Systems Design: Process Costing. M. En C. Eduardo Bustos Farías

|

|

|

- Patricia Poole

- 6 years ago

- Views:

Transcription

1 Systems Design: Process Costing M. En C. Eduardo Bustos Farías 1

2 Types of Costing Systems Used to Determine Product Costs Process Costing Job-order Costing Many units of of a single, homogeneous product flow evenly through a continuous production process. One unit of of product is is indistinguishable from any other unit of of product. Each unit of of product is is assigned the same average cost. 2

3 Types of Costing Systems Used to Determine Product Costs Process Costing Job-order Costing Typical process cost applications: Petrochemical refinery Paint manufacturer Paper mill Fabricación de papel 3

4 Differences Between Job- Order and Process Costing Job order costing Many jobs are worked during the period. Costs are accumulated by individual jobs. Job cost sheet is the key document. Unit cost computed by job. Process costing A single product is produced for a long period of time. Costs are accumulated by departments. Department production report is key document. Unit costs are computed by department. 4

5 An Operational Process System Mixing Selecting Sifting Measuring Blending Tableting Loading Pressing Costing Bottling Loading Counting Capping Packaging 5

6 Quick Check Process costing is used for products that are: a. Different and produced continuously. b. Similar and produced continuously. c. Individual units produced to customer specifications. d. Purchased from vendors. 6

7 Quick Check Process costing is used for products that are: a. Different and produced continuously. b. Similar and produced continuously. c. Individual units produced to customer specifications. d. Purchased from vendors. 7

8 Job-Order Costing Estrella Company Manufacturing Costs Direct Materials Direct Labor Applied Overhead Job 205 Job 206 Job 207 Finished Goods Finished Goods Finished Goods 8

9 Process Costing Estrella Company Manufacturing Costs Direct Materials Direct Labor Applied Overhead Picking Tableting Bottling Finished Goods 9

10 Process Costing Dollar Amount Direct Labor Direct Materials Conversion Direct labor costs may be be small in in comparison to to other product costs in in process cost systems. Type of Product Cost 10

11 Process Costing Dollar Amount Direct Materials Conversion Direct labor costs may be be small in in comparison to to other product costs in in process cost systems. Type of Product Cost So, direct labor and manufacturing overhead are often combined into one product cost called conversion. 11

12 Comparing Job-Order and Process Costing Direct Materials Direct Labor Work in Process Finished Goods Manufacturing Overhead Cost of Goods Sold 12

13 Comparing Job-Order and Process Costing Direct Materials Costs are traced and applied to individual jobs in a job-order cost system. Direct Labor Jobs Finished Goods Manufacturing Overhead Cost of Goods Sold 13

14 Comparing Job-Order and Process Costing Direct Materials Costs are traced and applied to departments in a process cost system. Direct Labor Processing Department Finished Goods Manufacturing Overhead Cost of Goods Sold 14

15 Characteristics of Process Costing Homogeneous units pass through a series of similar processes. Each unit in each process receives a similar dose of manufacturing costs. Manufacturing costs are accumulated by a process for a given period of time. 15

16 Characteristics of Process Costing There is a work-in-process account for each process. Manufacturing cost flows and the associated journal entries are generally similar to job-order costing. The departmental production report is the key document for tracking manufacturing activity and costs. Unit costs are computed by dividing the departmental costs of the period by the output for the period. 16

17 Equivalent Units of Production Equivalent units are partially complete and are part of work in process inventory. Partially completed products are expressed in terms of a smaller number of fully completed units. 17

18 Equivalent Units of Production Two half completed products are equivalent to one completed product. + = 1 So, 10,000 units 70 percent complete are equivalent to 7,000 complete units. 18

19 Cost of Production Report 1. Analysis of the flow of physical units 2. Calculation of equivalent units 3. Computation of unit cost 4. Valuation of inventories (goods transferred out and ending work in process) 5. Cost reconciliation Unit Information Units to be accounted for: Units in beginning work in process 0 Units started and completed 24,000 Units to be accounted for 24,000 Physical Flow Equivalent Units Units accounted for: Units 20,000 20,000 20,000 Units in ending work in process (25% complete) 4,000 1,000 Units accounted for 24,000 Work completed 21,000 19

20 Cost of Production Report Unit Information Units to account for: Units in beginning work in process 0 Units started 24,000 Total units to account for 24,000 Units accounted for: Physical Flow Equivalent Units Units completed 20,000 20,000 Units in ending work in process (25% complete) 4,000 1,000 Units accounted for 24,000 Work completed 21,000 Continued 20

21 Cost of Production Report Cost Information Costs to account for: Beginning work in process $ 0 Incurred during the period 168,000 Total costs to account for 168,000 Divided by equivalent units 21,000 Cost per equivalent unit $ 8 Cost accounted for: Goods transferred out ($8 x 20,000) $160,000 Ending work in process ($8 x 1,000) 8,000 Total costs accounted for $168,000 21

22 Quick Check For the current period, Jones started 15,000 units and completed 10,000 units, leaving 5,000 units in process 30 percent complete. How many equivalent units of production did Jones have for the period? a. 10,000 b. 11,500 c. 13,500 d. 15,000 22

23 Quick Check For the current period, Jones started 15,000 units and completed 10,000 units, leaving 5,000 units in process 30 percent complete. How many equivalent units of production did Jones have for the period? a. 10,000 b. 11,500 c. 13,500 d. 15,000 10,000 units + (5,000 units 0.30) = 11,500 equivalent units 23

24 Calculating and Using Equivalent Units of Production To calculate the cost per equivalent unit for the period: Cost per equivalent unit = Costs for the period Equivalent units of production for the period 24

25 Quick Check Now assume that Jones incurred $27,600 in production costs for the 11,500 equivalent units of production. What was Jones cost per equivalent unit for the period? a. $1.84 b. $2.40 c. $2.76 d. $

26 Quick Check Now assume that Jones incurred $27,600 in production costs for the 11,500 equivalent units of production. What was Jones cost per equivalent unit for the period? a. $1.84 b. $2.40 = $2.40 per equivalent unit c. $2.76 d. $2.90 $27,600 11,500 equivalent units 26

27 PELICULA 27

28 Equivalent Units of Production Weighted Average Method The weighted average method... Makes no distinction between work done in prior and current period. Blends together units and costs from prior mezcla period and current period. Antes de Let s see how this works! 28

29 Weighted Average Example Smith Company reported the following activity in Department A for the month of June: Percent Completed Units Materials Conversion Work in process, June % 20% Units started into production in June 6,000 Units completed and transferred out 5,400 of Department A during June Work in process, June % 30% 29

30 Weighted Average Example Equivalent units are calculated as follows: Materials Conversion Units completed and transferred out of Department A in June 5,400 5,400 30

31 Weighted Average Example Equivalent units are calculated as follows: Materials Conversion Units completed and transferred out of Department A in June 5,400 5,400 Work in process, June 30: 900 units 60% 540 Equivalent units of Production in Department A during June 5,940 31

32 Weighted Average Example Equivalent units are calculated as follows: Materials Conversion Units completed and transferred out of Department A in June 5,400 5,400 Work in process, June 30: 900 units 60% units 30% 270 Equivalent units of Production in Department A during June 5,940 5,670 32

33 Weighted Average Example Equivalent units of production always equals: Units completed and transferred + Equivalent units remaining in work in process Materials Conversion Units completed and transferred out of Department A in June 5,400 5,400 Work in process, June 30: 900 units 60% units 30% 270 Equivalent units of Production in Department A during June 5,940 5,670 33

34 Weighted Average Example Materials 6,000 Units Started Beginning Work in Process 300 Units 40% Complete 5,100 Units Started and Completed Ending Work in Process 900 Units 60% Complete 5,400 Units Completed 540 Equivalent Units 5,940 Equivalent units of production % 34

35 Weighted Average Example Conversion 6,000 Units Started Beginning Work in Process 300 Units 20% Complete 5,100 Units Started and Completed Ending Work in Process 900 Units 30% Complete 5,400 Units Completed 270 Equivalent Units 5,670 Equivalent units of production % 35

36 PELÍCULA 36

37 Production Report Shows the flow of units and costs through work in process Provides cost information for financial statements Production Report Becomes the job cost sheet in process costing Helps managers control their departments 37

38 Production Report Production Report Section 1 Section 2 A quantity schedule showing the flow of units and the computation of equivalent units. A computation of cost per equivalent unit. Section 3 38

39 Production Report Production Report Section 1 Section 2 Section 3 A reconciliation of cost flows for the period, including: Total cost for units completed and transferred from the processing department. Total cost for partially completed units remaining in work in process. 39

40 Production Report Example Double Diamond Skis uses process costing to determine unit costs in its Shaping and Milling Formado y molido Department. Double Diamond uses the weighted average cost procedure. Using the following information for the month of May, let s prepare a production report for Shaping and Milling. 40

