Dairy Economic Consulting Firm

|

|

|

- Kelley Marshall

- 6 years ago

- Views:

Transcription

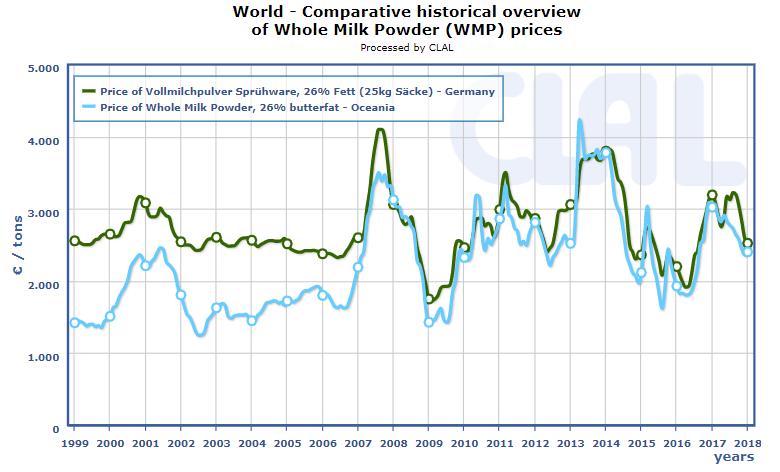

1 EU Dairy Markets, Situation and Outlook January-June 2018 by Erhard Richarts, Dairy Market Consultant, Chairman of IFE (Informations- und Forschungszentrum für Ernährungswirtschaft e. V., Kiel) Special report produced for CLAL Highlights: Milk and dairy markets will be characterized in the first half of 2018 by increasing supplies of milk resulting in ongoing growth of dairy production. Like in past years most of all additional milk supplies in the EU will be used for additional cheese production and more whole milk powder, absorbing most of all raw milk including the major parts of the additional volumes. Also output of butter and SMP will expand in the first half of Outside EU milk production will continue to grow, but not as fast as in Europe. Domestic demand in the EU will continue to increase at modest rates, which in absolute terms will require a large part of the additional milk volumes. Demand for exports will remain strong, also since commodity prices will be closer to international levels than they were in The butter prices will display moderate fluctuations when compared to 2017, but will continue to move significantly above the intervention level. Cheese prices will be lower in the first half of EU prices of SMP and other nonfat dairy commodities EU will be the lowest of the last decade and continue to be very close to the international level. Milkfat values are underpinning farm milk prices, but large stocks of SMP are overshadowing the markets and do not leave space for a sustainable recovery of prices in the nonfat sector. 1

2 Ongoing growth of milk production Most of the growth of EU milk supplies in 2018 will happen in the first half of the year, since 2017 ended with strong rates which might go on for some time. Until mid of May the seasonal pattern will go along with cyclical growth. The cyclical growth is likely to continue after the peak, but at reduced rates compared to the first trimester. On average of the whole EU area, the usual seasonal peak will be reached in May, with France and Italy earlier and North Eastern member states later. The major reason for the expected slowdown of the growth is that it is easier to increase milk yields in the lower season by advanced calving and use of concentrates, in particular in those farms where the feed management is traditionally based mainly on spring and summer pasturing or daily harvestedfresh forages supplied to the animals in the stables. This is different to the situation under quotas, when efforts toward the end of the quota years to increase milk yields were not useful, when they ended up in over quota fines. 2

3 As experienced in the cyclical fluctuations of milk prices and milk supplies, the response of dairy farmers to poorer prospects regarding the payout prices for raw milk will come later, if there should be a significant one anyway. It might happen in the second half of 2018, depending on whether the market turns into a longer ongoing depression of milk prices. To recognize that already now just at the beginning of 2018 seems to be premature. The difference of 2017 to earlier observed market situations with high price levels is that it is unilaterally based on the fat component of the milk. The returns for milkfat have declined from the all time high levels of mid and fall of 2017, but they are still higher than at any bullish butter market situation in the past. 3

are the major obstacle that prices might stabilize at higher levels, and therefore")

4 The contrast to the milkfat situation are the markets of the nonfat components. Large public stocks of SMP (skim milk powder) are the major obstacle that prices might stabilize at higher levels, and therefore volatility in this sector will be limited. The returns from the different dairy products will adjustwith some delay, to the mix of prices for milkfat, which are mainly depending on butter, and the prices realized in the nonfat part which will mainly depend on the situation in the SMP market. It is not clear yet what will be the impacts of the 4

5 proceedings of the EU Commission regarding buying into intervention and selling out of intervention. In the first months of 2018, it seems to be very likely that temporary surpluses have to be removed from the market: Selling to intervention at conditions which provide lower returns than in 2017 is the one option, another could be the increased use of raw milk for other for other dairy products, notably for cheese and WMP (whole milk powder) manufacturing. More cheese and more WMP would also absorb larger volumes of milkfat which are not available for butter and cream. Thus the split market evolution between the fat and nonfat might continue in Major exporters beyond EU: Modest Growth The price evolution will also largely depend on the ability of foreign markets to absorb additional EU milk volumes, which itself is also depending on what can be supplied from major exporting competitors and the demand which can not be covered by the domestic production of the major importing countries. In the United States, a smaller increase of milk production is expected than in 2017, mainly resulting from lower price prospects. Domestic demand is developing in view of favorable economic fundamentals, which all together could result in stagnation of exportable surpluses from current production. But 5

6 also here larger SMP stocks are available, mainly in the industry and not in public stores. The milk production of Oceania has recovered in H2 of 2017 from the depressed situation of the year before. But the prospects for the remainder of the dairy years(ending in New Zealand May 31 st and in Australia June 30, 2018) are mixed since they depend on weather conditions which can change within short periods. 6

7 For the first half year it is supposed that EU milk supplies will increase by 2,0 million metric tons and the total of the U. S. and Oceania by 1,0 m. metric tons. 7

8 Taking into account modest increases of domestic consumption on both sides of the Atlantic Ocean, the exportable volumes resulting from bigger productions are likely to keep pace with the demand of the international markets, in particular since prices are more favorable for buyers now. The major growth of the international dairy trade could be observed in SMP and cheese volumes. Also the trade in fresh products like liquid milk, yogurt, cream and other items is developing with strong rates, but modest in terms of milk equivalents when compared to milk powders, butter and cheese. 8

9 The trade in butter and WMP has declined in 2017, which is mainly due to the reduced availability for exports and high prices. Milk prices with strong short term fluctuations 9

10 Towards the end of 2017, milk prices paid to farmers were close to the high levels of 2007 and 2013, but unlike four years ago the hausse was not as sustainable as it had been then. The main reason is that it was only based on the milkfat side with an extraordinary and historically high level. The contribution of milkfat to the overall value of raw milk reached in Germany 73% in October 2017, which similar to the first years of the European milk regime in the early Seventies of the 20 th Century. But the difference to that time is that this relationship is mainly resulting from the markets and not from the policy. The equivalent of butter and SMP prices in terms of whole milk is a major indicator of the direction where the overall prices are moving to, but not in general displaying the lowest or highest levels in advance. Therefore it remains to be seen if and when milk payout prices (for milk containing 4% fat) willgo down to the levels of around 28Ct/kg which result from recently quoted EEX futures of butter and SMP for the first half of Contracts of cheese and liquid dairy products are still providing higher returns, but further producer milk price reductions can not be ruled out later in the year.but a general change of the market situationis not in sight yet. 10

