Vitosha Blvd. in Sofia, also register increasing tenant interest. After the years of recovery, the rent for 100 square meters store remains stable at 46/sqm/ month.

28

29 Optional Section Divider Investment Market

30 Investment Market Capital Goes After Prime Assets for the First Time Since 2011 Investor Profile Moves from Opportunistic to Value-add Prime Shopping Centers Take Center Stage As at the first half of 2017 Bulgaria has finally started to reap the benefits of the CEE real estate investment market growth story. With investors closing in on several big-ticket acquisitions, institutional quality transactions are expected to post a turnaround this year, easily surpassing the development land and the distressed segments which dominated the market since This is not to say that land and distressed transactions are missing but they would be dwarfed by the sheer size of the income-generating commercial real estate sector, even if only a part of the present pipeline materializes. After real estate capital flows went up to their highest level since 2008 in 2016 several large transactions in the pipeline may bring 2017 into that orbit again and make 2016 s trading look small-time. Investment was already 90 mln well into the first half of the year with at least two large transactions expected to bring the number to 150 million, already more than half the 283 million in Forecasts are in the area of million this year, depending on the several large transactions. There has been a notable shift from opportunistic to value-add deal-making. In part this reflects the changing profile of investors with more balanced strategies now present along with the high-risk and development-focused, mainly local and regional players who have dominated the scene in the recent years. The second part of the explanation is that distressed opportunities are now more limited and concentrated in sales of non-performing loan portfolios (and, unsurprisingly, international investors are involved again). Growth Story Investor interest is underpinned by steady GDP growth at more than 3 per cent in 2015 and 2016, recovery of household spending consumption and private investment which supported the strongest economic expansion since 2008 in finished on a similar note despite a cyclical slowdown in consumption. The above has helped the continued recovery of the occupier markets. Offices are seen ahead in the market cycle with strong interest in development supporting the land market in Sofia. So is residential where recent price rises have spurred end-user demand and land acquisitions. Retail Focus Across segments shopping centers have taken the dominant position with large deals getting publicity GTC s two malls in Burgas and Stara Zagora respectively. While the deals have signaled the return of large international investors to the market, they also underscored the value-add potential in the segment with prime rents increasing along with opportunity to easily extend the retail offer in the space vacated by the large food hypermarkets over the recent years. Restructuring remains a trend with Mall Varna transacted in May being a case in point although this opportunity appears limited. Prime Sofia offices are also firmly in the radar. Smaller deals, below 10 million, are suitable for local investors while large scale transactions, above 50 million, are in the focus of international investors. An increase in development backed by strong pre-leasing volumes in Sofia s modern office sector

31 looks likely to bring more product in the pipeline over the next couple of years. Mixed-use schemes with substantial office element are also appreciated by investors and developers alike due to the relatively stable cash flows produced by offices which counterbalance the more volatile hotel, retail or residential elements. Industrial real estate is set to remain an opportunity-driven segment due to the scarcity of multi-tenant modern buildings. Local investors are however well-placed to take advantage of opportunities as they emerge, notably the acquisition of the 40,000-sqm logistics and office complex Vienna Real Estate along with additional development potential on the 13-ha site. Although its contribution is likely to be small, hotel investment remains a focus for specialist domestic or regional buyers. The opportunity is now in Sofia where growth in visitation last year supported both occupancy and room rates (f) 2016 Investment Volumes ( mln) Annual To date Forecast Real Estate Investment Sector Split The Outlook Whereas real estate capital has been made available from both domestic and international sources, the latter look likely to overwhelm as foreign investors chase big-ticket deals. The share of cross-border flows which was between per cent of the market over the last five years is now likely to surge to more than 80 per cent. Across geographies, South-African money should dominate, in line with the broader trend across CEE. NEPI, Prime Kapital and several new players have been active in the market. The shift from riskier to prime product has also helped yield expectations tighten, especially in offices and retail. Prime yields are hovering around 8 per cent in both segments with downward 0% 20% 40% 60% 80% 100% offices industrial retail hospitality land pressure caused by capital chasing the top assets and potential income increases due to expansion and rental growth potential priced in. Altogether, Bulgaria s market has started to generate international interest with the availability of reasonably priced product, continued economic growth and the possibility to add value to prime assets through repositioning, re-tenanting and extensions where development potential exists. The outlook therefore remains broadly positive as improved liquidity is likely to make more investors consider this market.

32 47A Tsarigradsko Shose Blvd Sofia, Bulgaria Copyright 2016 Cushman & Wakefield. All rights reserved.

Bulgaria, Logistics Market Overview

Economic Overview During the first 9 months of 2008 Bulgaria registers economic growth of 7%, compared to the same period of 2007. GDP amounts to 48 037.4 million leva. During the period January-October

Economic Overview During the first 9 months of 2008 Bulgaria registers economic growth of 7%, compared to the same period of 2007. GDP amounts to 48 037.4 million leva. During the period January-October

GLOBAL PROPERTY TRENDS. Leonard Michau Director and Head of Africa Operations Broll Property Group

GLOBAL PROPERTY TRENDS Leonard Michau Director and Head of Africa Operations Broll Property Group GLOBAL OFFICE MARKET Global Outlook INTERNATIONAL OFFICE TRENDS US - Demand side, office leasing activity

GLOBAL PROPERTY TRENDS Leonard Michau Director and Head of Africa Operations Broll Property Group GLOBAL OFFICE MARKET Global Outlook INTERNATIONAL OFFICE TRENDS US - Demand side, office leasing activity

HUNGARY. Country Snapshots. First quarter Please click on the appropriate sector to view. Offices Retail Industrial.

Country s First quarter 2017 Please click on the appropriate sector to view Offices Retail Industrial About & Contacts Office Market The Hungarian office market continued to enjoy healthy activity levels

Country s First quarter 2017 Please click on the appropriate sector to view Offices Retail Industrial About & Contacts Office Market The Hungarian office market continued to enjoy healthy activity levels

PROJECT STATISTICS ON FAMILY BUSINESSES IN BULGARIA MAIN RESULTS, 2015

Introduction PROJECT STATISTICS ON FAMILY BUSINESSES IN BULGARIA MAIN RESULTS, 2015 Small and medium-sized enterprises (SMEs) play a crucial role in reaching the objectives of the Europe 2020 Strategy.

Introduction PROJECT STATISTICS ON FAMILY BUSINESSES IN BULGARIA MAIN RESULTS, 2015 Small and medium-sized enterprises (SMEs) play a crucial role in reaching the objectives of the Europe 2020 Strategy.

