FY16 Preliminary Results Presentation December 2016

|

|

|

- Cecily Wheeler

- 6 years ago

- Views:

Transcription

1 FY16 Preliminary Results Presentation December 2016

2 Agenda Simon Cooper CEO FY16 Highlights Wendy Parry CFO Financial Performance FY16 Simon Cooper CEO Evolution of Key Drivers Summary and Outlook Q and A 2

3 Profit & Loss Account UK Segment FY16 EBITDA growth of 25.5% in the UK Strong growth year on year: Revenue +12.3% EBITDA +25.5% Efficient increase in our market traffic share with marketing spend excluding offline as a % of revenue falling to 44.7% Investment in place in supply function supports increasing % of direct contracting and fixed and variable cost per booking dropped from 16.0% to 14.6% of Revenue EBITDA % revenue at 35.8% in FY16 up from 32.0% in FY15 3

4 Profit and Loss Account - International Investment continues in Sweden to build scale and brand Success in international markets defined as profitable performance within 2-3 years of launch at scale OTB has invested to grow its share of market both online and offline 4

5 Profit and Loss Account - Group Underlying profit before tax +47% increase YOY External financing costs reduced significantly through renegotiation of facilities post IPO Shareholder loan interest and amortisation of acquired intangibles below underlying profit before tax Effective tax rate in FY15 affected by disallowed shareholder interest Note: Effective tax rate is based on corporation tax divided by retained earnings excluding deal fees and amortisation of intangibles 5

6 Balance Sheet All customer monies are paid into a trust account which is effectively a debtor to the business Net cash position has increased from 10.9m to 26.1m Bank loans repaid in full out of the Group s existing cash balances post IPO Seasonal cash flow requirements are covered by a revolving credit facility 6

7 Cash Flow Strong cash conversion at 90% The Board recommends a dividend of 2.2p per share and thereafter intends to adopt a progressive dividend policy 3m of deal costs accrued in FY15 relating to the IPO were paid in the first half of FY16 Source: Company Information 7

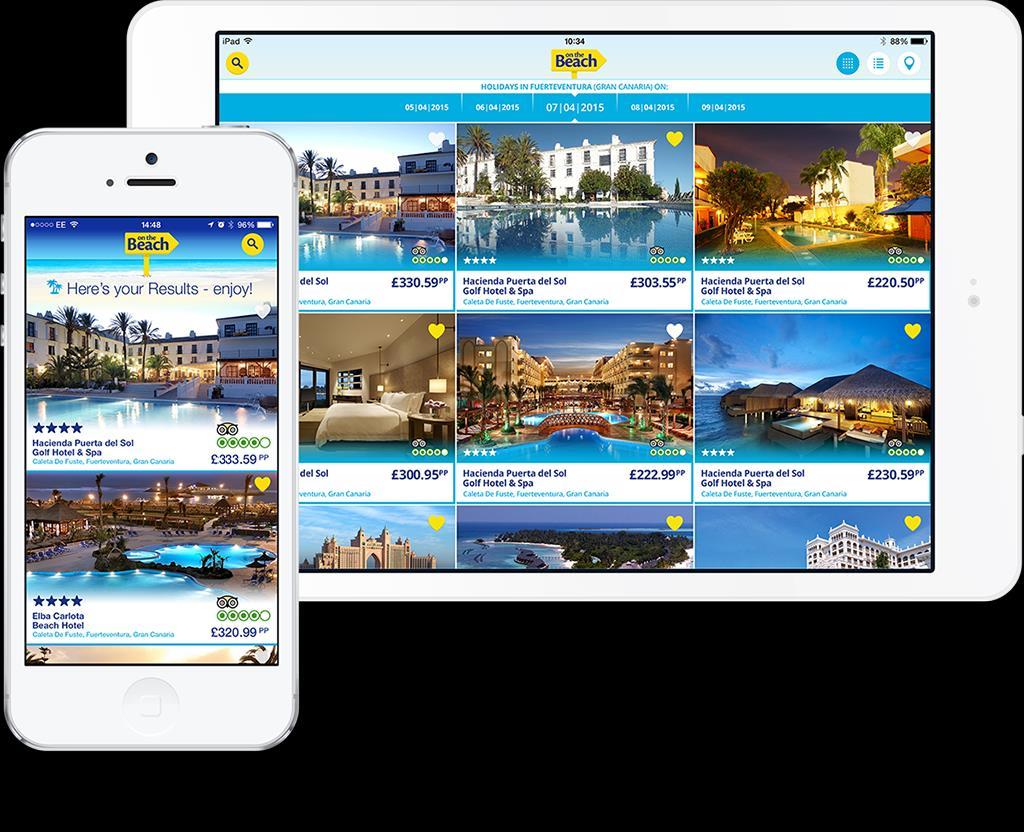

8 Business Highlights OTB is disrupting the retail of beach holidays through innovative technology and customer value proposition Structural Market Growth & Market Share Growth A number of external events disrupted the overall holiday market OTB continued to grow share of market, growing daily unique visitors to site by 12.6% YOY Optimise Customer Proposition Continued investment in technology and talent increased the pace of innovation 77% increase in smartphone bookings YOY with 96% increase YOY in visitors logging in to site Leverage Revenue Focus on profitable growth drove revenue per booking up 7.5% YOY Direct contracts achieving up to 70% of forward arrivals by month Drive Efficient Share Growth & Strengthen Brand Efficiencies in online marketing reduced spend as a % of revenue to 44.7% (FY %) Offline investment continues to increase awareness of our brand nationally Drive Operational Leverage & Expand Internationally 47% YOY growth in Underlying Group PBT Strong growth in Sweden with Norway launch planned for December

9 Disruptive retailer of beach package holidays On the Beach has the product advantages of a tour operator with the model advantages of an OTA Tour Operator OTA HIGH Cost Base LOW HIGH Risk LOW HIGH NARROW Margin Product Range LOW BROAD Specialist Generalist 9

10 Market FY16 The market backdrop in FY16 was unsettled by multiple external events Overall short haul beach holiday volumes are resilient and online penetration continues to increase Dynamic packaging offers greater value and flexibility and steals share from traditional package Short haul beach online versus offline (UK) 16,000 Short haul beach offline Short haul beach online 14,000 +5% 12,000 10,000 +7% 2 8, was disrupted by multiple external events 6,000 4,000 2, Traditional package versus dynamic package 25% % 15% 10% 5% 0% -5% Traditional Package Dynamically Packaged % 10

11 Competitive Landscape and Barriers to Success On the Beach sells high margin tour operator style product with a lightweight OTA style fixed cost base FOCUS EXPERTISE AGILITY SCALE BRAND UK Short Haul Beach Online - Estimated Market Share Tour operator short haul volumes (m pax) 10 TUI 9 Thomas Cook Jet2holidays Cosmos Holidays Olympic Holidays On The Beach % Travel Republic 4 Low Cost Holidays 3 JET2 Love Holidays Easyjet Holidays Other OTA Other tour operator

12 Key Drivers of Growth

13 Innovate through investment in talent & technology Continued investment into in-house technology extends our ability to out innovate the competition Continued investment in our technology capability will allow us to innovate at an increasing pace Team is currently 75 specialists Evolution to an ever more agile way of working Technology platform architecture Service management, monitoring and alerting Management information system Technology platform New features building on our existing platform CMS Basket CRM Services Geolocation myotb Recommendat ion engine Deals app Backoffice App API app Flights app Hotels app Currency App Manage Your Booking Search Service Personalisation Order Processing Data aggregation Data acquisition 13

14 Optimise Customer Proposition Our ambition is to drive a fully personalised cross-device experience for all users on all devices Revenue per booking Conversion Revenue per unique visitor Logged in visitors FY16 vs FY15 4,500,000 4,000,000 3,500,000 Increases to Revenue per UV driven through multiple projects: 3,000,000 2,500,000 Device level 2,000,000 1,500,000 Log in and cross device optimisation 1,000, ,000 Real time personalisation - FY15 FY16 Off site personalisation Traffic shaping Smartphone Bookings FY16 vs FY15 120, , % Increase in mobile RPUV The features we are developing are supported by the infrastructure that has been built into the heart of our platform over a number of years 80,000 60,000 40,000 20,000 - FY15 FY16 14

