A VISION FOR THE UK HYDROGEN ECONOMY SUPPORTING THE ROLE OF JOHNSON MATTHEY FUEL CELLS AS A POLICY AND COMMERCIAL LEADER

|

|

|

- Jemima Hudson

- 6 years ago

- Views:

Transcription

1 A VISION FOR THE UK HYDROGEN ECONOMY SUPPORTING THE ROLE OF JOHNSON MATTHEY FUEL CELLS AS A POLICY AND COMMERCIAL LEADER

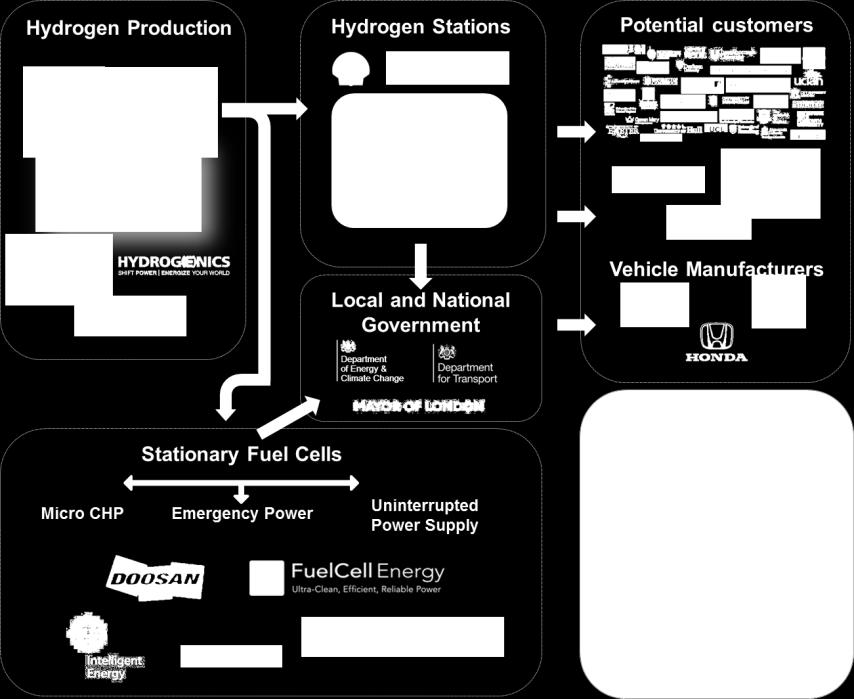

2 Overview Johnson Matthey is in a unique position to both drive the advancement of the UK hydrogen economy, and also ultimately benefit from it as a large UK-based company. Holding a respected position among industry peers and government alike, Johnson Matthey has the potential to develop the public and private collaborations necessary for the development of the hydrogen economy, and influence its direction also. In addition with the company selling fuel cell (FC) components to a wide range of applications, it has the benefit of being able to develop synergies between differing industries and also being in a position to foster a holistic image of a hydrogen fuelled economy. Hydrogen technologies offer the UK a long-term opportunity to cost-effectively deliver secure, high quality energy services whilst significantly reducing greenhouse gas (GHG) emissions and local pollution. Infrastructure development is vitally needed to facilitate the advancement of the hydrogen economy, yet this will be slow to emerge without adequate demonstration and growth of demand for fuel cells and hydrogen energy. The following roadmap will outline a template for financially practicable phases which can support the transition from small scale demonstrations to greater energy system contribution, and has three steps: Phase 1 o Stationary fuel-cell applications in targeted sources of demand (e.g. hospitals or universities) Phase 2 o The initial development of a refuelling station network characterised by hydrogen produced by steam reforming, pre-determined back-to-base vehicle fleet demand, and a mother-anddaughter style refuelling station network set up Phase 3 o Further refuelling station network development, with green hydrogen produced by water electrolysis powered from renewable electricity 2

3 In terms of taking forward the conclusions of this analysis, the roadmap identifies the following related activities: Engage with private actors o Proactively identify and approach in a concerted manner specific potential consumers, including owners of captive vehicle fleets and large building owners with significant heating and power demand o Lead on the formation of a consortium of companies across the supply chain wishing to develop hydrogen hub projects and influence policy Engage with the new UK government; o Pursue greater recognition for stationary applications in government publications based on feasible policy change (e.g. CCC s 5th carbon budget) and ultimately support in the form of a mandate to public bodies, and/or policy such as a fuel cell FiT, improved CHPQA, support for hydrogen generation etc. o Pursue financial support for specific hydrogen hub demonstration projects Increased exposure and publicity o Develop proactive and focused collaboration with policy stakeholders so as to become the point of reference for the hydrogen economy in the UK o Engage in publication of informed positions on the hydrogen economy and proactive participation in key conferences and fora 3

4 4

5 Contents Introduction 6 Scope 7 Key recommendations 8 Stationery fuel cell market 8 The hydrogen hub 9 A policy engagement plan for 2015/16 10 Hydrogen Hub Roadmap 12 Towards the hydrogen economy 12 Hydrogen hub roadmap overview 13 Phase 1 Deployment of stationary fuel cells 14 Phase 2 Targeted hydrogen hub projects 17 Phase 3 Wider hydrogen infrastructure 21 UK Energy Policy: Energy Trilemma 25 1 Energy cost 25 2 Energy security 26 3 CO 2 and environmental performance 26 Appendix 28 1 Data assumptions 28 2 Levelised cost methodology 30 3 Case study 1: fuel cell installations in hospitals 31 4 Delivery of Hydrogen 35 5 Case study 2:fuel cell material handling vehicles (MHVs) 38 5

6 Introduction With a range of end-use applications and production methods, hydrogen is an incredibly versatile energy carrier which can transform the energy landscape. However realising the potential of hydrogen has been hindered by low deployment volumes. Without scaling production, costs have not been able to fall low enough to attract a large market share. In order to break this cycle, a variety of actions will need to be taken. Firstly, financial support can create lower costs for consumers facilitating the higher production volumes necessary to achieve economies of scale and learning-by-doing. There is also a need for cohesion amongst the supply chain to avoid a first mover disadvantage; fuel cell electric vehicle (FCEV) deployment is not viable until hydrogen refuelling stations are deployed and vice versa. This high level business case develops a roadmap which draws from government support and the hydrogen supply chain to deliver hydrogen infrastructure projects. Starting from smaller scale operations, Ecuity assesses the opportunities for Johnson Matthey and partners to deliver targeted schemes (hydrogen hubs) which demonstrate hydrogen generation, distribution and utilisation in different markets. These hydrogen hubs can help to facilitate the necessary industry collaboration, government endorsement and customer demand to bring hydrogen technologies to the wider market. 6

7 Scope The development and operation of hydrogen hubs today may not be immediately profitable, but the long-term goal of mass-market stationary and FCEV applications has enormous potential. As this document will demonstrate the targeted deployment of fuel cells is already commercially viable in many areas, whilst the development of integrated hydrogen hubs requires further steps to reach wider market adoption. Johnson Matthey is in a strong position to drive this process which begins with the demonstration that this hydrogen future is viable from: Crucially the hydrogen hub should demonstrate scalability and through wider applications and increased volumes the potential for learning-by-doing, expertise and supply chain efficiencies, and ultimately cost reductions through economies of scale. By driving this process Johnson Matthey will stand to best benefit from any infrastructure and industry development, and will become an integral part of the supply chain. (a) a technical perspective (b) that supply chains can be developed to provide a reliable supply of hydrogen (c) a positive consumer experience and need 7

8 Key Recommendations 2015 is an important time to start engaging with public and private actors in particular following 7 th May and the voting in of a new government. Fuel cell technologies have been underacknowledged and supported in previous UK government documents such as DECC s Heat Strategy and CCC Carbon Budgets - which underpin policy design. Stationary fuel cell market The analysis included in this paper has demonstrated the economic viability and environmental benefits of stationary fuel cells. The technology is easily integrated into current energy systems and the next step for Johnson Matthey and partners would be engagement with: (i) Sources of specific demand. In particular organisations with consistently high heat loads. Aim of publicising the technology and reducing any perceived risk of investment (ii) The new government. Both in terms of hard policy and recognition of the benefits of fuel cells, greater support may be required to increase exposure, volumes of sales and ultimately reduce costs Again scalability is an important element of any strategy for Johnson Matthey. In the case of initial demonstrations, these could ideally be targeted at public institutions such as universities or hospitals which are highly visible. Publicising the experienced benefit of such installations can lower the perceived risk of investment in a nascent technology for NHS Trusts and other potential customers. This is especially important for organisations operating in the third sector which can commonly be conservative in regards to investment decisions and therefore precedents are needed. With organisations initially perceiving investment in new technologies as risky, government support can be instrumental in addressing concerns and supporting the growth of the nascent industry. At the very least Johnson Matthey should be engaging with policymakers to encourage greater acknowledgment of fuel cells in government publications. Ultimately the industry would benefit from greater support in policy perhaps through a wider feed-intariff (FiT) scheme or a more supportive (of higher electrical efficiency) CHPQA policy. 8 8

