Digital Humanities with Unison pervasive computing

|

|

|

- Bruno Ross

- 5 years ago

- Views:

Transcription

1 Digital Humanities with Unison pervasive computing 1

2 2 Solving the complex B (The Unbankable Billions).

3 3 The look of pass, present and future The increasing popularity of mobile computing devices has allowed for new research and application areas. Specifically, urban areas exhibit an elevated concentration of such devices enabling potential operation and sharing of resources among citizens. People, architecture and technology together provide the infrastructure for these applications and implementation of such infrastructure is important for effective design and development. 1950s brought us credit cards to ease the burden of carrying cash and 1960s ATMs to replace tellers and branches. In the 1970s, electronic stock trading began on exchange trading floors and in 1980s we saw the rise of bank mainframe computers and more sophisticated data record-keeping systems but in the 1990s, the Internet and e-commerce business models flourished. As of the result with the introduction of online stock brokerage websites aimed at retail investors.

4 4 These five decades of developments have created a financial technology infrastructure which most people never think about, but use almost every day. Fintech in the last 50 year develop the necessary liquidity into the market. Sophisticated risk management, trade processing, treasury management and data analysis tools at the institutional level for banks and financial services firms. While these systems are not apparent to retail banking customers, they make up a multibillion industry aimed at supporting the needs of the financial services sector. Now, in the 21 st century, retail financial services are being further digitized via mobile wallets, payment apps, robo-advisors for wealth and retirement planning, equity crowd funding platforms for access to private and alternative investment opportunities and online lending platforms. These fintech services are not simple enhancements to banking services, but rather replacing banking services completely. So, fintech can be thought of in two broad categories, consumer-facing and institutional. It is these consumer-facing fintech services which are quickly gaining customers and competing with banks. Despite initial hurdles posed by financial regulations, fintech has revolutionized the financial world and will continue to do so long into the foreseeable future. Technology s role is to simplify lives and streamline daily operations and that s exactly where fintech excels and delivers. And the understanding of Digital Humanities has now gone beyond simple data mining. With Fintech developing new methodologies, and to motivate both reflections on and paradigm shift of humanities with Unison platform. Unison platform with pervasive computing to solve the most complex issue (The Unbankable Billions)

5 5 Most of the world s 2.5 billion unbanked adults live in developing economies. According to the most recent Global Fintex data, 89 percent of adults in high-income economies report having an account at a formal financial institution; in developing economies, 41 percent of adults do. Regionally, according to this same database, the rate of unbanked adults is highest in the Middle East and North Africa, at four out of every five adults, followed by Sub- Saharan Africa and South Asia. In several developing economies, more than 95 percent of adults do not have an account at a formal financial institution. Disparities also exist by gender. Among adults in developing economies living below the $2-a-day poverty line, women are 28 percent less likely than men to have an account at a formal financial institution. Indeed, there is a persistent gender gap of six to nine percentage points across income groups within developing economies. Four Important Facts: often known as a unbankable group Under Unbanked Bank Banking term A Curved 4 Unbanked population

6 6 (B) Billion worldwide Under Banked Assoiated with limited access 1 2 Unbank Term Banking system that only limited to those with access Banked a Curved Condition whereby banks organize By those with access to the system. 3 4 Unbankable population (B) Billion with limited access to the banking system 2 billion people worldwide are unbanked here's how to change this

7 2.5 billion of the world s adults unserved doesn t mean unservable. 7 the world s adults don t use formal banks or semiformal microfinance institutions to save or borrow money, our research finds. Nearly 2.2 billion of these unserved adults live in Africa, Asia, Latin America, and the Middle East. Unserved, however, does not mean unservable. The microfinance movement, for example, has long helped expand credit use among the world s poor reaching more than 150 million clients in 2008 alone. 1 Similarly, we find that of the approximately 1.2 billion adults in Africa, Asia, and the Middle East who use formal or semiformal credit or savings products, about 800 million live on less than $5 a day. Large unserved populations represent opportunities for institutions that are able to offer an innovative range of high-quality, affordable financial products and services. Moreover, with the right financial education and support to make good choices, lower-income consumers will benefit from credit, savings, insurance, and payments products that help them invest in economic opportunities, better manage their money, reduce risks, and plan for the future.

8 8

9 9 Our Reports Write here a great subtitle

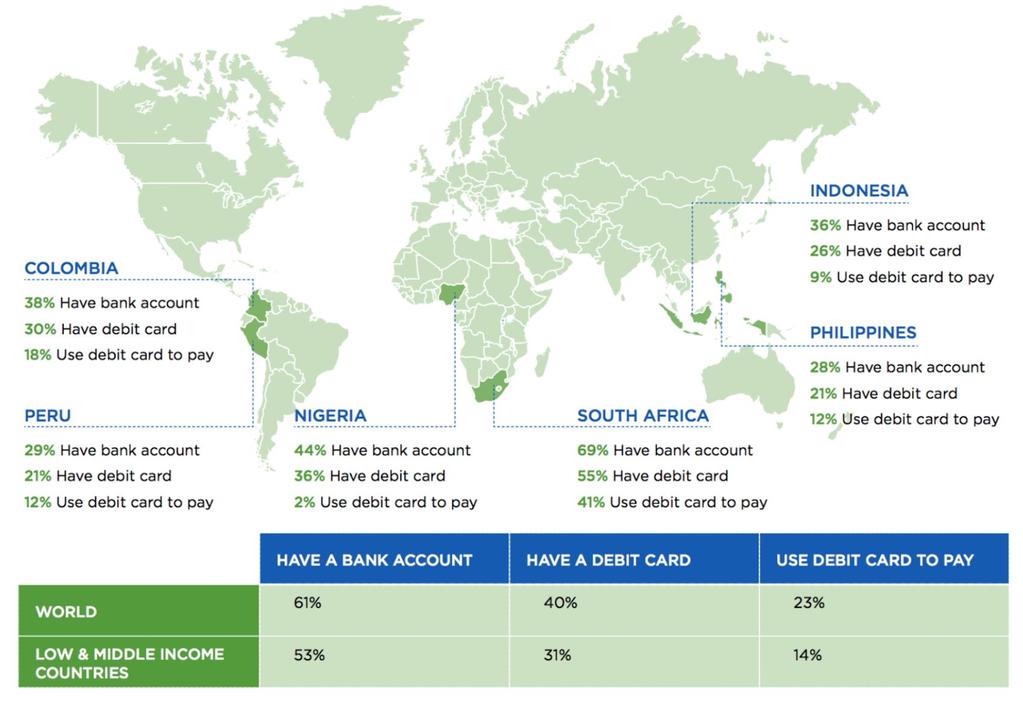

10 10 Global financial institutions invest significant resources into closing tremendous gap in access to banking. Mastercard and Visa, along with other financial institutions, shaped a coalition of partners last year to reach universal financial access by The coalition will focus efforts on 25 countries (mostly African), where 73% of all financially excluded people live. India and China have the largest share of unbanked people. Together, they account for some 32% of them. The rest of the top-priority countries include Bangladesh, Brazil, Colombia, Cote d Ivoire, DRC, Egypt, Ethiopia, Indonesia, Kenya, Mexico, Morocco, Mozambique, Myanmar, Nigeria, Pakistan, Peru, the Philippines, Rwanda, South Africa, Vietnam, Tanzania, Turkey and Zambia. Global Initiatives with Union Platform

11 11 Unison platform with pervasive computing to solve the most complex issue (The Unbankable Billions) Pervasive computing, is a growing trend of embedding computational capability into everyday objects to make them effectively communicate and perform useful tasks in a way that minimizes the end user's need to interact with computers as computers. Pervasive computing devices are networkconnected and constantly available. The goal of Unison platform using pervasive computing to make devices smart to create a sensor network capable of collecting, processing and sending data, and communicating as a means to adapt to the data's context and activity; in essence, a network that can understand its surroundings and improve the human experience and quality of life. Thus provide the unbankable billions into the next frontier of financial needs. Understanding of Digital Humanities has now gone beyond simple data mining. With Fintech developing new methodologies with Unison platform.

