Fire Department Inventory Management Audit

|

|

|

- Kevin Gilbert

- 6 years ago

- Views:

Transcription

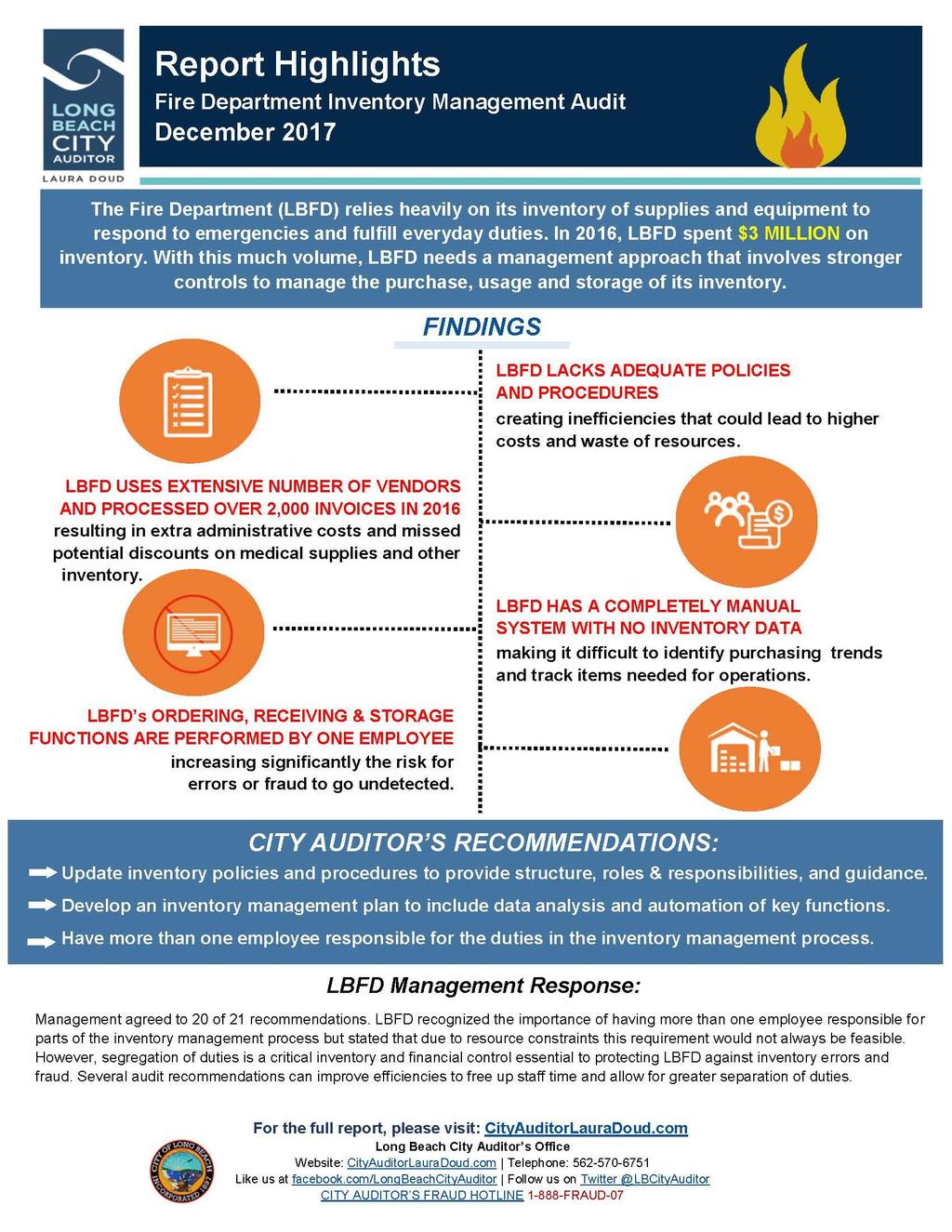

1 Fire Department Inventory Management Audit With over $3 million spent annually on inventory, the Fire Department needs stronger inventory management practices and controls Independence you can rely on December 2017 Laura L. Doud City Auditor Sharon Best Performance Audit Manager Brenda Auner Senior Performance Auditor Angie Maina Performance Auditor Jessica Villalobos Performance Auditor

2

3 Table of Contents Executive Summary... 1 I. Overall Management of Inventory Process... 4 Finding #1 Inadequate Policy Governing Inventory Process a) Roles & Responsibilities Are Not Clearly Defined b) Lack of a Strategic Approach for Vendor Management c) No Policy Requiring a Physical Inventory Count... 7 Finding #2 Completely Manual Process with No Inventory Data... 9 Finding #3 Lack of Segregation of Duties II. Background...13 III. Objective, Scope, and Methodology...15 IV. Management s Response...17

4 Executive Summary The City Auditor s Office completed an audit of the Long Beach Fire Department s (Department) inventory management and associated internal controls at the request of Department management. We commend management for this proactive effort to identify and correct operational weaknesses to function more effectively and efficiently. Appropriate inventory is critical to respond to emergencies. The Department purchased $3M worth of inventory in 2016, averaging $58K per week. The Department s mission is to protect lives, property and the environment, improving the quality of life and safety of the community. Having the appropriate inventory stocked and available is critical to the Department s ability to respond effectively to emergencies and fulfill everyday duties. The Department purchased an estimated $3 million of inventory in calendar year 2016, averaging approximately $58,000 of purchases per week or $11,500 per day. This inventory is added to existing inventory stored at the warehouse and throughout the City s 23 fire stations and other facilities. The Department s inventory is comprised of three primary types of items as illustrated in Figure 1 below, along with miscellaneous items. Figure 1. Examples of Types of Inventory in Each Category The United States Government Accountability Office (GAO) 1 issued best practices as a framework and guide to improve the accuracy and reliability of the government s inventory related data. The GAO s best practices have been successfully implemented by organizations recognized for their inventory management practices and is applicable to any governmental or nongovernmental entity holding inventory, property or equipment. Managing inventory is critical to controlling cost, operational efficiency and mission readiness. Per the GAO, accurate and reliable data is essential to an efficient and effective operating environment. Managers need to know how much inventory there is and where it is to make effective budgeting, operating, and financial decisions. Managing the purchases, storage and usage of inventory is critical to controlling cost, operational efficiency and mission readiness. Due to the amount of funds the Department spends on inventory and the importance of inventory items to operations, a well-thought-out management 1 The U.S. Government Accountability Office (GAO) is an independent nonpartisan agency that works for Congress and investigates how the federal government spends taxpayer dollars by auditing agency operations and reporting on how well government policies and programs are meeting objectives. 1 P a g e

5 strategy along with effective controls are critical to ensure that the Department s resources are spent appropriately, and that inventory is accounted for and readily available for operational needs. Our audit found that the Department needs a sound strategic inventory management approach that can ensure accountability. The current environment exposes the Department to the risk for error, fraud and waste that could easily go undetected. Our audit found the Department lacks an overall strategic approach to manage inventory that can ensure accountability throughout the inventory management process. Accountability with respect to inventory is created through sound policy that is enforced and ensures adequate separation of inventory duties. Policies and procedures define roles and responsibilities for all employees conducting physical inventory counts, managing vendors appropriately, and using data to monitor activity and make management decisions. These elements do not exist in the current environment which exposes the Department to significant risk for error, fraud and waste. Furthermore, the current inventory operations rely on a completely manual system that lacks meaningful data to inform inventory purchasing and control decisions. Current operations allow an environment for fraud, waste and error to occur and easily be undetected. We have categorized the results of our audit into three overarching issues, as illustrated in Figure 2 below. Figure 2. Best Practices Compared to the Environment Found in the Department 2 P a g e

6 We recommend the Department develop an inventory management plan and upgrade from a manual to automated system. We recommend the Department develop an achievable inventory management plan that includes sound policy, effective controls, and the usage of reliable data to make decisions and manage inventory. We recommend that the inventory plan encompasses all three key components of the process: purchases, usage and storage. We also recommend the Department upgrade from a manual to automated system which provides detailed records and will assist the Department with meeting the goals of their strategic plan and develop a level of accountability around the management of their inventory. We would like to thank Department staff for their remarkable level of cooperation, and we appreciate their efforts and desire to improve processes and better secure inventory. 3 P a g e

