Thesaurus of Producer Price Indices for Services (SPPI s)

|

|

|

- Buddy Riley

- 5 years ago

- Views:

Transcription

1 VOORBURG GROUP 2016 Thesaurus of Producer Price Indices for Services (SPPI s) you cannot use language to get in between language and reality. If you describe reality, you always use words; so when you compare a concept with reality, you in fact compare only a concept with another concept. Roger Scruton (after Wittgenstein) Main writer and editor: Aurél Kenessey (Statistics Netherlands), with contributions from Seppo Varjonen (OECD), Richard McKenzie (OECD), Pam Davies (Office of National Statistics), and Kuniko Moriya (Bank of Japan). The draft was discussed at the 2006 Voorburg group meeting where a small Task Force was established to continue the work. The members of the Task Force were Kuniko Moriya, Roslyn Swick (BLS), and Seppo Varjonen. This 2016 update was compiled by Bonnie Murphy (BLS) and will be discussed at the 2016 Voorburg group meeting.

2 1. Introduction Producer Price Indices for services (SPPI s) have received increasing attention in the Voorburg Group. Here, an important problem emerged: members of the Group use ad hoc terminology. This is not surprising as SPPI s deal with new statistics, not discussed conceptually before internationally. Within one National Statistical Office, it is easy to share a clear and common terminology, as the group of SPPI statisticians is small and their contacts are frequent. This is not the case in an international exchange, where statisticians from many different mother tongues convene. Consequently, the prices session of the Voorburg Group was hampered by confusion in terminology, although individual papers were clear as they used the ad hoc terminology of a single writer. Problems were bigger in reaching the main goal of the OECD/Eurostat SPPI Guide: codification of the present state of knowledge on SPPI s. In the compilation of this Guide a Babel on terminology erupted. After considerable effort, a satisfactory consensus was reached. The Guide was presented at the 2005 Voorburg Group meeting, as well as the paper Pricing methods which analyses difficulties in terminology on SPPI s. As a consequence, the Task Force that reviewed the Voorburg Group process, voiced the need for a dictionary or thesaurus to standardise the vocabulary and terminology of SPPI s. The guide was further discussed at the 2006 Voorburg meeting and updates have been made to clarify the meaning of the different pricing methods. An addendum of examples that illustrate the use of the different pricing methods was also added. In 2016, the margin pricing method was added and matches the definition from the Second Edition of the Eurostat/OECD SPPI Guide. The Eurostat/OECD SPPI Guide provides extensive discussions on eight pricing methods. These eight pricing methods are the basis for a good description of a pricing method of an individual SPPI. Additional clarification has been added to facilitate the classification of practices in the various pricing methods. However, to describe an SPPI well and unambiguously, it has to be described in the light of an additional concept: the data type in the survey. The principal part of this thesaurus consists of the terms in the table hereunder: eight pricing methods, and seven data types in the survey. It is envisaged that these terms are the main ones used in future mini-papers and sector-papers of the Voorburg Group. They are discussed in section 2 Main terms. Pricing methods (Section 2.1) Component pricing Contract pricing Direct use of prices of repeated services Model pricing Percentage fees Pricing based on working time Unit values Margin pricing Data type in the survey Percentages fees and related value List prices Input prices Real transaction prices Revenue and amount sold Expert estimate Acquisition and selling prices

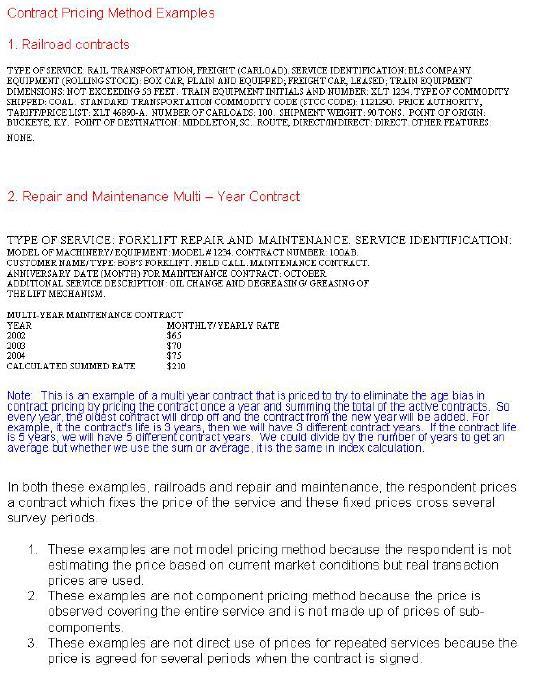

3 Section 3 Other preferred terms, discusses further terms, also envisaged for future use in papers. Section 4 Related terms, lists many more terms (including many used in Voorburg Group papers between 2000 and 2005). The use of these is discouraged, mostly because they mean (almost) the same as terms in sections 2 and 3; having multiple terms for one concept is considered not necessary, even confusing. The underlining of a term means that it has its own entry in section 2, 3 or Main terms 2.1 The eight pricing methods from the OECD/Eurostat SPPI Guide Component pricing: a pricing method that divides the service into a number of key output components of which one or more are then priced separately. The data type in the survey for this pricing method concerns existing hard company data (real transaction prices, revenue and amount sold, list prices, etc. except time-based prices). The statistician enters all the prices on a worksheet or bill, resulting in an aggregate price. Component pricing is different from model pricing because component pricing is fully based on real transaction prices that have been combined to form a price. To be categorized as component pricing, time based prices (as price for one hour s work) should not be in use in the pricing of components because, due to their often significant weight in a price, the method would become pricing based on working time. On the other hand, assessing required working time rather than keeping it fixed would mean that the method falls into the category of model pricing where at least some subjective estimation is made. Note that the component price is not (necessarily) a price of any transacted service because quantities of sub-services in the component price may differ from actually transacted services. The method s best-known use is in telephony SPPI s, were it is sometimes known by a synonym, bill method, a term which should not to be used to avoid confusion. Contract pricing: a pricing method which uses real transaction prices of a special kind as the data type in the survey. They are special because the prices are charged for the same (or very similar) service that is repeated each survey period by the same producer for the same client. Prices of contracts are agreed for more than one period when the contract is signed or renewed. Prices may be the same for a certain period of time or change according to an agreed pattern. This pricing method may work if the pricing mechanism entails these contracts, for instance in cleaning, security services and freight transport. The method should be used with caution because periodical payments are normally agreed when a contract is signed. As a result, payments may be flat or follow an agreed pattern and are not necessarily in line with market evolution. Therefore, inclusion of a sufficient number of price observations in a survey and adequate updating of the sample are of crucial importance. Updating should be made with care to avoid the resulting SPPI being largely influenced by changes in the sample rather than showing true price development in the market. Note that the surveyed price data may be based on a contract but this does not presuppose that the pricing method used is contract pricing. In contract pricing, the contract is supposed to cover more than one survey period, services provided in each period are the same and prices are agreed at the same time for more than one period.

