Le capital humain comme ressourse immatérielle : la vision du World Intellectual Capital Initiative (WICI)

|

|

|

- Warren Powell

- 6 years ago

- Views:

Transcription

Prof.")

1 WORKSHOP «De la théorie à la pratique, quels enjeux aujourd hui pour le management et le reporting du capital humain?» Le capital humain comme ressourse immatérielle : la vision du World Intellectual Capital Initiative (WICI) Prof. Stefano Zambon Université de Ferrare Global Chairman, WICI Network Table Ronde autour des enjeux du capital humain pour les professionels Bordeaux, 24 June

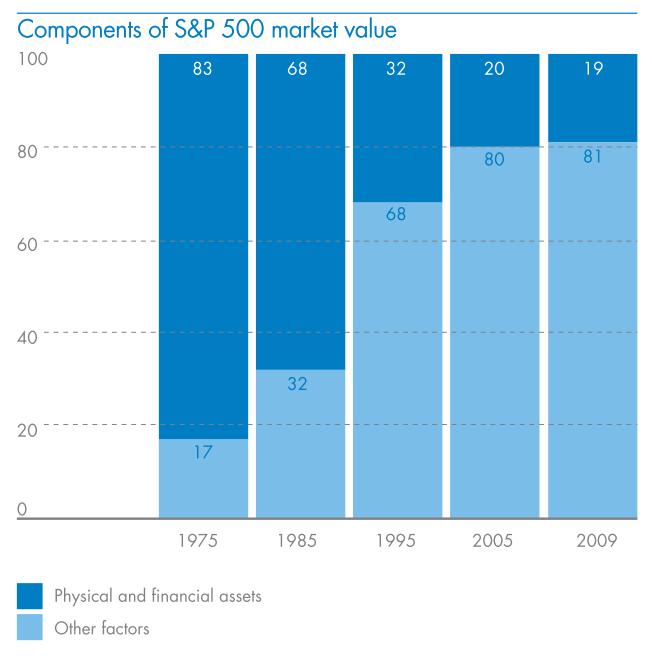

2 The Intangibles-Tangible Widening Gap Investment (% nonfarm business output) 16% 14% 12% 10% 8% 6% 4% U.S. Intangible vs. Tangible Investment tangible investment intangible investment 2% 0% Source: Carol Corrado & Charles R. Hulten, How Do You Measure a Technological Revolution? American Economic Review, American Economic Association, vol. 100(2), pages , May

3 Intangible investment dominates billion nominal 250 UK Market Sector investment Intangible Tangible Knowledge investment by firms for future returns: - Software, Creative works, R&D, Designs, Business organisation / processes, Workplace skills, Reputation / brands Source; UK Investment in Intangible Assets and IPRs, Haskel et al

4

5 DIFFICULTIES IN MEASURING HUMAN CAPITAL - In traditional accounting human capital is essentially a cost - Problem of clearly linking human capital with value creation - Problem of linking inputs (e.g. training activities) with outputs and outcomes - Problem of confusion between measuring human capital in a value creation perspective and measuring it in a sustainability perspective - Problem in understanding and representing the dynamic & systemic inter-relationships between human capital and other intangible resourses avoid a tick-the-box approach or to create new unconnected layers of information 5

6 W I C I World Intellectual Capital /Assets Initiative The World s Business Reporting Network WICI World Intellectual Capital/Assets Initiative Network Global collaborative, non-profit Network, officially born on 31 March 2008 with the signature of a Memorandum of Understanding (MoU) in Washington DC at the American Enterprise Institute (AEI)

, Desirée VAN WELSUM, OECD (Paris/France), Douglas LIPPOLDT, OECD (Paris/ France), Alexander WELZL, European Federation of Financial Analysts Societies")

7 World Intellectual Capital Initiative (WICI) 1 st Informal Meeting 1 st October 2007 OECD, Paris Monaco Annex, 2, rue du Conseiller Collignon Participants (from left to right): Prof. Yasuhito HANADO, Waseda University (Tokyo/Japan), Desirée VAN WELSUM, OECD (Paris/France), Douglas LIPPOLDT, OECD (Paris/ France), Alexander WELZL, European Federation of Financial Analysts Societies EFFAS (Frankfurt a. M./Germany), Yoshiko SHIBASAKA, KPMG (Tokyo/Japan), Bob LAUX Microsoft Corporation (Redmond/USA), Amy PAWLICKI, American Institute of Certified Public Accountants AICPA (New York/USA), Gert-Jan KOOPMAN European Commission (Bruxelles/Belgium), Annabel BISMUTH, OECD (Paris/France), Prof. Stefano ZAMBON, University of Ferrara (Ferrara/Italy), Grant KIRKPATRICK, OECD (Paris/France), Michael KRZUS, Grant Thornton (Chicago/USA), Christina BOEDKER, Society for Knowledge Economics (Crows Nest/Australia); Participants not on the picture: Rainer GEIGER, OECD (Paris/France), Jean- Philippe DESMARTIN, ODDO Securities (Paris/France), Yoshiaki TOJO, OECD (Paris/France)

The Promoting Parties of WICI are: Enhanced Business Reporting Consortium (USA) (American Institute of Certified Public Accountants")

Society for Knowledge Economics of Australia University of Ferrara Waseda")

8 Who We Are ( The Promoting Parties of WICI are: Enhanced Business Reporting Consortium (USA) (American Institute of Certified Public Accountants (AICPA), Microsoft Corporation, PricewaterhouseCoopers and Grant Thornton) European Federation of Financial Analysts Societies (EFFAS) Japanese Ministry of Economy, Trade and Industry (METI) Society for Knowledge Economics of Australia University of Ferrara Waseda University The European Commission, the OECD, and the Brazilian Development Bank (BNDES) participate in WICI as Observers. 8

9 The Structure of WICI (from 1st July 2015) General Assembly (Promoting Parties = EFFAS, METI, EBRC, Ferrara, Waseda) Governance Group WICI Global Chairperson + US (AICPA/Amy Pawlicky), Europe (EFFAS/Jean-Philippe Desmartin), Japan (METI/Takayuki Sumita) + Former Chairperson Chairperson Stefano Zambon (EFFAS) Deputy Chairman Eisuke Nagatomo (WICI Japan) Secretariat Observers European Commission, BNDES (Brazil), OECD WICI WICI Europe + WICI WICI USA Australia WICIs of European Countries Japan (EBRC) (Italy; France) 9

10 Our Vision Our Vision and Goals WICI, the world s business reporting network, is a private/public sector collaboration aimed at improving company reporting for representing value creation and, hence, capital allocation through better corporate reporting information Our Goals The first is to contribute to develop a new global framework for measuring and reporting corporate performance to shareholders and other stakeholders The second is to develop guidelines for measuring and reporting on industry-specific key performance indicators (KPIs). The third is to facilitate the development of XBRL taxonomies for this content. We believe that such better information will improve capital allocation decisions both within companies and between investors and companies. The result will be more value creation for a better world economy. 10

11 INTERNATIONAL OVERVIEW of REPORTING SCENE EFRAG/OIC/ANC/GASB/FRC FINANCIAL REPORTING A/C STANDARDS VALUATION IIRC IASB SUSTAINABILITY (ENVIRONMENTAL/SOCIAL) GRI/UN GLOBAL COMPACT/ DJ & FT SUST. INDEX IVSC / ISO VALUE CREATION (INTANGIBLES/KEY VALUE DRIVERS) WICI X B R L WICI EUROPE/FRANCE/ITALY/JAPAN/USA NON-FINANCIAL REPORTING

12 12

- WICI took on the leadership of the IIRC Background Paper for <IR> devoted to the principle")

13 Updates Collaboration between WICI and IIRC - Collaboration formalised in a Memorandum of Understanding (MoU) which is in place since June 2013 and it has been extended to November WICI has the right to have a seat in the Council of the IIRC (International Integrated Reporting Council) - WICI took on the leadership of the IIRC Background Paper for <IR> devoted to the principle of CONNECTIVITY 13

14 WICI Connectivity Project for <IR>/IIRC 14

15 Financial report does not reflect the real strengths of a company. We cannot see the - origin of the competitiveness - value chain as a combination of company-specific Intangibles - sustainability of the strengths, and - long term value WICI Background of a company from financial information. In this situation, financial people cannot properly evaluate a company. Therefore, we need some reporting mechanism to describe the real origin of strengths and business sustainability of a company

16 Towards a New Concept of «Business Sustainability» and Integrated Reporting Business Model BUSINESS SUSTAINABILITY (including financial sustainability) Knowledge and Intellectual Capital Natural and Societal Capital

.")