11 Milk utilisation: Most of the milk for cheese As already happened in recent years, cheese manufacturing will absorb most of all milk which is delivered to dairy companies. With the ongoing growth of demand from both domestic and foreign markets also the major part of the expected additional supplies will be used for cheese and WMP, leaving some volumes to produce more butter and SMP. Volatile butter prices, but significantly above intervention level As mentioned the increase of butter production will not use the total additional milkfat which is available from the additionalmilk volumes. With poor prospects of the SMP market more volumes of milk will be processed into cheese and WMP. Therefore EU butter production will mainly grow in the first half of 2018 and be reduced in the second half, even if milk production should continue to expand. Export markets might develop also more demand since also here tight supplies are expected. With lower prices in spring and prospects of higher prices later in the year, taking butter in storages can be attractive, even if the prices do not develop in a similar way as they did in For the first half, the future prices of butter quoted at the EEX in Leipzig are moving around 4,00 /kg, which can be regarded as high level when it is compared to earlier years. The domestic EU price level has come close to the international level, which might enable Europe to export even more volumes than in Low prices are also attractive to attractmore demand from internal markets. Consequently the 11

12 expected higher production will not necessarily bring prices down close to intervention. Ongoing expansion of cheese manufacturing As mentioned above, cheese manufacturing will go up and will not always follow just the market opportunities, since it can be necessary to process increasing milk volumestemporarily. In the late months of 2017, prices of commodity type block cheeses have came down from higher levels which were not far from the historical peaks of In the first half of 2018 there is no 12

13 scope for a recovery of the prices back to the level of August/ September 2017; further weaknesses seem to be more realistic. Weak EU milk powder markets Despite the expected increases of cheese and WMP output, also more skim milk will be available for drying in the first half of The final proceedings of buying into intervention are not clear yet, but it is doubtful it will be managed at the fixed intervention price. After intervention buying in has been ended in August, market prices have fallen and the prospect that they will recover in the 13

14 first half of 2018 is poor. So far only small volumes have been sold out of the stocks. Demand for SMP is expected to grow on the domestic market but even stronger for exports. Nevertheless stocks will grow in the first half year, but a lot of them will be cleared in the second half. For the international market also stocks in the United States have to be taken into account. Together with European stocks of tons more than a half million tons have to be reduced significantly before prices can find back from the lowest level of the decade since And substantial reduction of the stocks seems to be unlikely in 2018, but it could start in the second half. Also whole milk powder prices are expected to stay at reduced levels, as consequence of the expected production growth and reduced values of milkfat though at high level - and nonfat components at low level. 14

15 15

16 Annex Table 1 Dairy Economic Consulting Firm EU 28: Dairy Markets and Forecast t * 2017* 2018** Milk deliveries Liquid products Production Consumption Butter Production Consumption Cheese Production Consumption Skim Milk Powder Production Consumption Whole Milk Powder Production Consumption Resident Population, Jan 1 st, m. head 505,2 506,9 508,3 510,1 512,0 513,4 *)Provisional. **) Forecast ife, December 2017 Sources: ife, Kiel, according to ZMB, Berlin, Milk Market Observatoy, Brussels, own calculations. Table 2 EU 28: Balance Sheet of Liquid Dairy Products t * 2017** 2018** Production Imports Exports Consumption per capita (kg) 91,4 90,2 90,5 90,1 90,1 89,8 *)Provisional. **) Forecast Sources: ife, Kiel, according to ZMB, Berlin, Milk Market Observatoy, Brussels, own calculations. ife, December

17 Table 3 Dairy Economic Consulting Firm EU28: Butter Balance Sheet t * 2017** 2018** Production Imports Exports Final stocks Consumption per capita (kg) 4,0 4,2 4,3 4,4 4,3 4,3 *)Provisional. **) Forecast Sources: ife, Kiel, according to ZMB, Berlin, Milk Market Observatoy, Brussels, own calculations. ife, December 2017 Table 4 EU Cheese Balance Sheet t * 2017** 2018** Production Processed cheese impact Imports Exports Stock change Consumption per capita (kg) 17,9 18,2 18,5 18,9 18,9 19,0 *)Provisional. **) Forecast Sources: ife, Kiel, according to ZMB, Berlin, Milk Market Observatoy, Brussels, own calculations. ife, December 2017 Table 5 EU SMP Balance Sheet t * 2017** 2018** Production Imports Exports Final stocks in intervention Consumption as Feed *)Provisional. **) Forecast Sources: ife, Kiel, according to ZMB, Berlin, Milk Market Observatoy, Brussels, own calculations. ife, December

18 Table 6 EU WMP Balance Sheet t * 2017** 2018** Production Exports Stock change Consumption *)Provisional. **) Forecast Sources: ife, Kiel, according to ZMB, Berlin, Milk Market Observatoy, Brussels, own calculations. ife, December

DAIRY AND DAIRY PRODUCTS

3. COMMODITY SNAPSHOTS Market situation DAIRY AND DAIRY PRODUCTS International dairy prices started to increase in the last half of 2016, with butter and whole milk powder (WMP) accounting for most of

3. COMMODITY SNAPSHOTS Market situation DAIRY AND DAIRY PRODUCTS International dairy prices started to increase in the last half of 2016, with butter and whole milk powder (WMP) accounting for most of

The McCully Report December 5, 2014

The McCully Report December 5, 2014 DAIRY MARKETS KEY DRIVERS Feed Prices and Farm Margins: After a long harvest, record corn and soybean crops are largely in the bin. However, despite the large crops,

The McCully Report December 5, 2014 DAIRY MARKETS KEY DRIVERS Feed Prices and Farm Margins: After a long harvest, record corn and soybean crops are largely in the bin. However, despite the large crops,

GLOBAL DAIRY UPDATE. Welcome to our November 2014 Global Dairy Update IN THIS EDITION Financial Calendar

GLOBAL DAIRY UPDATE Welcome to our ember Global Dairy Update IN THIS EDITION Fonterra milk collection New Zealand 4% higher in ober and 4% higher for the season to date Australia 8% higher in ober and

GLOBAL DAIRY UPDATE Welcome to our ember Global Dairy Update IN THIS EDITION Fonterra milk collection New Zealand 4% higher in ober and 4% higher for the season to date Australia 8% higher in ober and

Dairy Market R E P O R T

Volume 17 No. 7 Dairy Market R E P O R T September 2014 DMI NMPF Overview Milk and dairy product prices generally moved higher in August as most domestic dairy product markets remain in tight supply-demand

Volume 17 No. 7 Dairy Market R E P O R T September 2014 DMI NMPF Overview Milk and dairy product prices generally moved higher in August as most domestic dairy product markets remain in tight supply-demand

Price developments in the EU

Price developments in the EU Content 1. Development of world agricultural prices over time... 3 2. Price gap between EU and world prices... 7 3. Price volatility... 8 This document does not necessarily

Price developments in the EU Content 1. Development of world agricultural prices over time... 3 2. Price gap between EU and world prices... 7 3. Price volatility... 8 This document does not necessarily

Dairy Outlook. January By Jim Dunn Professor of Agricultural Economics, Penn State University. Market Psychology

Dairy Outlook January 2015 By Jim Dunn Professor of Agricultural Economics, Penn State University Market Psychology Dairy prices have fallen in the past month, especially butter prices. The dollar is still

Dairy Outlook January 2015 By Jim Dunn Professor of Agricultural Economics, Penn State University Market Psychology Dairy prices have fallen in the past month, especially butter prices. The dollar is still

Global Dairy Export Prices Weaken Oceania Mid-point $/Ton FOB

Department of Agriculture Foreign Agricultural Service December Since the start of the year (through November ) global dairy prices have diverged; butter and cheese prices posted gains while prices for

Department of Agriculture Foreign Agricultural Service December Since the start of the year (through November ) global dairy prices have diverged; butter and cheese prices posted gains while prices for

Adelaide Hills, Fleurieu & Kangaroo Island. Sustainable Growth For Food & Wine DAIRY

Adelaide Hills, Fleurieu & Kangaroo Island Sustainable Growth For Food & Wine DAIRY The Sustainable Food and Wine Project has four key objectives 1. Combined and Informed 2. Collaboration Initiatives 3.

