The Future of Retail Banking

|

|

|

- Evelyn Whitehead

- 6 years ago

- Views:

Transcription

1 The Future of Retail Banking Navigating the digital banking revolution The digital banking landscape Market trends Challenges & opportunities Digital transformation with HID Global

2 43% Mobile phone users with a bank account use mobile banking 1 82% Mobile banking users that have installed their bank s applications 1 43x Greater transaction cost in branch than via mobile 2 Introduction Mobile banking as a channel is growing fast. Its increasing use as a lifestyle engagement tool, links to social media and the rapid growth in mobile payment options, including mobile wallets and contactless payments, has enhanced the customer s experience in the banking world. Most mobile applications supported by banks lead to greater cost efficiency. Reduced manual processing of small-value transactions is a significant advantage. Banks must align fully with new compliance standards (e.g. PSD2, FFIEC, MAS, FSA, BaFin) to ensure secure authentication. Recent developments in mobile banking have enabled banks to create trust alongside added value services, helping to build a remarkable customer experience. 2

3 2 1 3 The digital banking landscape Hyper-connected world on the move Increasingly competitive landscapes Ever-increasing fraud, across multiple channels New regulations There is a greater need for banks to develop an action plan that ensures them a central role in an increasingly digital and interconnected world. According to the World Retail Banking Report 5, banks overwhelmingly agree that their core systems are not able to support the future evolution of banking. In response, they are exploring pathways to transforming their core systems, which will be fundamental in preparing for the digital banking ecosystem of the future. Ever-increasing fraud across multiple channels, coupled with new regulations and competitive landscapes, pose greater challenges for banks. Being productive will allow banks to reduce the risk of being marginalized as the ecosystem evolves. They will also be better equipped to meet rising customer expectations and to offer enhanced experiences and innovative services. 3

4 Market Trends 4

5 2.5B 36% 67% Trend 1 Hyper-connected world on the move Number of smartphones in Increase in smartphone penetration by Population using smartphones in Market digitization is expected to accelerate the use of online mobile channels, creating greater customer loyalty and retention, and therefore positively impacting the bottom and top line for banks. The number of smartphone users is forecast to grow to around 2.5 billion in 2019, with smartphone penetration rates to increase by 67%. The success of mobile wallet solutions and mobile contactless payments are expected to increase the use of mobile phones for banking. This evolving customer demand, caused by the always-on nature of personal smart devices, is forcing banks to look at ways of achieving the convergence of their online and mobile banking offerings to make them more consistent. Drivers The increasing affordability of smartphones, internet services and low-cost data plans, coupled with the rise of smartphone and tablet use over traditional PCs and computers, are driving the adoption of mobile banking. Alongside this, there is a growing need for banks to offer end users flexible, secure financial transactions by providing a functional, easy-to-use customer experience. 5

6 Trend 2 Market landscape Digital and real-time payments Transfer funds between people Access to account provisions Banks have been investing in digital to serve their customers better. However, although 95% of bank executives understand the industry is evolving towards a digital ecosystem, only 13% think their current core systems can sustain such an ecosystem. 5 As Google, Amazon, Facebook and Apple (GAFA) continue to enter the payment market, banks are constantly battling competition from these giants. What s more, Fintechs are rapidly changing customer perceptions and creating market disruption with flexible platforms. 80% of Fintech users say they have had a good experience, compared to 40% of retail banks. 5 Paying with your phone Drivers Asset management Open banking initiatives and open API platforms enable banks to drive speed and cost-effectiveness while creating new revenue models. As a result, customers can access personalized resources and take advantage of better loan terms with improved borrower risk levels, due to historical transactional data. In-person authentication needs to evolve and embrace new technologies in order to accelerate communication between consumers and banks. Open banking standards and APIs help consumers transact, save, borrow, lend and invest their money in better ways than they used to in the past. 6

7 2.55B 77% 45% 92% Global social networks in Fortune 500 with Twitter accounts in Visit their local branch fewer than x5 per year 8 18 to 29 year-olds use social media 8 Trend 3 The rise of the social bank Security enables banks to create trust with their customers while offering new and creative ways for transactions anytime, anywhere. New technologies allow for stronger integration between social media and mobile banking. 69% of respondents to the Accenture 2014 North America Consumer Digital Banking Survey said they are active on social media. According to the same survey, 22% of millennials look for financial service advice via social media. 10 Drivers Instead of looking at social media as a tool for outbound marketing, banks should view it as a tool for personal and relevant interactions with customers. Delivering customer service, financial advice and offers, while allowing customers to provide feedback through social media, can increase engagement and create a stronger customer experience. 7

8 Trend 4 Regulatory changes and complexity Going beyond two-factor authentication A large number of regulations have been introduced to the world, aimed at safeguarding banks and their customers interests. Drivers PCI DSS: Worldwide payment card industry standards* Changing customer preferences and increasing mobility have given rise to free, and fair competition and strengthened consumer protection. Decreasing risk of fines and penalties from non-compliance of regulations is essential for banks. However, current risk management processes are failing to achieve this. Banks must translate these regulatory requirements into management actions to contain risk and protect their clients, while creating a robust market structure with increased transparency. By adopting less risky approaches - granted by new regulations - banks can fully integrate risk management and compliance as a medium to respond to technology changes. * Not a fully comprehensive list of all worldwide regulations 8

9 Challenges As financial institutions adapt to evolving demands in today s market, delivering innovative new services becomes imperative to stay ahead of the competition. This new era of digital banking brings compelling challenges that impact user experience, regulatory compliance and operational effectiveness, while also providing new opportunities for growth. TRENDS CHALLENGES Mobility A seamless user experience across different channels Competition Differentiation against the competition Increased fraud Multi-layered approach to tackle sophisticated fraud Regulations & compliance Investment in compliance 9

10 Opportunities Banks have more trust than any other institution. As consumer confidence grows, banks must use new technology to win and retain these customers while offering multi-layered security. By taking advantage of this latest technology, banks can strengthen retention, create customer loyalty and enhance customer acquisition. Developments in security have become an enabler for banks to create value, and therefore to grow. TRENDS OPPORTUNITIES Mobility Enhance customer acquisition Competition Create customer loyalty Increased fraud Decrease operational costs Regulations & compliance Business growth 10

11 Digital Transformation with HID Global 11

12 Application security Transaction signing and pattern-based intelligence Browser protection Device authentication Adaptive security approach User authentication (MFA) Something you know Something you have Something you are PSD2 multi-factor authentication Replication prevention Transaction signing and pattern-based intelligence Confidentiality, authenticity and integrity of the data User authentication (MFA) Knowledge (passwords) Possession (token or tokenless) Inherence (biometrics, behaviour metrics) Adaptive multi-layered authentication With HID Global, financial institutions can inspire confidence and increase adoption of online and mobile channels by offering their customers a worry-free, secure and convenient experience, which in turn contributes to their bottom line. Our solutions comply with the key banking authentication regulations around the world, offering an unparalleled user experience, ideal for banks and financial organizations looking to enhance their digital offering while increasing security for the customer. Our approach enables multi-factor authentication for all leading mobile phones and tablets, and has a pluggable platform that is extensible for future authentication methods. In a landscape of evolving threats, banks should embrace regulatory changes and complexities to contain risk and protect their customers. 12

