The State of Open Banking in the UK. APIdays London, 11th October 2016

|

|

|

- Kelley Todd

- 6 years ago

- Views:

Transcription

1 The State of Open Banking in the UK APIdays London, 11th October 2016

2 Background: UK Banking Market Highly concentrated - Top 5 banking groups control 85% of the market Poor competition - 57% of customers >10 years - 37% of customers >20 years - 3% of customers switched in 2014 Co-op 2% Nationwide 6% TSB 4.2% Other 2.8% HSBC 12% Barriers to Entry - Regulatory requirements - Incumbents ownership of payment schemes Competition = Innovation RBS 18% Santander 10% Barclays 18% Lloyds 27%

3 No Competition = No Innovation - No banking APIs for retail or SME customers UK FinTech leadership under threat - Germany: HBCI / FinTS fosters a FinTech sector - US: Greater competition amongst banks fosters innovation No Competition = No investment in technology

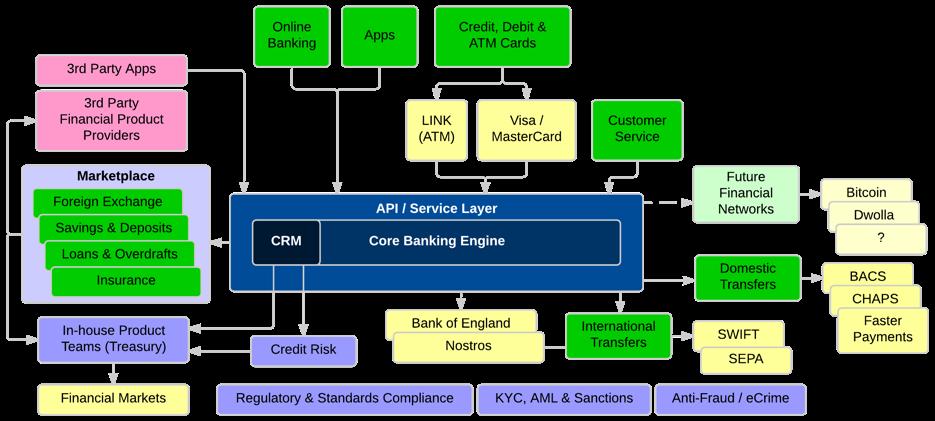

4 The next-generation bank will be powered by APIs

5 September 2014: Fingleton Report Data Sharing and Open Data for Banks Key Recommendations: 1. Banks agree on an open API standard for third party access. 2. Independent guidance provided on technology, security and data protection standards that banks can adopt to ensure data sharing meets all legal requirements. 3. Industry wide approach established to vet third party applications and publish a list of vetted applications as open data. 4. Standard data on PCA terms and conditions published by banks as open data. 5. Credit data made available as open data.

6 March 2015: Support for FinTech, RegTech and APIs announced in the Budget

7 September 2015: Open Banking Working Group convened Tasked with designing a detailed framework to enable the development of an open API standard in UK banking Over 100 people from banks, fintechs, industry bodies, schemes, Open Bank Project Multiple sub-groups looking at different facets: - User reference group - Governance - Data - Security & Authentication - Standards & Technical Design - Regulation & Legal

8 Open Banking Working Group Key Areas of Focus Liability - Who pays if fraud is perpetrated through a third party? Governance - How can banks concerns and duty to protect their customers interests be balanced against the need to foster innovation and competition? Security - How to ensure that third parties will adequately protect customers data and access to their accounts? Data Protection - If your name appears on my bank statement because I sent you a payment, am I allowed to share that with a third party?

9 November 2015: PSD2 Payment Initiation Service - a service to initiate a payment order at the request of the payment service user with respect to a payment account held at another payment service provider Account Information Service - an online service to provide consolidated information on one or more payment accounts held by the payment service user with either another payment service provider or with more than one payment service provider Comes into effect 13 January 2018

10 February 2016: OBWG Report published Key Recommendations: Open Banking Standard to be overseen by an Independent Authority - Should act transparently and support wide participation Third parties to be vetted and whitelisted - Subject to security standards, insurance requirements OAuth-style authorisation of third parties access to customers data and accounts - Bank retains ability to shut down access if evidence of fraud is detected

and payment initiation service providers (PISPs) \"set up an entity")

11 August 2016: Competition & Markets Authority Retail Banking market investigation Requires that the nine largest banks in GB and NI: adopt and maintain common API standards through which they will share data with other providers and with third party service providers including PCWs, account information service providers (AISPs) and payment initiation service providers (PISPs) "set up an entity (the Implementation Entity) that will be tasked with agreeing, implementing and maintaining open and common banking standards

12 August 2016: Competition & Markets Authority Retail Banking market investigation appoint following approval of the CMA a suitably qualified, independent person (the Implementation Trustee) to act as chair of the Implementation Entity agree to be bound by the decisions of the Implementation Trustee agree with the IT open standards for APIs with full read and write functionality and make available through them PCA and BCA transaction data sets, to be released no later than the transposition deadline of the second Payment Services Directive (PSD2) ie by 13 January 2018.

13 Today Open Data Institute formed an Open Banking Development Group Banks have formed an Implementation Entity Steering Group within Payments UK Implementation Trustee to be appointed in coming weeks? Challenger banks (and Barclays!) forging ahead

14

15

16 Jack Gavigan

Work stream 3 Implementation Plan Industry Landscape

DRAFT Work stream 3 Implementation Plan Industry Landscape Payments Strategy Forum April 2017 Payments Industry Landscape NPA Implementation The purpose of this document is to provide a view of the change

DRAFT Work stream 3 Implementation Plan Industry Landscape Payments Strategy Forum April 2017 Payments Industry Landscape NPA Implementation The purpose of this document is to provide a view of the change

Technology Innovation Exchange 2017

1 2 3 Significant period of change in the next 9 months Between PSD2, OBWG and CMA alone, there is significant, directionally aligned, activity aimed at transforming the landscape. The timing and degree

1 2 3 Significant period of change in the next 9 months Between PSD2, OBWG and CMA alone, there is significant, directionally aligned, activity aimed at transforming the landscape. The timing and degree

What new roles could a bank adopt in this transformed environment? New products and services: what opportunities does open banking provide?

1 What new roles could a bank adopt in this transformed environment? 2 New products and services: what opportunities does open banking provide? 3 How can the relationship between the bank and customer

1 What new roles could a bank adopt in this transformed environment? 2 New products and services: what opportunities does open banking provide? 3 How can the relationship between the bank and customer

PAYMENT SERVICES DIRECTIVE 2 WHAT IS ALL THE FUSS ABOUT ANYWAY?