15 Jan 14 Mar 14 May 14 Jul 14 Sep 14 Nov 14 Jan 15 Mar 15 May 15 Jul 15 Sep 15 Nov 15 Jan 16 Mar 16 May 16 Jul 16 Sep 16 Nov 16 Jan 17 Mar 17 May 17 Jul 17 Leverage Increased Revenue We have scaled our supply function to achieve significant incremental net margin contribution Investment made in FY14 and FY15 to scale our supply function Direct contracting hotels performs ahead of expectations Future opportunities include: Product: Expand product offering to address long haul and luxury segments Exclusivity: See over Direct contracting - share of monthly arrivals FY14 to FY % 70.0% 60.0% 50.0% 40.0% 30.0% 20.0% 10.0% 0.0% 70% Investments made to technology to optimise point of sale margin Revenue per product type FY15 vs FY16 Hotels (3rd party) Hotels (direct contract) Transfers (direct contract) Flights Other 15

16 Sales Volume and Margin Opportunity Target exclusivity Driving an increasing % of exclusivity presents a huge margin opportunity Independent hoteliers want to spread their distribution Hotels: Incremental volume / margin opportunity B2B airlines need a distribution partner without aircraft We can drive incremental volume and higher margin at point of sale With exclusive programme of flying By driving UK OTA rate and total exclusivity in hotels HIGH >10% Total UK exclusivity TARGET AREA By ringfencing last room availability 10% UK OTA exclusivity Whilst maintaining a risk-free model Ringfenced last room availability 6% UK OTA rate exclusivity 3-4% Standard direct contracts disintermediate 3 rd parties LOW Long tail 3 rd party stock 16

17 Drive Efficient Market Share Growth Superior customer proposition delivers increased margins and fuels market share growth The business has historically invested c.50% of growing revenue in marketing to drive share Growing share cost effectively % 49.9% 50.7% 48.6% 44.7% Online Marketing spend as % of Revenue A multi-channel strategy supported by sophisticated in house bid modelling and attribution tool allows efficient share growth Advantage maintained through continued Investment into: Cross device attribution through login Econometric attribution of offline advertising Revenue per daily UV Marketing cost per daily UV EBITDA per daily UV Data management platform integration 0.00 FY12 FY13 FY14 FY15 FY16 % Revenue spent on online marketing monthly evolution 75% 70% FY14 FY15 FY16 65% 60% 55% 50% 45% 40% 35% Oct Nov Dec Jan Feb Mar Apr May Jun Jul Aug Sep 17

18 Strengthen Brand Continued investment offline has strengthened awareness of our brand FY16 offline campaign was fully national Prompted Brand Awareness FY13 to FY16 50% Repeat purchase volume and rates continues to increase 40% 30% 20% 10% 0% FEB '13 APR '14 DEC '14 FEB '15 DEC '15 FEB '16 First / All Mentions Beach Holidays Thomson 18% 31% Repeat booking volumes and % of overall business 160, , % 18.0% 25.6% 32.5% 37.1% Repeat as % of all bookings Thomas Cook On the Beach First Choice 16% 15% 19% 29% 120, ,000 80,000 60,000 58% CAGR Travel Republic First mention Low Cost Holidays All mentions 0% 10% 20% 30% 40% 50% 60% 40,000 20,000 0 FY12 FY13 FY14 FY15 FY16 13

19 Drive Operational Leverage We continue to drive further operational leverage of a lightweight cost base OTB fixed and variable cost per booking is well below tour operator competitors OTB fixed and variable costs as a % of revenue are reducing through operational leverage Fixed / Variable Cost Per Booking X OTB 8X OTB OTB TUI TC Fixed / Variable costs as % Revenue FY12 to FY % 20.00% 15.00% 10.00% 5.00% 0.00% FY12 FY13 FY14 FY15 FY16 19

20 Expand model internationally We remain encouraged with the improvement to KPIs being achieved in Sweden Sweden has the a number of characteristics which make it attractive for our international expansion Driving improvement in 3 KPIs will determine success in new source markets Our objective in Sweden remains to deliver a positive return within 3 years of launch Cost per UV FY16 YOY % FY15 FY16 Traffic and brand growth in Sweden FY16 YOY % 19.6% Branded share % 50% Brand UVs Non-Brand UVs 0 FY15 FY16 20

21 Summary & Outlook We have enjoyed a strong start to the new FY and performance is in line with the Board s expectations Structural Market Growth & Market Share Growth Addressable market growth with increasing online penetration Risk capacity in market being downsized Optimise Customer Proposition Continue to invest in our technology talent and infrastructure to out innovate the competition Leverage Revenue Target increasing % of direct supply and drive exclusivity Ringfence peak season capacity in key Western Mediterranean destinations Drive Efficient Share Growth & Strengthen Brand Increased offline investment to further drive brand awareness Auction dynamics have improved post LCTG failure Drive Operational Leverage & Expand Internationally Drive significant PBT growth in the UK Leverage capabilities to breakeven in Sweden and launch in Norway 21

22 Appendix

23 OTB history Passenger numbers Share of online short haul beach Technology team recruited, web development and support insourced, complete platform rebuild Investment to launch offline advertising and scale direct contracting nd round private equity investment 2015 Ebeach.se launched IPO 28 th September Drive flight and hotel exclusivity, grow offline share 17% 20% First version website launched, paid search visibility increased Executive and senior management team recruited CMO, CFO, CTO End 2011 Tech and MI platforms relaunched end % 16% Excess charter supply Growing online penetration Simple, outsourced DP technology ,000 passengers First round private equity investment 9% 13% FY04 FY05 FY06 FY07 FY08 FY09 FY10 FY11 FY12 FY13 FY14 FY15 FY16

24 Business Model (3 year CAGR) STRUCTURAL MARKET GROWTH & MARKET SHARE GROWTH ADDRESSABLE MARKET Short haul beach holidays dynamically packaged Online penetration OTB share of market traffic Unique visitors +15% OPTIMISE CUSTOMER PROPOSITION & LEVERAGE REVENUE Revenue per booking Conversion Revenue per unique visitor +7% +23% Revenue DRIVE EFFICIENT SHARE GROWTH & STRENGTHEN BRAND Unique visitors Marketing spend per unique visitor Marketing as % of Revenue -3% SCALE DRIVES OPERATIONAL LEVERAGE OTB s business model is centred on driving efficient growth in market share while maintaining and improving both conversion and revenue per booking Our strategic initiatives are focused on driving the performance of all of these levers EBITDA growth is the cumulative effect of improvements in performance of all of the levers individually Fixed and Variable Costs EBITDA -5% +27% 24

Customer returns from holiday These payments are held in")

25 Cash Flow Flow of funds On The Beach provides clear and comprehensive consumer protection The trust protects all customer payments until after the provision of holiday services Trust account funds flow for a 1,200 holiday Checkout stage Booking stage Immediately after booking Holiday build up Return date All customer receipts are paid into the trust account in full before the holiday departure date 600 Hotel ATOL Trust Fund (Protected) Customer returns from holiday These payments are held in the trust account until the service is provided On The Beach does not therefore use customer pre-payments to fund its business operations CUSTOMER 1,214.85* 550 Flights 50 Coach Transfer Customer Pays Deposit Receive flight balance 28 days post booking Receive full balance 14 days before departure If booked more than 45 days in advance of departure, customers can secure booking with a deposit which is a percentage of flight cost plus hotel deposit Transfer to On the Beach of flight sales value on receipt into trust from customer Transfer to On the Beach of flight sales value on receipt into trust from customer Transfer to On the Beach of balance of sales value OTB MPB SUPPLIER Airline paid in full by On the Beach on booking Hotel, Bed bank and ancillary supplier paid * 1,200 holiday for 2 people via low deposit scheme includes 2 bags and assumes a direct debit card fee each balance payment, so in the example it is paid three times 25

26 Cash Flow - Seasonality Peak booking trading period between January and June and travelled June and August Booked by month Revenue is recognised on a booked basis The period prior to Christmas is quiet, particularly November and December Traffic volumes ramp up immediately following Christmas as customers start to research and book their holidays for the following summer period Travelled by month Peak departure months are July and August Funds Flow Invest in marketing and low deposits to drive bookings but margin and cash are earned on a travelled basis % FY16 Booked by month 18.0% 15.5% 16.0% 14.0% 12.0% 11.1% 10.4% 10.0% 9.6% 10.0% 8.2% 8.1% 8.0% 7.2% 5.8% 5.6% 6.0% 4.3% 4.1% 4.0% 2.0% 0.0% Oct Nov Dec Jan Feb Mar Apr May Jun Jul Aug Sep % FY16 Travelled by month 18.0% 16.3% 16.0% 15.1% 13.8% 14.0% 12.1% 11.7% 12.0% 9.7% 10.0% 8.0% 7.2% 6.0% 4.8% 4.0% 2.4% 2.3% 2.7% 1.8% 2.0% 0.0% Oct Nov Dec Jan Feb Mar Apr May Jun Jul Aug Sep Source: Company Information 26