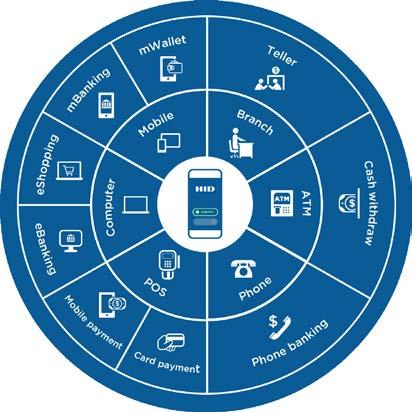

13 Secure Multi-Channel Banking Branch ATM Landline ebanking mbanking ecommerce POS One-time password Static credentials Push notification Out of band Methods Behavioural analysis Certificates Threat detection Biometry The HID Global approach HID Global s ActivID Authentication Server and Threat Detection Service provide corporate, financial and government organizations with risk-appropriate, cost-efficient user authentication. The solution enables end users to have convenient anytime, anywhere access to sensitive data from their smartphones, tablets, computers and virtually any other device. Deployment is simplified too, through the platform s pre-integration with major cloud apps, VPN systems, application servers, banking applications and other third-party systems. As banks enhance online and mobile channels in response to competition and user demand, they must successfully address risks associated with authenticating their customers and employees, and integrate their front and back-end systems with a central ActivID Authentication Server. 13

14 Use cases Transaction signing No matter the place and time - buying a coffee, purchasing a book online or withdrawing cash from the ATM - the user can conveniently process transactions by receiving a notification which ensures verification and validation. As a result, customers are confident and have full control of their account debits in a fully secured environment. Banking anytime, anywhere With the acceleration of digital activity, users need to bank anytime, anywhere with the guarantee of staying secure. The expectation for secure authentication, even when users behave unsafely, is growing and many banks are challenged to deliver a safe banking environment without compromising on convenience and user experience. Call center verification Establishing trust is one of the most valuable assets between banks and customers. Therefore, a reliable way of ID verification and mutual authentication is critical for prompt, seamless banking. When the user calls the bank s call center, they will receive a push notification to authenticate. This mutual authentication is safe and the user is in full control. 14

15 Multi-channel for all banking use cases t 15

16 GET IN TOUCH If you would like to find out how you can provide your customers with a more secure and convenient banking experience, you can now request a free consultation. ActivID Authentication Platform ActivID Threat Detection Service ActivID Trusted Transactions Request consultation Additional resources INFOGRAPHIC Top 5 Considerations: What to Look for in a Mobile Banking Security Solution INFOGRAPHIC FAQ: Why Banks Need a Dedicated Mobile Banking Security System 16

, June 2016 4.")

17 Sources 1. Board of Governors of the Federal Reserve System, Consumers and Mobile Financial Services 2016, March Javelin Strategy & Research, Javelin Identifies $1.5 B in Mobile Banking Cost Savings by Leveraging Omnichannel Approach, July Statista, Number of smartphone users worldwide from 2014 to 2020 (in millions), June Statista, Number of mobile phone users worldwide from 2013 to 2019 (in billions), August Capgemini Group, World Retail Banking Report 2016, April Accenture Banking Customer 2020, Rising Expectations Point to the Everyday Bank, BBVA, The Open Banking Standard: The open banking road map, June Accenture, There s a Lot for Banks to Like About Social Media, January Brian Yercan, Information Week Banking & Systems Technology, May 12, Accenture, 2014 North America Consumer Digital Banking Survey, January SAP, Omni-Channel Banking, Juniper Research, Online Payment Fraud: Key Vertical Strategies & Management , May 2016 North America: Toll Free: Europe, Middle East, Africa: Asia Pacific: Latin America: HID Global Corporation/ASSA ABLOY AB. All rights reserved. HID, HID Global, the HID Blue Brick logo, the Chain Design and HID, the HID logo and ActivID are trademarks or registered trademarks of HID Global or its licensor(s)/supplier(s) in the US and other countries and may not be used without permission. All other trademarks, service marks, and product or service names are trademarks or registered trademarks of their respective owners hid-iam-banking-eb-en PLT An ASSA ABLOY Group brand

Workplace Optimization

HID Location Services: Workplace Optimization WORKPLACE OPTIMIZATION FROM HID GLOBAL Workplace optimization for a smarter building and a more dynamic workforce Organizations are profiting from the increased

HID Location Services: Workplace Optimization WORKPLACE OPTIMIZATION FROM HID GLOBAL Workplace optimization for a smarter building and a more dynamic workforce Organizations are profiting from the increased

Payment Digitalization and the University Smart Card

Payment Digitalization and the University Smart Card Payment Digitalization and the University Smart Card 1 EVOLVING LANDSCAPE 2 PAYMENTS CONVERGENCE 3 PARTNERSHIP APPROACH 2 1 There are two rapidly evolving

Payment Digitalization and the University Smart Card Payment Digitalization and the University Smart Card 1 EVOLVING LANDSCAPE 2 PAYMENTS CONVERGENCE 3 PARTNERSHIP APPROACH 2 1 There are two rapidly evolving

Accenture Digital Customer Solutions: Design to Delivery

Accenture Digital Customer Solutions: Design to Delivery Your digital customers are here to stay: They can make or break your future Digital customers are always connected at home, at work and at play.

Accenture Digital Customer Solutions: Design to Delivery Your digital customers are here to stay: They can make or break your future Digital customers are always connected at home, at work and at play.

Digital 2025: Digital is Core, Digital is Data. Lee J. Volante, Head of Strategic Engagement, Temenos Asia Pacific 19 th May 2017

Digital 2025: Digital is Core, Digital is Data Lee J. Volante, Head of Strategic Engagement, Temenos Asia Pacific 19 th May 2017 Who are We 2000+ Banking & Finance Clients, 140+ Countries 150 across Asia

Digital 2025: Digital is Core, Digital is Data Lee J. Volante, Head of Strategic Engagement, Temenos Asia Pacific 19 th May 2017 Who are We 2000+ Banking & Finance Clients, 140+ Countries 150 across Asia

Digital Banking BPC s Vision

Digital Banking BPC s Vision MEXICO CLIENT CONFERENCE 2017 BPC Banking Technologies 2017 Mexico City bpcbt.com Topics 1 Future of banking 2 Global digital innovation market trends 3 BPC Vision 4 BPC Solution

Digital Banking BPC s Vision MEXICO CLIENT CONFERENCE 2017 BPC Banking Technologies 2017 Mexico City bpcbt.com Topics 1 Future of banking 2 Global digital innovation market trends 3 BPC Vision 4 BPC Solution

MOBILE PAYMENTS: A Key Opportunity in Today s Business Landscape

MOBILE PAYMENTS: A Key Opportunity in Today s Business Landscape CONTENTS Introduction 2 What are we talking about when we talk about mobile payments? 3 What types of POS systems best fit your business?

MOBILE PAYMENTS: A Key Opportunity in Today s Business Landscape CONTENTS Introduction 2 What are we talking about when we talk about mobile payments? 3 What types of POS systems best fit your business?

HID Global Advantage Partner Program

HID Global Advantage Partner Program Program Overview HID Global Advantage Partner Program More than a sales reward a true partnership. The Advantage Partner Program is more of a partnership... a more

HID Global Advantage Partner Program Program Overview HID Global Advantage Partner Program More than a sales reward a true partnership. The Advantage Partner Program is more of a partnership... a more

Beyond Payments: The Digital Commerce opportunity for Banks. Giorgio Andreoli Managing Director Accenture Digital mcommerce

Beyond Payments: The Digital Commerce opportunity for Banks Giorgio Andreoli Managing Director Accenture Digital mcommerce Mobey Day Barcelona, Oct 8 th, 2014 Agenda 1. Digital disruption and the impact

Beyond Payments: The Digital Commerce opportunity for Banks Giorgio Andreoli Managing Director Accenture Digital mcommerce Mobey Day Barcelona, Oct 8 th, 2014 Agenda 1. Digital disruption and the impact

Accenture and Adobe: Delivering Digital Experiences Together

Accenture and Adobe: Delivering Digital Experiences Together Connect data, content and analytics to power customer experience. With so much crosstalk in today s global, digitally driven marketplace, it

Accenture and Adobe: Delivering Digital Experiences Together Connect data, content and analytics to power customer experience. With so much crosstalk in today s global, digitally driven marketplace, it

Your Business. The Cloud. Business Cloud.

