CASHLESS ECONOMY (DIGITAL INDIA)

|

|

|

- Benedict Carpenter

- 6 years ago

- Views:

Transcription

")

1 CASHLESS ECONOMY (DIGITAL INDIA)

, debit and credit cards, card-swipe or point of sales (POS) machines and")

2 CASHLESS ECONOMY? A Cashless Economy is an economy in which all types of transactions are carried out through digital means. It includes e- banking (Mobile banking or banking through computers), debit and credit cards, card-swipe or point of sales (POS) machines and digital wallets.

3 We want to have one mission and target: Take the nation forward Digitally and Economically -NARENDRA MODI(PRIME MINISTER OF INDIA)

4 PRACTICAL IMPLEMENTATION FOR MOVING ON PATH OF GOING CASHLESS (IN CONTEXT OF INDIA): Payment banks Electronic Fund Transfer Systems Mobile Wallets Internet Banking Banking cards Banks pre-paid cards Point of sale Mobile Banking

5 1. Payment Banks 2.Electronic Fund Transfer Systems: 3.Mobile Wallets 4.Internet Banking

6 5.Banking Cards 6.Bank Pre-Paid cards 7.Point of Sale 8.Mobile Banking

7 GOVERNMENTS RURAL PUSH FOR CASHLESS ECONOMY In an attempt to encourage poor and illiterate people in rural areas to make digital payments, the government is promoting Aadhaar Pay which ensures financial transactions by just using fingerprint.

8 INDIA IS TAKING A STEP ON THE ROAD TO CASHLESS ECONOMY: The government has been working hard to promote digital payment systems. So far, it seems to be working: the government has reported a 400-1,000% increase in digital transactions since the demonetization The National Payments Corporation of India, together with the RBI, has launched UPI ( united payment interface )

9

can be used to open a Bank Account using just an")

10 The Digital India Initiative has been set up to provide internet access and comprehensive mobile phone coverage across India, helping over a billion people to get online and utilize digital payment techniques. The RBI has been promoting a biometric authentication system for banking. The Aadhar Enabled Payment System (AEPS) can be used to open a Bank Account using just an identification number and fingerprint.

11 ACHIEVING A CASHLESS ECONOMY ON RURAL AREAS: Rural areas are home to two thirds of the country s population. Number of connected rural consumers is expected to increase from 120 million in 2015 to almost 315 in Over 93% of people in rural India have not done any digital transactions. The government has taken steps including announcing zero balance accounts for people. but growth of Bank branches has been low.

12 STEPS TAKEN BY RBI AND GOVERNMENT TO DISCOURAGE THE USE OF CASH: Government is also promoting mobile wallets. Recently, the RBI had issued certain guidelines that allow the users to increase their limit to Rs 1, 00,000 based on certain Know your customer verification. Various incentives offered by government to promote digital India on Cashless India: On digital transactions up to rupees 2000, Service Tax of 15% waived off

app to")

13 Digital purchase of fuel through credit cards, mobile wallets or e-wallets, discount of 0.75% Free accident insurance worth rupees 10 lakh on account of online ticket buyers On purchase of new LIC policies online via its site, 8% discount is offered. Government has introduced various technologies like BHIM (Bharat Interface for Money) app to transact between each other as well as with other merchants.

14 In addition to government or RBI, Companies are also participating in combating of cybercrimes. Microsoft opened full scale cyber security Center called Cyber security Engagement center (CSEC) in India.This centre monitors how viruses are spreading, from where cyber attacks are originating and helping customers to tap pool of security specialists.

15 CHALLENGES IN INDIA MAKING A CASHLESS ECONOMY: There are a number of obstacles in making India a cashless economy. Some of them are as under:- Currency denominated economy: Transactions are mainly in cash: ATM use is mainly for cash withdrawals and not for settling online transactions Limited availability of point of sale terminals. (pos machines) Mobile Internet penetration remains weak in rural India

16 Though bank accounts have been opened through Jan Dhan Yojana, most of them are lying unoperational The low literacy rates in rural India & lack of infrastructure In India, there are approx. 350 million internet users. The internet penetration rate is just 27% which is very low,it has to be at least 67% which is global median Since, India is dominated by small retailers; therefore they don t have enough resources to invest in electronic payment infrastructure.

can")

17 STEPS SHOULD BE TAKEN TO FOCUS CASHLESS ECONOMY ON RURAL AREAS: The Jan Dhan Aadhaar Mobile (JAM) can encourage digital transaction culture. A large number of government transfers are made through JAM mode.

18 A tax rebate (of say 1% to 2%) on payments made by households as salary to unorganized sector can boost cashless payments. The 5 A's of promoting financial inclusion through cashless payment instruments. Government should assure basic necessities in rural areas and focus on developing infrastructure. Financial literacy is a must for bringing more and more people to the digital platform.

19 Linkage of all welfare activities with bank accounts is a very strategic step. Targeted financial education programs can improve financial skills and Credit Management, and increase account ownership in rural India.

20 A STEP ON THE ROAD TO CASHLESS TRANSACTIONS TOWARDS FARMERS: The Indian Farmers Fertilizer Cooperative Limited (IFFCO), the world's largest fertilizer cooperative, has initiated a pan India outreach programme to educate farmers. Through live demonstrations and interactive sessions. Separate stalls will be set up in each of the Rural locations to conduct live demonstrations and also answer the queries posed by farmers regarding the same.

21 To expand digital payment infrastructure in rural areas, The Central Government through NABARD will extend financial support to eligible banks for development of 2 POS devices each in 1 lakh villages with population of less than 10,000. This will benefit farmers of one lakh village covering a total population of nearly 75crore who will have facility to transact cashlessly in their villages for their agriculture needs.

22 MEASURES TO BE TAKEN FOR DEVELEPING CASHLESS INDIA: Basic cyber hygiene (Better access to control techniques with strong authentication measures should be implemented by mobile e-wallet companies.) Bank accounts Abolishment of government fees Tax rebates for consumers and for merchants who adopt electronic payments. Making Electronic payment infrastructure completely safe and secure. The Reserve Bank of India too will have to come to terms with a few issues.

23 DIGITAL PAYMENT METHODS: The Digital India programme is a flagship programme of the Government of India Faceless, Paperless, Cashless is one of professed role of Digital India. As part of promoting cashless transactions and converting India into less-cash society, various modes of digital payments are available.

24

25 INTERNET BANKING: Internet banking, is an electronic payment system. Different types of online financial transactions are here National Electronic Funds Transfer (NEFT) NEFT is a nation-wide payment system facilitating one-to-one funds transfer. NEFT operates in hourly batches - there are twelve settlements from 8 am to 7 pm on week days (Monday through Friday) and from 8 am to 1 pm on Saturdays.

26 2.Real Time Gross Settlement (RTGS): RTGS is defined as the continuous (real-time) settlement of funds transfers The RTGS system is primarily meant for large value transactions. The minimum amount to be remitted through RTGS is 2 lakh. 3.Electronic Clearing System(ECS): ECS is an alternative method for effecting payment transactions in respect of the utility-bill-payments such as: telephone bills, electricity bills, insurance premier, card payments and loan repayments, etc.

27 4. Immediate Payment Service (IMPS): IMPS offers an instant, 24X7, interbank electronic fund transfer service through mobile phones.

28 CAPACITY BUILDING AND AWARENESS FOR CASHLESS ECONOMY: 1. Impart education related to the digital payment ecosystem, its tools, benefits and processes 2. Inform and educate citizens about Digital India - cashless, faceless and paperless 3. Encourage citizens especially in rural and semi urban areas to use digital payments as well as other products and services offered by Digital India 4. DigiShala Programme Portfolio.

29 Digital Finance for Rural India: Creating Awareness and Access through Common Service Centers (CSCs): 2 lakhs Common Service Centers (CSCs) to provide capacity building, Awareness access for digital payments methods to around1 core rural citizens and 25 lakhs merchants across India. Each CSC would reach out to 40 households in the catchment area, covering one person from each household. It also targets 10 Merchants per panchayat (for getting POS machines or digital payment mechanism.)

