Shippers Meeting. Hoofddorp, 27 May 2015

|

|

|

- Hugo Gregory

- 5 years ago

- Views:

Transcription

1 Shippers Meeting Hoofddorp, 27 May 2015

2 Programme 11:00 13:00 13:00 14:00 14:00 19:00 Plenary session Lunch including individual consults Social event

3 Agenda plenary session The Evolution of European Gas Hubs Patrick Heather The European Network Codes Peter Schultz Auction Results PRISMA Diederik Top Miscellaneous Dewi Telehala

4 PatrickHeatherConsultancy The Evolution of European Gas Hubs Gasunie Transport Services Shippers Meeting Amsterdam, 27 th May, 2015 The contents of this presentation are subject to PHCL copyright. This presentation may not be reproduced in whole or in part without the written permission of Patrick Heather, PHCL, Lulworth, Longfield Road, Twyford, READING RG10 9AT Tel: Mobile: Patrick Heather Consultancy Limited

5 Outline Wholesale markets Terminology and Market Pricing The development of gas exchanges The European gas exchanges and their role A comparison of EU hubs European gas hubs and trading data Setting the scene The 5 Key Elements Summary and Conclusion 2015 Patrick Heather Consultancy Limited 2

6 Wholesale markets Gas contract price formation 2015 Patrick Heather Consultancy Limited 3

7 Terminology Traded gas: Gas traded at the hubs, whether for physical delivery or for financial hedging or for speculative reasons Usually a standard product, either OTC or exchange Usually for spot, prompt or near to mid curve maturity In Britain, about 50% of consumed gas is (net) traded And, about 20 times consumption is (gross) traded: churn Contracted gas: Gas traded or contracted bilaterally, for delivery at a hub Can be of a standard product or bespoke Can be of any time duration, often medium to long term In Britain, about 50% of consumed gas is contracted There is no churn Gas Exchanged at a hub: Gas physically nominated and delivered at a hub There is much confusion in the use of these three terms 2015 Patrick Heather Consultancy Limited 4

8 Market pricing Separates the financial from the physical Usually flat gas volumes Allows for separate financial risk management Provides the right gas price at any given time Open and transparent Can apply to contracts of any length Increasing demand for market pricing Seller and buyer can each choose when to hedge Seller & buyer can each choose how much to hedge Market pricing is gradually gaining ground in Continental Europe but fully mature, liquid hubs essential to enable transition 2015 Patrick Heather Consultancy Limited 5

9 The development of gas exchanges European gas exchanges and their role 2015 Patrick Heather Consultancy Limited 6

10 Exchange function Risk Management Providing a facility for managing price risk through a secure and regulated market hedging and trading Price Transparency The ability to know the price of gas now and in the future (up to six years ahead on ICE NBP and five years for ICE-Endex TTF) Supply/Pricing flexibility The ability to separate price function from supply function Physical balancing Providing a market place for the buying and selling of, usually, marginal quantities of physical gas 2015 Patrick Heather Consultancy Limited 7

11 The gas exchanges volumes Futures Spot ICE/Endex EEX PNXT CEGH GME Totals ICE/Endex EEX PNXT CEGH GME ICE/Endex futures ICE/Endex spot EEX futures EEX spot PNXT futures PNXT spot CEGH futures CEGH spot GME futures GME spot The ICE/ICE-Endex dominates with 95% of the total exchange volumes 2015 Patrick Heather Consultancy Limited 8

12 OTC + Exchange traded market shares VOB VTP PSV PEGs ZEE+ZTP NCG+GPL OTC and Exchange Market shares of each gas hub TTF NBP 0% 20% 40% 60% 80% 100% OTC EXCH OTC and Exchange market shares of total European gas trading 0% 1% 1% 0% 2%1% 0% 7% 25% 5% 30% 28% NBP OTC NBP Exch TTF OTC TTF Exch NCG+GPL OTC NCG+GPL Exch ZEE+ZTP OTC ZEE+ZTP Exch PEGs OTC PEGs Exch PSV OTC PSV Exch VTP OTC VTP Exch VOB OTC VOB Exch OTC dominates across traded hubs overall but exchange trading rising fast at NBP (~30%/2011 to ~52%/2014) and growing at TTF (~6%/2011 to ~15%/2014) 2015 Patrick Heather Consultancy Limited 9

13 A comparison of EU hubs European gas hubs and trading data Setting the scene 2015 Patrick Heather Consultancy Limited 10

14 European gas regions, markets and hubs This is my interpretation of the European gas scene in 2015, based on gas market liberalisation and commercial development 2015 Patrick Heather Consultancy Limited 11

15 Development of the hubs The most developed part of Europe in terms of liberalised gas hubs is in the North-West but this is also the one with the most disparity between the mature, poor and illiquid hubs The Central European region is the one showing most promise for further development over the coming years, both in infrastructure and in market development Most of Eastern Europe is still heavily dependant on Russian gas supplies, arriving through the historic network of transit pipelines; their local gas networks are generally poor and there is a major need for better north/south connectivity Europe is not one homogenous gas market: neither in infrastructure nor in political desire to change 2015 Patrick Heather Consultancy Limited 12

16 Market development hurdles Liquidity and transparency are key but assessment needs defined measures and criteria Physical connectivity is also key to realise the EU s aim for regional Market Areas Political willingness and cultural attitudes to trading are also key to the development of successful gas trading hubs Much has happened in the development of the European gas hubs but there are still some hurdles to overcome 2015 Patrick Heather Consultancy Limited 13

17 NWE/CE/SE hubs price correlation: Price correlation means prices move in the same direction at the same time by about the same amount; it does not mean same price Price correlation in itself is no indicator of one hub being active or inactive, in absolute terms or in relation to the other hubs 2015 Patrick Heather Consultancy Limited 14

18 European gas regions, markets and hubs Not all hubs are developing in the same way or at the same speed Only two mature gas trading hubs in Europe: NBP and TTF 2015 Patrick Heather Consultancy Limited 15

19 A comparison of EU hubs European gas hubs and trading data The 5 Key Elements 2015 Patrick Heather Consultancy Limited 16

20 5 key elements In order to evaluate the depth, liquidity and transparency of the traded gas hubs across Europe, I analyse the results of 5 key elements; as far as these are available The 5 key elements analysed are: who trades in each of the hubs what products are traded there how much volume is traded, and over which periods the Tradability Index the churn rates They are all important but the churn is the most It is essential to review as a minimum these 5 criteria to permit a rigorous analysis; but not all of the elements are always available in all of the hubs 2015 Patrick Heather Consultancy Limited 17

21 Key Element 1: Market Participants The absolute number of market participants can be misleading as, in reality, it s the number of active participants that really counts Active participants are those who regularly trade and, the more there are, the more liquidity there will be in a market 2015 Patrick Heather Consultancy Limited 18

22 Key Element 2: Traded Products Sources: ICE ; ICE-Endex ; EEX ; Powernext ; CEGH ; GME; P. Heather The type of products available to trade and their traded volumes are a good indication of whether a market is used for balancing or risk management 2015 Patrick Heather Consultancy Limited 19

23 Key Element 3: Traded volumes Volumes are very important in the analysis of the development of a traded gas hubs. The traded volumes compared to the overall size of the underlying market determine the churn rate, which is probably the most important factor in determining the success of a traded market High absolute traded volumes usually indicate a market with high churn, a large and varied range of participants and free from price manipulation 2015 Patrick Heather Consultancy Limited 20

24 Traded volume development: NOTE: NBP and TTF volumes divided by 5 in this graph Sources: LEBA; ICIS; ICE ; ICE-Endex ; EEX ; Powernext ; CEGH ; GME; P. Heather NBP has lost volume to TTF but remains the predominant hub for how long? TTF has seen phenomenal rise in activity since 2011/12, especially in 2014; 2015 Patrick Heather Consultancy Limited 21

25 Key element 4: Tradability Index: Q1-15 The ICIS Tradability Index is not in itself an indication of a deep, liquid and transparent market but it can assist the analysis of the development of a traded hub, in conjunction with other metrics For the result to have any indication, you need to look firstly at the progression of the Index over time, then at the actual number: Sources: ICIS European Gas Hub Reports ; P. Heather A result below 16 is not very meaningful, whereas a result of 18 or above does indicate that the hub in question does have reasonable liquidity 2015 Patrick Heather Consultancy Limited 22

26 Key element 5: Churn rates Probably the most important factor in determining the success of a traded market. Commodity markets are deemed to have reached maturity when the churn is in excess of 10 times When looking at market liquidity, you simply cannot transfer liquidity from a mature hub to a neighbouring hub that does not have the same characteristics, even if the headline price of the spot marginal gas is closely correlated There are two clear benchmark hubs today: NBP and TTF; no other hub is even near to the 10x criterion for mature markets; ZEE continues as essential trading location for large shippers, now joined by VTP; PEGs struggling 2015 Patrick Heather Consultancy Limited 23

27 Summary and conclusion 2015 Patrick Heather Consultancy Limited 24

28 Summary and Conclusion Britain s gas markets liberalised in the mid-1990 s and, with a very successful benchmark hub, reached maturity within 10 years, albeit at a high cost NBP is the benchmark for gas in the British Isles and some LNG supplies West European gas markets really started in the mid s and, despite a successful Dutch hub, are still some way from being fully liberalised across all countries East European gas markets have barely started their evolution towards liberalised, competitive markets but, through EU Directives and commercial pressure, will change in time Further down the line another European hub is feasible European Gas Hubs already provide price markers for physical contracts but the EU vision for a Single Energy Market is still many years off However, today, TTF has become the benchmark hub for North West European gas supplies and is being widely used for risk management 2015 Patrick Heather Consultancy Limited 25