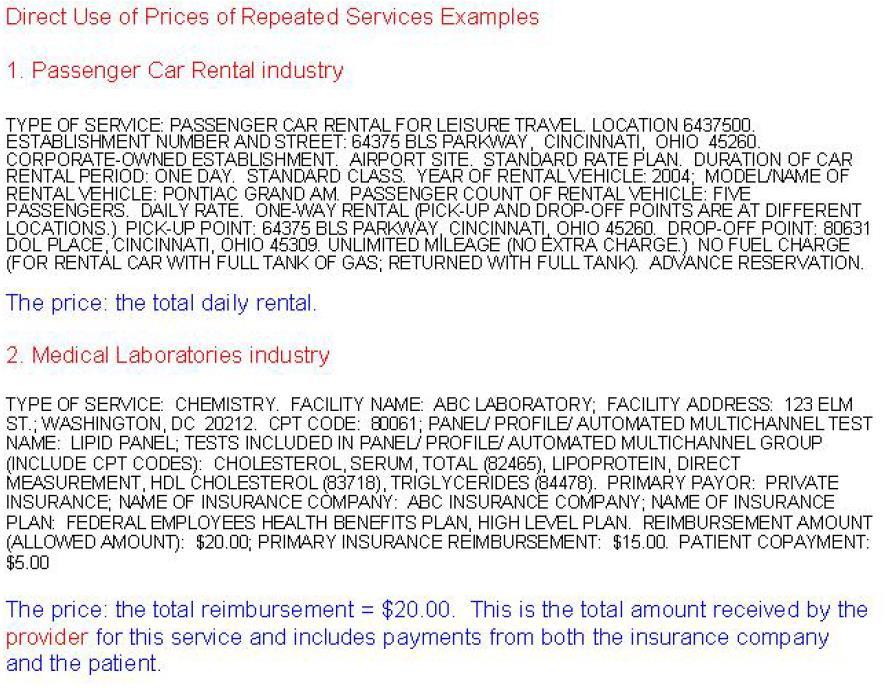

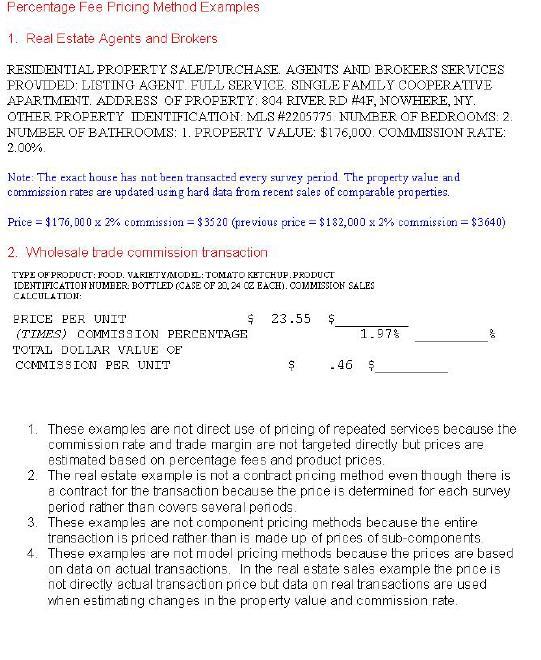

4 Direct use of prices of repeated services: a straightforward pricing method which surveys a real transaction price or (although not preferably) a list price, thereby acquiring directly the price of a service that occurs every survey period (a real transaction). This coincides with the PPI Manual s transaction pricing and is standard PPI and CPI practice. It is the preferred and easiest method because there is no difference between the surveyed prices and the price entering standard PPI compilation procedures. Assumptions or calculations are necessary only when services in the sample are replaced or their quality changes requiring price adjustments. Model pricing: a pricing method in which a price is estimated for a standardised product, a model transaction, which is not transacted in the comparison period. A single fictitious service can be set as the re-pricable product for a group of respondents. Alternatively, the specifications of an actual service provided can be developed as the model to price. When selecting an actual transaction to use for the model, generally a recent transaction is selected. An advantage in using a recent transaction is that the service may represent better current activity of an enterprise and the price may also be easier to update. Synonyms for this second type found in the literature, which should not be used to avoid confusion, are: estimated net transaction price or billed method. In estimating a realistic transaction price, the expert might consider real transaction prices, revenue and amount sold, list prices, input prices as data type in the survey for calculating this price. A particularly central task is to estimate working time required in a service provision. A subjective judgement based on the overall market situation is needed, for instance, by keeping recent bids in mind. The resulting total price for the standardised product is a fully fictitious expert estimate. The model pricing method is used for unique services, notably the professional business services for which hourly charge-out rates are also used often. It is often a challenge to make an adequate quality adjustment when the service becomes outdated and is replaced by a new service. Model pricing differs from component pricing because model pricing always involves estimation of the prices or expert evaluation to determine prices whereas component pricing is fully based on real transaction prices. Model pricing is also different from pricing based on working time. It captures the price of the whole service provided to a client, while pricing based on working time does not. Instead, it captures a price of time (e.g. rate per hour) in service provision. Pricing factors such as hours worked are updated in model prices when the hours required to provide the service change. As noted, the re-evaluation of the required working time is essential for model pricing to capture changes in the efficiency in service provision. If the working time is not evaluated but assumed automatically unchanged, the method cannot be called model pricing but would be categorized as pricing based on working time. Percentage fees: a pricing method that estimates a price by multiplying a percentage and the value of the good that the service and the percentage fee are tied to. This is only possible if the pricing mechanism uses these figures. For example, prices for service of real estate agencies use the price of the real estate and a percentage fee. Other examples include placing advertisements, architecture and rental. If the percentages or values are estimated by the respondent, then this is still the percentage fee pricing method. Note that the case where the price development is measured by directly comparing the fees tied to the same product (in trade, the difference between selling and acquisition price) in consecutive periods, would be categorized as direct use of prices of repeated services. In the percentage fee method, the price change is split into two parts, change of the percentage fee and change of the product price. Doing this is often appropriate for practical reasons, mainly because prices for exactly the same products are not necessarily available in consecutive periods. Each data type in the survey (the percentage and the price of the good) can be surveyed from a different source. Strictly speaking, the percentage can be taken from a list or be estimated by an expert

5 or calculated as an average. Often, the price (index) of the good is already available within the statistical institute, like the price index for house prices or goods rented (e.g. office equipment). A synonym, not to be used to avoid confusion is ad valorem price. Pricing based on working time: a pricing method which surveys the money amount charged to a buyer of a service, for a standard amount (e.g. one hour) of work by an employee of the producer, contributing to the production (provision) of that service. It is only used in the professional business services were the pricing mechanism is such that the price of a service is largely based on the number and charge-out rates of the hours needed to produce the service (not to be mistaken for the employee s wage). The data type in the survey can differ highly: 1. unit values type information of revenue divided by number of hours worked (also known as realised hourly rates and fee income per grade of worker), 2. list prices (also known as standard hourly rates), 3. input data in the form of wages increased by a overhead costs and mark up, or 4. expert estimate. In general, pricing based on working time is inferior to the other pricing methods in the sense that prices of the whole service provided to a client is not directly targeted. Thus, despite the fact that charge-out rates are typically used as pricing mechanisms, these prices do not necessarily conform to the central principle of the index compilation where prices for some products are surveyed in consecutive periods. The method may omit changes in the quality of services and, more importantly, disregard possible changes in the efficiency of service provision resulting in a possible productivity bias A risk of bias is significant in service activities that are capital intensive or undergoing strong technological development. Note that pricing based on working time usually results in an hourly charge-out rate, but prices for working time can also be entered into a model transaction. If the price of a model transaction is highly determined by hourly rates and no re-evaluation of required working time is made, the OECD/Eurostat SPPI Guide recommends that the pricing method is classified as pricing based on working time, to make clear to users that the resulting SPPI has potentially a productivity bias. If the hours required to provide the service is updated when the service changes, then the pricing method would be model pricing. Unit values: a pricing method that uses revenue and amount sold as data type in the survey. The quotient of these two results in an average price over a large number of transactions, which may be regarded as an output component or a real transaction but it is usually an average price over a whole group of transactions. For example, in telephony, the local calling price is the total revenue from local phone calls divided by the total number of local phone calls. The unit value method is applicable in cases when transactions in a group are sufficiently homogeneous. In other words, quality of individual services is unchanged and their quantities in the transactions do not vary. If this is not the case, changes within a group would be erroneously recorded as price changes. Note that the term unit value is often used for any average price over multiple transactions and/or a survey period, being preferred over the alternative, a single price observation. However, average prices where the average is the sum of service prices divided by the number of service prices quoted are NOT included in the unit value pricing method. The unit value pricing method is where the price is the revenue for providing the services divided by the amount of service provided. Note also the term unit price. Margin pricing: a pricing method where prices are not directly observable but where the value of the service can be measured as the difference between the observed acquisition and selling prices of a given product.

6 The margin pricing method is used to measure price development in services that are not separately invoiced and where the service is related to the transformation in space or time of an item. The item may be a product, such as a good purchased and sold by a retailer or a loan provided by a financial intermediary. The price of the service can be estimated as the difference between the price paid by the service provider for the good or service they transformed and the price paid by the final consumer (at the same point in time). 2.2 Data types in surveys Expert estimate: a data type in the survey which bases a price on the potentially subjective judgement of the expert in the responding company who fills in the survey form. The estimate can reflect different types of units, for instance only components of an entire service or prices per working time and per product. If an SPPI uses expert estimates, it effectively transfers the responsibility and burden of pricing to the expert. The pricing statistician therefore has less control over how the price that enters SPPI calculation is established. Input prices: a data type in the survey which corresponds to the prices of all (or a number of) input components needed to make a set amount of output. The profit margin is always to be included as an important input component. The pricing mechanism is sometimes such that an enterprise applies a set factor to calculate an output price from an input price. This practice is best known from the pricing method pricing based on working time which multiplies an hourly wage with a factor (see also markup) to arrive at an hourly charge-out rate. The other pricing method using this data type in the survey is model pricing. Strictly speaking, the input prices can be taken from a list or be estimated by an expert or calculated as an average from real transactions, but an input price is set apart as it is not an output price, unlike every standard data type in the survey. List price: a data type in the survey in which the price of a product is quoted from the producer s price list, catalogue, Internet site, etc. It is generally the gross price exclusive of all discounts, surcharges, rebates, etc. that may apply to an actual transaction. A list price is therefore inferior to a real transaction price or shipment price for SPPI compilation, although from case to case the assumption of correspondence with a real transaction price can differ from reasonable to poor. List prices for fixed amounts of working time are known as standard hourly rates. Another synonym which should not be used to avoid confusion is book price. Percentage fees and related value: a data type in the survey, only used in the pricing method percentage fees. Strictly speaking, the percentage can be taken from a list or be estimated by an expert or calculated as an average from real transactions, but a percentage is set apart as it is not a price, unlike every other data type in the survey. The related value (see percentage fees) is an unusual data type as well and refers to an underlying good or other product to which the service relates. Real transaction price: a data type in the survey in which the price was truly paid in the market, taken form a receipt, bank statement or electronic database with transactions. Revenue and amount sold: a data type in the survey in which the quotient of the two variables (revenue and amount sold) results in a price, which can be used in almost any pricing method. In calculating this price, the equation Value (v) = Price(p)* Quantity(q) is re-written at the micro level into p=v/q. Acquisition and selling prices: a data type in the survey where the difference between the two (acquisition and selling prices) allows for calculation of a margin price. The acquisition price is the cost to the seller of purchasing a product or a service from