27 Millions Millions Cash Flow: Seasonality and cash profile Facility used to fund low deposits during peak trading periods between January and June /15 10/15 11/15 12/15 01/16 02/16 03/16 04/16 05/16 06/16 07/16 08/16 09/ Funding of Low Deposits FY16 Annual cash cycle sees investment into working capital as bookings are achieved in Jan - June, with cash unwinding from the trust as customers travel Facility available in FY16 was 35m, maximum drawdown was 13.5m Bank Balance Profile FY /15 10/15 11/15 12/15 01/16 02/16 03/16 04/16 05/16 06/16 07/16 08/16 09/ Source: Company Information 27

Strong Brands, Technology & Talent

Click to edit Strong Brands, Technology & Talent November 2017 Click Disclaimer to edit NOT FOR PUBLICATION OR DISTRIBUTION IN WHOLE OR IN PART IN, INTO OR FROM ANY JURISDICTION WHERE TO DO SO WOULD CONSTITUTE

Click to edit Strong Brands, Technology & Talent November 2017 Click Disclaimer to edit NOT FOR PUBLICATION OR DISTRIBUTION IN WHOLE OR IN PART IN, INTO OR FROM ANY JURISDICTION WHERE TO DO SO WOULD CONSTITUTE

2009 Full Year Result

2009 Full Year Result 23 February, 2010 Chief Executive Brendan Hopkins Chief Financial Officer Peter Myers Overview Result in line with guidance Strong cost outcome high operating leverage February/March

2009 Full Year Result 23 February, 2010 Chief Executive Brendan Hopkins Chief Financial Officer Peter Myers Overview Result in line with guidance Strong cost outcome high operating leverage February/March

For personal use only

For personal use only FIRST HALF RESULTS AND GUIDANCE UPDATE 31 Dec 2015 25/2/16 Brian Shanahan CEO and Co-Founder Deborah Kelly Group CFO Summary: Proforma First Half Results FY16 Temple & Webster is

For personal use only FIRST HALF RESULTS AND GUIDANCE UPDATE 31 Dec 2015 25/2/16 Brian Shanahan CEO and Co-Founder Deborah Kelly Group CFO Summary: Proforma First Half Results FY16 Temple & Webster is

Paddy Power Betfair plc Prelim Results

Paddy Power Betfair plc 2017 Prelim Results Overview 2 Observations Solid financial performance in 2017 Many important competitive advantages Merger integration successfully completed Sportsbet has an

Paddy Power Betfair plc 2017 Prelim Results Overview 2 Observations Solid financial performance in 2017 Many important competitive advantages Merger integration successfully completed Sportsbet has an

5 Star London Hotels - Example Report

5 Star London Hotels - Example Report January 2018 CONTENTS Your Benchmark Report Website Traffic Conversion Rates Ecommerce Performance AdWords Spend Your Traffic Index Your Conversion Rate Index Your

5 Star London Hotels - Example Report January 2018 CONTENTS Your Benchmark Report Website Traffic Conversion Rates Ecommerce Performance AdWords Spend Your Traffic Index Your Conversion Rate Index Your

WebBedsB2B Investor Day

WebBedsB2B Investor Day 22 November 2017 - Melbourne 23 November 2017 - Sydney Page 1 Agenda Page 2 1. What is the B2B market? 2. Strategy update 3. Business overview 1. WebBeds Europe 2. WebBeds Asia

WebBedsB2B Investor Day 22 November 2017 - Melbourne 23 November 2017 - Sydney Page 1 Agenda Page 2 1. What is the B2B market? 2. Strategy update 3. Business overview 1. WebBeds Europe 2. WebBeds Asia

Investor Presentation. June 2014

Investor Presentation June 2014 Safe Harbor Certain statements contained in this presentation are forward-looking statements within the meaning of the safe harbor provisions of the U.S. Private Securities

Investor Presentation June 2014 Safe Harbor Certain statements contained in this presentation are forward-looking statements within the meaning of the safe harbor provisions of the U.S. Private Securities

HOLIDAYCHECK GROUP COMPANY PRESENTATION

HOLIDAYCHECK GROUP COMPANY PRESENTATION Agenda 1 2 3 4 5 Who we are Drivers of growth Financials Outlook Appendix 2 Who we are 3 The HolidayCheck Group Four leading portals with a strategic focus on local

HOLIDAYCHECK GROUP COMPANY PRESENTATION Agenda 1 2 3 4 5 Who we are Drivers of growth Financials Outlook Appendix 2 Who we are 3 The HolidayCheck Group Four leading portals with a strategic focus on local

Producer of the ShopEasy Family of Technology Products

Shopping Solutions, Inc. (A fictitious Company) Improving the way people shop & consumer products are sold Producer of the Family of Technology Products Investor Briefing April 1 Our Leadership Team and

Shopping Solutions, Inc. (A fictitious Company) Improving the way people shop & consumer products are sold Producer of the Family of Technology Products Investor Briefing April 1 Our Leadership Team and

20m Customers. The World s Number One Integrated Tourism Group. 67,000 colleagues retail shops hotels. ships. 150 aircraft 14 cruise

1 The World s Number One Integrated Tourism Group Financial Results 2016 Turnover: 17.2bn Underlying EBITA: 1,001m Source Markets TUI are the market leader in all our major markets Germany UK Netherlands

1 The World s Number One Integrated Tourism Group Financial Results 2016 Turnover: 17.2bn Underlying EBITA: 1,001m Source Markets TUI are the market leader in all our major markets Germany UK Netherlands

JUNE 2017 QUARTERLY OPERATIONAL UPDATE: RECORD QUARTER AND STRONGEST CUSTOMER GROWTH SINCE IPO

ASX ANNOUNCEMENT 17 July 2017 JUNE 2017 QUARTERLY OPERATIONAL UPDATE: RECORD QUARTER AND STRONGEST CUSTOMER GROWTH SINCE IPO ChimpChange Limited (ASX: CCA) ( ChimpChange, or the Company ), Australia s

ASX ANNOUNCEMENT 17 July 2017 JUNE 2017 QUARTERLY OPERATIONAL UPDATE: RECORD QUARTER AND STRONGEST CUSTOMER GROWTH SINCE IPO ChimpChange Limited (ASX: CCA) ( ChimpChange, or the Company ), Australia s

France Telecom investor day, June 10th 2004: Building the integrated broadband communication services Group

1 France Telecom investor day, June 10th 2004: Building the integrated broadband communication services Group 2 FT Personal Strategy 3 FT / Orange Personal Strategy leveraging international assets portfolio

1 France Telecom investor day, June 10th 2004: Building the integrated broadband communication services Group 2 FT Personal Strategy 3 FT / Orange Personal Strategy leveraging international assets portfolio

Administration Division Public Works Department Anchorage: Performance. Value. Results.