Adelaide Hills, Fleurieu & Kangaroo Island Sustainable Growth For Food & Wine DAIRY The Sustainable Food and Wine Project has four key objectives 1. Combined and Informed 2. Collaboration Initiatives 3.

Overview. Dairy. U.S. Industry

Dairy Overview U.S. Industry The United States is the world s largest milk producer, its output of almost 78.2 million mt in 2003 having accounted for about 15 percent of the world s milk supply. 37 Dairy

Dairy Overview U.S. Industry The United States is the world s largest milk producer, its output of almost 78.2 million mt in 2003 having accounted for about 15 percent of the world s milk supply. 37 Dairy

Status and trends in milk production world wide

Milk production is a very important element of the whole dairy chain. In this part of the value chain the major share of a) the costs, b) resources used, c) emissions created and d) the political challenges

Milk production is a very important element of the whole dairy chain. In this part of the value chain the major share of a) the costs, b) resources used, c) emissions created and d) the political challenges

Milk and Milk Products: Price and Trade Update

Milk and Milk Products: Price and Trade Update International dairy prices December 2017 1 The FAO Dairy Price Index d 204.2 points in November, up 11.2 points (5.8 percent) from January 2017. At this level,

Milk and Milk Products: Price and Trade Update International dairy prices December 2017 1 The FAO Dairy Price Index d 204.2 points in November, up 11.2 points (5.8 percent) from January 2017. At this level,

Dairy Outlook. April By Jim Dunn Professor of Agricultural Economics, Penn State University. Market Psychology

Dairy Outlook April 2017 By Jim Dunn Professor of Agricultural Economics, Penn State University Market Psychology The Class III price in March was $1.07 lower than in February, while the Class IV price

Dairy Outlook April 2017 By Jim Dunn Professor of Agricultural Economics, Penn State University Market Psychology The Class III price in March was $1.07 lower than in February, while the Class IV price

South African Milk Processors Organisation

South African Milk Processors Organisation The voluntary organisation of milk processors for the promotion of the development of the secondary dairy industry to the benefit of the dairy industry, the consumer

South African Milk Processors Organisation The voluntary organisation of milk processors for the promotion of the development of the secondary dairy industry to the benefit of the dairy industry, the consumer

World butter production

The Global Butter Market New Opportunities? International Dairy Magazine. PM FOOD & DAIRY CONSULTING has publishing a report about the Global Butter Market. It is a comprehensive analysis of the butter

The Global Butter Market New Opportunities? International Dairy Magazine. PM FOOD & DAIRY CONSULTING has publishing a report about the Global Butter Market. It is a comprehensive analysis of the butter

Dairy Market. January 2018

Dairy Market Dairy Management Inc. R E P O R T Volume 21 No. 1 January 2018 DMI NMPF Overview Looking back at 2017, the U.S. Department of Agriculture (USDA) estimates an average U.S. all-milk price of

Dairy Market Dairy Management Inc. R E P O R T Volume 21 No. 1 January 2018 DMI NMPF Overview Looking back at 2017, the U.S. Department of Agriculture (USDA) estimates an average U.S. all-milk price of

Dairy Outlook. September By Jim Dunn Professor of Agricultural Economics, Penn State University. Market Psychology

Dairy Outlook September 2015 By Jim Dunn Professor of Agricultural Economics, Penn State University Market Psychology The world s financial markets were rattled last month by a pair of Chinese currency

Dairy Outlook September 2015 By Jim Dunn Professor of Agricultural Economics, Penn State University Market Psychology The world s financial markets were rattled last month by a pair of Chinese currency

Organization of the dairy industry in Europe. Overview

Organization of the dairy industry in Europe Overview Clotilde Patry, Xavier David, Didier Boichard, Eric Venot, Vincent Ducrocq, 06/05/2014 _01 Contribution of EU in the dairy worldwide market C.PATRY,

Organization of the dairy industry in Europe Overview Clotilde Patry, Xavier David, Didier Boichard, Eric Venot, Vincent Ducrocq, 06/05/2014 _01 Contribution of EU in the dairy worldwide market C.PATRY,

Dairy Outlook. March By Jim Dunn Professor of Agricultural Economics, Penn State University. Market Psychology

Dairy Outlook March 2015 By Jim Dunn Professor of Agricultural Economics, Penn State University Market Psychology Cheese and butter prices have d slightly in the past month, while the powdered product

Dairy Outlook March 2015 By Jim Dunn Professor of Agricultural Economics, Penn State University Market Psychology Cheese and butter prices have d slightly in the past month, while the powdered product

For personal use only

MAY 2016 GLOBAL DAIRY UPDATE #431AM SHARE YOUR STORY OUR MARKETS OUR PERFORMANCE In April, Fonterra New Zealand milk collection decreased 3 and Fonterra Australia milk collection decreased 5. Forecast

MAY 2016 GLOBAL DAIRY UPDATE #431AM SHARE YOUR STORY OUR MARKETS OUR PERFORMANCE In April, Fonterra New Zealand milk collection decreased 3 and Fonterra Australia milk collection decreased 5. Forecast

Agri-Service Industry Report

Years Since Presidential Election 1950 1955 1960 1965 1970 1975 1980 1985 1990 1995 2000 2005 2010 2015 Billions Agri-Service Industry Report November 2016 Dan Hassler Farm Income and Presidential Elections

Years Since Presidential Election 1950 1955 1960 1965 1970 1975 1980 1985 1990 1995 2000 2005 2010 2015 Billions Agri-Service Industry Report November 2016 Dan Hassler Farm Income and Presidential Elections

For personal use only

18 April 2013 ASX Release TRADING UPDATE Warrnambool Cheese and Butter Factory Company Holdings Limited (WCB) announces that consistent with its half year results announcement on 28 February 2013, the

18 April 2013 ASX Release TRADING UPDATE Warrnambool Cheese and Butter Factory Company Holdings Limited (WCB) announces that consistent with its half year results announcement on 28 February 2013, the

The milk package and the prospects for the dairy sector

The milk package and the prospects for the dairy sector Answers to five questions in the light of the French experience Vincent CHATELLIER INRA, SMART-LERECO (France) European Parliament Commission Agriculture

The milk package and the prospects for the dairy sector Answers to five questions in the light of the French experience Vincent CHATELLIER INRA, SMART-LERECO (France) European Parliament Commission Agriculture

Hog Producers Near the End of Losses

Hog Producers Near the End of Losses January 2003 Chris Hurt Last year was another tough one for many hog producers unless they had contracts that kept the prices they received much above the average spot

Hog Producers Near the End of Losses January 2003 Chris Hurt Last year was another tough one for many hog producers unless they had contracts that kept the prices they received much above the average spot

Dairy Outlook. June By Jim Dunn Professor of Agricultural Economics, Penn State University. Market Psychology

Dairy Outlook June 2015 By Jim Dunn Professor of Agricultural Economics, Penn State University Market Psychology Cheese prices have been rising this past month, rising 16 cents/lb. in a fairly steady climb.

Dairy Outlook June 2015 By Jim Dunn Professor of Agricultural Economics, Penn State University Market Psychology Cheese prices have been rising this past month, rising 16 cents/lb. in a fairly steady climb.