12 12 the key thing is to provide tools that allow quick and easy access for security and longer term planning, preventing unnecessary spending, and emphasising the security and certainty that banking services can provide. Unison 4.0, let your most key access available at all time, any time.

13 Three Important Step in life 13 First Day of Life: World of data provided and social service match Life progress into childhood: Education and interest created Adulthood: Prodocitivity into creation. Very poor people in emerging economies not only have a surprising degree of interest in financial services but also, when possible, use them enthusiastically.

14 14 when it comes to assist is to provide mobile options beyond basic needs. Is to offer ways to improve usability and functionality: Creating a mobile user experience more similar to interface. Leveraging advanced biometric security systems to increase customers comfort with activities such as paying bills. Allowing greater flexibility in policies, such as higher limits or currency conversions; Creating a superior omnichannel experience by integrating click-to-call, click-to-chat and video banking options. Online account openings should include a personal component Objective is to be data-centric strategy, an opportunity for differentiation in the marketplace but also a powerful driver of customer engagement.

15 Open discussion 15

Measuring Financial Inclusion of Adults Engaged in Agricultural Activities: Lessons from Demand-Side Surveys

Measuring Financial Inclusion of Adults Engaged in Agricultural Activities: Lessons from Demand-Side Surveys Leora Klapper Lead Economist, Finance and Private Sector Development Team Development Research

Measuring Financial Inclusion of Adults Engaged in Agricultural Activities: Lessons from Demand-Side Surveys Leora Klapper Lead Economist, Finance and Private Sector Development Team Development Research

Financial Regulation and Financial Inclusion

Financial Regulation and Financial Inclusion Nestor A. Espenilla, Jr. Deputy Governor, Supervision and Examination Sector Bangko Sentral ng Pilipinas 1 04 June 2010 Towards a Brave New World Re-shaping

Financial Regulation and Financial Inclusion Nestor A. Espenilla, Jr. Deputy Governor, Supervision and Examination Sector Bangko Sentral ng Pilipinas 1 04 June 2010 Towards a Brave New World Re-shaping

Resource Efficient Industries and Cities: Exploring Opportunities for Austrian Companies and Experts in Emerging Markets

Resource Efficient Industries and Cities: Exploring Opportunities for Austrian Companies and Experts in Emerging Markets WORKSHOP INTRODUCTION Daniel James Crabtree February 21 st, 2018 A member of the

Resource Efficient Industries and Cities: Exploring Opportunities for Austrian Companies and Experts in Emerging Markets WORKSHOP INTRODUCTION Daniel James Crabtree February 21 st, 2018 A member of the

Erasmus Mundus Master Program in Plant Breeding emplant. Selection results Intake 1 ( ) Candidates under EM-scholarships

Candidates under EM-scholarships") Erasmus Mundus Master Program in Plant Breeding emplant Selection results Intake 1 (2018-2020) Candidates under EM-scholarships 1. Program Country Students a. Main list (selected students) b. Reserve list

Erasmus Mundus Master Program in Plant Breeding emplant Selection results Intake 1 (2018-2020) Candidates under EM-scholarships 1. Program Country Students a. Main list (selected students) b. Reserve list

Global Developments in Financial Inclusion

2011/GFPN/WKSP/005 Session 1 Global Developments in Financial Inclusion Submitted by: Alliance for Financial Inclusion (AFI) Workshop on Microfinance Best Practices Ha Noi, Viet Nam 7-8 April 2011 Global

2011/GFPN/WKSP/005 Session 1 Global Developments in Financial Inclusion Submitted by: Alliance for Financial Inclusion (AFI) Workshop on Microfinance Best Practices Ha Noi, Viet Nam 7-8 April 2011 Global

THE IMPACT OF SMARTPHONES ON FINANCIAL INCLUSION Click to edit Master title style

THE IMPACT OF SMARTPHONES ON FINANCIAL INCLUSION Click to edit Master title style Photo: Supratim Bhattachargee, 2017 CGAP Photo Contest Vered Konijnendijk, Joep Roest December 2017 Agenda 1 The smartphone

THE IMPACT OF SMARTPHONES ON FINANCIAL INCLUSION Click to edit Master title style Photo: Supratim Bhattachargee, 2017 CGAP Photo Contest Vered Konijnendijk, Joep Roest December 2017 Agenda 1 The smartphone

Micro, Small and Medium Enterprise Finance

Micro, Small and Medium Enterprise Finance Financial services advisory Strategy formulation Market research and product design Processes and systems design Implementation support Enterprise and staff training

Micro, Small and Medium Enterprise Finance Financial services advisory Strategy formulation Market research and product design Processes and systems design Implementation support Enterprise and staff training

Maya Makanjee. AFI Global Policy Forum 14 September 2009

Bringing Smart Policies to Life The First AFI Global Policy Forum Nairobi, Kenya 14.09.2009 Financial Inclusion in Africa Maya Makanjee FinMark Trust AFI Global Policy Forum 14 September 2009 FinMark Trust

Bringing Smart Policies to Life The First AFI Global Policy Forum Nairobi, Kenya 14.09.2009 Financial Inclusion in Africa Maya Makanjee FinMark Trust AFI Global Policy Forum 14 September 2009 FinMark Trust

Global Best Practices for Women s Financial Inclusion Jennifer McDonald Lagos, November 14, 2013

Global Best Practices for Women s Financial Inclusion Jennifer McDonald Lagos, November 14, 2013 Women s World Banking Global Footprint + 30 years being the largest network in microfinance 19 million active

Global Best Practices for Women s Financial Inclusion Jennifer McDonald Lagos, November 14, 2013 Women s World Banking Global Footprint + 30 years being the largest network in microfinance 19 million active

2015 State of the Industry Report Mobile Money EXECUTIVE SUMMARY

2015 State of the Industry Report Mobile Money EXECUTIVE SUMMARY STATE OF THE INDUSTRY REPORT ON MOBILE MONEY The GSMA represents the interests of mobile operators worldwide, uniting nearly 800 operators

2015 State of the Industry Report Mobile Money EXECUTIVE SUMMARY STATE OF THE INDUSTRY REPORT ON MOBILE MONEY The GSMA represents the interests of mobile operators worldwide, uniting nearly 800 operators

Digital Financial Services for the Micro Finance Sector. May, 2017

Digital Financial Services for the Micro Finance Sector May, 2017 Financial Inclusion? The players in the space of financial inclusion include: Government which handles the policy level issues, Financial