29 PatrickHeatherConsultancy Thank you! The contents of this presentation are subject to PHCL copyright. This presentation may not be reproduced in whole or in part without the written permission of Patrick Heather, PHCL, Lulworth, Longfield Road, Twyford, READING RG10 9AT Tel: Mobile: Patrick Heather Consultancy Limited

30 Agenda plenary session The Evolution of European Gas Hubs Patrick Heather The European Network Codes Peter Schultz Auction Results PRISMA Diederik Top Miscellaneous Dewi Telehala

31 The European Network Codes Functionality of Network Codes (FuNC) Peter Schultz Long Term Use It or Lose It (LT UIOLI) Network Code Tariff (NC TAR) Adaptation of tariff for connections (BAT)

32 Functionality of Network Codes Aim of the working group Progress and status Identified issues Way forward

33 Aim of the working group Identify and solve issues resulting from imperfections in network codes Issues relevant for majority of stakeholders Solutions supported by involved TSOs Most issues related to bundled capacity, solutions involve multiple TSOs

34 Progress and status Until 21 April First selection of issues and potential solutions presented by EFET and ENTSOG at Madrid Forum Other interested stakeholders invited to participate Questionnaire to express views Two workshops to identify issues and find solutions 2 May GTS sent letter to inform and encourage participation of customers 20 May First workshop; no new insights

35 Identified issues The working group identified four issues: I. Different CMP measures implemented; Oversubscription & Buy Back vs restriction of renomination rights II. Different lead times for trading at PRISMA secondary III. Different procedures for surrender of capacity IV. Different technical capacities each side of the border

36 I Different CMP measures Problem description: NRAs can choose between restriction of renomination rights or overbook & buy back. At IPs with unidirectional flow the downward restriction of renomination rights does not result in the TSO being able to offer firm backhaul capacity. Proposed solutions: NRAs are to enforce same mechanism at both sides, alignment per IP or per product Increase liquidity secondary market

37 II Different lead times for trading Problem description: GTS processes trading requests on a near real time basis, other TSOs take up to 10 days. Harmonization of lead times will enhance the secondary market for bundled capacity. Proposed solutions: Define best practice as standard solution for all TSOs Define maximum lead time for each product; 5 days for monthly, quarterly and yearly capacity. Best endeavours for DA capacity trades

38 III a Different procedures for SoC; Pro rata vs FcFs Problem description: TSOs use different mechanisms when re-assigning surrendered capacity. Bundled capacity becomes (partly) unbundled. Implemented solution: All TSOs have implemented or will implement FcFs mechanism.

39 III b Different procedures for SoC; return/recall capacity Problem description: GTS returns capacity immediately after the auction, other TSOs roll over until DA auction. Surrendered bundeled capacity can become trapped because of automatic roll over. Proposed solution: Where a TSO automatically rolls over SoC, shippers can recall their capacity when an auction is finished but only until capacity is uploaded by TSO to PRISMA for next auction.

40 IV Differences in technical capacity; Primarily bundled capacity offered Lack of unbundled capacity to be matched with existing contracts of unbundled capacity at the other side of the IP

41 IV Capacity mismatch; Proposed solutions: Conditional surrender Allocation of CAM leftovers Capacity is offered as bundled and unbundled capacity in competing auctions

42 Way forward Planning meeting on 3 June 2015 in Brussels where experts from stakeholders and working group will: Re-assess discussions and conclusions of first workshop Discuss concrete business rules / proposals for the four identified issues based on the conclusions from the workshop Prepare material and positions for second workshop on 30 June 2015

43 The European Network Codes Functionality of Network Codes (FuNC) Peter Schultz Long Term Use It or Lose It (LT UIOLI) Network Code Tariff (NC TAR) Adaptation of tariff for connections (BAT)

44 Content Background ACM, CREG, Ofgem paper Roles of ACM, GTS & shippers

45 Background The LT UIOLI measure was launched August 2012 as one of the CMP measures valid as of 1 October 2013 During the CMP implementation period GTS asked your opinion on the implementation of LT UIOLI measure End 2014, the NRAs from the Netherlands, Belgium and UK decided to launch a joint paper on the implementation of LT UIOLI This paper was officially published by ACM on the 8 th of April 2015 In this session GTS will inform you on the details of this paper and on potential consequences for GTS customers

46 ACM, CREG, Ofgem paper 1. Process timeline 2. Process steps

47 1. Timeline of the process Period to process information Yearly auction y+1 Quarterly auction y+1 Yearly auction y+2 Quarterly auction y+2 Period for which Monitoring period capacity is withdrawn Oct y-1 Apr y Oct y Oct y+1 Oct y+2 Oct y+3 Processing steps

48 2. Process steps

49 Contractual congestion? There is contractual congestion if, for the monitoring period all technical capacity offered in Y or Q auctions is sold out or any technical capacity offered in Y or Q auctions is sold at a premium or the TSO did not offer any capacity in the Y or Q auctions

request for firm capacity if, for the monitoring period all firm capacity offered in Y or Q auctions is sold out or any firm")

50 Request for firm capacity? There is an (unfulfilled) request for firm capacity if, for the monitoring period all firm capacity offered in Y or Q auctions is sold out or any firm capacity product offered in Y or Q auctions is sold at a premium or the TSO did not offer any firm capacity in the Y or Q auctions

51 Systematically underutilised? When is a contract systematically underutilised Capacity is not liable to be withdrawn under the LT UIOLI mechanism if the utilisation rate was 80% or higher from 1 April until 30 September and/or from 1 October until 31 March The utilisation rate is the average utilisation per gas day In a portfolio of multiple contracts (profiled bookings), the capacity in contracts with a duration of one year or longer is assumed to be used before any other contracts with shorter duration

52 Unused capacity sold, offered under reasonable conditions? When has a shipper offered enough capacity Shipper has surrendered capacity and/or offered capacity on the PRISMA secondary platform for at least three consecutive months ahead against a price up to the reserve price (as given in the latest yearly CAM auction within the monitoring period) The capacity offer should be accessible for all interested counterparts registered as a trader on the PRISMA platform

53 Proper justification? Shipper will have the opportunity to properly justify a utilisation rate lower than 80% by proving that he needs the capacity. Justifications will be assessed on a case by case basis Typical justification: Existence of a delivery contract Security of supply contract Shipper may use this opportunity to prove that it has offered unused capacity under reasonable conditions at another platform than PRISMA.

54 The capacity to withdraw? If at the end of the day the average utilisation for both periods is still < 80% then the NRA will instruct the TSO to withdraw capacity: up to 80% threshold for an effective duration of two gas years via obligatory surrender yearly capacity rolled over to auction quarterly capacity shippers rights and obligations remain for unsold part

55 Roles of ACM, GTS, shipper Paper is guideline from NRAs towards shippers NRAs are to decide ultimately on withdrawal If required GTS provides ACM with all necessary data to assess long term contracts Shippers can appeal against withdrawal decision

56 The European Network Codes Functionality of Network Codes (FuNC) Peter Schultz Long Term Use It or Lose It (LT UIOLI) Network Code Tariff (NC TAR) Adaptation of tariff for connections (BAT)

57 Content of NC TAR Brief overview Ensure a stable, transparent and cost reflective transmission tariff structure that prevents cross subsidies between network users and leads to efficient investments Make cost allocation mechanisms and impact on tariffs understandable Is applicable to all Entry/Exit points, not only to Interconnection Points (IPs) Cost allocation methodologies Transparency obligations Consultation obligations

58 European process NC TAR Several ongoing dialogues ENTSOG submits draft NC TAR 26/12 ACER reasoned opinion 26/3 ENTSOG to be resubmitted draft NC TAR EC NC TAR proposal? Publication Final NC TAR? 19/3 TODAY 1 st informal Comitology 2 nd formal Comitoloy: DECISION? EC and Member States 2 nd formal Comitology: DECISION? PWC Impact Assessment for EC Market (IOGP/EFET) proposal for reduced NC TAR

59 Dutch implementation of NC TAR Potential planning, timing dependent on EU process GTS updates you on process TODAY GTS and ACM market consultation GTS submits change proposal Dutch tariff code ACM to consult and decide on Dutch tariff code (after 6 months) GTS submits tariff proposal for next year ACM to take tariff decision (after 3 months) EC NC TAR proposal? Publication Final NC TAR? 24 months implementation deadline GTS and ACM to engage in consultation with market

60 The European Network Codes Functionality of Network Codes (FuNC) Peter Schultz Long Term Use It or Lose It (LT UIOLI) Network Code Tariff (NC TAR) Adaptation of tariff for connections (BAT)

61 Adaptation of tariff for connections (BAT) Since 1 January 2014 there is a BAT tariff, separate from transport, balancing and quality conversion The BAT tariff is applied to connections in operation before 1 April 2011 For 2014 & 2015, BAT is a uniform, capacity dependent tariff of 0,111 & 0,119 /kwh/h/y GTS has proposed a new tariff calculation method that reflects the actual costs for maintaining a connection better than the current method

62 Proposed change for BAT The new tariff calculation method is based on the new-build cost of the connection which is based on the cost for GOS, the connection valves, and the diameter of the connection line As before the tariff is invoiced to the shippers Expected introduction of new tariff calculation method is 1 January 2016

63 Effects for network users Current yearly fee New yearly fee average of the bottom 50% average average of the top 50% average of the bottom 50% average average of the top 50% Industry Feeders Storages Industrial connections will have a significant higher tariff: for some small connections the tariff will change from less than k 1 to k 85 The average feeder will have an increase of approximately 50% The tariffs for storages will decrease to approximately 10% of the current tariff

64 Agenda plenary session The Evolution of European Gas Hubs Patrick Heather The European Network Codes Peter Schultz Auction Results PRISMA Diederik Top Miscellaneous Dewi Telehala