17 WICI INTANGIBLES REPORTING FRAMEWORK (WIRF) - Publication on 16 February 2016 of the Consultation Draft of the WICI Intangibles Reporting Framework (WIRF). Deadline for comments: 16 May 2016 (ca. 20 responses). The Final version of the WIRF is in course of elaboration Aimed to fill a well-known and large reporting gap present today, which is the guidance on measuring and disclosing an organization s intangible resources It essentially addresses the non-financial (or extra-financial) information on intangibles, insofar as financial information on them is covered by accounting and valuation standards and rules. 17

18 WICI INTANGIBLES REPORTING FRAMEWORK 18

19 WICI INTANGIBLES REPORTING FRAMEWORK WIRF crystallizes in one conceptually consistent Framework the best practices and proposals that have emerged in the field of intangibles reporting over the last twenty years. It is important to underline that many of the principles stated in the 2008 document Principles for Effective Communication of Intellectual Capital by the EFFAS Commission on Intellectual Capital (CIC), have been inserted in the WIRF Responses received for example from the International Integrated Reporting Council (IIRC), the Climate Disclosure Standards Board (CDSB), Erste Bank Group, Ernst & Young, KPMG, the Observatoire de l Immatériel, and the Sustainability Accounting Standards Board (SASB). In general, comments are positive and encouraging. Final version of WIRF is expected by August

20 Monetar y/financi al Capital Physical Capital

21 WICI-KPIs W I C I Global WICI Network the world's business reporting network 21

22 Our Concept of KPIs It is important to provide KPIs as factors which impact the corporate value creation and integrate them into business reporting to make the data and information more accessible, comparable and credible. Concept Paper on WICI KPI in Business Reporting ver. 1.0 (July 2010) introduces features of WICI KPIs and we will develop them based on this concept. - Electronic components (WICI Japan) - Pharmaceutical (WICI Japan) - Automotive/automobile (WICI Japan) - Telecommunications (Joint WICI Europe + EFFAS) - High Technology (in XBRL) (WICI USA) - Mining (in XBRL) (WICI USA + WICI Australia) - Fashion & Luxury (Joint WICI Europe + EFFAS) - Electricity (WICI Europe + WICI Italy) - Oil & Gas (WICI Europe) All available for free download in the WICI website ( Next WICI-KPIs project assigned to WICI Europe/WICI France will deal with the Food and Beverage Industry 22

23 Enterprise level Sector level Company-Specific Intangibles Indicators (no limit) Industry-Specific Intangibles Indicators (20-40 max.) General level Basic Intangibles Indicators (3-5 max.) Reporting on Intangibles: combining comparability & specificity 23

24 W I C I World Intellectual Capital Initiative The World s Business Reporting Network THE WICI-KPIs PROJECT on FASHION & LUXURY by the Joint WICI Europe-EFFAS CIC KPI Task Force-NIBR/WICI ITALY

25 Fashion industry core competences & value chain Operating processes Core Competencies Brand Management Style/Design Production Distribution Services Partnering 1 2 Nurturing talent quality Valuable customer relations 3 Rapid and quality product innovation Systematic and trusted partnering Organizational flexibility and adaptability Efficient and reliable execution

26 Fashion s KPIs per core competences Nurturing of talent quality Valuable customer relationship Average employee s age and seniority Staff turnover Training hours HR education Job rotation MBO Boutique sales staff training experience Employee commitment index High quality recruitment Management/Employee share of ownership Annual career review rate Share of women in upper/top mgmt. Share of employees in talent programs Training costs (also per employee) Access rate to training Financial KPI forecast hit rate by management Position in students annual employer ranking survey Formal mentorship No. of CVs received Proportion of staff covered by collective bargaining agreements Executive compensation on total revenues/net income Share of executive positions filled internally 4 Systematic and trusted partnering Suppliers by main raw material Suppliers turnover rate Dependence rate from key suppliers Raw materials purchase cost Raw materials purchase cost by main raw material Average distance from key suppliers Shipment times Outside contractors' number and saturation level External product development Number of exclusive suppliers vs. total suppliers Number of second - tier suppliers that have become first - tier Weight of licensing Brand value Number of brands Loyalty of clients to a specific brand Customer satisfaction index Brand awareness Brand preference Reputation index/external image Internet community Customer list Behavior of customers on the list in relation to loyalty activities Elasticity of demand Customer loyalty rate Exhibition participation ratio Items being bought by customers on the list Longevity of customers on the list Top of the line Avg. breadth of information available on customers Advertising costs % of total income generated from brand 5 Organizational flexibility and adaptability Share of employees familiar with strategy Average expenditure per capita Employee Satisfaction Index Child Labour Rapid and quality product innovation Number of meetings between purchasers and suppliers No. of new patents registered during the year No. of new products developed Local production rate Internal communication Competitors Portion outsourced on total sales 6 Efficient and reliable execution Sales by geographic area, main products, lines, brands, distribution channels Gross margin by geographic area, main products, brands, distribution channels Market share by geographic area Average number of sales people per 100 sq meters of shop Sale volume per square meter Franchisee average sale Outlets sales per square metre DOS sales per square meter Headcount Headcount by contract's type HR absenteeism Headcount by Department Number of staff in boutique Revenue of sales to customers on the list Number of franchisee Break - even point of franchisees Maintenance costs for franchisees Number of outlets DOS number of wholesale stores Maintenance costs and break - even point for DOS (direct operation stores) Products selected that were out of stock Delivery's delay Delivery costs that were too high Problems with connection to website No confirmation or status report given (To be continued)

27 List of KPIs for the Fashion and Luxury sector Nr Focus Process IC area KPI KPI Formula KPI s features Nurturing of talent quality Nurturing of talent quality Nurturing of talent quality Nurturing of talent quality All processes All processes All processes All processes Human Capital Human Capital Human Capital Human Capital Average employee' s age Average employee's seniority Staff turnover Training hours Ratio of the sum of employee's age and the total number of employees. Ratio of the sum of employee' seniority and the total number of employees. Number of people who left the company during the year on the total workforce at the beginning of the year (in all company and specifically in the Design Office and development Office. Amount of training hours on the number of employees (total and for HQ employees and sales people). age and trend time and trend percentage and trend percentage and trend Suggested relevance Nice to Have Must Have Must Have Nice to Have Nurturing of talent quality Nurturing of talent quality Nurturing of talent quality Nurturing of talent quality Nurturing of talent quality Nurturing of talent quality Nurturing of talent quality Nurturing of talent quality Nurturing of talent quality Nurturing of talent quality All processes All processes All processes Distribution process Services Partnering Services Partnering Services Partnering Services Partnering Services Partnering Services Partnering Human Capital Human Capital Human Capital Human Capital Human Capital Human Capital Human Capital Human Capital Human Capital Human Capital HR education Percentage of employees by the education's degree. percentage and trend Nice to Have Job rotation Percentage of employees who changed their task in the percentage Nice to Have last year on the total number of employees. and trend MBO Percentage of bonuses on the successful objectives percentage Must Have achieved by the employees. and trend Boutique sales staff training Sum of the training hours. time and trend Must Have experience Employee commitment index It is scored from an annual Employee Survey which score and Must Have provides a reliable measure of employees' commitment to trend their work and the company. High quality recruitment (e.g., recruitment from the 5 best business schools and/or the 5 best technical schools) Management/Employee share of ownership Annual career review rate Share of women in upper/top mgmt (to attract female talents) Share of employees in talent programs Percentage of high quality recruitment on total recruitment. percentage and trend Percentage of stocks of company owned by percentage employees/management. and trend Number of career advancement cases on total employees. percentage and trend Number of women on the total upper/top managers. percentage and trend Number of employees in talent program on the total employees. percentage and trend Must Have Nice to Have Nice to Have Must Have Must Have

28 WICI-KPI for the OIL & GAS Sector (Upstream and Midstream) April 2016 Proposed Model W I C I Global WICI Network the world's business reporting network

29 Value Chain The target of this Working Group is to identify relevant KPIs for the Oil & Gas industry engaged in upstream and midstream activities. The upstream includes the searching for potential underground or underwater crude oil and natural gas fields, drilling of exploratory wells, and subsequently drilling and operating the wells that recover and bring the crude oil and/or raw natural gas to the surface. The midstream involves the transportation (by pipeline, rail, barge, oil tanker or truck), storage, and wholesale marketing of crude petroleum products. No inclusions of unconventional Oil & Gas (i.e. oil sands; extra heavy oil; gas to liquid). Prospecting & acquisition of rights Exploration and evaluation Development Production Transportation Decommissioning 29

