DISCLAIMER. This presentation does not constitute an offer of securities for sale in the United States of America or any other jurisdiction.

|

|

|

- Roger Anderson

- 5 years ago

- Views:

Transcription

1

2 DISCLAIMER This presentation does not constitute an offer of securities for sale in the United States of America or any other jurisdiction. Certain information contained in this document may include projections and forecasts. They express objectives based on current assessments and estimates of the Group s executive management which are subject to numerous factors, risks and uncertainties. Consequently, reported figures and assessments may differ significantly from projected figures. The following factors among others set out in the Reference Document (Document de Référence) filed with the French Financial Markets Authority (Autorité des Marchés Financiers - AMF) on March 30th, 2017 which is available on Kering s website at may cause actual figures to differ materially from projected figures: any unfavourable development affecting consumer spending in the activities of the Group in France and abroad, notably for products and services sold by the Luxury Goods and Sport & Lifestyle brands, the events, crises, fears, and resulting costs of complying with environmental, health and safety regulations and all other regulations with which Group companies are required to comply; the competitive situation on each of our markets; exchange rate and other risks related to international activities; risks arising from current or future litigation. Kering gives no commitment to updating and/or revising and/or commenting any projections and forecasts, or their impact on the results and perspectives of the Group, which may be contained in this presentation. The information contained in this document has been selected by the Group s executive management to present YSL brand vision and strategy. This document has not been independently verified. Kering makes no representation or undertaking as to the accuracy or completeness of such information. None of the Kering or any of its affiliates representatives shall bear any liability (in negligence or otherwise) for any loss arising from any use of this presentation or its contents or otherwise arising in connection with this presentation. IN NO WAY DOES KERING ASSUME ANY RESPONSIBILITY FOR ANY INVESTMENT OR OTHER DECISIONS MADE BASED UPON THE INFORMATION PROVIDED IN THIS PRESENTATION. INFORMATION IN THIS PRESENTATION, INCLUDING FORECAST FINANCIAL INFORMATION, SHOULD NOT BE CONSIDERED AS ADVICE OR A RECOMMENDATION TO INVESTORS OR POTENTIAL INVESTORS IN RELATION TO HOLDING, PURCHASING OR SELLING SECURITIES OR OTHER FINANCIAL PRODUCTS OR INSTRUMENTS AND DOES NOT TAKE INTO ACCOUNT YOUR PARTICULAR INVESTMENT OBJECTIVES, FINANCIAL SITUATION OR NEEDS. BEFORE ACTING ON ANY INFORMATION YOU SHOULD CONSIDER THE APPROPRIATENESS OF THE INFORMATION HAVING REGARD TO THESE MATTERS, ANY RELEVANT OFFER DOCUMENT AND IN PARTICULAR, YOU SHOULD SEEK INDEPENDENT FINANCIAL ADVICE. ALL SECURITIES AND FINANCIAL PRODUCT OR INSTRUMENT TRANSACTIONS INVOLVE RISKS, WHICH INCLUDE (AMONG OTHERS) THE RISK OF ADVERSE OR UNANTICIPATED MARKET, FINANCIAL OR POLITICAL DEVELOPMENTS AND, IN INTERNATIONAL TRANSACTIONS, CURRENCY RISK. READERS ARE ADVISED TO REVIEW THE COMPANY'S REFERENCE DOCUMENT AND THE COMPANY'S APPLICABLE AMF FILINGS BEFORE MAKING ANY INVESTMENT OR OTHER DECISION. 2

3 3

4 SAINT LAURENT

5 KEY MILESTONES 5

6 THE FOUNDING FATHER 6

7 2012 REFORM: BRING BACK BRAND CLARITY 7

8 BRAND MINDSET: RIVE GAUCHE ATTITUDE & HAUTE COUTURE SPIRIT In 1966 Yves Saint Laurent decided to offer his couture designs to the street. He found a way to industrialize his couture collections thanks to the great experience of a manufacture based in western France, in Angers. At that time, the difference between couture and ready-to-wear was mainly in fabrication (produced in a factory versus done by hand and adapted to the body fit) rather than a difference of style. His goal was to bring style to the street. 8

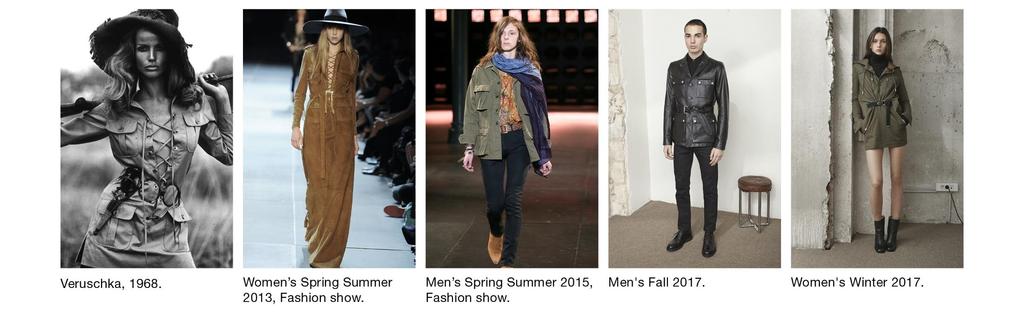

9 BRAND MINDSET: RIVE GAUCHE ATTITUDE & HAUTE COUTURE SPIRIT PARIS CITY MAP 1966 FRENCH MAISONS STORE LOCATIONS 9

10 YOUTH: UNDERSTANDING WHAT IS EMERGING 10

11 FEMALE AND MALE PARITY 11

12 FEMALE AND MALE PARITY 12

13 #YSL01: FEMALE AND MALE PARITY & YOUTH SPIRIT 13

14 AUTHENTIC DRESS CODE 14

15 LE SMOKING 15

16 THE SAHARIENNE 16

17 THE SAC DE JOUR 17

18 ONE COLOR: BLACK 18

19 CASSANDRE LOGO TRANSVERSAL ACROSS COUTURE, PRÊT À PORTER AND ACCESSORIES 19

20 BRAND MISSION STATEMENT SAINT LAURENT IS A LUXURY COUTURE COOL BRAND LIVING IN ITS EPOCA EMBODYING THE FREE SPIRIT OF THE YOUTH CULTURE WHILE STAYING TRUE TO ITS HERITAGE AND DNA 20

21 KEY FIGURES

22 KEY FIGURES

23 6 CONSECUTIVE YEARS OF GROWTH EXCEEDING 20% 1, REVENUE IN M DOS: 78 DOS:

24 14 CONSECUTIVE QUARTERS OF GROWTH EXCEEDING 20% 42.0% 33.9% 33.4% 27.1% 29.4% 27.5% 25.3% 27.3% 26.6% 27.4% 26.5% 18.7% 21.2% 22.1% 20.5% 14.2% 12.0% Q Q Q Q Q Q Q Q Q Q Q Q Q Q Q Q Q Y-O-Y COMPARABLE SALES GROWTH 24

25 STRONG INCREASE IN RECURRING OPERATING INCOME AND MARGIN 22.0% % % 13.7% 13.8% % EBIT MARGIN 4.3% 41 EBIT IN M FASHION AND LEATHER GOODS EBIT BREAKEVEN 25

26 REVENUE 2016 BY CHANNEL 26

27 REVENUE 2016 BY REGIONS 27

28 REVENUE 2016 BY PRODUCT CATEGORIES 28

29 AT YEAR END STORES AS OF MARCH 31ST,

30 A WELL-BALANCED STORE NETWORK 159 #DOS WESTERN EUROPE NORTH AMERICA JAPAN EMERGING MARKETS NEW COUNTRIES MAINLAND CHINA MACAU UAE AUSTRIA THAILAND MEXICO BRAZIL QATAR MALAYSIA CANADA 30

