MOBILE MONEY REMITTANCE SYSTEM

|

|

|

- Linette Marsh

- 6 years ago

- Views:

Transcription

1 MOBILE MONEY REMITTANCE SYSTEM White paper Feb

2 Contents Bank4YOU Group... 3 ABOUT... 2 PRODUCTS... 2 Mobile Money Remittance System... 3 DESCRIPTION... 2 WORKflOW... 2 PROJECT GOALS... 2 MARKET OVERVIEW... 2 Technical information... 3 INTRODUCTION... 2 CHALLENGES... 2 LOWERING FEES... 2 LOWERING THE VOLATILITY OF PAYMENT MEANS... 2 CREDIT GRANTING SYSTEM AND KNOW YOUR CUSTOMER... 2 Crowdfunding... 3 ICO... 2 REFERRAL PROGRAM... 2 ROADMAP

3 Bank4YOU Group About Established in 2013 and headquartered in London, UK, in 2016 Bank4YOU transformed into Bank4YOU Group, an international consortium of fin-tech service companies operating within the electronic mobile payment services arena. FCA License No715451, issued by the UK's Financial Conduct Authority authorizes Bank4YOU to provide credit. Luxembourg B4YOU United Kingdom London FCA License No issued by Financial Services Authority, UK grants right to provide credit to consumers PSP Payments United Kingdom The company is engaged in emission of electronic money, provision of making payments services and the management of payment systems. Bank4YOU FINTECH Macau Operations division, Southeast Asia market. Bank4YOU Group provides customers with a wide range of pre-paid card options as well as other financial solutions. State of the art fin-tech products are developed for people with active lifestyles, such as students, tourists, migrant workers, and frequent travelers. One of the biggest concerns for most people travelling to another country for extended periods is how to obtain access to banking services without the need to be a resident of that country. Bank4You Group makes it really easy for visitors to make in-country as well as cross-border payments, without the need for proof of residency or a local bank account. Its secure money transfer is based on use of state-of-the-art mobile app. 3

and Play Market (Google).")

4 Bank4YOU Group Products Bank4YOU customers no longer need to depend on bureaucratic procedures associated with traditional banking. Its service has been created to ensure time-efficiency, convenience and secure transactions. Bank4You already works with a number of blue-chip organizations, delivering state-of-the-art prepaid card programs that target different user groups. Its customers are able to choose their ideal product from a wide range of pre-paid card options including Bank4You Group s Corporate card and Premium card, along with mobile banking services. One of Bank4YOU Group s core services is TaxFree4U, a VAT refund mobile app available to non-eu customers shopping in Europe. An international network of local offices supports this service, provided on behalf of seven major partners in Europe, Middle East, and Asia. It offers the highest VAT refunds on purchases made within Europe, with the money credited into the customer s account within 48-hours of presenting the necessary documentation. Mobile Bank4YOU Best fin-tech specialists have been developing our app. Bank4YOU app can be downloaded in App Store (Apple) and Play Market (Google). Thanks to the careful application testing on different target groups we created the application, which can be effortlessly used by customers of all age categories. Bank4YOU Card Bank4YOU Card Premium The card has been designed for individuals, who don t want or don t have a possibility to obtain a foreign bank account. The card can be used to withdraw funds globally. Ideal option for frequent travelers and students. Perfect card for exceptional customer experience. Best set of features capable to satisfy most demanding clients along with premium VAT refunding option. 4

5 Mobile Money Remittance System Description Mobile money transfer or remittance is a peer-to-peer (P2P) application making use of a mobile device to send money to family or friends, primarily across international borders 2. Usually, mobile money is a term used to describe services that allow electronic money transactions over a mobile device. It is also referred to as mobile financial services, mobile wallets, and mobile payments. For the purpose of this white paper, we shall consider mobile money to be a system of electronic payments that allows crossborder money transfers to any country. It also includes the withdrawal of funds in local currency (cash out) via the mobile money service or mobile airtime. Bank4You Group is an innovative consortium, acting as solution provider operating in the dynamic mobile payments sector. It aims to integrate crypto currency convergence with the convenience of mobile money solutions. The company has also created the internal digital unit, which underpins its Blockchain system for mobile money transfers. Remittances will be executed via mutual agreements between customers and partners regardless of their respective locations. The main component of the MMRS is a utility token BEEFY tied to local currencies of the countries of system user s countries, which enables fast, reliable and cheap remittance of values across the borders of states and continents. Operating such tokens makes it possible to increase the user trust in the system providing the simplest and the most understandable mechanism for converting fiat currencies into electronic ones. The issue of tokens occurs only on condition of the fiat money being brought into the system, which is intended to ensure the stability of the exchange rate. 2 MOBILE MONEY. AN OVERVIEW FOR GLOBAL TELECOMMUNICATIONS OPERATORS. % %20%28single%20view%29.pdf 5

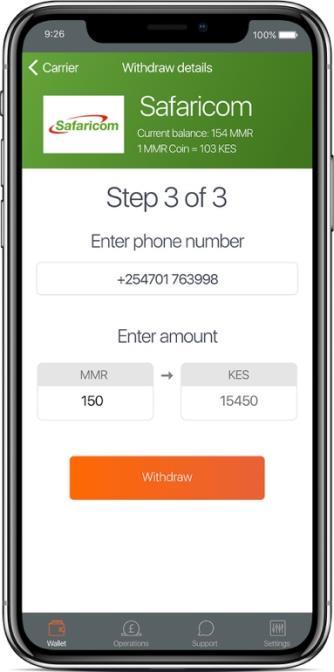

6 Mobile Money Remittance System Description The system is transparent and allows auditing by independent assessors who are not affiliated with Bank4YOU Group. Each user of Bank4YOU s mobile wallet has an account where tokens can be stored in different local currencies as well as in the BEEFY token. Users can use available tokens for money remittances, to exchange them for other tokens, or can exchange them for local fiat currencies through an agent system or use as payment for goods and services. Access to the account management system can be carried out through a web interface to manage available funds efficiently. You can create a transaction request Send remittance Exchange mobile or card balance on Internal digital unit 6

7 Mobile Money Remittance System Workflow Unlike traditional banks, who are typically permitted to invest most of the funds received from customers into loans and other less liquid investments, non-bank mobile money providers are required to hold funds equivalent to 100 per cent of outstanding mobile money liabilities in safe, liquid investments such as commercial bank deposits and low-risk government securities 3. Bank4YOU Group plans to open wholesale accounts with mobile network operators negotiating maximum discounts against guaranteed airtime purchases of $200,000 to $500,000. Operators will also benefit from increased subscriber activity as new customers join as a result of Bank4YOU Group s local marketing activities. The service will support intra-operator transfers so individuals on different networks can still engage with each other using their Bank4YOU mobile wallets. Customers would be able to transfer money to other countries with minimal commission fees and without being at the mercy of restricted opening hours or the challenges faced when dealing with traditional financial institutions. Business users will also have the opportunity to reduce their transaction costs and potentially execute free payments to their suppliers. In most developing countries remittances are now the largest source of external financing and, for some, this can account for as much as a third of GDP 4. More than one-third of global respondents in this report said they are highly likely to transfer money to, and/or receive money from, another person using their mobile device in the next six months. Bank4You Group s sophisticated platform is capable of supporting an unlimited volume of remittance flows between countries. In a move away from traditional remittance channels, the service would allow under-served consumers to benefit from a much more affordable, convenient and secure mobile money remittance service. 3 SAFEGUARDING MOBILE MONEY: HOW PROVIDERS AND REGULATORS CAN ENSURE THAT CUSTOMER FUNDS ARE PROTECTED. protected.pdfw%29.pdf 4 COMMITTEE ON PAYMENT AND SETTLEMENT SYSTEMS. THE WORLD BANK. GENERAL PRINCIPLES FOR INTERNATIONAL REMITTANCE SERVICES. 7

8 Mobile Money Remittance System Workflow 8

9 Mobile Money Remittance System Project goals Bank4YOU Group s Mobile Money Remittance System will set a new trend in international money transfers and will contribute to the creation of fast, convenient, and secure money transfers worldwide. The mobile app will also enable financial inclusion for people who are in desperate need of easy access to financial services in countries across Africa, Asia, and Latin America. It would also lead to new opportunities for businesses, financial institutions, and mobile network operators to use crypto currencies. As per the World Bank report, half of the unbanked people all over the world equals to about 1 Billion adults and they belong to poorest 40% of the people. We at Bank4You Group undertake this as a challenge to boost prosperity using Financial Inclusion. Our aim is to use our Blockchain enabled Mobile Money Remittance System (MMRS) to offer services at affordable rates and ease to our customers in the frontier markets. Not just can they use cash, but also spend on basic utilities like electricity, water, school fee and many others using their mobile phones. Shantnu Saxena CEO BANK4YOU GROUP. 9

10 Mobile Money Remittance System Market overview The market associated with convergence of crypto currencies and mobile accounts is poised to grow at a compound annual growth rate (CAGR) of 38.9 per cent in the next decade and is forecasted to reach approximately $405 billion by With more than 271 services in 93 countries 6, mobile money represents a considerable breakthrough for the financial services. Compared to global money transfer operators, the cost of sending international remittances through mobile money is, on average, 50 per cent less expensive. Billions of underserved consumers can look to benefit from the more accessible, reachable, and assured money transfer services employed by mobile money. Two or more MM services One MM service ММ service is planned to be launched by the end of GLOBAL MOBILE MONEY MARKET ANALYSIS & TRENDS - INDUSTRY FORECAST TO MOBILE MONEY. FROM SHOPPING TO BANKING TO PAYMENTS, HOW MOBILE IS TRANSFORMING COMMERCE AROUND THE WORLD. 10