7 I. Overall Management of Inventory Process The responsibility and accountability of safeguarding inventory belongs to all levels in the Department. Our audit found areas for improvement in policy, inventory data reliability, and segregation of duties. Inventory 2 needs to be managed as if it is money. Like cash, it is an asset of value that is heavily exposed to the risk of fraud, waste and abuse. The basics of an effective inventory control system include policies and procedures, training, compliance, inventory counts, storage, and a reliable set of data. However, the responsibility and accountability of the safeguarding of inventory belongs to all levels involved and is instrumental to the effectiveness of the plan. The Department purchases an estimated $3 million of inventory per year and relies heavily on the inventory to fulfill its mission of protecting lives, property and environment. We found areas for improvement with all key elements of the inventory process and grouped results into three overarching categories: inadequate policy, no inventory data, and segregation of duties. We encourage management to move forward with obtaining an automated system, and to develop a comprehensive strategic plan to govern and create accountability over all key areas of the inventory process. Finding #1 Inadequate Policy Governing Inventory Process The GAO 3 states that establishing and documenting policies and defined procedures are the foundation of managing an effective and reliable inventory. Policies and procedures demonstrate management s commitment to the inventory process and provide clear communication, comprehensive instructions, and guidelines to all employees. Established written policies and procedures also help to ensure consistent and accurate compliance and application. Policies and procedures should also become the basis for training employees and be reviewed periodically for updates. The Department s inventory process is complex due to the volume, nature, storage locations, and number of individuals involved. The Department purchases a significant amount of inventory per year, consisting of items such as ladders, hoses, pharmaceuticals, and stretchers. Inventory is stored at the warehouse and throughout the Department s 23 fire stations. All employees are involved, in some capacity, throughout the entire process of purchasing, usage and storage of inventory. Due to the volume, nature, storage locations and number of individuals involved, the inventory process is complex. The Department provided us with four written policies that are intended to govern the inventory process. Policy Storekeeper General & Specific Duties & Responsibilities 2 pages Policy Inventory Control Report 1.5 pages Policy Medical Supplies & Pharmaceuticals 1.5 pages Policy Inventory & Ordering of Medical Supplies 2.5 pages 2 Inventory represents items such as stretchers, pharmaceuticals, ladders and hoses, tools, custodial supplies, etc. 3 GAO G Best Practices in Achieving Consistent, Accurate Physical Counts of Inventory and Related Property. 4 P a g e

8 Current policies are not comprehensive enough for the complex inventory process. These brief policies do not reflect current practice, are not comprehensive enough, and lack critical information needed to provide effective structure and guidance to employees. The effects of inadequate policy and guidance are significant for the overall accountability for inventory and the ability of the Department to fulfill its critical mission. 1.a) Roles & Responsibilities Are Not Clearly Defined Holding the appropriate level of management responsible for the overall inventory process establishes accountability. Accountability within an organization should exist from the top of the organization to the lowest level. Roles and responsibilities should be specifically designated and assigned. Accountability should be established in job descriptions and expectations and then communicated to employees. Inventory inefficiencies exist due to employees not clearly understanding their roles. Roles and responsibilities for those involved in the Department s inventory process are not clearly defined in policy or understood by those involved. This results in employees not clearly understanding their role and how to perform their functions effectively, leading to inefficiencies and inconsistency in the process and exposing the Department to waste and abuse of resources. Throughout the audit, we found numerous examples of how the lack of sufficient policy to guide employees and their behaviors can lead to questionable decisions and business practices. Table 1 illustrates three examples that highlight risks resulting from undefined or unclear employee roles and responsibilities in purchasing inventory. Table 1. Examples of the Effects of Not Having Clear Roles and Responsibilities Noted During Audit - Calendar Year 2016 No policy exists to govern when employee purchases are allowed and appropriate. There is also no policy to place other parameters around these purchases. Example #1: Approximately 91 employees made purchases from vendors of their choice and were reimbursed directly. Many of the items purchased are easily transferable to personal property such as power tools, printer ink, digital cameras, etc. No policy exists to govern shipment location of purchases made by employees. While an approval process exists for employee purchases, this process is not defined in policy and is not communicated to employees. Example #2: Employees have inventory items shipped to their personal residence versus the warehouse or fire station. This practice exposes the Department to not only risk and abuse but also liability. Example #3: The approval process is not consistently followed by employees. Items such as drill bit sets and barstools 4 were purchased without adequate approval by management. 4 The Department explained that the barstools were purchased to fit under a work bench in a newly purchased Fire Boat. 5 P a g e

9 1.b) Lack of a Strategic Approach for Vendor Management Per the GAO 5, an effective strategic plan for vendor management can assist the organization to better leverage its buying power, reduce costs, better manage vendors, and improve the quality of products purchased. This approach should be outlined in a documented policy that includes instructions on the discharge of duties. These responsibilities should be clearly explained to individual staff, so that they know exactly what authorities and discretion are given. This policy should also include establishment of criteria in selection of vendors. The Department lacks a strategic approach for managing its vendors. The Department neither has a clear plan nor policy for effective vendor management. Except for using citywide contracts, vendor selection is generally left to the discretion of the employee making the purchase. Further, the Department often approaches purchases from an as needed perspective and does not sufficiently consider future needs and/or existing inventory when placing orders. Risk and inefficiencies occur when organizations lack a plan to manage vendors and purchases. Throughout the audit, we found numerous examples of how the absence of sufficient policy to guide employees and their behaviors can lead to questionable decisions and business practices. Table 2 illustrates three examples that highlight risks and inefficiencies that occur when an organization lacks a plan to manage vendors and purchases. Table 2. Examples of the Effects of Lacking a Strategic Approach to Vendor Management Noted During Audit - Calendar Year 2016 There is no plan or identified list of preferred vendors. Employees order from their vendor of choice. Example #1: The Department used a total of 134 vendors to purchase inventory and potentially benefits from discount or set pricing for an estimated 71 vendors that are used by other City departments or have BPOs/contracts directly with the Department. The remaining 63 vendors are exclusively used by the Department and do not have BPOs/contracts with the Department. Reducing the number of vendors, along with the volume of orders, will streamline the purchasing process, reduce administrative costs, and create more price discount opportunities. Reducing the number of vendors will increase the Department s ability to negotiate discounted pricing and focus on quality products. Example #2: The Department processed over 2,000 invoices related to inventory purchases. This equates to an average of 8 invoices processed per day. The Department s as needed purchasing approach creates inefficiencies and does not use their resources in the most effective way. Example #3: The Department purchased approximately $837,000 of medical inventory from 16 different vendors. While we acknowledge that the Department has needs for specialized items, based on our research, it appears that many of these purchases could have been made with two vendors instead of GAO SP: General government: Applying strategic sourcing best practices throughout the federal procurement system could save billions of dollars annually. 6 P a g e

10 The fire departments surveyed use an average of 46 vendors, while Long Beach Fire uses 134. We surveyed five fire departments to compare the number of vendors used by other agencies. As shown in Graph 1 below, other comparable fire departments use an average of 46 vendors, which is 66% fewer than the Long Beach Fire Department s vendor count of 134. Graph 1. Fire Department Benchmarking Analysis Number of Vendors Used FD: Fire Department The risk of not managing vendors can expose the Department to errors, fraud and waste. While vendor management may not be viewed as a priority in many organizations, the risk of not managing vendors can be significant and can expose the Department to fraud, waste and abuse of resources. For example, Department employees could be purchasing from suppliers with poor track records and sub-standard products. To develop a strategic plan and to better manage vendors, the Department needs to better track its needs so that the plan developed can leverage vendors to make best use of the Department s resources. 1.c) No Policy Requiring a Physical Inventory Count The inventory count process is an integral component of an organization s internal control environment, and management s commitment is critical to establishing effective and reliable internal controls. The Department spent $3M worth of inventory, but does not have policy requiring physical inventory verification. With an estimated $3 million of inventory purchases in calendar year 2016 and multiple storage locations, physical inventory counts are critical to verify the existence and completeness of inventory records. However, inventory counts are neither required by policy nor conducted by the Department. Conducting inventory counts would not only verify the existence and completeness of inventory, but would also provide reliable information for management to make decisions. 7 P a g e

11 Recommendations: 1.1. Update policy to include guidance and procedures for the employees who are involved in the inventory process, including key responsibilities and tasks in purchasing, usage and storage Require Department employees to ship all inventory purchases to Department locations Ensure employee requests for reimbursement memoranda are complete and have the approval signature from the proper approval level authority Develop policy and processes that discourage employee reimbursements. However, if employee reimbursements continue to be allowed: a. Develop policies that outline reimbursement purchases; b. Communicate policy to all Department employees regarding purchases made outside of the warehouse; and c. Periodically analyze inventory needed by fire stations and Department employees to better stock the warehouse Analyze purchasing and usage patterns, and identify opportunities to consolidate the number of orders for similar items Analyze the number of vendors used and identify the items that can be purchased from these vendors. Take this information to vendors and shop for discounted prices and other incentives vendors can offer the Department. Use these vendors as preferred vendors and when prudent, enter into a contract to secure cost savings Consider using vendors that can deliver inventory, such as medical inventory, directly to fire stations to free up resources for the warehouse Update policy to include guidance and procedures to: a. Perform periodic inventories and document the results; b. Track inventory usage at the warehouse and the fire stations; c. Communicate the results of the inventories on a regular basis to enhance transparency and to open communication channels between the warehouse and the fire stations; and d. Create methods of oversight for management to employ to verify compliance with the policies. 8 P a g e

12 Finding #2 Completely Manual Process with No Inventory Data Per the GAO, managers and decision-makers need to know how much inventory there is and where it is to make effective decisions related to budgeting, purchasing and storage. Managing the acquisition, usage and storage of inventory is critical to controlling cost, operational efficiency, and mission readiness. Inventory accountability necessitates that detailed records of acquired inventory be maintained. Accountability reduces the risk of undetected theft and loss, unexpected shortages of critical items, and unnecessary purchases of items already on hand. The inventory management process is manual and does not involve the use of technology. The lack of sufficient inventory data is resulting in waste and inefficiencies. The Department s process surrounding the management of inventory is manual and disconnected. Items are purchased as needed, usage is not tracked, and items in storage at the warehouse are tracked manually. At no point is data related to the three key process components of purchasing, usage and storage pulled together and reconciled to identify what is occurring and needed with the inventory. This is especially concerning given that the inventory directly supports the Department s core operations and its ability to fulfill its mission. Figure 3 below illustrates the effects of the absence of an automated system that can track data and provide reports to management so that it can effectively manage the inventory. Figure 3. Effects of Manual System with No Inventory Data Purchases Without aggregated data related to purchases of inventory, it is difficult for management to determine what items have been purchased or the volume, frequency and cost of those purchases. If this information were available, management could review trends to determine if purchases are excessive or unnecessary. Usage/Needs Without consolidated data on usage and needs, it is difficult for management to identify items that are critical to the operation and need to be readily available and/or items that are not used frequently and could be reduced in storage. If this information were available, management could review trends to ensure usage is appropriate and warranted. Storage Without data on purchases and usage, it is very time consuming for management to know what items exist in storage at any given point, the quantity of those items and how frequently they are used. Without this information, management cannot make effective decisions regarding use of storage to ensure the limited space is used as efficiently as possible. 9 P a g e