31 THE AMBITION 31

32 THE AMBITION 32

33 THE ROAD TO FULL POTENTIAL

34 THE ROAD TO FULL POTENTIAL SUSTAINING BRAND EQUITY 34

35 CULTIVATE DESIRE 35

36 CULTIVATE DESIRE SUMMER 2017 SHOW 36

37 CULTIVATE DESIRE WINTER 2017 SHOW 37

38 ADVERTISING CAMPAIGNS SHE IS A REBEL WITH A SERIOUS BANK ACCOUNT WWD 38

39 PRESS LEVERAGE SAINT LAURENT MOMENTUM 39

40 PRESS LEVERAGE SAINT LAURENT MOMENTUM 40

41 INSTAGRAM AS A STRONG IMAGE PLATFORM 41

42 EXPANSION ON OTHER PLATFORMS 42

43 EXPANSION ON OTHER PLATFORMS: YOUTUBE 43

44 OUTDOOR VISIBILITY 44

45 WILD POSTING 45

46 THE ROAD TO FULL POTENTIAL SUSTAINING BRAND EQUITY LEVERAGE PRODUCT OPPORTUNITIES 46

47 A BROAD PRODUCT PORTFOLIO COMPLETE WARDROBES IN READY-TO-WEAR FOR BOTH WOMEN AND MEN A WELL-BALANCED PORTFOLIO OF LEATHER GOODS STRONG DEVELOPMENT IN SHOES EXPANSION OF ASPIRATIONAL ACCESSORIES 47

48 THE ROAD TO FULL POTENTIAL FUEL GROWTH IN ALL CHANNELS SUSTAINING BRAND EQUITY LEVERAGE PRODUCT OPPORTUNITIES 48

49 FUEL GROWTH IN ALL CHANNELS CUSTOMER OBSESSION LOCAL CLIENTS COMP GROWTH STRATEGIC NEW OPENINGS PARTNERSHIPS WITH KEY WHOLESALERS TRAVEL RETAIL EXPANSION E-COMMERCE BOOST 49

50 FURTHER ROOM FOR GROWTH IN SALES DENSITY AVERAGE LUXURY GIANTS TOTAL STORES SAINT LAURENT STORES OPENED FOR MORE THAN A YEAR IN LINE WITH INDUSTRY AVERAGE FURTHER POTENTIAL TO INCREASE THANKS TO EXCELLENCE IN RETAIL 0 20, , 000 /sqm SOURCES: INDUSTRY DATA, INTERNAL ESTIMATES 50

51 ROOM FOR STORE EXPANSION #DOS BY REGION ROW Asia Japan Americas Europe SAINT LAURENT 51

52 FLAGSHIPS & KEY STORES SPREAD THE BRAND IMAGE WORLDWIDE TORONTO BERLIN SEOUL HONOLULU VANCOUVER LOS ANGELES MEXICO NEW YORK MIAMI LONDON PARIS X2 X2 MILAN MADRID BARCELONA DOHA DUBAI BEIJING SHANGHAI X2 TOKYO X2 HONG KONG BANGKOK KUALA LUMPUR SAO PAULO SINGAPORE FLAGSHIPS KEY REGULAR STORE 52

53 KEY COMING OPENINGS HONOLULU VANCOUVER LOS ANGELES TORONTO X2 X2 NEW YORK MIAMI LONDON PARIS X2 X2 BERLIN MUNICH, ZURICH GENEVA MILAN MADRID BARCELONA KUWAIT SHANGHAI BEIJING X2 X2 SEOUL TOKYO X2 HONG KONG MEXICO DOHA X2 DUBAI BANGKOK KUALA LUMPUR SAO PAULO SINGAPORE MELBOURNE FLAGSHIPS KEY REGULAR STORE 53

54 TRAVEL RETAIL EXPANSION C. 2.6% 1.8% LONDON PARIS X2 X2 VENICE TOKYO SEOUL x6 % SALES M 0.7% 1% HONG KONG x2 TAIPEI BANGKOK MACAU HAINAN SIEM REAP (EST.) x4 SINGAPORE 54

55 A CONSISTENT AND DIFFERENTIATING STORE CONCEPT 55

56 THE ROAD TO FULL POTENTIAL FUEL GROWTH IN ALL CHANNELS MASTERING SAVOIR-FAIRE SUSTAINING BRAND EQUITY LEVERAGE PRODUCT OPPORTUNITIES 56

57 MASTERING SAVOIR-FAIRE 57

58 MASTERING SAVOIR-FAIRE 58

SHOES ATELIER IN")

59 SAINT LAURENT LEATHERGOODS AND SHOES ATELIERS LG ATELIER IN SCANDICCI (FLORENCE) SHOES ATELIER IN VIGONZA (PADUA) 59

60 REPLENISHING LUXURY RELUX IS THE REPLENISHMENT PROGRAM FOR RETAIL STORES, WHOSE KEY OBJECTIVES ARE: MAXIMIZE SALES Securing best sellers constantly on hand to maximize sales opportunities OPTIMIZE MARGINS Shipping seasonal merchandise based on sales to reduce the slow-movers inventory SIMPLIFY IN-STORE OPERATIONS Right-sized inventory = simplified stock taking & pricing, less transfers, visual focus MARKET DISTRIBUTION DISCOVERY MATURITY END OF LIFE 60 1 Buy Newness only 2 Receive the initial Assortment 3 Replenish based on Sales 60

61 PURSUE THE INCREASE IN OPERATING MARGIN AND CASH FLOW STEADY INCREASE OF GROSS MARGINS INTERNALIZATION OF MATERIAL CUTTING AND PRODUCTION WILL ENABLE THE OPTIMIZATION OF THE COST OF GOODS SOLD EXPANSION OF HIGH MARGIN CATEGORIES AS WELL AS THE EVOLUTION OF THE GEOGRAPHIC MIX WILL DRIVE MARGINS UPWARDS LEVERAGE ON OPERATING EXPENSES FIXED COSTS IN PRODUCTION, DEVELOPMENT, DISTRIBUTION AND G&A WILL CONTINUE TO BE LEVERAGED / INCLUDING SAVINGS ON PARIS BUILDINGS RENT RENEGOTIATION IN CHINA ADVERTISING AND COMMUNICATION INVESTMENTS IN LINE WITH A TARGETED 6% RATIO TO SALES DIGITAL TO REPRESENT 22% OF ADVERTISING COSTS IN 2017, 2.5X VS 2016 CAPEX PACE OF APPROX 20 NET STORE OPENINGS / EXPANSIONS PER YEAR TARGETED AVERAGE YEARLY CAPEX: 5% OF REVENUE 61

62 THE ROAD TO FULL POTENTIAL MASTERING SAVOIR-FAIRE PEOPLE MAKE THE DIFFERENCE FUEL GROWTH IN ALL CHANNELS SUSTAINING BRAND EQUITY LEVERAGE PRODUCT OPPORTUNITIES 62

63 HEADCOUNT DOUBLED IN 4 YEARS 63

64 HR KEY FIGURES

65 GLOBAL RETAIL MEETING 65

66 THE ROAD TO FULL POTENTIAL FUEL GROWTH IN ALL CHANNELS MASTERING SAVOIR-FAIRE PEOPLE MAKE THE DIFFERENCE BUILDING AN INNOVATIVE & SUSTAINABLE FUTURE SUSTAINING BRAND EQUITY LEVERAGE PRODUCT OPPORTUNITIES 66

67 A FRONT RUNNER ON SUSTAINABILITY WITH 4 PILLARS 67

AND")

68 BUILDING THE FUTURE THROUGH INNOVATION EXPAND THE CROSS CHANNEL SERVICE LANDSCAPE ON YSL.COM PLATFORM ROLL-OUT TECHNOLOGIES WITHIN CURRENT CORE PROCESSES (3D PRINTING, DIGITALIZATION), THAT OPTMIZE RESOURCES AND SPEED INCUBATE PROJECTS TO ENHANCE CLIENT EXPERIENCE AND STORE EFFICIENCY EXPLORE AND TEST EMERGING TECHNOLOGIES (VR, AI) AND BUSINESS MODELS 68

69 IN CONCLUSION

70 SAINT LAURENT IN 2017 AND IN THE FUTURE A LUXURY COUTURE COOL BRAND LIVING IN ITS EPOCA, EMBODYING THE FREE SPIRIT OF THE YOUTH CULTURE, WHILE STAYING TRUE TO ITS HERITAGE AND DNA A NATURAL AND SUCCESSFUL CREATIVE EVOLUTION, IN LINE WITH THE BRAND DNA A WELL-BALANCED BUSINESS MODEL IN TERMS OF PRODUCT PORTFOLIO AND GEOGRAPHIES A GENUINE AMBITION IN TERMS OF REVENUE AND PROFITABILITY CLEAR LEVERS OF ACTION TO ACHIEVE THE FULL POTENTIAL OF THE BRAND 70

