NextGenPSD2 Conference 2017

|

|

|

- Avice McKinney

- 6 years ago

- Views:

Transcription

1 THE Berlin GROUP A EUROPEAN STANDARDS INITIATIVE NextGenPSD2 Conference 2017 Payment Initiation Service, PIS Oliver Bieser, Deutsche Bank Ortwin Scheja, SRC ««««««««««««

2 Content 1 Payment Types 2 Payment Initiation Interfaces Interfaces to be defined by the specification Interfaces out of scope 3 JSON and XML Structures 4 Combined Services AIS/PIS 5 Status Requests Copyright Berlin Group 2

3 XS2A interface: Payment Initiation Service Focus of the work of the Berlin Group Copyright Berlin Group 3

4 Use cases Wallet vs. Payment Initiation only TPP - Wallet Payment Initiation Service (Online Shop) Payment Service User (PSU) TPP Wallet Consolidated view of all Payment Accounts Payment Initiation 1. Consent Mgmt. 2. Get Accounts 3. Payment Initiation ASPSP Payment Service User (PSU) Online Shop TPP 1. Payment Initiation ASPSP Use Case: Use Case: n This TPP provides the PSU a consolidated view of his payment accounts across all banks and allows the initiation of payments from these accounts. n Regular usage of this service by the PSU, based on a contract between PSU and TPP. Payment Initiation n In case of a TPP-Wallet, all PSU data needed for the payment Initiation are available on TTP side. n The main purpose of this service is a payment initiation for an online Shop. n The PSU uses this Service only on demand, no permanent relationship between PSU and TPP Payment Initiation n The TPP needs for the Payment Initiation additional information from the PSU or the ASPSP (e.g.: IBAN). To be captured by the PSU or via an additional AIS request provided by the ASPSP. Deutsche Bank Copyright Berlin Group 4

Payment PL-SE 6. USD Payment DE-DE USA 5.")

Payment DE-HR 7.")

5 Payment Flows 9. SEK (Krona) Payment SE-SE 3. EUR Payment DE-SE 8. PLN (Zloty) Payment PL-SE 6. USD Payment DE-DE USA 5. USD Payment DE-US 2. EUR Payment DE-ES. 1. EUR Payment DE-DE 4. HRK (Kuna) Payment DE-HR 7. EUR Payment HR-PL Deutsche Bank Copyright Berlin Group 5

SCHEME RULEBOOK from EPC) Deutsche Bank Copyright Berlin")

6 Conceptual work flow of an SCT Instant payment (Source: SEPA INSTANT CREDIT TRANSFER (SCT INST) SCHEME RULEBOOK from EPC) Deutsche Bank Copyright Berlin Group 6

7 Impact Analysis Approach: required PIS Formats Analyse current situation based on the client facing products Compare the elements per country and channel Result: List with supported payment Formats in SEPA/per Country n Mapping of all fields in the client facing products to ISO20022 elements. n Identify which Payment Products are in Scope. n n n Identify the min.needed elements for payment initiation in all countries. Issue: If an ASPSP online banking offers additional fileds, this breaks the non-discrimination rule, but covers 99% of the business needs. Solution: n n Extend JSON with additional fields ISO XML (for corporates) n Compile complete list of all European payment formats supported by the PSD2 interface. n Target: one simplified JSON format for each basic payment product. n Additional payment types published (products for single markets, e.g dedicated format for tax payments). Deutsche Bank Copyright Berlin Group 7

n IBAN (Ordering Party) 12 n Address (Ordering Party) <Dbtr><Nm>")

8 Typical Online Banking Screen SEPA Credit Transfer (SCT) 12 Mapping to ISO20022 n Captured by the PSU ISO20022 XML Tags n Name <Cdtr><Nm> n IBAN n Amount n Remittance Information n End to End ID <CdtrAcct><Id><IBAN> <Amt><InstdAmt> <RmtInf><Ustrd> <PmtId><EndToEndId> n Selected by the PSU n Name (Ordering Party) n IBAN (Ordering Party) 12 n Address (Ordering Party) <Dbtr><Nm> <DbtrAcct><Id><IBAN> <Dbtr><AdrLine> Deutsche Bank Copyright Berlin Group 8

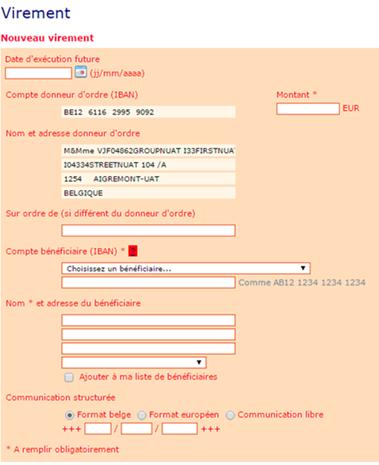

9 SEPA Credit Transfer Screens (examples) Deutsche Bank Copyright Berlin Group 9

10 Impact Analysis Result per Payment Product (SEPA SCT) Beneficiary Name Beneficiary Account Amount Country Product Client DE SCT Retail man. man. man. opt. opt. man. man. n/a n/a n/a n/a n/a DE SCT Corporate man. man. man. opt. opt. man. man. opt. opt.? n/a n/a ES SCT Retail man. man. man. opt. opt. man. man. opt. n/a n/a n/a n/a BE SCT Retail man. man. man. opt. opt. man. man. n/a n/a n/a opt. opt. PL SCT Retail man. man. man. opt. opt. man. man. opt. opt. n/a opt. opt. IT SCT Retail man. man. man. man. opt. man. man. n/a n/a n/a n/a n/a Remittance Information End to End ID Ordering Party Name Ordering Party Account SCT based on minimum needed ISO20022 fields Purpose Code Category Purpose Code Ordering Party Account Cur. Beneficiary Address Ordering Party Address Deutsche Bank Copyright Berlin Group 10

11 Tax Payment F24 in Italy Deutsche Bank Copyright Berlin Group 11

12 Payment Types/Endpoints n Simple JSON structures e.g. for retail business n Full SEPA XML structures e.g. for corporate customers n Typical private customers SEPA payment initiation endpoints /payments/sepa-credit-transfers /payments/instant-sepa-credit-transfers /payments/target-2-payments /payments/crossborder-credit-transfers n Typical corporate XML endpoint e.g. /payments/pain.001-sepa-credit-transfers PISP XS2A Interface ASPSP Supported payment endpoints are published by ASPSP. Can differ for retail and corporates. PSU Account Deutsche Bank Copyright Berlin Group 12

13 Extending JSON Structures n Usage of Berlin Group specified JSON-Scheme for initiating a standard payment at a standard endpoint. n Usage of ASPSP specific JSON for specific transactions or specific markets Extensions by new optional fields Make mandatory fields optional e.g. ultimate entries, structured remittance information n Extended JSON Schemes will apply to standard endpoints too. PISP Payment Initiation Extension fields Berlin Group JSON Scheme ASPSP specific JSON Scheme ASPSP Deutsche Bank Copyright Berlin Group 13

14 Example for JSON SCT SCT Endpoint Format information Processing IDs Device Data for Risk Management Processing Date/Time POST Content-Encoding gzip Content-Type application/json Process-ID 3dc3d5b f5400a64e80f Request-ID 99391c7e-ad88-49ec-a2ad-99ddcb1f7721 PSU-IP-Address PSU-Agent Mozilla/5.0 (Windows NT 10.0; WOW64; rv:54.0) Gecko/ Firefox/54.0 Date Sun, 06 Aug :02:37 GMT https Body: Payment Data { } "instructed_amount" : {"currency" : "EUR", "amount" : "123"}, "debtor_account" : { "iban" : "DE "}, "creditor" : { "name" : "Merchant123"}, "creditor_account" : {"iban" : "DE "}, "remittance_information_unstructured" : "Ref Number Merchant" Deutsche Bank Copyright Berlin Group 14