30 HOW COME LOW-WAGE EARNERS ADAPT TO CASHLESS DIGITAL SYSTEM: Open a Jan-Dhan account Get valid ID proof Use e-wallets to transact Save for emergencies Invest in small instruments

31 CYBER SECURITY FOR DIGITAL PAYMENTS: Digital payments are likely to cost more if the National Democratic Alliance (NDA) government decides to impose a token 'security fee' or cess on each online payment. According to several media reports, the government is contemplating imposing a cybersecurity cess on e-payments companies. This 'security fee' or cess like the Swachh Bharat cess, could be used to create better infrastructure for secure digital transactions.

32 ADVANTAGES OF GOING CASHLESS: Convenience Discounts Tracking spends Budget discipline Lower risk Small Gains

33 DISADVANTAGES OF CASHLESS ECONOMY: Higher risk of identity theft Losing phone Difficult for tech-unsavy Overspending

34 SURVEY AND ANALYSES REGARDING CASHLESS ECONOMY

35

36

37

38

39

40

41

42

43

44

45 CONCLUSION:. A cashless economy is secure, it is clean. We have a leadership role to play in taking India towards an increasingly digital economy. Thus, as citizens and youths of India it is in our hands to promote this magnificent India encouraged by our PM Mr. Narendra Modi who has a bright vision towards the upcoming of future India. Big success and it will help to attain vision of DIGITAL INDIA Coming together is a beginning; keeping together is progress; Working together is success

Retail Digital Payments. August 2017

Retail Digital Payments August 2017 1 Safe Harbour Except for the historical information contained herein, statements in this release which contain words or phrases such as will, aim, will likely result,

Retail Digital Payments August 2017 1 Safe Harbour Except for the historical information contained herein, statements in this release which contain words or phrases such as will, aim, will likely result,

Study on Introduction of Cashless Economy in India 2016: Benefits & Challenge s

IOSR Journal of Business and Management (IOSR-JBM) e-issn: 2278-487X, p-issn: 2319-7668. Volume 19, Issue 4. Ver. II (Apr. 2017), PP 116-120 www.iosrjournals.org Study on Introduction of Cashless Economy

IOSR Journal of Business and Management (IOSR-JBM) e-issn: 2278-487X, p-issn: 2319-7668. Volume 19, Issue 4. Ver. II (Apr. 2017), PP 116-120 www.iosrjournals.org Study on Introduction of Cashless Economy

ISSUES IN NETWORKED DIGITAL PAYMENT METHODS IN INDIA Dr. Biku Abraham Professor & Head MCA, Saintgits College of Engineering, Pathamuttom, Kottayam

ISSUES IN NETWORKED DIGITAL PAYMENT METHODS IN INDIA Dr. Biku Abraham Professor & Head MCA, Saintgits College of Engineering, Pathamuttom, Kottayam Abstract Since the decision to demonetize the high value

ISSUES IN NETWORKED DIGITAL PAYMENT METHODS IN INDIA Dr. Biku Abraham Professor & Head MCA, Saintgits College of Engineering, Pathamuttom, Kottayam Abstract Since the decision to demonetize the high value

Contents. 02

INNOVATIONS IN BANKING TECHNOLOGY THE INDIA PERSPECTIVE Abstract The digital transformation in banking is evident as an outcome of advances in Information Technology over the period. The Indian banking

INNOVATIONS IN BANKING TECHNOLOGY THE INDIA PERSPECTIVE Abstract The digital transformation in banking is evident as an outcome of advances in Information Technology over the period. The Indian banking

Digital payments system and rural India: A review of transaction to cashless economy

International Journal of Commerce and Management Research ISSN: 2455-1627, Impact Factor: RJIF 5.22 www.managejournal.com Volume 3; Issue 5; May 2017; Page No. 169-173 Digital payments system and rural

International Journal of Commerce and Management Research ISSN: 2455-1627, Impact Factor: RJIF 5.22 www.managejournal.com Volume 3; Issue 5; May 2017; Page No. 169-173 Digital payments system and rural

The Growth of Payments Bank in India: A Road Ahead

The Growth of Payments Bank in India: A Road Ahead Nipun Aggarwal 1, Dr. Dyal Bhatnagar 2 1 Research Scholar, School of Management Studies, Punjabi University, Patiala. 2 School of Management Studies,

The Growth of Payments Bank in India: A Road Ahead Nipun Aggarwal 1, Dr. Dyal Bhatnagar 2 1 Research Scholar, School of Management Studies, Punjabi University, Patiala. 2 School of Management Studies,

Brief Introduction UPI, BHIM & *99#

on Brief Introduction UPI, BHIM & *99# National Payments Corporation of India NPCI Inception Dec 2008 Setup by Reserve Bank of India and Indian Bankers Association Ten promoter Banks A Section 25 Company,

on Brief Introduction UPI, BHIM & *99# National Payments Corporation of India NPCI Inception Dec 2008 Setup by Reserve Bank of India and Indian Bankers Association Ten promoter Banks A Section 25 Company,

Banking Technology in India 2017

Now Available Banking Technology in India 2017 Segment Analysis and Outlook; Opportunities and Projections Report (PDF) Data-set (Excel) India Infrastructure Research Banking Technology in India 2017 Table

Now Available Banking Technology in India 2017 Segment Analysis and Outlook; Opportunities and Projections Report (PDF) Data-set (Excel) India Infrastructure Research Banking Technology in India 2017 Table

National Common Mobility Card (NCMC) Integrated Multi-modal Ticketing

Integrated Multi-modal Ticketing") www.pwc.co.in National Common Mobility Card (NCMC) Integrated Multi-modal Ticketing Budget 2017-18 Announcements Mission to be set up to target 2,500 crore digital transactions in FY 2017-18 through UPI,

www.pwc.co.in National Common Mobility Card (NCMC) Integrated Multi-modal Ticketing Budget 2017-18 Announcements Mission to be set up to target 2,500 crore digital transactions in FY 2017-18 through UPI,

