US Energy Independence & Energy Exports

|

|

|

- Mercy Cole

- 6 years ago

- Views:

Transcription

1 US Energy Independence & Energy Exports Fred C. Beach, Ph.D. Earth Wind & Fire Conference Addison, TX. 4 October, /12/2014 1

2 Global Consumption Trends 2011 Energy Consumption, + 2.5% OEDC, Down Non-OEDC, Up Oil Consumption, + 0.7% OEDC, -1.2% Non-OEDC, +2.8% Natural Gas Consumption, +2.2% EU, -9.9% China, +21.5% 87 % of the Worlds Energy Consumption Comes from Fossil Fuels and the Percentage Is Growing Coal Consumption, +5.4% OEDC, -1.1% Non-OEDC, +8.4% 10/12/2014 2

3 Energy Dependence % 80% 70% 60% 50% 40% % 20% 10% 0% US Germany France UK Italy Spain Japan 10/12/2014 3

4 U.S. Energy Independence Trend US for 2012 (Quads) Consumption = 95 Production = 80 Imports = 15.8% % 10/12/2014 4

5 EIA 2010 vs 2012 Forecast Change 10/12/2014 5

6 U.S. Oil Production /12/2014 6

7 U.S. Oil Production, Technology Breakthrough? 10/12/2014 7

8 Actually, It Was A Price Revolution 10/12/2014 8

9 U.S. Petroleum Liquids Net Imports 10/12/2014 9

10 U.S. Petroleum Liquids Net Imports 10/12/

11

12

13 U.S. Coal Production 10/12/

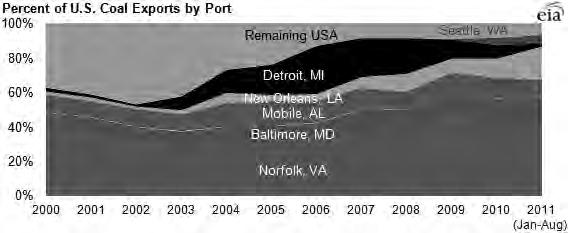

14 U.S. Coal Exports 10/12/

15

16

17

18 Coal Retirements About 50 GW of coal capacity may retire by 2020 Almost 21 GW already retired in (mostly older units) Announced about 29 GW ( )

19

20

21

22 Gürcan Gülen, Ph.D. CEE-UT, 7

23 US Natural Gas Production Source: EIA Annual Energy Outlook 2013

24 U.S. Natural Gas Production 10/12/

25 Technically Recoverable Resource Estimates Source: Based on a widely used chart produced by Gas Technology Institute (GTI).

26 At What Price Can Producers Deliver? $9 $8 $ % Return $7 $6 $7.28 $7.16 $0.66 $0.65 $6.67 $0.61 $0.71 U.S. Cash Operating Costs $/MCFE U.S. All Source FD Costs $/MCFE Henry Hub Spot Price $4/MCF $/MCFE $5 $4 GL Uplift: how much, $3.73 when & where? $2.7N 1 $2.99 $3.66 Note: All Source FD Costs are 3-year rolling averages As of: December 4, 2013 $3 $2 $3.91 $3.52 $3.40 $1 $2.41 $- Average All Average All Average All Average All Producers Producers Producers Producers (2009) (2010) (2011) (2012) Monitoring U.S./Global Oil and Gas: Upstream Attainment, Producer Challenges Gürcan Gülen, Ph.D.

27 How Much Demand? At What Price? Power generation Industrial demand Exports (LNG and pipeline) Transportation (LNG, CNG) not covered today

28 Different Views of the World 2.5 Consumption of Natural Gas in Power Generation (Index, 2010 = 1) 2.0 Avg y-y growth of 2.5% AEO Real GDP IHS Real GDP AEO Electricity IHS Electricity Based on data from EIA AEO 2013 & IHS Global Insight

29 Nuclear Relicensing? 4 recent announcements 5,500 MW in 3 plants under construction

30 Industrial Gas Demand A Growth Scenario based on Projects in Progress 9 8 TCF GTL MTG Metals Propylene Polyethylene Chlor-Alkali Methanol Ammonia-urea-fertilizer Ethylene Crackers Base Demand (2012) Source: CEE Industrial Projects Database

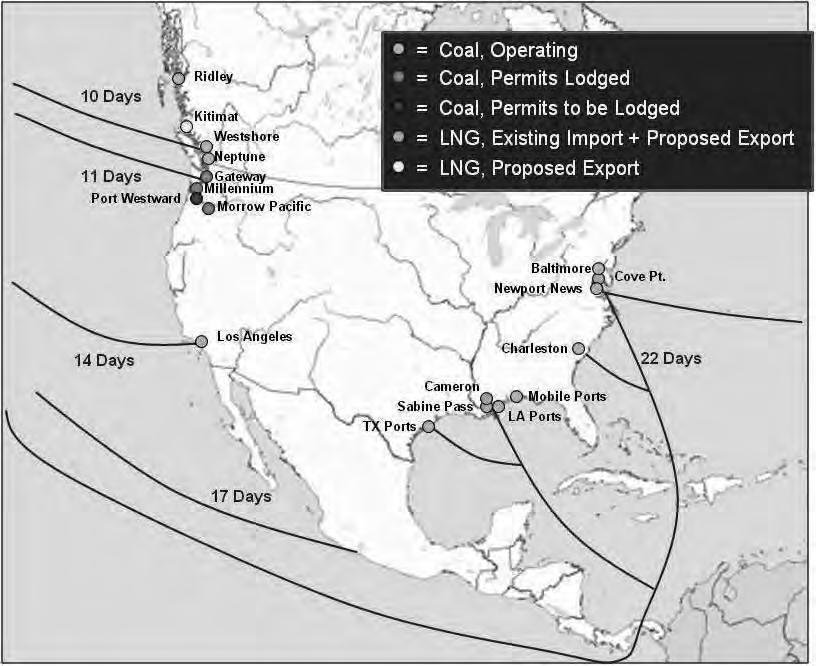

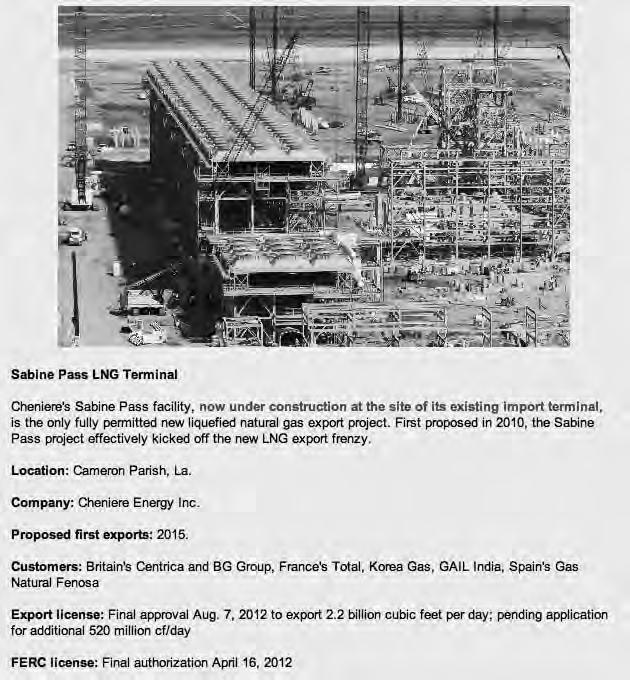

31 Increasing Gas Exports? 7 terminals received 8 permits to export LNG to non-fta countries (as of April 2014) Only 3 with FERC approval Construction started on 2 liquefaction trains of the Sabine Pass terminal in August 2012 The first exports are not expected until 2016 Forecasts cover a wide range from 1.6 to 3.6 tcf by 2025 Pipe exports to Mexico have been increasing and are expected to reach 2.4 tcf by 2040 (EIA AEO) or early 2020s (based on pipe projects).