Administration Division Anchorage: Performance. Value. Results. Mission Provide administrative, budgetary, fiscal, and personnel support to ensure departmental compliance with Municipal policies and procedures,

Administration Division Anchorage: Performance. Value. Results. Mission Provide administrative, budgetary, fiscal, and personnel support to ensure departmental compliance with Municipal policies and procedures,

Analyst and Investor Day Vodafone Italy

Analyst and Investor Day Vodafone Italy Margherita Della Valle, Chief Financial Officer 3 October 2006 This presentation does not constitute an offering of securities or otherwise constitute an invitation

Analyst and Investor Day Vodafone Italy Margherita Della Valle, Chief Financial Officer 3 October 2006 This presentation does not constitute an offering of securities or otherwise constitute an invitation

The ROI from Marketing to Existing Online Customers

The ROI from Marketing to Existing Online Customers Adobe Digital Index The ROI from Marketing to Existing Online Customers Table of contents 2: Executive summary 3: Introduction 3: Marketers budgets biased

The ROI from Marketing to Existing Online Customers Adobe Digital Index The ROI from Marketing to Existing Online Customers Table of contents 2: Executive summary 3: Introduction 3: Marketers budgets biased

Juan Asúa. General Manager Banking in Spain. Anticipating the new environment

Juan Asúa General Manager Banking in Spain Anticipating the new environment Index Excellent positioning: Customers and Products New environment, New opportunities Strategic Drivers: Innovation and Transformation

Juan Asúa General Manager Banking in Spain Anticipating the new environment Index Excellent positioning: Customers and Products New environment, New opportunities Strategic Drivers: Innovation and Transformation

Retail Digital Payments. August 2017

Retail Digital Payments August 2017 1 Safe Harbour Except for the historical information contained herein, statements in this release which contain words or phrases such as will, aim, will likely result,

Retail Digital Payments August 2017 1 Safe Harbour Except for the historical information contained herein, statements in this release which contain words or phrases such as will, aim, will likely result,

Preliminary results Year ended 31 January 2017

Insert Text Here Preliminary results Year ended 31 January 2017 28 March 2017 Forward-looking statements This presentation contains certain forward-looking statements with respect to the financial condition,

Insert Text Here Preliminary results Year ended 31 January 2017 28 March 2017 Forward-looking statements This presentation contains certain forward-looking statements with respect to the financial condition,

Predictive Conversations

Predictive Conversations Measuring Word of Mouth and Predicting Business Outcomes Ed Keller, CEO Rick Larkin, VP Analytics August 11, 2017 MASB Opening thoughts Intrinsically people know conversations

Predictive Conversations Measuring Word of Mouth and Predicting Business Outcomes Ed Keller, CEO Rick Larkin, VP Analytics August 11, 2017 MASB Opening thoughts Intrinsically people know conversations

Investors Day. Mittelstand Bank: An increasing source of profit

Investors Day Mittelstand Bank: An increasing source of profit Frankfurt, 14.09.2005 Martin Blessing Good start H1 2005 results 1. 2. 3. 4. Agenda 1. 2. 3. 4. Good start for the new Mittelstand Bank segment

Investors Day Mittelstand Bank: An increasing source of profit Frankfurt, 14.09.2005 Martin Blessing Good start H1 2005 results 1. 2. 3. 4. Agenda 1. 2. 3. 4. Good start for the new Mittelstand Bank segment

For personal use only DRAFT

DRAFT We ve had a good year here s our F17 financial result 1 Operating EBITDA and Operating NPAT exclude one-off non operating items of $1.4m in F17 ($8.1m in F16). Reported NPAT is $94m, which is up

DRAFT We ve had a good year here s our F17 financial result 1 Operating EBITDA and Operating NPAT exclude one-off non operating items of $1.4m in F17 ($8.1m in F16). Reported NPAT is $94m, which is up

microgen plc Audited Preliminary Results for the year ended 31 December 2015

microgen plc Audited Preliminary Results for the year ended 31 December 2015 To be read in conjunction with the audited preliminary results announcement released on 3 March 2016 1 Group Overview Across

microgen plc Audited Preliminary Results for the year ended 31 December 2015 To be read in conjunction with the audited preliminary results announcement released on 3 March 2016 1 Group Overview Across

Yatra s Fiscal First Quarter 2018 Financial Results Conference Call Prepared Remarks

Yatra s Fiscal First Quarter 2018 Financial Results Conference Call Prepared Remarks Manish Hemrajani: Thank you, Good morning everyone. Welcome to Yatra s Fiscal First Quarter 2018 financial results for

Yatra s Fiscal First Quarter 2018 Financial Results Conference Call Prepared Remarks Manish Hemrajani: Thank you, Good morning everyone. Welcome to Yatra s Fiscal First Quarter 2018 financial results for

COMPANY PROFILE 2016

COMPANY PROFILE 2016 takasolutions upgrades buildings to reduce the energy, water and costs at no expense to the owner while sharing the savings. TARGET CLIENTS THE CONCEPT Clients and buildings that are

COMPANY PROFILE 2016 takasolutions upgrades buildings to reduce the energy, water and costs at no expense to the owner while sharing the savings. TARGET CLIENTS THE CONCEPT Clients and buildings that are

Integrating Energy Efficiency and Demand Response

Integrating Energy Efficiency and Demand Response Energy Efficiency and Active Demand Management Colleen M. Snee, Director - Integrated Demand Resources Johnson Controls, Inc. ACEEE Energy Efficiency as

Integrating Energy Efficiency and Demand Response Energy Efficiency and Active Demand Management Colleen M. Snee, Director - Integrated Demand Resources Johnson Controls, Inc. ACEEE Energy Efficiency as

Berendsen plc. Timetable

Timetable 14:00 14:10 Trading Update & Q&A 14:10 15:20 Group Strategy Update & Q&A 15:20 15:30 Break 15:30 17:20 Breakout session by Business Line Workwear Facility Cleanroom Mats Washroom Hospitality

Timetable 14:00 14:10 Trading Update & Q&A 14:10 15:20 Group Strategy Update & Q&A 15:20 15:30 Break 15:30 17:20 Breakout session by Business Line Workwear Facility Cleanroom Mats Washroom Hospitality

BUSINESS PLAN COVER PAGE

BUSINESS PLAN COVER PAGE OWNERS Your Business Name Street Address City, State ZIP Code E-Mail Telephone Table of Contents EXECUTIVE SUMMARY... 1 BUSINESS DESCRIPTION... 2 Overview... 2 Targeted Market

BUSINESS PLAN COVER PAGE OWNERS Your Business Name Street Address City, State ZIP Code E-Mail Telephone Table of Contents EXECUTIVE SUMMARY... 1 BUSINESS DESCRIPTION... 2 Overview... 2 Targeted Market

SMALL CAP Italiana 29th November Speaker: Simone Ranucci Brandimarte, Chairman

SMALL CAP CONFERENCE @Borsa Italiana 29th November 2016 Speaker: Simone Ranucci Brandimarte, Chairman Nov 2015 Apr 2007 DigiTouch set up Jan 2009 DigiTouch becomes member of IAB Italia Nov 2009 DigiTouch

SMALL CAP CONFERENCE @Borsa Italiana 29th November 2016 Speaker: Simone Ranucci Brandimarte, Chairman Nov 2015 Apr 2007 DigiTouch set up Jan 2009 DigiTouch becomes member of IAB Italia Nov 2009 DigiTouch

Welcome to the Annual General Meeting 2014 of the Nemetschek AG. Munich, May 20, 2014, Conference Center Munich at the Hanns-Seidel-Stiftung

Welcome to the Annual General Meeting 2014 of the Nemetschek AG Munich, May 20, 2014, Conference Center Munich at the Hanns-Seidel-Stiftung Annual General Meeting 2014 Kurt Dobitsch, Chairman of the Supervisory

Welcome to the Annual General Meeting 2014 of the Nemetschek AG Munich, May 20, 2014, Conference Center Munich at the Hanns-Seidel-Stiftung Annual General Meeting 2014 Kurt Dobitsch, Chairman of the Supervisory

Electric Forward Market Report

Mar-01 Mar-02 Jun-02 Sep-02 Dec-02 Mar-03 Jun-03 Sep-03 Dec-03 Mar-04 Jun-04 Sep-04 Dec-04 Mar-05 May-05 Aug-05 Nov-05 Feb-06 Jun-06 Sep-06 Dec-06 Mar-07 Jun-07 Sep-07 Dec-07 Apr-08 Jun-08 Sep-08 Dec-08

Mar-01 Mar-02 Jun-02 Sep-02 Dec-02 Mar-03 Jun-03 Sep-03 Dec-03 Mar-04 Jun-04 Sep-04 Dec-04 Mar-05 May-05 Aug-05 Nov-05 Feb-06 Jun-06 Sep-06 Dec-06 Mar-07 Jun-07 Sep-07 Dec-07 Apr-08 Jun-08 Sep-08 Dec-08

FERRY SHIPPING AND LOGISTICS. DFDS Group Overview

FERRY SHIPPING AND LOGISTICS DFDS Group Overview September 2017 Disclaimer The statements about the future in this announcement contain risks and uncertainties. This entails that actual developments may

FERRY SHIPPING AND LOGISTICS DFDS Group Overview September 2017 Disclaimer The statements about the future in this announcement contain risks and uncertainties. This entails that actual developments may