9 The hydrogen hub The long-term goal is the development of the hydrogen and fuel cell economy. Johnson Matthey can deliver this vision to a new government following the May elections. Engagement with the Committee on Climate Change who are writing the UK s 5 th Carbon Budget this year 1, DECC, DEFRA, the Department of Transport and the Office for Low Emission Vehicles will all also be important. It is essential for policymakers to understand and start endorsing the aspirational aims of the development of hydrogen hubs. In the nearer term, Johnson Matthey can start engaging with other supply chain actors to develop a consortium of companies who wish to collaborate on the delivery of at least one hydrogen hub project. This will likely be able to attract support from a UK public body (e.g. Innovate UK) or an EUwide initiative (e.g. Horizon 2020) 9

10 A policy engagement plan for 2015/16 Following the May 2015 General Elections, the focus will now return to policy design. That generates a unique opportunity to engage policy makers towards the attainment of strategic recognition and concrete policy support for fuel cells and hydrogen applications and projects. An engagement plan based on specific and feasible policy objectives is necessary to achieve results based on prior experience with novel low carbon technologies. Johnson Matthey, as major domestic player with a wide presence across the supply chain, is well placed to drive discussions during 2015/16 based on the below objectives: 1. Strategic recognition for fuel cells and hydrogen The potential strategic role of fuel cells and hydrogen is currently note capture in strategic documents that underpin energy policy including the Heat Strategy, the Carbon Plan or the Carbon Budgets. A review of the Heat Strategy and the development of the 5 th Carbon Budget provide an opportunity for formal strategic recognition, subsequent policy support and market exposure. 2. Support for stationary fuel cells under FITs Although primary legislation, based on the 2008 Energy Act, envisages support for fuel cells under the FIT scheme currently the technology is not supported. The formal 2015 FIT review provides an opportunity to achieve some form of formal and separate financial support for fuel cell technologies under the scheme. 3. Support for the generation of hydrogen A Department for Transport (DfT) consultation during 2014 proposed to consider allowing in the future synthetic fuels or hydrogen from renewable electricity to receive support under the RTFO. It is important to take note and follow up on this development, based on comprehensive evidence, so as to achieve the support of hydrogen generation from renewable electricity.

11 4. Enhanced support vs. conventional CHP DECC undertook a review of CHP financial support during 2014 that did not incorporate or consider fuel cells. DECC CHP work continued during 2015 focusing on non-financial obstacles again not capturing fuel cells. An opportunity exists to pursue a structured review of financial and non-financial obstacles for stationary fuel cells with a view to enhanced support or tax incentives vs. conventional engine driven CHP applications. 5. A targeted mandate or demonstration for fuel cells Efficiency is expected to be a central component of energy policy irrespective of the party, or coalition of parties, that will be in power following the May elections. A mandate or a demonstration project for a fixed number of stationary fuel cell applications in public buildings with high energy demand (e.g. hospitals) where the technology already makes financial sense is a feasible and defendable policy outcome. 6. Enhancing the economics of electrolysis The National Grid provides constraint payments to wind generators to stop generating when balancing requirements dictate. This led to circa 55m of payments during 2014 at an average price of 86/MWh. This is a highly emotive topic for a range of policy stakeholders. Diverting some of these payments for the generation of hydrogen from excess wind could be explored as an option following the elections. 11

12 Hydrogen Hub Roadmap Towards the hydrogen economy While a hydrogen economy has the potential to displace much of the embedded hydrocarbon infrastructure, widespread uptake cannot be achieved overnight. Hydrogen utilisation is not viable without supporting infrastructure, and this infrastructure not viable without appropriate demand. The high capital costs of infrastructure warrant targeted approaches initially, where projects are focused in locations of suitable demand. These initial infrastructure projects can be described as hydrogen hubs. A hydrogen hub does not refer to a specific application of hydrogen technology. Rather, it is a broadly defined infrastructure project which incorporates several components of the hydrogen supply chain to serve a targeted market. The range of scales of production, distribution and applications of hydrogen at the hubs is vast. By starting with smaller, more targeted hubs with assured markets, Johnson Matthey can begin to develop the infrastructure, lower the production costs and demonstrate the commercial attractiveness which is necessary for creating a larger hydrogen economy. This analysis proposes a roadmap for hydrogen deployment. The roadmap defines three broad phases which describes how hydrogen technologies, and their associated supply chains, can be developed with hydrogen hubs before widespread adoption is achieved. This section will describe the business case for proposed hydrogen hubs in phases one, two and three. Each hydrogen hub proposal brings about its own contextually specific risks, opportunities, costs and benefits. These characteristics are discussed within the context of current and future policy frameworks. A financial analysis is presented to inform what benefits are accessible for investors and consumers. 12

13 Hydrogen hub roadmap overview PHASE 1 PHASE 2 PHASE 3 HYDROGEN HUBS Deployment of stationary fuel cells in Targeted hydrogen hub projects with Development of wider hydrogen targeted markets (e.g. public sector, transport applications in a mother-daughter infrastructure to accommodate a mass hospitals, retail, multifamily residential) arrangement market HYDROGEN Steam reforming of natural gas on-site Large scale steam reforming of natural gas at Growth in water electrolysis using DELIVERY mother stations. Delivered to daughter renewable electricity stations by CH truck OUTCOMES Fuel cell cost reduction; Demonstration of hydrogen hub supply chain Hydrogen infrastructure achieves scale and Familiarity with technology in favourable settings; meaningful energy system contribution; Cost reduction throughout supply chain; Widespread deployment of FCEV Initial deployment of FCEV POSSIBLE POLICY FIT for stationary fuel cells above 2kW; Financial support (RTFO) for synthetic fuels; Binding hydrogen targets; INSTRUMENTS Mandates/standards on Project financing; Support for mass roll-out of infrastructure heating/efficiency; enhanced CHP Air quality mandates support; strategic recognition 13

14 Phase 1 Deployment of stationary fuel cells Targeted deployment of stationary combined heat and power (CHP) fuel cells in mid-sized commercial applications such as hospitals, universities, retail and multiresidential buildings. Hydrogen is produced onsite by steam reforming of natural gas. These applications require relatively minimal infrastructure commitment: the existing gas grid can provide natural gas for the onsite steam reformer, and the heat generated by the fuel cell can be delivered via the existing central heating system. They are therefore likely to be easier to implement in the nearterm, as investment costs are lower and fewer supply chain actors are required. By targeting the suggested mid-sized commercial markets securing demand in this pathway is lower risk; there is no reliance on external developments such as hydrogen vehicle deployment to generate sources of demand. Instead consistently high energy demand can provide the high load factors which may be necessary to recoup the capital costs. Financial benefits are available immediately with lower bills arising from higher efficiencies as well as potential eligibility for Feed in Tariff payments. For Johnson Matthey demonstration will create familiarity with hydrogen technologies, encouraging other consumers to use hydrogen who were unwilling to be firstmovers. As more demand is created, manufacturing can be scaled to facilitate learning and economies of scale. There are opportunities to bring laboratory innovation from Johnson Matthey s Test Facility to the market. These actions will lower costs and improve performance of fuel cells and steam reformers. Due to the use of natural gas in the production process, the hydrogen in this pathway is not renewable. However, the improvements in efficiency and lack of combustion will lower carbon and local pollutant emissions, meaning there is a strong case for government backing. Critically, this is a low cost pathway to deploy the infrastructure which can utilise renewable hydrogen when it becomes more economically viable in the future. 14

15 Levelised Cost ( /MWh) Financial analysis Financial analysis suggests that for an illustrative hospital (modelled on the Royal Free in Hampstead using data for the Doosan Model 400 fuel cell), the installation of a number of FCs meeting the building s power demand can lower the hospital s levelised cost of energy ( /MWh) by 20% whilst also lowering annual carbon emissions by another 35% (compared to an oil boiler counterfactual). With energy bill savings the net present value of this investment is over 3 million, with a rate of return of 6% and a payback period of just over 7 years (for more details see the appendix). 80 Figure 1: Levelised Cost of Energy ( /MWh) Fuel Cells + Auxillary Gas Boiler Grid Electricity + Gas Boiler Grid Electricity + Oil Boiler Ecuity Economics 15

16 Annual CO 2 e savings (tco2 e ) The UK has over 1,000 hospital sites. Figure 2 below considers the carbon emission savings that could be accrued nationally if only 30 average-sized hospitals installed fuel cells every year. The exact level of savings depends on the proportion of oil or gas counterfactual fuel heating systems being displaced yet by 2022 cumulatively the UK could have saved between 7-10 Mt CO e 2. To put this into the context of national climate change and emission targets, from the UK needs to cut national emissions by 238 MtCO 2 e to meet its 3 rd carbon budget. 1 Figure 2: CO 2e savings from installation of FCs in 30 new hospitals per year 3,000,000 2,500,000 2,000,000 1,500,000 1,000, , Ecuity Economics 1 Committee on Climate Change (2014) Carbon Budgets and targets. Available from: 16

