GSM ASSOCIATION RESPONSE TO BEREC QUESTIONS TO STAKEHOLDERS BEREC REPORT ON OLIGOPOLY ANALYSIS AND REGULATION JANUARY 2015

|

|

|

- Harriet Stewart

- 5 years ago

- Views:

Transcription

1 BoR PC01 (15) 21 GSM ASSOCIATION RESPONSE TO BEREC QUESTIONS TO STAKEHOLDERS BEREC REPORT ON OLIGOPOLY ANALYSIS AND REGULATION JANUARY 2015 About the GSMA The GSMA represents the interests of mobile operators worldwide, uniting nearly 800 operators with more than 250 companies in the broader mobile ecosystem, including handset and device makers, software companies, equipment providers and Internet companies, as well as organisations in adjacent industry sectors. The GSMA also produces industry-leading events such as Mobile World Congress, Mobile World Congress Shanghai and the Mobile 360 Series conferences. For more information, please visit the GSMA corporate website at Follow the GSMA on Policy Contacts Tom Phillips Matthew Bloxham Laszlo Toth Chief Regulatory Officer Head of Policy Research Senior Director, Europe (Acting) GSM Association The Walbrook Building 25 Walbrook London EC4N 8AF 1

2 Introduction and Summary The GSMA is pleased to provide input to BEREC as it prepares to consider the implications of oligopolistic structures on the functioning of Electronic Communications markets in Europe. As the GSMA represents specifically the mobile industry, the following comments refer to, and are limited to, issues concerning mobile networks. While we welcome the opportunity to address these issues in a public forum, we are concerned by some of the premises and underlying assumptions in this questionnaire, which seem to imply a need to lower thresholds for a regulatory intervention. 1. The scope of the report is too narrow. As further detailed below, electronic communications markets overall are characterised by increased competition, as convergence adds to existing competitive pressures. It is the view of the GSMA that the forthcoming review of the electronic communications regulatory framework should focus on modernising and wherever possible reducing regulation in the sector taking full account of new sources of disruptive competition that are emerging from non-traditional sources. And it should focus on the broader citizen interest by supporting investment in connectivity rather than managing prices. Limiting the report to the treatment of oligopolies is insufficient and at risk of missing the bigger picture. 2. Oligopolistic market structure does not per se lead to inefficient outcomes BEREC s choice of terminology is debatable. In economics, the notion of oligopoly comprises different market structures, not all of which are applicable here. A number of communications markets are characterised by high infrastructure investment needs and a concentrated market structure, but do not bear other characteristics associated with oligopolistic competition, such as greater coordination. In the following submission GSMA does not use the term oligopoly but speaks of concentrated markets or where the legal concept of oligopolistic market power is concerned - of joint SMP or joint dominance. 3. Telecoms markets do not require more regulation, they require better regulation. Existing data and future trends show that there is no clear rationale for ex-ante regulation. Only entrenched structural competition problems that are not expected to be resolved absent regulation can justify regulation on an upstream market. For highly concentrated markets, competition law foresees the established legal test of joint dominance, which has been included in the present framework in the form of joint SMP. There is no need to devise a different threshold. Indeed, any different threshold would have to be stricter than the joint dominance criteria, as ex-ante regulation places higher regulatory burdens on undertakings than scrutiny under expost competition law (notably by not requiring a proof of anti-competitive behaviour before regulation applies). As will be shown below, the existence of market concentration in mobile wholesale markets has not resulted, and is highly unlikely to result, in a restriction of competition in retail markets, or consumer detriment overall. Market outcomes should be measured not against the model of perfect competition, but in terms of price, innovation and quality of service. All these indicators show that overall, the market is evolving in the right direction and additional ex-ante regulation is unnecessary. 2

3 Situations of oligopolistic competition in the electronic communications sector 1. In the electronic communications sector, do you consider that there are markets that were characterised by oligopolistic structures from the outset? In your view, which factors (scarcity of spectrum, high level of required investments, etc.) explain the existence of these market structures? Are wholesale markets more prone to oligopolies than retail markets? Electronic communications markets, particularly at the retail level, have changed drastically since the liberalisation of telecoms markets in Europe. Today s communication services are characterised by a rapidly increasing scope and convergence. Consumers are faced with a wide array of technologies and providers, many from adjacent industries, who offer functionally equivalent or similar solutions to consumer demand. While national licensing regimes and high investment requirements preserve the characteristics of more concentrated structures at the wholesale level, competition at the retail level is subject to competitive pressure from all sides: MVNOs, Internetbased service providers and global content players all compete with telecoms operators in providing end-to-end communications services. New retail markets are not oligopolistic with voice calls and SMS being classic examples of markets that were previously limited to the number of licenced operators in a market and that is now open to rapid entry and exit (see the recent Commission decision in Facebook/WhatsApp). Similar trends are observed across the service spectrum with innovation being driven from all quarters. Thus, the arrival of MVNOs and Internet based participation in the retail market for mobile communication services has evolved to reflect high levels of competition with market participants serving a broad range of customer segments with tailored offerings. 3

4 Mobile wholesale markets have higher levels of industry concentration compared to retail markets. This is due to a combination of factors including scarcity of spectrum and the high levels of investment required to build out network infrastructure. Clearly, ex post competition law is well established to deal with any individual or collective abuses of a dominant position in any wholesale markets and the GSMA is not aware of any current allegation or case concerning such an abuse. This is expected to continue as the ability to leverage any concentration has significantly diminished. Further, the existence of an oligopoly characterized by few players in a given market does not necessarily result in a market structure where companies are in a position of joint dominance. Oligopolies are often mentioned by regulators in relation to the market power these companies wield rather than to the given number of actors. In most oligopolies, companies maintain their independence and do not directly partner with each other. However, as a result of the characteristics of the limited marketplace, it is assumed that there is a risk these companies indirectly synchronize the pricing and policy decisions they make, an action often labelled tacit coordination or conscious parallelism. For a number of reasons outlined below, this assumption does not hold true in mobile telecommunications markets. The telecommunications industry is, at wholesale level, concentrated by nature: because of certain economic characteristics the market can sustain only a small number of infrastructure players. Empirical evidence shows that this concentrated market structure does not per se lead to inefficient outcomes. With very few exceptions, even wholesale markets with fewer than four operators prove to be highly competitive and have not halted a rapid price fall in the vast majority of downstream and retail markets. In the few cases where collusion between operators was found and cases of abuse of joint dominance have been proved, ex-post competition law remedies have been effective and sufficient in dealing with such market failure. No ex-ante regulation is necessary or indeed appropriate to prevent such cases. Issues of potential market failure have also been addressed in several merger review cases. Notably the Commission s decision in the Irish and German merger cases have shown that even in a forward-looking analysis, unilateral effects are unlikely have any real impact on the competitive structure in the markets concerned. The GSMA believes that the regulatory measures imposed by the Commissions in these cases to allow a reduction from 4 to 3 players were excessive in relation to the effective impact they have had. 1. Any general pre-emptive regulation, in the absence of a specific merger case, would be even more disproportionate

If so, please state in which electronic communications services markets you observe this evolution, making reference to specific retail and wholesale electronic communications services markets.")