PAYMENT SERVICES DIRECTIVE 2 WHAT IS ALL THE FUSS ABOUT ANYWAY? An extract from the Scandinavian financial services newsletter Winter 2016 Newsletter 2 SCANDINAVIAN FINANCIAL SERVICES 2016 WINTER EDITION

PAYMENT SERVICES DIRECTIVE 2 WHAT IS ALL THE FUSS ABOUT ANYWAY? An extract from the Scandinavian financial services newsletter Winter 2016 Newsletter 2 SCANDINAVIAN FINANCIAL SERVICES 2016 WINTER EDITION

Turning PSD2 Challenges into Business Opportunities.

Turning PSD2 Challenges into Business Opportunities www.ebankit.com PSD2 in a nutshell Perfect Competition Payment Services Directive 2 (PSD2) The PSD2 updates and complements the EU rules put in place

Turning PSD2 Challenges into Business Opportunities www.ebankit.com PSD2 in a nutshell Perfect Competition Payment Services Directive 2 (PSD2) The PSD2 updates and complements the EU rules put in place

The revised Payment Services Directive (PSD2)

") Regulatory agenda updates The revised Payment Services Directive (PSD2) What you need to know Revised Payment Services Directive (PSD2) to increase scope, obligations, and to offer business opportunities

Regulatory agenda updates The revised Payment Services Directive (PSD2) What you need to know Revised Payment Services Directive (PSD2) to increase scope, obligations, and to offer business opportunities

The Future of Open Banking with the CMA

The Future of Open with the CMA Secretariat Innovate Finance Address: Level39 One Canada Square Canary Wharf, London United Kingdom E14 5AB Telephone: 020 3819 0179 Email: info@appgfintech.org.uk www.appgfintech.org.uk

The Future of Open with the CMA Secretariat Innovate Finance Address: Level39 One Canada Square Canary Wharf, London United Kingdom E14 5AB Telephone: 020 3819 0179 Email: info@appgfintech.org.uk www.appgfintech.org.uk

Review of Priviti PSD2 Use Case and its positioning compared to alternative marketplace offerings

Review of Priviti PSD2 Use Case and its positioning compared to alternative marketplace offerings The revised Payment Service Directive (PDS2) is a directive focused on better integration of an internal

Review of Priviti PSD2 Use Case and its positioning compared to alternative marketplace offerings The revised Payment Service Directive (PDS2) is a directive focused on better integration of an internal

The communication between Third Party Providers and Banks. PSD2 in a nutshell

www.pwc.ch The communication between Third Party Providers and Banks. What will the impact of technology be? PSD2 in a nutshell Summary The banking system is at a turning point, under the pressure of the

www.pwc.ch The communication between Third Party Providers and Banks. What will the impact of technology be? PSD2 in a nutshell Summary The banking system is at a turning point, under the pressure of the

Turning the Revised Payment Services Directive into Digital Opportunity

Turning the Revised Payment Services Directive into Digital Opportunity Contents 1. Introduction 3 2. The Business Risk PSD2 Presents 4 3. The Opportunity for Value Creation 6 4. Making it Happen 7 2 Turning

Turning the Revised Payment Services Directive into Digital Opportunity Contents 1. Introduction 3 2. The Business Risk PSD2 Presents 4 3. The Opportunity for Value Creation 6 4. Making it Happen 7 2 Turning

FinTechs as a catalyst for improving payment services

FinTechs as a catalyst for improving payment services Heike Winter, Retail Payment Policy, Deutsche Bundesbank Annual Global Conference of the European Banking Institute Frankfurt, 28 October 2016 Worldwide

FinTechs as a catalyst for improving payment services Heike Winter, Retail Payment Policy, Deutsche Bundesbank Annual Global Conference of the European Banking Institute Frankfurt, 28 October 2016 Worldwide

CURRENT ACCOUNT SWITCH SERVICE DASHBOARD Issue 16: Covering the period 1 July 2017 to 30 September 2017

CURRENT ACCOUNT SWITCH SERVICE DASHBOARD Issue 16: Covering the period 1 July 2017 to 30 September 2017 MARKET COMMENTARY September 2017 marked the Current Account Switch Service s (CASS) fourth anniversary,

CURRENT ACCOUNT SWITCH SERVICE DASHBOARD Issue 16: Covering the period 1 July 2017 to 30 September 2017 MARKET COMMENTARY September 2017 marked the Current Account Switch Service s (CASS) fourth anniversary,

UK Open Banking: the future belongs to the flexible

UK Open Banking: the future belongs to the flexible 2 The future belongs to the flexible 3 The future belongs to the flexible Tom Wood, Managing Director and UK Head of Global Liquidity and Cash Management,

UK Open Banking: the future belongs to the flexible 2 The future belongs to the flexible 3 The future belongs to the flexible Tom Wood, Managing Director and UK Head of Global Liquidity and Cash Management,

PSD2 & Open Banking The Future of Payments

PSD2 & Open Banking The Future of Payments A White Paper (abridged) by Brendan Jones Bryan Cave, a global firm, is uniquely well-positioned to serve fintech companies. We work closely with several fintech

PSD2 & Open Banking The Future of Payments A White Paper (abridged) by Brendan Jones Bryan Cave, a global firm, is uniquely well-positioned to serve fintech companies. We work closely with several fintech

Dirk Haubrich, Nilixa Devlukia. Public Hearing, EBA, London, 25 July 2018

Draft Guidelines on the conditions to be met to benefit from an exemption from contingency measures under Article 33(6) of Regulation (EU) 2018/389 (RTS on SCA & CSC under PSD2) Dirk Haubrich, Nilixa Devlukia

Draft Guidelines on the conditions to be met to benefit from an exemption from contingency measures under Article 33(6) of Regulation (EU) 2018/389 (RTS on SCA & CSC under PSD2) Dirk Haubrich, Nilixa Devlukia

Open banking. Potential pricing implications

Open banking Potential pricing implications March 2018 Information about a customer s financial position and transactions has been a key source of competitive advantage for established financial institutions.

Open banking Potential pricing implications March 2018 Information about a customer s financial position and transactions has been a key source of competitive advantage for established financial institutions.

Open banking. Potential pricing implications

Open banking Potential pricing implications March 2018 Information about a customer s financial position and transactions has been a key source of competitive advantage for established financial institutions.

Open banking Potential pricing implications March 2018 Information about a customer s financial position and transactions has been a key source of competitive advantage for established financial institutions.

PSD2 - Second Payment Services Directive. Information Set

PSD2 - Second Payment Services Directive Information Set PSD2: at the starting line February 2017 EBA published the final draft RTS on SCA November 2017 EC published the final RTS on SCA January 13 2018

PSD2 - Second Payment Services Directive Information Set PSD2: at the starting line February 2017 EBA published the final draft RTS on SCA November 2017 EC published the final RTS on SCA January 13 2018

Project Innovate. Anna Wallace, Head of Innovation Hub UK Financial Conduct Authority

Project Innovate Anna Wallace, Head of Innovation Hub UK Financial Conduct Authority 1 About the FCA Independent regulatory body. Consumer protection, financial system integrity and competition objectives.

