FINAL REPORT ON THE AREA PLANTED TO GM MAIZE IN SOUTH AFRICA FOR THE 2007/2008 SEASON

|

|

|

- Norman Howard

- 5 years ago

- Views:

Transcription

1 FINAL REPORT ON THE AREA PLANTED TO GM MAIZE IN SOUTH AFRICA FOR THE 2007/2008 SEASON Wynand J. van der Walt, PhD FoodNCropBio tel / Pretoria, 24 July

2 FINAL REPORT ON THE AREA PLANTED TO GM MAIZE IN SOUTH AFRICA FOR THE 2007/2008 SEASON LIST OF CONTENTS 1. EXECUTIVE SUMMARY INTRODUCTION 5 3. METHODS AND APPROACHES RESULTS Global overview 6 South African overview 7 GM maize farmer profiles.. 12 SANSOR report on GM crops 13 South African added value of Bt maize. 14 Analysis of GMO permits 14 Incidents of potential stalk borer resistance to Bt 15 Regulatory developments.16 Media coverage ANNEXES Global adoption of GM crops 5.2 List of permits 5.3 Analysis of farmer benefits ACKNOWLEDGEMENTS The author wishes to extend his appreciation to the Maize Trust for having provided the funds for this survey and to all collaborators -- specifically the biotech seed companies -- for having submitted confidential data and inputs. 2

3 1. EXECUTIVE SUMMARY The study has a primary objective to survey and analyze GM (genetically modified) maize production in order to serve as a database for stakeholder parties ranging from seed suppliers to producers, silo owners, grain traders, millers, food industry, consumers, and government departments. Such information may be required for imports and exports, as well as serving local markets that may have special requirements. The survey is based on analyzing actual seed sales data provided on a confidential basis by seed companies, calculating the hectares planted according to seeding rates for different regions, and expressing GM areas in terms of percentages of total area planted as estimated by the Crop Estimates Committee. It covers analyses by GM trait separately for white and yellow maize. The survey goes through three stages: estimates based on seed orders and intention to plant, final seed sales and CEC estimated area under maize, and final analyses to reconcile seed industry inputs on seeding rates and total market estimates. Global GM crop plantings increased by 12% to reach million hectares, grown by 12 million farmers in 23 countries. An additional 29 countries have approved use of GM products for feed or food. The cumulative hectares under GM crops over 11 years stand at 690 million hectares. Approvals cover 124 genetic modifications in 23 crops. Soybean remains the major GM crop and herbicide tolerance the major trait. Farmer benefits from 1996 to 2006 totalled US$34 billion and reduced pesticide use by some MT a.i. South Africa still ranks 8 th in the world with 1.8 million hectares combined of the three crops: maize, soybeans and cotton. Total GM maize came to million hectares, million white and million yellow, with share of the total planting at 56% for total maize, 56% for white and 55% for yellow. Part of the increase was due to 9% increase in maize area over the previous season. Nevertheless, white maize increases its market share by 8% and yellow by 25%, Insect resistance accounted for 71%, herbicide tolerance for 24% and stacked traits for 5% of total GM area. Cumulatively, total GM maize area from 2000 to 2008 covered million hectares and produced a grain yield of over 15 million MT, the 10.6% average yield benefit of which was estimated at some R2 billion at farm gate prices. A rough estimate of GM maize farmers indicated that about commercial farmers plant GM maize. Less information was available on subsistence, smallholders and emergent farmers. Responses from three companies indicated that about out of of these planted GM maize or 23% of farmers. The difference between SANSOR estimates of GM seed market share and my survey was investigated and discussed with seed companies. The major reason 3

4 was identified as the former being based on seed volumes and the latter on hectares planted using seeding rates and seed counts, coupled with a possible overestimate of total market by SANSOR. Analysis of permits approved during 2007 for GMOs showed that maize permits accounted for 91% of the 379 total. GM grain imports numbered 223 permits with a total of 1.9 million MT but it does not imply that all permits were used in the volume or the time period indicated. GM seed imports were 1196 MT and exports 1509 MT. Other GM seed imports and exports were for trials, seed multiplication or contained use evaluation. An incidence of apparent resistance in stalk borer larvae to GM maize with the Bt gene was reported by the ARC-GCI. This indicates the need for a stronger effort in monitoring fields and follow-up research to ascertain resistance and application of measures to counteract or delay such resistance mechanisms to develop. Regulatory developments include creation of a Directorate for Biosafety in the Department of Agriculture which will include administering the GMO Act, appointment of a Director of Biosafety, appointment of a new GMO Registrar, creation of a section within the SA National Biodiversity Institute to monitor GMO impact on biodiversity, and discussions in the GMO Executive Council on handling stacked gene applications and applications for grain imports that may contain unapproved genetic events. A media release on GM crop adoption globally and in South Africa received wide coverage locally and internationally. Finally, some 4.5 million hectares of GM maize were grown over the past nine years, all without any substantiated incidence of damage to human or animal health, or to the environment. This is evidence of a biosafety framework that helps to ensure assessment of safety of GM products prior to approval for commercial release, and compliance by biotech stakeholders with regulations. 4

5 2. INTRODUCTION The objective of the study was to survey and analyze adoption of genetically modified (GM) maize by producers in South Africa in order to establish an updated database on GM plantings, available to maize industry stakeholders as a source of information. This would preclude confusion that may result from conflicting data being distributed by various parties. It would also enable traders in maize grain and products to convey information to trading partners as may be required by customers domestically and in other countries, and to comply with the Cartagena Protocol on Biosafety. Beneficiaries of this information include the following parties and their clients or colleagues: AgriSA, GrainSA, grain traders, millers, silo industry, industrial processors, food and animal feed manufacturers and their clients, seed industry, CEC, SAGIS, SAGL, National Department of Agriculture, ARC, the GMO Secretariat, Executive Council, Advisory Committee, and the media. Data in this report are based on reliable confidential statistics provided by biotechnology seed companies and cover hectares of GM maize planted and percentage of market with a breakdown per trait -- insect resistant (IR) or herbicide tolerant (HT) and stacked genes (IR/HR) -- shown separately for white and yellow maize, as well as historic data since 2000/2001 in order to highlight trends. An analysis of permits granted during 2007 is also included as maize seed and grain imports and exports that are GM or may contain material of GM origin have trade relevance for the industry. Statistics are based on commercial maize plantings as official data on subsistence farming are at best unreliable guesstimates and as most planting is based on farmsaved seed and the crops are consumed on-farm. Some information is included on sale of GM maize seed to the smallholder farming sector. 3. METHODOLOGY AND APPROACH USED IN SURVEY The survey goes through three stages so that information is refined with latest information available at each stage. Seed companies provide a breakdown of seed sales per GM trait (Bt insect resistance, glyphosate herbicide tolerance, and stacked genes for both traits), per white and yellow maize, and per seed density used (6-8 kg/ha for drier Western and Northern regions, kg/ha for Eastern and South-Eastern regions, and kg/ha for irrigation farming. Seed is mostly sold on seed count basis in pockets containing or seeds and these are converted to kg. In fact, seed count gives a more accurate picture of area planted to a pocket than kg as 5