65 Agenda Auction points and products Congestion status PRISMA platform statistics Auction capacity bookings Within-Day product Fall Back PRISMA

")

66 Auction points and products Julianadorp BBL Emden GASSCO NPT, EPT Oude Statenzijl H GASCADE GUD OGE Oude Statenzijl L GUD GTG Nord Zevenaar OGE/Thyssengas Winterswijk OGE Tegelen OGE H-gas G-gas Zelzate Zandvliet-H Fluxys Hilvarenbeek Fluxys s Gravenvoeren Fluxys Bocholtz OGE Fluxys (TENP) Bocholtz Vetschau Thyssengas

67 Congestion status Dutch Southern border GTS Southern border exits plus BBL & entry Zelzate

68 Congestion status Dutch Eastern border

69 PRISMA platform statistics Currently 35 TSOs >400 registered shippers on PRISMA platform Registered GTS shippers increased from 95 to 111 since start Average of 23 shippers per month that actually book capacity Number of bookings doubled compared to GEA C&B Number of Number bookings of contracts received by GTS doubled Capacity sold in kwh/h Entry Exit Entry Exit Year Quarter Month Day-Ahead avg Day-Ahead Total

70 Auction capacity bookings Total of booked entry and exit capacity FCFS Entry: 45 million FCFS Exit: 130 million Auction bookings on top of already booked FCFS Too early to draw conclusions

71 Auction capacity bookings Share per product type (average per day in kwh/h) Exit Capacity Entry Capacity Year Quarterly Month Day No long term entry capacity sold Month Day

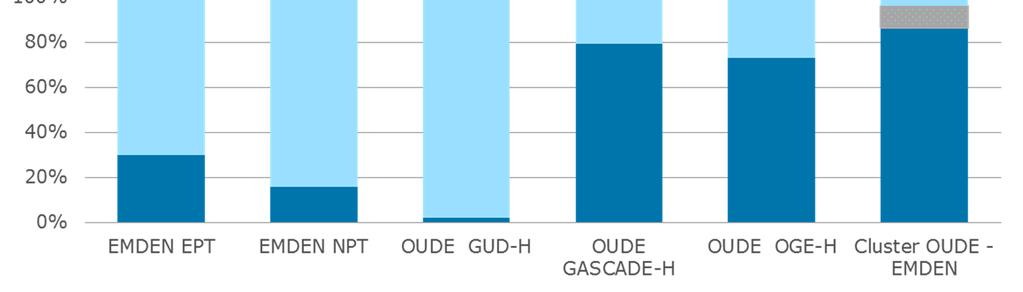

72 Auction capacity bookings Yearly exit capacity in kwh/h 65% less yearly capacity booked for Gas Year No yearly capacity sold with surcharge Quarterly auction on 1st of June

73 Auction capacity bookings (Monthly)

")

74 Auction capacity bookings (Daily)

75 Start Within-Day product (1 November 2015) First Within-Day auction starts on 31 October 2015 at 7 PM Remaining Day-Ahead capacity is rolled over to Within-Day auction Within-Day auction is 4 hours before runtime capacity Within-Day tariff is based on hours: x/24th of daily tariff

76 Within-Day Schedule 1st bidding window open for 7½ hours (7 PM to 2.30 AM) Duration of each following bidding window is 30 minutes Each bidding round opens at the start of every hour FIRST AUCTION WINDOW FOR NEXT GAS DAY S T A R T N E X T G A S D A Y FIRST AUCTION WINDOW OPEN FOR 7,5 HOURS CAPACITY UNTIL THE END OF THE RELEVANT GAS DAY Day D-1 Day D

77 Fall Back PRISMA Availability of the PRISMA platform: 99,99% PRISMA is working on a Fall Back procedure No Fall Back procedure required for Yearly, Quarterly and Monthly auctions Fall Back for Day-Ahead in place by offering the WiD product

78 Agenda plenary session The Evolution of European Gas Hubs Patrick Heather The European Network Codes Peter Schultz Auction Results PRISMA Diederik Top Miscellaneous Dewi Telehala

79 Miscellaneous Supplier of last resort Dewi Telehala Merger of Emden NPT and Emden EPT Interlocutory decision Court of Appeal (CBb) on ACM Method Decision Single sided nominations (SSN) Intended split GTS Access to Gasport Customer satisfaction survey

80 Supplier of last resort Follow-up: 1. Code improvement process is still going on After consultation with Reporgs, GTS and TenneT submitted a code change proposal to ACM at 11 December 2014 Implementation is expected summer Robustness codes with regard to bankruptcy of bigger market parties Analysis performed by ACM, EZ, TenneT and GTS is finalized The results will be published shortly after the summer Ministry of Economic Affairs (EZ) is expected to start consultation sessions with Reporgs after publication

81 Miscellaneous Supplier of last resort Dewi Telehala Merger of Emden NPT and Emden EPT Interlocutory decision Court of Appeal (CBb) on ACM Method Decision Single sided nominations (SSN) Intended split GTS Access to Gasport Customer satisfaction survey

82 Merger of Emden NPT and Emden EPT Gassco will merge the NPT entry point with the EPT entry point at Emden The merging of booking and nominations points will take place on 1 October 2015 GTS will contact shippers with capacity bookings at Emden NPT on short notice

83 Miscellaneous Supplier of last resort Dewi Telehala Merger of Emden NPT and Emden EPT Interlocutory decision Court of Appeal (CBb) on ACM Method Decision Single sided nominations (SSN) Intended split GTS Access to Gasport Customer satisfaction survey

84 Interlocutory decision Court of Appeal (CBb) on ACM Method Decision Interlocutory decision on the 5 th of March 2015 This interlocutory decision currently has no effect on the status of the method decision , x-factor decision or tariff decision 2015 The final decision of the CBb is expected at the end of 2015 Financial recalculations, if any, depend on final decision With regard to timing, we do not expect any financial recalculations before 2017

85 Miscellaneous Supplier of last resort Dewi Telehala Merger of Emden NPT and Emden EPT Interlocutory decision Court of Appeal (CBb) on ACM Method Decision Single sided nominations (SSN) Intended split GTS Access to Gasport Customer satisfaction survey

86 Single Sided Nominations As of 1 November 2015 GTS will enable shippers to nominate the flows of their capacity via a single nomination Single sided nominations (SSN) for bundled AND unbundled capacity Alignment with other TSOs for exact implementation per network point; date, role of TSO, Edigas messages Market parties will be informed in due course via GTS website

87 Implementation by GTS Preparation for SSN Shippers A & B to agree on use of SSN; shipper B will nominate on behalf of shipper A Shipper A informs his TSO (TSO 1) via Edigas message which shipper which network point which period Nomination process Shipper B submits SSN to his TSO (TSO 2) TSO 2 that receives SSN from shipper B informs TSO 1 TSO 1 and TSO 2 send confirmations to their shippers

88 Please note that: Regular nominations (double sided) still possible Shipper A can still submit nominations, overruling the SSN SSN requires Edigas version 5.1 or higher

89 Miscellaneous Supplier of last resort Dewi Telehala Merger of Emden NPT and Emden EPT Interlocutory decision Court of Appeal (CBb) on ACM Method Decision Single sided nominations (SSN) Intended split GTS Access to Gasport Customer satisfaction survey

90 Gasunie intends to split its subsidiary Gasunie Transport Services (GTS) Split will result into two separate transmission system operators as of 1 January 2016 a network operator for the national main transmission system (Gasunie Transport Services, GTS) a network operator for the regional high-pressure transmission system (Gasunie Grid Services, GGS) GTS will submit the necessary code changes within the coming weeks The split has minimal practical implications for customers and GTS will inform its customers in due time

91 Miscellaneous Supplier of last resort Dewi Telehala Merger of Emden NPT and Emden EPT Interlocutory decision Court of Appeal (CBb) on ACM Method Decision Single sided nominations (SSN) Intended split GTS Access to Gasport Customer satisfaction survey

92 Access to Gasport GTS is presently researching alternatives for the use of certificates for access to Gasport Examples of alternatives: Hardware tokens (little device that generates passcodes), Software tokens (mobile app that generates passcodes), SMS verification, verification Identity federation (security integration between companies: we trust your user accounts) Etc. GTS will send a questionnaire in Q to certificate holders to gain insight in your preferences

93 Miscellaneous Supplier of last resort Dewi Telehala Merger of Emden NPT and Emden EPT Interlocutory decision Court of Appeal (CBb) on ACM Method Decision Single sided nominations (SSN) Intended split GTS Access to Gasport Customer satisfaction survey

94 Customer satisfaction survey Taken actions as a result of the survey 2014 Customer Desk Complaint handling Invoices Other action taken to improve our customer processes Customer Desk for shippers Industry Desk for connected parties The next customer satisfaction survey will be conducted in September 2015

95 Thank you for your attention 13:00 14:00 14:00 19:00 Lunch including individual consults Social event (Madurodam and beach BBQ) There are busses to bring you to Madurodam. Busses are parked in front of the hotel and will depart at 14:00 hours. After the beach BBQ, there will be one bus driving to Schiphol. The other bus will drive back to the hotel. Busses depart at 19:00 hours.