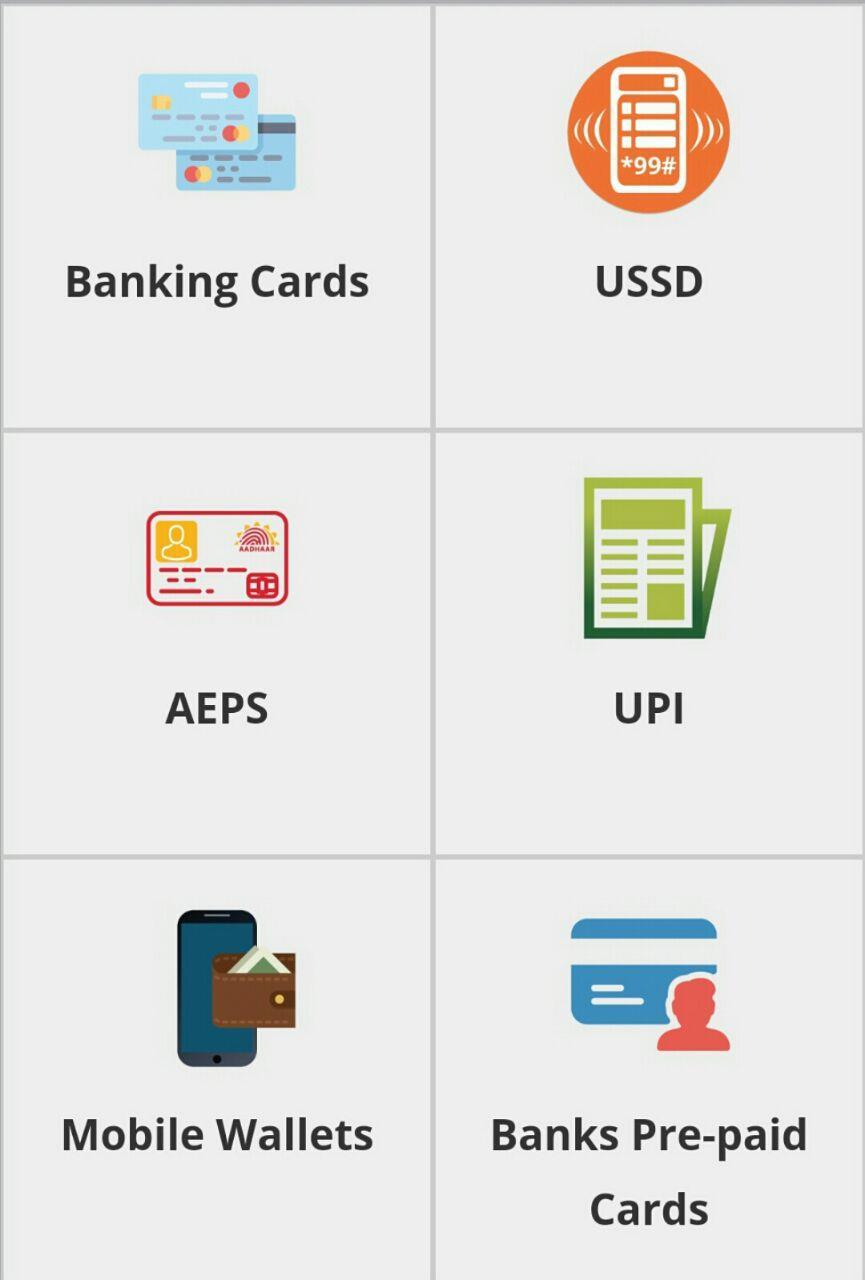

Digital Payments STEP BY STEP INSTRUCTIONS FOR VARIOUS MODES OF PAYMENT: Cards, USSD, AEPS, UPI, Wallets

Digital Payments STEP BY STEP INSTRUCTIONS FOR VARIOUS MODES OF PAYMENT: Cards, USSD, AEPS, UPI, Wallets Bank Cards Getting a Bank Card 1 2 HOW TO ISSUE A CARD FROM YOUR ACCOUNT Approach nearest bank branch

Digital Payments STEP BY STEP INSTRUCTIONS FOR VARIOUS MODES OF PAYMENT: Cards, USSD, AEPS, UPI, Wallets Bank Cards Getting a Bank Card 1 2 HOW TO ISSUE A CARD FROM YOUR ACCOUNT Approach nearest bank branch

A STUDY ON CONSUMER AWARENESS OF E-BANKING SERVICES IN PUBLIC SECTOR BANKS IN COIMBATORE DISTRICT

A STUDY ON CONSUMER AWARENESS OF E-BANKING SERVICES IN PUBLIC SECTOR BANKS IN COIMBATORE DISTRICT Mrs. T. Amsaveni 1 and Dr. M. Kanagarathinam 2 ABSTRACT Consumer awareness is the basic for the success

A STUDY ON CONSUMER AWARENESS OF E-BANKING SERVICES IN PUBLIC SECTOR BANKS IN COIMBATORE DISTRICT Mrs. T. Amsaveni 1 and Dr. M. Kanagarathinam 2 ABSTRACT Consumer awareness is the basic for the success

KNOW YOUR RUPAY DEBIT CARD

KNOW YOUR RUPAY DEBIT CARD ABSTRACT The objective of this document is to introduce the member banks to RuPay Debit Card program and to guide the issuing banks on the RuPay Debit Card features including

KNOW YOUR RUPAY DEBIT CARD ABSTRACT The objective of this document is to introduce the member banks to RuPay Debit Card program and to guide the issuing banks on the RuPay Debit Card features including

UNLEASH YOUR DREAMS TAP TO BENEFITS AND USAGE GUIDE FOR MONEYTAP

UNLEASH YOUR DREAMS TAP TO BENEFITS AND USAGE GUIDE FOR MONEYTAP EXPERIENCE MONEYTAP MONEY AS YOU LIKE IT. How it works HOW IT WORKS MONEY AS YOU LIKE IT YOUR BANK ACCOUNT MoneyTap App In a few taps, transfer

UNLEASH YOUR DREAMS TAP TO BENEFITS AND USAGE GUIDE FOR MONEYTAP EXPERIENCE MONEYTAP MONEY AS YOU LIKE IT. How it works HOW IT WORKS MONEY AS YOU LIKE IT YOUR BANK ACCOUNT MoneyTap App In a few taps, transfer

A step towards cashless economy - Unified Payments Interface (UPI)

") A step towards cashless economy - Unified Payments Interface (UPI) What is Unified Payment Interface? Objective of a unified payments system is to offer an architecture and a set of APIs on top of existing

A step towards cashless economy - Unified Payments Interface (UPI) What is Unified Payment Interface? Objective of a unified payments system is to offer an architecture and a set of APIs on top of existing

Electronic Banking Bonanza

Total Points Earned 24 Total Points Possible Percentage Electronic Banking Bonanza 2.7.1.L1 Note Taking Guide Name Date Class Directions: Complete the following note taking guide during the PowerPoint

Total Points Earned 24 Total Points Possible Percentage Electronic Banking Bonanza 2.7.1.L1 Note Taking Guide Name Date Class Directions: Complete the following note taking guide during the PowerPoint

Frontier Agents Learning Agenda Oxigen India Case Study Focus on Deployment Models. Vartika Shukla Pablo Garcia Arabehety June 2017

Frontier Agents Learning Agenda Oxigen India Case Study Focus on Deployment Models Vartika Shukla Pablo Garcia Arabehety June 2017 Disclaimer This work was funded in whole or in part by CGAP. Unlike CGAP's

Frontier Agents Learning Agenda Oxigen India Case Study Focus on Deployment Models Vartika Shukla Pablo Garcia Arabehety June 2017 Disclaimer This work was funded in whole or in part by CGAP. Unlike CGAP's

How the Cashless Society Reshape Commerce in Asia

1 Presentation on How the Cashless Society Reshape Commerce in Asia by Mr. Sayan Pariwat Senior Director, Payment Systems Department Bank of Thailand Conference on MarcusEvans Card Technology & Strategies

1 Presentation on How the Cashless Society Reshape Commerce in Asia by Mr. Sayan Pariwat Senior Director, Payment Systems Department Bank of Thailand Conference on MarcusEvans Card Technology & Strategies

Unified Payment Interface An Advancement in Payment Systems

American Journal of Industrial and Business Management, 2017, 7, 1174-1191 http://www.scirp.org/journal/ajibm ISSN Online: 2164-5175 ISSN Print: 2164-5167 Unified Payment Interface An Advancement in Payment

American Journal of Industrial and Business Management, 2017, 7, 1174-1191 http://www.scirp.org/journal/ajibm ISSN Online: 2164-5175 ISSN Print: 2164-5167 Unified Payment Interface An Advancement in Payment

NPCI assigns RS Software to build Digital Payments Enablement Platform

NPCI assigns RS Software to build Digital Payments Enablement Platform Will implement Unified Payment Interface to facilitate & accelerate digital payment adoption in India Mumbai, India July 23, 2015

NPCI assigns RS Software to build Digital Payments Enablement Platform Will implement Unified Payment Interface to facilitate & accelerate digital payment adoption in India Mumbai, India July 23, 2015

Payment Systems Review July - December, 2016

Payment Systems Review July - December, 2016 Payment Systems Department PREAMBLE Payment Systems Review (PSR) is based on quarterly submission of payment systems data submitted by Commercial and Microfinance

Payment Systems Review July - December, 2016 Payment Systems Department PREAMBLE Payment Systems Review (PSR) is based on quarterly submission of payment systems data submitted by Commercial and Microfinance

At the Microsoft CEO Conference hosted by Bill Gates, in my speech I shared that FINTECH is the key issue of our times

UKIBC Forum Digital Disruption in India Thursday, July 6 6:40 PM 7:00 PM LexisNexis, 30 Farringdon Street Keynote Address on UK-India Fintech Opportunity *** His Excellency Mr. Dinesh Patnaik, Deputy High

