Edgardo Curcio President AIEE

|

|

|

- Denis Casey

- 5 years ago

- Views:

Transcription

1 Edgardo Curcio President AIEE The First National Conference on Liquefied Natural Gas for Transports - Italy and the Mediterranean Sea April 11, 2013

2 What is LNG? The LNG (Liquefied Natural Gas) is a fluid in the liquid state, colorless, odorless, composed primarily of methane, contains small amounts of ethane, propane, nitrogen and other components normally present in natural gas. It does not contain carbon dioxide and water. At atmospheric pressure, it becomes liquid at about -160 C LNG takes up about 1/600th the volume of natural gas in the gaseous state 2

3 The LNG represents an alternative way to the transport by pipeline of the natural gas, allowing a direct connection between the regions of production and of consumption where connection by pipeline is not possible. The use of LNG responds to the strategic need to diversify geographically the sources of supply and make the natural gas market truly global and not limited geographically. 3

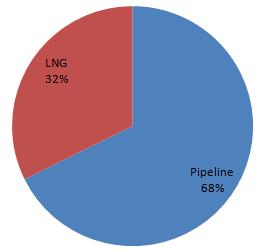

4 For transport over long distances, the LNG is more profitable than the pipeline transport. 4

5 The history of LNG The LNG industry is a young industry with a background of only 40 years. The first experimental transport was made in the 1959 (Lake Charles/Canvey Island). 5

6 The LNG chain LNG submersible pumps loading natural gas liquefaction LNG field purification treatment heavy hydrocarbons storage tanks jetty transport GASIFICATION PLANT distribution LNG submersible pumps LNG natural gas gasification storage tanks jetty landfill 6

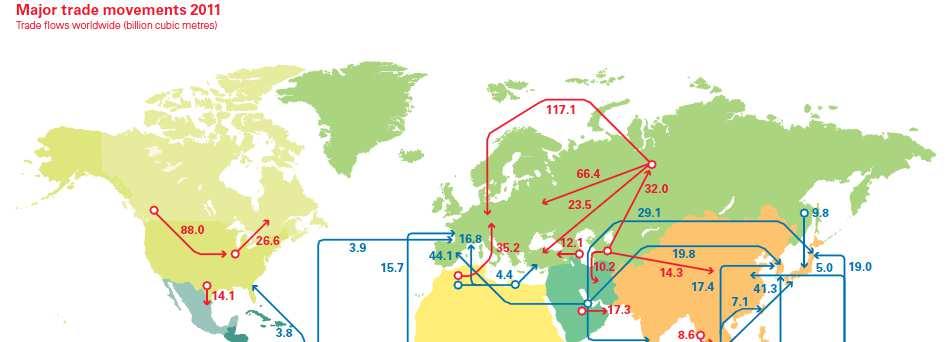

7 International trade flow of natural gas Fonte BP Statistical Review 7

8 LNG movement in Europe 8 8

9 LNG exporter suppliers in 2011 Egypt Other Russian Federation Malaysia 10% 9

10 LNG trade has incresed by 141% in the last decade 10

11 According to the BP data in 2011, about 32% of the natural gas world trade was represented by LNG, equivalent to bcm. According to GIIGNL in 2012 there was a 1.9% decrease of the imported LNG due to the global economic crisis. However, the weight of LNG trade is likely to grow in the coming years thanks to the increased use of natural gas in all end uses due to its higher efficiency and to its lower environmental impact. About 25% of the quantities traded in the LNG market goes to the spot market. 11

12 Spot and short-term LNG trade development since

13 At the end of 2012, 8 Countries out of a total of 18 made up 83% of global LNG exports. In the same period, the LNG supply of the Pacific Basin has declined by 3% and the supply of the Atlantic Basin by 2.2%. Although the production of Nigeria, Norway, Trinidad & Tobago increased its level it could not fill the gap of the lower exports from Algeria, Egypt and Equatorial Guinea. 13

14 In the Middle East, in 2012, production shutdowns in Yemen reduced total exports despite the increased production of Qatar. 63%, of Qatar volumes were exported to Asian countries, with Japan retaining the largest share. For , Qatar doubled its LNG exports to Japan 14

15 On the demand side, 7 importing countries out of a total of 26 (Japan, South Korea, China, India, Taiwan, Spain, UK) attracted 81% of the total LNG volumes. Japan and South Korea s combined share was around 53%. At the end 2012, there are: - 93 regasification terminals in 26 Countries, for a total capacity of 668 million tons/years; - 89 liquefaction plants in 18 Countries, for a total capacity of 282 million tons/years. The total LNG tanker fleet was of 378 vessels. 15

16 Liquefaction and regasification plants 16

17 17

18 18

19 Regasification capacity vs LNG imports in

20 The challenge of unconventional gas The gas revolution in the USA, aiming to exploit the large reserves of unconventional gas (bed methane, shale methane, etc.), has changed again the natural gas market. on one hand, the higher volumes of gas produced in the U.S. have lowered the prices of the domestic market, on the other hand the possibility to transport it, thanks to LNG in more profitable markets, have allowed the market to assume a global connotation dropping the geographical logic of the market, existing so far. 20

21 Higher prices of natural gas that provide access to higher costs for the production of coal bed methane, an improvement of related technologies, a new U.S. energy policy, aiming to energy independence and enhancement of national sources, have produced a great boost to the development of unconventional gas, such as coal bed methane (CBM) and shale gas. 21

22 World natural gas stocks 22

23 The exploitation of these two types of unconventional gas, not only led to the cancellation of most of U.S. regasification plant projects, which planned the arrival of LNG from different sources, both from the Middle East and North Africa, but it is changing the U.S. strategy that aims to build new LNG liquefaction plant projects to export in Europe. This policy is based on the higher LNG available volumes in USA and on the spread of 4-5 $/MBtu between the U.S. gas price and the European gas price, which allows transport and sale the U.S. LNG in Europe. 23

24 The first import contract was signed recently by the UK s Centrica with the U.S. Cheniere for the purchase of US LNG for about 2,5 bcm/year by the Sabine Pass plant. The agreement is for the supply of approximately 1.75 tons/year of LNG by 2018, for 20 years extendable to 30 years. The price will be equal to 115% of that on the Henry Hub, plus a fixed fee of 3 $/Mbtu. This agreement will make a valuable contribution to the diversification of suppliers in the UK, when it became the first LNG European importer in period in which UK has seen very slow flows of LNG increasingly attracted by Asian markets. 24

25 In the future, other contracts will come with an increase in US LNG flows in Europe and then in Asia, so as to completely alter the traditional take-or-pay gas market configuration. The ENI s CEO, Paolo Scaroni, sees a lowering of the current prices of gas in Europe in view of the increasingly active role of US LNG. The development of LNG, not only in USA but also in other regions, such as Asia and Australia, will also allow to increase the contribution of gas to the world s energy needs. 25

26 According to the last IEA report, there will be more new LNG plants in the next years expecially in Asia, and the LNG would represent almost 50% of the gas sold in the world in 2020, compared to 30% today. 26

27 IEA estimates that the North American exports of LNG will reach 35 billion cubic metres by 2020 and more than 40 bcm by 2035, two-thirds of which is expected to go to the Asian market. The prospect of LNG exports has set off a debate in the USA about the extent to which they will drive up domestic prices, by taking gas off the local market, and the US Department of Energy is waiting to review the results of a price impact study before dealing with the pending export applications. 27