Digital Financial Services for the Micro Finance Sector May, 2017 Financial Inclusion? The players in the space of financial inclusion include: Government which handles the policy level issues, Financial

The Growth of Payments Bank in India: A Road Ahead

The Growth of Payments Bank in India: A Road Ahead Nipun Aggarwal 1, Dr. Dyal Bhatnagar 2 1 Research Scholar, School of Management Studies, Punjabi University, Patiala. 2 School of Management Studies,

The Growth of Payments Bank in India: A Road Ahead Nipun Aggarwal 1, Dr. Dyal Bhatnagar 2 1 Research Scholar, School of Management Studies, Punjabi University, Patiala. 2 School of Management Studies,

An eid Card to Bank the Unbanked Rolan Jahn, NXP

An eid Card to Bank the Unbanked Rolan Jahn, NXP cv cryptovision GmbH T: +49 (0) 209.167-24 50 F: +49 (0) 209.167-24 61 info(at)cryptovision.com 1 AGENDA 1. Market Trends 2. Electronic Payment Benefits

An eid Card to Bank the Unbanked Rolan Jahn, NXP cv cryptovision GmbH T: +49 (0) 209.167-24 50 F: +49 (0) 209.167-24 61 info(at)cryptovision.com 1 AGENDA 1. Market Trends 2. Electronic Payment Benefits

Yusuf Hussain December 14, 2017

Ministry of IT & Telecom Government of Pakistan Yusuf Hussain December 14, 2017 www.ignite.org.pk 1 Digital Finance Definitions are Still Evolving Financial services delivered over digital infrastructure

Ministry of IT & Telecom Government of Pakistan Yusuf Hussain December 14, 2017 www.ignite.org.pk 1 Digital Finance Definitions are Still Evolving Financial services delivered over digital infrastructure

DFS Interoperability and Financial Inclusion: A 20-Country Scan

DFS Interoperability and Financial Inclusion: A 20-Country Scan Presenter Date SMS Transactions Before and After Interconnection SMS volumes, UK Interconnection implemented 1996 97 98 99 2000 01 02 03

DFS Interoperability and Financial Inclusion: A 20-Country Scan Presenter Date SMS Transactions Before and After Interconnection SMS volumes, UK Interconnection implemented 1996 97 98 99 2000 01 02 03

A Market-Building Approach to Financial Inclusion

A Market-Building Approach to Financial Inclusion For many people around the world, gaining access to basic financial services such as savings, remittances, and credit might be the key to unlock poverty.

A Market-Building Approach to Financial Inclusion For many people around the world, gaining access to basic financial services such as savings, remittances, and credit might be the key to unlock poverty.

4-6 October 2017 Geneva. Contribution by BURUNDI

Intergovernmental Group of Experts on E-Commerce and the Digital Economy First session 4-6 October 2017 Geneva Contribution by BURUNDI The views expressed are those of the author and do not necessarily

Intergovernmental Group of Experts on E-Commerce and the Digital Economy First session 4-6 October 2017 Geneva Contribution by BURUNDI The views expressed are those of the author and do not necessarily

UBA Business Direct. Africa s global bank

UBA Business Direct Africa s global bank AFRICA... UNITED BY ONE BANK ABOUT UBA United Bank for Africa (UBA) Plc is a leading financial service institution in sub-saharan Africa with its headquarters in

UBA Business Direct Africa s global bank AFRICA... UNITED BY ONE BANK ABOUT UBA United Bank for Africa (UBA) Plc is a leading financial service institution in sub-saharan Africa with its headquarters in

Seizing E-Government Opportunities: Assessment, Prioritization, & Action. June 12, 2001

Seizing E-Government Opportunities: Assessment, Prioritization, & Action June 12, 2001 Today s Topics Understanding E-Readiness Assessing Readiness for E-Government Learning from Successes Prioritizing

Seizing E-Government Opportunities: Assessment, Prioritization, & Action June 12, 2001 Today s Topics Understanding E-Readiness Assessing Readiness for E-Government Learning from Successes Prioritizing

:?8GK

:?8GK How Financial Chatbots Are Transforming Digital Banking Produced by Abe

How Financial Chatbots Are Transforming Digital Banking Produced by Abe Abe builds conversational banking solutions for progressive community banks. CONTENTS Keeping Pace with Evolving Financial Technologies....3

How Financial Chatbots Are Transforming Digital Banking Produced by Abe Abe builds conversational banking solutions for progressive community banks. CONTENTS Keeping Pace with Evolving Financial Technologies....3

The MasterCard Foundation Savings Learning Lab

The MasterCard Foundation Savings Learning Lab The MasterCard Foundation works with visionary organisations to provide greater access to education, skills training and financial services for people living

The MasterCard Foundation Savings Learning Lab The MasterCard Foundation works with visionary organisations to provide greater access to education, skills training and financial services for people living

MOBILE APP. Today s solution for tomorrow s self-service bank BANKWORLD BANK ON THE FUTURE WITH TODAY S TECHNOLOGY CR2.COM

MOBILE APP Today s solution for tomorrow s self-service bank BANKWORLD BANK ON THE FUTURE WITH TODAY S TECHNOLOGY CR2.COM BANKWORLD MOBILE APP FUTURE READY SOLUTIONS As mobile technology continues to develop

MOBILE APP Today s solution for tomorrow s self-service bank BANKWORLD BANK ON THE FUTURE WITH TODAY S TECHNOLOGY CR2.COM BANKWORLD MOBILE APP FUTURE READY SOLUTIONS As mobile technology continues to develop

BANKWORLD POS. Today s solution for tomorrow s self-service bank BANKWORLD BANK ON THE FUTURE WITH TODAY S TECHNOLOGY CR2.COM

BANKWORLD POS Today s solution for tomorrow s self-service bank BANKWORLD BANK ON THE FUTURE WITH TODAY S TECHNOLOGY CR2.COM BANKWORLD POS CONVENIENT, SIMPLE POS SOLUTIONS Ease of use and fast processing

BANKWORLD POS Today s solution for tomorrow s self-service bank BANKWORLD BANK ON THE FUTURE WITH TODAY S TECHNOLOGY CR2.COM BANKWORLD POS CONVENIENT, SIMPLE POS SOLUTIONS Ease of use and fast processing

The Future of Microfinance in the Fintech Age Jubert Maquiling Country Manager

Digital Financial Services The Future of Microfinance in the Fintech Age Jubert Maquiling Country Manager Software Group Global Experts Global technology company, focused on delivery channels solutions

Digital Financial Services The Future of Microfinance in the Fintech Age Jubert Maquiling Country Manager Software Group Global Experts Global technology company, focused on delivery channels solutions

The Future of Microfinance in the Fintech Age Jubert Maquiling Country Manager

Digital Financial Services The Future of Microfinance in the Fintech Age Jubert Maquiling Country Manager Software Group Global Experts Global technology company, focused on delivery channels solutions

Digital Financial Services The Future of Microfinance in the Fintech Age Jubert Maquiling Country Manager Software Group Global Experts Global technology company, focused on delivery channels solutions

Financial Inclusion Strategies: Global Trends and Lessons Learnt from the AFI Network

Financial Inclusion Strategies: Global Trends and Lessons Learnt from the AFI Network Istanbul, Turkey June 3, 2014 Klaus Prochaska Senior Policy Analyst & Knowledge Manager Alliance for Financial Inclusion(AFI)