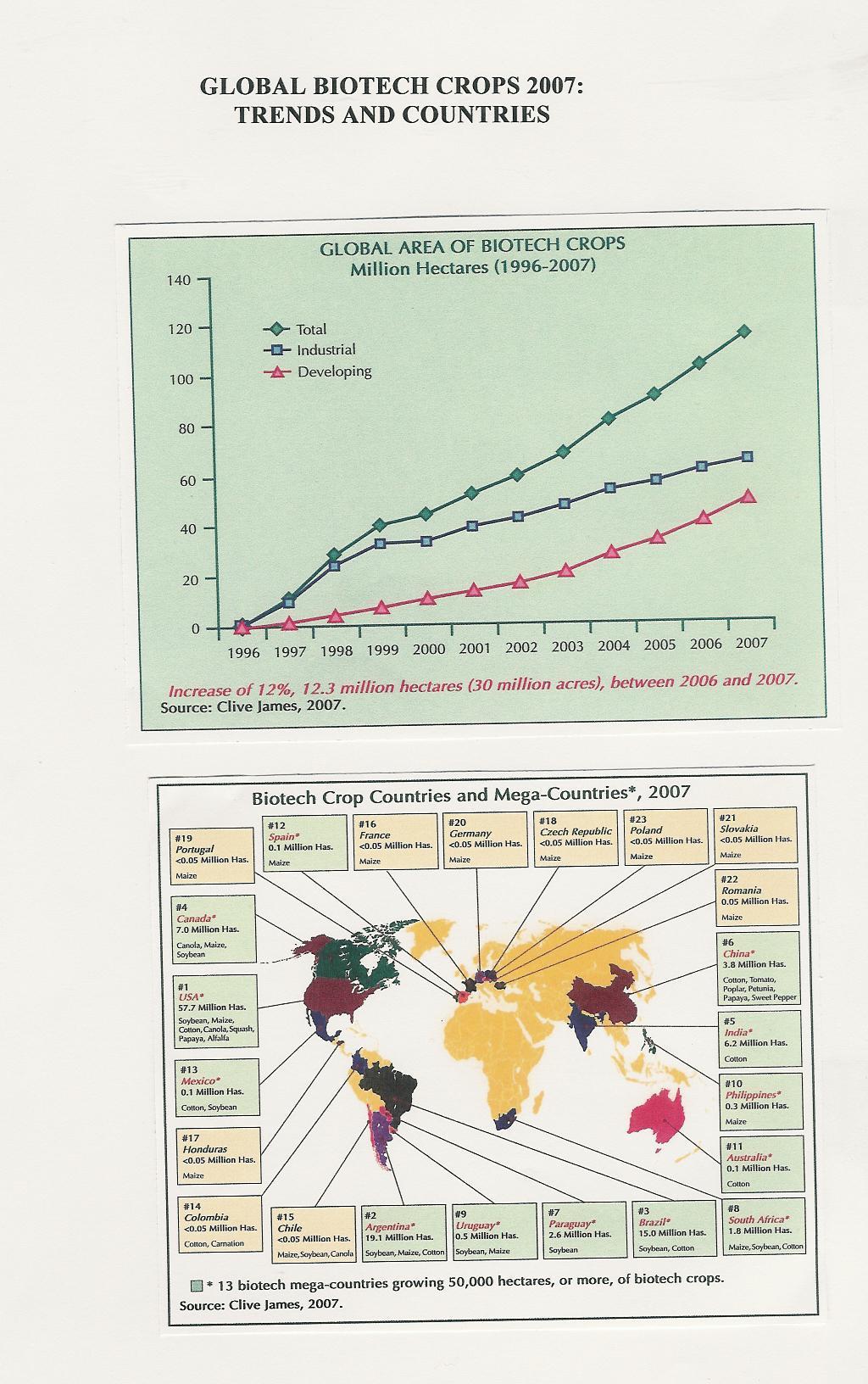

6 the seeds per kg vary from to 3 500, depending upon seed size and shape. It was not possible to survey areas planted to GM maize per CEC region as each seed company has its own sales regions based on its analysis of agroecological parameters and its marketing infrastructure, and they do not record sales per CEC provincial regions. It is interesting that CEC inludes the Loskop scheme with Limpopo and not with Mpumalanga. The first estimate in early November 2007 of GM maize plantings was based on discussions and meetings with six seed companies (Pannar, Pioneer, Monsanto, Link Seed, Syngenta, Agricol, and Afgri) that are marketing GM maize seeds. The total maize area planted (2.8 million hectares) was derived from an average of expectations expressed by seed companies from seed orders and was higher than the Crop Estimates Committee report available at that time on intention to plant maize. In fact, this estimate matched the CEC s April report. The second estimate derived in April-May 2008 made use of confidential company audited seed sales information and the CEC April and May reports on maize area planted and crop yields. A third analysis in May-June was considered necessary in view of the discrepancy between analyses contained in this report and the information contained in the SANSOR annual report. Personal discussions were held with all GM seed companies on seeding rates for all nine CEC regions and for irrigation farming systems, commercial and smallholder maize areas, as well as seed count per kg so as to identify possible reasons for this discrepancy. This round extended into an attempt to ascertain irrigation area planted to maize from which one could estimate GM market share, and into a first attempt at surveying subsistence and emergent maize farming to estimate total farmers involved and GM market share. Time was also spent on informal discussions with officials and visiting the Department of Agriculture website to ascertain updated information on regulatory matters. 4.1 Global overview 4. RESULTS Annual overviews are compiled by ISAAA (the International Service for the Acquisition of Agri-Biotech Applications), an international non-profit organization. These overviews are released by way of international media conferences and published as Briefs. Other updates are printed in the form of small brochures and updates provided in the form of a weekly e- newsletter. Surveys and studies are executed by independent groups in various countries. Salient points from the 2007 Brief 37 (C. James, 2007, 6

7 Brief 37: Global Status of Commercialized Biotech/GM Crops:2007, and available in summary form on are as follows: Global planting of GM crops increased by 12% to reach million ha in These crops were planted by 12 million farmers in 23 countries, 11 million being smallholder farmers. Cumulative area under GM crops since 1996 now amounts to 690 million ha. For 2007, the USA leads with 57.7 million ha, followed by Argentina 19.1, Brazil 15.0, Canada 7.0, India 6.2, China 3.8, Paraguay 2.6, and South Africa with 1.8 million ha. The remaining 15 countries are Uruguay, Philippines, Australia, Spain, Mexico, Colombia, Chile, France, Honduras, Czech Republic, Portugal, Germany, Slovakia, Romania, and Poland. In addition to the 23 countries growing GM crops, another 29 have approved biotech crops for import as food and feed, and /or for trial planting. These 615 approvals involve 124 genetic modifications in 23 crops. Soybean remains the major GM crop (58.6 million ha), followed by maize (35.2 million ha, cotton (15 million ha) and canola (5.5 million ha). The major trait is herbicide tolerance at 63% share of total GM, followed by stacked traits at 19% and insect resistance at 18%. Cumulative farmer benefits for were US$34 billion, and pesticide savings amounted to MT active ingredients. Most growth in adoption now comes from developing countries, driven by Bt cotton in China and India, and soybeans in Brazil. The global trends are shown in Annex South African overview The final estimate of genetically modified maize (GM) plantings is based on discussions and meetings with seed companies (Pannar, Pioneer, Monsanto, Link Seed, Syngenta, Agricol, and Afgri) that are marketing GM maize seeds. The total maize area planted (2.799 million hectares) is based on the most recent Crop Estimates Committee report available at the time of drafting of this final report. 7

8 South Africa retained its 8 th ranking on the ISAAA list of biotech crop countries with 1.8 million ha planted in Genetic modifications approved for commercial release are: 1997/8: Bt insect resistance Mon 810, Monsanto 2002: RR glyphosate tolerance NK 603, Monsanto 2003: Bt 11 insect resistance + herbicide tolerance, Syngenta 2007: Bt insect resistance + glyphosate tolerance, Mon810 x NK603, Monsanto. Seed companies are in the process of testing hybrids for water use efficiencies. It is of special interest to note that the past season saw the first field trials of a GM drought tolerant maize strain Sometimes delayed adoption of such traits is due to having the beneficial genes in the appropriate hybrid adapted to South African conditions and to bulking up of seed. The impact of the stacked genes for insect resistance and herbicide tolerance will only become visible as from 2009 to 2010 when seed production is sufficient to replace single gene hybrids. This impact is expected to be substantial. As regards the survey and analyses of results, it should be explained that the reports to the Maize Trust comprise an interim report based on the first round of the survey, followed by an updated final report that uses final seed sales data. The initial results are used in the ISAAA global report that is released in January-February each year and these results are also provided to the International Grains Council in a cryptic format, as requested by the Department of Agriculture. The year-on-year comparisons in the ISAAA reports are based on first survey data, while those in the final report to the Maize Trust on the final survey data. Historically, the total GM hectares have changed very little from the first to the final survey: in 2006/7 it was 2% higher, and in 2007/8 it was 1% lower in the final report. However, the ratio of GM white and yellow maize adoption, and the shares of the traits differed by more than 2% each year; hence, the differences in percentages of changes. The analyses expressed as percentages GM, are based of total commercial plantings published by the CEC, as statistics on subsistence and smallholder crops are unreliable. It has already become evident that GM maize will be the mainstream product and conventional and organic production will remain secondary segments. The first survey, based on seed sales estimates in October- November, indicated that the GM share had moved up by 33% to million ha (57% of total), comprising 1.04 million white (62% of white) and million yellow (51% of yellow), as contained in the interim report. 8

9 These figures were submitted to the ISAAA global report and to the IGC via the Department of Agriculture. The second survey in May, excluding data on smallholder farmers, required a few adjustments due to slightly lower white GM seed sales and more yellow sales. GM maize for the 2007/8 season stood at million ha (56% of total), comprising million ha for white (35% of total maize and 56% of white) and million ha for yellow (21% of total maize and 55% of yellow). The major trait is Bt insect resistance being 71% per cent of total GM maize, and herbicide tolerance being 24% of total. Stacked traits (insect resistance plus herbicide tolerance) was approved for commercial sales in February 2007 and on ha commanded a 5% share of GM ha. The latter trend is expected to grow substantially at the expense of single traits, provided that the combined traits are inserted in locally adapted varieties and sufficient seed is available. More details are contained in Tables 1 and 2 below and the trend graph is contained on p. 12 in the text. TABLE 1 TOTAL GM MAIZE CHANGES 2007/8 OVER 2006/7 CLASS 2006/7 HA x /8 HA x1000 CHANGE 2006/7 % MKT SHARE 2007/8 % MKT SHARE CHANGE WHITE % % YELLOW % % TOTAL % % SUMMARY: GM white maize hectares increased by 15%, yellow maize by 44% and total maize by 24% from 2006/7 to 2007/8 GM white maize market share increased by 8%, yellow maize by 25% and total maize by 14% from 2006/7 to 2007/8 NOTE: Changes are based on straight percentages for white and yellow, but weighted on white : yellow market shares for total maize changes. TABLE 2: GM TRAIT MARKET SHARE CHANGES 2007/8 OVER 2006/7 TRAIT 2006/7 HA X 2007/8 HA X CHANGE 2006/7 % GM 2007/8 % GM CHANGE 9

10 SHARE SHARE Bt IR % % HT % % Bt+HT SUMMARY: Bt insect resistant maize hectares increased by 11% and herbicide tolerant hectares by 40%. Stacked traits (Bt IR+ HT) sales commenced in 2007 and achieved hectares. Bt maize market share decreased by 6% from 77% to 71% of total GM maize grown, while HT maize increased by 3% to 24% share. Stacked traits (Bt + HT) achieved 5% of total GM maize market at the expense of Bt maize. Cumulatively, some million hectares of GM maize have been planted over the past nine seasons, constituting million white ha and million yellow ha. The summarized data over nine years, and a graph, are shown below. Area planted to GM white maize (IR = Bt insect resistant, HT =herbicide tolerant) 2000: nil 2001: nil 2002: ha out of 1.7 mil. ha. = 0.4% of white maize area (all IR) 2003: ha out of 2.1 mil.ha. = 2.9% (all IR) 2004: ha out of 1.8 mil.ha = 8.0% (all IR, HT negligible) 2005: ha out of 1.8 mil.ha = 8.2% ( IR = 7.9% HT= 0.3%) 2006: ha out of 1.0 mil.ha = 28.8% ( IR = 22.8% HT = 6.0%) 2007: ha out of mil. ha = 52.3% ( IR = 43.8% HT = 8.5%) 2008: ha out of mill ha = 56% of total white ( IR =40% HT = 13% IR/HT =3%) Cumulative area planted to GM white maize over nine years = mill ha Area planted to GM yellow maize (IR = Bt insect resistance, HT = herbicide tolerant) 10