28 Due to this debate, the esteem is that 93% of the natural gas produced in the USA remains available to meet domestic demand. In addition the WEO projections assume that the gas prices in the U.S. will increase from their current level 2 $/Mbtu in 2012 to 5.5 $/Mbtu in 2020, largely driven by the domestic dynamics of supply and demand. 28

29 29

30 Thanks for your attention

Lecture 12. LNG Markets

Lecture 12 LNG Markets Data from BP Statistical Review of World Energy 1991 to 2016 Slide 1 LNG Demand LNG demand is expected to grow from China, India and Europe in particular. Currently biggest importer

Lecture 12 LNG Markets Data from BP Statistical Review of World Energy 1991 to 2016 Slide 1 LNG Demand LNG demand is expected to grow from China, India and Europe in particular. Currently biggest importer

LNG Market Outlook and Development Pierre Cotin. 3 rd Annual LNG Shipping Forum 2013, Lillestrøm, 6 June 2013

LNG Market Outlook and Development Pierre Cotin 3 rd Annual LNG Shipping Forum 2013, Lillestrøm, 6 June 2013 Who we are GLE is one of the three columns of GIE (Gas Infrastructure Europe), the European

LNG Market Outlook and Development Pierre Cotin 3 rd Annual LNG Shipping Forum 2013, Lillestrøm, 6 June 2013 Who we are GLE is one of the three columns of GIE (Gas Infrastructure Europe), the European

7. Liquefied Natural Gas (LNG)

") 7. Liquefied Natural Gas (LNG) Figure 7-1: LNG supply chain Source; Total Liquid natural gas (LNG) is a good alternative to natural gas in remote locations or when the distance between the producer and

7. Liquefied Natural Gas (LNG) Figure 7-1: LNG supply chain Source; Total Liquid natural gas (LNG) is a good alternative to natural gas in remote locations or when the distance between the producer and

Gas Markets Globalization: Perspectives and Limits

Gas Markets Globalization: Perspectives and Limits By: Sid Ahmed Hamdani, Senior Business Analyst, Sonatrach, Algeria Date:04 June 2012 Venue: Kuala Lumpur Towards Gas Market Globalization? Increasing

Gas Markets Globalization: Perspectives and Limits By: Sid Ahmed Hamdani, Senior Business Analyst, Sonatrach, Algeria Date:04 June 2012 Venue: Kuala Lumpur Towards Gas Market Globalization? Increasing

IPTC MS The Outlook for LNG Supply to Asia. Stuart Traver, Lalitha Seelam and Nick Fulford Baker Hughes Inc. and Gaffney, Cline & Associates

IPTC 17774 - MS The Outlook for LNG Supply to Asia Stuart Traver, Lalitha Seelam and Nick Fulford Baker Hughes Inc. and Gaffney, Cline & Associates Slide 2 2013 GLOBAL NATURAL GAS TRADE Units: billion

IPTC 17774 - MS The Outlook for LNG Supply to Asia Stuart Traver, Lalitha Seelam and Nick Fulford Baker Hughes Inc. and Gaffney, Cline & Associates Slide 2 2013 GLOBAL NATURAL GAS TRADE Units: billion

Energy Market in Asia-Pacific and Canada s Potential for Natural Gas Export. Shahidul Islam

Energy Market in Asia-Pacific and Canada s Potential for Natural Gas Export Shahidul Islam Objective Examine energy demand in Asia-Pacific Especially natural gas Canada s natural gas situation Potential

Energy Market in Asia-Pacific and Canada s Potential for Natural Gas Export Shahidul Islam Objective Examine energy demand in Asia-Pacific Especially natural gas Canada s natural gas situation Potential

LNG TRADE FLOWS. Hans Stinis Shell Upstream International

LNG TRADE FLOWS Hans Stinis Shell Upstream International ABSTRACT The LNG industry has witnessed a great deal of change recently, and indications are that this will only continue. Global gas demand is

LNG TRADE FLOWS Hans Stinis Shell Upstream International ABSTRACT The LNG industry has witnessed a great deal of change recently, and indications are that this will only continue. Global gas demand is

NARUC. Global Liquefied Natural Gas Supply: An Introduction for Public Utility Commissioners

2009 Global Liquefied Natural Gas Supply: An Introduction for Public Utility Commissioners NARUC October 2009 The National Association of Regulatory Utility Commissioners Funded by the U.S. Department

2009 Global Liquefied Natural Gas Supply: An Introduction for Public Utility Commissioners NARUC October 2009 The National Association of Regulatory Utility Commissioners Funded by the U.S. Department

The Role of GCC s Natural Gas in the World s Gas Markets

World Review of Business Research Vol. 1. No. 2. May 2011 Pp. 168-178 The Role of GCC s Natural Gas in the World s Gas Markets Abdulkarim Ali Dahan* The objective of this research is to analyze the growth

World Review of Business Research Vol. 1. No. 2. May 2011 Pp. 168-178 The Role of GCC s Natural Gas in the World s Gas Markets Abdulkarim Ali Dahan* The objective of this research is to analyze the growth

Does LNG Threaten Russian Supplies to Europe?

Does LNG Threaten Russian Supplies to Europe? Sergei Komlev Head of Contract Structuring and Price Formation Directorate Gazprom Export IEA workshop on Eurasian gas markets Paris, April15 th, 2016 2010

Does LNG Threaten Russian Supplies to Europe? Sergei Komlev Head of Contract Structuring and Price Formation Directorate Gazprom Export IEA workshop on Eurasian gas markets Paris, April15 th, 2016 2010

The IEA s Gas 2017 Report - LNG moves to the front

The IEA s Gas 2017 Report - LNG moves to the front Peter Fraser, Head of the Gas, Coal and Power Division EMART Energy, Amsterdam, 5 October 2017 IEA Gas in today s world The contribution of gas Versatile

The IEA s Gas 2017 Report - LNG moves to the front Peter Fraser, Head of the Gas, Coal and Power Division EMART Energy, Amsterdam, 5 October 2017 IEA Gas in today s world The contribution of gas Versatile

Liquefied Natural Gas (LNG) Production and Markets. By: Jay Drexler, Dino Kasparis, and Curt Knight

Production and Markets. By: Jay Drexler, Dino Kasparis, and Curt Knight") Liquefied Natural Gas (LNG) Production and Markets By: Jay Drexler, Dino Kasparis, and Curt Knight Outline Purpose of the presentation What is Liquefied Natural Gas? (LNG) LNG Operations Brief History

Liquefied Natural Gas (LNG) Production and Markets By: Jay Drexler, Dino Kasparis, and Curt Knight Outline Purpose of the presentation What is Liquefied Natural Gas? (LNG) LNG Operations Brief History

LNG Facts A Primer. Presentation before US Department of Energy, Office of Fossil Energy, LNG Forums. March 10, Kristi A. R.

LNG Facts A Primer Presentation before US Department of Energy, Office of Fossil Energy, LNG Forums March 10, 2006 Kristi A. R. Darby Center for Louisiana State University Overview What is Natural Gas?

LNG Facts A Primer Presentation before US Department of Energy, Office of Fossil Energy, LNG Forums March 10, 2006 Kristi A. R. Darby Center for Louisiana State University Overview What is Natural Gas?