71 SAINT LAURENT IN THE FUTURE KEY DRIVERS MID TERM AMBITION LONG TERM AMBITION LOCAL CLIENTS REVENUE COMPARABLE AND NON COMPARABLE GROWTH OMNICHANNEL 2 BILLION 3 BILLION EBIT INCREASING GROSS MARGINS LEVERAGE FIXED COSTS EBIT MARGIN TO GRADUALLY REACH 25% REACH AND SUSTAIN 27% EBIT MARGIN CAPEX NETWORK FULLY ON SAINT LAURENT CONCEPT PACE OF 20 NET STORE OPENINGS / EXPANSIONS PER YEAR TARGETED AVERAGE YEARLY CAPEX: 5% OF REVENUE OVER 200 STORES 71

72 QUESTIONS & ANSWERS

73

Investor Day Refine the way we sell

01 Investor Day Refine the way we sell Bernd Hake Chief Sales Officer November 15, 2018 02 CUSTOMER- CENTRICITY IS KEY IN AN EVER CHANGING WORLD 03 Wholesale Retail Customer-centric From Point of Sale

01 Investor Day Refine the way we sell Bernd Hake Chief Sales Officer November 15, 2018 02 CUSTOMER- CENTRICITY IS KEY IN AN EVER CHANGING WORLD 03 Wholesale Retail Customer-centric From Point of Sale

China Strategy. HUGO BOSS Investor Day Mr. Gareth Incledon, Managing Director China Hong Kong, November 26, 2013

HUGO BOSS Investor Day 2013 China Strategy Mr. Gareth Incledon, Managing Director China Hong Kong, November 26, 2013 Investor Day 2013 // China Strategy HUGO BOSS November 26, 2013 2 / 34 Agenda HUGO BOSS

HUGO BOSS Investor Day 2013 China Strategy Mr. Gareth Incledon, Managing Director China Hong Kong, November 26, 2013 Investor Day 2013 // China Strategy HUGO BOSS November 26, 2013 2 / 34 Agenda HUGO BOSS

- cosmetics & high-end fragrances -

- cosmetics & high-end fragrances - May 2013 AGENDA 2 AGENDA 3 THE AMBITION OF A DEDICATED STUDY A new international study, building on previous learning. How do Global Shoppers associate travelling and

- cosmetics & high-end fragrances - May 2013 AGENDA 2 AGENDA 3 THE AMBITION OF A DEDICATED STUDY A new international study, building on previous learning. How do Global Shoppers associate travelling and

LUXURY GOODS WORLDWIDE MARKET STUDY, SPRING 2018 CLAUDIA D ARPIZIO FEDERICA LEVATO

LUXURY GOODS WORLDWIDE MARKET STUDY, SPRING 2018 CLAUDIA D ARPIZIO FEDERICA LEVATO PERSONAL LUXURY GOODS: AFTER 2016 STAGNATION, THE MARKET EXPERIENCED A HEALTHIER NEW NORMAL IN 2017 SORTIE DU TEMPLE DEMOCRATIZATION

LUXURY GOODS WORLDWIDE MARKET STUDY, SPRING 2018 CLAUDIA D ARPIZIO FEDERICA LEVATO PERSONAL LUXURY GOODS: AFTER 2016 STAGNATION, THE MARKET EXPERIENCED A HEALTHIER NEW NORMAL IN 2017 SORTIE DU TEMPLE DEMOCRATIZATION

First Half 2011 Results

First Half 2011 Results Tuesday July 26, 2011 revenue by business group Reported growth Organic growth Wines & Spirits 1 302 1 435 + 10% + 13% Fashion & Leather Goods 3 516 3 971 + 13% + 14% Perfumes &

First Half 2011 Results Tuesday July 26, 2011 revenue by business group Reported growth Organic growth Wines & Spirits 1 302 1 435 + 10% + 13% Fashion & Leather Goods 3 516 3 971 + 13% + 14% Perfumes &

The Global Luxury market is worth 1.5 trillion

The Global Luxury market is worth 1.5 trillion Luxury market ( B, 2015 retail value @current) 2,000 Personal luxury (323 B) Experiential luxury (522 B) Cars & Yachts (404 B) Others (284 B) 1,500 P&E 1

The Global Luxury market is worth 1.5 trillion Luxury market ( B, 2015 retail value @current) 2,000 Personal luxury (323 B) Experiential luxury (522 B) Cars & Yachts (404 B) Others (284 B) 1,500 P&E 1

INTERIM REPORT Q2 2018/19 8 JANUARY 2019

INTERIM REPORT 8 JANUARY 209 DISCLAIMER This presentation does not constitute or form part of and should not be construed as, an offer to sell or issue or the solicitation of an offer to buy or acquire

INTERIM REPORT 8 JANUARY 209 DISCLAIMER This presentation does not constitute or form part of and should not be construed as, an offer to sell or issue or the solicitation of an offer to buy or acquire

Q Trading Update

Q3 2017 Trading Update Agenda Financial Review Operational Support Strategy Regional Review Digital and Innovation Summary and Outlook Financial Review Q3 Trading Performance Year-on-Year Gross Profit

Q3 2017 Trading Update Agenda Financial Review Operational Support Strategy Regional Review Digital and Innovation Summary and Outlook Financial Review Q3 Trading Performance Year-on-Year Gross Profit

Digital Excellence index

Digital Excellence index Key findings - September 2018 Marko Derča, Vice president, Head of Digital Transformation, Eastern Europe Marko.derca@atkearney.com 1 Digital transformation is entering a new phase,

Digital Excellence index Key findings - September 2018 Marko Derča, Vice president, Head of Digital Transformation, Eastern Europe Marko.derca@atkearney.com 1 Digital transformation is entering a new phase,

The Digital Imperative in Container Shipping

The Digital Imperative in Container Shipping BCG is the leading strategy advisor in shipping 350+ projects in last 3 years across entire value chain Operators, owners, managers Tanker, bulkers, containers,

The Digital Imperative in Container Shipping BCG is the leading strategy advisor in shipping 350+ projects in last 3 years across entire value chain Operators, owners, managers Tanker, bulkers, containers,

6

6 LA-Z-BOY INCORPORATED

LA-Z-BOY INCORPORATED February 2018 Providing comfort to America for 90 years FORWARD-LOOKING DISCLAIMER This presentation contains forward-looking statements that involve uncertainties and risks as detailed

LA-Z-BOY INCORPORATED February 2018 Providing comfort to America for 90 years FORWARD-LOOKING DISCLAIMER This presentation contains forward-looking statements that involve uncertainties and risks as detailed

FY 2016 Results Update Analyst Presentation

FY 2016 Results Update Analyst Presentation March 14, 2017-6.30 PM CET Disclaimer This presentation contains forward-looking statements regarding future events and results of the Company that are based

FY 2016 Results Update Analyst Presentation March 14, 2017-6.30 PM CET Disclaimer This presentation contains forward-looking statements regarding future events and results of the Company that are based

Leadership Jumping Ship. Attracting and retaining the best performers at professional services firms

Leadership Jumping Ship Attracting and retaining the best performers at professional services firms 2 Summary In September 2016, Russell Reynolds Associates surveyed 333 senior executives at professional

Leadership Jumping Ship Attracting and retaining the best performers at professional services firms 2 Summary In September 2016, Russell Reynolds Associates surveyed 333 senior executives at professional

LA-Z-BOY INCORPORATED

LA-Z-BOY INCORPORATED November 2017 Providing comfort to America for 90 years FORWARD-LOOKING DISCLAIMER This presentation contains forward-looking statements that involve uncertainties and risks as detailed

LA-Z-BOY INCORPORATED November 2017 Providing comfort to America for 90 years FORWARD-LOOKING DISCLAIMER This presentation contains forward-looking statements that involve uncertainties and risks as detailed

SURVEY OF CORPORATE GOVERNANCE PRACTICES IN EUROPEAN FAMILY BUSINESSES

SURVEY OF CORPORATE GOVERNANCE PRACTICES IN EUROPEAN FAMILY BUSINESSES 1 In the summer of 2014, Russell Reynolds Associates and IESE conducted a survey of 400 of Europe s largest family-controlled businesses.

SURVEY OF CORPORATE GOVERNANCE PRACTICES IN EUROPEAN FAMILY BUSINESSES 1 In the summer of 2014, Russell Reynolds Associates and IESE conducted a survey of 400 of Europe s largest family-controlled businesses.