17 Phase 2 Targeted hydrogen hub projects Development of hydrogen hubs which produce and supply hydrogen to the nascent fuel cell electric vehicle (FCEV) market in the UK. Economic analysis and field evidence will demonstrate that in the early stages of adoption the hub is best clustered around specific sources of secure demand, with a large station producing the hydrogen and supplying smaller refuelling stations. This model of distribution has been termed the mother and daughter model and has been demonstrated by Tokyo Gas in Japan. 1 To reduce costs, phase 2 considers hydrogen produced by steam reforming of natural gas. The transport sector has the potential to be the most important market for hydrogen fuel cells, with major opportunities for massmarket deployment and no alternative technology which can provide zero-carbon tailpipe pollutants, with quick refuelling times and long distance operation. Yet FCEVs are unviable without refuelling infrastructure, whilst the refuelling network is unviable without FCEVs. Thus the primary objective of the second phase of the roadmap is to start developing infrastructure in targeted areas of secure demand, with the aim of supporting the initial deployment of hydrogen vehicles, which will in turn increase the demand for further refuelling stations. A contracted vehicle fleet with back-to-base operating regimes (e.g. busses, taxis, or material handling vehicles) could be considered a reliable and appropriate end-user for this stage of demonstration. Surveys have shown that access to more than one hydrogen refuelling station significantly increases consumer receptiveness to FCEVs 2. Phase 2 allows the development of multiple refuelling stations relatively cheaply, as the expensive generation is not required at each site. Instead a single generator station can operate at a higher load factor improving its financial credentials. Once this set-up has facilitated sufficient demand, further generation facilities can be built and the hydrogen refuelling network expanded. Research focusing on Southern California 3 suggests that a small number of strategically placed stations reduces infrastructure costs while delivering good convenience and reliability. 2 UK H2 Mobility, Phase 1 results. 3 Ogden and Nicholas, Analysis of a cluster strategy for introducing hydrogen vehicles in Southern California Energy Policy 39(4):

18 Initial demand for the fuel should be secured in advance. A fleet of vehicles with regular, back-to-base routes may be most appropriate when there are few refuelling stations; buses, taxis and material handling vehicles present a suitable opportunity to offer this early demand. Indeed the French Mobilité Hydrogène programme offers a good example of a targeted roll-out of clustered refuelling stations centring on captive fleets, which offer predictable demand to the station operators 4. As this phase incorporates much more of the hydrogen supply chain, there is greater potential for scaling and learning, to reduce overall costs. Beyond the tangible increases in production volumes and improved manufacturing techniques, supply chain actors can strengthen relationships and coordinate their business activity. There is an opportunity for Johnson Matthey and its supply chain partners to create a separate business entity which can manage delivery of hydrogen hub projects. Financial analysis Mother & Daughter versus distributed model M M M M M D D M D D Figure 5 Hydrogen station configurations: Distributed vs Mother & Daughter Ecuity s economic modelling compared the cost of hydrogen produced and supplied through a distributed refuelling network of 5 stations with onsite reformers, to a clustered mother and daughter model which utilises one station s large reforming capabilities to supply 4 refuelling stations with hydrogen. Both scenarios envisage a total of 2,000 kg of 4 Mobilité Hydrogène France (2015) Proposition d un plan de déploiement national des véhicules hydrogène Available from: 18

19 Cost of Hydrogen ( /kg) hydrogen being supplied daily (400 kg from each station). When distribution is involved, this is done through the operation of compressed gas tube trailers which Ecuity s modelling has demonstrated to be the lowest cost option for delivery from mother to daughter stations (see Appendix for details of analysis). Figure 6 illustrates the cost savings graphically. The distributed model which consists of 5 separate stations producing (through steam methane reforming) and dispensing condensed hydrogen, delivers the gas at a cost-price of 5.51/kg. The introduction of a clustered mother and daughter model whereby one large station reforms natural gas (at a rate of 2,000 kg/day) and supplies 4 refuelling station reduces the cost-price of hydrogen at the pump by 31 p./kg. Given that over the assumed 15 year lifetime (for other modelling assumptions see the appendix) both scenarios have been calibrated to produce and supply over 8.4 million kg of hydrogen, the cost saving is thus sizeable and in the region of 2.5 million. 5.6 Figure 6: Distributed Model vs. Mother & Daughter % reduction Distributed Model Mother & Daughter Ecuity Economics Scalability economies of scale Table 1 Cost of Hydrogen ( /kg) Distributed Model Mother & Daughter Capital & Installation Costs NPV of Operating Costs Total

20 Cost of Hydrogen ( /kg) Hydrogen hub projects need to demonstrate cost-down properties over time as scale is increased. Figure 7 gives a demonstration of this (utilising data sources that are available in the appendix), with the volume of hydrogen As the size of the mother station is increased, despite further expenditure needed to meet the need for additional infrastructure and daughter stations, the overall cost-price of hydrogen falls. produced and supplied by hubs increasing over time as demand follows the development of infrastructure. 14 Figure 7: Impact of scale on cost of hydrogen NPV of operating costs Capex & installation costs Total hydrogen cost Hydrogen Hub Size (kg/day) D D M D D D M D D D M D D Ecuity Economics 20

21 Phase 3 Wider hydrogen infrastructure Phase 3 continues to focus on the transport industry, but envisages a movement from hydrogen produced from steam methane reformation, to water electrolysis (WE). Phase 3 considers the mother and daughter model with onsite electrolysers producing hydrogen centrally, before being distributed to daughter stations via compressed gas trucks. Following the proliferation of renewable electricity generation the production of hydrogen could be seen as an efficient mechanism to help balance the grid. Following phase 2, hydrogen has reached high levels of familiarity and consumer receptiveness. This is facilitated and enhanced by the expanding infrastructure; the refuelling network is sufficient for members of the public to uptake hydrogen FCEVs in significant volumes, massively increasing the fuel cell market. The transition to WE is an essential part of the developing hydrogen economy. Firstly, as the hydrogen generated in phase 3 is renewable, the contribution towards meeting the UK s carbon targets increases substantially. Access to more generous subsidy schemes is likely, while, the fuel cell technologies will be shielded from green levies such as carbon prices or pollution taxes. Secondly, hydrogen begins to make a meaningful energy system contribution in this stage. As the penetration of intermittent renewables in the power sector increases, hydrogen offers a mechanism to store this energy. When wind generating capacity exceeds electrical demand, the excess electricity can be used to generate hydrogen at zero marginal cost. When there is a deficit of generation on the grid, the stored energy can efficiently generate electricity in stationary fuel cells. In an analysis undertaken by H 2 Mobility, the services offered by WE in balancing and stabilising the grid could lead to a 20% reduction in the cost of hydrogen production 2. 21

22 Financial analysis Under commercial electricity prices, WE is a more expensive method of producing hydrogen than SMR. Ecuity s modelling suggests that given the same mother and daughter model replicated in phase 2, the utilisation of WE increases the cost of hydrogen by 3.31/kg (a 64% increase), from 5.21 to 8.52/kg. As illustrated in figures 6 and 7 the cost of hydrogen is increasingly determined by the electricity price as it is produced by the more energy intensive process of electrolysis. Thus the economic viability of the hydrogen hub becomes increasingly linked to the cost paid for the electricity consumed in the production process. Figure 6: SMR Sensitivity Analysis (CH2 Truck) Electricity price NPV of opex Capex +20% -20% Distance (km) Cost of Hydrogen ( /kg H2) Ecuity Economics Figure 7: Water Electrolysis Sensitivity Analysis (CH2 Truck) Electricity price NPV of opex Capex +20% -20% Distance (km) Cost of Hydrogen ( /kg H2) Ecuity Economics 22

allocated by DECC for wind energy, which is indicative of an industry price for electricity generated by turbines in the UK.")

23 The analysis in this paper utilises the Contract for Difference strike price (9.5p./kWh) allocated by DECC for wind energy, which is indicative of an industry price for electricity generated by turbines in the UK. However there exists the potential for hydrogen hubs to benefit from a lower electricity price, because of the opportunity for hydrogen production to assist in the difficult task of balancing an ageing and geographically disparate grid network. When power supply exceeds demand, as part of the settlement process the National Grid will bid to generators to stop supplying electricity in exchange for a balancing payment. At these times wind energy can be thought of as having a negative resource cost for the National Grid. To be more specific the largest wind farms in the UK which own Transmission Licences and operate in the balancing mechanism, receive constraint payments when they cannot use the access to the network that they have paid for. This often happens because of difficulty distributing the electricity generated in one area of the country (e.g. Scotland) to another (e.g. South East of England). It thus follows that there is an opportunity for this excess electricity to be utilised more efficiently if powering water electrolysers and the production of green hydrogen. Indeed there is an opportunity for policy to mandate that the national grid should be paying the owners of the electrolysers, who in turn could purchase the excess electricity from the generators. Thereby supporting low-cost renewable hydrogen and FCEVs, whilst also effectively managing the balancing of the grid. Figure 8 considers how a reduced price of power could significantly reduce the cost of producing and distributing hydrogen to endusers under the phase 3 mother and daughter assumptions. Every 10 reduction in the price of electricity ( /MWh) results in a 70p reduction in the cost of hydrogen ( /kg), and given a 40/MWh price of electricity the costprice of renewable green hydrogen reaches parity with SMR-produced gas. 23