11 2000: ha 2001: ha 2002: ha out of 1.1 mil.ha = 14.5% of yellow maize area (all IR) 2003: ha out of 0.9 mil.ha = 19.5% (all IR) 2004: ha out of 1.0 mil.ha = 19.7% (all IR, negligible HT) 2005: ha out of 1.1 mil.ha = 23.9% ( IR= 22.6% HT = 1.3%) 2006: ha out of 0.6 mil.ha = 29.0% ( IR= 17.8% HT = 11.3%) 2007: ha out of mil.ha = 44.0% ( IR= 35.5% HT = 12.5%) 2008: ha out of 1.06 mill ha = 55% of total yellow ( IR = 38% HT = 15% IR/HT = 2%) Cumulative GM yellow maize area over nine years = mil.ha Total GM maize area planted over nine years (*harvest seasons) 2000: ha 2001: ha 2002: ha 2003: ha 2004: ha 2005: ha 2006: ha 2007: mil. ha 2008: mill ha Cumulative GM maize area planted over six years = mil.ha. 11

12 4.3 Farmer profiles As there are no official data on maize farmer numbers available and not all maize farmers produce maize every season, an estimation of farmer numbers is a bit of a guess. Seed companies agree with a figure of between and large-scale commercial farmers. While some farmers plant only GM maize (discounting the mandatory conventional refuge areas) and others plant both GM and conventional, it is estimated that the between and commercial farmers plant GM maize. The number of smallholder maize farmers was more difficult to establish as there were no clear data on numbers of subsistence, smallholder and emergent farmers in South Africa and as seed companies do not maintain accurate records on each farmer who procure conventional or GM seed. Some seed is sold by distributors, some seed is supplied to municipalities, projects, or agri-development groups and the end user is not identified, and some buyers share seed with neighbours or members of their farmers association. Company information was requested from GM seed suppliers: three responded and another indicated that they serve minimal smallholders directly but some direct sales may end up with communities or small-scale farmers. The data obtained were discussed with the three respondents (only one provided a breakdown by seed pocket size) who provided information on conventional and GM volumes, and analyzed on the following assumptions: Buyers of 2, 5. and 10 kg pockets are household and subsistence farmers 12

13 Those that buy pockets of 25 kg (or , or seed count) are smallholders and emergent farmers, and buy 1.3 pockets on average to plant 3 ha. Buyers of yellow maize seed are mostly emergent commercial farmers and where basic services provided by the seed supplier include ploughing, crop management, mentorship and harvesting, and the average emergent commercial farm size is estimated at 4 ha. White maize seed sales to farming areas where most of the maize is consumed or marketed fresh, with an average purchase of 25kg of seed. Based on these assumptions it was estimated that a total of farmers were reached by the three companies, of whom planted GM maize or 23% of total. Total sales amounted to MT of which 337 MT was GM. In terms of surface area, GM covered approximately Ha. This analysis is based on respondents data and there may be much more information from other seed companies, development groups and agribusinesses. The analysis is based in respondents data and information from other companies will contribute to a more complete picture. The majority of smallholder maize farmers surveyed by the University of Pretoria in KZN who plant a GM variety or varieties (albeit Bt, RR or Stacked) also plant other maize seed including the conventional isoline, other conventional hybrids from other seed companies or the same, some open pollinated varieties and almost everyone still planted a small plot to traditional varieties, with the latter usually earmarked for chicken feed. 4.4 SANSOR GM crop data The 2007/2008 SANSOR annual report indicated that the domestic maize seed market for the 2007 planting season was MT and the GM share was 42%. The size of this difference with analyses done in collaboration with seed companies, based on their audited sales data, was larger than in the past and an investigation was considered necessary. Individual discussions, therefore, were held with representatives of all biotech seed companies and the reasons for the differences were identified as follows: My analyses have historically been based only on adoption of GM maize by the commercial sector as reliable data on area planted and seed used by subsistence and smallholder farmers have not been available to date. The latter sector contributes only 2.5% of the national crop. My data are based on area planted while that from SANSOR on seed sales. The area was derived from plant density and seed count for the different agro-ecological regions, and not on seed volumes alone. 13

14 These scenarios for the CEC nine provinces were discussed with seed companies and all agreed that the seed count and planting densities were correct. SANSOR data may contain an under-estimate of GM as some biotech company financial year ends in December while my data cover the season to end February. The Northern Cape irrigation and Eastern Mpumulanga regions have some areas devoted to non-gm to serve local special industrial or export markets. It should be noted that the Free State and North- West provinces, having low seeding rates of 6-8 kg/ha, account for 75% of total white area, yielding 68% of total white maize, and for yellow 61% and 49%, respectively. All seed companies agreed that the total commercial seed market is about MT, showing a national average seeding rate of just below 10 kg/ha with a minor variation between estimates. Not all of the ha under smallholder planting (CEC estimate, June 2008) is served by the formal sector. The general estimate is about 50%. Thus, the SANSOR estimate of the domestic seed market is too high and may contain some elements of double sales and sales that move across border. Taking the above variables into account, seed companies agreed that my calculations still present the best estimate to date. 4.5 South Africa added value of Bt maize The total volume of GM maize produced from harvest year 2000 to 2008 amounts to over 15.0 million MT, 7.4 being white and 7.6 yellow. Comparisons of added seed cost versus benefit of herbicide tolerance benefits showed that the net effect over two years, two regions and irrigation and dryland, is about the same. Therefore, only the benefit of Bt insect resistance was analyzed (single Bt and combined Bt/HT), using an average dry-land yield increase of 10.6% (University of Pretoria studies). Average farm gate prices were obtained from official statistics. The commercial value is estimated at almost R20 billion, and the added value of 10.6% yield benefit estimated at about R2 billion over these nine years. The analysis is contained in the Annex Analysis of GMO maize permits Some 379 permits were approved during the calendar year January to December As regards imports of commodity maize, the information summarized below will not harmonize with that of SAGIS; firstly, as a 14

15 permit granted does not imply that the permit will be used for imports or in the quantities or specified time requested; secondly, as the permits apply to the date approved in the calendar year and not for execution in a marketing period. The different types of permits and approvals are contained in Annex 5.3 The permit analysis is summarized as follows: Maize accounted for 91% or 345 permits out of 379 issued GM maize grain imports numbered 223 involving 1.9 million MT, all grain coming from Argentina No permits were issued for GM grain exports. 70 Permits applied for seed imports; 11 amounting to 1196 MT for sale as planting seed estimated at a cost of R40 million to make up shortfalls in local supplies, and another 59 for small shipments intended for breeding, multiplication, trials, and re-export. Seed export permits covered 7 permits for 1509 MT commercial seed at an estimated value of R55 million. The balance of GM seed exports were small samples for breeding, multiplication, trials, or contained use research. 4.7 Incidence of potential stalk borer resistance to Bt maize It is inevitable that some degree of resistance to Bt genes may develop, as has been the case with pest and disease resistance developed through conventional breeding. Likewise, the case of pest resistance to chemical insecticides pyrethrum is at present fairly ineffective and pest resistance to some 500 chemicals have been recorded. However, the Bt bio-pesticide as spray and inserted gene has had a unique track record of persistent efficacy over 60 years. Only one substantiated case is on record (although experts do not always agree), namely that of diamond black moth in covered cabbage production sprayed with high doses of Bt toxin. Efficacy of the Bt gene has never been 100% but estimated at about 97%. Counteracting potential resistance has been based on using different Bt genes individually or stacked, and mandatory planting of conventional maize adjacent to Bt fields to serve as refugia. The identification by Prof Koos van Rensburg, ARC-GCI, of resistant larvae in isolated cases of Bt maize plantings under irrigation in the Christiana area has indicated that resistance could break down under certain cultural practices. This investigation is being continued in collaboration with biotech seed companies. 15

16 4.8 Regulatory developments The GMO Act is comprehensive and its scope covers all genetic modification technologies, as defined, on all organisms, from registration of facilities where GMO work is done to application on-farm. Approval for GMO activities is based on a permit system. The extent of these permits and policies is contained in Annex 5.3. Salient points of new regulatory developments can be summarized as follows: The GMO Act 15 of 1997 has been amended in 2007 to include improved wording in several definitions, addition of the Department of Arts & Culture and the Department of Water Affairs & Forestry in the composition of the Executive Council; to specify two members of the Advisory Committee (one an ecologist and one a human and animal health expert); to include wording to ensure compliance with the Cartagena Protocol on Biosafety; inserting more details pertaining to environmental safety; and some general improvements of texts. The President has signed approval of the Bill into an Amended Act. GMO Regulations have been amended as a draft to harmonize with the Amended Act and have been widely circulated for comments. Several amendments have been pointed out as being problematic and my inputs have been copied to the Maize Trust. The Act will enter into force once these regulations have been approved and only then will representatives of the Departments of Arts & Culture and Water Affairs & Forestry be appointed to the Executive Council. Ms Chantal Arendse has been appointed as Director: Biosafety in the Directorate of Plant Production, Health and Quality, responsible for the GMO Act (after the responsibility had been moved from the Directorate of Genetic Resources). Ms Gillian Christies was appointed in May as Registrar of GMOs. The S A National Biodiversity Institute (SANBI, comprising Kirstenbosch Botanical Gardens and the Botanical Research Institute) has been charged with various functions under the Biodiversity Act and Ms Tsepang Makholela has been appointed to manage impact of GMOs on biodiversity. Part of their mandate is to develop post-release monitoring protocols. Personal meetings have been held with these three officials. The issue of evaluating and regulating GMOs with stacked genes was delegated by the Executive Council to the Department of Environment & Tourism to develop a draft policy document on ecological risk assessment for staked genes. It is not clear why this assignment was not given to the scientific Advisory Committee. To date DEAT has not yet produced this document. It remains also unclear why stacked genes should be subjected 16