5 2. Do you consider that there has been an increase in oligopolistic market structures (including duopolies) in any of the electronic communications services markets or more generally in the sector? i) If so, please state in which electronic communications services markets you observe this evolution, making reference to specific retail and wholesale electronic communications services markets. Please state whether you observe this evolution at a subnational, national or European level. ii) What do you consider to be the main drivers of this increase (if any) in oligopolistic situations (mergers, fixed-mobile convergence, bundled offers, roll-out of next generation or other networks, operators strategies, etc.)? Do you expect this trend to continue? As stated above, the GSMA considers that the majority of retail markets are competitive, and continue to become more competitive as new players enter the market and new services are launched. In virtually all Member States even core communications services retail markets have, over time, become less concentrated due to the increasing number of both vertically integrated MNOs but more importantly MVNOs, many of which have achieved high levels of market share. 5

6 Wholesale mobile markets have, over time, generally also become less concentrated due to the licensing of new network operators. Only recently has this trend been reversed in some Member States due to M&A activity. This more recent trend in network consolidation is the direct result of the transition to data-centric communications networks and services. In most markets this transition has meant that mobile network operators have to achieve a larger scale in order to compete effectively in these changing markets. Key drivers of the efficient scale required include technology developments, strong consumer demand for data and increasingly faster speeds; and direct competition from highly concentrated players in adjacent markets including OTT players. More importantly, deployment of high speed broadband networks, providing consumers with the best possible quality of service, depends on high levels of investment which smaller players often cannot achieve. Where mobile network consolidation occurred, it has not adversely impacted competition at the retail level. Contrary to some Commission analysis, GSMA data has shown that this is not because of the remedies required to gain approval from competition authorities, but mainly because MNOs and MVNOs profit from more efficient networks. Many transactions have enabled smaller operators to make the 6

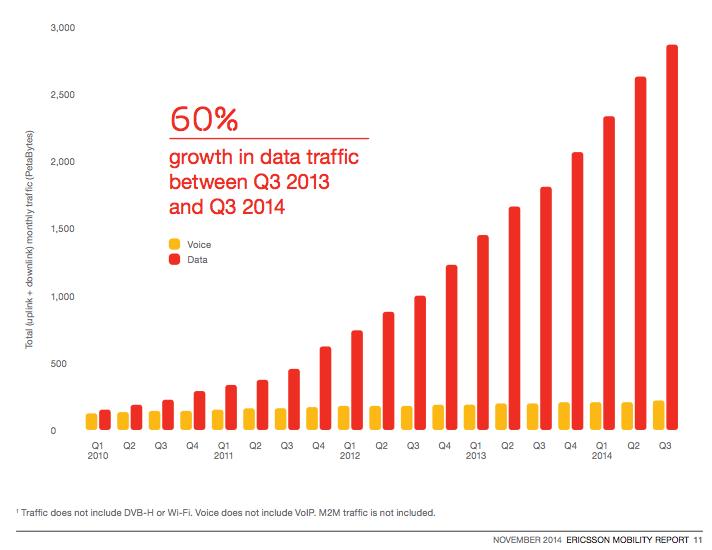

7 necessary investments to compete more effectively and provide end consumers with wider (real) choice and improved service provision. None of the EU markets currently has a duopoly in wholesale network access. Once a central licensing system and single EU market has been achieved, even after consolidation there will be many more competitors than in comparable single markets (such as the US). To reach this goal, the intermediate step of domestic consolidation has to be encouraged so as to allow the creation of stronger players which could then compete at the European and the global level. Other mobile services markets, such as the market for mobile operating systems, have for some time been characterised by a much more concentrated market structure (i.e. a quasi-duopoly), with repercussions in downstream (mobile apps) and neighbouring (handsets) markets. The GSMA believes BEREC s analysis should make a careful distinction between industry-specific drivers of market concentration (fast technological progress, high rate of innovation and patent licensing) and market drivers of market concentration (mergers, exit). The question text refers to both examples of mechanisms (e.g. mergers) as well as drivers (e.g. technology evolution). The GSMA believes there is an endogenous tendency towards concentrated market structures in the wholesale market for mobile electronic communications services. This is driven by a number of factors, not least the need to generate sufficient returns on the high levels of long-term investment required. Investment in new technology is the most important determinant of consumer outcomes in mobile markets. Frequent technology cycles significantly increase capacity, and reducing unit prices through higher volumes. New network technology cycles also unlock new cycles of innovation in services and devices along the supply chain, which then drive further growth in user demand for new services. The economic equation for investments in fixed and mobile network infrastructure in Europe is becoming increasingly challenging. This, in part, reflects the growing appetite from end users for very high-speed connections and also the rapid increase in consumption of data traffic. 7

8 8

9 These trends are driving significant incremental investments by operators to push fibre deeper into their networks, create greater capillarity and network density (serving fewer customers from any given access node), acquire more spectrum and invest in new access technologies (e.g. LTE). In addition, we are witnessing increasing, disruptive competition from over-the-top (OTT) players in the retail markets for messaging and voice services. As a result, in addition to an increase in the required level of investment, the industry is experiencing a reduction in the size of the revenue pool. These economic realities are the principle driver of higher levels of industry concentration as network-based operators seek to invest and remain competitive in the convergent market through mergers (mobile to mobile and, increasingly, mobile to fixed) and/or organic expansion into adjacent service markets (e.g. quad play offerings). Concentrated market structures are much evident in adjacent markets such as social networking, instant messaging and online search. All of these markets are dominated by a small number of global players who are able to leverage of regulatory and fiscal asymmetries to gain shares of EU markets. Also, MNOs are subject to laws and regulations which are not applied to these new global players, thus giving them a significant competitive advantage. Possible effects of oligopolistic competition 3. What are the main threats to competition and to the interests of end-users, which might result from the oligopolistic market structures referred to above? As stated above, mobile operators compete vigorously both at wholesale and at retail level. Data collected by Frontier Economics 2 suggest that there is no actual risk of price increases linked to concentrated markets, even in cases of 4-3 consolidation at wholesale level. The European mobile communications industry has seen significant reductions in absolute and per unit pricing alongside improvements in coverage, reliability and capability. These consumer benefits have been delivered despite relatively high levels of concentration, typically with only three, four or five infrastructure-based network operators. Some of the lowest priced markets for mobile services in Europe (e.g. Finland) only have three network operators

10 Going forward, we expect the potential need for larger scale and concentration in some markets to be heavily counterbalanced by very strong constraints and competitive drivers arising from the transition to a data-centric model which, as discussed above, includes direct competition from highly concentrated content and service provider structures, as well as a continued consumer demand for more capacity and data. 4. Do you consider that there are any benefits or opportunities (for instance related to the roll-out of NGA networks in the context of broadband access) that could arise from oligopolistic situations? Please explain your reasoning. The GSMA believes that scale is a critical success factor in network-based industries such as electronic communications. A certain degree of consolidation is necessary in some markets to provide operators with the resources and incentives to invest in network upgrades and new services. This benefits end users in a number of ways including: better network coverage, improved reliability, faster download speeds, higher throughput capacity, better customer service and an improved choice (and pricing) of devices. 5. In your view, are there any electronic communications services where oligopolistic markets are more susceptible than others to uncompetitive outcomes? Please explain your view. As stated above, the GSMA has not seen any evidence that higher degrees of concentration in some (wholesale) mobile markets lead to uncompetitive outcomes. Restrictions of competition typically arise where oligopolies are linked to joint dominance, and this is not the case in any of the markets in questions. 10

11 Regulating oligopolies 6. In your view, are there any areas of concern in relation to oligopolistic outcomes which are not adequately addressed by the current regulatory framework (i.e. both the European Union relevant texts and NRAs policies)? In particular, what is your appreciation of the concept of collective dominance? What do you consider to be the most effective regulation of anti-competitive oligopolistic situations? The GSMA believes that the European Union text (e.g. the Framework Directive) makes explicit and sufficient provision for the identification of situations of Significant Market Power and Joint Dominance. Regulation should only be introduced where there is evidence of market failure or abuse and, even then, when no other remedies exist. It is contended that there is little or no evidence of market failure and competition law has all the tools necessary to address any concerns should they arise. It is contended that the burden upon the regulators to show any lack in the ability of competition law to address the very issues being discussed has not been addressed. Remedies in the context of oligopolies 7. In your view, what are the main ex ante remedies (which are currently present or could be introduced in the European ex ante regulatory framework) that could be applied to electronic communications services markets exhibiting oligopolistic market structures? (similar or differentiated remedies, symmetric regulation, etc.)? The GSMA believes that there should not be a presumption that oligopolistic market structures require ex-ante regulatory remedies. Ex ante remedies should only be considered following careful analysis with clear evidence of durable anti-competitive behaviour. The GSMA believes that European mobile markets in general provide end users with a good balance of low prices (especially compared to the US market) and quality (LTE roll-out is increasingly rapidly following the release of digital dividend spectrum). Electronic communications markets are characterized by high levels of innovation and fast rates of technological change which, as has been observed over the last two decades, reflects very positively on consumers as new and better services are developed in the sector and rapidly diffused in the economy, for the benefit of consumers. Ex-ante regulation can have a large impact on investment decisions and can change market conditions in a way that impacts negatively on innovation and investment decisions. This is particularly the case if the incumbents incentives and decisions as to whether or how to invest or innovate are reduced or the risks increased. 11

