Perfect Competition CHAPTER14

|

|

|

- Colleen Burns

- 5 years ago

- Views:

Transcription

1 Perfect Competition CHAPTER14

2 MARKET TYPES The four market types are Perfect competition Monopoly Monopolistic competition Oligopoly

3 MARKET TYPES Perfect Competition Perfect competition exists when Many firms sell an identical product to many buyers. There are no restrictions on entry into (or exit from) the market. Established firms have no advantage over new firms. Sellers and buyers are well informed about prices.

4 Other Market Types Monopoly is a market for a good or service that has no close substitutes and in which there is one supplier that is protected from competition by a barrier preventing the entry of new firms. (patent, natural resource like diamond) Oligopoly is a market in which a small number of firms compete. (media industry) Monopolistic competition is a market in which a large number of firms compete by making similar but slightly different products.(hamburger chains)

5 14.1 A FIRM S PROFIT-MAXIMIZING CHOICES Price Taker A price taker is a firm that cannot influence the price of the good or service that it produces. The firm in perfect competition is a price taker. So, even if it changes production level, it cannot expect to get a higher price.

6 14.1 A FIRM S PROFIT-MAXIMIZING CHOICES Revenue Concepts In perfect competition, market demand and market supply determine price. A firm s total revenue equals the market price multiplied by the quantity sold. A firm s marginal revenue is the change in total revenue that results from a one-unit increase in the quantity sold. Figure 14.1 on the next slide illustrates the revenue concepts.

7 14.1 A FIRM S PROFIT-MAXIMIZING CHOICES Part (a) shows the market for maple syrup. The market price is $8 a can.

8 14.1 A FIRM S PROFIT-MAXIMIZING CHOICES In part (b), the market price determines the demand curve for the Dave s syrup, which is also his marginal revenue curve. So, no matter how much he sells, consumers will pay $8 for each unit.. price taking behavior

9 14.1 A FIRM S PROFIT-MAXIMIZING CHOICES In part (c), if Dave sells 10 cans of syrup a day, his total revenue is $80 a day at point A.

10 14.1 A FIRM S PROFIT-MAXIMIZING CHOICES Dave s total revenue curve is TR. The table shows the calculations of TR and MR.

11 14.1 A FIRM S PROFIT-MAXIMIZING CHOICES Profit-Maximizing Output As output increases, total revenue increases. But total cost also increases. Because of decreasing marginal returns, total cost eventually increases faster than total revenue. Then we can find one output level that maximizes economic profit, and a perfectly competitive firm chooses this output level.

12 Finding the Profit Maximizing Output Level There are 2 approaches to do this: 1. Use total revenue and total cost curves 2. Use marginal analysis (compare MR and MC)

13 14.1 A FIRM S PROFIT-MAXIMIZING CHOICES One way to find the profit-maximizing output is to use a firm s total revenue and total cost curves. Profit is maximized at the output level at which total revenue exceeds total cost by the largest amount.

14 14.1 A FIRM S PROFIT-MAXIMIZING CHOICES Total revenue increases as the quantity increases shown by the TR curve. Total cost increases as the quantity increases shown by the TC curve. As the quantity increases, economic profit (TR TC) increases, reaches a maximum, and then decreases.

15 14.1 A FIRM S PROFIT-MAXIMIZING CHOICES At low output levels, the firm incurs an economic loss. When total revenue exceeds total cost, the firm earns an economic profit. Profit is maximized when the gap between total revenue and total cost is the largest, at 10 cans per day.

16 14.1 A FIRM S PROFIT-MAXIMIZING CHOICES Marginal Analysis and the Supply Decision Marginal analysis compares marginal revenue, MR, with marginal cost, MC.

17 As output increases, marginal revenue remains constant (always at $8) but marginal cost increases. If marginal revenue exceeds marginal cost (if MR > MC), the extra revenue from selling one more unit exceeds the extra cost incurred to produce it. Economic profit increases if output increases.

18 14.1 A FIRM S PROFIT-MAXIMIZING CHOICES If marginal revenue is less than marginal cost (if MR < MC), the extra revenue from selling one more unit is less than the extra cost incurred to produce it. Then if you continue to produce, profits will decrease. Economic profit increases if output decreases.

19 If marginal revenue equals marginal cost (if MR = MC), the extra revenue from selling one more unit is equal to the extra cost incurred to produce it. Economic profit decreases if output increases or decreases, so economic profit is maximized.

20 Maximizing Profit MR>MC..Revenue from each additional unit is more than its cost, profit increases when production goes up MC>MR Cost of each unit is more than the revenue it creates..then decrease production. MR=MC You don t want to change your production anymore..this is max profit output level

21 14.1 A FIRM S PROFIT-MAXIMIZING CHOICES Marginal revenue is a constant $8 per can.

22 Marginal cost decreases at low outputs but then increases.

23 Profit is maximized when marginal revenue equals marginal cost at 10 cans a day.

24 If output increases from 9 to 10 cans a day, marginal cost is $7, which is less than the marginal revenue of $8 and profit increases.

25 If output increases from 10 to 11 cans a day, marginal cost is $9, which exceeds the marginal revenue of $8 and profit decreases.

26 Profit is $29 when output is 10 units..it gives the max profit

27 Temporary Shutdown Decisions If a firm is incurring an economic loss that it believes is temporary, it will remain in the market, and it might produce some output or temporarily shut down.

28 1. If the firm shuts down temporarily, it incurs an economic loss equal to total fixed cost. 2. If the firm produces some output, it incurs an economic loss equal to total fixed cost plus total variable cost (labor needed for production) minus total revenue (sell the production).

29 3. If total revenue exceeds total variable cost, the firm s economic loss is less than total fixed cost. So it pays the firm to produce and incur an economic loss. 4. If total revenue were less than total variable cost, the firm s economic loss would exceed total fixed cost. So the firm would shut down temporarily.

30 If it shuts down, total fixed cost is the largest economic loss that the firm will incur. No cost coming from labor.. The firm s economic loss equals total fixed cost when price equals average variable cost. (TVC=TR) So, if you are selling your production at price P and if the variable cost of each unit you produce (AVC=TVC/Q) is the same as this price, then the only cost of production is the FC. But this is the same as producing nothing..no need to produce..

31 So the firm produces some output if price exceeds average variable cost and shuts down temporarily if average variable cost exceeds price. ***The firm s shutdown point is the output and price at which price equals minimum average variable cost.

32 14.1 A FIRM S PROFIT-MAXIMIZING CHOICES Marginal revenue curve is MR. The firm s cost curves are MC, ATC, and AVC.

33 With a market price (and MR) of $3 a can, the firm minimizes its loss by producing 7 cans a day at its shutdown point. (-15 is the min loss)

34 At the shutdown point, the firms incurs an economic loss equal to total fixed cost. (ATC-AVC=AFC and AFC*Q=TFC)

35 The Firm s Short-Run Supply Curve A perfectly competitive firm s short-run supply curve shows how the firm s profit-maximizing output varies as the price varies, other things remaining the same.

36 14.1 FIRM S CHOICES The firm s marginal cost curve is MC. Its average variable cost curve is AVC, and its marginal revenue curve is MR 0. With a market price (and MR 0 ) of $3 a can, the firm maximizes profit by producing 7 cans a day (MR=MC) at its shutdown point. Point T is one point on the firm s supply curve.

37 14.1 FIRM S CHOICES If the market price rises to $8 a can, the marginal revenue curve shifts upward to MR 1. Profit-maximizing output increases to 10 cans per day. (MR=MC at that point) The black dot in part (b) is another point of the firm s supply curve.

38 MR=MC=8.max profit $29

is another point of the firm s supply curve.")

39 14.1 FIRM S CHOICES If the price rises to $12 a can, the marginal revenue curve shifts upward to MR 2. Profit-maximizing output increases to 11 cans per day. The new black dot in part (b) is another point of the firm s supply curve. The blue curve in part (b) is the firm s supply curve.

40 14.1 FIRM S CHOICES The blue curve is the firm s supply curve. At prices below $3 a can, the firm shuts down and output is zero. At prices above $3 a can, the firm produces along its MC curve. The supply curve is the same as the MC curve at prices above the minimum point of AVC.

41 Market Supply in the Short Run The market supply curve in the short run shows the quantity supplied at each price by a fixed number of firms. The quantity supplied at a given price is the sum of the quantities supplied by all firms at that price.

42 Figure 14.6 shows the market supply curve in a market with 10,000 identical firms. At the shutdown price of $3, each firm produces either 0 or 7 cans a day.