41 Production Report Example Work in process, May 1: 200 units Materials: 55% complete. $ 9,600 Conversion: 30% complete. 5,575 Production started during May: Production completed during May: 5,000 units 4,800 units Costs added to production in May Materials cost $ 368,600 Conversion cost 350,900 Work in process, May 31: 400 units Materials 40% complete. Conversion 25% complete. 41

42 Production Report Example Section 1: Quantity Schedule with Equivalent Units Units to be accounted for: Work in process, May Started into production 5,000 Total units 5,200 Equivalent units Materials Conversion Units accounted for as follows: Completed and transferred 4,800 4,800 4,800 Work in process, May

43 Production Report Example Section 1: Quantity Schedule with Equivalent Units Units to be accounted for: Work in process, May Started into production 5,000 Total units 5,200 Equivalent units Materials Conversion Units accounted for as follows: Completed and transferred 4,800 4,800 4,800 Work in process, May Materials 40% complete 160 5,200 4,960 43

44 Production Report Example Section 1: Quantity Schedule with Equivalent Units Units to be accounted for: Work in process, May Started into production 5,000 Total units 5,200 Equivalent units Materials Conversion Units accounted for as follows: Completed and transferred 4,800 4,800 4,800 Work in process, May Materials 40% complete 160 Conversion 25% complete 100 5,200 4,960 4,900 44

45 Production Report Example Section 2: Compute cost per equivalent unit Total Cost Materials Conversion Cost to be accounted for: Work in process, May 1 $ 15,175 $ 9,600 $ 5,575 Costs added in the Shipping and Milling Department 719, , ,900 Total cost $ 734,675 $ 378,200 $ 356,475 Equivalent units 4,960 4,900 Cost per equivalent unit 45

46 Production Report Example Section 2: Compute cost per equivalent unit Total Cost Materials Conversion Cost to be accounted for: Work in process, May 1 $ 15,175 $ 9,600 $ 5,575 Costs added in the Shipping and Milling Department 719, , ,900 Total cost $ 734,675 $ 378,200 $ 356,475 Equivalent units 4,960 4,900 Cost per equivalent unit $ $378,200 4,960 units = $

47 Production Report Example Section 2: Compute cost per equivalent unit Total Cost Materials Conversion Cost to be accounted for: Work in process, May 1 $ 15,175 $ 9,600 $ 5,575 Costs added in the Shipping and Milling Department 719, , ,900 Total cost $ 734,675 $ 378,200 $ 356,475 Equivalent units 4,960 4,900 Cost per equivalent unit $ $ Total cost per equivalent unit = $ $72.75 = $ $356,475 4,900 units = $

48 Production Report Example Section 3: Cost Reconciliation Total Equivalent Units Cost Materials Conversion Cost accounted for as follows: Transferred out during May 4,800 4,800 Work in process, May 31: Materials 160 Conversion 100 Total work in process, May 31 Total cost accounted for 48

49 Production Report Example Section 3: Cost Reconciliation 4,800 $ Total Equivalent Units Cost Materials Conversion Cost accounted for as follows: Transferred out during May $ 715,200 4,800 4,800 Work in process, May 31: Materials 160 Conversion 100 Total work in process, May 31 Total cost accounted for 49

50 Production Report Example Section 3: Cost Reconciliation 160 units X $76.25 Total Equivalent Units Cost Materials Conversion 100 units X $72.75 Cost accounted for as follows: Transferred out during May $ 715,200 4,800 4,800 Work in process, May 31: Materials 12, Conversion 7, Total work in process, May 31 19,475 Total cost accounted for $ 734,675 All costs accounted for 50

51 Operation Costing Operation costing employs some aspects of both job-order and process costing. Job-order Costing Operation Costing (Products produced in batches) Process Costing Material Costs Charged to to batches as as in in job-order costing. Conversion costs assigned to to batches as as in in process costing. 51

52 PELÍCULA 52

53 Review exercise 53

54 1. Calcular las unidades equivalentes para el período actual utilizando el método de promedios ponderados. 54

55 55

56 2. Calculate equivalent units and understand how to use them. 56

57 Five Steps in Process Costing Step 1: Summarize the flow of physical units of output. Step 2: Compute output in terms of equivalent units. Step 3: Compute equivalent unit costs. Step 4: Summarize total costs to account for. Step 5: Assign total costs to units completed and to units in ending work in process inventory. 57

58 Physical Units (Step 1) Physical units Flow of Production Work in process, beginning 0 Started during current period 35,000 To account for 35,000 Completed and transferred out during current period 30,000 Work in process, ending (100%/20%) 5,000 Accounted for 35,000 58

59 Compute Equivalent Units (Step 2) Equivalent units Direct Conversion Flow of Production Materials Costs Completed and transferred out 30,000 30,000 Work in process, ending 5,000 (100%) 1,000 (20%) Current period work 35,000 31,000 59

60 Compute Equivalent Unit Costs (Step 3) Total production costs are $146,050. Direct Conversion Materials Costs $84,050 $62,000 Equivalent units 35,000 31,000 Cost per equivalent unit $ $

Direct materials 5,000 $2.4014 12,007 Conversion costs 1,000 $2.")

61 Summarize and Assign Total Costs (Steps 4 and 5) Step 4: Total costs to account for: $146,050 Step 5: Assign total costs: Completed and transferred out 30,000 $ $132,043 Work in process, ending (5,000 units) Direct materials 5,000 $ ,007 Conversion costs 1,000 $2.00 2,000 Total $146,050 61

62 PELÍCULA 62

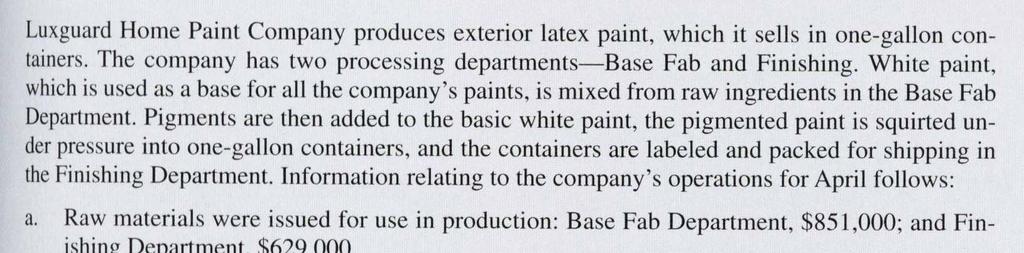

63 5. Lexguard Home Paiting 63

64 64

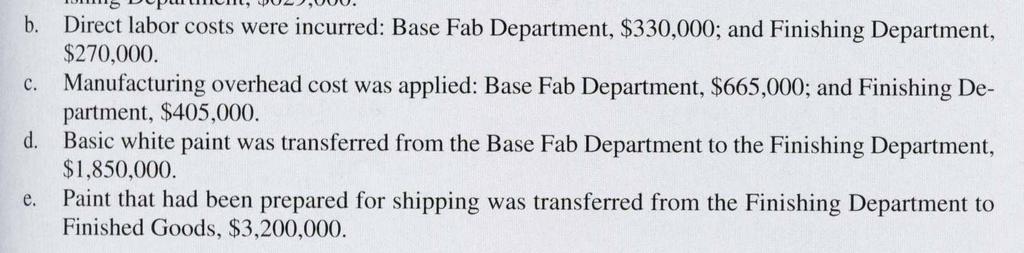

65 65

66 66

67 67

68 68

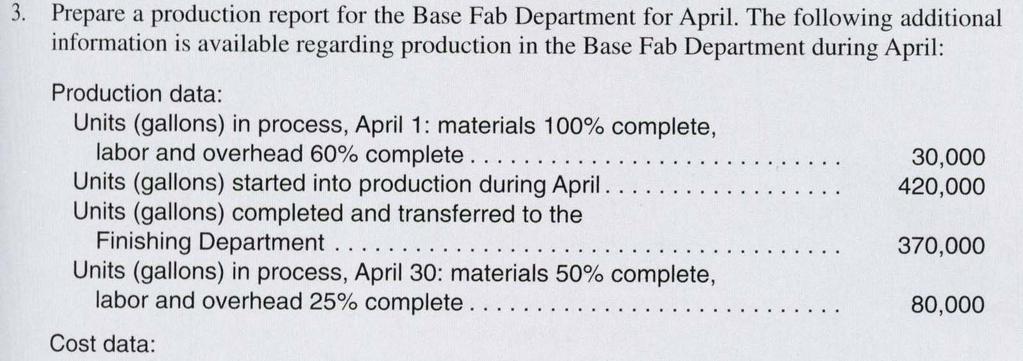

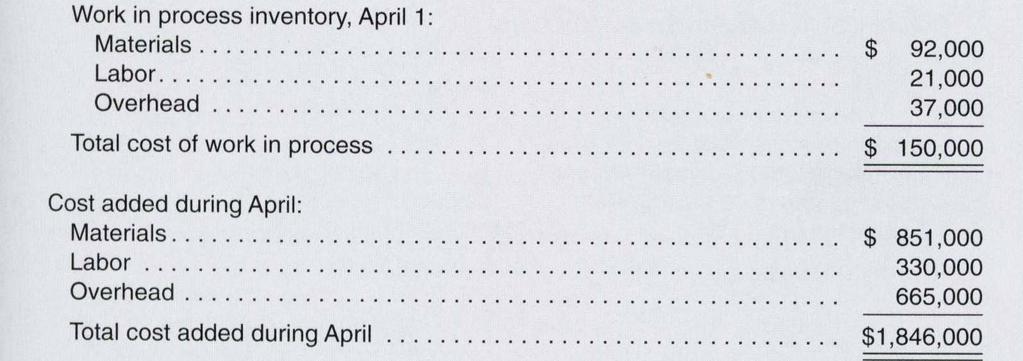

69 FIFO Costing Method Under the FIFO costing method, the equivalent units and manufacturing costs in beginning work in process are excluded from the currentperiod unit cost calculation. Thus, FIFO recognizes that the work and costs carried over from the prior period legitimately belong to that period. 69