UKIBC Forum Digital Disruption in India Thursday, July 6 6:40 PM 7:00 PM LexisNexis, 30 Farringdon Street Keynote Address on UK-India Fintech Opportunity *** His Excellency Mr. Dinesh Patnaik, Deputy High

International Journal of Marketing & Financial Management, Volume 5, Issue 3, Mar-2017, pp ISSN: (Online) ISSN: (Print)

ISSN: (Print)") International Journal of Marketing & Financial Management, Volume 5, Issue 3, Mar-2017, pp 21-26 ISSN: 2348 3954 (Online) ISSN: 2349 2546 (Print) www.arseam.com Impact Factor: 3.43 DOI: 10.5281/zenodo.581796

International Journal of Marketing & Financial Management, Volume 5, Issue 3, Mar-2017, pp 21-26 ISSN: 2348 3954 (Online) ISSN: 2349 2546 (Print) www.arseam.com Impact Factor: 3.43 DOI: 10.5281/zenodo.581796

Corporate Presentation. Author: DIMPAY Foundation

Corporate Presentation Author: DIMPAY Foundation Table of Contents Table of Contents What is DIMPAY? 01 DIMPAY Foundation 02 DIMPAY Features 04 DIMPAY ICO 06 ICO Funds 08 DEPOTWALLET 10 DIMPAY Applications

Corporate Presentation Author: DIMPAY Foundation Table of Contents Table of Contents What is DIMPAY? 01 DIMPAY Foundation 02 DIMPAY Features 04 DIMPAY ICO 06 ICO Funds 08 DEPOTWALLET 10 DIMPAY Applications

RuPay Contactless Ideathon (1.2)

") RuPay Contactless Ideathon (1.2) Table of Contents CONTACTLESS PAYMENTS... 3 EXECUTIVE SUMMARY... 3 2.1 Objectives of RuPay Contactless... 4 2.2 Product Description... 4 2.3 Benefits Of RuPay Contactless...

RuPay Contactless Ideathon (1.2) Table of Contents CONTACTLESS PAYMENTS... 3 EXECUTIVE SUMMARY... 3 2.1 Objectives of RuPay Contactless... 4 2.2 Product Description... 4 2.3 Benefits Of RuPay Contactless...

Saraswat Co-operative Bank Ltd. Digital Banking Department. Frequently Asked Questions (FAQs) on Bharat QR. Version 1.0

on Bharat QR. Version 1.0") Saraswat Co-operative Bank Ltd Digital Banking Department Frequently Asked Questions (FAQs) on Bharat QR Version 1.0 1 P a g e Frequently Asked Questions (FAQs) 1. What is QR code? QR code is the digital

Saraswat Co-operative Bank Ltd Digital Banking Department Frequently Asked Questions (FAQs) on Bharat QR Version 1.0 1 P a g e Frequently Asked Questions (FAQs) 1. What is QR code? QR code is the digital

To: Financial Services Policy Committee of the Conference of Presidents Federal Reserve System

December 24, 2013 To: Financial Services Policy Committee of the Conference of Presidents Federal Reserve System Re: Response to Federal Reserve s Payment System Improvement - Public Consultation Paper

December 24, 2013 To: Financial Services Policy Committee of the Conference of Presidents Federal Reserve System Re: Response to Federal Reserve s Payment System Improvement - Public Consultation Paper

Innovation in Retail Payments Activities of the CPSS Working Group on Innovation

Innovation in Retail Payments Activities of the CPSS Working Group on Innovation The views and opinions expressed in this presentation are those of the speaker and do not necessarily reflect the position

Innovation in Retail Payments Activities of the CPSS Working Group on Innovation The views and opinions expressed in this presentation are those of the speaker and do not necessarily reflect the position

Journal of Internet Banking and Commerce

Journal of Internet Banking and Commerce An open access Internet journal (http://www.icommercecentral.com) Journal of Internet Banking and Commerce, December 2017, vol. 22, no. 3 STUDY OF CONSUMER PERCEPTION

Journal of Internet Banking and Commerce An open access Internet journal (http://www.icommercecentral.com) Journal of Internet Banking and Commerce, December 2017, vol. 22, no. 3 STUDY OF CONSUMER PERCEPTION

Cash Management Integrated solutions to consolidate your company s growth towards the future

Cash Management Integrated solutions to consolidate your company s growth towards the future 1 Cash Management, An integrated solution to consolidate your company s growth towards the future Scotiabank

Cash Management Integrated solutions to consolidate your company s growth towards the future 1 Cash Management, An integrated solution to consolidate your company s growth towards the future Scotiabank

LIST OF TABLES. Table No. Title Page No.

LIST OF TABLES Table No. Title Page No. 1.1 Number of Banks in Salem District 15 1.2 Number of bank Branches in Salem District 16 1.3 Number of Sample Size in Customers and Bank Executives in Salem District

LIST OF TABLES Table No. Title Page No. 1.1 Number of Banks in Salem District 15 1.2 Number of bank Branches in Salem District 16 1.3 Number of Sample Size in Customers and Bank Executives in Salem District

DIGITAL FINANCIAL SERVICES BASIC TERMINOLOGY

INCLUDING ACRONYMS FOR DFS TRANSACTIONS THIS GUIDELINE NOTE WAS DEVELOPED BY THE AFI DIGITAL FINANCIAL SERVICES (DFS) WORKING GROUP TO PROVIDE UNIVERSAL DEFINITIONS OF KEY DIGITAL FINANCIAL SERVICES TERMS.

INCLUDING ACRONYMS FOR DFS TRANSACTIONS THIS GUIDELINE NOTE WAS DEVELOPED BY THE AFI DIGITAL FINANCIAL SERVICES (DFS) WORKING GROUP TO PROVIDE UNIVERSAL DEFINITIONS OF KEY DIGITAL FINANCIAL SERVICES TERMS.

The Changing Landscape of Card Acceptance

The Changing Landscape of Card Acceptance Troy Byram Vice-President Sr. E-Receivables Consultant February 6, 2015 Agenda EMV (Chip and Pin) PCI Compliance and Data Security New Regulations for Municipalities

The Changing Landscape of Card Acceptance Troy Byram Vice-President Sr. E-Receivables Consultant February 6, 2015 Agenda EMV (Chip and Pin) PCI Compliance and Data Security New Regulations for Municipalities

Adoption of M- Wallet: A way Ahead

Volume-7, Issue-4, July-August 2017 International Journal of Engineering and Management Research Page Number: 1-7 Adoption of M- Wallet: A way Ahead Teena Wadhera 1, Richa Dabas 2, Parul Malhotra 3 1,2

Volume-7, Issue-4, July-August 2017 International Journal of Engineering and Management Research Page Number: 1-7 Adoption of M- Wallet: A way Ahead Teena Wadhera 1, Richa Dabas 2, Parul Malhotra 3 1,2

THE ROLE OF ICT INFRASTRUCTURE IN FINANCIAL INCLUSION: AN EMPIRICAL ANALYSIS

ISSN (Print): 0976-7185; ISSN (Online): 2349-2325 DOI: 10.16962/EAPJFRM/6_3_5 www.elkjournals.com Volume 6 Issue 3, 69-72 THE ROLE OF ICT INFRASTRUCTURE IN FINANCIAL INCLUSION: AN EMPIRICAL ANALYSIS Kawaljeet

ISSN (Print): 0976-7185; ISSN (Online): 2349-2325 DOI: 10.16962/EAPJFRM/6_3_5 www.elkjournals.com Volume 6 Issue 3, 69-72 THE ROLE OF ICT INFRASTRUCTURE IN FINANCIAL INCLUSION: AN EMPIRICAL ANALYSIS Kawaljeet

HOW WAS PAYCOR SELECTED AS THE SERVICE

PAYCOR FAQS HOW WAS PAYCOR SELECTED AS THE SERVICE PROVIDER? Representatives from all dioceses were involved in the selection process over the course of three months. Requests for Proposals sent to a dozen