13 Throughout the audit, we found numerous examples of how the absence of sufficient inventory data to guide decisions can lead to inefficiencies and waste. Table 3 illustrates examples that highlight inefficiencies and waste that occur when data is not available to manage purchases, usage, and storage of inventory. Table 3. Examples of the Effects of a Completely Manual Inventory Process with No Data Noted During Audit - Calendar Year 2016 It is difficult to ensure items are used before they expire and reduce waste without tracking what exists in storage and the life of those items. Example #1: Expired medications worth an estimated $17,000 were found at the warehouse and disposed of. If needs/usage were tracked, then personnel could identify how many items are typically used/needed on a periodic basis and order from the warehouse in bulk to reduce administrative and delivery costs. Inventory lists of some equipment items (not all) are maintained by nine subject matter experts who are sworn personnel. This is an attempt by the Department to maintain a manual account of what equipment is available on hand. Example #3: Fire stations order medical items from the warehouse almost daily. The manual process creates inefficiencies as requisitions must be processed and warehouse personnel must make multiple trips to deliver items. Example #4: The inventory lists are not complete, not consistent, and were missing key information relating to the equipment such as location of equipment, unique identifiers, last test date, etc. This key information for all equipment could easily be maintained in an automated system. This would also free up sworn personnel, who currently spend time managing these lists, to spend time on other duties. The Department requested this audit to improve the current inventory process. Management must ensure the reliability of the inventory data for the automated system to work effectively. We commend the Department for recognizing the need to improve its current inventory process and, thus, requesting this audit. We recommend the Department not only upgrade from a manual to an automated system, but that it also consider the effects of not managing the key components of the inventory process, and implement policies and processes to ensure reliable data exists in the system. However, an automated system and the integrated data that the system would subsequently produce will not, by themselves, bring about the improvements that the Department seeks. Management must ensure that the data is used effectively through reconciliations and reporting, so that management can use the data to make better informed decisions as to how to manage the key components of the inventory process. Recommendations: We recognize that the root cause of the issue goes beyond implementing an inventory management software system. Therefore, we recommend that the Department: 10 P a g e

14 2.1. Develop an achievable inventory management plan that considers all the key policy components. This plan should aim to help the Department assess what its needs are and should be treated as a foundation to build valuable inventory data Once an achievable inventory management plan is in motion and has been communicated to and is understood by employees, implement a software system to integrate purchasing with warehousing and accounting to facilitate inventory tracking. Finding #3 Separation of duties is essential to protect the Department against errors and fraud. Lack of Segregation of Duties Segregation of duties entails separating key duties and responsibilities among different people to reduce the risk of error and fraud, so that no one single individual can adversely affect the accuracy and integrity of the inventory. The three key areas of separation are the physical custody of inventory, processing of inventory transactions, and approval of transactions. The Department s current controls involve the Operations Deputy Chief approving orders and invoices. However, during the audit, we found a lack of separation of duties at the warehouse as one employee performs all three of the critical functions. One employee initiates orders and selects the vendor. Once the order is delivered, the same employee receives the invoice, initials it noting that inventory was received, and forwards it for payment approval. The same employee keeps custody of the inventory while in the warehouse. An employee assigned to multiple roles could easily abuse the controls in the Department s inventory process. Although we did not find fraud, one employee s ability to perform all three of these functions significantly increases the risk for fraud or error to occur and go undetected. Furthermore, the manual system used to track purchases and items in storage only heightens the risk of fraud or error. Examples of the three critical functions in the Department s inventory process performed by one employee, along with the potential consequences, are illustrated in Table 4 below. Table 4. Potential Risks Associated with Limited Segregation of Duties Functions that should be separated but are currently performed by one employee Potential Risks of Not Separating Functions 1. Determines the item and quantity to order and places order from selected vendor 2. Receives the shipment and records receipt of items 3. Receives the vendor invoice and reviews for accuracy before forwarding to accoutning for payment Improper over-ordering from selected vendor Falsify incoming shipments Personal use of inventory Theft or loss of goods Vendor kickbacks Improper purchasing 11 P a g e

15 Recommendations: 3.1 Stop having one employee be responsible for key parts of the inventory management process from ordering to reviewing invoices. 3.2 Update and revise the warehouse policies and procedures, and formalize guidance to include at a minimum: a. Language that includes inventory management functions at the warehouse describing how duties will remain segregated. b. Use the available warehouse clerk to divide the duties and responsibilities, ensuring that loopholes in the process are closed. 3.3 Assess the current procedures and add mitigating controls for these processes: a. Ordering: use the data gathered from the recommendations identified in Findings 1 and 2 and have management from the Administration Bureau periodically analyze the volume of purchases to check for any irregularities or red flags. b. Receiving: require dual counts with signatures from both warehouse employees. 12 P a g e

16 II. Background Fire Department Inventory Structure The Fire Department is responsible for protecting the lives, property and the environment, and improving the quality and safety of the citizens of Long Beach. To accomplish its mission, the Department relies heavily on its inventory to respond to emergencies and complete everyday duties and tasks. As shown in Chart 1, the Department is organized into four main bureaus: Administration, Fire Prevention, Support Services and Operations. Although each bureau purchases its own inventory, the two main bureaus responsible for inventory management are the Administration and Operations Bureaus. Chart 1. Fire Department Organizational Structure The Administration Bureau includes the warehouse which is staffed by a Storekeeper and Store Clerk. The warehouse is responsible for purchasing and receiving general, medical and equipment inventory from vendors and distributing those items to the Department s 23 fire stations. To obtain necessary inventory, fire station employees submit orders to the warehouse via requisition forms. The warehouse maintains separate catalogs for general and medical inventory which fire station employees can reference when placing their orders. The Operations Bureau oversees fire and marine personnel who work at the fire stations and who are responsible for managing the general and medical 13 P a g e

17 inventory at the fire stations. In addition to managing the general and medical inventory, fire station employees are required to conduct daily inspections of equipment used on the emergency vehicles. To further oversee its equipment, the Department assigns a Battalion Chief as Equipment Committee Chair and designates nine employees as Subject Matter Experts (SMEs) to monitor and track specific equipment items. The Equipment Committee Chair, together with the SMEs and warehouse Storekeeper, determine equipment needs and initiate equipment purchases. Types of Inventory For the purposes of this audit, we categorized the Department s inventory purchases into four main groupings general inventory and medical inventory (based on items directly listed in the catalogs), equipment inventory (based on the SME designations) and miscellaneous. Inventory Expenditures As shown in Table 5, the Fire Department spent approximately $3 million on inventory related purchases during calendar year To estimate the breakdown of purchases across the four inventory categories, we used the City s financial data in conjunction with our own analysis of purchases. Table 5. Fire Department Inventory Purchases by Inventory Category For Calendar Year 2016 Inventory Category Amount General $219,526 Medical 836,898 Equipment 1,017,495 Miscellaneous 938,103 Totals $3,012, P a g e

18 III. Objective, Scope, and Methodology The objective of this audit was to assess the effectiveness of the Fire Department s inventory management approach to ensuring cost effectiveness and internal controls. The audit scope covered inventory related purchases during Calendar Year To achieve this objective, we: Conducted site visits and interviewed management and staff involved in the authorization, ordering, receiving, and oversight of Department supplies and equipment; Analyzed controls surrounding the processes for purchasing general, medical, equipment and miscellaneous inventory, as well as those surrounding receiving of shipments and invoice approval; Reviewed a sample of vendor invoices and other Department documentation for general, medical, equipment and miscellaneous inventory purchases during calendar year 2016; Benchmarked other fire departments with similar characteristics to identify best practices for handling inventory (see below for more details); and Researched inventory management best practices that could be incorporated into the Fire Department s processes for improvement (see below for more details). Benchmarking To better understand fire department inventory management strategies, the audit team benchmarked against comparable fire departments. The audit team selected fire departments with a similar number of employees, fire stations, emergency calls received, as well as similar populations served as Long Beach s Fire Department. We asked these departments about their overall inventory management strategies, which included discussions about their policies, organizational structure, inventory tracking practices, and vendor management. GAO Best Practices To strengthen our inventory management knowledge, the audit team thoroughly researched inventory management best practices. Best practices can provide a framework for creating an organized, effective, and costefficient inventory system. Throughout the audit, we compared these best practices to current practice at the Fire Department, and sought opportunities for the Department to improve upon its inventory management, when practical, by incorporating best practices. 15 P a g e

19 Government Auditing Standards We conducted this performance audit in accordance with Generally Accepted Government Auditing Standards (GAGAS). Those standards require that we plan and perform the audit to obtain sufficient, appropriate evidence to provide a reasonable basis for our findings and conclusions based on our audit objectives. We believe that the evidence obtained provides a reasonable basis for our findings and conclusions based on our audit objective. 16 P a g e