15 XML Definitions n EPC pain.001 schemes will be supported on endpoint /payments/pain.001-sepa-credit-transfers /payments/pain.001-instant-credit-transfers n Community specific pain.001 structures will be additionally supported on these endpoints. References to community specific specifications will be contained in the Berlin Group specification. n No generic pain.001 scheme available for crossborder-payments, Berlin Group specification relies on community specific specifications Copyright Berlin Group 15

16 Instant Payment Workflow and Status Concept 2. Payment Processing & Clearing 1. Payment Initiation 1 Bank A Response Step Description Payment Status 4 Bank B max. 10 sec. overall timeout e.g.: 20 sec. 1 Payment Initiation (Bank A) - PSU Authorization - Limit & compliance checks - Block amount on PSU account 2 Payment Processing and Clearing (Bank A) - Settlement Process (Clearing House) 3 Payment Processing (Bank B) - Compliance Checks (Bank B) - Made funds available to payee (Bank B) 4 Response to Bank A - OK: final booking on the payer account - NOK: delete PreNote - OK - Payment accepted & amount blocked - NOK - Payment rejected (e.g. not enough funds) - NOK - Payment rejected (e.g. Clearing failure) Out of Scope for PIS (Bank A) - Optional: Bank B provides Info to Payee - NOK Payment rejected (e.g. unknown account) Optional: - OK Bank B made the funds available to payee Deutsche Bank Copyright Berlin Group 16

17 Payment Status Definitions Batch booking banks Online booking banks Instant Payments Transaction Status Meaning Received Payment initiation has been received by the ASPSP. AcceptedTechnicalValidation Authentication and syntactical and semantical validation are successful. AcceptedCustomerProfile In addition, Customer profile check was also successful (Limits etc.) AcceptedSettlementInProcess The payment initiation has been accepted for execution. AcceptedSettlementCompleted Settlement on the debtor's account has been completed. (For instant payment only.) Pending Payment initiation or individual transaction included in the payment initiation is pending, e.g. where a second PSU must authorise the transaction. Rejected Payment initiation has been rejected n Detailed transaction status will be part of every response of ASPSP during the payment initiation process. n Modelling is following ISO20022 encoding. Deutsche Bank Copyright Berlin Group 17

18 Combination of AIS and PIS (Consent ID or optional OAuth2) n TPP can always combine AIS and PIS results in the TPP/PSU interface, e.g. in a wallet like TPP solution, where recurring account access is supported. n In addition, a combination of AIS and PIS is supported in the standard e.g. for batch booking banks to also support easy access and risk management solutions of TPPs. n This is an optional function for the ASPSP in the standard. TPP 1. AIS Service with combined service flag 2. Consent-ID or OAuth2-Token 3. PIS Service with Consent-ID or OAuth2-Token without additional PSU authentication ASPSP Enables ASPSP to implement same behaviour in Online-Banking and XS2A. Deutsche Bank Copyright Berlin Group 18

19 High Level Overview: Bank Systems for Online Banking and API Dedicated Interface Client Facing Interfaces Client PSU Client PSU TPP 3 rd Party Provider Website Certificate (e-idas) TLS (one way) Mutual TLS API Website Certificate Firewall (DMZ) Firewall (Reverse Proxy) Website Certificate ASPSP Online Banking http-server Payments WebServices Account Information WebServices Payment WebServices Account Information WebServices Online Banking Services Strong Customer Autentication PSD2 Exemptions Payment Initiation Account Informations Copyright Berlin Group 19

20 THE Berlin GROUP A EUROPEAN STANDARDS INITIATIVE ««««««««««««Example Prototype Payment Initiation Service 20

21

22

23

24

25

26

27

28

29

30

31

32

33

34

35 Beneficiary: John Smith DE Amount: EUR Created: 10/23/2017 Initiated via PayZooo Payer: Andrei Meyer DE

36

37 THE Berlin GROUP A EUROPEAN STANDARDS INITIATIVE Thank you for your attention ««««««««««««

PSD2 - Second Payment Services Directive. Information Set

PSD2 - Second Payment Services Directive Information Set PSD2: at the starting line February 2017 EBA published the final draft RTS on SCA November 2017 EC published the final RTS on SCA January 13 2018

PSD2 - Second Payment Services Directive Information Set PSD2: at the starting line February 2017 EBA published the final draft RTS on SCA November 2017 EC published the final RTS on SCA January 13 2018

Aktualitātes no Berlin Group NextGen PSD2 konferences. Māris Ozoliņš

Aktualitātes no Berlin Group NextGen PSD2 konferences. Māris Ozoliņš Rīga, 2017. gada 15. novembris THE Berlin GROUP A EUROPEAN STANDARDS INITIATIVE ««««««««««««««««««««««««NextGenPSD2 Conference 2017

Aktualitātes no Berlin Group NextGen PSD2 konferences. Māris Ozoliņš Rīga, 2017. gada 15. novembris THE Berlin GROUP A EUROPEAN STANDARDS INITIATIVE ««««««««««««««««««««««««NextGenPSD2 Conference 2017

NextGen PSD2. A European Standard for PSD2 XS2A

NextGen PSD2 A European Standard for PSD2 XS2A Berlin Group NextGenPSD2 The NextGenPSD2 Initiative is a dedicated Task Force of the Berlin Group with the goal to create an open, common and harmonised European

NextGen PSD2 A European Standard for PSD2 XS2A Berlin Group NextGenPSD2 The NextGenPSD2 Initiative is a dedicated Task Force of the Berlin Group with the goal to create an open, common and harmonised European

NextGen PSD2. A European Standard for PSD2 XS2A

NextGen PSD2 A European Standard for PSD2 XS2A Berlin Group and NextGenPSD2 The NextGenPSD2 Initiative is a dedicated Task Force of the Berlin Group with the goal to create an open, common and harmonised

NextGen PSD2 A European Standard for PSD2 XS2A Berlin Group and NextGenPSD2 The NextGenPSD2 Initiative is a dedicated Task Force of the Berlin Group with the goal to create an open, common and harmonised

Quali-Sign Banking. An example of how to meet the PSD2 segregation requirements. Michael Adams 3 rd November Quali-Sign Ltd

Quali-Sign Banking Quali-Sign Ltd An example of how to meet the PSD2 segregation requirements. Michael Adams 3 rd November 2016 2016 Quali-Sign Ltd michael_adams@quali-sign.com Context The PSD2 segregation

Quali-Sign Banking Quali-Sign Ltd An example of how to meet the PSD2 segregation requirements. Michael Adams 3 rd November 2016 2016 Quali-Sign Ltd michael_adams@quali-sign.com Context The PSD2 segregation

API Banking. The shift to open banking

API Banking The shift to open banking The shift to open banking and move towards value added services. as the platform for compliance and beyond Open banking is set to have a major impact on the financial

API Banking The shift to open banking The shift to open banking and move towards value added services. as the platform for compliance and beyond Open banking is set to have a major impact on the financial

PSD2 is on top of our agenda

PSD2 is on top of our agenda Stating the obvious There is no do nothing option for payment service providers Even basic PSD2 compliance requires strategic choices There is a highway of opportunities The

