Case M TIL / PSA / PSA DGD. REGULATION (EC) No 139/2004 MERGER PROCEDURE. Article 6(1)(b) NON-OPPOSITION Date: 31/07/2017

|

|

|

- Mary Griffith

- 6 years ago

- Views:

Transcription

No 139/2004 MERGER PROCEDURE Article 6(1)(b) NON-OPPOSITION Date: 31/07/2017 In electronic form on the EUR-Lex website under")

1 EUROPEAN COMMISSION DG Competition Case M TIL / PSA / PSA DGD Only the English text is available and authentic. REGULATION (EC) No 139/2004 MERGER PROCEDURE Article 6(1)(b) NON-OPPOSITION Date: 31/07/2017 In electronic form on the EUR-Lex website under document number 32017M8459

2 EUROPEAN COMMISSION In the published version of this decision, some information has been omitted pursuant to Article 17(2) of Council Regulation (EC) No 139/2004 concerning non-disclosure of business secrets and other confidential information. The omissions are shown thus [ ]. Where possible the information omitted has been replaced by ranges of figures or a general description. Brussels, C(2017) 5497 final PUBLIC VERSION To the notifying parties: Subject: Case M.8459 TIL/ PSA/ PSA DGD Commission decision pursuant to Article 6(1)(b) of Council Regulation No 139/ and Article 57 of the Agreement on the European Economic Area 2 Dear Sir or Madam, (1) On 23 June 2017, the Commission received notification of a proposed concentration pursuant to Article 4 of Council Regulation (EC) No 139/2004 by which Europe Terminal NV ("ET", Switzerland), a wholly-owned subsidiary of Terminal Investment Limited Sàrl (''TIL'', Switzerland), and Kranji (Netherlands) Investments BV ("Kranji", Netherlands), a holding company controlled by PSA International Pte Ltd (''PSA'', Singapore), acquire within the meaning of Article 3(1)(b) of the Merger Regulation joint control over PSA DGD NV (''PSA DGD'', Belgium), a full-function joint venture, by way of purchase of shares. PSA and TIL are hereafter referred to as the "Notifying Parties". PSA, TIL and PSA DGD are hereafter referred to as the "Parties" THE PARTIES AND THE CONCENTRATION (2) PSA is an operator of shipping terminals, ultimately controlled by Temasek Holdings, a Singaporean government fund. PSA is mainly active in the provision of stevedoring services at ports, with a particular focus on providing terminal services for containerised liner ships. Kranji is a holding company, controlled by PSA. PSA, through Kranji, controls four container terminals in the harbour of 1 OJ L 24, , p. 1 (the 'Merger Regulation'). With effect from 1 December 2009, the Treaty on the Functioning of the European Union ('TFEU') has introduced certain changes, such as the replacement of 'Community' by 'Union' and 'common market' by 'internal market'. The terminology of the TFEU will be used throughout this decision. 2 OJ L 1, , p. 3 (the 'EEA Agreement'). 3 Publication in the Official Journal of the European Union No C 212, , p. 23.

3 Antwerp: the PSA DGD Terminal, the Noordzee Terminal, the Europa Terminal and, jointly with ET, the MSC PSA European Terminal NV ( MPET ). (3) TIL is a terminal operating company indirectly jointly controlled by MSC Mediterranean Shipping Company Holding SA ( MSC Holding ) and certain financial investment vehicles managed by Global Infrastructure Management, LLC and relevant funds controlled by Global Infrastructure Partners ("GIP Funds"). TIL invests in, develops and manages container terminals around the world, often in joint ventures with other major terminal operators. ET is an indirectly wholly-owned subsidiary of TIL Holding, through which TIL Holding exercises joint control over MPET and through which TIL Holding also owns a non-controlling 49% stake in PSA DGD. (4) PSA DGD operates a container terminal in the Deurganck dock in the Port of Antwerp, in Belgium. It is a pre-existing company currently solely controlled by Kranji. (5) On 8 June 2017, Kranji (on behalf of PSA) and ET (on behalf of TIL) signed a Share Purchase Agreement, according to which ET will acquire 1% of the shares in PSA DGD from Kranji, thereby increasing its shareholding in PSA DGD from 49% to 50% (the "Transaction"). (6) As a consequence of this share transfer, ET and Kranji will post-transaction each hold 50% of the shares of PSA DGD. Shareholders' meetings (general annual, special and extraordinary) will require the minimum quorum of [...] per each party. In this way, neither Kranji nor ET will be able to reach the necessary quorum for the adoption of shareholder decisions in PSA DGD independently. PSA DGD s Board of Directors will comprise [...] Directors, [...] nominated by Kranji and [...] nominated by ET. All [...] Directors shall be appointed by ordinary resolution of the general shareholders meeting with simple majority. The Board decisions including strategic decisions such as the annual budget and the business plan shall require the vote of [...] Directors. On top of that, the deadlock resolution mechanism also demonstrates that Kranji and ET must reach a common understanding in determining the commercial policy including strategic decisions of PSA DGD and are required to cooperate. 4 (7) Thus, post-transaction, ET (that is, TIL) and Kranji (that is, PSA) will jointly control PSA DGD. (8) In light of the above, the Transaction constitutes a concentration within the meaning of Article 3(1)(b) of the Merger Regulation. (9) Furthermore, post-transaction, the Notifying Parties will undertake a number of internal restructuring steps, through which MPET, a 50%/50% joint venture between Kranji (PSA) and ET (TIL) operating another terminal in the harbour of Antwerp, will be absorbed by and merged with PSA DGD. However, this second step will not amount to a concentration pursuant to the Merger Regulation as it does not bring about any change in the quality of control of any of the undertakings involved. 4 If a deadlock situation arises at the Board level, [internal decision making mechanisms]. There is a similar procedure governing deadlock situations at shareholder level. 2

4 (10) The merged PSA DGD/MPET entity will be a full function joint venture. While MPET is and has been, since its inception, a non-full function joint venture, achieving more than [ 80%] of its terminal services throughput with its mother company MSC, PSA DGD has overall consistently achieved the vast majority of its business with third parties. The greatest part of that throughput was handled for Maersk, accounting for approximately [...]% of PSA DGD's throughput in the period The Notifying Parties intend that a significant portion of the throughput of the PSA DGD joint venture (including MPET) will be achieved with independent third party shipping lines, such as Maersk and others. The combined entity will thus become a hybrid terminal, handling MSC's cargo and third party cargo. The Notifying Parties intend that, after an initial ramp-up period, the projected throughput handled for third party shipping lines (other than MSC and WEC, one of MSC Holding's subsidiaries) will be in the order of [ 20%]. All terminal services for MSC and its affiliates will be at arm's length UNION DIMENSION (11) The undertakings concerned have a combined aggregate world-wide turnover of more than EUR million 6 [TIL: EUR [...]; PSA: EUR [...]; PSA DGD: EUR [...]. Each of at least two of them has an EU-wide turnover in excess of EUR 250 million [TIL: EUR [...]; PSA: EUR [...]], but they do not each achieve more than two-thirds of their aggregate EU-wide turnover within one and the same Member State. (12) The Transaction therefore has an EU dimension pursuant to Article 1(2) of the Merger Regulation. 3. MARKET DEFINITION (13) The present Transaction concerns two separate, vertically linked markets relating to the maritime sector, namely (i) the market for the provision of container terminal services; and (ii) the market for the provision of containerised liner shipping services Market for container terminal services Relevant product market (14) PSA DGD, the target, provides container terminal services to deep-sea container ships in the Port of Antwerp. (15) The Commission has consistently distinguished the provision of container terminal services to deep-sea container ships from the provision of container terminal services to vessels carrying non-containerised cargo (such as bulk, liquid 5 See answer to RFI 1, question 1. Market rates for terminal services provided to MSC seem credible also due to the shareholding structure, with two non-vertically integrated controlling shareholders, PSA and the GIP funds, which would have no incentive to offer MSC below market rates. 6 Turnover calculated in accordance with Article 5 of the Merger Regulation and the Commission Consolidated Jurisdictional Notice (OJ C 95, , p. 1). 3

5 bulk, etc.) and short sea vessels. 7 Since PSA DGD does not provide short-sea container terminal services nor container terminal services with respect to noncontainerised cargo, these market segments will not be analysed further. (16) As to provision of container terminal services for deep-sea container ships, the Commission has broken the market down further by traffic flows to i) hinterland traffic (that is, containers transported directly onto/from a deep-sea container vessel from/to the hinterland via barge, truck or train) and to ii) transhipment traffic (that is, containers destined for onward transportation to other ports). 8 (17) The Parties do not dispute the above mentioned market definitions Relevant geographic market (18) Regarding the geographic market definition, the Commission has previously considered that for container terminal services in deep sea ports, the relevant market is in essence determined by the geographic scope the container terminal generally serves (catchment area). For example, concerning Northern Europe and terminals in Hamburg in particular, the Commission considered that the relevant geographical dimension of stevedoring services is in its broadest scope Northern Europe (for transhipment traffic) and in its narrowest possible scope the catchment area of the ports in the range Hamburg Antwerp (for hinterland traffic) or possibly even narrower, comprising the German ports only. 9 (19) The Parties argue that the geographic market should not be narrower than regional and, for transhipment, should comprise all other terminals and ports in the Northern European range (including UK, Ireland, Scandinavia and the Baltic Sea) 10 and for hinterland traffic at least the Hamburg-Le Havre range, 11 because a national ports market definition would be artificial given the international nature of the container liner shipping business and the traffic flows, and would ignore the commercial, logistical and geographical reality. 12 (20) The market investigation results were inconclusive as to whether the market should be regional and at least include the Hamburg-Le Havre range for both 7 Cases COMP/JV.55 Hutchinson/RCPM/ECM, recital 25, M.5093 DP World/Conti7/Rickmers/DP World Breakbulk/JV, recital 13 8 Cases M.8120 Hapag-Lloyd/United Arab Shipping Company recital 21, M.7268 CSAV/HGV/Kühne Maritime/Hapag-Lloyd AG, recital 32; M.5398 Hutchison/Evergreen, recitals 9 11; M.3829 Maersk/PONL, recitals 17 19; M.3863 TUI/CP Ships, recital Cases M Hapag-Lloyd/United Arab Shipping Company, recital 22; M.5450 Kühne/HGV/TUI/Hapag-Lloyd, recital 16; M.5066 Eurogate/APMM, recitals See para 214 of Form CO. 11 According to the Parties, this range comprises the Ports of Le Havre, Dunkirk, Zeebrugge, Antwerp, Rotterdam, Amsterdam, Wilhelmshaven, Bremerhaven and Hamburg, See para.29 of the Form CO. Some market operators such as the Antwerp Port Authority also include Gent and Zeeland Seaports in this range. 12 For example, a geographic market limited only to the Belgian ports (Antwerp and Zeebrugge) would be implausibly narrow, as it would disregard that hinterland cargo can and is transported from Belgium to its neighbouring countries due to the quick, reliable and direct road, rail and barge connections eastwards (to the Netherlands and Germany) and westwards (France). This is also facilitated by the close proximity among the deep-sea ports in Northern Europe and the small size of Belgium and the Netherlands. 4