7 a supplier excluding any taxes and rebates. The selling price is the cost to the purchaser excluding any taxes and transport charges. 3. Other preferred terms Amount: the quantity of (a component of a) service which is homogenous enough to be useful in SPPI related calculations. E.g. the quantity of calling minutes in telephony is useful, but the quantity of projects of an engineering firm is not useful. See revenue and amount sold. Data type in the survey: a description of the raw data surveyed by a statistician from a respondent. The pricing method transforms these data into prices ready for standard PPI compilation procedures. Fictitious service: a service that is devised for a price survey only, used in model pricing. Hourly charge-out rates: the price of one hour s work by an employee of the producer which contributes to the production (provision) of a service. Input component pricing: a pricing method which is based on the assumption that a selection of input prices can be an acceptable estimate of an output price. This pricing method on its own, is not a desirable method and is, therefore, not listed with the main pricing methods. An example is the use of truck write-off, driver s wage, and fuel costs to estimate an output price for road haulage. Note that input prices can be used in a number of better pricing methods. Lump sum: a total price (quote) which is derived from substantial calculations based on (typically many) components, as opposed to separate price (quoting) of the components, e.g. the price of a large engineering project. Model transaction: a standardised service which is frozen to allow meaningful price comparisons over time. Order price: the price quoted at the time the order is placed by the purchaser. (From PPI manual). See also shipment price. Pricing method: the use of a specific type of information on prices to represent the evolution of price in price index compilation. It is a procedure put in place by statisticians to make price data eligible to be entered in an index. The pricing method is largely determined by the characteristics of the data. (from OECD/Eurostat SPPI Guide). Pricing mechanism: the way prices come about in the market between producer and client. It differs from a pricing method which is a method used by a statistician. In the ideal circumstance where the data type in the survey = real transaction prices, the difference between pricing mechanism and pricing method is unimportant. In the ideal case, a price that came about in the market is surveyed and directly used in SPPI calculation. Revenue: money paid to a producer, see revenue and amount sold. The same is sometimes meant by income and turnover. Shipment price: the price at the time the order is delivered to the purchaser. (From PPI manual). See also order price. Spot (market) price: a generic term referring to any short-term sales agreement, as opposed to prices in a long-term contract. It generally refers to a single provision of an uncustomized service, reflecting current (efficient) market conditions. (Largely from the PPI Manual). Tariff prices: money to be paid by a customer for regulatory tariffs, additional to the service price that a producer charges. Tariff prices are outside the pricing mechanism that arrives at a market price. Tender(ed) price: a price that is offered and which may differ from the transaction price finally arrived at. A list price and model pricing may involve tendered prices. Transaction: The buying and selling of a product on terms mutually agreed by the buyer and seller. (From PPI manual).

8 Transaction pricing: ideal pricing method using actually paid prices of individual transactions that are repeated in each survey period. For SPPI s, same as direct use of prices of repeated services. Unique service: a type of service such that any two actually provided services of the type differ too much to allow meaningful comparison of their prices for acquiring a price relative. Unit price: a price of an individual product, e.g. a price per kg etc. A unit price is not calculated from revenue and amount sold (not a unit value). User cost prices: prices calculated as forgone interest (compared to a standard interest rate), charged for FISIM of loans and savings in banking SPPI s. 4. Related terms The use of these is discouraged, as they mean (almost) the same as terms in sections 2 and 3. Ad valorem price: see percentage fee. Average invoiced hourly rate: see pricing based on working time. Average price per qualification: see pricing based on working time. Bill(ing) method: see component pricing. Billed method: see model pricing. Billing rate: a rate or price taken from a bill, and therefore a real transaction price. Book price: see list price. Competitive contract pricing: same as model pricing. Estimated net transaction price or estimated new transaction price: see model pricing. Estimated output price approach: pricing based on working time with input prices as data type in the survey; the input prices are hourly wages. Fee income per grade of worker: see pricing based on working time. Income: see revenue. Labour charge-out rates: same as hourly charge-out rates, (=output) despite the suggestion of a relation to wages for labour (=input). Market price: see real transaction price. Mark-up (markup): a term used in SPPI context for the factor between input (like wages) and output prices (hourly rates), see input prices. Term should not be used as it is defined differently in the SNA. Model contract pricing: same as model pricing. Model service: see model transaction. Offered price: see tender(ed) price. Price determination method: same as pricing mechanism. Price fixing method: same as pricing mechanism. Price setting: same as pricing mechanism. Rate method: roughly the same as component pricing. Term used for telephony SPPI s. A rate is the price of a unit of which typically large numbers are bought, e.g. a price per minute calling. Realised hourly rates: see pricing based on working time.

9 Specification pricing: a term to be avoided, used in different and irreconcilable ways. The word specification reflects that in a PPI, sampled products have to be specified and quality held constant. Standard hourly rates: see pricing based on working time.

10

11

12

13

14

15

16

17 Wholesale trade margin pricing example

Organization of Conventions and Trade Shows

31st Meeting of the Voorburg Group on Services Statistics Zagreb, Croatia 19 23 September, 2016 Sector Paper : Organization of Conventions and Trade Shows David M. Friedman U.S. Bureau of Labor Statistics

31st Meeting of the Voorburg Group on Services Statistics Zagreb, Croatia 19 23 September, 2016 Sector Paper : Organization of Conventions and Trade Shows David M. Friedman U.S. Bureau of Labor Statistics

Week 5. ACT102 Introduction to Accounting. Objectives 21/02/2018. What are retailing operations?

ACT102 Introduction to Accounting Week 5 Objectives Describe retailing operations, perpetual and periodic inventory systems and understand how to account for GST Account for the purchase of inventory using

ACT102 Introduction to Accounting Week 5 Objectives Describe retailing operations, perpetual and periodic inventory systems and understand how to account for GST Account for the purchase of inventory using

MERCHANDISING TRANSACTIONS: INTRODUCTION TO INVENTORIES AND CLASSIFIED INCOME STATEMENT

Learning Objectives CHAPTER 6 MERCHANDISING TRANSACTIONS: INTRODUCTION TO INVENTORIES AND CLASSIFIED INCOME STATEMENT 1. Record journal entries for sales transactions involving merchandise. 2. Describe

Learning Objectives CHAPTER 6 MERCHANDISING TRANSACTIONS: INTRODUCTION TO INVENTORIES AND CLASSIFIED INCOME STATEMENT 1. Record journal entries for sales transactions involving merchandise. 2. Describe

5. METHODOLOGY FOR PRICES, PRICE INDEX CALCULATION Cost and Volume Indictors of Construction Companies Activity

5. METHODOLOGY FOR PRICES, PRICE INDEX CALCULATION 5.1. Cost and Volume Indictors of Construction Companies Activity As planned the sample has a higher percentage of large and medium-sized companies than

5. METHODOLOGY FOR PRICES, PRICE INDEX CALCULATION 5.1. Cost and Volume Indictors of Construction Companies Activity As planned the sample has a higher percentage of large and medium-sized companies than

Type of Inventory. OVERVIEW In case of manufacturing concerns. Stores and Spares. Formulae for Determining Cost of Inventory

CHAPTER 4 INVENTORIES LEARNING OUTCOMES After studying this chapter, you will be able to: Understand the meaning of term 'Inventory'. Learn the technique of Specific identification method, FIFO, Average

CHAPTER 4 INVENTORIES LEARNING OUTCOMES After studying this chapter, you will be able to: Understand the meaning of term 'Inventory'. Learn the technique of Specific identification method, FIFO, Average

Financial Accounting Chapter 5 Notes The Operating Cycle And Merchandising Operations

Financial Accounting Chapter 5 Notes The Operating Cycle And Merchandising Operations I. Management Issues in Merchandising Business Merchandising business earns income by buying and selling goods. Such

Financial Accounting Chapter 5 Notes The Operating Cycle And Merchandising Operations I. Management Issues in Merchandising Business Merchandising business earns income by buying and selling goods. Such