30 Core competences On the basis of experiences, the identification of the core competencies (value drivers) has been made taking into account that the result of a certain activity along the value chain depends on and reflects a specific set of core competencies/capabilities, which in turn is driven by a pool of intangibles, each of which (as not measurable per se) is approximated in terms of measurement by a certain number of such KPIs. Nurturing of talent quality Valuable customer relations Efficient and reliable execution Competitive innovation Environmental & Social responsibility 30

31 The matrix approach Value Chain Core competencies Prospecting & acquisition of rights Exploration and evaluation Development Production Transportation Decommissioning Nurturing of of talent talent quality quality Valuable customer relations Efficient and reliable execution Competitive and innovation partnering Environmental & social responsibility The model matches the proposal of the WICI concept paper. Relationships between Value Chain and Core Competences Display the critical areas to be investigated and measured For each block : outline the most significant KPIs KPI Formula and Feature: entity specific 31

32 The KPIs Nurturing of talent quality Employee commitment index Days of strike Training hours per employee Employee turnover Fatal accidents Percentage of local workers Competitive innovation R&D expenses Number of Patents Oil spills Valuable customer relations Oil delivery contracts Delivery program index Average sell price for unit delivered Average cost for unit delivered Accommodation costs for spills Net direct emissions Development programs for local community engagement Safety and Environmental CAPEX Transparency (Corruption index) Disputes with local communities or NGO Company perception from customer/stakeholder survey s results Environmental & social responsibility Total number of incidents/violations involving human 32 rights

33 The KPIs Acquisition of new field/license Efficient and reliable execution Possible Reserves Costs of acquisition of new field/license New Product Sharing Agreement Fields/License acquisition planned Exploratory and appraisal fields planned Investments in exploration planned Exploratory and appraisal fields in place Costs of exploratory and appraisal fields in place Undeveloped reserves Success rate of exploratory activities Developed fields in place Cost of developed fields in place Timeline of main projects Project and target achieved Project and target not achieved Project and target deferred Reserves at the beginning of the year Reserves at the end of the year Extraction Mineral resources quality Value of reserves future cash flows Value of reserves future development costs Value of reserves future production costs Change in Reserves value Reserves revision Recovery of additional mineral resources Costs of recovery of additional mineral resources Reserves replacement rate Reserves life Fields disposal Decommissioning costs Proved Reserves Probable Reserves Value of future decommissioning costs 33

34 Concluding remarks - Difficulties of current accounting practice to capture long-term value creation drivers - We are moving towards new systems of corporate information based on general, industry and companyspecific KPIs focussing on key-factors of the business model and activities - Role of Human Capital universally recognised but no one model/standard for reference - WICI provides a comprehensive set of voluntary sectorbased KPIs from where a company can chose the most representative of its unique value creation story - Wide role of professionals in applying and developing these tools for a better representation of Human Capital 34

35 THANK YOU! Prof. Stefano Zambon Global Chairman, WICI W I C I Global WICI Network the world's business reporting network

Waseda Intellectual Capital Research Society & World Intellectual Capital/Assets Initiative. Senior Advisor YASUHITO HANADO. September 18, 2014

10 th EISMA INTERDISCIPLINARY WORKSHOP Interdisciplinary Workshop on Intangible, Intellectual Capital and Extra-Financial Information Our Experiences of Intellectual Assets Based Management and Its Future

10 th EISMA INTERDISCIPLINARY WORKSHOP Interdisciplinary Workshop on Intangible, Intellectual Capital and Extra-Financial Information Our Experiences of Intellectual Assets Based Management and Its Future

TELECOMMUNICATION SECTOR KPIs PROPOSED by the Joint WICI Europe EFFAS KPIs Task Force

www.wici-global.com TELECOMMUNICATION SECTOR KPIs PROPOSED by the Joint WICI Europe EFFAS KPIs Task Force The starting point for the identification of KPIs for the telecommunication sector is the below

www.wici-global.com TELECOMMUNICATION SECTOR KPIs PROPOSED by the Joint WICI Europe EFFAS KPIs Task Force The starting point for the identification of KPIs for the telecommunication sector is the below

Vision. WICI recognizes the need for a corporate reporting that integrates the communication of

About WICI Vision WICI recognizes the need for a corporate reporting that integrates the communication of narrative and quantified information on how organizations create value over the short, medium and

About WICI Vision WICI recognizes the need for a corporate reporting that integrates the communication of narrative and quantified information on how organizations create value over the short, medium and

Restoring Credibility and Winning Stakeholders Trust. Source: BUILDING PUBLIC TRUST: THE FUTURE OF CORPORATE REPORTING, Wiley, 2002.

Restoring Credibility and Winning Stakeholders Trust Source: BUILDING PUBLIC TRUST: THE FUTURE OF CORPORATE REPORTING, Wiley, 2002. 1 Critics are questioning key components of the U.S. capital markets:

Restoring Credibility and Winning Stakeholders Trust Source: BUILDING PUBLIC TRUST: THE FUTURE OF CORPORATE REPORTING, Wiley, 2002. 1 Critics are questioning key components of the U.S. capital markets:

International Integrated Reporting Committee IIRC

International Integrated Reporting Committee IIRC WICI symposium 2010 Strategic Approach for Integrated Business Reporting in Knowledge Economy W I C I the world's business reporting network www.wici-global.com

International Integrated Reporting Committee IIRC WICI symposium 2010 Strategic Approach for Integrated Business Reporting in Knowledge Economy W I C I the world's business reporting network www.wici-global.com

ELECTRICITY SECTOR KPIs PROPOSED by NIBR WICI Italy

Electricity sector KPIs proposed by WICI Italy (Interim Version.0) As of September 9, 03 www.wici-global.com ELECTRICITY SECTOR KPIs PROPOSED by NIBR WICI Italy The target of this framework is to identify

Electricity sector KPIs proposed by WICI Italy (Interim Version.0) As of September 9, 03 www.wici-global.com ELECTRICITY SECTOR KPIs PROPOSED by NIBR WICI Italy The target of this framework is to identify

2017 GRI CONTENT INDEX

2017 GRI CONTENT INDEX We report against the Global Reporting Initiative (GRI) G4 Sustainability Reporting Guidelines, at a core application level. Key: IR = 2017 Integrated Report BPR = online 2017 full

2017 GRI CONTENT INDEX We report against the Global Reporting Initiative (GRI) G4 Sustainability Reporting Guidelines, at a core application level. Key: IR = 2017 Integrated Report BPR = online 2017 full

GRI reference table. General Standard Disclosures. Strategy and analysis. Organizational Profile

GRI reference table General General Disclosures Strategy and analysis G4-1 Statement from the most senior decision-maker CEO statement 6-7 Profile, mission and strategy 8-10 Operational leadership 28-33

GRI reference table General General Disclosures Strategy and analysis G4-1 Statement from the most senior decision-maker CEO statement 6-7 Profile, mission and strategy 8-10 Operational leadership 28-33

Global Reporting Initiative and United Nations Global Compact Index. Bigger Picture 2017 Sustainability Report

Global Reporting Initiative and United Nations Global Compact Index Bigger Picture 2017 Sustainability Report Contents Global Reporting Initiative and United Nations Global Compact Index Telstra s sustainability

Global Reporting Initiative and United Nations Global Compact Index Bigger Picture 2017 Sustainability Report Contents Global Reporting Initiative and United Nations Global Compact Index Telstra s sustainability

Invisible Advantage: How Intangibles Are Driving Business Performance. Jonathan Low Federal Reserve Bank of New York.