6 hinterland and transhipment traffic, as suggested by the Parties, or whether a market definition as narrow as the Port of Antwerp should be considered, as suggested by one competitor. 13 However, a majority of both customers and competitors considered at the very minimum the Port of Rotterdam a clear alternative to the Port of Antwerp for hinterland traffic. 14 For instance, according to the Independent Maritime Terminal, a container terminal operator in the port of Antwerp, the main competition comes from other ports and Rotterdam is the number one competitor to the Port of Antwerp. Furthermore, Hapag Lloyd, a global container shipping company, which is already present in both the port of Antwerp and Rotterdam, indicated that, in case of a price increase of 5-10% in terminal services by PSA DGD at the Port of Antwerp, it could envisage switching part of its shipment volumes to the Port of Rotterdam. As for the Port of Zeebrugge, the only other Belgian deep sea harbour, 15 it was one of the least preferred alternatives amongst the respondents to the market investigation, due to hinterland connection issues and (related) cost considerations, size-related capacity constraints, draught restrictions for large vessels and customer preference for Antwerp and Rotterdam. Zeebrugge was nevertheless considered to constitute a valid alternative for transhipments. 16 The market respondents did not deny that for transhipment the relevant geographic market would be at least Hamburg-Le Havre range Conclusion (21) On the basis of the Commission previous case practice and the market investigation, the relevant geographic market for hinterland traffic would at least comprise the ports of Antwerp and Rotterdam and probably the entire Hamburg- Le Havre range. Concerning transhipment, the relevant geographic market would comprise at the very least the Hamburg-Le Havre range. (22) However, it is not necessary to conclude on a precise definition of the relevant product and geographic market since the Transaction would not raise serious doubts as to its compatibility with the internal market under any of the plausible definitions of the markets for container terminal services Market for containerised liner shipping services Relevant product market (23) Container terminal services are "input services" to container liner shipping. (24) In past cases, the Commission has found that the product market for container liner shipping involves the provision of regular, scheduled services for the 13 See the Non-confidential Minutes of the call with DP World Antwerp Gateway, para See the Non-confidential Minutes of call with customer Hapag-Lloyd AG, paragraphs 6-7; Non- Confidential Minutes of call with competitor Independent Maritime Terminal, paragraph 12; Port of Antwerp, Presentation of 5 July 2017, slide The third largest harbour in Belgium, Gent, is only reachable via the Gent-Terneuzen-Canal which limits the size of vessels that can reach it to the Panamax-Class, i.e TEU. Gent is therefore, for the purpose of this decision, not considered further. 16 Non- Confidential Minutes of the call with competitor Independent Maritime Terminal, paragraph 12; Non-Confidential Minutes of the call with competitor DP World Antwerp Gateway, para 16. 5

7 carriage of cargo by container. This market can be distinguished from non-liner shipping (tramp, specialised transport) because of the regularity and frequency of the service. In addition, the use of container transportation should be distinguished from other non-containerised transport such as bulk cargo. 17 (25) This product market could be further segmented into the transport of refrigerated goods, which could be limited to refrigerated (reefer) containers only or could include transport in conventional reefer vessels. In past cases, the Commission has looked separately at reefer and non-refrigerated (warm) containers only in the case of legs of trade with a share of reefer containers in relation to all containerised cargo of 10% or more in both directions. 18 (26) The Notifying Parties consider that no sub-segmentation of the Northern European containerised liner shipping market into reefer container services is warranted, due to supply side considerations according to which all deep sea container terminals can and do handle both reefer and non-refrigerated cargo, using the same equipment. Moreover, the Notifying Parties argue that the containerised liner shipping market should be assessed only as a result of a vertical overlap between the Notifying Parties container terminal services and MSC s containerised liner shipping activities, which also renders subsegmentation inappropriate. However, the Parties have provided information also with regard to the reefer and non-reefer containers segmentation. (27) In any case, for the purpose of the Transaction, it may be left open whether the deep-sea container liner shipping market could be further segmented into markets for reefer and non-reefer containers as well as for reefer containers and reefer vessels since the competitive assessment of the effects of the Transaction on various markets would not be altered by any such possible segmentation Relevant geographic market (28) Whereas, in prior decisions, the Commission had left open whether the geographic scope should comprise trades, defined as the range of ports which are served at both ends of the service (e.g. Northern Europe North America) or each individual leg of trade (e.g. westbound and eastbound within a given trade), in its most recent practice 19, the Commission has concluded that container liner shipping services are geographically defined on the basis of the legs of trade (e.g. Northern Europe North America eastbound). 17 Cases M.8120 Hapag-Lloyd/United Arab Shipping Company, recital 10; M.7908 CMA CGM/NOL, recital 8; M.7268 CSAV/HGV/Kühne Maritime/Hapag-Lloyd AG, recital 16; M.5450 Kühne/HGV/TUI/Hapag-Lloyd, recital Cases M.8120 Hapag-Lloyd/United Arab Shipping Company, recital 11; M.7908 CMA CGM/NOL, recital 9; M.7268 CSAV/HGV/Kühne Maritime/Hapag-Lloyd AG, recital 18; M.3829 Maersk/PONL, recital 10. On trades with a share of reefer containers in relation to all containerised cargo below 10% of total capacity, the ships have in general more reefer facilities than actually used. Carriers will therefore be able to shift volume from the transport of warm containers to transport of reefer containers in the short term and without significant additional costs. 19 Case M.8120 Hapag-Lloyd/United Arab Shipping Company, recital 19. 6

8 (29) The relevant legs of trade for the assessment of the present Transaction based on the Commission's previous decisional practice are those from and to Northern Europe areas: Northern Europe Australia and New Zealand Northern Europe West Africa Northern Europe South Africa Northern Europe East Africa Northern Europe Caribbean and Central America Northern Europe Far East Northern Europe Indian Subcontinent Northern Europe Middle East Northern Europe North America Northern Europe South America East Coast Northern Europe South America West Coast (30) The Notifying Parties consider that the above trade sub-segmentation is irrelevant for the purposes of the present Transaction, given that the market for containerised liner shipping services is only concerned due to the vertical link to the upstream market for container services, on which the Parties' activities overlap. They have, however, provided information also on the basis of the above segmentation Conclusion (31) In any case, for the purpose of the Transaction, it may be left open whether markets shall be segmented into the above trades since the competitive assessment of the effects of the Transaction on various markets would not be altered by any such possible segmentation. 4. COMPETITIVE ASSESSMENT (32) The transaction gives rise to both a horizontal overlap and a vertical link between the Parties' activities. (33) The activities of TIL and PSA overlap with those of PSA DGD in the market for container terminal services in the Hamburg-Le Havre range. (34) PSA' container terminal activities in Northern Europe are confined to the harbour of Antwerp where it controls four container terminals: PSA DGD and MPET on the Left bank of the river Scheldt on the west and south-east side of the Deurganck dock; and the Noordzee and the Europa Terminals on the Right Bank, located in front of the Berendrecht lock PSA also operates two multipurpose terminals in the Hamburg-Le Havre range: the Churchill Terminal in the port of Antwerp, which is located behind the Berendrecht lock, and one terminal in the Port of Zeebrugge through its subsidiary, PSA Zeebrugge NV (formerly Zeebrugge International Port NV). Its activities there mainly involve general cargo handling, i.e., the handling of commodities such as wood pulp, iron and steel, forest products and other cargo and related Ro-Ro activity. Previously, it also conducted a limited amount of container handling, which ceased entirely in

9 (35) TIL controls four terminals in the Hamburg-Le Havre range: the Terminaux de Normandie MSC in Le Havre (France), the Delta MSC Terminal in Rotterdam (the Netherlands), the MSC Gate terminal in Bremerhaven (Germany), and jointly with PSA, MPET in the port of Antwerp under a sub-concession from PSA DGD. Neither MSC Holding nor GIP has any container terminal facilities in Northern Europe (including in the Hamburg-Le Havre range). In fact, other than their respective shareholdings in TIL Holdings, the GIP Funds have no activities in the container terminal services business in the EEA. (36) Consequently, both TIL and PSA overlap in the operation of container terminal services in the Hamburg-Le Havre range as well as in the Port of Antwerp. (37) Given that TIL is vertically integrated with a containerised liner shipping company (MSC), the Transaction also leads to a vertical link between the Parties' activities in the upstream i) market for container terminal services and the downstream ii) market for containerised liner shipping services Horizontal overlap market for container terminal services Description of the Parties' activities (38) The Transaction leads to a horizontally affected market for the provision of container terminal services (i.e. including hinterland and transhipment) in the Hamburg-Le Havre range. In 2016, the Parties had a combined market share 21 of [20-30%] (TIL: [20-30%]; PSA: [5-10%]; PSA DGD: [0-5%]). (39) With regard to hinterland traffic, on the basis of the narrowest geographic market definition including national ports only, i.e. Belgium (ports of Antwerp and Zeebrugge), the Parties' combined market share would be [40-50%] (TIL, solely via MPET: [20-30%]; PSA: [10-20%]; PSA DGD: [0-5%]). On the larger alternative market, that is, the Hamburg-Le Havre range, the Parties' combined market share would be [20-30%] (TIL [10-20%]; PSA [5-10%]; PSA DGD [0-5%]). (40) If, as some market respondents stated, Zeebrugge is not a valid option for hinterland traffic, the combined market share of the Parties in 2016 in the Port of Antwerp alone would have been [70-80%] (TIL: [30-40%], solely via MPET; PSA: [20-30%]; PSA DGD: [0-5%]). (41) On a geographic market that would include the ports of Antwerp and Rotterdam only, as some respondents stated, the Parties' combined market share would be [30-40%] (TIL: [20-30%]; PSA: [5-10%]; PSA DGD: [0-5%]). The combined market share would be lower for hinterland traffic, that is, [20-30%]. (42) On the narrowest plausible market for the provision of transhipment container services in the Hamburg-Le Havre range, in 2016, the Parties had a combined market share of [30-40%] (TIL: [20-30%], mainly via MPET; PSA: [0-5%]; PSA DGD: [0-5%]). The Parties' market shares are summarized in Table 1 below. 21 The Parties' market shares were calculated on the most conservative basis, i.e. on a non-equity allocated basis (taking into account the Parties' controlling stakes in full), including captive sales, and spare capacity and were calculated in TEUs, based on the Commission's decisional practice 8