11 Mobile Money Remittance System Market overview According to a GSMA report, one in seven Africans (120 million) are recipients of remittances from friends and family abroad, with the total figure amounting to $60 billion, which makes as much as a third of total GDP in some African markets 7. Despite the fact that the bulk of remittance flows are North-South, one in three remittances is sent from Africa. In 2012, almost half of Asia s population 690 million subscribed to mobile services. By 2020, the figure would see the addition of another 460 million bringing the global total to over 3.1 billion 8. On average, 46 percent of subscribers in India and 45 percent in China prefer using their mobile money wallets at bars, restaurants and retail shops 9. According to a McKinsey Global Institute report 10 by 2020, the global payments industry would have generated, as a result of an average five percent growth rate, an estimated $2.2 trillion in revenue, which would be over $400 billion more than in 2015 ($1.8 trillion). The GSMA Mobile Economy report draws attention to the fact that between September 2015 and June 2016 the volume of flows to and from bank accounts grew more than +120% Crypto currencies (mainly Bitcoin and Ethereum) nowadays represent an active ecosystem for transactions, just like an existing banking system. The solution based on convergence of crypto currencies and mobile network operator s balances is estimated show the same growth as from mobile accounts and bank accounts 120% per year. 7 MOBILE MONEY CROSSES BORDERS: NEW REMITTANCE MODELS IN WEST AFRICA. ment/wpcontent/uploads/2015/04/2015_mmu_mobile-money-crosses-borders_new-remittance-models-in-west-africa.pdf 8 THE MOBILE ECONOMY ASIA PACIFIC see p GLOBAL PAYMENTS 2016: STRONG FUNDAMENTALS DESPITE UNCERTAIN TIMES. 11

12 Technical information Introduction Two billion people and 200 million businesses 11 in countries with underdeveloped economies today remain unbanked and, as such, remain financially excluded. Even those with access to financial services are forced to pay extra-high fees for a limited range of available products. The widespread availability of digital technologies has enabled individuals to receive financial services at reduced existing costs. It has also provided stimulation to general financial activity and labor productivity. The benefits of financial services conducted using mobile apps are becoming clear to millions of customers worldwide. Mobile money will enable unbanked individuals to access financial services. Factors influencing the popularity of mobile money as the next authoritative instrument are 12 : Economic attractiveness due to low remittance charges (compared like Western Union, MoneyGram, or the local companies) and easy flat fee system Simplicity and convenience. You only need a mobile phone to use the service Easily convertible to cash and vice versa by agents commissioned by mobile network operators The opportunity to offer microloans Easy registration procedure for agents (basic information and small deposit required as a starting point) To establish an agent network, agents need to benefit financially in the same way as it is done within the M-PESA 13 system. 11 ACCESS TO CASH: THE FIRST STEP TOWARD FINANCIAL INCLUSION: 12 MOBILE MONEY AND FINANCIAL DEVELOPMENT: THE CASE OF M-PESA IN KENYA MOBILE PAYMENTS GO VIRAL M-PESA IN KENYA sources/ /yac_chpt_20.pdf 12

13 Technical information Introduction GSMA report findings state that The average cost of sending $200 using mobile money is 2.7 percent across the 45 corridors surveyed, compared to 6.0 percent using global MTOs, suggesting that mobile money is driving a price revolution in international remittances. 14 Fig.1 Average remittances cost for global MTOs and mobile money providers (in percent; August 2016) Fig. 2 Distribution of country corridors by average remittance cost for mobile money providers and global MTOs (August 2016) 14 DRIVING A PRICE REVOLUTION MOBILE MONEY IN INTERNATIONAL REMITTANCES. FIG.1 AND FIG.2 ARE TAKEN FROM THE REPORT: 13

14 Technical information Introduction Fig.3 The Power of Digital Finance GLOBAL PAYMENTS 2016: STRONG FUNDAMENTALS DESPITE UNCERTAIN TIMES. 14

15 Technical information Introduction On the other hand, the technology has a serious problem with Cross-border interoperability. Cross-border remittances require interoperability between mobile money schemes. As with domestic mobile money interoperability, cross-border remittances depend on operators transacting across platforms and settling funds directly between each other. Beyond domestic interoperability, mobile money providers have demonstrated a strong appetite for cross-border interoperability, with 46 remittance corridors now active. These corridors continue to drive the price of sending remittances down, providing users increasingly competitive options for sending money internationally. Finally, discussions around regional interoperability projects are aiming to create payment systems that connect all mobile money services and banks across a number of countries. For instance, the Southern African Development Community Bankers Association is currently in the early stages of planning to allow for mobile money connection to a central transaction hub. This could enable users to transact across all services and banks spanning 15 markets. Similar discussions are also taking place in the West African Economic and Monetary Union, as well as the East African Community. Interoperability continues to play a significant role in increasing the adoption of mobile money by providing customers the opportunity to transact with more users across more use cases, services, and markets. An important question for both the mobile money industry and the broader financial system is how mobile money will be integrated into existing payments infrastructure going forward. Full interoperability across all services and country corridors remains a long-term goal of the mobile money industry. 16 The director of strategic investments and fin-tech innovations, UBS, Haider Geoffrey, spoke about the importance of the [unified bank coin issue] project in the future: «It can be an indication of how central banks intend to develop in the field of the Blockchain technology. We view this project as the first step towards a future in which central banks will sooner or later issue their own cryptocurrencies.» 17 Blockchain technology makes it possible to create payment tools that carry the advantages of fiat currencies and mobile money not only within a country but also around the world. 16 STATE OF THE INDUSTRY REPORT ON MOBILE MONEY DECADE EDITION: LARGE BANKS ARE PREPARING TO ISSUE OWN CRYPTO CURRENCY. ARTICLE. rect/2017/09/01/large-banks-arepreparing-to-issue-own-crypto-currency/ 15

18 However, at the same time, the development of Blockchain technology and its")

16 Technical information Introduction Fig.4 Distribution of country corridors by average remittance cost for money providers and global MTOs (August 2016) 18 However, at the same time, the development of Blockchain technology and its exposure with leading banks - such as Barclays, CIBC, Credit Suisse, HSBC, MUFG, State Street - has allowed banking experts to consider this kind of technology very promising for the development of innovative banking products. 18 DRIVING A PRICE REVOLUTION MOBILE MONEY IN INTERNATIONAL REMITTANCES. FIG.3.IS TAKEN FROM THE REPORT: 16

17 Technical information Challenges The proposed system will have all the advantages of the existing systems i.e. solving problems they deal with, as well as offering users an additional convenience or an economic advantage. Challenge 1 According to the McKinsey Global Institute report 19, for the free functioning of the remittance system both within and outside a country, there is a strong need for the absence of restrictions on part of the financial regulator of that particular country (the central bank), along with the availability of open markets. Solution The technological advantage of the Blockchain network solutions lies in the fact that they do not require a representation in a country, or the availability of a legal framework for their presence in order to function as a means of payment in that country. Restrictions in the form of a ban will create a black market for other electronic payment means, which is likely to complicate their use, but will not stop it completely. Technologically, a Blockchain solution can only be banned by completely banning network communications at the transport level. Such advantages of that technology provide a huge potential for creating open markets without borders. Challenge 2 The McKinsey report 20 states that for banking services to function properly, a large amount of digital infrastructure and user identification tools are needed. Solution Similar to mobile money systems, usage of the existing hardware base is proposed. Smartphones with a fingerprint scanner and a camera provide both Internet access for carrying out transactions of various types and possibility for user s biometric identification. In fact, this paradigm shift addresses the problem of user access to traditional banking services not by building new offices in inaccessible/sparsely populated areas but by bringing banking services to the user s mobile phones. 19 GLOBAL PAYMENTS 2016: STRONG FUNDAMENTALS DESPITE UNCERTAIN TIMES IBID 17

18 Technical information Challenges Challenge 3 The McKinsey report 21 further points out that users have to choose a solution that exists in the market but would be more expensive and will not be cross-border. To respond to these challenges, users need to be provided with: Lower money remittance fees than what compatible services offer. As low volatility as possible of the means of payment. Simplicity of conversion into other means of payment and B2C interaction, which implies: o Wide network of existing agents capable of cashing out a payment tool or, conversely, accepting cash in exchange for electronic money (more convenient to handle and/or to transport) Bank4YOU Group plans to develop the business in the countries with already formed market of mobile money, hence the expenses connected with creation of dealer and agency networks won t incur. o Possibility of automatically converting one payment tool into another means of payment mobile money and fiat electronic money. o Possibility of buying/selling goods and services using a means of payment o Micro-crediting system Since that problem is the most complicated and comprehensive of all mentioned, the following section is devoted to its solution mechanisms, which also describes the design of the proposed system. 21 IBID 18

19 Technical information Proposed solution to challenges It is proposed to implement a payment facility based on the Blockchain technology (digital tokens), which will be freely convertible into a fiat currency and mobile money, first in individual countries and then around the world. Lowering fees According to the aforementioned report on international remittances using mobile money 22, the average fee for country-to-country remittance is 2.7 percent excluding cashing out of funds for amounts higher than $200 (amounts below $200 are, on average, more expensive to remit; the smaller the amount, the more expensive it is to remit). Thanks to the technological advantages of the Blockchain technology, a lower remittance price is ensured than with the alternative services. The remittance fees in the Ethereum network, for example, are regulated in a special way so that they are always low regardless of the price of the Ethereum. Fig.5 The median transaction fees (percentage) in Ethereum network, from the network launch up to writing of this whitepaper 23. This makes it possible to offer lower fees, even when compared to the mobile money technology (for example, M-PESA charges a flat fee of $0.40 for P2P remittances and a withdrawal fee of $0.33 for withdrawals under $33), especially if there is no need for an instant execution of the transaction. In the event of increasing the transaction confirmation time to five minutes, the fee is significantly reduced. As can be seen, the remittance price in a public Blockchain Ethereum is much lower than that of any of the systems under consideration. It is proposed to set up a consortium of mobile operators. All mobile operators that have concluded partnership agreements will be able to give their subscribers the opportunity to receive or send cross-border payments to subscribers of all other partner mobile operators. 22 DRIVING A PRICE REVOLUTION MOBILE MONEY IN INTERNATIONAL REMITTANCES: 23 ETHEREUM MEDIAN TRANSACTION FEE HISTORICAL CHART tion_fee.html 19

with the existing mobile banking and card remittance systems, which will provide multiple")