WHO WE ARE BRANDING & IDENTITY & SPECIALIST COMMUNICATIONS ADVERTISING & MEDIA PUBLIC RELATIONS INFORMATION, INSIGHT & CONSULTANCY

SOUTH AMERICA WHO WE ARE ADVERTISING & MEDIA PUBLIC RELATIONS BRANDING & IDENTITY & SPECIALIST COMMUNICATIONS INFORMATION, INSIGHT & CONSULTANCY WHO WE ARE We serve leading manufacturers and retailers

SOUTH AMERICA WHO WE ARE ADVERTISING & MEDIA PUBLIC RELATIONS BRANDING & IDENTITY & SPECIALIST COMMUNICATIONS INFORMATION, INSIGHT & CONSULTANCY WHO WE ARE We serve leading manufacturers and retailers

The Battle of Big versus Small. Zenith Adspend Forecast 2017

The Battle of Big versus Small Zenith Adspend Forecast 2017 The global ad market will continue to grow steadily +5,9 Year-on-year growth (%) +5,6 +5,6 +5,5 +4,0 +4,1 +4,2 +4,1 2017 2018 2019 2020 Adspend

The Battle of Big versus Small Zenith Adspend Forecast 2017 The global ad market will continue to grow steadily +5,9 Year-on-year growth (%) +5,6 +5,6 +5,5 +4,0 +4,1 +4,2 +4,1 2017 2018 2019 2020 Adspend

EFFICIENCY AND COST EFFECTIVENESS: 2015 DRIVERS FOR TECHNOLOGY SPEND

EFFICIENCY AND COST EFFECTIVENESS: 2015 DRIVERS FOR TECHNOLOGY SPEND 2 Over the past few years, capital market participants have invested heavily in technology and services to meet critical regulatory

EFFICIENCY AND COST EFFECTIVENESS: 2015 DRIVERS FOR TECHNOLOGY SPEND 2 Over the past few years, capital market participants have invested heavily in technology and services to meet critical regulatory

RemCo Chairs in the Spotlight

RemCo Chairs in the Spotlight 2 Executive Summary As investor pressure on boards to reduce excessive pay and introduce greater transparency has increased, so too has the level of media scrutiny, with compensation

RemCo Chairs in the Spotlight 2 Executive Summary As investor pressure on boards to reduce excessive pay and introduce greater transparency has increased, so too has the level of media scrutiny, with compensation

German Corporate Conference // Kepler Cheuvreux HUGO BOSS Company Presentation. Mark Langer, CFO January 20, 2016

HUGO BOSS Company Presentation Mark Langer, CFO January 20, 2016 2 Agenda Group strategy update Omnichannel strategy Financial outlook and summary 3 Agenda Group strategy update Omnichannel strategy Financial

HUGO BOSS Company Presentation Mark Langer, CFO January 20, 2016 2 Agenda Group strategy update Omnichannel strategy Financial outlook and summary 3 Agenda Group strategy update Omnichannel strategy Financial

TMT CONFERENCE Morgan Stanley November 20 th Doha, QATAR

TMT CONFERENCE Morgan Stanley November 20 th 2008 Doha, QATAR 1 OUTDOOR INDUSTRY, Structural growth opportunities JCDECAUX COMPETITIVE ADVANTAGE, A market leader FINANCIAL HIGHLIGHTS A robust financial

TMT CONFERENCE Morgan Stanley November 20 th 2008 Doha, QATAR 1 OUTDOOR INDUSTRY, Structural growth opportunities JCDECAUX COMPETITIVE ADVANTAGE, A market leader FINANCIAL HIGHLIGHTS A robust financial

INVESTOR PRESENTATION. IC Companys: Our Ambition

INVESTOR PRESENTATION IC Companys: Our Ambition DECEMBER 2010 Contents Introduction Our ambition So far so good 2 2 One of the Top 5 Largest Fashion Companies in the North brands brands 11 Scandinavian

INVESTOR PRESENTATION IC Companys: Our Ambition DECEMBER 2010 Contents Introduction Our ambition So far so good 2 2 One of the Top 5 Largest Fashion Companies in the North brands brands 11 Scandinavian

INVESTOR MEETING / MARCH 9, 2010

INVESTOR MEETING / MARCH 9, 2010 1 Disclosure Regarding Forward-Looking Statements This presentation contains forward-looking statements within the meaning of the federal securities laws. All statements,

INVESTOR MEETING / MARCH 9, 2010 1 Disclosure Regarding Forward-Looking Statements This presentation contains forward-looking statements within the meaning of the federal securities laws. All statements,

Navigating through an uncertain tariff landscape and building an end-to-end digital supply chain of the future

Supply chain in 2019 and beyond: Navigating through an uncertain tariff landscape and building an end-to-end digital supply chain of the future Marc Compagnon, Group President, Li & Fung ICR Conference

Supply chain in 2019 and beyond: Navigating through an uncertain tariff landscape and building an end-to-end digital supply chain of the future Marc Compagnon, Group President, Li & Fung ICR Conference

The Rise of the Female Economy in B2B a source of UK competitiveness

A.T. Kearney in association with the CBI The Rise of the Female Economy in B2B a source of UK competitiveness January 29 th 2014 Agenda Introduction Part 1: The six drivers: Why is the female economy important

A.T. Kearney in association with the CBI The Rise of the Female Economy in B2B a source of UK competitiveness January 29 th 2014 Agenda Introduction Part 1: The six drivers: Why is the female economy important

Accelerating toward Amer Sports CMD 2015 // Heikki Takala, President & CEO

Accelerating toward 2020 // Heikki Takala, President & CEO What we will do today Confirm that our strategies are working Present a new strategic glidepath and building blocks for acceleration toward 2020

Accelerating toward 2020 // Heikki Takala, President & CEO What we will do today Confirm that our strategies are working Present a new strategic glidepath and building blocks for acceleration toward 2020

Kasper Rorsted Carsten Knobel London Nov 16, November 16, 2012 Henkel Strategy

Henkel Strategy Kasper Rorsted Carsten Knobel London Nov 16, 2012 1 November 16, 2012 Henkel Strategy Disclaimer This information contains forward-looking statements which are based on current estimates

Henkel Strategy Kasper Rorsted Carsten Knobel London Nov 16, 2012 1 November 16, 2012 Henkel Strategy Disclaimer This information contains forward-looking statements which are based on current estimates

SMART TOURISM DESTINATIONS Current and Future Trends

SMART TOURISM DESTINATIONS Current and Future Trends CIO at Comunidad de Madrid (Nuevo Arpegio) Associate Professor at IE School of Architecture & Design (Master in Real Estate Development) Political Advisor

SMART TOURISM DESTINATIONS Current and Future Trends CIO at Comunidad de Madrid (Nuevo Arpegio) Associate Professor at IE School of Architecture & Design (Master in Real Estate Development) Political Advisor

Pricing strategy and optimization to steer traffic and profitability

Pricing strategy and optimization to steer traffic and profitability Presentation of Simon-Kucher s Restaurant Practice November 2017 david.vidal@simon-kucher.com www.simon-kucher.com Simon-Kucher & Partners

Pricing strategy and optimization to steer traffic and profitability Presentation of Simon-Kucher s Restaurant Practice November 2017 david.vidal@simon-kucher.com www.simon-kucher.com Simon-Kucher & Partners

Corporate presentation

Corporate presentation To be among the best developers of sports and fashion brands August 2012 Index 1 INTRODUCTION 2 HISTORY 3 ORGANISATION 4 BRANDS 5 CORPORATE STRATEGY 6 KNOWLEDGE CENTRE 7 CORPORATE

Corporate presentation To be among the best developers of sports and fashion brands August 2012 Index 1 INTRODUCTION 2 HISTORY 3 ORGANISATION 4 BRANDS 5 CORPORATE STRATEGY 6 KNOWLEDGE CENTRE 7 CORPORATE

[International] Source of Value-Creating Capability: Diversifying the Portfolio on a Global Basis

![[International] Source of Value-Creating Capability: Diversifying the Portfolio on a Global Basis](/thumbs/89/97829951.jpg "[International] Source of Value-Creating Capability: Diversifying the Portfolio on a Global Basis") [International] Source of Value-Creating Capability: Diversifying the Portfolio on a Global Basis Diversifying the portfolio on a global basis Progress and future strategy Tim Andree Director and Executive

[International] Source of Value-Creating Capability: Diversifying the Portfolio on a Global Basis Diversifying the portfolio on a global basis Progress and future strategy Tim Andree Director and Executive