70 FIFO Costing Method Estrella Company Mixing Department Production and Cost Data for October Production: Units in process, October 1, 70% complete 10,000 Units completed and transferred out 60,000 Units in process, October 31, 40% complete 20,000 Costs: Work in process, October 1: Direct materials $1,000 Conversion costs 350 Total work in process $1,350 Continued 70

71 Estrella Company Mixing Department Production and Cost Data for October Costs: Current costs: Direct materials $12,600 Conversion costs 3,050 Total current costs $15,650 71

72 FIFO Costing Method Step 1: Physical Flow Analysis Units to account for: Units, beginning work in process 10,000 Units started during October 70,000 Total units to account for 80,000 Units accounted for: Units completed and transferred out: Started and completed 50,000 From beginning work in process 10,000 60,000 Units in ending work in process (40% complete) 20,000 Total units accounted for 80,000 72

73 FIFO Costing Method Step 2: Calculation of Equivalent Units Direct Materials Conversion Costs Units started and completed 50,000 50,000 Add: Units in beginning work in process x percentage to complete: 10,000 x 0% materials ,000 x 30% conversion 3,000 Add: Units in ending work in process x percentage complete: 20,000 x 100% materials 20,000 20,000 x 40% conversion 8,000 Equivalent units of output 70,000 61,000 73

74 FIFO Costing Method Step 3: Computation of Unit Cost Unit direct materials costs = $12,600/70,000 = $0.18 Unit conversion costs = $3,500/61,000 = $0.05 Unit cost = Unit materials cost + Unit conversion costs = $ $0.05 = $0.23 per ounce 74

75 FIFO Costing Method Step 4: Valuation of Inventories Cost of ending work in process: Direct materials ($0.18 x 20,000) $ 3,600 Conversion costs ($0.05 x 8,000) 400 Total $ 4,000 Units started and completed ($0.23 x 50,000) $11,500 Units, beginning work in process: Prior period costs $1,350 Cost to finish ($0.05 x 3,000) 150 1,500 Total $13,000 75

76 FIFO Costing Method Step 5: Cost Reconciliation Costs to account for: Beginning work in process $1,350 Incurred during the period: Direct materials $12,600 Conversion costs 3,050 15,650 Total costs to account for $17,000 Costs accounted for Goods transferred out: Units, beginning work in process $ 1,500 Units started and completed 11,500 Goods in ending work in process 4,000 Total costs accounted for $17,000 76

77 Estrella Company Mixing Department Production Report for October (FIFO Method) Units to account for: Units accounted for: Unit Information Units, beginning work Units completed 60,000 in process 10,000 Units started 70,000 Units, EWIP 20,000 Total units to account for 80,000 Total units accounted for 80,000 Equivalent Units Direct Conversion Materials Costs Units started and completed 50,000 50,000 Units, beginning work in process --- 3,000 Units, ending work in process 20,000 8,000 Equivalent units of output 70,000 61,000 Continued 77

78 Cost Information Costs to account for: Direct Conversion Materials Costs Total Beginning work in process $ 1,000 $ 350 $ 1,350 Incurred during the period 12,600 3,050 15,650 Total costs to account for $13,600 $ 3,400 $17,000 Costs per equivalent unit: Current costs $12,600 $ 3,050 Divided by equivalent units 70,000 61,000 Cost per equivalent unit $ 0.18 $ 0.05 $ 0.23 Continued 78

79 Costs accounted for: Units transferred out: Units, beginning work in process: From prior period $ From current period ($0.05 x 3,000) 150 Units started and completed ($0.23 x 50,000) 11,500 $13,000 Ending work in process: Direct materials (20,000 x $0.18) $ 3,600 Conversion costs (8,000 x $0.05) 400 4,000 Total costs accounted for $17,000 79

Chapter 4. Systems Design: Process Costing. Types of Costing Systems Used to Determine Product Costs. Job-order Costing.

4-1 Chapter 4 Systems Design: Process Costing Types of Costing Systems Used to Determine Product Costs Process Costing Job-order Costing F Many units of a single, homogeneous product flow evenly through

4-1 Chapter 4 Systems Design: Process Costing Types of Costing Systems Used to Determine Product Costs Process Costing Job-order Costing F Many units of a single, homogeneous product flow evenly through

Similarities Between Job-Order and Process Costing

Similarities Between Job-Order and Process Costing 4-1 Both systems assign material, labor, and overhead costs to products and they provide a mechanism for computing unit product costs. Both systems use

Similarities Between Job-Order and Process Costing 4-1 Both systems assign material, labor, and overhead costs to products and they provide a mechanism for computing unit product costs. Both systems use

PROCESS COSTING FIRST-IN FIRST-OUT METHOD

PROCESS COSTING FIRST-IN FIRST-OUT METHOD Key Terms and Concepts to Know Differences between Job-Order Costing and Processing Costing Process costing is used when a single product is made on a continuous

PROCESS COSTING FIRST-IN FIRST-OUT METHOD Key Terms and Concepts to Know Differences between Job-Order Costing and Processing Costing Process costing is used when a single product is made on a continuous

Process Costing. Chapter 17 ACCT Fall Jay K. Baker, MSFS, MBA, CPA, CFP

Process Costing Chapter 17 ACCT 3270 Fall 2016 Jay K. Baker, MSFS, MBA, CPA, CFP J. Keith Baker 2015 Job Costing Versus Process Costing LO 17-1 Identify the situations in which process-costing systems

Process Costing Chapter 17 ACCT 3270 Fall 2016 Jay K. Baker, MSFS, MBA, CPA, CFP J. Keith Baker 2015 Job Costing Versus Process Costing LO 17-1 Identify the situations in which process-costing systems

JOB ORDER COSTING. LO 1: Cost Systems. Determine whether job order costing or process costing would be more appropriate for each industry.

JOB ORDER COSTING Terms Cost Accounting Process Cost System Job Order Cost System LO 1: Cost Systems Job-Order Costing Used for custom or unique items Each job is accounted for separately Measures cost

JOB ORDER COSTING Terms Cost Accounting Process Cost System Job Order Cost System LO 1: Cost Systems Job-Order Costing Used for custom or unique items Each job is accounted for separately Measures cost

Variable Costing: A Tool for Management. M. En C. Eduardo Bustos Farías

Variable Costing: A Tool for Management M. En C. Eduardo Bustos Farías 1 Absorption Costing A system of accounting for costs in which both fixed and variable production costs are considered product costs.

Variable Costing: A Tool for Management M. En C. Eduardo Bustos Farías 1 Absorption Costing A system of accounting for costs in which both fixed and variable production costs are considered product costs.

CHAPTER 17 PROCESS COSTING Give three examples of industries that use process-costing systems.