12 Other issues 8. Please, provide any other insight or opinion regarding oligopoly analysis and regulation. We are most concerned by the premise and presuppositions in this document. Telecoms markets do not need more regulation. Much rather, the GSMA believes there is a need to review existing regulation with a view to simplifying and lighten rules where justified, and to take into account the new sources of disruptive competition that are emerging from non-traditional sources. The GSMA believes that consumer benefit should not be exclusively framed by a debate about lowest price. In the context of the mobile industry consumer benefit (and the competitive positioning of the EU as a region) is best served by balancing price with investments to deliver best-in-class networks in terms of (amongst other attributes) coverage, capacity, reliability and speed. A broad and bold reform of the European regulatory framework is required, which deals decisively with issues such as the new Internet bottlenecks and the years of accumulated legacy regulation in Europe. 12

BEREC Report on Oligopoly analysis and regulation. Questions to stakeholders

BoR PC01 (15) 05 BEREC Report on Oligopoly analysis and regulation Questions to stakeholders Telenor Group submission to BEREC 23 January 2014 Introduction Telenor Group is pleased to provide input to

BoR PC01 (15) 05 BEREC Report on Oligopoly analysis and regulation Questions to stakeholders Telenor Group submission to BEREC 23 January 2014 Introduction Telenor Group is pleased to provide input to

GSMA general statement with regards to BEREC Consultation on Draft BEREC Strategy (BoR (17) 109) 5 July 2017

109) 5 July 2017") BoR PC02 (17) 07 GSMA general statement with regards to BEREC Consultation on Draft BEREC Strategy 2018-2020 (BoR (17) 109) 5 July 2017 About the GSMA The GSMA represents the interests of mobile operators

BoR PC02 (17) 07 GSMA general statement with regards to BEREC Consultation on Draft BEREC Strategy 2018-2020 (BoR (17) 109) 5 July 2017 About the GSMA The GSMA represents the interests of mobile operators

Regulating oligopolies in telecoms: the new European Commission guidelines

Agenda Advancing economics in business Regulating oligopolies in telecoms: the new European Commission guidelines In February 2018 the European Commission published draft guidelines on determining significant

Agenda Advancing economics in business Regulating oligopolies in telecoms: the new European Commission guidelines In February 2018 the European Commission published draft guidelines on determining significant

GSM Association comments on the Draft BEREC Report on Oligopoly Analysis and Regulation (BoR (15) 74) 1 August 2015

74) 1 August 2015") BEREC ref. No BoR PC03 (15) 14 GSM Association comments on the Draft BEREC Report on Oligopoly Analysis and Regulation (BoR (15) 74) 1 August 2015 About the GSMA The GSMA represents the interests of mobile

BEREC ref. No BoR PC03 (15) 14 GSM Association comments on the Draft BEREC Report on Oligopoly Analysis and Regulation (BoR (15) 74) 1 August 2015 About the GSMA The GSMA represents the interests of mobile

GSMA comments on the Draft BEREC Report on OTT services (BoR (15) 142)

142)") BoR PC06 (15) 19 GSMA comments on the Draft BEREC Report on OTT services (BoR (15) 142) About the GSMA The GSMA represents the interests of mobile operators worldwide, uniting nearly 800 operators with

BoR PC06 (15) 19 GSMA comments on the Draft BEREC Report on OTT services (BoR (15) 142) About the GSMA The GSMA represents the interests of mobile operators worldwide, uniting nearly 800 operators with

COMMISSION RECOMMENDATION. of (Text with EEA relevance)

") EUROPEAN COMMISSION Brussels, 9.10.2014 C(2014) 7174 final COMMISSION RECOMMENDATION of 9.10.2014 on relevant product and service markets within the electronic communications sector susceptible to ex ante

EUROPEAN COMMISSION Brussels, 9.10.2014 C(2014) 7174 final COMMISSION RECOMMENDATION of 9.10.2014 on relevant product and service markets within the electronic communications sector susceptible to ex ante

RECOMMENDATIONS. (Text with EEA relevance) (2014/710/EU)

(2014/710/EU)") 11.10.2014 L 295/79 RECOMMDATIONS COMMISSION RECOMMDATION of 9 October 2014 on relevant product and service markets within the electronic communications sector susceptible to ex ante regulation in accordance

11.10.2014 L 295/79 RECOMMDATIONS COMMISSION RECOMMDATION of 9 October 2014 on relevant product and service markets within the electronic communications sector susceptible to ex ante regulation in accordance

Subject: COOPVOCE Response to BoR (5) 74 - BEREC Report on Oligopoly Analysis and Regulation

74 - BEREC Report on Oligopoly Analysis and Regulation") BEREC Ref. No BoR PC03 (15) 07 Bologna-Bruxelles 31 July 2015 BEREC Body of European Regulators for Electronic Communications Riga - Latvia By E-mail: pm@berec.europa.eu Subject: COOPVOCE Response to BoR

BEREC Ref. No BoR PC03 (15) 07 Bologna-Bruxelles 31 July 2015 BEREC Body of European Regulators for Electronic Communications Riga - Latvia By E-mail: pm@berec.europa.eu Subject: COOPVOCE Response to BoR

Mergers: Commission clears proposed merger between Telefónica Deutschland (Telefónica) E-Plus subject to conditions-frequently asked questions

E-Plus subject to conditions-frequently asked questions") EUROPEAN COMMISSION MEMO Brussels, 2 July 2014 Mergers: Commission clears proposed merger between Telefónica Deutschland (Telefónica) E-Plus subject to conditions-frequently asked questions (See also IP/14/771)

EUROPEAN COMMISSION MEMO Brussels, 2 July 2014 Mergers: Commission clears proposed merger between Telefónica Deutschland (Telefónica) E-Plus subject to conditions-frequently asked questions (See also IP/14/771)

Review of the 2002 SMP Guidelines. Anthony Whelan WIK workshop Revising the SMP Guidelines 27 March 2018

Review of the 2002 SMP Guidelines Anthony Whelan WIK workshop Revising the SMP Guidelines 27 March 2018 Review Process March to June 2017 - Public Consultation 5 Oct 2017 - Synopsis report of responses

Review of the 2002 SMP Guidelines Anthony Whelan WIK workshop Revising the SMP Guidelines 27 March 2018 Review Process March to June 2017 - Public Consultation 5 Oct 2017 - Synopsis report of responses

BEREC study on Oligopoly Analysis and Regulation

BEREC study on Oligopoly Analysis and Regulation Comments by Richard Feasey, Independent Consultant/Fronfraith Ltd (fronfraithltd@gmail.com, +447748776618) 1. I welcome BEREC s study of oligopolistic market

BEREC study on Oligopoly Analysis and Regulation Comments by Richard Feasey, Independent Consultant/Fronfraith Ltd (fronfraithltd@gmail.com, +447748776618) 1. I welcome BEREC s study of oligopolistic market

COOPVOCE Response to BoR (14) 172. Questions to stakeholders related to the. BEREC Report on Oligopoly - Analysis and Regulation

172. Questions to stakeholders related to the. BEREC Report on Oligopoly - Analysis and Regulation") BoR PC01 (15) 11 COOPVOCE Response to BoR (14) 172 Questions to stakeholders related to the BEREC Report on Oligopoly - Analysis and Regulation A. Introduction COOPVOCE, one of the leading MVNO operator

BoR PC01 (15) 11 COOPVOCE Response to BoR (14) 172 Questions to stakeholders related to the BEREC Report on Oligopoly - Analysis and Regulation A. Introduction COOPVOCE, one of the leading MVNO operator

Vodafone s response to

Vodafone s response to BEREC s draft Report on oligopoly analysis and regulation 29 July 2015 1 1 For any further information on this submission, please contact Markus Reinisch, Group Public Policy Director,

Vodafone s response to BEREC s draft Report on oligopoly analysis and regulation 29 July 2015 1 1 For any further information on this submission, please contact Markus Reinisch, Group Public Policy Director,

Oligopolies in electronic communications: more concentration, more regulation?

