Section 1.2 Introduction to Economics

|

|

|

- Gillian Reed

- 6 years ago

- Views:

Transcription

1 Section 1.2 Introduction to Economics

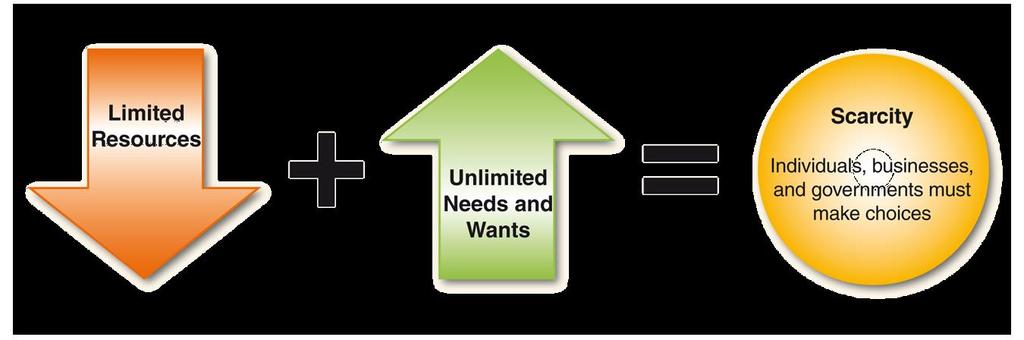

2 Economics Economics is a science that examines how goods and services are produced, sold, and used All economic resources are limited; needs and wants are unlimited Factors of production are the economic resources a nation uses to make goods and supply services for its population Land, labor, capital, and entrepreneurship

3 Economics Land includes all of a nation s natural resources; raw materials found in nature Labor is the work performed by people in organizations; human resources Capital is all the tools, equipment, and machinery used to produce goods or provide services Capital goods are products businesses use to produce final products for consumers Entrepreneurship is the willingness and ability to start a new business People who start new businesses are entrepreneurs

4 Economics Economic problem: Unlimited wants cannot be filled with limited resources Scarcity develops when demand is higher than the available resources Trade-off is when something is given up in order to gain something else Opportunity cost is the value of the next best option that was not selected Value is the relative worth of something

5 Economics

6 Economics Systematic decisionmaking is a process of choosing an option after evaluating the available information and weighing the costs and benefits of the alternatives

7 Economic Systems Economic system is an organized way in which a nation chooses to use its resources to create goods and services Scarcity leads to three economic questions: What should we produce? How should we produce it? For whom should we produce it?

8 Economic Systems In a traditional economy, economic decisions are based on a society s values, culture, and customs Large rural populations that rely on farming and hunting activities to meet needs Little or no manufacturing People barter for goods or services

9 Economic Systems In a command economy, government makes all economic decisions for its citizens Centrally-planned economy Found in communist or socialist societies Government owns and controls all factors of production, decides quantity of production, and sets prices

10 Economic Systems In a market economy, individuals are free to make their own economic decisions Free enterprise or private enterprise Capitalism is an economic system where the economic resources are privately owned by individuals rather than the government

11 Economic Systems Characteristics of a free enterprise system

12 Economic Systems In a mixed economy, both government and individuals make decisions about economic resources Level of government involvement in mixed economies can vary

13 Market Forces Market forces are economic factors that affect the price, demand, and availability of a good or service Include supply and demand, the profit motive, and competition Law of supply and demand Price of a product is determined by the relationship of the supply of a product and the demand for the product Market price is determined at the point where supply equals demand for a product; this point is called equilibrium

14 Market Forces

15 Market Forces Supply curve Producers supply greater quantity at higher prices Demand curve Consumers buy fewer goods at higher prices When demand is greater than supply, a shortage develops When demand is less than supply, a surplus develops

Things people like and desire.

1 Wants 1 Things people like and desire. 2 Needs 2 Things you must have to live. 3 Scarcity 3 When there is not enough for all who want it. 4 Choice 4 To make a decision. 5 Goods 5 Things that can satisfy

1 Wants 1 Things people like and desire. 2 Needs 2 Things you must have to live. 3 Scarcity 3 When there is not enough for all who want it. 4 Choice 4 To make a decision. 5 Goods 5 Things that can satisfy

After studying this chapter you will be able to

3 Demand and Supply After studying this chapter you will be able to Describe a competitive market and think about a price as an opportunity cost Explain the influences on demand Explain the influences

3 Demand and Supply After studying this chapter you will be able to Describe a competitive market and think about a price as an opportunity cost Explain the influences on demand Explain the influences

Unit 2 Economics. Chapter 3 Political and Economic Analysis Chapter 4 Global Analysis

Unit 2 Economics Chapter 3 Political and Economic Analysis Chapter 4 Global Analysis Chapter 3 Political and Economic Analysis Section 3.1 What Is an Economy? Section 3.2 Understanding the Economy What

Unit 2 Economics Chapter 3 Political and Economic Analysis Chapter 4 Global Analysis Chapter 3 Political and Economic Analysis Section 3.1 What Is an Economy? Section 3.2 Understanding the Economy What

Contemporary s Economics McGraw Hill Wright Group 2006 Alignment to Arizona Social Studies Standards Strand 5: Economics

Concept 1: Foundations of Economics The foundations of economics are the application of basic economic concepts and decision-making skills. This includes scarcity and the different methods of allocation

Concept 1: Foundations of Economics The foundations of economics are the application of basic economic concepts and decision-making skills. This includes scarcity and the different methods of allocation

Factors that Lead to Economic Growth

Factors that Lead to Economic Growth E.Q: What are the 4 factors of production and how does it affect the GDP? DEFINING FACTORS OF PRODUCTION Factors of production are resources used to produce goods and

Factors that Lead to Economic Growth E.Q: What are the 4 factors of production and how does it affect the GDP? DEFINING FACTORS OF PRODUCTION Factors of production are resources used to produce goods and

Entrepreneurship. & the Economy. Section 2.1 Importance of. Entrepreneurship. in the Economy Section 2.2 Thinking Globally, Acting Locally CHAPTER

CHAPTER Entrepreneurship & the Economy Section 2.1 Importance of Entrepreneurship in the Economy Section 2.2 Thinking Globally, Acting Locally SECTION Importance of Entrepreneurship in the Economy OBJECTIVES