Project Innovate Anna Wallace, Head of Innovation Hub UK Financial Conduct Authority 1 About the FCA Independent regulatory body. Consumer protection, financial system integrity and competition objectives.

Minutes of the meeting of the PAYMENT SERVICES STAKEHOLDER LIAISON GROUP

Minutes Minutes of the meeting of the PAYMENT SERVICES STAKEHOLDER LIAISON GROUP Held on 1 December 2016, 15.00 17.00 At Committee Room 02, FCA, 25 The North Colonnade, London Present: Graeme Mclean, FCA

Minutes Minutes of the meeting of the PAYMENT SERVICES STAKEHOLDER LIAISON GROUP Held on 1 December 2016, 15.00 17.00 At Committee Room 02, FCA, 25 The North Colonnade, London Present: Graeme Mclean, FCA

PSD2 DATA FINTECH MARKETPLACE AISP CUSTOMER AWARENESS ALLIANCES MOBILE ECONOMY PISP API DIGITAL COMPLY REVENUE RTS SCORING BANKING STRATEGIC

DISRUPTION FINTECH DATA OPEN STRATEGIC CORPORATE CHANGE BIGTECH PSD2 IMPACT INSTANT PAYMENTS RISK INTERNET INNOVATION REVENUE RTS ALLIANCES PISP SCA ECOSYSTEM AUTHENTICATION ANALYTICS MARKETPLACE MOBILE

DISRUPTION FINTECH DATA OPEN STRATEGIC CORPORATE CHANGE BIGTECH PSD2 IMPACT INSTANT PAYMENTS RISK INTERNET INNOVATION REVENUE RTS ALLIANCES PISP SCA ECOSYSTEM AUTHENTICATION ANALYTICS MARKETPLACE MOBILE

Unlocking the full business potential of PSD2

Unlocking the full business potential of PSD2 How to create value for customers following PSD2 regulation equensworldline Sibos 2017 Open Theater equensworldline Position in Worldline Group 2 equensworldline

Unlocking the full business potential of PSD2 How to create value for customers following PSD2 regulation equensworldline Sibos 2017 Open Theater equensworldline Position in Worldline Group 2 equensworldline

PSD2 open banking for Prepaid Programme Managers. Implications and Requirements

A RegTech Company PSD2 open banking for Prepaid Programme Managers Implications and Requirements White Paper September 2018 1 Regulatory challenge in the EU In January 2018 the European Union Payment Services

A RegTech Company PSD2 open banking for Prepaid Programme Managers Implications and Requirements White Paper September 2018 1 Regulatory challenge in the EU In January 2018 the European Union Payment Services

Challenges and solutions

Challenges and solutions related to the entry into force of the RTS SCA on the 14 September 2019 Introduction The PSD2 and the so-called open banking are two of the most frequently discussed topics in

Challenges and solutions related to the entry into force of the RTS SCA on the 14 September 2019 Introduction The PSD2 and the so-called open banking are two of the most frequently discussed topics in

MARKET REVIEW INTO THE OWNERSHIP AND COMPETITIVENESS OF INFRASTRUCTURE PROVISION PSR MR15/2.1

8 September 2015 infrastructurereview@psr.org.uk Direct Line 020 3217 8276 Stuart.Cole@chequeandcredit.co.uk Infrastructure Review Team Payment Systems Regulator (15th floor) 25 The North Colonnade Canary

8 September 2015 infrastructurereview@psr.org.uk Direct Line 020 3217 8276 Stuart.Cole@chequeandcredit.co.uk Infrastructure Review Team Payment Systems Regulator (15th floor) 25 The North Colonnade Canary

PSD2 TAS Open Banking

PSD2 A challenge for Banks but a huge opportunity at the same time for new services TAS Group 2017 Some highlights on PSD2 driven changes PSD2 introduces a new legal structure to payments in the EU, challenging

PSD2 A challenge for Banks but a huge opportunity at the same time for new services TAS Group 2017 Some highlights on PSD2 driven changes PSD2 introduces a new legal structure to payments in the EU, challenging

The communication between Third Party Providers and Banks. PSD2 in a nutshell

www.pwc.com/psd2 The communication between Third Party Providers and Banks. What will the impact of technology be? PSD2 in a nutshell Summary The banking system is at a turning point, under the pressure

www.pwc.com/psd2 The communication between Third Party Providers and Banks. What will the impact of technology be? PSD2 in a nutshell Summary The banking system is at a turning point, under the pressure

The Second Payment Services Directive: Scoping out the impacts of the Regulatory Technical Standards

The Second Payment Services Directive: Scoping out the impacts of the Regulatory Technical Standards TABLE OF CONTENTS INTRODUCTION: A CRITICAL MOMENT FOR PSD2 KEY ASPECTS OF THE FINAL DRAFT RTS IMPACTS

The Second Payment Services Directive: Scoping out the impacts of the Regulatory Technical Standards TABLE OF CONTENTS INTRODUCTION: A CRITICAL MOMENT FOR PSD2 KEY ASPECTS OF THE FINAL DRAFT RTS IMPACTS

Market environment and implementation timeline PSD2 in a nutshell

www.pwc.ch Market environment and implementation timeline PSD2 in a nutshell Why do we need a new Payment Services Directive (PSD)? By 13 th January 2018, Member States will have to implement the Directive

www.pwc.ch Market environment and implementation timeline PSD2 in a nutshell Why do we need a new Payment Services Directive (PSD)? By 13 th January 2018, Member States will have to implement the Directive

Trusted KYC Data Sharing Standards Scope and Governance Oversight

November 2017 Trusted KYC Data Sharing Standards Scope and Governance Oversight Handover Document Contents Preface... 3 Overview... 5 1 Sharing Capabilities and Interoperability... 7 1.1 Data Sharing Behaviour

November 2017 Trusted KYC Data Sharing Standards Scope and Governance Oversight Handover Document Contents Preface... 3 Overview... 5 1 Sharing Capabilities and Interoperability... 7 1.1 Data Sharing Behaviour

The Payments Strategy Forum Being responsive to user needs Draft strategy for consultation

Respondents basic details Consultation title: Name of respondent: Being responsive to user needs Draft strategy TSB Bank Plc Contact details/job title: Representing (self or organisation/s): Email: Address:

Respondents basic details Consultation title: Name of respondent: Being responsive to user needs Draft strategy TSB Bank Plc Contact details/job title: Representing (self or organisation/s): Email: Address:

DATE: 17/11/2017 Open Banking

DATE: 17/11/2017 Open Banking FAO CMA: Proposed amendments to the Agreed Arrangements Adam Land Senior Director of Remedies, Business and Financial Analysis Competition and Markets Authority Victoria House

DATE: 17/11/2017 Open Banking FAO CMA: Proposed amendments to the Agreed Arrangements Adam Land Senior Director of Remedies, Business and Financial Analysis Competition and Markets Authority Victoria House

40% of banks in CEE have not yet decided which strategy to pursue. Cautious optimism reigns

Staying relevant in a disruptive market. EU member states have until January 2018 to implement the revised EU Payment Services Directive 2. But many banks in Central and Eastern Europe are still hesitant

Staying relevant in a disruptive market. EU member states have until January 2018 to implement the revised EU Payment Services Directive 2. But many banks in Central and Eastern Europe are still hesitant

PSD2 is on top of our agenda

PSD2 is on top of our agenda Stating the obvious There is no do nothing option for payment service providers Even basic PSD2 compliance requires strategic choices There is a highway of opportunities The

PSD2 is on top of our agenda Stating the obvious There is no do nothing option for payment service providers Even basic PSD2 compliance requires strategic choices There is a highway of opportunities The

WHITE PAPER. REVENUE OPPORTUNITIES CREATED BY OPEN APIs. Venkataraman Durghados IBS Open APIs Solution Architect

REVENUE OPPORTUNITIES CREATED BY OPEN APIs Venkataraman Durghados IBS Open APIs Solution Architect Financial service providers must embrace new technologies and leverage data held in their systems to secure

REVENUE OPPORTUNITIES CREATED BY OPEN APIs Venkataraman Durghados IBS Open APIs Solution Architect Financial service providers must embrace new technologies and leverage data held in their systems to secure

WHITE PAPER. Revenue Opportunities Created by Open APIs

Revenue Opportunities Created by Open APIs Financial service providers must embrace modern technologies and leverage data held in their systems to secure their long-term futures. Open Banking initiatives,

Revenue Opportunities Created by Open APIs Financial service providers must embrace modern technologies and leverage data held in their systems to secure their long-term futures. Open Banking initiatives,

PSD2 Antoine Larmanjat

PSD2 Antoine Larmanjat Brussels May 2017 Card Issuers Winners and Losers of PSD2 PISPs AISPs Card schemes Retailers Card Issuing PSPs Fintechs PSPs Banks Clearing Houses Consumers 2 AISPs New Business

PSD2 Antoine Larmanjat Brussels May 2017 Card Issuers Winners and Losers of PSD2 PISPs AISPs Card schemes Retailers Card Issuing PSPs Fintechs PSPs Banks Clearing Houses Consumers 2 AISPs New Business

Open Banking: the technology revolution sweeping across the banking industry. Policy Pulse June 2018 compendium

Open Banking: the technology revolution sweeping across the banking industry Policy Pulse June 2018 compendium Eamonn McGrath UK Head of Regulatory & Public Policy Loree M. Gourley UK Director of Regulatory

Open Banking: the technology revolution sweeping across the banking industry Policy Pulse June 2018 compendium Eamonn McGrath UK Head of Regulatory & Public Policy Loree M. Gourley UK Director of Regulatory

Edgar, Dunn & Company A Closer Look at the Payment Regulations. Webinar 25 th June 2015

Edgar, Dunn & Company A Closer Look at the Payment Regulations Webinar 25 th June 2015 Edgar, Dunn & Company, 2015 Introduction This webinar will focus on two key regulatory topics: Multilateral Interchange

Edgar, Dunn & Company A Closer Look at the Payment Regulations Webinar 25 th June 2015 Edgar, Dunn & Company, 2015 Introduction This webinar will focus on two key regulatory topics: Multilateral Interchange

Payment Services Directive 2: What it Means for Banks, Customers, and Payment Service Providers

Payment Services Directive 2: What it Means for Banks, Customers, and Payment Service Providers Abstract The Payment Services Directive 2 (PSD2) can have a significant impact on customers, banks, and payment

Payment Services Directive 2: What it Means for Banks, Customers, and Payment Service Providers Abstract The Payment Services Directive 2 (PSD2) can have a significant impact on customers, banks, and payment

The Open Banking PSD2 Implementation Strategies

The Open Banking PSD2 Implementation Strategies How to meet the challenge of Open Banking Introduction Open Banking is the next step in a technology evolution driven by the API economy. Technology giants

The Open Banking PSD2 Implementation Strategies How to meet the challenge of Open Banking Introduction Open Banking is the next step in a technology evolution driven by the API economy. Technology giants

INDEX. Is your company ready for tomorrow? Middleware by eresolute. Functional Architecture. Features. Security. Applications. Benefits.

INDEX Is your company ready for tomorrow? Middleware by eresolute Functional Architecture Features Security Applications Benefits Our Clients Case Studies Our Reach About eresolute 1 3 6 8 10 12 14 16

INDEX Is your company ready for tomorrow? Middleware by eresolute Functional Architecture Features Security Applications Benefits Our Clients Case Studies Our Reach About eresolute 1 3 6 8 10 12 14 16

Open Banking / Future Banking. Kasper Sylvest, head of Financial Market Infrastructures, Transaction Banking Operations

Open Banking / Future Banking Kasper Sylvest, head of Financial Market Infrastructures, Transaction Banking Operations Disclaimer it is difficult to make predictions especially about the future Before

Open Banking / Future Banking Kasper Sylvest, head of Financial Market Infrastructures, Transaction Banking Operations Disclaimer it is difficult to make predictions especially about the future Before

Board Terms of Reference

Group Board of Directors Board Terms of Reference Chair Members Attendees Additional Invitees Quorum Meeting Frequency Secretary This Board receives its authority from The Chairman of Group 1 as appointed

Group Board of Directors Board Terms of Reference Chair Members Attendees Additional Invitees Quorum Meeting Frequency Secretary This Board receives its authority from The Chairman of Group 1 as appointed

Horizontal Integration in the Payments Industry

Horizontal Integration in the Payments Industry Gerard Hartsink Senior Executive Vice President 2007 Payments Conference Santa Fe, 3 May 2007 Content European landscape Restructuring of functions Impact

Horizontal Integration in the Payments Industry Gerard Hartsink Senior Executive Vice President 2007 Payments Conference Santa Fe, 3 May 2007 Content European landscape Restructuring of functions Impact

NextGen PSD2. A European Standard for PSD2 XS2A

NextGen PSD2 A European Standard for PSD2 XS2A Berlin Group and NextGenPSD2 The NextGenPSD2 Initiative is a dedicated Task Force of the Berlin Group with the goal to create an open, common and harmonised

NextGen PSD2 A European Standard for PSD2 XS2A Berlin Group and NextGenPSD2 The NextGenPSD2 Initiative is a dedicated Task Force of the Berlin Group with the goal to create an open, common and harmonised