Invisible Advantage: How Intangibles Are Driving Business Performance Jonathan Low Federal Reserve Bank of New York July 11, 2002 2002 Cap Gemini Ernst & Young 1 The markets are valuing your intangibles

Invisible Advantage: How Intangibles Are Driving Business Performance Jonathan Low Federal Reserve Bank of New York July 11, 2002 2002 Cap Gemini Ernst & Young 1 The markets are valuing your intangibles

2018 SUSTAINABILITY REPORT GRI CONTENT INDEX

2018 SUSTAINABILITY REPORT GRI CONTENT INDEX INDEX 1 GRI 102: General Disclosures Organisational profile Front cover Disclosure 102-1 Name of the organisation Disclosure 102-2 Activities, brands, products,

2018 SUSTAINABILITY REPORT GRI CONTENT INDEX INDEX 1 GRI 102: General Disclosures Organisational profile Front cover Disclosure 102-1 Name of the organisation Disclosure 102-2 Activities, brands, products,

Integrated Scoreboard Taxonomy: Extending IFRS & COREP

XBRL Europe Day & Eurofiling Workshop Frankfurt, 11 th -14 th December 2012 Integrated Scoreboard Taxonomy: Extending IFRS & COREP Speaker: María Mora (maria.mora@atos.net ) XBRL Europe Day & Eurofiling

XBRL Europe Day & Eurofiling Workshop Frankfurt, 11 th -14 th December 2012 Integrated Scoreboard Taxonomy: Extending IFRS & COREP Speaker: María Mora (maria.mora@atos.net ) XBRL Europe Day & Eurofiling

Challenges for human resource management in global business strategy

Challenges for human resource management in global business strategy World Textile Congress, Mumbai 16 th September 2016 Dr. Sanjay Muthal Executive Director RGF India Mumbai Changing Paradigm Consumer

Challenges for human resource management in global business strategy World Textile Congress, Mumbai 16 th September 2016 Dr. Sanjay Muthal Executive Director RGF India Mumbai Changing Paradigm Consumer

The Business Model concept in Integrated Reporting

This IR Update comprises the following: - To propose a definition of the term business model for IR - To provide guidance on how to disclose the business model in an IR Integrated Reporting Update The

This IR Update comprises the following: - To propose a definition of the term business model for IR - To provide guidance on how to disclose the business model in an IR Integrated Reporting Update The

GROWING AS A BUSINESS AND AS INDIVIDUALS

GROWING AS A BUSINESS AND AS INDIVIDUALS For us, 'success' means supporting the prosperity of our clients, our own financial growth, and ensuring that our people grow and enjoy challenging careers. It

GROWING AS A BUSINESS AND AS INDIVIDUALS For us, 'success' means supporting the prosperity of our clients, our own financial growth, and ensuring that our people grow and enjoy challenging careers. It

Leading the Board, challenging the effectiveness of the group as a whole, and each director individually

Air Partner plc Roles and responsibilities of key Board members Chairman The Chairman is accountable to the board of directors (the "Board"). The Chairman is not responsible for executive matters regarding

Air Partner plc Roles and responsibilities of key Board members Chairman The Chairman is accountable to the board of directors (the "Board"). The Chairman is not responsible for executive matters regarding

The Latest Trend of IIRC And Integrated Report. Kiyoshi Ichimura, Ernst & Young Japan, IIRC Working Group Member Kenji Sawami, Ernst & Young Japan

The Latest Trend of IIRC And Integrated Report Kiyoshi Ichimura, Ernst & Young Japan, IIRC Working Group Member Kenji Sawami, Ernst & Young Japan Contents Part I- The latest trend of IIRC and Integrated

The Latest Trend of IIRC And Integrated Report Kiyoshi Ichimura, Ernst & Young Japan, IIRC Working Group Member Kenji Sawami, Ernst & Young Japan Contents Part I- The latest trend of IIRC and Integrated

Level of Reporting on GRI Indicators, 'in accordance' Core. Fully Significant Changes during 2016

Level of Reporting on GRI Indicators, 'in accordance' Core GENERAL STANDARD DISCLOSURES 'IN ACCORDANCE' CORE General Standard Disclosures Description Level of Reporting Location: For partially or not reported

Level of Reporting on GRI Indicators, 'in accordance' Core GENERAL STANDARD DISCLOSURES 'IN ACCORDANCE' CORE General Standard Disclosures Description Level of Reporting Location: For partially or not reported

GRI G4 Guidelines Public Comment Period Survey Report

GRI G4 Guidelines Public Comment Period Survey Report BACKGROUND Q1) Please provide the following personal details: Name : Stephen Hine Email address : stephen.hine@eiris.org Country of residence : UNITED

GRI G4 Guidelines Public Comment Period Survey Report BACKGROUND Q1) Please provide the following personal details: Name : Stephen Hine Email address : stephen.hine@eiris.org Country of residence : UNITED

GRI Guidelines (2006) - Content Index

- Content Index") 1 GRI Guidelines (2006) - Content Index The Global Reporting Initiative (GRI) is a non-governmental organization (NGO) tasked with formulating international guidelines for sustainability reporting. The

1 GRI Guidelines (2006) - Content Index The Global Reporting Initiative (GRI) is a non-governmental organization (NGO) tasked with formulating international guidelines for sustainability reporting. The

Intellectual Assets and Investment Professionals: The View of the Users

Intellectual Assets and Investment Professionals: The View of the Users Speech by Fritz H. Rau*, President EFFAS Conference Intellectual Assets and Innovation: Value Creation in the Knowledge Economy Ferrara,

Intellectual Assets and Investment Professionals: The View of the Users Speech by Fritz H. Rau*, President EFFAS Conference Intellectual Assets and Innovation: Value Creation in the Knowledge Economy Ferrara,

Global Reporting Initiative

Global Reporting Initiative 2013 GRI Application Level B Orica s 2013 Sustainability Report has been prepared in accordance with the Global Reporting Initiative (GRI) sustainability reporting guidelines,

Global Reporting Initiative 2013 GRI Application Level B Orica s 2013 Sustainability Report has been prepared in accordance with the Global Reporting Initiative (GRI) sustainability reporting guidelines,

GLOBAL REPORTING INITIATIVE 2012

GLOBAL REPORTING INITIATIVE 2012 G3.1 Content Index GRI Application Level B Orica s 2012 Sustainability Report has been prepared in accordance with the Global Reporting Initiative (GRI) Sustainability

GLOBAL REPORTING INITIATIVE 2012 G3.1 Content Index GRI Application Level B Orica s 2012 Sustainability Report has been prepared in accordance with the Global Reporting Initiative (GRI) Sustainability

The Community Innovation Survey 2010

The Community Innovation Survey 2010 (CIS 2010) THE HARMONISED SURVEY QUESTIONNAIRE The Community Innovation Survey 2010 FINAL VERSION July 9, 2010 This survey collects information on your enterprise s

The Community Innovation Survey 2010 (CIS 2010) THE HARMONISED SURVEY QUESTIONNAIRE The Community Innovation Survey 2010 FINAL VERSION July 9, 2010 This survey collects information on your enterprise s

GLOBAL REPORTING INITIATIVE (GRI) CONTENT INDEX 2017

CONTENT INDEX 2017") GLOBAL REPORTING INITIATIVE (GRI) CONTENT INDEX 2017 1 Global Reporting Initiative (GRI) content index GLOBAL REPORTING INITIATIVE (GRI) CONTENT INDEX 2017 Our sustainability reporting is aligned with

GLOBAL REPORTING INITIATIVE (GRI) CONTENT INDEX 2017 1 Global Reporting Initiative (GRI) content index GLOBAL REPORTING INITIATIVE (GRI) CONTENT INDEX 2017 Our sustainability reporting is aligned with

CORPORATE VALUE CREATION, INTANGIBLES, AND VALUATION: A DYNAMIC MODEL OF CORPORATE VALUE CREATION AND DISCLOSURE

CORPORATE VALUE CREATION, INTANGIBLES, AND VALUATION: A DYNAMIC MODEL OF CORPORATE VALUE CREATION AND DISCLOSURE by John Holland, Department of Accounting and Finance, University of Glasgow, 65-71 Southpark

CORPORATE VALUE CREATION, INTANGIBLES, AND VALUATION: A DYNAMIC MODEL OF CORPORATE VALUE CREATION AND DISCLOSURE by John Holland, Department of Accounting and Finance, University of Glasgow, 65-71 Southpark

Indicator Description Relevant Section Expanded Version Digest Version GENERAL STANDARD DISCLOSURES

GRI Index GENERAL STANDARD DISCLOSURES Strategy and Analysis G4-1 Provide a statement from the most senior decision-maker of the organization (such as CEO, chair, or equivalent senior position) about the

GRI Index GENERAL STANDARD DISCLOSURES Strategy and Analysis G4-1 Provide a statement from the most senior decision-maker of the organization (such as CEO, chair, or equivalent senior position) about the

EOWA REPORT C:\Documents and Settings\alysonowen\Desktop\EOWA Report 2010 For Web.doc 1