Your Business. The Cloud. Business Cloud. For the world of business today, change is the new constant, unpredictable is the new normal. In this rapidly evolving IT landscape, companies are constantly trying

Your Business. The Cloud. Business Cloud. For the world of business today, change is the new constant, unpredictable is the new normal. In this rapidly evolving IT landscape, companies are constantly trying

Competing for growth. Creating a customer-centric, connected enterprise. KPMG Customer Advisory. kpmg.com/customer

Competing for growth Creating a customer-centric, connected enterprise KPMG Customer Advisory kpmg.com/customer Contents Introduction 02 How can you stay ahead of rising customer expectations? 04 Becoming

Competing for growth Creating a customer-centric, connected enterprise KPMG Customer Advisory kpmg.com/customer Contents Introduction 02 How can you stay ahead of rising customer expectations? 04 Becoming

Accenture Interactive Point of View Series. Banking on Digital. Building trust and innovation in Financial Services

Accenture Interactive Point of View Series Banking on Building trust and innovation in Financial Services Banking on Building trust and innovation in Financial Services The digital era could not have come

Accenture Interactive Point of View Series Banking on Building trust and innovation in Financial Services Banking on Building trust and innovation in Financial Services The digital era could not have come

Towards transparency and freedom of choice An unbundled pricing model for retail banks

Towards transparency and freedom of choice An unbundled pricing model for retail banks Tian Yu Wu Manager Advisory & Consulting Strategy, Regulatory & Corporate Finance Deloitte Arek Kwapien Manager Advisory

Towards transparency and freedom of choice An unbundled pricing model for retail banks Tian Yu Wu Manager Advisory & Consulting Strategy, Regulatory & Corporate Finance Deloitte Arek Kwapien Manager Advisory

The Changing Landscape of Card Acceptance

The Changing Landscape of Card Acceptance Troy Byram Vice-President Sr. E-Receivables Consultant February 6, 2015 Agenda EMV (Chip and Pin) PCI Compliance and Data Security New Regulations for Municipalities

The Changing Landscape of Card Acceptance Troy Byram Vice-President Sr. E-Receivables Consultant February 6, 2015 Agenda EMV (Chip and Pin) PCI Compliance and Data Security New Regulations for Municipalities

SAP Hybris Solution Brief for Wholesale Distribution

SAP Hybris Solution Brief for Wholesale Distribution Today s competitive markets demand that Wholesale Distributors evolve faster, become more efficient, and provide memorable customer experiences. For

SAP Hybris Solution Brief for Wholesale Distribution Today s competitive markets demand that Wholesale Distributors evolve faster, become more efficient, and provide memorable customer experiences. For

HID Location Services and Condition Monitoring. Enabled by Bluvision

HID Location Services and Condition Monitoring Enabled by Bluvision Powering an End-to-end Internet of Things Ecosystem Passive RFID transponders are used across numerous industries to simplify inventory

HID Location Services and Condition Monitoring Enabled by Bluvision Powering an End-to-end Internet of Things Ecosystem Passive RFID transponders are used across numerous industries to simplify inventory

Global Mobile Payments Market

Published on NOVONOUS (https://www.novonous.com) Home > Global Mobile Payments Market 2016-2020 Global Mobile Payments Market 2016-2020 Publication ID: NOV0216002 Publication Date: February 18, 2016 Pages:

Published on NOVONOUS (https://www.novonous.com) Home > Global Mobile Payments Market 2016-2020 Global Mobile Payments Market 2016-2020 Publication ID: NOV0216002 Publication Date: February 18, 2016 Pages:

The Future of Payment Security in Canada

The Future of Payment Security in Canada October 2017 1 Visa Canada Public The Future of Payment Security in Canada Notices Forward-Looking Statements This presentation contains forward-looking statements

The Future of Payment Security in Canada October 2017 1 Visa Canada Public The Future of Payment Security in Canada Notices Forward-Looking Statements This presentation contains forward-looking statements

Lecture Materials RETAIL BANKING

Lecture Materials RETAIL BANKING Virginia Heyburn Vice President, Strategic Pursuits Fiserv virginia.heyburn@fiserv.com Miami Beach, Florida 786-239-4898 August 8, 2017 Vision 2020: Growing the Banking

Lecture Materials RETAIL BANKING Virginia Heyburn Vice President, Strategic Pursuits Fiserv virginia.heyburn@fiserv.com Miami Beach, Florida 786-239-4898 August 8, 2017 Vision 2020: Growing the Banking

CIO INSIGHTS Are You Meeting Today s Mobile Mandate?

CIO INSIGHTS Are You Meeting Today s Mobile Mandate? Are You Meeting Today s Mobile Mandate? How your business can transform the customer experience by optimizing for mobile The Business Case for Mastering

CIO INSIGHTS Are You Meeting Today s Mobile Mandate? Are You Meeting Today s Mobile Mandate? How your business can transform the customer experience by optimizing for mobile The Business Case for Mastering

Avanade Digital Fashion

Avanade Digital Fashion For the Retail Fashion Industry Overview Avanade Digital Fashion offers a complete and integrated digital solution and service portfolio, enabling fashion and apparel retailers

Avanade Digital Fashion For the Retail Fashion Industry Overview Avanade Digital Fashion offers a complete and integrated digital solution and service portfolio, enabling fashion and apparel retailers

Product. DigitalAccess A Single Digital Solution for Online Banking, Mobile and Tablet

Product DigitalAccess A Single Digital Solution for Online Banking, Mobile and Tablet Product The world is moving toward a new kind of financial services experience: the kind that serves customers in

Product DigitalAccess A Single Digital Solution for Online Banking, Mobile and Tablet Product The world is moving toward a new kind of financial services experience: the kind that serves customers in

Embracing Mobile Commerce: How Accenture and Paydiant Help Companies Move Beyond Payments

Embracing Mobile Commerce: How Accenture and Paydiant Help Companies Move Beyond Payments 2 As smartphones become the norm, more people want to use their phones to make their daily lives more convenient

Embracing Mobile Commerce: How Accenture and Paydiant Help Companies Move Beyond Payments 2 As smartphones become the norm, more people want to use their phones to make their daily lives more convenient

API Gateway Digital access to meaningful banking content

API Gateway Digital access to meaningful banking content Unlocking The Core Jason Williams, VP Solution Architecture April 10 2017 APIs In Banking A Shift to Openness Major shift in Banking occurring whereby

API Gateway Digital access to meaningful banking content Unlocking The Core Jason Williams, VP Solution Architecture April 10 2017 APIs In Banking A Shift to Openness Major shift in Banking occurring whereby

Mobile Banking Impact: Quantifying the ROI and Customer Engagement Benefits. Understanding the Value of Engaging Consumers in the Mobile Channel

Mobile Banking Impact: Quantifying the ROI and Customer Engagement Benefits Understanding the Value of Engaging Consumers in the Mobile Channel It goes without saying that mobile is an important channel