PSD2 is on top of our agenda Stating the obvious There is no do nothing option for payment service providers Even basic PSD2 compliance requires strategic choices There is a highway of opportunities The

Open Banking PSD2, GDPR and the American Merchant

Your source for payments education Open Banking PSD2, GDPR and the American Merchant Scott Adams Evolutioneer FraudPVP Rene Pelegero President & Managing Director Retail Payments Global Consulting Group

Your source for payments education Open Banking PSD2, GDPR and the American Merchant Scott Adams Evolutioneer FraudPVP Rene Pelegero President & Managing Director Retail Payments Global Consulting Group

Opinion of the European Banking Authority on the implementation of the

EBA-Op-2018-04 13 June 2018 Opinion of the European Banking Authority on the implementation of the RTS on SCA and CSC Introduction and legal basis 1. The competence of the European Banking Authority (EBA)

EBA-Op-2018-04 13 June 2018 Opinion of the European Banking Authority on the implementation of the RTS on SCA and CSC Introduction and legal basis 1. The competence of the European Banking Authority (EBA)

Challenges and solutions. related to Digital Transformation Training & workshop

Challenges and solutions related to Digital Transformation Training & workshop Agenda 09:00-09:30 Registration, coffee 09:30 11:00 Trends in digitalization Regulatory challenges (PSD2 & other) Business

Challenges and solutions related to Digital Transformation Training & workshop Agenda 09:00-09:30 Registration, coffee 09:30 11:00 Trends in digitalization Regulatory challenges (PSD2 & other) Business

Shaping the future of payments

Helmut Wacket Head of Market Integration Division Shaping the future of payments QED Brussels, 29 March 2017 Changes in the retail payments landscape Classical payment instruments innovative payment solutions

Helmut Wacket Head of Market Integration Division Shaping the future of payments QED Brussels, 29 March 2017 Changes in the retail payments landscape Classical payment instruments innovative payment solutions

PSD2 IMPLICATIONS OF THE REGULATION August 8, Regina Lau, Chief Strategy Officer, Ingenico epayments Zainab Mir, Counsel Payments, Netflix

PSD2 IMPLICATIONS OF THE REGULATION August 8, 2017 Regina Lau, Chief Strategy Officer, Ingenico epayments Zainab Mir, Counsel Payments, Netflix OVERVIEW 1. PSD2 Overview Regina Lau 2. Strong Customer Authentication

PSD2 IMPLICATIONS OF THE REGULATION August 8, 2017 Regina Lau, Chief Strategy Officer, Ingenico epayments Zainab Mir, Counsel Payments, Netflix OVERVIEW 1. PSD2 Overview Regina Lau 2. Strong Customer Authentication

Doing More for European Banks

Doing More for European Banks STET s History STET was founded in 2004 by a group of major French banks with a particular goal in mind: to undertake the development of a new platform that would meet the

Doing More for European Banks STET s History STET was founded in 2004 by a group of major French banks with a particular goal in mind: to undertake the development of a new platform that would meet the

OPF FAST INSTANT SEPA PAYMENTS CAPABILITIES

OPF FAST INSTANT SEPA PAYMENTS CAPABILITIES OPF FAST FIS SOLUTION FOR REAL-TIME PAYMENTS PROCESSING EUROPEAN INSTANT PAYMENTS CAPABILITIES Established payment systems do not work in the way most consumers

OPF FAST INSTANT SEPA PAYMENTS CAPABILITIES OPF FAST FIS SOLUTION FOR REAL-TIME PAYMENTS PROCESSING EUROPEAN INSTANT PAYMENTS CAPABILITIES Established payment systems do not work in the way most consumers

Nordea webinar 29/ : PSD2 Access to Accounts a game changer

Nordea webinar 29/11-2017: PSD2 Access to Accounts a game changer Brief intro setting the scene Some practicalities: 9.00-9.45 CET Webinar is being recorded - material will be uploaded to www.nordea.com/vendors

Nordea webinar 29/11-2017: PSD2 Access to Accounts a game changer Brief intro setting the scene Some practicalities: 9.00-9.45 CET Webinar is being recorded - material will be uploaded to www.nordea.com/vendors

The revised Payment Services Directive (PSD2)

") Regulatory agenda updates The revised Payment Services Directive (PSD2) What you need to know Revised Payment Services Directive (PSD2) to increase scope, obligations, and to offer business opportunities

Regulatory agenda updates The revised Payment Services Directive (PSD2) What you need to know Revised Payment Services Directive (PSD2) to increase scope, obligations, and to offer business opportunities

Corporate Access The first-class solution to upgrade our customer s payment processes

Corporate Access The first-class solution to upgrade our customer s payment processes Agenda Corporate Access Repetition from previous seminars Why introduce a new file-based payment service? What is the

Corporate Access The first-class solution to upgrade our customer s payment processes Agenda Corporate Access Repetition from previous seminars Why introduce a new file-based payment service? What is the

Turning PSD2 Challenges into Business Opportunities.

Turning PSD2 Challenges into Business Opportunities www.ebankit.com PSD2 in a nutshell Perfect Competition Payment Services Directive 2 (PSD2) The PSD2 updates and complements the EU rules put in place

Turning PSD2 Challenges into Business Opportunities www.ebankit.com PSD2 in a nutshell Perfect Competition Payment Services Directive 2 (PSD2) The PSD2 updates and complements the EU rules put in place

Challenges and solutions

Challenges and solutions related to the entry into force of the RTS SCA on the 14 September 2019 Introduction The PSD2 and the so-called open banking are two of the most frequently discussed topics in

Challenges and solutions related to the entry into force of the RTS SCA on the 14 September 2019 Introduction The PSD2 and the so-called open banking are two of the most frequently discussed topics in

Instant Payments. An International Update and a Romanian approach

Instant Payments An International Update and a Romanian approach Bucharest, October 26 th, 2016 IP Project in Romania, by RBA and TRANSFOND (scheme and infrastructure) RBA and TRANSFOND are currently waiting

Instant Payments An International Update and a Romanian approach Bucharest, October 26 th, 2016 IP Project in Romania, by RBA and TRANSFOND (scheme and infrastructure) RBA and TRANSFOND are currently waiting

Speed for real-time payments With Open payment ecosystem

Speed for real-time payments With Open payment ecosystem Sami Uski Head of Business Development, Banking & Digital Channels @SamiUski I @TietoCorp 2 Ecosystem introduction So-far accomplished with Siirto.

Speed for real-time payments With Open payment ecosystem Sami Uski Head of Business Development, Banking & Digital Channels @SamiUski I @TietoCorp 2 Ecosystem introduction So-far accomplished with Siirto.

The EU Regulations on payments

The EU Regulations on payments Impacts - Options - Customer ownership Prepaid Summit Europe VISA Timetric - Milano - 2016.10.27 E- Payment & SEPA Adviser 2010 Colt Telecom Group Limited. All rights reserved.

The EU Regulations on payments Impacts - Options - Customer ownership Prepaid Summit Europe VISA Timetric - Milano - 2016.10.27 E- Payment & SEPA Adviser 2010 Colt Telecom Group Limited. All rights reserved.