24 Cost of Hydrogen ( /kg) Price of electricity ( /MWh) Figure 8: Impact of electricity price on cost of hydrogen under WE CfD strike price Av capacity payment price Wholesale price of electricity Free Cost of hydrogen ( /kg) Price of electricity Ecuity Economics The above analysis has focused on wind energy because of the significant capacity installed in the UK and the opportunity for hydrogen production to assist with the balancing mechanism in regard to wind farms. It should however be noted that hydrogen hubs and refuelling stations can operate from other forms of renewable energy. Honda s 200kg/day refuelling station in Swindon is a good example of a hub generating green hydrogen and powered by a 15MW solar power plant. Note that perhaps a constraint of using solar rather than wind energy as the renewable energy source is the potential for scaling to bigger sized stations and more applications. Using Ecuity s modelling an averaged sized (400 kg/day) station with onsite electrolyser would require 5,000 m 2 of installed capacity of solar panels, given an average UK PV production rate of 2.3kWh/m 2 /day. With an estimated solar irradiance to hydrogen process efficiency of 8%, a 400kg/day station would need a solar plant in excess of 15MW. 5 5 Hankin, A. (2015) Hydrogen Production using Solar Energy. Online webinar 24

25 UK Energy Policy: Energy Trilemma The concept of an energy trilemma shapes much of the rhetoric used by politicians when discussing energy issues, and has thus been influential on policy objectives and details. The argument and vision for the development of hubs and more broadly the hydrogen economy can be framed in this context. 1. Energy cost As demonstrated by the analysis in phase 1 of the roadmap, stationary fuel cells in certain applications deliver energy at a lower total resource cost than traditional sources. For the hospital modelled in this paper, the site stands to save around 3 million a year in energy bill savings, which given a 10 year fuel cell system lifetime amounts to just under 30 million savings in current prices ( 25 million in present value terms). This is in excess of the initial 20 million capital cost and demonstrates the cost effectiveness of stationary fuel cells. Toyota estimate that it will cost around $50 ( 34) to fill a Mirai with hydrogen. Ecuity s analysis of water electrolysis produced hydrogen suggests a price closer to 50 per 5 kg of hydrogen needed to fill the tank. Given a 300 mile range, this pricing though speculative is competitive with petrol and diesel-ran vehicles. The problem is that FCEVs are currently expensive to buy, yet there are a number of niche applications today where they can be considered the most costeffective solution, as demonstrated in section 5 of the appendix which profiles indoor material handling vehicles. Looking to the future, it is expected that increased volumes will lower both fuel and vehicle costs. In addition the Renewable Energy Foundation 6 calculate that during 2014 the National Grid paid generators to stop 658 GWh worth of wind electricity being supplied, at a total cost of 53 million. Thus it follows that to the extent that the production of hydrogen could mitigate some of the need for those capacity payments by utilising excess electricity, that the operation of green hydrogen hubs is even more cost effective from a national perspective. 6 Renewable Energy Foundation (2015) Balancing Mechanism Wind Farm Constraint Payments. Available from: 25

26 2. Energy security Under the hospital modelling scenario used in this paper, the operation of 11 Doosan fuel cells would in net terms save 6,800 MWh of gas consumption annually compared to a gas boiler and grid electricity counterfactual. As with the analysis above, assuming that this installation is by 30 new sites per year, by 2018 the operation of fuel cells in 120 average-sized hospitals would cut gas consumption aggregately by 817 GWh a year. 3. CO2 and environmental performance Hydrogen is inherently a zero carbon energy carrier; combustion or conversion to electrical energy in a fuel cell produces no carbon emissions. However, there can be carbon emissions associated with the generation of hydrogen. Steam reforming, whereby hydrocarbons are reacted with high temperature steam, is currently the dominant form of hydrogen production, and is associated with carbon emissions as a consequence of utilising fossil fuels. Steam reforming also offers a method by which the chemical energy in natural gas can be harnessed without releasing harmful local pollutants which are associated with its combustion in air. The lower temperature employed leads to emissions from fuel cells being about one tenth of those from gascombusting technologies per kwh of fuel input 7. Meanwhile, water electrolysis, the production method proposed in phase three provides potential for near zero-carbon hydrogen generation. This process, in which an electric current splits water into hydrogen and oxygen, will only be as carbon intensive as the electricity. Therefore, the proposed wind driven system means lifecycle pollution emissions of hydrogen production will be incredibly low as wind produces no pollution during operation. Transport emissions account for approximately 25% of all CO 2 released in the UK 8. Since 1990, emissions have fallen just 2.4%, lower than any other sector accounted for. With operating regimes similar to current petrol and diesel vehicles hydrogen presents the UK with a substantial opportunity to reduce carbon emissions in this sector. HFCEVs can be expected to achieve 75% lower emissions than their diesel counterparts by 2030 in accordance with UK H 2 Mobility s roadmap 2. This is based on an assumption that HFCEVs would require 254,000 tonnes of hydrogen per year, and this demand would be met through an approximately 50:50 mix of water electrolysis and steam methane reforming. This UK H 2 Mobility analysis uses only production methods which are currently commercially available, and thus there is the 7 H2FC Supergen, The Role of Hydrogen and Fuel Cells in Providing Affordable, Secure Low- Carbon Heat. 8 DECC, UK Greenhouse Gas Emissions, Provisional Figures and 2012 UK Greenhouse Gas Emissions, Final Figures by Fuel Type and End-User 26

27 potential for emissions to fall further with technological developments. Figure 13 Carbon savings associated with roll out of HFCEVs towards 2050 (UK H 2 Mobility, 2013) The vehicles also provide the benefit of reducing local pollutants. Measured annual mean values of nitrogen dioxide, 46% of which is associated with traffic 9, exceeded annual target values in 38 of 43 geographical zones of the UK in The consequences of vehicular associated air pollution can be severe. Public Health England 11 estimates 29,000 premature deaths are related to longterm exposure to poor air quality; in some urban areas, this amounts to 8% of all mortality. Recent national headlines brought the issue to public attention as the Environmental Audit Committee described air pollution as a public health crisis 9. 9 Environmental Audit Committee, Action on Air Quality 10 Defra, Updated Projections for Nitrogen Dioxide (NO2) Compliance. 11 Public Health England, Estimates of mortality in local authority areas associated with air pollution 27

28 Appendix 1. Data Assumptions Economic Assumptions Discount rate 3.5% GHG emission factors Gas (kgco2/mwh) Electricity Source: DEFRA (2014) Oil Energy prices (p/kwh) Gas* 3.15 *Source: DECC (2014) Electricity (stationary)* Electricity (H2 hub=cfd strike price) 9.50 Oil (estimated on $65/bbl) 3.80 Stationary Application Data Stationary Fuel Cell based on Doosan Model 400 System size (kwe) 400 Lifetime (years) 10 Capital cost ( /unit) 1,890,000 Fixed operating cost ( /unit/year) 75,600 Doosan FC emission factor (kgco2/mwh) 476 Heat output (kwh/hour) Gas consumption (kwh/hour) 1,172 Hospital counterfactual heating system (source: DECC, 2013) System size (MW) 4.6 Efficiency (%) 90% Load factor (%) 89% Capital cost ( /kw) 103 Fixed operating costs ( /kw/year)

29 Hydrogen Hub Data Source: Nicholas and Ogden (2010) Capital cost for 400 kg/day onsite reformer station ( millions) 3.40 Capital cost for 1000 kg/day onsite reformer station ( millions) 5.48 Natural gas feed (kwh/kg H2) SMR station H2 compression rate (kwh/kg H2) 3.08 SMR station fixed operating cost ( /year) 237,916 Capital cost for 400 kg/day onsite electrolyser station ( millions) 3.71 Capital cost for 1000 kg/day onsite electrolyser station ( millions) 6.54 Electrolysis station fixed operating cost ( /year) 259,680 Capital cost for LH2 refuelling station ( million) 1.99 LH2 station compression rate (kwh/kg H2) 0.33 LH2 station fixed operating cost ( /year) 218,414 CH2 station fixed operating cost ( /year) 115,066 Pipeline station fixed operating cost ( /year) 156,886 Source: NREL (2014) Installation factor 1.3 CH2 truck station compressor efficiency 80% CH2 truck station compressor cost 240,706 CH2 truck station system electricity usage (kwh/kg H2) 1.53 CH2 truck station storage cost 97,482 CH2 truck station dispenser cost (x2) 141,724 CH2 truck station cooling cost 152,972 CH2 truck station electrical cost 30,744 CH2 pipeline station compression cost 781,356 CH2 pipeline station compressor efficiency 65% CH2 pipeline station system electricity usage (kwh/kg H2) 1.89 CH2 pipeline station low pressure storage costs 187,466 CH2 pipeline station cascade costs 145,473 CH2 pipeline station dispenser costs (x2) 141,724 CH2 pipeline station cooling costs 170,219 Liquefier capital cost 4,574,231 Liquefier capacity (kg/day) 1091 Liquefier electricity needed (kwh/kg H2)

30 CH2 pipeline capital costs ( /km) 175,021 CH2 pipeline land costs ( /km) 87,593 Source: Hydrogenics (2014) HySTAT 60 electrolyser Possible nominal hydrogen flow/unit (Nm3/hour) 60 Water consumption (l/nm3 H2) 2 Electricity consumption (kwh/nm3) 4.9 Source: Hexagon Composites (2014) CH2 tube trailer cost 382,430 CH2 tube trailer size (kg) 616 CH2 tube trailer pressure (bar) Levelised Cost Methodology Where: I = Initial capital cost C t = Operating cost (in year t) r = Interest rate E t = Energy generated/used (in year t) C t I + t=1 ( (1 + r) LCoE = t ) T E ( t t=1 (1 + r) t ) T 30