CHAPTER Entrepreneurship & the Economy Section 2.1 Importance of Entrepreneurship in the Economy Section 2.2 Thinking Globally, Acting Locally SECTION Importance of Entrepreneurship in the Economy OBJECTIVES

Exploring the World of Business and Economics

Chapter 1 Exploring the World of Business and Economics 1 Discuss what you must do to be successful in the world of business. 2 Define business and identify potential risks and rewards. 3 Define economics

Chapter 1 Exploring the World of Business and Economics 1 Discuss what you must do to be successful in the world of business. 2 Define business and identify potential risks and rewards. 3 Define economics

Supply and Demand: CHAPTER Theory

3 Supply and Demand: CHAPTER Theory Markets and Prices A market is any arrangement that enables buyers and sellers to get information and do business with each other. A competitive market is a market that

3 Supply and Demand: CHAPTER Theory Markets and Prices A market is any arrangement that enables buyers and sellers to get information and do business with each other. A competitive market is a market that

Unit 1: Fundamental Concepts. Types of Economic Systems. Types of Economic Systems

Unit 1: Fundamental Concepts 1-2 Economic Systems 1 Ch. 2 Types of Economic Systems An economic system is the way in which a society uses its resources to satisfy its people s unlimited wants. An economic

Unit 1: Fundamental Concepts 1-2 Economic Systems 1 Ch. 2 Types of Economic Systems An economic system is the way in which a society uses its resources to satisfy its people s unlimited wants. An economic

Test Yourself: Basic Terminology. If all economists were laid end to end, they would still not reach a conclusion. GB Shaw

Test Yourself: Basic Terminology If all economists were laid end to end, they would still not reach a conclusion. GB Shaw What is economics? What is macroeconomics? What is microeconomics? Economics is

Test Yourself: Basic Terminology If all economists were laid end to end, they would still not reach a conclusion. GB Shaw What is economics? What is macroeconomics? What is microeconomics? Economics is

Economic Systems. E.Q: What are the 3 questions each country must answer to decide on its economic system?

Economic Systems E.Q: What are the 3 questions each country must answer to decide on its economic system? Different Economic Systems Scarcity refers to the limited supply of something Every country must

Economic Systems E.Q: What are the 3 questions each country must answer to decide on its economic system? Different Economic Systems Scarcity refers to the limited supply of something Every country must

1. List the five factors of production and give and example of each. land labor capital entrepunuership human capital or technology

Intro to Economics Review Name Hour 1. List the five factors of production and give and example of each. land labor capital entrepunuership human capital or technology 2. Describe a situation and then

Intro to Economics Review Name Hour 1. List the five factors of production and give and example of each. land labor capital entrepunuership human capital or technology 2. Describe a situation and then

How is it decided which goods and services will be produced, how they will be produced, and who will buy them?

Chapter 2: The Market System and Circular Flow Learning objectives: Differentiate between laissez-faire capitalism, the command system and the market system. List the main characteristics of the market

Chapter 2: The Market System and Circular Flow Learning objectives: Differentiate between laissez-faire capitalism, the command system and the market system. List the main characteristics of the market

Marginal Analysis. Thinking on the Margin. This is what you do when you make a decision. You weigh your options, and make a choice.

1 Marginal Analysis 6 Thinking on the Margin This is what you do when you make a decision. You weigh your options, and make a choice. If I do this, then I can t do that is it worth it? 7 Marginal Analysis

1 Marginal Analysis 6 Thinking on the Margin This is what you do when you make a decision. You weigh your options, and make a choice. If I do this, then I can t do that is it worth it? 7 Marginal Analysis

Total Test Questions: 80 Levels: Grades Units of Credit:.50

DESCRIPTION This course focuses on the study of economic problems and the methods by which societies solve them. Characteristics of the market economy of the United States and its function in the world

DESCRIPTION This course focuses on the study of economic problems and the methods by which societies solve them. Characteristics of the market economy of the United States and its function in the world

Which term means making decisions based on what you believe to be the best combination of costs and benefits?

Quiz Show Game Which term means making decisions based on what you believe to be the best combination of costs and benefits? Which term means making decisions based on what you believe to be the best combination

Quiz Show Game Which term means making decisions based on what you believe to be the best combination of costs and benefits? Which term means making decisions based on what you believe to be the best combination

Module 5: Trade and Money

1. The Economic Problem What is Scarcity? Available in quantities too small to meet demand. We have to exercise choice because of scarce resources. We all have to make choices because humans have unlimited

1. The Economic Problem What is Scarcity? Available in quantities too small to meet demand. We have to exercise choice because of scarce resources. We all have to make choices because humans have unlimited

Economics Unit 1 Exam Scarcity and Economic Reasoning

Economics Unit 1 Exam Scarcity and Economic Reasoning Multiple Choice (2 points each) Identify the choice that best completes the statement or answers the question. Directions: Use the chart below to answer

Economics Unit 1 Exam Scarcity and Economic Reasoning Multiple Choice (2 points each) Identify the choice that best completes the statement or answers the question. Directions: Use the chart below to answer

2. Which of the following is a distinguishing feature of a market system? A. public ownership of all capital.

Practice Test Chapter 2 1. Which of the following is a distinguishing feature of a command system? A. private ownership of all capital. B. central planning. C. heavy reliance on markets. D. wide-spread

Practice Test Chapter 2 1. Which of the following is a distinguishing feature of a command system? A. private ownership of all capital. B. central planning. C. heavy reliance on markets. D. wide-spread

Production Possibilities, Opportunity Cost, and Economic Growth

Chapter 2 Production Possibilities, Opportunity Cost, and Economic Growth CHAPTER SUMMARY The What, How and For Whom are introduced as the fundamental economic questions that must be addressed by all societies.

Chapter 2 Production Possibilities, Opportunity Cost, and Economic Growth CHAPTER SUMMARY The What, How and For Whom are introduced as the fundamental economic questions that must be addressed by all societies.