Creating value from the open API economy A blueprint for banks

WHITE PAPER Creating value from the open API economy A blueprint for banks Change is inevitable as banks explore opportunities for leveraging open APIs to extend and transform their business models. This

WHITE PAPER Creating value from the open API economy A blueprint for banks Change is inevitable as banks explore opportunities for leveraging open APIs to extend and transform their business models. This

The Payment Services Directive 2 Background and Content

The Payment Services Directive 2 Background and Content The Jon Bing Memorial Seminar 2017 27 April 2017 Siv Bergit Pedersen Legal counsel MNBA DNB Bank ASA Background Norway Financial Agreements Act (Finansavtaleloven)

The Payment Services Directive 2 Background and Content The Jon Bing Memorial Seminar 2017 27 April 2017 Siv Bergit Pedersen Legal counsel MNBA DNB Bank ASA Background Norway Financial Agreements Act (Finansavtaleloven)

7 November Corporate Governance Principles

7 November 2017 Corporate Governance Principles Corporate Governance Principles of Hannover Rück SE 1. Introduction The present Corporate Governance Principles of Hannover Rück SE were adopted by the Executive

7 November 2017 Corporate Governance Principles Corporate Governance Principles of Hannover Rück SE 1. Introduction The present Corporate Governance Principles of Hannover Rück SE were adopted by the Executive

117 shades of black within PSD2

117 shades of black within PSD2 Thoughts on PSD2 implementation from strategic and technical perspective. Preface Last 2+ years has brought a lot of changes within payment industry. It all started on October

117 shades of black within PSD2 Thoughts on PSD2 implementation from strategic and technical perspective. Preface Last 2+ years has brought a lot of changes within payment industry. It all started on October

PSD2 IMPLICATIONS OF THE REGULATION August 8, Regina Lau, Chief Strategy Officer, Ingenico epayments Zainab Mir, Counsel Payments, Netflix

PSD2 IMPLICATIONS OF THE REGULATION August 8, 2017 Regina Lau, Chief Strategy Officer, Ingenico epayments Zainab Mir, Counsel Payments, Netflix OVERVIEW 1. PSD2 Overview Regina Lau 2. Strong Customer Authentication

PSD2 IMPLICATIONS OF THE REGULATION August 8, 2017 Regina Lau, Chief Strategy Officer, Ingenico epayments Zainab Mir, Counsel Payments, Netflix OVERVIEW 1. PSD2 Overview Regina Lau 2. Strong Customer Authentication

IBM Watson Financial Services

IBM Watson Financial Services Risk & Compliance Innovation Forum Adapting to a New Regulatory Environment in Europe Tim Roberts London 24 May 2017 2016 IBM Corporation Agenda for Today All financial institutions

IBM Watson Financial Services Risk & Compliance Innovation Forum Adapting to a New Regulatory Environment in Europe Tim Roberts London 24 May 2017 2016 IBM Corporation Agenda for Today All financial institutions

Introducing CGI Open Finance for the Open Banking Economy

Introducing CGI Open Finance for the Open Banking Economy Open power. Connected innovation. Financial sector challenges We are witnessing a profound and radical change to the traditional banking model.

Introducing CGI Open Finance for the Open Banking Economy Open power. Connected innovation. Financial sector challenges We are witnessing a profound and radical change to the traditional banking model.

Navigating the PSD2 and GDPR challenges faced by banks. Minds made for protecting financial services

Navigating the PSD2 and GDPR challenges faced by banks Minds made for protecting financial services When the financial services industry works well, it creates growth, prosperity and peace of mind for

Navigating the PSD2 and GDPR challenges faced by banks Minds made for protecting financial services When the financial services industry works well, it creates growth, prosperity and peace of mind for

Fintech Post trade clearing and settlement

Fintech 2.0 - Post trade clearing and settlement Udayan Goyal Co-Founder and Co-Managing Partner, Apis Partners 09 July 2015 Cover TBU 1 What is Fintech? Redesigned Financial Services for a new competitive

Fintech 2.0 - Post trade clearing and settlement Udayan Goyal Co-Founder and Co-Managing Partner, Apis Partners 09 July 2015 Cover TBU 1 What is Fintech? Redesigned Financial Services for a new competitive

Payment Infrastructure and Collections

Payment Infrastructure and Collections Payment Infrastructure and Collections Companies in the consumer brands, retail and healthcare (CBRH) sector face a broad range of collections and accounts receivables

Payment Infrastructure and Collections Payment Infrastructure and Collections Companies in the consumer brands, retail and healthcare (CBRH) sector face a broad range of collections and accounts receivables

Navigating the PSD2 and GDPR challenges faced by banks. Minds made for protecting financial services

Navigating the PSD2 and GDPR challenges faced by banks Minds made for protecting financial services When the financial services industry works well, it creates growth, prosperity and peace of mind for

Navigating the PSD2 and GDPR challenges faced by banks Minds made for protecting financial services When the financial services industry works well, it creates growth, prosperity and peace of mind for

API Banking. The shift to open banking

API Banking The shift to open banking The shift to open banking and move towards value added services. as the platform for compliance and beyond Open banking is set to have a major impact on the financial

API Banking The shift to open banking The shift to open banking and move towards value added services. as the platform for compliance and beyond Open banking is set to have a major impact on the financial

Accelerating Compliance & the API Economy with Open Banking & PSD2

Briefing Accelerating Compliance & the API Economy with Open Banking & PSD2 Rohan Consulting Banking is undergoing Digital Disruption and it s about to get worse 02 Banks and financial services providers

Briefing Accelerating Compliance & the API Economy with Open Banking & PSD2 Rohan Consulting Banking is undergoing Digital Disruption and it s about to get worse 02 Banks and financial services providers

Challenges and solutions. related to Digital Transformation Training & workshop

Challenges and solutions related to Digital Transformation Training & workshop Agenda 09:00-09:30 Registration, coffee 09:30 11:00 Trends in digitalization Regulatory challenges (PSD2 & other) Business

Challenges and solutions related to Digital Transformation Training & workshop Agenda 09:00-09:30 Registration, coffee 09:30 11:00 Trends in digitalization Regulatory challenges (PSD2 & other) Business

PSD2 Strategy. Comply, Compete or Innovate? November kpmg.nl

PSD2 Strategy Comply, Compete or Innovate? November 2017 kpmg.nl The Dutch market view on PSD2 Will PSD2 determine the future of payments and banking? Account Servicing Payment Service Providers (AS-PSPs,

PSD2 Strategy Comply, Compete or Innovate? November 2017 kpmg.nl The Dutch market view on PSD2 Will PSD2 determine the future of payments and banking? Account Servicing Payment Service Providers (AS-PSPs,