31 Levelised Cost ( /MWh) 3. Case Study 1 Fuel Cell Installation in Hospitals A cheaper source of energy A valuable feature of fuel cells is their ability to operate efficiently at high load factors and match the load profile of the buildings they re installed in. They thus represent an effective solution to the energy generation demands of hospitals. The following analysis will consider the financial and environmental implications of the installation of multiple fuel cells providing baseload generation for an illustrative hospital (modelled on the Royal Free Hospital in Hampstead). Financial modelling based on current market data suggests that the operation of 11, 400 kw e fuel cells (modelled on the Doosan Model 400) with an auxiliary gas boiler providing the illustrative hospital with power and heat, is a lower cost option over the lifetime of the investment than the use of grid electricity in conjunction with either a gas or oil boiler providing heat. Figure A1 below illustrates this graphically, and shows the respective levelised cost of energy of each scenario, with the installation of fuel cells reducing the cost of energy for the hospital by ~ 11.50/MWh compared to the gas boiler counterfactual and by ~ 15.50/MWh compared to the oil boiler counterfactual, over the technologies lifetime (assumed to be 15 years). 80 Figure A1: Levelised Cost of Energy ( /MWh) Fuel Cells + Auxillary Gas Boiler Grid Electricity + Gas Boiler Grid Electricity + Oil Boiler Ecuity Economics 31

32 Over an assumed 10 year lifetime of the investment, figure A2 below illustrates the positive return on investment available for the illustrative hospital. In this scenario where the fuel cell is providing baseload power for the site in addition to heat which replaces oilfuelled generation, the NPV is in excess of 3 million with a 6% rate of return. The hospital stands to break even (as illustrated graphically) just after 7 years following the initial investment. Figure A2: 11 Doosan 400 PureCell Fuel Cells 10,000,000 5,000, ,000, ,000,000-15,000,000-20,000,000-25,000,000 Period (years) Expenditure Energy Bill Savings Cumulative cashflow Ecuity Economics Lower emissions Another benefit of operating a large-scale stationary fuel cell is the reduction of carbon emissions. For a private company, public institution or hospital a precedent exists to control and where possible lower carbon emissions. Thus switching from traditional sources of energy and generation to the operation of a fuel cell which provides both power and heat, offers the opportunity to lower emissions and potentially save money. Figure A3 below considers the annual carbon emissions of the hospital under three scenarios. The first involves the building s electricity demand being met by the grid, and heat demand being serviced by condensing gas boilers. The second setup considers oil boilers providing heat. The final scenario considers the multiple fuel cell and auxiliary gas boiler scenario. The installation and operation of stationary fuel cells reduces annual carbon emissions by 26% compared to the gas boiler counterfactual and by 35% compared to the oil boiler counterfactual. 32

33 Annual Carbon Emissions (tco 2 ) Figure A3: Annual Carbon Emissions Fuel Cells + Auxillary Gas Boiler Grid Electricity + Gas Boiler Grid Electricity + Oil Boiler Ecuity Economics Figure A4 illustrates these emission savings graphically. Consider also that hospitals in the UK are regulated under the EU Emission Trading Scheme (ETS) and despite being exempt from having to trade and hold credits, they are obliged to meet certain specific emission targets. If the party exceeds their limit they incur a pecuniary penalty. There is often a cost to bear when abating emissions, which as described the hospital may be obliged to do so. DECC valued the marginal cost of reducing 1 tco2 in the nontraded sector of the EU ETS to be 66 (2015 prices) 12. Under classical economic theory assuming that the MAC is equal to the value of marginal social damage then this 66/tCO2 could be considered to be equivalent to the efficient level of carbon tax/permit price. Thus figure A4 also uses the MAC to provide a monetary value to the hospital s annual carbon emission abatement which depending on fuel source counterfactual is between 400,000 and 620,000 a year. 12 DECC (2012) EU ETS Small Emitter and Hospital Phase III Opt- Out: Impact Assessment. Available from: 33

34 Levelised Cost ( /MWh) Annual Emission Savings (tco 2 /year) Monetised Annual Carbon Savings ( /year) Figure A4: Fuel Cell Annual Emission Savings - Compared To Counterfactual 720, , , , , , ,000 90,000 0 Grid Electricity + Gas Boiler Grid Electricity + Oil Boiler Counterfactual Technology Ecuity Economics 0 Monetising the carbon emission savings also has an impact on the financial attractiveness of the stationary fuel cell proposition, and as shown in figure A5, reduces the levelised cost for the hospital by an additional 6 for every MWh of energy consumed over the 15 years modelled. 80 Figure A5: Levelised Cost of Energy ( /MWh) Fuel Cells (with monestised Fuel Cells (without monestised emission savings) + Gas Boiler emission savings) + Gas Boiler Grid Electricity + Gas Boiler Grid Electricity + Oil Boiler Ecuity Economics 34

35 4. Delivery of Hydrogen Hydrogen has a low volumetric energy density at normal temperatures and pressures, and therefore is best transported in a compressed or liquefied state. This gives three principal options for hydrogen delivery from production (steam reformer or water electrolysis in our scenarios) to the refuelling station: i. Compressed hydrogen transported by tube trailers ii. Liquefied hydrogen transported by tube trailers iii. Compressed hydrogen passed through gas pipelines This analysis considers the use of pipelines to transport hydrogen as involving the construction and operation of specialist infrastructure. A separate analysis would be needed to assess the viability of blending hydrogen with natural gas in the UK s existing pipelines. This process would involve hydrogen separation from natural gas, which requires a significant investment in capital and the extraction process can increase costs by 1-7/kg H 1 2 (depending on production and delivery method this can be anywhere from 10%-100% of total cost). It thus remains a prohibitively expensive delivery method under current low volumes, but could be considered a potential option in the future given increased scale of demand and supply. 35

36 Cost of Hydrogen ( /kg) Least Cost Option Given the SMR mother and daughter model proposed in phase 2 of the hydrogen hub roadmap, figure A1 compares the forecourt cost-price of hydrogen given the three different delivery methods, from mother to 4 smaller daughter stations. This analysis assumes no existing infrastructure, and compares the cost of installation and operation of the three scenarios. Note that compressed hydrogen can be transported in the natural gas pipeline infrastructure, but requires separation technologies which command a high upfront capital cost. This could become an economic form of delivery in the future given greater volumes. 9 Figure A6: Comparison of Hydrogen Hub Delivery Methods CH2 Truck LH2 Truck CH2 Pipeline Capital & Installation Costs NPV of Operating Costs Ecuity Economics Table A1 Cost of Hydrogen CH2 Truck LH2 Truck CH2 Pipeline Capital & Installation Costs NPV of Operating Costs Total Especially for initial low volumes of hydrogen production and delivery, compressed hydrogen trucks will remain the lowest cost method at 5.20/kg. As illustrated in the sensitivity analysis below (figures A7, A8 and A9) compressed gas trucks are in large part the cheapest current delivery option because of the modest capital costs involved in relation to liquefied trucks (liquefiers require high upfront costs and operating costs) and compressed gas pipelines. 36

37 Figure A7: Sensitivity Analysis - CH2 Truck Electricity price NPV of opex Capex +20% -20% Distance (km) Cost of Hydrogen ( /kg H2) Ecuity Economics Figure A8: Sensitivity Analysis - LH2 Truck Electricity price NPV of opex Capex +20% -20% Distance (km) Cost of Hydrogen ( /kg H2) Ecuity Economics Figure A9: Sensitivity Analysis - CH2 Pipeline Electricity price NPV of opex Capex +20% -20% Distance (km) Cost of Hydrogen ( /kg H2) Ecuity Economics 37

38 Minutes per vehicle per day 5. Case Study 2 Fuel Cell Material Handling Vehicles (MHVs) Material handling vehicles (MHVs) are currently powered by either electric motors or internal combustion engines. For many indoor applications electric MHVs are preferred because of the potential for lower running costs and zero exhaust emissions. Though currently more expensive in relation to the upfront cost of capital, fuel cell MHVs can be considered a more attractive alternative to electric MHVs for a number of reasons. Firstly unlike batteries fuel cells operate consistently and deliver the required power level at temperature extremes and in particular cold conditions (such as in refrigeration units perhaps) 13. In addition figure A10 illustrates graphically the reduced refuelling times that a fuel cell powered MHV (6 minutes per day) enjoys over an electric alternative (closer to 50 minutes per day). Consider also that batteries require up to 8 hours cooling time in between change overs, and the potential for improved productivity per vehicle (and battery) when operating fuel cell MHVs is clear. Figure A10: Time for refuelling/changing batteries FC MHV Electric MHV Source: NREL (2013) 13 Mansouri, I. & Calay, R, K. (2012) Materials handling vehicles; policy framework for an emerging fuel cell market. World Hydorgen Energy Conference