German Equity Forum 2014

SNP Schneider-Neureither & Partner AG German Equity Forum 2014 25. - 26. November 2014 Dr. Andreas Schneider-Neureither, CEO Jörg Vierfuß, CFO German Equity Forum 2014 2 Agenda 1 Executive summary 2 Business

SNP Schneider-Neureither & Partner AG German Equity Forum 2014 25. - 26. November 2014 Dr. Andreas Schneider-Neureither, CEO Jörg Vierfuß, CFO German Equity Forum 2014 2 Agenda 1 Executive summary 2 Business

Panalpina a leading global Supply Chain Management company

Geneva, 22 nd September 2009 Panalpina a leading global Supply Chain Management company 22 nd September 2009 2 Panalpina at a glance Comprehensive global network Worldwide no. 3 in Air freight, no. 4 in

Geneva, 22 nd September 2009 Panalpina a leading global Supply Chain Management company 22 nd September 2009 2 Panalpina at a glance Comprehensive global network Worldwide no. 3 in Air freight, no. 4 in

For personal use only

FY16 Cash NPAT update and Strategy briefing 31 May 2016 A briefing will occur today at 9:30am AEST; refer to FlexiGroup website for webcast details Where we are now Focusing on our core (high ROE) business

FY16 Cash NPAT update and Strategy briefing 31 May 2016 A briefing will occur today at 9:30am AEST; refer to FlexiGroup website for webcast details Where we are now Focusing on our core (high ROE) business

Results 2Q15_. Investor Relations Telefônica Brasil S.A. July, Investor Relations Telefônica Brasil S.A.

Results _ July, 2015. Disclaimer For the first time, in this quarter we are presenting pro forma numbers combining Telefônica Brasil and GVT results for all financial and operational indicators. For a

Results _ July, 2015. Disclaimer For the first time, in this quarter we are presenting pro forma numbers combining Telefônica Brasil and GVT results for all financial and operational indicators. For a

INTERIM RESULTS. 6 months to 30 th June 2017

INTERIM RESULTS 6 months to 30 th June 2017 AGENDA Business overview Financial performance A revitalised, repositioned & repurposed B2B business Summary 2 BUSINESS OVERVIEW FINANCIAL HIGHLIGHTS Underlying

INTERIM RESULTS 6 months to 30 th June 2017 AGENDA Business overview Financial performance A revitalised, repositioned & repurposed B2B business Summary 2 BUSINESS OVERVIEW FINANCIAL HIGHLIGHTS Underlying

MakeMyTrip Limited (NASDAQ: MMYT) Investor Presentation November 2017

Investor Presentation November 2017") MakeMyTrip Limited (NASDAQ: MMYT) Investor Presentation November 2017 Safe Harbor Certain statements contained in this presentation are forward-looking statements within the meaning of the safe harbor

MakeMyTrip Limited (NASDAQ: MMYT) Investor Presentation November 2017 Safe Harbor Certain statements contained in this presentation are forward-looking statements within the meaning of the safe harbor

DR. MARKUS BRAUN CEO, CTO

DR. MARKUS BRAUN CEO, CTO TO OUR SHAREHOLDERS LETTER FROM THE CEO Letter from the CEO Dear ladies and gentlemen, Dear shareholders, Wirecard AG was able to report a successful 2014 fiscal year. Transaction

DR. MARKUS BRAUN CEO, CTO TO OUR SHAREHOLDERS LETTER FROM THE CEO Letter from the CEO Dear ladies and gentlemen, Dear shareholders, Wirecard AG was able to report a successful 2014 fiscal year. Transaction

Directions EMEA Connected InNAVation! Mannheim, Germany, October 5-7, 2015.

Directions EMEA 2015 Connected InNAVation! Mannheim, Germany, October 5-7, 2015. George Brown Founded Salesworks 1986 Started working with Navision in Denmark in 1997 Developed OnTarget Methodology Marketing

Directions EMEA 2015 Connected InNAVation! Mannheim, Germany, October 5-7, 2015. George Brown Founded Salesworks 1986 Started working with Navision in Denmark in 1997 Developed OnTarget Methodology Marketing

BRANDED GOODS CONFERENCE. September,

BRANDED GOODS CONFERENCE September, 15 2016 THE BRAND FACTS 69.3 million turnover in FY 2015-16, up 3.1% 3.88 million net profit in FY 2015-16 37% generated by DOS, 63% by wholesale 100 free-standing stores

BRANDED GOODS CONFERENCE September, 15 2016 THE BRAND FACTS 69.3 million turnover in FY 2015-16, up 3.1% 3.88 million net profit in FY 2015-16 37% generated by DOS, 63% by wholesale 100 free-standing stores

Tradedoubler. Interim report January-September 2015 Stockholm, 12 November 2015

Tradedoubler Interim report January-September 2015 Stockholm, 12 November 2015 1 CEO comment In the third quarter we saw good financial results in some markets while others were more challenging. We are

Tradedoubler Interim report January-September 2015 Stockholm, 12 November 2015 1 CEO comment In the third quarter we saw good financial results in some markets while others were more challenging. We are

New Higg.org Platform Training. Understanding and Navigating the new platform

New Higg.org Platform Training Understanding and Navigating the new platform Sustainable Apparel Coalition 1 Attendees are all muted. Please type your questions into the Q&A box in the top left side of

New Higg.org Platform Training Understanding and Navigating the new platform Sustainable Apparel Coalition 1 Attendees are all muted. Please type your questions into the Q&A box in the top left side of

Investor Presentation

Investor Presentation As of August 2, 2017 Advanced Signal Processing Products Safe Harbor Statement Except for historical information contained herein, the matters set forth in this presentation contain

Investor Presentation As of August 2, 2017 Advanced Signal Processing Products Safe Harbor Statement Except for historical information contained herein, the matters set forth in this presentation contain

Aerolabs. E-commerce platform

Aerolabs E-commerce platform Aerolabs Key products A-Data A- Loyalty A- Check -in e-aero Data Base, firewall and integration Gateway Members Area Platform with customers profiles Online check-in system

Aerolabs E-commerce platform Aerolabs Key products A-Data A- Loyalty A- Check -in e-aero Data Base, firewall and integration Gateway Members Area Platform with customers profiles Online check-in system

Extreme Agile Implementation and Creating a Value Delivery Office

Extreme Agile Implementation and Creating a Value Delivery Office Anup Deshpande Sr. Leader of Agile Portfolio Management 1 COPYRIGHT 2017 Anup Deshpande. ALL RIGHTS RESERVED For Informational Purposes

Extreme Agile Implementation and Creating a Value Delivery Office Anup Deshpande Sr. Leader of Agile Portfolio Management 1 COPYRIGHT 2017 Anup Deshpande. ALL RIGHTS RESERVED For Informational Purposes

Creating Customized Solutions

Creating Customized Solutions We Work Collaboratively to Deliver High-Impact Results Kelley Blue Book partners with advertisers to create tailor-made products and campaigns that meet unique goals and objectives

Creating Customized Solutions We Work Collaboratively to Deliver High-Impact Results Kelley Blue Book partners with advertisers to create tailor-made products and campaigns that meet unique goals and objectives

ZETES FINANCIAL RESULTS Alain Wirtz - CEO Pierre Lambert - CFO

ZETES FINANCIAL RESULTS 2015 Alain Wirtz - CEO Pierre Lambert - CFO AGENDA 1. Zetes at a glance 2. Goods ID 3. People ID 4. Financial results 5. Outlook 2 ZETES AT A GLANCE MAIN MARKET DRIVERS Search for

ZETES FINANCIAL RESULTS 2015 Alain Wirtz - CEO Pierre Lambert - CFO AGENDA 1. Zetes at a glance 2. Goods ID 3. People ID 4. Financial results 5. Outlook 2 ZETES AT A GLANCE MAIN MARKET DRIVERS Search for

Financial Results for the Fiscal Year Ended December 31, 2017

OUTSOURCING Inc. (Securities Code: 2427/TSE 1st Section) Financial Results for the Fiscal Year Ended December 31, 2017 February 2018 Contents P. 2 Consolidated Financial Results for FY12/17 (IFRS) P. 20

OUTSOURCING Inc. (Securities Code: 2427/TSE 1st Section) Financial Results for the Fiscal Year Ended December 31, 2017 February 2018 Contents P. 2 Consolidated Financial Results for FY12/17 (IFRS) P. 20

% Change. Total. Total Retail Sales Index* Estimate ($M)