Business plan of the Mercator Group and the company Poslovni sistem Mercator, d.d., for the year 2018

Business plan of the Mercator Group and the company Poslovni sistem Mercator, d.d., for the year 2018 Ljubljana, December 2017 TABLE OF CONTENTS EXECUTIVE SUMMARY... 1 MERCATOR GROUP COMPOSITION... 2 EFFECT

Business plan of the Mercator Group and the company Poslovni sistem Mercator, d.d., for the year 2018 Ljubljana, December 2017 TABLE OF CONTENTS EXECUTIVE SUMMARY... 1 MERCATOR GROUP COMPOSITION... 2 EFFECT

FINAL METHODOLOGICAL REPORT ON IMPLEMENTAION OF THE ACTION ENTITLED STATISTICS FOR FAMILY BUSINESSES SFB_NSI BULGARIA

Ref. Ares(2017)2891300-09/06/2017 FINAL METHODOLOGICAL REPORT ON IMPLEMENTAION OF THE ACTION ENTITLED STATISTICS FOR FAMILY BUSINESSES SFB_NSI BULGARIA GRANT AGREEMENT NUMBER: 692654 SFB_NSI Bulgaria Prepared

Ref. Ares(2017)2891300-09/06/2017 FINAL METHODOLOGICAL REPORT ON IMPLEMENTAION OF THE ACTION ENTITLED STATISTICS FOR FAMILY BUSINESSES SFB_NSI BULGARIA GRANT AGREEMENT NUMBER: 692654 SFB_NSI Bulgaria Prepared

Jeddah Warehouse & Logistics Market Overview

Warehouse & Logistics Market Overview JEDDAH H 205 Jeddah Warehouse & Logistics Market Overview JEDDAH Jeddah s warehouse and logistics market is currently undergoing a major redevelopment, driven by the

Warehouse & Logistics Market Overview JEDDAH H 205 Jeddah Warehouse & Logistics Market Overview JEDDAH Jeddah s warehouse and logistics market is currently undergoing a major redevelopment, driven by the

Economy. Denmark Market Report Q Slow growth. Annual real GDP growth

Denmark Market Report Q1 15 Economy Slow growth The Danish economy is experiencing an upturn, but growth is low. Statistics Denmark has not yet published the GDP growth rate for the whole of 1, but the

Denmark Market Report Q1 15 Economy Slow growth The Danish economy is experiencing an upturn, but growth is low. Statistics Denmark has not yet published the GDP growth rate for the whole of 1, but the

Development activity driven by Built-to-Suit schemes. Rents and yields remain stable.

Photo credit: YIT Latvia Industrial Market, H1 218 Development activity driven by Built-to-Suit schemes. Rents and yields remain stable. Industrial Stock 922, sq m Vacancy 4.2 % Average Rent 4 EUR/sq m/month

Photo credit: YIT Latvia Industrial Market, H1 218 Development activity driven by Built-to-Suit schemes. Rents and yields remain stable. Industrial Stock 922, sq m Vacancy 4.2 % Average Rent 4 EUR/sq m/month

EUROPEAN LOGISTICS VIEW

EUROPE EUROPEAN LOGISTICS VIEW AUTUMN 2010 Key highlights European Logistics markets The outlook for European logistics markets remains cautiously positive as prime transaction yields compress faster than

EUROPE EUROPEAN LOGISTICS VIEW AUTUMN 2010 Key highlights European Logistics markets The outlook for European logistics markets remains cautiously positive as prime transaction yields compress faster than

FINLAND. Country Snapshots. First quarter Please click on the appropriate sector to view. Offices Retail Industrial.

Country s First quarter 2017 Please click on the appropriate sector to view Offices Retail Industrial About & Contacts Office Market During Q1 2017 the GDP growth estimate for 2016 was revised up by 20

Country s First quarter 2017 Please click on the appropriate sector to view Offices Retail Industrial About & Contacts Office Market During Q1 2017 the GDP growth estimate for 2016 was revised up by 20

The Changing Face of the Industrial Investment Market in Europe

Million The Changing Face of the Industrial Investment Market in Europe By Guy Frampton, SIOR Guy Frampton, RICS, SIOR, CB Richard Ellis, London, England, specializes in and heads up the industrial and

Million The Changing Face of the Industrial Investment Market in Europe By Guy Frampton, SIOR Guy Frampton, RICS, SIOR, CB Richard Ellis, London, England, specializes in and heads up the industrial and

REGIONAL STRUCTURAL ECONOMIC DISPARITIES IN BULGARIA

Trakia Journal of Sciences, No 4, pp 381-385, 2017 Copyright 2017 Trakia University Available online at: http://www.uni-sz.bg ISSN 1313-7069 (print) ISSN 1313-3551 (online) doi:10.15547/tjs.2017.04.021

Trakia Journal of Sciences, No 4, pp 381-385, 2017 Copyright 2017 Trakia University Available online at: http://www.uni-sz.bg ISSN 1313-7069 (print) ISSN 1313-3551 (online) doi:10.15547/tjs.2017.04.021

Logistics Park MULTIMODAL LOGISTICS PARK IN THE CENTER OF EUROPE LINKING EAST AND WEST ON THE NEW SILK ROAD

Logistics Park MULTIMODAL LOGISTICS PARK IN THE CENTER OF EUROPE LINKING EAST AND WEST ON THE NEW SILK ROAD IN BRIEF The underlying idea of Eurohub is to create a logistics and industrial hub bringing

Logistics Park MULTIMODAL LOGISTICS PARK IN THE CENTER OF EUROPE LINKING EAST AND WEST ON THE NEW SILK ROAD IN BRIEF The underlying idea of Eurohub is to create a logistics and industrial hub bringing

INDUSTRY OVERVIEW. The F&S Report was compiled based on the following assumptions:

The information set forth in this section has been derived from the F&S Report. We believe that the sources of the information are appropriate sources for such information, and we have taken reasonable

The information set forth in this section has been derived from the F&S Report. We believe that the sources of the information are appropriate sources for such information, and we have taken reasonable

OVERVIEW THE PORTFOLIO FINANCIAL METRICS ANNEXURES. Our conversation FINANCIAL METRICS. Section ANNEXURES

1 Our conversation Section 01 OVERVIEW Section 02 THE PORTFOLIO Section 03 FINANCIAL METRICS Section 04 ANNEXURES OVERVIEW Section 01 4 Rationale The Polish industrial market, which has a total supply