Tumi Holdings, Inc. ICR XChange Presentation January 2014

Tumi Holdings, Inc. ICR XChange Presentation January 2014 Forward Looking Statements Disclaimer This presentation contains forward-looking statements within the meaning of the Private Securities Litigation

Tumi Holdings, Inc. ICR XChange Presentation January 2014 Forward Looking Statements Disclaimer This presentation contains forward-looking statements within the meaning of the Private Securities Litigation

H&M group capital markets day Stockholm 2018 H&M GROUP CAPITAL MARKETS DAY 2018

H&M group capital markets day Stockholm 2018 Disclaimer THIS PRESENTATION IS NOT AN OFFER OR SOLICITATION OF AN OFFER TO BUY OR SELL SECURITIES. IT IS SOLELY FOR USE AT A CAPITAL MARKETS EVENT AND IS PROVIDED

H&M group capital markets day Stockholm 2018 Disclaimer THIS PRESENTATION IS NOT AN OFFER OR SOLICITATION OF AN OFFER TO BUY OR SELL SECURITIES. IT IS SOLELY FOR USE AT A CAPITAL MARKETS EVENT AND IS PROVIDED

(R)Evolution in the Telco & Media Sector

Evolution in the Telco & Media Sector") 15. konference Telekomunikacije (R)Evolution in the Telco & Media Sector Future challenges - Extract November 2014 Marko Derča This document is exclusively intended for selected client employees. Distribution,

15. konference Telekomunikacije (R)Evolution in the Telco & Media Sector Future challenges - Extract November 2014 Marko Derča This document is exclusively intended for selected client employees. Distribution,

TXT e-solutions. Corporate Presentation March 2015

TXT e-solutions Corporate Presentation March 2015 2014: Another year of Growth Revenues: 55.9 m (+6.3%), 57% from Int l Operations EBIT: 5.5 m (+10%) Cash Flow from Op. 9.3% of Revenues NFP: 8.5m (+ Treasury

TXT e-solutions Corporate Presentation March 2015 2014: Another year of Growth Revenues: 55.9 m (+6.3%), 57% from Int l Operations EBIT: 5.5 m (+10%) Cash Flow from Op. 9.3% of Revenues NFP: 8.5m (+ Treasury

The glittering power of cities for luxury growth

SEPTEMBER 2014 The glittering power of cities for luxury growth Aimee Kim, Nathalie Remy, and Jennifer Schmidt The global economy is experiencing an unprecedented shift toward emerging-market cities. Here

SEPTEMBER 2014 The glittering power of cities for luxury growth Aimee Kim, Nathalie Remy, and Jennifer Schmidt The global economy is experiencing an unprecedented shift toward emerging-market cities. Here

10 Steps. to Achieve Virtual Integration. A guide to building a bond of game-changing collaboration

10 Steps to Achieve Virtual Integration A guide to building a bond of game-changing collaboration Capturing the power of integration without a merger Virtual integration Manufacturer Benefits Jointly pursue

10 Steps to Achieve Virtual Integration A guide to building a bond of game-changing collaboration Capturing the power of integration without a merger Virtual integration Manufacturer Benefits Jointly pursue

AUSTRALIA SUMMER INTERN PROGRAM STREAMS

AUSTRALIA SUMMER INTERN PROGRAM STREAMS Explore your options in Australia Before you apply for the ANZ Australia Summer Intern Program, you ll need to work out what part of our business best suits your

AUSTRALIA SUMMER INTERN PROGRAM STREAMS Explore your options in Australia Before you apply for the ANZ Australia Summer Intern Program, you ll need to work out what part of our business best suits your

Macau International Airport Advertising. Media Kit

Macau International Airport Advertising Media Kit JCDecaux Transport July 2009 JCDecaux Group Worldwide Outdoor Experts Leaders in Outdoor Advertising 1 in Asia-Pacific in Outdoor Media 1 in China in Outdoor

Macau International Airport Advertising Media Kit JCDecaux Transport July 2009 JCDecaux Group Worldwide Outdoor Experts Leaders in Outdoor Advertising 1 in Asia-Pacific in Outdoor Media 1 in China in Outdoor

Q EARNINGS CONFERENCE CALL PREPARED REMARKS AUGUST 16, 2018

Q2 2018 EARNINGS CONFERENCE CALL PREPARED REMARKS AUGUST 16, 2018 BLAKE NORDSTROM CO-PRESIDENT Good afternoon, everyone. Many of you joined us for our Investor Day last month. We appreciate the opportunity

Q2 2018 EARNINGS CONFERENCE CALL PREPARED REMARKS AUGUST 16, 2018 BLAKE NORDSTROM CO-PRESIDENT Good afternoon, everyone. Many of you joined us for our Investor Day last month. We appreciate the opportunity

Welcome to the 2012 update

Welcome to the 2012 update 1 About the programme 2 Why trends? Don t explain the past, predict the future Stan Sthanunathan VP Marketing Strategy & Insights, The Coca Cola Company In his AdMap article

Welcome to the 2012 update 1 About the programme 2 Why trends? Don t explain the past, predict the future Stan Sthanunathan VP Marketing Strategy & Insights, The Coca Cola Company In his AdMap article

Ross Stores, Inc. Investor Overview November 2017

Ross Stores, Inc. Investor Overview Disclosure of Risk Factors Forward-Looking Statements: This presentation contains forward-looking statements regarding expected sales, earnings levels, and other financial

Ross Stores, Inc. Investor Overview Disclosure of Risk Factors Forward-Looking Statements: This presentation contains forward-looking statements regarding expected sales, earnings levels, and other financial

Staying on the Leading Edge

Human Resources Staying on the Leading Edge Five important qualities for aspiring chief human resources officers So you want to be a CHRO. That s an admirable goal, but keep in mind that the responsibilities

Human Resources Staying on the Leading Edge Five important qualities for aspiring chief human resources officers So you want to be a CHRO. That s an admirable goal, but keep in mind that the responsibilities

We help organisations. work. by transforming strategy into reality

We help organisations work by transforming strategy into reality 2 Helping organisations work Hay Group is a global management consulting firm that works with leaders to transform strategy into reality

We help organisations work by transforming strategy into reality 2 Helping organisations work Hay Group is a global management consulting firm that works with leaders to transform strategy into reality

The Emerging Markets Acceleration Program and Globalization Readiness Index. Capturing Breakthrough Growth in Emerging Markets

The Emerging Markets Acceleration Program and Globalization Readiness Index Capturing Breakthrough Growth in Emerging Markets The Boston Consulting Group (BCG) is a global management consulting firm and

The Emerging Markets Acceleration Program and Globalization Readiness Index Capturing Breakthrough Growth in Emerging Markets The Boston Consulting Group (BCG) is a global management consulting firm and

MICHAEL KORS JOHN IDOL, CHAIRMAN & CEO TOM EDWARDS, CFO & COO

MICHAEL KORS JOHN IDOL, CHAIRMAN & CEO TOM EDWARDS, CFO & COO FORWARD LOOKING STATEMENTS This presentation contains forward-looking statements. You should not place undue reliance on such statements because

MICHAEL KORS JOHN IDOL, CHAIRMAN & CEO TOM EDWARDS, CFO & COO FORWARD LOOKING STATEMENTS This presentation contains forward-looking statements. You should not place undue reliance on such statements because

TODAY AGENDA. Results Highlights 2009 Key Achievements Financial Highlights Business and Investment Plan Update Q&A

Important notice The information contained in this presentation is for information purposes only and does not constitute an offer or invitation to sell or the solicitation of an offer or invitation to

Important notice The information contained in this presentation is for information purposes only and does not constitute an offer or invitation to sell or the solicitation of an offer or invitation to

From the Back Office to Strategic Thought Leadership

From the Back Office to Strategic Thought Leadership Driving Organizational Value with Knowledge Management APQC Houston, May 13 th, 2011 Helen Clegg Hugo Evans [Herding Cats Video] A.T. Kearney xx/mm.yyyy/00000

From the Back Office to Strategic Thought Leadership Driving Organizational Value with Knowledge Management APQC Houston, May 13 th, 2011 Helen Clegg Hugo Evans [Herding Cats Video] A.T. Kearney xx/mm.yyyy/00000

Opportunities for Action in Consumer Markets. Myths and Realities of On-Line Retailing

Opportunities for Action in Consumer Markets Myths and Realities of On-Line Retailing Myths and Realities of On-Line Retailing Business success is grounded in the ability to understand where the economy

Opportunities for Action in Consumer Markets Myths and Realities of On-Line Retailing Myths and Realities of On-Line Retailing Business success is grounded in the ability to understand where the economy