20 Technical information Proposed solution to challenges Thus, each of the operators needs to conclude only one partner agreement, which is with the Bank4YOU Group consortium, instead of entering into an individual partnership agreement with each of the operators participating in the consortium. This will give the operator s subscribers the opportunity to send international remittances to subscribers of all other partner operators. The proposed solution also gives the opportunity to integrate a new payment facility (utility tokens) with the existing mobile banking and card remittance systems, which will provide multiple points of contact for the users, convenience, and guarantees on the reliability of use. Fig.6 - A consortium of the Bank4YOU Group mobile operators 20

21 Technical information Proposed solution to challenges The arrangement of a private Blockchain system may even still further (in comparison with a public Blockchain one) lower the remittance fees within the network 24. It is proposed to organize a private Blockchain system as follows: the virtual Bank4YOU Group s divisions (private nodes) will serve as nodes for transaction verification within the consortium of Organizations participating in the system of international payment transfers. They will provide fast and cheap validation of transactions made by other network members. It is assumed that as the popularity of the system grows, mobile operators will have an economic incentive for placing the peer-to-peer nodes of the system in their data centers. This can significantly reduce the transaction costs associated with money circulation. Fig.7 Design of private Blockchain system 24 VITALIK BUTERIN'S BLOGPOST ON PUBLIC AND PRIVATE BLOCKCHAINS: lic-and-privateblockchains/-money_2016.pdf 21

22 Technical information Proposed solution to challenges In order for participating peers to be convinced of the unfalsifiable nature of the data inside the private Blockchain system, it is proposed to record reference points into the public Blockchain systems (Bitcoin, Ethereum). Any member of the system will therefore be able to verify at any time the data stored in the system. A private Blockchain system makes it possible to renounce the deployment of an expensive IT infrastructure for financial transfers while ensuring the necessary level of trust between the consortium entities. Hence, a private Blockchain system ensures: Cutting costs and opportunity thereof to provide users with even cheaper international money remittance services Improving scalability of system by not having to deploy expensive infrastructure Sufficient level of trust between members of the consortium for fast and reliable work on processing of user transactions (due to cryptographic mechanisms of transaction validation) Lowering the Volatility of Payment Means The volatility of payments means intended for remittances is obviously undesirable. To deal with such volatility, solutions similar to those are used: NuBits, LHT, Minex, Digix, dai, Steem, USDT, BitShares, all of which boil down to trying to tie a digital token to some other asset and a liquidity provider mechanism implemented as a price floor repurchase by the central banking authority or a fund organized as a reserve one in state-run economies. The proposed solution is to link the token to a payment facility freely convertible in the target economies and make it freely convertible into a fiat electronic currency and cash one as well as into mobile money. Considering the preferences of the project s target audiences it is decided to use internal digital unit provision with mobile money and minutes of operator s cellular communications. Internal digital unit, as payment capability enables payment with fiat money stored on Bank 4YOU Group s account at mobile network operators with deposits mainly in US dollars. The internal digital units are issued once fiat money is placed and can be freely converted into several means of payment in various countries: fiat currencies, mobile money, airtime minutes depending on user needs and local markets. 22

23 Technical information Lowering the Volatility of Payment Means Bank4YOU Group determines the conversion rate in partnership with mobile operators with exchanges made via mobile application. The volatility of the token is protected by a fixed exchange rate. The Bank4YOU Group utility token (BEEFY) on the Ethereum platform will be implemented for those keen on long-term system activities. The BEEFY token will allow performing transactions and other financial operations in the system. Besides, the BEEFY token holder will be allowed to purchase internal digital unit on discounted price, which means cheaper services on cross-border transfers. Internal digital unit purchase in return for tokens of BEEFY is possible on the floating rate, but with a fixed 2.5 percent discount. This provides BEEFY holders with exclusive access to the system of cross-border money transfers. Thus the system rewards the users for supporting it. Internal digital unit holders will be paid by automatic accrued payment system. Availability of audit trail of a private Blockchain in public Ethereum/Bitcoin Blockchain will provide for a transparent and fair scheme. If necessary, each participant of the system can check the fairness of own share charges or that of any other user. As payments are made once in a payment period, it is necessary to consider balance changes in one s account during this payment period so it is distributed equally between all holders. Therefore, BEEFY utility token grants the right to receive discounts for purchasing internal digital unit. Integration with existing systems It is planned to provide as many points of contact with existing payment and monetary systems as possible facilitated by a verified network of affiliated and economically motivated agents. 23

24 Technical information Credit granting system and know your customer Intending to provide convenient and fast mechanism for providing consumer credit financing based on money transfer platform, we give customers an opportunity to arrange smartphone credit for friends and family. For evaluation of demand on this service, our group specialists held an opinion survey in UK and France. Ten thousand respondents (mostly migrants from Asia and Africa) were surveyed with 78.8 percent showing strong interest in service. They agreed that they are ready to take a loan for purchasing the latest smartphone model under their personal guarantee for friends and family. They confirmed that they were ready to pay from five to 10 euros per month for the smartphone (e.g. Great Wall Smart 12 model with retail price of 40 euros was offered, with proposed credit set for a period of 12 months). To provide customers with accurate lending mechanism it is offered to transfer the mechanism of credit history on Blockchain. In order to avoid disclosure of private data no personal user s information will be stored in the Blockchain, just the biometric information protected by cryptographic means. The user will voluntarily provide it in order to receive lending assets or access transaction history connected with the digital identity of the real person. The benefit of the system is knowing it is impossible to obtain any information on the transaction history of a specific person without possessing their biometric data, thus protecting users against any malefactors. It is indeed very difficult to counterfeit biological identifiers. There is a plan to create a Blockchain that would store the crypto currency loan credit history of those who voluntarily provide this information. Bank4YOU Group s affiliated agents/ partnering organizations will be able to make records on Blockchain. In other words, an initiation of the smart contract in which the next information will be specified. Amount of loan Address of creditor Credit interest rates Series of loan charges Unique biometric indicator of borrower The smart contract checks whether payments are made fully and in time to the creditor. If payments are made according to stipulated conditions, the borrower's credit score is automatically raised or in the opposite case it is reduced. In case the borrower attempts to apply for new credit, they would be refused. Provided biometric data allows to unambiguously identify the person s credit history, the reverse procedure is impossible. Credit history cannot be associated with a person due to the realization of unique biometric identifier. 24

25 Technical information Unique biometric identifier The unique biometric identifier consists of a person s scanned eye retina and scanned fingerprints. These indicators allow for quick and reliable identification of each person in the world. This feature does not require provision of any passport data as it is subject to just minor mistakes. The only problem lies in the compatibility with the existing standards of know your customer procedure. The professional team of specialists hired by Bank4YOU Group has provided the statistical analysis of the predicted performance revenues of above-mentioned operations. Data with planned profitability over the next three years is given in table below: 25

26 Crowdfunding ICO CNBC cites 25 that in the first half of 2017 alone, startups have raised an enormous sum of $1.27 billion through ICOs, surpassing the amount invested in fin-tech startups with venture capital. ICO or initial coin offering (primary coins placement) is a mechanism to raise funds for a crypto currency venture. It is also a model of crowd funding 3.0, which helps participants to finance the development of the company in order to benefit from such investments in future. Fig.8 Totals raised are grouped by the ICO closing date and are valued using BTC exchange rate at that time. Data correct on 16th October 2017 The ICO means will be distributed as per the development of the project. Bank4YOU Group plans to spend crowd funded means on elaboration of its system of mobile money, development of new software, incorporation of micro crediting system, and new financial services based on Blockchain. 25 Article: 26 Picture taken from the Article: ing-climbs-as-record-500-million-invested-in-july/ 26

27 Crowdfunding Use of ICO Funding BEEFY Utility Token Allocation NOTE. Distribution depends on the crowd funded sums. Tokens will be issued in equivalent of $50 million, when the ICO will reach this hard cap it will be stopped ahead of scheduled dates. The scheduled duration of ICO is 146 days. The general amount of BEEFY utility tokens is

28 Crowdfunding ICO (6% of the whole amount) is reserved for bonus payments for users. Bonuses will be stopped sharing when the planned amount will be exceeded. In case if one wishes to purchase BEEFY via fiat money, there ll be provided an additional 5% bonus. These currencies are accepted during the ICO: BTC, ETH, GBP, USD, EUR. Special Packages have been designed for those purchasing 5000 tokens (Standard Package) and tokens (Premium Package). Corporate card and Premium card respectively will become our gifts to devoted investors. Minimal amount of investment is 105$ Referral program The referral program works by means of distribution of a referral code and provides fixed remuneration at a rate of 40 BEEFY. The main condition should be followed such as there should be BEEFY utility tokens purchased during the ICO campaign on the user's account. The one who sent and the one who activated the referral BEEFY code will receive bonus at a rate of 20 BEEFY each and referral tokens will be granted after the end of ICO only to those who made an investment and will be sent to the user's Bank4YOU wallet. 28