43 14.2 OUTPUT, PRICE, PROFIT IN THE SHORT RUN At prices below the shutdown price, firms produce no output. At prices above the shutdown price, firms produce along their marginal cost curve.

44 14.2 OUTPUT, PRICE, PROFIT IN THE SHORT RUN At prices below the shutdown price, the market supply curve runs along the y-axis.if every firm decides to produce max output is 70,000 at a price of $3 At the shutdown price, the market supply is perfectly elastic. Above the shutdown price, the market supply slopes upward.

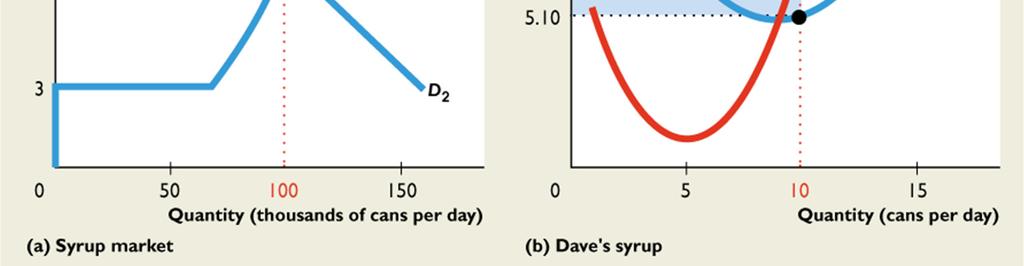

45 When P=$3, we don t know how many firms will produce The Q can be anything between 0 and 70,000.

46 14.2 OUTPUT, PRICE, PROFIT IN THE SHORT RUN Short-Run Equilibrium in Normal Times Market demand and market supply determine the market price and quantity bought and sold. Figure 14.7 on the next slide illustrates short-run equilibrium when the firm makes zero economic profit.

47 In part (a), with market supply curve, S, and market demand curve, D 1, the market price is $5 a can.

48 In part (b), marginal revenue is $5 a can. Dave produces 9 cans a day, where marginal cost equals marginal revenue.

49 At this quantity, price equals average total cost, so Dave makes zero economic profit. (When market is in equilibrium, each firm is making zero profit in normal times. This is the normal profit)

50 Price=MR=MC=ATC

51 Do not confuse this with Shut down point: Price=$3=MR=MC=AVC

52 Short-Run Equilibrium in Good Times In the short-run equilibrium that we ve just examined, Dave made zero economic profit. Although such an outcome is normal, economic profit can be positive or negative in the short run. Figure 14.8 on the next slide illustrates short-run equilibrium when the firm makes a positive economic profit.

53 In part (a), with market demand curve D 2 and market supply curve S, the market price is $8 a can.

54 In part (b), Dave s marginal revenue is $8 a can. Dave produces 10 cans a day, where marginal cost equals marginal revenue.

55 At this quantity, price ($8 a can) exceeds average total cost ($5.10 a can). Dave makes an economic profit shown by the blue rectangle.

56 P> ATC positive profit

57 Short-Run Equilibrium in Bad Times In the short-run equilibrium that we ve just examined, Dave is enjoying an economic profit. But such an outcome is not inevitable. Figure 14.9 on the next slide illustrates short-run equilibrium when the firm incurs an economic loss.

58 In part (a), with the market supply curve, S, and the market market demand curve, D 3, the market price is $3 a can.

59 In part (b), Dave s marginal revenue is $3 a can. Dave produces 7 cans a day, where marginal cost equals marginal revenue and not less than average variable cost.

.")

60 At this quantity, price ($3 a can) is less than average total cost ($5.14 a can). Dave incurs an economic loss shown by the red rectangle.

61 P<ATC..economic loss (negative profit)

62 14.3 OUTPUT, PRICE, PROFIT IN THE LONG RUN Neither good times nor bad times last forever in perfect competition. In the long run, a firm in perfect competition makes zero profit. Figure on the next slide illustrates equilibrium in the long run.

63 Part (a) illustrates the firm in long-run equilibrium. The market price is $5 a can and Dave produces 9 cans a day.

64 In part (a), minimum ATC is $5 a can. In the long run, Dave produces at minimum average total cost.

65 If the price rises above or falls below $5 a can, market forces (entry and exit) move the price back to $5 a can.

66 In the long-run, the price is pulled to $5 a can and Dave makes zero economic profit.

67 In part (b), with this demand curve, price equals minimum average total cost only if the market supply curve is S.

would change supply.")

68 If supply were less than S, the price would exceed $5 a can; if supply were greater than S, the price would be below $5 a can. Market forces (entry and exit) would change supply.(if profit is positive, entry)

69 In long run equilibrium, the market price equals minimum average total cost and the firm makes zero economic profit.

70 14.3 OUTPUT, PRICE, PROFIT IN THE LONG RUN Entry and Exit In the long run, firms respond to economic profit and economic loss by either entering or exiting a market. New firms enter a market in which the existing firms are making positive economic profits. Existing firms exit the market in which firms are incurring economic losses. Entry and exit influence price, the quantity produced, and economic profit.

71 14.3 OUTPUT, PRICE, PROFIT IN THE LONG RUN The immediate effect of the decision to enter or exit is to shift the market supply curve. If more firms enter a market, supply increases and the market supply curve shifts rightward. If firms exit a market, supply decreases and the market supply curve shifts leftward.

72 14.3 OUTPUT, PRICE, PROFIT IN THE LONG RUN The Effects of Entry Economic profit is an incentive for new firms to enter a market, but as they do so, the price falls and the economic profit of each existing firm decreases. Profit=Total Revenue- Total Cost= P*Q-TC

73 14.3 OUTPUT, PRICE, PROFIT IN THE LONG RUN Figure shows the effects of entry. Starting in long-run equilibrium, 1. If demand increases from D 0 to D 1, the price rises from $5 to $8 a can. Firms now make economic profit.

74 14.3 OUTPUT, PRICE, PROFIT IN THE LONG RUN Economic profit brings entry. 2. As firms enter the market, the supply curve shifts rightward, from S 0 to S 1. The equilibrium price falls from $8 to $5 a can, and the quantity produced increases from 100,000 to 140,000 cans a day.

75 14.3 OUTPUT, PRICE, PROFIT IN THE LONG RUN The Effects of Exit Economic loss is an incentive for firms to exit a market, but as they do so, the price rises and the economic loss of each remaining firm decreases.

Firms now make economic losses.")

76 14.3 OUTPUT, PRICE, PROFIT IN THE LONG RUN Figure shows The effects of exit. Starting in long-run equilibrium, 1. If demand decreases from D 0 to D 2, the price falls from $5 to $3 a can. (which is the shutdown point) Firms now make economic losses. (P higher than ATC)

77 14.3 OUTPUT, PRICE, PROFIT IN THE LONG RUN Economic loss brings exit. 2. As firms exit the market, the supply curve shifts leftward, from S 0 to S 2. The equilibrium price rises from $3 to $5 a can, and the quantity produced decreases from 70,000 to 50,000 cans a day.

78 A Change in Demand The only difference between the initial long-run equilibrium and the final long-run equilibrium is the number of firms in the market.( cause price will be the same eventually). An increase in demand increases the number of firms. Each firm produces the same output in the new long-run equilibrium as initially and makes zero economic profit. In the process of moving from the initial equilibrium to the new one, firms make positive economic profits.

79 14.3 OUTPUT, PRICE, PROFIT IN THE LONG RUN A decrease in demand triggers a similar response, except in the opposite direction. The decrease in demand brings a lower price, economic loss, and some firms exit. Exit decreases market supply and eventually raises the price to its original level.

80 Technological Change New technology allows firms to produce at a lower cost. As a result, as firms adopt a new technology, their cost curves shift downward. Market supply increases, and the market supply curve shifts rightward. With a given demand, the quantity produced increases and the price falls.

81 14.3 OUTPUT, PRICE, PROFIT IN THE LONG RUN Two forces are at work in a market undergoing technological change. 1. Firms that adopt the new technology make an economic profit. So new-technology firms have an incentive to enter. 2. Firms that stick with the old technology incur economic losses. These firms either exit the market or switch to the new technology.