Agenda Advancing economics in business Oligopolies in electronic communications: more concentration, more regulation? The consolidation trend in fixed and mobile telecoms is leading to more concentrated

Agenda Advancing economics in business Oligopolies in electronic communications: more concentration, more regulation? The consolidation trend in fixed and mobile telecoms is leading to more concentrated

BEREC Strategy

Draft BEREC Strategy 2018-2020 2 June 2017 Introduction BEREC, the Body of European Regulators of Electronic Communications) was established by Regulation (EC) 1211/2009. BEREC s membership comprises the

Draft BEREC Strategy 2018-2020 2 June 2017 Introduction BEREC, the Body of European Regulators of Electronic Communications) was established by Regulation (EC) 1211/2009. BEREC s membership comprises the

ETNO Comments on the BEREC report on the impact of premium content on ECS markets and the effect of devices on the open use of the Internet

BoR PC07 (17) 01 November 2017 ETNO Comments on the BEREC report on the impact of premium content on ECS markets and the effect of devices on the open use of the Internet BEREC approved for public consultation

BoR PC07 (17) 01 November 2017 ETNO Comments on the BEREC report on the impact of premium content on ECS markets and the effect of devices on the open use of the Internet BEREC approved for public consultation

Cable Europe response to BEREC s consultation on its draft report on oligopoly analysis and regulation

Cable Europe response to BEREC s consultation on its draft report on oligopoly analysis and regulation 30 July 2015 Cable Europe welcomes the opportunity to comment on the BEREC s draft report on oligopoly

Cable Europe response to BEREC s consultation on its draft report on oligopoly analysis and regulation 30 July 2015 Cable Europe welcomes the opportunity to comment on the BEREC s draft report on oligopoly

BoR (17) 175. BEREC Strategy

175. BEREC Strategy") BEREC Strategy 2018-2020 5 October, 2017 Introduction BEREC, the Body of European Regulators of Electronic Communications, was established by Regulation (EC) 1211/2009. BEREC s membership comprises the

BEREC Strategy 2018-2020 5 October, 2017 Introduction BEREC, the Body of European Regulators of Electronic Communications, was established by Regulation (EC) 1211/2009. BEREC s membership comprises the

GSMA comments on the Review of the BEREC Medium-Term Strategy (BoR (17) 38) 5 April 2017

38) 5 April 2017") BoR PC01 (17) 008 GSMA comments on the Review of the BEREC Medium-Term Strategy 2018-2020 (BoR (17) 38) 5 April 2017 About the GSMA The GSMA represents the interests of mobile operators worldwide, uniting

BoR PC01 (17) 008 GSMA comments on the Review of the BEREC Medium-Term Strategy 2018-2020 (BoR (17) 38) 5 April 2017 About the GSMA The GSMA represents the interests of mobile operators worldwide, uniting

Contribution of Orange to BEREC Report on Oligopoly analysis and regulation

Contribution of Orange to BEREC Report on Oligopoly analysis and regulation Document number: BoR (15) 74 July 2015 - Name of the organization responding to the questionnaire: Orange - Brief description

Contribution of Orange to BEREC Report on Oligopoly analysis and regulation Document number: BoR (15) 74 July 2015 - Name of the organization responding to the questionnaire: Orange - Brief description

Official Journal of the European Union L 344/65 RECOMMENDATIONS COMMISSION

28.12.2007 Official Journal of the European Union L 344/65 RECOMMENDATIONS COMMISSION COMMISSION RECOMMENDATION of 17 December 2007 on relevant product and service markets within the electronic communications

28.12.2007 Official Journal of the European Union L 344/65 RECOMMENDATIONS COMMISSION COMMISSION RECOMMENDATION of 17 December 2007 on relevant product and service markets within the electronic communications

Part I PRELIMINARY. Part II MARKET DEFINITION ASSESSING SIGNIFICANT MARKET POWER. Part IV IMPOSITION OF OBLIGATIONS UNDER THE REGULATORY FRAMEWORK

201[ ] ELECTRONIC COMMUNICATIONS (GUIDELINES ON MARKET ANALYSIS AND THE ASSESSMENT OF SIGNIFICANT MARKET POWER FOR NETWORKS AND SERVICES) (ARRANGEMENT OF GUIDELINES) Table of Contents 1. [Short Title]

201[ ] ELECTRONIC COMMUNICATIONS (GUIDELINES ON MARKET ANALYSIS AND THE ASSESSMENT OF SIGNIFICANT MARKET POWER FOR NETWORKS AND SERVICES) (ARRANGEMENT OF GUIDELINES) Table of Contents 1. [Short Title]

The Review of the Telecommunications Regulatory Framework

POSITION PAPER 16 December 2015 The Review of the Telecommunications Regulatory Framework 1. INTRODUCTION Embracing the digital information revolution is crucial to ensure Europe s competitive advantage

POSITION PAPER 16 December 2015 The Review of the Telecommunications Regulatory Framework 1. INTRODUCTION Embracing the digital information revolution is crucial to ensure Europe s competitive advantage

The new European Electronic Communications Code (EECC)

") The new European Electronic Communications Code (EECC) A concise legal appraisal of its final draft Ελληνικό Τμήμα FITCE Thessaloniki, 15 th December 2017 By Ioannis Tzionas Professor of European & International

The new European Electronic Communications Code (EECC) A concise legal appraisal of its final draft Ελληνικό Τμήμα FITCE Thessaloniki, 15 th December 2017 By Ioannis Tzionas Professor of European & International

Position Paper. Cable Europe position paper on the Telecoms Review. Executive Summary. Policy objectives

4 April 2016 Position Paper Cable Europe position paper on the Telecoms Review Executive Summary This Position Paper outlines Cable Europe s response to the Commission s consultation on the revision of

4 April 2016 Position Paper Cable Europe position paper on the Telecoms Review Executive Summary This Position Paper outlines Cable Europe s response to the Commission s consultation on the revision of

BEREC views on the European Parliament first reading legislative resolution on the European Commission s proposal for a Connected Continent Regulation

BEREC views on the European Parliament first reading legislative resolution on the European Commission s proposal for a Connected Continent Regulation General remarks In line with its statutory duty of

BEREC views on the European Parliament first reading legislative resolution on the European Commission s proposal for a Connected Continent Regulation General remarks In line with its statutory duty of

EU Telecoms Sector: Regulatory Developments, Threats and. Opportunities

EU Telecoms Sector: Regulatory Developments, Threats and Opportunities Institute of International and European Affairs Dublin, 11 November 2013 Intervention by Mr Luigi Gambardella Chairman of the Executive

EU Telecoms Sector: Regulatory Developments, Threats and Opportunities Institute of International and European Affairs Dublin, 11 November 2013 Intervention by Mr Luigi Gambardella Chairman of the Executive

Response to the consultation on the Draft review of the BEREC Common Position on geographical aspects of market analysis (definition and remedies).

.") Response to the consultation on the Draft review of the BEREC Common Position on geographical aspects of market analysis (definition and remedies). 7 February 2014 FTTH Council Europe ASBL Rue des Colonies

Response to the consultation on the Draft review of the BEREC Common Position on geographical aspects of market analysis (definition and remedies). 7 February 2014 FTTH Council Europe ASBL Rue des Colonies

experience Principal, International Ofcom April 2008

Functional separation: the UK experience Tom Kiedrowski Tom Kiedrowski Principal, International Ofcom April 2008 Agenda Section 1 Background and context Section 2 Approach and rationale Section 3 Taking

Functional separation: the UK experience Tom Kiedrowski Tom Kiedrowski Principal, International Ofcom April 2008 Agenda Section 1 Background and context Section 2 Approach and rationale Section 3 Taking

BoR (15)74. BEREC Report on Oligopoly analysis and regulation

74. BEREC Report on Oligopoly analysis and regulation") BoR (15)74 BEREC Report on Oligopoly analysis and regulation June 2015 Contents 1 Executive summary and main findings... 5 2 Contents of the report... 7 3 Context and objectives of the report... 8 4 Oligopoly

BoR (15)74 BEREC Report on Oligopoly analysis and regulation June 2015 Contents 1 Executive summary and main findings... 5 2 Contents of the report... 7 3 Context and objectives of the report... 8 4 Oligopoly

BoR (15) 195. BEREC Report on. Oligopoly analysis and regulation

195. BEREC Report on. Oligopoly analysis and regulation") BEREC Report on Oligopoly analysis and regulation December 2015 Contents 1 Executive summary and main findings... 5 2 Contents of the report... 7 3 Context and objectives of the report... 8 4 Oligopoly

BEREC Report on Oligopoly analysis and regulation December 2015 Contents 1 Executive summary and main findings... 5 2 Contents of the report... 7 3 Context and objectives of the report... 8 4 Oligopoly

INTUG Position Statement on the European Commission s proposals following review of the European Telecommunications Framework.