29 Mobile Money Remittance System Roadmap 2013 Establishment of Bank4YOU Implementation of Bank4YOU card Q1 Launch of mobile banking app followed by its release on App Store and Google Play Transformation into Bank4YOU Group due to business growth and market expansion 2016 Q Q4 ICO Mobile Money Remittance System project launch Participation at FinovateAsia Presentation of demo version of mobile app with MMRS functionality Q1 Creation of Bank4YOU mobile network operator consortium to provide digital infrastructure for MMRS project MMRS project beta version launch 2018 Q Q4 MMRS final version release 29

MOBILE MONEY REMITTANCE SYSTEM

MOBILE MONEY REMITTANCE SYSTEM Group White Paper January 2018 Contents Bank4YOU Group About 3 Products 4 Mobile Money Remittance System Description Workflow Project goals Market overview 5 7 9 10 Technical

MOBILE MONEY REMITTANCE SYSTEM Group White Paper January 2018 Contents Bank4YOU Group About 3 Products 4 Mobile Money Remittance System Description Workflow Project goals Market overview 5 7 9 10 Technical

Whitepaper. Abstract. Introduction

Whitepaper Proxy Ethereum for Everyone We do not offer securities or a collective investment scheme. You are advised to read this document carefully in full, and perform due diligence. According to the

Whitepaper Proxy Ethereum for Everyone We do not offer securities or a collective investment scheme. You are advised to read this document carefully in full, and perform due diligence. According to the

THE NEXT GENERATION CRYPTOCURRENCY REVOLUTION

1. About Us "Anteros Coin" is a Digital Currency that will be Launched and Introduced in 2018. This currency is just as good as Fiat, But only Available in the Digital World. "Anteros coin" Describes how

1. About Us "Anteros Coin" is a Digital Currency that will be Launched and Introduced in 2018. This currency is just as good as Fiat, But only Available in the Digital World. "Anteros coin" Describes how

Prepared by Influ Token. Revision 1.0

1 I N F L U W H I T E T O K E N P A P E R Prepared by Influ Token. Revision 1.0 Table of content 2 Disclaimer...3 Abstract...4 Problem...5 Influ Token...6 Mission...7 InfluWay...8 - InfluWay...9 - Reatil...

1 I N F L U W H I T E T O K E N P A P E R Prepared by Influ Token. Revision 1.0 Table of content 2 Disclaimer...3 Abstract...4 Problem...5 Influ Token...6 Mission...7 InfluWay...8 - InfluWay...9 - Reatil...

ProfytPro ICO CONTENTS

1 ProfytPro ICO CONTENTS ProfytPro ICO CONTENTS... 2 INTRODUCTION... 4 WHAT IS ProfytPro (PFTC) PLATFORM... 5 CORE OBJECTIVES... 6 ADVANTAGES OF BLOCKCHAIN... 7 WHY WE DO TOKEN SALE... 8 TOKEN FUNCTIONS

1 ProfytPro ICO CONTENTS ProfytPro ICO CONTENTS... 2 INTRODUCTION... 4 WHAT IS ProfytPro (PFTC) PLATFORM... 5 CORE OBJECTIVES... 6 ADVANTAGES OF BLOCKCHAIN... 7 WHY WE DO TOKEN SALE... 8 TOKEN FUNCTIONS

PDX COIN.

PDX COIN www.petrodollars.io www.pdxcoin.io DISCLOSURE STATEMENT The following presentation contains forward looking statements that may reflect our plans, estimates, and beliefs. Such forward looking

PDX COIN www.petrodollars.io www.pdxcoin.io DISCLOSURE STATEMENT The following presentation contains forward looking statements that may reflect our plans, estimates, and beliefs. Such forward looking

PDX COIN

PDX COIN WWW.PDXCOIN.IO DISCLOSURE STATEMENT The following presentation contains forward looking statements that may reflect our plans, estimates, and beliefs. Such forward looking statements are dependent

PDX COIN WWW.PDXCOIN.IO DISCLOSURE STATEMENT The following presentation contains forward looking statements that may reflect our plans, estimates, and beliefs. Such forward looking statements are dependent

Crypto assets trading platform

Crypto assets trading platform SUMMARY: This document introduces Kompler to the market; a trading platform for crypto assets that focus on emerging cryptocurrencies and already consolidated projects. Kompler

Crypto assets trading platform SUMMARY: This document introduces Kompler to the market; a trading platform for crypto assets that focus on emerging cryptocurrencies and already consolidated projects. Kompler

MEGAMALL COIN WHITE PAPER

MEGAMALL COIN WHITE PAPER May 2018 Summary Introduction... 2 Problem definition... 2 Solution proposal... 2 Introduction to MEGAMALL Coin... 2 Smart Contracts... 3 What Are Blockchains?... 3 What Is a

MEGAMALL COIN WHITE PAPER May 2018 Summary Introduction... 2 Problem definition... 2 Solution proposal... 2 Introduction to MEGAMALL Coin... 2 Smart Contracts... 3 What Are Blockchains?... 3 What Is a

Corporate Presentation. Author: DIMPAY Foundation

Corporate Presentation Author: DIMPAY Foundation Table of Contents Table of Contents What is DIMPAY? 01 DIMPAY Foundation 02 DIMPAY Features 04 DIMPAY ICO 06 ICO Funds 08 DEPOTWALLET 10 DIMPAY Applications

Corporate Presentation Author: DIMPAY Foundation Table of Contents Table of Contents What is DIMPAY? 01 DIMPAY Foundation 02 DIMPAY Features 04 DIMPAY ICO 06 ICO Funds 08 DEPOTWALLET 10 DIMPAY Applications

NILECOIN. WhitePaper

1 NILECOIN WhitePaper December 08, 2017 OVERVIEW OF NILECOIN NILECOIN (NIL) is a digital currency developed in the form of open-source software (OSS). Nilecoin operates on a peer-to-peer network protocol

1 NILECOIN WhitePaper December 08, 2017 OVERVIEW OF NILECOIN NILECOIN (NIL) is a digital currency developed in the form of open-source software (OSS). Nilecoin operates on a peer-to-peer network protocol

1. GUARIUM e-commerce Automation A fully automated online sales platform

Table of contents 1. GUARIUM e-commerce Automation 2. Why is the e-commerce industry an excellent opportunity? 3. A study which provided tips for us what the e-commerce industry expects 4. An ideal product

Table of contents 1. GUARIUM e-commerce Automation 2. Why is the e-commerce industry an excellent opportunity? 3. A study which provided tips for us what the e-commerce industry expects 4. An ideal product

Shareel Whitepaper V.1.2

Shareel Whitepaper V.1.2 Table of content 1. Introduction 2. Why Invest in Shareel? 3. Shareel Investment Opportunities Social Media Syndication Lending To Miners Mining (Proof-of-Stake) 4. Trading 5.

Shareel Whitepaper V.1.2 Table of content 1. Introduction 2. Why Invest in Shareel? 3. Shareel Investment Opportunities Social Media Syndication Lending To Miners Mining (Proof-of-Stake) 4. Trading 5.

Introduction. What is Cryptocurrency?

Table of Contents 1. Introduction 1.1. Cryptocurrency 1.2. ERC20 Standard 1.3. P2P Networks 2. Adverx (AVX) 2.1. Token Specifications 2.2. Token Allocation 3. Real-time bidding (RTB) 3.1. How RTB works

Table of Contents 1. Introduction 1.1. Cryptocurrency 1.2. ERC20 Standard 1.3. P2P Networks 2. Adverx (AVX) 2.1. Token Specifications 2.2. Token Allocation 3. Real-time bidding (RTB) 3.1. How RTB works

ICO BASICS. RedCab LLC. Frequently Asked Questions (FAQs) Website: ICO Website What is an ICO?

Website: ICO Website What is an ICO?") RedCab LLC. Frequently Asked Questions (FAQs) Website: https://redcab.co ICO Website https://redcab.io ICO BASICS 1.1 What is an ICO? An initial coin offering (ICO), also known as a digital token sale

RedCab LLC. Frequently Asked Questions (FAQs) Website: https://redcab.co ICO Website https://redcab.io ICO BASICS 1.1 What is an ICO? An initial coin offering (ICO), also known as a digital token sale

TABLE OF CONTENTS. 3 Disclosure. 4 What is Feast Coin? 4. Brief Overview. 4. Special Features of Feast Coin (FSC) 4. User Benefits of Feast Coin

4. User Benefits of Feast Coin") TABLE OF CONTENTS 3 Disclosure 4 What is Feast Coin? 4. Brief Overview 4. Special Features of Feast Coin (FSC) 4. User Benefits of Feast Coin 5. Vendor Benefits of Feast Coin 5. Work It Works 5. Service

TABLE OF CONTENTS 3 Disclosure 4 What is Feast Coin? 4. Brief Overview 4. Special Features of Feast Coin (FSC) 4. User Benefits of Feast Coin 5. Vendor Benefits of Feast Coin 5. Work It Works 5. Service

Integrative Wallet. Whitepaper. An electronic version of this whitepaper is available at iwtoken.com.

Integrative Wallet Whitepaper An electronic version of this whitepaper is available at iwtoken.com. Contents 1 Introduction 1 1.1 Background............................................ 1 1.2 Our objective...........................................

Integrative Wallet Whitepaper An electronic version of this whitepaper is available at iwtoken.com. Contents 1 Introduction 1 1.1 Background............................................ 1 1.2 Our objective...........................................