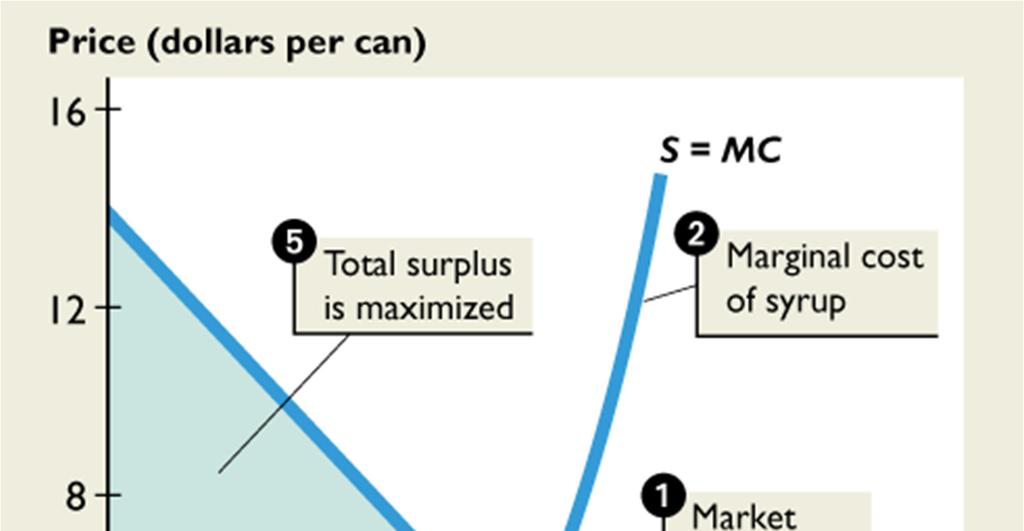

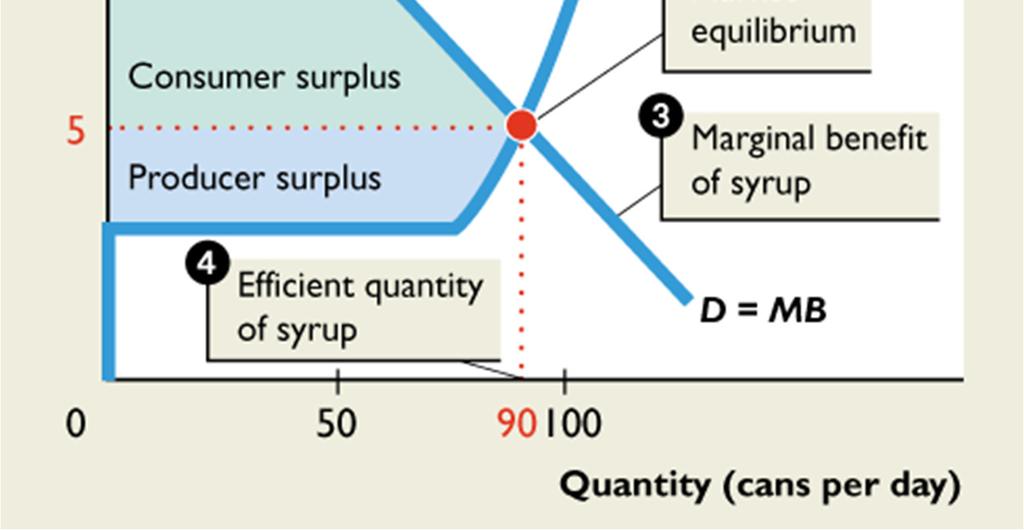

82 14.3 OUTPUT, PRICE, PROFIT IN THE LONG RUN Is Perfect Competition Efficient? Resources are used efficiently when it is not possible to get more of one good without giving up something that is valued more highly. To achieve this outcome, marginal benefit must equal marginal cost. That is what perfect competition achieves. The market supply curve is the marginal cost curve. It is the sum of the firms marginal cost curves at all points above the minimum of average variable cost (the shutdown price).

83 14.3 OUTPUT, PRICE, PROFIT IN THE LONG RUN The market supply curve is the marginal cost curve. The market demand curve is the marginal benefit curve. Because the market supply and market demand curves intersect at the equilibrium price, that price equals both marginal cost and marginal benefit. Figure on the next slide shows the efficiency of perfect competition.

84 14.3 OUTPUT, PRICE, PROFIT IN THE LONG RUN 1. Market equilibrium occurs at a price of $5 a can and a quantity of 90 cans a day. 2. Supply curve is also the marginal cost curve. 3. Demand curve is also the marginal benefit curve.

85 14.3 OUTPUT, PRICE, PROFIT IN THE LONG RUN Because marginal benefit equals marginal cost 4. Efficient quantity is produced. 5. Total surplus (sum of consumer surplus and producer surplus) is maximized.

86

87 14.3 OUTPUT, PRICE, PROFIT IN THE LONG RUN Is Perfect Competition Fair? Perfect competition places no restrictions on anyone s actions everyone is free to try to make an economic profit. The process of competition eliminates economic profit and brings maximum attainable benefit to consumers. Fairness as equality of opportunity and fairness as equality of outcomes are achieved in long-run equilibrium.

88 14.3 OUTPUT, PRICE, PROFIT IN THE LONG RUN But in the short run, economic profit and economic loss can arise. These unequal outcomes might seem unfair.

2010 Pearson Education Canada

What Is Perfect Competition? Perfect competition is an industry in which Many firms sell identical products to many buyers. There are no restrictions to entry into the industry. Established firms have

What Is Perfect Competition? Perfect competition is an industry in which Many firms sell identical products to many buyers. There are no restrictions to entry into the industry. Established firms have

Where are we? Second midterm on November 19. Review questions on th course web site. Today: chapter on perfect competition

Where are we? Second midterm on November 19 Review questions on th course web site. Today: chapter on perfect competition Topic for the second paper: Pick a chapter in Ariely after Chapter 4 and compare

Where are we? Second midterm on November 19 Review questions on th course web site. Today: chapter on perfect competition Topic for the second paper: Pick a chapter in Ariely after Chapter 4 and compare

Lecture 11. Firms in competitive markets

Lecture 11 Firms in competitive markets By the end of this lecture, you should understand: what characteristics make a market competitive how competitive firms decide how much output to produce how competitive

Lecture 11 Firms in competitive markets By the end of this lecture, you should understand: what characteristics make a market competitive how competitive firms decide how much output to produce how competitive

CH 14: Perfect Competition

CH 14: Perfect Competition Characteristics of Perfect Competition 1. Both buyers and sellers are price takers A price taker is a firm (or individual) who takes the price determined by market supply and

CH 14: Perfect Competition Characteristics of Perfect Competition 1. Both buyers and sellers are price takers A price taker is a firm (or individual) who takes the price determined by market supply and

CH 13. Name: Class: Date: Multiple Choice Identify the choice that best completes the statement or answers the question.

Class: Date: CH 13 Multiple Choice Identify the choice that best completes the statement or answers the question. 1. One requirement for an industry to be perfectly competitive is that a. sellers and buyers

Class: Date: CH 13 Multiple Choice Identify the choice that best completes the statement or answers the question. 1. One requirement for an industry to be perfectly competitive is that a. sellers and buyers

MULTIPLE CHOICE. Choose the one alternative that best completes the statement or answers the question.

PRACTICE FOR PERFECT COMPETITION Fatma Nur Karaman MULTIPLE CHOICE. Choose the one alternative that best completes the statement or answers the question. 1) What is the difference between perfect competition

PRACTICE FOR PERFECT COMPETITION Fatma Nur Karaman MULTIPLE CHOICE. Choose the one alternative that best completes the statement or answers the question. 1) What is the difference between perfect competition

INTRODUCTION ECONOMIC PROFITS

INTRODUCTION This chapter addresses the following key questions: What are profits? What are the unique characteristics of competitive firms? How much output will a competitive firm produce? Chapter 7 THE

INTRODUCTION This chapter addresses the following key questions: What are profits? What are the unique characteristics of competitive firms? How much output will a competitive firm produce? Chapter 7 THE

2007 Thomson South-Western

WHAT IS A COMPETITIVE MARKET? A competitive market has many buyers and sellers trading identical products so that each buyer and seller is a price taker. Buyers and sellers must accept the price determined

WHAT IS A COMPETITIVE MARKET? A competitive market has many buyers and sellers trading identical products so that each buyer and seller is a price taker. Buyers and sellers must accept the price determined

Firms in Competitive Markets

1 Basic Economics Chapter 14 Firms in Competitive Markets Competitive markets (1) Market with many buyers and sellers (e.g., ) (2) Trading identical products (e.g., ) (3) Each buyer and seller is a price

1 Basic Economics Chapter 14 Firms in Competitive Markets Competitive markets (1) Market with many buyers and sellers (e.g., ) (2) Trading identical products (e.g., ) (3) Each buyer and seller is a price