1. List the five factors of production and give and example of each. land labor capital entrepreneurship technology

Intro to Economics Review Name Hour 1. List the five factors of production and give and example of each. land labor capital entrepreneurship technology 2. Describe a situation and then explain the opportunity

Intro to Economics Review Name Hour 1. List the five factors of production and give and example of each. land labor capital entrepreneurship technology 2. Describe a situation and then explain the opportunity

Price = The Interaction of Supply and Demand WEDNESDAY, FEBRUARY 17 THURSDAY, FEBRUARY 18

Price = The Interaction of Supply and Demand WEDNESDAY, FEBRUARY 17 THURSDAY, FEBRUARY 18 Chapter 4: Section 1 Understanding Demand What Is Demand? Markets are where people come together to buy and sell

Price = The Interaction of Supply and Demand WEDNESDAY, FEBRUARY 17 THURSDAY, FEBRUARY 18 Chapter 4: Section 1 Understanding Demand What Is Demand? Markets are where people come together to buy and sell

A market economy typically allows producers to decide what they want to produce and how much.

Quizizz Mid Term Review Econ Fund Name : Class : Date : 1. In economics rational decisions occur when a) a budget is used for spending and saving decisions c) marginal benefits equal or exceed marginal

Quizizz Mid Term Review Econ Fund Name : Class : Date : 1. In economics rational decisions occur when a) a budget is used for spending and saving decisions c) marginal benefits equal or exceed marginal

Economics Guided Reading Chapter Two Economic Systems Section 1 Answering the Three Economic Questions

Name: Date: Block # Economics Guided Reading Chapter Two Economic Systems Section 1 Answering the Three Economic Questions Directions Following the page and heading prompts to read your Economics textbook

Name: Date: Block # Economics Guided Reading Chapter Two Economic Systems Section 1 Answering the Three Economic Questions Directions Following the page and heading prompts to read your Economics textbook

OCR Economics A-level

OCR Economics A-level Microeconomics Topic 1: Scarcity and Choice 1.4 Opportunity cost Notes The scarcity of resources gives rise to opportunity cost. The opportunity cost of a choice is the value of the

OCR Economics A-level Microeconomics Topic 1: Scarcity and Choice 1.4 Opportunity cost Notes The scarcity of resources gives rise to opportunity cost. The opportunity cost of a choice is the value of the

Chapter 1 What Is Economics?

Chapter 1 What Is Economics? CHAPTER INTRODUCTION SECTION 1 Scarcity and the Science Scarcity and the Science of Economics SECTION 2 Concepts Basic Economic SECTION 3 Economic Choices and Economic Choices

Chapter 1 What Is Economics? CHAPTER INTRODUCTION SECTION 1 Scarcity and the Science Scarcity and the Science of Economics SECTION 2 Concepts Basic Economic SECTION 3 Economic Choices and Economic Choices

Goal 8 The United States Economic System

Practice Test of Goal 8 The United States Economic System Note to teachers: These unofficial sample questions were created to help students review state Goal 8 content, as well as practice for the Civics

Practice Test of Goal 8 The United States Economic System Note to teachers: These unofficial sample questions were created to help students review state Goal 8 content, as well as practice for the Civics

Principles of Microeconomics , 10e (Case/Fair/Oster) TB2 Chapter 2 The Economic Problem: Scarcity and Choice

TB2 Chapter 2 The Economic Problem: Scarcity and Choice") Principles of Microeconomics, 10e (Case/Fair/Oster) TB2 Chapter 2 The Economic Problem: Scarcity and Choice 2.1 Scarcity, Choice, and Opportunity Cost 1) Production is the process by which A) products

Principles of Microeconomics, 10e (Case/Fair/Oster) TB2 Chapter 2 The Economic Problem: Scarcity and Choice 2.1 Scarcity, Choice, and Opportunity Cost 1) Production is the process by which A) products

EC 201 Lecture Notes 1 Page 1 of 1

EC 201 Lecture Notes 1 Page 1 of 1 ECON 201 - Macroeconomics Lecture Notes 1 Metropolitan State University Allen Bellas The textbooks for this course are Macroeconomics: Principles and Policy by William

EC 201 Lecture Notes 1 Page 1 of 1 ECON 201 - Macroeconomics Lecture Notes 1 Metropolitan State University Allen Bellas The textbooks for this course are Macroeconomics: Principles and Policy by William

Chapter 1: What is Economics? Section 3

Chapter 1: What is Economics? Section 3 Objectives 1. Interpret a production possibilities curve. 2. Explain how production possibilities curves show efficiency, growth, and cost. 3. Explain why a country

Chapter 1: What is Economics? Section 3 Objectives 1. Interpret a production possibilities curve. 2. Explain how production possibilities curves show efficiency, growth, and cost. 3. Explain why a country

PowerPoint to accompany

PowerPoint to accompany Chapter 2 Markets, Demand and Supply Learning Objectives 2.1 Economic systems How do countries differ in the way their economies are organised? 2.2 Demand How much will people buy

PowerPoint to accompany Chapter 2 Markets, Demand and Supply Learning Objectives 2.1 Economic systems How do countries differ in the way their economies are organised? 2.2 Demand How much will people buy

Needs and Wants. Want: something we would like to have (but you can live without) Need: something we can t live without. Food, water, air, shelter

Need: something we can t live without. Food, water, air, shelter") Basics of Economics SS6E5 The student will analyze different economic systems. a. Compare how traditional, command, and market economies answer the economic questions of 1 what to produce, 2 how to produce,

Basics of Economics SS6E5 The student will analyze different economic systems. a. Compare how traditional, command, and market economies answer the economic questions of 1 what to produce, 2 how to produce,

Professor Christina Romer. LECTURE 3 SUPPLY AND DEMAND FRAMEWORK January 24, 2017

Economics 2 Spring 2017 Professor Christina Romer Professor David Romer LECTURE 3 SUPPLY AND DEMAND FRAMEWORK January 24, 2017 I. INTRODUCTION TO MARKETS A. Implications of scarcity and the gains from

Economics 2 Spring 2017 Professor Christina Romer Professor David Romer LECTURE 3 SUPPLY AND DEMAND FRAMEWORK January 24, 2017 I. INTRODUCTION TO MARKETS A. Implications of scarcity and the gains from