DREAM BIT DREAM BIT (MAB) THE FUTURE OF CURRENCY GLOBAL WALLET, DIGITAL CASH

THE FUTURE OF CURRENCY GLOBAL WALLET, DIGITAL CASH") (MAB) THE FUTURE OF CURRENCY 0 MAB The Future of Currency 1 1. ABSTRACT In recent years, mobile shopping has been on the rise. The worldwide mobile payment revenue in 2015 was 450 billion U.S. dollars

(MAB) THE FUTURE OF CURRENCY 0 MAB The Future of Currency 1 1. ABSTRACT In recent years, mobile shopping has been on the rise. The worldwide mobile payment revenue in 2015 was 450 billion U.S. dollars

EasyDex Bridge Assets

EasyDex White Paper Introduction Since Bitcoin was released in 2008, cryptocurrencies have rapidly become a major influence in both the online and greater economic global communities. The technologies

EasyDex White Paper Introduction Since Bitcoin was released in 2008, cryptocurrencies have rapidly become a major influence in both the online and greater economic global communities. The technologies

Obirum WHITEPAPER. Version 2.1.1

Obirum WHITEPAPER Version 2.1.1 Obirum White paper is a living document. We are constantly upgrading our white paper to answer all your questions and provide all information you could possibly need before

Obirum WHITEPAPER Version 2.1.1 Obirum White paper is a living document. We are constantly upgrading our white paper to answer all your questions and provide all information you could possibly need before

etcetera EXECUTIVE SUMMARY

etcetera EXECUTIVE SUMMARY There have been many different attempts to increase adoption of cryptocurrencies by the general public. Some more successful than others. The most important challenges are availability,

etcetera EXECUTIVE SUMMARY There have been many different attempts to increase adoption of cryptocurrencies by the general public. Some more successful than others. The most important challenges are availability,

OLXA COIN WHITE PAPER DECENTRALIZED APPLICATIONS AND CROWD-PROJECTS THROUGH THE BLOCKCHAIN TECHNOLOGY.

OLXA COIN WHITE PAPER DECENTRALIZED APPLICATIONS AND CROWD-PROJECTS THROUGH THE BLOCKCHAIN TECHNOLOGY www.olxacoin.com info@olxacoin.com Table of Contents 1 Introduction 1.1 Introduction to BitCoin and

OLXA COIN WHITE PAPER DECENTRALIZED APPLICATIONS AND CROWD-PROJECTS THROUGH THE BLOCKCHAIN TECHNOLOGY www.olxacoin.com info@olxacoin.com Table of Contents 1 Introduction 1.1 Introduction to BitCoin and

Disclaimer 3 Introduction 4

Disclaimer 3 Introduction 4 USDC: A Digital Coin that Equals USD 4 How Blockchain Changed The Financial Landscape 5 Price Guarantee Plan 6 Token Sale 8 Discounted USDC for ICO 9 Why our token sale is beneficial

Disclaimer 3 Introduction 4 USDC: A Digital Coin that Equals USD 4 How Blockchain Changed The Financial Landscape 5 Price Guarantee Plan 6 Token Sale 8 Discounted USDC for ICO 9 Why our token sale is beneficial

CryptoCarbon (CCRB):

:") CryptoCarbon (CCRB): A NEW TYPE OF CRYPTOCURRENCY WHITEPAPER - FEBRUARY 2018 Contact Information: CRYPTOCARBON GLOBAL LTD info@cryptocarbon.co.uk Table of Contents 1. ABSTRACT 2. INTRODUCTION 3. CRYPTOCARBON

CryptoCarbon (CCRB): A NEW TYPE OF CRYPTOCURRENCY WHITEPAPER - FEBRUARY 2018 Contact Information: CRYPTOCARBON GLOBAL LTD info@cryptocarbon.co.uk Table of Contents 1. ABSTRACT 2. INTRODUCTION 3. CRYPTOCARBON

WHITE PAPER. The First Decentralized Second-Hand Market Platform. Version 1.0

WHITE PAPER The First Decentralized Second-Hand Market Platform http://jlinkcoin.com/ Version 1.0 Abstract. In the existing second-hand market, there have been quite a number of unreliable sellers. This

WHITE PAPER The First Decentralized Second-Hand Market Platform http://jlinkcoin.com/ Version 1.0 Abstract. In the existing second-hand market, there have been quite a number of unreliable sellers. This

CONTENT 1. Legal Disclaimer 2. About the Company Mission II. Vision III. Problem Statement IV. Solution

QURALT WHITEPAPER CONTENT 1. Legal Disclaimer 2. About the Company I. Mission II. Vision III. Problem Statement IV. Solution V. Our Major Products Multicurrency Wallet Multicurrency Prepaid Debit Card

QURALT WHITEPAPER CONTENT 1. Legal Disclaimer 2. About the Company I. Mission II. Vision III. Problem Statement IV. Solution V. Our Major Products Multicurrency Wallet Multicurrency Prepaid Debit Card

FSMN: A Payment Gateway and Merchant Settlement Services for Instant, Secured Global Payments

FSMN: A Payment Gateway and Merchant Settlement Services for Instant, Secured Global Payments Abstract FSMN is a cryptography-based digital coin and payment gateway introduced to the market in 2018 to

FSMN: A Payment Gateway and Merchant Settlement Services for Instant, Secured Global Payments Abstract FSMN is a cryptography-based digital coin and payment gateway introduced to the market in 2018 to

CryptoCarbon (CCRB):

:") CryptoCarbon (CCRB): A NEW TYPE OF CRYPTOCURRENCY WHITEPAPER - FEBRUARY 201 8 Contact Information: CRYPTOCARBON info@cryptocarbon.co.uk Table of Contents 1. ABSTRACT 2. INTRODUCTION 3. CRYPTOCARBON (CCRB)

CryptoCarbon (CCRB): A NEW TYPE OF CRYPTOCURRENCY WHITEPAPER - FEBRUARY 201 8 Contact Information: CRYPTOCARBON info@cryptocarbon.co.uk Table of Contents 1. ABSTRACT 2. INTRODUCTION 3. CRYPTOCARBON (CCRB)

Decentralized Fiat & Crypto. Point of Sale Systems WHITE PAPER 1.0

WHITE PAPER 1.0 Decentralized Fiat & Crypto Point of Sale Systems support@mimicoin.me Please Note: This is not a securities offering and we do not offer this token sale to citizens or residents of United

WHITE PAPER 1.0 Decentralized Fiat & Crypto Point of Sale Systems support@mimicoin.me Please Note: This is not a securities offering and we do not offer this token sale to citizens or residents of United

The first blockchain-based social marketplace for handmade goods by trusted crafters

The first blockchain-based social marketplace for handmade goods by trusted crafters INTRO TANZO is a first of its kind social marketplace for handmade goods, where crafters are protected and craftsmanship

The first blockchain-based social marketplace for handmade goods by trusted crafters INTRO TANZO is a first of its kind social marketplace for handmade goods, where crafters are protected and craftsmanship

CRYPTOCURRENCIES, THE UNBANKED AND INTRINSIC VALUE

CRYPTOCURRENCIES, THE UNBANKED AND INTRINSIC VALUE JA S M I N GÜNGÖR GUESTSPEAKER OF COINTED Facebook Post from an Austrian Banker So now we re involved in trying to make sure we get a very efficient digital

CRYPTOCURRENCIES, THE UNBANKED AND INTRINSIC VALUE JA S M I N GÜNGÖR GUESTSPEAKER OF COINTED Facebook Post from an Austrian Banker So now we re involved in trying to make sure we get a very efficient digital

Abstract 3. Merchants 3. End-user 4. External Merchants 5. Blockchain 5. Development 6. Liquidity and Exchange Network 6.

Contents Abstract 3 Merchants 3 End-user 4 External Merchants 5 Blockchain 5 Development 6 Liquidity and Exchange Network 6 Integrations 6 Point of Sale 7 Payroll 7 Wire Transfers 8 Conclusion 8 Abstract

Contents Abstract 3 Merchants 3 End-user 4 External Merchants 5 Blockchain 5 Development 6 Liquidity and Exchange Network 6 Integrations 6 Point of Sale 7 Payroll 7 Wire Transfers 8 Conclusion 8 Abstract

CMD Venture Technology S.R.L. All rights reserved SAVE Whitepaper V3.0

Content Legal Disclaimer... 2 Abstract... 3 Problem... 3 Solution... 3 Benefits of users... 3 Benefits of investors... 4 Solution to complicated paradigm... 4 SAVE Token... 4 Vision... 4 Decentralization...

Content Legal Disclaimer... 2 Abstract... 3 Problem... 3 Solution... 3 Benefits of users... 3 Benefits of investors... 4 Solution to complicated paradigm... 4 SAVE Token... 4 Vision... 4 Decentralization...

USAGI COIN - Usagi Coin White Paper. Prepared for: Usagicoin.com Prepared by: Punch, Piti

USAGI COIN - Usagi Coin White Paper Prepared for: Usagicoin.com Prepared by: Punch, Piti USAGI COIN - BE 2 BASIC SYSTEM SUMMARY Abstract Nowadays, technology allows people to communicate and send messages

USAGI COIN - Usagi Coin White Paper Prepared for: Usagicoin.com Prepared by: Punch, Piti USAGI COIN - BE 2 BASIC SYSTEM SUMMARY Abstract Nowadays, technology allows people to communicate and send messages

BIT GREEN COIN IS DIGITAL CASH

WHITE PAPER ` BIT GREEN COIN IS DIGITAL CASH The next generation of advance dissolution for global money transaction A break through digital solution related to money transaction. BIT GREEN is a kind of

WHITE PAPER ` BIT GREEN COIN IS DIGITAL CASH The next generation of advance dissolution for global money transaction A break through digital solution related to money transaction. BIT GREEN is a kind of

Quantum Coins its Power of CryptoCurrency

White Paper TABLE OF CONTENTS Introduction... 1 Our Vision.... 2 Our Mission.. 3 Initial Coin Offering (ICO)... 4 Services To Be Offered... 5 Airdrop and Rewards. 6 Virtual World Gaming.... 7 Coins Distribution

White Paper TABLE OF CONTENTS Introduction... 1 Our Vision.... 2 Our Mission.. 3 Initial Coin Offering (ICO)... 4 Services To Be Offered... 5 Airdrop and Rewards. 6 Virtual World Gaming.... 7 Coins Distribution

Whitepaper. Version 2.0. September 2018

Whitepaper Version 2.0 September 2018 Contents Overview... 3 Highlights... 3 Background... 4 Problem Statement... 4 Solution... 4 Transparency... 4 Mining Activities... 5 Strategy... 5 Hardware... 5 Locations...