") Index % Change RETAIL SALES INDEX RETAIL SALES ROSE 2.6 PER CENT The total retail sales index was 2.6 per cent higher than the level reached in January. Building material stores recorded the largest growth

Index % Change RETAIL SALES INDEX RETAIL SALES ROSE 2.6 PER CENT The total retail sales index was 2.6 per cent higher than the level reached in January. Building material stores recorded the largest growth

Redefining Travel Commerce. Bernstein Strategic Decisions Conference 2016

Redefining Travel Commerce Bernstein Strategic Decisions Conference 2016 Disclaimers Related to Forward-Looking Statements Certain items in this presentation and in today s discussion, including matters

Redefining Travel Commerce Bernstein Strategic Decisions Conference 2016 Disclaimers Related to Forward-Looking Statements Certain items in this presentation and in today s discussion, including matters

Third Quarter 2017 Conference Call

Third Quarter 2017 Conference Call October 24, 2017 Forward-Looking Statements This presentation contains forward-looking statements. Actual results may differ materially from results anticipated in the

Third Quarter 2017 Conference Call October 24, 2017 Forward-Looking Statements This presentation contains forward-looking statements. Actual results may differ materially from results anticipated in the

Metro Division Strategy Update. Macquarie Online Conference - November 2012

Metro Division Strategy Update Macquarie Online Conference - November 2012 Our strategy is to transform Fairfax from a print classifieds model to a multi platform business We are conducting this transformation

Metro Division Strategy Update Macquarie Online Conference - November 2012 Our strategy is to transform Fairfax from a print classifieds model to a multi platform business We are conducting this transformation

Results for Q3 FY14 Ended December 31, 2014 (Financial version)

") Results for FY14 Ended December 31, 2014 (Financial version) Net One Systems Co., Ltd. TSE : 7518 Contents 1 Q1-3 FY14 (Apr-Dec 9months) P. 1-7 2 FY14 (Oct-Dec 3months) P. 8-11 3 Outlook of Consolidated

Results for FY14 Ended December 31, 2014 (Financial version) Net One Systems Co., Ltd. TSE : 7518 Contents 1 Q1-3 FY14 (Apr-Dec 9months) P. 1-7 2 FY14 (Oct-Dec 3months) P. 8-11 3 Outlook of Consolidated

European Freight Forwarding Index

European Freight Forwarding Index 1 February 1 Sentiment is improving in the freight market Johannes Møller joml@danskebank.dk +45 45 12 36 Main conclusion from survey Our proprietary European Freight

European Freight Forwarding Index 1 February 1 Sentiment is improving in the freight market Johannes Møller joml@danskebank.dk +45 45 12 36 Main conclusion from survey Our proprietary European Freight

QIAGEN - Financials. Roland Sackers Chief Financial Officer. Sample & Assay Technologies -1- QIAGEN Analyst and Investor Day, February 14, 2008

QIAGEN - Financials -1- Roland Sackers Chief Financial Officer Forward Looking Statements Safe Harbor Statement: Certain of the statements contained in this presentation may be considered forward-looking

QIAGEN - Financials -1- Roland Sackers Chief Financial Officer Forward Looking Statements Safe Harbor Statement: Certain of the statements contained in this presentation may be considered forward-looking

Optimal Pricing & Market Positioning. Innovations in RM to maximise sales & optimise revenue

Optimal Pricing & Market Positioning Innovations in RM to maximise sales & optimise revenue Starting off on the right path Setting off on the right path Copyr i g ht 2013, SAS Ins titut e Inc. All rights

Optimal Pricing & Market Positioning Innovations in RM to maximise sales & optimise revenue Starting off on the right path Setting off on the right path Copyr i g ht 2013, SAS Ins titut e Inc. All rights

SEPA Direct Debits indicator evolution (Spanish basic indicator vs Euro area)

") Payment Systems Department Settlement Systems Analysis Division STATISTICS SEPA INDICATORS 100,00% 90,00% 80,00% 70,00% 60,00% 50,00% 40,00% 30,00% 20,00% 10,00% 0,00% SEPA Direct Debits indicator evolution

Payment Systems Department Settlement Systems Analysis Division STATISTICS SEPA INDICATORS 100,00% 90,00% 80,00% 70,00% 60,00% 50,00% 40,00% 30,00% 20,00% 10,00% 0,00% SEPA Direct Debits indicator evolution

Organic Produce. Data Ending 28 th February 16

Organic Produce Data Ending 28 th February 16 SUMMARY In the latest quarter Organic Produce has reached its highest level in both Value and Volume, following an overall strong 2015. During 2015 Organic

Organic Produce Data Ending 28 th February 16 SUMMARY In the latest quarter Organic Produce has reached its highest level in both Value and Volume, following an overall strong 2015. During 2015 Organic

Custom Benchmarking Report for Mobile Money. Anonymised version Dummy Data March 2017

Custom Benchmarking Report for Mobile Money Anonymised version Dummy Data March 2017 Analysis is based on 100+ mobile money providers who participated in the 2016 Global Annual Adoption survey Europe &

Custom Benchmarking Report for Mobile Money Anonymised version Dummy Data March 2017 Analysis is based on 100+ mobile money providers who participated in the 2016 Global Annual Adoption survey Europe &

Investor presentation

Investor presentation May 2007 REVIEW OF 2006: REVENUE AND PROFIT CONTRIBUTORS Revenue structure EBIT structure Outdoor +20 mln Internet Radio 50-7 mln Metro Radio Outdoor 40 Agora Group Magazines +10

Investor presentation May 2007 REVIEW OF 2006: REVENUE AND PROFIT CONTRIBUTORS Revenue structure EBIT structure Outdoor +20 mln Internet Radio 50-7 mln Metro Radio Outdoor 40 Agora Group Magazines +10

For personal use only

DateTix Group Ltd (ASX:DTX) 25 January 2017 DateTix Group revenue up 43% quarter-on-quarter Revenue of $484,000 for the quarter, +43% quarter-on-quarter growth o Revenue of $268,000 in Hong Kong, +115%

DateTix Group Ltd (ASX:DTX) 25 January 2017 DateTix Group revenue up 43% quarter-on-quarter Revenue of $484,000 for the quarter, +43% quarter-on-quarter growth o Revenue of $268,000 in Hong Kong, +115%

Q SOCIAL TRENDS REPORT

Q4 2015 SOCIAL TRENDS REPORT WWW.KINETICSOCIAL.COM Q4 Topline Summary Q4 is an exciting time of year in the advertising space. The speed of work picks up significantly as brands clamor for share of wallet

Q4 2015 SOCIAL TRENDS REPORT WWW.KINETICSOCIAL.COM Q4 Topline Summary Q4 is an exciting time of year in the advertising space. The speed of work picks up significantly as brands clamor for share of wallet

Set to be the leading digital omni-channel bank

Set to be the leading digital omni-channel bank AGENDA Business model and key success factors Key highlights of 2013-16 Business Plan Closing remarks 82 BACK IN 2008 LAUNCHING ANOTHER ME TOO BANK WOULD

Set to be the leading digital omni-channel bank AGENDA Business model and key success factors Key highlights of 2013-16 Business Plan Closing remarks 82 BACK IN 2008 LAUNCHING ANOTHER ME TOO BANK WOULD

XING AG. Dr. Stefan Gross-Selbeck (CEO) & Ingo Chu (CFO) Hamburg, May 12, 2010

& Ingo Chu (CFO) Hamburg, May 12, 2010") Q1 Results Presentation XING AG Dr. Stefan Gross-Selbeck (CEO) & Ingo Chu (CFO) Hamburg, May 12, 2010 01 Starting Position Recap from FY 2009 results presentation... 2010: The year of profitable growth...

Q1 Results Presentation XING AG Dr. Stefan Gross-Selbeck (CEO) & Ingo Chu (CFO) Hamburg, May 12, 2010 01 Starting Position Recap from FY 2009 results presentation... 2010: The year of profitable growth...