LNG basics. Juan Manuel Martín Ordax

LNG basics Juan Manuel Martín Ordax LNG basics Definition: Liquefied Natural Gas (LNG) is the liquid form of natural gas. LNG is a natural gas. LNG is a liquid. When cooled at atmospheric pressure to temperatures

LNG basics Juan Manuel Martín Ordax LNG basics Definition: Liquefied Natural Gas (LNG) is the liquid form of natural gas. LNG is a natural gas. LNG is a liquid. When cooled at atmospheric pressure to temperatures

2011 Institute of Energy Economics, Japan - IEEJ

A Changing World of LNG Pacific Energy Summit: Unlocking the Potential of Natural Gas in the Asia-Pacific Session 2: Market Evolution and Adaptation: Contracts, pricing mechanisms, and supply security

A Changing World of LNG Pacific Energy Summit: Unlocking the Potential of Natural Gas in the Asia-Pacific Session 2: Market Evolution and Adaptation: Contracts, pricing mechanisms, and supply security

World LNG Trade 2014 & Outlook 2015

World LNG Trade 2014 & Outlook 2015 By: Global LNG Info (GLNGI) May 2015 www.globallnginfo.com LNG Trades 2014 (1) 239.2 MMT of LNG traded in 2014, effectively flat for the third year running as reduced

World LNG Trade 2014 & Outlook 2015 By: Global LNG Info (GLNGI) May 2015 www.globallnginfo.com LNG Trades 2014 (1) 239.2 MMT of LNG traded in 2014, effectively flat for the third year running as reduced

The Impact of the Recession on Gas Markets

The Impact of the Recession on Gas Markets What has changed in our Brave New World Gas demand dropped by 2% Bigger drops in OECD region, FSU, Latin America But some notable exceptions: China, India Some

The Impact of the Recession on Gas Markets What has changed in our Brave New World Gas demand dropped by 2% Bigger drops in OECD region, FSU, Latin America But some notable exceptions: China, India Some

Summary LNG, an increasingly important energy option in Asia and the rest of the world But challenges remain for LNG to play an expected bigger role S

Prospect and Challenges in the World and Asian LNG Market LNG Producer Consumer Conference September 19, 2012 The Institute of Energy Economics Japan Ken Koyama 0 Summary LNG, an increasingly important

Prospect and Challenges in the World and Asian LNG Market LNG Producer Consumer Conference September 19, 2012 The Institute of Energy Economics Japan Ken Koyama 0 Summary LNG, an increasingly important

PGC B Strategy - Triennium November 18 20, 2014 Bratislava. By: Ashkan Esmaeilifar

1 PGC B Strategy - Triennium 2012 2015 November 18 20, 2014 Bratislava By: Ashkan Esmaeilifar 2 COUNTRY PROFILE Area (km 2 ): 49,035 Population: 5,379,000 Capital: Bratislava Member of OECD, WTO, NATO,

1 PGC B Strategy - Triennium 2012 2015 November 18 20, 2014 Bratislava By: Ashkan Esmaeilifar 2 COUNTRY PROFILE Area (km 2 ): 49,035 Population: 5,379,000 Capital: Bratislava Member of OECD, WTO, NATO,

Liquefied Natural Gas (LNG) Sector Overview June 2018

Sector Overview June 2018") Liquefied Natural Gas (LNG) Sector Overview June 2018 Global Industry Life Cycle Changes in Gas Markets Global Demand & Supply Dynamics Global Trade Regional Mix Global State of the Industry Trade Countries

Liquefied Natural Gas (LNG) Sector Overview June 2018 Global Industry Life Cycle Changes in Gas Markets Global Demand & Supply Dynamics Global Trade Regional Mix Global State of the Industry Trade Countries

Russia s Changing Role in the Global Gas Market

Russia s Changing Role in the Global Gas Market Dr. Tatiana Mitrova Head of Oil and Gas Department Energy Research Institute of the Russian Academy of Sciences Daegu June 18, 2013 1 1 CHANGING GLOBAL GAS

Russia s Changing Role in the Global Gas Market Dr. Tatiana Mitrova Head of Oil and Gas Department Energy Research Institute of the Russian Academy of Sciences Daegu June 18, 2013 1 1 CHANGING GLOBAL GAS

LNG Projects & Markets Past, Present & Challenges Ahead

LNG Projects & Markets Past, Present & Challenges Ahead Presented by: Don Andress Mostefa Ouki Nexant [Part 2: Markets, Past, Present & Challenges Ahead] United States Association for Energy Economics

LNG Projects & Markets Past, Present & Challenges Ahead Presented by: Don Andress Mostefa Ouki Nexant [Part 2: Markets, Past, Present & Challenges Ahead] United States Association for Energy Economics

Russian Pipeline Gas: Problem or Part of the Solution?

Russian Pipeline Gas: Problem or Part of the Solution? Sergei Komlev Head of Contract Structuring and Price Formation Directorate Gazprom Export* Flame, Amsterdam, May 14, 2018 *Views expressed in this

Russian Pipeline Gas: Problem or Part of the Solution? Sergei Komlev Head of Contract Structuring and Price Formation Directorate Gazprom Export* Flame, Amsterdam, May 14, 2018 *Views expressed in this

Table 1 Trade movements 2004 LNG (Bcm)

") LNG Prospects for the Future The prospect that LNG could become a major global energy source is one of the most keenly debated issues in the sector. This was reflected in this quarter's survey, conducted

LNG Prospects for the Future The prospect that LNG could become a major global energy source is one of the most keenly debated issues in the sector. This was reflected in this quarter's survey, conducted

European Gas Market State and Prospects: View from Gazprom Export

European Gas Market State and Prospects: View from Gazprom Export Sergei Komlev Head of Contract Structuring and Price Formation Gazprom Export Flame Conference Amsterdam, April 15, 2015 Short-Term Trends

European Gas Market State and Prospects: View from Gazprom Export Sergei Komlev Head of Contract Structuring and Price Formation Gazprom Export Flame Conference Amsterdam, April 15, 2015 Short-Term Trends

Global LNG Market Overview

Global LNG Market Overview 27 September, 2018 Toronto stock exchange listed, global intelligence solutions Request a demonstration of Evaluate Energy at this link 1 Who we serve 2 Global natural gas supply

Global LNG Market Overview 27 September, 2018 Toronto stock exchange listed, global intelligence solutions Request a demonstration of Evaluate Energy at this link 1 Who we serve 2 Global natural gas supply

Outlook for Gas Markets

IEEJ IEEJ:Published 2015 年 7 in 月 August 禁無断転載 2015 All rights reserved The 420th Forum on Research Work July 10, 2015 Outlook for Gas Markets The Institute of Energy Economics, Japan Tetsuo Morikawa Manager,

IEEJ IEEJ:Published 2015 年 7 in 月 August 禁無断転載 2015 All rights reserved The 420th Forum on Research Work July 10, 2015 Outlook for Gas Markets The Institute of Energy Economics, Japan Tetsuo Morikawa Manager,

SONATRACH PERSPECTIVES ON ASIAN LNG MARKETS

SONATRACH PERSPECTIVES ON ASIAN LNG MARKETS 65% of global gas demand growth by 2030 is expected to come from Asia, with traditional demand centers remaining stagnant Global gas demand by region to 2030

SONATRACH PERSPECTIVES ON ASIAN LNG MARKETS 65% of global gas demand growth by 2030 is expected to come from Asia, with traditional demand centers remaining stagnant Global gas demand by region to 2030

Gas Market Report 2017

Gas Market Report 2017 Center on Global Energy Policy, Columbia/SIPA Columbia Club, 13 July 2017 IEA Gas in today s world q The contribution of gas Versatile fuel within the energy system, helping to address

Gas Market Report 2017 Center on Global Energy Policy, Columbia/SIPA Columbia Club, 13 July 2017 IEA Gas in today s world q The contribution of gas Versatile fuel within the energy system, helping to address

Atlantic LNG: Has the boat sailed? Is the US out of the LNG trade and what are the implications for Europe?