10

11 container throughput than the Port of Antwerp 24, constitutes a valid alternative. 25 If the assessment is based on a larger, regional market including the Port of Rotterdam, the market share would go down to [30-40%], with an increment of [0-5%]. On a market comprising the entire Hamburg-Le Havre range, the combined market share of the parties would be [20-30%] with an increment of [0-5%]. (47) In the Hamburg-Le Havre range, there will remain numerous other credible competitors to the Parties, such as Hutchinson Port Holdings (in Rotterdam) with a [10-20%] market share, HHLA (in Hamburg) with a [10-20%] market share, Eurogate (Bremerhaven, Hamburg, Wilhelmshaven) with a [10-20%] market share and APM Terminals (in Bremerhaven, Wilhelmshaven, Rotterdam and Zeebrugge) with a [10-20%] market share. (48) Fourth, the customers of the terminal operators are global shipping companies such as Maersk, Hapag Lloyd, Hamburg Süd, OOCL, CMA CGM, bring in significant volumes which affords them significant bargaining power vis a vis the terminal operators and in particular in case of a threat of price increase. 26 The bargaining power of container liner companies has even increased since most of them are part of consortia and global alliances. In this respect there is a certain grouping in the Port of Antwerp. While the Ocean Alliance is using Antwerp Gateway as their main gateway, with two of its members, Cosco and CMA CGM having equity stakes in that terminal, THE Alliance uses the Noordzee/Europa terminals and 2M uses MPET and PSA DGD. (49) Fifth, given that MPET was until now a non-full function joint venture, realising more than [ 80%] of its turnover with one of its ultimate parent companies, MSC, its market presence and therefore market shares have been significantly overstated as they include captive sales. Therefore, MPET's market share is likely to be substantially lower if these captive sales are excluded. 27 (50) Lastly, the majority of the respondents to the market investigation confirmed that the Transaction will not change the competitive situation on the market for the provision of container terminal services Port of Antwerp presentation of 05/07/2017 at page 12 in 2016 the container throughput of the Port of Rotterdam was TEU, whereas the Port of Antwerp handled containers of TEU. 25 See the Non-confidential Minutes of the call with competitor Independent Maritime Terminal, para 12; Non-Confidential Minutes of the call with customer Hapag-Lloyd, para 6. Port of Antwerp, presentation of 5 July 2017, p See the Non-confidential Minutes with customer Hapag-Lloyd AG of , paragraph 13 and In the Commission's standard practice, captive volumes are taken out of the Commission's assessment, see, for instance, Case COMP/JV.55-Hutchison/RCP/ECT, paragraphs 44 and See for instance. the Non- Confidential Minutes with competitor Independent Maritime Terminal, paragraph 13; Non-confidential Minutes with customer Hapag-Lloyd AG of , paragraph

12 4.2. Vertical link market for container terminal services (upstream); market for containerised liner shipping services (downstream) Description of the Parties' activities (51) TIL is vertically integrated with MSC, a containerised liner shipping company. The transaction will therefore create a vertical link between the Parties' activities in the market for container terminal services and the market for containerised liner shipping services. (52) When looking at container liner shipping as a whole (that is, without splitting between the transport of reefer and non-reefer goods), the following affected markets arise: Northern Europe- South Africa (southbound) where MSC accounts for [40-50%] and the market share rises to [50-60%] when its consortia partners are taken into account; Northern Europe-Indian Subcontinent where MSC accounts for [30-40%] on the eastbound leg and the market share rises to [40-50%] when its consortia partners are taken into account. For the westbound leg, an affected market only arises when MSC's consortia partners are taken into account leading to [40-50%] market share (from [20-30%] for MSC only). Similarly for both legs of the Northern Europe-North America trade, where an affected market arises only when consortia partners are taken into account leading to [50-60%] and [50-60%] market share for the westbound and eastbound leg respectively (from, respectively, [20-30%] and [20-30%] market share for MSC only). (53) Under the narrowest plausible market definition of the vertically linked market for containerised liner shipping services in reefer (refrigerated cargo), the Transaction will lead to vertically affected markets for the Northern Europe-South Africa trade (northbound only) and for both legs of the Northern Europe-South America East Coast Trade. More specifically, for the South Africa-Northern Europe leg of trade, MSC would account for [30-40%] and the market share would rise to [30-40%] when consortia partners are taken into account. For the southbound leg of the Northern Europe to South America East Coast trade, MSC would only account for [20-30%]. However, when consortia partners are taken into account, the market share would reach [90-100%]. For the northbound leg of this trade, MSC would only account for [10-20%]; if consortia partners are taken into account, then the market share would reach [80-90%] Commission's assessment (54) The Commission considers that the Transaction will not lead to any foreclosure of either competing container liner shipping companies or terminal operators. In particular, it seems highly unlikely that the resulting vertically affected markets for containerised liner shipping services will lead to foreclosure of competing container liner shipping companies, despite MSC and its consortia partners' high market shares on certain trades to and from Northern Europe. (55) First, the vertical link between legs of trades and container terminal services based on the established geographic market definitions does not reflect business reality, as no terminal, let alone a harbour relevant is specific to any individual trade in this Transaction. Every terminal serves vessels sailing on a variety of trades. The relevant end of trade in this Transaction, Northern Europe, encompasses the full range of harbours from the Atlantic coast of the Iberian Peninsula to the Baltic Sea. Any high market share of MSC, including its 11

13 consortia partners as the case may be, on an affected leg of trade does not mean that it can foreclose the remaining container liner shipping companies active on that trade because it has also a substantial market share in the market for terminal services in a given harbour, here the Port of Antwerp. Instead, competing container liner shipping companies serving Northern Europe as one relevant end of a trade could procure port terminal services from several alternative providers in the Hamburg-Le Havre range, in particular from terminals in the Port of Rotterdam, the closest competitor of the Port of Antwerp, and to some extent the Port of Zeebrugge. 29 Competing terminal providers in the Hamburg-Le Havre range include Hutchison Port Holdings ( HPH ) with a total throughput in the Hamburg-Le Havre range of [10-20%], Eurogate with a total throughput of [10-20%] and APMT, a subsidiary of Maersk with a total throughput of [10-20%]. (56) Second, even in the Port of Antwerp four container terminals remain which are not controlled by vertically integrated MSC. Other than the Noordzee Terminal and the Europa Terminal, both solely controlled by PSA, there is the Antwerp Gateway terminal, operated by Antwerp Gateway NV, and the Independent Maritime Terminal (IMT) operated by Sea-Invest. Antwerp Gateway is a large terminal, currently operating close to its full capacity of approximately [ ] TEU million TEUs (including barges). IMT is a smaller terminal behind the locks which limits the size of container vessels to about [ ] TEU, which has spare capacity. 30 Given that PSA DGD is a very small terminal with a nominal capacity of [...] TEU and a throughput of only [...] TEU in 2016 is coming under MSC's control. (57) Furthermore, the Port of Antwerp has already started an expansion project, the Saeftinghe terminal project, which foresees the building of a new dock just north of Deurganckdok which would add a capacity of 6 to 7 million TEU. This new dock would be able to accommodate mega vessels of 18,000 TEUs. However, this expansion project is in its very early stages and will not be completed in the near future. Other ports in the region, including Rotterdam, also have expansion plans, which according to Dynamar 31, would increase container terminal capacity in Northern Europe from 86 million TEUs as of the end of 2014 to nearly 143 million TEUs by the end of (58) Third, there is no risk that the merged entity will stop providing port terminal services to competing liner shipping companies in Antwerp, as this would run counter to PSA s financial objectives. The Notifying Parties intend that a significant portion of PSA DGD s throughput (including MPET s, following the internal restructuring) amounting to [ 20%] of the throughput will be achieved with third-party shipping lines. Moreover, GIP Funds, the other shareholder in TIL, is an institutional investor, with no activities in the container liner terminal services business in the EEA. GIP Funds is keen to defend its financial interests to ensure profit returns and would not have an incentive to block access of MSC's 29 See, for instance, the Non- Confidential Minutes of the call with competitor Independent Maritime Terminal, paragraph 12; Non-confidential Minutes of the call with customer Hapag-Lloyd AG, paragraph See the Non- Confidential Minutes of the call with competitor Independent Maritime Terminal, paragraph See Container Throughput & Terminal Capacity in North Europe II, April 2015, Dynamar B.V (p. 18), (Annex 7.4.c. to the Form CO). 12

14 rivals or to give preferential treatment to MSC, but would insist on arm's length dealings. (59) Regarding any customer foreclosure strategy, namely foreclosing competing terminal operators' access to container liner shipping companies as customers, in this case to MSC and its 2M alliance partner Maersk, this can also be excluded as already pre-merger these two companies [ ] as a result of this Transaction Conclusion (60) In light of the above considerations, the Commission concludes that the Transaction does not raise serious doubts as to its compatibility with the internal market as a result of input or customer foreclosure on the market for container terminal services. 5. CONCLUSION (61) For the above reasons, the Commission has decided not to oppose the notified operation and to declare it compatible with the internal market and with the EEA Agreement. This decision is adopted in application of Article 6(1)(b) of the Merger Regulation and Article 57 of the EEA Agreement. For the Commission (signed) Julian KING Member of the Commission 13

Case No COMP/M ASTRIUM HOLDING/ VIZADA GROUP. REGULATION (EC) No 139/2004 MERGER PROCEDURE. Article 6(1)(b) NON-OPPOSITION Date: 30/11/2011

No 139/2004 MERGER PROCEDURE. Article 6(1)(b) NON-OPPOSITION Date: 30/11/2011") EN Case No COMP/M.6393 - ASTRIUM HOLDING/ VIZADA GROUP Only the English text is available and authentic. REGULATION (EC) No 139/2004 MERGER PROCEDURE Article 6(1)(b) NON-OPPOSITION Date: 30/11/2011 In

EN Case No COMP/M.6393 - ASTRIUM HOLDING/ VIZADA GROUP Only the English text is available and authentic. REGULATION (EC) No 139/2004 MERGER PROCEDURE Article 6(1)(b) NON-OPPOSITION Date: 30/11/2011 In

Case No M MITSUBISHI HEAVY INDUSTRIES / SIEMENS / METAL TECHNOLOGIES JV

EN Case No M.7330 - MITSUBISHI HEAVY INDUSTRIES / SIEMENS / METAL TECHNOLOGIES JV Only the English text is available and authentic. REGULATION (EC) No 139/2004 MERGER PROCEDURE Article 6(1)(b) NON-OPPOSITION

EN Case No M.7330 - MITSUBISHI HEAVY INDUSTRIES / SIEMENS / METAL TECHNOLOGIES JV Only the English text is available and authentic. REGULATION (EC) No 139/2004 MERGER PROCEDURE Article 6(1)(b) NON-OPPOSITION

Case No COMP/M TNT FORWARDING HOLDING / WILSON LOGISTICS. REGULATION (EEC) No 139/2004 MERGER PROCEDURE

No 139/2004 MERGER PROCEDURE") EN Case No COMP/M.3496 - TNT FORWARDING HOLDING / WILSON LOGISTICS Only the English text is available and authentic. REGULATION (EEC) No 139/2004 MERGER PROCEDURE Article 6(1)(b) NON-OPPOSITION Date: 02/08/2004