1 Our conversation Section 01 OVERVIEW Section 02 THE PORTFOLIO Section 03 FINANCIAL METRICS Section 04 ANNEXURES OVERVIEW Section 01 4 Rationale The Polish industrial market, which has a total supply

Vacancy sinks to post-recession low; tightest market in 7 years

El Paso Industrial, Q2 2015 Vacancy sinks to post-recession low; tightest market in 7 years Vacancy Rate 10.9% Avg. Asking Rate 3.87 $/SF Net Absorption 577,578 SF Construction 126,456 SF Completions 0

El Paso Industrial, Q2 2015 Vacancy sinks to post-recession low; tightest market in 7 years Vacancy Rate 10.9% Avg. Asking Rate 3.87 $/SF Net Absorption 577,578 SF Construction 126,456 SF Completions 0

Introduction. Expansion of the Construction Sector

Introduction Kenya Vision 2030 overall goal for the construction sector is to increase its contribution to Gross Domestic Product (GDP) by at least 10% per annum and propel Kenya towards becoming Africa

Introduction Kenya Vision 2030 overall goal for the construction sector is to increase its contribution to Gross Domestic Product (GDP) by at least 10% per annum and propel Kenya towards becoming Africa

HIGHER EDUCATION AS A FACTOR FOR ECONOMIC DEVELOPMENT OF THE REGIONS IN BULGARIA

Trakia Journal of Sciences, Vol. 15, Suppl. 1, pp 66-70, 2017 Copyright 2017 Trakia University Available online at: http://www.uni-sz.bg ISSN 1313-7069 (print) ISSN 1313-3551 (online) doi:10.15547/tjs.2017.s.01.012

Trakia Journal of Sciences, Vol. 15, Suppl. 1, pp 66-70, 2017 Copyright 2017 Trakia University Available online at: http://www.uni-sz.bg ISSN 1313-7069 (print) ISSN 1313-3551 (online) doi:10.15547/tjs.2017.s.01.012

Chapter 9 6/2/10. Global Strategy. Framework for Global Competition. Labor Pooling. Why Do Regions Matter? Technological Spillovers

Chapter 9 Global Strategy Framework for Global Competition The economic logic of global competition depends on the costs and benefits of geographical location Regional advantages National advantages Global

Chapter 9 Global Strategy Framework for Global Competition The economic logic of global competition depends on the costs and benefits of geographical location Regional advantages National advantages Global

Quarterly Market Report

AUSTIN OFFICE OCTOBER EXECUTIVE SUMMARY Vacancy down despite new deliveries to market Austin s overall vacancy rate dropped to 8.4% in, a decrease of 20 basis points quarterover-quarter, and down 10 basis

AUSTIN OFFICE OCTOBER EXECUTIVE SUMMARY Vacancy down despite new deliveries to market Austin s overall vacancy rate dropped to 8.4% in, a decrease of 20 basis points quarterover-quarter, and down 10 basis

1. Foreign Trade Figures in the Czech Republic in 2010

1. Foreign Trade Figures in the Czech Republic in 2010 Foreign trade in the Czech Republic ended 2010 with a surplus of CZK 121.2 billion. Although this is CZK 28.4 billion less than in 2009, it is still

1. Foreign Trade Figures in the Czech Republic in 2010 Foreign trade in the Czech Republic ended 2010 with a surplus of CZK 121.2 billion. Although this is CZK 28.4 billion less than in 2009, it is still

Market Report Serbia

Market Report 2013 Serbia Belgrade Office Market 2013 meant a year of stagnation for the supply side of Belgrade s office market. Hence, the total inventory of Class A and Class B office buildings has

Market Report 2013 Serbia Belgrade Office Market 2013 meant a year of stagnation for the supply side of Belgrade s office market. Hence, the total inventory of Class A and Class B office buildings has

Industrial Snapshot H1 2014

Industrial Snapshot H1 2014 Industrial & Logistics Demand What s driving change? Executive Summary The European industrial and logistics market is diversifying and becoming more complex in response to

Industrial Snapshot H1 2014 Industrial & Logistics Demand What s driving change? Executive Summary The European industrial and logistics market is diversifying and becoming more complex in response to

STRATEGY AND KEY OUTCOMES PROPERTY ASSET PLATFORM FINANCIAL REVIEW WRAP UP. Our conversation PORTFOLIO OVERVIEW WESTERN CAPE PROJECTS.

STRATEGY AND KEY OUTCOMES PROPERTY ASSET PLATFORM FINANCIAL REVIEW WRAP UP Our conversation Section 01 SECTOR TRENDS Section 02 PORTFOLIO OVERVIEW Section 03 WESTERN CAPE PROJECTS Section 04 OUTLOOK SECTOR

STRATEGY AND KEY OUTCOMES PROPERTY ASSET PLATFORM FINANCIAL REVIEW WRAP UP Our conversation Section 01 SECTOR TRENDS Section 02 PORTFOLIO OVERVIEW Section 03 WESTERN CAPE PROJECTS Section 04 OUTLOOK SECTOR

1. Reasons for Recommendation

Recommendation: BUY Target Stock Price (12/31/2015): $148 1. Reasons for Recommendation Union Pacific Corporation will continue to lead the railroad industry in the years to come with continuous expansion

Recommendation: BUY Target Stock Price (12/31/2015): $148 1. Reasons for Recommendation Union Pacific Corporation will continue to lead the railroad industry in the years to come with continuous expansion

CBI Product Factsheet for Rubber and Metal Parts for Vehicles in Eastern Europe

CBI Product Factsheet for Rubber and Metal Parts for Vehicles in Eastern Europe Practical market insights for your product Eastern European demand for rubbertometal bonded automotive parts is increasing

CBI Product Factsheet for Rubber and Metal Parts for Vehicles in Eastern Europe Practical market insights for your product Eastern European demand for rubbertometal bonded automotive parts is increasing

TURKEY MARKET STATEMENT. 70th Session of UNECE Timber Committee October 2012, GENEVA

TURKEY MARKET STATEMENT 70th Session of UNECE Timber Committee 16-19 October 2012, GENEVA 1. General Economic Trends Affecting the Forest and Forest Industry Sectors Strong economic recovery was realized

TURKEY MARKET STATEMENT 70th Session of UNECE Timber Committee 16-19 October 2012, GENEVA 1. General Economic Trends Affecting the Forest and Forest Industry Sectors Strong economic recovery was realized