17 to other assessments when the individual genes have already passed through biosafety approval. Uncertainties on commodity clearance for genetic events not yet approved for commercial release in South Africa has led to a temporary moratorium on such maize grain imports. To date the maize grain industry, in terms of the planned contingency grain plan, has not yet submitted documents on the plan. It should be noted that Argentina has recently approved a new maize modification: TC1507 x NK603 that combines tolerance to glufosinate-ammonium with resistance to Diatraea sugarcane borer and to Spodoptera fall army worm, plus moderate resistance to Heliothis earworm. The Department of Trade& Industry is aware of practical and logistical constraints, apart from adequate oversight by the Department of Agriculture, when such grain imports are to be milled before distribution. The GMO Executive Council has entered into discussions with the Medicines Control Council in the Department of Health on the process for approval of GM vaccines (such as HIV/AIDS and TB) and pharmaceuticals. To date, the MCC made these decisions on its own, contrary to provisions in the GMO Act. The Consumer Rights Bill drafted by the Department Trade & Industry, made provision for mandatory labeling of all foods and their ingredients/derivatives from GM plants. The third revised draft excludes this paragraph but it seems that anti-gm lobbyists, supported by some parliamentarians, are pushing for comprehensive GM labeling. Members of the GMO Executive Council have taken note of the immense costs of compliance and verification of such legislation. Lack of food and feed industries to speak up and to support the identity preservation systems for non-gm products leaves the lobby field open to activism. 4.9 Media coverage ISAAA media releases include simultaneous media conferences held in February 2008 in some 20 major cities globally, a weekly crop biotech update newsletter distributed to over recipients, and many interviews held by their chairman and regional representatives. In all, several hundred million persons were reached in this way. South Africa featured prominently in both the executive summary and in the complete report. A media conference arranged in Pretoria by Hans Lombard PR in collaboration with myself, tied in with the global release of the ISAAA Brief 37 on global status of GM crops. Mr Lourie Bosman, AgriSA President, was guest speaker and Ms Hanfie Neuhoff of the SA Women s Agricultural Union gave a presentation as second speaker. The key South African GM crop data were combined with global data. Media coverage in South Africa amounted to: 17

18 13 newspapers, 5 magazines, 4 radio stations and one hour on RSG, plus news items on web sites, calculated at having reached at least 5 million listeners and readers. Presentations were also given at the bi-annual SA Plant Breeders Symposium in March, the FANRPAN Stakeholders Meeting in June and other events while other articles appeared in printed media at a later stage. No further media releases are planned ======================================================== Report submitted by Wynand J. van der Walt, FoodNCropBio, Pretoria, 16 April 2007 wynandjvdw@telkomsa.net Tel / End.. 18

19 19

20 20

21 ANNEX 5.2 Calculation of the value of Bt maize yield impact Harvest year Total hectares ('1000) Production ('1000 tons) % Bt Bt crop ('1000 tons) Price / ton Bt crop value ('1000 Rand) Bt benefit ('1000 Rands) WHITE MAIZE ,149 6, ,562 4,260-1, ,722 5, ,540 31,207 2, ,232 6, , ,352 17, ,842 5, ,201 36, ,700 6, ,053 43, ,033 4, ,206 1,422 1,714, , ,625 4, ,890 1,799 3,400, , ,737 6, ,950 1,810 5,339, ,782 SUB-TOTAL 7,252 1,103,273 YELLOW MAIZE ,281 4, , ,112 3, , ,702 19, ,174 4, , ,312 75, , , ,803 59, ,001 3, ,130 59, ,110 4, , ,891 84, , , ,296 58, , ,852 1,847, , ,062 4, ,894 1,764 3,341, ,273 SUB-TOTAL 6, ,641 GRAND TOTAL 13,788 1,957,914 Source: Prices University op Pretoria s Bureau for Food and Agricultural Policy Production data - Crop Estimates Committee GM adoption data provided by Wynand van der Walt, FoodNCropBio 21

22 ANNEX 5.3 GMO ACT 15/2007 APPLICATION FORMS, POLICIES, GUIDELINES Guidance document for use by the applicant to complete the application forms Application for a non GMO status certificate for export Application for commodity clearance of genetically modified organisms Application for general release of genetically modified organisms Application for intentional introduction (conduct a trial release) of a genetically modified organism Application for contained use of genetically modified organisms Application for an extended permit (fast track) for activities with GMOs in SA Application for authorisation to export LMOs from South Africa that are destined for (i) contained use or (ii) use as food, feed or processing Application for authorisation to export LMOs from South Africa that are destined for intentional introduction into the environment Application for authorisation to import LMOs into South Africa that are destined for contained use Application for authorisation to import LMOs into South Africa that are destined for intentional introduction (trial release) into the environment Application for authorisation to import LMOs that have general release and/or commodity clearance status in South Africa Application for affidavit to be completed in the presence of a Commissioner of Oaths Application to register a facility for activities involving genetic modification Application for authorisation to use imported GMOs as food, feed or for processing in South Africa Policy and guideline documents Standard Operating Procedures with regard to regulation 4 of the GMO Act GMO Annual Report Standard Operating Procedures with regard to regulation 2(2) of the GMO Act Guidelines for compiling a public notice in terms of the Genetically Modified Organisms Act, 1997 Guideline document for work with genetically modified organisms Guideline document for use by the Advisory Committee when considering proposals/applications for activities with genetically modified organisms Policy on GMO consignments in transit Policy on extension of permits Terms of reference for subcommittees to assist the Advisory Committee in terms of section 11(2) of the Genetically Modified Organisms Act,

Global Review of Commercialized Transgenic Crops: 2002 Feature: Bt Maize

I S A A A INTERNATIONAL SERVICE FOR THE ACQUISITION OF AGRI-BIOTECH APPLICATIONS EXECUTIVE SUMMARY Global Review of Commercialized Transgenic Crops: 2002 Feature: Bt Maize by Clive James Chair, ISAAA Board

I S A A A INTERNATIONAL SERVICE FOR THE ACQUISITION OF AGRI-BIOTECH APPLICATIONS EXECUTIVE SUMMARY Global Review of Commercialized Transgenic Crops: 2002 Feature: Bt Maize by Clive James Chair, ISAAA Board

Top Ten Facts on Biotechnology and Biosafety in South Africa by th Anniversary of Global Commercialization of Biotech Crops ( )

") Top Ten Facts on Biotechnology and Biosafety in South Africa by 2015 20 th Anniversary of Global Commercialization of Biotech Crops (1996-2016) Fact 1 2015, marked 18 years of successful biotech crop cultivation

Top Ten Facts on Biotechnology and Biosafety in South Africa by 2015 20 th Anniversary of Global Commercialization of Biotech Crops (1996-2016) Fact 1 2015, marked 18 years of successful biotech crop cultivation

Pocket K No. 16. Biotech Crop Highlights in 2016

Pocket K No. 16 Biotech Crop Highlights in 2016 In 2016, the 21 st year of commercialization of biotech crops, 185.1 million hectares of biotech crops were planted by ~18 million farmers in 26 countries.

Pocket K No. 16 Biotech Crop Highlights in 2016 In 2016, the 21 st year of commercialization of biotech crops, 185.1 million hectares of biotech crops were planted by ~18 million farmers in 26 countries.

Global impact of Biotech crops: economic & environmental effects

Global impact of Biotech crops: economic & environmental effects 1996-2009 Graham Brookes PG Economics UK www.pgeconomics.co.uk Coverage Presenting findings of full report available on www.pgeconomics.co.uk

Global impact of Biotech crops: economic & environmental effects 1996-2009 Graham Brookes PG Economics UK www.pgeconomics.co.uk Coverage Presenting findings of full report available on www.pgeconomics.co.uk

Genetically Modified Foods: Are They Safe?

Genetically Modified Foods: Are They Safe? W.F. Kee Industry Analyst Technical Insights Group AGRI-FOOD SAFETY AND STANDARDS SEMINAR 2010 Berjaya Times Square Hotel & Convention Centre, Kuala Lumpur January

Genetically Modified Foods: Are They Safe? W.F. Kee Industry Analyst Technical Insights Group AGRI-FOOD SAFETY AND STANDARDS SEMINAR 2010 Berjaya Times Square Hotel & Convention Centre, Kuala Lumpur January

[ 2 ] [ 3 ] WHAT IS BIOTECHNOLOGY? HOW IS BIOTECHNOLOGY DIFFERENT FROM THE TRADITIONAL WAY OF IMPROVING CROPS?

![[ 2 ] [ 3 ] WHAT IS BIOTECHNOLOGY? HOW IS BIOTECHNOLOGY DIFFERENT FROM THE TRADITIONAL WAY OF IMPROVING CROPS?](/thumbs/78/77240529.jpg "[ 2 ] [ 3 ] WHAT IS BIOTECHNOLOGY? HOW IS BIOTECHNOLOGY DIFFERENT FROM THE TRADITIONAL WAY OF IMPROVING CROPS?") WHAT IS BIOTECHNOLOGY? Biotechnology is a modern technology that makes use of organisms (or parts thereof) to make or modify products; improve and develop microorganisms, plants or animals; or develop

WHAT IS BIOTECHNOLOGY? Biotechnology is a modern technology that makes use of organisms (or parts thereof) to make or modify products; improve and develop microorganisms, plants or animals; or develop

Crop * Share

1a. Global acreage with genetically modified crops by crop, 1996-211 (in mln. hectare) Crop 1996 1997 1998 1999 2 21 22 23 24 25 26 27 28 29 21 211* Share Growth 21-211 Soya.4 5.1 14.5 21.6 25.8 33.3 36.5

1a. Global acreage with genetically modified crops by crop, 1996-211 (in mln. hectare) Crop 1996 1997 1998 1999 2 21 22 23 24 25 26 27 28 29 21 211* Share Growth 21-211 Soya.4 5.1 14.5 21.6 25.8 33.3 36.5

GMOs in South Africa Series

GMOs and the law in South Africa: the GMO Act Introduction South Africa began planting GM crops in 1998. It was only in 1999, after much pressure from civil society groups that the Genetically Modified

GMOs and the law in South Africa: the GMO Act Introduction South Africa began planting GM crops in 1998. It was only in 1999, after much pressure from civil society groups that the Genetically Modified

Genetically modified sugarcane and Eldana. Sandy Snyman Agronomist s Association Annual Symposium 27 October 2015

Genetically modified sugarcane and Eldana Sandy Snyman Agronomist s Association Annual Symposium 27 October 2015 GM=Genetically modified What is GM? DNA/gene from one source is transferred to another organism

Genetically modified sugarcane and Eldana Sandy Snyman Agronomist s Association Annual Symposium 27 October 2015 GM=Genetically modified What is GM? DNA/gene from one source is transferred to another organism

MONTHLY FOOD SECURITY BULLETIN OF SOUTH AFRICA: FEBRUARY 2011

MONTHLY FOOD SECURITY BULLETIN OF SOUTH AFRICA: FEBRUARY 2011 Issued: 7 March 2011 Directorate: Statistics and Economic Analysis Highlights: The weather conditions in the eastern parts of the country have

MONTHLY FOOD SECURITY BULLETIN OF SOUTH AFRICA: FEBRUARY 2011 Issued: 7 March 2011 Directorate: Statistics and Economic Analysis Highlights: The weather conditions in the eastern parts of the country have

What is Biotechnology?