SEB Nordic Seminar January 8, 2016, Copenhagen

SEB Nordic Seminar 2016 January 8, 2016, Copenhagen The Thule Group Vision Active Life, Simplified. Slide 2 We are a Global Premium Branded Sports&Outdoor Company Outdoor&Bags Region Americas 34% Specialty

SEB Nordic Seminar 2016 January 8, 2016, Copenhagen The Thule Group Vision Active Life, Simplified. Slide 2 We are a Global Premium Branded Sports&Outdoor Company Outdoor&Bags Region Americas 34% Specialty

Striving for Excellence Investor Presentation December 2011

Striving for Excellence Investor Presentation December 2011 Contents Introduction Striving for excellence Our financial perspective 2 2 One of the Top 5 Largest Sports and Fashion Companies in the North

Striving for Excellence Investor Presentation December 2011 Contents Introduction Striving for excellence Our financial perspective 2 2 One of the Top 5 Largest Sports and Fashion Companies in the North

DAX 30 Supervisory Board Study 2018

DAX 30 Supervisory Board Study 2018 2 Key insights from this year s analysis Super election year 2018 : 35% of seats were up for election 167 continuing mandates 47 re-elections 47 167 42 42 newly elected

DAX 30 Supervisory Board Study 2018 2 Key insights from this year s analysis Super election year 2018 : 35% of seats were up for election 167 continuing mandates 47 re-elections 47 167 42 42 newly elected

ARCADIS AUTOMOTIVE SECTOR OVERVIEW

ARCADIS AUTOMOTIVE SECTOR OVERVIEW April 21, 2017 Optimising productivity & efficiency through facility design and operational readiness Arcadis overview Leading global natural and built asset design &

ARCADIS AUTOMOTIVE SECTOR OVERVIEW April 21, 2017 Optimising productivity & efficiency through facility design and operational readiness Arcadis overview Leading global natural and built asset design &

Cargo Sales & Service Presentation. Air Logistics Group

Cargo Sales & Service Presentation Air Logistics Group Air Logistics Group Introduction Introducing Air Logistics Group IATA Approved Over $450m cargo sales 280 employees worldwide Experienced management

Cargo Sales & Service Presentation Air Logistics Group Air Logistics Group Introduction Introducing Air Logistics Group IATA Approved Over $450m cargo sales 280 employees worldwide Experienced management

Geneva European Midcap Event. December 1 st, 2016

Geneva European Midcap Event December 1 st, 2016 AGENDA 01 About Wavestone Page 3 02 Financial results Page 8 03 Building Wavestone Page 14 04 Outlook Page 18 2 / 01 About Wavestone In a world where permanent

Geneva European Midcap Event December 1 st, 2016 AGENDA 01 About Wavestone Page 3 02 Financial results Page 8 03 Building Wavestone Page 14 04 Outlook Page 18 2 / 01 About Wavestone In a world where permanent

Update of the 2020 Group Business Plan. August 3, 2018

Update of the 2020 Group Business Plan August 3, 2018 DISCLAIMER This presentation may contain forward looking statements based on current expectations and projects of the Group in relation to future events.

Update of the 2020 Group Business Plan August 3, 2018 DISCLAIMER This presentation may contain forward looking statements based on current expectations and projects of the Group in relation to future events.

VANCOUVER S GREEN ECONOMY. Presented by: Bryan Buggey

VANCOUVER S GREEN ECONOMY Presented by: Bryan Buggey VANCOUVER: Global Gateway Tokyo Beijing Seoul HELSINKI Frankfurt London VANCOUVER VANCOUVER: Natural & Cultural Competitive Advantages Fastest Growing

VANCOUVER S GREEN ECONOMY Presented by: Bryan Buggey VANCOUVER: Global Gateway Tokyo Beijing Seoul HELSINKI Frankfurt London VANCOUVER VANCOUVER: Natural & Cultural Competitive Advantages Fastest Growing

Q Business review

Q1 2018 Business review Paris, May 14 th, 2018 JCDecaux SA (Euronext Paris: DEC), the number one outdoor advertising company worldwide, published today its revenue for the three months ended March 31 st,

Q1 2018 Business review Paris, May 14 th, 2018 JCDecaux SA (Euronext Paris: DEC), the number one outdoor advertising company worldwide, published today its revenue for the three months ended March 31 st,

Small & MidCap seminar. Thursday, October 7 th 2010

BoConcept Holding A/S Small & MidCap seminar Thursday, October 7 th 2010 1 Agenda BoConcept in short Strategic focus back on profitable growth Financial developments in Q1 2010/11 Long-term targets short-term

BoConcept Holding A/S Small & MidCap seminar Thursday, October 7 th 2010 1 Agenda BoConcept in short Strategic focus back on profitable growth Financial developments in Q1 2010/11 Long-term targets short-term

Bauhaus International (Holdings) Limited (stock code: 483) FY2008/09 Interim Results December 16, 2008

Limited (stock code: 483) FY2008/09 Interim Results December 16, 2008") Bauhaus International (Holdings) Limited (stock code: 483) FY2008/09 Interim Results December 16, 2008 Agenda Financial Highlights Business Review Future Development 2 Financial Highlights Results Highlights

Bauhaus International (Holdings) Limited (stock code: 483) FY2008/09 Interim Results December 16, 2008 Agenda Financial Highlights Business Review Future Development 2 Financial Highlights Results Highlights

Strengthening the experience and embracing the shift

Strengthening the experience and embracing the shift THIS PRESENTATION IS NOT AN OFFER OR SOLICITATION OF AN OFFER TO BUY OR SELL SECURITIES. IT IS SOLELY FOR USE AT A CAPITAL MARKETS EVENT AND IS PROVIDED

Strengthening the experience and embracing the shift THIS PRESENTATION IS NOT AN OFFER OR SOLICITATION OF AN OFFER TO BUY OR SELL SECURITIES. IT IS SOLELY FOR USE AT A CAPITAL MARKETS EVENT AND IS PROVIDED

DealReader. Solar Energy. Inside this Issue Q Q Deal Volume Comparison. Recent Solar Energy Transaction Announcements

DealReader Solar Energy Q3 217 Inside this Issue Q3 217 Deal Volume Comparison Recent Solar Energy Transaction Announcements An Analysis of Global Solar Energy Trends Global Energy & Power Group Q3 217

DealReader Solar Energy Q3 217 Inside this Issue Q3 217 Deal Volume Comparison Recent Solar Energy Transaction Announcements An Analysis of Global Solar Energy Trends Global Energy & Power Group Q3 217

INVESTOR PRESENTATION FY 2007/08 17 SEPTEMBER 2008

INVESTOR PRESENTATION FY 2007/08 17 SEPTEMBER 2008 IC COMPANYS HOME OF FASHION BRANDS AGENDA > INTRODUCTION > Niels Mikkelsen, CEO > 2007/08 DEVELOPMENTS & 2008/09 GUIDANCE > Chris Bigler, CFO > DISTRIBUTION

INVESTOR PRESENTATION FY 2007/08 17 SEPTEMBER 2008 IC COMPANYS HOME OF FASHION BRANDS AGENDA > INTRODUCTION > Niels Mikkelsen, CEO > 2007/08 DEVELOPMENTS & 2008/09 GUIDANCE > Chris Bigler, CFO > DISTRIBUTION

DealReader. Solar Energy. Inside this Issue Q Q Deal Volume Comparison. Recent Solar Energy Transaction Announcements

DealReader Solar Energy Q3 216 Inside this Issue Q3 216 Deal Volume Comparison Recent Solar Energy Transaction Announcements An Analysis of Global Solar Energy Trends Renewable Energy Q3 216 Announcements

DealReader Solar Energy Q3 216 Inside this Issue Q3 216 Deal Volume Comparison Recent Solar Energy Transaction Announcements An Analysis of Global Solar Energy Trends Renewable Energy Q3 216 Announcements

Cashless Cities and Digital Payments Opportunities and Challenges in Supporting the Shift to Digital Commerce

Visa Inc. Cashless Cities and Digital Payments Opportunities and Challenges in Supporting the Shift to Digital Commerce Eduardo Perez Senior Vice President, Regional Risk Officer, Latin America and Caribbean

Visa Inc. Cashless Cities and Digital Payments Opportunities and Challenges in Supporting the Shift to Digital Commerce Eduardo Perez Senior Vice President, Regional Risk Officer, Latin America and Caribbean