SHARED SERVICES CENTRES BUSINESS PROCESS OUTSOURCING

MARKET OVERVIEW SHARED SERVICES CENTRES BUSINESS PROCESS OUTSOURCING POLAND 2016 MARKET INSIGHTS SHARED SERVICES CENTRES POLAND IN FIGURES Economy Average monthly income in the companies sector (2015)

MARKET OVERVIEW SHARED SERVICES CENTRES BUSINESS PROCESS OUTSOURCING POLAND 2016 MARKET INSIGHTS SHARED SERVICES CENTRES POLAND IN FIGURES Economy Average monthly income in the companies sector (2015)

Short Term Energy Outlook March 2011 March 8, 2011 Release

Short Term Energy Outlook March 2011 March 8, 2011 Release Highlights West Texas Intermediate (WTI) and other crude oil spot prices have risen about $15 per barrel since mid February partly in response

Short Term Energy Outlook March 2011 March 8, 2011 Release Highlights West Texas Intermediate (WTI) and other crude oil spot prices have risen about $15 per barrel since mid February partly in response

IN BRIEF Uncertainties such as Brexit and weak global demand loom large. But German manufacturers propensity to innovate leave it better positioned th

GERMANY TRADE REPORT IN BRIEF Uncertainties such as Brexit and weak global demand loom large. But German manufacturers propensity to innovate leave it better positioned than other EU economies. Germany

GERMANY TRADE REPORT IN BRIEF Uncertainties such as Brexit and weak global demand loom large. But German manufacturers propensity to innovate leave it better positioned than other EU economies. Germany

More Positive Signals for European Office Markets

The Jones Lang LaSalle Office Property Clock - Q2 2010 More Positive Signals for European Office Markets Prime office rents across the region stabilised further with the first markets showing rental growth;

The Jones Lang LaSalle Office Property Clock - Q2 2010 More Positive Signals for European Office Markets Prime office rents across the region stabilised further with the first markets showing rental growth;

Freight Village Vorsino

PROJECT FINANCIAL PARTNER INDUSTRIAL-LOGISTICS CLUSTER Freight Village Vorsino 67 km to MKAD. M-3 Moscow-Kiev highway Cross-docking class «A» warehouses +7 (495) 268 12 86 www.freightvillage.ru 2 FREIGHT

PROJECT FINANCIAL PARTNER INDUSTRIAL-LOGISTICS CLUSTER Freight Village Vorsino 67 km to MKAD. M-3 Moscow-Kiev highway Cross-docking class «A» warehouses +7 (495) 268 12 86 www.freightvillage.ru 2 FREIGHT

Zagreb City Report H1 2015

Zagreb City Report GDP Growth Q1 Inflation May Net Salary April Economy/ Investment market Economics -0.3% 875 Unemployment Rate Q1 0.5% Retail Sales Index May (y-o-y) 4.1% Tourist Arrivals May (y-o-y)

Zagreb City Report GDP Growth Q1 Inflation May Net Salary April Economy/ Investment market Economics -0.3% 875 Unemployment Rate Q1 0.5% Retail Sales Index May (y-o-y) 4.1% Tourist Arrivals May (y-o-y)

Thiel Logistik AG. Presentation Annual Results March 16, 2006

Thiel Logistik AG Presentation Annual Results 2005 March 16, 2006 Agenda Introduction - Review of FY 2005 Berndt-Michael Winter Financial Review 2005 and Outlook Dr. Antonius Wagner Performance enhancements

Thiel Logistik AG Presentation Annual Results 2005 March 16, 2006 Agenda Introduction - Review of FY 2005 Berndt-Michael Winter Financial Review 2005 and Outlook Dr. Antonius Wagner Performance enhancements

A GATïà ^ GÉNÉRAL SUR LES TARIFS DOUA RS ET LE COMMEM

Press Relea ommuniqu iepr< GENERAL AGREEMENT ON TARIFFS AND TRADE A GATïà ^ GÉNÉRAL SUR LES TARIFS DOUA RS ET LE COMMEM >ntre William Rappard, Rue de Lausanne 154, 1211 Genève 21 M W Tél. (022M 31 02 31

Press Relea ommuniqu iepr< GENERAL AGREEMENT ON TARIFFS AND TRADE A GATïà ^ GÉNÉRAL SUR LES TARIFS DOUA RS ET LE COMMEM >ntre William Rappard, Rue de Lausanne 154, 1211 Genève 21 M W Tél. (022M 31 02 31

Agility Distribution Parks

Agility Distribution Parks Agility ADP Tema, Ghana Agility at a glance 5Billion $ Global network of 500 offices in More than 100 22,000 annual revenue employees countries Freight, Logistics,Warehousing

Agility Distribution Parks Agility ADP Tema, Ghana Agility at a glance 5Billion $ Global network of 500 offices in More than 100 22,000 annual revenue employees countries Freight, Logistics,Warehousing

Independant divisions in Belgium, the Netherlands, Bulgaria & Romania

CORDEEL GROUP 100% family owned More than80 yearsof experience Independant divisions in Belgium, the Netherlands, Bulgaria & Romania More than a thousand employees Turnover 450 millioneuro / year Various

CORDEEL GROUP 100% family owned More than80 yearsof experience Independant divisions in Belgium, the Netherlands, Bulgaria & Romania More than a thousand employees Turnover 450 millioneuro / year Various

U.S. Trade Deficit and the Impact of Changing Oil Prices

U.S. Trade Deficit and the Impact of Changing Oil Prices James K. Jackson Specialist in International Trade and Finance 16, 2016 Congressional Research Service 7-5700 www.crs.gov RS22204 Summary Imported

U.S. Trade Deficit and the Impact of Changing Oil Prices James K. Jackson Specialist in International Trade and Finance 16, 2016 Congressional Research Service 7-5700 www.crs.gov RS22204 Summary Imported

Internal Trade From the mid-1990s on concentration vertical integration major international retail corporations buying groups, franchise networks

Internal Trade The term internal trade covers a diverse range of activities supporting the flow of goods from the producer to the final consumer, including wholesale, and a series of intermediary actions

Internal Trade The term internal trade covers a diverse range of activities supporting the flow of goods from the producer to the final consumer, including wholesale, and a series of intermediary actions

Warehouse Market Report Moscow. Research H1 2015

Research H1 2015 Warehouse Market Report Highlights In H1 2015, the total area of new quality warehouse space has amounted to a record 570.1 thousand sq m. The take-up of quality warehouse space in the