Atlantic LNG: Has the boat sailed? Is the US out of the LNG trade and what are the implications for Europe? James Osten Principal North American Energy Markets LNG Trade Different for U.S. Than Europe

Atlantic LNG: Has the boat sailed? Is the US out of the LNG trade and what are the implications for Europe? James Osten Principal North American Energy Markets LNG Trade Different for U.S. Than Europe

Fabio Ballini World Maritime University

Pricing on gas: focus on LNG sectors Fabio Ballini World Maritime University What are the benefits of LNG? Environmental Benefits Table 3: Compering alterative technologies and fuels Source: SSPA, TC/1208-05-2100

Pricing on gas: focus on LNG sectors Fabio Ballini World Maritime University What are the benefits of LNG? Environmental Benefits Table 3: Compering alterative technologies and fuels Source: SSPA, TC/1208-05-2100

World LNG Report industry trends-

World LNG Report-218 -industry trends- Satoshi Yoshida General Manager, International Section, Policy and Planning Department Japan Gas Association International Gas Union (IGU) Who we are Founded in 1931,

World LNG Report-218 -industry trends- Satoshi Yoshida General Manager, International Section, Policy and Planning Department Japan Gas Association International Gas Union (IGU) Who we are Founded in 1931,

The Global Natural Gas Industry

The Global Natural Gas Industry Orlando CABRALES SEGOVIA Presidente de Naturgas, Colombia Regional Coordinator International Gas Union August 28 218 IGU Members serve 97% of the Worlds Gas Market 91 Charter

The Global Natural Gas Industry Orlando CABRALES SEGOVIA Presidente de Naturgas, Colombia Regional Coordinator International Gas Union August 28 218 IGU Members serve 97% of the Worlds Gas Market 91 Charter

The New Global Gas Market Dynamic. Emmanuel Grand, FTI-CL Energy

The New Global Gas Market Dynamic Emmanuel Grand, FTI-CL Energy May 2017 Contents I. Key uncertainties on gas demand II. Drivers of global LNG prices III. Conclusion 2 I. Key uncertainties on gas demand

The New Global Gas Market Dynamic Emmanuel Grand, FTI-CL Energy May 2017 Contents I. Key uncertainties on gas demand II. Drivers of global LNG prices III. Conclusion 2 I. Key uncertainties on gas demand

Rice World Gas Trade Model: Russian Natural Gas and Northeast Asia

Rice World Gas Trade Model: Russian Natural Gas and Northeast Asia Peter Hartley Kenneth B Medlock III James A. Baker III Institute of Public Policy RICE 1 Overview and motivation Worldwide, the demand

Rice World Gas Trade Model: Russian Natural Gas and Northeast Asia Peter Hartley Kenneth B Medlock III James A. Baker III Institute of Public Policy RICE 1 Overview and motivation Worldwide, the demand

gas 2O18 Analysis and Forecasts to 2O23

Market Report Series gas 2O18 Analysis and Forecasts to 2O23 executive summary INTERNATIONAL ENERGY AGENCY The IEA examines the full spectrum of energy issues including oil, gas and coal supply and demand,

Market Report Series gas 2O18 Analysis and Forecasts to 2O23 executive summary INTERNATIONAL ENERGY AGENCY The IEA examines the full spectrum of energy issues including oil, gas and coal supply and demand,

The Economics of LNG Export Contract Flexibility: a quantitative approach

The Economics of LNG Export Contract Flexibility: a quantitative approach By Yichi Zhang, 29 October 2012, EPRG weekly seminar Supervisors: Pierre Noel, Chi Kong Chyong shebazhang@gmail.com Introduction

The Economics of LNG Export Contract Flexibility: a quantitative approach By Yichi Zhang, 29 October 2012, EPRG weekly seminar Supervisors: Pierre Noel, Chi Kong Chyong shebazhang@gmail.com Introduction

Rice University World Gas Trade Model

Rice University World Gas Trade Model Peter Hartley Kenneth B Medlock III Jill Nesbitt James A. Baker III Institute of Public Policy RICE 1 What does the model capture? World gas supply potential is large

Rice University World Gas Trade Model Peter Hartley Kenneth B Medlock III Jill Nesbitt James A. Baker III Institute of Public Policy RICE 1 What does the model capture? World gas supply potential is large

Japan s LNG Prices Trending Upwards

Japan s LNG Prices Trending Upwards David Wood David Wood & Associates, Lincoln UK Published in Energy Tribune December 2007 Japan is the world's largest LNG consumer and imported 81.86 bcm of natural

Japan s LNG Prices Trending Upwards David Wood David Wood & Associates, Lincoln UK Published in Energy Tribune December 2007 Japan is the world's largest LNG consumer and imported 81.86 bcm of natural

RIM LNG Trade Annual 2010 Edition

RIM LNG Trade Annual 2010 Edition -Contents Volume 1 = Liquefacation Terminals in the world 1. Liquefacation Terminals in Asian Pacific Region 1 United states of America(Alaska) 2 Brunei 3 Indonesia 4

RIM LNG Trade Annual 2010 Edition -Contents Volume 1 = Liquefacation Terminals in the world 1. Liquefacation Terminals in Asian Pacific Region 1 United states of America(Alaska) 2 Brunei 3 Indonesia 4

Natural Gas Medium-term Outlook and Security Review

Natural Gas Medium-term Outlook and Security Review Jean-Baptiste Dubreuil Columbia University, New York, 30 October 2018 IEA Context Gas markets in the next five years Gas demand is in the fast lane,

Natural Gas Medium-term Outlook and Security Review Jean-Baptiste Dubreuil Columbia University, New York, 30 October 2018 IEA Context Gas markets in the next five years Gas demand is in the fast lane,

North America OECD Europe Asia Pacific

Australian LNG: Asia s natural supplier of LNG Peter Cleary, Vice President LNG Markets and Eastern Australia Commercial AJBCC: 52nd Australia-Japan Joint Business Conference Plenary Session Four: Energy

Australian LNG: Asia s natural supplier of LNG Peter Cleary, Vice President LNG Markets and Eastern Australia Commercial AJBCC: 52nd Australia-Japan Joint Business Conference Plenary Session Four: Energy

Global LNG Market dynamics, key trends and market outlook

REUTERS / Anne Kat Brevik Global LNG Market dynamics, key trends and market outlook December 14, 217 What to address Market dynamics, key trends and market outlook The role and outlook for U.S. LNG China

REUTERS / Anne Kat Brevik Global LNG Market dynamics, key trends and market outlook December 14, 217 What to address Market dynamics, key trends and market outlook The role and outlook for U.S. LNG China

LNG Markets in Transition : Will East meet West?