CHAPTER 3. Economic Challenges Facing Contemporary Business

CHAPTER 3 Economic Challenges Facing Contemporary Business Chapter Summary: Key Concepts Opening Overview Economics Microeconomics Macroeconomics A social science that analyzes the choices people and governments

CHAPTER 3 Economic Challenges Facing Contemporary Business Chapter Summary: Key Concepts Opening Overview Economics Microeconomics Macroeconomics A social science that analyzes the choices people and governments

Level 1 Economics, 2013

90986 909860 1SUPERVISOR S Level 1 Economics, 2013 90986 Demonstrate understanding of how consumer, producer and / or government choices affect society, using market equilibrium 9.30 am Tuesday 26 November

90986 909860 1SUPERVISOR S Level 1 Economics, 2013 90986 Demonstrate understanding of how consumer, producer and / or government choices affect society, using market equilibrium 9.30 am Tuesday 26 November

IGCSE Business Studies

IGCSE Business Studies Chapter 1 The Purpose of Business Activity Identifying Goods and Services Think of this situation You are at a supermarket. What do you see? Make a list of what you see. Identifying

IGCSE Business Studies Chapter 1 The Purpose of Business Activity Identifying Goods and Services Think of this situation You are at a supermarket. What do you see? Make a list of what you see. Identifying

Multiple Choice Identify the letter of the choice that best completes the statement or answers the question.

Final day 2 Multiple Choice Identify the letter of the choice that best completes the statement or answers the question. 1. What determines how a change in prices will affect total revenue for a company?

Final day 2 Multiple Choice Identify the letter of the choice that best completes the statement or answers the question. 1. What determines how a change in prices will affect total revenue for a company?

Econ 101, sections 2 and 6, S06 Schroeter Exam #2, Red. Choose the single best answer for each question.

Econ 101, sections 2 and 6, S06 Schroeter Exam #2, Red Choose the single best answer for each question. 1. If the own-price elasticity of demand for a good is -2.0, this implies that consumers would a.

Econ 101, sections 2 and 6, S06 Schroeter Exam #2, Red Choose the single best answer for each question. 1. If the own-price elasticity of demand for a good is -2.0, this implies that consumers would a.

2. New words or definitions are highlighted in italics in the text. Other key points are highlighted in bold type.

1 How to Study for Class 2 Class 2 introduces two important concepts. The first is that opportunity costs rise as more of something is done. The second involves the manner by which rational decisions are

1 How to Study for Class 2 Class 2 introduces two important concepts. The first is that opportunity costs rise as more of something is done. The second involves the manner by which rational decisions are

Macroeconomics, 4e (Hubbard/O'Brien) Chapter 1 Economics: Foundations and Models. 1.3 Economic Models

Chapter 1 Economics: Foundations and Models. 1.3 Economic Models") Macroeconomics, 4e (Hubbard/O'Brien) Chapter 1 Economics: Foundations and Models 1.3 Economic Models 1) Economic models do all of the following except A) answer economic questions. B) portray reality in

Macroeconomics, 4e (Hubbard/O'Brien) Chapter 1 Economics: Foundations and Models 1.3 Economic Models 1) Economic models do all of the following except A) answer economic questions. B) portray reality in

Economics Challenge Online State Qualification Practice Test. 1. An increase in aggregate demand would tend to result from

1. An increase in aggregate demand would tend to result from A. an increase in tax rates. B. a decrease in consumer spending. C. a decrease in net export spending. D. an increase in business investment.

1. An increase in aggregate demand would tend to result from A. an increase in tax rates. B. a decrease in consumer spending. C. a decrease in net export spending. D. an increase in business investment.

Social Studies Curriculum Guide GRADE 12 ECONOMICS

Social Studies Curriculum Guide GRADE 12 ECONOMICS It is the policy of the Fulton County School System not to discriminate on the basis of race, color, sex, religion, national origin, age, or disability

Social Studies Curriculum Guide GRADE 12 ECONOMICS It is the policy of the Fulton County School System not to discriminate on the basis of race, color, sex, religion, national origin, age, or disability

Supply and Demand. Price and Quantity. Demand. The Law of Demand. Coach Burnett AP Macroeconomics

upply and emand Coach Burnett A Macroeconomics 1 rice and uantity rice - the amount of money paid for an economic good/service. Ex. A gallon of gas is roughly $3.00 a gallon (national average) OUCH!!!

upply and emand Coach Burnett A Macroeconomics 1 rice and uantity rice - the amount of money paid for an economic good/service. Ex. A gallon of gas is roughly $3.00 a gallon (national average) OUCH!!!

1.3. Levels and Rates of Change Levels: example, wages and income versus Rates: example, inflation and growth Example: Box 1.3

1 Chapter 1 1.1. Scarcity, Choice, Opportunity Cost Definition of Economics: Resources versus Wants Wants: more and better unlimited Versus Needs: essential limited Versus Demand: ability to pay + want

1 Chapter 1 1.1. Scarcity, Choice, Opportunity Cost Definition of Economics: Resources versus Wants Wants: more and better unlimited Versus Needs: essential limited Versus Demand: ability to pay + want

Chapter 1. The Art and Science of Economic Analysis. These slides supplement the textbook, but should not replace reading the textbook

Chapter 1 The Art and Science of Economic Analysis These slides supplement the textbook, but should not replace reading the textbook What is the economic problem? Because we live in a world of scarce resources,

Chapter 1 The Art and Science of Economic Analysis These slides supplement the textbook, but should not replace reading the textbook What is the economic problem? Because we live in a world of scarce resources,

This image cannot currently be displayed. Course Catalog. Career and Technical Education Series: Small Business Entrepreneurship Glynlyon, Inc.