Research H1 2015 Warehouse Market Report Highlights In H1 2015, the total area of new quality warehouse space has amounted to a record 570.1 thousand sq m. The take-up of quality warehouse space in the

Southeastern Europe: engine for growth Kostas Macheras, CEO Southeastern Europe

Southeastern Europe: engine for growth Kostas Macheras, CEO Southeastern Europe 29/11/2011 1 Agenda Strategic context Macro-economic context Drivers of success at Alfa Beta and Mega Image Why Maxi? Maxi:

Southeastern Europe: engine for growth Kostas Macheras, CEO Southeastern Europe 29/11/2011 1 Agenda Strategic context Macro-economic context Drivers of success at Alfa Beta and Mega Image Why Maxi? Maxi:

Current Economic & Carbon Black Market Scenario in South Asia

Current Economic & Carbon Black Market Scenario in South Asia November 2017 Plan - 2023 Content Sl No Table of Content 1. South Asia.. 2. Economic Environment 4. South Asia Economic Indicators 5. India

Current Economic & Carbon Black Market Scenario in South Asia November 2017 Plan - 2023 Content Sl No Table of Content 1. South Asia.. 2. Economic Environment 4. South Asia Economic Indicators 5. India

INDUSTRY OVERVIEW. According to the Frost & Sullivan Report, consumers in different regions share the following consumption patterns.

In addition, certain information in this section is extracted from an industry report prepared by Frost & Sullivan, dated 9 September 2013 (the Frost & Sullivan Report ), which we commissioned. For a discussion

In addition, certain information in this section is extracted from an industry report prepared by Frost & Sullivan, dated 9 September 2013 (the Frost & Sullivan Report ), which we commissioned. For a discussion

U.S. Trade Deficit and the Impact of Changing Oil Prices

U.S. Trade Deficit and the Impact of Changing Oil Prices James K. Jackson Specialist in International Trade and Finance February 21, 2013 CRS Report for Congress Prepared for Members and Committees of

U.S. Trade Deficit and the Impact of Changing Oil Prices James K. Jackson Specialist in International Trade and Finance February 21, 2013 CRS Report for Congress Prepared for Members and Committees of

Arnold Schuh FDI in CEE The Business Perspective

Arnold Schuh FDI in CEE The Business Perspective OeNB Workshop 20 June 2017 Agenda Research on going east of Western MNCs since the fall of the Iron Curtain Before & after 2009: Expansion and consolidation

Arnold Schuh FDI in CEE The Business Perspective OeNB Workshop 20 June 2017 Agenda Research on going east of Western MNCs since the fall of the Iron Curtain Before & after 2009: Expansion and consolidation

ACTUAL STATE AND POTENTIAL OF LOGISTICS CENTERS IN SMALL AND MEDIUM SIZED CITIES NEAR THE EUROPEAN CORRIDORS 4 & 8 in BULGARIA

ACTUAL STATE AND POTENTIAL OF LOGISTICS CENTERS IN SMALL AND MEDIUM SIZED CITIES NEAR THE EUROPEAN CORRIDORS 4 & 8 in BULGARIA Prof. Assoc., Dr. Vikenti SPASSOV Chef of Department Logistics of engineering

ACTUAL STATE AND POTENTIAL OF LOGISTICS CENTERS IN SMALL AND MEDIUM SIZED CITIES NEAR THE EUROPEAN CORRIDORS 4 & 8 in BULGARIA Prof. Assoc., Dr. Vikenti SPASSOV Chef of Department Logistics of engineering

U.S. Trade Deficit and the Impact of Changing Oil Prices

U.S. Trade Deficit and the Impact of Changing Oil Prices James K. Jackson Specialist in International Trade and Finance May 9, 2013 CRS Report for Congress Prepared for Members and Committees of Congress

U.S. Trade Deficit and the Impact of Changing Oil Prices James K. Jackson Specialist in International Trade and Finance May 9, 2013 CRS Report for Congress Prepared for Members and Committees of Congress

Financial Results Meeting: The 1st 3 Months of FY Ending March (April 1, 2015 June 30, 2015)

") Financial Results Meeting: The 1st 3 Months of FY Ending March 2016 (April 1, 2015 June 30, 2015) August 7, 2015 Contents Summary of Business Results for Three Months ended June 30, 2015, for FY Ending

Financial Results Meeting: The 1st 3 Months of FY Ending March 2016 (April 1, 2015 June 30, 2015) August 7, 2015 Contents Summary of Business Results for Three Months ended June 30, 2015, for FY Ending

Automakers and Auto Parts manufacturers

Last updated: July 13, 2011 Rating Methodology by Sector Automakers and Auto Parts manufacturers 1. Business base Susceptible as it is to business fluctuations, the demand for new automobiles is relatively

Last updated: July 13, 2011 Rating Methodology by Sector Automakers and Auto Parts manufacturers 1. Business base Susceptible as it is to business fluctuations, the demand for new automobiles is relatively

Another Record Year For Industrial

Research & Forecast Report 127.1 OAKLAND METROPOLITAN AREA OFFICE INDUSTRIAL Q1 Q3 Q2 10-Year Nominal Interest Rate 2.85 2.85 127.1 Another Record Year For Industrial Market Indicators 10-Year Nominal

Research & Forecast Report 127.1 OAKLAND METROPOLITAN AREA OFFICE INDUSTRIAL Q1 Q3 Q2 10-Year Nominal Interest Rate 2.85 2.85 127.1 Another Record Year For Industrial Market Indicators 10-Year Nominal

Budapest City Report Q City Reports

Budapest City Report Q3 City Reports COPYRIGHT JONES LANG LASALLE IP, INC. Budapest City Report Q3 million GDP Growth ( H1) Unemployment rate (Q3 ) Economy & Investment Economy Inflation 1.9% 4.9% ( -).1%

Budapest City Report Q3 City Reports COPYRIGHT JONES LANG LASALLE IP, INC. Budapest City Report Q3 million GDP Growth ( H1) Unemployment rate (Q3 ) Economy & Investment Economy Inflation 1.9% 4.9% ( -).1%

Home Textiles. Trade Route & Competitive Forces in the European Market

Home Textiles Trade Route & Competitive Forces in the Market The nature of trade in home textiles is set to keep changing in the near future. The market is becoming increasingly globalised, resulting in

Home Textiles Trade Route & Competitive Forces in the Market The nature of trade in home textiles is set to keep changing in the near future. The market is becoming increasingly globalised, resulting in