LNG Markets in Transition : Will East meet West? Jean-Marc Hosanski World Conference Tokyo, June 2nd, 2003 WOC 10 Thank you Mister Chairman, Ladies and Gentlemen, Distinguished Guests, My objective today

LNG Markets in Transition : Will East meet West? Jean-Marc Hosanski World Conference Tokyo, June 2nd, 2003 WOC 10 Thank you Mister Chairman, Ladies and Gentlemen, Distinguished Guests, My objective today

European Gas Market in 2017: State and Perspectives

European Gas Market in 2017: State and Perspectives Sergei Komlev Head of Contract Structuring and Price Formation Directorate Gazprom Export Oil & Gas Forum, Thompson Reuters Moscow, December 14, 2017

European Gas Market in 2017: State and Perspectives Sergei Komlev Head of Contract Structuring and Price Formation Directorate Gazprom Export Oil & Gas Forum, Thompson Reuters Moscow, December 14, 2017

Gas Market Report 2018

Gas Market Report 2018 Jean-Baptiste Dubreuil, Senior Natural Gas Analyst, IEA Spanish Energy Club, Madrid 2 July 2018 IEA Context Gas markets in the next five years Gas demand is in the fast lane, thanks

Gas Market Report 2018 Jean-Baptiste Dubreuil, Senior Natural Gas Analyst, IEA Spanish Energy Club, Madrid 2 July 2018 IEA Context Gas markets in the next five years Gas demand is in the fast lane, thanks

Will the growth of LNG create a global gas market?

Will the growth of LNG create a global gas market? Chris Evans Vice President Global LNG Supply Shell Gas & Power FLAME, Amsterdam 25 th February 25 Increasing choice for consumers and producers Environmental

Will the growth of LNG create a global gas market? Chris Evans Vice President Global LNG Supply Shell Gas & Power FLAME, Amsterdam 25 th February 25 Increasing choice for consumers and producers Environmental

Arbitrage in Natural Gas Markets?

Arbitrage in Natural Gas Markets? Yuri Yegorov University of Vienna Seminar on Energy Economics Paris, School of Mines April 13 th, 2016, 16:30-18:30 Based on article with J.Dehnavi and F.Wirl in Intern.

Arbitrage in Natural Gas Markets? Yuri Yegorov University of Vienna Seminar on Energy Economics Paris, School of Mines April 13 th, 2016, 16:30-18:30 Based on article with J.Dehnavi and F.Wirl in Intern.

Gas Markets in 2015: Outlook and Challenges

The 418th Forum on Research Work Gas Markets in 2015: Outlook and Challenges December 19, 2014 Tetsuo Morikawa The Institute of Energy Economics, Japan Natural Gas Demand in Major Regions Natural Gas Demand

The 418th Forum on Research Work Gas Markets in 2015: Outlook and Challenges December 19, 2014 Tetsuo Morikawa The Institute of Energy Economics, Japan Natural Gas Demand in Major Regions Natural Gas Demand

Energy in Perspective

Energy in Perspective BP Statistical Review of World Energy 27 Christof Rühl Deputy Chief Economist London, 12 June 27 Outline Introduction What has changed? The medium term What is new? 26 in review Conclusion

Energy in Perspective BP Statistical Review of World Energy 27 Christof Rühl Deputy Chief Economist London, 12 June 27 Outline Introduction What has changed? The medium term What is new? 26 in review Conclusion

New York Energy Forum

Presentation to the New York Energy Forum Antoine Halff 30 June 2014 Key highlights Gas demand grew just 1.2% in 2013, underperforming other fuels Gas demand will grow at 2.2%/y over 2013-19, on its way

Presentation to the New York Energy Forum Antoine Halff 30 June 2014 Key highlights Gas demand grew just 1.2% in 2013, underperforming other fuels Gas demand will grow at 2.2%/y over 2013-19, on its way

The increasing role of LNG in Europe. 7th US-EU Energy Regulators Roundtable Nov , New Orleans

The increasing role of LNG in Europe Agenda World outlook European demand and supply Growing role for LNG in Europe Conclusion Gas supply/demand in the world : Geographic dissociation of reserves and demand

The increasing role of LNG in Europe Agenda World outlook European demand and supply Growing role for LNG in Europe Conclusion Gas supply/demand in the world : Geographic dissociation of reserves and demand

The IEA outlook for gas. Laszlo Varro Head, Gas Coal and Power Markets

The IEA outlook for gas Laszlo Varro Head, Gas Coal and Power Markets For gas the Asian century is just starting 3 000 Mtoe Primary energy consumption 2 500 coal gas 2 000 1 500 1 000 500 - Asia Europe

The IEA outlook for gas Laszlo Varro Head, Gas Coal and Power Markets For gas the Asian century is just starting 3 000 Mtoe Primary energy consumption 2 500 coal gas 2 000 1 500 1 000 500 - Asia Europe

AFRICA A NEW PLAYER IN THE ENERGY MARKET: - EAST AFRICA - EAST MEDITERRANEAN

AFRICA A NEW PLAYER IN THE ENERGY MARKET: - EAST AFRICA - EAST MEDITERRANEAN Eng. Khaled Abubakr Middle East & Africa Regional Coordinator, IGU Chairman, Egyptian Gas Association Chairman, TAQA Arabia

AFRICA A NEW PLAYER IN THE ENERGY MARKET: - EAST AFRICA - EAST MEDITERRANEAN Eng. Khaled Abubakr Middle East & Africa Regional Coordinator, IGU Chairman, Egyptian Gas Association Chairman, TAQA Arabia

The Future Role of Gas

The Future Role of Gas GECF Global Gas Outlook 24 Insights Presentation for the 3rd IEA-IEF-OPEC Symposium on Gas and Coal Market Outlooks Dmitry Sokolov Head of Energy Economics and Forecasting Department

The Future Role of Gas GECF Global Gas Outlook 24 Insights Presentation for the 3rd IEA-IEF-OPEC Symposium on Gas and Coal Market Outlooks Dmitry Sokolov Head of Energy Economics and Forecasting Department

Security of natural gas supply in Spain. Mariano Marzo Fac. Geology Univ. Barcelona

Security of natural gas supply in Spain Mariano Marzo Fac. Geology Univ. Barcelona 1 Spain s Primary Energy Mix 2007 HC = 84% 2 Natural Gas Consumption in EU27 in 2007 3 The Spanish gas market differs

Security of natural gas supply in Spain Mariano Marzo Fac. Geology Univ. Barcelona 1 Spain s Primary Energy Mix 2007 HC = 84% 2 Natural Gas Consumption in EU27 in 2007 3 The Spanish gas market differs

Gas Market Report 2017

Gas Market Report 2017 Peter Fraser, Head of the Gas Coal and Power Markets Division Norwegian Ministry of Petroleum and Energy, Oslo, 5 th September 2017 IEA Gas in today s world The contribution of gas

Gas Market Report 2017 Peter Fraser, Head of the Gas Coal and Power Markets Division Norwegian Ministry of Petroleum and Energy, Oslo, 5 th September 2017 IEA Gas in today s world The contribution of gas

THE DYNAMICS of LNG INDUSTRY. Prof. Valeria Termini AEEGSI Commissioner - MEDREG Vice President

THE DYNAMICS of LNG INDUSTRY Prof. Valeria Termini AEEGSI Commissioner - MEDREG Vice President INDEX I. NEW GLOBAL TRENDS II. LNG INDUSTRY: the game changers III. IN EUROPE IV. THE MEDITERRANEAN CONTEXT