The Payment Services Directive 2 Background and Content

The Payment Services Directive 2 Background and Content The Jon Bing Memorial Seminar 2017 27 April 2017 Siv Bergit Pedersen Legal counsel MNBA DNB Bank ASA Background Norway Financial Agreements Act (Finansavtaleloven)

The Payment Services Directive 2 Background and Content The Jon Bing Memorial Seminar 2017 27 April 2017 Siv Bergit Pedersen Legal counsel MNBA DNB Bank ASA Background Norway Financial Agreements Act (Finansavtaleloven)

Transformation of the European Payments Landscape. SWIFT Instant Payments Messaging

Transformation of the European Payments Landscape SWIFT Payments Messaging November 2017 Matthieu de Heering Head of Central and Eastern Europe EMEA - SWIFT Challenges for the Payments Industry Many disruptions

Transformation of the European Payments Landscape SWIFT Payments Messaging November 2017 Matthieu de Heering Head of Central and Eastern Europe EMEA - SWIFT Challenges for the Payments Industry Many disruptions

OBP at the heart of your PSD2 strategy

OBP at the heart of your PSD2 strategy API Days Nov 2017 Simon Redfern Open Banking Open APIs for every bank.! Open Standards! Open Source! Open Data! Open Innovation! Why do we need a Web site?! Of course

OBP at the heart of your PSD2 strategy API Days Nov 2017 Simon Redfern Open Banking Open APIs for every bank.! Open Standards! Open Source! Open Data! Open Innovation! Why do we need a Web site?! Of course

Euro Retail Payments Board (ERPB) Final Report of the ERPB Working Group on Payment Initiation Services. ERPB Meeting 29 November 2017

Final Report of the ERPB Working Group on Payment Initiation Services. ERPB Meeting 29 November 2017") ERPB/2017/012 ERPB PIS 034-17 Version 1.0 15 November 2017 Euro Retail Payments Board (ERPB) Final Report of the ERPB Working Group on Payment Initiation Services ERPB Meeting 29 November 2017 ERPB PIS

ERPB/2017/012 ERPB PIS 034-17 Version 1.0 15 November 2017 Euro Retail Payments Board (ERPB) Final Report of the ERPB Working Group on Payment Initiation Services ERPB Meeting 29 November 2017 ERPB PIS

WHITE PAPER. Encouraging innovation in payments through the PSD2 initiative. Abstract

WHITE PAPER Encouraging innovation in payments through the PSD2 initiative Abstract Revised Directive on Payment Services (PSD2) is primarily aimed at bringing new, online modes of payments initiation

WHITE PAPER Encouraging innovation in payments through the PSD2 initiative Abstract Revised Directive on Payment Services (PSD2) is primarily aimed at bringing new, online modes of payments initiation

Utilising our strengths to enhance yours. Payment solutions for the Travel Sector

Utilising our strengths to enhance yours Payment solutions for the Travel Sector EQ Global EQ GLOBAL PROVIDES PAYMENT TECHNOLOGY, DELIVERING TO THE TRAVEL AND LEISURE INDUSTRY A SOLUTION THAT WILL SIMPLIFY

Utilising our strengths to enhance yours Payment solutions for the Travel Sector EQ Global EQ GLOBAL PROVIDES PAYMENT TECHNOLOGY, DELIVERING TO THE TRAVEL AND LEISURE INDUSTRY A SOLUTION THAT WILL SIMPLIFY

Siirto & Open Payment Ecosystem

Siirto & Open Payment Eco ecommerce workshop 1 Tieto Tieto as catalyst to speed up development in eco We are open eco for all stakeholders driving for new real-time payment services and consumer innovations

Siirto & Open Payment Eco ecommerce workshop 1 Tieto Tieto as catalyst to speed up development in eco We are open eco for all stakeholders driving for new real-time payment services and consumer innovations

The Open Banking PSD2 Implementation Strategies

The Open Banking PSD2 Implementation Strategies How to meet the challenge of Open Banking Introduction Open Banking is the next step in a technology evolution driven by the API economy. Technology giants

The Open Banking PSD2 Implementation Strategies How to meet the challenge of Open Banking Introduction Open Banking is the next step in a technology evolution driven by the API economy. Technology giants

Overview card payment current workflow. October 2016

Overview card payment current workflow October 0 DISCLAIMER NOTICE The information contained in this document is subject to review in the light of changing business needs of the industry, government requirements

Overview card payment current workflow October 0 DISCLAIMER NOTICE The information contained in this document is subject to review in the light of changing business needs of the industry, government requirements

Market environment and implementation timeline PSD2 in a nutshell

www.pwc.com/psd2 Market environment and implementation timeline PSD2 in a nutshell Why do we need a new Payment Services Directive (PSD)? By 13 th January 2018, Member States will have to implement the

www.pwc.com/psd2 Market environment and implementation timeline PSD2 in a nutshell Why do we need a new Payment Services Directive (PSD)? By 13 th January 2018, Member States will have to implement the

dd-mm-yyyy Worldline

dd-mm-yyyy Worldline Digital transformation # Digital disruption «Digital transformation involves transformation of internal processes and it aims to digitalize and optimize operations. Digital disruption

dd-mm-yyyy Worldline Digital transformation # Digital disruption «Digital transformation involves transformation of internal processes and it aims to digitalize and optimize operations. Digital disruption

Integrating Payments: Design Principles For A Cashless Future. Monojit Basu, Founder and Director, TechYugadi IT Solutions & Consulting

Integrating Payments: Design Principles For A Cashless Future Monojit Basu, Founder and Director, TechYugadi IT Solutions & Consulting Agenda Current and emerging techniques to integrate merchant apps

Integrating Payments: Design Principles For A Cashless Future Monojit Basu, Founder and Director, TechYugadi IT Solutions & Consulting Agenda Current and emerging techniques to integrate merchant apps

ERPB REACTION TO THE EUROPEAN COMMISSION S GREEN PAPER ON RETAIL FINANCIAL SERVICES

ERPB/2016/001 ERPB REACTION TO THE EUROPEAN COMMISSION S GREEN PAPER ON RETAIL FINANCIAL SERVICES 1. Introduction The Euro Retail Payments Board (ERPB) supports the European Commission s decision to launch

ERPB/2016/001 ERPB REACTION TO THE EUROPEAN COMMISSION S GREEN PAPER ON RETAIL FINANCIAL SERVICES 1. Introduction The Euro Retail Payments Board (ERPB) supports the European Commission s decision to launch

EUROSYSTEM S SEPA EXPECTATIONS

SEC/GovC/X/09/92a 4 March 2009 PAYMENT AND SETTLEMENT SYSTEMS COMMITTEE RESTRICTED EUROSYSTEM S SEPA EXPECTATIONS Executive Summary A lot has been achieved; a lot remains to be done. The creation of the

SEC/GovC/X/09/92a 4 March 2009 PAYMENT AND SETTLEMENT SYSTEMS COMMITTEE RESTRICTED EUROSYSTEM S SEPA EXPECTATIONS Executive Summary A lot has been achieved; a lot remains to be done. The creation of the

Payment Services Directive 2 and other European Laws on Payments Systems Ayse Zoodsma-Sungur

Payment Services Directive 2 and other European Laws on Payments Systems Ayse Zoodsma-Sungur Seventh Conference on Payment and Securities Settlement Systems, Ohrid 7-10 July 2014 Outline Regulation, yes

Payment Services Directive 2 and other European Laws on Payments Systems Ayse Zoodsma-Sungur Seventh Conference on Payment and Securities Settlement Systems, Ohrid 7-10 July 2014 Outline Regulation, yes

The on What s ISO 20022

The 4-1-1 on 20022 What s ISO 20022 Nell Campbell-Drake Vice President Retail Payments Office Federal Reserve Bank of Atlanta EPCOR Payments Conference Spring 2017 ISO 20022 What it is. ISO ISO 20022 for

The 4-1-1 on 20022 What s ISO 20022 Nell Campbell-Drake Vice President Retail Payments Office Federal Reserve Bank of Atlanta EPCOR Payments Conference Spring 2017 ISO 20022 What it is. ISO ISO 20022 for

UK Finance welcome the clarity the EBA is giving on availability and performance of dedicated interfaces.