32 Proposed Does Not Equate to Realized

33 Gürcan Gülen, Ph.D. Is U.S. LNG Competitive? $/MMBtu $10 Japan pre- Fukushima $9-11 NBP Regasification Sep 14 NBP $ Shipping Liquefaction Field to Terminal Henry Hub $14-19 Asia spot The Attraction "Reality" High Cost Delivery to Atlantic Basin High Cost Delivery to Pacific Basin Sep 14 LNG $ Super High Cost Delivery to Pacific Basin CEE-UT, 33

34 A strong demand stack scenario TCF LNG Exports 2030 = 1.0 (EIA ER = 3.5) Pipe Exports 2030 = 3.9 (EIA ER = 3.4) LNG exports CEE Pipeline exports CEE 30 Power generation CEE 25 Power 2030 = 15.9 (EIA ER = 10.1) Industrial CEE Industrial 2030 = 8.8 (EIA ER = 8.5) Other (Res, Comm, Trans) EIA ER Dec 2013 Total demand CEE High Case 5 Other 2030 = 10.8 (residential+ commercial 10.5) CEE analysis; EIA ER refers to EIA 2014 Early Release, Dec 2013 (reference case) Total supply EIA ER Dec 2013

35 EIA 2010 vs 2012 Forecast Change By 2020 North America Could be Energy Independent 10/12/

36 The Energy Economies In the US, not everywhere is like TX or ND Growth has been anemic and uneven Over time and across the states Labor force participation at historic lows ~2 million fewer jobs than early 2008 Public discontent with and distrust of the politicalsystem Can the US reach a path of steady growth at >3%? Especially if our trade partners falter (Europe, China) The World Economy Runs on Energy & Runs Best on Cheap Energy

37

38

39

40

41

42

43 Energy Dependence % 80% 70% 60% 50% 40% % 20% 10% 0% US Germany France UK Italy Spain Japan 10/12/

North, South, Texas and the Rest

North, South, Texas and the Rest CEE Annual Meeting 4 5 December 2013 BEG/CEE UT, 1 Welcome! Agenda highlights and other logistics Introductions Up at Night rules of the game and Chatham House rules for

North, South, Texas and the Rest CEE Annual Meeting 4 5 December 2013 BEG/CEE UT, 1 Welcome! Agenda highlights and other logistics Introductions Up at Night rules of the game and Chatham House rules for

Major Challenges for Gas: What Can be Expected for Mexico?

Major Challenges for Gas: What Can be Expected for Mexico? Gas Future Forum, Mexico, April 3, 2014 BEG/CEE UT, 1 Overall Observations Resources Reserves Deliverability Deliverability is key Sweet spot

Major Challenges for Gas: What Can be Expected for Mexico? Gas Future Forum, Mexico, April 3, 2014 BEG/CEE UT, 1 Overall Observations Resources Reserves Deliverability Deliverability is key Sweet spot

Going through Another Cycle

Global Rig Count Down 5 Since Nov ; Recent Uptick Driven by North America Capital spending cut significantly IEA: $583 billion upstream (25% less than ) IEA: Further 24% drop expected in 216 Going through

Global Rig Count Down 5 Since Nov ; Recent Uptick Driven by North America Capital spending cut significantly IEA: $583 billion upstream (25% less than ) IEA: Further 24% drop expected in 216 Going through

Natural Gas Supply, Demand, and the Prospects for North American LNG Exports

Natural Gas Supply, Demand, and the Prospects for North American LNG Exports December 3 rd, 2014 Robert D. Stibolt Senior Managing Director Observations on natural gas prices and project returns Price

Natural Gas Supply, Demand, and the Prospects for North American LNG Exports December 3 rd, 2014 Robert D. Stibolt Senior Managing Director Observations on natural gas prices and project returns Price

Shale Gas - From the Source Rock to the Market: An Uneven pathway. Tristan Euzen

Shale Gas - From the Source Rock to the Market: An Uneven pathway Tristan Euzen Shale Gas Definition Seal Conventional Oil & Gas Tight Gas Source Rock Reservoir (Shale Gas) Modified from Williams 2013

Shale Gas - From the Source Rock to the Market: An Uneven pathway Tristan Euzen Shale Gas Definition Seal Conventional Oil & Gas Tight Gas Source Rock Reservoir (Shale Gas) Modified from Williams 2013

Natural Gas Opportunities

Natural Gas Opportunities NAFTANEXT Summit Chicago, IL Erica Bowman, Chief Economist April 25, 2014 U.S. Natural Gas Reserves Source: Potential Gas Committee Abundant Supply Estimates of U.S. Recoverable

Natural Gas Opportunities NAFTANEXT Summit Chicago, IL Erica Bowman, Chief Economist April 25, 2014 U.S. Natural Gas Reserves Source: Potential Gas Committee Abundant Supply Estimates of U.S. Recoverable

Prospects for unconventional natural gas supply in Asia

Perth, 16 February 2016 Prospects for unconventional natural gas supply in Asia Roberto F. Aguilera Background Expansion of natural gas share in primary energy mix, especially Asia Gas demand is dominated

Perth, 16 February 2016 Prospects for unconventional natural gas supply in Asia Roberto F. Aguilera Background Expansion of natural gas share in primary energy mix, especially Asia Gas demand is dominated

Shale Gas as an Alternative Petrochemical Feedstock

Shale Gas as an Alternative Petrochemical Feedstock Tecnon OrbiChem Seminar at KICHEM 2012 Seoul - 2 November, 2012 Roger Lee SHALE GAS WHERE DOES IT COME FROM? Source: EIA SHALE GAS EXPLOITATION Commercial

Shale Gas as an Alternative Petrochemical Feedstock Tecnon OrbiChem Seminar at KICHEM 2012 Seoul - 2 November, 2012 Roger Lee SHALE GAS WHERE DOES IT COME FROM? Source: EIA SHALE GAS EXPLOITATION Commercial

Natural Gas Trends LNG 17 NYC, June 28, 2011

Bureau of Economic Geology, The University of Texas at Austin Natural Gas Trends LNG 17 NYC, June 28, 211 Balancing Our Energy Future What do we want? Safe, clean, affordable, (abundant) energy Reduced

Bureau of Economic Geology, The University of Texas at Austin Natural Gas Trends LNG 17 NYC, June 28, 211 Balancing Our Energy Future What do we want? Safe, clean, affordable, (abundant) energy Reduced

Gas Markets Globalization: Perspectives and Limits

Gas Markets Globalization: Perspectives and Limits By: Sid Ahmed Hamdani, Senior Business Analyst, Sonatrach, Algeria Date:04 June 2012 Venue: Kuala Lumpur Towards Gas Market Globalization? Increasing

Gas Markets Globalization: Perspectives and Limits By: Sid Ahmed Hamdani, Senior Business Analyst, Sonatrach, Algeria Date:04 June 2012 Venue: Kuala Lumpur Towards Gas Market Globalization? Increasing

US LNG Supply into Europe. Baltic Energy Summit, Vilnius November 25 th, 2015 Helena Wisden, Cheniere Marketing International

US LNG Supply into Europe Baltic Energy Summit, Vilnius November 25 th, 2015 Helena Wisden, Cheniere Marketing International Forward Looking Statements This presentation contains certain statements that

US LNG Supply into Europe Baltic Energy Summit, Vilnius November 25 th, 2015 Helena Wisden, Cheniere Marketing International Forward Looking Statements This presentation contains certain statements that

The Role of GCC s Natural Gas in the World s Gas Markets

World Review of Business Research Vol. 1. No. 2. May 2011 Pp. 168-178 The Role of GCC s Natural Gas in the World s Gas Markets Abdulkarim Ali Dahan* The objective of this research is to analyze the growth

World Review of Business Research Vol. 1. No. 2. May 2011 Pp. 168-178 The Role of GCC s Natural Gas in the World s Gas Markets Abdulkarim Ali Dahan* The objective of this research is to analyze the growth

Let our team of experienced analysts provide the information and insight you need to stay ahead of the global gas markets.