THE DYNAMICS of LNG INDUSTRY Prof. Valeria Termini AEEGSI Commissioner - MEDREG Vice President INDEX I. NEW GLOBAL TRENDS II. LNG INDUSTRY: the game changers III. IN EUROPE IV. THE MEDITERRANEAN CONTEXT

Hydrogen Would Prefer Russian Pipeline Gas

Hydrogen Would Prefer Russian Pipeline Gas Sergei Komlev Head of Contract Structuring and Price Formation Directorate Gazprom Export* 26th meeting of the EU-Russia Gas Advisory Council s Work Stream on

Hydrogen Would Prefer Russian Pipeline Gas Sergei Komlev Head of Contract Structuring and Price Formation Directorate Gazprom Export* 26th meeting of the EU-Russia Gas Advisory Council s Work Stream on

INTERNATIONAL CONVENTION ON LIABILITY AND COMPENSATION FOR DAMAGE IN CONNECTION WITH THE CARRIAGE OF HAZARDOUS AND NOXIOUS SUBSTANCES BY SEA

INTERNATIONAL OIL POLLUTION COMPENSATION FUND 1992 ASSEMBLY 92FUND/A/ES.12/9/1/Rev.1* 12th extraordinary session 15 May 2007 Agenda item 9 Original: ENGLISH INTERNATIONAL CONVENTION ON LIABILITY AND COMPENSATION

INTERNATIONAL OIL POLLUTION COMPENSATION FUND 1992 ASSEMBLY 92FUND/A/ES.12/9/1/Rev.1* 12th extraordinary session 15 May 2007 Agenda item 9 Original: ENGLISH INTERNATIONAL CONVENTION ON LIABILITY AND COMPENSATION

Dry and Liquefied Gas to European Markets

Dry and Liquefied Gas to European Markets Competing or Complementary? Graham Bennett Outline Introduction Supply/Demand changes affecting the gas market Innovations impacting gas import/export options

Dry and Liquefied Gas to European Markets Competing or Complementary? Graham Bennett Outline Introduction Supply/Demand changes affecting the gas market Innovations impacting gas import/export options

Copyright. Sinem Okumus

Copyright by Sinem Okumus 2015 The Thesis Committee for Sinem Okumus Certifies that this is the approved version of the following thesis: Impacts of US LNG Exports on the Supply Security of the EU Natural

Copyright by Sinem Okumus 2015 The Thesis Committee for Sinem Okumus Certifies that this is the approved version of the following thesis: Impacts of US LNG Exports on the Supply Security of the EU Natural

LNG: Towards a global natural gas market. The Mexican experience

LNG: Towards a global natural gas market. The Mexican experience Mr. Gerardo Bazan G., PEMEX CEO Advisor, +(52)-55-19448765, gbazan@dg.pemex.com The views and opinions presented in this paper do not represent

LNG: Towards a global natural gas market. The Mexican experience Mr. Gerardo Bazan G., PEMEX CEO Advisor, +(52)-55-19448765, gbazan@dg.pemex.com The views and opinions presented in this paper do not represent

Singapore s Import of LNG

Singapore s Import of LNG Panel Session 4: New Procurement Behaviors by Consumers Presentation at LNG Producer-Consumer Conference Tokyo, Japan 10 Sep 2013 0 Singapore Electricity Fuel Mix Natural Gas

Singapore s Import of LNG Panel Session 4: New Procurement Behaviors by Consumers Presentation at LNG Producer-Consumer Conference Tokyo, Japan 10 Sep 2013 0 Singapore Electricity Fuel Mix Natural Gas

Liquefied Natural Gas (LNG) Sector Overview March 2017

Sector Overview March 2017") Liquefied Natural Gas (LNG) Sector Overview March 2017 Global Industry LNG Industry Life Cycle Industry Dynamics Trade Regional Mix Exporting & Importing Countries Pricing Local Industry Dynamics Production

Liquefied Natural Gas (LNG) Sector Overview March 2017 Global Industry LNG Industry Life Cycle Industry Dynamics Trade Regional Mix Exporting & Importing Countries Pricing Local Industry Dynamics Production

LNG Shipping: How Long Will The Good Times Last?

LNG Shipping: How Long Will The Good Times Last? Poten & Partners November 1 HOUSTON NEW YORK LONDON ATHENS SINGAPORE GUANGZHOU PERTH A GLOBAL BROKER AND COMMERCIAL ADVISOR FOR THE ENERGY AND OCEAN TRANSPORTATION

LNG Shipping: How Long Will The Good Times Last? Poten & Partners November 1 HOUSTON NEW YORK LONDON ATHENS SINGAPORE GUANGZHOU PERTH A GLOBAL BROKER AND COMMERCIAL ADVISOR FOR THE ENERGY AND OCEAN TRANSPORTATION

TABLE OF CONTENTS GAS MARKET REPORT

TABLE OF CONTENTS Foreword... 3 Acknowledgements... 4 Executive summary... 11 1. Demand... 15 Global overview... 15 Assumptions... 18 OECD Demand... 19 Americas... 19 Europe... 26 Asia Oceania... 31 Non-OECD

TABLE OF CONTENTS Foreword... 3 Acknowledgements... 4 Executive summary... 11 1. Demand... 15 Global overview... 15 Assumptions... 18 OECD Demand... 19 Americas... 19 Europe... 26 Asia Oceania... 31 Non-OECD

How LNG Supply Additions Could Affect Gas Prices in Europe?

How LNG Supply Additions Could Affect Gas Prices in Europe? Sergei Komlev Head of Contract Structuring and Price Formation Directorate Gazprom Export* C5, Gas and LNG Supply Contracts Forum Berlin, June

How LNG Supply Additions Could Affect Gas Prices in Europe? Sergei Komlev Head of Contract Structuring and Price Formation Directorate Gazprom Export* C5, Gas and LNG Supply Contracts Forum Berlin, June

Gazprom s response to U.S. LNG exports and the changing global market. Tatiana Mitrova October 19, 2018

Gazprom s response to U.S. LNG exports and the changing global market Tatiana Mitrova October 19, 2018 1 1985 1987 1989 1991 1993 1995 1997 1999 2001 2003 2005 2007 2009 2011 2013 2015 2017 1985 1987 1989

Gazprom s response to U.S. LNG exports and the changing global market Tatiana Mitrova October 19, 2018 1 1985 1987 1989 1991 1993 1995 1997 1999 2001 2003 2005 2007 2009 2011 2013 2015 2017 1985 1987 1989

INTERNATIONAL ENERGY AGENCY WORLD ENERGY INVESTMENT OUTLOOK 2003 INSIGHTS

INTERNATIONAL ENERGY AGENCY WORLD ENERGY INVESTMENT OUTLOOK 2003 INSIGHTS Global Strategic Challenges Security of energy supplies Threat of environmental damage caused by energy use Uneven access of the

INTERNATIONAL ENERGY AGENCY WORLD ENERGY INVESTMENT OUTLOOK 2003 INSIGHTS Global Strategic Challenges Security of energy supplies Threat of environmental damage caused by energy use Uneven access of the

Orientation for a fast-changing energy world. Dr Fatih Birol IEA Chief Economist Tokyo, 21 April 2014

Orientation for a fast-changing energy world Dr Fatih Birol IEA Chief Economist Tokyo, 21 April 2014 The world energy scene today Some long-held tenets of the energy sector are being rewritten Countries

Orientation for a fast-changing energy world Dr Fatih Birol IEA Chief Economist Tokyo, 21 April 2014 The world energy scene today Some long-held tenets of the energy sector are being rewritten Countries