Exhibit G to the General Terms and Conditions Forward Flow as of 2018

CAM and CMP implementation and general rules General provisions Terms defined in the Conditions shall have the same meaning when used herein. This Exhibit G shall form part of the Conditions as amended

CAM and CMP implementation and general rules General provisions Terms defined in the Conditions shall have the same meaning when used herein. This Exhibit G shall form part of the Conditions as amended

Exhibit G to the General Terms and Conditions Forward Flow as of 2018

CAM and CMP implementation and general rules General provisions Terms defined in the Conditions shall have the same meaning when used herein. This Exhibit G shall form part of the Conditions as amended

CAM and CMP implementation and general rules General provisions Terms defined in the Conditions shall have the same meaning when used herein. This Exhibit G shall form part of the Conditions as amended

Exhibit G to the General Terms and Conditions Forward Flow November 2015

CAM and CMP implementation and general rules Introduction In this Exhibit G BBL Company sets out the conditions following from the implementation of CAM and CMP. This exhibit G is not exhaustive because

CAM and CMP implementation and general rules Introduction In this Exhibit G BBL Company sets out the conditions following from the implementation of CAM and CMP. This exhibit G is not exhaustive because

1 September 2017 GAS MARKET ENTRY REPORT: THE NETHERLANDS

1 September 2017 GAS MARKET ENTRY REPORT: THE NETHERLANDS 1 Table of Contents GAS WHOLESALE TRADING IN THE NETHERLANDS COUNTRY OVERVIEW TABLE... 4 Legal framework... 6 Structure of the market and services...

1 September 2017 GAS MARKET ENTRY REPORT: THE NETHERLANDS 1 Table of Contents GAS WHOLESALE TRADING IN THE NETHERLANDS COUNTRY OVERVIEW TABLE... 4 Legal framework... 6 Structure of the market and services...

Exhibit G to the General Terms and Conditions Forward Flow as of 2018November 2015

CAM and CMP implementation and general rules General provisions Terms defined in the Conditions shall have the same meaning when used herein. This Exhibit G shall form part of the Conditions as amended

CAM and CMP implementation and general rules General provisions Terms defined in the Conditions shall have the same meaning when used herein. This Exhibit G shall form part of the Conditions as amended

EU Gas Market Reform what does it mean in practice?

EU Gas Market Reform what does it mean in practice? Alex Barnes, Head of Regulatory Affairs Energy Forum 2012 Vilnius 18 th December 2012 European gas markets are facing major changes... DG ENERGY / ACER

EU Gas Market Reform what does it mean in practice? Alex Barnes, Head of Regulatory Affairs Energy Forum 2012 Vilnius 18 th December 2012 European gas markets are facing major changes... DG ENERGY / ACER

European Network Code Workshop

European Network Code Workshop Place your chosen image here. The four corners must just cover the arrow tips. For covers, the three pictures should be the same size and in a straight line. Gas European

European Network Code Workshop Place your chosen image here. The four corners must just cover the arrow tips. For covers, the three pictures should be the same size and in a straight line. Gas European

ENTSOG s Capacity conversion model

2017-07-24 ENTSOG AISBL; Av. de Cortenbergh 100, 1000-Brussels; Tel: +32 2 894 5100; Fax: +32 2 894 5101; info@entsog.eu, www.entsog.eu, VAT No. BE0822 653 040 Background On October 13 th, 2016 the amendment

2017-07-24 ENTSOG AISBL; Av. de Cortenbergh 100, 1000-Brussels; Tel: +32 2 894 5100; Fax: +32 2 894 5101; info@entsog.eu, www.entsog.eu, VAT No. BE0822 653 040 Background On October 13 th, 2016 the amendment

2 nd Technical Workshop: Gas Market Design and Natural Gas Transmission Grid Codes

2 nd Technical Workshop: Gas Market Design and Natural Gas Transmission Grid Codes Practices for Grid Code Harmonization Examining Capacity Allocation and Congestion Management Fotis Thomaidis Partner,

2 nd Technical Workshop: Gas Market Design and Natural Gas Transmission Grid Codes Practices for Grid Code Harmonization Examining Capacity Allocation and Congestion Management Fotis Thomaidis Partner,

Draft position paper for consultation. Exploring the feasibility of implicit allocation in the (North West) European gas market

European gas market") Draft position paper for consultation Exploring the feasibility of implicit allocation in the (North West) European gas market The Hague, 1 October 2012 1 / 16 1 Introduction 1.1 Background The Council

Draft position paper for consultation Exploring the feasibility of implicit allocation in the (North West) European gas market The Hague, 1 October 2012 1 / 16 1 Introduction 1.1 Background The Council

Roadmap for early implementation of the Network Code on Capacity Allocation Mechanisms (CAM NC)

") Roadmap for early implementation of the Network Code on Capacity Allocation Mechanisms (CAM NC) 1 st EU Stakeholders meeting Brussels, 6 March 2013 Agenda AGENDA TOPICS INDICATIVE TIMING 1. Opening and

Roadmap for early implementation of the Network Code on Capacity Allocation Mechanisms (CAM NC) 1 st EU Stakeholders meeting Brussels, 6 March 2013 Agenda AGENDA TOPICS INDICATIVE TIMING 1. Opening and

Workshop CAM, CMP. GTS shippermeeting, 21 November 2012

Workshop CAM, CMP GTS shippermeeting, 21 November 2012 1 Chatham house rule When a meeting, or part thereof, is held under the Chatham House Rule, participants are free to use the information received,

Workshop CAM, CMP GTS shippermeeting, 21 November 2012 1 Chatham house rule When a meeting, or part thereof, is held under the Chatham House Rule, participants are free to use the information received,

Stakeholder Workshop II

Brussels, 30 June 2015 Stakeholder Workshop II On issues related to bundling of capacities Brussels, 30 June 2015 Disclaimer This presentation does not reflect a commitment content wise nor time wise for

Brussels, 30 June 2015 Stakeholder Workshop II On issues related to bundling of capacities Brussels, 30 June 2015 Disclaimer This presentation does not reflect a commitment content wise nor time wise for

Introducing PRISMA European Capacity Platform

Introducing PRISMA European Capacity Platform Background of the company and current developments Allocation of Gas Transmission Capacities in the Energy Community Workshop 14 March 2016, Vienna Agenda

Introducing PRISMA European Capacity Platform Background of the company and current developments Allocation of Gas Transmission Capacities in the Energy Community Workshop 14 March 2016, Vienna Agenda

Network Code. on Capacity Allocation Mechanisms

6 March 2012 Network Code on Capacity Allocation Mechanisms An ENTSOG Network Code for ACER review and Comitology Procedure This document constitutes the Capacity Allocation Mechanisms Network Code developed

6 March 2012 Network Code on Capacity Allocation Mechanisms An ENTSOG Network Code for ACER review and Comitology Procedure This document constitutes the Capacity Allocation Mechanisms Network Code developed

NATURAL GAS TRANSPORTATION SERVICES PROVIDED BY IUK BETWEEN GB AND BELGIUM

NATURAL GAS TRANSPORTATION SERVICES PROVIDED BY IUK BETWEEN GB AND BELGIUM Issue 5 March 2018 www.interconnector.com DISCLAIMER This IUK Access Agreement Summary ( IAAS ) has been prepared by Interconnector

NATURAL GAS TRANSPORTATION SERVICES PROVIDED BY IUK BETWEEN GB AND BELGIUM Issue 5 March 2018 www.interconnector.com DISCLAIMER This IUK Access Agreement Summary ( IAAS ) has been prepared by Interconnector

EU Gas Market Reform what does it mean in practice?

EU Gas Market Reform what does it mean in practice? Alex Barnes, Head of Regulatory Affairs Energy Forum 2012 Vilnius 18 th December 2012 European gas markets are facing major changes... DG ENERGY / ACER

EU Gas Market Reform what does it mean in practice? Alex Barnes, Head of Regulatory Affairs Energy Forum 2012 Vilnius 18 th December 2012 European gas markets are facing major changes... DG ENERGY / ACER

European Developments

European Developments Place your chosen image here. The four corners must just cover the arrow tips. For covers, the three pictures should be the same size and in a straight line. Transmission Workgroup

European Developments Place your chosen image here. The four corners must just cover the arrow tips. For covers, the three pictures should be the same size and in a straight line. Transmission Workgroup

IUK Access Agreement Summary. 10 Oct 2013

IUK Access Agreement Summary 10 Oct 2013 Preface This document (the IUK Access Agreement Summary or IAAS ) describes the transportation model and the related services offered by Interconnector (UK) Limited

IUK Access Agreement Summary 10 Oct 2013 Preface This document (the IUK Access Agreement Summary or IAAS ) describes the transportation model and the related services offered by Interconnector (UK) Limited

Ellund capacity. - Creating new capacity at Ellund (DE) Maja Klejs Pedersen and Poul Johannes Jacobsen. 11 December 2014 User Group 1

Maja Klejs Pedersen and Poul Johannes Jacobsen. 11 December 2014 User Group 1") Ellund capacity - Creating new capacity at Ellund (DE) Maja Klejs Pedersen and Poul Johannes Jacobsen 11 December 2014 User Group 1 Capacity maximisation CAM Article 6 Energinet.dk sees two options We

Ellund capacity - Creating new capacity at Ellund (DE) Maja Klejs Pedersen and Poul Johannes Jacobsen 11 December 2014 User Group 1 Capacity maximisation CAM Article 6 Energinet.dk sees two options We

Introduction of Entry Capacity to Northern Ireland Transitional Arrangements

Introduction of Entry Capacity to Northern Ireland Transitional Arrangements Business Rules Revised Post-Consultation Version 1.1 13 th October 2014 Contents 1. Introduction: Background and Purpose...

Introduction of Entry Capacity to Northern Ireland Transitional Arrangements Business Rules Revised Post-Consultation Version 1.1 13 th October 2014 Contents 1. Introduction: Background and Purpose...