Waiheke Local Board Economic Overview 2016

Headlines One Two Three The Waiheke Local Board s GDP and employment is largely dependent on tourism related industries such as rental, hiring and real estate services, retail trade and accommodation and

Headlines One Two Three The Waiheke Local Board s GDP and employment is largely dependent on tourism related industries such as rental, hiring and real estate services, retail trade and accommodation and

Impact of Water Management on Water Saving in Some Pre-accession Countries

Impact of Water Management on Water Saving in Some Pre-accession Countries Galia Bardarska National Coordination Center for Global Changes, Bulgarian Academy of Sciences, Bulgaria, Sofia 1113, akad. Georgi

Impact of Water Management on Water Saving in Some Pre-accession Countries Galia Bardarska National Coordination Center for Global Changes, Bulgarian Academy of Sciences, Bulgaria, Sofia 1113, akad. Georgi

SBF NATIONAL BUSINESS SURVEY

SBF NATIONAL BUSINESS SURVEY 2015/2016 Survey Initiated by: Research Partner: Copyright 2016 Singapore Business Federation. All Rights Reserved. 1 SBF NATIONAL BUSINESS SURVEY 2015/2016 Business sentiments

SBF NATIONAL BUSINESS SURVEY 2015/2016 Survey Initiated by: Research Partner: Copyright 2016 Singapore Business Federation. All Rights Reserved. 1 SBF NATIONAL BUSINESS SURVEY 2015/2016 Business sentiments

Author: Michael Neubauer

Positionen & Meinungen Prologis Park Bratislava STORAGE LAND Logistics Market Slovakia.. It is one thing to write about a warehouse of 60,000 m² and something entirely different to stand inside it. I had

Positionen & Meinungen Prologis Park Bratislava STORAGE LAND Logistics Market Slovakia.. It is one thing to write about a warehouse of 60,000 m² and something entirely different to stand inside it. I had

Global Automotive Semiconductor Forecast: 1Q03 Update

Forecast Analysis Global Automotive Semiconductor Forecast: 1Q03 Update Abstract: Gartner Dataquest has cut its forecast for 2003 to $13.9 billion. Semiconductor vendors must expect market volatility if

Forecast Analysis Global Automotive Semiconductor Forecast: 1Q03 Update Abstract: Gartner Dataquest has cut its forecast for 2003 to $13.9 billion. Semiconductor vendors must expect market volatility if

Warehouse Market. Research Q Moscow

Q1 2015 Warehouse Market Report Highlights In Q1 2015, the total area of high-quality warehouse premises delivered was around 270,000 sq m, which is 35% higher than the same period last year. The vacancy

Q1 2015 Warehouse Market Report Highlights In Q1 2015, the total area of high-quality warehouse premises delivered was around 270,000 sq m, which is 35% higher than the same period last year. The vacancy

Investor Presentation

Investor Presentation Michael Willome, Group CEO Baader Helvea Swiss Equities Conference Content Group overview & priorities Page 3 Segment performance, sales trend & outlook Page 10 Appendix: Leadership

Investor Presentation Michael Willome, Group CEO Baader Helvea Swiss Equities Conference Content Group overview & priorities Page 3 Segment performance, sales trend & outlook Page 10 Appendix: Leadership

US$ Million Electrical machines and apparatus having individual functions

Opportunities Abound in Thailand s Machinery Industry Boasting 50,000 enterprises and 400,000 workers, Thailand s machinery and metalworking industry resounds with activity. Demand for more sophisticated

Opportunities Abound in Thailand s Machinery Industry Boasting 50,000 enterprises and 400,000 workers, Thailand s machinery and metalworking industry resounds with activity. Demand for more sophisticated

Global view on steel market dynamics Platt s Steel Markets Europe Conference Barcelona, June 30-July 1. June 30, 2016

Global view on steel market dynamics Platt s Steel Markets Europe Conference Barcelona, June 30-July 1 June 30, 2016 Agenda China: the bull in the porcelain shop. Global growth divergence and impact on

Global view on steel market dynamics Platt s Steel Markets Europe Conference Barcelona, June 30-July 1 June 30, 2016 Agenda China: the bull in the porcelain shop. Global growth divergence and impact on

Gross Domestic Product

Question 1: What is GDP? Answer 1: From a macroperspective, the broadest measure of economic activity is gross domestic product (GDP). GDP represents all the goods and services that are produced within

Question 1: What is GDP? Answer 1: From a macroperspective, the broadest measure of economic activity is gross domestic product (GDP). GDP represents all the goods and services that are produced within

Iron & Steel. Last updated: July 13, Rating Methodology by Sector

Last updated: July 13, 2011 Rating Methodology by Sector Iron & Steel 1. Business base Japan s steel industry is a basic materials industry, in which fluctuations in supply and demand and market conditions

Last updated: July 13, 2011 Rating Methodology by Sector Iron & Steel 1. Business base Japan s steel industry is a basic materials industry, in which fluctuations in supply and demand and market conditions

Machine buildings Electrical engineering and electronics Food industry and agriculture Light and heavy chemistry and related industries

Machine buildings Electrical engineering and electronics Food industry and agriculture Light and heavy chemistry and related industries Anelia Baklova, Victoria Director Angelova, Marketing, IBA IBA 130

Machine buildings Electrical engineering and electronics Food industry and agriculture Light and heavy chemistry and related industries Anelia Baklova, Victoria Director Angelova, Marketing, IBA IBA 130

Planning For The Future: The integration of organisational and real estate strategies, and the impact on investors

www.pwc.com/assetmanagement Planning For The Future: The integration of organisational and real estate strategies, and the impact on investors Insights from PwC s global asset management practice April

www.pwc.com/assetmanagement Planning For The Future: The integration of organisational and real estate strategies, and the impact on investors Insights from PwC s global asset management practice April

Logistics & Transportation Solutions Group Specialized Real Estate Services

COLLIERS INTERNATIONAL Logistics & Transportation Solutions Group Specialized Real Estate Services Accelerating success. Colliers International Law Firm Services P. 1 This document has been prepared by

COLLIERS INTERNATIONAL Logistics & Transportation Solutions Group Specialized Real Estate Services Accelerating success. Colliers International Law Firm Services P. 1 This document has been prepared by

QIMMA CONSULTING AND INVESTMENT COMPANY LTD.