PRICES, PROFITS, AND INDUSTRY PERFORMANCE P A R T

PRICES, PROFITS, AND INDUSTRY PERFORMANCE P A R T 5 Perfect Competition CHAPTER13 CHAPTER CHECKLIST When you have completed your study of this chapter, you will be able to 1 Explain a perfectly competitive

PRICES, PROFITS, AND INDUSTRY PERFORMANCE P A R T 5 Perfect Competition CHAPTER13 CHAPTER CHECKLIST When you have completed your study of this chapter, you will be able to 1 Explain a perfectly competitive

Slides and Images, Worth Publishers Inc. 8-1

Perfect Competition Michael J. Murray Slides and Images, Worth Publishers Inc. 8-1 Market Structure Analysis By observing a few industry characteristics, we can predict pricing and output behavior of the

Perfect Competition Michael J. Murray Slides and Images, Worth Publishers Inc. 8-1 Market Structure Analysis By observing a few industry characteristics, we can predict pricing and output behavior of the

Unit 6 Perfect Competition and Monopoly - Practice Problems

Unit 6 Perfect Competition and Monopoly - Practice Problems Multiple Choice Identify the choice that best completes the statement or answers the question. 1. One characteristic of a perfectly competitive

Unit 6 Perfect Competition and Monopoly - Practice Problems Multiple Choice Identify the choice that best completes the statement or answers the question. 1. One characteristic of a perfectly competitive

Course informa-on. Final exam. If you have a conflict, go to the Registrar s office for a form to bring to me

Course informa-on Final exam If you have a conflict, go to the Registrar s office for a form to bring to me To do today: Finish compe--on and start monopoly What it is and does: single price and price

Course informa-on Final exam If you have a conflict, go to the Registrar s office for a form to bring to me To do today: Finish compe--on and start monopoly What it is and does: single price and price

Some of the assumptions of perfect competition include:

This session focuses on how managers determine the optimal price, quantity and advertising decisions under perfect competition. In earlier sessions we have looked at the nature of competitive markets.

This session focuses on how managers determine the optimal price, quantity and advertising decisions under perfect competition. In earlier sessions we have looked at the nature of competitive markets.

Monopoly and How It Arises

13 MONOPOLY Monopoly and How It Arises A monopoly is a market: That produces a good or service for which no close substitute exists If a good has a close substitute, even if it is produced by only one

13 MONOPOLY Monopoly and How It Arises A monopoly is a market: That produces a good or service for which no close substitute exists If a good has a close substitute, even if it is produced by only one

CH 15: Monopoly. Lecture

CH 15: Monopoly Lecture Characteristics of Monopolies A monopoly is a market structure in which one firm makes up the entire market Firm=Industry Characteristics of Monopolies The monopolist is a price

CH 15: Monopoly Lecture Characteristics of Monopolies A monopoly is a market structure in which one firm makes up the entire market Firm=Industry Characteristics of Monopolies The monopolist is a price

Principles of Microeconomics Module 5.1. Understanding Profit

Principles of Microeconomics Module 5.1 Understanding Profit 180 Production Choices of Firms All firms have one goal in mind: MAX PROFITS PROFITS = TOTAL REVENUE TOTAL COST Two ways to reach this goal:

Principles of Microeconomics Module 5.1 Understanding Profit 180 Production Choices of Firms All firms have one goal in mind: MAX PROFITS PROFITS = TOTAL REVENUE TOTAL COST Two ways to reach this goal:

Quiz #5 Week 04/12/2009 to 04/18/2009

Quiz #5 Week 04/12/2009 to 04/18/2009 You have 30 minutes to answer the following 17 multiple choice questions. Record your answers in the bubble sheet. Your grade in this quiz will count for 1% of your

Quiz #5 Week 04/12/2009 to 04/18/2009 You have 30 minutes to answer the following 17 multiple choice questions. Record your answers in the bubble sheet. Your grade in this quiz will count for 1% of your

CONTENTS. Introduction to the Series. 1 Introduction to Economics 5 2 Competitive Markets, Demand and Supply Elasticities 37

CONTENTS Introduction to the Series iv 1 Introduction to Economics 5 2 Competitive Markets, Demand and Supply 17 3 Elasticities 37 4 Government Intervention in Markets 44 5 Market Failure 53 6 Costs of

CONTENTS Introduction to the Series iv 1 Introduction to Economics 5 2 Competitive Markets, Demand and Supply 17 3 Elasticities 37 4 Government Intervention in Markets 44 5 Market Failure 53 6 Costs of

FINALTERM EXAMINATION FALL 2006

FINALTERM EXAMINATION FALL 2006 QUESTION NO: 1 (MARKS: 1) - PLEASE CHOOSE ONE Compared to the equilibrium price and quantity sold in a competitive market, a monopolist Will charge a price and sell a quantity.

FINALTERM EXAMINATION FALL 2006 QUESTION NO: 1 (MARKS: 1) - PLEASE CHOOSE ONE Compared to the equilibrium price and quantity sold in a competitive market, a monopolist Will charge a price and sell a quantity.

Perfect Competition CHAPTER 14. Alfred P. Sloan. There s no resting place for an enterprise in a competitive economy. Perfect Competition 14

CHATER 14 erfect Competition There s no resting place for an enterprise in a competitive economy. Alfred. Sloan McGraw-Hill/Irwin Copyright 2010 by the McGraw-Hill Companies, Inc. All rights reserved.

CHATER 14 erfect Competition There s no resting place for an enterprise in a competitive economy. Alfred. Sloan McGraw-Hill/Irwin Copyright 2010 by the McGraw-Hill Companies, Inc. All rights reserved.

Firms in Competitive Markets

14 Firms in Competitive Markets PowerPoint Slides prepared by: Andreea CHIRITESCU Eastern Illinois University 1 What is a Competitive Market? Competitive market Perfectly competitive market Market with

14 Firms in Competitive Markets PowerPoint Slides prepared by: Andreea CHIRITESCU Eastern Illinois University 1 What is a Competitive Market? Competitive market Perfectly competitive market Market with

Econ 2113: Principles of Microeconomics. Spring 2009 ECU

Econ 2113: Principles of Microeconomics Spring 2009 ECU Chapter 12 Monopoly Market Power Market power is the ability to influence the market, and in particular the market price, by influencing the total

Econ 2113: Principles of Microeconomics Spring 2009 ECU Chapter 12 Monopoly Market Power Market power is the ability to influence the market, and in particular the market price, by influencing the total

Week One What is economics? Chapter 1

Week One What is economics? Chapter 1 Economics: is the social science that studies the choices that individuals, businesses, governments, and entire societies make as they cope with scarcity and the incentives

Week One What is economics? Chapter 1 Economics: is the social science that studies the choices that individuals, businesses, governments, and entire societies make as they cope with scarcity and the incentives

MICROECONOMICS - CLUTCH CH PERFECT COMPETITION.

!! www.clutchprep.com CONCEPT: THE FOUR MARKET MODELS Market structure describes the environment in which a firm operates, determined by the Perfect Competition Monopolistic Competition Oligopoly Monopoly

!! www.clutchprep.com CONCEPT: THE FOUR MARKET MODELS Market structure describes the environment in which a firm operates, determined by the Perfect Competition Monopolistic Competition Oligopoly Monopoly

Monopoly CHAPTER 15. Henry Demarest Lloyd. Monopoly is business at the end of its journey. Monopoly 15. McGraw-Hill/Irwin

CHAPTER 15 Monopoly Monopoly is business at the end of its journey. Henry Demarest Lloyd McGraw-Hill/Irwin Copyright 2010 by the McGraw-Hill Companies, Inc. All rights reserved. A Monopolistic Market A

CHAPTER 15 Monopoly Monopoly is business at the end of its journey. Henry Demarest Lloyd McGraw-Hill/Irwin Copyright 2010 by the McGraw-Hill Companies, Inc. All rights reserved. A Monopolistic Market A

WHAT IS A COMPETITIVE MARKET?

Chapter 14. Firms in Competitive Markets WHAT IS A COMPETITIVE MARKET? A perfectly competitive market has the following characteristics: There are many buyers and sellers in the market. small relative

Chapter 14. Firms in Competitive Markets WHAT IS A COMPETITIVE MARKET? A perfectly competitive market has the following characteristics: There are many buyers and sellers in the market. small relative

Chapter 13. Microeconomics. Monopolistic Competition: The Competitive Model in a More Realistic Setting

Microeconomics Modified by: Yun Wang Florida International University Spring, 2018 1 Chapter 13 Monopolistic Competition: The Competitive Model in a More Realistic Setting Chapter Outline 13.1 Demand and

Microeconomics Modified by: Yun Wang Florida International University Spring, 2018 1 Chapter 13 Monopolistic Competition: The Competitive Model in a More Realistic Setting Chapter Outline 13.1 Demand and

Practice Exam 3: S201 Walker Fall 2009

Practice Exam 3: S201 Walker Fall 2009 I. Multiple Choice (3 points each) 1. Which of the following statements about the short-run is false? A. The marginal product of labor may increase or decrease. B.