EOWA REPORT 2009-2010 C:\Documents and Settings\alysonowen\Desktop\EOWA Report 2010 For Web.doc 1 CONTENTS INTRODUCTION 3 CONSULTATION 4 YEAR IN REVIEW 5 TALENT MANAGEMENT AND DEVELOPMENT 5 RECRUITMENT,

EOWA REPORT 2009-2010 C:\Documents and Settings\alysonowen\Desktop\EOWA Report 2010 For Web.doc 1 CONTENTS INTRODUCTION 3 CONSULTATION 4 YEAR IN REVIEW 5 TALENT MANAGEMENT AND DEVELOPMENT 5 RECRUITMENT,

Global Reporting Initiative (GRI) Index

Index") Global Reporting Initiative (GRI) Index We do not base our report on the GRI guidelines but we have produced a GRI index below to show which elements of the guidelines are covered in our 2013 CR Report

Global Reporting Initiative (GRI) Index We do not base our report on the GRI guidelines but we have produced a GRI index below to show which elements of the guidelines are covered in our 2013 CR Report

Webinar on An Evolving Corporate Reporting Landscape

Webinar on An Evolving Corporate Reporting Landscape Speakers: June 25, 2015 1. Wesley Gee (Sustainability Reporting) 2. Alan Willis, CPA, CA (Integrated Reporting; SASB Standards) Moderator: Julie Desjardins,

Webinar on An Evolving Corporate Reporting Landscape Speakers: June 25, 2015 1. Wesley Gee (Sustainability Reporting) 2. Alan Willis, CPA, CA (Integrated Reporting; SASB Standards) Moderator: Julie Desjardins,

HR Connect Asia Pacific

Best Employers Trends in Hong Kong - Journey to High Performance By Andy Leung, Senior Consultant, and Project Manager of Best Employers Study, Aon Hewitt, Hong Kong In the Best Employers 2.0 Hong Kong

Best Employers Trends in Hong Kong - Journey to High Performance By Andy Leung, Senior Consultant, and Project Manager of Best Employers Study, Aon Hewitt, Hong Kong In the Best Employers 2.0 Hong Kong

GRI G4.0 Index CORPORATE RESPONSIBILITY & SUSTAINABILITY REPORT 2014/ /08

01/08 GRI G4.0 Index GRI G4.0 DISCLOSURES The table below shows where CCE s information and data corresponding to the Global Reporting Initiative s G4 Guidelines can be found. The majority of information

01/08 GRI G4.0 Index GRI G4.0 DISCLOSURES The table below shows where CCE s information and data corresponding to the Global Reporting Initiative s G4 Guidelines can be found. The majority of information

People Dig Deeper paper

People Dig Deeper paper Committed to being a great employer NAB plays a significant role in the lives of our 5,000 employees. Our focus on leadership, culture and capability supports our business strategy

People Dig Deeper paper Committed to being a great employer NAB plays a significant role in the lives of our 5,000 employees. Our focus on leadership, culture and capability supports our business strategy

Enterprise Value Stream Mapping and Analysis

Enterprise Value Stream Mapping and Analysis Stakeholder Value Metrics! March 25, 2002! Presented By:! C. Hallam, J. Mize! MIT LAI! Research Sponsored (Jointly) By ! Customer Value

Enterprise Value Stream Mapping and Analysis Stakeholder Value Metrics! March 25, 2002! Presented By:! C. Hallam, J. Mize! MIT LAI! Research Sponsored (Jointly) By ! Customer Value

EU Directive: disclosure of non-financial information and diversity information

EU Directive: disclosure of non-financial information and diversity information EU Directive on disclosure of non-financial information and diversity information From reporting year 2017, the legal requirements

EU Directive: disclosure of non-financial information and diversity information EU Directive on disclosure of non-financial information and diversity information From reporting year 2017, the legal requirements

Bidvest Group Limited GRI 3.0 content index (Annual integrated report 2014)

") Bidvest Group Limited GRI 3.0 content index (Annual integrated report 2014) GRI Indica tor Description Comments Chapter and link 1 Strategy and analysis 1.1 Statement from the most senior decision-maker

Bidvest Group Limited GRI 3.0 content index (Annual integrated report 2014) GRI Indica tor Description Comments Chapter and link 1 Strategy and analysis 1.1 Statement from the most senior decision-maker

Construction and real estate sector supplement GRI application level C. A year of opportunity

GRI application level C A year of opportunity 1 GRI application level C Standard disclosures part I: Profile disclosures Profile Disclosure Level of reporting Location of disclosures 1. Strategy and analysis

GRI application level C A year of opportunity 1 GRI application level C Standard disclosures part I: Profile disclosures Profile Disclosure Level of reporting Location of disclosures 1. Strategy and analysis

Assess record for 'Disclosure of Non-Financial Information by Companies'

Page 1 of 5 Assess record for 'Disclosure of Non-Financial Information by Companies' Meta Informations Creation date 28-01-2011 Last update date User name null Case Number 495876103431302811 Invitation

Page 1 of 5 Assess record for 'Disclosure of Non-Financial Information by Companies' Meta Informations Creation date 28-01-2011 Last update date User name null Case Number 495876103431302811 Invitation

Case study: Z Energy s approach to sustainability reporting

Case study: Z Energy s approach to sustainability reporting Case study: Z Energy s approach to sustainability reporting Creating value over time Our business model Z s sustainability journey started soon

Case study: Z Energy s approach to sustainability reporting Case study: Z Energy s approach to sustainability reporting Creating value over time Our business model Z s sustainability journey started soon

Mind the gap Closing the skills and gender gap in resources. Dr Matt Guthridge, Partner, PwC Mining, Oil & Gas Consulting Leader

Mind the gap Closing the skills and gender gap in resources Dr Matt Guthridge, Partner, PwC Mining, Oil & Gas Consulting Leader The resources boom is now 10 years old, as are the skills shortages that

Mind the gap Closing the skills and gender gap in resources Dr Matt Guthridge, Partner, PwC Mining, Oil & Gas Consulting Leader The resources boom is now 10 years old, as are the skills shortages that

THE COSTS AND BENEFITS OF DIVERSITY

Fundamental rights & anti-discrimination THE COSTS AND BENEFITS OF DIVERSITY European Commission Emplo 2 THE COSTS AND BENEFITS OF DIVERSITY A Study on Methods and Indicators to Measure the Cost-Effectiveness

Fundamental rights & anti-discrimination THE COSTS AND BENEFITS OF DIVERSITY European Commission Emplo 2 THE COSTS AND BENEFITS OF DIVERSITY A Study on Methods and Indicators to Measure the Cost-Effectiveness

GRI Index. 1. Strategy and Analysis. 2. Organizational Profile. GRI Indicator Description Page(s)

") GRI Index GRI Indicator Description Page(s) 1. Strategy and Analysis 1.1 Statement from the most senior decision-maker of the organization. 2-3 1.2 Description of key impacts, risks and opportunities.

GRI Index GRI Indicator Description Page(s) 1. Strategy and Analysis 1.1 Statement from the most senior decision-maker of the organization. 2-3 1.2 Description of key impacts, risks and opportunities.

Establishing a Multi-Stakeholder Group and National Secretariat

Construction Sector Transparency Initiative October 2013 / V1 Guidance Note: 4 Establishing a Multi-Stakeholder Group and National Secretariat Introduction An essential feature of CoST is the multi-stakeholder

Construction Sector Transparency Initiative October 2013 / V1 Guidance Note: 4 Establishing a Multi-Stakeholder Group and National Secretariat Introduction An essential feature of CoST is the multi-stakeholder

The concept of capital in Integrated Reporting. Integrated Reporting Update

This IR Update comprises the following: - Types of s - Maintaining s to create value in the future - Application of the s model for IR - Considerations in using the s model in IR - Examples of the different

This IR Update comprises the following: - Types of s - Maintaining s to create value in the future - Application of the s model for IR - Considerations in using the s model in IR - Examples of the different

Review of Operations and Activities: Listing Rule Guidance Note 10. Introduction. Issued: March 2003

: Listing Rule 4.10.17 Issued: March 2003 Key topics 1. Review of operations and activities guide 2. Assistance in preparing disclosures accompanying financial statements 3. Recommendations 4. Risk management

: Listing Rule 4.10.17 Issued: March 2003 Key topics 1. Review of operations and activities guide 2. Assistance in preparing disclosures accompanying financial statements 3. Recommendations 4. Risk management

<Insert Project Name>

Detailed Business Case Project Phase: Customer: Document ID: Initiation Name Position Title Organization Signature Date