10/02/2017 Version pptx. 1

The Information Commissioner s response to the Department for Business, Energy and Industrial Strategy call for evidence on implementing Midata in the energy sector The Information Commissioner has responsibility

The Information Commissioner s response to the Department for Business, Energy and Industrial Strategy call for evidence on implementing Midata in the energy sector The Information Commissioner has responsibility

DEFINING NEW CUSTOMER JOURNEYS

DEFINING NEW CUSTOMER JOURNEYS Payment Services Directive 2 (PSD2) Scoping out the impacts of the Regulatory Technical Standards (RTS) on Strong Customer Authentication and Common and Secure Open Standards

DEFINING NEW CUSTOMER JOURNEYS Payment Services Directive 2 (PSD2) Scoping out the impacts of the Regulatory Technical Standards (RTS) on Strong Customer Authentication and Common and Secure Open Standards

Access and governance report on payment systems: update on progress. March 2018

Access and governance report on payment systems: update on progress March 2018 Contents 1 Executive summary 3 Access 4 Governance 6 Developments in 2018 6 2 Introduction 8 3 Access and developments over

Access and governance report on payment systems: update on progress March 2018 Contents 1 Executive summary 3 Access 4 Governance 6 Developments in 2018 6 2 Introduction 8 3 Access and developments over

Quali-Sign Banking. An example of how to meet the PSD2 segregation requirements. Michael Adams 3 rd November Quali-Sign Ltd

Quali-Sign Banking Quali-Sign Ltd An example of how to meet the PSD2 segregation requirements. Michael Adams 3 rd November 2016 2016 Quali-Sign Ltd michael_adams@quali-sign.com Context The PSD2 segregation

Quali-Sign Banking Quali-Sign Ltd An example of how to meet the PSD2 segregation requirements. Michael Adams 3 rd November 2016 2016 Quali-Sign Ltd michael_adams@quali-sign.com Context The PSD2 segregation

OPEN BANKING: THE ART OF THE POSSIBLE MAKING OPEN BANKING WORK FOR YOUR ORGANISATION. An NCR white paper

OPEN BANKING: THE ART OF THE POSSIBLE MAKING OPEN BANKING WORK FOR YOUR ORGANISATION An NCR white paper TABLE OF CONTENTS 1 OPEN BANKING AT A GLANCE 2 UNDERSTAND THE CONTEXT: WHY HERE, WHY NOW? 3 WHAT

OPEN BANKING: THE ART OF THE POSSIBLE MAKING OPEN BANKING WORK FOR YOUR ORGANISATION An NCR white paper TABLE OF CONTENTS 1 OPEN BANKING AT A GLANCE 2 UNDERSTAND THE CONTEXT: WHY HERE, WHY NOW? 3 WHAT

UK Finance welcome the clarity the EBA is giving on availability and performance of dedicated interfaces.

UK Finance response to EBA consultation on draft Guidelines on the conditions to be met to benefit from an exemption from contingency measures under Article 33(6) of Regulation (EU) 2018/389 (RTS on SCA

UK Finance response to EBA consultation on draft Guidelines on the conditions to be met to benefit from an exemption from contingency measures under Article 33(6) of Regulation (EU) 2018/389 (RTS on SCA

How Circeo runs online Retail Loan Factory for Banks from IBM Cloud

How Circeo runs online Retail Loan Factory for Banks from IBM Cloud Bled 2018 Think Bled / DOC ID / Nov 6-7, 2018 / 2018 IBM Corporation Contents Introduction Part One Circeo & TheLoanFactory Part Two

How Circeo runs online Retail Loan Factory for Banks from IBM Cloud Bled 2018 Think Bled / DOC ID / Nov 6-7, 2018 / 2018 IBM Corporation Contents Introduction Part One Circeo & TheLoanFactory Part Two

BOM/BSD 2/November 1994 BANK OF MAURITIUS. Guideline on Maintenance of Accounting and other Records and Internal Control Systems

BOM/BSD 2/November 1994 BANK OF MAURITIUS Guideline on Maintenance of Accounting and other Records and Internal Control Systems November 1994 Revised November 2013 Revised December 2017 TABLE OF CONTENTS

BOM/BSD 2/November 1994 BANK OF MAURITIUS Guideline on Maintenance of Accounting and other Records and Internal Control Systems November 1994 Revised November 2013 Revised December 2017 TABLE OF CONTENTS

4.1. The quorum necessary for the transaction of business shall be two members.

AUDIT COMMITTEE - TERMS OF REFERENCE 1. Constitution 1.1. The board hereby resolves to establish a committee of the board to be known as the Audit Committee. 2. Membership 2.1. The committee shall consist

AUDIT COMMITTEE - TERMS OF REFERENCE 1. Constitution 1.1. The board hereby resolves to establish a committee of the board to be known as the Audit Committee. 2. Membership 2.1. The committee shall consist

The Future of Open Banking, beyond January 2018 An industry report by Pinsent Masons and Innovate Finance

The Future of Open Banking, beyond January 2018 An industry report by Pinsent Masons and Innovate Finance Contents 04 Foreword 06 Topic One The opportunity is immense 08 Topic Two Collaboration is essential

The Future of Open Banking, beyond January 2018 An industry report by Pinsent Masons and Innovate Finance Contents 04 Foreword 06 Topic One The opportunity is immense 08 Topic Two Collaboration is essential

Corporate Governance 2014 FINNLINES

Corporate Governance 2014 FINNLINES FINNLINES PLC CORPORATE GOVERNANCE STATEMENT Finnlines Plc applies the guidelines and provisions of the Finnish Limited Liability Companies Act, the NASDAQ OMX Helsinki

Corporate Governance 2014 FINNLINES FINNLINES PLC CORPORATE GOVERNANCE STATEMENT Finnlines Plc applies the guidelines and provisions of the Finnish Limited Liability Companies Act, the NASDAQ OMX Helsinki

PSD2 & Instant Payment

PSD2 & Instant Payment Presentation to Investors June 2017 Agenda Introduction PSD2/Instant Payment Impacts for Banks Worldline offering for Banks PSD2/Instant Payment Impacts for Merchants Worldline offering

PSD2 & Instant Payment Presentation to Investors June 2017 Agenda Introduction PSD2/Instant Payment Impacts for Banks Worldline offering for Banks PSD2/Instant Payment Impacts for Merchants Worldline offering

Searching and switching in retail banking

Searching and switching in retail banking Stefano Callari, Alexander Moore, Laura Rovegno * Competition and Markets Authority Pasquale Schiraldi London School of Economics Abstract This paper investigates

Searching and switching in retail banking Stefano Callari, Alexander Moore, Laura Rovegno * Competition and Markets Authority Pasquale Schiraldi London School of Economics Abstract This paper investigates