Whitepaper Version 2.0 September 2018 Contents Overview... 3 Highlights... 3 Background... 4 Problem Statement... 4 Solution... 4 Transparency... 4 Mining Activities... 5 Strategy... 5 Hardware... 5 Locations...

WHITEPAPER OF THE BORSABIT COIN

WHITEPAPER OF THE BORSABIT COIN EFLATUN SOFTWARE 30.07.2018 Intro Cryptocurrencies has been one of the hottest topic of 2017 as Bitcoin, Ethereum and other hundreds of alternative coins in existence attracting

WHITEPAPER OF THE BORSABIT COIN EFLATUN SOFTWARE 30.07.2018 Intro Cryptocurrencies has been one of the hottest topic of 2017 as Bitcoin, Ethereum and other hundreds of alternative coins in existence attracting

NASGO STAY FREE WITH US

NASGO STAY FREE WITH US CRYPTO-ECONOMY TO CONTRIBUTE 10% TO THE GLOBAL GDP BY 2022! Over half a billion people are aware of cryptocurrencies More than 50 million have interacted with cryptocurrencies Over

NASGO STAY FREE WITH US CRYPTO-ECONOMY TO CONTRIBUTE 10% TO THE GLOBAL GDP BY 2022! Over half a billion people are aware of cryptocurrencies More than 50 million have interacted with cryptocurrencies Over

CCPAY PROJECT. WHITEPAPER Version 3.

CCPAY PROJECT WHITEPAPER Version 3. 2 CCPAY preface The history of Crypto-currency began in 2009 when a programmer under the alias Satoshi Nakamoto released Bitcoin. Satoshi Nakamoto pointed out the government

CCPAY PROJECT WHITEPAPER Version 3. 2 CCPAY preface The history of Crypto-currency began in 2009 when a programmer under the alias Satoshi Nakamoto released Bitcoin. Satoshi Nakamoto pointed out the government

SHE Coin IS DIGITAL CASH

WHITE PAPER The next generation of advanced solution for global money transaction A breakthrough digital solution related to money transaction. SHE Coin is a kind of digital cash that you can use to make

WHITE PAPER The next generation of advanced solution for global money transaction A breakthrough digital solution related to money transaction. SHE Coin is a kind of digital cash that you can use to make

HOUTON TOKEN WHITE PAPER

HOUTON TOKEN WHITE PAPER W W W. H O U T O N. I N F O 1. 2. 3. 4. 5. 6. 7. 8. 9. 10. Abstract Introduction Our Vision Problems and Our Solution Technical Distribution Wallet Roadmap Conclusion Disclaimer

HOUTON TOKEN WHITE PAPER W W W. H O U T O N. I N F O 1. 2. 3. 4. 5. 6. 7. 8. 9. 10. Abstract Introduction Our Vision Problems and Our Solution Technical Distribution Wallet Roadmap Conclusion Disclaimer

CRYPTOCOIN. CCTCOIN June CYBERCRYPTO.IO

CRYPTOCOIN CCTCOIN June - 2018 CYBERCRYPTO.IO TABLE OF CONTENTS 1. INTRODUCTION... 01 2. CCTC TOKEN Applications... 04 3. TOKEN DETAILS...06 4. DISCOUNTS OF TIMELY PARTICIPATION FOR PUBLIC SALES OF TOKEN...

CRYPTOCOIN CCTCOIN June - 2018 CYBERCRYPTO.IO TABLE OF CONTENTS 1. INTRODUCTION... 01 2. CCTC TOKEN Applications... 04 3. TOKEN DETAILS...06 4. DISCOUNTS OF TIMELY PARTICIPATION FOR PUBLIC SALES OF TOKEN...

Innovation in the world of cryptocurrencies

Innovation in the world of cryptocurrencies NEW OPPORTUNITIES Innovative features are already reality within reach. 1. Team PrimeStone Presentation Agenda 2. PrimeStone Coin 3. New Coin Platform 4. ICO

Innovation in the world of cryptocurrencies NEW OPPORTUNITIES Innovative features are already reality within reach. 1. Team PrimeStone Presentation Agenda 2. PrimeStone Coin 3. New Coin Platform 4. ICO

DONCOIN (DCNX) Whitepaper

Whitepaper") DONCOIN (DCNX) Whitepaper 1 WHAT IS DONCOIN (DCNX)? Every Cryptocurrency that emerges is like a company which emerges to solve a pending world problem by proffering a lasting solution and raising funds

DONCOIN (DCNX) Whitepaper 1 WHAT IS DONCOIN (DCNX)? Every Cryptocurrency that emerges is like a company which emerges to solve a pending world problem by proffering a lasting solution and raising funds

WE ARE PART OF THE GLOBAL PAYMENT REVOLUTION

WE ARE PART OF THE GLOBAL PAYMENT REVOLUTION Table of contents Page no. 1. What Is ClickGem? 2 2. Disadvantages Of Traditional Money Transaction Methods & The Breakthroughs Of ClickGem 3. Key Applications

WE ARE PART OF THE GLOBAL PAYMENT REVOLUTION Table of contents Page no. 1. What Is ClickGem? 2 2. Disadvantages Of Traditional Money Transaction Methods & The Breakthroughs Of ClickGem 3. Key Applications

STENEUM. The unique Saving program Of Cryptocurrency

STENEUM The unique Saving program Of Cryptocurrency CONTENTS 1. INTRODUCTION 1.1 What is Steneum 2. SPECIFICATIONS 2.1 Algorithm Scrypt 3. ICO (INITIAL COIN OFFERING) 3.1 ICO Target 3.2 ICO Parameters

STENEUM The unique Saving program Of Cryptocurrency CONTENTS 1. INTRODUCTION 1.1 What is Steneum 2. SPECIFICATIONS 2.1 Algorithm Scrypt 3. ICO (INITIAL COIN OFFERING) 3.1 ICO Target 3.2 ICO Parameters

Coimatic a global decentralized blockchain deal and discount marketplace White Paper

1 P a g e Coimatic a global decentralized blockchain deal and discount marketplace White Paper 2 P a g e Table of Contents Description Introduction and Vision The Daily Deal Discount Coupon Model The Discount

1 P a g e Coimatic a global decentralized blockchain deal and discount marketplace White Paper 2 P a g e Table of Contents Description Introduction and Vision The Daily Deal Discount Coupon Model The Discount

Harnessing Innovation for Inclusive Finance

Harnessing Innovation for Inclusive Finance Global Symposium on Innovative Financial Inclusion Kuala Lumpur September, 2016 Douglas Pearce (@DougMPearce) Financial Inclusion Definition and Development

Harnessing Innovation for Inclusive Finance Global Symposium on Innovative Financial Inclusion Kuala Lumpur September, 2016 Douglas Pearce (@DougMPearce) Financial Inclusion Definition and Development

Pitch Deck. Monitor. Trade. Invest. Spend.

Pitch Deck Monitor. Trade. Invest. Spend. 1 The Crypto Market Key Facts : The popularity of crypto means that despite volatile prices, market caps and values are growing substantially every year As of

Pitch Deck Monitor. Trade. Invest. Spend. 1 The Crypto Market Key Facts : The popularity of crypto means that despite volatile prices, market caps and values are growing substantially every year As of

Revolutionary System that Bridge Helpers and Employers on a Blockchain Network

Revolutionary System that Bridge Helpers and Employers on a Blockchain Network ABSTRACT A fast, secure, and easily available cryptocurrency designed for "tipping and Rewarding", allows rewarding a worker

Revolutionary System that Bridge Helpers and Employers on a Blockchain Network ABSTRACT A fast, secure, and easily available cryptocurrency designed for "tipping and Rewarding", allows rewarding a worker

Overview.

Overview Now, I would like to talk to you about ORC Tokens. Simply put, with ORC Tokens, you can establish encrypted payment options for companies all over the world. This enables our company to combine

Overview Now, I would like to talk to you about ORC Tokens. Simply put, with ORC Tokens, you can establish encrypted payment options for companies all over the world. This enables our company to combine

Because we ve been asked a time or two what s new in AML & digital currency in Canada

Because we ve been asked a time or two what s new in AML & digital currency in Canada The following are a compilation of FINTRAC s policy positions 1 in relation to digital currency. This document is current

Because we ve been asked a time or two what s new in AML & digital currency in Canada The following are a compilation of FINTRAC s policy positions 1 in relation to digital currency. This document is current

1. About CryptoBite Coin... 3

1. About CryptoBite Coin... 3 2. Technical Specification....4 3. The CryptoBite Crypto Community... 5 4. CryptoBite Earning Packages... 6 5. CryptoBite USB Wallet... 7 6. CryptoBite Payment gateway...