Argentina. Poultry and Products Annual. Argentina Poultry & Products Annual

THIS REPORT CONTAINS ASSESSMENTS OF COMMODITY AND TRADE ISSUES MADE BY USDA STAFF AND NOT NECESSARILY STATEMENTS OF OFFICIAL U.S. GOVERNMENT POLICY Required Report - public distribution Date: GAIN Report

THIS REPORT CONTAINS ASSESSMENTS OF COMMODITY AND TRADE ISSUES MADE BY USDA STAFF AND NOT NECESSARILY STATEMENTS OF OFFICIAL U.S. GOVERNMENT POLICY Required Report - public distribution Date: GAIN Report

TPP and Canada s Dairy Sector: How Reducing Protection Can Increase Rents. Richard Barichello

TPP and Canada s Dairy Sector: How Reducing Protection Can Increase Rents Richard Barichello Selected Paper prepared for presentation at the International Agricultural Trade Research Consortium s (IATRC

TPP and Canada s Dairy Sector: How Reducing Protection Can Increase Rents Richard Barichello Selected Paper prepared for presentation at the International Agricultural Trade Research Consortium s (IATRC

Driving Productivity Growth in the Irish Agri-Food Sector

Driving Productivity Growth in the Irish Agri-Food Sector Dr. Pat Dillon Teagasc, Moorepark Dairy Production Research Centre, Fermoy, Co Cork Overview 1. Global Food Markets 2. Irish Agri-Food Industry

Driving Productivity Growth in the Irish Agri-Food Sector Dr. Pat Dillon Teagasc, Moorepark Dairy Production Research Centre, Fermoy, Co Cork Overview 1. Global Food Markets 2. Irish Agri-Food Industry

Executive summary. Butter prices at record levels

June 2017 Executive summary Butter prices at record levels South African milk production growth disappointed in the first five months of 2017. Total production during this period is marginally lower than

June 2017 Executive summary Butter prices at record levels South African milk production growth disappointed in the first five months of 2017. Total production during this period is marginally lower than

MILK AND MILK PRODUCTS

Market summaries MILK AND MILK PRODUCTS World milk production is set to reach 833.5 million tonnes in, 1.4 percent more than in. Much of the anticipated rise is expected in Asia and the Americas, while

Market summaries MILK AND MILK PRODUCTS World milk production is set to reach 833.5 million tonnes in, 1.4 percent more than in. Much of the anticipated rise is expected in Asia and the Americas, while

SOYBEANS: LARGE SUPPLIES CONFIRMED, BUT WHAT ABOUT 2005 PRODUCTION?

SOYBEANS: LARGE SUPPLIES CONFIRMED, BUT WHAT ABOUT 2005 PRODUCTION? JANUARY 2005 Darrel Good 2005 NO. 2 Summary USDA s January reports confirmed a record large 2004 U.S. crop, prospects for large year-ending

SOYBEANS: LARGE SUPPLIES CONFIRMED, BUT WHAT ABOUT 2005 PRODUCTION? JANUARY 2005 Darrel Good 2005 NO. 2 Summary USDA s January reports confirmed a record large 2004 U.S. crop, prospects for large year-ending

Analysis & Comments. Livestock Marketing Information Center State Extension Services in Cooperation with USDA. National Hay Situation and Outlook

Analysis & Comments Livestock Marketing Information Center State Extension Services in Cooperation with USDA April 2, 2015 Letter #12 www.lmic.info National Hay Situation and Outlook The 2014 calendar

Analysis & Comments Livestock Marketing Information Center State Extension Services in Cooperation with USDA April 2, 2015 Letter #12 www.lmic.info National Hay Situation and Outlook The 2014 calendar

U.S. Dairy Export Markets

Today s Topics US. Markets and Prices 2015 U.S. Dairy Safety Net Policy U.S. Dairy Export Markets Cameron Thraen, OSU-AEDE Extension State Specialist Dairy Markets & Policy Website @ AEDE/OSU: http://aede.osu.edu/research/ohio-dairy-web

Today s Topics US. Markets and Prices 2015 U.S. Dairy Safety Net Policy U.S. Dairy Export Markets Cameron Thraen, OSU-AEDE Extension State Specialist Dairy Markets & Policy Website @ AEDE/OSU: http://aede.osu.edu/research/ohio-dairy-web

"Economic analysis of the effects of the expiry of the EU milk quota system"

"Economic analysis of the effects of the expiry of the EU milk quota system" Contract 30-C3-0144181/00-30 FINAL REPORT Scientific Responsible: Vincent Réquillart Experts involved: Zohra Bouamra-Mechemache

"Economic analysis of the effects of the expiry of the EU milk quota system" Contract 30-C3-0144181/00-30 FINAL REPORT Scientific Responsible: Vincent Réquillart Experts involved: Zohra Bouamra-Mechemache

Food Price Outlook,

Provided By: Food Price Outlook, 2017-18 This page provides the following information for August 2017: Consumer Price Index (CPI) for Food (not seasonally adjusted) Producer Price Index (PPI) for Food

Provided By: Food Price Outlook, 2017-18 This page provides the following information for August 2017: Consumer Price Index (CPI) for Food (not seasonally adjusted) Producer Price Index (PPI) for Food

Speech by Vice President Jyrki Katainen, at the Extraordinary Agriculture and Fisheries Council 7 September 2015

Speech by Vice President Jyrki Katainen, at the Extraordinary Agriculture and Fisheries Council 7 September 2015 Introduction Mr President, Members of the Council, I should begin by apologising for the

Speech by Vice President Jyrki Katainen, at the Extraordinary Agriculture and Fisheries Council 7 September 2015 Introduction Mr President, Members of the Council, I should begin by apologising for the

Global Dairy Industry: The Milky Way

Global Dairy Industry: The Milky Way Table of Contents 1. Executive Summary 2. Global Overview 2.1 Global Milk Production 2.2 Milk Production by Species Cow 2.3 Milk Production by Species - Buffalo 2.4

Global Dairy Industry: The Milky Way Table of Contents 1. Executive Summary 2. Global Overview 2.1 Global Milk Production 2.2 Milk Production by Species Cow 2.3 Milk Production by Species - Buffalo 2.4

Dairy Situation and Outlook

Dairy Situation and Outlook Piasecki H-21 Improving Employee Engagement Sally Roberts, Blake Robinson, John Droppert June 2017 John Droppert Senior Industry Analyst Last time we spoke March 2017 2 The

Dairy Situation and Outlook Piasecki H-21 Improving Employee Engagement Sally Roberts, Blake Robinson, John Droppert June 2017 John Droppert Senior Industry Analyst Last time we spoke March 2017 2 The

Production, yields and productivity

Production, yields and productivity Contents 1. Production development... 3 2. Yield developments... 6 3. Total factor productivity (TFP)... 8 4. Costs of production in the EU... 1 This document does not

Production, yields and productivity Contents 1. Production development... 3 2. Yield developments... 6 3. Total factor productivity (TFP)... 8 4. Costs of production in the EU... 1 This document does not

U.S. Dairy at a New Crossroads in a Global Setting

U.S. Dairy at a New Crossroads in a Global Setting VOLUME 3 ISSUE 5 32 Don P. Blayney dblayney@ers.usda.gov Mark J. Gehlhar mgehlhar@ers.usda.gov Domestic dairy industries and markets worldwide are often

U.S. Dairy at a New Crossroads in a Global Setting VOLUME 3 ISSUE 5 32 Don P. Blayney dblayney@ers.usda.gov Mark J. Gehlhar mgehlhar@ers.usda.gov Domestic dairy industries and markets worldwide are often

Prospects for Agricultural Markets and Income in the EU

Prospects for Agricultural Markets and Income in the EU 2010-2020 December 2010 European Commission Agriculture and Rural Development Page blanche NOTE TO THE READERS The outlook presented in this publication

Prospects for Agricultural Markets and Income in the EU 2010-2020 December 2010 European Commission Agriculture and Rural Development Page blanche NOTE TO THE READERS The outlook presented in this publication

dairy: key outcomes Key outcomes trans-pacific partnership NZ$96m Estimated annual tariff savings when TPP is fully implemented.