INTUG Position Statement on the European Commission s proposals following review of the European Telecommunications Framework. Introduction The International Telecommunications Users Group (INTUG) was

INTUG Position Statement on the European Commission s proposals following review of the European Telecommunications Framework. Introduction The International Telecommunications Users Group (INTUG) was

ETNO comments on the ERG draft common position on geographic aspects of market analysis

August 2008 ETNO comments on the ERG draft common position on geographic aspects of market analysis ETNO welcomes the ERG consultation on geographic aspects of market analysis. The Common Position is a

August 2008 ETNO comments on the ERG draft common position on geographic aspects of market analysis ETNO welcomes the ERG consultation on geographic aspects of market analysis. The Common Position is a

Price regulation of unbundled broadband services

Price regulation of unbundled broadband services ARPCE, Brazzaville 19 February 2014 Pedro Seixas, expert ITU International Telecommunication Union Agenda Outline of regulatory issues Price regulation

Price regulation of unbundled broadband services ARPCE, Brazzaville 19 February 2014 Pedro Seixas, expert ITU International Telecommunication Union Agenda Outline of regulatory issues Price regulation

EUROPE NEEDS CHANGES

EUROPE NEEDS CHANGES Let me first welcome you today at this first Regulatory Summit organised jointly by ETNO and Total Telecom. I would like to thank our distinguished speakers for having accepted our

EUROPE NEEDS CHANGES Let me first welcome you today at this first Regulatory Summit organised jointly by ETNO and Total Telecom. I would like to thank our distinguished speakers for having accepted our

ReSPONSE by Deutsche Telekom. BEREC Public Consultation on the Draft Review of the BEREC Common Position on geographical aspects of market analysis

ReSPONSE by Deutsche Telekom BEREC Public Consultation on the Draft Review of the BEREC Common Position on geographical aspects of market analysis February 2014 Executive Summary Deutsche Telekom welcomes

ReSPONSE by Deutsche Telekom BEREC Public Consultation on the Draft Review of the BEREC Common Position on geographical aspects of market analysis February 2014 Executive Summary Deutsche Telekom welcomes

NewCo2015 Limited. Response to Preliminary Determination on

NewCo2015 Limited Response to Preliminary Determination on Assessment of Significant Market Power in Mobile Call and Short Messaging Termination Services on NewCo2015 Limited s Cellular Mobile Network

NewCo2015 Limited Response to Preliminary Determination on Assessment of Significant Market Power in Mobile Call and Short Messaging Termination Services on NewCo2015 Limited s Cellular Mobile Network

ECTA RESPONSE DRAFT BEREC PRELIMINARY REPORT IN VIEW OF A COMMON POSITION ON MONITORING MOBILE COVERAGE TO THE PUBLIC CONSULTATION BY BEREC ON THE

ECTA RESPONSE TO THE PUBLIC CONSULTATION BY BEREC ON THE DRAFT BEREC PRELIMINARY REPORT IN VIEW OF A COMMON POSITION ON MONITORING MOBILE COVERAGE BoR (17) 186 8 NOVEMBER 2017 1. Introduction ECTA, the

ECTA RESPONSE TO THE PUBLIC CONSULTATION BY BEREC ON THE DRAFT BEREC PRELIMINARY REPORT IN VIEW OF A COMMON POSITION ON MONITORING MOBILE COVERAGE BoR (17) 186 8 NOVEMBER 2017 1. Introduction ECTA, the

The Future of EU Access and Interconnection Regulation

The Future of EU Access and Interconnection Regulation BITS Brussels, 25 March 2015 Peter Alexiadis* Partner, Gibson, Dunn & Crutcher LLP, Brussels Visiting Professor, King s College, London * The views

The Future of EU Access and Interconnection Regulation BITS Brussels, 25 March 2015 Peter Alexiadis* Partner, Gibson, Dunn & Crutcher LLP, Brussels Visiting Professor, King s College, London * The views

UNI Europa ICTS position on the European Single Market for electronic communications

UNI Europa ICTS position on the European Single Market for electronic communications As a trade union federation representing 1.2 million workers in 41 countries in the ICT sector in Europe, UNI Europa

UNI Europa ICTS position on the European Single Market for electronic communications As a trade union federation representing 1.2 million workers in 41 countries in the ICT sector in Europe, UNI Europa

Wholesale call origination on the public telephone network provided at a fixed location

Wholesale call origination on the public telephone network provided at a fixed location Wholesale call termination on individual public telephone networks provided at a fixed location Response to Consultation

Wholesale call origination on the public telephone network provided at a fixed location Wholesale call termination on individual public telephone networks provided at a fixed location Response to Consultation

COMMISSION OF THE EUROPEAN COMMUNITIES COMMISSION STAFF WORKING DOCUMENT EXPLANATORY NOTE. Accompanying document to the

EN EN EN COMMISSION OF THE EUROPEAN COMMUNITIES Brussels, SEC(2007) 1483/2 rev1 COMMISSION STAFF WORKING DOCUMENT EXPLANATORY NOTE Accompanying document to the Commission Recommendation on Relevant Product

EN EN EN COMMISSION OF THE EUROPEAN COMMUNITIES Brussels, SEC(2007) 1483/2 rev1 COMMISSION STAFF WORKING DOCUMENT EXPLANATORY NOTE Accompanying document to the Commission Recommendation on Relevant Product

DCMS Future Telecoms Infrastructure Review Summary of findings

6 th August 2018 DCMS Future Telecoms Infrastructure Review Summary of findings 1. Introduction The Department for Culture, Media & Sport (DCMS) has published the findings of its Future Telecoms Infrastructure

6 th August 2018 DCMS Future Telecoms Infrastructure Review Summary of findings 1. Introduction The Department for Culture, Media & Sport (DCMS) has published the findings of its Future Telecoms Infrastructure

Regulating Tomorrow s Information Society and Media. International Institute of Communications (IIC), 14 April, Berlin

, 14 April, Berlin") EUROPEAN COMMISSION Competition DG Information, communication and multimedia Media The Head of Division Brussels, 14 April 2005 COMP/C2/HU Dr. Herbert Ungerer Regulating Tomorrow s Information Society

EUROPEAN COMMISSION Competition DG Information, communication and multimedia Media The Head of Division Brussels, 14 April 2005 COMP/C2/HU Dr. Herbert Ungerer Regulating Tomorrow s Information Society

The FTTH Council is concerned by a number of specific aspects of this consultation which it would like to set out at the outset.

Introduction The FTTH Council welcomes the opportunity to reply to these consultations, Review of the wholesale local access market and Review of the wholesale broadband access market. The FTTH Council

Introduction The FTTH Council welcomes the opportunity to reply to these consultations, Review of the wholesale local access market and Review of the wholesale broadband access market. The FTTH Council

Telecoms: how the Article 7 consultation and notification mechanism works: frequently asked questions (see also IP/10/644)

") MEMO/10/226 Brussels, 1 June 2010 Telecoms: how the Article 7 consultation and notification mechanism works: frequently asked questions (see also IP/10/644) What is the Article 7 procedure? Article 7 of

MEMO/10/226 Brussels, 1 June 2010 Telecoms: how the Article 7 consultation and notification mechanism works: frequently asked questions (see also IP/10/644) What is the Article 7 procedure? Article 7 of

The proposed Code appears (inappropriately) to support incumbents investment models at the expense of competition

to support incumbents investment models at the expense of competition") Sky s response to the European Commission s consultation on the proposed Directive establishing a new European Electronic Communications Code Introduction 1. Sky plc ( Sky ) 1 is Europe s leading pay TV

Sky s response to the European Commission s consultation on the proposed Directive establishing a new European Electronic Communications Code Introduction 1. Sky plc ( Sky ) 1 is Europe s leading pay TV

BEREC Opinion on. Phase II investigation. pursuant to Article 7 of Directive 2002/21/EC as amended by Directive 2009/140/EC: Case FI/2013/1498

BoR (13) 171 BEREC Opinion on Phase II investigation pursuant to Article 7 of Directive 2002/21/EC as amended by Directive 2009/140/EC: Case FI/2013/1498 Wholesale markets for call termination on individual

BoR (13) 171 BEREC Opinion on Phase II investigation pursuant to Article 7 of Directive 2002/21/EC as amended by Directive 2009/140/EC: Case FI/2013/1498 Wholesale markets for call termination on individual

How to regulate next-generation access (if at all)?