EN Case No COMP/M.3496 - TNT FORWARDING HOLDING / WILSON LOGISTICS Only the English text is available and authentic. REGULATION (EEC) No 139/2004 MERGER PROCEDURE Article 6(1)(b) NON-OPPOSITION Date: 02/08/2004

Case No COMP/M CVC / DSI. REGULATION (EC) No 139/2004 MERGER PROCEDURE. Article 6(1)(b) NON-OPPOSITION Date: 25/09/2007

No 139/2004 MERGER PROCEDURE. Article 6(1)(b) NON-OPPOSITION Date: 25/09/2007") EN Case No COMP/M.4850 - CVC / DSI Only the English text is available and authentic. REGULATION (EC) No 139/2004 MERGER PROCEDURE Article 6(1)(b) NON-OPPOSITION Date: 25/09/2007 In electronic form on the

EN Case No COMP/M.4850 - CVC / DSI Only the English text is available and authentic. REGULATION (EC) No 139/2004 MERGER PROCEDURE Article 6(1)(b) NON-OPPOSITION Date: 25/09/2007 In electronic form on the

Case No COMP/M SHELL / BEB. REGULATION (EEC) No 4064/89 MERGER PROCEDURE. Article 6(1)(b) NON-OPPOSITION Date: 20/11/2003

No 4064/89 MERGER PROCEDURE. Article 6(1)(b) NON-OPPOSITION Date: 20/11/2003") EN Case No COMP/M.3293 - SHELL / BEB Only the English text is available and authentic. REGULATION (EEC) No 4064/89 MERGER PROCEDURE Article 6(1)(b) NON-OPPOSITION Date: 20/11/2003 Also available in the

EN Case No COMP/M.3293 - SHELL / BEB Only the English text is available and authentic. REGULATION (EEC) No 4064/89 MERGER PROCEDURE Article 6(1)(b) NON-OPPOSITION Date: 20/11/2003 Also available in the

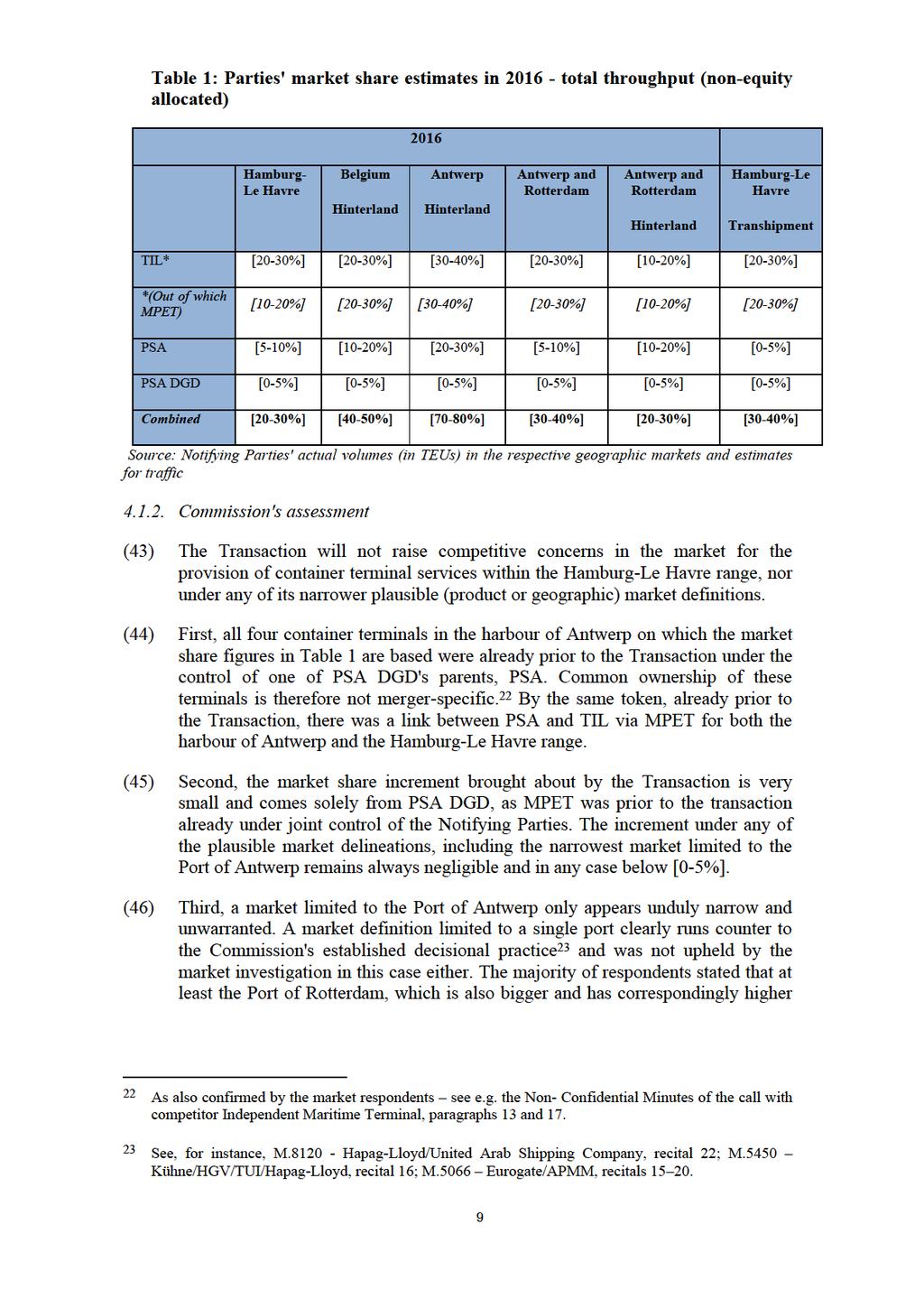

PORT COOPERATION BETWEEN EUROPEAN SEAPORTS FUNDAMENTALS, CHALLENGES AND GOOD PRACTICES

PORT COOPERATION BETWEEN EUROPEAN SEAPORTS FUNDAMENTALS, CHALLENGES AND GOOD PRACTICES Presentation of the study carried out on behalf of the GUE/NGL in the European Parliament, 19th October 2016, Brussels

PORT COOPERATION BETWEEN EUROPEAN SEAPORTS FUNDAMENTALS, CHALLENGES AND GOOD PRACTICES Presentation of the study carried out on behalf of the GUE/NGL in the European Parliament, 19th October 2016, Brussels

Case No COMP/M S&B / HALLIBURTON / CEBO JV. REGULATION (EC) No 139/2004 MERGER PROCEDURE. Article 6(1)(b) NON-OPPOSITION Date: 18/04/2007

No 139/2004 MERGER PROCEDURE. Article 6(1)(b) NON-OPPOSITION Date: 18/04/2007") EN Case No COMP/M.4562 - S&B / HALLIBURTON / CEBO JV Only the English text is available and authentic. REGULATION (EC) No 139/2004 MERGER PROCEDURE Article 6(1)(b) NON-OPPOSITION Date: 18/04/2007 In electronic

EN Case No COMP/M.4562 - S&B / HALLIBURTON / CEBO JV Only the English text is available and authentic. REGULATION (EC) No 139/2004 MERGER PROCEDURE Article 6(1)(b) NON-OPPOSITION Date: 18/04/2007 In electronic

Case No COMP/M G SPECIAL SITUATIONS FUND III/ BERKSHIRE HATHAWAY/ H J HEINZ COMPANY. REGULATION (EC) No 139/2004 MERGER PROCEDURE

No 139/2004 MERGER PROCEDURE") EN Case No COMP/M.6895-3G SPECIAL SITUATIONS FUND III/ BERKSHIRE HATHAWAY/ H J HEINZ COMPANY Only the English text is available and authentic. REGULATION (EC) No 139/2004 MERGER PROCEDURE Article 6(1)(b)

EN Case No COMP/M.6895-3G SPECIAL SITUATIONS FUND III/ BERKSHIRE HATHAWAY/ H J HEINZ COMPANY Only the English text is available and authentic. REGULATION (EC) No 139/2004 MERGER PROCEDURE Article 6(1)(b)

Case No IV/M HAVAS ADVERTISING / MEDIA PLANNING. REGULATION (EEC) No 4064/89 MERGER PROCEDURE. Article 6(1)(b) NON-OPPOSITION Date: 10/06/1999

No 4064/89 MERGER PROCEDURE. Article 6(1)(b) NON-OPPOSITION Date: 10/06/1999") EN Case No IV/M.1529 - HAVAS ADVERTISING / MEDIA PLANNING Only the English text is available and authentic. REGULATION (EEC) No 4064/89 MERGER PROCEDURE Article 6(1)(b) NON-OPPOSITION Date: 10/06/1999

EN Case No IV/M.1529 - HAVAS ADVERTISING / MEDIA PLANNING Only the English text is available and authentic. REGULATION (EEC) No 4064/89 MERGER PROCEDURE Article 6(1)(b) NON-OPPOSITION Date: 10/06/1999

Case No COMP/M PAI / CHR. HANSEN. REGULATION (EC) No 139/2004 MERGER PROCEDURE. Article 6(1)(b) NON-OPPOSITION Date: 18/07/2005

No 139/2004 MERGER PROCEDURE. Article 6(1)(b) NON-OPPOSITION Date: 18/07/2005") EN Case No COMP/M.3845 - PAI / CHR. HANSEN Only the English text is available and authentic. REGULATION (EC) No 139/2004 MERGER PROCEDURE Article 6(1)(b) NON-OPPOSITION Date: 18/07/2005 In electronic form

EN Case No COMP/M.3845 - PAI / CHR. HANSEN Only the English text is available and authentic. REGULATION (EC) No 139/2004 MERGER PROCEDURE Article 6(1)(b) NON-OPPOSITION Date: 18/07/2005 In electronic form

Case No COMP/M AVNET/ BELL MICRO. REGULATION (EC) No 139/2004 MERGER PROCEDURE. Article 6(1)(b) NON-OPPOSITION Date: 02/07/2010

No 139/2004 MERGER PROCEDURE. Article 6(1)(b) NON-OPPOSITION Date: 02/07/2010") EN Case No COMP/M.5864 - AVNET/ BELL MICRO Only the English text is available and authentic. REGULATION (EC) No 139/2004 MERGER PROCEDURE Article 6(1)(b) NON-OPPOSITION Date: 02/07/2010 In electronic form

EN Case No COMP/M.5864 - AVNET/ BELL MICRO Only the English text is available and authentic. REGULATION (EC) No 139/2004 MERGER PROCEDURE Article 6(1)(b) NON-OPPOSITION Date: 02/07/2010 In electronic form

Case No COMP/M OTTO VERSAND / SABRE / TRAVELOCITY JV. REGULATION (EEC) No 4064/89 MERGER PROCEDURE

No 4064/89 MERGER PROCEDURE") EN Case No COMP/M.2627 - OTTO VERSAND / SABRE / TRAVELOCITY JV Only the English text is available and authentic. REGULATION (EEC) No 4064/89 MERGER PROCEDURE Article 6(1)(b) NON-OPPOSITION Date: 19/12/2001