39 This improved productivity has a financial bearing on the operation costs associated with running a fuel cell MHV. Figure A11 utilises data from a US Department of Energy study on the comparative costs of MHVs to demonstrate the cost savings that can be obtained when investing in the fuel cell option rather than an electric alternative over the lifetime of the investment 14. Figure A11: NPV of MHVs (US$) $160,000 $140,000 $120,000 $100,000 $80,000 $60,000 $40,000 $20,000 $0 FC MHV NPV of capital costs NPV of operating costs Electric MHV Source: NREL (2013) 14 NREL (2013) U.S. Department of Energy-Funded Performance Validation of Fuel Cell Material Handling Equipment. Available from: 39

40 Turning energy policy insights into commercial results This report has been produced by Ecuity Consulting LLP on behalf of Johnson Matthey Fuel Cells to develop a hydrogen economy vision in the UK and promote the company s role as a driver for positive change to making this reality. Ecuity s mission is to make sustainable energy mainstream by using our unique strategic insight to connect the commercial day to day reality of running a business and the political challenges of sustainable energy policy making. Ecuity Consulting LLP ǀ Radcliffe House ǀ Blenheim Court ǀ Solihull ǀ B91 2AA T: +44 (0) ǀ E info@ecuity.com ǀ 40

The pathway towards fossil parity for renewable hydrogen

The pathway towards fossil parity for renewable hydrogen Bjørn Simonsen VICE PRESIDENT MARKET DEVELOPMENT AND PUBLIC RELATIONS 90 years..of hydrogen technology experience and excellence Hydrogen Fueling

The pathway towards fossil parity for renewable hydrogen Bjørn Simonsen VICE PRESIDENT MARKET DEVELOPMENT AND PUBLIC RELATIONS 90 years..of hydrogen technology experience and excellence Hydrogen Fueling

Hydrogen as fuel: Zero emission mobility, available today. Linde, Hydrogen mobility solutions Munich, June 2018

Hydrogen as fuel: Zero emission mobility, available today Linde, Hydrogen mobility solutions Munich, June 2018 Topics. 01 H2 molecule a game changer in the mobility market 02 H2 value chain & technologies

Hydrogen as fuel: Zero emission mobility, available today Linde, Hydrogen mobility solutions Munich, June 2018 Topics. 01 H2 molecule a game changer in the mobility market 02 H2 value chain & technologies

Fuel Cell Initiatives in Europe

Outreach Event of the IEA Advanced Fuel Cell Implementing Agreement April 23rd, 2015, Zurich, Switzerland Fuel Cell Initiatives in Europe Laurent ANTONI CEA - France laurent.antoni@cea.fr H 2 & FUEL CELLS:

Outreach Event of the IEA Advanced Fuel Cell Implementing Agreement April 23rd, 2015, Zurich, Switzerland Fuel Cell Initiatives in Europe Laurent ANTONI CEA - France laurent.antoni@cea.fr H 2 & FUEL CELLS:

Nel Group. Jon André Løkke Chief Executive Officer

Nel Group Jon André Løkke Chief Executive Officer Three business segments Nel ASA Global pure-play hydrogen company facilities in Norway, Denmark and the U.S. Significant foothold in fast-growing markets

Nel Group Jon André Løkke Chief Executive Officer Three business segments Nel ASA Global pure-play hydrogen company facilities in Norway, Denmark and the U.S. Significant foothold in fast-growing markets

Sectoral integration long term perspective in the EU energy system

Sectoral integration long term perspective in the EU energy system By Prof. Pantelis Capros, March 1 st 2018 Consortium E3-Modelling, Ecofys and Tractebel- ENGIE 1 Structure of the study Hydrogen roadmap

Sectoral integration long term perspective in the EU energy system By Prof. Pantelis Capros, March 1 st 2018 Consortium E3-Modelling, Ecofys and Tractebel- ENGIE 1 Structure of the study Hydrogen roadmap

Impact Assessment (IA)

") Title: Comprehensive Review Phase 2B - Consultation on Feed-in Tariffs for anaerobic digestion, wind, hydro and micro-chp installations IA No: DECC0077 Lead department or agency: DECC Other departments

Title: Comprehensive Review Phase 2B - Consultation on Feed-in Tariffs for anaerobic digestion, wind, hydro and micro-chp installations IA No: DECC0077 Lead department or agency: DECC Other departments

This response considers the issues at an overall level, concentrating on the nonnetwork businesses within ScottishPower.

SUBMISSION FROM SCOTTISHPOWER You have already received evidence from our networks business on the matters within their areas of responsibility as a transmission owner and distribution network operator

SUBMISSION FROM SCOTTISHPOWER You have already received evidence from our networks business on the matters within their areas of responsibility as a transmission owner and distribution network operator

Hydrogen storage & distribution

Hydrogen storage & distribution in a Power to H2 context April 2014 l Air Liquide Nordic Countries Air Liquide - Our activities World leader in gases for industry, health and the environment Production

Hydrogen storage & distribution in a Power to H2 context April 2014 l Air Liquide Nordic Countries Air Liquide - Our activities World leader in gases for industry, health and the environment Production

A Joint Hydrogen Strategy Framework for the North Sea Region

HyTrEc Hydrogen Transport Economy for the North Sea Region A Joint Hydrogen Strategy Framework for the North Sea Region Recommendations by the HyTrEc project partnership to support the deployment of hydrogen-fuelled

HyTrEc Hydrogen Transport Economy for the North Sea Region A Joint Hydrogen Strategy Framework for the North Sea Region Recommendations by the HyTrEc project partnership to support the deployment of hydrogen-fuelled

Response to Department for Transport Call for Evidence on Advanced Fuels. Summary

Response to Department for Transport Call for Evidence on Advanced Fuels Summary 1. The Energy Technologies Institute (ETI), a public-private partnership between global energy and engineering firms and

Response to Department for Transport Call for Evidence on Advanced Fuels Summary 1. The Energy Technologies Institute (ETI), a public-private partnership between global energy and engineering firms and

NewBusFuel: Recommendations for Large Scale Hydrogen Refuelling

SSB 2013 Hydrogenics 2014 Siemens 2013 McPhy, 2011 Linde 2012 Linde 2012 ITM Power 2014 Air Products 2014 Transport for London 2013 Aberdeen Hydrogen Transport Summit NewBusFuel: Recommendations for Large

SSB 2013 Hydrogenics 2014 Siemens 2013 McPhy, 2011 Linde 2012 Linde 2012 ITM Power 2014 Air Products 2014 Transport for London 2013 Aberdeen Hydrogen Transport Summit NewBusFuel: Recommendations for Large

New Bus ReFuelling for European Hydrogen Bus Depots

SSB 2013 Hydrogenics 2014 Siemens 2013 McPhy, 2011 Linde 2012 ITM Power 2014 Air Products 2014 New Bus ReFuelling for European Hydrogen Bus Depots Summary of NewBusFuel Linde 2012 Transport for London

SSB 2013 Hydrogenics 2014 Siemens 2013 McPhy, 2011 Linde 2012 ITM Power 2014 Air Products 2014 New Bus ReFuelling for European Hydrogen Bus Depots Summary of NewBusFuel Linde 2012 Transport for London

Long-Term Energy Storage: Hydrogen Opportunity. Stanford Natural Gas Initiative

Long-Term Energy Storage: Hydrogen Opportunity Stanford Natural Gas Initiative October 17, 2018 Background Rationale Growing mismatch of timing of supply and demand due to increasing penetration of renewables

Long-Term Energy Storage: Hydrogen Opportunity Stanford Natural Gas Initiative October 17, 2018 Background Rationale Growing mismatch of timing of supply and demand due to increasing penetration of renewables

Analysis of Alternative UK Heat Decarbonisation Pathways. For the Committee on Climate Change

Analysis of Alternative UK Heat Decarbonisation Pathways For the Committee on Climate Change June 2018 Project Team Imperial College: Goran Strbac, Danny Pudjianto, Robert Sansom, Predrag Djapic, Hossein

Analysis of Alternative UK Heat Decarbonisation Pathways For the Committee on Climate Change June 2018 Project Team Imperial College: Goran Strbac, Danny Pudjianto, Robert Sansom, Predrag Djapic, Hossein

Nel Hydrogen. DNB's 14th Annual Small & Medium Conference. Jon André Løkke CHIEF EXECUTIVE OFFICER

Nel Hydrogen DNB's 14th Annual Small & Medium Conference Jon André Løkke CHIEF EXECUTIVE OFFICER 90 years..of hydrogen technology experience and excellence Hydrogen Fueling Hydrogen Solutions 2 Nel ASA

Nel Hydrogen DNB's 14th Annual Small & Medium Conference Jon André Løkke CHIEF EXECUTIVE OFFICER 90 years..of hydrogen technology experience and excellence Hydrogen Fueling Hydrogen Solutions 2 Nel ASA

HYDROGEN ROADMAP EUROPE

HYDROGEN EUROPE A sustainable pathway for the European energy transition February 6, 2019 PAGE 1 WHY HYDROGEN: TO REALIZE THE AMBITIOUS TRANSITION OF THE EU'S ENERGY SYSTEM, A NUMBER OF CHALLENGES NEED

HYDROGEN EUROPE A sustainable pathway for the European energy transition February 6, 2019 PAGE 1 WHY HYDROGEN: TO REALIZE THE AMBITIOUS TRANSITION OF THE EU'S ENERGY SYSTEM, A NUMBER OF CHALLENGES NEED