Practice Exam 3: S201 Walker Fall 2009 I. Multiple Choice (3 points each) 1. Which of the following statements about the short-run is false? A. The marginal product of labor may increase or decrease. B.

Monopoly. 3 Microeconomics LESSON 5. Introduction and Description. Time Required. Materials

LESSON 5 Monopoly Introduction and Description Lesson 5 extends the theory of the firm to the model of a Students will see that the profit-maximization rules for the monopoly are the same as they were

LESSON 5 Monopoly Introduction and Description Lesson 5 extends the theory of the firm to the model of a Students will see that the profit-maximization rules for the monopoly are the same as they were

Firms in Competitive Markets. UAPP693 Economics in the Public & Nonprofit Sectors Steven W. Peuquet, Ph.D.

Firms in Competitive Markets UAPP693 Economics in the Public & Nonprofit Sectors Steven W. Peuquet, Ph.D. 1 These slides are for use only as part of a formal instructional course and may not be copied,

Firms in Competitive Markets UAPP693 Economics in the Public & Nonprofit Sectors Steven W. Peuquet, Ph.D. 1 These slides are for use only as part of a formal instructional course and may not be copied,

23 Perfect Competition

23 Perfect Competition Learning Objectives After you have studied this chapter, you should be able to 1. define price taker, total revenues, marginal revenue, short-run shutdown price, short-run breakeven

23 Perfect Competition Learning Objectives After you have studied this chapter, you should be able to 1. define price taker, total revenues, marginal revenue, short-run shutdown price, short-run breakeven

- pure monopoly: only one seller of a good/service with no close substitutes

Micro 101, Chapter 10 1 Chapter 10: Monopoly Main objectives: 1. Define what constitutes a monopoly - pure monopoly: only one seller of a good/service with no close substitutes 2. Describe types of barriers

Micro 101, Chapter 10 1 Chapter 10: Monopoly Main objectives: 1. Define what constitutes a monopoly - pure monopoly: only one seller of a good/service with no close substitutes 2. Describe types of barriers

Ch. 9 LECTURE NOTES 9-1

Ch. 9 LECTURE NOTES I. Four market models will be addressed in Chapters 9-11; characteristics of the models are summarized in Table 9.1. A. Pure competition entails a large number of firms, standardized

Ch. 9 LECTURE NOTES I. Four market models will be addressed in Chapters 9-11; characteristics of the models are summarized in Table 9.1. A. Pure competition entails a large number of firms, standardized

Practice Exam 3: S201 Walker Fall with answers to MC

Practice Exam 3: S201 Walker Fall 2007 - with answers to MC Print Your Name: I. Multiple Choice (3 points each) 1. If marginal utility is falling then A. total utility must be falling. B. marginal utility

Practice Exam 3: S201 Walker Fall 2007 - with answers to MC Print Your Name: I. Multiple Choice (3 points each) 1. If marginal utility is falling then A. total utility must be falling. B. marginal utility

ECON 102 Kagundu Final Exam (New Material) Practice Exam Solutions

Practice Exam Solutions") www.liontutors.com ECON 102 Kagundu Final Exam (New Material) Practice Exam Solutions 1. A A large number of firms will be able to operate in the industry because you only need to produce a small amount

www.liontutors.com ECON 102 Kagundu Final Exam (New Material) Practice Exam Solutions 1. A A large number of firms will be able to operate in the industry because you only need to produce a small amount

Introduction. Learning Objectives. Chapter 24. Perfect Competition

Chapter 24 Perfect Competition Introduction Estimates indicate that since 2003, the total amount of stored digital data on planet Earth has increased from 5 exabytes to more than 200 exabytes. Accompanying

Chapter 24 Perfect Competition Introduction Estimates indicate that since 2003, the total amount of stored digital data on planet Earth has increased from 5 exabytes to more than 200 exabytes. Accompanying

Chapter 1- Introduction

Chapter 1- Introduction A SIMPLE ECONOMY Central PROBLEMS OF AN ECONOMY: scarcity of resources problem of choice Every society has to decide on how to use its scarce resources. Production, exchange and

Chapter 1- Introduction A SIMPLE ECONOMY Central PROBLEMS OF AN ECONOMY: scarcity of resources problem of choice Every society has to decide on how to use its scarce resources. Production, exchange and

Teaching about Market Structures

Teaching about Market Structures Felix B. Kwan, Ph.D. Professor of Econ/Finance, Maryville University AP Econ Conference - FRB St. Louis June 17-19, 2015 Profits Foundational Concepts Some basic terms/concepts

Teaching about Market Structures Felix B. Kwan, Ph.D. Professor of Econ/Finance, Maryville University AP Econ Conference - FRB St. Louis June 17-19, 2015 Profits Foundational Concepts Some basic terms/concepts

Chapter 6. Competition

Chapter 6 Competition Copyright 2014 McGraw-Hill Education. All rights reserved. No reproduction or distribution without the prior written consent of McGraw-Hill Education. 1-1 Chapter 6 The goal of this

Chapter 6 Competition Copyright 2014 McGraw-Hill Education. All rights reserved. No reproduction or distribution without the prior written consent of McGraw-Hill Education. 1-1 Chapter 6 The goal of this

MARKETS. Part Review. Reading Between the Lines SONY CORP. HAS CUT THE U.S. PRICE OF ITS PLAYSTATION 2

Part Review 4 FIRMS AND MARKETS Reading Between the Lines SONY CORP. HAS CUT THE U.S. PRICE OF ITS PLAYSTATION 2 On May 14, 2002 Sony announced it was cutting the cost of its PlayStation 2 by 33 percent,

Part Review 4 FIRMS AND MARKETS Reading Between the Lines SONY CORP. HAS CUT THE U.S. PRICE OF ITS PLAYSTATION 2 On May 14, 2002 Sony announced it was cutting the cost of its PlayStation 2 by 33 percent,

ECON 102 Brown Final Exam Practice Exam Solutions

www.liontutors.com ECON 102 Brown Final Exam Practice Exam Solutions 1. B 2. C 3. C All products are identical (homogenous) in perfect competition so there is no such thing as brand preference. 4. C Breakeven

www.liontutors.com ECON 102 Brown Final Exam Practice Exam Solutions 1. B 2. C 3. C All products are identical (homogenous) in perfect competition so there is no such thing as brand preference. 4. C Breakeven

ECON 311 MICROECONOMICS THEORY I

ECON 311 MICROECONOMICS THEORY I Profit Maximisation & Perfect Competition (Short-Run) Dr. F. Kwame Agyire-Tettey Department of Economics Contact Information: fagyire-tettey@ug.edu.gh Session Overview

ECON 311 MICROECONOMICS THEORY I Profit Maximisation & Perfect Competition (Short-Run) Dr. F. Kwame Agyire-Tettey Department of Economics Contact Information: fagyire-tettey@ug.edu.gh Session Overview

MICROECONOMICS CHAPTER 10A/23 PERFECT COMPETITION. Professor Charles Fusi

MICROECONOMICS CHAPTER 10A/23 PERFECT COMPETITION Professor Charles Fusi Learning Objectives Identify the characteristics of a perfectly competitive market structure Discuss the process by which a perfectly

MICROECONOMICS CHAPTER 10A/23 PERFECT COMPETITION Professor Charles Fusi Learning Objectives Identify the characteristics of a perfectly competitive market structure Discuss the process by which a perfectly

= AFC + AVC = (FC + VC)

") Chapter 13-14: Marginal Product, Costs, Revenue, and Profit Production Function The relationship between the quantity of inputs (workers) and quantity of outputs Total product (TP) is the total amount

Chapter 13-14: Marginal Product, Costs, Revenue, and Profit Production Function The relationship between the quantity of inputs (workers) and quantity of outputs Total product (TP) is the total amount

Total revenue Quantity. Price Quantity Quantity

s in Competitive Markets WHAT IS A COMPETITIVE MARKET? A perfectly competitive market has the following characteristics: There are many buyers and sellers in the market. The goods offered by the various

s in Competitive Markets WHAT IS A COMPETITIVE MARKET? A perfectly competitive market has the following characteristics: There are many buyers and sellers in the market. The goods offered by the various

Perfect competition: occurs when none of the individual market participants (ie buyers or sellers) can influence the price of the product.

can influence the price of the product.") Perfect Competition In this section of work and the next one we derive the equilibrium positions of firms in order to determine whether or not it is profitable for a firm to produce and, if so, what quantities

Perfect Competition In this section of work and the next one we derive the equilibrium positions of firms in order to determine whether or not it is profitable for a firm to produce and, if so, what quantities

What is a Competitive Market?