OCTOBER 2017 Natural Gas Service overview The global gas market is going through a rapid evolution. Disparate and regionally separate gas markets are being brought together through the expansion of global

OCTOBER 2017 Natural Gas Service overview The global gas market is going through a rapid evolution. Disparate and regionally separate gas markets are being brought together through the expansion of global

CHENIERE ENERGY, INC.

CHENIERE ENERGY, INC. Factors Affecting Global Coal-Gas Competition NGI Workshop - Global Competition Between Coal and Natural Gas October 15th 218 Najla Jamoussi Director, Market Fundamentals & Corporate

CHENIERE ENERGY, INC. Factors Affecting Global Coal-Gas Competition NGI Workshop - Global Competition Between Coal and Natural Gas October 15th 218 Najla Jamoussi Director, Market Fundamentals & Corporate

Five Things You Should Know

Bureau of Economic Geology, Jackson School of Geosciences, The University of Texas at Austin Five Things You Should Know Tx Industries of the Future, March 7, 2013 M.M. Foss, 9/25/2012, BEG/CEE-UT, 1 #1

Bureau of Economic Geology, Jackson School of Geosciences, The University of Texas at Austin Five Things You Should Know Tx Industries of the Future, March 7, 2013 M.M. Foss, 9/25/2012, BEG/CEE-UT, 1 #1

INTERNATIONAL ENERGY AGENCY WORLD ENERGY INVESTMENT OUTLOOK 2003 INSIGHTS

INTERNATIONAL ENERGY AGENCY WORLD ENERGY INVESTMENT OUTLOOK 2003 INSIGHTS Global Strategic Challenges Security of energy supplies Threat of environmental damage caused by energy use Uneven access of the

INTERNATIONAL ENERGY AGENCY WORLD ENERGY INVESTMENT OUTLOOK 2003 INSIGHTS Global Strategic Challenges Security of energy supplies Threat of environmental damage caused by energy use Uneven access of the

International gas markets: recent developments and prospects

International gas markets: recent developments and prospects Christopher Allsopp New College Oxford Director, Oxford Institute for Energy Studies December 2012 International gas markets are changing rapidly

International gas markets: recent developments and prospects Christopher Allsopp New College Oxford Director, Oxford Institute for Energy Studies December 2012 International gas markets are changing rapidly

Gas Markets in 2015: Outlook and Challenges

The 418th Forum on Research Work Gas Markets in 2015: Outlook and Challenges December 19, 2014 Tetsuo Morikawa The Institute of Energy Economics, Japan Natural Gas Demand in Major Regions Natural Gas Demand

The 418th Forum on Research Work Gas Markets in 2015: Outlook and Challenges December 19, 2014 Tetsuo Morikawa The Institute of Energy Economics, Japan Natural Gas Demand in Major Regions Natural Gas Demand

Industrial Energy Consumers of America The Voice of the Industrial Energy Consumers WHY MANUFACTURERS ARE CONCERNED ABOUT UNFETTERED LNG EXPORTS

The Voice of the Industrial Energy Consumers 1776 K Street, NW, Suite 720 Washington, D.C. 20006 Telephone (202) 223-1420 www.ieca-us.org June 19, 2014 WHY MANUFACTURERS ARE CONCERNED ABOUT UNFETTERED

The Voice of the Industrial Energy Consumers 1776 K Street, NW, Suite 720 Washington, D.C. 20006 Telephone (202) 223-1420 www.ieca-us.org June 19, 2014 WHY MANUFACTURERS ARE CONCERNED ABOUT UNFETTERED

The Global Natural Gas Industry

The Global Natural Gas Industry Orlando CABRALES SEGOVIA Presidente de Naturgas, Colombia Regional Coordinator International Gas Union August 28 218 IGU Members serve 97% of the Worlds Gas Market 91 Charter

The Global Natural Gas Industry Orlando CABRALES SEGOVIA Presidente de Naturgas, Colombia Regional Coordinator International Gas Union August 28 218 IGU Members serve 97% of the Worlds Gas Market 91 Charter

Gas in Power Generation Sector, the story as told by Jodi-Gas database.

1 GECF Gas in Power Generation Sector, the story as told by Jodi-Gas database. Mohamed Arafat Data Bank Analyst, GECF 14th Regional JODI Training Workshop 9-11 November 2016, Moscow, Russia 2 Agenda Why

1 GECF Gas in Power Generation Sector, the story as told by Jodi-Gas database. Mohamed Arafat Data Bank Analyst, GECF 14th Regional JODI Training Workshop 9-11 November 2016, Moscow, Russia 2 Agenda Why

RYSTAD ENERGY GAS PERSPECTIVES. Jakarta, November 20 th 2017

RYSTAD ENERGY GAS PERSPECTIVES Jakarta, November 2 th 217 Agenda 1. Global LNG market outlook Oversupply and new Asian demand 2. Japan LNG Market outlook LNG demand in a nuclear restart 2 Longer distances

RYSTAD ENERGY GAS PERSPECTIVES Jakarta, November 2 th 217 Agenda 1. Global LNG market outlook Oversupply and new Asian demand 2. Japan LNG Market outlook LNG demand in a nuclear restart 2 Longer distances

A Global View of Sustainable Energy and Deregulation

GE Energy A Global View of Sustainable Energy and Deregulation Eric Gebhardt April 2008 Global trends Population Consumption Energy security Environment Create big challenges 2 2008 2030 And the challenges

GE Energy A Global View of Sustainable Energy and Deregulation Eric Gebhardt April 2008 Global trends Population Consumption Energy security Environment Create big challenges 2 2008 2030 And the challenges

The Shifting Sands of Natural Gas Abundance

August 17, 2016 The Shifting Sands of Natural Gas Abundance Richard Meyer Manager, Energy Analysis & Standards Here s how global energy changed between 2014 and 2015. Winners were oil, natural gas, renewables.

August 17, 2016 The Shifting Sands of Natural Gas Abundance Richard Meyer Manager, Energy Analysis & Standards Here s how global energy changed between 2014 and 2015. Winners were oil, natural gas, renewables.