WHITE PAPER HOW BANKS CAN CREATE VALUE FROM THE RISE OF THE OPEN API ECONOMY IN FINANCIAL SERVICES

WHITE PAPER HOW BANKS CAN CREATE VALUE FROM THE RISE OF THE OPEN API ECONOMY IN FINANCIAL SERVICES 2 How Banks Can Create Value from the Rise of the Open API Economy in Financial Services - WHITE PAPER

WHITE PAPER HOW BANKS CAN CREATE VALUE FROM THE RISE OF THE OPEN API ECONOMY IN FINANCIAL SERVICES 2 How Banks Can Create Value from the Rise of the Open API Economy in Financial Services - WHITE PAPER

Corporate Governance. Syllabus

Corporate Governance Syllabus Corporate Governance Module outline and aims The aim of the Corporate Governance module is to equip the Chartered Secretary with the knowledge and key skills necessary to

Corporate Governance Syllabus Corporate Governance Module outline and aims The aim of the Corporate Governance module is to equip the Chartered Secretary with the knowledge and key skills necessary to

17 TH J A N U A R Y. Future of Banking. Emerging trends and Archetypes

17 TH J A N U A R Y Future of Banking Emerging trends and Archetypes F U T U R E O F F S I Numerous emerging forces are shaping the future of Banking Open, API Standards (e.g. PSD2) Heightened Expectations

17 TH J A N U A R Y Future of Banking Emerging trends and Archetypes F U T U R E O F F S I Numerous emerging forces are shaping the future of Banking Open, API Standards (e.g. PSD2) Heightened Expectations

No digitalization without risks

No digitalization without risks How to equip your organization against the new fraud threads? Frédéric Hennequin Senior Solution Specialist Fraud & Compliance Agenda SAS Introduction Online Fraud in Belgium

No digitalization without risks How to equip your organization against the new fraud threads? Frédéric Hennequin Senior Solution Specialist Fraud & Compliance Agenda SAS Introduction Online Fraud in Belgium

on remuneration policies and practices related to the sale and provision of retail banking products and services

EBA/GL/2016/06 13/12/2016 Guidelines on remuneration policies and practices related to the sale and provision of retail banking products and services 1. Compliance and reporting obligations Status of these

EBA/GL/2016/06 13/12/2016 Guidelines on remuneration policies and practices related to the sale and provision of retail banking products and services 1. Compliance and reporting obligations Status of these

Informa PLC TERMS OF REFERENCE AUDIT COMMITTEE. Adopted by the Board on

Informa PLC TERMS OF REFERENCE AUDIT COMMITTEE Adopted by the Board on 12 th December 2017 CONTENTS Constitution and Purpose... 1 1. Membership... 1 2. Secretary... 3 3. Quorum... 3 4. Frequency of Meetings...

Informa PLC TERMS OF REFERENCE AUDIT COMMITTEE Adopted by the Board on 12 th December 2017 CONTENTS Constitution and Purpose... 1 1. Membership... 1 2. Secretary... 3 3. Quorum... 3 4. Frequency of Meetings...

Informa PLC TERMS OF REFERENCE AUDIT COMMITTEE. Effective 1 st January

Informa PLC TERMS OF REFERENCE AUDIT COMMITTEE Effective 1 st January 2019 CONTENTS Constitution and Purpose... 1 1. Membership... 1 2. Secretary... 3 3. Quorum... 3 4. Frequency of Meetings... 3 5. Notice

Informa PLC TERMS OF REFERENCE AUDIT COMMITTEE Effective 1 st January 2019 CONTENTS Constitution and Purpose... 1 1. Membership... 1 2. Secretary... 3 3. Quorum... 3 4. Frequency of Meetings... 3 5. Notice

Market environment and implementation timeline PSD2 in a nutshell

www.pwc.com/psd2 Market environment and implementation timeline PSD2 in a nutshell Why do we need a new Payment Services Directive (PSD)? By 13 th January 2018, Member States will have to implement the

www.pwc.com/psd2 Market environment and implementation timeline PSD2 in a nutshell Why do we need a new Payment Services Directive (PSD)? By 13 th January 2018, Member States will have to implement the

WHITE PAPER. Encouraging innovation in payments through the PSD2 initiative. Abstract

WHITE PAPER Encouraging innovation in payments through the PSD2 initiative Abstract Revised Directive on Payment Services (PSD2) is primarily aimed at bringing new, online modes of payments initiation

WHITE PAPER Encouraging innovation in payments through the PSD2 initiative Abstract Revised Directive on Payment Services (PSD2) is primarily aimed at bringing new, online modes of payments initiation

Changing Payments Landscape

Changing Payments Landscape How 2017 will change the way we pay for good A Payments UK Report January 2017 Contents Introduction 2017 A tipping point 4 Maurice Cleaves, Chief Executive Context Great expectations:

Changing Payments Landscape How 2017 will change the way we pay for good A Payments UK Report January 2017 Contents Introduction 2017 A tipping point 4 Maurice Cleaves, Chief Executive Context Great expectations:

Bank of the future Surf on the tsunami of disruption and get ready for the new paradigm

Bank of the future Surf on the tsunami of disruption and get ready for the new paradigm Patrick Laurent Partner Technology & Enterprise Application Leader Deloitte Thibault Chollet Director Technology

Bank of the future Surf on the tsunami of disruption and get ready for the new paradigm Patrick Laurent Partner Technology & Enterprise Application Leader Deloitte Thibault Chollet Director Technology

Navigating the components of Open Banking

White Paper Navigating the components of Open Banking How to create a suitable architecture Creating value from your infrastructure Open Banking will bring new challenges for lenders - their technology

White Paper Navigating the components of Open Banking How to create a suitable architecture Creating value from your infrastructure Open Banking will bring new challenges for lenders - their technology

AUDIT COMMITTEE TERMS OF REFERENCE

AUDIT COMMITTEE TERMS OF REFERENCE These terms of reference (the Terms of Reference) of the audit committee (the Audit Committee) have been established by the supervisory board (the Supervisory Board)

AUDIT COMMITTEE TERMS OF REFERENCE These terms of reference (the Terms of Reference) of the audit committee (the Audit Committee) have been established by the supervisory board (the Supervisory Board)

Helping ASPSPs implement PSD2 and take advantage of Open Banking January 2019

Helping ASPSPs implement PSD2 and take advantage of Open Banking January 2019 Version 1.36 1 We make it easier for ASPSPs to implement PSD2 and take advantage of Open Banking We have developed a comprehensive

Helping ASPSPs implement PSD2 and take advantage of Open Banking January 2019 Version 1.36 1 We make it easier for ASPSPs to implement PSD2 and take advantage of Open Banking We have developed a comprehensive

People, Culture and Remuneration Committee Charter. The Hospitals Contribution Fund of Australia Ltd (ACN ) (the Company )

(the Company )") People, Culture and Remuneration Committee Charter The Hospitals Contribution Fund of Australia Ltd (ACN 000 026 746) (the Company ) Board approval date: 29 June 2017 Contents 1. Introduction and Purpose

People, Culture and Remuneration Committee Charter The Hospitals Contribution Fund of Australia Ltd (ACN 000 026 746) (the Company ) Board approval date: 29 June 2017 Contents 1. Introduction and Purpose

The EU Regulations on payments

The EU Regulations on payments Impacts - Options - Customer ownership Prepaid Summit Europe VISA Timetric - Milano - 2016.10.27 E- Payment & SEPA Adviser 2010 Colt Telecom Group Limited. All rights reserved.