Detailed Business Case Project Phase: Customer: Document ID: Initiation Name Position Title Organization Signature Date

CRE ATING A BE T TER WAY T O L IVE

2 0 17 G R I C O N T E N T I N D E X CRE ATING A BE T TER WAY T O L IVE Global Reporting Initiative Content Index GRI-G4 General Standard Strategy and Analysis G4-1 CEO statement about the relevance of

2 0 17 G R I C O N T E N T I N D E X CRE ATING A BE T TER WAY T O L IVE Global Reporting Initiative Content Index GRI-G4 General Standard Strategy and Analysis G4-1 CEO statement about the relevance of

Global Reporting Initiative (GRI) G4 Content Index

G4 Content Index") Global Reporting Initiative (GRI) G4 Content Index EVRAZ Highveld has adopted the GRI framework and guidelines for sustainability reporting since 2007. Following release of the GRI G4 sustainability reporting

Global Reporting Initiative (GRI) G4 Content Index EVRAZ Highveld has adopted the GRI framework and guidelines for sustainability reporting since 2007. Following release of the GRI G4 sustainability reporting

Financial Acumen for HR

Financial Acumen for HR Human Capital Management Institute October 23, 2014 Human Capital Management Institute 1 Jeff Higgins Chief Executive Officer Human Capital Management Institute Our Speaker Jeff

Financial Acumen for HR Human Capital Management Institute October 23, 2014 Human Capital Management Institute 1 Jeff Higgins Chief Executive Officer Human Capital Management Institute Our Speaker Jeff

The Fourth Community Innovation Survey (CIS IV)

") The Fourth Community Innovation Survey (CIS IV) THE HARMONISED SURVEY QUESTIONNAIRE The Fourth Community Innovation Survey (Final Version: October 20 2004) This survey collects information about product

The Fourth Community Innovation Survey (CIS IV) THE HARMONISED SURVEY QUESTIONNAIRE The Fourth Community Innovation Survey (Final Version: October 20 2004) This survey collects information about product

Practical how-to guide: Implementing Integrated Reporting

Practical how-to guide: Implementing Integrated Reporting Background The UK Green Building Council (UK-GBC) The UK Green Building Council (UK-GBC) is a membership organisation campaigning for a sustainable

Practical how-to guide: Implementing Integrated Reporting Background The UK Green Building Council (UK-GBC) The UK Green Building Council (UK-GBC) is a membership organisation campaigning for a sustainable

Voices on Reporting -

Voices on Reporting - Integrated Reporting 10 May 2018 KPMG.com/in Welcome 01 An introduction to Integrated Reporting 02 Business case for 03 Our perspectives 04 Thought leadership publications on

Voices on Reporting - Integrated Reporting 10 May 2018 KPMG.com/in Welcome 01 An introduction to Integrated Reporting 02 Business case for 03 Our perspectives 04 Thought leadership publications on

Atlas Copco annual report GRI Index 2017

Atlas Copco annual report GRI Index 2017 Global Reporting Initiative (GRI) Index Atlas Copco is committed to transparent, reliable and timely reporting on the most material sustainability aspects. Atlas

Atlas Copco annual report GRI Index 2017 Global Reporting Initiative (GRI) Index Atlas Copco is committed to transparent, reliable and timely reporting on the most material sustainability aspects. Atlas

Total employees by employment contract and gender

GRI Index GRI G4 index and applicable construction and real estate sector supplement Under GRI requirements, as a core responder, must comment on the most pertinent indicator per aspect. Where a material

GRI Index GRI G4 index and applicable construction and real estate sector supplement Under GRI requirements, as a core responder, must comment on the most pertinent indicator per aspect. Where a material

CORPORATE GOVERNANCE STATEMENT

CORPORATE GOVERNANCE STATEMENT SOLID FOUNDATIONS FOR MANAGEMENT AND OVERSIGHT This statement outlines Icon Energy s Corporate Governance practices that were in place during the financial year. ROLE OF

CORPORATE GOVERNANCE STATEMENT SOLID FOUNDATIONS FOR MANAGEMENT AND OVERSIGHT This statement outlines Icon Energy s Corporate Governance practices that were in place during the financial year. ROLE OF

SD General Standard Disclosure

3M 2016 Sustainability Report Index 159 About Report Global Reporting Initiative () Content Index and UN Global Compact Report on Progress Element SD General Standard G4-1 Statement from the most senior

3M 2016 Sustainability Report Index 159 About Report Global Reporting Initiative () Content Index and UN Global Compact Report on Progress Element SD General Standard G4-1 Statement from the most senior

Advanced Higher Accounting Course Assessment Specification (C700 77)

") Advanced Higher Accounting Course Assessment Specification (C700 77) Valid from May 2015 This edition: May 2015, version 2.1 This specification may be reproduced in whole or in part for educational purposes

Advanced Higher Accounting Course Assessment Specification (C700 77) Valid from May 2015 This edition: May 2015, version 2.1 This specification may be reproduced in whole or in part for educational purposes

GENERAL STANDARD DISCLOSURES

GRI Index GRI G4 index and applicable construction and real estate sector supplement Under GRI requirements, as a core responder, Basil Read must comment on the most pertinent indicator per aspect. Where

GRI Index GRI G4 index and applicable construction and real estate sector supplement Under GRI requirements, as a core responder, Basil Read must comment on the most pertinent indicator per aspect. Where

Beyond Cost Reduction

Beyond Cost Reduction Measuring How Procurement Creates Business Value By Alex Brown, Kyle Appell and Meghan Truchan Over the past decade, successful businesses have proactively developed strategies that

Beyond Cost Reduction Measuring How Procurement Creates Business Value By Alex Brown, Kyle Appell and Meghan Truchan Over the past decade, successful businesses have proactively developed strategies that

for the year ended 30 june 2014

GLOBAL REPORTING INITIATIVE (GRI) INDEX for the year ended 30 june 2014 Our response to GRI G3.1 is aligned with application level C. This is with reference to the information disclosed in the integrated

GLOBAL REPORTING INITIATIVE (GRI) INDEX for the year ended 30 june 2014 Our response to GRI G3.1 is aligned with application level C. This is with reference to the information disclosed in the integrated

4. Organic documents. Please provide an English translation of the company s charter, by-laws and other organic documents.

Commitment to Good Corporate Governance 1. Ownership structure. Please provide a chart setting out the important shareholdings, holding companies, affiliates and subsidiaries of the company. If the company

Commitment to Good Corporate Governance 1. Ownership structure. Please provide a chart setting out the important shareholdings, holding companies, affiliates and subsidiaries of the company. If the company

EDITION #02 Driving employer branding up the agenda

EDITION #02 Driving employer branding up the agenda Making the intangible asset tangible two years on EMPEROR INSIGHT: EMPLOYER BRAND MANAGEMENT When we commissioned our research on employer brand management

EDITION #02 Driving employer branding up the agenda Making the intangible asset tangible two years on EMPEROR INSIGHT: EMPLOYER BRAND MANAGEMENT When we commissioned our research on employer brand management

External and Internal Analyses. External and Internal Analyses. Nature of an Internal Audit. Key Internal Forces. Basis for objectives & strategies:

Comprehensive Strategic Management Model External Audit External and Internal Analyses Vision & Mission Statements Chapter 2 Chapter Long-Term Objectives Chapter 5 Internal Audit Chapter 4 Generate, Evaluate,

Comprehensive Strategic Management Model External Audit External and Internal Analyses Vision & Mission Statements Chapter 2 Chapter Long-Term Objectives Chapter 5 Internal Audit Chapter 4 Generate, Evaluate,

Rieter Group. Social, Environmental and Economic Key Data Social, Environmental and Economic Key Data 2017

Rieter Group. Social, Environmental and Economic Key Data 217 1 Social, Environmental and Economic Key Data 217 Rieter Group. Social, Environmental and Economic Key Data 217 2 CONTENTS 3 Rieter Group 4

Rieter Group. Social, Environmental and Economic Key Data 217 1 Social, Environmental and Economic Key Data 217 Rieter Group. Social, Environmental and Economic Key Data 217 2 CONTENTS 3 Rieter Group 4

Governance G4-34 G4-35 G4-36 G4-37 The governance structure of the organization Any committees responsible for decision-making on economic, environmen

General Standard Disclosures Global Reporting Initiative (G4) Content Index Indicators Description Page No. Strategy and Analysis G4-1 A statement from the most senior decision-maker of the organization