CHAPTER 17 PROCESS COSTING 17-1 Give three examples of industries that use process-costing systems. Industries using process costing in their manufacturing area include chemical processing, oil refining,

CHAPTER 17 PROCESS COSTING 17-1 Give three examples of industries that use process-costing systems. Industries using process costing in their manufacturing area include chemical processing, oil refining,

CHAPTER 6 PROCESS COST ACCOUNTING ADDITIONAL PROCEDURES

CHAPTER 6 PROCESS COST ACCOUNTING ADDITIONAL PROCEDURES Review Summary 1. In many industries where a process cost system is used, the materials may be put into production in irregular quantities and at

CHAPTER 6 PROCESS COST ACCOUNTING ADDITIONAL PROCEDURES Review Summary 1. In many industries where a process cost system is used, the materials may be put into production in irregular quantities and at

MANAGERIAL ACCOUNTING Hilton Chapter 4 Adobe Connect Process Costing

1 MANAGERIAL ACCOUNTING Hilton Chapter 4 Adobe Connect Process Costing Overview Chapter 4 introduces another classic cost accounting system, Process Costing. Then, combined with knowledge of Job-Order

1 MANAGERIAL ACCOUNTING Hilton Chapter 4 Adobe Connect Process Costing Overview Chapter 4 introduces another classic cost accounting system, Process Costing. Then, combined with knowledge of Job-Order

Chapter 8 Inventories: Measurement

Chapter 8 Inventories: Measurement QUESTIONS FOR REVIEW OF KEY TOPICS Question 8 1 Inventory for a manufacturing company consists of (1) raw materials, (2) work in process, and (3) finished goods. Raw

Chapter 8 Inventories: Measurement QUESTIONS FOR REVIEW OF KEY TOPICS Question 8 1 Inventory for a manufacturing company consists of (1) raw materials, (2) work in process, and (3) finished goods. Raw

By-Product, Joint, & Other Costing

Question 1: What is joint product costing and by-products? Answer 1: A joint product cost is the cost of a production process that yields multiple products at the same time or produces a product that goes

Question 1: What is joint product costing and by-products? Answer 1: A joint product cost is the cost of a production process that yields multiple products at the same time or produces a product that goes

Chapter 17 Job Order Costing Study Guide Solutions Fill-in-the-Blank Equations. Exercises. 1. Estimated activity base. 2. Underapplied. 3.

Chapter 17 Job Order Costing Study Guide Solutions Fill-in-the-Blank Equations 1. Estimated activity base 2. Underapplied 3. Overapplied Exercises 1. An automobile manufacturer produces various lines of

Chapter 17 Job Order Costing Study Guide Solutions Fill-in-the-Blank Equations 1. Estimated activity base 2. Underapplied 3. Overapplied Exercises 1. An automobile manufacturer produces various lines of

CHAPTER 17 PROCESS COSTING

CHAPTER 17 PROCESS COSTING TRUE/FALSE 1. Examples of industries that would use process costing include the pharmaceutical and semiconductor industry.. True process-costing system 1 The principal difference

CHAPTER 17 PROCESS COSTING TRUE/FALSE 1. Examples of industries that would use process costing include the pharmaceutical and semiconductor industry.. True process-costing system 1 The principal difference

Chapter 3 Systems Design: Job-Order Costing

Chapter 3 Systems Design: Job-Order Costing Solutions to Questions 3-1 By definition, manufacturing overhead consists of costs that cannot be practically traced to products or jobs. Therefore, if these

Chapter 3 Systems Design: Job-Order Costing Solutions to Questions 3-1 By definition, manufacturing overhead consists of costs that cannot be practically traced to products or jobs. Therefore, if these

ACCTG 221 / ABC Costing

ACCTG 221 / ABC Costing ACTIVITY BASED COSTING SYSTEMS First identifies activities in an organization and then assigns the cost of each activity to products and services based on actual consumption The

ACCTG 221 / ABC Costing ACTIVITY BASED COSTING SYSTEMS First identifies activities in an organization and then assigns the cost of each activity to products and services based on actual consumption The

Chapter 3 Activity-Based Costing

Chapter 3 -Based Costing Solutions to Questions 3-1 The most common methods of assigning overhead costs to products are plantwide overhead rates, departmental overhead rates, and activity-based costing.

Chapter 3 -Based Costing Solutions to Questions 3-1 The most common methods of assigning overhead costs to products are plantwide overhead rates, departmental overhead rates, and activity-based costing.

Chapter 7 Condensed (Day 1)

") Chapter 7 Condensed (Day 1) I. Valuing and Cost of Goods Sold (COGS) II. Costing Methods: Specific Identification, FIFO, LIFO, and Average Cost III. When managers use FIFO, LIFO, and Average Cost IV. Lower-of-Cost-or-Market

Chapter 7 Condensed (Day 1) I. Valuing and Cost of Goods Sold (COGS) II. Costing Methods: Specific Identification, FIFO, LIFO, and Average Cost III. When managers use FIFO, LIFO, and Average Cost IV. Lower-of-Cost-or-Market

CHAPTER 7 Accounting 1B. Activity-Based Costing(ABC): A tool to Aid Decision Making

: A tool to Aid Decision Making") CHAPTER 7 Accounting 1B Activity-Based Costing(ABC): A tool to Aid Decision Making Global Business Situation Using technology and productivity More emphasis on cost measurement and control Increasingly

CHAPTER 7 Accounting 1B Activity-Based Costing(ABC): A tool to Aid Decision Making Global Business Situation Using technology and productivity More emphasis on cost measurement and control Increasingly

Chapter 2--Measuring Product Costs

Chapter 2--Measuring Product Costs Student: 1. Which of the following is notone of the three major manufacturing cost categories? A. Direct materials costs that can be easily traced to a product B. Direct

Chapter 2--Measuring Product Costs Student: 1. Which of the following is notone of the three major manufacturing cost categories? A. Direct materials costs that can be easily traced to a product B. Direct

Costing for Jobs or Batces

Cost Accounting Acct 362/562 Costing for Jobs or Batces In an earlier time, units of a product were mass produced. Each was exactly like the others. In today s age, customization is the key. Products are

Cost Accounting Acct 362/562 Costing for Jobs or Batces In an earlier time, units of a product were mass produced. Each was exactly like the others. In today s age, customization is the key. Products are

Cost Accounting. Multiple Choice Questions:

Multiple Choice Questions: 1- The Value Chain a- Involves external companies as well as internal activities. b- Is the sequence of business functions in which customer usefulness is added to products or

Multiple Choice Questions: 1- The Value Chain a- Involves external companies as well as internal activities. b- Is the sequence of business functions in which customer usefulness is added to products or

1. Cost accounting involves the measuring, recording, and reporting of: A. product costs. B. future costs. C. manufacturing processes.

1. Cost accounting involves the measuring, recording, and reporting of: A. product costs. B. future costs. C. manufacturing processes. D. managerial accounting decisions. 2. In accumulating raw materials

1. Cost accounting involves the measuring, recording, and reporting of: A. product costs. B. future costs. C. manufacturing processes. D. managerial accounting decisions. 2. In accumulating raw materials

Chapter 02 - Cost Concepts and Cost Allocation

Chapter 02 - Cost Concepts and Cost Allocation Student: 1. Product costs for a manufacturing company consist of direct materials, direct labor, and overhead. 2. Period cost and product cost are synonymous

Chapter 02 - Cost Concepts and Cost Allocation Student: 1. Product costs for a manufacturing company consist of direct materials, direct labor, and overhead. 2. Period cost and product cost are synonymous

Part 1 Study Unit 5. Cost Accumulations Systems Jim Clemons, CMA Ronald Schmidt, CMA, CFM

Part 1 Study Unit 5 Cost Accumulations Systems Jim Clemons, CMA Ronald Schmidt, CMA, CFM 1 Overview Cost accounting systems record manufacturing activities using a perpetual inventory system, which continuously

Part 1 Study Unit 5 Cost Accumulations Systems Jim Clemons, CMA Ronald Schmidt, CMA, CFM 1 Overview Cost accounting systems record manufacturing activities using a perpetual inventory system, which continuously

Value Stream Mapping Train the Trainer

Value Stream Mapping Train the Trainer Information For A Process Data Box (to be collected on the shop floor) Cycle time Changeover time Process reliability (uptime) Scrap/Rework/Defect rate Number of

Value Stream Mapping Train the Trainer Information For A Process Data Box (to be collected on the shop floor) Cycle time Changeover time Process reliability (uptime) Scrap/Rework/Defect rate Number of

CHAPTER 8. Valuation of Inventories: A Cost-Basis Approach 1, 2, 3, 4, 5, 6, 7, 8, 11, 12, 14, 15, 16

CHAPTER 8 Valuation of Inventories: A Cost-Basis Approach ASSIGNMENT CLASSIFICATION TABLE (BY TOPIC) Topics Questions Brief Exercises Exercises Problems Concepts for Analysis 1. Inventory accounts; determining

CHAPTER 8 Valuation of Inventories: A Cost-Basis Approach ASSIGNMENT CLASSIFICATION TABLE (BY TOPIC) Topics Questions Brief Exercises Exercises Problems Concepts for Analysis 1. Inventory accounts; determining

Chapter 6 Process Costing

Chapter 6: Process Costing 239 Chapter 6 Process Costing LEARNING OBJECTIVES Chapter 6 addresses the following questions: LO1 LO2 LO3 LO4 LO5 Assign costs to mass-produced products using equivalent units

Chapter 6: Process Costing 239 Chapter 6 Process Costing LEARNING OBJECTIVES Chapter 6 addresses the following questions: LO1 LO2 LO3 LO4 LO5 Assign costs to mass-produced products using equivalent units