The EU Regulations on payments Impacts - Options - Customer ownership Prepaid Summit Europe VISA Timetric - Milano - 2016.10.27 E- Payment & SEPA Adviser 2010 Colt Telecom Group Limited. All rights reserved.

References to Board Committees shall mean the Audit, Nominations, Remuneration and Health, Safety, Environment and Community Relations Committees.

Fresnillo plc (the Company ) Schedule of Matters Reserved for the Board Terms of Reference: References to Board Committees shall mean the Audit, Nominations, Remuneration and Health, Safety, Environment

Fresnillo plc (the Company ) Schedule of Matters Reserved for the Board Terms of Reference: References to Board Committees shall mean the Audit, Nominations, Remuneration and Health, Safety, Environment

PSD2 ACCELERATOR CAPTURE OPPORTUNITIES, ADDRESS CHALLENGES, AND DRIVE SUCCESS THROUGH PROVEN EXPERTISE

PSD2 ACCELERATOR CAPTURE OPPORTUNITIES, ADDRESS CHALLENGES, AND DRIVE SUCCESS THROUGH PROVEN EXPERTISE INTRODUCING OLIVER WYMAN S PSD2 ACCELERATOR PSD2 will have profound implications for the participation

PSD2 ACCELERATOR CAPTURE OPPORTUNITIES, ADDRESS CHALLENGES, AND DRIVE SUCCESS THROUGH PROVEN EXPERTISE INTRODUCING OLIVER WYMAN S PSD2 ACCELERATOR PSD2 will have profound implications for the participation

Input to Members of the European Parliament on the PSD2 RTS proposal covering banks obligations

Input to Members of the European Parliament on the PSD2 RTS proposal covering banks obligations ESBG (European Savings and Retail Banking Group) Rue Marie-Thérèse, 11 - B-1000 Brussels ESBG Transparency

Input to Members of the European Parliament on the PSD2 RTS proposal covering banks obligations ESBG (European Savings and Retail Banking Group) Rue Marie-Thérèse, 11 - B-1000 Brussels ESBG Transparency

Eurofinas and Roland Berger are pleased to invite you to participate in their second joint survey on The Future of European Consumer Finance.

2018 Future of European Consumer Finance Survey Eurofinas and Roland Berger are pleased to invite you to participate in their second joint survey on The Future of European Consumer Finance. The survey

2018 Future of European Consumer Finance Survey Eurofinas and Roland Berger are pleased to invite you to participate in their second joint survey on The Future of European Consumer Finance. The survey

Water Act. New Water Act receives Royal Assent

New Water Act receives Royal Assent On 27 June 2013, the Water Bill 2013-2014 1 was introduced into the House of Commons. The Bill received Royal Assent on 14 May 2014 and the Water Act 2014 (the Act )

New Water Act receives Royal Assent On 27 June 2013, the Water Bill 2013-2014 1 was introduced into the House of Commons. The Bill received Royal Assent on 14 May 2014 and the Water Act 2014 (the Act )

SOLUTION BRIEF BUSINESS-DRIVEN, OMNI-CHANNEL FRAUD MANAGEMENT RSA FRAUD & RISK INTELLIGENCE

BUSINESS-DRIVEN, OMNI-CHANNEL FRAUD MANAGEMENT RSA FRAUD & RISK INTELLIGENCE RSA FRAUD & RISK INTELLIGENCE SUITE Inspire confidence without inconvenience Reduce fraud, not customers or revenue Expose risk

BUSINESS-DRIVEN, OMNI-CHANNEL FRAUD MANAGEMENT RSA FRAUD & RISK INTELLIGENCE RSA FRAUD & RISK INTELLIGENCE SUITE Inspire confidence without inconvenience Reduce fraud, not customers or revenue Expose risk

Finance, Audit & Risk Management Committee Terms of Reference

Finance, Audit & Risk Management Committee Terms of Reference Version: 1.0 Effective date:14/04/2016 Name of Document: Finance, Audit and Risk Committee - Terms of Reference Version: Version 1.0 Created/Reviewed:

Finance, Audit & Risk Management Committee Terms of Reference Version: 1.0 Effective date:14/04/2016 Name of Document: Finance, Audit and Risk Committee - Terms of Reference Version: Version 1.0 Created/Reviewed:

THE PAYMENT SERVICES DIRECTIVE II (PSD II) Liberalisation of electronic payment transactions

Liberalisation of electronic payment transactions") April 2017 THE PAYMENT SERVICES DIRECTIVE II (PSD II) Liberalisation of electronic payment transactions Hurry up! Only a few more months until January 2018, when payment service providers are obliged to

April 2017 THE PAYMENT SERVICES DIRECTIVE II (PSD II) Liberalisation of electronic payment transactions Hurry up! Only a few more months until January 2018, when payment service providers are obliged to

THE RISE OF OPEN APIs MANAGING NEW THREE-WAY RELATIONSHIPS UNDER PSD2 & OPEN BANKING

ARTICLE MANAGING NEW THREE-WAY RELATIONSHIPS UNDER PSD2 & OPEN BANKING THE RISE OF OPEN APIS MANAGING NEW THREE-WAY RELATIONSHIPS UNDER PSD2 & OPEN BANKING PRESENTED BY FIS & MARKETFORCE The rather dry

ARTICLE MANAGING NEW THREE-WAY RELATIONSHIPS UNDER PSD2 & OPEN BANKING THE RISE OF OPEN APIS MANAGING NEW THREE-WAY RELATIONSHIPS UNDER PSD2 & OPEN BANKING PRESENTED BY FIS & MARKETFORCE The rather dry

IoD Code of Practice for Directors

The Four Pillars of Governance Best Practice Institute of Directors in New Zealand (Inc). IoD Code of Practice for Directors This Code provides guidance to directors to assist them in carrying out their

The Four Pillars of Governance Best Practice Institute of Directors in New Zealand (Inc). IoD Code of Practice for Directors This Code provides guidance to directors to assist them in carrying out their