What is Biotechnology? Biotechnology is a modern technology that makes use of organisms (or parts thereof) to: make or modify products; improve and develop microorganisms, plants or animals; or develop

What is Biotechnology? Biotechnology is a modern technology that makes use of organisms (or parts thereof) to: make or modify products; improve and develop microorganisms, plants or animals; or develop

Global review of commercialized transgenic crops

Global review of commercialized transgenic crops SPECIAL SECTION: TRANSGENIC CROPS Clive James Chair, ISAAA Board of Directors, ISAAA AmeriCenter, 260 Emerson Hall, Cornell University, Ithaca, NY 14853,

Global review of commercialized transgenic crops SPECIAL SECTION: TRANSGENIC CROPS Clive James Chair, ISAAA Board of Directors, ISAAA AmeriCenter, 260 Emerson Hall, Cornell University, Ithaca, NY 14853,

tractors. Using herbicides avoids that, while herbicide tolerant crops make the use of herbicides simpler.

Benefits of GM crops Monsanto, as a company is committed to sustainable agriculture and development and recognises that there are many challenges in delivering the results of research to the great diversity

Benefits of GM crops Monsanto, as a company is committed to sustainable agriculture and development and recognises that there are many challenges in delivering the results of research to the great diversity

OVERVIEW. ARC; MNCs; Local seed companies; Universities

SOUTH AFRICA BRIEF March, 2015 INTRODUCTION A competitive seed sector is key to ensuring timely availability of appropriate, high quality seeds at affordable prices to smallholder farmers in South Africa.

SOUTH AFRICA BRIEF March, 2015 INTRODUCTION A competitive seed sector is key to ensuring timely availability of appropriate, high quality seeds at affordable prices to smallholder farmers in South Africa.

This Pocket K documents some of the GM crop experiences of selected developing countries.

Pocket K No. 5 Documented Benefits of GM Crops The global area planted to GM crops has consistently increased over the past years. Substantial share of GM crops has been grown in developed countries. In

Pocket K No. 5 Documented Benefits of GM Crops The global area planted to GM crops has consistently increased over the past years. Substantial share of GM crops has been grown in developed countries. In

Biotech and Society Interface: Concerns and Expectations

Biotech and Society Interface: Concerns and Expectations Diran Makinde AU-NEPAD Agency ABNE Ouagadougou, Burkina Faso www.nepadbiosafety.net Presentation at the 5 th Asian Biotech & Dev Conference. Kanya,

Biotech and Society Interface: Concerns and Expectations Diran Makinde AU-NEPAD Agency ABNE Ouagadougou, Burkina Faso www.nepadbiosafety.net Presentation at the 5 th Asian Biotech & Dev Conference. Kanya,

Biosafety Regulation in Kenya

Biosafety Regulation in Kenya Prof. Theophilus M. Mutui, PhD Chief Biosafety Officer GM Food / Feed Safety Assessment Training Workshop for Regulators 7 th August 2014, KCB Leadership Center, Nairobi MISSION

Biosafety Regulation in Kenya Prof. Theophilus M. Mutui, PhD Chief Biosafety Officer GM Food / Feed Safety Assessment Training Workshop for Regulators 7 th August 2014, KCB Leadership Center, Nairobi MISSION

GENETICALLY MODIFIED ORGANISM PRESENTATION. 13 September 2013 by Department of Trade and Industry

GENETICALLY MODIFIED ORGANISM PRESENTATION 13 September 2013 by Department of Trade and Industry Introduction - A genetically modified organism (GMO) means any organism; the genes (or genetic material)

GENETICALLY MODIFIED ORGANISM PRESENTATION 13 September 2013 by Department of Trade and Industry Introduction - A genetically modified organism (GMO) means any organism; the genes (or genetic material)

I S A A A. International Service for the Acquisition of Agri-biotech Applications (ISAAA)

") Global Overview of Biotech/GM Crops and df Future Prospects by Dr. Clive James, Founder and Chair, ISAAA IICA, Costa Rica, September, 2009 International Service for the Acquisition of Agri-biotech Applications

Global Overview of Biotech/GM Crops and df Future Prospects by Dr. Clive James, Founder and Chair, ISAAA IICA, Costa Rica, September, 2009 International Service for the Acquisition of Agri-biotech Applications

GM maize. Stakeholder Consultation on Animal Feeding Studies and in-vitro Studies in GMO Risk Assessment. (3-4 December 2012, Vienna)

") Human Health Environment Socio-Economy GM maize Stakeholder Consultation on Animal Feeding Studies and in-vitro Studies in GMO Risk Assessment (3-4 December 2012, Vienna) www.grace-fp7.eu Top countries

Human Health Environment Socio-Economy GM maize Stakeholder Consultation on Animal Feeding Studies and in-vitro Studies in GMO Risk Assessment (3-4 December 2012, Vienna) www.grace-fp7.eu Top countries

I S A A A INTERNATIONAL SERVICE FOR THE ACQUISITION OF AGRI-BIOTECH APPLICATIONS EXECUTIVE SUMMARY PREVIEW

I S A A A INTERNATIONAL SERVICE FOR THE ACQUISITION OF AGRI-BIOTECH APPLICATIONS EXECUTIVE SUMMARY PREVIEW Global Status of Commercialized Transgenic Crops: 2003 by Clive James Chair, ISAAA Board of Directors

I S A A A INTERNATIONAL SERVICE FOR THE ACQUISITION OF AGRI-BIOTECH APPLICATIONS EXECUTIVE SUMMARY PREVIEW Global Status of Commercialized Transgenic Crops: 2003 by Clive James Chair, ISAAA Board of Directors

5/24/ Food & Agriculture National Conference. Jim Schweigert. Managing the First Genetically Engineered. Events to Go Off Patent 1.

Events to Go Off Patent Panel Jarrett Abramson Senior Intellectual Property Counsel at International Maize and Wheat Improvement Center (CIMMYT) CGIAR Consortium Jim Schweigert President Gro Alliance Stacey

Events to Go Off Patent Panel Jarrett Abramson Senior Intellectual Property Counsel at International Maize and Wheat Improvement Center (CIMMYT) CGIAR Consortium Jim Schweigert President Gro Alliance Stacey

Managing the First Genetically Engineered Events to Go Off Patent

Managing the First Genetically Engineered Events to Go Off Patent Panel Jarrett Abramson Senior Intellectual Property Counsel at International Maize and Wheat Improvement Center (CIMMYT) CGIAR Consortium

Managing the First Genetically Engineered Events to Go Off Patent Panel Jarrett Abramson Senior Intellectual Property Counsel at International Maize and Wheat Improvement Center (CIMMYT) CGIAR Consortium

G enetically. M odified. O rganisms Act, agriculture, forestry & fisheries

G enetically M odified O rganisms Act, 1997 Annual Report 2008/09 agriculture, forestry & fisheries Department: Agriculture, Forestry and Fisheries REPUBLIC OF SOUTH AFRICA G M O enetically odified rganisms

G enetically M odified O rganisms Act, 1997 Annual Report 2008/09 agriculture, forestry & fisheries Department: Agriculture, Forestry and Fisheries REPUBLIC OF SOUTH AFRICA G M O enetically odified rganisms

GMO Crops, Trade Wars, and a New Site Specific Mutagensis System. A. Lawrence Christy, Ph.D.

GMO Crops, Trade Wars, and a New Site Specific Mutagensis System A. Lawrence Christy, Ph.D. Background PhD in Plant Physiology from Ohio State University 12 years with Monsanto R&D in PGR s and herbicides

GMO Crops, Trade Wars, and a New Site Specific Mutagensis System A. Lawrence Christy, Ph.D. Background PhD in Plant Physiology from Ohio State University 12 years with Monsanto R&D in PGR s and herbicides

GM crops: global socio-economic and environmental impacts

GM crops: global socio-economic and environmental impacts 1996-2016 Graham Brookes & Peter Barfoot PG Economics Ltd, UK Dorchester, UK June 2018 Table of contents Foreword...8 Executive summary and conclusions...9

GM crops: global socio-economic and environmental impacts 1996-2016 Graham Brookes & Peter Barfoot PG Economics Ltd, UK Dorchester, UK June 2018 Table of contents Foreword...8 Executive summary and conclusions...9

Seed technology and production system comparisons South African subsistence / smallholder farmers

Seed technology and production system comparisons South African subsistence / smallholder farmers An internal report to the University of Missouri led Creating a Community of Practise in KwaZulu-Natal

Seed technology and production system comparisons South African subsistence / smallholder farmers An internal report to the University of Missouri led Creating a Community of Practise in KwaZulu-Natal

SANBI s GMO monitoring and research programme: contribution towards GMO sustainability R&D

SANBI s GMO monitoring and research programme: contribution towards GMO sustainability R&D Tlou Masehela 1 st Biosafety Symposium; 01/02/2018 ? (NEMBA) Act 10 of 2004 Programme timeline Ms Tsepang Makholela

SANBI s GMO monitoring and research programme: contribution towards GMO sustainability R&D Tlou Masehela 1 st Biosafety Symposium; 01/02/2018 ? (NEMBA) Act 10 of 2004 Programme timeline Ms Tsepang Makholela

ADOPTION AND IMPACT OF GENETICALLY MODIFIED (GM) CROPS IN AUSTRALIA:

CROPS IN AUSTRALIA:") ADOPTION AND IMPACT OF GENETICALLY MODIFIED (GM) CROPS IN AUSTRALIA: 20 YEARS EXPERIENCE Report prepared by Graham Brookes, PG Economics The Adoption and Impact of Genetically Modified (GM) Crops in Australia:

ADOPTION AND IMPACT OF GENETICALLY MODIFIED (GM) CROPS IN AUSTRALIA: 20 YEARS EXPERIENCE Report prepared by Graham Brookes, PG Economics The Adoption and Impact of Genetically Modified (GM) Crops in Australia:

MONTHLY FOOD SECURITY BULLETIN OF SOUTH AFRICA: MARCH 2011

MONTHLY FOOD SECURITY BULLETIN OF SOUTH AFRICA: MARCH 2011 Issued: 8 April 2011 Directorate: Statistics and Economic Analysis Highlights: Vegetation conditions for March 2011 were normal to above-normal

MONTHLY FOOD SECURITY BULLETIN OF SOUTH AFRICA: MARCH 2011 Issued: 8 April 2011 Directorate: Statistics and Economic Analysis Highlights: Vegetation conditions for March 2011 were normal to above-normal

The Role of Biotechnology to Enhance Agricultural Productivity, Production and Farmer Incomes.