General Standard Disclosures Global Reporting Initiative (G4) Content Index Indicators Description Page No. Strategy and Analysis G4-1 A statement from the most senior decision-maker of the organization

ATLAS COPCO ANNUAL REPORT SUSTAINABILITY INFORMATION 2016

ATLAS COPCO SUSTAINABILITY INFORMATION 2016 Atlas Copco s priorities for sustainable profitable growth In 2015, Atlas Copco launched its strategic priorities for sustainable, profitable growth. They were

ATLAS COPCO SUSTAINABILITY INFORMATION 2016 Atlas Copco s priorities for sustainable profitable growth In 2015, Atlas Copco launched its strategic priorities for sustainable, profitable growth. They were

STANDARD DISCLOSURE DESCRIPTION LOCATION OR COMMENT EXPLANATIONS AND OMISSIONS STRATEGY AND ANALYSIS

This table contains Standard Disclosures from the Global Reporting Initiative (GRI) Sustainability Reporting Guidelines and is aligned with the GRI G4 Guidelines 'in accordance' core. STRATEGY AND ANALYSIS

This table contains Standard Disclosures from the Global Reporting Initiative (GRI) Sustainability Reporting Guidelines and is aligned with the GRI G4 Guidelines 'in accordance' core. STRATEGY AND ANALYSIS

Global Reporting Initiative Index

Global Reporting Initiative Index At RBC we have adopted a multi-pronged approach to sustainability reporting, and we publish information about our social, environmental and ethical performance in a number

Global Reporting Initiative Index At RBC we have adopted a multi-pronged approach to sustainability reporting, and we publish information about our social, environmental and ethical performance in a number

SUSTAINABILITY REPORTING GRI

SUSTAINABILITY REPORTING GRI Concentric describes its work with sustainability and reports on fulfilment of financial, environment and social goals and indicators in Sustainability Report on pages 50 57

SUSTAINABILITY REPORTING GRI Concentric describes its work with sustainability and reports on fulfilment of financial, environment and social goals and indicators in Sustainability Report on pages 50 57

Respect for Human Rights. Environmental Management G4-17 P3 P10 P82 G4-18 G4-19 G4-20 G4-21 G4-22 G4-23 G4-24 P57 P95 G4-25 G4-27 P15 P24 P82 P9 P13

103 Data IndexIndependent Practitioners AssuranceGRI Content Index GRI Content Index The following table compares Sustainability Report 2017 and GRI Sustainability Reporting Guidelines version 4. Information

103 Data IndexIndependent Practitioners AssuranceGRI Content Index GRI Content Index The following table compares Sustainability Report 2017 and GRI Sustainability Reporting Guidelines version 4. Information

Consultation questions

Consultation questions The IIRC welcomes comments on all aspects of the Draft International Framework (Draft Framework) from all stakeholders, whether to express agreement or to recommend changes.

Consultation questions The IIRC welcomes comments on all aspects of the Draft International Framework (Draft Framework) from all stakeholders, whether to express agreement or to recommend changes.

GRI INDEX SUSTAINABILITY REPORT 2014/15 JAGUAR LAND ROVER AUTOMOTIVE PLC

SUSTAINABILITY REPORT 2014/15 JAGUAR LAND ROVER AUTOMOTIVE PLC GRI INDEX This report is in accordance with the Global Reporting Initiative s (GRI) G4 Sustainability Reporting Guidelines at the Core level.

SUSTAINABILITY REPORT 2014/15 JAGUAR LAND ROVER AUTOMOTIVE PLC GRI INDEX This report is in accordance with the Global Reporting Initiative s (GRI) G4 Sustainability Reporting Guidelines at the Core level.

WELCOME Human Capital Project Workshop Center for Safety and Health Sustainability (CSHS) March 13, #humancapital

March 13, #humancapital") WELCOME Human Capital Project Workshop Center for Safety and Health Sustainability (CSHS) March 13, 2018 @CenterSHS #humancapital Agenda Welcome & Opening Remarks Corporate Disclosure: Measuring, Managing

WELCOME Human Capital Project Workshop Center for Safety and Health Sustainability (CSHS) March 13, 2018 @CenterSHS #humancapital Agenda Welcome & Opening Remarks Corporate Disclosure: Measuring, Managing

International Integrated Reporting Council

International Integrated Reporting Council Who is the IIRC? Regulators Investors Standard setters Companies Accounting NGOs Chair: Prof Mervyn King CEO: Paul Druckman IIRC Pilot Programme Business Network

International Integrated Reporting Council Who is the IIRC? Regulators Investors Standard setters Companies Accounting NGOs Chair: Prof Mervyn King CEO: Paul Druckman IIRC Pilot Programme Business Network

Evolving Core Tasks for Improved Internal Audit Performance. Copyright 2018 AuditBoard Inc. 1

Evolving Core Tasks for Improved Internal Audit Performance Copyright 2018 AuditBoard Inc. 1 Introductions Built by experienced auditors, AuditBoard allows enterprises to collaborate, manage, analyze and

Evolving Core Tasks for Improved Internal Audit Performance Copyright 2018 AuditBoard Inc. 1 Introductions Built by experienced auditors, AuditBoard allows enterprises to collaborate, manage, analyze and

ISO INTERNATIONAL STANDARD. Brand valuation Requirements for monetary brand valuation

INTERNATIONAL STANDARD ISO 10668 First edition 2010-09-01 Brand valuation Requirements for monetary brand valuation Evaluation d'une marque Exigences pour l'évaluation monétaire d'une marque Reference

INTERNATIONAL STANDARD ISO 10668 First edition 2010-09-01 Brand valuation Requirements for monetary brand valuation Evaluation d'une marque Exigences pour l'évaluation monétaire d'une marque Reference

stakeholder engagement The Connected Corporate L&T Sustainability Report 2017

stakeholder engagement The Connected Corporate 44 L&T Sustainability Report 2017 Stakeholder Engagement Our key stakeholders are customers, shareholders and investors, suppliers, contractors, employees,

stakeholder engagement The Connected Corporate 44 L&T Sustainability Report 2017 Stakeholder Engagement Our key stakeholders are customers, shareholders and investors, suppliers, contractors, employees,

Public Service Secretariat Business Plan

Public Service Secretariat 2008-11 Business Plan Message from the Minister The Public Service Secretariat is a Category 2 entity that provides leadership in the area of strategic human resource management.

Public Service Secretariat 2008-11 Business Plan Message from the Minister The Public Service Secretariat is a Category 2 entity that provides leadership in the area of strategic human resource management.

Global Reporting Initiative G3.1 Sustainability Reporting Guidelines. Covalence EthicalQuote Criteria

Global Reporting Initiative G3.1 Sustainability Reporting Guidelines Covalence EthicalQuote Criteria The Global Reporting Initiative (GRI) is a non-profit organization that promotes economic, environmental

Global Reporting Initiative G3.1 Sustainability Reporting Guidelines Covalence EthicalQuote Criteria The Global Reporting Initiative (GRI) is a non-profit organization that promotes economic, environmental

The role of performance management JTI Sibel Gursoy, Regional HR VP. Copyright JTI

The role of performance management JTI Sibel Gursoy, Regional HR VP Copyright JTI Copyright JTI 2 JTI today JTI is the JT Group s international tobacco business A global Fortune 500 company We employ people

The role of performance management JTI Sibel Gursoy, Regional HR VP Copyright JTI Copyright JTI 2 JTI today JTI is the JT Group s international tobacco business A global Fortune 500 company We employ people

5 Core Must-Haves for Improved Internal Audit Performance. Copyright 2018 AuditBoard Inc. 1

5 Core Must-Haves for Improved Internal Audit Performance Copyright 2018 AuditBoard Inc. 1 Introductions Built by experienced auditors, AuditBoard allows enterprises to collaborate, manage, analyze and

5 Core Must-Haves for Improved Internal Audit Performance Copyright 2018 AuditBoard Inc. 1 Introductions Built by experienced auditors, AuditBoard allows enterprises to collaborate, manage, analyze and

Value-creating topics

ABN AMRO Group N.V. Value-creating topics We carry out a regular assessment of our operating environment. This allows us to identify our most important social, economic, financial and environmental issues.

ABN AMRO Group N.V. Value-creating topics We carry out a regular assessment of our operating environment. This allows us to identify our most important social, economic, financial and environmental issues.