Firms in Competitive Markets Competitive market (1) Market with many buyers and sellers (e.g., ) (2) Trading identical products (e.g., ) (3) Each buyer and seller is a price taker (no price influence)

Firms in Competitive Markets Competitive market (1) Market with many buyers and sellers (e.g., ) (2) Trading identical products (e.g., ) (3) Each buyer and seller is a price taker (no price influence)

Quiz #4 Week 04/05/2009 to 04/11/2009

Quiz #4 Week 04/05/2009 to 04/11/2009 You have 30 minutes to answer the following 15 multiple choice questions. Record your answers in the bubble sheet. Your grade in this quiz will count for 1% of your

Quiz #4 Week 04/05/2009 to 04/11/2009 You have 30 minutes to answer the following 15 multiple choice questions. Record your answers in the bubble sheet. Your grade in this quiz will count for 1% of your

Chapter 11 Perfect Competition

Chapter 11 Perfect Competition Introduction: To an economist, a competitive firm is a firm that does not determine its market price. This type of firm is free to sell as many units of its good as it wishes

Chapter 11 Perfect Competition Introduction: To an economist, a competitive firm is a firm that does not determine its market price. This type of firm is free to sell as many units of its good as it wishes

AGENDA Mon 10/12. Economics in Action Review QOD #21: Competitive Farming HW Review Pure Competition MR = MC HW: Read pp Q #7

AGENDA Mon 10/12 Economics in Action Review QOD #21: Competitive Farming HW Review Pure Competition MR = MC HW: Read pp 173-176 Q #7 QOD #21: Competitive Farming A purely competitive wheat farmer can sell

AGENDA Mon 10/12 Economics in Action Review QOD #21: Competitive Farming HW Review Pure Competition MR = MC HW: Read pp 173-176 Q #7 QOD #21: Competitive Farming A purely competitive wheat farmer can sell

Principles of. Economics. Week 6. Firm in Competitive & Monopoly market. 7 th April 2014

Principles of Economics Week 6 Firm in Competitive & Monopoly market 7 th April 2014 In this week, look for the answers to these questions:!what is a perfectly competitive market?!what is marginal revenue?

Principles of Economics Week 6 Firm in Competitive & Monopoly market 7 th April 2014 In this week, look for the answers to these questions:!what is a perfectly competitive market?!what is marginal revenue?

Chapter Summary and Learning Objectives

CHAPTER 11 Firms in Perfectly Competitive Markets Chapter Summary and Learning Objectives 11.1 Perfectly Competitive Markets (pages 369 371) Explain what a perfectly competitive market is and why a perfect

CHAPTER 11 Firms in Perfectly Competitive Markets Chapter Summary and Learning Objectives 11.1 Perfectly Competitive Markets (pages 369 371) Explain what a perfectly competitive market is and why a perfect

Monopoly. Cost. Average total cost. Quantity of Output

While a competitive firm is a price taker, a monopoly firm is a price maker. A firm is considered a monopoly if... it is the sole seller of its product. its product does not have close substitutes. The

While a competitive firm is a price taker, a monopoly firm is a price maker. A firm is considered a monopoly if... it is the sole seller of its product. its product does not have close substitutes. The

FIRMS IN COMPETITIVE MARKETS

14 FIRMS IN COMPETITIVE MARKETS WHAT S NEW IN THE FOURTH EDITION: The rules for profit maximization are written more clearly. LEARNING OBJECTIVES: By the end of this chapter, students should understand:

14 FIRMS IN COMPETITIVE MARKETS WHAT S NEW IN THE FOURTH EDITION: The rules for profit maximization are written more clearly. LEARNING OBJECTIVES: By the end of this chapter, students should understand:

Lesson 3-2 Profit Maximization

Lesson 3-2 Profit Maximization Standard 3b: Students will explain the 5 dimensions of market structure and identify how perfect competition, monopoly, monopolistic competition, and oligopoly are characterized

Lesson 3-2 Profit Maximization Standard 3b: Students will explain the 5 dimensions of market structure and identify how perfect competition, monopoly, monopolistic competition, and oligopoly are characterized

Monopolistic Competition

Monopolistic Competition CHAPTER16 C H A P T E R C H E C K L I S T When you have completed your study of this chapter, you will be able to 1 Describe and identify monopolistic competition. 2 Explain how

Monopolistic Competition CHAPTER16 C H A P T E R C H E C K L I S T When you have completed your study of this chapter, you will be able to 1 Describe and identify monopolistic competition. 2 Explain how

Market structures. Why Monopolies Arise. Why Monopolies Arise. Market power. Monopoly. Monopoly resources

Market structures Why Monopolies Arise Market power Alters the relationship between a firm s costs and the selling price Charges a price that exceeds marginal cost A high price reduces the quantity purchased

Market structures Why Monopolies Arise Market power Alters the relationship between a firm s costs and the selling price Charges a price that exceeds marginal cost A high price reduces the quantity purchased

2000 AP Microeconomics Exam Answers

2000 AP Microeconomics Exam Answers 1. B Scarcity is the main economic problem!!! 2. D If the wages of farm workers and movie theater employee increase, the supply of popcorn and movies will decrease (shift

2000 AP Microeconomics Exam Answers 1. B Scarcity is the main economic problem!!! 2. D If the wages of farm workers and movie theater employee increase, the supply of popcorn and movies will decrease (shift

Monopoly. Basic Economics Chapter 15. Why Monopolies Arise. Monopoly

1 Why Monopolies Arise Basic Economics Chapter 15 Monopoly Monopoly - The monopolist is a firm that is the sole seller of a product (or service) without close substitutes - The monopolist is a price maker

1 Why Monopolies Arise Basic Economics Chapter 15 Monopoly Monopoly - The monopolist is a firm that is the sole seller of a product (or service) without close substitutes - The monopolist is a price maker

Monopoly and How It Arises

Monopoly and How It Arises A monopoly is a market: That produces a good or service for which no close substitute exists In which there is one supplier that is protected from competition by a barrier preventing

Monopoly and How It Arises A monopoly is a market: That produces a good or service for which no close substitute exists In which there is one supplier that is protected from competition by a barrier preventing

ECON 102 Brown Final Exam (New Material) Practice Exam Solutions

Practice Exam Solutions") www.liontutors.com ECON 102 Brown Final Exam (New Material) Practice Exam Solutions 1. B A very large percent of their earnings comes from economic rent 2. B Any funds left, after everyone who has a claim

www.liontutors.com ECON 102 Brown Final Exam (New Material) Practice Exam Solutions 1. B A very large percent of their earnings comes from economic rent 2. B Any funds left, after everyone who has a claim

CHAPTER NINE MONOPOLY

CHAPTER NINE MONOPOLY This chapter examines how a market controlled by a single producer behaves. What price will a monopolist charge for his output? How much will he produce? The basic characteristics

CHAPTER NINE MONOPOLY This chapter examines how a market controlled by a single producer behaves. What price will a monopolist charge for his output? How much will he produce? The basic characteristics

Monopoly. PowerPoint Slides prepared by: Andreea CHIRITESCU Eastern Illinois University

15 Monopoly PowerPoint Slides prepared by: Andreea CHIRITESCU Eastern Illinois University 1 Market power Why Monopolies Arise Alters the relationship between a firm s costs and the selling price Monopoly

15 Monopoly PowerPoint Slides prepared by: Andreea CHIRITESCU Eastern Illinois University 1 Market power Why Monopolies Arise Alters the relationship between a firm s costs and the selling price Monopoly

ECON 2100 Principles of Microeconomics (Summer 2016) Behavior of Firms in Perfectly Competitive Markets

Behavior of Firms in Perfectly Competitive Markets") ECON 21 Principles of Microeconomics (Summer 216) Behavior of Firms in Perfectly Competitive Markets Relevant readings from the textbook: Mankiw, Ch. 14 Firms in Competitive Markets Suggested problems

ECON 21 Principles of Microeconomics (Summer 216) Behavior of Firms in Perfectly Competitive Markets Relevant readings from the textbook: Mankiw, Ch. 14 Firms in Competitive Markets Suggested problems

ECON 102 Wooten Final Exam Practice Exam Solutions

www.liontutors.com ECON 102 Wooten Final Exam Practice Exam Solutions 1. A monopolist will increase price and decrease quantity to maximize profits when compared to perfect competition because a monopolist

www.liontutors.com ECON 102 Wooten Final Exam Practice Exam Solutions 1. A monopolist will increase price and decrease quantity to maximize profits when compared to perfect competition because a monopolist

Pure Competition in the Short Run

08 Pure Competition in the Short Run McGraw-Hill/Irwin Copyright 2012 by The McGraw-Hill Companies, Inc. All rights reserved. LO1 8-2 Four Market Models Pure competition Pure monopoly Monopolistic competition

08 Pure Competition in the Short Run McGraw-Hill/Irwin Copyright 2012 by The McGraw-Hill Companies, Inc. All rights reserved. LO1 8-2 Four Market Models Pure competition Pure monopoly Monopolistic competition

Microeonomics. Firms in Competitive Markets. In this chapter, look for the answers to these questions: Introduction: A Scenario. N.