?") Agenda Advancing economics in business How to regulate next-generation access (if at all)? European telecoms regulators have, for some time, been faced with the question of how next-generation access (NGA)

Agenda Advancing economics in business How to regulate next-generation access (if at all)? European telecoms regulators have, for some time, been faced with the question of how next-generation access (NGA)

ECTA Response to BoR (15) 74. BEREC draft Report on Oligopoly Analysis and Regulation. 7 August 2015

74. BEREC draft Report on Oligopoly Analysis and Regulation. 7 August 2015") BEREC ref. No BoR PC03 (15) 18 ECTA Response to BoR (15) 74 BEREC draft Report on Oligopoly Analysis and Regulation 7 August 2015 This ECTA response is attributable to ECTA as an association and cannot

BEREC ref. No BoR PC03 (15) 18 ECTA Response to BoR (15) 74 BEREC draft Report on Oligopoly Analysis and Regulation 7 August 2015 This ECTA response is attributable to ECTA as an association and cannot

EXPERT LEVEL TRAINING ON TELECOM NETWORK COST MODELLING FOR THE HIPSSA REGIONS

EXPERT LEVEL TRAINING ON TELECOM NETWORK COST MODELLING FOR THE HIPSSA REGIONS Banjul 19-23 August, 2013 David Rogerson, ITU Expert International Telecommunication Union 1 Session 2: Understanding the

EXPERT LEVEL TRAINING ON TELECOM NETWORK COST MODELLING FOR THE HIPSSA REGIONS Banjul 19-23 August, 2013 David Rogerson, ITU Expert International Telecommunication Union 1 Session 2: Understanding the

Strategic and Retail Market Review. 3 June 2008

Strategic and Retail Market Review 3 June 2008 Purpose: To outline a comprehensive package of proportionate regulatory measures that will further promote competition and the interest of consumers arising

Strategic and Retail Market Review 3 June 2008 Purpose: To outline a comprehensive package of proportionate regulatory measures that will further promote competition and the interest of consumers arising

The University of Oxford Centre for Competition Law and Policy

The University of Oxford Centre for Competition Law and Policy Working Paper (L) 13/05 Under (and Over) Prescribing of Behavioural Remedies Ariel Ezrachi Preliminary Definitions There are various ways

The University of Oxford Centre for Competition Law and Policy Working Paper (L) 13/05 Under (and Over) Prescribing of Behavioural Remedies Ariel Ezrachi Preliminary Definitions There are various ways

The EU electronic communications framework: is it on track?

Agenda Advancing economics in business The EU electronic communications framework: is it on track? Across Europe, around 450 detailed market reviews are taking place, as the national regulatory authorities

Agenda Advancing economics in business The EU electronic communications framework: is it on track? Across Europe, around 450 detailed market reviews are taking place, as the national regulatory authorities

Review of the Electronic Communications Regulatory Framework. Executive Summary 6: NRAs and BEREC

Review of the Electronic Communications Regulatory Framework Executive Summary 6: NRAs and BEREC 1. General context and objectives An efficient governance with modernised institutions is essential in order

Review of the Electronic Communications Regulatory Framework Executive Summary 6: NRAs and BEREC 1. General context and objectives An efficient governance with modernised institutions is essential in order

TeliaSonera s response to the European Commission s public consultation on the revision of the Recommendation on relevant markets.

Contact Robert Liljeström +46-72-7349091 robert.liljestrom@teliasonera.com Stockholm, 8 January 2013 TeliaSonera s response to the European Commission s public consultation on the revision of the Recommendation

Contact Robert Liljeström +46-72-7349091 robert.liljestrom@teliasonera.com Stockholm, 8 January 2013 TeliaSonera s response to the European Commission s public consultation on the revision of the Recommendation

Mobile Privacy Principles

Mobile Privacy Principles Promoting consumer privacy in the mobile ecosystem Copyright 2016 GSM Association About the GSMA The GSMA represents the interests of mobile operators worldwide, uniting nearly

Mobile Privacy Principles Promoting consumer privacy in the mobile ecosystem Copyright 2016 GSM Association About the GSMA The GSMA represents the interests of mobile operators worldwide, uniting nearly

ETNO Reflection Document on the European Commission Communication on Challenges for the European Information Society beyond 2005

January 2005 ETNO Reflection Document on the European Commission Communication on Challenges for the European Information Society beyond 2005 Executive Summary ETNO welcomes the opportunity to provide

January 2005 ETNO Reflection Document on the European Commission Communication on Challenges for the European Information Society beyond 2005 Executive Summary ETNO welcomes the opportunity to provide

telecom regulation The stakes are high. The vision of the By Wolfgang Bock, Björn Röber, and Peter Soos

Reforming Europe s telecom regulation By Wolfgang Bock, Björn Röber, and Peter Soos The Boston Consulting Group recently completed a major study, commissioned by the European Telecommunications Network

Reforming Europe s telecom regulation By Wolfgang Bock, Björn Röber, and Peter Soos The Boston Consulting Group recently completed a major study, commissioned by the European Telecommunications Network

Comments on the BEREC Work Programme for 2010

Comments on the BEREC Work Programme for 2010 1. Preliminary Remarks by VON Europe The Voice on the Net Coalition Europe ( VON ) welcomes the opportunity to comment on the Draft BEREC Work Programme for

Comments on the BEREC Work Programme for 2010 1. Preliminary Remarks by VON Europe The Voice on the Net Coalition Europe ( VON ) welcomes the opportunity to comment on the Draft BEREC Work Programme for

New powers for telecoms and media regulators? Part 1: the rise of oligopolists

Agenda Advancing economics in business New powers for telecoms and media regulators? Part 1: the rise of oligopolists Continued M&A activity in the fixed and mobile telecoms sector is creating more concentrated

Agenda Advancing economics in business New powers for telecoms and media regulators? Part 1: the rise of oligopolists Continued M&A activity in the fixed and mobile telecoms sector is creating more concentrated

Principles of implementation and best practice regarding the application of Retail Minus pricing methodologies IRG (05) 39

39") Principles of implementation and best practice regarding the application of Retail Minus pricing methodologies IRG (05) 39 IRG PUBLIC CONSULTATION DOCUMENT Principles of Implementation and Best Practice

Principles of implementation and best practice regarding the application of Retail Minus pricing methodologies IRG (05) 39 IRG PUBLIC CONSULTATION DOCUMENT Principles of Implementation and Best Practice

BoR (18) 240. BEREC Work Programme 2019

240. BEREC Work Programme 2019") BEREC Work Programme 2019 7 December 2018 Contents I. INTRODUCTION... 3 II. BACKGROUND... 5 III. BEREC WORK IN 2019 AND 2020... 8 1. Strategic priority 1: Responding to connectivity challenges and to new

BEREC Work Programme 2019 7 December 2018 Contents I. INTRODUCTION... 3 II. BACKGROUND... 5 III. BEREC WORK IN 2019 AND 2020... 8 1. Strategic priority 1: Responding to connectivity challenges and to new

Undue discrimination by SMP providers Consideration of responses to a proposal for investigating potential contraventions on competition grounds of

Undue discrimination by SMP providers Consideration of responses to a proposal for investigating potential contraventions on competition grounds of Requirements not to unduly discriminate imposed on SMP

Undue discrimination by SMP providers Consideration of responses to a proposal for investigating potential contraventions on competition grounds of Requirements not to unduly discriminate imposed on SMP

Response to the consultation on the BEREC Report on Oligopoly analysis and regulation. FTTH Council Europe ASBL Rue des Colonies Brussels

Response to the consultation on the BEREC Report on Oligopoly analysis and regulation. FTTH Council Europe ASBL Rue des Colonies 11 1000 Brussels Belgium Transparency Register ID: 09838612482-61 31 July

Response to the consultation on the BEREC Report on Oligopoly analysis and regulation. FTTH Council Europe ASBL Rue des Colonies 11 1000 Brussels Belgium Transparency Register ID: 09838612482-61 31 July

The Role of the Regulator in Respect of Encouraging Consumer Choice, Affordable & Quality Services, Encouraging Investment etc.