An overview of the European Energy Markets

An overview of the European Energy Markets The European energy markets remain very unsettled Despite positive achievements, many challenges have to be overcome at COP21 conference Utilities financial performances

An overview of the European Energy Markets The European energy markets remain very unsettled Despite positive achievements, many challenges have to be overcome at COP21 conference Utilities financial performances

Regasification N. Atlantic

North Atlantic Basin LNG Week in Review 1 The report is for the week ending December 13. Table 1 to the right tracks 2013 LNG consumption in the Atlantic Basin through December 13 versus the same time

North Atlantic Basin LNG Week in Review 1 The report is for the week ending December 13. Table 1 to the right tracks 2013 LNG consumption in the Atlantic Basin through December 13 versus the same time

UNECE Expert Group on Resource Classification April, 2016

UNECE Expert Group on Resource Classification April, 216 Scott W. Tinker Bureau of Economic Geology University of Texas at Austin Framing Conundrum Many people do not know how electricity is made or where

UNECE Expert Group on Resource Classification April, 216 Scott W. Tinker Bureau of Economic Geology University of Texas at Austin Framing Conundrum Many people do not know how electricity is made or where

Milken Institute: Center for Accelerating Energy Solutions

Milken Institute: Center for Accelerating Energy Solutions Center for Accelerating Energy Solutions Promotes policy and market mechanisms to build a more stable and sustainable energy future Identifies

Milken Institute: Center for Accelerating Energy Solutions Center for Accelerating Energy Solutions Promotes policy and market mechanisms to build a more stable and sustainable energy future Identifies

Fabio Ballini World Maritime University

Pricing on gas: focus on LNG sectors Fabio Ballini World Maritime University What are the benefits of LNG? Environmental Benefits Table 3: Compering alterative technologies and fuels Source: SSPA, TC/1208-05-2100

Pricing on gas: focus on LNG sectors Fabio Ballini World Maritime University What are the benefits of LNG? Environmental Benefits Table 3: Compering alterative technologies and fuels Source: SSPA, TC/1208-05-2100

BP Statistical Review of World Energy

BP Statistical Review of World Energy July 2016 bp.com/statisticalreview #BPstats BP p.i.c.2016 BP Statistical Review of World Energy July 2016 2015: A year of plenty Richard de Caux, head of refining

BP Statistical Review of World Energy July 2016 bp.com/statisticalreview #BPstats BP p.i.c.2016 BP Statistical Review of World Energy July 2016 2015: A year of plenty Richard de Caux, head of refining

Rice University World Gas Trade Model

Rice University World Gas Trade Model Peter Hartley Kenneth B Medlock III Jill Nesbitt James A. Baker III Institute of Public Policy RICE 1 What does the model capture? World gas supply potential is large

Rice University World Gas Trade Model Peter Hartley Kenneth B Medlock III Jill Nesbitt James A. Baker III Institute of Public Policy RICE 1 What does the model capture? World gas supply potential is large

PGC B Strategy - Triennium November 18 20, 2014 Bratislava. By: Ashkan Esmaeilifar

1 PGC B Strategy - Triennium 2012 2015 November 18 20, 2014 Bratislava By: Ashkan Esmaeilifar 2 COUNTRY PROFILE Area (km 2 ): 49,035 Population: 5,379,000 Capital: Bratislava Member of OECD, WTO, NATO,

1 PGC B Strategy - Triennium 2012 2015 November 18 20, 2014 Bratislava By: Ashkan Esmaeilifar 2 COUNTRY PROFILE Area (km 2 ): 49,035 Population: 5,379,000 Capital: Bratislava Member of OECD, WTO, NATO,

API Automotive/Petroleum Industry Forum Alessandro Faldi

API Automotive/Petroleum Industry Forum Alessandro Faldi April 17, 2018 2018 Outlook for Energy: A View to 2040 The Outlook for Energy includes Exxon Mobil Corporation s internal estimates and forecasts

API Automotive/Petroleum Industry Forum Alessandro Faldi April 17, 2018 2018 Outlook for Energy: A View to 2040 The Outlook for Energy includes Exxon Mobil Corporation s internal estimates and forecasts

The Impact of US LNG Exports on India s Gas Market Jason Bordoff

The Impact of US LNG Exports on India s Gas Market Jason Bordoff November 30, 2016 Delhi, India US Natural Gas Outlook 2 US Shale: There Will Be Gas US Dry Gas Production Under the EIA s Reference Case

The Impact of US LNG Exports on India s Gas Market Jason Bordoff November 30, 2016 Delhi, India US Natural Gas Outlook 2 US Shale: There Will Be Gas US Dry Gas Production Under the EIA s Reference Case

OVERVIEW OF DESERT SOUTHWEST POWER MARKET AND ECONOMIC ASSESSMENT OF THE NAVAJO GENERATING STATION

OVERVIEW OF DESERT SOUTHWEST POWER MARKET AND ECONOMIC ASSESSMENT OF THE NAVAJO GENERATING STATION ARIZONA CORPORATION COMMISSION APRIL 6, 2017 DALE PROBASCO MANAGING DIRECTOR ROGER SCHIFFMAN DIRECTOR

OVERVIEW OF DESERT SOUTHWEST POWER MARKET AND ECONOMIC ASSESSMENT OF THE NAVAJO GENERATING STATION ARIZONA CORPORATION COMMISSION APRIL 6, 2017 DALE PROBASCO MANAGING DIRECTOR ROGER SCHIFFMAN DIRECTOR

Louisiana Unconventional Natural Gas and Industrial Redevelopment

Louisiana Unconventional Natural Gas and Industrial Redevelopment Risk Management Association Luncheon March 21, 2013 David E. Dismukes, Ph.D. Center for Energy Studies Louisiana State University STUDY

Louisiana Unconventional Natural Gas and Industrial Redevelopment Risk Management Association Luncheon March 21, 2013 David E. Dismukes, Ph.D. Center for Energy Studies Louisiana State University STUDY

The Evolving Landscape of the LNG Sector.

The Evolving Landscape of the LNG Sector Four Divisions One Team One integrated full-service team for your project to serve you from concept to commercial operations Ship Broking Logistics Braemar ACM

The Evolving Landscape of the LNG Sector Four Divisions One Team One integrated full-service team for your project to serve you from concept to commercial operations Ship Broking Logistics Braemar ACM

LNG Shipping: How Long Will The Good Times Last?

LNG Shipping: How Long Will The Good Times Last? Poten & Partners November 1 HOUSTON NEW YORK LONDON ATHENS SINGAPORE GUANGZHOU PERTH A GLOBAL BROKER AND COMMERCIAL ADVISOR FOR THE ENERGY AND OCEAN TRANSPORTATION

LNG Shipping: How Long Will The Good Times Last? Poten & Partners November 1 HOUSTON NEW YORK LONDON ATHENS SINGAPORE GUANGZHOU PERTH A GLOBAL BROKER AND COMMERCIAL ADVISOR FOR THE ENERGY AND OCEAN TRANSPORTATION

AIChE: Natural Gas Utilization Workshop Overcoming Hurdles of Technology Implementation

AIChE: Natural Gas Utilization Workshop Overcoming Hurdles of Technology Implementation Natural Gas in the United States: An Overview of Resources and Factors Affecting the Market November 2, 216 Justin

AIChE: Natural Gas Utilization Workshop Overcoming Hurdles of Technology Implementation Natural Gas in the United States: An Overview of Resources and Factors Affecting the Market November 2, 216 Justin

Developments in gas pipelines and LNG infrastructure for closing EU-30 gas supply demand gap

ECN Seminar Prague, June 12th, 2003 Gas Supply Security in an Enlarged Europe Developments in gas pipelines and LNG infrastructure for closing EU-30 gas supply demand gap Presentation by: Patrick Cayrade

ECN Seminar Prague, June 12th, 2003 Gas Supply Security in an Enlarged Europe Developments in gas pipelines and LNG infrastructure for closing EU-30 gas supply demand gap Presentation by: Patrick Cayrade

LNG Facts A Primer. Presentation before US Department of Energy, Office of Fossil Energy, LNG Forums. March 10, Kristi A. R.