C H A T E R 14 Firms in Competitive Markets R I N C I L E S O F Microeonomics N. Gregory Mankiw remium oweroint Slides by Ron Cronovich 2009 South-Western, a part of Cengage Learning, all rights reserved

C H A T E R 14 Firms in Competitive Markets R I N C I L E S O F Microeonomics N. Gregory Mankiw remium oweroint Slides by Ron Cronovich 2009 South-Western, a part of Cengage Learning, all rights reserved

ECON 101 Introduction to Economics1

ECON 101 Introduction to Economics1 Session 11 Market Structures(Perfect Competition) Lecturer: Mrs. Hellen A. Seshie-Nasser, Department of Economics Contact Information: haseshie@ug.edu.gh College of

ECON 101 Introduction to Economics1 Session 11 Market Structures(Perfect Competition) Lecturer: Mrs. Hellen A. Seshie-Nasser, Department of Economics Contact Information: haseshie@ug.edu.gh College of

2007 Thomson South-Western

Monopolistic Competition Characteristics: Many sellers Product differentiation Free entry and exit In the long run, profits are driven to zero Firms have some control over price What does the costs graph

Monopolistic Competition Characteristics: Many sellers Product differentiation Free entry and exit In the long run, profits are driven to zero Firms have some control over price What does the costs graph

4. Which of the following statements about marginal revenue for a perfectly competitive firm is incorrect? A) TR

TR") Name: Date: 1. Which of the following will not be true of a perfectly competitive market? A) Buyers and sellers will have an imperceptible effect on the market. B) Firms can freely enter and exit the market.

Name: Date: 1. Which of the following will not be true of a perfectly competitive market? A) Buyers and sellers will have an imperceptible effect on the market. B) Firms can freely enter and exit the market.

Sample Exam Questions/Chapter 12. Use the following to answer question 1: Figure: Short-Run Costs

Sample Exam Questions/Chapter 12 Use the following to answer question 1: Figure: Short-Run Costs 1. (Figure: Short-Run Costs) Look at the figure Short-Run Costs. At the given price, the most profitable

Sample Exam Questions/Chapter 12 Use the following to answer question 1: Figure: Short-Run Costs 1. (Figure: Short-Run Costs) Look at the figure Short-Run Costs. At the given price, the most profitable

Chapter 14 Perfectly competitive Market

Chapter 14 Perfectly competitive Market But first lets look at this Profit Maximization Profit Maximization This occurs where marginal revenue (MR) = marginal cost (MC). MR = MC Marginal revenue is the

Chapter 14 Perfectly competitive Market But first lets look at this Profit Maximization Profit Maximization This occurs where marginal revenue (MR) = marginal cost (MC). MR = MC Marginal revenue is the

Firms in competitive markets: Perfect Competition and Monopoly

Lesson 6 Firms in competitive markets: Perfect Competition and Monopoly Henan University of Technology Sino-British College Transfer Abroad Undergraduate Programme 0 In this lesson, look for the answers

Lesson 6 Firms in competitive markets: Perfect Competition and Monopoly Henan University of Technology Sino-British College Transfer Abroad Undergraduate Programme 0 In this lesson, look for the answers

short run long run short run consumer surplus producer surplus marginal revenue

Test 3 Econ 3144 Name Fall 2005 Dr. Rupp 20 Multiple Choice Questions (50 points) & 4 Discussion (50 points) Signature I have neither given nor received aid on this exam Use this table to answer questions

Test 3 Econ 3144 Name Fall 2005 Dr. Rupp 20 Multiple Choice Questions (50 points) & 4 Discussion (50 points) Signature I have neither given nor received aid on this exam Use this table to answer questions

Chapter 13. What will you learn in this chapter? A competitive market. Perfect Competition

Chapter 13 Perfect Competition 214 by McGraw-Hill Education 1 What will you learn in this chapter? What the characteristics of a perfectly competitive market are. How to calculate average, marginal, and

Chapter 13 Perfect Competition 214 by McGraw-Hill Education 1 What will you learn in this chapter? What the characteristics of a perfectly competitive market are. How to calculate average, marginal, and

Introduction: A Scenario. Firms in Competitive Markets. In this chapter, look for the answers to these questions:

14 Firms in Competitive Markets R I N C I L E S O F ECONOMICS FOURTH EDITION N. GREGORY MANKIW remium oweroint Slides by Ron Cronovich 2008 update 2008 South-Western, a part of Cengage Learning, all rights

14 Firms in Competitive Markets R I N C I L E S O F ECONOMICS FOURTH EDITION N. GREGORY MANKIW remium oweroint Slides by Ron Cronovich 2008 update 2008 South-Western, a part of Cengage Learning, all rights

Firms in Competitive Markets

Firms in Competitive Markets Yan Zeng Version 1.0.2, last revised on 2014-02-24. Abstract Study notes based on (Mankiw, 1998, pp. 263-302). The Costs of Production The amount that the firm receives for

Firms in Competitive Markets Yan Zeng Version 1.0.2, last revised on 2014-02-24. Abstract Study notes based on (Mankiw, 1998, pp. 263-302). The Costs of Production The amount that the firm receives for

MULTIPLE CHOICE. Choose the one alternative that best completes the statement or answers the question.

Micro - HW 4 MULTIPLE CHOICE. Choose the one alternative that best completes the statement or answers the question. 1) In central Florida during the spring, strawberry growers are price takers. The reason

Micro - HW 4 MULTIPLE CHOICE. Choose the one alternative that best completes the statement or answers the question. 1) In central Florida during the spring, strawberry growers are price takers. The reason

ECON 260 (2,3) Practice Exam #4 Spring 2007 Dan Mallela

Practice Exam #4 Spring 2007 Dan Mallela") ECON 260 (2,3) Practice Exam #4 Spring 2007 Dan Mallela Multiple Choice Identify the letter of the choice that best completes the statement or answers the question. 1. Profit is defined as a. net revenue

ECON 260 (2,3) Practice Exam #4 Spring 2007 Dan Mallela Multiple Choice Identify the letter of the choice that best completes the statement or answers the question. 1. Profit is defined as a. net revenue

ECON 2100 (Summer 2015 Sections 07 & 08) Exam #3A

Exam #3A") ECON 2100 (Summer 2015 Sections 07 & 08) Exam #3A Multiple Choice Questions: (3 points each) 1. I am taking of the exam. A. Version A 2. For a firm with market power Marginal Revenue, while for a firm

ECON 2100 (Summer 2015 Sections 07 & 08) Exam #3A Multiple Choice Questions: (3 points each) 1. I am taking of the exam. A. Version A 2. For a firm with market power Marginal Revenue, while for a firm

Chapter 8 Managing in Competitive, Monopolistic, and Monopolistically Competitive Markets

Managerial Economics & Business Strategy Chapter 8 Managing in Competitive, Monopolistic, and Monopolistically Competitive Markets McGraw-Hill/Irwin Copyright 2010 by the McGraw-Hill Companies, Inc. All

Managerial Economics & Business Strategy Chapter 8 Managing in Competitive, Monopolistic, and Monopolistically Competitive Markets McGraw-Hill/Irwin Copyright 2010 by the McGraw-Hill Companies, Inc. All

Practice Exam 3: S201 Walker Fall 2004

Practice Exam 3: S201 Walker Fall 2004 I. Multiple Choice (3 points each) 1. Which of the following statements about the short-run is false? A. The marginal product of labor may increase or decrease. B.