Chapter 2. Job Order Costing and Analysis QUESTIONS

Chapter 2 Job Order Costing and Analysis QUESTIONS 1. Factory overhead is not identified with specific units (jobs) or batches (job lots). Therefore, to assign costs, estimates of the relation between

Chapter 2 Job Order Costing and Analysis QUESTIONS 1. Factory overhead is not identified with specific units (jobs) or batches (job lots). Therefore, to assign costs, estimates of the relation between

Basic Cost Management Concepts. M. En C. Eduardo Bustos as

Basic Cost Management Concepts M. En C. Eduardo Bustos Farías as 1 Objectives 1. Explain what is meant by the word "cost." 2. Distinguish among product costs, period costs,, and expenses. 3. Describe the

Basic Cost Management Concepts M. En C. Eduardo Bustos Farías as 1 Objectives 1. Explain what is meant by the word "cost." 2. Distinguish among product costs, period costs,, and expenses. 3. Describe the

Dynamics AX 2012 Trade & Logistics

Dynamics AX 2012 Trade & Logistics COURSE OVERIEW About this Course Supply Chain Foundation in Microsoft Dynamics AX 2012, provides students with the necessary tools and resources to perform basic tasks

Dynamics AX 2012 Trade & Logistics COURSE OVERIEW About this Course Supply Chain Foundation in Microsoft Dynamics AX 2012, provides students with the necessary tools and resources to perform basic tasks

Inventory Cost Accounting Tips and Tricks. Nick Bergamo, Senior Manager Linda Pei, Senior Manager

1 Inventory Cost Accounting Tips and Tricks Nick Bergamo, Senior Manager Linda Pei, Senior Manager 2 Disclaimer The material appearing in this presentation is for informational purposes only and is not

1 Inventory Cost Accounting Tips and Tricks Nick Bergamo, Senior Manager Linda Pei, Senior Manager 2 Disclaimer The material appearing in this presentation is for informational purposes only and is not

Financial Accounting Chapter 6 Notes Inventories

Financial Accounting Notes Inventories I. Management Issues Associated with Accounting with Inventory. Defining Inventory: 1. Assets held for resale purpose in a normal course of business. (Current Asset)

Financial Accounting Notes Inventories I. Management Issues Associated with Accounting with Inventory. Defining Inventory: 1. Assets held for resale purpose in a normal course of business. (Current Asset)

B.COM 2 PRIVATE COST ACCOUNTING. B.com-2 PRIVATE Annual Examination COMPILED & SOLVED BY: Jahangeer Khan

B.COM 2 PRIVATE COST ACCOUNTING B.com-2 PRIVATE Annual Examination 20 COMPILED & SOLVED BY: Jahangeer Khan 20 Q.1: MANUFACTURING CONCERN: Consider the following information taken from the books of SAHAB

B.COM 2 PRIVATE COST ACCOUNTING B.com-2 PRIVATE Annual Examination 20 COMPILED & SOLVED BY: Jahangeer Khan 20 Q.1: MANUFACTURING CONCERN: Consider the following information taken from the books of SAHAB

Chapter Outline. Study Objective 1 - Describe the Steps in Determining Inventory Quantities

Chapter 6 Financial Notes and BE Chapter Outline Study Objective 1 - Describe the Steps in Determining Inventory Quantities In a merchandising company, inventory consists of many different items. These

Chapter 6 Financial Notes and BE Chapter Outline Study Objective 1 - Describe the Steps in Determining Inventory Quantities In a merchandising company, inventory consists of many different items. These

MBP1133 Managerial Accounting Prepared by Dr Khairul Anuar

1 MBP1133 Managerial Accounting Prepared by Dr Khairul Anuar L8 Activity-Based Costing: A Tool to Aid Decision Making www.notes638.wordpress.com 2 Activity Based Costing (ABC) ABC is designed to provide

1 MBP1133 Managerial Accounting Prepared by Dr Khairul Anuar L8 Activity-Based Costing: A Tool to Aid Decision Making www.notes638.wordpress.com 2 Activity Based Costing (ABC) ABC is designed to provide

An Introduction to Cost terms and Purposes. Session 2

An Introduction to Cost terms and Purposes Session 2 Learning Objectives Define and illustrate a cost object Distinguish between direct costs and indirect costs Explain variable costs and fixed costs Interpret

An Introduction to Cost terms and Purposes Session 2 Learning Objectives Define and illustrate a cost object Distinguish between direct costs and indirect costs Explain variable costs and fixed costs Interpret

1. F; I 2. V ; D 3. V ; D 4. F; I 5. F; I 6. F; I 7. V ; D 8. F; I 9. F; I 10. V ; D 11. F; I 12. F; I 13. F; I 14. F; I

SOLUTIONS TO EERCISES EERCISE 2-1 (15 minutes) 1. F; I 2. V ; D 3. V ; D 4. F; I 5. F; I 6. F; I 7. V ; D 8. F; I 9. F; I 10. V ; D 11. F; I 12. F; I 13. F; I 14. F; I EERCISE 2-2 (15 minutes) 1. Product

SOLUTIONS TO EERCISES EERCISE 2-1 (15 minutes) 1. F; I 2. V ; D 3. V ; D 4. F; I 5. F; I 6. F; I 7. V ; D 8. F; I 9. F; I 10. V ; D 11. F; I 12. F; I 13. F; I 14. F; I EERCISE 2-2 (15 minutes) 1. Product

An Introduction to Cost Terms and Purposes. Dr. Osama Al Meanazel

An Introduction to Cost Terms and Purposes Dr. Osama Al Meanazel Lecture 5 Other Cost Concepts Cost driver a variable that causally affects costs over a given time span Relevant range the band of normal

An Introduction to Cost Terms and Purposes Dr. Osama Al Meanazel Lecture 5 Other Cost Concepts Cost driver a variable that causally affects costs over a given time span Relevant range the band of normal

1. The following data pertains to activity and utility cost for two recent periods:

Student ID: 22036501 Exam: 061400RR - Cost Concepts and Types of Costing When you have completed your exam and reviewed your answers, click Submit Exam. Answers will not be recorded until you hit Submit

Student ID: 22036501 Exam: 061400RR - Cost Concepts and Types of Costing When you have completed your exam and reviewed your answers, click Submit Exam. Answers will not be recorded until you hit Submit

CHAPTER 6 PROCESS COSTING. 1. Which cost accumulation procedure is most applicable in continuous mass-production manufacturing environments?

CHAPTER 6 PROCESS COSTING MULTIPLE CHOICE 1. Which cost accumulation procedure is most applicable in continuous mass-production manufacturing environments? a. standard b. actual c. process d. job order

CHAPTER 6 PROCESS COSTING MULTIPLE CHOICE 1. Which cost accumulation procedure is most applicable in continuous mass-production manufacturing environments? a. standard b. actual c. process d. job order

Welcome to the topic on purchasing items.

Welcome to the topic on purchasing items. 1 In this topic, we will perform the basic steps for purchasing items. As we go through the process, we will explain the consequences of each process step on inventory

Welcome to the topic on purchasing items. 1 In this topic, we will perform the basic steps for purchasing items. As we go through the process, we will explain the consequences of each process step on inventory

Trade and Logistics II in Microsoft Dynamics AX 2009 Course 80025A: 3 Days; Instructor-Led

Trade and Logistics II in Microsoft Dynamics AX 2009 Course 80025A: 3 Days; Instructor-Led About this Course The two-day Microsoft Dynamics AX 2009 Trade & Logistics II, course introduces advanced Trade

Trade and Logistics II in Microsoft Dynamics AX 2009 Course 80025A: 3 Days; Instructor-Led About this Course The two-day Microsoft Dynamics AX 2009 Trade & Logistics II, course introduces advanced Trade

KPI ENCYCLOPEDIA. A Comprehensive Collection of KPI Definitions for. Supply Chain

KPI ENCYCLOPEDIA A Comprehensive Collection of KPI Definitions for Supply Chain w w w. o p s d o g. c o m info@opsdog.com 844.650.2888 Table of Contents Supply Chain KPI Encyclopedia Supply Chain Metric

KPI ENCYCLOPEDIA A Comprehensive Collection of KPI Definitions for Supply Chain w w w. o p s d o g. c o m info@opsdog.com 844.650.2888 Table of Contents Supply Chain KPI Encyclopedia Supply Chain Metric

CHAPTER 5: MERCHANDISING OPERATIONS

CHAPTER 5: MERCHANDISING OPERATIONS CHAPTER SYNOPSIS Chapter 5 first compares a service business with a merchandising business and then discusses the purchase and sale of merchandise inventory. The chapter

CHAPTER 5: MERCHANDISING OPERATIONS CHAPTER SYNOPSIS Chapter 5 first compares a service business with a merchandising business and then discusses the purchase and sale of merchandise inventory. The chapter

Welcome to the topic on warehouses.