The Role of the Regulator in Respect of Encouraging Consumer Choice, Affordable & Quality Services, Encouraging Investment etc. Seminar on Economic and Market Analysis for CEE and Baltic States Prague,

The Role of the Regulator in Respect of Encouraging Consumer Choice, Affordable & Quality Services, Encouraging Investment etc. Seminar on Economic and Market Analysis for CEE and Baltic States Prague,

AIIP comments on the

AIIP comments on the BEREC Common Position on best practice remedies on the market for wholesale broadband access (including bitstream access) imposed as a consequence of a position of significant market

AIIP comments on the BEREC Common Position on best practice remedies on the market for wholesale broadband access (including bitstream access) imposed as a consequence of a position of significant market

ECTA POLICY POSITION

BoR PC02 (15) 14 Annex 1 ECTA POLICY POSITION ENABLING SERVICE DIFFERENTIATION FOR THE BENEFITS OF CONSUMERS THROUGH THE UNBUNDLING OF LINE ACTIVATION AND FAULT REPAIR SERVICES NOVEMBER 2014 THE ISSUE

BoR PC02 (15) 14 Annex 1 ECTA POLICY POSITION ENABLING SERVICE DIFFERENTIATION FOR THE BENEFITS OF CONSUMERS THROUGH THE UNBUNDLING OF LINE ACTIVATION AND FAULT REPAIR SERVICES NOVEMBER 2014 THE ISSUE

Wholesale call origination on the public telephone network provided at a fixed location

Wholesale call origination on the public telephone network provided at a fixed location Wholesale call termination on individual public telephone networks provided at a fixed location Response to Consultation

Wholesale call origination on the public telephone network provided at a fixed location Wholesale call termination on individual public telephone networks provided at a fixed location Response to Consultation

Public Hearing. MTC Presentation as per Public Notice Nº62, 20 March Miguel Geraldes 11 May 2012

Public Hearing MTC Presentation as per Public Notice Nº62, 20 March 2012 Miguel Geraldes 11 May 2012 Understanding the market analysis Benchmark Comments on CRAN approaches Suggestion 2 Market Analysis

Public Hearing MTC Presentation as per Public Notice Nº62, 20 March 2012 Miguel Geraldes 11 May 2012 Understanding the market analysis Benchmark Comments on CRAN approaches Suggestion 2 Market Analysis

BEREC Strategy

BoR PC02 (17) 03 BEREC Strategy 2018-2020 ETNO contribution (marked in Blue) 5 July 2017 Introduction BEREC, the Body of European Regulators of Electronic Communications) was established by Regulation

BoR PC02 (17) 03 BEREC Strategy 2018-2020 ETNO contribution (marked in Blue) 5 July 2017 Introduction BEREC, the Body of European Regulators of Electronic Communications) was established by Regulation

Mobile Privacy Principles

Mobile Privacy Principles Promoting consumer privacy in the mobile ecosystem About the GSMA The GSMA represents the interests of mobile operators worldwide, uniting nearly 800 operators with more than

Mobile Privacy Principles Promoting consumer privacy in the mobile ecosystem About the GSMA The GSMA represents the interests of mobile operators worldwide, uniting nearly 800 operators with more than

DTI/HMT Review on Concurrent Competition Powers in Sectoral Regulation

12 January 2007 Emma Campbell Assistant Director Economic Regulation Team Consumer and Competition Policy Directorate Department of Trade and Industry 1 Victoria Street LONDON SW1H 0ET DAVID STEWART Director

12 January 2007 Emma Campbell Assistant Director Economic Regulation Team Consumer and Competition Policy Directorate Department of Trade and Industry 1 Victoria Street LONDON SW1H 0ET DAVID STEWART Director

2015 State of the Industry Report Mobile Money EXECUTIVE SUMMARY

2015 State of the Industry Report Mobile Money EXECUTIVE SUMMARY STATE OF THE INDUSTRY REPORT ON MOBILE MONEY The GSMA represents the interests of mobile operators worldwide, uniting nearly 800 operators

2015 State of the Industry Report Mobile Money EXECUTIVE SUMMARY STATE OF THE INDUSTRY REPORT ON MOBILE MONEY The GSMA represents the interests of mobile operators worldwide, uniting nearly 800 operators

Market power and market definition in electronic communications

Market power and market definition in electronic communications Alexandre de Streel University of Namur and CRIDS CERRE Expert Workshop 21 June 2011 1 Four steps to impose economic regulation in electronic

Market power and market definition in electronic communications Alexandre de Streel University of Namur and CRIDS CERRE Expert Workshop 21 June 2011 1 Four steps to impose economic regulation in electronic

Margin squeeze: defining a reasonably efficient operator*

by Richard Cadman Margin squeeze: defining a reasonably efficient operator* Is this the biggest challenge in telecom margin squeeze? What standard should a regulator or competition authority apply when

by Richard Cadman Margin squeeze: defining a reasonably efficient operator* Is this the biggest challenge in telecom margin squeeze? What standard should a regulator or competition authority apply when

UPS Response to the ERGP 2019 Work Program September 2018

UPS Response to the ERGP 2019 Work Program September 2018 We would like to thank the ERGP for the opportunity to provide input on their 2019 work program and we would also like to congratulate you on the

UPS Response to the ERGP 2019 Work Program September 2018 We would like to thank the ERGP for the opportunity to provide input on their 2019 work program and we would also like to congratulate you on the

Trends in Telecommunications: Implications for Regulation

Trends in Telecommunications: Implications for Regulation 20 September 2017 Mark DJ Williams, Managing Director, BRG mark.williams@thinkbrg.com +44 (0) 7825 862 132 Trends in Telecommunications Regulatory

Trends in Telecommunications: Implications for Regulation 20 September 2017 Mark DJ Williams, Managing Director, BRG mark.williams@thinkbrg.com +44 (0) 7825 862 132 Trends in Telecommunications Regulatory

Regulatory challenges posed by next generation access networks Public discussion document

Regulatory challenges posed by next generation access networks Public discussion document Publication date: 23 November 2006 Contents Section Page 1 Executive summary 1 2 Introduction 5 3 Definition of

Regulatory challenges posed by next generation access networks Public discussion document Publication date: 23 November 2006 Contents Section Page 1 Executive summary 1 2 Introduction 5 3 Definition of

6 Wholesale geographic market definition

Section 6 6 Wholesale geographic market definition Introduction 6.1 Having considered in Section 5 the relevant wholesale product market definitions, the wholesale geographic market definition for each

Section 6 6 Wholesale geographic market definition Introduction 6.1 Having considered in Section 5 the relevant wholesale product market definitions, the wholesale geographic market definition for each

BEREC views on Article 74 of the draft Code Co-investment and very high-capacity (VHC) networks

networks") BEREC views on Article 74 of the draft Code Co-investment and very high-capacity (VHC) networks The Commission s proposals The Commission is seeking to encourage co-investment as a means of mitigating

BEREC views on Article 74 of the draft Code Co-investment and very high-capacity (VHC) networks The Commission s proposals The Commission is seeking to encourage co-investment as a means of mitigating

PURC Roundtable Tallahassee, Florida 29 September Real Competition and Real Regulation Lessons from Europe

PURC Roundtable Tallahassee, Florida 29 September 2004 Real Competition and Real Regulation Lessons from Europe Martin Cave Warwick Business School University of Warwick, UK Martin.Cave@wbs.ac.uk me53

PURC Roundtable Tallahassee, Florida 29 September 2004 Real Competition and Real Regulation Lessons from Europe Martin Cave Warwick Business School University of Warwick, UK Martin.Cave@wbs.ac.uk me53

Keynote ECTA Conference

Keynote ECTA Conference Brussels, November 28th, 2017 Good Afternoon ladies and gentlemen, Thank you very much for inviting me to this distinguished conference and for the opportunity to enter into a dialogue

Keynote ECTA Conference Brussels, November 28th, 2017 Good Afternoon ladies and gentlemen, Thank you very much for inviting me to this distinguished conference and for the opportunity to enter into a dialogue

Convergence in the electronic communications markets: challenges for the EU regulatory policies

SPEECH/09/551 Viviane Reding Member of the European Commission responsible for Information Society and Media Convergence in the electronic communications markets: challenges for the EU regulatory policies

SPEECH/09/551 Viviane Reding Member of the European Commission responsible for Information Society and Media Convergence in the electronic communications markets: challenges for the EU regulatory policies

Non-Horizontal Mergers Guidelines: Ten Principles. A Note by the EAGCP Merger Sub-Group

Non-Horizontal Mergers Guidelines: Ten Principles A Note by the EAGCP Merger Sub-Group The Directorate General of Competition is contemplating the introduction of Non Horizontal Merger (NHM) Guidelines.