G4 Content Index Oil & Gas Sector Supplement

Oil & Gas Sector Supplement STANDARD DISCLOSURES PART I: General Standard Disclosures Indicator Disclosure STRATEGY AND ANALYSIS G4-1 Statement from the most senior decision-maker of the organisation.

Oil & Gas Sector Supplement STANDARD DISCLOSURES PART I: General Standard Disclosures Indicator Disclosure STRATEGY AND ANALYSIS G4-1 Statement from the most senior decision-maker of the organisation.

GLOSSARY OF TERMS ENTREPRENEURSHIP AND BUSINESS INNOVATION

Accounts Payable - short term debts incurred as the result of day-to-day operations. Accounts Receivable - monies due to your enterprise as the result of day-to-day operations. Accrual Based Accounting

Accounts Payable - short term debts incurred as the result of day-to-day operations. Accounts Receivable - monies due to your enterprise as the result of day-to-day operations. Accrual Based Accounting

ALLIANZ GRI TABLE 2017

This table contains Standard Disclosures from the Global Reporting Initiative (GRI) Sustainability Reporting Guidelines and is aligned with the GRI G4 Guidelines 'in accordance' core. STRATEGY AND ANALYSIS

This table contains Standard Disclosures from the Global Reporting Initiative (GRI) Sustainability Reporting Guidelines and is aligned with the GRI G4 Guidelines 'in accordance' core. STRATEGY AND ANALYSIS

DEVELOPING KEY PERFORMANCE INDICATORS. - The Balanced Scorecard Framework -

DEVELOPING KEY PERFORMANCE INDICATORS - The Balanced Scorecard Framework - The purpose of this presentation is to identify and address the key questions necessary to design an effective framework for performance

DEVELOPING KEY PERFORMANCE INDICATORS - The Balanced Scorecard Framework - The purpose of this presentation is to identify and address the key questions necessary to design an effective framework for performance

LDC Services: Geneva Practitioners Seminar Series: Making Sense of GATS and Applying Good Practices in Services Negotiations

LDC Services: Geneva Practitioners Seminar Series: Making Sense of GATS and Applying Good Practices in Services Negotiations Seminar 4: Drivers of services competitiveness WTO Building, Room B 27 March

LDC Services: Geneva Practitioners Seminar Series: Making Sense of GATS and Applying Good Practices in Services Negotiations Seminar 4: Drivers of services competitiveness WTO Building, Room B 27 March

Center for Plain English Accounting AICPA s National A&A Resource Center available exclusively to PCPS members

REPORT February 22, 2017 Center for Plain English Accounting AICPA s National A&A Resource Center available exclusively to PCPS members ASU 2017-01 Clarifying the Definition of a Business On January 5,

REPORT February 22, 2017 Center for Plain English Accounting AICPA s National A&A Resource Center available exclusively to PCPS members ASU 2017-01 Clarifying the Definition of a Business On January 5,

G4-1 CEO / Chair statement Sustainable Development Report 2014 (SDR): 3 4; 7 8

: 3 4; 7 8") GRI G4 INDEX We report in line with the requirements of the Global Reporting Initiative (GRI). Based on our internal assessment, we believe the 2014 report is compliant with the core option of the G4 Guidelines.

GRI G4 INDEX We report in line with the requirements of the Global Reporting Initiative (GRI). Based on our internal assessment, we believe the 2014 report is compliant with the core option of the G4 Guidelines.

BALANCE SCORECARD. Introduction. What is Balance Scorecard?

BALANCE SCORECARD Introduction In this completive world where techniques are change in nights, it s very hard for an organization to stay on one technique to grow business. To maintain the business performance

BALANCE SCORECARD Introduction In this completive world where techniques are change in nights, it s very hard for an organization to stay on one technique to grow business. To maintain the business performance

People Count 2014 List of measures reported in the Study

People Count 2014 List of measures reported in the Study Table A GENERAL INFORMATION 1.1 Total income of organisation ( million) 1.2 Total expenditure of organisation ( million) 1.3 Organisational paybill

People Count 2014 List of measures reported in the Study Table A GENERAL INFORMATION 1.1 Total income of organisation ( million) 1.2 Total expenditure of organisation ( million) 1.3 Organisational paybill

Belden s Talent Management Approach BUILDING A METRIC-DRIVEN APPROACH TO MASTERING THE SUCCESSION PIPELINE

Belden s Talent Management Approach BUILDING A METRIC-DRIVEN APPROACH TO MASTERING THE SUCCESSION PIPELINE 1 COMPANY SNAPSHOT Belden s Talent Management Approach As a fast-paced, results-oriented company

Belden s Talent Management Approach BUILDING A METRIC-DRIVEN APPROACH TO MASTERING THE SUCCESSION PIPELINE 1 COMPANY SNAPSHOT Belden s Talent Management Approach As a fast-paced, results-oriented company

GLOBAL REPORTING INITIATIVE 2014 G4 CONTENT INDEX NAVIGATOR TABLE

GLOBAL REPORTING INITIATIVE 2014 G4 CONTENT INDEX NAVIGATOR TABLE GENERAL STANDARD DISCLOSURES GENERAL STANDARD DISCLOSURES STRATEGY AND ANALYSIS G4-1 Statement from the most senior decision maker of the

GLOBAL REPORTING INITIATIVE 2014 G4 CONTENT INDEX NAVIGATOR TABLE GENERAL STANDARD DISCLOSURES GENERAL STANDARD DISCLOSURES STRATEGY AND ANALYSIS G4-1 Statement from the most senior decision maker of the

Global Reporting Initiative (G4) Content Index

Content Index") Global Reporting Initiative (G4) Content Index General Standard Disclosures Indicators Description Page no. or URL Strategy and Analysis G4-1 A statement from the most senior decision-maker of the organization

Global Reporting Initiative (G4) Content Index General Standard Disclosures Indicators Description Page no. or URL Strategy and Analysis G4-1 A statement from the most senior decision-maker of the organization

Statement of Corporate Governance Practices 2016

Statement of Corporate Governance Practices 2016 Introduction The Board of Directors of Coventry Group Ltd (CGL) is responsible for the corporate governance of the Company. The practices outlined in this

Statement of Corporate Governance Practices 2016 Introduction The Board of Directors of Coventry Group Ltd (CGL) is responsible for the corporate governance of the Company. The practices outlined in this

GRI Guideline Reference Chart

GRI Guideline Reference Chart The information contained within this report conforms to Global Reporting Initiative (GRI) Sustainability Reporting Guidelines 4.0. Also shown are references to the applied

GRI Guideline Reference Chart The information contained within this report conforms to Global Reporting Initiative (GRI) Sustainability Reporting Guidelines 4.0. Also shown are references to the applied

Pacific Hydro 2011 Sustainability Report Global Reporting Initiative (GRI) Index

Index") Pacific Hydro 2011 Sustainability Report Global Reporting Initiative (GRI) Index This report applies the Global Reporting Initiative (GRI) G3 guidelines to a B level. Core indicators appear in bold. GRI

Pacific Hydro 2011 Sustainability Report Global Reporting Initiative (GRI) Index This report applies the Global Reporting Initiative (GRI) G3 guidelines to a B level. Core indicators appear in bold. GRI

CORPORATE GOVERNANCE STATEMENT

CORPORATE GOVERNANCE STATEMENT Approach to Corporate Governance Mincor Resources NL ACN 072 745 692 (Company) has established a corporate governance framework, the key features of which are set out in

CORPORATE GOVERNANCE STATEMENT Approach to Corporate Governance Mincor Resources NL ACN 072 745 692 (Company) has established a corporate governance framework, the key features of which are set out in

This statement has been approved by the Board of Reliance Worldwide Corporation Limited and is current at 28 September 2017.

Reliance Worldwide Corporation Limited (ACN 610 855 877) Corporate Governance Statement Current at 28 September 2017 The Board of Directors is responsible for the overall corporate governance of Reliance

Reliance Worldwide Corporation Limited (ACN 610 855 877) Corporate Governance Statement Current at 28 September 2017 The Board of Directors is responsible for the overall corporate governance of Reliance

The Board of Directors of Forise International Limited (the Board ) is pleased to present our inaugural Sustainability Report.

is pleased to present our inaugural Sustainability Report.") ABOUT THIS REPORT The Board of Directors of Forise International Limited (the Board ) is pleased to present our inaugural Sustainability Report. The Company s sustainability report is prepared in compliance

ABOUT THIS REPORT The Board of Directors of Forise International Limited (the Board ) is pleased to present our inaugural Sustainability Report. The Company s sustainability report is prepared in compliance