Welcome to the topic on warehouses. In this topic, we will discuss the importance of warehouses in the business processes. We will create a warehouse and view the available options. We take a quick look

Welcome to the topic on warehouses. In this topic, we will discuss the importance of warehouses in the business processes. We will create a warehouse and view the available options. We take a quick look

An Introduction to Cost Terms and Purposes

CHAPTER 2 An Introduction to Cost Terms and Purposes Overview This chapter introduces the basic terminology of cost accounting. Communication among managers and management accountants is greatly facilitated

CHAPTER 2 An Introduction to Cost Terms and Purposes Overview This chapter introduces the basic terminology of cost accounting. Communication among managers and management accountants is greatly facilitated

CHAPTER 2. Job Order Costing 1, 2, 3, 4 5, 6, 7, 8 1, 2, 3, 4

CHAPTER 2 Job Order Costing ASSIGNMENT CLASSIFICATION TABLE Study Objectives Questions Brief Exercises Do It! Exercises A Problems B Problems 1. Explain the characteristics and purposes of cost accounting.

CHAPTER 2 Job Order Costing ASSIGNMENT CLASSIFICATION TABLE Study Objectives Questions Brief Exercises Do It! Exercises A Problems B Problems 1. Explain the characteristics and purposes of cost accounting.

Spoilage, Rework, and Scrap

18 Spoilage, Rework, and Scrap Learning Objectives 1. Understand the definitions of spoilage, rework, and scrap 2. Identify the differences between normal and abnormal spoilage 3. Account for spoilage

18 Spoilage, Rework, and Scrap Learning Objectives 1. Understand the definitions of spoilage, rework, and scrap 2. Identify the differences between normal and abnormal spoilage 3. Account for spoilage

MGACO1 INTERMEDIATE ACCOUNTING I

MGACO1 INTERMEDIATE ACCOUNTING I S. Daga Topic: INVENTORY TEXT: Chapter 8 (excl. appendix) TEXT QUESTIONS: E8-11, E8-22, P8-3, Case IC8-1 LEARNING GOALS: 1. RECOGNITION - Understand key inventory concerns.

MGACO1 INTERMEDIATE ACCOUNTING I S. Daga Topic: INVENTORY TEXT: Chapter 8 (excl. appendix) TEXT QUESTIONS: E8-11, E8-22, P8-3, Case IC8-1 LEARNING GOALS: 1. RECOGNITION - Understand key inventory concerns.

OPERATIONAL AND CONSUMABLE INVENTORY POLICY

OPERATIONAL AND CONSUMABLE INVENTORY POLICY PURPOSE The purpose of this policy is to establish guidelines for the management of inventory as a key institutional resource. This policy lays the foundation

OPERATIONAL AND CONSUMABLE INVENTORY POLICY PURPOSE The purpose of this policy is to establish guidelines for the management of inventory as a key institutional resource. This policy lays the foundation

FFQA 1. Complied by: Mohammad Faizan Farooq Qadri Attari ACCA (Finalist) Contact:

Contact:") FFQA 1 Objective of IAS 2 The objective of IAS 2 is to prescribe the accounting treatment for inventories. It provides guidance for determining the cost of inventories and for subsequently recognising

FFQA 1 Objective of IAS 2 The objective of IAS 2 is to prescribe the accounting treatment for inventories. It provides guidance for determining the cost of inventories and for subsequently recognising

QuickBooks Online Student Guide. Chapter 10. Inventory

QuickBooks Online Student Guide Chapter 10 Inventory Chapter 2 Chapter 10 In this chapter, you ll learn how QuickBooks handles inventory. You can use QuickBooks to track the items you keep in inventory

QuickBooks Online Student Guide Chapter 10 Inventory Chapter 2 Chapter 10 In this chapter, you ll learn how QuickBooks handles inventory. You can use QuickBooks to track the items you keep in inventory

CEBU CPAR CENTER. M a n d a u e C I t y

Page 1 of 9 CEBU CPAR CENTER M a n d a u e C I t y AUDITING PROBLEMS AUDIT OF INVENTORIES PROBLEM NO. 1 The Pasay Company is a wholesale distributor of automobile replacement parts. Initial amounts taken

Page 1 of 9 CEBU CPAR CENTER M a n d a u e C I t y AUDITING PROBLEMS AUDIT OF INVENTORIES PROBLEM NO. 1 The Pasay Company is a wholesale distributor of automobile replacement parts. Initial amounts taken

Activity Based Costing: A Decision Making Tool. with Dr. Joseph Ugras December 2017

Activity Based Costing: A Decision Making Tool with Dr. Joseph Ugras December 2017 1 7-2 Learning Objectives Know the Need for Cost and Profitability Understand how traditional and activity-based costing

Activity Based Costing: A Decision Making Tool with Dr. Joseph Ugras December 2017 1 7-2 Learning Objectives Know the Need for Cost and Profitability Understand how traditional and activity-based costing

QMRP Base System. Highlights:

The QMRP Base System consists of the menu and security systems, inventory control, product structure processing, product costing, and manufacturing order processing. Additional functionality is provided

The QMRP Base System consists of the menu and security systems, inventory control, product structure processing, product costing, and manufacturing order processing. Additional functionality is provided

Process Costing. Created by Rex A Schildhouse, Slide 2

Accounting presentation created by Rex A Schildhouse 2015-01-01 www.schildhouse.com Created by Rex A Schildhouse, www.schildhouse.com Slide 1 Process costing works with departments manufacturing homogenous

Accounting presentation created by Rex A Schildhouse 2015-01-01 www.schildhouse.com Created by Rex A Schildhouse, www.schildhouse.com Slide 1 Process costing works with departments manufacturing homogenous

CA IPC ASSIGNMENT MATERIAL, MARGINAL COSTING & BUDGETARY CONTROL

CA IPC ASSIGNMENT MATERIAL, MARGINAL COSTING & BUDGETARY CONTROL MM: 87 Marks Question 1: Arnav Udyog, a small scale manufacturer, produces a product X by using two raw materials A and B in the ratio of

CA IPC ASSIGNMENT MATERIAL, MARGINAL COSTING & BUDGETARY CONTROL MM: 87 Marks Question 1: Arnav Udyog, a small scale manufacturer, produces a product X by using two raw materials A and B in the ratio of

Online Course Manual By Craig Pence. Module 12

Online Course Manual By Craig Pence Copyright Notice. Each module of the course manual may be viewed online, saved to disk, or printed (each is composed of 10 to 15 printed pages of text) by students enrolled

Online Course Manual By Craig Pence Copyright Notice. Each module of the course manual may be viewed online, saved to disk, or printed (each is composed of 10 to 15 printed pages of text) by students enrolled

Akuntansi Biaya. Modul ke: 09FEB. Direct Material Cost. Fakultas. Diah Iskandar SE., M.Si dan Nurul Hidayah,SE,Ak,MSi. Program Studi Akuntansi

Modul ke: Akuntansi Biaya Direct Material Cost Fakultas 09FEB Diah Iskandar SE., M.Si dan Nurul Hidayah,SE,Ak,MSi Program Studi Akuntansi Effective Cost Control Specific assignment of duties and responsibilities.

Modul ke: Akuntansi Biaya Direct Material Cost Fakultas 09FEB Diah Iskandar SE., M.Si dan Nurul Hidayah,SE,Ak,MSi Program Studi Akuntansi Effective Cost Control Specific assignment of duties and responsibilities.

Financial Accounting. John J. Wild. Sixth Edition. Copyright 2013 by The McGraw-Hill Companies, Inc. All rights reserved.

Financial Accounting John J. Wild Sixth Edition McGraw-Hill/Irwin Copyright 2013 by The McGraw-Hill Companies, Inc. All rights reserved. Chapter 04 Reporting and Analyzing Merchandising Operations Conceptual

Financial Accounting John J. Wild Sixth Edition McGraw-Hill/Irwin Copyright 2013 by The McGraw-Hill Companies, Inc. All rights reserved. Chapter 04 Reporting and Analyzing Merchandising Operations Conceptual

CHAPTER 6. Inventories ASSIGNMENT CLASSIFICATION TABLE For Instructor Use Only 6-1. Brief. B Problems. A Problems 1, 2, 3, 4, 5

CHAPTER 6 Inventories ASSIGNMENT CLASSIFICATION TABLE Study Objectives Questions Brief Exercises Exercises A Problems B Problems 1. Describe the steps in determining inventory quantities. 1, 2, 3, 4, 5

CHAPTER 6 Inventories ASSIGNMENT CLASSIFICATION TABLE Study Objectives Questions Brief Exercises Exercises A Problems B Problems 1. Describe the steps in determining inventory quantities. 1, 2, 3, 4, 5

ODE Child Nutrition Programs. Commodity Food Distribution Program Terminology

ODE Child Nutrition Programs Commodity Food Distribution Program Terminology Agencies State Agency (SA) The Oregon Department of Education enters into an agreement with USDA for the distribution of commodities

ODE Child Nutrition Programs Commodity Food Distribution Program Terminology Agencies State Agency (SA) The Oregon Department of Education enters into an agreement with USDA for the distribution of commodities

6) Items purchased for resale with a right of return must be presented separately from other inventories.