Gas & Steam Turbines in the planned Environmental Goods Agreement

Gas & Steam Turbines in the planned Environmental Goods Agreement Gas & steam turbines are a technology for generating thermal power in the form of electricity and/or heat or mechanical energy. They are

Gas & Steam Turbines in the planned Environmental Goods Agreement Gas & steam turbines are a technology for generating thermal power in the form of electricity and/or heat or mechanical energy. They are

International motivations for hydrogen

International motivations for hydrogen Dr David Hart Metrolinx Hydrail Symposium 16 November 2017 Strategy Energy Sustainability Contents E4tech The international and local context Hydrogen in the energy

International motivations for hydrogen Dr David Hart Metrolinx Hydrail Symposium 16 November 2017 Strategy Energy Sustainability Contents E4tech The international and local context Hydrogen in the energy

Methodology for calculating subsidies to renewables

1 Introduction Each of the World Energy Outlook scenarios envisages growth in the use of renewable energy sources over the Outlook period. World Energy Outlook 2012 includes estimates of the subsidies

1 Introduction Each of the World Energy Outlook scenarios envisages growth in the use of renewable energy sources over the Outlook period. World Energy Outlook 2012 includes estimates of the subsidies

The impacts of nuclear energy and renewables on network costs. Ron Cameron OECD Nuclear Energy Agency

The impacts of nuclear energy and renewables on network costs Ron Cameron OECD Nuclear Energy Agency Energy Mix A country s energy mix depends on both resources and policies The need for energy depends

The impacts of nuclear energy and renewables on network costs Ron Cameron OECD Nuclear Energy Agency Energy Mix A country s energy mix depends on both resources and policies The need for energy depends

Energy Networks Australia. Consultation on how best to transition to a two-way grid

Energy Networks Australia Consultation on how best to transition to a two-way grid First of all, I speak as a non-expert in energy management over a large electrical grid. However there are some broad

Energy Networks Australia Consultation on how best to transition to a two-way grid First of all, I speak as a non-expert in energy management over a large electrical grid. However there are some broad

How achievable are the UK s 2020 renewable energy targets?

How achievable are the UK s 2020 renewable energy targets? Gareth Redmond Office for Renewable Energy Deployment What is the target? A legally binding, EU target to deliver 15% of the UK s energy needs

How achievable are the UK s 2020 renewable energy targets? Gareth Redmond Office for Renewable Energy Deployment What is the target? A legally binding, EU target to deliver 15% of the UK s energy needs

SUCCESSFUL IMPLEMENTATION OF POWER-TO-GAS IN EUROPE - A ROADMAP FOR FLANDERS

SUCCESSFUL IMPLEMENTATION OF POWER-TO-GAS IN EUROPE - A ROADMAP FOR FLANDERS European Utility Week 2015, 4 Nov 2015 Session 13: Main energy storage applications and how they are evolving By Denis Thomas,

SUCCESSFUL IMPLEMENTATION OF POWER-TO-GAS IN EUROPE - A ROADMAP FOR FLANDERS European Utility Week 2015, 4 Nov 2015 Session 13: Main energy storage applications and how they are evolving By Denis Thomas,

Renewable Energy and the CCC Renewables Review

Renewable Energy and the CCC Renewables Review Presentation to the EPRG Spring Conference Cambridge, 12 May 2011 Professor Michael Grubb Faculty of Economics, Cambridge University Context: a rich body

Renewable Energy and the CCC Renewables Review Presentation to the EPRG Spring Conference Cambridge, 12 May 2011 Professor Michael Grubb Faculty of Economics, Cambridge University Context: a rich body

IEA North American Roadmap Workshop

Hydrogen Supply/Demand IEA North American Roadmap Workshop January 28, 2014 Eric Miller U.S. Department of Energy Fuel Cell Technologies Office Hydrogen Production Technology Manager 1 Fuel Cell Technologies

Hydrogen Supply/Demand IEA North American Roadmap Workshop January 28, 2014 Eric Miller U.S. Department of Energy Fuel Cell Technologies Office Hydrogen Production Technology Manager 1 Fuel Cell Technologies

Development of Business Cases for Fuel Cells and Hydrogen Applications for Regions and Cities. Hydrogen injection into the natural gas grid

Development of Business Cases for Fuel Cells and Hydrogen Applications for Regions and Cities Hydrogen injection into the natural gas grid Brussels, Fall 2017 This compilation of application-specific information

Development of Business Cases for Fuel Cells and Hydrogen Applications for Regions and Cities Hydrogen injection into the natural gas grid Brussels, Fall 2017 This compilation of application-specific information

ITM Power has developed a range of materials and technologies to reduce the cost of Hydrogen production

ITM Power has developed a range of materials and technologies to reduce the cost of Hydrogen production The company is developing equipment to convert renewable energy to a clean fuel; storing the energy

ITM Power has developed a range of materials and technologies to reduce the cost of Hydrogen production The company is developing equipment to convert renewable energy to a clean fuel; storing the energy

Renewable Electricity Financial Incentive Consultation Fuel Cells UK Response

Response 1. Introduction This paper represents the response from to the Government s Renewable Electricity Financial Incentives Consultation, Section 3 Feed-in Tariffs (FITs). is the UK trade association

Response 1. Introduction This paper represents the response from to the Government s Renewable Electricity Financial Incentives Consultation, Section 3 Feed-in Tariffs (FITs). is the UK trade association

Commercialisation of Energy Storage in Europe. Nikolaos Lymperopoulos, Project Manager

Commercialisation of Energy Storage in Europe Nikolaos Lymperopoulos, Project Manager Contents Introduction and context to the study Key findings of the study H2 specific messages The study was authored

Commercialisation of Energy Storage in Europe Nikolaos Lymperopoulos, Project Manager Contents Introduction and context to the study Key findings of the study H2 specific messages The study was authored

Guidance Note for CLA members

Guidance Note for CLA members Feed in Tariff (FIT) for Solar Photovoltaic (PV) Installations Date: 10 February 2015 CLA Guidance Note Reference: GN11-15 Introduction The Feed in Tariff (FiT) scheme was

Guidance Note for CLA members Feed in Tariff (FIT) for Solar Photovoltaic (PV) Installations Date: 10 February 2015 CLA Guidance Note Reference: GN11-15 Introduction The Feed in Tariff (FiT) scheme was

community energy ! Our market strategy is:!

avalon community energy Business Plan 2014/2016 1 Executive Summary This outline business plan, describes the mission and objectives of Avalon Community Energy Co-op (ACE), and uses PESTLE and SWOT analysis

avalon community energy Business Plan 2014/2016 1 Executive Summary This outline business plan, describes the mission and objectives of Avalon Community Energy Co-op (ACE), and uses PESTLE and SWOT analysis

Download the report:

Download the report: www.iea.org/publications/insights Outlook for Hydrogen Cédric Philibert, Renewable Energy Division, International Energy Agency Green Hydrogen for the Chilean Energy Transition, Santiago

Download the report: www.iea.org/publications/insights Outlook for Hydrogen Cédric Philibert, Renewable Energy Division, International Energy Agency Green Hydrogen for the Chilean Energy Transition, Santiago

THE ECONOMIC IMPACT OF HYDROGEN AND FUEL CELLS IN THE UK

THE ECONOMIC IMPACT OF HYDROGEN AND FUEL CELLS IN THE UK A Preliminary Assessment based on Analysis of the Replacement of Refined Transport Fuels and Vehicles White Papers Launch London City Hall 17 th

THE ECONOMIC IMPACT OF HYDROGEN AND FUEL CELLS IN THE UK A Preliminary Assessment based on Analysis of the Replacement of Refined Transport Fuels and Vehicles White Papers Launch London City Hall 17 th

Evaluation of Hydrogen Production and Utilization under Various Renewable Energy Curtailment Scenarios

Evaluation of Hydrogen Production and Utilization under Various Renewable Energy Curtailment Scenarios Prepared for the: State of Hawaii Department of Business, Economic Development and Tourism Under Supplemental

Evaluation of Hydrogen Production and Utilization under Various Renewable Energy Curtailment Scenarios Prepared for the: State of Hawaii Department of Business, Economic Development and Tourism Under Supplemental

Techno-economic Comparison Between Multiple Forecourt Electrolysers and Central Hydrogen Production

Techno-economic Comparison Between Multiple Forecourt Electrolysers and Central Hydrogen Production By Abdulla Rahil (P1363959@my365.dmu.ac.uk) Supervisors: 1 st Rupert Gammon 2 nd Neil Brown Fuel Cell

Techno-economic Comparison Between Multiple Forecourt Electrolysers and Central Hydrogen Production By Abdulla Rahil (P1363959@my365.dmu.ac.uk) Supervisors: 1 st Rupert Gammon 2 nd Neil Brown Fuel Cell

On the road to a green energy UK

On the road to a green energy UK consumer willingness and ability to pay for decarbonised heat Chris Clarke Director of Asset Management and HS&E Wales & West Utilities April 2018 (Research commissioned

On the road to a green energy UK consumer willingness and ability to pay for decarbonised heat Chris Clarke Director of Asset Management and HS&E Wales & West Utilities April 2018 (Research commissioned

Electro fuels an introduction

Electro fuels an introduction Cédric Philibert, Renewable Energy Division, International Energy Agency EC-IEA Workshop on Electro fuels, Brussels, 10 Sept 2018 IEA Industry and transports: the hard-to-abate