CANADA JAPAN UNITED STATES OF AMERICA MEXICO VIET NAM BRUNEI MALAYSIA SINGAPORE PERU AUSTRALIA NEW ZEALAND CHILE trans-pacific partnership dairy: key outcomes FACT SHEET New Zealand dairy exports to the

CANADA JAPAN UNITED STATES OF AMERICA MEXICO VIET NAM BRUNEI MALAYSIA SINGAPORE PERU AUSTRALIA NEW ZEALAND CHILE trans-pacific partnership dairy: key outcomes FACT SHEET New Zealand dairy exports to the

The Common Agricultural Policy (CAP) is the first common policy adopted by the

is the first common policy adopted by the") Evaluation of Agricultural Policy Reforms in the European Union OECD 2011 Executive Summary The Common Agricultural Policy (CAP) is the first common policy adopted by the European Community under the Treaty

Evaluation of Agricultural Policy Reforms in the European Union OECD 2011 Executive Summary The Common Agricultural Policy (CAP) is the first common policy adopted by the European Community under the Treaty

THIS REPORT CONTAINS ASSESSMENTS OF COMMODITY AND TRADE ISSUES MADE BY USDA STAFF AND NOT NECESSARILY STATEMENTS OF OFFICIAL U.S.

THIS REPORT CONTAINS ASSESSMENTS OF COMMODITY AND TRADE ISSUES MADE BY USDA STAFF AND NOT NECESSARILY STATEMENTS OF OFFICIAL U.S. GOVERNMENT POLICY Required Report - public distribution Date: GAIN Report

THIS REPORT CONTAINS ASSESSMENTS OF COMMODITY AND TRADE ISSUES MADE BY USDA STAFF AND NOT NECESSARILY STATEMENTS OF OFFICIAL U.S. GOVERNMENT POLICY Required Report - public distribution Date: GAIN Report

US Imported Beef Market A Weekly Update

US Imported Beef Market A Weekly Update Prepared Exclusively for Meat & Livestock Australia - Sydney Volume XVII, Issue 47 November 24, 2017 Prepared by: Steiner Consulting Group SteinerConsulting.com

US Imported Beef Market A Weekly Update Prepared Exclusively for Meat & Livestock Australia - Sydney Volume XVII, Issue 47 November 24, 2017 Prepared by: Steiner Consulting Group SteinerConsulting.com

Michigan s Dairy Industry. Ken Nobis, MMPA President

Michigan s Dairy Industry Ken Nobis, MMPA President ONE CENTURY STRONG 1,200 DAIRY FARMS 5 Billion LBS. OF MILK Quality Integrity Leadership Progressive Community MMPA Locations Products made at Ovid &

Michigan s Dairy Industry Ken Nobis, MMPA President ONE CENTURY STRONG 1,200 DAIRY FARMS 5 Billion LBS. OF MILK Quality Integrity Leadership Progressive Community MMPA Locations Products made at Ovid &

THE DRIVERS OF HAY AND FORAGE CROP EXPORTS FOR THE WESTERN UNITED STATES. William A. Matthews and Daniel A. Sumner 1 ABSTRACT

THE DRIVERS OF HAY AND FORAGE CROP EXPORTS FOR THE WESTERN UNITED STATES William A. Matthews and Daniel A. Sumner 1 ABSTRACT Exports have provided an economic boost to the Western U.S. forage crop industry

THE DRIVERS OF HAY AND FORAGE CROP EXPORTS FOR THE WESTERN UNITED STATES William A. Matthews and Daniel A. Sumner 1 ABSTRACT Exports have provided an economic boost to the Western U.S. forage crop industry

WORLD AGRICULTURAL OUTLOOK

WORLD AGRICULTURAL OUTLOOK FEBRUARY 21 FAPRI Food and Agricultural Policy Research Institute CENTER FOR AGRICULTURAL AND RURAL DEVELOPMENT IOWA STATE UNIVERSITY AMES, IOWA 511-17 TELEPHONE: 515.294.7519

WORLD AGRICULTURAL OUTLOOK FEBRUARY 21 FAPRI Food and Agricultural Policy Research Institute CENTER FOR AGRICULTURAL AND RURAL DEVELOPMENT IOWA STATE UNIVERSITY AMES, IOWA 511-17 TELEPHONE: 515.294.7519

MONTHLY DAIRY. Zero growth for NZ s milk supply 6.36 OCTOBER Inside this issue

OCTOBER 217 MONTHLY DAIRY NZ MILK PRODUCTION FORECAST 217-18 % Inside this issue Dairy commodity markets 2 Milk production 7 Milk price 1 Dairy company share prices 12 AGRIHQ WMP PRICE NZX WMP FUTURES

OCTOBER 217 MONTHLY DAIRY NZ MILK PRODUCTION FORECAST 217-18 % Inside this issue Dairy commodity markets 2 Milk production 7 Milk price 1 Dairy company share prices 12 AGRIHQ WMP PRICE NZX WMP FUTURES

Missouri Dairy Grazing Conference

Missouri Dairy Grazing Conference GRAZING AROUND THE WORLD Michael Murphy Dairy Producer Dairy Producer Ireland By 2050 Estimated NEED + 60% more food than now 2009 Eti Estimated td12 16% land very under

Missouri Dairy Grazing Conference GRAZING AROUND THE WORLD Michael Murphy Dairy Producer Dairy Producer Ireland By 2050 Estimated NEED + 60% more food than now 2009 Eti Estimated td12 16% land very under

Seventh Multi-year Expert Meeting on Commodities and Development April 2015 Geneva

Seventh Multi-year Expert Meeting on Commodities and Development 15-16 April 2015 Geneva Recent Developments in Global Commodity Markets By Georges Rapsomanikis Senior Economist in the Trade and Markets

Seventh Multi-year Expert Meeting on Commodities and Development 15-16 April 2015 Geneva Recent Developments in Global Commodity Markets By Georges Rapsomanikis Senior Economist in the Trade and Markets

LATEST POSITION ACROSS NORTH-WESTERN EUROPE

7 July 2015 AHDB Potatoes business report for Northern Europe The following articles include: 7 July 2015 North-Western European (NEPG) 2015 area estimate, market update and crop update. Potential GB 2015

7 July 2015 AHDB Potatoes business report for Northern Europe The following articles include: 7 July 2015 North-Western European (NEPG) 2015 area estimate, market update and crop update. Potential GB 2015

Wheat Year in Review (International): Low 2007/08 Stocks and Higher Prices Drive Outlook

: Low 2007/08 Stocks and Higher Prices Drive Outlook") United States Department of Agriculture WHS-2008-01 May 2008 A Report from the Economic Research Service Wheat Year in Review (International): Low 2007/08 Stocks and Higher Prices Drive Outlook www.ers.usda.gov

United States Department of Agriculture WHS-2008-01 May 2008 A Report from the Economic Research Service Wheat Year in Review (International): Low 2007/08 Stocks and Higher Prices Drive Outlook www.ers.usda.gov

THIS REPORT CONTAINS ASSESSMENTS OF COMMODITY AND TRADE ISSUES MADE BY USDA STAFF AND NOT NECESSARILY STATEMENTS OF OFFICIAL U.S.

THIS REPORT CONTAINS ASSESSMENTS OF COMMODITY AND TRADE ISSUES MADE BY USDA STAFF AND NOT NECESSARILY STATEMENTS OF OFFICIAL U.S. GOVERNMENT POLICY Required Report - public distribution Date: GAIN Report

THIS REPORT CONTAINS ASSESSMENTS OF COMMODITY AND TRADE ISSUES MADE BY USDA STAFF AND NOT NECESSARILY STATEMENTS OF OFFICIAL U.S. GOVERNMENT POLICY Required Report - public distribution Date: GAIN Report

STANDARDIZED MILK PRICE CALCULATIONS for JUNE 2009 deliveries

STANDARDIZED MILK PRICE CALCULATIONS for JUNE deliveries Company Milcobel Alois Müller Humana Milchunion eg Nordmilch Arla Foods Hämeenlinnan Osuusmeijeri Bongrain CLE (Basse Normandie) Da (Pas de Calais)

STANDARDIZED MILK PRICE CALCULATIONS for JUNE deliveries Company Milcobel Alois Müller Humana Milchunion eg Nordmilch Arla Foods Hämeenlinnan Osuusmeijeri Bongrain CLE (Basse Normandie) Da (Pas de Calais)

THIS REPORT CONTAINS ASSESSMENTS OF COMMODITY AND TRADE ISSUES MADE BY USDA STAFF AND NOT NECESSARILY STATEMENTS OF OFFICIAL U.S.