This image cannot currently be displayed. Course Catalog Career and Technical Education Series: Small Business Entrepreneurship 2016 Glynlyon, Inc. Table of Contents COURSE OVERVIEW... 1 UNIT 1: OVERVIEW

This image cannot currently be displayed. Course Catalog Career and Technical Education Series: Small Business Entrepreneurship 2016 Glynlyon, Inc. Table of Contents COURSE OVERVIEW... 1 UNIT 1: OVERVIEW

Chapter 1. Introduction

Chapter 1 You must have already been introduced to a study of basic microeconomics. This chapter begins by giving you a simplified account of how macroeconomics differs from the microeconomics that you

Chapter 1 You must have already been introduced to a study of basic microeconomics. This chapter begins by giving you a simplified account of how macroeconomics differs from the microeconomics that you

D. People would continue to consume the same amount of the good.

17. Because prices serve as incentives in a market economy, which of the following would be a likely result of a large increase in the price of a good? A. People would increase their consumption of the

17. Because prices serve as incentives in a market economy, which of the following would be a likely result of a large increase in the price of a good? A. People would increase their consumption of the

Econ 200 Lecture 4 April 12, 2016

Econ 200 Lecture 4 April 12, 2016 0. Learning Catalytics Session 62335486 1. Change in Demand 2. Supply and the Law of Supply 3. Changes in Supply 4. Equilibrium Putting Supply and Demand Together 5. Impact

Econ 200 Lecture 4 April 12, 2016 0. Learning Catalytics Session 62335486 1. Change in Demand 2. Supply and the Law of Supply 3. Changes in Supply 4. Equilibrium Putting Supply and Demand Together 5. Impact

AP Microeconomics Review With Answers

AP Microeconomics Review With Answers 1. Firm in Perfect Competition (Long-Run Equilibrium) 2. Monopoly Industry with comparison of price & output of a Perfectly Competitive Industry (which means show

AP Microeconomics Review With Answers 1. Firm in Perfect Competition (Long-Run Equilibrium) 2. Monopoly Industry with comparison of price & output of a Perfectly Competitive Industry (which means show

Chapter 2 Production Possibilities, Opportunity Cost,

Chapter 2 Production Possibilities, Opportunity Cost, and Economic Growth CHAPTER IN A NUTSHELL In this chapter, you continue your quest to learn the economic way of thinking. The chapter begins with the

Chapter 2 Production Possibilities, Opportunity Cost, and Economic Growth CHAPTER IN A NUTSHELL In this chapter, you continue your quest to learn the economic way of thinking. The chapter begins with the

Flip Comparing Economic Systems

Flip Comparing Economic Systems In small groups (3-4) answer the following for A King of Long Ago and The Communist Manifesto 1. Who makes the major decisions? 2. What degree of Economic Freedom do citizens

Flip Comparing Economic Systems In small groups (3-4) answer the following for A King of Long Ago and The Communist Manifesto 1. Who makes the major decisions? 2. What degree of Economic Freedom do citizens

The Foundations of Microeconomics

The Foundations of Microeconomics D I A N N A D A S I L V A - G L A S G O W D E P A R T M E N T O F E C O N O M I C S U N I V E R S I T Y O F G U Y A N A 1 4 S E P T E M B E R, 2 0 1 7 Wk 3 Lectures I

The Foundations of Microeconomics D I A N N A D A S I L V A - G L A S G O W D E P A R T M E N T O F E C O N O M I C S U N I V E R S I T Y O F G U Y A N A 1 4 S E P T E M B E R, 2 0 1 7 Wk 3 Lectures I

Chapter 2 Economic Systems and Decision Making

Chapter 2 Economic Systems and Decision Making CHAPTER INTRODUCTION SECTION 1 SECTION 2 SECTION 3 Economic Systems Evaluating Economic Performance Capitalism and Economic Freedom CHAPTER SUMMARY CHAPTER

Chapter 2 Economic Systems and Decision Making CHAPTER INTRODUCTION SECTION 1 SECTION 2 SECTION 3 Economic Systems Evaluating Economic Performance Capitalism and Economic Freedom CHAPTER SUMMARY CHAPTER

EFFICIENCY OF MARKETS

7 CONSUMERS, PRODUCERS, AND EFFICIENCY OF MARKETS Problems and Applications 1. If a drought in Nova Scotia reduces the apple harvest, the supply curve for apples shifts to the left, as shown in Figure

7 CONSUMERS, PRODUCERS, AND EFFICIENCY OF MARKETS Problems and Applications 1. If a drought in Nova Scotia reduces the apple harvest, the supply curve for apples shifts to the left, as shown in Figure

Market Equilibrium: Part II

Market Equilibrium: Part II Announcements PS #4 is posted on web page. It is big and not all questions are very easy. It is time to start studying. PS#5 will be even bigger. (also more challenging) A sample

Market Equilibrium: Part II Announcements PS #4 is posted on web page. It is big and not all questions are very easy. It is time to start studying. PS#5 will be even bigger. (also more challenging) A sample

Slides and Images, Worth Publishers Inc. 8-1

Perfect Competition Michael J. Murray Slides and Images, Worth Publishers Inc. 8-1 Market Structure Analysis By observing a few industry characteristics, we can predict pricing and output behavior of the

Perfect Competition Michael J. Murray Slides and Images, Worth Publishers Inc. 8-1 Market Structure Analysis By observing a few industry characteristics, we can predict pricing and output behavior of the

EOCT Test Semester 2 final

EOCT Test Semester 2 final 1. The best definition of Economics is a. The study of how individuals spend their money b. The study of resources and government c. The study of the allocation of scarce resources

EOCT Test Semester 2 final 1. The best definition of Economics is a. The study of how individuals spend their money b. The study of resources and government c. The study of the allocation of scarce resources

Demand, Supply, and Price

Demand, Supply, and Price The amount of a good or service that we demand, the amount of a good or service that suppliers supply, and the price of a good or service all affect one another. Let's examine

Demand, Supply, and Price The amount of a good or service that we demand, the amount of a good or service that suppliers supply, and the price of a good or service all affect one another. Let's examine

Lecture 1: Introduction

Lecture 1: Introduction Yulei Luo SEF of HKU January 19, 2013 Luo, Y. (SEF of HKU) ECON1002C/D January 19, 2013 1 / 16 Economics, Microeconomics and Macroeconomics Economics: The study of the choices people

Lecture 1: Introduction Yulei Luo SEF of HKU January 19, 2013 Luo, Y. (SEF of HKU) ECON1002C/D January 19, 2013 1 / 16 Economics, Microeconomics and Macroeconomics Economics: The study of the choices people

Grade 9 EMS Demand and Supply

Grade 9 EMS Demand and Supply Name: Class Teach a parrot the terms "supply and demand" and you've got an economist. - Thomas Carlyle Demand and Supply booklet 2014 Shifts Vs. Movements In Demand and Supply

Grade 9 EMS Demand and Supply Name: Class Teach a parrot the terms "supply and demand" and you've got an economist. - Thomas Carlyle Demand and Supply booklet 2014 Shifts Vs. Movements In Demand and Supply

Introduction. Learning Objectives. Learning Objectives. Chapter 2. Scarcity and the World of Trade-Offs

Chapter 2 and the World of Trade-Offs Introduction Society always faces choices regarding use of its scarce resources. The need to devote more law enforcement resources to antiterrorism efforts means that

Chapter 2 and the World of Trade-Offs Introduction Society always faces choices regarding use of its scarce resources. The need to devote more law enforcement resources to antiterrorism efforts means that

1. Welfare economics is the study of a. the well-being of less fortunate people. b. welfare programs in the United States.