Mobile Banking Impact: Quantifying the ROI and Customer Engagement Benefits Understanding the Value of Engaging Consumers in the Mobile Channel It goes without saying that mobile is an important channel

USTGlobal. DIGITAL BANKING TRENDS AND INNOVATIONS A UST Global POV

USTGlobal DIGITAL BANKING TRENDS AND INNOVATIONS A UST Global POV September, 2016 DIGITAL BANKING TRENDS & INNOVATIONS Introduction Digital banking is not an option; rather, it is a must-have strategy

USTGlobal DIGITAL BANKING TRENDS AND INNOVATIONS A UST Global POV September, 2016 DIGITAL BANKING TRENDS & INNOVATIONS Introduction Digital banking is not an option; rather, it is a must-have strategy

The Age of Agile Solutions

>> Whitepaper The Age of Agile Solutions Creating Interconnected Ecosystems October 2017 Sell Side Sponsored by The Age of Agile Solutions Contents Executive Summary... Technology and Services to Unlock

>> Whitepaper The Age of Agile Solutions Creating Interconnected Ecosystems October 2017 Sell Side Sponsored by The Age of Agile Solutions Contents Executive Summary... Technology and Services to Unlock

BANKWORLD KIOSK Today s solution for tomorrow s self-service bank BANKWORLD BANK ON THE FUTURE WITH TODAY S TECHNOLOGY CR2.COM

BANKWORLD KIOSK Today s solution for tomorrow s self-service bank BANKWORLD BANK ON THE FUTURE WITH TODAY S TECHNOLOGY CR2.COM BANKWORLD KIOSK As the Kiosk continues to play an important role in the ongoing

BANKWORLD KIOSK Today s solution for tomorrow s self-service bank BANKWORLD BANK ON THE FUTURE WITH TODAY S TECHNOLOGY CR2.COM BANKWORLD KIOSK As the Kiosk continues to play an important role in the ongoing

Banking at the speed of your life. Online. Mobile. Superior. Safe. PARKSTERLING. Answers You Can Bank On.

Banking at the speed of your life. Online. Mobile. Superior. Safe. PARKSTERLING SM Answers You Can Bank On. At Park Sterling Bank, we know that there are times when our answer can help expand a child s

Banking at the speed of your life. Online. Mobile. Superior. Safe. PARKSTERLING SM Answers You Can Bank On. At Park Sterling Bank, we know that there are times when our answer can help expand a child s

EMV in the U.S. Liability shift; what does this mean for the U.S.?

EMV in the U.S. Liability shift; what does this mean for the U.S.? Questions and answers What the liability shift really means with regards to costs, risks and benefits. Fraud is on the rise in the U.S.

EMV in the U.S. Liability shift; what does this mean for the U.S.? Questions and answers What the liability shift really means with regards to costs, risks and benefits. Fraud is on the rise in the U.S.

SecuRe Pay recommendations for the security of mobile payments

ECB-PUBLIC FINAL SecuRe Pay recommendations for the security of mobile payments Stephanie Czák Senior Market Infrastructure Expert European Central Bank ETSI/EC Collaborative Ecosystem for M-Payments Workshop

ECB-PUBLIC FINAL SecuRe Pay recommendations for the security of mobile payments Stephanie Czák Senior Market Infrastructure Expert European Central Bank ETSI/EC Collaborative Ecosystem for M-Payments Workshop

CONSUMER BANKING: GREATER EXPECTATIONS

CONSUMER BANKING: GREATER EXPECTATIONS EXECUTIVE SUMMARY In the U.S. alone, more than 207 million consumers own and use a smartphone every day, and worldwide, that number is expected to exceed 2 billion

CONSUMER BANKING: GREATER EXPECTATIONS EXECUTIVE SUMMARY In the U.S. alone, more than 207 million consumers own and use a smartphone every day, and worldwide, that number is expected to exceed 2 billion

The Technology Frontier

NEDBANK GROUP LIMITED 19th Annual UBS South African Financial Services Conference NEDBANK GROUP LIMITED The Technology Frontier 13 October 2016 Fred Swanepoel, CIO A Member of the Group Agenda Digitisation

NEDBANK GROUP LIMITED 19th Annual UBS South African Financial Services Conference NEDBANK GROUP LIMITED The Technology Frontier 13 October 2016 Fred Swanepoel, CIO A Member of the Group Agenda Digitisation

BankWorld Agent Solution

BankWorld Agent Solution Today s solution for tomorrow s self-service bank Approximately 2.5 billion of the world s population are unbanked. In many countries it is a lack of proper banking infrastructure

BankWorld Agent Solution Today s solution for tomorrow s self-service bank Approximately 2.5 billion of the world s population are unbanked. In many countries it is a lack of proper banking infrastructure

ADDING VALUE TO SECURITY. How Issuers Can Leverage Tokenization to Capture New Revenue-Generating Opportunities. firstdata.com

A First Data Position Paper ADDING VALUE TO SECURITY How Issuers Can Leverage Tokenization to Capture New Revenue-Generating Opportunities firstdata.com Introduction The payments world is undergoing a

A First Data Position Paper ADDING VALUE TO SECURITY How Issuers Can Leverage Tokenization to Capture New Revenue-Generating Opportunities firstdata.com Introduction The payments world is undergoing a

THE NEXT EVOLUTION IN COMMERCE: INVISIBLE PAYMENTS

THE NEXT EVOLUTION IN COMMERCE: INVISIBLE PAYMENTS WHAT THIS SHIFT MEANS FOR CONSUMERS AND THE COMPANIES THAT SERVE THEM A White Paper by i2c, Inc. 1300 Island Drive Suite 105 Redwood City, CA 94065 USA

THE NEXT EVOLUTION IN COMMERCE: INVISIBLE PAYMENTS WHAT THIS SHIFT MEANS FOR CONSUMERS AND THE COMPANIES THAT SERVE THEM A White Paper by i2c, Inc. 1300 Island Drive Suite 105 Redwood City, CA 94065 USA

Banking in the Balance: Security vs. Convenience. IBM Trusteer s Valerie Bradford on How to Assess Digital Identities

Banking in the Balance: Security vs. Convenience IBM Trusteer s Valerie Bradford on How to Assess Digital Identities In an interview about overcoming these challenges, Bradford discusses: The fundamental

Banking in the Balance: Security vs. Convenience IBM Trusteer s Valerie Bradford on How to Assess Digital Identities In an interview about overcoming these challenges, Bradford discusses: The fundamental

Workspace ONE. Insert Presenter Name. Empowering a Digital Workspace. Insert Presenter Title

Workspace ONE Empowering a Digital Workspace Insert Presenter Name Insert Presenter Title Every dimension of our lives is GOING DIGITAL 2 Consumerization is driving DIGITAL TRANSFORMATION Modern Workforce

Workspace ONE Empowering a Digital Workspace Insert Presenter Name Insert Presenter Title Every dimension of our lives is GOING DIGITAL 2 Consumerization is driving DIGITAL TRANSFORMATION Modern Workforce

When the hard-to-reach become your preferred customers. Finc / the offering which addresses financial inclusion challenges

When the hard-to-reach become your preferred customers Finc / the offering which addresses financial inclusion challenges Powering the Financial Inclusion revolution Today, 75% of the world s population

When the hard-to-reach become your preferred customers Finc / the offering which addresses financial inclusion challenges Powering the Financial Inclusion revolution Today, 75% of the world s population