PAYCOR FAQS HOW WAS PAYCOR SELECTED AS THE SERVICE PROVIDER? Representatives from all dioceses were involved in the selection process over the course of three months. Requests for Proposals sent to a dozen

Digital Banking BPC s Vision

Digital Banking BPC s Vision MEXICO CLIENT CONFERENCE 2017 BPC Banking Technologies 2017 Mexico City bpcbt.com Topics 1 Future of banking 2 Global digital innovation market trends 3 BPC Vision 4 BPC Solution

Digital Banking BPC s Vision MEXICO CLIENT CONFERENCE 2017 BPC Banking Technologies 2017 Mexico City bpcbt.com Topics 1 Future of banking 2 Global digital innovation market trends 3 BPC Vision 4 BPC Solution

Fintech Revolution - A Step towards Digitization of Payments: A Theoretical Framework

(Volume1, Issue2) Available online at: www.ijarnd.com Fintech Revolution - A Step towards Digitization of Payments: A Theoretical Framework Ms. Smrity Baiju, Prof. Ch. RadhaKumari 1 MBA II student, Department

(Volume1, Issue2) Available online at: www.ijarnd.com Fintech Revolution - A Step towards Digitization of Payments: A Theoretical Framework Ms. Smrity Baiju, Prof. Ch. RadhaKumari 1 MBA II student, Department

Project Financing Models

Project Financing Models Implementation of an e-passport or eid card can cost $ millions. There are 3 ways for a Government to allocate the budget: Direct Payment BOT (Build-Operate-Transfer) PPP (Public-Private

Project Financing Models Implementation of an e-passport or eid card can cost $ millions. There are 3 ways for a Government to allocate the budget: Direct Payment BOT (Build-Operate-Transfer) PPP (Public-Private

RESOLVING THE ISSUE OF LONG QUEUES IN CENTENARY BANK USING E-COMMERCE. Edgar Ahimbe - VUU-PGDBA Virtual University of Uganda

RESOLVING THE ISSUE OF LONG QUEUES IN CENTENARY BANK USING E-COMMERCE Edgar Ahimbe - VUU-PGDBA-2013-032 Virtual University of Uganda EXECUTIVE SUMMARY Centenary Bank is a leading microfinance commercial

RESOLVING THE ISSUE OF LONG QUEUES IN CENTENARY BANK USING E-COMMERCE Edgar Ahimbe - VUU-PGDBA-2013-032 Virtual University of Uganda EXECUTIVE SUMMARY Centenary Bank is a leading microfinance commercial

Financial Sector Master Plan Phase III ( ) Financial Sector Master Plan Phase III ( )

Financial Sector Master Plan Phase III ( )") Financial Sector Master Plan Phase III (2016-2020) Financial Sector Master Plan Phase III (2016-2020) Message from the Governor The Bank of Thailand (BOT) is committed to its role in supporting the Thai

Financial Sector Master Plan Phase III (2016-2020) Financial Sector Master Plan Phase III (2016-2020) Message from the Governor The Bank of Thailand (BOT) is committed to its role in supporting the Thai

VISO BUSINESS PLAN. Token sale level Funds raised. Technologies launched. Share of Georgia s cash-desk equipment market

B U S I N E S S P L A N VISO BUSINESS PLAN The business plan is designed for five scenarios based on the amount collected during the Token sale. The profitability of the VISO business model depends on

B U S I N E S S P L A N VISO BUSINESS PLAN The business plan is designed for five scenarios based on the amount collected during the Token sale. The profitability of the VISO business model depends on

Mobile banking: Moving beyond microfinance

Mobile banking: Moving beyond microfinance Thought Paper www.infosys.com/finacle Universal Banking Solution Systems Integration Consulting Business Process Outsourcing Mobile banking: Moving beyond microfinance

Mobile banking: Moving beyond microfinance Thought Paper www.infosys.com/finacle Universal Banking Solution Systems Integration Consulting Business Process Outsourcing Mobile banking: Moving beyond microfinance

CFO Perspectives India CFO Newsletter March 2017

CFO Perspectives India CFO Newsletter March 2017 CFO Speaks Mr. Sashi Jagdishan CFO HDFC Bank Ltd 1. What is your overall view on the union budget and more specifically how will it impact the Banking industry?

CFO Perspectives India CFO Newsletter March 2017 CFO Speaks Mr. Sashi Jagdishan CFO HDFC Bank Ltd 1. What is your overall view on the union budget and more specifically how will it impact the Banking industry?

MICROFINANCE INSTITUTIONS AND DIGITIZATION IN INDIA

MICROFINANCE INSTITUTIONS AND DIGITIZATION IN INDIA Adapted from the Handbook on Digital Financial Inclusion and Consumer Capabilities in India December 2017 SUMMARY The ecosystem of digital financial

MICROFINANCE INSTITUTIONS AND DIGITIZATION IN INDIA Adapted from the Handbook on Digital Financial Inclusion and Consumer Capabilities in India December 2017 SUMMARY The ecosystem of digital financial

GNFC Cashless Transactions

1 GNFC Cashless Transactions GNFC is the first and only Fertilizer Company in the Country for having adopted all of following methods of CASHLESS Transactions for sale of fertilizer since 3rd December

1 GNFC Cashless Transactions GNFC is the first and only Fertilizer Company in the Country for having adopted all of following methods of CASHLESS Transactions for sale of fertilizer since 3rd December

Developing financial services through the Post-Forum Berne, 23 April 2010 (POC C3 Forum Doc 1) Korea Post Financial Services

Korea Post Financial Services") Developing financial services through the Post-Forum Berne, 23 April 2010 (POC C3 Forum 2010. 1. Doc 1) Korea Post Financial Services 1. Positioning & Context 2. Organization 3. System & Network 4. Targets,

Developing financial services through the Post-Forum Berne, 23 April 2010 (POC C3 Forum 2010. 1. Doc 1) Korea Post Financial Services 1. Positioning & Context 2. Organization 3. System & Network 4. Targets,

EXPRESSION OF INTEREST FOR ONLINE PAYMENT COLLECTON SYSTEM

EXPRESSION OF INTEREST FOR ONLINE PAYMENT COLLECTON SYSTEM Indian Institute of Technology Guwahati Guwahati 781 039 Telephone :: 258 2021/258 2033 E-mail :: hosacc@iitg.ernet.in, iitgepay@iitg.ernet.in

EXPRESSION OF INTEREST FOR ONLINE PAYMENT COLLECTON SYSTEM Indian Institute of Technology Guwahati Guwahati 781 039 Telephone :: 258 2021/258 2033 E-mail :: hosacc@iitg.ernet.in, iitgepay@iitg.ernet.in

Basic Account. The essential guide to your new account

Basic Account The essential guide to your new account Our commitment to you We re committed to becoming Scotland s most helpful bank. It s not just words, it s a goal at our very core, guided by four commitments

Basic Account The essential guide to your new account Our commitment to you We re committed to becoming Scotland s most helpful bank. It s not just words, it s a goal at our very core, guided by four commitments

THE ADOPTION OF EMV TECHNOLOGY IN THE U.S. By Guy Berg Global Industry Sales Consultant Datacard Group

THE ADOPTION OF EMV TECHNOLOGY IN THE U.S. By Guy Berg Global Industry Sales Consultant Datacard Group Abstract: Visa Inc. and MasterCard recently announced plans to accelerate chip migration in the United

THE ADOPTION OF EMV TECHNOLOGY IN THE U.S. By Guy Berg Global Industry Sales Consultant Datacard Group Abstract: Visa Inc. and MasterCard recently announced plans to accelerate chip migration in the United

Strategy to Accelerate Migration to e-payments in Malaysia

Strategy to Accelerate Migration to e-payments in Malaysia Nurul Ashikin Mohammad Bokhari Payment System Policy Department Bank Negara Malaysia 1 Global Payments Week 20 September 2016 Despite a highly

Strategy to Accelerate Migration to e-payments in Malaysia Nurul Ashikin Mohammad Bokhari Payment System Policy Department Bank Negara Malaysia 1 Global Payments Week 20 September 2016 Despite a highly