2009 Changing the scene

2009 Changing the scene Gas demand in Europe and in other major economies is weakening Industrial demand strongly affected by the economic crisis Demand in the power generation sector suffers from relatively

2009 Changing the scene Gas demand in Europe and in other major economies is weakening Industrial demand strongly affected by the economic crisis Demand in the power generation sector suffers from relatively

Prospects for unconventional natural gas supply in Asia

Perth, 16 February 2016 Prospects for unconventional natural gas supply in Asia Roberto F. Aguilera Background Expansion of natural gas share in primary energy mix, especially Asia Gas demand is dominated

Perth, 16 February 2016 Prospects for unconventional natural gas supply in Asia Roberto F. Aguilera Background Expansion of natural gas share in primary energy mix, especially Asia Gas demand is dominated

LNG strategy and the outlook for global gas markets

LNG strategy and the outlook for global gas markets October 16 th, 2012 Jean-Marie Dauger Executive Vice-president GDF SUEZ The LNG market Strong growth particularly in Asia An LNG market of ~550 Mt in

LNG strategy and the outlook for global gas markets October 16 th, 2012 Jean-Marie Dauger Executive Vice-president GDF SUEZ The LNG market Strong growth particularly in Asia An LNG market of ~550 Mt in

Oxford Institute for Energy Studies Natural Gas Programme Howard V Rogers

Oxford Institute for Energy Studies Natural Gas Programme Howard V Rogers LNG Costs, Russian Exports and Global Interactions December 9 th & 1 th 215 WE ARE: A gas research programme at a Recognised Independent

Oxford Institute for Energy Studies Natural Gas Programme Howard V Rogers LNG Costs, Russian Exports and Global Interactions December 9 th & 1 th 215 WE ARE: A gas research programme at a Recognised Independent

Global and Russian Energy Sector at the Crossroad: New Challenges

Global and Russian Energy Sector at the Crossroad: New Challenges Dr. Tatiana Mitrova Head of Oil and Gas Department Energy Research Institute of the Russian Academy of Sciences Washington 6 December,

Global and Russian Energy Sector at the Crossroad: New Challenges Dr. Tatiana Mitrova Head of Oil and Gas Department Energy Research Institute of the Russian Academy of Sciences Washington 6 December,

The 3 rd International LNG Summit

OAPEC Organization of Arab Petroleum Exporting Countries 3 rd Annual Future Prospects for LNG in the Arab Countries and Implications on the Global LNG Market Gas Industries Expert OAPEC Agenda Setting

OAPEC Organization of Arab Petroleum Exporting Countries 3 rd Annual Future Prospects for LNG in the Arab Countries and Implications on the Global LNG Market Gas Industries Expert OAPEC Agenda Setting

Why it Makes Sense for Europe to Embrace Nord Stream 2?

Why it Makes Sense for Europe to Embrace Nord Stream 2? Sergei Komlev Head of Contract Structuring and Price Formation Directorate Gazprom Export Global Gas Centre Meeting Brussels, December 10 th, 2015

Why it Makes Sense for Europe to Embrace Nord Stream 2? Sergei Komlev Head of Contract Structuring and Price Formation Directorate Gazprom Export Global Gas Centre Meeting Brussels, December 10 th, 2015

RYSTAD ENERGY GAS PERSPECTIVES. Jakarta, November 20 th 2017

RYSTAD ENERGY GAS PERSPECTIVES Jakarta, November 2 th 217 Agenda 1. Global LNG market outlook Oversupply and new Asian demand 2. Japan LNG Market outlook LNG demand in a nuclear restart 2 Longer distances

RYSTAD ENERGY GAS PERSPECTIVES Jakarta, November 2 th 217 Agenda 1. Global LNG market outlook Oversupply and new Asian demand 2. Japan LNG Market outlook LNG demand in a nuclear restart 2 Longer distances

Impact of American Unconventional Oil and Gas Revolution

National University of Singapore Energy Studies Institute 18 May 215 Impact of American Unconventional Oil and Gas Revolution Edward C. Chow Senior Fellow Revenge of the Oil Price Cycle American Innovation:

National University of Singapore Energy Studies Institute 18 May 215 Impact of American Unconventional Oil and Gas Revolution Edward C. Chow Senior Fellow Revenge of the Oil Price Cycle American Innovation:

The impact of US LNG on European gas prices

January 2018 The impact of US LNG on European gas prices Increasing US exports of LNG will change how gas prices are determined in Europe Import dependency for the European Union, pushed higher as a result

January 2018 The impact of US LNG on European gas prices Increasing US exports of LNG will change how gas prices are determined in Europe Import dependency for the European Union, pushed higher as a result

6 th World LNG Series Asia Pacific Summit Wednesday 24 September The changing LNG Demand and Supply Outlook Jérôme Ferrier President IGU

IGU 6 th World LNG Series Asia Pacific Summit Wednesday 24 September 2014 The changing LNG Demand and Supply Outlook Jérôme Ferrier President IGU Allocated title: 15 minutes The Hon. Nixon Philip Duban,

IGU 6 th World LNG Series Asia Pacific Summit Wednesday 24 September 2014 The changing LNG Demand and Supply Outlook Jérôme Ferrier President IGU Allocated title: 15 minutes The Hon. Nixon Philip Duban,

Regional Cooperation on Gas Pipeline and LNG Market in Northeast Asia ``````````````

3 rd Northeast Asia Energy Security Forum Seoul, Korea Regional Cooperation on Gas Pipeline and LNG Market in Northeast Asia `````````````` Views and opinions expressed in this presentation are those of

3 rd Northeast Asia Energy Security Forum Seoul, Korea Regional Cooperation on Gas Pipeline and LNG Market in Northeast Asia `````````````` Views and opinions expressed in this presentation are those of

Natural Gas Facts & Figures. New Approach & Proposal

Natural Gas Facts & Figures New Approach & Proposal 1. Production and reserves Sources : Total G&P, WOC1, IEA, IHS Cera, Resources- Reserves o Conventional o Unconventional : types and reserves Countries,

Natural Gas Facts & Figures New Approach & Proposal 1. Production and reserves Sources : Total G&P, WOC1, IEA, IHS Cera, Resources- Reserves o Conventional o Unconventional : types and reserves Countries,

Natural Gas Facts & Figures. Section 3: LNG

Natural Gas Facts & Figures Section 3: LNG September 214 3. LNG Trade movements Terminals for import, terminals for exports Liquefaction, regazeification LNG Fleet Sources : Total LNG group, PGCD special

Natural Gas Facts & Figures Section 3: LNG September 214 3. LNG Trade movements Terminals for import, terminals for exports Liquefaction, regazeification LNG Fleet Sources : Total LNG group, PGCD special

International Pressures on European Energy Supplies: what are the natural gas issues?