WHITE PAPER. Retail banking trends for Australia

WHITE PAPER Retail banking trends for Australia The retail banking industry in Australia has always aligned itself to the ever-changing consumer demands, by fine-tuning its services and customizing its

WHITE PAPER Retail banking trends for Australia The retail banking industry in Australia has always aligned itself to the ever-changing consumer demands, by fine-tuning its services and customizing its

Aconite Smart Solutions

Aconite Smart Solutions PIN Management Services Contents PIN MANAGEMENT... 3 CURRENT CHALLENGES... 3 ACONITE PIN MANAGER SOLUTION... 4 OVERVIEW... 4 CENTRALISED PIN VAULT... 5 CUSTOMER PIN SELF SELECT

Aconite Smart Solutions PIN Management Services Contents PIN MANAGEMENT... 3 CURRENT CHALLENGES... 3 ACONITE PIN MANAGER SOLUTION... 4 OVERVIEW... 4 CENTRALISED PIN VAULT... 5 CUSTOMER PIN SELF SELECT

THE FUTURE OF TRANSACTING

1 Payments - Create and Protect Recurring Revenue Opportunities THE FUTURE OF TRANSACTING The Future is Genius SuperDeck Creative v.1 10.22.2015 Who are we? 2 Our payment solutions enable businesses to

1 Payments - Create and Protect Recurring Revenue Opportunities THE FUTURE OF TRANSACTING The Future is Genius SuperDeck Creative v.1 10.22.2015 Who are we? 2 Our payment solutions enable businesses to

Enterprise CX Cloud. About NICE

About NICE NICE (Nasdaq:NICE) is the worldwide leading provider of both cloud and on-premises enterprise software solutions that empower organizations to make smarter decisions based on advanced analytics

About NICE NICE (Nasdaq:NICE) is the worldwide leading provider of both cloud and on-premises enterprise software solutions that empower organizations to make smarter decisions based on advanced analytics

Payment Acceptance Solutions

Payment Acceptance Solutions Increase sales, enhance agility, and mitigate risks with CyberSource CyberSource is a Visa solution Businesses today are developing new strategies for acquiring and retaining

Payment Acceptance Solutions Increase sales, enhance agility, and mitigate risks with CyberSource CyberSource is a Visa solution Businesses today are developing new strategies for acquiring and retaining

STAR Network Overview

STAR Network Overview Presented by: Jeff Jakopec, Sr. Strategy Business Development September 26, 2017 What Differentiates STAR Network From the Rest STAR provides market leading fraud solutions that help

STAR Network Overview Presented by: Jeff Jakopec, Sr. Strategy Business Development September 26, 2017 What Differentiates STAR Network From the Rest STAR provides market leading fraud solutions that help

How Will Your Bank Thrive?

How Will Your Bank Thrive? Pennsylvania Association of Community Bankers Annual Convention September 24, 2016 Timothy Reimink Managing Director Crowe Horwath LLP Session Description Some people wonder

How Will Your Bank Thrive? Pennsylvania Association of Community Bankers Annual Convention September 24, 2016 Timothy Reimink Managing Director Crowe Horwath LLP Session Description Some people wonder

Technology evolution. Managing the risk in four key areas

Technology evolution Managing the risk in four key areas The message is widespread: the concept of as-a-service is real and has the potential to unleash the power of processing, increased capacity, cost

Technology evolution Managing the risk in four key areas The message is widespread: the concept of as-a-service is real and has the potential to unleash the power of processing, increased capacity, cost

IBM Sterling B2B Integrator

IBM Sterling B2B Integrator B2B integration software to help synchronize your extended business partner communities Highlights Enables connections to practically all of your business partners, regardless

IBM Sterling B2B Integrator B2B integration software to help synchronize your extended business partner communities Highlights Enables connections to practically all of your business partners, regardless

TRUSTED IDENTITIES TRUSTED DEVICES TRUSTED TRANSACTIONS. Investor Presentation - December 2017

TRUSTED IDENTITIES TRUSTED DEVICES TRUSTED TRANSACTIONS Investor Presentation - December 2017 Safe Harbor Statement This presentation contains forward-looking statements within the meaning of Section 21E

TRUSTED IDENTITIES TRUSTED DEVICES TRUSTED TRANSACTIONS Investor Presentation - December 2017 Safe Harbor Statement This presentation contains forward-looking statements within the meaning of Section 21E

Mobile and Contactless Payments Requirements and Interactions

Mobile and Contactless Payments Requirements and Interactions Version 1.0 Date: February 2018 2018 U.S. Payments Forum and Smart Card Alliance. All rights reserved. Page 1 About the U.S. Payments Forum

Mobile and Contactless Payments Requirements and Interactions Version 1.0 Date: February 2018 2018 U.S. Payments Forum and Smart Card Alliance. All rights reserved. Page 1 About the U.S. Payments Forum

The Role of Core in Digital Adoption

Accenture Core Banking Services The Role of Core in Digital Adoption Will your core banking platform be an enabler or an inhibitor of the Everyday Bank? Multiple disruptive forces, ushered in by the digital

Accenture Core Banking Services The Role of Core in Digital Adoption Will your core banking platform be an enabler or an inhibitor of the Everyday Bank? Multiple disruptive forces, ushered in by the digital

Big Data - Its Impacts on Economies, Finance and Central Banking

November 1, 2017 Bank of Japan Big Data - Its Impacts on Economies, Finance and Central Banking Remarks at the Fourth FinTech Forum Hiroshi Nakaso Deputy Governor of the Bank of Japan (English translation

November 1, 2017 Bank of Japan Big Data - Its Impacts on Economies, Finance and Central Banking Remarks at the Fourth FinTech Forum Hiroshi Nakaso Deputy Governor of the Bank of Japan (English translation

Identity Management Services

WHITE PAPER AUGUST 2014 Identity Management Services How Telcos Can Outpace Commoditization in the Application Economy 2 WHITE PAPER: IDENTITY MANAGEMENT SERVICES ca.com Table of Contents Executive Summary

WHITE PAPER AUGUST 2014 Identity Management Services How Telcos Can Outpace Commoditization in the Application Economy 2 WHITE PAPER: IDENTITY MANAGEMENT SERVICES ca.com Table of Contents Executive Summary

OPTIMISING INFORMATION WORKFLOW MANAGEMENT (IWM) IN BANKING

IN BANKING") OPTIMISING INFORMATION WORKFLOW MANAGEMENT (IWM) IN BANKING Powerful forces are reshaping the banking industry. Customer expectations, technological capabilities, regulatory requirements, demographics

OPTIMISING INFORMATION WORKFLOW MANAGEMENT (IWM) IN BANKING Powerful forces are reshaping the banking industry. Customer expectations, technological capabilities, regulatory requirements, demographics

Satisfy customers. Grow their loyalty.