QIMMA CONSULTING AND INVESTMENT COMPANY LTD. C O M P A N Y P R O F I L E WE ARE THE LANDING PAD FOR YOUR EXPANSION INTO THE AFRICAN MARKET WE DEVELOP VIABLE MARKETING STRATEGIES THAT INTEGRATE THE COMPANY

QIMMA CONSULTING AND INVESTMENT COMPANY LTD. C O M P A N Y P R O F I L E WE ARE THE LANDING PAD FOR YOUR EXPANSION INTO THE AFRICAN MARKET WE DEVELOP VIABLE MARKETING STRATEGIES THAT INTEGRATE THE COMPANY

Rating Methodology by Sector. Iron & Steel

Last updated: March 26, 2012 Rating Methodology by Sector Iron & Steel *This rating methodology is a modification of the rating methodology made public on July 13, 2011, and modifications are made to the

Last updated: March 26, 2012 Rating Methodology by Sector Iron & Steel *This rating methodology is a modification of the rating methodology made public on July 13, 2011, and modifications are made to the

2009 LETTER TO SHAREHOLDERS

2009 LETTER TO SHAREHOLDERS Gary Butler, ADP President & CEO Fiscal 2009 was in many ways the most challenging year of my nearly 35 years at ADP. As we began the fiscal year, we anticipated some level

2009 LETTER TO SHAREHOLDERS Gary Butler, ADP President & CEO Fiscal 2009 was in many ways the most challenging year of my nearly 35 years at ADP. As we began the fiscal year, we anticipated some level

Corporate Presentation March 2009

Corporate Presentation March 2009 1 Agenda Ι Company Profile ΙΙ Product Range ΙΙΙ Sector s Data ΙV Strategy V Expansion in the Balkans VI Investment Program VII FY 2008 Results Highlights 2 Ι. Company

Corporate Presentation March 2009 1 Agenda Ι Company Profile ΙΙ Product Range ΙΙΙ Sector s Data ΙV Strategy V Expansion in the Balkans VI Investment Program VII FY 2008 Results Highlights 2 Ι. Company

On Track Rail Boom in the UAE and GCC

On Track Rail Boom in the UAE and GCC Breakbulk Abu Dhabi 27 October 2014 Teresa Lehovd Head of Market Intelligence Höegh Autoliners 1 / 15 October 2015 Mega Forces Drive Rail Growth Across the World Population

On Track Rail Boom in the UAE and GCC Breakbulk Abu Dhabi 27 October 2014 Teresa Lehovd Head of Market Intelligence Höegh Autoliners 1 / 15 October 2015 Mega Forces Drive Rail Growth Across the World Population

Presentation of Licenses and Control in Gas Supply Division

Presentation of Licenses and Control in Gas Supply Division Kostadin Balachev Director Sofia, 23-27 September 2002 Contents: 1. Functions and tasks 2. Structure and composition 4. Development, aims and

Presentation of Licenses and Control in Gas Supply Division Kostadin Balachev Director Sofia, 23-27 September 2002 Contents: 1. Functions and tasks 2. Structure and composition 4. Development, aims and

Gorenje Gorenje Group Summary of the Strategic plan

Group Summary of the Strategic plan 2010 2013 Summary off tthe Sttrattegiic pllan 2010 -- 2013 Gorrenjje Grroup Velenje, Slovenia, January 2010 1 Group Summary of the Strategic plan 2010 2013 Letter by

Group Summary of the Strategic plan 2010 2013 Summary off tthe Sttrattegiic pllan 2010 -- 2013 Gorrenjje Grroup Velenje, Slovenia, January 2010 1 Group Summary of the Strategic plan 2010 2013 Letter by

SOUTHERN EUROPE MARCO SIMONETTI BUSINESS UNIT DIRECTOR, SOUTHERN EUROPE

SOUTHERN EUROPE MARCO SIMONETTI BUSINESS UNIT DIRECTOR, SOUTHERN EUROPE Diversified asset and customer base Assets under management (Completed assets, land and developments as at 31 December 2017) Poland,

SOUTHERN EUROPE MARCO SIMONETTI BUSINESS UNIT DIRECTOR, SOUTHERN EUROPE Diversified asset and customer base Assets under management (Completed assets, land and developments as at 31 December 2017) Poland,

Financial Information

Financial Information of 4.9 billion in Q1 2011, Continued strong organic at +12% Industry continued on a very solid momentum IT and Buildings expanded at double-digit thanks to solutions Power also solid,

Financial Information of 4.9 billion in Q1 2011, Continued strong organic at +12% Industry continued on a very solid momentum IT and Buildings expanded at double-digit thanks to solutions Power also solid,

2001 Summary. Financial Ratio. Sales and Service Income. Total Revenue. Net Income. Total Assets. Total Liabilities. Shareholders Equity

2001 Summary Million Baht Sales and Service Income Total Revenue Net Income Total Assets Total Liabilities Shareholders Equity Earning Per Share (Baht) Financial Ratio Year Current Ratio Net Debt to Equity

2001 Summary Million Baht Sales and Service Income Total Revenue Net Income Total Assets Total Liabilities Shareholders Equity Earning Per Share (Baht) Financial Ratio Year Current Ratio Net Debt to Equity

Migros Ticaret A.Ş. 1H 2018 Financial Results

Migros Ticaret A.Ş. 1H 2018 Financial Results Disclaimer Statement Migros Ticaret A.Ş. (the Company ) has prepared this presentation for the sole purpose of providing information about its business, operations

Migros Ticaret A.Ş. 1H 2018 Financial Results Disclaimer Statement Migros Ticaret A.Ş. (the Company ) has prepared this presentation for the sole purpose of providing information about its business, operations

Best Practices for Vendors to Lead in Retail in Multiple Markets

Best Practices for Vendors to Lead in Retail in Multiple Markets Presented by: David Marcotte Vice President - Retail Insights October 2011 Kantar Retail Innovation and Action Springs from our Heritage

Best Practices for Vendors to Lead in Retail in Multiple Markets Presented by: David Marcotte Vice President - Retail Insights October 2011 Kantar Retail Innovation and Action Springs from our Heritage

Country Report of Taiwan

1. REVIEW Country Report of Taiwan June 2018 OF ECONOMY IN 2017 AND OUTLOOK IN 2018 (1) Macro economy in 2017 In 2017 Taiwan GDP grew 2.86% that is higher than expected mainly due to strengthened global

1. REVIEW Country Report of Taiwan June 2018 OF ECONOMY IN 2017 AND OUTLOOK IN 2018 (1) Macro economy in 2017 In 2017 Taiwan GDP grew 2.86% that is higher than expected mainly due to strengthened global

Recommendation: HOLD Estimated Fair Value: $58.00-$77.00*

Recommendation: HOLD Estimated Fair Value: $58.00-$77.00* 1. Reasons for the Recommendation Reason #1 PepsiCo s strongest asset is their snack portfolio. PepsiCo is the world s largest snack food company.