Shippers Meeting. Schiphol. 15 June 2010

Shippers Meeting Schiphol 15 June 2010 Programme Introduction Petra Smeets Link4Hubs Mark Hobbelink Wiekens Market Transition Process update Antwa Munnik Changes in information exchange Peter Scholtens

Shippers Meeting Schiphol 15 June 2010 Programme Introduction Petra Smeets Link4Hubs Mark Hobbelink Wiekens Market Transition Process update Antwa Munnik Changes in information exchange Peter Scholtens

European Update. 2nd July 2015

European Update Place your chosen image here. The four corners must just cover the arrow tips. For covers, the three pictures should be the same size and in a straight line. 2nd July 2015 1. General Update

European Update Place your chosen image here. The four corners must just cover the arrow tips. For covers, the three pictures should be the same size and in a straight line. 2nd July 2015 1. General Update

CEER Vision for a European Gas Target Model Conclusions Paper Ref: C11-GWG December 2011

CEER Vision for a European Gas Target Model Conclusions Paper Ref: C11-GWG-82-03 1 December 2011 European Regulators Group for Electricity and Gas Contact: Council of European Energy Regulators ASBL 28

CEER Vision for a European Gas Target Model Conclusions Paper Ref: C11-GWG-82-03 1 December 2011 European Regulators Group for Electricity and Gas Contact: Council of European Energy Regulators ASBL 28

on the conditions for the application of FDA UIOLI pursuant to paragraph a) - d) of the CMP Guidelines

- d) of the CMP Guidelines") Case Id: 3a123382-8301-48f8-a8f7-a674b1c3a961 Date: 19/09/2016 11:44:04 ACER Call for Evidence on the conditions for the application of FDA UIOLI pursuant to paragraph 2.2.3.1 a) - d) of the CMP Guidelines

Case Id: 3a123382-8301-48f8-a8f7-a674b1c3a961 Date: 19/09/2016 11:44:04 ACER Call for Evidence on the conditions for the application of FDA UIOLI pursuant to paragraph 2.2.3.1 a) - d) of the CMP Guidelines

The present ACER Guidance to ENTSOG provides a framework for the development of a

ACER guidance to ENTSOG on the development of amendment proposals to the Network Code on Capacity Allocation Mechanisms on the matter of incremental and new capacity 1. Introduction a) The Network Code

ACER guidance to ENTSOG on the development of amendment proposals to the Network Code on Capacity Allocation Mechanisms on the matter of incremental and new capacity 1. Introduction a) The Network Code

on the conditions for the application of FDA UIOLI pursuant to paragraph a) - d) of the CMP Guidelines

- d) of the CMP Guidelines") Case Id: c8d4ee05-ccfc-464f-a253-4c5fad681ae0 Date: 13/09/2016 11:53:22 ACER Call for Evidence on the conditions for the application of FDA UIOLI pursuant to paragraph 2.2.3.1 a) - d) of the CMP Guidelines

Case Id: c8d4ee05-ccfc-464f-a253-4c5fad681ae0 Date: 13/09/2016 11:53:22 ACER Call for Evidence on the conditions for the application of FDA UIOLI pursuant to paragraph 2.2.3.1 a) - d) of the CMP Guidelines

EU Network Code Implementation Project

EU Network Code Implementation Project Frequently Asked Questions Version 3.0 1 Contents 1. Introduction... 3 1.1. New Questions... 3 2. General... 3 2.1. CAM Network Code: Background and Scope... 3 2.2.

EU Network Code Implementation Project Frequently Asked Questions Version 3.0 1 Contents 1. Introduction... 3 1.1. New Questions... 3 2. General... 3 2.1. CAM Network Code: Background and Scope... 3 2.2.

Role Model for the Gas Sector

Role Model for the Gas Sector 12 May 2016 AGENDA Welcome & Introduction Aim of the Workshop Approach of the developement of the Role Model Explanation of the Project Roles and Parties Common Roles Parties

Role Model for the Gas Sector 12 May 2016 AGENDA Welcome & Introduction Aim of the Workshop Approach of the developement of the Role Model Explanation of the Project Roles and Parties Common Roles Parties

COMMISSION STAFF WORKING DOCUMENT EXECUTIVE SUMMARY OF THE IMPACT ASSESSMENT. Accompanying the document. Commission decision

EUROPEAN COMMISSION Brussels, XXX [ ](2012) XXX draft COMMISSION STAFF WORKING DOCUMENT EXECUTIVE SUMMARY OF THE IMPACT ASSESSMENT Accompanying the document Commission decision amending Annex I to Regulation

EUROPEAN COMMISSION Brussels, XXX [ ](2012) XXX draft COMMISSION STAFF WORKING DOCUMENT EXECUTIVE SUMMARY OF THE IMPACT ASSESSMENT Accompanying the document Commission decision amending Annex I to Regulation

Key elements of the 2025 vision on Gas

Key elements of the 2025 vision on Gas Walter Boltz ACER Board of Regulators Vice-Chair Chair ACER Gas Working Group Launch event Green Paper Energy TITRE Regulation: A Bridge to 2025 Brussels, 29 April

Key elements of the 2025 vision on Gas Walter Boltz ACER Board of Regulators Vice-Chair Chair ACER Gas Working Group Launch event Green Paper Energy TITRE Regulation: A Bridge to 2025 Brussels, 29 April

Demand assessment report for the incremental capacity process starting 2017

Demand assessment report for the incremental capacity process starting 2017 between GASPOOL and TTF market area 2017 07 27 This report is a joint assessment of the potential for incremental capacity projects

Demand assessment report for the incremental capacity process starting 2017 between GASPOOL and TTF market area 2017 07 27 This report is a joint assessment of the potential for incremental capacity projects

Towards efficient and effective congestion management of the European gas transmission network:

Amstelveenseweg 998 1081 JS Amsterdam Phone: + 31 20 520 7970 Email: secretariat@efet.org Website: www.efet.org Towards efficient and effective congestion management of the European gas transmission network:

Amstelveenseweg 998 1081 JS Amsterdam Phone: + 31 20 520 7970 Email: secretariat@efet.org Website: www.efet.org Towards efficient and effective congestion management of the European gas transmission network:

Consultation on the ZIGMA Model and Implementation of the Capacity Allocation Mechanism and Balancing EU Network Codes

8 April 2014 Dear Stakeholder, Consultation on the ZIGMA Model and Implementation of the Capacity Allocation Mechanism and Balancing EU Network Codes Interconnector (UK) Ltd (IUK), Fluxys Belgium and National

8 April 2014 Dear Stakeholder, Consultation on the ZIGMA Model and Implementation of the Capacity Allocation Mechanism and Balancing EU Network Codes Interconnector (UK) Ltd (IUK), Fluxys Belgium and National

ACCESS CODE FOR TRANSMISSION. Attachment B: Subscription & Allocation of Services

NON BINDING DOCUMENT FOR CONSULTATION PURPOSES ONLY ACCESS CODE FOR TRANSMISSION Attachment B: Subscription & Allocation of Services Based on version approved by CREG on 26 March 2015 1 of 72 Table of

NON BINDING DOCUMENT FOR CONSULTATION PURPOSES ONLY ACCESS CODE FOR TRANSMISSION Attachment B: Subscription & Allocation of Services Based on version approved by CREG on 26 March 2015 1 of 72 Table of

Official Journal of the European Union. (Non-legislative acts) REGULATIONS

REGULATIONS") 17.3.2017 L 72/1 II (Non-legislative acts) REGULATIONS COMMISSION REGULATION (EU) 2017/459 of 16 March 2017 establishing a network code on capacity allocation mechanisms in gas transmission systems and

17.3.2017 L 72/1 II (Non-legislative acts) REGULATIONS COMMISSION REGULATION (EU) 2017/459 of 16 March 2017 establishing a network code on capacity allocation mechanisms in gas transmission systems and

Market Consultation Session

Market Consultation Session February 19, 2013 Fluxys non-binding document for discussion & information purposes only (subject to managment approval) Objective of today s session Feedback on consultation

Market Consultation Session February 19, 2013 Fluxys non-binding document for discussion & information purposes only (subject to managment approval) Objective of today s session Feedback on consultation

Development of Gas Hubs in Europe

Development of Gas Hubs in Europe Caterina Miriello, Michele Polo IEFE - Centre for Research on Energy and Environmental Economics and Policy Department of Economics Bocconi University May 28, 2014 Outline

Development of Gas Hubs in Europe Caterina Miriello, Michele Polo IEFE - Centre for Research on Energy and Environmental Economics and Policy Department of Economics Bocconi University May 28, 2014 Outline

EASEE-gas. European Association for the Streamlining of Energy Exchange gas

1 1 2 EASEE-gas European Association for the Streamlining of Energy Exchange gas Harmonised Gas Role Model Specification From the Business Process perspective 3 4 5 Number: 2017-001/01.2 Subject: Harmonised

1 1 2 EASEE-gas European Association for the Streamlining of Energy Exchange gas Harmonised Gas Role Model Specification From the Business Process perspective 3 4 5 Number: 2017-001/01.2 Subject: Harmonised

Outline of the European Roadmap for CAM

Outline of the European Roadmap for CAM Clara Poletti GRI Coordinator 10 th NW Stakeholder Group TITRE 22-23 November 2012 Background (1/2) Madrid Forum XXI (March 2012) => called for the early implementation

Outline of the European Roadmap for CAM Clara Poletti GRI Coordinator 10 th NW Stakeholder Group TITRE 22-23 November 2012 Background (1/2) Madrid Forum XXI (March 2012) => called for the early implementation

Framework Guidelines on Capacity Allocation Mechanisms for the European Gas Transmission Network FG-2011-G August 2011

Framework Guidelines on Capacity Allocation Mechanisms for the European Gas Transmission Network FG-2011-G-001 3 August 2011 Agency for the Cooperation of Energy Regulators Trg Republike 3 1000 Ljubljana

Framework Guidelines on Capacity Allocation Mechanisms for the European Gas Transmission Network FG-2011-G-001 3 August 2011 Agency for the Cooperation of Energy Regulators Trg Republike 3 1000 Ljubljana

PEGAS response to German Grid Development Plan Gas

PEGAS response to German Grid Development Plan Gas 2018-2028 25.05.2017 Paris Powernext SAS Summary PEGAS welcomes the German Transmission System Operator s draft Grid Development Plan 2018-2028. Hereby,

PEGAS response to German Grid Development Plan Gas 2018-2028 25.05.2017 Paris Powernext SAS Summary PEGAS welcomes the German Transmission System Operator s draft Grid Development Plan 2018-2028. Hereby,

Tariff Network Code. An Overview

Tariff Network Code An Overview SEPTEMBER 2018 Content INTRODUCTION................. 2 AIM OF THE CODE............... 4 DESCRIPTION OF KEY ELEMENTS... 6 SCOPE...........................................