1. Welfare economics is the study of a. the well-being of less fortunate people. b. welfare programs in the United States. c. the effect of income redistribution on work effort. d. how the allocation of

1. Welfare economics is the study of a. the well-being of less fortunate people. b. welfare programs in the United States. c. the effect of income redistribution on work effort. d. how the allocation of

Econ Test 2B Dr. Rupp Tuesday, March 3, 2009 Pledge: I have neither given or received aid on this exam Signature

Econ 2113 - Test 2B Dr. Rupp Tuesday, March 3, 2009 Name Pledge: I have neither given or received aid on this exam Signature Multiple Choice Identify the letter of the choice that best completes the statement

Econ 2113 - Test 2B Dr. Rupp Tuesday, March 3, 2009 Name Pledge: I have neither given or received aid on this exam Signature Multiple Choice Identify the letter of the choice that best completes the statement

ECONOMICS (Povletich) Unit 1 Review Sheet Introduction to Economics

Unit 1 Review Sheet Introduction to Economics") ECONOMICS (Povletich) Unit 1 Review Sheet Introduction to Economics There will be 30-40 multiple choice questions and 4-5 free-response questions on your test that will take place on Tuesday 2/9 (periods

ECONOMICS (Povletich) Unit 1 Review Sheet Introduction to Economics There will be 30-40 multiple choice questions and 4-5 free-response questions on your test that will take place on Tuesday 2/9 (periods

12 ECONOMICS 3 MARKS MATERIAL LESSON 1 1. State Alfred Marshall s definition of Economics? Alfred Marshall defines; economics as a study of mankind in the ordinary business of Life 2. What is the main

12 ECONOMICS 3 MARKS MATERIAL LESSON 1 1. State Alfred Marshall s definition of Economics? Alfred Marshall defines; economics as a study of mankind in the ordinary business of Life 2. What is the main

FIRST INTRODUCTION TO. Dr. Mohammed A. Alwosabi. ECON140: Microeconomics Ch.1 Dr. Mohammed Alwosabi. Chapter 1

Chapter 1 FIRST INTRODUCTION TO ECONOMICS Dr. Mohammed A. Alwosabi 1 The Fundamental Problem of Economics: Scarcity and Choice It is a fact of life that we cannot get everything we want. We all want more

Chapter 1 FIRST INTRODUCTION TO ECONOMICS Dr. Mohammed A. Alwosabi 1 The Fundamental Problem of Economics: Scarcity and Choice It is a fact of life that we cannot get everything we want. We all want more

Supply, Demand, and Government Policies. Copyright 2004 South-Western

Supply, Demand, and Government Policies Copyright 2004 South-Western Supply, Demand, and Government Policies In a free, unregulated market system, market forces establish equilibrium prices and exchange

Supply, Demand, and Government Policies Copyright 2004 South-Western Supply, Demand, and Government Policies In a free, unregulated market system, market forces establish equilibrium prices and exchange

AS Economics. Introductory Microeconomics. Sixth Form pre-reading

AS Economics Introductory Microeconomics Sixth Form pre-reading The economic problem Economics is a social science which studies how humans behave when faced by the economic problem of scarcity. Economic

AS Economics Introductory Microeconomics Sixth Form pre-reading The economic problem Economics is a social science which studies how humans behave when faced by the economic problem of scarcity. Economic

Problem Set #2 - Answers. Due February 2, 2000

S/Econ 573 roblem Set # - Answers age 1 of 11 roblem Set # - Answers ue February, [Numbers in brackets are the points allocated in the grading. There are 13 points total] 1. [19]In the figure at the right

S/Econ 573 roblem Set # - Answers age 1 of 11 roblem Set # - Answers ue February, [Numbers in brackets are the points allocated in the grading. There are 13 points total] 1. [19]In the figure at the right

Golspie High School. Business Management National 4/5. Understanding Business 1 Role of business in society Pupil Notes

Golspie High School Business Management National 4/5 Understanding Business 1 Role of business in society Pupil Notes Understanding Business Role of business in society National 5 how businesses satisfy

Golspie High School Business Management National 4/5 Understanding Business 1 Role of business in society Pupil Notes Understanding Business Role of business in society National 5 how businesses satisfy

Economics: Foundations and Models

R. GLENN HUBBARD ANTHONY PATRICK O BRIEN Macroeconomics FOURTH EDITION CHAPTER 1 Economics: Foundations and Models Chapter Outline and Learning Objectives 1.1 Three Key Economic Ideas 1.2 The Economic

R. GLENN HUBBARD ANTHONY PATRICK O BRIEN Macroeconomics FOURTH EDITION CHAPTER 1 Economics: Foundations and Models Chapter Outline and Learning Objectives 1.1 Three Key Economic Ideas 1.2 The Economic

2010 Pearson Education Canada

What Is Perfect Competition? Perfect competition is an industry in which Many firms sell identical products to many buyers. There are no restrictions to entry into the industry. Established firms have

What Is Perfect Competition? Perfect competition is an industry in which Many firms sell identical products to many buyers. There are no restrictions to entry into the industry. Established firms have

Opportunity Cost. First quiz on Monday. Your First Job Ten Principles Scarcity Opportunity Cost. Fundamental Economic Concepts and Reasoning

Opportunity Cost First quiz on Monday. Your First Job Ten Principles Scarcity Opportunity Cost Fundamental Economic Concepts and Reasoning But first, a review of scarcity https://www.youtube.com/watch?v=np-dzsdzymk&li

Opportunity Cost First quiz on Monday. Your First Job Ten Principles Scarcity Opportunity Cost Fundamental Economic Concepts and Reasoning But first, a review of scarcity https://www.youtube.com/watch?v=np-dzsdzymk&li

Entrepreneurship Pacing Guide Time Frame Topic Competency/Essential Knowledge Unit Formative Assessments

Entrepreneurship Pacing Guide Time Frame Topic Competency/Essential Knowledge Unit Formative Assessments 3 Weeks Entrepreneurs and Entrepreneurial Opportunities What is entrepreneurship? Who are entrepreneurs?