UK Finance response to EBA consultation on draft Guidelines on the conditions to be met to benefit from an exemption from contingency measures under Article 33(6) of Regulation (EU) 2018/389 (RTS on SCA

UK Finance response to EBA consultation on draft Guidelines on the conditions to be met to benefit from an exemption from contingency measures under Article 33(6) of Regulation (EU) 2018/389 (RTS on SCA

Turning the Revised Payment Services Directive into Digital Opportunity

Turning the Revised Payment Services Directive into Digital Opportunity Contents 1. Introduction 3 2. The Business Risk PSD2 Presents 4 3. The Opportunity for Value Creation 6 4. Making it Happen 7 2 Turning

Turning the Revised Payment Services Directive into Digital Opportunity Contents 1. Introduction 3 2. The Business Risk PSD2 Presents 4 3. The Opportunity for Value Creation 6 4. Making it Happen 7 2 Turning

DATE: 17/11/2017 Open Banking

DATE: 17/11/2017 Open Banking FAO CMA: Proposed amendments to the Agreed Arrangements Adam Land Senior Director of Remedies, Business and Financial Analysis Competition and Markets Authority Victoria House

DATE: 17/11/2017 Open Banking FAO CMA: Proposed amendments to the Agreed Arrangements Adam Land Senior Director of Remedies, Business and Financial Analysis Competition and Markets Authority Victoria House

PSD2 Antoine Larmanjat

PSD2 Antoine Larmanjat Brussels May 2017 Card Issuers Winners and Losers of PSD2 PISPs AISPs Card schemes Retailers Card Issuing PSPs Fintechs PSPs Banks Clearing Houses Consumers 2 AISPs New Business

PSD2 Antoine Larmanjat Brussels May 2017 Card Issuers Winners and Losers of PSD2 PISPs AISPs Card schemes Retailers Card Issuing PSPs Fintechs PSPs Banks Clearing Houses Consumers 2 AISPs New Business

PSD2 & Instant Payment

PSD2 & Instant Payment Presentation to Investors June 2017 Agenda Introduction PSD2/Instant Payment Impacts for Banks Worldline offering for Banks PSD2/Instant Payment Impacts for Merchants Worldline offering

PSD2 & Instant Payment Presentation to Investors June 2017 Agenda Introduction PSD2/Instant Payment Impacts for Banks Worldline offering for Banks PSD2/Instant Payment Impacts for Merchants Worldline offering

PSD2 Final RTS: The Good, the Bad and the Ugly

WHITEPAPER PSD2 Final RTS: The Good, the Bad and the Ugly The EBA s new final RTS on Strong Customer Authentication (SCA) and Secure Communications is an acceptable offering that seems to cover a lot of

WHITEPAPER PSD2 Final RTS: The Good, the Bad and the Ugly The EBA s new final RTS on Strong Customer Authentication (SCA) and Secure Communications is an acceptable offering that seems to cover a lot of

PRETA and PSD2. Access to Accounts (XS2A) PRETA All rights reserved. PRETA All rights reserved.

PRETA All rights reserved. PRETA All rights reserved.") PRETA and PSD2 Access to Accounts (XS2A) Aims of PSD2 Access to Account PSD2 State of play PSD2 was published in EU's OJ on 23 December 2015; PSD2 comes into force 2 years later, i.e. 13 January 2018 Subject

PRETA and PSD2 Access to Accounts (XS2A) Aims of PSD2 Access to Account PSD2 State of play PSD2 was published in EU's OJ on 23 December 2015; PSD2 comes into force 2 years later, i.e. 13 January 2018 Subject

New Payments Platform API Framework

New Payments Platform API Framework Publication Version 1.0 28 September 2018 NPP Australia Limited and SWIFT SCRL The authors NPP Australia Limited and SWIFT accept no liability to any third party in

New Payments Platform API Framework Publication Version 1.0 28 September 2018 NPP Australia Limited and SWIFT SCRL The authors NPP Australia Limited and SWIFT accept no liability to any third party in

Top business challenges imposed by the market s shift towards Open Banking. Technological foundation for your new service offering

WHAT IS IT ABOUT This white paper describes challenges and strategies of banks, merchants and other financial institutions who serve consumers within the PSD2 payment ecosystem. 2 ❶ Top business challenges

WHAT IS IT ABOUT This white paper describes challenges and strategies of banks, merchants and other financial institutions who serve consumers within the PSD2 payment ecosystem. 2 ❶ Top business challenges

Market environment and implementation timeline PSD2 in a nutshell

www.pwc.ch Market environment and implementation timeline PSD2 in a nutshell Why do we need a new Payment Services Directive (PSD)? By 13 th January 2018, Member States will have to implement the Directive

www.pwc.ch Market environment and implementation timeline PSD2 in a nutshell Why do we need a new Payment Services Directive (PSD)? By 13 th January 2018, Member States will have to implement the Directive

DEFINING NEW CUSTOMER JOURNEYS

DEFINING NEW CUSTOMER JOURNEYS Payment Services Directive 2 (PSD2) Scoping out the impacts of the Regulatory Technical Standards (RTS) on Strong Customer Authentication and Common and Secure Open Standards

DEFINING NEW CUSTOMER JOURNEYS Payment Services Directive 2 (PSD2) Scoping out the impacts of the Regulatory Technical Standards (RTS) on Strong Customer Authentication and Common and Secure Open Standards

Manual OPplus 365 Pmt. Export

Manual OPplus 365 Pmt. Export Prepared for Customers & Partners Project OPplus 365 Pmt. Export Prepared by gbedv GmbH & Co. KG manual_bc_opp_zahlungsexport_en.docx page 1 of 153 Andree Steding Contents

Manual OPplus 365 Pmt. Export Prepared for Customers & Partners Project OPplus 365 Pmt. Export Prepared by gbedv GmbH & Co. KG manual_bc_opp_zahlungsexport_en.docx page 1 of 153 Andree Steding Contents

What is new with innovative payments?