1. About CryptoBite Coin... 3 2. Technical Specification....4 3. The CryptoBite Crypto Community... 5 4. CryptoBite Earning Packages... 6 5. CryptoBite USB Wallet... 7 6. CryptoBite Payment gateway...

A DECENTRALIZED CURRENCY FOR GAMBLING WHITE PAPER 2018

A DECENTRALIZED CURRENCY FOR GAMBLING CASINOLIZE WHITE PAPER 2018 1 CASINOLIZE GAMBLING IS NOT ABOUT HOW WELL YOU PLAY THE GAMES, IT S REALLY ABOUT HOW WELL YOU HANDLE YOUR MONEY. 2 Contents INTRODUCTION...

A DECENTRALIZED CURRENCY FOR GAMBLING CASINOLIZE WHITE PAPER 2018 1 CASINOLIZE GAMBLING IS NOT ABOUT HOW WELL YOU PLAY THE GAMES, IT S REALLY ABOUT HOW WELL YOU HANDLE YOUR MONEY. 2 Contents INTRODUCTION...

Shaping the future. Light Paper

Shaping the future A revolutionary platform, which: Combines more than 50 years world top scientific and business experience in agriculture Unites all the players of agroindustry Ensures highest possible

Shaping the future A revolutionary platform, which: Combines more than 50 years world top scientific and business experience in agriculture Unites all the players of agroindustry Ensures highest possible

Blockchain platform for freelancers

Blockchain platform for freelancers CONTENT Description 3 Introduction 4 PoS algorithm 6 Masternodes 7 Flex Work Ecosystem 8 Prospects 9 Flex Work Features 10 Flex Work Advantages 11 Flex Work Coin Data

Blockchain platform for freelancers CONTENT Description 3 Introduction 4 PoS algorithm 6 Masternodes 7 Flex Work Ecosystem 8 Prospects 9 Flex Work Features 10 Flex Work Advantages 11 Flex Work Coin Data

Venus Coin 2 I. ABSTRACT

Venus Coin 1 Venus Coin 2 I. ABSTRACT Cryptocurrency has been proven to be a groundbreaking technology in digital assets today, classified as a subset of digital currencies and are also classified as a

Venus Coin 1 Venus Coin 2 I. ABSTRACT Cryptocurrency has been proven to be a groundbreaking technology in digital assets today, classified as a subset of digital currencies and are also classified as a

GLOBAL B2B E-COMMERCE MARKET 2018

PUBLICATION DATE: SEPTEMBER 2018 PAGE 2 GENERAL INFORMATION I PAGE 3 KEY FINDINGS I PAGE 4-7 TABLE OF CONTENTS I PAGE 8 REPORT-SPECIFIC SAMPLE CHARTS I PAGE 9 METHODOLOGY I PAGE 10 RELATED REPORTS I PAGE

PUBLICATION DATE: SEPTEMBER 2018 PAGE 2 GENERAL INFORMATION I PAGE 3 KEY FINDINGS I PAGE 4-7 TABLE OF CONTENTS I PAGE 8 REPORT-SPECIFIC SAMPLE CHARTS I PAGE 9 METHODOLOGY I PAGE 10 RELATED REPORTS I PAGE

zmint Blockchain Introduction

zmint Blockchain Introduction https://zmint.co Recorded November 2017 Introduction for Beginners We are going to introduce you to some new words, and try to make it simple When the Internet was first released

zmint Blockchain Introduction https://zmint.co Recorded November 2017 Introduction for Beginners We are going to introduce you to some new words, and try to make it simple When the Internet was first released

OLYMPIC COIN IT CHANGES EVERYTHING

OLYMPIC COIN IT CHANGES EVERYTHING 1 Whitepaper Table of Contents Table of Contents...2 Introduction 3 Olympic Coin.4 POS/MN based cryptoccurency....4 Why Olympic Coin 4 Proof of Stake.5 Masternodes 5

OLYMPIC COIN IT CHANGES EVERYTHING 1 Whitepaper Table of Contents Table of Contents...2 Introduction 3 Olympic Coin.4 POS/MN based cryptoccurency....4 Why Olympic Coin 4 Proof of Stake.5 Masternodes 5

The Growth of Payments Bank in India: A Road Ahead

The Growth of Payments Bank in India: A Road Ahead Nipun Aggarwal 1, Dr. Dyal Bhatnagar 2 1 Research Scholar, School of Management Studies, Punjabi University, Patiala. 2 School of Management Studies,

The Growth of Payments Bank in India: A Road Ahead Nipun Aggarwal 1, Dr. Dyal Bhatnagar 2 1 Research Scholar, School of Management Studies, Punjabi University, Patiala. 2 School of Management Studies,

Overview - Short Version Whitepaper

Overview - Short Version Whitepaper Blockchain technology has paved way for a new era of value transfer. It has become the most reliable, fast and open source of exchange in the financial industry. However,

Overview - Short Version Whitepaper Blockchain technology has paved way for a new era of value transfer. It has become the most reliable, fast and open source of exchange in the financial industry. However,

Mobile money in Africa

Mobile money in Africa Mobile money in Africa Mobile money and related financial services are continuing to see rapid growth in Africa, and are of major interest to a number of businesses in the region

Mobile money in Africa Mobile money in Africa Mobile money and related financial services are continuing to see rapid growth in Africa, and are of major interest to a number of businesses in the region

beginning of civilized communication platform services like Facebook, YouTube, and

INTRODUCTION Current ages have observed a prosperous era of digital seats, and with the beginning of civilized communication platform services like Facebook, YouTube, and Twitter, the digital biosphere

INTRODUCTION Current ages have observed a prosperous era of digital seats, and with the beginning of civilized communication platform services like Facebook, YouTube, and Twitter, the digital biosphere

Sikka A digital asset transfer platform designed for the financially marginalized.

Sikka A digital asset transfer platform designed for the financially marginalized. Jefferson Scott Davis, Kuldeep Bandhu Aryal, Sandesh Pandey and Saujanya Acharya www.sikka.me 1 2 Overview Sikka is a

Sikka A digital asset transfer platform designed for the financially marginalized. Jefferson Scott Davis, Kuldeep Bandhu Aryal, Sandesh Pandey and Saujanya Acharya www.sikka.me 1 2 Overview Sikka is a

Digital Fiat Currency. The true alternative to physical currency

Digital Fiat Currency The true alternative to physical currency The single largest opportunity for Central Banks in fintech is to digitize cash $75 trillion worth of cash transactions globally 85% of global

Digital Fiat Currency The true alternative to physical currency The single largest opportunity for Central Banks in fintech is to digitize cash $75 trillion worth of cash transactions globally 85% of global

Rupaya Platform White Paper World-class cryptocurrency platform designed for South Asia

Rupaya Platform White Paper World-class cryptocurrency platform designed for South Asia Released May 23, 2018 Revised May 24, 2018 Table of Contents Forward Looking Statements.... 3 Abstract.... 3 Overview....

Rupaya Platform White Paper World-class cryptocurrency platform designed for South Asia Released May 23, 2018 Revised May 24, 2018 Table of Contents Forward Looking Statements.... 3 Abstract.... 3 Overview....

CryptFinTra Exchange & DANU Coin

Exchange & DANU Coin Whitepaper 2017 2222sss KEEP YOU DATA AND MONEY SAFE 2018 1 CONTENT Introduction 3 Market Opportunities 5 Problem Statement 6 Our Technology 8 Exchange Goals 8 What are Innovations?

Exchange & DANU Coin Whitepaper 2017 2222sss KEEP YOU DATA AND MONEY SAFE 2018 1 CONTENT Introduction 3 Market Opportunities 5 Problem Statement 6 Our Technology 8 Exchange Goals 8 What are Innovations?

Custom Benchmarking Report for Mobile Money. Anonymised version Dummy Data March 2017

Custom Benchmarking Report for Mobile Money Anonymised version Dummy Data March 2017 Analysis is based on 100+ mobile money providers who participated in the 2016 Global Annual Adoption survey Europe &

Custom Benchmarking Report for Mobile Money Anonymised version Dummy Data March 2017 Analysis is based on 100+ mobile money providers who participated in the 2016 Global Annual Adoption survey Europe &

Shaping the future. Light Paper

Shaping the future A revolutionary platform, which: Combines more than 50 years world top scientific and business experience in agriculture Unites all the players of agroindustry Ensures highest possible

Shaping the future A revolutionary platform, which: Combines more than 50 years world top scientific and business experience in agriculture Unites all the players of agroindustry Ensures highest possible

Copyright All rights reserved. Page 1

Copyright 2017 www.confercoin.com. All rights reserved. Page 1 1. Introduction 1.1 What is Confer coin 2. Specifications 2.1 Platform 3. Initial Coin Offering (ICO) 3.1 ICO Aim 3.2 ICO Structure 3.3 ICO

Copyright 2017 www.confercoin.com. All rights reserved. Page 1 1. Introduction 1.1 What is Confer coin 2. Specifications 2.1 Platform 3. Initial Coin Offering (ICO) 3.1 ICO Aim 3.2 ICO Structure 3.3 ICO

WHITE PAPER RAVE COIN IS DIGITAL CASH

WHITE PAPER RAVE COIN IS DIGITAL CASH The next generation of advanced solution for global money transaction A breakthrough digital solution related to money transaction. Rave Coin is a kind of digital

WHITE PAPER RAVE COIN IS DIGITAL CASH The next generation of advanced solution for global money transaction A breakthrough digital solution related to money transaction. Rave Coin is a kind of digital

Posted: 1/30/2018 by Fidelity Viewpoints Learn how this digital currency works, plus some risks to consider

Bitcoin Primer Posted: 1/30/2018 by Fidelity Viewpoints Learn how this digital currency works, plus some risks to consider Key Takeaways Digital currencies like Bitcoin have surged to the forefront of

Bitcoin Primer Posted: 1/30/2018 by Fidelity Viewpoints Learn how this digital currency works, plus some risks to consider Key Takeaways Digital currencies like Bitcoin have surged to the forefront of

This isn't surprising after all, a Bitcoin was sold for dollars in the very beginning, and now it is traded at around USD 3500.