Financial Inclusion Strategies: Global Trends and Lessons Learnt from the AFI Network Istanbul, Turkey June 3, 2014 Klaus Prochaska Senior Policy Analyst & Knowledge Manager Alliance for Financial Inclusion(AFI)

Mobile banking: Moving beyond microfinance

Mobile banking: Moving beyond microfinance Thought Paper www.infosys.com/finacle Universal Banking Solution Systems Integration Consulting Business Process Outsourcing Mobile banking: Moving beyond microfinance

Mobile banking: Moving beyond microfinance Thought Paper www.infosys.com/finacle Universal Banking Solution Systems Integration Consulting Business Process Outsourcing Mobile banking: Moving beyond microfinance

THE ROLE OF PAYMENTS IN A SMART CITIES LANDSCAPE

THE ROLE OF PAYMENTS IN A SMART CITIES LANDSCAPE BERT SCHUILING WIRECARD FINANCIAL INSTITUTIONS EUROPE 07.08.2017 1 WHO WE ARE Wirecard combines the skills of a technology company with those of a bank.

THE ROLE OF PAYMENTS IN A SMART CITIES LANDSCAPE BERT SCHUILING WIRECARD FINANCIAL INSTITUTIONS EUROPE 07.08.2017 1 WHO WE ARE Wirecard combines the skills of a technology company with those of a bank.

Addressing gaps in the traditional Banking model in SEA

1 THE OPPORTUNITY FOR FINTECH Addressing gaps in the traditional Banking model in SEA Supriya Sen Senior Advisor, McKinsey Brunei Darussalam 8 April 2018 2 Contents Problem: The size of the financial inclusion

1 THE OPPORTUNITY FOR FINTECH Addressing gaps in the traditional Banking model in SEA Supriya Sen Senior Advisor, McKinsey Brunei Darussalam 8 April 2018 2 Contents Problem: The size of the financial inclusion

CRYPTOCURRENCIES, THE UNBANKED AND INTRINSIC VALUE

CRYPTOCURRENCIES, THE UNBANKED AND INTRINSIC VALUE JA S M I N GÜNGÖR GUESTSPEAKER OF COINTED Facebook Post from an Austrian Banker So now we re involved in trying to make sure we get a very efficient digital

CRYPTOCURRENCIES, THE UNBANKED AND INTRINSIC VALUE JA S M I N GÜNGÖR GUESTSPEAKER OF COINTED Facebook Post from an Austrian Banker So now we re involved in trying to make sure we get a very efficient digital

OPPORTUNITIES TO GROW THE EGG BUSINESS IN AFRICA

OPPORTUNITIES TO GROW THE EGG BUSINESS IN AFRICA Vincent Guyonnet, DVM, Ph.D, Dipl. ACPV FFI Consulting Managing Director Poultry Africa 2017 Kigali, Rwanda October 5, 2017 AGENDA The Egg A global food

OPPORTUNITIES TO GROW THE EGG BUSINESS IN AFRICA Vincent Guyonnet, DVM, Ph.D, Dipl. ACPV FFI Consulting Managing Director Poultry Africa 2017 Kigali, Rwanda October 5, 2017 AGENDA The Egg A global food

SBF Position Paper Megatrends shaping Singapore s Future Economic Strategies and Businesses Ng Siew Quan PwC Singapore

www.pwc.com/sg SBF Position Paper Ng Siew Quan Megatrends shaping Singapore s Future Economic Strategies and Businesses Singapore What is a Megatrend? 1. Megatrends are macroeconomic forces that are shaping

www.pwc.com/sg SBF Position Paper Ng Siew Quan Megatrends shaping Singapore s Future Economic Strategies and Businesses Singapore What is a Megatrend? 1. Megatrends are macroeconomic forces that are shaping

Global IT Procurement and Logistics. Simplifying the complex: an end-to-end IT supply chain solution

Global IT Procurement and Logistics Simplifying the complex: an end-to-end IT supply chain solution We make the complex simple Managing an international IT supply chain isn t an easy task, and comes with

Global IT Procurement and Logistics Simplifying the complex: an end-to-end IT supply chain solution We make the complex simple Managing an international IT supply chain isn t an easy task, and comes with

Customer engagement: transforming the business in the age of the client

Customer engagement: transforming the business in the age of the client Silvia Carlassara CRM and Sales Planning, Intesa Sanpaolo Customer Experience Conference, Financial Services London, 25 October 2017

Customer engagement: transforming the business in the age of the client Silvia Carlassara CRM and Sales Planning, Intesa Sanpaolo Customer Experience Conference, Financial Services London, 25 October 2017

USTGlobal. DIGITAL BANKING TRENDS AND INNOVATIONS A UST Global POV

USTGlobal DIGITAL BANKING TRENDS AND INNOVATIONS A UST Global POV September, 2016 DIGITAL BANKING TRENDS & INNOVATIONS Introduction Digital banking is not an option; rather, it is a must-have strategy

USTGlobal DIGITAL BANKING TRENDS AND INNOVATIONS A UST Global POV September, 2016 DIGITAL BANKING TRENDS & INNOVATIONS Introduction Digital banking is not an option; rather, it is a must-have strategy

FIVE FACTS ABOUT DIRECT BANKS EVERY FINANCIAL INSTITUTION NEEDS TO KNOW

WHITE PAPER FIVE FACTS ABOUT DIRECT BANKS EVERY FINANCIAL INSTITUTION NEEDS TO KNOW Andrew Beatty FIS Product Management Executive 1 877.776.3706 Five Facts About Direct Banks Every Financial. Institution

WHITE PAPER FIVE FACTS ABOUT DIRECT BANKS EVERY FINANCIAL INSTITUTION NEEDS TO KNOW Andrew Beatty FIS Product Management Executive 1 877.776.3706 Five Facts About Direct Banks Every Financial. Institution

Banking beyond branches

Banking beyond branches NETinfo Digital Banking Platform The NETinfo Digital Banking Platform is a comprehensive omnichannel solution, empowering financial institutions to achieve digital transformation

Banking beyond branches NETinfo Digital Banking Platform The NETinfo Digital Banking Platform is a comprehensive omnichannel solution, empowering financial institutions to achieve digital transformation

3-Year System Business Plan Companion Document Action 7- Implement a new country collaboration strategy

3-Year System Business Plan Companion Document Action 7- Implement a new country collaboration strategy Prepared by: CGIAR Science Leaders with input from the DGs working group Document Status: Request

3-Year System Business Plan Companion Document Action 7- Implement a new country collaboration strategy Prepared by: CGIAR Science Leaders with input from the DGs working group Document Status: Request

Promoting Financial Inclusion through Innovation

Promoting Financial Inclusion through Innovation APEC Senior Finance Officials Meeting 23 May 2017 ICT4D, Asian Development Bank What does financial inclusion mean? A client does not need to be banked

Promoting Financial Inclusion through Innovation APEC Senior Finance Officials Meeting 23 May 2017 ICT4D, Asian Development Bank What does financial inclusion mean? A client does not need to be banked

Welcome to Today s Web Seminar SPONSOR BY CONTENT FROM

Welcome to Today s Web Seminar SPONSOR BY CONTENT FROM HOSTED BY Moderator: Michael Sisk Contributing Editor, American Banker Michael Sisk is a New York-based journalist who has covered business and the