Tariff Network Code An Overview SEPTEMBER 2018 Content INTRODUCTION................. 2 AIM OF THE CODE............... 4 DESCRIPTION OF KEY ELEMENTS... 6 SCOPE...........................................

IUK is key infrastructure in physically connecting pipeline systems and markets

2018 Introduction to IUK IUK is key infrastructure in physically connecting pipeline systems and markets First Gas 1 st October 1998 System Capacity GB to BE: 20bcm/yr BE to GB: 25.5bcm/yr IUK Flows: April

2018 Introduction to IUK IUK is key infrastructure in physically connecting pipeline systems and markets First Gas 1 st October 1998 System Capacity GB to BE: 20bcm/yr BE to GB: 25.5bcm/yr IUK Flows: April

Applicable TSO Terms for Use of the PRISMA Capacity Platform. 01 November 2015

Applicable TSO Terms for Use of the PRISMA Capacity Platform 01 November 2015 TERMS APPLICABLE FOR BAYERNETS GMBH, FLUXYS DEUTSCHLAND GMBH, FLUXYS TENP GMBH, GASTRANSPORT NORD GMBH, GASCADE GASTRANSPORT

Applicable TSO Terms for Use of the PRISMA Capacity Platform 01 November 2015 TERMS APPLICABLE FOR BAYERNETS GMBH, FLUXYS DEUTSCHLAND GMBH, FLUXYS TENP GMBH, GASTRANSPORT NORD GMBH, GASCADE GASTRANSPORT

Gas transmission Technical and Economic Aspects for TSOs

European Summer School 2015 Economic and Legal Aspects of the Electricity, Gas and Heat Market Gas transmission Technical and Economic Aspects for TSOs Ina Adler (ONTRAS Gastransport GmbH) 1 Agenda 1.

European Summer School 2015 Economic and Legal Aspects of the Electricity, Gas and Heat Market Gas transmission Technical and Economic Aspects for TSOs Ina Adler (ONTRAS Gastransport GmbH) 1 Agenda 1.

EU Code Implementation Programme

EU Code Implementation Programme Place your chosen image here. The four corners must just cover the arrow tips. For covers, the three pictures should be the same size and in a straight line. Transmission

EU Code Implementation Programme Place your chosen image here. The four corners must just cover the arrow tips. For covers, the three pictures should be the same size and in a straight line. Transmission

COMMISSION STAFF WORKING DOCUMENT. Guidance on best practices for congestion management procedures in natural gas transmission networks

EUROPEAN COMMISSION Brussels, 11.7.2014 SWD(2014) 250 final COMMISSION STAFF WORKING DOCUMENT Guidance on best practices for congestion management procedures in natural gas transmission networks EN EN

EUROPEAN COMMISSION Brussels, 11.7.2014 SWD(2014) 250 final COMMISSION STAFF WORKING DOCUMENT Guidance on best practices for congestion management procedures in natural gas transmission networks EN EN

Brussels/Ljubljana, TITRE 1 April 2015

Open House meeting Stakeholder input for ACER s recommendation on the Network Code on rules regarding harmonised Transmission tariff structures for gas Brussels/Ljubljana, TITRE 1 April 2015 1 Agenda Agenda

Open House meeting Stakeholder input for ACER s recommendation on the Network Code on rules regarding harmonised Transmission tariff structures for gas Brussels/Ljubljana, TITRE 1 April 2015 1 Agenda Agenda

Coordinated implementation of the Network Code on Capacity Allocation Mechanisms. Information Memorandum

Coordinated implementation of the Network Code on Capacity Allocation Information Memorandum February 2014 INDEX Disclaimer... 4 1 Background... 5 2 Auctions... 6 2.1 2014 auctions... 6 2.2 2015 auctions

Coordinated implementation of the Network Code on Capacity Allocation Information Memorandum February 2014 INDEX Disclaimer... 4 1 Background... 5 2 Auctions... 6 2.1 2014 auctions... 6 2.2 2015 auctions

The shift from oil-indexation to market pricing:

PatrickHeatherConsultancy The shift from oil-indexation to market pricing: What is the situation and what is needed for the development of flexible markets? CEE Gas Conference Zagreb, 8 th March, 2018

PatrickHeatherConsultancy The shift from oil-indexation to market pricing: What is the situation and what is needed for the development of flexible markets? CEE Gas Conference Zagreb, 8 th March, 2018

1. Principles for transmission capacity management in common Baltic gas market

Assessment of the responses received for Baltic Transmission System Operators Public Consultation on Principles for transmission capacity management in common Baltic gas market, Analysis on Alternatives

Assessment of the responses received for Baltic Transmission System Operators Public Consultation on Principles for transmission capacity management in common Baltic gas market, Analysis on Alternatives

APPENDIX E.1: PROCEDURE FOR THE MARKETING OF CAPACITIES AT THE PIRINEOS VIRTUAL INTERCONNECTION POINT

APPENDIX E.1: PROCEDURE FOR THE MARKETING OF CAPACITIES AT THE PIRINEOS VIRTUAL INTERCONNECTION POINT Version dated [01/04/2017] NOTICE The purpose of this document is to describe in detail the procedures

APPENDIX E.1: PROCEDURE FOR THE MARKETING OF CAPACITIES AT THE PIRINEOS VIRTUAL INTERCONNECTION POINT Version dated [01/04/2017] NOTICE The purpose of this document is to describe in detail the procedures

The conclusions from the 20 th Madrid Forum (September 2011) form an important input for ACER. In this matter, the forum stressed that both ACER and t

form an important input for ACER. In this matter, the forum stressed that both ACER and t") North West IG meeting 8 March 2012 EK offices, The Hague DRAFT MINUTES Participants Menno van Liere NMa/EK (Chair) Gijsbert Lybaart NMa/EK Marie-Claire Aoun CRE Pitt Wangen ILR Bjorn ter Bruggen EI Sigrún

North West IG meeting 8 March 2012 EK offices, The Hague DRAFT MINUTES Participants Menno van Liere NMa/EK (Chair) Gijsbert Lybaart NMa/EK Marie-Claire Aoun CRE Pitt Wangen ILR Bjorn ter Bruggen EI Sigrún

EFET perspective. Andrea Bonzanni Regulatory Advisor, EDF Trading. 8 th ENTSOG Transparency Workshop Brussels, 11 th December 2014

8 th ENTSOG Transparency Workshop Brussels, 11 th December 2014 EFET perspective European Federation of Energy Traders New ENTSOG Transparency Platform Andrea Bonzanni Regulatory Advisor, EDF Trading Andrea

8 th ENTSOG Transparency Workshop Brussels, 11 th December 2014 EFET perspective European Federation of Energy Traders New ENTSOG Transparency Platform Andrea Bonzanni Regulatory Advisor, EDF Trading Andrea

where implicit capacity allocation methods are applied, national regulatory authorities may decide not to apply Articles 8 to 37.

System Operator's METHODOLOGY OF GAS TRANSMISSION CAPACITY ALLOCATION AND CONGESTION MANAGEMENT PROCEDURE AND STANDARD TERMS FOR ACCESSING THE CROSS-BORDER INFRASTRUCTURE 30 th June 2017 1. General provisions...

System Operator's METHODOLOGY OF GAS TRANSMISSION CAPACITY ALLOCATION AND CONGESTION MANAGEMENT PROCEDURE AND STANDARD TERMS FOR ACCESSING THE CROSS-BORDER INFRASTRUCTURE 30 th June 2017 1. General provisions...

ACER and the Transparency Platform

ACER and the Transparency Platform Csilla Bartók Team Leader Network Codes, Gas Department ENTSOG 11 th Transparency Workshop Vienna, 6 December 2017 ACER s transparency assessment - Background The legal

ACER and the Transparency Platform Csilla Bartók Team Leader Network Codes, Gas Department ENTSOG 11 th Transparency Workshop Vienna, 6 December 2017 ACER s transparency assessment - Background The legal

What are your main views of the proposed measures? Do you think Network codes

EDP Gás and Naturgas Energia Comercializadora Response to ERGEG Pilot Framework Guidelines on Capacity Allocation on European gas Transmission Networks EDP has activities in the gas sector in transportation,

EDP Gás and Naturgas Energia Comercializadora Response to ERGEG Pilot Framework Guidelines on Capacity Allocation on European gas Transmission Networks EDP has activities in the gas sector in transportation,

Virtual Reverse Flow: at Interconnection Points. Implementing EU Regulations. Code Modification No. A064. Business Rules. 17 th July Version 3.