National Common Mobility Card (NCMC) RuPay qsparc Dual Interface Card

RuPay qsparc Dual Interface Card") NCMC National Common Mobility Card (NCMC) RuPay qsparc Dual Interface Card Payment Platforms by NPCI Number of Banks covered so far Sr. no. Product/ Platform Member Banks Direct Sub- Member Total 1 NFS

NCMC National Common Mobility Card (NCMC) RuPay qsparc Dual Interface Card Payment Platforms by NPCI Number of Banks covered so far Sr. no. Product/ Platform Member Banks Direct Sub- Member Total 1 NFS

NATIONAL CTS A way forward

NATIONAL CTS A way forward By Anand Natarajan With the implementation of Cheque Truncation on a Pilot basis in New Delhi, India, RBI has ushered a beginning to the era of paper cheques and instruments

NATIONAL CTS A way forward By Anand Natarajan With the implementation of Cheque Truncation on a Pilot basis in New Delhi, India, RBI has ushered a beginning to the era of paper cheques and instruments

Custom Benchmarking Report for Mobile Money. Anonymised version Dummy Data March 2017

Custom Benchmarking Report for Mobile Money Anonymised version Dummy Data March 2017 Analysis is based on 100+ mobile money providers who participated in the 2016 Global Annual Adoption survey Europe &

Custom Benchmarking Report for Mobile Money Anonymised version Dummy Data March 2017 Analysis is based on 100+ mobile money providers who participated in the 2016 Global Annual Adoption survey Europe &

Security enhancement on HSBC India Debit Card

Security enhancement on HSBC India Debit Card A Secure Debit Card HSBC India Debit Cards are more secure and enabled with the Chip and PIN technology. In addition to this you can restrict usage of the

Security enhancement on HSBC India Debit Card A Secure Debit Card HSBC India Debit Cards are more secure and enabled with the Chip and PIN technology. In addition to this you can restrict usage of the

Procedural Guidelines RuPay QR code

Procedural Guidelines RuPay QR code Version 1.0 Version 1.0 Page 1 of 8 Amendment History Sr. Version number Summary of Change Change Month & Year 1 1.0 Initial Version Feb 2017 2 3 Version 1.0 Page 1

Procedural Guidelines RuPay QR code Version 1.0 Version 1.0 Page 1 of 8 Amendment History Sr. Version number Summary of Change Change Month & Year 1 1.0 Initial Version Feb 2017 2 3 Version 1.0 Page 1

EMPIRICAL ANALYSIS OF E-BANKING IN INDIA

EMPIRICAL ANALYSIS OF E-BANKING IN INDIA CHAND SINGH M.Com, JRF, UGC-NET ABSTRACT Under the impact of banking sector reforms, the Indian banking has transformed to a dynamic entity. This transformation

EMPIRICAL ANALYSIS OF E-BANKING IN INDIA CHAND SINGH M.Com, JRF, UGC-NET ABSTRACT Under the impact of banking sector reforms, the Indian banking has transformed to a dynamic entity. This transformation

USTGlobal. DIGITAL BANKING TRENDS AND INNOVATIONS A UST Global POV

USTGlobal DIGITAL BANKING TRENDS AND INNOVATIONS A UST Global POV September, 2016 DIGITAL BANKING TRENDS & INNOVATIONS Introduction Digital banking is not an option; rather, it is a must-have strategy

USTGlobal DIGITAL BANKING TRENDS AND INNOVATIONS A UST Global POV September, 2016 DIGITAL BANKING TRENDS & INNOVATIONS Introduction Digital banking is not an option; rather, it is a must-have strategy

Empowering Citizens through Open APIs. Digital India Case Study

Empowering Citizens through Open APIs Digital India Case Study India One of the Oldest Civilization Spiritual Center of the World Culmination of diverse cultures 1.25 Billion 29 States and 7 Union Territories

Empowering Citizens through Open APIs Digital India Case Study India One of the Oldest Civilization Spiritual Center of the World Culmination of diverse cultures 1.25 Billion 29 States and 7 Union Territories

AGENT INSTITUTION Presentation

AGENT INSTITUTION Presentation Agenda All About BBPS RBI Circular Agent Institution within BBPS On-boarding Process Technical Requirement Agenda All About BBPS RBI Circular Agent Institution within BBPS

AGENT INSTITUTION Presentation Agenda All About BBPS RBI Circular Agent Institution within BBPS On-boarding Process Technical Requirement Agenda All About BBPS RBI Circular Agent Institution within BBPS

Cash account. Current accounts

Cash account. Current accounts What you can do with your Cash account. Here s a quick look at what you get with your Cash account. You can find out more about these features further on in the brochure.

Cash account. Current accounts What you can do with your Cash account. Here s a quick look at what you get with your Cash account. You can find out more about these features further on in the brochure.

EXCESS CAPACITY EXCHANGE

EXCESS CAPACITY EXCHANGE Automated Sales Platform for selling off all your products in 24 hours. 100% GUARANTEED! Every day, there is $34 trillion of excess production capacity, idle space, unsold products

EXCESS CAPACITY EXCHANGE Automated Sales Platform for selling off all your products in 24 hours. 100% GUARANTEED! Every day, there is $34 trillion of excess production capacity, idle space, unsold products

ADDENDUM NO. 3 REQUEST FOR PROPOSAL NO. R BANKING AND MERCHANT SERVICES FOR HIGHER EDUCATION

ADDENDUM NO. 3 Attention to Proposers: This constitutes Addendum No. 3 to the referenced Request for Proposals (RFP), and consists of this ten (10) page cover letter, which provides responses to questions

ADDENDUM NO. 3 Attention to Proposers: This constitutes Addendum No. 3 to the referenced Request for Proposals (RFP), and consists of this ten (10) page cover letter, which provides responses to questions

The Emerging Trends In Indian Banking And Payment System

The Emerging Trends In Indian Banking And Payment System Gurmeet Singh Assistant Professor in Economics, Government College for Girls, Ludhiana Abstract: With the ushering in f economic reforms in India

The Emerging Trends In Indian Banking And Payment System Gurmeet Singh Assistant Professor in Economics, Government College for Girls, Ludhiana Abstract: With the ushering in f economic reforms in India

The Commission Card is a Direct Selling Company branded VISA debit card issued by Money Network.

The Commission Card is a Direct Selling Company branded VISA debit card issued by Money Network. Consultants will be able to access their commissions by: Electronically transferring their commission payment

The Commission Card is a Direct Selling Company branded VISA debit card issued by Money Network. Consultants will be able to access their commissions by: Electronically transferring their commission payment

Diploma in Indian Payroll & Statutory Compliances Management

PREMIER ACADEMY OF HR PROFESSIONLS EIGHTH INNOVATIVE CONSULTANTS PRIVATE LIMITED Launching Diploma in Indian Payroll & Statutory Compliances Management (DIPSCM) 6 Months Enrollment starts for June 2014

PREMIER ACADEMY OF HR PROFESSIONLS EIGHTH INNOVATIVE CONSULTANTS PRIVATE LIMITED Launching Diploma in Indian Payroll & Statutory Compliances Management (DIPSCM) 6 Months Enrollment starts for June 2014

E-Banking: A Pioneering Service Approach in Commercial Banks in India

Volume 8, Issue 4, October 2015 E-Banking: A Pioneering Service Approach in Commercial Banks in India Pooja Research Scholar (SRF) Faculty of Commerce, Banaras Hindu University Abstract Demand for financial

Volume 8, Issue 4, October 2015 E-Banking: A Pioneering Service Approach in Commercial Banks in India Pooja Research Scholar (SRF) Faculty of Commerce, Banaras Hindu University Abstract Demand for financial

Financial Literacy Project in Digitally Enabled Vattavada Gram Panchayat, Kerala

Financial Literacy Project in Digitally Enabled Vattavada Gram Panchayat, Kerala Submitted to NPCI July 2017 Acknowledgement MicroSave has developed this report with support of National Payments Corporation

Financial Literacy Project in Digitally Enabled Vattavada Gram Panchayat, Kerala Submitted to NPCI July 2017 Acknowledgement MicroSave has developed this report with support of National Payments Corporation

BancAnalysts Association of Boston Conference

BancAnalysts Association of Boston Conference Avid Modjtabai Senior Executive Vice President Payments, Virtual Solutions, and Innovation November 2, 2017 2017 Wells Fargo Bank, N.A. All rights reserved.