Business transformation and the role of change agents

Kuwait Change Management Conference Business transformation and the role of change agents Presentation Kuwait, December 2017 Eduard Gracia Principal A.T. Kearney Every major business transformation is

Kuwait Change Management Conference Business transformation and the role of change agents Presentation Kuwait, December 2017 Eduard Gracia Principal A.T. Kearney Every major business transformation is

Investor Presentation

Investor Presentation Michael Willome, Group CEO Baader Helvea Swiss Equities Conference Content Group overview & priorities Page 3 Segment performance, sales trend & outlook Page 10 Appendix: Leadership

Investor Presentation Michael Willome, Group CEO Baader Helvea Swiss Equities Conference Content Group overview & priorities Page 3 Segment performance, sales trend & outlook Page 10 Appendix: Leadership

China Luxury Survey 2013

SIMON-KUCHER & PARTNERS Luxury Goods China Luxury Survey 2013 Changing tides: catching the next profit wave The results presented in this document cover all the brands surveyed. Brand-specific results

SIMON-KUCHER & PARTNERS Luxury Goods China Luxury Survey 2013 Changing tides: catching the next profit wave The results presented in this document cover all the brands surveyed. Brand-specific results

FORWARD LOOKING STATEMENTS

1 FORWARD LOOKING STATEMENTS Certain statements included in this presentation are "forward-looking statements" within the meaning of the federal securities laws. Forward-looking statements are made based

1 FORWARD LOOKING STATEMENTS Certain statements included in this presentation are "forward-looking statements" within the meaning of the federal securities laws. Forward-looking statements are made based

Clear Eyes Provide Boards with Better Vision. Insights into Activist Investors Approaches to Targeting Boards

Clear Eyes Provide Boards with Better Vision Insights into Activist Investors Approaches to Targeting Boards 2 Clients who are anticipating or early in the process of an activist situation, and a potential

Clear Eyes Provide Boards with Better Vision Insights into Activist Investors Approaches to Targeting Boards 2 Clients who are anticipating or early in the process of an activist situation, and a potential

2015 ANNUAL GENERAL MEETING Friday 27 th November 2015, 11am The Hilton Sydney, Level 2, Room 4, 488 George Street, Sydney

2015 ANNUAL GENERAL MEETING Friday 27 th November 2015, 11am The Hilton Sydney, Level 2, Room 4, 488 George Street, Sydney CHAIRMAN S ADDRESS At our year end results announcement in September, we highlighted

2015 ANNUAL GENERAL MEETING Friday 27 th November 2015, 11am The Hilton Sydney, Level 2, Room 4, 488 George Street, Sydney CHAIRMAN S ADDRESS At our year end results announcement in September, we highlighted

9 Must-Haves for a Successful Implementation of a Pricing Strategy

9 Must-Haves for a Successful Implementation of a Pricing Strategy Arjen Brasz Nina Hoette March 2017 www.simon-kucher.com 1 Successful Price Strategy Implementation in B2B No other lever has more impact

9 Must-Haves for a Successful Implementation of a Pricing Strategy Arjen Brasz Nina Hoette March 2017 www.simon-kucher.com 1 Successful Price Strategy Implementation in B2B No other lever has more impact

Being truly global is not just a buzzword at White &

Together we make a mark Being truly global is not just a buzzword at White & Case. Associates have the opportunity to work with a variety of clients and colleagues from around the world on a daily basis.

Together we make a mark Being truly global is not just a buzzword at White & Case. Associates have the opportunity to work with a variety of clients and colleagues from around the world on a daily basis.

Adidas Investor Day 2017: Riding the Athleisure and E-Commerce Waves

Adidas Investor Day 2017: Riding the Athleisure and E-Commerce Waves 1) In March 2015, Adidas introduced a strategic business plan named Creating the New, which defines the company s strategies and objectives

Adidas Investor Day 2017: Riding the Athleisure and E-Commerce Waves 1) In March 2015, Adidas introduced a strategic business plan named Creating the New, which defines the company s strategies and objectives

LVMH Q Revenue. 9 months 2011 revenue highlights

LVMH Q3 Revenue October 18, 9 months revenue highlights Double-digit organic revenue growth for all business groups Confirmation in Q3 of excellent trends seen since beginning of the year Sustained growth

LVMH Q3 Revenue October 18, 9 months revenue highlights Double-digit organic revenue growth for all business groups Confirmation in Q3 of excellent trends seen since beginning of the year Sustained growth

A shared global vision Helping you do business all over the world

Helping you do business all over the world Client Commitment Innovative Solutions Global Service Contents Client Commitment. Innovative Solutions. Global Service. 5 Why work with us? 6 Welcome to our world

Helping you do business all over the world Client Commitment Innovative Solutions Global Service Contents Client Commitment. Innovative Solutions. Global Service. 5 Why work with us? 6 Welcome to our world

Second Quarter Results 2018 Presentation

Second Quarter Results 2018 Presentation Metzingen, August 2, 2018 Yves Müller (Chief Financial Officer) Christian Stöhr (Head of Investor Relations) - The spoken word shall prevail Good afternoon ladies

Second Quarter Results 2018 Presentation Metzingen, August 2, 2018 Yves Müller (Chief Financial Officer) Christian Stöhr (Head of Investor Relations) - The spoken word shall prevail Good afternoon ladies

American Eagle Outfitters: Staying On Trend and Within Budget Using SAP Ariba Solutions

American Eagle Outfitters: Staying On Trend and Within Budget Using SAP Ariba Solutions From season to season, American Eagle Outfitters Inc. is focused on understanding young consumers. As the apparel

American Eagle Outfitters: Staying On Trend and Within Budget Using SAP Ariba Solutions From season to season, American Eagle Outfitters Inc. is focused on understanding young consumers. As the apparel

Fourth Quarter 2018 Investor Presentation

Fourth Quarter 2018 Investor Presentation Forward-looking statements Forward-looking statements are subject to the safe harbor provisions of the Private Securities Litigation Reform Act of 1995. These

Fourth Quarter 2018 Investor Presentation Forward-looking statements Forward-looking statements are subject to the safe harbor provisions of the Private Securities Litigation Reform Act of 1995. These

ENVIRONMENTAL PROFIT & LOSS (EP&L) 2016 GROUP RESULTS

2016 GROUP RESULTS") ENVIRONMENTAL PROFIT & LOSS (EP&L) 2016 GROUP RESULTS 02 03 WHAT IS AN EP&L? An Environmental Profit & Loss (EP&L) measures and monetises the costs and benefits generated by a company's environmental impact,

ENVIRONMENTAL PROFIT & LOSS (EP&L) 2016 GROUP RESULTS 02 03 WHAT IS AN EP&L? An Environmental Profit & Loss (EP&L) measures and monetises the costs and benefits generated by a company's environmental impact,

ISM Travel & Events. Graham Crawshaw MCIPS Director of Content June 2017

ISM Travel & Events Graham Crawshaw MCIPS Director of Content June 2017 Best in Class: What does good look like? Global Network of Procurement Professionals 10,000+ active participants 70 countries represented

ISM Travel & Events Graham Crawshaw MCIPS Director of Content June 2017 Best in Class: What does good look like? Global Network of Procurement Professionals 10,000+ active participants 70 countries represented

HUGO BOSS And Its Global Customer A 360 Approach

HUGO BOSS And Its Global Customer A 360 Approach Milan, Italy Wednesday, April 22 th 2015 HUGO BOSS Agenda 1 HUGO BOSS as a Global Retail Brand 2 Growth Strategy 2020 3 Capturing the Global Customer 4

HUGO BOSS And Its Global Customer A 360 Approach Milan, Italy Wednesday, April 22 th 2015 HUGO BOSS Agenda 1 HUGO BOSS as a Global Retail Brand 2 Growth Strategy 2020 3 Capturing the Global Customer 4

SUPPLY CHAIN MANAGEMENT

Sixth Edition Global Edition SUPPLY CHAIN MANAGEMENT STRATEGY, PLANNING, AND OPERATION Sunil Chopra Kellogg School of Management Peter Meindl Kepos Capital PEARSON Boston Columbus Indianapolis New York

Sixth Edition Global Edition SUPPLY CHAIN MANAGEMENT STRATEGY, PLANNING, AND OPERATION Sunil Chopra Kellogg School of Management Peter Meindl Kepos Capital PEARSON Boston Columbus Indianapolis New York