20 IV. Management s Response Following this page is Management s Response to the audit findings and recommendations. 17 P a g e

21 18 P a g e

22 19 P a g e

23 20 P a g e

24 21 P a g e

25 22 P a g e

26 Long Beach City Auditor s Office 333 W. Ocean Blvd., 8 th Floor, Long Beach, CA Telephone: Website: CityAuditorLauraDoud.com Like us at facebook.com/longbeachcityauditor Follow us on CITY AUDITOR S FRAUD HOTLINE FRAUD-07 or lbcityauditor.ethicspoint.com

Internal Audit Work Plan

Internal Audit Work Plan Fiscal Year 2018 Department of Management and Finance 1 Internal Audit Services Arlington County s Internal Audit Division is organizationally located in the Department of Management

Internal Audit Work Plan Fiscal Year 2018 Department of Management and Finance 1 Internal Audit Services Arlington County s Internal Audit Division is organizationally located in the Department of Management

Office of the City Auditor. Committed to increasing government efficiency, effectiveness, accountability and transparency

Office of the City Auditor Committed to increasing government efficiency, effectiveness, accountability and transparency Issue Date: TABLE OF CONTENTS Executive Summary... ii Recommendation... iv Background...1

Office of the City Auditor Committed to increasing government efficiency, effectiveness, accountability and transparency Issue Date: TABLE OF CONTENTS Executive Summary... ii Recommendation... iv Background...1

Wire Transfer Audit. Craig Hametner, CPA, CIA, CMA, CFE City Auditor. Prepared By: Jed Johnson Senior Audit Analyst. Michelle Taylor Audit Analyst

Wire Transfer Audit Craig Hametner, CPA, CIA, CMA, CFE City Auditor Prepared By: Jed Johnson Senior Audit Analyst Michelle Taylor Audit Analyst INTERNAL AUDIT DEPARTMENT March 1, 2010 Report 0902 Table

Wire Transfer Audit Craig Hametner, CPA, CIA, CMA, CFE City Auditor Prepared By: Jed Johnson Senior Audit Analyst Michelle Taylor Audit Analyst INTERNAL AUDIT DEPARTMENT March 1, 2010 Report 0902 Table

Prince William County Public Schools Annual Audit Plan

Prince William County Public Schools 2011 Annual Audit Plan Office of Internal Audit Vivian Calkins-McGettigan, MBA, CPA, CPFO Chief Internal Auditor Table of Contents Foreword 3 Introduction to the Office

Prince William County Public Schools 2011 Annual Audit Plan Office of Internal Audit Vivian Calkins-McGettigan, MBA, CPA, CPFO Chief Internal Auditor Table of Contents Foreword 3 Introduction to the Office

INTERNAL AUDIT OF PROCUREMENT AND CONTRACTING

OFFICE OF THE COMMISSIONNER OF LOBBYING OF CANADA INTERNAL AUDIT OF PROCUREMENT AND CONTRACTING AUDIT REPORT Presented by: Samson & Associates February 20, 2015 TABLE OF CONTENT EXECUTIVE SUMMARY... I

OFFICE OF THE COMMISSIONNER OF LOBBYING OF CANADA INTERNAL AUDIT OF PROCUREMENT AND CONTRACTING AUDIT REPORT Presented by: Samson & Associates February 20, 2015 TABLE OF CONTENT EXECUTIVE SUMMARY... I

Audit and Advisory Services Integrity, Innovation and Quality. Audit of Internal Controls over Financial Reporting

Audit and Advisory Services Integrity, Innovation and Quality Audit of Internal Controls over Financial Reporting October 2015 Table of Contents i Audit of Internal Controls over Financial Reporting EXECUTIVE

Audit and Advisory Services Integrity, Innovation and Quality Audit of Internal Controls over Financial Reporting October 2015 Table of Contents i Audit of Internal Controls over Financial Reporting EXECUTIVE

Washington Headquarters Services ADMINISTRATIVE INSTRUCTION

Washington Headquarters Services ADMINISTRATIVE INSTRUCTION NUMBER 94 October 19, 2007 Incorporating Change 2, July 17, 2017 DFD FSD SUBJECT: Personal Property Management and Accountability References:

Washington Headquarters Services ADMINISTRATIVE INSTRUCTION NUMBER 94 October 19, 2007 Incorporating Change 2, July 17, 2017 DFD FSD SUBJECT: Personal Property Management and Accountability References:

Using Transactional Analysis for

Using Transactional Analysis for Effective Fraud Detection Date: 15 th January 2009 Nishith Seth Seth Services.P. Ltd. www.sspl.net.in Cost Indirect costs: image, morale Fraud Issues & Impact Direct costs:

Using Transactional Analysis for Effective Fraud Detection Date: 15 th January 2009 Nishith Seth Seth Services.P. Ltd. www.sspl.net.in Cost Indirect costs: image, morale Fraud Issues & Impact Direct costs:

Managing Risk in Your P2P Process: 10 Ways that Automation Can Help Mitigate Risk

Managing Risk in Your P2P Process: 10 Ways that Automation Can Help Mitigate Risk Chris Doxey, CAPP, CCSA, CICA, CPC President, Doxey, Inc. chris@chrisdoxey.com 571-267-9107 Agenda Introduction to Risk

Managing Risk in Your P2P Process: 10 Ways that Automation Can Help Mitigate Risk Chris Doxey, CAPP, CCSA, CICA, CPC President, Doxey, Inc. chris@chrisdoxey.com 571-267-9107 Agenda Introduction to Risk

OFFICE OF THE CITY AUDITOR Long Beach, California

OFFICE OF THE CITY AUDITOR Long Beach, California LAURA L. DOUD, CPA City Auditor February 9, 2010 HONORABLE MAYOR AND CITY COUNCIL City of Long Beach California RECOMMENDATION: Receive and file the attached

OFFICE OF THE CITY AUDITOR Long Beach, California LAURA L. DOUD, CPA City Auditor February 9, 2010 HONORABLE MAYOR AND CITY COUNCIL City of Long Beach California RECOMMENDATION: Receive and file the attached

BOM/BSD 2/November 1994 BANK OF MAURITIUS. Guideline on Maintenance of Accounting and other Records and Internal Control Systems

BOM/BSD 2/November 1994 BANK OF MAURITIUS Guideline on Maintenance of Accounting and other Records and Internal Control Systems November 1994 Revised November 2013 Revised December 2017 TABLE OF CONTENTS

BOM/BSD 2/November 1994 BANK OF MAURITIUS Guideline on Maintenance of Accounting and other Records and Internal Control Systems November 1994 Revised November 2013 Revised December 2017 TABLE OF CONTENTS

Chapter 7 Internal Controls

Chapter 7 Internal Controls Establishment of and adherence to internal controls is a major part of managing an organization. Internal controls serve as the first line of defense in safeguarding assets

Chapter 7 Internal Controls Establishment of and adherence to internal controls is a major part of managing an organization. Internal controls serve as the first line of defense in safeguarding assets

EMPLOYEE FRAUD OPPORTUNITIES CHECKLIST

Page 128 of 174 EMPLOYEE FRAUD OPPORTUNITIES CHECKLIST Recognizing Warning Signs and Preventing Problem Situations Why are consistent internal controls important? Management decisions, financial reports,

Page 128 of 174 EMPLOYEE FRAUD OPPORTUNITIES CHECKLIST Recognizing Warning Signs and Preventing Problem Situations Why are consistent internal controls important? Management decisions, financial reports,

Audit Report 2016-A-0002 City of Delray Beach Purchasing

PALM BEACH COUNTY John A. Carey Inspector General Inspector General Accredited Enhancing Public Trust in Government Redacted Audit Report 2016-A-0002 City of Delray Beach Purchasing March 2, 2016 Insight

PALM BEACH COUNTY John A. Carey Inspector General Inspector General Accredited Enhancing Public Trust in Government Redacted Audit Report 2016-A-0002 City of Delray Beach Purchasing March 2, 2016 Insight

Success is all in the Design!