EN Case No COMP/M.2627 - OTTO VERSAND / SABRE / TRAVELOCITY JV Only the English text is available and authentic. REGULATION (EEC) No 4064/89 MERGER PROCEDURE Article 6(1)(b) NON-OPPOSITION Date: 19/12/2001

Case No COMP/M WPP / CORDIANT. REGULATION (EEC) No 4064/89 MERGER PROCEDURE. Article 6(1)(b) NON-OPPOSITION Date: 25/07/2003

No 4064/89 MERGER PROCEDURE. Article 6(1)(b) NON-OPPOSITION Date: 25/07/2003") EN Case No COMP/M.3209 - WPP / CORDIANT Only the English text is available and authentic. REGULATION (EEC) No 4064/89 MERGER PROCEDURE Article 6(1)(b) NON-OPPOSITION Date: 25/07/2003 Also available in

EN Case No COMP/M.3209 - WPP / CORDIANT Only the English text is available and authentic. REGULATION (EEC) No 4064/89 MERGER PROCEDURE Article 6(1)(b) NON-OPPOSITION Date: 25/07/2003 Also available in

Case No IV/M DAIMLER - BENZ / CHRYSLER. REGULATION (EEC) No 4064/89 MERGER PROCEDURE. Article 6(1)(b) NON-OPPOSITION Date: 22/07/1998

No 4064/89 MERGER PROCEDURE. Article 6(1)(b) NON-OPPOSITION Date: 22/07/1998") EN Case No IV/M.1204 - DAIMLER - BENZ / CHRYSLER Only the English text is available and authentic. REGULATION (EEC) No 4064/89 MERGER PROCEDURE Article 6(1)(b) NON-OPPOSITION Date: 22/07/1998 Also available

EN Case No IV/M.1204 - DAIMLER - BENZ / CHRYSLER Only the English text is available and authentic. REGULATION (EEC) No 4064/89 MERGER PROCEDURE Article 6(1)(b) NON-OPPOSITION Date: 22/07/1998 Also available

Case No COMP/M EDP / HIDROELECTRICA DEL CANTABRICO. REGULATION (EC) No 139/2004 MERGER PROCEDURE

No 139/2004 MERGER PROCEDURE") EN Case No COMP/M.3448 - EDP / HIDROELECTRICA DEL CANTABRICO Only the English text is available and authentic. REGULATION (EC) No 139/2004 MERGER PROCEDURE Article 6(1)(b) NON-OPPOSITION Date: 09/09/2004

EN Case No COMP/M.3448 - EDP / HIDROELECTRICA DEL CANTABRICO Only the English text is available and authentic. REGULATION (EC) No 139/2004 MERGER PROCEDURE Article 6(1)(b) NON-OPPOSITION Date: 09/09/2004

Case No COMP/M GOLDMAN SACHS / CINVEN / AHLSELL. REGULATION (EC) No 139/2004 MERGER PROCEDURE. Article 6(1)(b) NON-OPPOSITION Date: 06/01/2006

No 139/2004 MERGER PROCEDURE. Article 6(1)(b) NON-OPPOSITION Date: 06/01/2006") EN Case No COMP/M.4050 - GOLDMAN SACHS / CINVEN / AHLSELL Only the English text is available and authentic. REGULATION (EC) No 139/2004 MERGER PROCEDURE Article 6(1)(b) NON-OPPOSITION Date: 06/01/2006

EN Case No COMP/M.4050 - GOLDMAN SACHS / CINVEN / AHLSELL Only the English text is available and authentic. REGULATION (EC) No 139/2004 MERGER PROCEDURE Article 6(1)(b) NON-OPPOSITION Date: 06/01/2006

Case No IV/M VIVENDI / US FILTERS. REGULATION (EEC) No 4064/89 MERGER PROCEDURE. Article 6(1)(b) NON-OPPOSITION Date: 29/04/1999

No 4064/89 MERGER PROCEDURE. Article 6(1)(b) NON-OPPOSITION Date: 29/04/1999") EN Case No IV/M.1514 - VIVENDI / US FILTERS Only the English text is available and authentic. REGULATION (EEC) No 4064/89 MERGER PROCEDURE Article 6(1)(b) NON-OPPOSITION Date: 29/04/1999 Also available

EN Case No IV/M.1514 - VIVENDI / US FILTERS Only the English text is available and authentic. REGULATION (EEC) No 4064/89 MERGER PROCEDURE Article 6(1)(b) NON-OPPOSITION Date: 29/04/1999 Also available

Case No COMP/M BUNGE / CEREOL. REGULATION (EEC) No 4064/89 MERGER PROCEDURE. Article 6(1)(b) NON-OPPOSITION Date: 20/09/2002

No 4064/89 MERGER PROCEDURE. Article 6(1)(b) NON-OPPOSITION Date: 20/09/2002") EN Case No COMP/M.2886 - BUNGE / CEREOL Only the English text is available and authentic. REGULATION (EEC) No 4064/89 MERGER PROCEDURE Article 6(1)(b) NON-OPPOSITION Date: 20/09/2002 Also available in

EN Case No COMP/M.2886 - BUNGE / CEREOL Only the English text is available and authentic. REGULATION (EEC) No 4064/89 MERGER PROCEDURE Article 6(1)(b) NON-OPPOSITION Date: 20/09/2002 Also available in

&DVH 1R,90 '(876&+( 3267 $6* 5(*8/$7,21((&1R 0(5*(5352&('85( Article 6(1)(b) NON-OPPOSITION Date: 08/07/1999

(b) NON-OPPOSITION Date: 08/07/1999") EN &DVH 1R,90 '(876&+( 3267 $6* Only the English text is available and authentic. 5(*8/$7,21((&1R 0(5*(5352&('85( Article 6(1)(b) NON-OPPOSITION Date: 08/07/1999 $OVRDYDLODEOHLQWKH&(/(;GDWDEDVH 'RFXPHQW1R0

EN &DVH 1R,90 '(876&+( 3267 $6* Only the English text is available and authentic. 5(*8/$7,21((&1R 0(5*(5352&('85( Article 6(1)(b) NON-OPPOSITION Date: 08/07/1999 $OVRDYDLODEOHLQWKH&(/(;GDWDEDVH 'RFXPHQW1R0

Case M SYSCO / BRAKES

EUROPEAN COMMISSION DG Competition Case M.7986 - SYSCO / BRAKES Only the English text is available and authentic. REGULATION (EC) No 139/2004 MERGER PROCEDURE Article 6(1)(b) NON-OPPOSITION Date: 09/06/2016

EUROPEAN COMMISSION DG Competition Case M.7986 - SYSCO / BRAKES Only the English text is available and authentic. REGULATION (EC) No 139/2004 MERGER PROCEDURE Article 6(1)(b) NON-OPPOSITION Date: 09/06/2016

Case No COMP/M COMPAGNIE DE SAINT-GOBAIN / RAAB KARCHER. REGULATION (EEC) No 4064/89 MERGER PROCEDURE

No 4064/89 MERGER PROCEDURE") EN Case No COMP/M.1974 - COMPAGNIE DE SAINT-GOBAIN / RAAB KARCHER Only the English text is available and authentic. REGULATION (EEC) No 4064/89 MERGER PROCEDURE Article 6(1)(b) NON-OPPOSITION Date: 22/06/2000

EN Case No COMP/M.1974 - COMPAGNIE DE SAINT-GOBAIN / RAAB KARCHER Only the English text is available and authentic. REGULATION (EEC) No 4064/89 MERGER PROCEDURE Article 6(1)(b) NON-OPPOSITION Date: 22/06/2000

Containing. the future

Containing the future Antwerp, the fastest route to Europe Of the 190 million tonnes handled at the Port of Antwerp in 2008, some 100 million tonnes was containerized cargo, representing 8.7 million TEU.

Containing the future Antwerp, the fastest route to Europe Of the 190 million tonnes handled at the Port of Antwerp in 2008, some 100 million tonnes was containerized cargo, representing 8.7 million TEU.

Cool Logistics Asia. Lars Kastrup, Senior Vice President - Asia, CMA CGM September 2, 2015

Cool Logistics Asia Lars Kastrup, Senior Vice President - Asia, CMA CGM September 2, 2015 CMA CGM, a Leader in Container Shipping Led by its founder, Mr Jacques R. Saadé, CMA CGM is a leading worldwide

Cool Logistics Asia Lars Kastrup, Senior Vice President - Asia, CMA CGM September 2, 2015 CMA CGM, a Leader in Container Shipping Led by its founder, Mr Jacques R. Saadé, CMA CGM is a leading worldwide

Case No COMP/M ALCOA / BRITISH ALUMINIUM. REGULATION (EEC) No 4064/89 MERGER PROCEDURE. Article 6(1)(b) NON-OPPOSITION Date: 27/10/2000

No 4064/89 MERGER PROCEDURE. Article 6(1)(b) NON-OPPOSITION Date: 27/10/2000") EN Case No COMP/M.2111 - ALCOA / BRITISH ALUMINIUM Only the English text is available and authentic. REGULATION (EEC) No 4064/89 MERGER PROCEDURE Article 6(1)(b) NON-OPPOSITION Date: 27/10/2000 Also available

EN Case No COMP/M.2111 - ALCOA / BRITISH ALUMINIUM Only the English text is available and authentic. REGULATION (EEC) No 4064/89 MERGER PROCEDURE Article 6(1)(b) NON-OPPOSITION Date: 27/10/2000 Also available

Theo Notteboom ITMMA - University of Antwerp and Antwerp Maritime Academy

THE RELATIONSHIP BETWEEN SEAPORTS AND THE INTERMODAL HINTERLAND IN LIGHT OF GLOBAL SUPPLY CHAINS: EUROPEAN CHALLENGES Theo Notteboom ITMMA - University of Antwerp and Antwerp Maritime Academy Research

THE RELATIONSHIP BETWEEN SEAPORTS AND THE INTERMODAL HINTERLAND IN LIGHT OF GLOBAL SUPPLY CHAINS: EUROPEAN CHALLENGES Theo Notteboom ITMMA - University of Antwerp and Antwerp Maritime Academy Research

Container Shipping Services and their Impact on Container Port Competitiveness

Container Shipping Services and their Impact on Container Port Competitiveness Proefschrift voorgedragen tot het behalen van de graad van Doctor in Transport en Maritieme Economie op 3 november 2009 om

Container Shipping Services and their Impact on Container Port Competitiveness Proefschrift voorgedragen tot het behalen van de graad van Doctor in Transport en Maritieme Economie op 3 november 2009 om

USA Trade: Export BAF Notices

USA Trade: Export BAF Notices Shipping Line Current BAF NEW BAF ANL USD824 per TEU to West Coast USA USD931 per TEU to East Coast USA USD820 per TEU effective 01 Dec CMA-CGM USD931 per TEU to East Coast