What is new with innovative payments? Monika E. Hartmann Payment System Policy Division Directorate General Payment Systems and Market Infrastructure Frankfurt am Main 10 November 2004 Presentation outline

What is new with innovative payments? Monika E. Hartmann Payment System Policy Division Directorate General Payment Systems and Market Infrastructure Frankfurt am Main 10 November 2004 Presentation outline

Horizontal Integration in the Payments Industry

Horizontal Integration in the Payments Industry Gerard Hartsink Senior Executive Vice President 2007 Payments Conference Santa Fe, 3 May 2007 Content European landscape Restructuring of functions Impact

Horizontal Integration in the Payments Industry Gerard Hartsink Senior Executive Vice President 2007 Payments Conference Santa Fe, 3 May 2007 Content European landscape Restructuring of functions Impact

Service description Corporate Access Payables

Service description Corporate Access Payables Page 2 of 12 Table of contents 1 INTRODUCTION... 3 2 STRUCTURE OF DOCUMENTATION... 4 3 AGREEMENT SET-UP... 4 4 AVAILABLE MESSAGE TYPES... 5 5 OFFERED PAYMENT

Service description Corporate Access Payables Page 2 of 12 Table of contents 1 INTRODUCTION... 3 2 STRUCTURE OF DOCUMENTATION... 4 3 AGREEMENT SET-UP... 4 4 AVAILABLE MESSAGE TYPES... 5 5 OFFERED PAYMENT

CONSULTING. Instant Payments. The Coming Paradigm Shift in European Banking Payment Services

CONSULTING Instant Payments The Coming Paradigm Shift in European Banking Payment Services EXECUTIVE SUMMARY Instant payments are the next wave of retail electronic payment solutions in the Single Euro

CONSULTING Instant Payments The Coming Paradigm Shift in European Banking Payment Services EXECUTIVE SUMMARY Instant payments are the next wave of retail electronic payment solutions in the Single Euro

Designing the future of payments. Steve Kirsch CEO, Token

Designing the future of payments Steve Kirsch CEO, Token AGENDA Payments today Can we fix it? How? Next steps Over the next 10 years we will see a number of very significant disruptions in financial services,

Designing the future of payments Steve Kirsch CEO, Token AGENDA Payments today Can we fix it? How? Next steps Over the next 10 years we will see a number of very significant disruptions in financial services,

Opening Keynote. Digital payments in the context of the evolving financial market infrastructure in the euro area

Opening Keynote Digital payments in the context of the evolving financial market infrastructure in the euro area Marc Bayle de Jessé, Director General Market Infrastructure and Payments, ECB, Conference

Opening Keynote Digital payments in the context of the evolving financial market infrastructure in the euro area Marc Bayle de Jessé, Director General Market Infrastructure and Payments, ECB, Conference

PSD2 TAS Open Banking

PSD2 A challenge for Banks but a huge opportunity at the same time for new services TAS Group 2017 Some highlights on PSD2 driven changes PSD2 introduces a new legal structure to payments in the EU, challenging

PSD2 A challenge for Banks but a huge opportunity at the same time for new services TAS Group 2017 Some highlights on PSD2 driven changes PSD2 introduces a new legal structure to payments in the EU, challenging

Euro Retail Payment Board

CSG 153-15 (v1.0) Euro Retail Payment Board Acquirer to Issuer Processing Study 13 June 2016 CSG Secretariat - Cours Saint-Michel 30 A - B 1040 Brussels Tel: +32 2 733 35 33 Fax: +32 2 736 49 88 Enterprise

CSG 153-15 (v1.0) Euro Retail Payment Board Acquirer to Issuer Processing Study 13 June 2016 CSG Secretariat - Cours Saint-Michel 30 A - B 1040 Brussels Tel: +32 2 733 35 33 Fax: +32 2 736 49 88 Enterprise

Payment Services Directive 2: What it Means for Banks, Customers, and Payment Service Providers

Payment Services Directive 2: What it Means for Banks, Customers, and Payment Service Providers Abstract The Payment Services Directive 2 (PSD2) can have a significant impact on customers, banks, and payment

Payment Services Directive 2: What it Means for Banks, Customers, and Payment Service Providers Abstract The Payment Services Directive 2 (PSD2) can have a significant impact on customers, banks, and payment

BAYPORT BUSINESS ONLINE BANKING USER GUIDE TABLE OF CONTENTS

BAYPORT BUSINESS ONLINE BANKING USER GUIDE TABLE OF CONTENTS ADD/MANAGE BUSINESS USERS Add a user 3 Modify account specific access 4 Set access for all accounts 7 Steps to approve a user 8 Set transaction

BAYPORT BUSINESS ONLINE BANKING USER GUIDE TABLE OF CONTENTS ADD/MANAGE BUSINESS USERS Add a user 3 Modify account specific access 4 Set access for all accounts 7 Steps to approve a user 8 Set transaction

820 Payment Order/Remittance Advice

820 Payment Order/Remittance Advice X12/V4030/820 : 820 Payment Order/Remittance Advice Version: 1.0 Draft Author: Alain Bérubé Company: DiCentral Publication: 8/10/2016 Trading Partner: Notes: Table of

820 Payment Order/Remittance Advice X12/V4030/820 : 820 Payment Order/Remittance Advice Version: 1.0 Draft Author: Alain Bérubé Company: DiCentral Publication: 8/10/2016 Trading Partner: Notes: Table of

Edgar, Dunn & Company A Closer Look at the Payment Regulations. Webinar 25 th June 2015

Edgar, Dunn & Company A Closer Look at the Payment Regulations Webinar 25 th June 2015 Edgar, Dunn & Company, 2015 Introduction This webinar will focus on two key regulatory topics: Multilateral Interchange

Edgar, Dunn & Company A Closer Look at the Payment Regulations Webinar 25 th June 2015 Edgar, Dunn & Company, 2015 Introduction This webinar will focus on two key regulatory topics: Multilateral Interchange

AMI-Pay National Stakeholders Group

AMI-Pay National Stakeholders Group 22 March 2018 Patrick Heyvaert Chairperson Ami-Pay National Stakeholders Group Replacing TARGET2 National User Groups Discuss matters related to payments RTGS Retail

AMI-Pay National Stakeholders Group 22 March 2018 Patrick Heyvaert Chairperson Ami-Pay National Stakeholders Group Replacing TARGET2 National User Groups Discuss matters related to payments RTGS Retail

PSD2 and Open Banking Summary of the most important lessons learned from the PSD2 workshop of June 22, 2018

PSD2 and Open Banking Summary of the most important lessons learned from the PSD2 workshop of June 22, 2018 On June 22, 2018, ICT Solutions Ltd. and Online Business Technologies held a joint international

PSD2 and Open Banking Summary of the most important lessons learned from the PSD2 workshop of June 22, 2018 On June 22, 2018, ICT Solutions Ltd. and Online Business Technologies held a joint international

Implementation. Guide For. ComEd. Electronic Data Interchange. Transaction Set. Version Remittance. Version 1.

Implementation ComEd Guide For Electronic Data Interchange Transaction Set Version 4010 820 Remittance Version 1.03 July 30, 2007 820 Payment Order/Remittance Advice Functional Group ID=RA Introduction:

Implementation ComEd Guide For Electronic Data Interchange Transaction Set Version 4010 820 Remittance Version 1.03 July 30, 2007 820 Payment Order/Remittance Advice Functional Group ID=RA Introduction:

Helping ASPSPs implement PSD2 and take advantage of Open Banking January 2019

Helping ASPSPs implement PSD2 and take advantage of Open Banking January 2019 Version 1.36 1 We make it easier for ASPSPs to implement PSD2 and take advantage of Open Banking We have developed a comprehensive

Helping ASPSPs implement PSD2 and take advantage of Open Banking January 2019 Version 1.36 1 We make it easier for ASPSPs to implement PSD2 and take advantage of Open Banking We have developed a comprehensive

Dirk Haubrich, Nilixa Devlukia. Public Hearing, EBA, London, 25 July 2018

Draft Guidelines on the conditions to be met to benefit from an exemption from contingency measures under Article 33(6) of Regulation (EU) 2018/389 (RTS on SCA & CSC under PSD2) Dirk Haubrich, Nilixa Devlukia

Draft Guidelines on the conditions to be met to benefit from an exemption from contingency measures under Article 33(6) of Regulation (EU) 2018/389 (RTS on SCA & CSC under PSD2) Dirk Haubrich, Nilixa Devlukia