For personal use only

ASX Announcement December Quarter Review Cash receipts for the quarter were $2,632,655 Receivables relating to work completed during the quarter were approximately $123,500, with payments expected to be

ASX Announcement December Quarter Review Cash receipts for the quarter were $2,632,655 Receivables relating to work completed during the quarter were approximately $123,500, with payments expected to be

Harmony Home Control Logitech Analyst & Investor Day. Bruce Lancaster 11 March 2015

Harmony Home Control Logitech Analyst & Investor Day Bruce Lancaster 11 March 2015 1 Forward Looking Statements This presentation contains forward-looking statements within the meaning of the U.S. federal

Harmony Home Control Logitech Analyst & Investor Day Bruce Lancaster 11 March 2015 1 Forward Looking Statements This presentation contains forward-looking statements within the meaning of the U.S. federal

Recommended acquisition of The BSS Group plc. 5 July 2010

Recommended acquisition of The BSS Group plc 5 July 2010 Important information This document is being made available only to persons who fall within the exemptions contained in Article 19 and Article 49

Recommended acquisition of The BSS Group plc 5 July 2010 Important information This document is being made available only to persons who fall within the exemptions contained in Article 19 and Article 49

2016 half year results August 10 th 2016

2016 half year results August 10 th 2016 HALF YEAR RESULTS 2016 1 Certain statements in this document are forward looking statements. These forward looking statements speak only as at the date of this

2016 half year results August 10 th 2016 HALF YEAR RESULTS 2016 1 Certain statements in this document are forward looking statements. These forward looking statements speak only as at the date of this

GLOSSARY OF SALES TERMS

Accommodation Marketing Consortia: Commonly representing luxury hotels / heritage and exclusive accommodations. Examples from international markets include; Preferred Hotels, Leading Hotels, Design Hotels.

Accommodation Marketing Consortia: Commonly representing luxury hotels / heritage and exclusive accommodations. Examples from international markets include; Preferred Hotels, Leading Hotels, Design Hotels.

REDBUBBLE INVESTMENT OVERVIEW

REDBUBBLE INVESTMENT OVERVIEW 18 May 2016 RB: A creative marketplace As a marketplace RB has strong, reinforcing growth ARTISTS CUSTOMERS CONTENT 399,000 1.25M 1H FY16 9.8M 3 rd PARTY FULFILLERS 12 FULFILLERS,

REDBUBBLE INVESTMENT OVERVIEW 18 May 2016 RB: A creative marketplace As a marketplace RB has strong, reinforcing growth ARTISTS CUSTOMERS CONTENT 399,000 1.25M 1H FY16 9.8M 3 rd PARTY FULFILLERS 12 FULFILLERS,

German Corporate Conference // Kepler Cheuvreux HUGO BOSS Company Presentation. Mark Langer, CFO January 20, 2016

HUGO BOSS Company Presentation Mark Langer, CFO January 20, 2016 2 Agenda Group strategy update Omnichannel strategy Financial outlook and summary 3 Agenda Group strategy update Omnichannel strategy Financial

HUGO BOSS Company Presentation Mark Langer, CFO January 20, 2016 2 Agenda Group strategy update Omnichannel strategy Financial outlook and summary 3 Agenda Group strategy update Omnichannel strategy Financial

Aristocrat Leisure Limited Acquisition of Plarium Global Limited. 10 August 2017

Aristocrat Leisure Limited Acquisition of Plarium Global Limited 10 August 2017 Disclaimer This document and any oral presentation accompanying it has been prepared in good faith, however, no express or

Aristocrat Leisure Limited Acquisition of Plarium Global Limited 10 August 2017 Disclaimer This document and any oral presentation accompanying it has been prepared in good faith, however, no express or

Good morning everyone. I m Julia Sattel, Senior Vice President of Airline IT. It sapleasuretobehere.

Good morning everyone I m Julia Sattel, Senior Vice President of Airline IT. It sapleasuretobehere. This morning both Luis and Holger have described a growing airline industry which is becoming increasingly

Good morning everyone I m Julia Sattel, Senior Vice President of Airline IT. It sapleasuretobehere. This morning both Luis and Holger have described a growing airline industry which is becoming increasingly

Vivo Investor Day Unique combination of Value and Growth

Vivo Investor Day Unique combination of Value and Growth Eduardo Navarro CEO New York March 12 th 2018 Disclaimer This presentation may contain forwardlooking statements concerning future prospects and

Vivo Investor Day Unique combination of Value and Growth Eduardo Navarro CEO New York March 12 th 2018 Disclaimer This presentation may contain forwardlooking statements concerning future prospects and

2015 China Marketing Plan. Presented by Brenda He

2015 China Marketing Plan Presented by Brenda He Today s Agenda Who are the Chinese tourists likely to come to Hawai i? What How do they want in their Hawai i experience? are we doing in 2014? 2015 Strategies

2015 China Marketing Plan Presented by Brenda He Today s Agenda Who are the Chinese tourists likely to come to Hawai i? What How do they want in their Hawai i experience? are we doing in 2014? 2015 Strategies

2009 Full Year Results. September, 2009

2009 Full Year Results September, 2009 Doug Rathbone Managing Director 2009 Full Year results A challenging year Glyphosate profit impact was substantial Credit related pressures in Brazil Non-glyphosate

2009 Full Year Results September, 2009 Doug Rathbone Managing Director 2009 Full Year results A challenging year Glyphosate profit impact was substantial Credit related pressures in Brazil Non-glyphosate

*Only these positions earn points for reward dollars. Parts Managers are not eligible for these promotions. New Mechanical customer acquisition

Page 1 Parts Consultants Performance Points = CASH is a comprehensive incentive program based upon your dealership s After Sales performance. Simply put, AIM rewards you for growing your service and parts

Page 1 Parts Consultants Performance Points = CASH is a comprehensive incentive program based upon your dealership s After Sales performance. Simply put, AIM rewards you for growing your service and parts

TCS Financial Results

TCS Financial Results Quarter I FY 2017-18 July 13, 2017 1 Copyright 2017 Tata Consultancy Services Limited Disclaimer Certain statements in this release concerning our future prospects are forward-looking

TCS Financial Results Quarter I FY 2017-18 July 13, 2017 1 Copyright 2017 Tata Consultancy Services Limited Disclaimer Certain statements in this release concerning our future prospects are forward-looking

Creating Unique Data Assets to Drive Marketing Predictions and Actions. The Second-Party Data Advantage

Creating Unique Data Assets to Drive Marketing Predictions and Actions The Second-Party Data Advantage 1 Industry Trends The second-party data movement has quickly emerged as an innovative solution for

Creating Unique Data Assets to Drive Marketing Predictions and Actions The Second-Party Data Advantage 1 Industry Trends The second-party data movement has quickly emerged as an innovative solution for

Topic 5 External Factors. Higher Business Management

Topic 5 External Factors Higher Business Management 1 Learning Intentions / Success Criteria Learning Intentions External factors Success Criteria Learners should be aware of the impact that external factors

Topic 5 External Factors Higher Business Management 1 Learning Intentions / Success Criteria Learning Intentions External factors Success Criteria Learners should be aware of the impact that external factors

It s been a good six months.

DRAFT It s been a good six months. Revenue growth was driven by the excellent performance of our classified businesses particularly Motors and Jobs Total expenses increased 9% due to headcount growth and

DRAFT It s been a good six months. Revenue growth was driven by the excellent performance of our classified businesses particularly Motors and Jobs Total expenses increased 9% due to headcount growth and

! "#$$%& MY BLOG 2014

!"#%& 2014 =/*55&- 789:/4; RESOLUNTIONS!"# 20(5< SMART GOAL: GOAL: GOAL: GOAL: Often people set resolutions and don t look at them again after the month of January. One way to make sure that you are actively

!"#%& 2014 =/*55&- 789:/4; RESOLUNTIONS!"# 20(5< SMART GOAL: GOAL: GOAL: GOAL: Often people set resolutions and don t look at them again after the month of January. One way to make sure that you are actively

Organic revenue growth in H1 2018

2 Preliminary results 2017 Continued delivery against strategy geographic expansion, product innovation and partnership development Completed Comapi acquisition - facilitating shift to omnichannel offering

2 Preliminary results 2017 Continued delivery against strategy geographic expansion, product innovation and partnership development Completed Comapi acquisition - facilitating shift to omnichannel offering

Official Visitor Guide Four Edition Media Kit 2016 /17 OFFICIAL VISITOR GUIDE FOUR EDITION MEDIA KIT 1

Official Visitor Guide Four Edition Media Kit 2016 /17 OFFICIAL VISITOR GUIDE FOUR EDITION MEDIA KIT 1 Overview The one and only official visitor guide to Melbourne. The Official Visitor Guide (OVG) is