Reading Essentials and Study Guide

Lesson 3 Cost, Revenue, and Profit Maximization ESSENTIAL QUESTION How do companies determine the most profitable way to operate? Reading HELPDESK Academic Vocabulary generates produces or brings into

Lesson 3 Cost, Revenue, and Profit Maximization ESSENTIAL QUESTION How do companies determine the most profitable way to operate? Reading HELPDESK Academic Vocabulary generates produces or brings into

Eco402 - Microeconomics Glossary By

Eco402 - Microeconomics Glossary By Break-even point : the point at which price equals the minimum of average total cost. Externalities : the spillover effects of production or consumption for which no

Eco402 - Microeconomics Glossary By Break-even point : the point at which price equals the minimum of average total cost. Externalities : the spillover effects of production or consumption for which no

Exemplar for Internal Achievement Standard. Accounting Level 3

Exemplar for Internal Achievement Standard Accounting Level 3 This exemplar supports assessment against: Achievement Standard 91409 Demonstrate understanding of a job cost subsystem for an entity An annotated

Exemplar for Internal Achievement Standard Accounting Level 3 This exemplar supports assessment against: Achievement Standard 91409 Demonstrate understanding of a job cost subsystem for an entity An annotated

NACE 82.2 Activities of call centres in Sweden

STATISTICS SWEDEN 29th Voorburg Group Meeting Dublin, Ireland September 22-26, 2014 Mini-presentation for SPPI on: NACE 82.2 Activities of call centres in Sweden Kristoffer Olsson Price Unit, Statistics

STATISTICS SWEDEN 29th Voorburg Group Meeting Dublin, Ireland September 22-26, 2014 Mini-presentation for SPPI on: NACE 82.2 Activities of call centres in Sweden Kristoffer Olsson Price Unit, Statistics

The Measurement and Importance of Profit

The Measurement and Importance of Profit The term profit comes from the Old French prufiter, porfiter, meaning to benefit. Throughout history, the notion of profit has always been a controversial subject.

The Measurement and Importance of Profit The term profit comes from the Old French prufiter, porfiter, meaning to benefit. Throughout history, the notion of profit has always been a controversial subject.

VOORBURG 2004 MINI PRESENTATIONS ON PRODUCER PRICE INDICES DEVELOPMENT OF A UK PRICE INDEX FOR LABOUR RECRUITMENT SERVICES

VOORBURG 2004 MINI PRESENTATIONS ON PRODUCER PRICE INDICES DEVELOPMENT OF A UK PRICE INDEX FOR LABOUR RECRUITMENT SERVICES Anthony Luke and Pam Davies UK Office for National Statistics Introduction The

VOORBURG 2004 MINI PRESENTATIONS ON PRODUCER PRICE INDICES DEVELOPMENT OF A UK PRICE INDEX FOR LABOUR RECRUITMENT SERVICES Anthony Luke and Pam Davies UK Office for National Statistics Introduction The

Chapter 8 Inventories: Measurement

Chapter 8 Inventories: Measurement QUESTIONS FOR REVIEW OF KEY TOPICS Question 8 1 Inventory for a manufacturing company consists of (1) raw materials, (2) work in process, and (3) finished goods. Raw

Chapter 8 Inventories: Measurement QUESTIONS FOR REVIEW OF KEY TOPICS Question 8 1 Inventory for a manufacturing company consists of (1) raw materials, (2) work in process, and (3) finished goods. Raw

Copyright holder is licensing this under the Creative Commons License, Attribution 3.0.

2010 by Scott Richards of Beyond the Numbers Copyright holder is licensing this under the Creative Commons License, Attribution 3.0. http://creativecommons.org/licenses/by/3.0/us/ This is a free e-book

2010 by Scott Richards of Beyond the Numbers Copyright holder is licensing this under the Creative Commons License, Attribution 3.0. http://creativecommons.org/licenses/by/3.0/us/ This is a free e-book

P2 Performance Management

DO NOT OPEN THIS QUESTION PAPER UNTIL YOU ARE TOLD TO DO SO Performance Pillar P2 Performance Management 20 November 2013 Wednesday Afternoon Session Instructions to candidates You are allowed three hours

DO NOT OPEN THIS QUESTION PAPER UNTIL YOU ARE TOLD TO DO SO Performance Pillar P2 Performance Management 20 November 2013 Wednesday Afternoon Session Instructions to candidates You are allowed three hours

Copyright ownership: United Business Services (Aust) Pty Ltd.

Pty Ltd.") Assessment Tasks Candidate Guide BSBSMB402A Plan small business finances Copyright ownership: United Business Services (Aust) Pty Ltd. This book is copyright protected under the Berne Convention. All rights

Assessment Tasks Candidate Guide BSBSMB402A Plan small business finances Copyright ownership: United Business Services (Aust) Pty Ltd. This book is copyright protected under the Berne Convention. All rights

Cross cutting issues:

31 st Voorburg Group Meeting Zagreb, Croatia 19 23 September 2016 Cross cutting issues: Time based pricing methods Dorothee Blang Destatis Kat Pegler ONS Gert Jan van Steeg CBS 1 P age 1. Introduction

31 st Voorburg Group Meeting Zagreb, Croatia 19 23 September 2016 Cross cutting issues: Time based pricing methods Dorothee Blang Destatis Kat Pegler ONS Gert Jan van Steeg CBS 1 P age 1. Introduction

Session 4: Extrapolation, modelling, econometric and sampling techniques used in preparation of rapid estimates Discussant: Geert Bruinooge

SEMINAR ON TIMELINESS, METHODOLOGY AND COMPARABILITY OF RAPID ESTIMATES OF ECONOMIC TRENDS Session 4: Extrapolation, modelling, econometric and sampling techniques used in preparation of rapid estimates

SEMINAR ON TIMELINESS, METHODOLOGY AND COMPARABILITY OF RAPID ESTIMATES OF ECONOMIC TRENDS Session 4: Extrapolation, modelling, econometric and sampling techniques used in preparation of rapid estimates

6) Items purchased for resale with a right of return must be presented separately from other inventories.

Items purchased for resale with a right of return must be presented separately from other inventories.") Chapter 8 Cost-based Inventories and Cost of Sales 1) Inventories are assets consisting of goods owned by the business and held for future sale or for use in the manufacture of goods for sale. Answer:

Chapter 8 Cost-based Inventories and Cost of Sales 1) Inventories are assets consisting of goods owned by the business and held for future sale or for use in the manufacture of goods for sale. Answer:

WORKING PARTY NO 1 HARMONISATION OF TURNOVER TAXES

EUROPEAN COMMISSION DIRECTORATE-GENERAL TAXATION AND CUSTOMS UNION Indirect Taxation and Tax administration VAT and other turnover taxes TAXUD/2131/07 rev 1 - EN Brussels, May 21, 2007 WORKING PARTY NO

EUROPEAN COMMISSION DIRECTORATE-GENERAL TAXATION AND CUSTOMS UNION Indirect Taxation and Tax administration VAT and other turnover taxes TAXUD/2131/07 rev 1 - EN Brussels, May 21, 2007 WORKING PARTY NO

IAS - 02 INVENTORIES

IAS - 02 INVENTORIES Objective To prescribe the accounting treatment for inventories. Scope All inventories except: (a) (b) Financial instruments (see IAS 32 Financial Instruments: Presentation and IFRS

IAS - 02 INVENTORIES Objective To prescribe the accounting treatment for inventories. Scope All inventories except: (a) (b) Financial instruments (see IAS 32 Financial Instruments: Presentation and IFRS

Note on Marketing Arithmetic and Related Marketing Terms

Harvard Business School 574-082 Rev. April 29, 1983 Note on Marketing Arithmetic and Related Marketing Terms This note is about several terms and basic calculations used in the analysis of marketing problems.

Harvard Business School 574-082 Rev. April 29, 1983 Note on Marketing Arithmetic and Related Marketing Terms This note is about several terms and basic calculations used in the analysis of marketing problems.