Success is all in the Design! IIA Auditing Seminar, San Diego, CA March 14, 2013 Erin Noel, Fiscal and Policy Analyst Office of the Independent Budget Analyst, City of San Diego, CA Introductions - My

Success is all in the Design! IIA Auditing Seminar, San Diego, CA March 14, 2013 Erin Noel, Fiscal and Policy Analyst Office of the Independent Budget Analyst, City of San Diego, CA Introductions - My

Internal Audit How the Internal Audit Function Facilitates Internal Controls. Office of the City Auditor City of Tallahassee

Internal Audit How the Internal Audit Function Facilitates Internal Controls Office of the City Auditor City of Tallahassee 1 Internal Audits and Internal Controls Session Purpose: How does an internal

Internal Audit How the Internal Audit Function Facilitates Internal Controls Office of the City Auditor City of Tallahassee 1 Internal Audits and Internal Controls Session Purpose: How does an internal

CITY OF CORPUS CHRISTI

CITY OF CORPUS CHRISTI CITY AUDITOR S OFFICE Audit of Purchasing Program Project No. AU12-004 September 20, 2012 City Auditor Celia Gaona, CIA CISA CFE Auditor Nora Lozano, CIA CISA Executive Summary In

CITY OF CORPUS CHRISTI CITY AUDITOR S OFFICE Audit of Purchasing Program Project No. AU12-004 September 20, 2012 City Auditor Celia Gaona, CIA CISA CFE Auditor Nora Lozano, CIA CISA Executive Summary In

Maryland School for the Deaf

Audit Report Maryland School for the Deaf December 2015 OFFICE OF LEGISLATIVE AUDITS DEPARTMENT OF LEGISLATIVE SERVICES MARYLAND GENERAL ASSEMBLY For further information concerning this report contact:

Audit Report Maryland School for the Deaf December 2015 OFFICE OF LEGISLATIVE AUDITS DEPARTMENT OF LEGISLATIVE SERVICES MARYLAND GENERAL ASSEMBLY For further information concerning this report contact:

Understanding Internal Controls Office of Internal Audit

Understanding Internal Controls Office of Internal Audit July 2015 Objectives for this manual Provide guidance to help management understand their responsibility to ensure that internal controls are established,

Understanding Internal Controls Office of Internal Audit July 2015 Objectives for this manual Provide guidance to help management understand their responsibility to ensure that internal controls are established,

3.07. Hydro One Inc. Acquisition of Goods and Services. Chapter 3 Section. Background. Audit Objectives and Scope

Chapter 3 Section 3.07 Hydro One Inc. Acquisition of Goods and Services Background As part of the reorganization of the former Ontario Hydro, Hydro One Inc. was created pursuant to the Electricity Act,

Chapter 3 Section 3.07 Hydro One Inc. Acquisition of Goods and Services Background As part of the reorganization of the former Ontario Hydro, Hydro One Inc. was created pursuant to the Electricity Act,

Palm Beach County Clerk & Comptroller s Office Customer Survey Kiosk Special Review

Palm Beach County Clerk & Comptroller s Office Customer Survey Kiosk Special Review SHARON R. BOCK Clerk & Comptroller Palm Beach County Audit Services Division November 7, 2008 Report 2008 6 November

Palm Beach County Clerk & Comptroller s Office Customer Survey Kiosk Special Review SHARON R. BOCK Clerk & Comptroller Palm Beach County Audit Services Division November 7, 2008 Report 2008 6 November

Reining in Maverick Spend. 3 Ways to Save Costs and Improve Compliance with e-procurement

3 Ways to Save Costs and Improve Compliance with e-procurement Contents The Need to Eliminate Rogue Spending Exists for all Businesses...3 Leveraging Technology to Improve Visibility...5 Integrate your

3 Ways to Save Costs and Improve Compliance with e-procurement Contents The Need to Eliminate Rogue Spending Exists for all Businesses...3 Leveraging Technology to Improve Visibility...5 Integrate your

Diocese of Covington Policies & Procedures Manual Section: Compliance Accounting Policy: Internal Control & Segregation of Duties

Internal Control refers to the policies and procedures established to provide reasonable assurance that parish assets are safeguarded, that accountability is achieved, and that errors in financial records

Internal Control refers to the policies and procedures established to provide reasonable assurance that parish assets are safeguarded, that accountability is achieved, and that errors in financial records

Fraud Risk Management

Fraud Risk Management Specific Anti-Fraud Controls (Process or Transaction Level) 2017 Association of Certified Fraud Examiners, Inc. Discussion Questions 1. Does your organization have adequate staffing

Fraud Risk Management Specific Anti-Fraud Controls (Process or Transaction Level) 2017 Association of Certified Fraud Examiners, Inc. Discussion Questions 1. Does your organization have adequate staffing

Contract and Procurement Fraud. Fraud in Procurement without Competition

Contract and Procurement Fraud Fraud in Procurement without Competition Sole-Source Awards Noncompetitive procurement process through the solicitation of only one source Procurement through sole-source

Contract and Procurement Fraud Fraud in Procurement without Competition Sole-Source Awards Noncompetitive procurement process through the solicitation of only one source Procurement through sole-source

PHASE TWO FOLLOW-UP REPORT ON THE AUDIT OF CONTRACTS (2008)

") PHASE TWO FOLLOW-UP REPORT ON THE AUDIT OF CONTRACTS (2008) PREPARED BY: Government Audit Services Branch Government of Yukon APPROVED BY: Audit Committee Table of Contents Page PREFACE 3 EXECUTIVE SUMMARY

PHASE TWO FOLLOW-UP REPORT ON THE AUDIT OF CONTRACTS (2008) PREPARED BY: Government Audit Services Branch Government of Yukon APPROVED BY: Audit Committee Table of Contents Page PREFACE 3 EXECUTIVE SUMMARY

Eric Anderson, City Manager. Scottie Nix, Internal Auditor

City of Tacoma Internal Audit Office Memorandum TO: FROM: SUBJECT: Eric Anderson, City Manager Scottie Nix, Internal Auditor Improving SAP Roles Assignment and Monitoring at the City of Tacoma Follow Up

City of Tacoma Internal Audit Office Memorandum TO: FROM: SUBJECT: Eric Anderson, City Manager Scottie Nix, Internal Auditor Improving SAP Roles Assignment and Monitoring at the City of Tacoma Follow Up

REPORT 2014/137 INTERNAL AUDIT DIVISION. Audit of management of expendable inventory in the African Union-United Nations Hybrid Operation in Darfur

INTERNAL AUDIT DIVISION REPORT 2014/137 Audit of management of expendable inventory in the African Union-United Nations Hybrid Operation in Darfur Overall results relating to the effective management of

INTERNAL AUDIT DIVISION REPORT 2014/137 Audit of management of expendable inventory in the African Union-United Nations Hybrid Operation in Darfur Overall results relating to the effective management of

Risk assessment checklist - Purchasing cycle

Check Yes or No or N/A (where not applicable). Where a No is indicated, some action may be required to rectify the situation. Cross-references (e.g., See FN 1.01) point to the relevant policy in the First

Check Yes or No or N/A (where not applicable). Where a No is indicated, some action may be required to rectify the situation. Cross-references (e.g., See FN 1.01) point to the relevant policy in the First

ANNUAL WORK PLAN & ACCOMPLISHMENTS REPORT

INDEPENDENCE YOU CAN RELY ON 2016 ANNUAL WORK PLAN & ACCOMPLISHMENTS REPORT LONG BEACH CITY AUDITOR S OFFICE 333 West Ocean Boulevard, 8th Floor Long Beach, California 90802 562-570-6751 CityAuditorLauraDoud.com

INDEPENDENCE YOU CAN RELY ON 2016 ANNUAL WORK PLAN & ACCOMPLISHMENTS REPORT LONG BEACH CITY AUDITOR S OFFICE 333 West Ocean Boulevard, 8th Floor Long Beach, California 90802 562-570-6751 CityAuditorLauraDoud.com

University System of Maryland University of Baltimore

Audit Report University System of Maryland University of Baltimore January 2018 OFFICE OF LEGISLATIVE AUDITS DEPARTMENT OF LEGISLATIVE SERVICES MARYLAND GENERAL ASSEMBLY For further information concerning

Audit Report University System of Maryland University of Baltimore January 2018 OFFICE OF LEGISLATIVE AUDITS DEPARTMENT OF LEGISLATIVE SERVICES MARYLAND GENERAL ASSEMBLY For further information concerning

Internal Controls Required for Systems Involved in Procurement to Payment Processes

Internal Controls Required for Systems Involved in Procurement to Payment Processes Definition: Procure to Pay encompasses all business functions necessary to obtain goods and services through contracting.

Internal Controls Required for Systems Involved in Procurement to Payment Processes Definition: Procure to Pay encompasses all business functions necessary to obtain goods and services through contracting.

Role of Procurement / Purchasing Within the Authority

Role of Procurement / Purchasing Within the Authority What is Purchasing s Role / Why Is Purchasing Important? The Authorized entity within the Water Authority that procures the goods / services required.

Role of Procurement / Purchasing Within the Authority What is Purchasing s Role / Why Is Purchasing Important? The Authorized entity within the Water Authority that procures the goods / services required.

Audit Report. Audit of Contracting and Procurement Activities

Audit Report August 2012 Recommended for Approval to the Deputy Minister by the Departmental Audit Committee on October 12, 2012 Approved by the Deputy Minister on October 18, 2012 Table of Contents Table

Audit Report August 2012 Recommended for Approval to the Deputy Minister by the Departmental Audit Committee on October 12, 2012 Approved by the Deputy Minister on October 18, 2012 Table of Contents Table

SEMINOLE COUNTY OFFICE OF MANAGEMENT AND BUDGET PURCHASING DIVISION BLANKET PURCHASE ORDER PROCESS AUDIT. March 31, 1998

SEMINOLE COUNTY OFFICE OF MANAGEMENT AND BUDGET PURCHASING DIVISION BLANKET PURCHASE ORDER PROCESS AUDIT March 31, 1998 March 31, 1998 The Honorable Randall C. Morris Chairman The Board of County Commissioners

SEMINOLE COUNTY OFFICE OF MANAGEMENT AND BUDGET PURCHASING DIVISION BLANKET PURCHASE ORDER PROCESS AUDIT March 31, 1998 March 31, 1998 The Honorable Randall C. Morris Chairman The Board of County Commissioners

HFTP Hospitality Financial and Technology Professionals

About our Sample Accounting Jobs Descriptions for Clubs: The HFTP Americas Research Center, with guidance from members of the HFTP Club Advisory Council, has developed example job descriptions for accounting

About our Sample Accounting Jobs Descriptions for Clubs: The HFTP Americas Research Center, with guidance from members of the HFTP Club Advisory Council, has developed example job descriptions for accounting