BancAnalysts Association of Boston Conference Avid Modjtabai Senior Executive Vice President Payments, Virtual Solutions, and Innovation November 2, 2017 2017 Wells Fargo Bank, N.A. All rights reserved.

Scheme Document of Pradhan Mantri Kaushal Vikas Yojana

Scheme Document of Pradhan Mantri Kaushal Vikas Yojana Date of Release: 28 April 2015 Page 1 of 10 Table of Contents 1. Objectives... 3 2. Background... 3 3. Strategy and Approach... 4 4. Key features...

Scheme Document of Pradhan Mantri Kaushal Vikas Yojana Date of Release: 28 April 2015 Page 1 of 10 Table of Contents 1. Objectives... 3 2. Background... 3 3. Strategy and Approach... 4 4. Key features...

A Conversation with Visa on Consumer Debit Growth Connie Davis FIS Global Retail Payments Greg Borchardt Visa Consumer Debit Products

A Conversation with Visa on Consumer Debit Growth Connie Davis FIS Global Retail Payments Greg Borchardt Visa Consumer Debit Products May 2017 Visa Notice of Confidentiality This presentation is furnished

A Conversation with Visa on Consumer Debit Growth Connie Davis FIS Global Retail Payments Greg Borchardt Visa Consumer Debit Products May 2017 Visa Notice of Confidentiality This presentation is furnished

COMMERCIAL STUDIES (63)

") COMMERCIAL STUDIES (63) Aims: 1. To enable students to develop a perceptive, sensitive and critical response to the role of business in a global, national and local context. 2. To allow students to balance

COMMERCIAL STUDIES (63) Aims: 1. To enable students to develop a perceptive, sensitive and critical response to the role of business in a global, national and local context. 2. To allow students to balance

Genesis Block Development

Genesis Block Development Who we are We are a group of companies engaged in software development, payment systems implementation, software and web solutions for e-commerce and blockchain solutions for

Genesis Block Development Who we are We are a group of companies engaged in software development, payment systems implementation, software and web solutions for e-commerce and blockchain solutions for

Revolutionize Your Business with Harbortouch

Revolutionize Your Business with Harbortouch Swipe Card Regardless of the business you are in, Harbortouch has the ideal processing solution for you. Allow Harbortouch to demonstrate why our company is

Revolutionize Your Business with Harbortouch Swipe Card Regardless of the business you are in, Harbortouch has the ideal processing solution for you. Allow Harbortouch to demonstrate why our company is

The Future of Payment Security in Canada

The Future of Payment Security in Canada October 2017 1 Visa Canada Public The Future of Payment Security in Canada Notices Forward-Looking Statements This presentation contains forward-looking statements

The Future of Payment Security in Canada October 2017 1 Visa Canada Public The Future of Payment Security in Canada Notices Forward-Looking Statements This presentation contains forward-looking statements

Virtual Currency and Electronic Money Movers: AML Red Flags. John A. Beccia, Circle Internet Financial

Virtual Currency and Electronic Money Movers: AML Red Flags John A. Beccia, Circle Internet Financial Discussion Topics Background on Digital Currency and Emerging Payments Regulatory Update Assessing

Virtual Currency and Electronic Money Movers: AML Red Flags John A. Beccia, Circle Internet Financial Discussion Topics Background on Digital Currency and Emerging Payments Regulatory Update Assessing

MODERN OFFICE PRACTICE

MODERN OFFICE PRACTICE UNIT 1: ACCOUNTS & FINANCE Basic Accounting concepts Capital & Revenue Financial statements - Preparation of final Accounts Schedule VI Part I & Part II. Partnership Accounts - Admission,

MODERN OFFICE PRACTICE UNIT 1: ACCOUNTS & FINANCE Basic Accounting concepts Capital & Revenue Financial statements - Preparation of final Accounts Schedule VI Part I & Part II. Partnership Accounts - Admission,

Prepaid Cards. Coles Gift Mastercard Conditions of Use. Issued by: Indue Ltd Issue Date: July 2017 ABN

Prepaid Cards Coles Gift Mastercard Conditions of Use Issued by: Indue Ltd Issue Date: July 2017 ABN 97 087 822 464 1 Coles Gift Mastercard Conditions of Use Contents What you re agreeing to 3 Tips to

Prepaid Cards Coles Gift Mastercard Conditions of Use Issued by: Indue Ltd Issue Date: July 2017 ABN 97 087 822 464 1 Coles Gift Mastercard Conditions of Use Contents What you re agreeing to 3 Tips to

Retail banking in a digital world. December 2015

Retail banking in a digital world December 2015 Certain statements in these slides are forward-looking statements. These statements are based on management's current expectations and are subject to uncertainty

Retail banking in a digital world December 2015 Certain statements in these slides are forward-looking statements. These statements are based on management's current expectations and are subject to uncertainty

Mobile Financial Services : Perspectives with Agent Networks

Mobile Financial Services : Perspectives with Agent Networks Discussion Leaders Jordan Weinstock, OpenRevolution Leo Tobias, Grameen Foundation Session Information Introductions Approaching the Business

Mobile Financial Services : Perspectives with Agent Networks Discussion Leaders Jordan Weinstock, OpenRevolution Leo Tobias, Grameen Foundation Session Information Introductions Approaching the Business

One Signature. Many Privileges.

One Signature. Many Privileges. Discover the power of Your new Signature Card Signature Contactless Your Signature Contactless Card allows you to transact at express speed. Simply wave your Signature Contactless

One Signature. Many Privileges. Discover the power of Your new Signature Card Signature Contactless Your Signature Contactless Card allows you to transact at express speed. Simply wave your Signature Contactless

CHALLENGES (BARRIERS) IN ADOPTING THE ELECTRONIC COMMERCE SYSTEM IN LIC OF INDIA

IN ADOPTING THE ELECTRONIC COMMERCE SYSTEM IN LIC OF INDIA") CHAPTER-6 CHALLENGES (BARRIERS) IN ADOPTING THE ELECTRONIC COMMERCE SYSTEM IN LIC OF INDIA 6.1 Introduction : e-insurance is the application of Internet and related technologies to the production and distribution

CHAPTER-6 CHALLENGES (BARRIERS) IN ADOPTING THE ELECTRONIC COMMERCE SYSTEM IN LIC OF INDIA 6.1 Introduction : e-insurance is the application of Internet and related technologies to the production and distribution

SNAP and CASH EBT 201: The Detailed ins and outs of SNAP and CASH EBT. EBT Next Generation 2016

SNAP and CASH EBT 201: The Detailed ins and outs of SNAP and CASH EBT Presenters: Todd Halter, MBA, PMP Vice President Xerox State and Local Solutions, Inc. Doug Darr, MS, PMP Regional Director Xerox State

SNAP and CASH EBT 201: The Detailed ins and outs of SNAP and CASH EBT Presenters: Todd Halter, MBA, PMP Vice President Xerox State and Local Solutions, Inc. Doug Darr, MS, PMP Regional Director Xerox State

Muhammad bin Ibrahim: The dawn of a new era in Malaysia's payment systems

Muhammad bin Ibrahim: The dawn of a new era in Malaysia's payment systems Keynote address by Mr Muhammad bin Ibrahim, Governor of the Central Bank of Malaysia (Bank Negara Malaysia), at the Malaysian E-Payments

Muhammad bin Ibrahim: The dawn of a new era in Malaysia's payment systems Keynote address by Mr Muhammad bin Ibrahim, Governor of the Central Bank of Malaysia (Bank Negara Malaysia), at the Malaysian E-Payments