PROFESSOR S CLASS NOTES FOR UNIT 8 COB 241 Sections 13, 14, 15 Class on October 3, 2018

PROFESSOR S CLASS NOTES FOR UNIT 8 COB 241 Sections 13, 14, 15 Class on October 3, 2018 Acquisition Cost of Long-Term Assets A video accompanying Unit 6 introduced the concept of Acquisition Cost. To review:

PROFESSOR S CLASS NOTES FOR UNIT 8 COB 241 Sections 13, 14, 15 Class on October 3, 2018 Acquisition Cost of Long-Term Assets A video accompanying Unit 6 introduced the concept of Acquisition Cost. To review:

Managerial Accounting Prof. Dr. Varadraj Bapat School of Management Indian Institute of Technology, Bombay

Managerial Accounting Prof. Dr. Varadraj Bapat School of Management Indian Institute of Technology, Bombay Module - 9 Lecture - 20 Accounting for Costs Dear students, in our last session we have started

Managerial Accounting Prof. Dr. Varadraj Bapat School of Management Indian Institute of Technology, Bombay Module - 9 Lecture - 20 Accounting for Costs Dear students, in our last session we have started

Accounting for Merchandising Businesses

CHAPTER 3 Accounting for Merchandising Businesses LEARNING OBJECTIVES After you have mastered the material in this chapter, you will be able to: 1 Identify and explain the primary features of the perpetual

CHAPTER 3 Accounting for Merchandising Businesses LEARNING OBJECTIVES After you have mastered the material in this chapter, you will be able to: 1 Identify and explain the primary features of the perpetual

Valuation of inventories

Valuation of inventories The sale of inventory at a price greater than total cost is the primary source of income for manufacturing and retail businesses. Inventories are asset items held for sale in the

Valuation of inventories The sale of inventory at a price greater than total cost is the primary source of income for manufacturing and retail businesses. Inventories are asset items held for sale in the

Financial Accounting. John J. Wild. Sixth Edition. Copyright 2013 by The McGraw-Hill Companies, Inc. All rights reserved.

Financial Accounting John J. Wild Sixth Edition McGraw-Hill/Irwin Copyright 2013 by The McGraw-Hill Companies, Inc. All rights reserved. Chapter 04 Reporting and Analyzing Merchandising Operations Conceptual

Financial Accounting John J. Wild Sixth Edition McGraw-Hill/Irwin Copyright 2013 by The McGraw-Hill Companies, Inc. All rights reserved. Chapter 04 Reporting and Analyzing Merchandising Operations Conceptual

The Methodological guide for developing producer price indices for services, issues and challenges

The Methodological guide for developing producer price indices for services, issues and challenges Anne-Sophie Fraisse, OECD 1 INTRODUCTION 1. The objective of the paper is to present the main contributions

The Methodological guide for developing producer price indices for services, issues and challenges Anne-Sophie Fraisse, OECD 1 INTRODUCTION 1. The objective of the paper is to present the main contributions

In order to measure industry total factor productivity

The Challenge of Total Factor Productivity Measurement Erwin Diewert * Department of Economics University of British Columbia Vancouver, Canada In order to measure industry total factor productivity accurately,

The Challenge of Total Factor Productivity Measurement Erwin Diewert * Department of Economics University of British Columbia Vancouver, Canada In order to measure industry total factor productivity accurately,

The Management of Marketing Profit: An Investment Perspective

The Management of Marketing Profit: An Investment Perspective Draft of Chapter 1: A Philosophy of Competition and An Investment in Customer Value Ted Mitchell, May 1 2015 Learning Objectives for Chapter

The Management of Marketing Profit: An Investment Perspective Draft of Chapter 1: A Philosophy of Competition and An Investment in Customer Value Ted Mitchell, May 1 2015 Learning Objectives for Chapter

Mini-presentation on Turnover/Output for Office Administrative and Support Activities (ISIC 8210) in Poland

in Poland") 30 th Voorburg Group Meeting Sydney, Australia September 21 st to September 25 th, 2015 Mini-presentation on Turnover/Output for Office Administrative and Support Activities (ISIC 8210) in Poland Central

30 th Voorburg Group Meeting Sydney, Australia September 21 st to September 25 th, 2015 Mini-presentation on Turnover/Output for Office Administrative and Support Activities (ISIC 8210) in Poland Central

The Recording of Factoryless Goods Production in National and International Accounts

Twenty-Seventh Meeting of the IMF Committee on Balance of Payments Statistics Washington, D.C. October 27 29, 2014 BOPCOM 14/13 The Recording of Factoryless Goods Production in National and International

Twenty-Seventh Meeting of the IMF Committee on Balance of Payments Statistics Washington, D.C. October 27 29, 2014 BOPCOM 14/13 The Recording of Factoryless Goods Production in National and International

The Top 3 Must Do s for Every Business Owner

The Top 3 Must Do s for Every Business Owner Cash Flow, Sales & People Start here Small businesses - we salute you UK small and medium enterprises are the heroes of the private sector, generating an eye-popping

The Top 3 Must Do s for Every Business Owner Cash Flow, Sales & People Start here Small businesses - we salute you UK small and medium enterprises are the heroes of the private sector, generating an eye-popping

CHAPTER 1 INTRODUCTION

CHAPTER 1 INTRODUCTION Cost is a major factor in most decisions regarding construction, and cost estimates are prepared throughout the planning, design, and construction phases of a construction project,

CHAPTER 1 INTRODUCTION Cost is a major factor in most decisions regarding construction, and cost estimates are prepared throughout the planning, design, and construction phases of a construction project,

Improving Business Services Price Indexes in Canada

Improving Business Services Price Indexes in Canada INTRODUCTION Statistics Canada 1 May, 2004 1. As in most developed economies, services have become increasingly important to the Canadian economy relative

Improving Business Services Price Indexes in Canada INTRODUCTION Statistics Canada 1 May, 2004 1. As in most developed economies, services have become increasingly important to the Canadian economy relative

18 th Meeting of the Voorburg Group on Service Statistics. The development of a PPI for Post and Courier Services in Austria

18 th Meeting of the Voorburg Group on Service Statistics Tokyo, Japan 6 10 th October 2003 SESSION 2: Mini presentation on producer price indices The development of a PPI for Post and Courier Services

18 th Meeting of the Voorburg Group on Service Statistics Tokyo, Japan 6 10 th October 2003 SESSION 2: Mini presentation on producer price indices The development of a PPI for Post and Courier Services

Financial Accounting Chapter 6 Notes Inventories

Financial Accounting Notes Inventories I. Management Issues Associated with Accounting with Inventory. Defining Inventory: 1. Assets held for resale purpose in a normal course of business. (Current Asset)

Financial Accounting Notes Inventories I. Management Issues Associated with Accounting with Inventory. Defining Inventory: 1. Assets held for resale purpose in a normal course of business. (Current Asset)

NRV vs. FV NRV is entity-specific value; FV is not. NRV for inventories may not equal FV-CTS.

IAS 2 DEFINITIONS NRV FV are assets: (a) held for sale in the ordinary course of business (finished goods); (b) in the process of production for such sale (WIP); or (c) in the form of materials or supplies

IAS 2 DEFINITIONS NRV FV are assets: (a) held for sale in the ordinary course of business (finished goods); (b) in the process of production for such sale (WIP); or (c) in the form of materials or supplies

FFQA 1. Complied by: Mohammad Faizan Farooq Qadri Attari ACCA (Finalist) Contact:

Contact:") FFQA 1 Objective of IAS 2 The objective of IAS 2 is to prescribe the accounting treatment for inventories. It provides guidance for determining the cost of inventories and for subsequently recognising

FFQA 1 Objective of IAS 2 The objective of IAS 2 is to prescribe the accounting treatment for inventories. It provides guidance for determining the cost of inventories and for subsequently recognising

BUY ASSETS INVENTORY BUSINESSES

HOW WE BUY ASSETS INVENTORY BUSINESSES AND EXCESS FROM WE WOULD LIKE TO PURCHASE YOUR ASSETS AND COMPLETE PRODUCT INVENTORY AND PAY YOU IN 24 HOURS. Dear friend, We are interested in purchasing your complete

HOW WE BUY ASSETS INVENTORY BUSINESSES AND EXCESS FROM WE WOULD LIKE TO PURCHASE YOUR ASSETS AND COMPLETE PRODUCT INVENTORY AND PAY YOU IN 24 HOURS. Dear friend, We are interested in purchasing your complete

2 Measuring output of the service industries to constant price

National accounts general methodology - addressing cross-cutting issues arising when measuring the constant price output of Service Industries Paper prepared for the 23 rd Voorburg Group, Agusaclientes,

National accounts general methodology - addressing cross-cutting issues arising when measuring the constant price output of Service Industries Paper prepared for the 23 rd Voorburg Group, Agusaclientes,

Course Report Level National 5

Course Report 2018 Subject Accounting Level National 5 This report provides information on the performance of candidates. Teachers, lecturers and assessors may find it useful when preparing candidates

Course Report 2018 Subject Accounting Level National 5 This report provides information on the performance of candidates. Teachers, lecturers and assessors may find it useful when preparing candidates

Chapter 5: Merchandising Operations and the Multiple-Step Income Statement

Vocabulary Quiz 1. A detailed inventory system in which the cost of each inventory item is maintained and the records continuously show the inventory that should be on hand. 2. A reduction given by a seller

Vocabulary Quiz 1. A detailed inventory system in which the cost of each inventory item is maintained and the records continuously show the inventory that should be on hand. 2. A reduction given by a seller

Resolution concerning an integrated system of wages statistics, adopted by the Twelfth International Conference of Labour Statisticians (October 1973)

") Resolution concerning an integrated system of wages statistics, adopted by the Twelfth International Conference of Labour Statisticians (October 1973) The Twelfth International Conference of Labour Statisticians,......