The Role of Biotechnology to Enhance Agricultural Productivity, Production and Farmer Incomes. SACAU Policy Conference 16-17 May 2011 Enock Chikava AFSTA President Agenda 1. AFSTA and position on Biotechnology.

The Role of Biotechnology to Enhance Agricultural Productivity, Production and Farmer Incomes. SACAU Policy Conference 16-17 May 2011 Enock Chikava AFSTA President Agenda 1. AFSTA and position on Biotechnology.

FACT The insect resistant variety is sold under the commercial name Bollgard II (BGII ).

.") ~ ISAAA FACT 1 2015 was the 8th year for farmers in Burkina Faso to cultivate insect resistant cotton (Bt cotton). 1. From the initial 8,500 hectares planted in 2008, a total of 350,000 hectares of Bt

~ ISAAA FACT 1 2015 was the 8th year for farmers in Burkina Faso to cultivate insect resistant cotton (Bt cotton). 1. From the initial 8,500 hectares planted in 2008, a total of 350,000 hectares of Bt

Implementation of the Documentation Requirements of Paragraphs 2(b) and 2(c) of the Cartagena Protocol: Experiences of the Global Industry Coalition

and 2(c) of the Cartagena Protocol: Experiences of the Global Industry Coalition") Implementation of the Documentation Requirements of Paragraphs 2(b) and 2(c) of the Cartagena Protocol: Experiences of the Global Industry Coalition Further to the request by the Parties to Cartagena Protocol

Implementation of the Documentation Requirements of Paragraphs 2(b) and 2(c) of the Cartagena Protocol: Experiences of the Global Industry Coalition Further to the request by the Parties to Cartagena Protocol

The Toolbox. The Solutions: Current Technologies. Transgenic DNA Sequences. The Toolbox. 128 bp

The Solutions: Current Technologies Anne R. Bridges, Ph.D. Technical Director AACC International annebridges001@earthlink.net Acknowledgement: Ray Shillito, Bayer Corp. The Toolbox Mutation creation produce

The Solutions: Current Technologies Anne R. Bridges, Ph.D. Technical Director AACC International annebridges001@earthlink.net Acknowledgement: Ray Shillito, Bayer Corp. The Toolbox Mutation creation produce

BRAZILIAN SEED MARKET NEWS. By MNAGRO

BRAZILIAN SEED MARKET NEWS By MNAGRO AGRIBUSINESS IN BRAZIL KEEPS GROWING CONAB, the Brazilian Agriculture Supply government entity recently estimate what should be the last figure for Brazilian grain

BRAZILIAN SEED MARKET NEWS By MNAGRO AGRIBUSINESS IN BRAZIL KEEPS GROWING CONAB, the Brazilian Agriculture Supply government entity recently estimate what should be the last figure for Brazilian grain

Maize and Biodiversity: The Effects of Transgenic Maize in Mexico. Issues Summary. Prepared by Chantal Line Carpentier and Hans Herrmann

Maize and Biodiversity: The Effects of Transgenic Maize in Mexico Issues Summary Prepared by Chantal Line Carpentier and Hans Herrmann Secretariat of the Commission for Environmental Cooperation of North

Maize and Biodiversity: The Effects of Transgenic Maize in Mexico Issues Summary Prepared by Chantal Line Carpentier and Hans Herrmann Secretariat of the Commission for Environmental Cooperation of North

MONTHLY FOOD SECURITY BULLETIN OF SOUTH AFRICA: DECEMBER 2012

MONTHLY FOOD SECURITY BULLETIN OF SOUTH AFRICA: DECEMBER 2012 Issued: 17 January 2013 Directorate: Statistics and Economic Analysis Highlights: During December 2012 significant rainfall events were recorded

MONTHLY FOOD SECURITY BULLETIN OF SOUTH AFRICA: DECEMBER 2012 Issued: 17 January 2013 Directorate: Statistics and Economic Analysis Highlights: During December 2012 significant rainfall events were recorded

MONTHLY FOOD SECURITY BULLETIN OF SOUTH AFRICA: JANUARY 2016

MONTHLY FOOD SECURITY BULLETIN OF SOUTH AFRICA: JANUARY 2016 Issued: 4 February 2016 Directorate: Statistics and Economic Analysis Highlights: During January 2016, significant rainfall events were limited

MONTHLY FOOD SECURITY BULLETIN OF SOUTH AFRICA: JANUARY 2016 Issued: 4 February 2016 Directorate: Statistics and Economic Analysis Highlights: During January 2016, significant rainfall events were limited

MONTHLY FOOD SECURITY BULLETIN OF SOUTH AFRICA: JULY 2017

MONTHLY FOOD SECURITY BULLETIN OF SOUTH AFRICA: JULY Issued: 4 August Directorate: Statistics and Economic Analysis Highlights: During July, significant rainfall events were mainly limited to the south-western

MONTHLY FOOD SECURITY BULLETIN OF SOUTH AFRICA: JULY Issued: 4 August Directorate: Statistics and Economic Analysis Highlights: During July, significant rainfall events were mainly limited to the south-western

benefits of bt cotton in burkina faso

Burkina Faso 2015 was the eighth year for farmers in Burkina Faso to benefit significantly from Bt cotton (Bollgard II ). The total Bt cotton planted in Burkina Faso in 2015 was 350,000 hectares, or 50%

Burkina Faso 2015 was the eighth year for farmers in Burkina Faso to benefit significantly from Bt cotton (Bollgard II ). The total Bt cotton planted in Burkina Faso in 2015 was 350,000 hectares, or 50%

SOUTH AFRICAN GRAIN SEEDS MARKET ANALYSIS REPORT 2016

SOUTH AFRICAN GRAIN SEEDS MARKET ANALYSIS REPORT 2016 Directorate Marketing Tel: 012 319 8455 Private Bag X15 Fax: 012 319 8131 Arcadia Email: MogalaM@daff.gov.za 0007 wwww.daff.gov.za TABLE OF CONTENT

SOUTH AFRICAN GRAIN SEEDS MARKET ANALYSIS REPORT 2016 Directorate Marketing Tel: 012 319 8455 Private Bag X15 Fax: 012 319 8131 Arcadia Email: MogalaM@daff.gov.za 0007 wwww.daff.gov.za TABLE OF CONTENT

Level 20, 9 Castlereagh St, Sydney NSW 2000 T: E:

Regulation of GM crops and factors impacting GM crop penetration in Australia Greg Bodulovic September 2008 Level 20, 9 Castlereagh St, Sydney NSW 2000 T: +61 2 9232 5000 E: gbodulovic@cp-law.com.au www.cp-law.com.au

Regulation of GM crops and factors impacting GM crop penetration in Australia Greg Bodulovic September 2008 Level 20, 9 Castlereagh St, Sydney NSW 2000 T: +61 2 9232 5000 E: gbodulovic@cp-law.com.au www.cp-law.com.au

The Importance of Biotechnology in Meeting Global Food Requirements

The Importance of Biotechnology in Meeting Global Food Requirements Jennifer A Thomson Department of Molecular and Cell Biology University of Cape Town South Africa Projected cereal yield in 2025 Region

The Importance of Biotechnology in Meeting Global Food Requirements Jennifer A Thomson Department of Molecular and Cell Biology University of Cape Town South Africa Projected cereal yield in 2025 Region

GM crops: global socio-economic and environmental impacts

GM crops: global socio-economic and environmental impacts 1996-2011 Graham Brookes & Peter Barfoot PG Economics Ltd, UK Dorchester, UK April 2013 Table of contents Foreword...8 Executive summary and conclusions...9

GM crops: global socio-economic and environmental impacts 1996-2011 Graham Brookes & Peter Barfoot PG Economics Ltd, UK Dorchester, UK April 2013 Table of contents Foreword...8 Executive summary and conclusions...9

PROGRESS REPORT. Grain SA s growth strategy up to 2016

PROGRESS REPORT Grain SA s growth strategy up to 2016 As at 1 August 2013 Grain SA has made the following progress with the strategic focus areas set for 2013/2014: 2 1. Market expansion The first monthly

PROGRESS REPORT Grain SA s growth strategy up to 2016 As at 1 August 2013 Grain SA has made the following progress with the strategic focus areas set for 2013/2014: 2 1. Market expansion The first monthly

1 A Genetically Modified Solution? Th e u n i t e d n a t i o n s World Food Program has clearly stated, Hunger

1 A Genetically Modified Solution? Th e u n i t e d n a t i o n s World Food Program has clearly stated, Hunger and malnutrition are in fact the number one risk to health worldwide greater than AIDS, malaria,

1 A Genetically Modified Solution? Th e u n i t e d n a t i o n s World Food Program has clearly stated, Hunger and malnutrition are in fact the number one risk to health worldwide greater than AIDS, malaria,

Top 10 Facts About Biotech/GM Crops in Africa Beyond Promises: Top 10 Facts about Biotech/Gm Crops in 2013