Official Visitor Guide Four Edition Media Kit 2016 /17 OFFICIAL VISITOR GUIDE FOUR EDITION MEDIA KIT 1 Overview The one and only official visitor guide to Melbourne. The Official Visitor Guide (OVG) is

Kingston Hospital NHS Foundation Trust Recovery Plan Update. Trust Board Meeting 29 th July 2015

Kingston Hospital NHS Foundation Trust Recovery Plan Update Trust Board Meeting 29 th July 2015 Summary We have been through a robust process to set the plan and have subsequently focused on further actions

Kingston Hospital NHS Foundation Trust Recovery Plan Update Trust Board Meeting 29 th July 2015 Summary We have been through a robust process to set the plan and have subsequently focused on further actions

Corporate Presentation

Corporate Presentation November 2017 THE FUTURE OF TRUCKING Company Overview Leading Technology Transportation Company Value Proposition & Business Description Technology is transforming the transportation

Corporate Presentation November 2017 THE FUTURE OF TRUCKING Company Overview Leading Technology Transportation Company Value Proposition & Business Description Technology is transforming the transportation

Improve Engagement by Driving a Development Culture

Improve Engagement by Driving a Development Culture Amy Freshman Sr. Director, Global Workforce Enablement - ADP Sandy Thomas Sr. Director, Global Talent and Development - ADP Thank You for Joining Us!!!

Improve Engagement by Driving a Development Culture Amy Freshman Sr. Director, Global Workforce Enablement - ADP Sandy Thomas Sr. Director, Global Talent and Development - ADP Thank You for Joining Us!!!

Unilever Investor Event 2017 Graeme Pitkethly 29 th November 2017

Unilever Investor Event 2017 Graeme Pitkethly 29 th November 2017 What you have heard so far Driving growth in each Category Fuelling growth and margin expansion Personal Care Home Care Foods & Refreshment

Unilever Investor Event 2017 Graeme Pitkethly 29 th November 2017 What you have heard so far Driving growth in each Category Fuelling growth and margin expansion Personal Care Home Care Foods & Refreshment

Accelerating innovation and growth

Accelerating innovation and growth November 2017 Financial facts Customer sales in 2016: EUR 1 493 million Adjusted *) EBIT margin: 10.2% Tieto s market position: Market leader in Finland Among top 3 in

Accelerating innovation and growth November 2017 Financial facts Customer sales in 2016: EUR 1 493 million Adjusted *) EBIT margin: 10.2% Tieto s market position: Market leader in Finland Among top 3 in

FACEBOOK USER-GENERATED CONTENT (UGC) BENCHMARK REPORT

BENCHMARK REPORT") FACEBOOK USER-GENERATED CONTENT (UGC) BENCHMARK REPORT PUBLISHED: FEBRUARY 13, 2017 2 TABLE OF CONTENTS Executive Summary Introduction Methodology 2016 Trends UGC Benchmarks 2017 Opportunities Contact

FACEBOOK USER-GENERATED CONTENT (UGC) BENCHMARK REPORT PUBLISHED: FEBRUARY 13, 2017 2 TABLE OF CONTENTS Executive Summary Introduction Methodology 2016 Trends UGC Benchmarks 2017 Opportunities Contact

Institutional Presentation. May 2016

Institutional Presentation May 2016 Section 1 Unidas At a Glance Unidas At a Glance 3 rd largest Brazilian car rental company by total fleet, with nationwide operations in fleet management solutions, car

Institutional Presentation May 2016 Section 1 Unidas At a Glance Unidas At a Glance 3 rd largest Brazilian car rental company by total fleet, with nationwide operations in fleet management solutions, car

MAKING M&S SPECIAL HALF YEAR RESULTS 8 NOVEMBER 2017

MAKING M&S SPECIAL HALF YEAR RESULTS 8 NOVEMBER 2017 FINANCIAL HEADLINES Group Revenue 5.1bn +2.6% Profit before tax 118.3m +371.3% Profit before tax & adjusted items 219.1m -5.3% Free cash flow before

MAKING M&S SPECIAL HALF YEAR RESULTS 8 NOVEMBER 2017 FINANCIAL HEADLINES Group Revenue 5.1bn +2.6% Profit before tax 118.3m +371.3% Profit before tax & adjusted items 219.1m -5.3% Free cash flow before

Analyst Presentation. First Quarter 2013 ADLER

Analyst Presentation First Quarter 2013 1 2 Highlights Steilmann Group 3 Financials 4 Outlook 2013 2 Highlights Q1 2013 Revenue and Profitability Revenue of 104.4 mio. Gross profit margin increase of 2.9

Analyst Presentation First Quarter 2013 1 2 Highlights Steilmann Group 3 Financials 4 Outlook 2013 2 Highlights Q1 2013 Revenue and Profitability Revenue of 104.4 mio. Gross profit margin increase of 2.9

Half-year figures 2017

1 Half-year figures 2017 Beter Bed Holding N.V. 30 August 2017 1 2 Agenda Financials Objectives and strategy Formats Outlook 2 3 Revenue per quarter Eur x 1.000 3 4 EBITDA per half-year Eur x 1.000 4 5

1 Half-year figures 2017 Beter Bed Holding N.V. 30 August 2017 1 2 Agenda Financials Objectives and strategy Formats Outlook 2 3 Revenue per quarter Eur x 1.000 3 4 EBITDA per half-year Eur x 1.000 4 5

KEY CONSIDERATIONS FOR EXAMINING CHANNEL PARTNER LOYALTY AN ICLP RESEARCH STUDY IN ASSOCIATION WITH CHANNEL FOCUS BAPTIE & COMPANY

KEY CONSIDERATIONS FOR EXAMINING CHANNEL PARTNER LOYALTY AN ICLP RESEARCH STUDY IN ASSOCIATION WITH CHANNEL FOCUS BAPTIE & COMPANY NOVEMBER 2014 Executive summary The changing landscape During this time

KEY CONSIDERATIONS FOR EXAMINING CHANNEL PARTNER LOYALTY AN ICLP RESEARCH STUDY IN ASSOCIATION WITH CHANNEL FOCUS BAPTIE & COMPANY NOVEMBER 2014 Executive summary The changing landscape During this time

CITI MARKETS GLOBAL FINANCIAL CONFERENCE

CITI MARKETS GLOBAL FINANCIAL CONFERENCE 19 November 2014 António Horta-Osório Group Chief Executive FINANCIAL PERFORMANCE 2014 TO DATE Continued successful execution of our strategy, profit and returns

CITI MARKETS GLOBAL FINANCIAL CONFERENCE 19 November 2014 António Horta-Osório Group Chief Executive FINANCIAL PERFORMANCE 2014 TO DATE Continued successful execution of our strategy, profit and returns

Pay Per Click Advertising

Pay Per Click Advertising What is Pay Per Click Advertising? Pay Per Click (PPC) is a model of advertising where you pay each time your ad is clicked, rather than earning clicks organically (like SEO).

Pay Per Click Advertising What is Pay Per Click Advertising? Pay Per Click (PPC) is a model of advertising where you pay each time your ad is clicked, rather than earning clicks organically (like SEO).

Quality Impact Assessment Procedure. July 2012

Quality Impact Assessment Procedure July 2012 1 Document name Quality Impact Assessment Procedure Version 3.0 Document author (name/title) Karen Warner Compliance lead (name/title) Mark Turner, Assurance

Quality Impact Assessment Procedure July 2012 1 Document name Quality Impact Assessment Procedure Version 3.0 Document author (name/title) Karen Warner Compliance lead (name/title) Mark Turner, Assurance

Our purpose To use the power of communications to make a better world. Growth to deliver sustainable profitable revenue growth.

Our strategy Our strategy has evolved since last year. The three main pillars are broadly the same but we ve placed more emphasis on the overall customer experience (rather than just on customer service).

Our strategy Our strategy has evolved since last year. The three main pillars are broadly the same but we ve placed more emphasis on the overall customer experience (rather than just on customer service).

Create a better today. Investor Day I 25 May 2016

Create a better today Investor Day I 25 May 2016 Agenda Speaker Michael Cameron Introduction Mark Reinke Customer experience Morning Tea Gary Dransfield Customer platforms Amanda Revis People experience

Create a better today Investor Day I 25 May 2016 Agenda Speaker Michael Cameron Introduction Mark Reinke Customer experience Morning Tea Gary Dransfield Customer platforms Amanda Revis People experience