Bitcoin, Litecoin, cryptocurrencies, mining... It seems like these new words are popping up everywhere in recent months. In part, the cryptocurrency boom is due to the fact that historically they have

Bitcoin, Litecoin, cryptocurrencies, mining... It seems like these new words are popping up everywhere in recent months. In part, the cryptocurrency boom is due to the fact that historically they have

01 WHAT IS BBNCOIN? * PoW - Proof of Work

O N E P A P E R CONTENTS 01 WHAT IS BBNCOIN? 02 VALUE OF BBNCOIN 03 VISION 04 HOW DOES BBNCOIN WORK? 05 BBNCOIN USE CASE 06 TECHNOLOGY 07 ICO OWNERSHIP 08 WHY SHOULD SOMEONE LIKE YOU BE INTERESTED? 09

O N E P A P E R CONTENTS 01 WHAT IS BBNCOIN? 02 VALUE OF BBNCOIN 03 VISION 04 HOW DOES BBNCOIN WORK? 05 BBNCOIN USE CASE 06 TECHNOLOGY 07 ICO OWNERSHIP 08 WHY SHOULD SOMEONE LIKE YOU BE INTERESTED? 09

A Decentralized Online Marketplace Powered by: Facebucks Token

A Decentralized Online Marketplace Powered by: Facebucks Token Whitepaper V.1 2018 EXECUTIVE SUMMARY The global freelance services marketplace is in a state of both expansion and consolidation. More buyers

A Decentralized Online Marketplace Powered by: Facebucks Token Whitepaper V.1 2018 EXECUTIVE SUMMARY The global freelance services marketplace is in a state of both expansion and consolidation. More buyers

Cross Platform Payment Gateway

White Paper Version: 1.0.0 Index Disclaimer... 2 Executive Summary... 4 Motivation... 5 Problems... 7 Solutions... 8 Our Platform... 11 Advantages... 12 RoadMap... 13 CPPG Token... 14 Company Details...

White Paper Version: 1.0.0 Index Disclaimer... 2 Executive Summary... 4 Motivation... 5 Problems... 7 Solutions... 8 Our Platform... 11 Advantages... 12 RoadMap... 13 CPPG Token... 14 Company Details...

1Word Initial Coin Offering (ICO) O C T O B E R 2017

O C T O B E R 2017") 1Word Initial Coin Offering (ICO) O C T O B E R 2017 Blockchain-powered ENGAGEMENT & REVENUE PLATFORM for publishers & brands 1World Value Proposition 1World Interactive Platform for publishers and brands

1Word Initial Coin Offering (ICO) O C T O B E R 2017 Blockchain-powered ENGAGEMENT & REVENUE PLATFORM for publishers & brands 1World Value Proposition 1World Interactive Platform for publishers and brands

HOARD. Blockchain banking in your pocket. Jason Davis, Hoard, Incorporated. 2018

HOARD Blockchain banking in your pocket Jason Davis, Hoard, Incorporated. 2018 1 The Problem The world cannot adapt to a technology if an individual cannot adopt that technology. Accessibility Simplicity

HOARD Blockchain banking in your pocket Jason Davis, Hoard, Incorporated. 2018 1 The Problem The world cannot adapt to a technology if an individual cannot adopt that technology. Accessibility Simplicity

TABLE OF CONTENTS. INTRODUCTION About Storeplex. ECOMMERCE Marketplace Problems Solution Features Fees. PLEX TOKEN About Distribution Advantages

TABLE OF CONTENTS INTRODUCTION About Storeplex ECOMMERCE Marketplace Problems Solution Features Fees PLEX TOKEN About Distribution Advantages MINIMUM VIABLE PRODUCT About CROWDSALE Pre-sale Main sale Fund

TABLE OF CONTENTS INTRODUCTION About Storeplex ECOMMERCE Marketplace Problems Solution Features Fees PLEX TOKEN About Distribution Advantages MINIMUM VIABLE PRODUCT About CROWDSALE Pre-sale Main sale Fund

Bitcoin Growth Bot Whitepaper

Bitcoin Growth Bot Whitepaper Nucleus Coin Jordan Lindsey, Founder, CEO September 29, 2017 Index of contents Abstract... 2 Background...... 3 The Bitcoin Trading Bot Algorithm. 3 What is Nucleus Coin?....

Bitcoin Growth Bot Whitepaper Nucleus Coin Jordan Lindsey, Founder, CEO September 29, 2017 Index of contents Abstract... 2 Background...... 3 The Bitcoin Trading Bot Algorithm. 3 What is Nucleus Coin?....

A new way of doing business, 100% secure, easy and totally controlled by you!

A new way of doing business, 100% secure, easy and totally controlled by you! 2 1. Who are we We are a dynamic team of developers based in Santos, Brazil. Our core business is financial development. We

A new way of doing business, 100% secure, easy and totally controlled by you! 2 1. Who are we We are a dynamic team of developers based in Santos, Brazil. Our core business is financial development. We

CMC COINS CMC COINS. 11 November, W H I T E P A P E R v W H I T E P A P E R v CMC COINS ICO WHITEPAPER v1.

CMC COINS W H I T E P A P E R v 1. 0 CMC COINS W H I T E P A P E R v 1. 0 11 November, 2018. CMC COINS ICO WHITEPAPER v1.0 Page 1 TABLE OF CONTENTS Abstract 3 Introduction 4 Statement of the problem 5

CMC COINS W H I T E P A P E R v 1. 0 CMC COINS W H I T E P A P E R v 1. 0 11 November, 2018. CMC COINS ICO WHITEPAPER v1.0 Page 1 TABLE OF CONTENTS Abstract 3 Introduction 4 Statement of the problem 5

GoshenCoin 2.0 Do Business The Smarter Way

GoshenCoin 2.0 Do Business The Smarter Way Contents 1. Introduction 2. Market Overview 3. Value Proposition 4. Blockchain Technology 5. Smart Contracts 6. Decentralized Apps (DApps) 7. GoshenCoin History

GoshenCoin 2.0 Do Business The Smarter Way Contents 1. Introduction 2. Market Overview 3. Value Proposition 4. Blockchain Technology 5. Smart Contracts 6. Decentralized Apps (DApps) 7. GoshenCoin History

DEMYSTIFYING DIGITAL PAYMENTS

DEMYSTIFYING DIGITAL PAYMENTS Amitabh Saxena Managing Director, Digital Disruptions November 12, 2014 We ll spend the next 60 minutes going over two main topics. 1 Fundamentals of Card Payments Roles of

DEMYSTIFYING DIGITAL PAYMENTS Amitabh Saxena Managing Director, Digital Disruptions November 12, 2014 We ll spend the next 60 minutes going over two main topics. 1 Fundamentals of Card Payments Roles of

The Crypto Advertising Platform & Vendicoin token system

The Crypto Advertising Platform & Vendicoin token system Version 1.0 1.1.2018 DISCLAIMER OF LIABILITY The purpose of this White Paper is to present Vendio, the crypto advertising platform, and VendiCoin

The Crypto Advertising Platform & Vendicoin token system Version 1.0 1.1.2018 DISCLAIMER OF LIABILITY The purpose of this White Paper is to present Vendio, the crypto advertising platform, and VendiCoin

BlocSide ICO FAQ March 2018

BlocSide ICO FAQ March 2018 BlocSide ICO 1. Why is BlocSide doing an ICO? Initial coin offerings (also known as token sales or token origination events) enable purchasers from multiple socio-economic backgrounds

BlocSide ICO FAQ March 2018 BlocSide ICO 1. Why is BlocSide doing an ICO? Initial coin offerings (also known as token sales or token origination events) enable purchasers from multiple socio-economic backgrounds

Appendix State of the Industry Report on Mobile Money

Appendix 2017 State of the Industry Report on Mobile Money Appendix 1: Methodology In 2013, GSMA Mobile Money Programme started developing a statistical model to estimate mobile money indicators at the

Appendix 2017 State of the Industry Report on Mobile Money Appendix 1: Methodology In 2013, GSMA Mobile Money Programme started developing a statistical model to estimate mobile money indicators at the

Digital Humanities with Unison pervasive computing

Digital Humanities with Unison pervasive computing 1 2 Solving the complex B (The Unbankable Billions). 3 The look of pass, present and future The increasing popularity of mobile computing devices has

Digital Humanities with Unison pervasive computing 1 2 Solving the complex B (The Unbankable Billions). 3 The look of pass, present and future The increasing popularity of mobile computing devices has

Web: NEW ERA OF THE CRYPTO WORLD SIMPLE SHOPPING AND SAFE PAY ICO-2018 WHITEPAPER COPYRIGHT

E-mail: info@payera.io Web: www.payera.io NEW ERA OF THE CRYPTO WORLD SIMPLE SHOPPING AND SAFE PAY ICO-2018 WHITEPAPER COPYRIGHT ALL RIGHTS RESERVED 20. April 2018 TABLE OF CONTENTS 01 Introduction 02

E-mail: info@payera.io Web: www.payera.io NEW ERA OF THE CRYPTO WORLD SIMPLE SHOPPING AND SAFE PAY ICO-2018 WHITEPAPER COPYRIGHT ALL RIGHTS RESERVED 20. April 2018 TABLE OF CONTENTS 01 Introduction 02