Top 10 Facts About Biotech/GM Crops in Africa 2013 Beyond Promises: Top 10 Facts about Biotech/Gm Crops in 2013 FaCT 1 2013 Marked was the the 1816th year consecutive year of of commercialization cultivation

Top 10 Facts About Biotech/GM Crops in Africa 2013 Beyond Promises: Top 10 Facts about Biotech/Gm Crops in 2013 FaCT 1 2013 Marked was the the 1816th year consecutive year of of commercialization cultivation

GM crops: global socio-economic and environmental impacts

GM crops: global socio-economic and environmental impacts 1996-2008 Graham Brookes & Peter Barfoot PG Economics Ltd, UK Dorchester, UK April 2010 Table of contents Executive summary and conclusions...8

GM crops: global socio-economic and environmental impacts 1996-2008 Graham Brookes & Peter Barfoot PG Economics Ltd, UK Dorchester, UK April 2010 Table of contents Executive summary and conclusions...8

South Africa - Republic of LOCK-UP REPORT. Grain and Feed Update. Required Report - public distribution. Date: 5/7/2009 GAIN Report Number: SF9020

Required Report - public distribution Date: 5/7/2009 GAIN Report Number: SF9020 South Africa - Republic of LOCK-UP REPORT Grain and Feed Update Approved By: Charles Rush Prepared By: Dirk Esterhuzien Report

Required Report - public distribution Date: 5/7/2009 GAIN Report Number: SF9020 South Africa - Republic of LOCK-UP REPORT Grain and Feed Update Approved By: Charles Rush Prepared By: Dirk Esterhuzien Report

A User's Guide to the Central Portal of the Biosafety Clearing House. Using the BCH for Customs and Border Control tasks

A User's Guide to the Central Portal of the Biosafety Clearing House Using the BCH for Customs and Border Control tasks October 2012 MANUAL OUTLINE 1. INTRODUCTION TO THE MANUAL... 3 2. CARTAGENA PROTOCOL

A User's Guide to the Central Portal of the Biosafety Clearing House Using the BCH for Customs and Border Control tasks October 2012 MANUAL OUTLINE 1. INTRODUCTION TO THE MANUAL... 3 2. CARTAGENA PROTOCOL

briefing false industry claims of increased biotech crop cultivation in europe

International pradeep tewari www.foeeurope.org/gmos/index.htm briefing february 2009 friends of the earth international false industry claims of increased biotech crop cultivation in europe In 2008, the

International pradeep tewari www.foeeurope.org/gmos/index.htm briefing february 2009 friends of the earth international false industry claims of increased biotech crop cultivation in europe In 2008, the

Contributions of Agricultural Biotechnology to Alleviate Poverty and Hunger

Pocket K No. 30 Contributions of Agricultural Biotechnology to Alleviate Poverty and Hunger Introduction In 2016, the number of chronically undernourished people in the world is estimated to have increased

Pocket K No. 30 Contributions of Agricultural Biotechnology to Alleviate Poverty and Hunger Introduction In 2016, the number of chronically undernourished people in the world is estimated to have increased

RSA Agricultural Commodities Weekly Wrap 23 September 2016

AGBIZ RESEARCH AGRI-COMMODITIES WEEKLY WRAP RSA Agricultural Commodities Weekly Wrap 23 September 2016 This season South Africa is a net importer of grains and oilseeds. Therefore, the price movements

AGBIZ RESEARCH AGRI-COMMODITIES WEEKLY WRAP RSA Agricultural Commodities Weekly Wrap 23 September 2016 This season South Africa is a net importer of grains and oilseeds. Therefore, the price movements

THIS REPORT CONTAINS ASSESSMENTS OF COMMODITY AND TRADE ISSUES MADE BY USDA STAFF AND NOT NECESSARILY STATEMENTS OF OFFICIAL U.S.

THIS REPORT CONTAINS ASSESSMENTS OF COMMODITY AND TRADE ISSUES MADE BY USDA STAFF AND NOT NECESSARILY STATEMENTS OF OFFICIAL U.S. GOVERNMENT POLICY Voluntary - Public Date: 7/17/2014 GAIN Report Number:

THIS REPORT CONTAINS ASSESSMENTS OF COMMODITY AND TRADE ISSUES MADE BY USDA STAFF AND NOT NECESSARILY STATEMENTS OF OFFICIAL U.S. GOVERNMENT POLICY Voluntary - Public Date: 7/17/2014 GAIN Report Number:

impact the first nine years

GM crops: the global socioeconomic and environmental impact the first nine years 1996-2004 Graham Brookes & Peter Barfoot PG Economics Ltd, UK Dorchester, UK October 2005 Table of contents Executive summary

GM crops: the global socioeconomic and environmental impact the first nine years 1996-2004 Graham Brookes & Peter Barfoot PG Economics Ltd, UK Dorchester, UK October 2005 Table of contents Executive summary

Bt maize technologies: Insect pest control Anani Bruce

Bt maize technologies: Insect pest control Anani Bruce Training course on identification and management of biotic stresses in maize 8-10 December 2015, Islamabad 1. What is Bt? Outline 2. How does Bt work

Bt maize technologies: Insect pest control Anani Bruce Training course on identification and management of biotic stresses in maize 8-10 December 2015, Islamabad 1. What is Bt? Outline 2. How does Bt work

ISF View on Implementation of National Policies for Seed Low Level Presence

ISF View on Implementation of National Policies for Seed Low Level Presence Adopted in Beijing (China) on 28 May 2014 Table of Contents Executive Summary... 2 Purpose and Scope... 2 1 Description of the

ISF View on Implementation of National Policies for Seed Low Level Presence Adopted in Beijing (China) on 28 May 2014 Table of Contents Executive Summary... 2 Purpose and Scope... 2 1 Description of the

I S A A A INTERNATIONAL SERVICE FOR THE ACQUISITION OF AGRI-BIOTECH APPLICATIONS. ISAAA Briefs PREVIEW

I S A A A INTERNATIONAL SERVICE FOR THE ACQUISITION OF AGRI-BIOTECH APPLICATIONS ISAAA Briefs PREVIEW Global Status of Commercialized Transgenic Crops: 2002 by Clive James Chair, ISAAA Board of Directors

I S A A A INTERNATIONAL SERVICE FOR THE ACQUISITION OF AGRI-BIOTECH APPLICATIONS ISAAA Briefs PREVIEW Global Status of Commercialized Transgenic Crops: 2002 by Clive James Chair, ISAAA Board of Directors

Outline. USAID Biotechnology. Biotech cotton, yield improvement and impacts on global biotechnology policy. Current Status & Impact of Biotech Cotton

Outline USAID Biotechnology Biotech cotton, yield improvement and impacts on global biotechnology policy John McMurdy, PhD Biotechnology Advisor US Agency for International Development March 5, 2009 Current

Outline USAID Biotechnology Biotech cotton, yield improvement and impacts on global biotechnology policy John McMurdy, PhD Biotechnology Advisor US Agency for International Development March 5, 2009 Current

The following are answers to frequently asked questions

Genetically Medified Organisms Production, Regulation, and Maricoting The following are answers to frequently asked questions about what constitutes genetically modified organisms and foods, and how these

Genetically Medified Organisms Production, Regulation, and Maricoting The following are answers to frequently asked questions about what constitutes genetically modified organisms and foods, and how these

Genetically modified pasture dairy s opportunity? Paula Fitzgerald

Genetically modified pasture dairy s opportunity? Paula Fitzgerald Global GM statistics 2013 cultivation 18 years old 175.2 million hectares of GM crops were planted 27 countries grew GM crops 19 developing

Genetically modified pasture dairy s opportunity? Paula Fitzgerald Global GM statistics 2013 cultivation 18 years old 175.2 million hectares of GM crops were planted 27 countries grew GM crops 19 developing

GM crops: global socio-economic and environmental impacts

GM crops: global socio-economic and environmental impacts 1996-2009 Graham Brookes & Peter Barfoot PG Economics Ltd, UK Dorchester, UK 2011 Table of contents Executive summary and conclusions...8 1 Introduction...22

GM crops: global socio-economic and environmental impacts 1996-2009 Graham Brookes & Peter Barfoot PG Economics Ltd, UK Dorchester, UK 2011 Table of contents Executive summary and conclusions...8 1 Introduction...22

Prospects of GM Crops and Regulatory considerations

Prospects of GM Crops and Regulatory considerations Dr.R.S.Kulkarni Professor of Genetics & Plant Breeding University of Agricultural Sciences GKVK, Bangalore THE GLOBAL VALUE OF THE BIOTECH CROP MARKET

Prospects of GM Crops and Regulatory considerations Dr.R.S.Kulkarni Professor of Genetics & Plant Breeding University of Agricultural Sciences GKVK, Bangalore THE GLOBAL VALUE OF THE BIOTECH CROP MARKET

GM crops in Australia Costs, profits and economic risks

GM crops in Australia Costs, profits and economic risks Max Foster Economist Overview Adoption and performance of current GM crops in Australia cotton Canola/rapeseed Risks with GM crops in Australia Market

GM crops in Australia Costs, profits and economic risks Max Foster Economist Overview Adoption and performance of current GM crops in Australia cotton Canola/rapeseed Risks with GM crops in Australia Market

Potential impact of crop diversification and biotechnological inventions on the use of micronutrients

Potential impact of crop diversification and biotechnological inventions on the use of micronutrients Hillel Magen & Patricia Imas, ICL Fertilizers. Prophecy was given to fools = no more prophets available,

Potential impact of crop diversification and biotechnological inventions on the use of micronutrients Hillel Magen & Patricia Imas, ICL Fertilizers. Prophecy was given to fools = no more prophets available,

Kenya. Agricultural Biotechnology Annual. Kenya Biotechnology Update Report

THIS REPORT CONTAINS ASSESSMENTS OF COMMODITY AND TRADE ISSUES MADE BY USDA STAFF AND NOT NECESSARILY STATEMENTS OF OFFICIAL U.S. GOVERNMENT POLICY Required Report - public distribution Date: 8/2/ GAIN

THIS REPORT CONTAINS ASSESSMENTS OF COMMODITY AND TRADE ISSUES MADE BY USDA STAFF AND NOT NECESSARILY STATEMENTS OF OFFICIAL U.S. GOVERNMENT POLICY Required Report - public distribution Date: 8/2/ GAIN

MONTHLY FOOD SECURITY BULLETIN OF SOUTH AFRICA: JANUARY 2017

MONTHLY FOOD SECURITY BULLETIN OF SOUTH AFRICA: JANUARY 2017 Issued: 3 February 2017 Directorate: Statistics and Economic Analysis Highlights: During January 2017, significant rainfall events were limited

MONTHLY FOOD SECURITY BULLETIN OF SOUTH AFRICA: JANUARY 2017 Issued: 3 February 2017 Directorate: Statistics and Economic Analysis Highlights: During January 2017, significant rainfall events were limited

THIS REPORT CONTAINS ASSESSMENTS OF COMMODITY AND TRADE ISSUES MADE BY USDA STAFF AND NOT NECESSARILY STATEMENTS OF OFFICIAL U.S.