THIS REPORT CONTAINS ASSESSMENTS OF COMMODITY AND TRADE ISSUES MADE BY USDA STAFF AND NOT NECESSARILY STATEMENTS OF OFFICIAL U.S. GOVERNMENT POLICY Required Report - public distribution Date: 11/10/2009

THIS REPORT CONTAINS ASSESSMENTS OF COMMODITY AND TRADE ISSUES MADE BY USDA STAFF AND NOT NECESSARILY STATEMENTS OF OFFICIAL U.S. GOVERNMENT POLICY Required Report - public distribution Date: 11/10/2009

Livestock products: Domestic and international market a view of 2015

Livestock products: Domestic and international market a view of 2015 Alina Zharko Association Ukrainian agribusiness club Dairy products Production of milk and dairy products in Ukraine Dairy products

Livestock products: Domestic and international market a view of 2015 Alina Zharko Association Ukrainian agribusiness club Dairy products Production of milk and dairy products in Ukraine Dairy products

Market Review of the Organic Dairy Sector in Wales, Executive Summary and Recommendations. Organic Centre Wales Better Organic Business Links

Market Review of the Organic Dairy Sector in Wales, 2009 Executive Summary and Recommendations Organic Centre Wales Better Organic Business Links March 2010 Submitted to: Organic Centre Wales Date: March

Market Review of the Organic Dairy Sector in Wales, 2009 Executive Summary and Recommendations Organic Centre Wales Better Organic Business Links March 2010 Submitted to: Organic Centre Wales Date: March

Competitiveness of Livestock Production in the Process of Joining the EU

REVIEW 37 Competitiveness of Livestock Production in the Process of Joining the EU SUMMARY The accession of the eight CEE member states to the EU will integrate about 450 million consumers with rather

REVIEW 37 Competitiveness of Livestock Production in the Process of Joining the EU SUMMARY The accession of the eight CEE member states to the EU will integrate about 450 million consumers with rather

Discontinuing Dairy Product Price Support Program (DPPSP) would allow greater flexibility to meet increased global demand and shorten periods of low

would allow greater flexibility to meet increased global demand and shorten periods of low") Discontinuing Dairy Product Price Support Program (DPPSP) would allow greater flexibility to meet increased global demand and shorten periods of low prices by reducing foreign competition Creating a program

Discontinuing Dairy Product Price Support Program (DPPSP) would allow greater flexibility to meet increased global demand and shorten periods of low prices by reducing foreign competition Creating a program

agri benchmark Organic A standard operating procedure to define typical organic farms

agri benchmark Organic A standard operating procedure to define typical organic farms Braunschweig, 2016 Thünen Institute of Farm Economics Johann Heinrich von Thünen-Institut Bundesforschungsinstitut

agri benchmark Organic A standard operating procedure to define typical organic farms Braunschweig, 2016 Thünen Institute of Farm Economics Johann Heinrich von Thünen-Institut Bundesforschungsinstitut

CORN: DECLINING WORLD GRAIN STOCKS OFFERS POTENTIAL FOR HIGHER PRICES

CORN: DECLINING WORLD GRAIN STOCKS OFFERS POTENTIAL FOR HIGHER PRICES OCTOBER 2000 Darrel Good Summary The 2000 U.S. corn crop is now estimated at 10.192 billion bushels, 755 million (8 percent) larger

CORN: DECLINING WORLD GRAIN STOCKS OFFERS POTENTIAL FOR HIGHER PRICES OCTOBER 2000 Darrel Good Summary The 2000 U.S. corn crop is now estimated at 10.192 billion bushels, 755 million (8 percent) larger

Irish Agricultural Land Market Review

Irish Agricultural Land Market Review Q2 2015 Irish Agricultural Land Market Review 1 2 Irish Agricultural Land Market Review Irish Agricultural Land Market Review All Farmland Prices in the Irish agricultural

Irish Agricultural Land Market Review Q2 2015 Irish Agricultural Land Market Review 1 2 Irish Agricultural Land Market Review Irish Agricultural Land Market Review All Farmland Prices in the Irish agricultural

THIS REPORT CONTAINS ASSESSMENTS OF COMMODITY AND TRADE ISSUES MADE BY USDA STAFF AND NOT NECESSARILY STATEMENTS OF OFFICIAL U.S.

THI REPORT CONTIN EMENT OF COMMOITY N TRE IE ME BY TFF N NOT NECERILY TTEMENT OF OFFICIL.. GOVERNMENT POLICY Required Report - public distribution ate: GIN Report Number: G4 // lgeria airy and Products

THI REPORT CONTIN EMENT OF COMMOITY N TRE IE ME BY TFF N NOT NECERILY TTEMENT OF OFFICIL.. GOVERNMENT POLICY Required Report - public distribution ate: GIN Report Number: G4 // lgeria airy and Products

October 20, 1998 Ames, Iowa Econ. Info U.S., WORLD CROP ESTIMATES TIGHTEN SOYBEAN SUPPLY- DEMAND:

October 20, 1998 Ames, Iowa Econ. Info. 1752 U.S., WORLD CROP ESTIMATES TIGHTEN SOYBEAN SUPPLY- DEMAND: USDA's domestic and world crop estimates show a less burdensome world supply-demand balance for soybeans

October 20, 1998 Ames, Iowa Econ. Info. 1752 U.S., WORLD CROP ESTIMATES TIGHTEN SOYBEAN SUPPLY- DEMAND: USDA's domestic and world crop estimates show a less burdensome world supply-demand balance for soybeans

Developments, strategies and challenges for the French dairy sector

Developments, strategies and challenges for the French dairy sector Brocard Valérie, Perrot Christophe, You Gérard, Le Gall André - Institut de l Elevage www.idele.fr EAAP 2016 Belfast 29/8/16 www.idele.fr

Developments, strategies and challenges for the French dairy sector Brocard Valérie, Perrot Christophe, You Gérard, Le Gall André - Institut de l Elevage www.idele.fr EAAP 2016 Belfast 29/8/16 www.idele.fr

Eric Erba. California Dairies, Inc.

Dairy Situation and Outlook Eric Erba California Dairies, Inc. Dairy Situation and Outlook Thoughts from 2008 Dairy industry at a crossroads Level of government involvement Modifications of decades-old

Dairy Situation and Outlook Eric Erba California Dairies, Inc. Dairy Situation and Outlook Thoughts from 2008 Dairy industry at a crossroads Level of government involvement Modifications of decades-old

High commodity prices and volatility what lies behind the roller coaster ride?