Items purchased for resale with a right of return must be presented separately from other inventories.") Chapter 8 Cost-based Inventories and Cost of Sales 1) Inventories are assets consisting of goods owned by the business and held for future sale or for use in the manufacture of goods for sale. Answer:

Chapter 8 Cost-based Inventories and Cost of Sales 1) Inventories are assets consisting of goods owned by the business and held for future sale or for use in the manufacture of goods for sale. Answer:

Week 4 Chapter 4 MATERIALS COSTING. FNSACC507A Provide Management Accounting Information

Week 4 Chapter 4 MATERIALS COSTING FNSACC507A Provide Management Accounting Information In this lesson you will learn 1. About the documents used to cost and control factory materials. 2. How to prepare

Week 4 Chapter 4 MATERIALS COSTING FNSACC507A Provide Management Accounting Information In this lesson you will learn 1. About the documents used to cost and control factory materials. 2. How to prepare

C H A P T E R. Inventories. Corporate Financial Accounting 13e. human/istock/360/getty Images. Warren Reeve Duchac

C H A P T E R 6 Inventories Corporate Financial Accounting 13e Warren Reeve Duchac human/istock/360/getty Images Safeguarding Inventory (slide 1 of 2) Controls for safeguarding inventory begin as soon

C H A P T E R 6 Inventories Corporate Financial Accounting 13e Warren Reeve Duchac human/istock/360/getty Images Safeguarding Inventory (slide 1 of 2) Controls for safeguarding inventory begin as soon

CHAPTER 6. Inventories 12, 13, , , 11 16, , 13

CHAPTER 6 Inventories ASSIGNMENT CLASSIFICATION TABLE Study Objectives Questions Brief Exercises Do It! Exercises A Problems B Problems 1. Describe the steps in determining inventory quantities. 1, 2,

CHAPTER 6 Inventories ASSIGNMENT CLASSIFICATION TABLE Study Objectives Questions Brief Exercises Do It! Exercises A Problems B Problems 1. Describe the steps in determining inventory quantities. 1, 2,

Chapter One Introduction to Inventory

Chapter One Introduction to Inventory This chapter introduces Inventory, its features, the organization of the User s Guide, common toolbar buttons and frequently used keyboard and report commands. Introduction...

Chapter One Introduction to Inventory This chapter introduces Inventory, its features, the organization of the User s Guide, common toolbar buttons and frequently used keyboard and report commands. Introduction...

Accounting Information Systems, 12e (Romney/Steinbart) Chapter 14 The Production Cycle

Chapter 14 The Production Cycle") Accounting Information Systems, 12e (Romney/Steinbart) Chapter 14 The Production Cycle 1) The AIS compiles and feeds information among the business cycles. What is the relationship between the revenue

Accounting Information Systems, 12e (Romney/Steinbart) Chapter 14 The Production Cycle 1) The AIS compiles and feeds information among the business cycles. What is the relationship between the revenue

1). Fixed cost per unit decreases when:

. Fixed cost per unit decreases when:") 1). Fixed cost per unit decreases when: a. Production volume increases. b. Production volume decreases. c. Variable cost per unit decreases. d. Variable cost per unit increases. 2). Prime cost + Factory

1). Fixed cost per unit decreases when: a. Production volume increases. b. Production volume decreases. c. Variable cost per unit decreases. d. Variable cost per unit increases. 2). Prime cost + Factory

*Brief Exercise

*Brief Exercise 19-1 0 Presented below are incomplete manufacturing cost data. Determine the missing amounts for three different situations. Direct Materials Used Direct Labor Used Factory Overhead (a)

*Brief Exercise 19-1 0 Presented below are incomplete manufacturing cost data. Determine the missing amounts for three different situations. Direct Materials Used Direct Labor Used Factory Overhead (a)

Activity-Based Costing. Managerial Accounting, Fourth Edition

Study Objectives Study CHAPTER Objectives 4 Activity-Based Costing Managerial Accounting, Fourth Edition Study Objectives 1. Recognize the difference between traditional costing and activity based costing.

Study Objectives Study CHAPTER Objectives 4 Activity-Based Costing Managerial Accounting, Fourth Edition Study Objectives 1. Recognize the difference between traditional costing and activity based costing.

Fundamentals of Product and Service Costing:

Fundamentals of Product and Service Costing: Demonstration Problems 1 Demonstration Problem 1 In the first quarter of operation, the Blending Department of ChemUSA produced 50,000 barrels of Compound X

Fundamentals of Product and Service Costing: Demonstration Problems 1 Demonstration Problem 1 In the first quarter of operation, the Blending Department of ChemUSA produced 50,000 barrels of Compound X

Acct 1B Week 8, Chap 7

Acct 1B Week 8, Chap 7 Activity Based Costing (ABC) Instructor: Michael Booth Cabrillo College Activity Based Costing: A Tool to Aid Decision Making Global Business Situation Using technology and productivity

Acct 1B Week 8, Chap 7 Activity Based Costing (ABC) Instructor: Michael Booth Cabrillo College Activity Based Costing: A Tool to Aid Decision Making Global Business Situation Using technology and productivity

Problem Exercise 3-12

Exercise 3-12 1. The overhead applied to Ms. Miyami s account would be computed as follows: 2002 2001 Estimated overhead cost (a)... $144,000 $144,000 Estimated professional staff hours (b)... 2,250 2,400

Exercise 3-12 1. The overhead applied to Ms. Miyami s account would be computed as follows: 2002 2001 Estimated overhead cost (a)... $144,000 $144,000 Estimated professional staff hours (b)... 2,250 2,400

Warehouse and Production Management with SAP Business One

SAP Product Brief SAP s for Small Businesses and Midsize Companies SAP Business One Objectives Warehouse and Production Management with SAP Business One Real-time inventory and production management Real-time

SAP Product Brief SAP s for Small Businesses and Midsize Companies SAP Business One Objectives Warehouse and Production Management with SAP Business One Real-time inventory and production management Real-time

Job Costing. Costing Systems. After studying this chapter, you should be able to...

C H A P T E R F O U R Job Costing After studying this chapter, you should be able to.... Explain the types of costing systems. Explain the strategic role of costing 3. Explain the flow of costs in a job

C H A P T E R F O U R Job Costing After studying this chapter, you should be able to.... Explain the types of costing systems. Explain the strategic role of costing 3. Explain the flow of costs in a job

Why Fishbowl Manufacturing and Fishbowl Warehouse Are #1 Among QuickBooks Users

Why Fishbowl Manufacturing and Fishbowl Warehouse Are #1 Among QuickBooks Users Fishbowl is the most popular manufacturing and warehouse management software for QuickBooks users. Fishbowl Manufacturing

Why Fishbowl Manufacturing and Fishbowl Warehouse Are #1 Among QuickBooks Users Fishbowl is the most popular manufacturing and warehouse management software for QuickBooks users. Fishbowl Manufacturing

Activity-Based Costing and Analysis

A Look Back Chapters 2 and 3 described costing systems used by companies to accumulate product costing information for the reporting of inventories and cost of goods sold. 4Chapter Learning Objectives

A Look Back Chapters 2 and 3 described costing systems used by companies to accumulate product costing information for the reporting of inventories and cost of goods sold. 4Chapter Learning Objectives

Chapter 7: Merchandise Inventory

1 Chapter 7: Merchandise Inventory 2 3 Merchandise Inventory What is inventory? Items held for resale to customers Who has inventory? Wholesaler or Retailer - Merchandise Inventory Manufacturer - Raw Materials

1 Chapter 7: Merchandise Inventory 2 3 Merchandise Inventory What is inventory? Items held for resale to customers Who has inventory? Wholesaler or Retailer - Merchandise Inventory Manufacturer - Raw Materials

NCR Counterpoint. Reports Handbook

NCR Counterpoint Reports Handbook Copyright 1995 2011 by Radiant Systems, Inc. PROPRIETARY RIGHTS NOTICE: All rights reserved. No part of this material may be reproduced or transmitted in any form or by

NCR Counterpoint Reports Handbook Copyright 1995 2011 by Radiant Systems, Inc. PROPRIETARY RIGHTS NOTICE: All rights reserved. No part of this material may be reproduced or transmitted in any form or by

2. Standard costs imply a) Predetermined cost for a period b) Incurred cost c) Conversion cost d) Incremental cost

Predetermined cost for a period b) Incurred cost c) Conversion cost d) Incremental cost") QUESTION BANK PAPER: COST ACCOUNTING COURSE: B.Com (Semester IV) MCQs 1. The basic objective of cost accounting is a) Recording of cost b) Reporting of cost c) Cost control d) EarningProfit 2. Standard