Welcome to Today s Web Seminar SPONSOR BY CONTENT FROM HOSTED BY Moderator: Michael Sisk Contributing Editor, American Banker Michael Sisk is a New York-based journalist who has covered business and the

Increasing Financial Inclusion Through E/M- Banking: Insights from International Experiences. May 2014

Increasing Financial Inclusion Through E/M- Banking: Insights from International Experiences May 2014 IFC s Purpose To promote open and competitive markets in developing countries To help generate productive

Increasing Financial Inclusion Through E/M- Banking: Insights from International Experiences May 2014 IFC s Purpose To promote open and competitive markets in developing countries To help generate productive

Global Survey on Internet Security and Trust. April 16, 2018

Global Survey on Internet Security and Trust April 16, 2018 Methodology Methdology, Part 1 This survey was conducted by Ipsos on behalf of the Centre for International Governance Innovation (CIGI), the

Global Survey on Internet Security and Trust April 16, 2018 Methodology Methdology, Part 1 This survey was conducted by Ipsos on behalf of the Centre for International Governance Innovation (CIGI), the

WHITE PAPER COMING OF AGE

WHITE PAPER COMING OF AGE Credit Unions Must Position Themselves Now to Compete in Today s Tech Landscape CONTENTS Executive summary 3 01 Navigating the Credit Union Landscape for Change 4 02 Where the

WHITE PAPER COMING OF AGE Credit Unions Must Position Themselves Now to Compete in Today s Tech Landscape CONTENTS Executive summary 3 01 Navigating the Credit Union Landscape for Change 4 02 Where the

Moving Forward with the FG Agenda: Lessons from Indian Financial Inclusion

Moving Forward with the FG Agenda: Lessons from Indian Financial Inclusion Prof Rekha Jain IIMA IDEA Telecom Centre of Excellence, IIM Ahmedabad, India rekha@iimahd.ernet.in (Source: McKinsey Report- Global

Moving Forward with the FG Agenda: Lessons from Indian Financial Inclusion Prof Rekha Jain IIMA IDEA Telecom Centre of Excellence, IIM Ahmedabad, India rekha@iimahd.ernet.in (Source: McKinsey Report- Global

World Bank Group Korea Green Growth Trust Fund

World Bank Group Korea Green Growth Trust Fund Eun Joo Yi Sr. Operations Officer Korea Green Growth Trust Fund Sustainable Development Practice Group The World Bank Group WHO WE ARE 2 EMBED KGGTF Intro

World Bank Group Korea Green Growth Trust Fund Eun Joo Yi Sr. Operations Officer Korea Green Growth Trust Fund Sustainable Development Practice Group The World Bank Group WHO WE ARE 2 EMBED KGGTF Intro

GLOBAL B2B E-COMMERCE MARKET 2018

PUBLICATION DATE: SEPTEMBER 2018 PAGE 2 GENERAL INFORMATION I PAGE 3 KEY FINDINGS I PAGE 4-7 TABLE OF CONTENTS I PAGE 8 REPORT-SPECIFIC SAMPLE CHARTS I PAGE 9 METHODOLOGY I PAGE 10 RELATED REPORTS I PAGE

PUBLICATION DATE: SEPTEMBER 2018 PAGE 2 GENERAL INFORMATION I PAGE 3 KEY FINDINGS I PAGE 4-7 TABLE OF CONTENTS I PAGE 8 REPORT-SPECIFIC SAMPLE CHARTS I PAGE 9 METHODOLOGY I PAGE 10 RELATED REPORTS I PAGE

Citi Commercial Cards. Efficiency, control and business intelligence in one global solution. Transaction Services Latin America and Mexico

Citi Commercial Cards Efficiency, control and business intelligence in one global solution Transaction Services Latin America and Mexico 2 Citi Transaction Services I Latin America and Mexico Global partner,

Citi Commercial Cards Efficiency, control and business intelligence in one global solution Transaction Services Latin America and Mexico 2 Citi Transaction Services I Latin America and Mexico Global partner,

BANKWORLD KIOSK Today s solution for tomorrow s self-service bank BANKWORLD BANK ON THE FUTURE WITH TODAY S TECHNOLOGY CR2.COM

BANKWORLD KIOSK Today s solution for tomorrow s self-service bank BANKWORLD BANK ON THE FUTURE WITH TODAY S TECHNOLOGY CR2.COM BANKWORLD KIOSK As the Kiosk continues to play an important role in the ongoing

BANKWORLD KIOSK Today s solution for tomorrow s self-service bank BANKWORLD BANK ON THE FUTURE WITH TODAY S TECHNOLOGY CR2.COM BANKWORLD KIOSK As the Kiosk continues to play an important role in the ongoing

Mobile Money regulation

Mobile Money regulation ITU Arab Regional Workshop on "Dgital Financial Inclusion": Session 5 - Harmonized Regulatory Framework of the Digital Financial Services 25 August 2016 Mobile money continues to

Mobile Money regulation ITU Arab Regional Workshop on "Dgital Financial Inclusion": Session 5 - Harmonized Regulatory Framework of the Digital Financial Services 25 August 2016 Mobile money continues to

About This Whitepaper

About This Whitepaper This report focuses on case studies from 5 economies of Asia to assess the status and the future potential of these economies to transition from an Intenret economy towards a fully

About This Whitepaper This report focuses on case studies from 5 economies of Asia to assess the status and the future potential of these economies to transition from an Intenret economy towards a fully

Contextualizing Innovation: Technology-Enabled Microfinance in Haiti, Nicaragua, and Zambia

Branchless Banking Brief 1 Contextualizing Innovation: Technology-Enabled Microfinance in Haiti, Nicaragua, and Zambia MEDA believes that low-income customers are better able to access and benefit from

Branchless Banking Brief 1 Contextualizing Innovation: Technology-Enabled Microfinance in Haiti, Nicaragua, and Zambia MEDA believes that low-income customers are better able to access and benefit from

OPTIMISING INFORMATION WORKFLOW MANAGEMENT (IWM) IN BANKING

IN BANKING") OPTIMISING INFORMATION WORKFLOW MANAGEMENT (IWM) IN BANKING Powerful forces are reshaping the banking industry. Customer expectations, technological capabilities, regulatory requirements, demographics

OPTIMISING INFORMATION WORKFLOW MANAGEMENT (IWM) IN BANKING Powerful forces are reshaping the banking industry. Customer expectations, technological capabilities, regulatory requirements, demographics

Skills development in the informal sector. Arvil V. Adams

Skills development in the informal sector Arvil V. Adams Initial observations The informal sector plays a predominant role in job and national wealth creation in developing countries worldwide, but particularly

Skills development in the informal sector Arvil V. Adams Initial observations The informal sector plays a predominant role in job and national wealth creation in developing countries worldwide, but particularly

Information & Communication Technologies

World Bank Group Information & Communication Technologies Strategy Consultations 2011 CONNECT INNOVATE TRANSFORM www.worldbank.org/ict/strategy ICTStrategy@worldbank.org Objective ICT The World Bank Group

World Bank Group Information & Communication Technologies Strategy Consultations 2011 CONNECT INNOVATE TRANSFORM www.worldbank.org/ict/strategy ICTStrategy@worldbank.org Objective ICT The World Bank Group