Agricultural Markets Brief Brief nº 1 June 2011 High commodity prices and volatility what lies behind the roller coaster ride? 1. Is agricultural price volatility on the rise? 2. Is increased price volatility

Agricultural Markets Brief Brief nº 1 June 2011 High commodity prices and volatility what lies behind the roller coaster ride? 1. Is agricultural price volatility on the rise? 2. Is increased price volatility

Sugar market post quota. Short Term Outlook and Medium Term Prospects

Sugar market post quota Short Term Outlook and Medium Term Prospects Sugar market observatory 15 November 2017 Content Short term outlook for the European sugar market Autumn 2017 published early October

Sugar market post quota Short Term Outlook and Medium Term Prospects Sugar market observatory 15 November 2017 Content Short term outlook for the European sugar market Autumn 2017 published early October

Rice Outlook and Baseline Projections. University of Arkansas Webinar Series February 13, 2015 Nathan Childs, Economic Research Service, USDA

Rice Outlook and Baseline Projections University of Arkansas Webinar Series February 13, 2015 Nathan Childs, Economic Research Service, USDA THE GLOBAL RICE MARKET PART 1 The 2014/15 Global Rice Market:

Rice Outlook and Baseline Projections University of Arkansas Webinar Series February 13, 2015 Nathan Childs, Economic Research Service, USDA THE GLOBAL RICE MARKET PART 1 The 2014/15 Global Rice Market:

Forecasting Techniques. 5/17/2008 Cromford Associates LLC Mike Orr

Forecasting Techniques 5/17/2008 Cromford Associates LLC Mike Orr Introduction It is true that no-one can predict with certainty what will happen in the future. However real estate is a cyclical market

Forecasting Techniques 5/17/2008 Cromford Associates LLC Mike Orr Introduction It is true that no-one can predict with certainty what will happen in the future. However real estate is a cyclical market

CHAPTER 5 INTERNATIONAL TRADE

CHAPTER 5 INTERNATIONAL TRADE LEARNING OBJECTIVES: 1. Describe the relation between international trade volume and world output, and identify overall trade patterns. 2. Describe mercantilism, and explain

CHAPTER 5 INTERNATIONAL TRADE LEARNING OBJECTIVES: 1. Describe the relation between international trade volume and world output, and identify overall trade patterns. 2. Describe mercantilism, and explain

RESULTS OF THE MULTI-NATIONAL FARMERS CONFIDENCE INDEX 2016Q3

ECON(16)11042:1 KT/al Brussels, 16 th December 2016 RESULTS OF THE MULTI-NATIONAL FARMERS CONFIDENCE INDEX 2016Q3 THE SENTIMENT OF EUROPEAN FARMERS HAS SLIGHTLY RECOVERED, BUT THE SITUATION REMAINS STILL

ECON(16)11042:1 KT/al Brussels, 16 th December 2016 RESULTS OF THE MULTI-NATIONAL FARMERS CONFIDENCE INDEX 2016Q3 THE SENTIMENT OF EUROPEAN FARMERS HAS SLIGHTLY RECOVERED, BUT THE SITUATION REMAINS STILL

Procurement, Production and Marketing at Supply-Driven Milk and Milk Products Cooperative

Procurement, Production and Marketing at Supply-Driven Milk and Milk Products Cooperative Omkar D. Palsule-Desai and Katta G. Murty MMPC - Milk and Milk Products Cooperative - is a cooperative organization

Procurement, Production and Marketing at Supply-Driven Milk and Milk Products Cooperative Omkar D. Palsule-Desai and Katta G. Murty MMPC - Milk and Milk Products Cooperative - is a cooperative organization

Global Dairy Industry: The Milky Way

Global Dairy Industry: The Milky Way Synopsis A steady rise in consumption demand for dairy and allied products has led to higher levels of technology adoption among the major dairy producing countries

Global Dairy Industry: The Milky Way Synopsis A steady rise in consumption demand for dairy and allied products has led to higher levels of technology adoption among the major dairy producing countries

VOL 20. NO 2 November 2017 LACTODATA. A Milk SA publication compiled by the Milk Producers Organisation. South African Milk Processors Organisation

VOL 20 NO 2 November 2017 A Milk SA publication compiled by the Milk Producers Organisation Suid-Afrikaanse Melkprosesseerdersorganisasie South African Milk Processors Organisation LACTODATA LACTODATA

VOL 20 NO 2 November 2017 A Milk SA publication compiled by the Milk Producers Organisation Suid-Afrikaanse Melkprosesseerdersorganisasie South African Milk Processors Organisation LACTODATA LACTODATA

Hog:Corn Ratio What can we learn from the old school?

October 16, 2006 Ames, Iowa Econ. Info. 1944 Hog:Corn Ratio What can we learn from the old school? Economists have studied the hog to corn ratio for over 100 years. This ratio is simply the live hog price

October 16, 2006 Ames, Iowa Econ. Info. 1944 Hog:Corn Ratio What can we learn from the old school? Economists have studied the hog to corn ratio for over 100 years. This ratio is simply the live hog price

Sheep meat balance in Republic of Macedonia

Sheep meat balance ORIGINAL in Republic SCIENTIFIC of Macedonia PAPER Sheep meat balance in Republic of Macedonia Ana KOTEVSKA, Jovan AŽDERSKI, Dragi DIMITRIEVSKI Faculty of Agricultural Sciences and Food

Sheep meat balance ORIGINAL in Republic SCIENTIFIC of Macedonia PAPER Sheep meat balance in Republic of Macedonia Ana KOTEVSKA, Jovan AŽDERSKI, Dragi DIMITRIEVSKI Faculty of Agricultural Sciences and Food

High-Specification Dairy Ingredients

High-Specification Dairy Ingredients Increasing Export Opportunities by Reducing Spore Formers in Milk powders The Dairy Practices Council 47 th Annual Conference November 10, 2016 Managed by Dairy Management

High-Specification Dairy Ingredients Increasing Export Opportunities by Reducing Spore Formers in Milk powders The Dairy Practices Council 47 th Annual Conference November 10, 2016 Managed by Dairy Management

Table 1. U.S. Agricultural Exports as a Share of Production, 1992

Export markets are important to U.S. agriculture, absorbing a substantial portion of total production of many important commodities. During the last two decades there have been periods of expansion and

Export markets are important to U.S. agriculture, absorbing a substantial portion of total production of many important commodities. During the last two decades there have been periods of expansion and

Canada s Dairy Industry at a Glance

Canada s Dairy Industry at a Glance Overview The Canadian dairy sector operates under a supply management system based on planned domestic production, administered pricing and dairy product import controls.

Canada s Dairy Industry at a Glance Overview The Canadian dairy sector operates under a supply management system based on planned domestic production, administered pricing and dairy product import controls.

DMSP POTENTIAL IMPACT ON U.S. DAIRY EXPORTS

DMSP POTENTIAL IMPACT ON U.S. DAIRY EXPORTS Prepared by: Prepared for: International Dairy Foods Association June 2012 Table of Contents Executive Summary... 2 I. Evolution of U.S. Dairy Exports... 3 Stage

DMSP POTENTIAL IMPACT ON U.S. DAIRY EXPORTS Prepared by: Prepared for: International Dairy Foods Association June 2012 Table of Contents Executive Summary... 2 I. Evolution of U.S. Dairy Exports... 3 Stage

Agriculture: expansions highlighted developments

Agriculture: expansions highlighted developments A broad-based expansion in livestock production and another bumper grain harvest highlighted agricultural developments in 1976. Meat production rose 9 percent

Agriculture: expansions highlighted developments A broad-based expansion in livestock production and another bumper grain harvest highlighted agricultural developments in 1976. Meat production rose 9 percent

AGOA s Final Frontier: Removing US Farm Trade Barriers

CGD NOTES AGOA s Final Frontier: Removing US Farm Trade Barriers 7/23/14 (http://dev.cgdev.org/publication/agoa%e2%80%99s-final-frontier-removing-us-farm-trade-barriers) Kimberly Ann Elliott If the African

CGD NOTES AGOA s Final Frontier: Removing US Farm Trade Barriers 7/23/14 (http://dev.cgdev.org/publication/agoa%e2%80%99s-final-frontier-removing-us-farm-trade-barriers) Kimberly Ann Elliott If the African

Opportunities and Challenges for Cow/Calf Producers 1. Rick Rasby Extension Beef Specialist University of Nebraska

Opportunities and Challenges for Cow/Calf Producers 1 Rick Rasby Extension Beef Specialist University of Nebraska Introduction The cow/calf enterprise has been a profitable enterprise over the last few

Opportunities and Challenges for Cow/Calf Producers 1 Rick Rasby Extension Beef Specialist University of Nebraska Introduction The cow/calf enterprise has been a profitable enterprise over the last few

IFA Medium-Term Fertilizer Outlook

IFA Medium-Term Fertilizer Outlook 2015 2019 Olivier Rousseau IFA Secretariat Afcome 2015 Reims, France October 21 st - 23 rd 2015 Outlook for World Agriculture and Fertilizer Demand Economic and policy