Satisfy customers. Grow their loyalty. In many industries, markets and businesses, contact center efficiency and surprisingly customer satisfaction don t directly drive customer loyalty. Customer loyalty

Satisfy customers. Grow their loyalty. In many industries, markets and businesses, contact center efficiency and surprisingly customer satisfaction don t directly drive customer loyalty. Customer loyalty

Cashless Payment Solutions

SECURE contactless. Making cashless payment more convenient, more secure and more profitable Committed Industry Leadership HID Global is an active member of a variety of industry and trade associations

SECURE contactless. Making cashless payment more convenient, more secure and more profitable Committed Industry Leadership HID Global is an active member of a variety of industry and trade associations

Expanding to New Verticals

Expanding to New Verticals Mobile Card Product and Feature Suite Dave Abouchar, Director New Mobile Products Krishna Rajamani, Mobile Product Manager April 12, 2017 Agenda 1. Introduction 2. Credit Card

Expanding to New Verticals Mobile Card Product and Feature Suite Dave Abouchar, Director New Mobile Products Krishna Rajamani, Mobile Product Manager April 12, 2017 Agenda 1. Introduction 2. Credit Card

Artificial Intelligence. Big Data Analytics

ENHANCING CUSTOMER EXPERIENCE WITH SECURE DIGITAL IDENTITY In the past decade, digitalization has had a profound impact on the financial services sector, supported by developments in major technology areas

ENHANCING CUSTOMER EXPERIENCE WITH SECURE DIGITAL IDENTITY In the past decade, digitalization has had a profound impact on the financial services sector, supported by developments in major technology areas

Enabling Branch Innovation: The Powerful Role of Self-Service Technology. Liam van Beek Sr. Manager, Physical Channel Strategy, BMO

Enabling Branch Innovation: The Powerful Role of Self-Service Technology Liam van Beek Sr. Manager, Physical Channel Strategy, BMO 1 Agenda A changing landscape Understanding shifts in customer behaviour

Enabling Branch Innovation: The Powerful Role of Self-Service Technology Liam van Beek Sr. Manager, Physical Channel Strategy, BMO 1 Agenda A changing landscape Understanding shifts in customer behaviour

CUSTOMER ENGAGEMENT STARTS WITH SINGLE SIGN-ON

E-BOOK CUSTOMER ENGAGEMENT STARTS WITH SINGLE SIGN-ON (BUT IT DOESN T END THERE) 03 ANSWERING HIGH EXPECTATIONS WITH CUSTOMER SSO 05 EXCEED EXPECTATIONS WITH CUSTOMER SSO 07 SSO IS WINNING THE CUSTOMER

E-BOOK CUSTOMER ENGAGEMENT STARTS WITH SINGLE SIGN-ON (BUT IT DOESN T END THERE) 03 ANSWERING HIGH EXPECTATIONS WITH CUSTOMER SSO 05 EXCEED EXPECTATIONS WITH CUSTOMER SSO 07 SSO IS WINNING THE CUSTOMER

PSD2. a directive of possibilities. Whitepaper by

PSD2 a directive of possibilities Whitepaper by INTRODUCTION European banks are facing a game-changing 2018. With the new PSD2-directive from EU banks need to rethink their business model and how they

PSD2 a directive of possibilities Whitepaper by INTRODUCTION European banks are facing a game-changing 2018. With the new PSD2-directive from EU banks need to rethink their business model and how they

Grow Deposits with FIS Digital Account Creation. Lynn Jordan April 11, 2017

Grow Deposits with FIS Digital Account Creation Lynn Jordan April 11, 2017 Expectations are rising The Competitive Landscape Is Changing Institutions are challenged with: Protecting customers from the

Grow Deposits with FIS Digital Account Creation Lynn Jordan April 11, 2017 Expectations are rising The Competitive Landscape Is Changing Institutions are challenged with: Protecting customers from the

How to modernize your ecommerce digital performance to improve customer experience

How to modernize your ecommerce digital performance to improve customer experience 2017 Dynatrace Executive Summary Today s consumers are tech and media savvy, with access to anything 24/7. They have high

How to modernize your ecommerce digital performance to improve customer experience 2017 Dynatrace Executive Summary Today s consumers are tech and media savvy, with access to anything 24/7. They have high

SECURE SSO TO OFFICE 365 & OTHER CLOUD APPLICATIONS WITH A CLOUD-BASED AUTHENTICATION SOLUTION

SECURE SSO TO OFFICE 365 & OTHER CLOUD APPLICATIONS WITH A CLOUD-BASED AUTHENTICATION SOLUTION ADVICE FOR SIMPLIFYING & SECURING YOUR DEPLOYMENT Evan O Regan, Director of Product Management for Authentication

SECURE SSO TO OFFICE 365 & OTHER CLOUD APPLICATIONS WITH A CLOUD-BASED AUTHENTICATION SOLUTION ADVICE FOR SIMPLIFYING & SECURING YOUR DEPLOYMENT Evan O Regan, Director of Product Management for Authentication

Engaging campus experience with transaction solutions CACUBO annual meeting

Engaging campus experience with transaction solutions 2017 CACUBO annual meeting Who we are 2 Dedicated to higher education 1,000+ Transaction solution clients Serve 2,100+ clients in 60 countries Staff

Engaging campus experience with transaction solutions 2017 CACUBO annual meeting Who we are 2 Dedicated to higher education 1,000+ Transaction solution clients Serve 2,100+ clients in 60 countries Staff

The Second Payment Services Directive: Scoping out the impacts of the Regulatory Technical Standards

The Second Payment Services Directive: Scoping out the impacts of the Regulatory Technical Standards TABLE OF CONTENTS INTRODUCTION: A CRITICAL MOMENT FOR PSD2 KEY ASPECTS OF THE FINAL DRAFT RTS IMPACTS

The Second Payment Services Directive: Scoping out the impacts of the Regulatory Technical Standards TABLE OF CONTENTS INTRODUCTION: A CRITICAL MOMENT FOR PSD2 KEY ASPECTS OF THE FINAL DRAFT RTS IMPACTS

Immediate GRATIFICATION through the. Cloud. Why You Should Consider SaaS for Instant Card Issuance

Immediate GRATIFICATION through the Cloud Why You Should Consider SaaS for Instant Card Issuance Software-as-a-service (SaaS) may be late to the banking world, but its merits make a compelling argument

Immediate GRATIFICATION through the Cloud Why You Should Consider SaaS for Instant Card Issuance Software-as-a-service (SaaS) may be late to the banking world, but its merits make a compelling argument

Digital Transformation - The Power of Physical to Digital Loyalty

Digital Transformation - The Power of Physical to Digital Loyalty Access Card Receive Notification LOYALTY Redeem Rewards Check Status RESEARCH PARTNER Introduction & Background When modern customer loyalty

Digital Transformation - The Power of Physical to Digital Loyalty Access Card Receive Notification LOYALTY Redeem Rewards Check Status RESEARCH PARTNER Introduction & Background When modern customer loyalty

PSD2 & The Future of Digital Banking. Bragi Fjalldal, CMO & VP Business Development

PSD2 & The Future of Digital Banking Bragi Fjalldal, CMO & VP Business Development About Meniga Meniga is helping leading banks around the world personalize their digital customer experience CONTINENTS

PSD2 & The Future of Digital Banking Bragi Fjalldal, CMO & VP Business Development About Meniga Meniga is helping leading banks around the world personalize their digital customer experience CONTINENTS

THE ARRIVAL OF PIN ON MOBILE. An Introduction to the Next Generation of Face-to-Face Mobile Payment Acceptance

THE ARRIVAL OF PIN ON MOBILE An Introduction to the Next Generation of Face-to-Face Mobile Payment Acceptance MYPINPAD Ltd 01 INTRODUCTION For most organisations, growing bottom-line profit is a crucial

THE ARRIVAL OF PIN ON MOBILE An Introduction to the Next Generation of Face-to-Face Mobile Payment Acceptance MYPINPAD Ltd 01 INTRODUCTION For most organisations, growing bottom-line profit is a crucial

JANUARY ecommerce Trends for PRESENTED BY BONSPACE.COM

JANUARY 2018 Top-13 ecommerce Trends for 2018 PRESENTED BY BONSPACE.COM Voice & Image 1 Search Voice will become one of the most important factors of innovation in the field of e-commerce, and not just