DEVELOPMENT AND CLIMATE CHANGE

DEVELOPMENT AND CLIMATE CHANGE Katherine Sierra, Vice President Sustainable Development, The World Bank Washington D.C. April 16, 2009 Overview Poverty reduction, economic growth and climate change must

DEVELOPMENT AND CLIMATE CHANGE Katherine Sierra, Vice President Sustainable Development, The World Bank Washington D.C. April 16, 2009 Overview Poverty reduction, economic growth and climate change must

UNIDO Energy and Climate Change Programme

UNIDO Energy and Climate Change Programme CONTEXT GLOBAL CHALLENGES Energy Poverty Energy Security Climate Change Access to Energy is a pre-requisite for Poverty Reduction and Achievements of MDGs SE4ALL

UNIDO Energy and Climate Change Programme CONTEXT GLOBAL CHALLENGES Energy Poverty Energy Security Climate Change Access to Energy is a pre-requisite for Poverty Reduction and Achievements of MDGs SE4ALL

Euronet s Integrated Prepaid Solution Gain Loyalty and Increase Revenue with Prepaid Cards

Serving millions of people worldwide with electronic payment convenience. Euronet s Integrated Prepaid Solution Gain Loyalty and Increase Revenue with Prepaid Cards Copyright 2010 Euronet Worldwide, Inc.

Serving millions of people worldwide with electronic payment convenience. Euronet s Integrated Prepaid Solution Gain Loyalty and Increase Revenue with Prepaid Cards Copyright 2010 Euronet Worldwide, Inc.

A C C E P T A N C E B R E A K I N G T H R O U G H T H E D I G I T A L A G E T O E X P A N D T R A N S A C T I O N S F O O T P R I N T

ACCEPTANCE B R E A K I N G T H R O U G H T H E D I G I T A L A G E T O E X P A N D T R A N S A C T I O N S F O O T P R I N T New Dynamics in the Acceptance Market in Latin America Marcos Peralta Senior

ACCEPTANCE B R E A K I N G T H R O U G H T H E D I G I T A L A G E T O E X P A N D T R A N S A C T I O N S F O O T P R I N T New Dynamics in the Acceptance Market in Latin America Marcos Peralta Senior

LINKAGE BANKING FOR VILLAGES IN EAST AFRICA

LINKAGE BANKING FOR VILLAGES IN EAST AFRICA Working with savings banks to double the number of savings accounts for the poor June 2014 RETAIL REGIONAL RESPONSIBLE Learning Paper LEARNING PAPER 3 LINKAGE

LINKAGE BANKING FOR VILLAGES IN EAST AFRICA Working with savings banks to double the number of savings accounts for the poor June 2014 RETAIL REGIONAL RESPONSIBLE Learning Paper LEARNING PAPER 3 LINKAGE

DIGITALIZATION IS NOT GOING DIGITAL THE CHALLENGE FOR RETAIL BANKS

DIGITALIZATION IS NOT GOING DIGITAL THE CHALLENGE FOR RETAIL BANKS FINANCIAL FORUM INNOVATIONS Sofia June 2016 1 TWO TRENDS ARE CONVERGING WHICH PRESENT BANKS WITH BOTH CHALLENGE AND OPPORTUNITY 1? Banks

DIGITALIZATION IS NOT GOING DIGITAL THE CHALLENGE FOR RETAIL BANKS FINANCIAL FORUM INNOVATIONS Sofia June 2016 1 TWO TRENDS ARE CONVERGING WHICH PRESENT BANKS WITH BOTH CHALLENGE AND OPPORTUNITY 1? Banks

WATER AND SANITATION PROGRAM

WATER AND SANITATION PROGRAM Changing Conditions for WSS WSP s Response Jae So Manager, Water and Sanitation Program May 20, 2008 Changing Global Conditions WSS Access WSS Challenges WSP Response WSP and

WATER AND SANITATION PROGRAM Changing Conditions for WSS WSP s Response Jae So Manager, Water and Sanitation Program May 20, 2008 Changing Global Conditions WSS Access WSS Challenges WSP Response WSP and

Agriculture Finance Support Facility

FAQ: Including Psychometric Testing Into Credit Risk Assessment Amie Vaccaro and Julia Reichelstein of the Entrepreneurial Finance Lab (EFL) on Including Psychometric Testing Into Credit Risk Assessment

FAQ: Including Psychometric Testing Into Credit Risk Assessment Amie Vaccaro and Julia Reichelstein of the Entrepreneurial Finance Lab (EFL) on Including Psychometric Testing Into Credit Risk Assessment

African Fintech Pitch 13 th October, 2016

African Fintech Pitch 13 th October, 2016 We believe in a world where technology is seamlessly integrated in our lives facilitating transactions in a clear, convenient and intuitive manner. Our Pitch

African Fintech Pitch 13 th October, 2016 We believe in a world where technology is seamlessly integrated in our lives facilitating transactions in a clear, convenient and intuitive manner. Our Pitch

BIOMETRICS IN BANKING

w h i t e pa p e r BIOMETRICS IN BANKING From Unbanked to Lifelong Customer January 2014 A Significant Opportunity for Financial Institutions Worldwide The financial world appears to be on the cusp of

w h i t e pa p e r BIOMETRICS IN BANKING From Unbanked to Lifelong Customer January 2014 A Significant Opportunity for Financial Institutions Worldwide The financial world appears to be on the cusp of

NFC. SPRING 2013 ul.com/newscience

NEW SCIENCE TRANSACTION SECURITY CASE STUDY NFC Implementation Model SPRING 2013 ul.com/newscience NEW SCIENCE TRANSACTION SECURITY OVERVIEW Technological advances in payments, mobile commerce and identity

NEW SCIENCE TRANSACTION SECURITY CASE STUDY NFC Implementation Model SPRING 2013 ul.com/newscience NEW SCIENCE TRANSACTION SECURITY OVERVIEW Technological advances in payments, mobile commerce and identity

Capacity building for Regional Air Pollution in the Developing regions

Capacity building for Regional Air Pollution in the Developing regions Sara Feresu (IES and APINA) Task Force on HTAP and GAP Forum Joint Meeting Brussels, June 2010 INSTITUTE OF ENVIRONMENTAL STUDIES

Capacity building for Regional Air Pollution in the Developing regions Sara Feresu (IES and APINA) Task Force on HTAP and GAP Forum Joint Meeting Brussels, June 2010 INSTITUTE OF ENVIRONMENTAL STUDIES

Global Food Security Index

Global Food Security Index Sponsored by 26 September 2012 Agenda Overview Methodology Overall results Results for India Website 2 Overview The Economist Intelligence Unit was commissioned by DuPont to

Global Food Security Index Sponsored by 26 September 2012 Agenda Overview Methodology Overall results Results for India Website 2 Overview The Economist Intelligence Unit was commissioned by DuPont to

BANKWORLD INTERNET Today s solution for tomorrow s self-sevice bank BANKWORLD BANK ON THE FUTURE WITH TODAY S TECHNOLOGY CR2.COM

BANKWORLD INTERNET Today s solution for tomorrow s self-sevice bank BANKWORLD BANK ON THE FUTURE WITH TODAY S TECHNOLOGY CR2.COM With BankWorld, your bank will have the foundation to develop your own internet