LNG Facts A Primer Presentation before US Department of Energy, Office of Fossil Energy, LNG Forums March 10, 2006 Kristi A. R. Darby Center for Louisiana State University Overview What is Natural Gas?

LNG Facts A Primer Presentation before US Department of Energy, Office of Fossil Energy, LNG Forums March 10, 2006 Kristi A. R. Darby Center for Louisiana State University Overview What is Natural Gas?

Coal Low Cost Fuel for the Future

Coal Low Cost Fuel for the Future NCSL Jacob Williams VP Global Energy Analytics Peabody Energy August 19, 2014 Coal: The World s Fastest Growing Major Fuel Million Tonnes of Oil Equivalent 2009 2011 2020

Coal Low Cost Fuel for the Future NCSL Jacob Williams VP Global Energy Analytics Peabody Energy August 19, 2014 Coal: The World s Fastest Growing Major Fuel Million Tonnes of Oil Equivalent 2009 2011 2020

The Economics of LNG Export Contract Flexibility: a quantitative approach

The Economics of LNG Export Contract Flexibility: a quantitative approach By Yichi Zhang, 29 October 2012, EPRG weekly seminar Supervisors: Pierre Noel, Chi Kong Chyong shebazhang@gmail.com Introduction

The Economics of LNG Export Contract Flexibility: a quantitative approach By Yichi Zhang, 29 October 2012, EPRG weekly seminar Supervisors: Pierre Noel, Chi Kong Chyong shebazhang@gmail.com Introduction

Energy Q&A. NAESB, 8 April 2015 BEG/CEE-UT, 1

Energy Q&A NAESB, 8 April 2015 BEG/CEE-UT, 1 PRICE TRENDS BEG/CEE-UT, 2 Oil Price History $160 $140 $120 Cushing, OK WTI Spot Price FOB (Dollars per Barrel) Europe Brent Spot Price FOB (Dollars per Barrel)

Energy Q&A NAESB, 8 April 2015 BEG/CEE-UT, 1 PRICE TRENDS BEG/CEE-UT, 2 Oil Price History $160 $140 $120 Cushing, OK WTI Spot Price FOB (Dollars per Barrel) Europe Brent Spot Price FOB (Dollars per Barrel)

Annual Energy Outlook 2015

Annual Energy Outlook 215 for Asia Pacific Energy Research Centre Annual Conference 215 Tokyo, Japan by Sam Napolitano Director of the Office of Integrated and International Energy Analysis U.S. Energy

Annual Energy Outlook 215 for Asia Pacific Energy Research Centre Annual Conference 215 Tokyo, Japan by Sam Napolitano Director of the Office of Integrated and International Energy Analysis U.S. Energy

Global LNG Market dynamics, key trends and market outlook

REUTERS / Anne Kat Brevik Global LNG Market dynamics, key trends and market outlook December 14, 217 What to address Market dynamics, key trends and market outlook The role and outlook for U.S. LNG China

REUTERS / Anne Kat Brevik Global LNG Market dynamics, key trends and market outlook December 14, 217 What to address Market dynamics, key trends and market outlook The role and outlook for U.S. LNG China

Comparison of Netbacks from Potential LNG Project with ALCAN Pipeline Project

Comparison of Netbacks from Potential LNG Project with ALCAN Pipeline Project June 20, 2008 Barry Pulliam Senior Economist Econ One Research 5th Floor 601 W 5th Street Los Angeles, California 90071 213

Comparison of Netbacks from Potential LNG Project with ALCAN Pipeline Project June 20, 2008 Barry Pulliam Senior Economist Econ One Research 5th Floor 601 W 5th Street Los Angeles, California 90071 213

Fairbanks to Anchorage Spur Report - Updated Analysis

Fairbanks to Anchorage Spur Report - Updated Analysis June 24.~ LUKES EERGY GROUP COP _745 Overview Projectdescription Earlier findings I conclusions Current analysis efforts Updated findings Implications

Fairbanks to Anchorage Spur Report - Updated Analysis June 24.~ LUKES EERGY GROUP COP _745 Overview Projectdescription Earlier findings I conclusions Current analysis efforts Updated findings Implications

NARUC. Global Liquefied Natural Gas Supply: An Introduction for Public Utility Commissioners

2009 Global Liquefied Natural Gas Supply: An Introduction for Public Utility Commissioners NARUC October 2009 The National Association of Regulatory Utility Commissioners Funded by the U.S. Department

2009 Global Liquefied Natural Gas Supply: An Introduction for Public Utility Commissioners NARUC October 2009 The National Association of Regulatory Utility Commissioners Funded by the U.S. Department

[LNG MARKET ANALYSIS ] 1. LNG Market Analysis

![[LNG MARKET ANALYSIS ] 1. LNG Market Analysis](/thumbs/82/85327793.jpg "[LNG MARKET ANALYSIS ] 1. LNG Market Analysis") [LNG MARKET ANALYSIS ] 1 LNG Market Analysis LNG Market Analysis Volume: 6 th April 2018 [LNG MARKET ANALYSIS ] 2 LNG and Natural Gas Price Assessment 26 th March 6 th April 2018 LNG Analysis Global LNG

[LNG MARKET ANALYSIS ] 1 LNG Market Analysis LNG Market Analysis Volume: 6 th April 2018 [LNG MARKET ANALYSIS ] 2 LNG and Natural Gas Price Assessment 26 th March 6 th April 2018 LNG Analysis Global LNG

Tracking New Coal-Fired Power Plants (data update 7/12/2011)

") Tracking New Coal-Fired Power Plants (data update 7/12/211) National Energy Technology Laboratory Office of Strategic Energy Analysis & Planning Erik Shuster July 12, 211 Tracking New Coal-Fired Power

Tracking New Coal-Fired Power Plants (data update 7/12/211) National Energy Technology Laboratory Office of Strategic Energy Analysis & Planning Erik Shuster July 12, 211 Tracking New Coal-Fired Power

Session 2: Gas demand growth beyond power generation

Session 2: Gas demand growth beyond power generation IEF-IGU Gas Ministerial 22 nd November 218 Key messages: Gas demand growth beyond power generation Key messages Session objectives Recent global gas

Session 2: Gas demand growth beyond power generation IEF-IGU Gas Ministerial 22 nd November 218 Key messages: Gas demand growth beyond power generation Key messages Session objectives Recent global gas

Natural Gas. Tuesday, May 1, 2012; 4:00 PM 5:15 PM

Natural Gas Tuesday, May 1, 2012; 4:00 PM 5:15 PM Moderator: Joel Kurtzman, Senior Fellow and Executive Director of the Center for Accelerating Energy Solutions, Milken Institute Speakers: Ralph Eads,

Natural Gas Tuesday, May 1, 2012; 4:00 PM 5:15 PM Moderator: Joel Kurtzman, Senior Fellow and Executive Director of the Center for Accelerating Energy Solutions, Milken Institute Speakers: Ralph Eads,

Natural Gas Issues and Emerging Trends for the Upcoming Winter and Beyond

Natural Gas Issues and Emerging Trends for the Upcoming Winter and Beyond 2013 NASEO WINTER ENERGY OUTLOOK CONFERENCE November 1, 2013 Kevin Petak Vice President, ICF International Kevin.Petak@icfi.com

Natural Gas Issues and Emerging Trends for the Upcoming Winter and Beyond 2013 NASEO WINTER ENERGY OUTLOOK CONFERENCE November 1, 2013 Kevin Petak Vice President, ICF International Kevin.Petak@icfi.com