IFA Medium-Term Fertilizer Outlook 2015 2019 Olivier Rousseau IFA Secretariat Afcome 2015 Reims, France October 21 st - 23 rd 2015 Outlook for World Agriculture and Fertilizer Demand Economic and policy

'Vision for the Irish Dairy Industry'

Presentation in Context 'Vision for the Irish Dairy Industry'» Recent Discussion 'Imperative that Ireland restructures its dairy industry to compete in global market'» Solution? 'Evolution or Revolution'

Presentation in Context 'Vision for the Irish Dairy Industry'» Recent Discussion 'Imperative that Ireland restructures its dairy industry to compete in global market'» Solution? 'Evolution or Revolution'

The World Dairy Situation

The World Dairy Situation 2014 1 1 Summary report on IDF Bull. 476/2014 World Dairy Situation 2013 available from IDF www.fil.idf.org Introduction The 2014 World Dairy Situation report was published in

The World Dairy Situation 2014 1 1 Summary report on IDF Bull. 476/2014 World Dairy Situation 2013 available from IDF www.fil.idf.org Introduction The 2014 World Dairy Situation report was published in

Despite Slowing Herd Expansion-- Can Domestic, Export Beef Demand Keep Pace?

Despite Slowing Herd Expansion-- Can Domestic, Export Beef Demand Keep Pace? Presented by Mike Sands MBS Research Forecasting Agricultural and Biofuels Interplay The Jacobsen--Chicago May 23, 2018 1 Livestock

Despite Slowing Herd Expansion-- Can Domestic, Export Beef Demand Keep Pace? Presented by Mike Sands MBS Research Forecasting Agricultural and Biofuels Interplay The Jacobsen--Chicago May 23, 2018 1 Livestock

The relation between commodity markets and resource markets. (and the impact of Russian embargo) Trevor Donnellan FAPRI-Ireland Teagasc

Trevor Donnellan FAPRI-Ireland Teagasc") The relation between commodity markets and resource markets (and the impact of Russian embargo) Trevor Donnellan FAPRI-Ireland Teagasc Overview Boom in Prices Relationship in Price Across Sectors Decline

The relation between commodity markets and resource markets (and the impact of Russian embargo) Trevor Donnellan FAPRI-Ireland Teagasc Overview Boom in Prices Relationship in Price Across Sectors Decline

Farm Management 17th International Farm Management Congress, Bloomington/Normal, Illinois, USA Peer Review Paper

Scenario analysis on farm income of Dutch dairy farmers through 2020; the effect of regionalisation and liberalisation on the future of Dutch dairying. Jeroen van den Hengel 1, Christien Ondersteijn 1,

Scenario analysis on farm income of Dutch dairy farmers through 2020; the effect of regionalisation and liberalisation on the future of Dutch dairying. Jeroen van den Hengel 1, Christien Ondersteijn 1,

Dairy Globalization Refresh: 2011 Update Summary Findings

Dairy Globalization Refresh: 2011 Update Summary Findings Commissioned by Dairy Management Inc. & U.S. Dairy Export Council Conducted by Bain & Company Background Study conducted by Bain and Co. in collaboration

Dairy Globalization Refresh: 2011 Update Summary Findings Commissioned by Dairy Management Inc. & U.S. Dairy Export Council Conducted by Bain & Company Background Study conducted by Bain and Co. in collaboration

November 18, 1996 Ames, Iowa Econ. Info. 1706

November 18, 1996 Ames, Iowa Econ. Info. 1706 LEAN HOG CARCASS BASIS The new Lean Hog futures contract differs from its predecessor in several ways. It is traded on carcass weight and price rather than

November 18, 1996 Ames, Iowa Econ. Info. 1706 LEAN HOG CARCASS BASIS The new Lean Hog futures contract differs from its predecessor in several ways. It is traded on carcass weight and price rather than

SOME ASPECTS OF AGRICULTURAL POLICY IN AUSTRALIA

SOME ASPECTS OF AGRICULTURAL POLICY IN AUSTRALIA R. A. Sherwin, Agricultural Attache Australian Embassy, Washington, D. C. Before discussing government programs relating to agriculture in Australia I propose

SOME ASPECTS OF AGRICULTURAL POLICY IN AUSTRALIA R. A. Sherwin, Agricultural Attache Australian Embassy, Washington, D. C. Before discussing government programs relating to agriculture in Australia I propose

Session 2. Competitiveness in the marketing and retail sectors

:RUNVKRSRQ(QKDQFLQJ&RPSHWLWLYHQHVVLQWKH$JURIRRG6HFWRU0DNLQJ3ROLFLHV:RUN -XQH9LOQLXV/LWKXDQLD Session 2. Competitiveness in the marketing and retail sectors *52&(5

:RUNVKRSRQ(QKDQFLQJ&RPSHWLWLYHQHVVLQWKH$JURIRRG6HFWRU0DNLQJ3ROLFLHV:RUN -XQH9LOQLXV/LWKXDQLD Session 2. Competitiveness in the marketing and retail sectors *52&(5

History of Milk Marketing Orders and Current Implications to Dairy Producers and Industry

History of Milk Marketing Orders and Current Implications to Dairy Producers and Industry By Andrew P. Griffith, Assistant Professor and Extension Economist Livestock Department of Agricultural and Resource

History of Milk Marketing Orders and Current Implications to Dairy Producers and Industry By Andrew P. Griffith, Assistant Professor and Extension Economist Livestock Department of Agricultural and Resource

Calving Pattern- The Most Important Decision on Your Farm?

Calving Pattern- The Most Important Decision on Your Farm? October 24th 2017 Joe Patton, Teagasc Dairy KT Dept. Joe.patton@teagasc.ie Presentation Outline Background trends in calving & fertility 2012-17

Calving Pattern- The Most Important Decision on Your Farm? October 24th 2017 Joe Patton, Teagasc Dairy KT Dept. Joe.patton@teagasc.ie Presentation Outline Background trends in calving & fertility 2012-17

John Deere. Committed to Those Linked to the Land. Market Fundamentals. Deere & Company June/July 2014

John Deere Committed to Those Linked to the Land Market Fundamentals Deere & Company June/July 2014 Safe Harbor Statement & Disclosures This presentation includes forward-looking comments subject to important

John Deere Committed to Those Linked to the Land Market Fundamentals Deere & Company June/July 2014 Safe Harbor Statement & Disclosures This presentation includes forward-looking comments subject to important

United Nations Conference on Trade and Development

United Nations Conference on Trade and Development 1th MULTI-YEAR EXPERT MEETING ON COMMODITIES AND DEVELOPMENT 25-26 April 218, Geneva Assessing the recent past and prospects for grains and oilseeds markets

United Nations Conference on Trade and Development 1th MULTI-YEAR EXPERT MEETING ON COMMODITIES AND DEVELOPMENT 25-26 April 218, Geneva Assessing the recent past and prospects for grains and oilseeds markets

11 EQ7: Structure of dairy industry

11 EQ7: Structure of dairy industry To what extent have the CAP measures applicable to the dairy sector influenced structural changes in the processing sector? 11.1 Interpretation and comprehension of

11 EQ7: Structure of dairy industry To what extent have the CAP measures applicable to the dairy sector influenced structural changes in the processing sector? 11.1 Interpretation and comprehension of

Milk Marketing. As 472, AVS472 Fall 2015 John Swain. Resources. The Market Administrator s Report -

Milk Marketing As 472, AVS472 Fall 2015 John Swain Resources www.ams@usda.gov/dairy - The Market Administrator s Report - www.fmmaseattle.com National Milk Producers Federation Nmpf.org The Dairy Markets

Milk Marketing As 472, AVS472 Fall 2015 John Swain Resources www.ams@usda.gov/dairy - The Market Administrator s Report - www.fmmaseattle.com National Milk Producers Federation Nmpf.org The Dairy Markets