BANKWORLD INTERNET Today s solution for tomorrow s self-sevice bank BANKWORLD BANK ON THE FUTURE WITH TODAY S TECHNOLOGY CR2.COM With BankWorld, your bank will have the foundation to develop your own internet

Challenges to Adopting Artificial Intelligence

Challenges to Adopting Artificial Intelligence Augmented Intelligence for Enterprise 17 November 2017 Drew Perez dperez@adatos.com Managing Director, Adatos A.I. Timing & Opportunity What Keeps CEOs Awake

Challenges to Adopting Artificial Intelligence Augmented Intelligence for Enterprise 17 November 2017 Drew Perez dperez@adatos.com Managing Director, Adatos A.I. Timing & Opportunity What Keeps CEOs Awake

Three African Futures. John Page The Brookings Institution University of Nevada at Las Vegas 7 April 2014

Three African Futures John Page The Brookings Institution University of Nevada at Las Vegas 7 April 2014 The Next Frontier? Africa has become the new frontier market Africa is the world s fastest-growing

Three African Futures John Page The Brookings Institution University of Nevada at Las Vegas 7 April 2014 The Next Frontier? Africa has become the new frontier market Africa is the world s fastest-growing

Building Financial Systems for the Poor

Building Financial Systems for the Poor Gautam Ivatury (givatury@worldbank.org) Center for Global Development June 14, 2006 1 Waterpoort, South Africa nearest bank branch 100km 2 3 4 5 Who are these firms

Building Financial Systems for the Poor Gautam Ivatury (givatury@worldbank.org) Center for Global Development June 14, 2006 1 Waterpoort, South Africa nearest bank branch 100km 2 3 4 5 Who are these firms

Whitepaper. Abstract. Introduction

Whitepaper Proxy Ethereum for Everyone We do not offer securities or a collective investment scheme. You are advised to read this document carefully in full, and perform due diligence. According to the

Whitepaper Proxy Ethereum for Everyone We do not offer securities or a collective investment scheme. You are advised to read this document carefully in full, and perform due diligence. According to the

Cisco Remote Expert Smart Solution for Retail Banking Enabling Personalized and Pervasive Sales and Service Across Delivery Channels

Solution Overview Cisco Remote Expert Smart Solution for Retail Banking Enabling Personalized and Pervasive Sales and Service Across Delivery Channels For too long, the financial services industry has

Solution Overview Cisco Remote Expert Smart Solution for Retail Banking Enabling Personalized and Pervasive Sales and Service Across Delivery Channels For too long, the financial services industry has

FINACLE CORE BANKING TRANSFORMATION MAKES EQUITY BANK STRONGER, LEANER AND FITTER

FINACLE CORE BANKING TRANSFORMATION MAKES EQUITY BANK STRONGER, LEANER AND FITTER Profile Equity Bank is a leading commercial bank in Kenya offering retail banking, microfinance and related services. The

FINACLE CORE BANKING TRANSFORMATION MAKES EQUITY BANK STRONGER, LEANER AND FITTER Profile Equity Bank is a leading commercial bank in Kenya offering retail banking, microfinance and related services. The

Gemalto Consulting Services. Take control of your smart card implementation

Gemalto Consulting Services Take control of your smart card implementation FINANCIAL SERVICES & RETAIL > SERVICE ENTERPRISE INTERNET CONTENT PROVIDERS PUBLIC SECTOR TELECOMMUNICATIONS TRANSPORT Gemalto

Gemalto Consulting Services Take control of your smart card implementation FINANCIAL SERVICES & RETAIL > SERVICE ENTERPRISE INTERNET CONTENT PROVIDERS PUBLIC SECTOR TELECOMMUNICATIONS TRANSPORT Gemalto

Plantwise: A global alliance led by CABI for plant health and sustainable agriculture

Plantwise: A global alliance led by CABI for plant health and sustainable agriculture Dr Ulli Kuhlmann, Executive Director Global Operations & Dr Wade Jenner, Global Director Plant Health Systems Development

Plantwise: A global alliance led by CABI for plant health and sustainable agriculture Dr Ulli Kuhlmann, Executive Director Global Operations & Dr Wade Jenner, Global Director Plant Health Systems Development

FUTURE OF BUSINESS SURVEY

Future of Business Survey 01 FUTURE OF BUSINESS SURVEY TRADE REPORT JULY 2017 Future of Business Survey 02 INTRODUCTION¹ In January 2017, we published a report² based on findings from the Future of Business

Future of Business Survey 01 FUTURE OF BUSINESS SURVEY TRADE REPORT JULY 2017 Future of Business Survey 02 INTRODUCTION¹ In January 2017, we published a report² based on findings from the Future of Business

Population Distribution by Income Tiers, 2001 and 2011

1 Updated August 13, 2015: This new edition includes corrected estimates for Iceland, Luxembourg, Netherlands and Taiwan, and some related aggregated data. TABLE A1 Distribution by Income Tiers, 2001 and

1 Updated August 13, 2015: This new edition includes corrected estimates for Iceland, Luxembourg, Netherlands and Taiwan, and some related aggregated data. TABLE A1 Distribution by Income Tiers, 2001 and

How Banks Can Generate More Revenue and Profit by Enabling Customer Centricity

executive brief How Banks Can Generate More Revenue and Profit by Enabling Customer Centricity Customer centricity is not a new concept. For the past 15 years, banks have been talking about overcoming

executive brief How Banks Can Generate More Revenue and Profit by Enabling Customer Centricity Customer centricity is not a new concept. For the past 15 years, banks have been talking about overcoming

SME Finance Forum. November 2017

SME Finance Forum November 2017 While advances have been made to promote financial inclusion, Mexico s population is largely unbanked Breakdown of 43MM adults in Mexico by level of financial inclusion,

SME Finance Forum November 2017 While advances have been made to promote financial inclusion, Mexico s population is largely unbanked Breakdown of 43MM adults in Mexico by level of financial inclusion,

HIGHLIGHTS OF THE BOTSWANA COUNTRY REPORT

HIGHLIGHTS OF THE BOTSWANA COUNTRY REPORT B Y D R K E I T H J E F F E R I S, E C O N S U L T B O T S W A N A 3 1 / 1 0 / 2 0 1 3 CONTENTS INTRODUCTION BOTSWANA STUDY Contribution of Agriculture to GDP

HIGHLIGHTS OF THE BOTSWANA COUNTRY REPORT B Y D R K E I T H J E F F E R I S, E C O N S U L T B O T S W A N A 3 1 / 1 0 / 2 0 1 3 CONTENTS INTRODUCTION BOTSWANA STUDY Contribution of Agriculture to GDP

What is the role of gender in smallholder farming?