Background, Issues, and Trends in Underground Hydrocarbon Storage

Background, Issues, and Trends in Underground Hydrocarbon Storage David E. Dismukes Center for Energy Studies Louisiana State University Environmental Permitting Class January 29, 2009 Description of the

Background, Issues, and Trends in Underground Hydrocarbon Storage David E. Dismukes Center for Energy Studies Louisiana State University Environmental Permitting Class January 29, 2009 Description of the

Emerging Fundamentals in Global Natural Gas Markets: The US, Shale and LNG

Emerging Fundamentals in Global Natural Gas Markets: The US, Shale and LNG Kenneth B Medlock III, PhD James A Baker III and Susan G Baker Fellow in Energy and Resource Economics, and Senior Director, Center

Emerging Fundamentals in Global Natural Gas Markets: The US, Shale and LNG Kenneth B Medlock III, PhD James A Baker III and Susan G Baker Fellow in Energy and Resource Economics, and Senior Director, Center

Global Energy Assessment: Shale Gas and Oil

Global Energy Assessment: Shale Gas and Oil KEEI September, 2014 Yonghun Jung Shale Gas: a new source of energy Shale gas deposits around the world vs. 2009 natural gas consumption (tcf) U.S. 862 22.8

Global Energy Assessment: Shale Gas and Oil KEEI September, 2014 Yonghun Jung Shale Gas: a new source of energy Shale gas deposits around the world vs. 2009 natural gas consumption (tcf) U.S. 862 22.8

Markets and Opportunities. Paul Burgener March 2015

Markets and Opportunities Paul Burgener March 2015 Disclaimer Copyright BP Energy Company. All rights reserved. Contents of this presentation do not necessarily reflect the Company s views. This presentation

Markets and Opportunities Paul Burgener March 2015 Disclaimer Copyright BP Energy Company. All rights reserved. Contents of this presentation do not necessarily reflect the Company s views. This presentation

World Energy Outlook Bo Diczfalusy, Näringsdepartementet

World Energy Outlook 2013 Bo Diczfalusy, Näringsdepartementet Energy demand & GDP Trillion dollars (2012) 50 40 30 20 10 000 Mtoe 8 000 6 000 4 000 GDP: OECD Non-OECD TPED (right axis): OECD Non-OECD 10

World Energy Outlook 2013 Bo Diczfalusy, Näringsdepartementet Energy demand & GDP Trillion dollars (2012) 50 40 30 20 10 000 Mtoe 8 000 6 000 4 000 GDP: OECD Non-OECD TPED (right axis): OECD Non-OECD 10

Rice World Gas Trade Model: Russian Natural Gas and Northeast Asia

Rice World Gas Trade Model: Russian Natural Gas and Northeast Asia Peter Hartley Kenneth B Medlock III James A. Baker III Institute of Public Policy RICE 1 Overview and motivation Worldwide, the demand

Rice World Gas Trade Model: Russian Natural Gas and Northeast Asia Peter Hartley Kenneth B Medlock III James A. Baker III Institute of Public Policy RICE 1 Overview and motivation Worldwide, the demand

Cheniere Energy Partners, L.P. / Cheniere Energy, Inc. Proposed Sabine Pass LNG Facility Expansion Adding Liquefaction Capabilities.

Cheniere Energy Partners, L.P. / Cheniere Energy, Inc. Proposed Sabine Pass LNG Facility Expansion Adding Liquefaction Capabilities June 4, 2010 Forward Looking Statements This presentation contains certain

Cheniere Energy Partners, L.P. / Cheniere Energy, Inc. Proposed Sabine Pass LNG Facility Expansion Adding Liquefaction Capabilities June 4, 2010 Forward Looking Statements This presentation contains certain

Energy in Perspective

Energy in Perspective BP Statistical Review of World Energy 27 Christof Rühl Deputy Chief Economist London, 12 June 27 Outline Introduction What has changed? The medium term What is new? 26 in review Conclusion

Energy in Perspective BP Statistical Review of World Energy 27 Christof Rühl Deputy Chief Economist London, 12 June 27 Outline Introduction What has changed? The medium term What is new? 26 in review Conclusion

After the Natural Gas Bubble: A Critique of the Modeling and Policy Evaluation Contained in the National Petroleum Council s 2003 Natural Gas Study

After the Natural Gas Bubble: A Critique of the Modeling and Policy Evaluation Contained in the National Petroleum Council s 2003 Natural Gas Study Ken Costello, Hillard G. Huntington, and James F. Wilson

After the Natural Gas Bubble: A Critique of the Modeling and Policy Evaluation Contained in the National Petroleum Council s 2003 Natural Gas Study Ken Costello, Hillard G. Huntington, and James F. Wilson

those where domestic gas prices and affordability both in absolute terms and relative to other sources of energy are likely to restrict development of

Can Demand for Imported LNG in Asia Increase Because It is a Cleaner Energy Source? Jonathan Stern * Introduction During the period 2014-21, global LNG supply is expected to increase from around 320 Bcm

Can Demand for Imported LNG in Asia Increase Because It is a Cleaner Energy Source? Jonathan Stern * Introduction During the period 2014-21, global LNG supply is expected to increase from around 320 Bcm

The Outlook for Energy: A View to 2040

The Outlook for Energy: A View to 2040 Rob Gardner March 2014 This presentation includes forward looking statements. Actual future conditions (including economic conditions, energy demand, and energy supply)

The Outlook for Energy: A View to 2040 Rob Gardner March 2014 This presentation includes forward looking statements. Actual future conditions (including economic conditions, energy demand, and energy supply)

Global and U.S. Coal Outlook American Waterways Symposium

Global and U.S. Coal Outlook 2013 American Waterways Symposium Jacob Williams Vice President Global Energy Analytics October 2, 2013 Global and U.S. Coal Outlook Key Discussion Points Coal is the fastest-growing

Global and U.S. Coal Outlook 2013 American Waterways Symposium Jacob Williams Vice President Global Energy Analytics October 2, 2013 Global and U.S. Coal Outlook Key Discussion Points Coal is the fastest-growing

LNG and global gas market trends: Challenges and opportunities for the Baltics Karen Sund Baltic Energy Forum Vilnius, 26 November 2013

LNG and global gas market trends: Challenges and opportunities for the Baltics Karen Sund Baltic Energy Forum Vilnius, 26 November 2013 Sund Energy helps navigate into the energy future Energy Economics

LNG and global gas market trends: Challenges and opportunities for the Baltics Karen Sund Baltic Energy Forum Vilnius, 26 November 2013 Sund Energy helps navigate into the energy future Energy Economics

Global LNG-based natural gas trade: The role of the US and Louisiana

Global LNG-based natural gas trade: The role of the US and Louisiana Energy Summit 2018 Louisiana s Place in the Global Energy Economy LSU Center for Energy Studies Baton Rouge, Louisiana October 24, 2018

Global LNG-based natural gas trade: The role of the US and Louisiana Energy Summit 2018 Louisiana s Place in the Global Energy Economy LSU Center for Energy Studies Baton Rouge, Louisiana October 24, 2018

Gas security and emergency preparedness

Gas security and emergency preparedness Didier Houssin Director, Sustainable Energy Policy and Technology G20 Energy Sustainability Working Group Melbourne, 11 February 2014 OECD/IEA 2012 2014 Gas is seeing

Gas security and emergency preparedness Didier Houssin Director, Sustainable Energy Policy and Technology G20 Energy Sustainability Working Group Melbourne, 11 February 2014 OECD/IEA 2012 2014 Gas is seeing

Trends in International LNG

Trends in International LNG Anthony Patten, Partner, Allens Presentation to AMPLA State Conference Fremantle, Western Australia 18 May 2012 Allens is an independent partnership operating in alliance with