Accenture Profit Recovery and Analytics

Business Process Outsourcing Accenture Profit Recovery and Analytics Delivering High Performance through Profit Recovery Accenture: Delivering high performance through profit recovery Are you leaving money

Business Process Outsourcing Accenture Profit Recovery and Analytics Delivering High Performance through Profit Recovery Accenture: Delivering high performance through profit recovery Are you leaving money

Spend visibility and shared services Strategies to address growing pains for long-term care organizations

Spend visibility and shared services Strategies to address growing pains for long-term care organizations Prepared by: Gerry Hodson, Director, Financial Advisory Practice, McGladrey LLP 816.751.4031, gerry.hodson@mcgladrey.com

Spend visibility and shared services Strategies to address growing pains for long-term care organizations Prepared by: Gerry Hodson, Director, Financial Advisory Practice, McGladrey LLP 816.751.4031, gerry.hodson@mcgladrey.com

Proven Methods for Accelerating Cost Reduction. Richard Peters, Sr. Director of Surgical Services, Provista

Proven Methods for Accelerating Cost Reduction Richard Peters, Sr. Director of Surgical Services, Provista Presentation objectives Importance of Cost Reduction Sources of Supply Chain Inefficiency Tips

Proven Methods for Accelerating Cost Reduction Richard Peters, Sr. Director of Surgical Services, Provista Presentation objectives Importance of Cost Reduction Sources of Supply Chain Inefficiency Tips

Internal and Governmental Financial Auditing and Operational Auditing

Internal and Governmental Financial Auditing and Operational Auditing Chapter 26 2012 Prentice Hall Business Publishing, Auditing 14/e, Arens/Elder/Beasley 5-5 Learning Objective 1 Explain the role of

Internal and Governmental Financial Auditing and Operational Auditing Chapter 26 2012 Prentice Hall Business Publishing, Auditing 14/e, Arens/Elder/Beasley 5-5 Learning Objective 1 Explain the role of

3.13. Supply Chain Ontario and Procurement Practices. Chapter 3 Section. 1.0 Summary

Chapter 3 Section 3.13 Supply Chain Ontario and Procurement Practices 1.0 Summary The process of procuring goods and services by the Government of Ontario is intended to be open, fair and transparent.

Chapter 3 Section 3.13 Supply Chain Ontario and Procurement Practices 1.0 Summary The process of procuring goods and services by the Government of Ontario is intended to be open, fair and transparent.

If an adequate segregation of duties does not exist, the following could occur:

Segregation of Duties Safeguarding Assets Review and Approval Accounting Policies and Procedures Efficiency and Effectiveness Reporting Timeliness Segregation of Duties Duties within the department or

Segregation of Duties Safeguarding Assets Review and Approval Accounting Policies and Procedures Efficiency and Effectiveness Reporting Timeliness Segregation of Duties Duties within the department or

FINANCIAL MANAGEMENT FOR GEORGIA LOCAL UNITS OF ADMINISTRATION

FINANCIAL MANAGEMENT FOR GEORGIA LOCAL UNITS OF ADMINISTRATION Date Effective Issued Date July 1, 1994 July 1, 1994 Section III Title: The Accounting Cycle Procedures Revision No. Date Revised Chapter

FINANCIAL MANAGEMENT FOR GEORGIA LOCAL UNITS OF ADMINISTRATION Date Effective Issued Date July 1, 1994 July 1, 1994 Section III Title: The Accounting Cycle Procedures Revision No. Date Revised Chapter

Workday Financial Management

Workday Financial Management Today s businesses compete in markets that are increasingly global and rapidly changing. Finance organizations face mounting pressure to go beyond just managing accounting

Workday Financial Management Today s businesses compete in markets that are increasingly global and rapidly changing. Finance organizations face mounting pressure to go beyond just managing accounting

PAYMENT OF UTILITY CHARGES

APPENDIX 1 PAYMENT OF UTILITY CHARGES August 31, 2009 Auditor General s Office Jeffrey Griffiths, C.A., C.F.E. Auditor General City of Toronto TABLE OF CONTENTS EXECUTIVE SUMMARY...1 BACKGROUND...3 AUDIT

APPENDIX 1 PAYMENT OF UTILITY CHARGES August 31, 2009 Auditor General s Office Jeffrey Griffiths, C.A., C.F.E. Auditor General City of Toronto TABLE OF CONTENTS EXECUTIVE SUMMARY...1 BACKGROUND...3 AUDIT

Minnesota State Community and Technical College

Office of Internal Auditing Minnesota State Community and Technical College Internal Control and Compliance Audit Reference Number 2017-01 Report Classification: Public Dear Members of the Minnesota State

Office of Internal Auditing Minnesota State Community and Technical College Internal Control and Compliance Audit Reference Number 2017-01 Report Classification: Public Dear Members of the Minnesota State

Visa Procure-To-Pay Best Practices for the Federal Government

Visa Procure-To-Pay Practices for the Federal Government b Table of Contents SECTION I: SECTION II: Introduction Background 4 Executive Summary Practives Overview 5 Scope 5 Study Approach 5 Comparison

Visa Procure-To-Pay Practices for the Federal Government b Table of Contents SECTION I: SECTION II: Introduction Background 4 Executive Summary Practives Overview 5 Scope 5 Study Approach 5 Comparison

AN AUDIT OF INTERNAL CONTROL THAT IS INTEGRATED WITH AN AUDIT OF FINANCIAL STATEMENTS: GUIDANCE FOR AUDITORS OF SMALLER PUBLIC COMPANIES

1666 K Street, NW Washington, D.C. 20006 Telephone: (202) 207-9100 Facsimile: (202) 862-8430 www.pcaobus.org PRELIMINARY STAFF VIEWS AN AUDIT OF INTERNAL CONTROL THAT IS INTEGRATED WITH AN AUDIT OF FINANCIAL

1666 K Street, NW Washington, D.C. 20006 Telephone: (202) 207-9100 Facsimile: (202) 862-8430 www.pcaobus.org PRELIMINARY STAFF VIEWS AN AUDIT OF INTERNAL CONTROL THAT IS INTEGRATED WITH AN AUDIT OF FINANCIAL

GATU Webinar Part 1 March 2017 Presented by Carol Kraus, CPA

GATU Webinar Part 1 March 2017 Presented by Carol Kraus, CPA Definition of Internal Controls COSO Internal Control Framework Internal Controls (2 CFR 200.303) Grantee responsibilities Awarding state agency

GATU Webinar Part 1 March 2017 Presented by Carol Kraus, CPA Definition of Internal Controls COSO Internal Control Framework Internal Controls (2 CFR 200.303) Grantee responsibilities Awarding state agency

Internal Controls: Need Them, Have Them, Love Them

Internal Controls: Need Them, Have Them, Love Them Tiffany R. Winters, Esquire twinters@bruman.com Brustein & Manasevit Fall Forum 2010 Why Do We Have Internal Controls? The Federal Managers Financial

Internal Controls: Need Them, Have Them, Love Them Tiffany R. Winters, Esquire twinters@bruman.com Brustein & Manasevit Fall Forum 2010 Why Do We Have Internal Controls? The Federal Managers Financial

Emmet County. Consulting Engagement Phase 1 Evaluation of Internal Controls over Financial Reporting. September 13, rehmann.

Emmet County Consulting Engagement Phase 1 Evaluation of Internal Controls over Financial Reporting September 13, 2017 616.975.4400 rehmann.com Table of Contents Letter to the Board of Commissioners 1

Emmet County Consulting Engagement Phase 1 Evaluation of Internal Controls over Financial Reporting September 13, 2017 616.975.4400 rehmann.com Table of Contents Letter to the Board of Commissioners 1

Enhancing Procurement Card Programs For E-Commerce & Mission Success. IntraMalls Assurance Services

Enhancing Procurement Card Programs For E-Commerce & Mission Success IntraMalls Assurance Services IntraMall Mission Deliver Extraordinary Value E-Purchase Payment Efficiencies P-Cards and Electronic Funds

Enhancing Procurement Card Programs For E-Commerce & Mission Success IntraMalls Assurance Services IntraMall Mission Deliver Extraordinary Value E-Purchase Payment Efficiencies P-Cards and Electronic Funds

Workday Financial Management

Workday Financial Management Today s businesses compete in markets that are increasingly global and rapidly changing. Finance organisations face mounting pressure to go beyond just managing accounting

Workday Financial Management Today s businesses compete in markets that are increasingly global and rapidly changing. Finance organisations face mounting pressure to go beyond just managing accounting

Internal Audit Policy and Procedures Internal Audit Charter

Mission Statement Internal Audit Policy and Procedures Internal Audit Charter The mission of the Internal Audit Department is to provide independent and objective reviews and assessments of the business

Mission Statement Internal Audit Policy and Procedures Internal Audit Charter The mission of the Internal Audit Department is to provide independent and objective reviews and assessments of the business

Segregation of Duties

Segregation of Duties The Basics of Accounting Controls Segregation of Duties The Basics of Accounting Controls 2014 SP Plus Corporation. All rights reserved. No part of this publication may be reproduced,

Segregation of Duties The Basics of Accounting Controls Segregation of Duties The Basics of Accounting Controls 2014 SP Plus Corporation. All rights reserved. No part of this publication may be reproduced,

Auditing Standards and Practices Council

Auditing Standards and Practices Council PHILIPPINE STANDARD ON AUDITING 315 UNDERSTANDING THE ENTITY AND ITS ENVIRONMENT AND ASSESSING THE RISKS OF MATERIAL MISSTATEMENT PHILIPPINE STANDARD ON AUDITING