QUESTION BANK PAPER: COST ACCOUNTING COURSE: B.Com (Semester IV) MCQs 1. The basic objective of cost accounting is a) Recording of cost b) Reporting of cost c) Cost control d) EarningProfit 2. Standard

Microsoft Dynamics GP2010 Inventory Year-End Closing Checklist

Microsoft Dynamics GP2010 Inventory Year-End Closing Checklist Inventory Control Year End Closing What happens when I close the year on Dynamics GP 2010? Transfers all summarized current-year quantity,

Microsoft Dynamics GP2010 Inventory Year-End Closing Checklist Inventory Control Year End Closing What happens when I close the year on Dynamics GP 2010? Transfers all summarized current-year quantity,

Management s Accountability to Stakeholders Stakeholders Provide Management is accountable for: Owners Operating activities Government Creditors

Chapter 15 Distinguish management accounting from financial accounting Management Management s Accountability to Stakeholders Stakeholders Owners Government Provide Management is accountable for: Operating

Chapter 15 Distinguish management accounting from financial accounting Management Management s Accountability to Stakeholders Stakeholders Owners Government Provide Management is accountable for: Operating

Visual Cash Focus - User Tip 32

Visual Cash Focus - User Tip 32 How do I model Work in Progress and Finished Goods? How to model WIP in service based organisations How to model WIP and Finished Goods for manufacturers and producers The

Visual Cash Focus - User Tip 32 How do I model Work in Progress and Finished Goods? How to model WIP in service based organisations How to model WIP and Finished Goods for manufacturers and producers The

MANAGEMENT 9 ACCOUNTING

9-1 9-2 Chapter MANAGEMENT 9 ACCOUNTING A BUSINESS PARTNER To explain the three principles guiding the design of management accounting systems. LO1 Management Accounting: Basic Framework 9-3 Management

9-1 9-2 Chapter MANAGEMENT 9 ACCOUNTING A BUSINESS PARTNER To explain the three principles guiding the design of management accounting systems. LO1 Management Accounting: Basic Framework 9-3 Management

CHAPTER 4 ACCOUNTING FOR MERCHANDISING OPERATIONS

CHAPTER 4 ACCOUNTING FOR MERCHANDISING OPERATIONS Key Terms and Concepts to Know Income Statements: Single-step income statement Multiple-step income statement Gross Margin = Gross Profit = Net Sales Cost

CHAPTER 4 ACCOUNTING FOR MERCHANDISING OPERATIONS Key Terms and Concepts to Know Income Statements: Single-step income statement Multiple-step income statement Gross Margin = Gross Profit = Net Sales Cost

Module 10 : Product and Process Costing. Lecture 1 : Product and Process Costing. Objectives

Module 10 : Product and Process Costing Lecture 1 : Product and Process Costing Objectives In this lecture you will learn the following Introduction. Product costing. Job costing. Process costing. Cost

Module 10 : Product and Process Costing Lecture 1 : Product and Process Costing Objectives In this lecture you will learn the following Introduction. Product costing. Job costing. Process costing. Cost

Chapter 20: Job Order Costing

Chapter 20: Job Order Costing DO IT! 1 Accumulating Manufacturing Costs During the current month, Ringling Company incurs the following manufacturing costs: (a) Raw material purchases of $4,200 on account.

Chapter 20: Job Order Costing DO IT! 1 Accumulating Manufacturing Costs During the current month, Ringling Company incurs the following manufacturing costs: (a) Raw material purchases of $4,200 on account.

Heintz & Parry. 20 th Edition. College Accounting

Heintz & Parry 20 th Edition College Accounting Chapter 13 Accounting for Merchandise Inventory 1 Explain the impact of merchandise inventory on the financial statements. Errors in inventory will cause

Heintz & Parry 20 th Edition College Accounting Chapter 13 Accounting for Merchandise Inventory 1 Explain the impact of merchandise inventory on the financial statements. Errors in inventory will cause

Acct 2301 (Spring 2006) - Exam 3

- Exam 3") Acct 2301 (Spring 2006) - Exam 3 Student: 1. During 2005, Truman Company incurred manufacturing costs of $40,000 to work on and complete 10,000 gizmos. The company sold 8,000 of the gizmos during the year.

Acct 2301 (Spring 2006) - Exam 3 Student: 1. During 2005, Truman Company incurred manufacturing costs of $40,000 to work on and complete 10,000 gizmos. The company sold 8,000 of the gizmos during the year.

Exercise E21-1 page 886. (a) Factory Labor 103,000 Factory Wages Payable 90,000 Employer Payroll Taxes Payable 9,000

Factory Labor 103,000 Factory Wages Payable 90,000 Employer Payroll Taxes Payable 9,000") Exercise E21-1 page 886 (a) Factory Labor 103,000 Factory Wages Payable 90,000 Employer Payroll Taxes Payable 9,000 Employer Fringe Benefits Payable 4,000 (b) Work in Process Inventory 87,550 Manufacturing

Exercise E21-1 page 886 (a) Factory Labor 103,000 Factory Wages Payable 90,000 Employer Payroll Taxes Payable 9,000 Employer Fringe Benefits Payable 4,000 (b) Work in Process Inventory 87,550 Manufacturing

Overview. 1. Basinger vs Main Line 2. Terminology 3. Cost Drivers 4. Breakeven Analysis 5. Other problems 6. Summary

Overview 1. Basinger vs Main Line 2. Terminology 3. Cost Drivers 4. Breakeven Analysis 5. Other problems 6. Summary 1 Basinger vs Mainline To read the Basinger vs. Mainline case, see: Barton, Thomas L.,

Overview 1. Basinger vs Main Line 2. Terminology 3. Cost Drivers 4. Breakeven Analysis 5. Other problems 6. Summary 1 Basinger vs Mainline To read the Basinger vs. Mainline case, see: Barton, Thomas L.,

CHAPTER 8. Valuation of Inventories: A Cost-Basis Approach 1, 2, 3, 4, 5, 6, 8, Perpetual vs. periodic. 2 9, 13, 14, 17, 20

CHAPTER 8 Valuation of Inventories: A Cost-Basis Approach ASSIGNMENT CLASSIFICATION TABLE (BY TOPIC) Topics Questions Brief Exercises Exercises Problems Concepts for Analysis 1. Inventory accounts; determining

CHAPTER 8 Valuation of Inventories: A Cost-Basis Approach ASSIGNMENT CLASSIFICATION TABLE (BY TOPIC) Topics Questions Brief Exercises Exercises Problems Concepts for Analysis 1. Inventory accounts; determining

Inventory and Labor. Fast Casual Solution. Back Office. Example Reports Version Cash Management. Forecast Engine.

Back Office Inventory and Labor Cash Management Inventory / Purchasing Labor Management Forecast Engine System Reporting Fast Casual Solution Example Reports Version 12.3 Inventory and Labor Cash and Sales

Back Office Inventory and Labor Cash Management Inventory / Purchasing Labor Management Forecast Engine System Reporting Fast Casual Solution Example Reports Version 12.3 Inventory and Labor Cash and Sales

Special Customer Pricing

Special Customer Pricing Create Special Price Automatically calculate customer price with rack + markup + other. Add freight to the price or bill freight as a separate line item. Example above has GASFRT

Special Customer Pricing Create Special Price Automatically calculate customer price with rack + markup + other. Add freight to the price or bill freight as a separate line item. Example above has GASFRT

Universidad Tecnológica de Coahuila

Universidad Tecnológica de Coahuila Production Cost Accounting Class Presented by: Lic. Celina A. Fernandez Jimenez December 11, 2013 OBJECTIVES: General Objective: To know the basic tools used by cost

Universidad Tecnológica de Coahuila Production Cost Accounting Class Presented by: Lic. Celina A. Fernandez Jimenez December 11, 2013 OBJECTIVES: General Objective: To know the basic tools used by cost

Accounting Overview. Presented by: Marisa Krieg

Accounting Overview Presented by: Marisa Krieg Agenda: Disclaimer Basic Concepts Common Functions Time Savers & Helpful Links Q&A Disclaimer Disclaimer The intent of today s presentation is solely to advise

Accounting Overview Presented by: Marisa Krieg Agenda: Disclaimer Basic Concepts Common Functions Time Savers & Helpful Links Q&A Disclaimer Disclaimer The intent of today s presentation is solely to advise

Chapter 2 An Introduction to Cost Terms and Purposes

Chapter 2 An Introduction to Cost Terms and Purposes Copyright 2003 Pearson Education Canada Inc. Slide 2-15 Costs and Cost Objects Cost a resource sacrificed or foregone to achieve a specific objective

Chapter 2 An Introduction to Cost Terms and Purposes Copyright 2003 Pearson Education Canada Inc. Slide 2-15 Costs and Cost Objects Cost a resource sacrificed or foregone to achieve a specific objective