What is the role of gender in smallholder farming? Libor Stloukal FAO, Rome, Italy ICRISAT s 40 th Science Symposium Patancheru, 24-25 September 2012 Key messages 1) Significant gender disparities continue

What is the role of gender in smallholder farming? Libor Stloukal FAO, Rome, Italy ICRISAT s 40 th Science Symposium Patancheru, 24-25 September 2012 Key messages 1) Significant gender disparities continue

CULTURAL MARKETING HURDLES

Topic: Marketing & Social Media CULTURAL MARKETING HURDLES In a globalized world products and marketing campaigns have long been crossing national borders. But the differences in the acceptance of online

Topic: Marketing & Social Media CULTURAL MARKETING HURDLES In a globalized world products and marketing campaigns have long been crossing national borders. But the differences in the acceptance of online

Excellence as a commitment, innovation as a goal. Flexibility and Experience

MICROFINANCE Excellence as a commitment, innovation as a goal. At TOP SYSTEMS we know how institution to trust a supplier and feel that they are an integral part of their team. Since 1987 we have been

MICROFINANCE Excellence as a commitment, innovation as a goal. At TOP SYSTEMS we know how institution to trust a supplier and feel that they are an integral part of their team. Since 1987 we have been

Our Journey. and the Future to Our Journey. DNA of Arise. Arise into the Future. Successes and Highlights

Our Journey Our Journey and the Future to 2030 Arise into the Future DNA of Arise Successes and Highlights The Story of Arise The start of our journey Arise Key Milestones September First close signing

Our Journey Our Journey and the Future to 2030 Arise into the Future DNA of Arise Successes and Highlights The Story of Arise The start of our journey Arise Key Milestones September First close signing

HIKMET ERSEK Chief Executive Officer

HIKMET ERSEK Chief Executive Officer Welcome Hosgeldiniz Willkommen Strategy Overview OUR VISION Western Union: The Network and Brand for Moving Money Focus on the underserved 1 COMPETITIVE ADVANTAGES

HIKMET ERSEK Chief Executive Officer Welcome Hosgeldiniz Willkommen Strategy Overview OUR VISION Western Union: The Network and Brand for Moving Money Focus on the underserved 1 COMPETITIVE ADVANTAGES

Retail Banking Insights

Retail Banking Insights nsights Number 9 January 2017 The Winning Formula for Omnichannel Banking in North America For more than a decade, traditional retailers have been designing customer journeys and

Retail Banking Insights nsights Number 9 January 2017 The Winning Formula for Omnichannel Banking in North America For more than a decade, traditional retailers have been designing customer journeys and

Sub-Saharan Africa: A major potential revenue opportunity for digital payments

FEBRUARY 2014 Sub-Saharan Africa: A major potential revenue opportunity for digital payments Jake Kendall, Robert Schiff, and Emmanuel Smadja Sub-Saharan Africa offers tantalizing potential for mobile

FEBRUARY 2014 Sub-Saharan Africa: A major potential revenue opportunity for digital payments Jake Kendall, Robert Schiff, and Emmanuel Smadja Sub-Saharan Africa offers tantalizing potential for mobile

Challenges and Opportunities in Pharma: Perspective for an Emerging Middle East April 24th, 2015

Challenges and Opportunities in Pharma: Perspective for an Emerging Middle East 2020 April 24th, 2015 Content Pharma Market Landscape Global Pharma Market Market Categories Middle East Markets Major Challenges

Challenges and Opportunities in Pharma: Perspective for an Emerging Middle East 2020 April 24th, 2015 Content Pharma Market Landscape Global Pharma Market Market Categories Middle East Markets Major Challenges

Innovation at Scale. James Anderson Executive Vice President Mastercard

Innovation at Scale James Anderson Executive Vice President Mastercard 1 trends in digital 2 implications for retail banking 3 Mastercard s innovations trends in digital Mobile Internet Usage mobile internet

Innovation at Scale James Anderson Executive Vice President Mastercard 1 trends in digital 2 implications for retail banking 3 Mastercard s innovations trends in digital Mobile Internet Usage mobile internet

Decentralized Fiat & Crypto. Point of Sale Systems WHITE PAPER 1.0

WHITE PAPER 1.0 Decentralized Fiat & Crypto Point of Sale Systems support@mimicoin.me Please Note: This is not a securities offering and we do not offer this token sale to citizens or residents of United

WHITE PAPER 1.0 Decentralized Fiat & Crypto Point of Sale Systems support@mimicoin.me Please Note: This is not a securities offering and we do not offer this token sale to citizens or residents of United

The Future of Retail Banking

The Future of Retail Banking Navigating the digital banking revolution The digital banking landscape Market trends Challenges & opportunities Digital transformation with HID Global 43% Mobile phone users

The Future of Retail Banking Navigating the digital banking revolution The digital banking landscape Market trends Challenges & opportunities Digital transformation with HID Global 43% Mobile phone users

Financial Inclusion. But how?

Financial Inclusion But how? Collaborative innovation The Tracom SPS group of companies Reinvent Inspire your customers Analyse and design Drive efficiencies Create Revenue streams Manage risks Secure

Financial Inclusion But how? Collaborative innovation The Tracom SPS group of companies Reinvent Inspire your customers Analyse and design Drive efficiencies Create Revenue streams Manage risks Secure

WOMEN AND MOBILE FINANCIAL SERVICES: THE CASE OF ZOONA IN ZAMBIA

WOMEN AND MOBILE FINANCIAL SERVICES: THE CASE OF ZOONA IN ZAMBIA Creating Business Solutions to Poverty Mennonite Economic Development Associates Inclusive Financial Services Expanding financial services

WOMEN AND MOBILE FINANCIAL SERVICES: THE CASE OF ZOONA IN ZAMBIA Creating Business Solutions to Poverty Mennonite Economic Development Associates Inclusive Financial Services Expanding financial services

SMALL BUSINESS BANKING: A $56.9 BILLION OPPORTUNITY FOR THE TAKING

SMALL BUSINESS BANKING: A $56.9 BILLION OPPORTUNITY FOR THE TAKING EXECUTIVE SUMMARY Small businesses are the hottest under-served market segment, offering outstanding revenue potential for financial institutions.

SMALL BUSINESS BANKING: A $56.9 BILLION OPPORTUNITY FOR THE TAKING EXECUTIVE SUMMARY Small businesses are the hottest under-served market segment, offering outstanding revenue potential for financial institutions.

It is a pleasure to be here in Adelaide with shareholders for one of my last official duties as Chief Executive of ANZ.

ANZ 2015 AGM Address Mike Smith Group Chief Executive Officer Good morning to everyone. It is a pleasure to be here in Adelaide with shareholders for one of my last official duties as Chief Executive of

ANZ 2015 AGM Address Mike Smith Group Chief Executive Officer Good morning to everyone. It is a pleasure to be here in Adelaide with shareholders for one of my last official duties as Chief Executive of

Partnering with Prepaid Technologies. Payments Technology for Banks

Partnering with Prepaid Technologies Payments Technology for Banks Prepaid Opportunity for Commercial Customers Pain Points of Paper Payments Checks are cumbersome and costly Burden of replacing lost and

Partnering with Prepaid Technologies Payments Technology for Banks Prepaid Opportunity for Commercial Customers Pain Points of Paper Payments Checks are cumbersome and costly Burden of replacing lost and

ACHIEVING UNIVERSAL FINANCIAL INCLUSION

5DC4-6A68- ACHIEVING UNIVERSAL FINANCIAL INCLUSION Advancing the Research Agenda Rebecca Mann Financial Services for the Poor 29 June Universal Financial Inclusion requires changing the underlying economics

5DC4-6A68- ACHIEVING UNIVERSAL FINANCIAL INCLUSION Advancing the Research Agenda Rebecca Mann Financial Services for the Poor 29 June Universal Financial Inclusion requires changing the underlying economics