Entrepreneurship Pacing Guide Time Frame Topic Competency/Essential Knowledge Unit Formative Assessments 3 Weeks Entrepreneurs and Entrepreneurial Opportunities What is entrepreneurship? Who are entrepreneurs?

IB Economics Competitive Markets: Demand and Supply 1.4: Price Signals and Market Efficiency

IB Economics: www.ibdeconomics.com 1.4 PRICE SIGNALS AND MARKET EFFICIENCY: STUDENT LEARNING ACTIVITY Answer the questions that follow. 1. DEFINITIONS Define the following terms: [10 marks] Allocative

IB Economics: www.ibdeconomics.com 1.4 PRICE SIGNALS AND MARKET EFFICIENCY: STUDENT LEARNING ACTIVITY Answer the questions that follow. 1. DEFINITIONS Define the following terms: [10 marks] Allocative

Types of Economic Systems

Name: Period: Types of Economic Systems What is an Economy? Economy: or exchange of goods and services by a group : things to be traded, bought, or sold : work done in exchange for payment : work force,

Name: Period: Types of Economic Systems What is an Economy? Economy: or exchange of goods and services by a group : things to be traded, bought, or sold : work done in exchange for payment : work force,

Personal Financial Literacy TEKS. Social Studies TEKS/Economics Strand

Personal Financial Literacy TEKS Kindergarten mathematical process standards to manage one's financial resources effectively for lifetime financial security. The student is expected to: K.9A identify ways

Personal Financial Literacy TEKS Kindergarten mathematical process standards to manage one's financial resources effectively for lifetime financial security. The student is expected to: K.9A identify ways

Economics 110 Midterm #2 Practice Multiple Choice Qs Spring 2014

Midterm #2 Practice Multiple Choice Questions: Elasticity is a. a measure of how much buyers and sellers respond to changes in market conditions. b. the study of how the allocation of resources affects

Midterm #2 Practice Multiple Choice Questions: Elasticity is a. a measure of how much buyers and sellers respond to changes in market conditions. b. the study of how the allocation of resources affects

Economic System & Factors of Economic Growth

Economic System & Factors of Economic Growth Standards SS6E1 The student will analyze different economic systems. a. Compare how traditional, command, and market, economies answer the economic questions

Economic System & Factors of Economic Growth Standards SS6E1 The student will analyze different economic systems. a. Compare how traditional, command, and market, economies answer the economic questions

What s Going on in the graph below?

Unit 2: Basic Econmic Principles: Supply, Demand & the U.S. Economy Lesson 3: Circular Flow Model & Factors of Production The fundamental decision making units in a market economy are firms and households.

Unit 2: Basic Econmic Principles: Supply, Demand & the U.S. Economy Lesson 3: Circular Flow Model & Factors of Production The fundamental decision making units in a market economy are firms and households.

Are You Satisfied? Leadership, Attitude, Performance...making learning pay! LAP 6 Performance Indicator: EC:001

AP Economics Leadership, Attitude, Performance...making learning pay! LAP 6 Performance Indicator: EC:001 Are You Satisfied? Economics and Economic Activities Using Scarce Resources Consider the Opportunity

AP Economics Leadership, Attitude, Performance...making learning pay! LAP 6 Performance Indicator: EC:001 Are You Satisfied? Economics and Economic Activities Using Scarce Resources Consider the Opportunity

MULTIPLE CHOICE. Choose the one alternative that best completes the statement or answers the question. FIGURE 1-2

Questions of this SAMPLE exam were randomly chosen and may NOT be representative of the difficulty or focus of the actual examination. The professor did NOT review these questions. MULTIPLE CHOICE. Choose

Questions of this SAMPLE exam were randomly chosen and may NOT be representative of the difficulty or focus of the actual examination. The professor did NOT review these questions. MULTIPLE CHOICE. Choose

Chapter 2 Market forces: Demand and Supply Demand

Chapter 2 Market forces: Demand and Supply Demand Market demand curve A curve indicating the total quantity of a good all consumers are willing and able to purchase at each possible price, holding the

Chapter 2 Market forces: Demand and Supply Demand Market demand curve A curve indicating the total quantity of a good all consumers are willing and able to purchase at each possible price, holding the

Economics Chapter 1 Section 1 Review (NOT and assignment)

") Name: Class: Date: ID: A Economics Chapter 1 Section 1 Review (NOT and assignment) Matching a. goods e. land b. economics f. capital c. shortage g. services d. labor h. human capital 1. when consumers

Name: Class: Date: ID: A Economics Chapter 1 Section 1 Review (NOT and assignment) Matching a. goods e. land b. economics f. capital c. shortage g. services d. labor h. human capital 1. when consumers

ECONS 101 Introduction to Economics 1

ECONS 101 Introduction to Economics 1 Session 2 Introduction II Lecturer: Mrs. Hellen Seshie-Nasser, Department of Economics Contact Information: haseshie@ug.edu.gh College of Education School of Continuing

ECONS 101 Introduction to Economics 1 Session 2 Introduction II Lecturer: Mrs. Hellen Seshie-Nasser, Department of Economics Contact Information: haseshie@ug.edu.gh College of Education School of Continuing

Supply and Demand Michael Powell, All Rights Reserved

Supply and Demand We have learnt that demand is the amount of a good or service consumers are willing to buy. The opposite of demand is supply. Supply is how much of a good or service a producer (a business)

Supply and Demand We have learnt that demand is the amount of a good or service consumers are willing to buy. The opposite of demand is supply. Supply is how much of a good or service a producer (a business)