SEPA Instant : Driving and Delivering Payments Harmonization

SEPA Instant : Driving and Delivering Payments Harmonization Moving from Faster to Instant Digital adoption globally has evolved and resulted in greater speed, convenience and simplicity in all areas of

SEPA Instant : Driving and Delivering Payments Harmonization Moving from Faster to Instant Digital adoption globally has evolved and resulted in greater speed, convenience and simplicity in all areas of

SEPA Experiences & Outlook

SEPA Experiences & Outlook Eurogiro General Customer Meeting Paris 10 12.06.2008 Discussion Group 1 Presented by Susanne Cihlar SEPA Experience and Outlook A G E N D A Starting position in Austria National

SEPA Experiences & Outlook Eurogiro General Customer Meeting Paris 10 12.06.2008 Discussion Group 1 Presented by Susanne Cihlar SEPA Experience and Outlook A G E N D A Starting position in Austria National

ESIDEL (European Steel Industry Data Exchange Language) Remittance advice

Remittance advice") ESIDEL (European Steel Industry Data Exchange Language) Remittance advice Version. EDIFER «XML Business Group» June 2005 Remittance advice By EUROFER - EDIFER committee - Business working group Creation

ESIDEL (European Steel Industry Data Exchange Language) Remittance advice Version. EDIFER «XML Business Group» June 2005 Remittance advice By EUROFER - EDIFER committee - Business working group Creation

Oracle Banking Digital Experience

Oracle Banking Digital Experience Retail Payments User Manual Release 17.2.0.0.0 Part No. E88573-01 July 2017 Retail Payments User Manual July 2017 Oracle Financial Services Software Limited Oracle Park

Oracle Banking Digital Experience Retail Payments User Manual Release 17.2.0.0.0 Part No. E88573-01 July 2017 Retail Payments User Manual July 2017 Oracle Financial Services Software Limited Oracle Park

INSTANT PAYMENTS. The right time to share investments.

INSTANT PAYMENTS The right time to share investments. INSTANT PAYMENTS: THE RIGHT TIME TO SHARE INVESTMENTS. European authorities have seen instant payments as being essential to support the Digital Single

INSTANT PAYMENTS The right time to share investments. INSTANT PAYMENTS: THE RIGHT TIME TO SHARE INVESTMENTS. European authorities have seen instant payments as being essential to support the Digital Single

NETS - AN IMMEDIATE SOLUTION FOR INSTANT

NETS REALTIME24/7 - AN IMMEDIATE SOLUTION FOR INSTANT PAYMENTS EXECUTIVE SUMMARY Payment systems around the world are changing fundamentally to meet the requirements of digitalisation. Customers expect

NETS REALTIME24/7 - AN IMMEDIATE SOLUTION FOR INSTANT PAYMENTS EXECUTIVE SUMMARY Payment systems around the world are changing fundamentally to meet the requirements of digitalisation. Customers expect

FinTechs as a catalyst for improving payment services

FinTechs as a catalyst for improving payment services Heike Winter, Retail Payment Policy, Deutsche Bundesbank Annual Global Conference of the European Banking Institute Frankfurt, 28 October 2016 Worldwide

FinTechs as a catalyst for improving payment services Heike Winter, Retail Payment Policy, Deutsche Bundesbank Annual Global Conference of the European Banking Institute Frankfurt, 28 October 2016 Worldwide

RESPONSES TO CONSULTATION PAPER

RESPONSES TO CONSULTATION PAPER re: for: Consultation Paper on the draft Regulatory Technical Standards specifying the requirements on strong customer authentication and common and secure communication

RESPONSES TO CONSULTATION PAPER re: for: Consultation Paper on the draft Regulatory Technical Standards specifying the requirements on strong customer authentication and common and secure communication

Open Forum on Open Banking. Brussels, 20 th March 2017

Open Forum on Open Banking Brussels, 20 th March 2017 Proposed programme 1. The progress towards PSD2 implementation and open issues The topic will be introduced with a presentation by Helmut Wacket, Head

Open Forum on Open Banking Brussels, 20 th March 2017 Proposed programme 1. The progress towards PSD2 implementation and open issues The topic will be introduced with a presentation by Helmut Wacket, Head

Who will survive in the payments World: banks, fintech or bigtech?

Who will survive in the payments World: banks, fintech or bigtech? 10th Conference on Payments and Securities Settlement Systems, Ohrid 5-7 July 2017 Michiel van Doeveren and Rui Pimentel 2017: A decisive

Who will survive in the payments World: banks, fintech or bigtech? 10th Conference on Payments and Securities Settlement Systems, Ohrid 5-7 July 2017 Michiel van Doeveren and Rui Pimentel 2017: A decisive

New Payments Platform. A Technical Overview

14 September 2017 New s Platform A Technical Overview NPPA Webinar Bob Masina General Manager, Technology & Operations, New s Platform Australia Today s Webinar Will be a technical overview of how the

14 September 2017 New s Platform A Technical Overview NPPA Webinar Bob Masina General Manager, Technology & Operations, New s Platform Australia Today s Webinar Will be a technical overview of how the

Technology Innovation Exchange 2017

1 2 3 Significant period of change in the next 9 months Between PSD2, OBWG and CMA alone, there is significant, directionally aligned, activity aimed at transforming the landscape. The timing and degree

1 2 3 Significant period of change in the next 9 months Between PSD2, OBWG and CMA alone, there is significant, directionally aligned, activity aimed at transforming the landscape. The timing and degree

How to comply with PSD2 Directive and the EBA-RTS? via Electra openapi

How to comply with PSD2 Directive and the EBA-RTS? via Electra openapi Gyimesi István Head of IT Development gyimesi.istvan@cardinal.hu CARDINAL Kft. Presentation on 31.05.2017 Heiter Ferenc Head of Product

How to comply with PSD2 Directive and the EBA-RTS? via Electra openapi Gyimesi István Head of IT Development gyimesi.istvan@cardinal.hu CARDINAL Kft. Presentation on 31.05.2017 Heiter Ferenc Head of Product

Moving Towards a SEPA-compliant Infrastructure

Moving Towards a SEPA-compliant Infrastructure JAN WILLEM MARS GTNEWS, NOVEMBER 22, 2007 Moving Towards a SEPA-compliant Infrastructure Author: Jan Willem Mars This article was published at GTNews, November

Moving Towards a SEPA-compliant Infrastructure JAN WILLEM MARS GTNEWS, NOVEMBER 22, 2007 Moving Towards a SEPA-compliant Infrastructure Author: Jan Willem Mars This article was published at GTNews, November

Universal Payment Gateway (UPG)

") Universal Payment Gateway () We offer two models: Direct Model All payments are made from your bank account and collections are settled directly into your bank account. Aggregation Model All payments are

Universal Payment Gateway () We offer two models: Direct Model All payments are made from your bank account and collections are settled directly into your bank account. Aggregation Model All payments are

The communication between Third Party Providers and Banks. PSD2 in a nutshell

www.pwc.com/psd2 The communication between Third Party Providers and Banks. What will the impact of technology be? PSD2 in a nutshell Summary The banking system is at a turning point, under the pressure

www.pwc.com/psd2 The communication between Third Party Providers and Banks. What will the impact of technology be? PSD2 in a nutshell Summary The banking system is at a turning point, under the pressure

Simplifying Payments. Payments Training. Learn more about Cards and Payments training offered by The EFT Company

Simplifying Payments Learn more about Cards and Payments training offered by The EFT Company Payments Training www.eftcompany.com 1 2 EFT Essentials provides comprehensive training courses in the areas