Trends in International LNG Anthony Patten, Partner, Allens Presentation to AMPLA State Conference Fremantle, Western Australia 18 May 2012 Allens is an independent partnership operating in alliance with

Global Petrochemical Market Outlook Planning For Growth Given Heightened Uncertainty In Market Fundamentals

ASIA CHEMICAL CONFERENCE Presentation Global Petrochemical Market Outlook Planning For Growth Given Heightened Uncertainty In Market Fundamentals November 2016, Singapore ihsmarkit.com Mark Eramo, VP Global

ASIA CHEMICAL CONFERENCE Presentation Global Petrochemical Market Outlook Planning For Growth Given Heightened Uncertainty In Market Fundamentals November 2016, Singapore ihsmarkit.com Mark Eramo, VP Global

Calculating the Economic Benefits of U.S. LNG Exports

Calculating the Economic Benefits of U.S. LNG Exports Prepared for LNG Allies April 17, 18 ICF 9300 Lee Highway, Fairfax, VA 231 USA +1.703.934.3000 +1.703.934.3740 fax icf.com Calculating the Economic

Calculating the Economic Benefits of U.S. LNG Exports Prepared for LNG Allies April 17, 18 ICF 9300 Lee Highway, Fairfax, VA 231 USA +1.703.934.3000 +1.703.934.3740 fax icf.com Calculating the Economic

Outlook for Gas Markets

IEEJ IEEJ:Published 2015 年 7 in 月 August 禁無断転載 2015 All rights reserved The 420th Forum on Research Work July 10, 2015 Outlook for Gas Markets The Institute of Energy Economics, Japan Tetsuo Morikawa Manager,

IEEJ IEEJ:Published 2015 年 7 in 月 August 禁無断転載 2015 All rights reserved The 420th Forum on Research Work July 10, 2015 Outlook for Gas Markets The Institute of Energy Economics, Japan Tetsuo Morikawa Manager,

Japan s LNG Prices Trending Upwards

Japan s LNG Prices Trending Upwards David Wood David Wood & Associates, Lincoln UK Published in Energy Tribune December 2007 Japan is the world's largest LNG consumer and imported 81.86 bcm of natural

Japan s LNG Prices Trending Upwards David Wood David Wood & Associates, Lincoln UK Published in Energy Tribune December 2007 Japan is the world's largest LNG consumer and imported 81.86 bcm of natural

Energy Trade Flows. U.S. LNG-based natural gas exports

Energy Trade Flows U.S. LNG-based natural gas exports Energy and the Economy: Charting the Course Ahead A joint conference hosted by the Federal Reserve Bank of Dallas and Federal Reserve Bank of Kansas

Energy Trade Flows U.S. LNG-based natural gas exports Energy and the Economy: Charting the Course Ahead A joint conference hosted by the Federal Reserve Bank of Dallas and Federal Reserve Bank of Kansas

BC Gas Exports and LNG Shipping: Unlocking the Export Potential

BC Gas Exports and LNG Shipping: Unlocking the Export Potential Christian Waldegrave Manager, Research, Strategic Development Tony Bingham Director, Business Development & Technology, Strategic Development

BC Gas Exports and LNG Shipping: Unlocking the Export Potential Christian Waldegrave Manager, Research, Strategic Development Tony Bingham Director, Business Development & Technology, Strategic Development

Medium Term Renewable Energy Market Report 2013

Renewable Energy Market Report 213 Michael Waldron Renewable Energy Division International Energy Agency OECD/IEA 213 OECD/IEA 213 MTRMR methodology and scope Analysis of drivers and challenges for RE

Renewable Energy Market Report 213 Michael Waldron Renewable Energy Division International Energy Agency OECD/IEA 213 OECD/IEA 213 MTRMR methodology and scope Analysis of drivers and challenges for RE

The US shale revolution Implications for the North American energy markets

The US shale revolution Implications for the North American energy markets NOG/Folk och Forsvar seminar Stockholm, 19 February, 13 Tor Kartevold Senior adviser Statoil The US shale revolution Outline focus

The US shale revolution Implications for the North American energy markets NOG/Folk och Forsvar seminar Stockholm, 19 February, 13 Tor Kartevold Senior adviser Statoil The US shale revolution Outline focus

NATURAL GAS MARKETS, STRUCTURES, AND MECHANISMS

NATURAL GAS MARKETS, STRUCTURES, AND MECHANISMS Mitchell DeRubis, Senior Energy Analyst Bob Yu, Senior Energy Analyst Restrictions on Use: You may use the prices, indexes, assessments and other related

NATURAL GAS MARKETS, STRUCTURES, AND MECHANISMS Mitchell DeRubis, Senior Energy Analyst Bob Yu, Senior Energy Analyst Restrictions on Use: You may use the prices, indexes, assessments and other related

LNG strategy and the outlook for global gas markets

LNG strategy and the outlook for global gas markets October 16 th, 2012 Jean-Marie Dauger Executive Vice-president GDF SUEZ The LNG market Strong growth particularly in Asia An LNG market of ~550 Mt in

LNG strategy and the outlook for global gas markets October 16 th, 2012 Jean-Marie Dauger Executive Vice-president GDF SUEZ The LNG market Strong growth particularly in Asia An LNG market of ~550 Mt in

Edgardo Curcio President AIEE

Edgardo Curcio President AIEE The First National Conference on Liquefied Natural Gas for Transports - Italy and the Mediterranean Sea April 11, 2013 What is LNG? The LNG (Liquefied Natural Gas) is a fluid

Edgardo Curcio President AIEE The First National Conference on Liquefied Natural Gas for Transports - Italy and the Mediterranean Sea April 11, 2013 What is LNG? The LNG (Liquefied Natural Gas) is a fluid

Global LNG Dynamics and South East Mediterranean Hydrocarbons Potential

Global LNG Dynamics and South East Mediterranean Hydrocarbons Potential Athanasios Pitatzis! Workshop of SPE Kavala Section activities and EMaTTech research advances! Global Oil&Gas: Black Sea & Mediterranean

Global LNG Dynamics and South East Mediterranean Hydrocarbons Potential Athanasios Pitatzis! Workshop of SPE Kavala Section activities and EMaTTech research advances! Global Oil&Gas: Black Sea & Mediterranean

Plenary session 4: Uptake of Clean Technologies: Disruption and Coexistence of New and Existing Technologies the Way Ahead.