ITALIA INDEPENDENT GROUP AT A GLANCE

OCTOBER 2016 1 2 2 DISCLAIMER This presentation is for informational purposes only and is not intended to and does not constitute an offer to sell or the solicitation of an offer to subscribe for or buy

OCTOBER 2016 1 2 2 DISCLAIMER This presentation is for informational purposes only and is not intended to and does not constitute an offer to sell or the solicitation of an offer to subscribe for or buy

Power Pricing. Proven strategies for sustainable sales success. Beograd, 19. May Dr. Thomas Haller Managing Partner

Power Pricing Proven strategies for sustainable sales success Beograd, 19. May 2016 Dr. Thomas Haller Managing Partner Vienna office Schubertring 14/Top 5. OG 1010 Vienna, Austria Tel. +43 1 5122979 0

Power Pricing Proven strategies for sustainable sales success Beograd, 19. May 2016 Dr. Thomas Haller Managing Partner Vienna office Schubertring 14/Top 5. OG 1010 Vienna, Austria Tel. +43 1 5122979 0

INVESTOR PRESENTATION. IC Companys: Our Ambition

INVESTOR PRESENTATION IC Companys: Our Ambition FEBRUARY 2011 Contents Introduction Our ambition So far so good 2 2 One of the Top 5 Largest Fashion Companies in the North brands brands 11 Scandinavian

INVESTOR PRESENTATION IC Companys: Our Ambition FEBRUARY 2011 Contents Introduction Our ambition So far so good 2 2 One of the Top 5 Largest Fashion Companies in the North brands brands 11 Scandinavian

Putting the Wholesaler in the Driver s Seat. Best practices from the retail industry to improve profitability and gain competitive advantage

Putting the Wholesaler in the Driver s Seat Best practices from the retail industry to improve profitability and gain competitive advantage Wholesalers are more than supply chain intermediaries controlling

Putting the Wholesaler in the Driver s Seat Best practices from the retail industry to improve profitability and gain competitive advantage Wholesalers are more than supply chain intermediaries controlling

March Company Description

March 2013 Company Description Jones Lang LaSalle Global real estate services Strategic, fully integrated services for real estate owners, occupiers and investors Productivity and cost solutions for corporate

March 2013 Company Description Jones Lang LaSalle Global real estate services Strategic, fully integrated services for real estate owners, occupiers and investors Productivity and cost solutions for corporate

2014 First Quarter Update 8 May 2014

2014 First Quarter Update 8 May 2014 Overview 1Q14 sales 9%; brand sales 7% Continued weakening consumer demand in Greater China Impact of weakening currencies in SEA Economic headwinds on demand in SEA

2014 First Quarter Update 8 May 2014 Overview 1Q14 sales 9%; brand sales 7% Continued weakening consumer demand in Greater China Impact of weakening currencies in SEA Economic headwinds on demand in SEA

FY16 AGM Rob Woolley, Chair Laura McBain, CEO 19 October 2016

FY16 AGM Rob Woolley, Chair Laura McBain, CEO 19 October 2016 SHARE PRICE $ 18 16 14 12 10 8 6 4 2 0 05-Aug-14 30-Aug-14 30-Sep-14 31-Oct-14 30-Nov-14 31-Dec-14 31-Jan-15 28-Feb-15 31-Mar-15 30-Apr-15

FY16 AGM Rob Woolley, Chair Laura McBain, CEO 19 October 2016 SHARE PRICE $ 18 16 14 12 10 8 6 4 2 0 05-Aug-14 30-Aug-14 30-Sep-14 31-Oct-14 30-Nov-14 31-Dec-14 31-Jan-15 28-Feb-15 31-Mar-15 30-Apr-15

Speech Nancy McKinstry Annual General Meeting of Shareholders 2008 April 22, 2008 Okura Hotel Amsterdam

Speech Nancy McKinstry Annual General Meeting of Shareholders 2008 April 22, 2008 Okura Hotel Amsterdam Welcome and good morning. It is a pleasure to be here today to share our 2007 results and provide

Speech Nancy McKinstry Annual General Meeting of Shareholders 2008 April 22, 2008 Okura Hotel Amsterdam Welcome and good morning. It is a pleasure to be here today to share our 2007 results and provide

Drive Insight from Retail Analytic and Leverage Predictive to Change the Game. Greg Wong, Director Analytics, Greater China July 26, 2016

Drive Insight from Retail Analytic and Leverage Predictive to Change the Game Greg Wong, Director Analytics, Greater China July 26, 2016 Why Retailers Must Restructure In 2016 Rapid Internet market share

Drive Insight from Retail Analytic and Leverage Predictive to Change the Game Greg Wong, Director Analytics, Greater China July 26, 2016 Why Retailers Must Restructure In 2016 Rapid Internet market share

2Q FY2/2013 Results Presentation

2Q FY2/2013 Results Presentation October 10, 2012 J. Front Retailing Co., Ltd. OKUDA Tsutomu Chairman and CEO Five Years as J. J. Front Retailing 1 Initiatives during These 5 Years Group Vision Establishing

2Q FY2/2013 Results Presentation October 10, 2012 J. Front Retailing Co., Ltd. OKUDA Tsutomu Chairman and CEO Five Years as J. J. Front Retailing 1 Initiatives during These 5 Years Group Vision Establishing

Eureka! It s a business

Eureka! It s a business Beauty & Go PORTO BUSINESS SCHOOL Team PBS Silvia Duarte Rui Rosas Francisco Cudell Pedro Vilas Boas Challenge Analysis Recommendations Challenges How you should prioritize markets

Eureka! It s a business Beauty & Go PORTO BUSINESS SCHOOL Team PBS Silvia Duarte Rui Rosas Francisco Cudell Pedro Vilas Boas Challenge Analysis Recommendations Challenges How you should prioritize markets

Edouard Lassalle - Head of Investor Relations Good morning everyone. Welcome to Criteo's second quarter 2016 earnings call.

1 2 3 4 5 6 7 8 9 10 11 12 13 14 15 16 17 18 19 20 21 22 23 24 25 26 27 Q2 2016 Financial Results Conference Call Prepared Remarks Edouard Lassalle - Head of Investor Relations Good morning everyone. Welcome

1 2 3 4 5 6 7 8 9 10 11 12 13 14 15 16 17 18 19 20 21 22 23 24 25 26 27 Q2 2016 Financial Results Conference Call Prepared Remarks Edouard Lassalle - Head of Investor Relations Good morning everyone. Welcome

Interim Results Presentation 17 August

Interim Results Presentation 17 August BUSINESS REVIEW AND OUTLOOK BRAND + PRODUCT Cherry Chen ( 陳晨 ), Executive Director and Brand VP FULL ENHANCEMENT OF BRAND VALUE Reinforcement and emphasis of brand

Interim Results Presentation 17 August BUSINESS REVIEW AND OUTLOOK BRAND + PRODUCT Cherry Chen ( 陳晨 ), Executive Director and Brand VP FULL ENHANCEMENT OF BRAND VALUE Reinforcement and emphasis of brand

Marketing Services Industry in Hong Kong

Feb 2018 Marketing Services Industry in Hong Kong Overview Hong Kong is the marketing services capital of Asia, where a full range of services can be found. The sophistication of the market has attracted

Feb 2018 Marketing Services Industry in Hong Kong Overview Hong Kong is the marketing services capital of Asia, where a full range of services can be found. The sophistication of the market has attracted

SUPPLY CHAIN MANAGEMENT

Fifth Edition SUPPLY CHAIN MANAGEMENT STRATEGY, PLANNING^ AND OPERATION Global Edition Sunil Chopra Kellogg School of Management Peter Meindl Kepos Capital PEARSON Boston Columbus Indianapolis New York

Fifth Edition SUPPLY CHAIN MANAGEMENT STRATEGY, PLANNING^ AND OPERATION Global Edition Sunil Chopra Kellogg School of Management Peter Meindl Kepos Capital PEARSON Boston Columbus Indianapolis New York

Goldman Sachs Internet Conference Las Vegas, NV. May 21, 2008

Goldman Sachs Internet Conference Las Vegas, NV May 21, 2008 Disclaimer These presentation materials have been prepared by Gmarket Inc. ( Gmarket or the Company ) and have not been independently verified.

Goldman Sachs Internet Conference Las Vegas, NV May 21, 2008 Disclaimer These presentation materials have been prepared by Gmarket Inc. ( Gmarket or the Company ) and have not been independently verified.