Simplifying Payments Learn more about Cards and Payments training offered by The EFT Company Payments Training www.eftcompany.com 1 2 EFT Essentials provides comprehensive training courses in the areas

820 Payment Order/Remittance Advice

820 Payment Order/Remittance Advice Functional Group ID=RA Introduction: This Draft Standard for Trial Use contains the format and establishes the data contents of the Payment Order/Remittance Advice Transaction

820 Payment Order/Remittance Advice Functional Group ID=RA Introduction: This Draft Standard for Trial Use contains the format and establishes the data contents of the Payment Order/Remittance Advice Transaction

Guidelines for PSD2 Implementation

nextdigitalbanking.com Guidelines for PSD2 Implementation Helping banks explore API strategies and options CONTENTS: Shifting mindsets and expectations Top five strategic considerations for PSD2 implementation

nextdigitalbanking.com Guidelines for PSD2 Implementation Helping banks explore API strategies and options CONTENTS: Shifting mindsets and expectations Top five strategic considerations for PSD2 implementation

Why you should adopt SWIFT gpi in 2018 to future-proof your payment operations

Why you should adopt SWIFT gpi in 2018 to future-proof your payment operations Stanley Wachs Jamy Maigre Alex Coutsouradis Webinar 4 October 2018 In this webinar 1 2 3 Benefits of SWIFT gpi for payment

Why you should adopt SWIFT gpi in 2018 to future-proof your payment operations Stanley Wachs Jamy Maigre Alex Coutsouradis Webinar 4 October 2018 In this webinar 1 2 3 Benefits of SWIFT gpi for payment

Assessment of follow-up on ERPB statements, positions and recommendations

ERPB Secretariat ECB-UNRESTRICTED 13 June 2016 ERPB/2016/003 Assessment of follow-up on ERPB statements, positions and recommendations 1. Introduction & summary The aim of this document is to provide an

ERPB Secretariat ECB-UNRESTRICTED 13 June 2016 ERPB/2016/003 Assessment of follow-up on ERPB statements, positions and recommendations 1. Introduction & summary The aim of this document is to provide an

Going Global Business without Borders

Treasury and Trade Solutions October 2017 Going Global Business without Borders Enabling International Growth Simona Anghel Romania Sales Head Treasury and Trade Solutions, Citi The Pursuit of Growth Treasury

Treasury and Trade Solutions October 2017 Going Global Business without Borders Enabling International Growth Simona Anghel Romania Sales Head Treasury and Trade Solutions, Citi The Pursuit of Growth Treasury

Lawrie Brown Grigori Goldman

Periodical Payments Using X.509 Restricted Proxy Certificates Lawrie Brown Grigori Goldman January 2010 University of New South Wales @ Australian Defence Force Academy Who Am I? senior lecturer at UNSW@ADFA

Periodical Payments Using X.509 Restricted Proxy Certificates Lawrie Brown Grigori Goldman January 2010 University of New South Wales @ Australian Defence Force Academy Who Am I? senior lecturer at UNSW@ADFA

TOKENIZATION: THE FUTURE OF ACCOUNT NUMBERS. Steve Ledford The Clearing House

TOKENIZATION: THE FUTURE OF ACCOUNT NUMBERS Steve Ledford The Clearing House Problem Statement: The proliferation of live account credentials creates huge risks Bank issues physical card Plastic at point

TOKENIZATION: THE FUTURE OF ACCOUNT NUMBERS Steve Ledford The Clearing House Problem Statement: The proliferation of live account credentials creates huge risks Bank issues physical card Plastic at point

Transforming Payments in an assembly game

Open Banking API for Payments Transforming Payments in an assembly game Jean-François Delorme Partner Paiements, DXC Technology The World of Yesterday The classic French Garden style 2 Payment Industry

Open Banking API for Payments Transforming Payments in an assembly game Jean-François Delorme Partner Paiements, DXC Technology The World of Yesterday The classic French Garden style 2 Payment Industry

Realex Payments Redirect/Remote PrestaShop Module for v 1.5+

Realex Payments Redirect/Remote PrestaShop Module for v 1.5+ Integration Guide Version: v 1.0 Document Information Document Name: Realex Payments Redirect/Remote PrestaShop Extension s v 1.5 Document Version:

Realex Payments Redirect/Remote PrestaShop Module for v 1.5+ Integration Guide Version: v 1.0 Document Information Document Name: Realex Payments Redirect/Remote PrestaShop Extension s v 1.5 Document Version:

Electronic Data Interchange

Implementation Guide For Electronic Data Interchange Transaction Set Version 4010 820 Remittance Version 1.03 June 12, 2000 820 Payment Order/Remittance Advice Functional Group ID=RA Introduction: This

Implementation Guide For Electronic Data Interchange Transaction Set Version 4010 820 Remittance Version 1.03 June 12, 2000 820 Payment Order/Remittance Advice Functional Group ID=RA Introduction: This

TRAVELEX GLOBALPAY. Managing all your payment needs online

TRAVELEX GLOBALPAY Managing all your payment needs online SIMPLIFYING THE PAYMENTS PROCESS At Travelex we believe in making the payments process simple, fast and accurate which is why we have introduced

TRAVELEX GLOBALPAY Managing all your payment needs online SIMPLIFYING THE PAYMENTS PROCESS At Travelex we believe in making the payments process simple, fast and accurate which is why we have introduced

Data Sheet. IBM Financial Transaction Manager. Deliver a fast and agile payments infrastructure

Data Sheet IBM Financial Transaction Manager Deliver a fast and agile payments infrastructure Highlights Match today s industry needs and enable progressive modernization with the IBM Financial Transaction

Data Sheet IBM Financial Transaction Manager Deliver a fast and agile payments infrastructure Highlights Match today s industry needs and enable progressive modernization with the IBM Financial Transaction

Strong Customer Authentication in Practice

Strong Customer Authentication in Practice A Signicat whitepaper June 2017 1 This white paper has been produced on behalf of Signicat by Norfico (www.norfico.net) and Consult Hyperion (www.chyp.com) Table

Strong Customer Authentication in Practice A Signicat whitepaper June 2017 1 This white paper has been produced on behalf of Signicat by Norfico (www.norfico.net) and Consult Hyperion (www.chyp.com) Table

Barzahlen Integration Guide. Version 6.2.2

Barzahlen Integration Guide Version 6.2.2 As of: 13.02.2017 Table of Contents About Barzahlen... 4 General information about Barzahlen... 4 Process flow chart... 5 Configuration for Barzahlen... 6 Paygate

Barzahlen Integration Guide Version 6.2.2 As of: 13.02.2017 Table of Contents About Barzahlen... 4 General information about Barzahlen... 4 Process flow chart... 5 Configuration for Barzahlen... 6 Paygate

A step towards cashless economy - Unified Payments Interface (UPI)

") A step towards cashless economy - Unified Payments Interface (UPI) What is Unified Payment Interface? Objective of a unified payments system is to offer an architecture and a set of APIs on top of existing

A step towards cashless economy - Unified Payments Interface (UPI) What is Unified Payment Interface? Objective of a unified payments system is to offer an architecture and a set of APIs on top of existing

Single Euro Payments Area

Single Euro Payments Area Background The Single Euro Payments Area (SEPA) is a payment-integration initiative of the European Union for simplification of bank transfers. As of March 2012, SEPA consists

Single Euro Payments Area Background The Single Euro Payments Area (SEPA) is a payment-integration initiative of the European Union for simplification of bank transfers. As of March 2012, SEPA consists