International Pressures on European Energy Supplies: what are the natural gas issues? Professor Jonathan Stern Chairman and Senior Research Fellow, Natural Gas Research Programme, Oxford Institute for

International Pressures on European Energy Supplies: what are the natural gas issues? Professor Jonathan Stern Chairman and Senior Research Fellow, Natural Gas Research Programme, Oxford Institute for

216 IEEJ216 Key points of this report Oversupply in the international LNG market will expand further in the coming years. Upstream industry is cutting

216 IEEJ216 423 rd Forum on Research Works on July 26, 216 Outlook for Gas Market The Institute of Energy Economics, Japan Yoshikazu Kobayashi Senior Economist, Manager, Gas Group, Fossil Fuels & Electric

216 IEEJ216 423 rd Forum on Research Works on July 26, 216 Outlook for Gas Market The Institute of Energy Economics, Japan Yoshikazu Kobayashi Senior Economist, Manager, Gas Group, Fossil Fuels & Electric

Japan s LNG Policies and Japan-Argentina Cooperation. December 2014

Japan s LNG Policies and Japan-Argentina Cooperation December 2014 High Dependency On Fossil Fuels For Power Generation The nuclear power ratio in domestic power generation has decreased after the Great

Japan s LNG Policies and Japan-Argentina Cooperation December 2014 High Dependency On Fossil Fuels For Power Generation The nuclear power ratio in domestic power generation has decreased after the Great

Gazprom s export strategy to Europe: Ensuring security of supply vs challenges from US LNG where does Asia fit in and how high can exports go?

From Russia to Europe. Gazprom s export strategy to Europe: Ensuring security of supply vs challenges from US LNG where does Asia fit in and how high can exports go? Elena Burmistrova Director General,

From Russia to Europe. Gazprom s export strategy to Europe: Ensuring security of supply vs challenges from US LNG where does Asia fit in and how high can exports go? Elena Burmistrova Director General,

Current Status of Gas Industry in Japan

Member Economy Report Current Status of Gas Industry in Japan Ryu Nishida General Manager, International Relations Department November 19, 2014 GASEX2014, Hong Kong Table of contents 2 1. Japan s Energy

Member Economy Report Current Status of Gas Industry in Japan Ryu Nishida General Manager, International Relations Department November 19, 2014 GASEX2014, Hong Kong Table of contents 2 1. Japan s Energy

ASIAN OFFSHORE ENERGY CONFERENCE DISPUTES IN LNG CONTRACTS

ASIAN OFFSHORE ENERGY CONFERENCE 28 SEPTEMBER 2017 DISPUTES IN LNG CONTRACTS Bob Broxson BDO USA, LLP, a Delaware limited liability partnership, is the U.S. member of BDO International Limited, a UK company

ASIAN OFFSHORE ENERGY CONFERENCE 28 SEPTEMBER 2017 DISPUTES IN LNG CONTRACTS Bob Broxson BDO USA, LLP, a Delaware limited liability partnership, is the U.S. member of BDO International Limited, a UK company

Australian LNG: Asia s natural supplier of LNG

Australian LNG: Asia s natural supplier of LNG Peter Cleary, Vice President LNG Markets and Eastern Australia Commercial AJBCC: 52nd Australia-Japan Joint Business Conference Plenary Session Four: Energy

Australian LNG: Asia s natural supplier of LNG Peter Cleary, Vice President LNG Markets and Eastern Australia Commercial AJBCC: 52nd Australia-Japan Joint Business Conference Plenary Session Four: Energy

The economic impact of South Stream on Hungarian energy consumption

The economic impact of South Stream on Hungarian energy consumption South Stream: Evolution of a Pipeline Natural Gas Europe ǀ Gas Dialogues Budapest November 18 th, 2013 Prepared by World Energy Expert

The economic impact of South Stream on Hungarian energy consumption South Stream: Evolution of a Pipeline Natural Gas Europe ǀ Gas Dialogues Budapest November 18 th, 2013 Prepared by World Energy Expert

European Gas & LNG Markets, Energy Policy, and Geopolitics October 2016

European Gas & LNG Markets, Energy Policy, and Geopolitics October 2016 www.rapidangroup.com Leslie.palti-guzman@rapidangroup.com t. +1 301.656.4480 No Quotation or Distribution 1 EU LNG Demand Key Themes:

European Gas & LNG Markets, Energy Policy, and Geopolitics October 2016 www.rapidangroup.com Leslie.palti-guzman@rapidangroup.com t. +1 301.656.4480 No Quotation or Distribution 1 EU LNG Demand Key Themes:

LNG in 2015 and MT perspectives

CEDIGAZ, the International Association for Natural Gas LNG in 2015 and MT perspectives Geoffroy Hureau Secretary General - CEDIGAZ THE LNG MARKET IN 2015 (Preliminary estimates) LNG Demand grew 2% in 2015

CEDIGAZ, the International Association for Natural Gas LNG in 2015 and MT perspectives Geoffroy Hureau Secretary General - CEDIGAZ THE LNG MARKET IN 2015 (Preliminary estimates) LNG Demand grew 2% in 2015

Pricing on gas: focus on LNG sectors. Monica Canepa World Maritime University

Pricing on gas: focus on LNG sectors Monica Canepa World Maritime University OVERVIEW The current status of the energy in the world is investigated by International Energy Agency (IEA) in cooperation with

Pricing on gas: focus on LNG sectors Monica Canepa World Maritime University OVERVIEW The current status of the energy in the world is investigated by International Energy Agency (IEA) in cooperation with

Dr. Fatih BIROL IEA Chief Economist Tokyo, 17 February 2015

Dr. Fatih BIROL IEA Chief Economist Tokyo, 17 February 2015 Signs of stress in the global energy system Current calm in markets should not disguise difficult road ahead Turmoil in the Middle East raises

Dr. Fatih BIROL IEA Chief Economist Tokyo, 17 February 2015 Signs of stress in the global energy system Current calm in markets should not disguise difficult road ahead Turmoil in the Middle East raises

[LNG MARKET ANALYSIS ] 1. LNG Market Analysis

![[LNG MARKET ANALYSIS ] 1. LNG Market Analysis](/thumbs/83/87599992.jpg "[LNG MARKET ANALYSIS ] 1. LNG Market Analysis") [LNG MARKET ANALYSIS ] 1 LNG Market Analysis LNG Market Analysis Volume: 8 th June 2018 LNG and Natural Gas Price Assessment 28 th May 8 th June 2018 [LNG MARKET ANALYSIS ] 2 LNG Analysis Stable to bullish

[LNG MARKET ANALYSIS ] 1 LNG Market Analysis LNG Market Analysis Volume: 8 th June 2018 LNG and Natural Gas Price Assessment 28 th May 8 th June 2018 [LNG MARKET ANALYSIS ] 2 LNG Analysis Stable to bullish

Shale Gas and LNG - Effects on Global Markets

Shale Gas and LNG - Effects on Global Markets STEVEN A. GABRIEL UNIVERSITY OF MARYLAND THE ROLE OF NATURAL GAS IN THE FUTURE ENERGY SYSTEM THE NEED FOR FLEXIBILITY NTNU ENERGY TRANSITION WORKSHOP NORWEGIAN

Shale Gas and LNG - Effects on Global Markets STEVEN A. GABRIEL UNIVERSITY OF MARYLAND THE ROLE OF NATURAL GAS IN THE FUTURE ENERGY SYSTEM THE NEED FOR FLEXIBILITY NTNU ENERGY TRANSITION WORKSHOP NORWEGIAN

The Evolving Landscape of the LNG Sector.

The Evolving Landscape of the LNG Sector Four Divisions One Team One integrated full-service team for your project to serve you from concept to commercial operations Ship Broking Logistics Braemar ACM

The Evolving Landscape of the LNG Sector Four Divisions One Team One integrated full-service team for your project to serve you from concept to commercial operations Ship Broking Logistics Braemar ACM