USA Trade: Export BAF Notices Shipping Line Current BAF NEW BAF ANL USD824 per TEU to West Coast USA USD931 per TEU to East Coast USA USD820 per TEU effective 01 Dec CMA-CGM USD931 per TEU to East Coast

Port of Antwerp A Reliable Link in your Supply Chain

Port of Antwerp A Reliable Link in your Supply Chain 19 March 2013 Chris Hoornaert Port Ambassador Movie 2 Overview 1. Port of Antwerp in figures 2. A multifunctional port in the heart of Europe 3. Excellent

Port of Antwerp A Reliable Link in your Supply Chain 19 March 2013 Chris Hoornaert Port Ambassador Movie 2 Overview 1. Port of Antwerp in figures 2. A multifunctional port in the heart of Europe 3. Excellent

Case No COMP/M HONEYWELL/ INTERMEC. REGULATION (EC) No 139/2004 MERGER PROCEDURE. Article 6(1)(b) NON-OPPOSITION Date: 13/06/2013

No 139/2004 MERGER PROCEDURE. Article 6(1)(b) NON-OPPOSITION Date: 13/06/2013") EN Case No COMP/M.6827 - HONEYWELL/ INTERMEC Only the English text is available and authentic. REGULATION (EC) No 139/2004 MERGER PROCEDURE Article 6(1)(b) NON-OPPOSITION Date: 13/06/2013 In electronic

EN Case No COMP/M.6827 - HONEYWELL/ INTERMEC Only the English text is available and authentic. REGULATION (EC) No 139/2004 MERGER PROCEDURE Article 6(1)(b) NON-OPPOSITION Date: 13/06/2013 In electronic

Case No COMP/M UNIVERSAL STUDIO NETWORKS / DE FACTO 829 (NTL) / STUDIO CHANNEL LIMITED. REGULATION (EEC) No 4064/89 MERGER PROCEDURE

/ STUDIO CHANNEL LIMITED. REGULATION (EEC) No 4064/89 MERGER PROCEDURE") EN Case No COMP/M.2211 - UNIVERSAL STUDIO NETWORKS / DE FACTO 829 (NTL) / STUDIO CHANNEL LIMITED Only the English text is available and authentic. REGULATION (EEC) No 4064/89 MERGER PROCEDURE Article 6(1)(b)

EN Case No COMP/M.2211 - UNIVERSAL STUDIO NETWORKS / DE FACTO 829 (NTL) / STUDIO CHANNEL LIMITED Only the English text is available and authentic. REGULATION (EEC) No 4064/89 MERGER PROCEDURE Article 6(1)(b)

International Port Holdings

JOINT PRESS RELEASE International Port Holdings 28 January 2008 PSA INTERNATIONAL & INTERNATIONAL PORT HOLDINGS, A WHOLLY-OWNED SUBSIDIARY OF GLOBAL INFRASTRUCTURE PARTNERS, AND ROMAN GROUP ANNOUNCE A

JOINT PRESS RELEASE International Port Holdings 28 January 2008 PSA INTERNATIONAL & INTERNATIONAL PORT HOLDINGS, A WHOLLY-OWNED SUBSIDIARY OF GLOBAL INFRASTRUCTURE PARTNERS, AND ROMAN GROUP ANNOUNCE A

Global Ports and Urban Development: Creative use of space

Global Ports and Urban Development: Creative use of space Jan Egbertsen Port of Amsterdam Paris, OECD Headquarters, December 9, 2011 Port of Amsterdam is a company of the city of Amsterdam Port of Amsterdam,

Global Ports and Urban Development: Creative use of space Jan Egbertsen Port of Amsterdam Paris, OECD Headquarters, December 9, 2011 Port of Amsterdam is a company of the city of Amsterdam Port of Amsterdam,

Coping with port competition in Europe: a state

Coping with port competition in Europe: a state of the art H. Meersman & E. Van de Voorde Faculty ofapplied Economics, University ofantwerp (UFSIA) Prinsstraat 13, 2000 Antwerpen, Belgium EMail: hilde.

Coping with port competition in Europe: a state of the art H. Meersman & E. Van de Voorde Faculty ofapplied Economics, University ofantwerp (UFSIA) Prinsstraat 13, 2000 Antwerpen, Belgium EMail: hilde.

ANNEX XIV COMPETITION

27.10.2017 - EEA AGREEMENT - ANNEX XIV p. 1 ANNEX XIV COMPETITION TABLE OF CONTENTS A. Merger Control B. Vertical Agreements and Concerted Practices C. Technology Transfer Agreements D. Specialization

27.10.2017 - EEA AGREEMENT - ANNEX XIV p. 1 ANNEX XIV COMPETITION TABLE OF CONTENTS A. Merger Control B. Vertical Agreements and Concerted Practices C. Technology Transfer Agreements D. Specialization

Case No COMP/M SECOP/ ACC AUSTRIA. REGULATION (EC) No 139/2004 MERGER PROCEDURE. Article 6(1)(b) NON-OPPOSITION Date: 11/12/2013

No 139/2004 MERGER PROCEDURE. Article 6(1)(b) NON-OPPOSITION Date: 11/12/2013") EN Case No COMP/M.6996 - SECOP/ ACC AUSTRIA Only the English text is available and authentic. REGULATION (EC) No 139/2004 MERGER PROCEDURE Article 6(1)(b) NON-OPPOSITION Date: 11/12/2013 In electronic

EN Case No COMP/M.6996 - SECOP/ ACC AUSTRIA Only the English text is available and authentic. REGULATION (EC) No 139/2004 MERGER PROCEDURE Article 6(1)(b) NON-OPPOSITION Date: 11/12/2013 In electronic

HAMBURGER HAFEN UND LOGISTIK AG COMPANY PRESENTATION

HAMBURGER HAFEN UND LOGISTIK AG COMPANY PRESENTATION UniCredit German Investment Conference Munich, 28 September 2011 Hamburger Hafen und Logistik AG DISCLAIMER The facts and information contained herein

HAMBURGER HAFEN UND LOGISTIK AG COMPANY PRESENTATION UniCredit German Investment Conference Munich, 28 September 2011 Hamburger Hafen und Logistik AG DISCLAIMER The facts and information contained herein

STATISTICS REPORT GERMANY

A project within the Interreg IIIB North Sea Programme STATISTICS REPORT GERMANY Unitised Goods Flows via Ports in Germany Annex 1.3.3.5 to the Final Report February 2007 PREFACE This technical paper including

A project within the Interreg IIIB North Sea Programme STATISTICS REPORT GERMANY Unitised Goods Flows via Ports in Germany Annex 1.3.3.5 to the Final Report February 2007 PREFACE This technical paper including

Ports SAILING AHEAD R. Nagesh. SAILING AILING AHEAD

Ports SAILING APM Terminals, one of the AHEAD world s largest operators of port terminals, has ambitious expansion plans in India. The company, which operates two facilities in the country, saw business

Ports SAILING APM Terminals, one of the AHEAD world s largest operators of port terminals, has ambitious expansion plans in India. The company, which operates two facilities in the country, saw business

Control test under the EU Merger Regulation

EU China Trade Project (II) Workshop on DG Competition Procedures Beijing, 7 June 2011 Control test under the EU Merger Regulation JM. Carpi Badia Case Manager, Mergers (E.4) DG Competition, European Commission

EU China Trade Project (II) Workshop on DG Competition Procedures Beijing, 7 June 2011 Control test under the EU Merger Regulation JM. Carpi Badia Case Manager, Mergers (E.4) DG Competition, European Commission

DIRECTIVE 2012/34/EU OF THE EUROPEAN PARLIAMENT AND OF THE COUNCIL of 21 November 2012 establishing a single European railway area (recast)

") 02012L0034 EN 24.12.2016 001.001 1 This text is meant purely as a documentation tool and has no legal effect. The Union's institutions do not assume any liability for its contents. The authentic versions

02012L0034 EN 24.12.2016 001.001 1 This text is meant purely as a documentation tool and has no legal effect. The Union's institutions do not assume any liability for its contents. The authentic versions

What Lies Ahead? David Arsenault Founder & President Logistics Transformation Solutions, LLC

What Lies Ahead? David Arsenault Founder & President Logistics Transformation Solutions, LLC June 7, 2017 1 Logistics Transformation Solutions, LLC Founded: October, 2016 Global Supply Chain & Maritime

What Lies Ahead? David Arsenault Founder & President Logistics Transformation Solutions, LLC June 7, 2017 1 Logistics Transformation Solutions, LLC Founded: October, 2016 Global Supply Chain & Maritime

DCT: Poland's Maritime Window on the World

DCT: Poland's Maritime Window on the World November 27th, 2013 Adam Żołnowski Chief Financial Officer Company Profile Ownership Structure DCT Gdansk is an infrastructure asset majority owned and managed

DCT: Poland's Maritime Window on the World November 27th, 2013 Adam Żołnowski Chief Financial Officer Company Profile Ownership Structure DCT Gdansk is an infrastructure asset majority owned and managed

The Ports of Flanders KEY FACTS & FIGURES

The Ports of Flanders KEY FACTS & FIGURES BERLIN LONDON The Ports of Flanders PORT OF PORT OF PORT OF PORT OF ROTTERDAM RUHR AREA 269 MILLION TONS GOODS TURNOVER NORDRHEIN WESTFALEN Antwerp 199mil. Ghent

The Ports of Flanders KEY FACTS & FIGURES BERLIN LONDON The Ports of Flanders PORT OF PORT OF PORT OF PORT OF ROTTERDAM RUHR AREA 269 MILLION TONS GOODS TURNOVER NORDRHEIN WESTFALEN Antwerp 199mil. Ghent

HAROPA-Ports of Paris Seine Normandy: a complete commercial offer for our South-American clients

BRAZIL Press kit April, 2015 HAROPA-Ports of Paris Seine Normandy: a complete commercial offer for our South-American clients From 7 till 9 April 2015, HAROPA will participate in the Intermodal South America

BRAZIL Press kit April, 2015 HAROPA-Ports of Paris Seine Normandy: a complete commercial offer for our South-American clients From 7 till 9 April 2015, HAROPA will participate in the Intermodal South America

Case No COMP/M SMITHFIELD / OAKTREE / SARA LEE FOODS EUROPE. REGULATION (EC) No 139/2004 MERGER PROCEDURE

No 139/2004 MERGER PROCEDURE") EN Case No COMP/M.4257 - SMITHFIELD / OAKTREE / SARA LEE FOODS EUROPE Only the English text is available and authentic. REGULATION (EC) No 139/2004 MERGER PROCEDURE Article 6(1)(b) NON-OPPOSITION Date:

EN Case No COMP/M.4257 - SMITHFIELD / OAKTREE / SARA LEE FOODS EUROPE Only the English text is available and authentic. REGULATION (EC) No 139/2004 MERGER PROCEDURE Article 6(1)(b) NON-OPPOSITION Date:

Case No COMP/M DOW / ENICHEM POLYURETHANE. REGULATION (EEC) No 4064/89 MERGER PROCEDURE. Article 6(1)(b) NON-OPPOSITION Date: 06/04/2001