THIS REPORT CONTAINS ASSESSMENTS OF COMMODITY AND TRADE ISSUES MADE BY USDA STAFF AND NOT NECESSARILY STATEMENTS OF OFFICIAL U.S. GOVERNMENT POLICY Required Report - public distribution Date: GAIN Report

THIS REPORT CONTAINS ASSESSMENTS OF COMMODITY AND TRADE ISSUES MADE BY USDA STAFF AND NOT NECESSARILY STATEMENTS OF OFFICIAL U.S. GOVERNMENT POLICY Required Report - public distribution Date: GAIN Report

REPORT ON KENYA SMALL-HOLDER FARMERS BIOTECHNOLOGY STUDY VISIT TO SOUTH AFRICA FROM 19 TH -23 RD APRIL, Report Prepared by

REPORT ON KENYA SMALL-HOLDER FARMERS BIOTECHNOLOGY STUDY VISIT TO SOUTH AFRICA FROM 19 TH -23 RD APRIL, 2015 Report Prepared by Doris Anjawa ROP Field Coordinator Email: drsanjawa@gmail.com The African

REPORT ON KENYA SMALL-HOLDER FARMERS BIOTECHNOLOGY STUDY VISIT TO SOUTH AFRICA FROM 19 TH -23 RD APRIL, 2015 Report Prepared by Doris Anjawa ROP Field Coordinator Email: drsanjawa@gmail.com The African

The Future of Ag-biotech in Africa and its Contribution to Household Food Security

The Future of Ag-biotech in Africa and its Contribution to Household Food Security By Florence Wambugu, PhD CEO Africa Harvest ABIC Conference, Calgary 2007 Africa Harvest International non-profit foundation

The Future of Ag-biotech in Africa and its Contribution to Household Food Security By Florence Wambugu, PhD CEO Africa Harvest ABIC Conference, Calgary 2007 Africa Harvest International non-profit foundation

Beyond Promises: Facts about Biotech/GM Crops in 2016

Beyond Promises: Facts about Biotech/GM Crops in 2016 Biotech crop area increased more than 100-fold from 1.7 million hectares in 1996 to 185.1 million hectares in 2016. introduction Beyond Promises: Facts

Beyond Promises: Facts about Biotech/GM Crops in 2016 Biotech crop area increased more than 100-fold from 1.7 million hectares in 1996 to 185.1 million hectares in 2016. introduction Beyond Promises: Facts

Overcoming farm level constraints

Overcoming farm level constraints International Policy Council workshop Lusaka June 3-5 2007 Kinyua M Mbijjewe Monsanto 1 Overcoming farm level constraints requires.. Partnerships A Business Unusual approach

Overcoming farm level constraints International Policy Council workshop Lusaka June 3-5 2007 Kinyua M Mbijjewe Monsanto 1 Overcoming farm level constraints requires.. Partnerships A Business Unusual approach

Assessment of the economic performance of GM crops worldwide

Final Report Assessment of the economic performance of GM crops worldwide ENV.B.3/ETU/2009/0010 Timo Kaphengst, Nadja El Benni, Clive Evans, Robert Finger, Sophie Herbert, Stephen Morse, Nataliya Stupak

Final Report Assessment of the economic performance of GM crops worldwide ENV.B.3/ETU/2009/0010 Timo Kaphengst, Nadja El Benni, Clive Evans, Robert Finger, Sophie Herbert, Stephen Morse, Nataliya Stupak

The North West and Free State provinces received good showers on Wednesday evening which should slightly

16 February 2018 South African Agricultural Commodities Weekly Wrap Apart from the United States Department of Agriculture s World Agricultural Supply and Demand Estimates report, and domestic weekly grain

16 February 2018 South African Agricultural Commodities Weekly Wrap Apart from the United States Department of Agriculture s World Agricultural Supply and Demand Estimates report, and domestic weekly grain

Dr Umi Kalsom Abu Bakar & Dr Chubashini Suntharalingam Malaysian Agricultural Research And Developement Institute (MARDI)

") Bio Borneo 2015 Conference and Exhibition 20-21 April 2015 Kota.Kinabalu, Sabah Dr Umi Kalsom Abu Bakar & Dr Chubashini Suntharalingam Malaysian Agricultural Research And Developement Institute (MARDI)

Bio Borneo 2015 Conference and Exhibition 20-21 April 2015 Kota.Kinabalu, Sabah Dr Umi Kalsom Abu Bakar & Dr Chubashini Suntharalingam Malaysian Agricultural Research And Developement Institute (MARDI)

Biotechnology and Genetically Modified Crops

Biotechnology and Genetically Modified Crops Suggestions for Your Presentation Use a Video to start your presentation. A couple of videos were provided with this slide deck that could be used or use another

Biotechnology and Genetically Modified Crops Suggestions for Your Presentation Use a Video to start your presentation. A couple of videos were provided with this slide deck that could be used or use another

Annex. Methods. The following search methods have been applied to obtain primary data for the impact assessment on genetically engineered plants:

Annex Methods The following search methods have been applied to obtain primary data for the impact assessment on genetically engineered plants: Questionnaire To acquire primary data, a questionnaire was

Annex Methods The following search methods have been applied to obtain primary data for the impact assessment on genetically engineered plants: Questionnaire To acquire primary data, a questionnaire was

While it is still early in the season, some international observers already forecast a decline in South Africa s 2017/18

17 November 2017 South African Agricultural Commodities Weekly Wrap Apart from the United States Department of Agriculture s World Agricultural Supply and Demand Estimates report, and domestic weekly grain

17 November 2017 South African Agricultural Commodities Weekly Wrap Apart from the United States Department of Agriculture s World Agricultural Supply and Demand Estimates report, and domestic weekly grain

Policy, Economics and IP Protection. by Howard Minigh, CropLife International

Policy, Economics and IP Protection Considerations for Biotech Crops by Howard Minigh, CropLife International Farmers Face Many Challenges Dramatic increases in consumer demand and need driven by population

Policy, Economics and IP Protection Considerations for Biotech Crops by Howard Minigh, CropLife International Farmers Face Many Challenges Dramatic increases in consumer demand and need driven by population

Can GM crops contribute to food security and sustainable agricultural development?

Can GM crops contribute to food security and sustainable agricultural development? Evidence from 20 years of impact research Matin Qaim Agricultural Economist 3 rd Forum of the International Industrial

Can GM crops contribute to food security and sustainable agricultural development? Evidence from 20 years of impact research Matin Qaim Agricultural Economist 3 rd Forum of the International Industrial

CONTENTS. About Biotech. Argentina. Brazil. Burkina Faso. India. Philippines. United States. Around the Globe - 3 -

CONTENTS 04 06 08 10 14 16 18 20 About Biotech Argentina Brazil Burkina Faso India Philippines United States Around the Globe - 3 - > CROPS AROUND THE WORLD > WHAT IS PLANT NOLOGY? As it becomes more challenging

CONTENTS 04 06 08 10 14 16 18 20 About Biotech Argentina Brazil Burkina Faso India Philippines United States Around the Globe - 3 - > CROPS AROUND THE WORLD > WHAT IS PLANT NOLOGY? As it becomes more challenging

MONTHLY FOOD SECURITY BULLETIN OF SOUTH AFRICA: JUNE 2017

MONTHLY FOOD SECURITY BULLETIN OF SOUTH AFRICA: JUNE 2017 Issued: 5 July 2017 Directorate: Statistics and Economic Analysis Highlights: According to the latest Seasonal Climate Watch of the SA Weather

MONTHLY FOOD SECURITY BULLETIN OF SOUTH AFRICA: JUNE 2017 Issued: 5 July 2017 Directorate: Statistics and Economic Analysis Highlights: According to the latest Seasonal Climate Watch of the SA Weather

COTTON DEVELOPMENT AUTHORITY

REPUBLIC OF KENYA COTTON DEVELOPMENT AUTHORITY THE STATUS REPORT ON THE COTTON INDUSTRY IN KENYA FOR ICAC PLENARY MEETING IN CAPETOWN SOUTH AFRICA, SEPTEMBER 7 TH -11 TH -2009 COMPILED BY COTTON DEVELOPMENT

REPUBLIC OF KENYA COTTON DEVELOPMENT AUTHORITY THE STATUS REPORT ON THE COTTON INDUSTRY IN KENYA FOR ICAC PLENARY MEETING IN CAPETOWN SOUTH AFRICA, SEPTEMBER 7 TH -11 TH -2009 COMPILED BY COTTON DEVELOPMENT

MONTHLY FOOD SECURITY BULLETIN OF SOUTH AFRICA: AUGUST 2012

MONTHLY FOOD SECURITY BULLETIN OF SOUTH AFRICA: AUGUST 2012 Issued: 4 September 2012 Directorate: Statistics and Economic Analysis Highlights: Significant rainfall occurrences for August 2012 were limited

MONTHLY FOOD SECURITY BULLETIN OF SOUTH AFRICA: AUGUST 2012 Issued: 4 September 2012 Directorate: Statistics and Economic Analysis Highlights: Significant rainfall occurrences for August 2012 were limited

HOW OUR FOOD IS GROWN