Resolution concerning an integrated system of wages statistics, adopted by the Twelfth International Conference of Labour Statisticians (October 1973) The Twelfth International Conference of Labour Statisticians,......

CHAPTER 8. Valuation of Inventories: A Cost-Basis Approach 1, 2, 3, 4, 5, 6, 7, 8, 11, 12, 14, 15, 16

CHAPTER 8 Valuation of Inventories: A Cost-Basis Approach ASSIGNMENT CLASSIFICATION TABLE (BY TOPIC) Topics Questions Brief Exercises Exercises Problems Concepts for Analysis 1. Inventory accounts; determining

CHAPTER 8 Valuation of Inventories: A Cost-Basis Approach ASSIGNMENT CLASSIFICATION TABLE (BY TOPIC) Topics Questions Brief Exercises Exercises Problems Concepts for Analysis 1. Inventory accounts; determining

A Guide to Costing and Pricing a Product or Service

A Guide to Costing and Pricing a Product or Service Business Information Factsheet BIF054 December 2016 Introduction Setting the right price for a new product or service can be one of the hardest tasks

A Guide to Costing and Pricing a Product or Service Business Information Factsheet BIF054 December 2016 Introduction Setting the right price for a new product or service can be one of the hardest tasks

COST COST OBJECT. Cost centre. Profit centre. Investment centre

COST The amount of money or property paid for a good or service. Cost is an expense for both personal and business assets. If a cost is for a business expense, it may be tax deductible. A cost may be paid

COST The amount of money or property paid for a good or service. Cost is an expense for both personal and business assets. If a cost is for a business expense, it may be tax deductible. A cost may be paid

Price and volume measures in national accounts - Resources

Price and volume measures in national accounts - Resources by A. Faramondi, S. Pisani 16-20 march 2014 CATEGORY (1) and output for own final use Output for own final use is to be valued at the basic prices

Price and volume measures in national accounts - Resources by A. Faramondi, S. Pisani 16-20 march 2014 CATEGORY (1) and output for own final use Output for own final use is to be valued at the basic prices

Customers and Sales Part I

QuickBooks Online Student Guide Chapter 3 Customers and Sales Part I Chapter 2 Chapter 3 Lesson Objectives In this chapter, you ll learn the steps necessary to set up customers, and enter sales in QuickBooks

QuickBooks Online Student Guide Chapter 3 Customers and Sales Part I Chapter 2 Chapter 3 Lesson Objectives In this chapter, you ll learn the steps necessary to set up customers, and enter sales in QuickBooks

CHAPTER 2 INTRODUCTION TO COST BEHAVIOR AND COST-VOLUME RELATIONSHIPS

CHAPTER 2 INTRODUCTION TO COST BEHAVIOR AND COST-VOLUME RELATIONSHIPS LEARNING OBJECTIVES: 1. Explain how cost drivers affect cost behavior. 2. Show how changes in cost-driver activity levels affect variable

CHAPTER 2 INTRODUCTION TO COST BEHAVIOR AND COST-VOLUME RELATIONSHIPS LEARNING OBJECTIVES: 1. Explain how cost drivers affect cost behavior. 2. Show how changes in cost-driver activity levels affect variable

Full file at

CHAPTER 2 INTRODUCTION TO COST BEHAVIOR AND COST-VOLUME RELATIONSHIPS LEARNING OBJECTIVES: 1. Explain how cost drivers affect cost behavior. 2. Show how changes in cost-driver activity levels affect variable

CHAPTER 2 INTRODUCTION TO COST BEHAVIOR AND COST-VOLUME RELATIONSHIPS LEARNING OBJECTIVES: 1. Explain how cost drivers affect cost behavior. 2. Show how changes in cost-driver activity levels affect variable

Programming and Broadcasting Activities: Sector Paper Presentation

Programming and Broadcasting Activities: Sector Paper Presentation 29 th Voorburg Group Meeting Dublin, Ireland Written by Hina Kikegawa, Bank of Japan Presented by Kat Pegler, ONS Overview Introduction

Programming and Broadcasting Activities: Sector Paper Presentation 29 th Voorburg Group Meeting Dublin, Ireland Written by Hina Kikegawa, Bank of Japan Presented by Kat Pegler, ONS Overview Introduction

Accounting for Merchandising Operations

5-1 Chapter 5 Accounting for Merchandising Operations Learning Objectives After studying this chapter, you should be able to: 1. Identify the differences between service and merchandising companies. 2.

5-1 Chapter 5 Accounting for Merchandising Operations Learning Objectives After studying this chapter, you should be able to: 1. Identify the differences between service and merchandising companies. 2.

Annual GDP by production approach in current and constant prices: main issues 1

Annual GDP by production approach in current and constant prices: main issues 1 Introduction This paper continues the series dedicated to extending the contents of the Handbook Essential SNA: Building

Annual GDP by production approach in current and constant prices: main issues 1 Introduction This paper continues the series dedicated to extending the contents of the Handbook Essential SNA: Building

Accounting for the Value of Inventories

2 Accounting for the Value of Inventories Accounting for the Value of Inventories 2 LEARNING OUTCOMES After completing this chapter, you should be able to: distinguish between the historical cost of an

2 Accounting for the Value of Inventories Accounting for the Value of Inventories 2 LEARNING OUTCOMES After completing this chapter, you should be able to: distinguish between the historical cost of an

Ebusiness: A Canadian Perspective for a Networked World, 4e Chapter 2 Internet Business Models and Strategies

1) Which of the following would be appropriate when defining a business model? A) the manner in which a business organizes itself so as to achieve its objectives B) traditional business models have usually

1) Which of the following would be appropriate when defining a business model? A) the manner in which a business organizes itself so as to achieve its objectives B) traditional business models have usually

Bringing the Power of OneStep Automation to Your Business

Bringing the Power of OneStep Automation to Your Business Are You in Control of Your Business? Business Control Systems Corp. Distribution Retail The Problem: Today, running a successful business is complicated.

Bringing the Power of OneStep Automation to Your Business Are You in Control of Your Business? Business Control Systems Corp. Distribution Retail The Problem: Today, running a successful business is complicated.

Accounting 1 Instructor Notes

Accounting 1 Instructor Notes CHAPTER 6 ACCOUNTING FOR MERCHANDISING BUSINESS Accounting for a merchandising business is much more complex than a service business. This is because a service business sells

Accounting 1 Instructor Notes CHAPTER 6 ACCOUNTING FOR MERCHANDISING BUSINESS Accounting for a merchandising business is much more complex than a service business. This is because a service business sells

10th Meeting of the Advisory Expert Group on National Accounts, April 2016, Paris, France

SNA/M1.16/4 10th Meeting of the Advisory Expert Group on National Accounts, 13-15 April 2016, Paris, France Agenda item: 4 The Internet economy Introduction This paper presents the challenges which the

SNA/M1.16/4 10th Meeting of the Advisory Expert Group on National Accounts, 13-15 April 2016, Paris, France Agenda item: 4 The Internet economy Introduction This paper presents the challenges which the

Economic and Social Council

United Nations E/CN.3/2018/28 Economic and Social Council Distr.: General 20 December 2017 Original: English Statistical Commission Forty-ninth session 6-9 March 2018 Item 4 (h) of the provisional agenda*

United Nations E/CN.3/2018/28 Economic and Social Council Distr.: General 20 December 2017 Original: English Statistical Commission Forty-ninth session 6-9 March 2018 Item 4 (h) of the provisional agenda*

National Accounts Framework in the ICP

Public Disclosure Authorized Public Disclosure Authorized Public Disclosure Authorized Public Disclosure Authorized International Comparison Program National Accounts Framework in the ICP Global Office

Public Disclosure Authorized Public Disclosure Authorized Public Disclosure Authorized Public Disclosure Authorized International Comparison Program National Accounts Framework in the ICP Global Office

JUNIOR CERT BUSINESS PAPER 2. DOCUMENTS (Higher)

") JUNIOR CERT BUSINESS PAPER 2 DOCUMENTS (Higher) 1 DEFINITE QUESTION EVERY YEAR! USUALLY QUESTION 2! Short questions with Documents 2012 Mark-Up Delivery Docket Processing Delivery Dockets Credit Note Sales

JUNIOR CERT BUSINESS PAPER 2 DOCUMENTS (Higher) 1 DEFINITE QUESTION EVERY YEAR! USUALLY QUESTION 2! Short questions with Documents 2012 Mark-Up Delivery Docket Processing Delivery Dockets Credit Note Sales

Get a clearer view of your business

Get a clearer view of your business Essential Tips for Every Business Owner START HERE Small businesses - we salute you Canada s small and medium businesses account for 95% of all net job creation.¹ That

Get a clearer view of your business Essential Tips for Every Business Owner START HERE Small businesses - we salute you Canada s small and medium businesses account for 95% of all net job creation.¹ That

Accounting for Merchandising Operations

5-1 Chapter 5 Accounting for Merchandising Operations Learning Objectives After studying this chapter, you should be able to: 1. Identify the differences between service and merchandising companies. 2.