Recommendation: HOLD Estimated Fair Value: $58.00-$77.00* 1. Reasons for the Recommendation Reason #1 PepsiCo s strongest asset is their snack portfolio. PepsiCo is the world s largest snack food company.

May 24, 2011 New York, NY

May 24, 2011 New York, NY Safe Harbor Statement The information provided in this presentation (both written and oral) relating to future events are subject to risks and uncertainties, such as competition;

May 24, 2011 New York, NY Safe Harbor Statement The information provided in this presentation (both written and oral) relating to future events are subject to risks and uncertainties, such as competition;

MARKET STATEMENT 2016

LATVIA MARKET STATEMENT 2016 1. GENERAL ECONOMIC TRENDS AFFECTING THE FOREST AND FOREST INDUSTRIES SECTOR The Latvian national economy is tightly integrated into international markets. As of the end of

LATVIA MARKET STATEMENT 2016 1. GENERAL ECONOMIC TRENDS AFFECTING THE FOREST AND FOREST INDUSTRIES SECTOR The Latvian national economy is tightly integrated into international markets. As of the end of

UNIROYAL GLOBAL ENGINEERED PRODUCTS, Inc. OTCQB: UNIR. January 2019

UNIROYAL GLOBAL ENGINEERED PRODUCTS, Inc. OTCQB: UNIR January 2019 Disclaimer The information contained in this presentation is for background purposes only and is subject to amendment, revision and updating.

UNIROYAL GLOBAL ENGINEERED PRODUCTS, Inc. OTCQB: UNIR January 2019 Disclaimer The information contained in this presentation is for background purposes only and is subject to amendment, revision and updating.

European Industrial Occupier Conditions

European Industrial Occupier Conditions Occupiers face looming supply shortage February 2013 Introduction Welcome to our latest industrial occupier conditions slide deck which accompanies our bi-annual

European Industrial Occupier Conditions Occupiers face looming supply shortage February 2013 Introduction Welcome to our latest industrial occupier conditions slide deck which accompanies our bi-annual

Contents. The Global Paper Market Current Review

Contents The Global Paper Market Current Review Introduction... 2 Current Global Outlook for the Paper Industry... 4 Key players & Risk Rating... 4 China... 5 The USA... 5 Japan... 5 Global paper and board

Contents The Global Paper Market Current Review Introduction... 2 Current Global Outlook for the Paper Industry... 4 Key players & Risk Rating... 4 China... 5 The USA... 5 Japan... 5 Global paper and board

Industry 4.0, Supply Chain 4.0

Nomura Research Institute (NRI) India Industry 4.0, Supply Chain 4.0 Evolution of India 4.0 - Make In India, Smart Factory of the World 10 th December 2015 Rajiv Bajaj VP & Partner Nomura Research Institute

Nomura Research Institute (NRI) India Industry 4.0, Supply Chain 4.0 Evolution of India 4.0 - Make In India, Smart Factory of the World 10 th December 2015 Rajiv Bajaj VP & Partner Nomura Research Institute

EUROPEAN LINGERIE GROUP AB QUARTERLY REPORT 9 MONTHS AND THIRD QUARTER Senselle by Felina

EUROPEAN LINGERIE GROUP AB QUARTERLY REPORT 9 MONTHS AND THIRD QUARTER 2018 Senselle by Felina Key numbers European Lingerie Group AB (ELG) is a fully vertically integrated intimate apparel and lingerie

EUROPEAN LINGERIE GROUP AB QUARTERLY REPORT 9 MONTHS AND THIRD QUARTER 2018 Senselle by Felina Key numbers European Lingerie Group AB (ELG) is a fully vertically integrated intimate apparel and lingerie

CURRICULUM SUMMARY COURSE DESCRIPTIONS & OUTLINES MENU MANUFACTURING INDUSTRIES INTRODUCTION TO MANUFACTURING OTHER INDUSTRIES ENERGY INDUSTRIES

CURRICULUM SUMMARY Cambashi s Manufacturing, Distribution and Energy off-the-shelf training courses, Cambashi- ItM, offer a consistent training solution for all your industries. Designed for sales, service,

CURRICULUM SUMMARY Cambashi s Manufacturing, Distribution and Energy off-the-shelf training courses, Cambashi- ItM, offer a consistent training solution for all your industries. Designed for sales, service,

DIVISIONAL REVIEWS IMPERIAL HOLDINGS LIMITED INTEGRATED ANNUAL REPORT. for the year ended 30 June 2016

62 DIVISIONAL REVIEWS 63 DIVISIONAL REVIEWS VEHICLES Key data In line with the group s strategic objectives, the consolidation, integration and restructuring of Imperial s various vehiclerelated businesses

62 DIVISIONAL REVIEWS 63 DIVISIONAL REVIEWS VEHICLES Key data In line with the group s strategic objectives, the consolidation, integration and restructuring of Imperial s various vehiclerelated businesses

Overview of the manufacturing sector

Overview of the manufacturing sector Jane Turner, Economics Department This article examines recent trends in New Zealand s manufacturing sector. It finds that sales to the domestic market have been reasonably

Overview of the manufacturing sector Jane Turner, Economics Department This article examines recent trends in New Zealand s manufacturing sector. It finds that sales to the domestic market have been reasonably

U.S. Trade Deficit and the Impact of Changing Oil Prices

U.S. Trade Deficit and the Impact of Changing Oil Prices James K. Jackson Specialist in International Trade and Finance November 22, 2013 Congressional Research Service 7-5700 www.crs.gov RS22204 Summary

U.S. Trade Deficit and the Impact of Changing Oil Prices James K. Jackson Specialist in International Trade and Finance November 22, 2013 Congressional Research Service 7-5700 www.crs.gov RS22204 Summary

Research. INDUSTRIAL REAL ESTATE Just confidence BUENOS AIRES 1Q17 INDUSTRIAL MARKET. Industrial

INDUSTRIAL REAL ESTATE Just confidence Real Estate Market The first quarter of 2017 had much in common with the fourth quarter of 2016: high expectations, new macroeconomic environment, anti-money laundering