No 4064/89 MERGER PROCEDURE. Article 6(1)(b) NON-OPPOSITION Date: 06/04/2001") EN Case No COMP/M.2355 - DOW / ENICHEM POLYURETHANE Only the English text is available and authentic. REGULATION (EEC) No 4064/89 MERGER PROCEDURE Article 6(1)(b) NON-OPPOSITION Date: 06/04/2001 Also available

EN Case No COMP/M.2355 - DOW / ENICHEM POLYURETHANE Only the English text is available and authentic. REGULATION (EEC) No 4064/89 MERGER PROCEDURE Article 6(1)(b) NON-OPPOSITION Date: 06/04/2001 Also available

Overview of SmartRivers 2006 Report

Overview of SmartRivers 2006 Report --- Folding Inland Waterways into the Global Supply Chain --- Arno Hart Group Integrated Logistics Chain Management Slide courtesy of ViaDonau What is SmartRivers? The

Overview of SmartRivers 2006 Report --- Folding Inland Waterways into the Global Supply Chain --- Arno Hart Group Integrated Logistics Chain Management Slide courtesy of ViaDonau What is SmartRivers? The

Meeting #2 August 3, :00-6:00 pm

Meeting #2 August 3, 2017 3:00-6:00 pm Welcome Michael Kosmala, Coraggio Group Committee Charge & Study Focus Charge: Provide industry knowledge and guidance to the Port of Portland leadership on the Port

Meeting #2 August 3, 2017 3:00-6:00 pm Welcome Michael Kosmala, Coraggio Group Committee Charge & Study Focus Charge: Provide industry knowledge and guidance to the Port of Portland leadership on the Port

HAMBURGER HAFEN UND LOGISTIK AG COMPANY PRESENTATION

HAMBURGER HAFEN UND LOGISTIK AG COMPANY PRESENTATION CHEUVREUX GERMAN CORPORATE CONFERENCE FRANKFURT, JANUARY 2011 Hamburger Hafen und Logistik AG DISCLAIMER The facts and information contained herein

HAMBURGER HAFEN UND LOGISTIK AG COMPANY PRESENTATION CHEUVREUX GERMAN CORPORATE CONFERENCE FRANKFURT, JANUARY 2011 Hamburger Hafen und Logistik AG DISCLAIMER The facts and information contained herein

Transload Insights: Better Flexibility and Cost Savings

Transload Insights: Better Flexibility and Cost Savings John Paul Jimenez, The Home Depot Don Esterbrook, NorthWest Seaport Alliance Rob Brown, Union Pacific Don Esterbrook, The Northwest Seaport Alliance

Transload Insights: Better Flexibility and Cost Savings John Paul Jimenez, The Home Depot Don Esterbrook, NorthWest Seaport Alliance Rob Brown, Union Pacific Don Esterbrook, The Northwest Seaport Alliance

HAMBURGER HAFEN UND LOGISTIK AG COMPANY PRESENTATION

HAMBURGER HAFEN UND LOGISTIK AG COMPANY PRESENTATION UNICREDIT GERMAN INVESTMENT CONFERENCE MUNICH, SEPTEMBER 2010 Hamburger Hafen und Logistik AG DISCLAIMER The facts and information contained herein

HAMBURGER HAFEN UND LOGISTIK AG COMPANY PRESENTATION UNICREDIT GERMAN INVESTMENT CONFERENCE MUNICH, SEPTEMBER 2010 Hamburger Hafen und Logistik AG DISCLAIMER The facts and information contained herein

Network Analysis of Container Barge Transport in the Port of Antwerp by means of Simulation

Network Analysis of Container Barge Transport in the Port of Antwerp by means of Simulation An Caris and Gerrit K. Janssens Transportation Research Institute Hasselt University - campus Diepenbeek Wetenschapspark

Network Analysis of Container Barge Transport in the Port of Antwerp by means of Simulation An Caris and Gerrit K. Janssens Transportation Research Institute Hasselt University - campus Diepenbeek Wetenschapspark

Simplified procedure: EU Practice

EU China Trade Project (II) Workshop on DG Competition Procedures Beijing, 7 June 2011 Simplified procedure: EU Practice JM. Carpi Badia Case Manager, Mergers (E.4) DG Competition, European Commission

EU China Trade Project (II) Workshop on DG Competition Procedures Beijing, 7 June 2011 Simplified procedure: EU Practice JM. Carpi Badia Case Manager, Mergers (E.4) DG Competition, European Commission

Editorial: Maritime and port economic geography

Belgeo Revue belge de géographie 4 2004 Maritime and port economic geography Editorial: Maritime and port economic geography Jacques Charlier, Antoine Frémont and Brian Slack Publisher Société Royale Belge

Belgeo Revue belge de géographie 4 2004 Maritime and port economic geography Editorial: Maritime and port economic geography Jacques Charlier, Antoine Frémont and Brian Slack Publisher Société Royale Belge

Market Place Seminar Rail Crossroads

Market Place Seminar Rail Crossroads 24-25 September 2015 Tom Paeshuys, General Manager IFB Key facts & figures (2014) Over 520,000 TEUs handled Operated 11,107 trains Door-to-door solutions in over 15

Market Place Seminar Rail Crossroads 24-25 September 2015 Tom Paeshuys, General Manager IFB Key facts & figures (2014) Over 520,000 TEUs handled Operated 11,107 trains Door-to-door solutions in over 15

In electronic form on the EUR-Lex website under document number 32011M6357

EN Case No COMP/M.6357 - KONINKLIJKE PHILIPS/ INDAL GROUP Only the English text is available and authentic. REGULATION (EC) No 139/2004 MERGER PROCEDURE Article 6(1)(b) NON-OPPOSITION Date: 23/11/2011

EN Case No COMP/M.6357 - KONINKLIJKE PHILIPS/ INDAL GROUP Only the English text is available and authentic. REGULATION (EC) No 139/2004 MERGER PROCEDURE Article 6(1)(b) NON-OPPOSITION Date: 23/11/2011

Case No IV/M RECTICEL / GREINER. REGULATION (EEC) No 4064/89 MERGER PROCEDURE. Article 6(1)(b) NON-OPPOSITION Date: 19/03/1997

No 4064/89 MERGER PROCEDURE. Article 6(1)(b) NON-OPPOSITION Date: 19/03/1997") EN Case No IV/M.835 - RECTICEL / GREINER Only the English text is available and authentic. REGULATION (EEC) No 4064/89 MERGER PROCEDURE Article 6(1)(b) NON-OPPOSITION Date: 19/03/1997 Also available in

EN Case No IV/M.835 - RECTICEL / GREINER Only the English text is available and authentic. REGULATION (EEC) No 4064/89 MERGER PROCEDURE Article 6(1)(b) NON-OPPOSITION Date: 19/03/1997 Also available in

Cool Logistics Asia. September 2017 RAUL SACA

1 Cool Logistics Asia September 2017 RAUL SACA 2 Agenda Fruit trades, Volumes and trends. Reefer Container Perishable Shipping. Trends and Developments affecting Fruit trades. Digitization of the industry.

1 Cool Logistics Asia September 2017 RAUL SACA 2 Agenda Fruit trades, Volumes and trends. Reefer Container Perishable Shipping. Trends and Developments affecting Fruit trades. Digitization of the industry.

Case No COMP/M LVMH / PRADA / FENDI. REGULATION (EEC) No 4064/89 MERGER PROCEDURE. Article 6(1)(b) NON-OPPOSITION Date: 25/05/2000

No 4064/89 MERGER PROCEDURE. Article 6(1)(b) NON-OPPOSITION Date: 25/05/2000") EN Case No COMP/M.1780 - LVMH / PRADA / FENDI Only the English text is available and authentic. REGULATION (EEC) No 4064/89 MERGER PROCEDURE Article 6(1)(b) NON-OPPOSITION Date: 25/05/2000 Also available

EN Case No COMP/M.1780 - LVMH / PRADA / FENDI Only the English text is available and authentic. REGULATION (EEC) No 4064/89 MERGER PROCEDURE Article 6(1)(b) NON-OPPOSITION Date: 25/05/2000 Also available

PASSENGER TRAFFIC AND FREIGHT HANDLING IN PORTS OF EUROPEAN UNION

PASSENGER TRAFFIC AND FREIGHT HANDLING IN PORTS OF EUROPEAN UNION Andrea Galieriková 1, Jarmila Sosedová 2 Summary: This paper informs about latest statistical data of passenger traffic and freight handling

PASSENGER TRAFFIC AND FREIGHT HANDLING IN PORTS OF EUROPEAN UNION Andrea Galieriková 1, Jarmila Sosedová 2 Summary: This paper informs about latest statistical data of passenger traffic and freight handling

HAMBURGER HAFEN UND LOGISTIK AG Investor Presentation

HAMBURGER HAFEN UND LOGISTIK AG Investor Presentation Warburg Highlights 2016 Hamburg, 30 June 2016 Disclaimer The facts and information contained herein are as up to date as is reasonably possible and

HAMBURGER HAFEN UND LOGISTIK AG Investor Presentation Warburg Highlights 2016 Hamburg, 30 June 2016 Disclaimer The facts and information contained herein are as up to date as is reasonably possible and

REPORT FROM THE COMMISSION TO THE EUROPEAN PARLIAMENT AND THE COUNCIL

EUROPEAN COMMISSION Brussels, 28.7.2015 COM(2015) 362 final REPORT FROM THE COMMISSION TO THE EUROPEAN PARLIAMENT AND THE COUNCIL on the exercise of the power to adopt delegated acts conferred on the Commission

EUROPEAN COMMISSION Brussels, 28.7.2015 COM(2015) 362 final REPORT FROM THE COMMISSION TO THE EUROPEAN PARLIAMENT AND THE COUNCIL on the exercise of the power to adopt delegated acts conferred on the Commission

Case No COMP/M CANON/ OCE. REGULATION (EC) No 139/2004 MERGER PROCEDURE. Article 6(1)(b) NON-OPPOSITION Date: 22/12/2009

No 139/2004 MERGER PROCEDURE. Article 6(1)(b) NON-OPPOSITION Date: 22/12/2009") EN Case No COMP/M.5672 - CANON/ OCE Only the English text is available and authentic. REGULATION (EC) No 139/2004 MERGER PROCEDURE Article 6(1)(b) NON-OPPOSITION Date: 22/12/2009 In electronic form on

EN Case No COMP/M.5672 - CANON/ OCE Only the English text is available and authentic. REGULATION (EC) No 139/2004 MERGER PROCEDURE Article 6(1)(b) NON-OPPOSITION Date: 22/12/2009 In electronic form on

Port regionalization: improving port competitiveness by reaching beyond the port perimeter

Port regionalization: improving port competitiveness by reaching beyond the port perimeter Dr. Jean-Paul Rodrigue, Hofstra University, New York, USA, & Dr. Theo Notteboom, President of ITMMA, University

Port regionalization: improving port competitiveness by reaching beyond the port perimeter Dr. Jean-Paul Rodrigue, Hofstra University, New York, USA, & Dr. Theo Notteboom, President of ITMMA, University

The Mediterranean corridor From a road corridor to a multimodal corridor A success story for the regional economy

The Mediterranean corridor From a road corridor to a multimodal corridor A success story for the regional economy Jordi Torrent Strategy Manager Barcelona Port Authority May 2014 Index of contents 1 Trends

The Mediterranean corridor From a road corridor to a multimodal corridor A success story for the regional economy Jordi Torrent Strategy Manager Barcelona Port Authority May 2014 Index of contents 1 Trends

Dynamics in the Port and Maritime Business: The Same Stage, Different Players, Another Game?