ATM Webinar Questions and Answers May, 2014

May, 2014 Debit Network Alliance LLC (DNA) is a Delaware Limited Liability Company currently comprised of 10 U.S. Debit Networks and open to all U.S. Debit Networks. The goal of this collaborative effort

May, 2014 Debit Network Alliance LLC (DNA) is a Delaware Limited Liability Company currently comprised of 10 U.S. Debit Networks and open to all U.S. Debit Networks. The goal of this collaborative effort

ECB-PUBLIC REGULATION OF THE EUROPEAN CENTRAL BANK. of 28 November on payments statistics (ECB/2013/43)

") EN ECB-PUBLIC REGULATION OF THE EUROPEAN CENTRAL BANK of 28 November 2013 on payments statistics (ECB/2013/43) THE GOVERNING COUNCIL OF THE EUROPEAN CENTRAL BANK, Having regard to the Statute of the European

EN ECB-PUBLIC REGULATION OF THE EUROPEAN CENTRAL BANK of 28 November 2013 on payments statistics (ECB/2013/43) THE GOVERNING COUNCIL OF THE EUROPEAN CENTRAL BANK, Having regard to the Statute of the European

Accelerating the deployment of mobile money The Haiti case

Accelerating the deployment of mobile money The Haiti case Michel Stéphane Bruno Chargé de mission pour les services numériques Sogebank 06.02.16 Plan The Haiti Mobile Money Initiative o Background o Description

Accelerating the deployment of mobile money The Haiti case Michel Stéphane Bruno Chargé de mission pour les services numériques Sogebank 06.02.16 Plan The Haiti Mobile Money Initiative o Background o Description

ANZ EFTPOS card and ANZ Visa Debit card CONDITIONS OF USE

ANZ EFTPOS card and ANZ Visa Debit card CONDITIONS OF USE As part of our commitment to you, this document meets the WriteMark Plain English Standard. If you have any questions about these Conditions of

ANZ EFTPOS card and ANZ Visa Debit card CONDITIONS OF USE As part of our commitment to you, this document meets the WriteMark Plain English Standard. If you have any questions about these Conditions of

The Bank of Elk River: Digital Wallet Terms and Conditions

The Bank of Elk River: Digital Wallet Terms and Conditions These Terms of Use ("Terms") govern your use of any eligible debit card issued by The Bank of Elk River (a "Payment Card") when you add, attempt

The Bank of Elk River: Digital Wallet Terms and Conditions These Terms of Use ("Terms") govern your use of any eligible debit card issued by The Bank of Elk River (a "Payment Card") when you add, attempt

Banking at the speed of your life. Online. Mobile. Superior. Safe. PARKSTERLING. Answers You Can Bank On.

Banking at the speed of your life. Online. Mobile. Superior. Safe. PARKSTERLING SM Answers You Can Bank On. At Park Sterling Bank, we know that there are times when our answer can help expand a child s

Banking at the speed of your life. Online. Mobile. Superior. Safe. PARKSTERLING SM Answers You Can Bank On. At Park Sterling Bank, we know that there are times when our answer can help expand a child s

Example - ETH-funded Purchase with Hash Card 5

1 of 19 Hash Card Executive Summary 3 The Hash Card 4 Example - ETH-funded Purchase with Hash Card 5 Hash Card Token Benefits 7 Card Variety 8 Payment system process 10 Technology and Security 11 Timeline

1 of 19 Hash Card Executive Summary 3 The Hash Card 4 Example - ETH-funded Purchase with Hash Card 5 Hash Card Token Benefits 7 Card Variety 8 Payment system process 10 Technology and Security 11 Timeline

A STUDY ON USAGE OF PAYTM

A STUDY ON USAGE OF PAYTM ABHIJIT M. TADSE Institute of Management Development and Research, Pune (MS) INDIA. HARMEET SINGH NANNADE Institute of Management Development and Research, Pune (MS) INDIA. Smartphone

A STUDY ON USAGE OF PAYTM ABHIJIT M. TADSE Institute of Management Development and Research, Pune (MS) INDIA. HARMEET SINGH NANNADE Institute of Management Development and Research, Pune (MS) INDIA. Smartphone

Gift & Loyalty Cards

Gift & Loyalty Cards Business Development Our Gift & Loyalty card program will afford you one of the most powerful and profitable tools to grow your business on a daily basis. Let our systems do the work

Gift & Loyalty Cards Business Development Our Gift & Loyalty card program will afford you one of the most powerful and profitable tools to grow your business on a daily basis. Let our systems do the work

The Future of Retail Banking Lies Within its Channels

The Future of Retail Banking Lies Within its Channels Thought Paper www.infosys.com/finacle Universal Banking Solution Systems Integration Consulting Business Process Outsourcing The future of retail banking

The Future of Retail Banking Lies Within its Channels Thought Paper www.infosys.com/finacle Universal Banking Solution Systems Integration Consulting Business Process Outsourcing The future of retail banking

The Payment Solution for Blockchain

OVERNODES The Payment Solution for Blockchain Jan. 2018 Overnodes Solution Brochure INFO@OVERNODES.COM This document is current as of the initial date of publication and may be changed by Overnodes at

OVERNODES The Payment Solution for Blockchain Jan. 2018 Overnodes Solution Brochure INFO@OVERNODES.COM This document is current as of the initial date of publication and may be changed by Overnodes at

(To be printed on stamp paper, signed and stamped on each page and duly notarized by an empanelled Notary Public)

") (To be printed on stamp paper, signed and stamped on each page and duly notarized by an empanelled Notary Public) Affidavit for PMGDISHA Scheme to be furnished by CSCs I,, Aged Years, representing (Name

(To be printed on stamp paper, signed and stamped on each page and duly notarized by an empanelled Notary Public) Affidavit for PMGDISHA Scheme to be furnished by CSCs I,, Aged Years, representing (Name

How Oracle FLEXCUBE can change the face of Rural Banking

How Oracle FLEXCUBE can change the face of Rural Banking Maha Srinivasan Oracle Financial Services Global Business Unit 1 Potential for Rural Banks profitable growth Young Population spurs demand Mobile

How Oracle FLEXCUBE can change the face of Rural Banking Maha Srinivasan Oracle Financial Services Global Business Unit 1 Potential for Rural Banks profitable growth Young Population spurs demand Mobile

Automation and optimization of the whole financial processing chain the key to success.

Tieto 2010 Automation and optimization of the whole financial processing chain the key to success. Table of contents Financial Processing Chain Implementation 4 Integrating Business Messages and Connectivity

Tieto 2010 Automation and optimization of the whole financial processing chain the key to success. Table of contents Financial Processing Chain Implementation 4 Integrating Business Messages and Connectivity

Banking on gender differences? Similarities and differences in financial services preferences of women and men in a digital world

Banking on gender differences? Similarities and differences in financial services preferences of women and men in a digital world are embracing mobile financial services at higher rates. Banking on gender

Banking on gender differences? Similarities and differences in financial services preferences of women and men in a digital world are embracing mobile financial services at higher rates. Banking on gender

LEANER AND ROBUST BACK END SUPPORTING FRONT END REQUISITES. - Rahul Modi, MD & CEO, Adarsh Credit Cooperative Society Ltd.

LEANER AND ROBUST BACK END SUPPORTING FRONT END REQUISITES - Rahul Modi, MD & CEO, Adarsh Credit Cooperative Society Ltd. 1 Core Transformation Journey and Financial Inclusion Co-operative Sector in India

LEANER AND ROBUST BACK END SUPPORTING FRONT END REQUISITES - Rahul Modi, MD & CEO, Adarsh Credit Cooperative Society Ltd. 1 Core Transformation Journey and Financial Inclusion Co-operative Sector in India

An Employer s Guide to Payroll Cards

An Employer s Guide to Payroll Cards An important part of your role as an employer is to ensure that you pay your workers promptly and accurately, and that you comply with federal and state payroll laws

An Employer s Guide to Payroll Cards An important part of your role as an employer is to ensure that you pay your workers promptly and accurately, and that you comply with federal and state payroll laws