5-1 Chapter 5 Accounting for Merchandising Operations Learning Objectives After studying this chapter, you should be able to: 1. Identify the differences between service and merchandising companies. 2.

Balance of Payments Classification of Services Progress and Unresolved Issues. Note by OECD Statistics Directorate

ESA/STAT/AC.103/20 21 June 2005 UNITED NATIONS DEPARTMENT OF ECONOMIC AND SOCIAL AFFAIRS STATISTICS DIVISION Meeting of the Expert Group on International Economic and Social Classifications New York, 20-24

ESA/STAT/AC.103/20 21 June 2005 UNITED NATIONS DEPARTMENT OF ECONOMIC AND SOCIAL AFFAIRS STATISTICS DIVISION Meeting of the Expert Group on International Economic and Social Classifications New York, 20-24

Impact on BOP Data of Changes in International Standards for Processing and Merchanting

BOPCOM-08/11 Twenty-First Meeting of the IMF Committee on Balance of Payments Statistics Washington, D.C., November 4 7, 2008 Impact on BOP Data of Changes in International Standards for Processing and

BOPCOM-08/11 Twenty-First Meeting of the IMF Committee on Balance of Payments Statistics Washington, D.C., November 4 7, 2008 Impact on BOP Data of Changes in International Standards for Processing and

IBM Renewal Value Incentive

IBM Renewal Value Incentive Operations Guide June 14, 2013 Version 2.0 This guide and updated versions will be posted on the IBM PartnerWorld website. Please check the PartnerWorld website: www.ibm.com/partnerworld/renewalvalueincentive

IBM Renewal Value Incentive Operations Guide June 14, 2013 Version 2.0 This guide and updated versions will be posted on the IBM PartnerWorld website. Please check the PartnerWorld website: www.ibm.com/partnerworld/renewalvalueincentive

CHAPTER 8: INVENTORY

CHAPTER 8: INVENTORY Inventory Categories Merchandise inventory - ready for sale units that are unsold at the end of the fiscal period raw materials inventory - costs assigned to goods and materials on

CHAPTER 8: INVENTORY Inventory Categories Merchandise inventory - ready for sale units that are unsold at the end of the fiscal period raw materials inventory - costs assigned to goods and materials on

Inventories. IAS Standard 2 IAS 2. IFRS Foundation

IAS Standard 2 Inventories In April 2001 the International Accounting Standards Board (the Board) adopted IAS 2 Inventories, which had originally been issued by the International Accounting Standards Committee

IAS Standard 2 Inventories In April 2001 the International Accounting Standards Board (the Board) adopted IAS 2 Inventories, which had originally been issued by the International Accounting Standards Committee

Bidding & Estimating Course Syllabus

Bidding & Estimating Course Syllabus 2 Hours (Interactive) Introduction & Overview to Bidding & Estimating Review Sundt/Walsh Abstracting Process Estimating Templates Introduction to Estimating Bid Documents

Bidding & Estimating Course Syllabus 2 Hours (Interactive) Introduction & Overview to Bidding & Estimating Review Sundt/Walsh Abstracting Process Estimating Templates Introduction to Estimating Bid Documents

Financial Transfer Guide DBA Software Inc.

Contents 3 Table of Contents 1 Introduction 4 2 Why You Need the Financial Transfer 6 3 Total Control Workflow 10 4 Financial Transfer Overview 12 5 Multiple Operating Entities Setup 15 6 General Ledger

Contents 3 Table of Contents 1 Introduction 4 2 Why You Need the Financial Transfer 6 3 Total Control Workflow 10 4 Financial Transfer Overview 12 5 Multiple Operating Entities Setup 15 6 General Ledger

Ella s Game Emporium Accounting for Imports Expressions in Industry Assignment 2

Name(s): Period: Date: Ella s Game Emporium Accounting for Imports Expressions in Industry Assignment 2 An SB1070 Project Objectives By the end of the day students should be able to write a multivariable

Name(s): Period: Date: Ella s Game Emporium Accounting for Imports Expressions in Industry Assignment 2 An SB1070 Project Objectives By the end of the day students should be able to write a multivariable

BUILDING ENTERPRISE BUDGETS FOR INDIANA SPECIALTY CROP GROWERS

BUILDING ENTERPRISE BUDGETS FOR INDIANA SPECIALTY CROP GROWERS Andres Gallegos and Ariana Torres Financial tools can help farmers improve farm s performance and assure profitability. Enterprise budgets,

BUILDING ENTERPRISE BUDGETS FOR INDIANA SPECIALTY CROP GROWERS Andres Gallegos and Ariana Torres Financial tools can help farmers improve farm s performance and assure profitability. Enterprise budgets,

Lesson IV: Economic Flows and Stocks

Lesson IV: Economic Flows and Stocks An Introduction to System of National Accounts - Basic Concepts Sixth e-learning Course on the 2008 System of National Accounts September November 2014 1 Content Definition

Lesson IV: Economic Flows and Stocks An Introduction to System of National Accounts - Basic Concepts Sixth e-learning Course on the 2008 System of National Accounts September November 2014 1 Content Definition

Accounting 101 Class Notes Chapter 4 Accounting for Merchandising Operations

I. WHAT IS A MERCHANDISER? Merchandiser vs. Service Business Wholesaler vs. retailer This chapter changes the focus from a service-oriented business to a merchandising form of business. Merchandisers buy

I. WHAT IS A MERCHANDISER? Merchandiser vs. Service Business Wholesaler vs. retailer This chapter changes the focus from a service-oriented business to a merchandising form of business. Merchandisers buy

20th International Conference of Labour Statisticians resolution concerning statistics on work relationships

INTERNATIONAL LABOUR ORGANIZATION Meeting of Experts on Labour Statistics in Preparation for the 20th International Conference of Labour Statisticians MEPICLS/2018 Geneva 5 9 February 2018 Revised draft

INTERNATIONAL LABOUR ORGANIZATION Meeting of Experts on Labour Statistics in Preparation for the 20th International Conference of Labour Statisticians MEPICLS/2018 Geneva 5 9 February 2018 Revised draft

Practice Finances New Concepts for Old Problems Guest Speaker: John Tait, BSc, MS (Fin.) DVM, MBA, CFP

DVM, MBA, CFP") VHMA 2013 Annual Meeting and Conference September 26-29, 2013 The Westin, Charlotte, NC Practice Finances New Concepts for Old Problems Guest Speaker: John Tait, BSc, MS (Fin.) DVM, MBA, CFP Inventory

VHMA 2013 Annual Meeting and Conference September 26-29, 2013 The Westin, Charlotte, NC Practice Finances New Concepts for Old Problems Guest Speaker: John Tait, BSc, MS (Fin.) DVM, MBA, CFP Inventory

Module One: Review and Assessment of Economic Census Tools. Session 1.3: Fundamental Principles of Questionnaire Design Economic Census / Surveys

Module One: Review and Assessment of Economic Census Tools Session 1.3: Fundamental Principles of Questionnaire Design Economic Census / Surveys Aloke Kar Indian Statistical Institute Regional Course on

Module One: Review and Assessment of Economic Census Tools Session 1.3: Fundamental Principles of Questionnaire Design Economic Census / Surveys Aloke Kar Indian Statistical Institute Regional Course on

Mr Sydney Armstrong ECN 1100 Introduction to Microeconomics Lecture Note (6) The costs of Production Economic Costs

The costs of Production Economic Costs") Mr Sydney Armstrong ECN 1100 Introduction to Microeconomics Lecture Note (6) The costs of Production Economic Costs Costs exist because resources are scarce, productive and have alternative uses. When

Mr Sydney Armstrong ECN 1100 Introduction to Microeconomics Lecture Note (6) The costs of Production Economic Costs Costs exist because resources are scarce, productive and have alternative uses. When

Business planning a guide

Business planning a guide prepared by David Irwin for the Esmee Fairbairn Foundation March 2006 Esmee Fairbairn Foundation 11 Park Place, London SW1A 1LP www.esmeefairbairn.org.uk What this guide aims

Business planning a guide prepared by David Irwin for the Esmee Fairbairn Foundation March 2006 Esmee Fairbairn Foundation 11 Park Place, London SW1A 1LP www.esmeefairbairn.org.uk What this guide aims

There are two fools in every market. One charges too little; the other charges too much Russian proverb