JANUARY 2018 Top-13 ecommerce Trends for 2018 PRESENTED BY BONSPACE.COM Voice & Image 1 Search Voice will become one of the most important factors of innovation in the field of e-commerce, and not just

The Digital Disruption in Banking

2014 North America Consumer Digital Banking Survey The Digital Disruption in Banking Demons, demands, and dividends While many North American banks have been able to retain their customers through traditional

2014 North America Consumer Digital Banking Survey The Digital Disruption in Banking Demons, demands, and dividends While many North American banks have been able to retain their customers through traditional

Retail Banking Insights

Retail Banking Insights nsights Number 9 January 2017 The Winning Formula for Omnichannel Banking in North America For more than a decade, traditional retailers have been designing customer journeys and

Retail Banking Insights nsights Number 9 January 2017 The Winning Formula for Omnichannel Banking in North America For more than a decade, traditional retailers have been designing customer journeys and

Digital Onboarding and RegTech

Wowing Customers, Simplifying Compliance Nick Holland, Author This paper outlines three key reasons for digitising identity verification processes: 1. Customer retention in a mobile-first era. Consumers

Wowing Customers, Simplifying Compliance Nick Holland, Author This paper outlines three key reasons for digitising identity verification processes: 1. Customer retention in a mobile-first era. Consumers

MAINTAINING TRUST AMID SHIFTING CONSUMER DEMANDS

MAINTAINING TRUST AMID SHIFTING CONSUMER DEMANDS ACCENTURE FINANCIAL SERVICES 2017 GLOBAL DISTRIBUTION & MARKETING CONSUMER STUDY: INVESTMENT ADVICE REPORT SHIFTING CONSUMER TRENDS CREATE NEW OPPORTUNITY

MAINTAINING TRUST AMID SHIFTING CONSUMER DEMANDS ACCENTURE FINANCIAL SERVICES 2017 GLOBAL DISTRIBUTION & MARKETING CONSUMER STUDY: INVESTMENT ADVICE REPORT SHIFTING CONSUMER TRENDS CREATE NEW OPPORTUNITY

At the Heart of Differentiating Customer Experiences

At the Heart of Differentiating Customer Experiences Future Ready: Multi-Channel Distribution in Life Insurance Effective Distribution strategy can Transcend Customer Demands to Deliver Exceptional Customer

At the Heart of Differentiating Customer Experiences Future Ready: Multi-Channel Distribution in Life Insurance Effective Distribution strategy can Transcend Customer Demands to Deliver Exceptional Customer

DIGITALISATION OF PAYMENTS DRIVING THE FUTURE OF PREPAID

DIGITALISATION OF PAYMENTS DRIVING THE FUTURE OF PREPAID WIRECARD Brian Lawlor, December 2017 CONTENTS Who we are Digitalisation Evolution of payments Emerging markets for prepaid Payment landscape Conclusion

DIGITALISATION OF PAYMENTS DRIVING THE FUTURE OF PREPAID WIRECARD Brian Lawlor, December 2017 CONTENTS Who we are Digitalisation Evolution of payments Emerging markets for prepaid Payment landscape Conclusion

THE ADOPTION OF EMV TECHNOLOGY IN THE U.S. By Guy Berg Global Industry Sales Consultant Datacard Group

THE ADOPTION OF EMV TECHNOLOGY IN THE U.S. By Guy Berg Global Industry Sales Consultant Datacard Group Abstract: Visa Inc. and MasterCard recently announced plans to accelerate chip migration in the United

THE ADOPTION OF EMV TECHNOLOGY IN THE U.S. By Guy Berg Global Industry Sales Consultant Datacard Group Abstract: Visa Inc. and MasterCard recently announced plans to accelerate chip migration in the United

OPEN BANKING: THE ART OF THE POSSIBLE MAKING OPEN BANKING WORK FOR YOUR ORGANISATION. An NCR white paper

OPEN BANKING: THE ART OF THE POSSIBLE MAKING OPEN BANKING WORK FOR YOUR ORGANISATION An NCR white paper TABLE OF CONTENTS 1 OPEN BANKING AT A GLANCE 2 UNDERSTAND THE CONTEXT: WHY HERE, WHY NOW? 3 WHAT

OPEN BANKING: THE ART OF THE POSSIBLE MAKING OPEN BANKING WORK FOR YOUR ORGANISATION An NCR white paper TABLE OF CONTENTS 1 OPEN BANKING AT A GLANCE 2 UNDERSTAND THE CONTEXT: WHY HERE, WHY NOW? 3 WHAT

Accenture Business Journal for India Shaping the Future with As-a-Service:

Accenture Business Journal for India Shaping the Future with As-a-Service: Transforming businesses with a new approach to boosting profitability and productivity For many companies in India, improving

Accenture Business Journal for India Shaping the Future with As-a-Service: Transforming businesses with a new approach to boosting profitability and productivity For many companies in India, improving

PROSPECTUS lafferty.com

PROSPECTUS 2018 lafferty.com ABOUT LAFFERTY GROUP Senior executives at retail banks, card issuers, and payments providers around the world rely on Lafferty Group for the research, news, data and insight

PROSPECTUS 2018 lafferty.com ABOUT LAFFERTY GROUP Senior executives at retail banks, card issuers, and payments providers around the world rely on Lafferty Group for the research, news, data and insight

Winning Your Customers by Creating a Smart and Connected Enterprises

TRIANZ WHITEPAPER Winning Your Customers by Creating a Smart and Connected Enterprises Engage, Enable, Empower December 2015 www.trianz.com Abstract This paper discusses how leveraging the advantages of

TRIANZ WHITEPAPER Winning Your Customers by Creating a Smart and Connected Enterprises Engage, Enable, Empower December 2015 www.trianz.com Abstract This paper discusses how leveraging the advantages of

Mobile Treasury and the Connected Bank

Treasury and Trade Solutions September 2014 Mobile Treasury and the Connected Bank Digital Trends that are Shaping the Market Digital Impact to Banking Industry Social Data Cloud Mobile 1 Treasury and

Treasury and Trade Solutions September 2014 Mobile Treasury and the Connected Bank Digital Trends that are Shaping the Market Digital Impact to Banking Industry Social Data Cloud Mobile 1 Treasury and

The e-commerce solution. Your key to successful online business

The e-commerce solution Your key to successful online business SIX Payment Services Table of contents The right choice for online and omni-channel payments 03 Your one-stop shop provider 04 How we can

The e-commerce solution Your key to successful online business SIX Payment Services Table of contents The right choice for online and omni-channel payments 03 Your one-stop shop provider 04 How we can

DELIVER A TRULY DIGITAL WALLET EXPERIENCE. Powering customer engagement and business growth. Finacle Digital Wallet Solution

DELIVER A TRULY DIGITAL WALLET EXPERIENCE Powering customer engagement and business growth Finacle Digital Wallet Solution The universal adoption of smart phones has opened up a ubiquitous channel which

DELIVER A TRULY DIGITAL WALLET EXPERIENCE Powering customer engagement and business growth Finacle Digital Wallet Solution The universal adoption of smart phones has opened up a ubiquitous channel which

Technology Innovation Exchange 2017

1 2 3 Significant period of change in the next 9 months Between PSD2, OBWG and CMA alone, there is significant, directionally aligned, activity aimed at transforming the landscape. The timing and degree

1 2 3 Significant period of change in the next 9 months Between PSD2, OBWG and CMA alone, there is significant, directionally aligned, activity aimed at transforming the landscape. The timing and degree