Non-Horizontal Mergers Guidelines: Ten Principles A Note by the EAGCP Merger Sub-Group The Directorate General of Competition is contemplating the introduction of Non Horizontal Merger (NHM) Guidelines.

SESSION 4: STRATEGIC COSTING FOR BROADBAND SERVICES

SESSION 4: STRATEGIC COSTING FOR BROADBAND SERVICES ITU-D REGIONAL ECONOMIC AND FINANCIAL FORUM OF TELECOMMUNICATIONS/ICTS FOR ASIA AND PACIFIC Yangon, The Republic of the Union of Myanmar, 1 September

SESSION 4: STRATEGIC COSTING FOR BROADBAND SERVICES ITU-D REGIONAL ECONOMIC AND FINANCIAL FORUM OF TELECOMMUNICATIONS/ICTS FOR ASIA AND PACIFIC Yangon, The Republic of the Union of Myanmar, 1 September

BEREC DRAFT STRATEGY

The Consumer Voice in Europe BEREC DRAFT STRATEGY 2018 2020 BEUC comments Contact: Guillermo Beltrà digital@beuc.eu BUREAU EUROPÉEN DES UNIONS DE CONSOMMATEURS AISBL DER EUROPÄISCHE VERBRAUCHERVERBAND

The Consumer Voice in Europe BEREC DRAFT STRATEGY 2018 2020 BEUC comments Contact: Guillermo Beltrà digital@beuc.eu BUREAU EUROPÉEN DES UNIONS DE CONSOMMATEURS AISBL DER EUROPÄISCHE VERBRAUCHERVERBAND

BoR PC05 (15) 08. Response to. BoR (15) 140 Draft BEREC Work Programme 2016

08. Response to. BoR (15) 140 Draft BEREC Work Programme 2016") BoR PC05 (15) 08 Response to BoR (15) 140 Draft BEREC Work Programme 2016 30 October 2015 Contents I. About MVNO Europe... 3 II. Introduction and Key Points... 4 III. Draft WP2016: Specific MVNO Europe

BoR PC05 (15) 08 Response to BoR (15) 140 Draft BEREC Work Programme 2016 30 October 2015 Contents I. About MVNO Europe... 3 II. Introduction and Key Points... 4 III. Draft WP2016: Specific MVNO Europe

BEREC DRAFT REPORT ON OTT SERVICES

BoR PC06 (15) 16 The Consumer Voice in Europe BEREC DRAFT REPORT ON OTT SERVICES BEUC response to the public consultation Contact: Guillermo Beltrà digital@beuc.eu BUREAU EUROPÉEN DES UNIONS DE CONSOMMATEURS

BoR PC06 (15) 16 The Consumer Voice in Europe BEREC DRAFT REPORT ON OTT SERVICES BEUC response to the public consultation Contact: Guillermo Beltrà digital@beuc.eu BUREAU EUROPÉEN DES UNIONS DE CONSOMMATEURS

Contents. BoR (18) 34

34") BEREC report on the outcome of the public consultation on the impact of premium content on ECS markets and the effect of devices on the open use of the Internet 8 March 2018 Contents 1. Introduction...

BEREC report on the outcome of the public consultation on the impact of premium content on ECS markets and the effect of devices on the open use of the Internet 8 March 2018 Contents 1. Introduction...

Telecom Italia response to. BEREC Consultations. Roaming Regulation Choice of decoupling method

Telecom Italia response to BEREC Consultations on Roaming Regulation Choice of decoupling method 10 th August 2012 Page 1 (10) Executive Summary TI shares BEREC s view that it would be inappropriate to

Telecom Italia response to BEREC Consultations on Roaming Regulation Choice of decoupling method 10 th August 2012 Page 1 (10) Executive Summary TI shares BEREC s view that it would be inappropriate to

THE FUTURE OF REGULATORS

LATINOAMERICAN TELECOM REGULATORS FORUM REGULATOR S ASSOCIATIONS MEETING THE FUTURE OF REGULATORS Colombo, Sri Lanka, Oct. 2012 Gustavo Peña Quiñones, General Secretary CONTENTS REGULATING THE ICT WORLD

LATINOAMERICAN TELECOM REGULATORS FORUM REGULATOR S ASSOCIATIONS MEETING THE FUTURE OF REGULATORS Colombo, Sri Lanka, Oct. 2012 Gustavo Peña Quiñones, General Secretary CONTENTS REGULATING THE ICT WORLD

ETNO response on BEREC consultation BoR (13) 186

186") ETNO response on BEREC consultation BoR (13) 186 February 2014 Executive Summary ETNO welcomes the review of BEREC s common position on geographical aspects of market analysis. ETNO believes that BEREC

ETNO response on BEREC consultation BoR (13) 186 February 2014 Executive Summary ETNO welcomes the review of BEREC s common position on geographical aspects of market analysis. ETNO believes that BEREC

Undue discrimination by SMP providers How Ofcom will investigate potential contraventions on competition grounds of Requirements not to unduly

Undue discrimination by SMP providers How Ofcom will investigate potential contraventions on competition grounds of Requirements not to unduly discriminate imposed on SMP providers Publication date: 15

Undue discrimination by SMP providers How Ofcom will investigate potential contraventions on competition grounds of Requirements not to unduly discriminate imposed on SMP providers Publication date: 15

Public Consultation on the Review of the Significant Market Power (SMP) Guidelines

Guidelines") Contribution ID: 48deea53-5371-4330-9994-3169fe71667b Date: 23/06/2017 17:57:54 Public Consultation on the Review of the Significant Market Power (SMP) Guidelines 1 Objective of the public consultation

Contribution ID: 48deea53-5371-4330-9994-3169fe71667b Date: 23/06/2017 17:57:54 Public Consultation on the Review of the Significant Market Power (SMP) Guidelines 1 Objective of the public consultation

OPERATOR STRATEGIES FOR THE esim ERA: OPPORTUNITIES IN DEVICE BUNDLING, SALES CHANNELS AND WHOLESALE

RESEARCH STRATEGY REPORT OPERATOR STRATEGIES FOR THE esim ERA: OPPORTUNITIES IN DEVICE BUNDLING, SALES CHANNELS AND WHOLESALE KEREM ARSAL analysysmason.com About this report An esim is an embedded (although

RESEARCH STRATEGY REPORT OPERATOR STRATEGIES FOR THE esim ERA: OPPORTUNITIES IN DEVICE BUNDLING, SALES CHANNELS AND WHOLESALE KEREM ARSAL analysysmason.com About this report An esim is an embedded (although

Arab Regional Forum on Future Networks Regulatory and Policy Aspects in Converged Networks. Rabat Morocco

Arab Regional Forum on Future Networks Regulatory and Policy Aspects in Converged Networks Rabat Morocco 19-20 May2015 1 Arab Regional Forum on Future Networks Regulatory and Policy Aspects in Converged

Arab Regional Forum on Future Networks Regulatory and Policy Aspects in Converged Networks Rabat Morocco 19-20 May2015 1 Arab Regional Forum on Future Networks Regulatory and Policy Aspects in Converged

GSMA REGULATORY POSITION ON DRONES. August 2017

GSMA REGULATORY POSITION ON DRONES August 2017 GSMA Messages to EASA Consultation GSMA welcomes the opportunity to contribute to EASA s consultation on the Introduction of a regulatory framework for the

GSMA REGULATORY POSITION ON DRONES August 2017 GSMA Messages to EASA Consultation GSMA welcomes the opportunity to contribute to EASA s consultation on the Introduction of a regulatory framework for the

A well-functioning mobile switching process should allow for an MNP system comprising of the following elements:

Brussels, August 17 2010 The Mobile Challengers would like to raise some issues following the recent consultation on BEREC s draft report on best practices to facilitate switching. The Mobile Challengers

Brussels, August 17 2010 The Mobile Challengers would like to raise some issues following the recent consultation on BEREC s draft report on best practices to facilitate switching. The Mobile Challengers

BoR (14) 73. BEREC Common Position on geographical aspects of market analysis (definition and remedies)

73. BEREC Common Position on geographical aspects of market analysis (definition and remedies)") BEREC Common Position on geographical aspects of market analysis (definition and remedies) 5 June 2014 Contents Executive summary... 3 I. Introduction... 6 II. Basic principles... 7 III. Main cases since

BEREC Common Position on geographical aspects of market analysis (definition and remedies) 5 June 2014 Contents Executive summary... 3 I. Introduction... 6 II. Basic principles... 7 III. Main cases since