Virtual Reverse Flow: at Interconnection Points Implementing EU Regulations Code Modification No. A064 Business Rules 17 th July 2015 Version 3.0 i VERSION CONTROL Version Date Description 1.0 19 th September

Virtual Reverse Flow: at Interconnection Points Implementing EU Regulations Code Modification No. A064 Business Rules 17 th July 2015 Version 3.0 i VERSION CONTROL Version Date Description 1.0 19 th September

UNC 0616: Capacity Conversion Mechanism for Interconnection Points. UNC Modification. 01 Modification. 02 Workgroup Report

UNC Modification UNC 0616: Capacity Conversion Mechanism for Interconnection Points At what stage is this document in the process? 01 Modification 02 Workgroup Report 03 04 Draft Modification Report Final

UNC Modification UNC 0616: Capacity Conversion Mechanism for Interconnection Points At what stage is this document in the process? 01 Modification 02 Workgroup Report 03 04 Draft Modification Report Final

European Developments

European Developments Place your chosen image here. The four corners must just cover the arrow tips. For covers, the three pictures should be the same size and in a straight line. Transmission Workgroup

European Developments Place your chosen image here. The four corners must just cover the arrow tips. For covers, the three pictures should be the same size and in a straight line. Transmission Workgroup

Shippers Meeting. Amsterdam. 25 March 2010

Shippers Meeting Amsterdam 25 March 2010 Programme Introduction Petra Smeets Balancing regime/market model Marcel Adrichem Transport Insight and Mark Hobbelink a new cross border service Wiekens Customer

Shippers Meeting Amsterdam 25 March 2010 Programme Introduction Petra Smeets Balancing regime/market model Marcel Adrichem Transport Insight and Mark Hobbelink a new cross border service Wiekens Customer

Interconnector (UK) Limited IUK Access Code

Limited IUK Access Code") Interconnector (UK) Limited IUK Access Code Issue 2 May 2015 subject to NRA approval Contents SECTION A INTRODUCTION... 1 1. IUK Access Code... 1 2. Capacity... 1 3. Nominations and Matching Procedures...

Interconnector (UK) Limited IUK Access Code Issue 2 May 2015 subject to NRA approval Contents SECTION A INTRODUCTION... 1 1. IUK Access Code... 1 2. Capacity... 1 3. Nominations and Matching Procedures...

European perspective on regional market integration

European perspective on regional market integration Dennis Hesseling, Head of the Gas Department 8 th Baltic Gas Market Forum, 15 November 2018, Helsinki Outline.Level of EU market integration.regional

European perspective on regional market integration Dennis Hesseling, Head of the Gas Department 8 th Baltic Gas Market Forum, 15 November 2018, Helsinki Outline.Level of EU market integration.regional

EU Gas Balancing Code - Daily Nominations at Interconnection Points (IP)

") UNC MODIFICATION PROPOSAL 0493 EU Gas Balancing Code - Daily Nominations at Interconnection Points (IP) COMMERCIAL BUSINESS RULES Text in red [BC 12(3)] [INT 12(3)] Key to format convention is reference

UNC MODIFICATION PROPOSAL 0493 EU Gas Balancing Code - Daily Nominations at Interconnection Points (IP) COMMERCIAL BUSINESS RULES Text in red [BC 12(3)] [INT 12(3)] Key to format convention is reference

Network code on harmonised transmission tariff structures for gas (NC TAR)

") Network code on harmonised transmission tariff structures for gas (NC TAR) Implementation of NC TAR in the Netherlands Disclaimer: This presentation has been prepared for informational and illustrative

Network code on harmonised transmission tariff structures for gas (NC TAR) Implementation of NC TAR in the Netherlands Disclaimer: This presentation has been prepared for informational and illustrative

Virtual Reverse Flow: at Interconnection Points. Implementing EU Regulations. Code Modification No. A064. Business Rules. Version 2.

Virtual Reverse Flow: at Interconnection Points Implementing EU Regulations Code Modification No. A064 Business Rules 16 th January 2015 Version 2.0 i VERSION CONTROL Version Date Description 1.0 19 th

Virtual Reverse Flow: at Interconnection Points Implementing EU Regulations Code Modification No. A064 Business Rules 16 th January 2015 Version 2.0 i VERSION CONTROL Version Date Description 1.0 19 th

Shippers Day LNG. 13 April Jean-Paul PINON Director Gas Market Commission for Electricity and Gas Regulation (CREG)

") Shippers Day LNG 13 April 2005 Jean-Paul PINON Director Gas Market Commission for Electricity and Gas Regulation (CREG) The CREG Belgian federal regulator for electricity and natural gas Autonomous organism

Shippers Day LNG 13 April 2005 Jean-Paul PINON Director Gas Market Commission for Electricity and Gas Regulation (CREG) The CREG Belgian federal regulator for electricity and natural gas Autonomous organism

Regional Gas Markets Recent Trends

Regional Gas Markets Recent Trends Energy and Environment Division Evening Lecture Engineers Ireland Clyde Road Wednesday 7 th Dec 2011 Donal Kissane - Bord Gáis Networks Contents Introduction Regional

Regional Gas Markets Recent Trends Energy and Environment Division Evening Lecture Engineers Ireland Clyde Road Wednesday 7 th Dec 2011 Donal Kissane - Bord Gáis Networks Contents Introduction Regional

Achieving a single European gas market. Walter Boltz Executive Director E-Control Austria, Vice Chair of ACER s Regulatory Board

1 Achieving a single European gas market Walter Boltz Executive Director E-Control Austria, Vice Chair of ACER s Regulatory Board Agenda Where we stand Vision for the European Gas Market The new Austrian

1 Achieving a single European gas market Walter Boltz Executive Director E-Control Austria, Vice Chair of ACER s Regulatory Board Agenda Where we stand Vision for the European Gas Market The new Austrian

Removing barriers to LNG and to gas storage product innovation

Removing barriers to LNG and to gas storage product innovation Rocío Prieto, LNG TF co-chair Ed Freeman, GST TF co-chair Madrid Forum, 6 October 2016 Removing barriers to LNG in European gas Objective

Removing barriers to LNG and to gas storage product innovation Rocío Prieto, LNG TF co-chair Ed Freeman, GST TF co-chair Madrid Forum, 6 October 2016 Removing barriers to LNG in European gas Objective

Implementation Workshop

Brussels 5 October 2017 Implementation Workshop Tariff Network Code Welcome Brussels 5 October 2017 Introduction TAR NC Implementation Workshop Irina Oshchepkova Tariff Subject Manager, ENTSOG Agenda 1.

Brussels 5 October 2017 Implementation Workshop Tariff Network Code Welcome Brussels 5 October 2017 Introduction TAR NC Implementation Workshop Irina Oshchepkova Tariff Subject Manager, ENTSOG Agenda 1.

8.1. GENERAL RULES OF CAPACITY BOOKING

8.1. GENERAL RULES OF CAPACITY BOOKING (a) Pursuant to the provisions of the Gas Supply Act and the Implementation Decree the free capacities of the natural gas network may and shall be offered to network

8.1. GENERAL RULES OF CAPACITY BOOKING (a) Pursuant to the provisions of the Gas Supply Act and the Implementation Decree the free capacities of the natural gas network may and shall be offered to network

INFO SESSION. 9 March :30 17:00. Fluxys Belgium non-binding document for discussion & information purposes only

INFO SESSION 9 March 2017 14:30 17:00 0 Fluxys Belgium non-binding document for discussion & information purposes only 1 Fluxys Belgium non-binding document for discussion & information purposes only 9

INFO SESSION 9 March 2017 14:30 17:00 0 Fluxys Belgium non-binding document for discussion & information purposes only 1 Fluxys Belgium non-binding document for discussion & information purposes only 9

Network codes workshop

4 October 2017 ENTSOG capacity model 2017 Network codes workshop Jan Vitovský Subject Manager, Capacity, ENTSOG Capacity according to Art. 21 CAM NC 1. As from 1 January 2018, transmission system operators

4 October 2017 ENTSOG capacity model 2017 Network codes workshop Jan Vitovský Subject Manager, Capacity, ENTSOG Capacity according to Art. 21 CAM NC 1. As from 1 January 2018, transmission system operators

Consultation on the integration of gas markets of Czech Republic and Austria

Consultation on the integration of gas markets of Czech Republic and Austria TABLE OF CONTENTS A. INTRODUCTION... 3 B. OBJECTIVE OF THE CONSULTATION... 5 C. RULES OF THE PUBLIC CONSULTATION... 5 D. THE

Consultation on the integration of gas markets of Czech Republic and Austria TABLE OF CONTENTS A. INTRODUCTION... 3 B. OBJECTIVE OF THE CONSULTATION... 5 C. RULES OF THE PUBLIC CONSULTATION... 5 D. THE

GTE+ Capacity Product Coordination First Phase Report

First Phase Report Rue Ducale 83 Tel +32 2 209 05 00 gie@gie.eu.com B 1000 Brussels Fax +32 2 209 05 01 www.gie.eu.com Gas Infrastructure Europe (GIE) represents the interest of the infrastructure industry

First Phase Report Rue Ducale 83 Tel +32 2 209 05 00 gie@gie.eu.com B 1000 Brussels Fax +32 2 209 05 01 www.gie.eu.com Gas Infrastructure Europe (GIE) represents the interest of the infrastructure industry

THE ITALIAN REGULATORY AUTHORITY FOR ELECTRICITY GAS AND WATER

RESOLUTION OF 4 AUGUST 2016 464/2016/R/GAS COMPLETING THE IMPLEMENTATION OF EUROPEAN PROVISIONS RELATING TO THE RESOLUTION OF CONGESTIONS AT INTERCONNECTION POINTS WITH OTHER COUNTRIES OF THE NATIONAL

RESOLUTION OF 4 AUGUST 2016 464/2016/R/GAS COMPLETING THE IMPLEMENTATION OF EUROPEAN PROVISIONS RELATING TO THE RESOLUTION OF CONGESTIONS AT INTERCONNECTION POINTS WITH OTHER COUNTRIES OF THE NATIONAL

Implementation of the Balancing Network Code: an overview of TSOs main challenges