There are two fools in every market. One charges too little; the other charges too much Russian proverb WHAT IS PRICE? Price is the amount of money charged for product or service, or the sum of all the

There are two fools in every market. One charges too little; the other charges too much Russian proverb WHAT IS PRICE? Price is the amount of money charged for product or service, or the sum of all the

Pay People Properly. QCommission Integration with QuickBooks. Overview

QCommission Integration with QuickBooks Pay People Properly Overview Sales commission programs are possibly the most variable programs conducted by a firm. These programs tend to vary significantly from

QCommission Integration with QuickBooks Pay People Properly Overview Sales commission programs are possibly the most variable programs conducted by a firm. These programs tend to vary significantly from

Manage Pricing Decisions

10 Manage Pricing Decisions Chapter Questions How do consumers process and evaluate prices? How should a company set prices initially for products or services? How should a company adapt prices to meet

10 Manage Pricing Decisions Chapter Questions How do consumers process and evaluate prices? How should a company set prices initially for products or services? How should a company adapt prices to meet

REVISION: MANUFACTURING 12 SEPTEMBER 2013

REVISION: MANUFACTURING 12 SEPTEMBER 2013 Lesson Description In this lesson we: Revise ledger accounts and the production cost statement Key Concepts Ledger Accounts for Manufacturing Differences between

REVISION: MANUFACTURING 12 SEPTEMBER 2013 Lesson Description In this lesson we: Revise ledger accounts and the production cost statement Key Concepts Ledger Accounts for Manufacturing Differences between

Sri Lanka Accounting Standard LKAS 2. Inventories

Sri Lanka Accounting Standard LKAS 2 Inventories CONTENTS paragraphs SRI LANKA ACCOUNTING STANDARD LKAS 2 INVENTORIES OBJECTIVE 1 SCOPE 2 5 DEFINITIONS 6 8 MEASUREMENT OF INVENTORIES 9 33 Cost of inventories

Sri Lanka Accounting Standard LKAS 2 Inventories CONTENTS paragraphs SRI LANKA ACCOUNTING STANDARD LKAS 2 INVENTORIES OBJECTIVE 1 SCOPE 2 5 DEFINITIONS 6 8 MEASUREMENT OF INVENTORIES 9 33 Cost of inventories

Section I (20 questions; 1 mark each)

") Foundation Course in Managerial Economics- Solution Set- 1 Final Examination Marks- 100 Section I (20 questions; 1 mark each) 1. Which of the following statements is not true? a. Societies face an important

Foundation Course in Managerial Economics- Solution Set- 1 Final Examination Marks- 100 Section I (20 questions; 1 mark each) 1. Which of the following statements is not true? a. Societies face an important

Customer Lifetime Value

Customer Lifetime Value Opportunities and Challenges Greg Firestone Mohamad Hindawi, PhD, FCAS March, 2013 Antitrust Notice The Casualty Actuarial Society is committed to adhering strictly to the letter

Customer Lifetime Value Opportunities and Challenges Greg Firestone Mohamad Hindawi, PhD, FCAS March, 2013 Antitrust Notice The Casualty Actuarial Society is committed to adhering strictly to the letter

Test Bank For Cost Accounting A Managerial Emphasis Fifth Canadian 5th Edition By Horngren Foster Datar And Gowing

Test Bank For Cost Accounting A Managerial Emphasis Fifth Canadian 5th Edition By Horngren Foster Datar And Gowing Link full download: https://digitalcontentmarket.org/download/test-bank-for-cost-accounting-amanagerial-emphasis-fifth-canadian-5th-edition-by-horngren-foster-datar-andgowing/

Test Bank For Cost Accounting A Managerial Emphasis Fifth Canadian 5th Edition By Horngren Foster Datar And Gowing Link full download: https://digitalcontentmarket.org/download/test-bank-for-cost-accounting-amanagerial-emphasis-fifth-canadian-5th-edition-by-horngren-foster-datar-andgowing/

Turnover/Output for Specialized Design Activities in Canada

Turnover/Output for Specialized Design Activities in Canada 29th Voorburg Group Meeting Fred Barzyk Dublin, Ireland September 22 nd to 26 th, 2014 Definition of the service (1) By industry - NAICS 2012

Turnover/Output for Specialized Design Activities in Canada 29th Voorburg Group Meeting Fred Barzyk Dublin, Ireland September 22 nd to 26 th, 2014 Definition of the service (1) By industry - NAICS 2012

The Examiner's Answers Specimen Paper. Performance Management

The Examiner's Answers Specimen Paper P2 - SECTION A Answer to Question One The Value Chain is the concept that there is a sequence of business factors by which value is added to an organisation s products

The Examiner's Answers Specimen Paper P2 - SECTION A Answer to Question One The Value Chain is the concept that there is a sequence of business factors by which value is added to an organisation s products

Contents ADJUSTING THE ACCOUNTS. Analyze Accounts and Prepare Adjusting Entries 43. Learning Goal 4: Explain the Meaning of Accounting Period 7

Contents Review The Essential Accounts for a Corporation 1 The Accounts For a Corporation 1 Equity Accounts 1 Corporate Financial Statements: Quick Review 2 SECTION I Goal 1: ADJUSTING THE ACCOUNTS Explain

Contents Review The Essential Accounts for a Corporation 1 The Accounts For a Corporation 1 Equity Accounts 1 Corporate Financial Statements: Quick Review 2 SECTION I Goal 1: ADJUSTING THE ACCOUNTS Explain

Whitepaper on PJM Forward Energy Reserve. A Centralized Call Option Market Proposal

Whitepaper on PJM Forward Energy Reserve A Centralized Call Option Market Proposal Jeff Bladen Manager, Retail Markets January 26, 2005 Docs #304175v1 2005 PJM Interconnection Table of Contents Forward

Whitepaper on PJM Forward Energy Reserve A Centralized Call Option Market Proposal Jeff Bladen Manager, Retail Markets January 26, 2005 Docs #304175v1 2005 PJM Interconnection Table of Contents Forward

Inventory and Cost of Goods Sold C AT EDRÁTICO U PR R I O P I EDRAS S EG. S EM

Inventory and Cost of Goods Sold E DWIN R ENÁN MALDONADO C AT EDRÁTICO U PR R I O P I EDRAS S EG. S EM. 2 017-18 Textbook: Financial Accounting, Spiceland This presentation contains information, in addition

Inventory and Cost of Goods Sold E DWIN R ENÁN MALDONADO C AT EDRÁTICO U PR R I O P I EDRAS S EG. S EM. 2 017-18 Textbook: Financial Accounting, Spiceland This presentation contains information, in addition

Mona Loa Malaysian Manufacturing cost per bag... $6.00 $5.00 Add markup at 30% Selling price per bag... $7.80 $6.50

Case 8-24 1. a. The predetermined overhead rate would be computed as follows: Expected manufacturing overhead cost $3,000,000 = Estimated direct labour-hours 50,000 DLHs =$60 per DLH b. The unit product

Case 8-24 1. a. The predetermined overhead rate would be computed as follows: Expected manufacturing overhead cost $3,000,000 = Estimated direct labour-hours 50,000 DLHs =$60 per DLH b. The unit product

Laws and Regulations. Valuation. Assists

Laws and Regulations When importing merchandise from foreign countries there are certain trade laws and regulations. U.S. Customs oversees the compliance of those laws. Our International Department is

Laws and Regulations When importing merchandise from foreign countries there are certain trade laws and regulations. U.S. Customs oversees the compliance of those laws. Our International Department is

Sage Partner Additional Modules

PHONE +27 [0]21 552 6052 FAX +27 [0]86 266 4620 EMAIL info@as2.co.za WEB www.as2.co.za Sage Partner Additional Modules 1. Bill of Materials 2. Debtors Manager 3. Fixed Assets 4. Multi-Warehousing 5. Point

PHONE +27 [0]21 552 6052 FAX +27 [0]86 266 4620 EMAIL info@as2.co.za WEB www.as2.co.za Sage Partner Additional Modules 1. Bill of Materials 2. Debtors Manager 3. Fixed Assets 4. Multi-Warehousing 5. Point

Chapter 2 Product Costing Concepts and Systems

Chapter 2 Product Costing Concepts and Systems LO 1: Understand and apply the concepts of cost, opportunity cost, committed cost, fixed cost, variable cost and sunk cost. Opportunity cost: The highest

Chapter 2 Product Costing Concepts and Systems LO 1: Understand and apply the concepts of cost, opportunity cost, committed cost, fixed cost, variable cost and sunk cost. Opportunity cost: The highest

presents: your guide to forecasting

presents: your guide to forecasting what can forecasting do for me? Having a robust forecast can be an invaluable tool in managing your business finances. If done thoroughly it can show where deficits

presents: your guide to forecasting what can forecasting do for me? Having a robust forecast can be an invaluable tool in managing your business finances. If done thoroughly it can show where deficits