Auditing Standards and Practices Council PHILIPPINE STANDARD ON AUDITING 315 UNDERSTANDING THE ENTITY AND ITS ENVIRONMENT AND ASSESSING THE RISKS OF MATERIAL MISSTATEMENT PHILIPPINE STANDARD ON AUDITING

INTERNATIONAL STANDARD ON AUDITING 315 UNDERSTANDING THE ENTITY AND ITS ENVIRONMENT AND ASSESSING THE RISKS OF MATERIAL MISSTATEMENT CONTENTS

INTERNATIONAL STANDARD ON AUDITING 315 UNDERSTANDING THE ENTITY AND ITS ENVIRONMENT AND ASSESSING THE RISKS OF MATERIAL MISSTATEMENT (Effective for audits of financial statements for periods beginning

INTERNATIONAL STANDARD ON AUDITING 315 UNDERSTANDING THE ENTITY AND ITS ENVIRONMENT AND ASSESSING THE RISKS OF MATERIAL MISSTATEMENT (Effective for audits of financial statements for periods beginning

Fraud Prevention, Detection, and Internal Controls

Fraud Prevention, Detection, and Internal Controls Budget, Accounting and Reporting Council May 28, 2015 Sherrie Ard, CPA, CFE Financial Management Specialist Local Government Performance Center Local

Fraud Prevention, Detection, and Internal Controls Budget, Accounting and Reporting Council May 28, 2015 Sherrie Ard, CPA, CFE Financial Management Specialist Local Government Performance Center Local

Sarbanes Oxley Impact on Supply Chain Management

Sarbanes Oxley Impact on Supply Chain Management Robert J. Engel, C.P.M. National Director of Client Service Resources Global Professionals-SCM Practice 713-403-1979: Bob.Engel@Resources-us.com 91 st Annual

Sarbanes Oxley Impact on Supply Chain Management Robert J. Engel, C.P.M. National Director of Client Service Resources Global Professionals-SCM Practice 713-403-1979: Bob.Engel@Resources-us.com 91 st Annual

In Control: Getting Familiar with the New COSO Guidelines. CSMFO Monterey, California February 18, 2015

In Control: Getting Familiar with the New COSO Guidelines CSMFO Monterey, California February 18, 2015 1 Background on COSO Part 1 2 Development of a comprehensive framework of internal control Internal

In Control: Getting Familiar with the New COSO Guidelines CSMFO Monterey, California February 18, 2015 1 Background on COSO Part 1 2 Development of a comprehensive framework of internal control Internal

Oakland County Department of Management and Budget Purchasing Division Policies and Procedures Adopted May 24, 1990 and Revised May 1, 2004

Oakland County Department of Management and Budget Purchasing Division Policies and Procedures Adopted May 24, 1990 and Revised May 1, 2004 Section 1000: Governing Authority The purchasing function is

Oakland County Department of Management and Budget Purchasing Division Policies and Procedures Adopted May 24, 1990 and Revised May 1, 2004 Section 1000: Governing Authority The purchasing function is

STATE OF NORTH CAROLINA

STATE OF NORTH CAROLINA PERFORMANCE AUDIT NORTH CAROLINA DEPARTMENT OF TRANSPORTATION FERRY DIVISION JULY 2011 OFFICE OF THE STATE AUDITOR BETH A. WOOD, CPA STATE AUDITOR PERFORMANCE AUDIT NORTH CAROLINA

STATE OF NORTH CAROLINA PERFORMANCE AUDIT NORTH CAROLINA DEPARTMENT OF TRANSPORTATION FERRY DIVISION JULY 2011 OFFICE OF THE STATE AUDITOR BETH A. WOOD, CPA STATE AUDITOR PERFORMANCE AUDIT NORTH CAROLINA

CGMA Competency Framework

CGMA Competency Framework Technical skills CGMA Competency Framework 1 Technical skills : This requires a basic understanding of the business structures, operations and financial performance, and includes

CGMA Competency Framework Technical skills CGMA Competency Framework 1 Technical skills : This requires a basic understanding of the business structures, operations and financial performance, and includes

City and County of San Francisco

City and County of San Francisco Office of the Controller City Services Auditor DEPARTMENT OF PUBLIC HEALTH: The Department s Siloed and Decentralized Purchasing Structure Results in Inefficiencies March

City and County of San Francisco Office of the Controller City Services Auditor DEPARTMENT OF PUBLIC HEALTH: The Department s Siloed and Decentralized Purchasing Structure Results in Inefficiencies March

How Can I Better Manage My Software Assets And Mitigate The Risk Of Compliance Audits?

SOLUTION BRIEF CA SERVICE MANAGEMENT - SOFTWARE ASSET MANAGEMENT How Can I Better Manage My Software Assets And Mitigate The Risk Of Compliance Audits? SOLUTION BRIEF CA DATABASE MANAGEMENT FOR DB2 FOR

SOLUTION BRIEF CA SERVICE MANAGEMENT - SOFTWARE ASSET MANAGEMENT How Can I Better Manage My Software Assets And Mitigate The Risk Of Compliance Audits? SOLUTION BRIEF CA DATABASE MANAGEMENT FOR DB2 FOR

Centralizing Your Energy Supply Spend

HAPPY NEW YEAR! The entire team at Siemens Retail & Commercial Systems wishes you all the best for a prosperous 2016. If saving more money is on your list of resolutions, then contact us. We d love to

HAPPY NEW YEAR! The entire team at Siemens Retail & Commercial Systems wishes you all the best for a prosperous 2016. If saving more money is on your list of resolutions, then contact us. We d love to

Several unallowable expenditures and exceptions to policy were noted.

Several unallowable expenditures and exceptions to policy were noted. In our testing of 16 disbursement/pcard transactions, 12 travel transactions, and 9 gift transactions, we noted 6 transactions contained

Several unallowable expenditures and exceptions to policy were noted. In our testing of 16 disbursement/pcard transactions, 12 travel transactions, and 9 gift transactions, we noted 6 transactions contained

Introducing MasterCard SmartLink *

Introducing MasterCard SmartLink * *MasterCard SmartLink is the program name in the United States only. Outside of the US, the program is referred to as MasterCard s ERP Integration Program. The promise

Introducing MasterCard SmartLink * *MasterCard SmartLink is the program name in the United States only. Outside of the US, the program is referred to as MasterCard s ERP Integration Program. The promise

CHAPTER 7. Internal Control. Review Questions

CHAPTER 7 Internal Control Review Questions 7 1 Internal control is a process, affected by the entity s board of directors, management and other personnel, designed to provide reasonable assurance regarding

CHAPTER 7 Internal Control Review Questions 7 1 Internal control is a process, affected by the entity s board of directors, management and other personnel, designed to provide reasonable assurance regarding

Seattle Public Schools The Office of Internal Audit

Seattle Public Schools The Office of Internal Audit Internal Audit Report September 1, 2014 through Current Issue Date: June 21, 2016 Executive Summary Background Information The function is centralized

Seattle Public Schools The Office of Internal Audit Internal Audit Report September 1, 2014 through Current Issue Date: June 21, 2016 Executive Summary Background Information The function is centralized

Utilities Department Capital Projects Contract Audit

City Auditor s Office Utilities Department Capital Projects Contract Audit Report Issued: March 3, 2017 Audit Report No. # 16 A 2 P O Box 150027 815 Nicholas Pkwy. Cape Coral, FL 33915-0027 Phone 239-242-3383

City Auditor s Office Utilities Department Capital Projects Contract Audit Report Issued: March 3, 2017 Audit Report No. # 16 A 2 P O Box 150027 815 Nicholas Pkwy. Cape Coral, FL 33915-0027 Phone 239-242-3383

Internal Control System Components. Workers Compensation Board

New York State Office of the State Comptroller Thomas P. DiNapoli Division of State Government Accountability Internal Control System Components Workers Compensation Board Report 2015-S-46 October 2015

New York State Office of the State Comptroller Thomas P. DiNapoli Division of State Government Accountability Internal Control System Components Workers Compensation Board Report 2015-S-46 October 2015

Justice Canada. Audit of Cost Recovery Process Improvement (CRPI) Initiative Phase 1. Audit Report. Internal Audit Services.