Electro fuels an introduction Cédric Philibert, Renewable Energy Division, International Energy Agency EC-IEA Workshop on Electro fuels, Brussels, 10 Sept 2018 IEA Industry and transports: the hard-to-abate

Speyside Power-to-Gas Project Feasibility Study

Speyside Power-to-Gas Project Feasibility Study UK Biomethane Day 2 nd May 2018 Simon Griew simon@griewconsulting.com 07767 890830 Summary Distilleries emit CO 2 in the fermentation process and by burning

Speyside Power-to-Gas Project Feasibility Study UK Biomethane Day 2 nd May 2018 Simon Griew simon@griewconsulting.com 07767 890830 Summary Distilleries emit CO 2 in the fermentation process and by burning

REA Response the Energy Technology List (ETL): Call for Evidence

: Call for Evidence") REA Response the Energy Technology List (ETL): Call for Evidence The Renewable Energy Association (REA) is pleased to submit this response to the above inquiry. The REA represents a wide variety of organisations,

REA Response the Energy Technology List (ETL): Call for Evidence The Renewable Energy Association (REA) is pleased to submit this response to the above inquiry. The REA represents a wide variety of organisations,

Hydrogen in New Zealand Report 1 Summary

www.concept.co.nz Hydrogen in New Zealand Report 1 Summary Version 04 29/01/2019 About Concept Concept Consulting Group Ltd (Concept) specialises in providing analysis and advice on energy-related issues.

www.concept.co.nz Hydrogen in New Zealand Report 1 Summary Version 04 29/01/2019 About Concept Concept Consulting Group Ltd (Concept) specialises in providing analysis and advice on energy-related issues.

Market Stabilisation Analysis: Enabling Investment in Established Low Carbon Electricity Generation

Click here to enter text. 21 April 2017 Market Stabilisation Analysis: Enabling Investment in Established Low Carbon Electricity Generation An Arup report for ScottishPower Renewables July 2017 21 April

Click here to enter text. 21 April 2017 Market Stabilisation Analysis: Enabling Investment in Established Low Carbon Electricity Generation An Arup report for ScottishPower Renewables July 2017 21 April

About Energy UK. Introduction

REC 34-15 Energy UK response to DG Comp investigation of Investment Contract (early Contract for Difference) for Lynemouth power station biomass conversion 10 May 2015 About Energy UK Energy UK is the

REC 34-15 Energy UK response to DG Comp investigation of Investment Contract (early Contract for Difference) for Lynemouth power station biomass conversion 10 May 2015 About Energy UK Energy UK is the

Potential for natural gas to reduce transportation emissions. October 2016

Potential for natural gas to reduce transportation emissions October 2016 Summary Natural gas can reduce transportation sector emissions with three main types of technologies: 1. Natural gas vehicles 2.

Potential for natural gas to reduce transportation emissions October 2016 Summary Natural gas can reduce transportation sector emissions with three main types of technologies: 1. Natural gas vehicles 2.

SHFCA & Member Activities

Areas we will cover SHFCA activities Scotland s journey to a Low Carbon Economy Hydrogen Office & Aberdeen Bus Projects Orkney Islands including Surf n Turf & BIG HIT Priority topics - 2016 HFC Roadmap

Areas we will cover SHFCA activities Scotland s journey to a Low Carbon Economy Hydrogen Office & Aberdeen Bus Projects Orkney Islands including Surf n Turf & BIG HIT Priority topics - 2016 HFC Roadmap

COGEN Europe Position Paper

COGEN Europe Position Paper Micro-CHP A cost-effective solution to save energy, reduce GHG emissions and partner with intermittent renewables Micro-CHP 1 is the state-of-the-art energy supply solution

COGEN Europe Position Paper Micro-CHP A cost-effective solution to save energy, reduce GHG emissions and partner with intermittent renewables Micro-CHP 1 is the state-of-the-art energy supply solution

Submission on the Draft report on transitioning to a low-emissions economy

Hiringa Energy Limited 15 Lismore Street, Strandon, New Plymouth, 4312 Ph: +64 27 704 7007 www.hiringa.co.nz 8 June, 2018 Submission on the Draft report on transitioning to a low-emissions economy Hiringa

Hiringa Energy Limited 15 Lismore Street, Strandon, New Plymouth, 4312 Ph: +64 27 704 7007 www.hiringa.co.nz 8 June, 2018 Submission on the Draft report on transitioning to a low-emissions economy Hiringa

Renewable Energy Strategy Consultation Fuel Cells UK Response

Fuel Cells UK Response 1. Introduction This paper represents the response from Fuel Cells UK to the Government s Renewable Energy Strategy Consultation. Fuel Cells UK is the UK trade association for the

Fuel Cells UK Response 1. Introduction This paper represents the response from Fuel Cells UK to the Government s Renewable Energy Strategy Consultation. Fuel Cells UK is the UK trade association for the

MicroCHP Updated market projections. Report, prepared by the Domestic CHP Section of the SBGI

MicroCHP Updated market projections Report, prepared by the Domestic CHP Section of the SBGI March 2006 About the SBGI The SBGI is a trade association that represents virtually all the major players in

MicroCHP Updated market projections Report, prepared by the Domestic CHP Section of the SBGI March 2006 About the SBGI The SBGI is a trade association that represents virtually all the major players in

LINKING ENERGY SYSTEM AND INFRASTRUCTURE MODELS TO EXPLORE THE TRANSITION TO A HYDROGEN- FUELLED ECONOMY IN THE UK

LINKING ENERGY SYSTEM AND INFRASTRUCTURE MODELS TO EXPLORE THE TRANSITION TO A HYDROGEN- FUELLED ECONOMY IN THE UK Nagore Sabio and Paul Dodds UCL Energy Institute, 14 Upper Woburn Place, WC1H 0NN, London

LINKING ENERGY SYSTEM AND INFRASTRUCTURE MODELS TO EXPLORE THE TRANSITION TO A HYDROGEN- FUELLED ECONOMY IN THE UK Nagore Sabio and Paul Dodds UCL Energy Institute, 14 Upper Woburn Place, WC1H 0NN, London

Fuel Cells and Hydrogen Joint Undertaking

Fuel Cells and Hydrogen Joint Undertaking Current status and perspectives Luciano GAUDIO Stakeholders Relationships Manager Rome, 13 December 2013 1 General context Security of energy supply: Transport

Fuel Cells and Hydrogen Joint Undertaking Current status and perspectives Luciano GAUDIO Stakeholders Relationships Manager Rome, 13 December 2013 1 General context Security of energy supply: Transport

The University of Essex Carbon Management Plan

The University of Essex Carbon Management Plan June 2010 Overview Executive Summary This Carbon Management Plan sets out the overall strategic vision of the University of Essex towards reducing carbon

The University of Essex Carbon Management Plan June 2010 Overview Executive Summary This Carbon Management Plan sets out the overall strategic vision of the University of Essex towards reducing carbon

European Distribution System Operators for Smart Grids. Retail energy market: Supplementary response to the European Commission s public consultation

European Distribution System Operators for Smart Grids Retail energy market: Supplementary response to the European Commission s public consultation April 2014 EDSO supplementary response to the European

European Distribution System Operators for Smart Grids Retail energy market: Supplementary response to the European Commission s public consultation April 2014 EDSO supplementary response to the European

Power Perspectives 2030

Executive Summary A contributing study to Roadmap 2050: a practical guide to a prosperous, low-carbon europe EXECUTIVE SUMMARY A. CONTEXT In October 2009, the European Council set an economy-wide greenhouse

Executive Summary A contributing study to Roadmap 2050: a practical guide to a prosperous, low-carbon europe EXECUTIVE SUMMARY A. CONTEXT In October 2009, the European Council set an economy-wide greenhouse

Firstly industrial, commercial and public sector dwellings are split over the following characteristics:

Annex 1 Input Assumptions In setting tariffs DECC has used a large dataset of performance and cost data for a large number of building types. This data is disclosed in full in the accompanying spreadsheet

Annex 1 Input Assumptions In setting tariffs DECC has used a large dataset of performance and cost data for a large number of building types. This data is disclosed in full in the accompanying spreadsheet

Doncaster Council Home Energy Conservation Act (1995) 2013 Report

2013 Report") Doncaster Council Home Energy Conservation Act (1995) 2013 Report Contents: Page 1. Report Introduction 1 2. The National Context 1 The Energy Act 2011 1 Green Deal 1 Energy Company Obligation 1 2 Renewable

Doncaster Council Home Energy Conservation Act (1995) 2013 Report Contents: Page 1. Report Introduction 1 2. The National Context 1 The Energy Act 2011 1 Green Deal 1 Energy Company Obligation 1 2 Renewable

Climate value for money funding carbon capture and storage demonstrations in the UK power sector

Climate value for money funding carbon capture and storage demonstrations in the UK power sector Updated September 2010 INTRODUCTION The Committee on Climate Change (CCC) have repeatedly recommended that

Climate value for money funding carbon capture and storage demonstrations in the UK power sector Updated September 2010 INTRODUCTION The Committee on Climate Change (CCC) have repeatedly recommended that

Queensland Renewable Energy Expert Panel Issues Paper