Dynamics in the Port and Maritime Business: The Same Stage, Different Players, Another Game? Prof. Dr. Theo Notteboom President and Professor, ITMMA University of Antwerp President International Association

Dynamics in the Port and Maritime Business: The Same Stage, Different Players, Another Game? Prof. Dr. Theo Notteboom President and Professor, ITMMA University of Antwerp President International Association

SUBJECT: NORTH EUROPE ATLANTIC SHIPPING INSTRUCTIONS & APPROVED CO-LOAD LIST DP3 YEAR 7

FROM NORTH ATLANTIC SERVICES NV BELGIUM TO: NORTH EUROPE, MED AND U.S PORT AGENTS May 2014, 20th SUBJECT: NORTH EUROPE ATLANTIC SHIPPING INSTRUCTIONS & APPROVED CO-LOAD LIST DP3 YEAR 7 A: APPROVED CARRIERS

FROM NORTH ATLANTIC SERVICES NV BELGIUM TO: NORTH EUROPE, MED AND U.S PORT AGENTS May 2014, 20th SUBJECT: NORTH EUROPE ATLANTIC SHIPPING INSTRUCTIONS & APPROVED CO-LOAD LIST DP3 YEAR 7 A: APPROVED CARRIERS

DCT Gdansk Presentation January 2017

DCT Gdansk Presentation January 2017 2 Company Profile DCT Gdansk: Resources and Technical Specifications Terminal description: The largest and the fastest-growing container terminal in the Baltic Sea

DCT Gdansk Presentation January 2017 2 Company Profile DCT Gdansk: Resources and Technical Specifications Terminal description: The largest and the fastest-growing container terminal in the Baltic Sea

In electronic form on the EUR-Lex website under document number 32014M7023

EN Case No COMP/M.7023 - PUBLICIS / OMNICOM Only the English text is available and authentic. REGULATION (EC) No 139/2004 MERGER PROCEDURE Article 6(1)(b) NON-OPPOSITION Date: 09/01/2014 In electronic

EN Case No COMP/M.7023 - PUBLICIS / OMNICOM Only the English text is available and authentic. REGULATION (EC) No 139/2004 MERGER PROCEDURE Article 6(1)(b) NON-OPPOSITION Date: 09/01/2014 In electronic

Port Koper, a green gateway to Europe

Key facts Port Koper, a green gateway to Europe By Peraphan Jittrapirom, Policy analyst Introduction Port Koper or Luka Koper situates on the south coast of the Gulf of Trieste, within the national border

Key facts Port Koper, a green gateway to Europe By Peraphan Jittrapirom, Policy analyst Introduction Port Koper or Luka Koper situates on the south coast of the Gulf of Trieste, within the national border

Green corridors: policy and regulatory issues

Green corridors: policy and regulatory issues Raimonds Aronietis, Paresa Markianidou, Hilde Meersman, Tom Pauwels, Eddy Van de Voorde, Thierry Vanelslander and Ann Verhetsel University of Antwerp Department

Green corridors: policy and regulatory issues Raimonds Aronietis, Paresa Markianidou, Hilde Meersman, Tom Pauwels, Eddy Van de Voorde, Thierry Vanelslander and Ann Verhetsel University of Antwerp Department

Legal Issues Regarding The Jamaica Logistics Hub

Legal Issues Regarding The Jamaica Logistics Hub Deniece Aiken BSc (Hons) LLB (Hons) MSc (Dist) Practising Attorney-at-Law BSC International Relations and Political Science (UWI MONA, JAMAICA) Bachelor

Legal Issues Regarding The Jamaica Logistics Hub Deniece Aiken BSc (Hons) LLB (Hons) MSc (Dist) Practising Attorney-at-Law BSC International Relations and Political Science (UWI MONA, JAMAICA) Bachelor

Preface. The Airports of Brussels and Liege are important hubs for Full Freighters and the preferred location for the European head offices of

1 Preface Belgium is the perfect country in which to set up a European logistics base, headquarters or distribution center because the country s infrastructure, skilled workforce and the IT opportunities

1 Preface Belgium is the perfect country in which to set up a European logistics base, headquarters or distribution center because the country s infrastructure, skilled workforce and the IT opportunities

Transport, Forwarding and Logistics in Poland. K e y n o t e s

Transport, Forwarding and Logistics in Poland K e y n o t e s Prague, the 10 th April 2013 Transportation roads and fleet 2000 2005 2010 Railway lines (thd km) 21,6 19,8 20,1 Hard surface public roads

Transport, Forwarding and Logistics in Poland K e y n o t e s Prague, the 10 th April 2013 Transportation roads and fleet 2000 2005 2010 Railway lines (thd km) 21,6 19,8 20,1 Hard surface public roads

Port of Nansha. Emerges as the Jewel of the West Pearl River Delta. A White Paper by Port of NANSHA, Guangzhou Port Group

Port of Nansha Emerges as the Jewel of the West Pearl River Delta A White Paper by Port of NANSHA, Guangzhou Port Group Port of NANSHA is the only deep-water terminal serving this crucial manufacturing

Port of Nansha Emerges as the Jewel of the West Pearl River Delta A White Paper by Port of NANSHA, Guangzhou Port Group Port of NANSHA is the only deep-water terminal serving this crucial manufacturing

BRINGING ECONOMIES OF SCALE IN MEGA CONTAINERSHIPS TO PORTS

BRINGING ECONOMIES OF SCALE IN MEGA CONTAINERSHIPS TO PORTS Arduino, Giulia Dipartimento di Economia e Metodi Quantitativi, Università degli Studi di Genova, Italy, T +39(0)102095204, F +39(0)102095511,

BRINGING ECONOMIES OF SCALE IN MEGA CONTAINERSHIPS TO PORTS Arduino, Giulia Dipartimento di Economia e Metodi Quantitativi, Università degli Studi di Genova, Italy, T +39(0)102095204, F +39(0)102095511,

Port and Maritime Transport Issues and Views

Port and Maritime Transport Issues and Views C. Bert Kruk, Lead Port Specialist Bradley C. Julian, Port and Maritime Transport Specialist Port and Maritime Transport Office (PMTO) Transport Division Energy,

Port and Maritime Transport Issues and Views C. Bert Kruk, Lead Port Specialist Bradley C. Julian, Port and Maritime Transport Specialist Port and Maritime Transport Office (PMTO) Transport Division Energy,

INTERNATIONAL LOGISTICS DAY 2012

INTERNATIONAL LOGISTICS DAY 2012 With the support of: 1 Future for Logistics 12.11.2012 2 Study: Future for Logistics 3 Study: Future for Logistics 4 Diagnostic of the Luxembourg logistics sector 5 World

INTERNATIONAL LOGISTICS DAY 2012 With the support of: 1 Future for Logistics 12.11.2012 2 Study: Future for Logistics 3 Study: Future for Logistics 4 Diagnostic of the Luxembourg logistics sector 5 World

Antwerp s view on extended gateways: from mainport to chainport

PORT-NET Workshop Antwerp, June 2009 Antwerp s view on extended gateways: from mainport to chainport Goedele Sannen Strategy and Development Development World port, centrally located in Europe Role of

PORT-NET Workshop Antwerp, June 2009 Antwerp s view on extended gateways: from mainport to chainport Goedele Sannen Strategy and Development Development World port, centrally located in Europe Role of

Member of the SEA-invest Group

Member of the SEA-invest Group The terminals, with a total capacity of more than 3.300.000 m3, offer state-of-the-art storage and handling infrastructure for mineral and vegetable oil products, liquid

Member of the SEA-invest Group The terminals, with a total capacity of more than 3.300.000 m3, offer state-of-the-art storage and handling infrastructure for mineral and vegetable oil products, liquid

SARJAK CONTAINER LINES PVT. LTD.

SARJAK CONTAINER LINES PVT. LTD. CARRIER S STANDARD CREDIT TERMS Credit on any owed sums may be granted by Sarjak Container Lines Pvt. Ltd. to the Client, hereinafter referred as the «Client» or «Sarjak»,

SARJAK CONTAINER LINES PVT. LTD. CARRIER S STANDARD CREDIT TERMS Credit on any owed sums may be granted by Sarjak Container Lines Pvt. Ltd. to the Client, hereinafter referred as the «Client» or «Sarjak»,

Domestic Container Supply Study

Domestic Container Supply Study Cubic Transport Services Ltd. Njord Ltd. Page - 1 - EXECUTIVE SUMMARY...3 E1. MAIN PURPOSE OF STUDY...3 E2. METHODOLOGY....3 E3. EXISTING INTERNATIONAL CARGO MOVEMENTS...3

Domestic Container Supply Study Cubic Transport Services Ltd. Njord Ltd. Page - 1 - EXECUTIVE SUMMARY...3 E1. MAIN PURPOSE OF STUDY...3 E2. METHODOLOGY....3 E3. EXISTING INTERNATIONAL CARGO MOVEMENTS...3

VOLTRI TERMINAL EUROPA

Genoa VOLTRI TERMINAL EUROPA Your Gateway to Central & Southern Europe 1 PSA: A Leading Global Terminal Operator 70,0 IN 2009 28 ports in 16 countries 56.93 million TEUs handled in 2009 26.000 staff 63,2

Genoa VOLTRI TERMINAL EUROPA Your Gateway to Central & Southern Europe 1 PSA: A Leading Global Terminal Operator 70,0 IN 2009 28 ports in 16 countries 56.93 million TEUs handled in 2009 26.000 staff 63,2

Case M DISCOVERY / SCRIPPS. REGULATION (EC) No 139/2004 MERGER PROCEDURE. Article 6(1)(b) in conjunction with Art 6(2) Date: 06/02/2018

No 139/2004 MERGER PROCEDURE. Article 6(1)(b) in conjunction with Art 6(2) Date: 06/02/2018") EUROPEAN COMMISSION DG Competition Case M.8665 - DISCOVERY / SCRIPPS Only the English text is available and authentic. REGULATION (EC) No 139/2004 MERGER PROCEDURE Article 6(1)(b) in conjunction with Art

EUROPEAN COMMISSION DG Competition Case M.8665 - DISCOVERY / SCRIPPS Only the English text is available and authentic. REGULATION (EC) No 139/2004 MERGER PROCEDURE Article 6(1)(b) in conjunction with Art