Practice Exam 3: S201 Walker Fall 2004 I. Multiple Choice (3 points each) 1. Which of the following statements about the short-run is false? A. The marginal product of labor may increase or decrease. B.

2) A production method that relies on large quantities of labor and smaller quantities of capital equipment is referred to as a: 2)

A production method that relies on large quantities of labor and smaller quantities of capital equipment is referred to as a: 2)") Micro: TA Session 4, Problem set MULTIPLE CHOICE. Choose the one alternative that best completes the statement or answers the question. 1) The main difference between a short-run production function and

Micro: TA Session 4, Problem set MULTIPLE CHOICE. Choose the one alternative that best completes the statement or answers the question. 1) The main difference between a short-run production function and

Econ 001: Midterm 2 (Dr. Stein) Answer Key March 23, 2011

Answer Key March 23, 2011") Instructions: Econ 001: Midterm 2 (Dr. Stein) Answer Key March 23, 2011 This is a 60-minute examination. Write all answers in the blue books provided. Show all work. Use diagrams where appropriate and

Instructions: Econ 001: Midterm 2 (Dr. Stein) Answer Key March 23, 2011 This is a 60-minute examination. Write all answers in the blue books provided. Show all work. Use diagrams where appropriate and

MULTIPLE CHOICE. Choose the one alternative that best completes the statement or answers the question.

AUBG, Fall 2015, Principles Micro with P. Stankov, Sample MT2 NOTE: The actual no. of questions on the actual MT will be 30, each for 0.67 grade points. MULTIPLE CHOICE. Choose the one alternative that

AUBG, Fall 2015, Principles Micro with P. Stankov, Sample MT2 NOTE: The actual no. of questions on the actual MT will be 30, each for 0.67 grade points. MULTIPLE CHOICE. Choose the one alternative that

ECON 2100 (Summer 2016 Sections 10 & 11) Exam #3C

Exam #3C") ECON 21 (Summer 216 Sections 1 & 11) Exam #3C Multiple Choice Questions: (3 points each) 1. I am taking of the exam. C. Version C 2. is a market structure in which there is one single seller of a unique

ECON 21 (Summer 216 Sections 1 & 11) Exam #3C Multiple Choice Questions: (3 points each) 1. I am taking of the exam. C. Version C 2. is a market structure in which there is one single seller of a unique

ECON 2100 (Summer 2016 Sections 10 & 11) Exam #3D

Exam #3D") ECON 21 (Summer 216 Sections 1 & 11) Exam #3D Multiple Choice Questions: (3 points each) 1. I am taking of the exam. D. Version D 2. is a market structure in which there is one single seller of a unique

ECON 21 (Summer 216 Sections 1 & 11) Exam #3D Multiple Choice Questions: (3 points each) 1. I am taking of the exam. D. Version D 2. is a market structure in which there is one single seller of a unique

MONOPOLISTIC COMPETITION

14 MONOPOLISTIC COMPETITION The online shoe store shoebuy.com lists athletic shooes made by 56 different producers in 40 different categories and price between$25 and $850. It offers 1,404 different types

14 MONOPOLISTIC COMPETITION The online shoe store shoebuy.com lists athletic shooes made by 56 different producers in 40 different categories and price between$25 and $850. It offers 1,404 different types

Perfect Competition Chapter 8

Perfect Competition Chapter 8 A Perfectly Competitive Market A perfectly competitive market is one in which economic forces operate unimpeded. A Perfectly Competitive Market For a market to be perfectly

Perfect Competition Chapter 8 A Perfectly Competitive Market A perfectly competitive market is one in which economic forces operate unimpeded. A Perfectly Competitive Market For a market to be perfectly

EconS Competitive Markets Part 1

EconS 305 - Competitive Markets Part 1 Eric Dunaway Washington State University eric.dunaway@wsu.edu October 11, 2015 Eric Dunaway (WSU) EconS 305 - Lecture 19 October 11, 2015 1 / 48 Introduction Today,

EconS 305 - Competitive Markets Part 1 Eric Dunaway Washington State University eric.dunaway@wsu.edu October 11, 2015 Eric Dunaway (WSU) EconS 305 - Lecture 19 October 11, 2015 1 / 48 Introduction Today,

Jacob: W hat if Framer Jacob has 10% percent of the U.S. wheat production? Is he still a competitive producer?

Microeconomics, Module 7: Competition in the Short Run (Chapter 7) Additional Illustrative Test Questions (The attached PDF file has better formatting.) Updated: June 9, 2005 Question 7.1: Pricing in a

Microeconomics, Module 7: Competition in the Short Run (Chapter 7) Additional Illustrative Test Questions (The attached PDF file has better formatting.) Updated: June 9, 2005 Question 7.1: Pricing in a

Microeconomics: MIE1102

TEXT CHAPTERS TOPICS 1, 2 ECONOMICS, ECONOMIC SYSTEMS, MARKET ECONOMY 3 DEMAND AND SUPPLY. MARKET EQUILIBRIUM 4 ELASTICITY OF DEMAND AND SUPPLY 5 DEMAND & CONSUMER BEHAVIOR 6 PRODUCTION FUNCTION 7 COSTS

TEXT CHAPTERS TOPICS 1, 2 ECONOMICS, ECONOMIC SYSTEMS, MARKET ECONOMY 3 DEMAND AND SUPPLY. MARKET EQUILIBRIUM 4 ELASTICITY OF DEMAND AND SUPPLY 5 DEMAND & CONSUMER BEHAVIOR 6 PRODUCTION FUNCTION 7 COSTS

Four Market Models. 1. Perfect Competition 2. Pure Monopoly 3. Monopolistic Competition 4. Oligopoly

Four Market Models 1. Perfect Competition 2. Pure Monopoly 3. Monopolistic Competition 4. Oligopoly Perfect Competition Chapter 14 Perfect Competition Characteristics 1. Very Large Numbers Many buyers/sellers

Four Market Models 1. Perfect Competition 2. Pure Monopoly 3. Monopolistic Competition 4. Oligopoly Perfect Competition Chapter 14 Perfect Competition Characteristics 1. Very Large Numbers Many buyers/sellers

Firm Behavior. Business Economics Managerial Decisions in Competitive Markets (Deriving the Supply Curve)) Perfect Competition.

) Perfect Competition.") Business Economics Managerial Decisions in Competitive Markets (Deriving the Supply Curve)) Thomas & Maurice, Chapter Herbert Stocker herbert.stocker@uibk.ac.at Institute of International Studies University

Business Economics Managerial Decisions in Competitive Markets (Deriving the Supply Curve)) Thomas & Maurice, Chapter Herbert Stocker herbert.stocker@uibk.ac.at Institute of International Studies University

Textbook Media Press. CH 12 Taylor: Principles of Economics 3e 1

CH 12 Taylor: Principles of Economics 3e 1 Monopolistic Competition and Differentiated Products Monopolistic competition refers to a market where many firms sell differentiated products. Differentiated

CH 12 Taylor: Principles of Economics 3e 1 Monopolistic Competition and Differentiated Products Monopolistic competition refers to a market where many firms sell differentiated products. Differentiated

Perfectly Competitive Supply. Chapter 6. Learning Objectives

Perfectly Competitive Supply Chapter 6 McGraw-Hill/Irwin Copyright 2013 by The McGraw-Hill Companies, Inc. All rights reserved. Learning Objectives 1.Explain how opportunity cost is related to the supply

Perfectly Competitive Supply Chapter 6 McGraw-Hill/Irwin Copyright 2013 by The McGraw-Hill Companies, Inc. All rights reserved. Learning Objectives 1.Explain how opportunity cost is related to the supply

Perfect Competition and The Supply Curve

chapter: 13 >> Perfect Competition and The Supply Curve The following materials are taken from Chap. 13, Economics, 2 nd ed., Krugman and Wells(2009), Worth Palgrave MaCmillan. 2009 Worth Publishers 1

chapter: 13 >> Perfect Competition and The Supply Curve The following materials are taken from Chap. 13, Economics, 2 nd ed., Krugman and Wells(2009), Worth Palgrave MaCmillan. 2009 Worth Publishers 1

Section I (20 questions; 1 mark each)

") Foundation Course in Managerial Economics- Solution Set- 1 Final Examination Marks- 100 Section I (20 questions; 1 mark each) 1. Which of the following statements is not true? a. Societies face an important

Foundation Course in Managerial Economics- Solution Set- 1 Final Examination Marks- 100 Section I (20 questions; 1 mark each) 1. Which of the following statements is not true? a. Societies face an important