Implementation of Balancing Network Code 20 November 2013 Rev 1 Implementation of the Balancing Network Code: an overview of TSOs main challenges ENTSOG AISBL; Av. de Cortenbergh 100, 1000-Brussels; Tel:

Implementation of Balancing Network Code 20 November 2013 Rev 1 Implementation of the Balancing Network Code: an overview of TSOs main challenges ENTSOG AISBL; Av. de Cortenbergh 100, 1000-Brussels; Tel:

New UI Design. Shipper training. October 2015

New UI Design Shipper training October 2015 Agenda Introduction New User Interface: General Changes New User Interface: Registration Process New User Interface: Auctions Special Focus: Within-day New User

New UI Design Shipper training October 2015 Agenda Introduction New User Interface: General Changes New User Interface: Registration Process New User Interface: Auctions Special Focus: Within-day New User

The New Market Model in Austria a case study

The New Market Model in Austria a case study Harald Stindl, Joint Managing Director, Gas Connect Austria Vienna, 31 January 2013 Gas Connect Austria and the OMV Group Gas &Power Activities OMV Group Activities:

The New Market Model in Austria a case study Harald Stindl, Joint Managing Director, Gas Connect Austria Vienna, 31 January 2013 Gas Connect Austria and the OMV Group Gas &Power Activities OMV Group Activities:

Energie-Control Austria Executive Board Ordinance on Provisions for the Gas Market Model (Gas Market Model Ordinance 2012) Title 1 Principles

Title 1 Principles") Energie-Control Austria Executive Board Ordinance on Provisions for the Gas Market Model (Gas Market Model Ordinance 2012) In exercise of section 41 Gaswirtschaftsgesetz (Natural Gas Act) 2011, BGBl. (Federal

Energie-Control Austria Executive Board Ordinance on Provisions for the Gas Market Model (Gas Market Model Ordinance 2012) In exercise of section 41 Gaswirtschaftsgesetz (Natural Gas Act) 2011, BGBl. (Federal

Stakeholder Support Process

CAP0234-12 30 January 2012 Capacity Allocation Mechanisms (CAM) Network Code Stakeholder Support Process Introduction This document explains the purpose of the Stakeholder Support Process for the CAM NC

CAP0234-12 30 January 2012 Capacity Allocation Mechanisms (CAM) Network Code Stakeholder Support Process Introduction This document explains the purpose of the Stakeholder Support Process for the CAM NC

Virtual Workshop on PJM ARR and FTR Market 2017/2018

Virtual Workshop on PJM ARR and FTR Market 2017/2018 PJM State & Member Training Dept. Webex February 10, 2017 PJM 2017 Disclaimer: PJM has made all efforts possible to accurately document all information

Virtual Workshop on PJM ARR and FTR Market 2017/2018 PJM State & Member Training Dept. Webex February 10, 2017 PJM 2017 Disclaimer: PJM has made all efforts possible to accurately document all information

Gas Charging Review. NTSCMF 5 April 2017 Final slide pack Update provided on 3 April All slides added or updated are marked with a blue star

Gas Charging Review Place your chosen image here. The four corners must just cover the arrow tips. For covers, the three pictures should be the same size and in a straight line. NTSCMF 5 April 2017 Final

Gas Charging Review Place your chosen image here. The four corners must just cover the arrow tips. For covers, the three pictures should be the same size and in a straight line. NTSCMF 5 April 2017 Final

Gas Transmission Charging Methodology Statement. Gas Year 2016/17

Gas Transmission Charging Methodology Statement Gas Year 2016/17 Contents 1. Introduction... 3 Part A - POSTALISED CHARGES... 6 2. Process for setting Forecast Postalised Charges... 6 3. Calculation of

Gas Transmission Charging Methodology Statement Gas Year 2016/17 Contents 1. Introduction... 3 Part A - POSTALISED CHARGES... 6 2. Process for setting Forecast Postalised Charges... 6 3. Calculation of

National Grid s specific response to questions raised in E10- GNM-13-03b: ERGEG consultation on Pilot Framework Guidelines on gas balancing rules.

National Grid s specific response to questions raised in E10- GNM-13-03b: ERGEG consultation on Pilot Framework Guidelines on gas balancing rules. Problem identification, scope, definitions, purpose, policy

National Grid s specific response to questions raised in E10- GNM-13-03b: ERGEG consultation on Pilot Framework Guidelines on gas balancing rules. Problem identification, scope, definitions, purpose, policy

Fluxys natural gas transport services in Belgium Indicative Conditions & Tariffs

Fluxys natural gas transport services in Belgium Indicative Conditions & Tariffs Page 1 of 51 Contents 1. Introduction 4 1.1 Natural gas transport services in Belgium: scope 4 1.2 Regulated tariffs 4 1.3

Fluxys natural gas transport services in Belgium Indicative Conditions & Tariffs Page 1 of 51 Contents 1. Introduction 4 1.1 Natural gas transport services in Belgium: scope 4 1.2 Regulated tariffs 4 1.3

The Outlook for a Gas Hub in SE Europe

Greece s Energy Futu re in a Constantly Changing International Environment 19 th N a t i o n a l E n e r g y C o n f e r e n c e E n e r g y a n d D e ve l o p m e n t 2 0 1 4 1 1-1 2 N o v e m b e r 2

Greece s Energy Futu re in a Constantly Changing International Environment 19 th N a t i o n a l E n e r g y C o n f e r e n c e E n e r g y a n d D e ve l o p m e n t 2 0 1 4 1 1-1 2 N o v e m b e r 2

ERGEG Guidelines for Good Practice on Open Season Procedures (GGPOS) Ref: C06-GWG-29-05c 21 May 2007

Ref: C06-GWG-29-05c 21 May 2007") ERGEG Guidelines for Good Practice on Open Season Procedures (GGPOS) Ref: C06-GWG-29-05c 21 May 2007 European Regulators Group for Electricity and Gas Contact: Council of European Energy Regulators ASBL

ERGEG Guidelines for Good Practice on Open Season Procedures (GGPOS) Ref: C06-GWG-29-05c 21 May 2007 European Regulators Group for Electricity and Gas Contact: Council of European Energy Regulators ASBL

Study about models for integration of the Spanish and Portuguese gas markets in a common Iberian Natural Gas Market

Study about models for integration of the Spanish and Portuguese gas markets in a common Iberian Natural Gas Market 6 th June 2014 Public Consultation Document Index Executive summary... 4 1. Introduction...

Study about models for integration of the Spanish and Portuguese gas markets in a common Iberian Natural Gas Market 6 th June 2014 Public Consultation Document Index Executive summary... 4 1. Introduction...

A study on the implementation status of TAR NC in six northwest European countries

A study on the implementation status of TAR NC in six northwest European countries A study for Gasunie Transport Services 1 SAFER, SMARTER, GREENER Presentation outline 1 Introduction DNV GL 2 Introduction

A study on the implementation status of TAR NC in six northwest European countries A study for Gasunie Transport Services 1 SAFER, SMARTER, GREENER Presentation outline 1 Introduction DNV GL 2 Introduction

Gas Target Model. Electricity and Gas Interactions Workshop. Keelin O Brien 3 rd July 2014

Gas Target Model Electricity and Gas Interactions Workshop Keelin O Brien 3 rd July 2014 Madrid Forum Observations Review of work on revision of GTM noted Welcomed considerations of closer coordination

Gas Target Model Electricity and Gas Interactions Workshop Keelin O Brien 3 rd July 2014 Madrid Forum Observations Review of work on revision of GTM noted Welcomed considerations of closer coordination

Interconnector (UK) Limited. IUK Access Code

Limited. IUK Access Code") Interconnector (UK) Limited IUK Access Code Issue 5 March 2018 Contents SECTION A INTRODUCTION... 1 1. IUK Access Code... 1 2. Transportation Services... 1 3. Nominations and Matching Procedures... 1 4.

Interconnector (UK) Limited IUK Access Code Issue 5 March 2018 Contents SECTION A INTRODUCTION... 1 1. IUK Access Code... 1 2. Transportation Services... 1 3. Nominations and Matching Procedures... 1 4.

Overview of issues, solutions and open questions in the CAM NC early implementation process

Overview of issues, solutions and open questions in the CAM NC early implementation process Information for 2 nd CAM Roadmap groups meetings ACER Ljubljana 18 September 2013 Issues and open questions being

Overview of issues, solutions and open questions in the CAM NC early implementation process Information for 2 nd CAM Roadmap groups meetings ACER Ljubljana 18 September 2013 Issues and open questions being

Business Rules. Incremental Proposal

INC00148-14 2 April 2014 DRAFT Business Rules I. Introduction The objective of this document is to specify business rules based on the ACER Guidance for the amendment on the CAM NC and the ACER Tariff

INC00148-14 2 April 2014 DRAFT Business Rules I. Introduction The objective of this document is to specify business rules based on the ACER Guidance for the amendment on the CAM NC and the ACER Tariff

UNOFFICIAL TRANSLATION

UNOFFICIAL TRANSLATION REPUBLIC OF LATVIA PUBLIC UTILITIES COMMISSION COUNCIL RESOLUTION Riga, 13.04.2017 No. 1/16 (Minutes No. 15, para. 4) Rules of Use of the Natural Gas Transmission System 1. The regulations

UNOFFICIAL TRANSLATION REPUBLIC OF LATVIA PUBLIC UTILITIES COMMISSION COUNCIL RESOLUTION Riga, 13.04.2017 No. 1/16 (Minutes No. 15, para. 4) Rules of Use of the Natural Gas Transmission System 1. The regulations

Gas Charging Review. NTSCMF 6 September 2016 Interim Slide Pack - Update to be provided on 1 September 2016.

Gas Charging Review Place your chosen image here. The four corners must just cover the arrow tips. For covers, the three pictures should be the same size and in a straight line. NTSCMF 6 September 2016