Initiative Phase 1. Audit Report. Internal Audit Services.") IA S AI Justice Canada Audit of Cost Recovery Process Improvement (CRPI) Initiative Phase 1 Audit Report Internal Audit Services March 2015 Information contained in this publication or product may be reproduced,

IA S AI Justice Canada Audit of Cost Recovery Process Improvement (CRPI) Initiative Phase 1 Audit Report Internal Audit Services March 2015 Information contained in this publication or product may be reproduced,

ORACLE ADVANCED FINANCIAL CONTROLS CLOUD SERVICE

ORACLE ADVANCED FINANCIAL CONTROLS CLOUD SERVICE Advanced Financial Controls (AFC) Cloud Service enables continuous monitoring of all expense and payables transactions in Oracle ERP Cloud, for potential

ORACLE ADVANCED FINANCIAL CONTROLS CLOUD SERVICE Advanced Financial Controls (AFC) Cloud Service enables continuous monitoring of all expense and payables transactions in Oracle ERP Cloud, for potential

THE UNIVERSITY OF TEXAS-PAN AMERICAN OFFICE OF AUDITS & CONSULTING SERVICES. Department of Communication Report No

THE UNIVERSITY OF TEXAS-PAN AMERICAN OFFICE OF AUDITS & CONSULTING SERVICES Report No. 15-02 OFFICE OF INTERNAL AUDITS THE UNIVERSITY OF TEXAS - PAN AMERICAN 1201 West University Drive Edinburg, Texas

THE UNIVERSITY OF TEXAS-PAN AMERICAN OFFICE OF AUDITS & CONSULTING SERVICES Report No. 15-02 OFFICE OF INTERNAL AUDITS THE UNIVERSITY OF TEXAS - PAN AMERICAN 1201 West University Drive Edinburg, Texas

College of Engineering and Computer Science Dean's Office

THE UNIVERSITY OF TEXAS-PAN AMERICAN OFFICE OF AUDITS & CONSULTING SERVICES College of Engineering and Computer Science Dean's Office Report No. 13-16 OFFICE OF INTERNAL AUDITS THE UNIVERSITY OF TEXAS

THE UNIVERSITY OF TEXAS-PAN AMERICAN OFFICE OF AUDITS & CONSULTING SERVICES College of Engineering and Computer Science Dean's Office Report No. 13-16 OFFICE OF INTERNAL AUDITS THE UNIVERSITY OF TEXAS

OVERVIEW 4/19/10. Internal Controls and the Audit Process May 4, 2010 OVERVIEW. Definition and historical perspective of internal auditing

and the Audit Process May 4, 2010 Presented by: Deborah A. Stevens CPA Wichita County Auditor 1 OVERVIEW Definition and historical perspective of internal auditing Role and responsibilities of the internal

and the Audit Process May 4, 2010 Presented by: Deborah A. Stevens CPA Wichita County Auditor 1 OVERVIEW Definition and historical perspective of internal auditing Role and responsibilities of the internal

Spend Analysis. The Business Case

Spend Analysis The Business Case Contents 3 The Business Case for Spend Analysis 3 What is Spend Analysis? 4-5 What Can You Achieve with Effective Spend Analysis? 6 Why Not To Do Spend Analysis On Your

Spend Analysis The Business Case Contents 3 The Business Case for Spend Analysis 3 What is Spend Analysis? 4-5 What Can You Achieve with Effective Spend Analysis? 6 Why Not To Do Spend Analysis On Your

JD Edwards EnterpriseOne Financial Management Overview

JD Edwards EnterpriseOne Financial Overview Karen L. Brown Senior Principal Product Manager Program Agenda 1 JD Edwards EnterpriseOne Overview 2 3 EnterpriseOne Financial Overview

JD Edwards EnterpriseOne Financial Overview Karen L. Brown Senior Principal Product Manager Program Agenda 1 JD Edwards EnterpriseOne Overview 2 3 EnterpriseOne Financial Overview

THE VALUE OF STRATEGIC SOURCING FOR PROCUREMENT PROFESSIONALS

THE VALUE OF STRATEGIC SOURCING FOR PROCUREMENT PROFESSIONALS UNDERSTANDING STRATEGIC SOURCING Maximizing value while minimizing cost is a business imperative across every discipline within organizations.

THE VALUE OF STRATEGIC SOURCING FOR PROCUREMENT PROFESSIONALS UNDERSTANDING STRATEGIC SOURCING Maximizing value while minimizing cost is a business imperative across every discipline within organizations.

Epicor for Distribution

Epicor for Distribution As a distributor, you know that employing a powerful technology strategy is a key to success and to staying ahead of the competition, which seems to get more sophisticated every

Epicor for Distribution As a distributor, you know that employing a powerful technology strategy is a key to success and to staying ahead of the competition, which seems to get more sophisticated every

LA14-15 STATE OF NEVADA. Performance Audit. Department of Tourism and Cultural Affairs Division of Tourism. Legislative Auditor Carson City, Nevada

LA14-15 STATE OF NEVADA Performance Audit Department of Tourism and Cultural Affairs Division of Tourism 2014 Legislative Auditor Carson City, Nevada Audit Highlights Highlights of performance audit report

LA14-15 STATE OF NEVADA Performance Audit Department of Tourism and Cultural Affairs Division of Tourism 2014 Legislative Auditor Carson City, Nevada Audit Highlights Highlights of performance audit report

Evaluating Internal Controls

A SSURANCE AND A DVISORY BUSINESS S ERVICES Fourth in the Series!@# Evaluating Internal Controls Evaluating Overall Effectiveness, Identifying Matters for Improvement, and Ongoing Assessment of Controls

A SSURANCE AND A DVISORY BUSINESS S ERVICES Fourth in the Series!@# Evaluating Internal Controls Evaluating Overall Effectiveness, Identifying Matters for Improvement, and Ongoing Assessment of Controls

CLASS SPECIFICATION SENIOR STOREKEEPER, 1837

Form PDES 8 THE CITY OF LOS ANGELES CIVIL SERVICE COMMISSION CLASS SPECIFICATION 12-11-08 SENIOR STOREKEEPER, 1837 Summary of Duties: Supervises and works with a group of employees involved in the purchasing,

Form PDES 8 THE CITY OF LOS ANGELES CIVIL SERVICE COMMISSION CLASS SPECIFICATION 12-11-08 SENIOR STOREKEEPER, 1837 Summary of Duties: Supervises and works with a group of employees involved in the purchasing,

Procurement Card Comparative Analysis. Prepared for American Express by Accenture

Procurement Card Comparative Analysis Prepared for American Express by Accenture 1 Contents Executive Summary...3 Process Efficiency...3 Sourcing Savings...3 Compliance Improvements...3 Study Overview...4

Procurement Card Comparative Analysis Prepared for American Express by Accenture 1 Contents Executive Summary...3 Process Efficiency...3 Sourcing Savings...3 Compliance Improvements...3 Study Overview...4

P-Cards Done Right. Katie Beatty Community Engagement Manager

P-Cards Done Right Katie Beatty Community Engagement Manager About the NAPCP We are an association committed to advancing YOU and other Commercial Card and Payment professionals worldwide by providing

P-Cards Done Right Katie Beatty Community Engagement Manager About the NAPCP We are an association committed to advancing YOU and other Commercial Card and Payment professionals worldwide by providing

LA16-19 STATE OF NEVADA. Performance Audit. Department of Motor Vehicles Legislative Auditor Carson City, Nevada

LA16-19 STATE OF NEVADA Performance Audit Department of Motor Vehicles 2016 Legislative Auditor Carson City, Nevada Audit Highlights Highlights of performance audit report on the Department of Motor Vehicles

LA16-19 STATE OF NEVADA Performance Audit Department of Motor Vehicles 2016 Legislative Auditor Carson City, Nevada Audit Highlights Highlights of performance audit report on the Department of Motor Vehicles

REPORT 2014/115 INTERNAL AUDIT DIVISION. Audit of information and communications technology management at the United Nations Office at Geneva

INTERNAL AUDIT DIVISION REPORT 2014/115 Audit of information and communications technology management at the United Nations Office at Geneva Overall results relating to the effective and efficient management

INTERNAL AUDIT DIVISION REPORT 2014/115 Audit of information and communications technology management at the United Nations Office at Geneva Overall results relating to the effective and efficient management

Internal Control Questionnaire and Assessment

Bureau of Financial Monitoring and Accountability Florida Department of Economic Opportunity September 30, 2017 107 East Madison Street Caldwell Building Tallahassee, Florida 32399 www.floridajobs.org

Bureau of Financial Monitoring and Accountability Florida Department of Economic Opportunity September 30, 2017 107 East Madison Street Caldwell Building Tallahassee, Florida 32399 www.floridajobs.org

OVERVIEW OF BUDGET RESPONSE TEAM IMPLEMENTATION STR ATEGIES REV. OCTOBER 17, 2017

OVERVIEW OF BUDGET RESPONSE TEAM IMPLEMENTATION STR ATEGIES REV. OCTOBER 17, 2017 OVERVIEW AND COST-SAVINGS Background and Overview of Budget Response Teams The University is facing a $49 million recurring

OVERVIEW OF BUDGET RESPONSE TEAM IMPLEMENTATION STR ATEGIES REV. OCTOBER 17, 2017 OVERVIEW AND COST-SAVINGS Background and Overview of Budget Response Teams The University is facing a $49 million recurring

TTC AUDIT COMMITTEE REPORT NO.

Form Revised: February 2005 TTC AUDIT COMMITTEE REPORT NO. MEETING DATE: January 23, 2011 SUBJECT: INTERNAL AUDIT PLANT MAINTENANCE DEPARTMENT BUILDING EQUIPMENT, FACILITIES, AND PLANT MAINTENANCE ENGINEERING

Form Revised: February 2005 TTC AUDIT COMMITTEE REPORT NO. MEETING DATE: January 23, 2011 SUBJECT: INTERNAL AUDIT PLANT MAINTENANCE DEPARTMENT BUILDING EQUIPMENT, FACILITIES, AND PLANT MAINTENANCE ENGINEERING

The FMA Institute Courses & Resources

The FMA Institute Courses & Resources Institute Overview The Blog Course Descriptions & Prices FUND E-Z FMA articles 1 The FMA Institute is committed to developing nonprofit financial leaders and facilitating

The FMA Institute Courses & Resources Institute Overview The Blog Course Descriptions & Prices FUND E-Z FMA articles 1 The FMA Institute is committed to developing nonprofit financial leaders and facilitating

DIGITAL STRATEGY SUMMARY