OCR Economics AS-level

OCR Economics AS-level Microeconomics Topic 1: Scarcity and Choice 1.1 The basic economic problem Notes Economic and free goods Economic goods benefit society, have the problem of scarcity and have an

OCR Economics AS-level Microeconomics Topic 1: Scarcity and Choice 1.1 The basic economic problem Notes Economic and free goods Economic goods benefit society, have the problem of scarcity and have an

Grades Prentice Hall. Economics Georgia Performance Standards, Economics. Grades 9-12

Prentice Hall Economics 2010 Grades 9-12 C O R R E L A T E D T O Georgia Performance Standards, Economics Grades 9-12 FORMAT FOR CORRELATION TO THE GEORGIA PERFORMANCE STANDARDS Subject Area: Economics

Prentice Hall Economics 2010 Grades 9-12 C O R R E L A T E D T O Georgia Performance Standards, Economics Grades 9-12 FORMAT FOR CORRELATION TO THE GEORGIA PERFORMANCE STANDARDS Subject Area: Economics

Discussion Handout 2 6/22/2016 TA: Anton Babkin

Consumer and Producer Surplus In economics, we assume that trade is mutually beneficial for both the suppliers and consumers of a good. This benefit is typically placed into two categories, consumer and

Consumer and Producer Surplus In economics, we assume that trade is mutually beneficial for both the suppliers and consumers of a good. This benefit is typically placed into two categories, consumer and

AGS Economics Michigan High School Content Expectations for Economics

AGS 2005 Correlated to Michigan High School Content Expectations for 5910 Rice Creek Pkwy, Suite 1000 Shoreview, MN 55126 Copyright 2007 Pearson Education, Inc. or its affiliate(s). All rights reserved.

AGS 2005 Correlated to Michigan High School Content Expectations for 5910 Rice Creek Pkwy, Suite 1000 Shoreview, MN 55126 Copyright 2007 Pearson Education, Inc. or its affiliate(s). All rights reserved.

3 CHAPTER OUTLINE CASE FAIR OSTER PEARSON. Demand, Supply, and Market Equilibrium. Input Markets and Output Markets: The Circular Flow

CASE FAIR OSTER PEARSON PRINCIPLES OF MICROECONOMICS E L E V E N T H E D I T I O N Prepared by: Fernando Quijano w/shelly Tefft 2of 68 Demand, Supply, and Market Equilibrium 3 CHAPTER OUTLINE Firms and

CASE FAIR OSTER PEARSON PRINCIPLES OF MICROECONOMICS E L E V E N T H E D I T I O N Prepared by: Fernando Quijano w/shelly Tefft 2of 68 Demand, Supply, and Market Equilibrium 3 CHAPTER OUTLINE Firms and

FROM CORN TO PLASTIC

FROM CORN TO PLASTIC Lesson Objective By the end of the lesson, students will be able to define the economic concept of scarcity and explain how scarcity and environmental concerns can lead to marketplace

FROM CORN TO PLASTIC Lesson Objective By the end of the lesson, students will be able to define the economic concept of scarcity and explain how scarcity and environmental concerns can lead to marketplace

Problem Set 3. I. Problem 1. Explain each of the following statements using supply-and-demand diagrams.

Problem Set 3 I. Problem 1. Explain each of the following statements using supply-and-demand diagrams. a) When the weather turns warm in New England every summer, the price of hotel rooms in Caribbean

Problem Set 3 I. Problem 1. Explain each of the following statements using supply-and-demand diagrams. a) When the weather turns warm in New England every summer, the price of hotel rooms in Caribbean

Total Test Questions: 80 Levels: Grades Units of Credit:.50

DESCRIPTION This course focuses on the study of economic problems and the methods by which societies solve them. Characteristics of the market economy of the United States and its function in the world

DESCRIPTION This course focuses on the study of economic problems and the methods by which societies solve them. Characteristics of the market economy of the United States and its function in the world

Perfectly Competitive Supply. Chapter 6. Learning Objectives

Perfectly Competitive Supply Chapter 6 McGraw-Hill/Irwin Copyright 2013 by The McGraw-Hill Companies, Inc. All rights reserved. Learning Objectives 1.Explain how opportunity cost is related to the supply

Perfectly Competitive Supply Chapter 6 McGraw-Hill/Irwin Copyright 2013 by The McGraw-Hill Companies, Inc. All rights reserved. Learning Objectives 1.Explain how opportunity cost is related to the supply

Market Equilibrium, the Price Mechanism and Market Efficiency. Chapter 3

Market Equilibrium, the Price Mechanism and Market Efficiency Chapter 3 Equilibrium Equilibrium is defined as a state of rest, self-perpetuating in the absence of any outside disturbance. Example: a book

Market Equilibrium, the Price Mechanism and Market Efficiency Chapter 3 Equilibrium Equilibrium is defined as a state of rest, self-perpetuating in the absence of any outside disturbance. Example: a book

Applications of supply and demand

Applications of supply and demand Comparative statics and government policy Comparative statics The simple supply and demand model we have developed can be used to analyze the effects of many events on

Applications of supply and demand Comparative statics and government policy Comparative statics The simple supply and demand model we have developed can be used to analyze the effects of many events on

TEN PRINCIPLES OF ECONOMICS. The word Economy... An individual economic agent faces many decisions: Intro Macroeconomic Theory Professor Minseong Kim

TEN PRINCIPLES OF ECONOMICS Chapter 1 The word Economy... Comes from a Greek word for one who manages a household. An individual economic agent faces many decisions: Should I go to college or should I

TEN PRINCIPLES OF ECONOMICS Chapter 1 The word Economy... Comes from a Greek word for one who manages a household. An individual economic agent faces many decisions: Should I go to college or should I

Chapter 6:3: The Role of Prices

Chapter 6:3: The Role of Prices In this section, we will see how prices affect consumer behavior and how producers respond. 1Co_6:20 For ye are bought with a price: therefore glorify God in your body,

Chapter 6:3: The Role of Prices In this section, we will see how prices affect consumer behavior and how producers respond. 1Co_6:20 For ye are bought with a price: therefore glorify God in your body,