India Plenary session 4: Uptake of Clean Technologies: Disruption and Coexistence of New and Existing Technologies the Way Ahead Background Paper New Delhi Disclaimer The observations presented herein

India Plenary session 4: Uptake of Clean Technologies: Disruption and Coexistence of New and Existing Technologies the Way Ahead Background Paper New Delhi Disclaimer The observations presented herein

Energy in 2011 disruption and continuity

June 212 bp.com/statisticalreview Energy in 211 disruption and continuity Richard de Caux, Refining Analyst, Group Economics Outline A year of disruptions Energy and the economy Fuel by fuel Concluding

June 212 bp.com/statisticalreview Energy in 211 disruption and continuity Richard de Caux, Refining Analyst, Group Economics Outline A year of disruptions Energy and the economy Fuel by fuel Concluding

Trends, Issues and Market Changes for Crude Oil and Natural Gas

Trends, Issues and Market Changes for Crude Oil and Natural Gas East Iberville Community Advisory Panel Meeting Syngenta September 26, 2012 Center for Energy Studies David E. Dismukes, Ph.D. Center for

Trends, Issues and Market Changes for Crude Oil and Natural Gas East Iberville Community Advisory Panel Meeting Syngenta September 26, 2012 Center for Energy Studies David E. Dismukes, Ph.D. Center for

New York Energy Forum

Presentation to the New York Energy Forum Antoine Halff 30 June 2014 Key highlights Gas demand grew just 1.2% in 2013, underperforming other fuels Gas demand will grow at 2.2%/y over 2013-19, on its way

Presentation to the New York Energy Forum Antoine Halff 30 June 2014 Key highlights Gas demand grew just 1.2% in 2013, underperforming other fuels Gas demand will grow at 2.2%/y over 2013-19, on its way

LNG and storage strategy - follow-up study - Final Presentation 27 September 2017 Jalil Jumriany Energy Markets Global Limited

LNG and storage strategy - follow-up study - Final Presentation 27 September 2017 Jalil Jumriany Energy Markets Global Limited LNG and storage strategy - follow-up study - LNG: Main Findings LNG: Main

LNG and storage strategy - follow-up study - Final Presentation 27 September 2017 Jalil Jumriany Energy Markets Global Limited LNG and storage strategy - follow-up study - LNG: Main Findings LNG: Main

An INDEPENDENT energy consulting company since 1996 No affiliation with any marketer, broker, agent, utility, pipeline or producer.

An INDEPENDENT energy consulting company since 1996 No affiliation with any marketer, broker, agent, utility, pipeline or producer. More than two decades of experience in the natural gas and electric industries

An INDEPENDENT energy consulting company since 1996 No affiliation with any marketer, broker, agent, utility, pipeline or producer. More than two decades of experience in the natural gas and electric industries

Global Gas and LNG in Flux. Michael Smith, Gas Trading Analytics BIEE Gas Outlook Seminar, 10th October 2011

Global Gas and LNG in Flux Michael Smith, Gas Trading Analytics BIEE Gas Outlook Seminar, th October 211 Cautionary Statement This presentation and its contents have been provided to you for informational

Global Gas and LNG in Flux Michael Smith, Gas Trading Analytics BIEE Gas Outlook Seminar, th October 211 Cautionary Statement This presentation and its contents have been provided to you for informational

AAPL 2011 Texas Land institute September 13, Christopher B. McGill Managing Director, Policy Analysis

AAPL 2011 Texas Land institute September 13, 2011 Christopher B. McGill Managing Director, Policy Analysis 0 Natural Gas Production Monthly 1998 2010 1 2011 Daily Dry Natural Gas Production (after extraction

AAPL 2011 Texas Land institute September 13, 2011 Christopher B. McGill Managing Director, Policy Analysis 0 Natural Gas Production Monthly 1998 2010 1 2011 Daily Dry Natural Gas Production (after extraction

BIEE Gas Seminar: Global Shifts in Gas Demand

October 213 BIEE Gas Seminar: Global Shifts in Gas Demand Kai Dunker, Lead Economist Global Gas Markets Disclaimer This presentation contains forward-looking statements, particularly those regarding global

October 213 BIEE Gas Seminar: Global Shifts in Gas Demand Kai Dunker, Lead Economist Global Gas Markets Disclaimer This presentation contains forward-looking statements, particularly those regarding global

The US shale revolution and its economic impact

The US shale revolution and its economic impact Sylvie Cornot-Gandolphe Groupe Idées, Rueil Malmaison, 16 mars 2015 1 The US shale revolution and its economic impact 1. Shale gas Coal-to-gas switching

The US shale revolution and its economic impact Sylvie Cornot-Gandolphe Groupe Idées, Rueil Malmaison, 16 mars 2015 1 The US shale revolution and its economic impact 1. Shale gas Coal-to-gas switching

Global Energy Investment Challenges

Global Energy Investment Challenges Dr. Fatih Birol Chief Economist Head, Economic Analysis Division International Energy Agency World Energy Outlook 2002: Key Strategic Challenges security of energy supplies

Global Energy Investment Challenges Dr. Fatih Birol Chief Economist Head, Economic Analysis Division International Energy Agency World Energy Outlook 2002: Key Strategic Challenges security of energy supplies

JAPAN S ENERGY POLICY AND JAPAN-RUSSIA ENERGY COOPERATION

JAPAN S ENERGY POLICY AND JAPAN-RUSSIA ENERGY COOPERATION November 07 Kazushige Tanaka Director, International Affairs Division Trade and Industry (METI) Trade and Industry Table of Contents. Japan s Energy

JAPAN S ENERGY POLICY AND JAPAN-RUSSIA ENERGY COOPERATION November 07 Kazushige Tanaka Director, International Affairs Division Trade and Industry (METI) Trade and Industry Table of Contents. Japan s Energy

Global energy markets outlook versus post-paris Agreement Impact on South East Europe

Global energy markets outlook versus post-paris Agreement Impact on South East Europe Sylvia Elisabeth Beyer International Energy Agency Thessaloniki, 29 June 2016 A 2 C pathway requires more technological

Global energy markets outlook versus post-paris Agreement Impact on South East Europe Sylvia Elisabeth Beyer International Energy Agency Thessaloniki, 29 June 2016 A 2 C pathway requires more technological

The Really Big Game Changer: Crude Oil Production from Shale Resources and the Tuscaloosa Marine Shale

The Really Big Game Changer: Crude Oil Production from Shale Resources and the Tuscaloosa Marine Shale Baton Rouge Chamber of Commerce Regional Stakeholders Breakfast June 27, 2012 Center for Energy Studies

The Really Big Game Changer: Crude Oil Production from Shale Resources and the Tuscaloosa Marine Shale Baton Rouge Chamber of Commerce Regional Stakeholders Breakfast June 27, 2012 Center for Energy Studies

Energy in 2011 disruption and continuity

June 212 bp.com/statisticalreview Energy in 211 disruption and continuity Paul Appleby, Head of Energy Economics Outline A year of disruptions Energy and the economy Fuel by fuel Concluding remarks Energy

June 212 bp.com/statisticalreview Energy in 211 disruption and continuity Paul Appleby, Head of Energy Economics Outline A year of disruptions Energy and the economy Fuel by fuel Concluding remarks Energy

LNG TRADE FLOWS. Hans Stinis Shell Upstream International

LNG TRADE FLOWS Hans Stinis Shell Upstream International ABSTRACT The LNG industry has witnessed a great deal of change recently, and indications are that this will only continue. Global gas demand is

LNG TRADE FLOWS Hans Stinis Shell Upstream International ABSTRACT The LNG industry has witnessed a great deal of change recently, and indications are that this will only continue. Global gas demand is

BP Energy Outlook 2016 edition

BP Energy Outlook 216 edition Mark Finley 14th February 216 Outlook to 235 bp.com/energyoutlook #BPstats Economic backdrop Trillion, $21 25 Other 2 India Africa 15 China 1 OECD 5 OECD 1965 2 235 GDP 2

BP Energy Outlook 216 edition Mark Finley 14th February 216 Outlook to 235 bp.com/energyoutlook #BPstats Economic backdrop Trillion, $21 25 Other 2 India Africa 15 China 1 OECD 5 OECD 1965 2 235 GDP 2

World LNG Report industry trends-

World LNG Report-218 -industry trends- Satoshi Yoshida General Manager, International Section, Policy and Planning Department Japan Gas Association International Gas Union (IGU) Who we are Founded in 1931,

World LNG Report-218 -industry trends- Satoshi Yoshida General Manager, International Section, Policy and Planning Department Japan Gas Association International Gas Union (IGU) Who we are Founded in 1931,