From Point of Service to Point of Differentiation

From Point of Service to Point of Differentiation Abstract The promise of a seamless omni-channel customer experience is the Holy Grail of retailing today. However, delivering a uni ed omni-channel experience

From Point of Service to Point of Differentiation Abstract The promise of a seamless omni-channel customer experience is the Holy Grail of retailing today. However, delivering a uni ed omni-channel experience

KEY CONSIDERATIONS FOR EXAMINING CHANNEL PARTNER LOYALTY AN ICLP RESEARCH STUDY IN ASSOCIATION WITH CHANNEL FOCUS BAPTIE & COMPANY

KEY CONSIDERATIONS FOR EXAMINING CHANNEL PARTNER LOYALTY AN ICLP RESEARCH STUDY IN ASSOCIATION WITH CHANNEL FOCUS BAPTIE & COMPANY NOVEMBER 2014 Executive summary The changing landscape During this time

KEY CONSIDERATIONS FOR EXAMINING CHANNEL PARTNER LOYALTY AN ICLP RESEARCH STUDY IN ASSOCIATION WITH CHANNEL FOCUS BAPTIE & COMPANY NOVEMBER 2014 Executive summary The changing landscape During this time

NCR SelfServ 80 SERIES ATM FAMILY. For more information, visit ncr.com, or

NCR SelfServ 80 SERIES ATM FAMILY For more information, visit ncr.com, or email ncr.financial@ncr.com REINVENTING SELF-SERVICE EMBRACING THE CONVERGENCE OF TECHNOLO GY AND HUMAN-CENTERED EXPERIENCE. In

NCR SelfServ 80 SERIES ATM FAMILY For more information, visit ncr.com, or email ncr.financial@ncr.com REINVENTING SELF-SERVICE EMBRACING THE CONVERGENCE OF TECHNOLO GY AND HUMAN-CENTERED EXPERIENCE. In

Security & Compliance Trends in Innovative Electronic Payments

Security & Compliance Trends in Innovative Electronic Payments Independently conducted by Ponemon Institute LLC Publication Date: October 2014 Ponemon Institute Research Report Security & Compliance Trends

Security & Compliance Trends in Innovative Electronic Payments Independently conducted by Ponemon Institute LLC Publication Date: October 2014 Ponemon Institute Research Report Security & Compliance Trends

About Cegid. What does the Cegid Group deliver for its customers?

About Cegid Cegid, leading enterprise and vertical software solutions provider was founded in 1983 by Jean-Michel Aulas and has been traded as Cegid Group (CGD:EN Paris) since 1986. Over the last 2 decades,

About Cegid Cegid, leading enterprise and vertical software solutions provider was founded in 1983 by Jean-Michel Aulas and has been traded as Cegid Group (CGD:EN Paris) since 1986. Over the last 2 decades,

ATM MODERNIZATION FOUR REASONS TO MODERNIZE YOUR AGING ATM INSTALL BASE. An NCR white paper

ATM MODERNIZATION FOUR REASONS TO MODERNIZE YOUR AGING ATM INSTALL BASE An NCR white paper MODERNIZE TO SERVE YOUR CUSTOMERS BETTER The financial services industry has undergone enormous change over the

ATM MODERNIZATION FOUR REASONS TO MODERNIZE YOUR AGING ATM INSTALL BASE An NCR white paper MODERNIZE TO SERVE YOUR CUSTOMERS BETTER The financial services industry has undergone enormous change over the

WHITE PAPER. Encouraging innovation in payments through the PSD2 initiative. Abstract

WHITE PAPER Encouraging innovation in payments through the PSD2 initiative Abstract Revised Directive on Payment Services (PSD2) is primarily aimed at bringing new, online modes of payments initiation

WHITE PAPER Encouraging innovation in payments through the PSD2 initiative Abstract Revised Directive on Payment Services (PSD2) is primarily aimed at bringing new, online modes of payments initiation

Gemalto Consulting Services. Take control of your smart card implementation

Gemalto Consulting Services Take control of your smart card implementation FINANCIAL SERVICES & RETAIL > SERVICE ENTERPRISE INTERNET CONTENT PROVIDERS PUBLIC SECTOR TELECOMMUNICATIONS TRANSPORT Gemalto

Gemalto Consulting Services Take control of your smart card implementation FINANCIAL SERVICES & RETAIL > SERVICE ENTERPRISE INTERNET CONTENT PROVIDERS PUBLIC SECTOR TELECOMMUNICATIONS TRANSPORT Gemalto

2017 First Data Corporation. All Rights Reserved. REACH BRAND RECOGNIZE INCENTIVIZE REWARD

2017 First Data Corporation. All Rights Reserved. REACH BRAND RECOGNIZE INCENTIVIZE REWARD Over 60% * of people say they prefer gift cards over other types of marketing offers. With Gift Solutions, your

2017 First Data Corporation. All Rights Reserved. REACH BRAND RECOGNIZE INCENTIVIZE REWARD Over 60% * of people say they prefer gift cards over other types of marketing offers. With Gift Solutions, your

White Paper. Building on the Four Pillars of Mobile Payments

White Paper Building on the Four Pillars of Mobile Payments Building on the Four Pillars of Mobile Payments: A Blueprint for Success The launch of Apple Pay in 2014 was heralded as a turning point for

White Paper Building on the Four Pillars of Mobile Payments Building on the Four Pillars of Mobile Payments: A Blueprint for Success The launch of Apple Pay in 2014 was heralded as a turning point for

DIGITAL TRANSFORMATION (DX)

") An IDC InfoBrief THE PROMISE OF DIGITAL TRANSFORMATION (DX) IN ASIAPACIFIC S LEADING INSTITUTIONS IDC PREDICTION: BY 2018 1/3 OF THE TOP 20 MARKET SHARE LEADERS IN VARIOUS INDUSTRIES WORLDWIDE WILL BE

An IDC InfoBrief THE PROMISE OF DIGITAL TRANSFORMATION (DX) IN ASIAPACIFIC S LEADING INSTITUTIONS IDC PREDICTION: BY 2018 1/3 OF THE TOP 20 MARKET SHARE LEADERS IN VARIOUS INDUSTRIES WORLDWIDE WILL BE

PSD2: An Open Banking Catalyst

PSD2: An Open Banking Catalyst Leverage Open APIs to unlock new business opportunities It is short-sighted to treat the European Union s second Payment Services Directive (PSD2) and other European regulations

PSD2: An Open Banking Catalyst Leverage Open APIs to unlock new business opportunities It is short-sighted to treat the European Union s second Payment Services Directive (PSD2) and other European regulations

Product. Mobiliti Business Grow Market Share and Attract Profitable Business Customers by Combining Mobiliti Business With Business Online

Product Mobiliti Business Grow Market Share and Attract Profitable Business Customers by Combining Mobiliti Business With Business Online Product The demand for anytime, anywhere business banking is growing

Product Mobiliti Business Grow Market Share and Attract Profitable Business Customers by Combining Mobiliti Business With Business Online Product The demand for anytime, anywhere business banking is growing

BEST PRACTICES: 2015 Credit Card Mobile Sites and Apps

BEST PRACTICES: 2015 Credit Card Mobile Sites and Apps Who is KLI? KEY LIME INTERACTIVE (KLI) is a user research firm that conducts both qualitative and quantitative research for Fortune 2000 companies,

BEST PRACTICES: 2015 Credit Card Mobile Sites and Apps Who is KLI? KEY LIME INTERACTIVE (KLI) is a user research firm that conducts both qualitative and quantitative research for Fortune 2000 companies,