Natural Gas Next: The Rockies and the West

|

|

|

- Terence Marsh

- 6 years ago

- Views:

Transcription

1 Natural Gas Next: The Rockies and the West Callie Kolbe, Manager, Energy Analysis Sadie Fulton, Senior Energy Analyst September 25, 2017

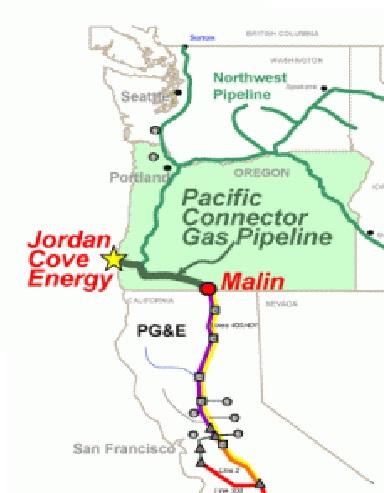

2 Jordan Cove Back again?

3 There is even more gas?

4 NIMBY!

5 Renewable Targets

6 The Rockies and the West Production: Where can it go? Demand: The impact of renewables How pipeline flows are changing Expectations through Summer 2018

7 Late-Summer Heat in West Population Weighted Degrees Western Temperatures Population Weighted Degrees Rockies Temperatures

8 Bakken-MT Bakken-ND Other-MT Williston, Non-Bakken-ND Big Horn-MT Powder River-MT Williston, Non-Bakken-SD Big Horn-WY Powder River-WY Other-SD Wind River Other-UT Overthrust Uinta Green River- WY Green River- CO Piceance Denver Julesburg- WY Denver Julesburg- CO Rocky Mountain Region 26 Producing Areas Paradox- UT Other-CO San Juan- CO Raton-CO Anadarko-CO

9 Rocky Mountain Region Gas Production, by Producing Area DJ Bakken Source: PointLogic Energy

10 Rockies Production Shrinking Bcf/d Powder River Uinta San Juan Piceance Denver - Julesburg Green River - Overthrust Other Forecast Rockies production expected to continue to succumb to pressures from Northeast production explosion, widely available Canadian gas, and shrinking western demand.

11 Rockies Supply & Demand Bcf/d In the last 5 years, winter balance has averaged 7 Bcf/d. Summer balance has averaged 8.9 Bcf/d Demand Balance Supply Demand Forecast Balance Forecast Supply Forecast

12 Rockies Gets Shorter (well less long) 2012 vs Supply Demand Lower production, combined with modest residential growth was second consecutive year of production decreases. Source: PointLogic Energy

13 Pet-Chem Projects Lead Industrial Demand Growth But Not in West Most of the gas-intensive projects are not slated for buildout along the West and Rockies. Source: IHS-Markit & PointLogic Energy

14 West Gets Shorter 2012 vs Supply Demand Higher demand driven by power and exports to Mexico. Source: PointLogic Energy

15 Power Burn Per Temp in the West 9 Jan.-Sept. Power Burn per Degree in the West, Western Power Burn in Bcf/d YTD 2017 Power YTD 2016 Power YTD 2015 Power YTD 2014 Power YTD 2017 Power Trendline YTD 2016 Power Trendline YTD 2015 Power Trendline YTD 2014 Power Trendline Western Temperatures in Population Weighted Degrees

16 Nat Gas Power Growth Stronger in West than in Rockies Western Electricity Generation by source Rockies Electricity Generation by source 500 1, Generation (Million MW Hours) ,150 1,100 1,050 1, Generation (Million MW Hours) Total Hydro Nuclear Wind Coal Natural Gas Solar Total Hydro Nuclear Wind Coal Natural Gas Solar

17 California Loves Renewables As California s drought conditions lightened, hydro came back in For context, natural gas generation bumps around 20,000-40,000 thousand MW hours in California.

18 Coal Retirements are History in the Rockies Source: EIA

19 West adds Solar and Gas; Rockies adds Wind GW Western Power Generation Additions GW Rockies Power Generation Additions Natural Gas Wind Solar Natural Gas Wind Solar

20 Western Supply & Demand Bcf/d In the last 5 years, winter balance has averaged -7 Bcf/d. Summer balance averaged -5.5 Bcf/d Supply Balance Demand Supply Forecast Balance Forecast Demand Forecast

21 The Flow Pattern Box Competition: Canada and Bakken Competition: Canada & constraints Competition: SCOOP/STACK & Northeast Competition: Growth from Permian

22 Bakken Supply: Large on Northern Border MMcf/d Northern Border Outflows (Jan.-Sept.) Outflows to Midcontinent Bakken Sourced Supply 40% 35% 30% 25% 20% 15% 10% 5% 0% Bakken % of Supplies

23 The Flow Pattern Box Competition: Canada and Bakken Competition: Canada & constraints Competition: SCOOP/STACK & Northeast Competition: Growth from Permian

24 Rockies Eastbound Flows (Jan.-Sept.) Bcf/d REX CIG Cheyenne Plains Southern Star

25 Rockies Westbound Flows MMcf/d Northwest Pipeline Ruby Pipeline Kern River TransColorado Northwest West Southwest South

26 2012 vs. 2017: Flow Patterns Jan.-Sept. Net Rockies (Bcf/d) 2012: (6.8) 2017: (7.0) Change: +(0.2) (0.1) Jan. Sept. Net West (Bcf/d) 2012: : 6.9 Change:

Change: -(0.3) +0.1 April-Sept. Net Flows to West (Bcf/d) 2016: 7.0 2017: 6.9 Change: - (0.15) +0.")

27 Summer 2016 vs. 2017: Flow Patterns April-Sept. Net Flows from Rockies (Bcf/d) 2016: (7.7) 2017: (7.4) Change: -(0.3) +0.1 April-Sept. Net Flows to West (Bcf/d) 2016: : 6.9 Change: - (0.15) +0.4

: 26% 2.4 Bcf/d 2016 - Kern River (Veyo): 93% 2.4 Bcf/d 2017 - Kern River (Veyo): 86% 2.4 Bcf/d Transwestern (W. Thoreau): 77% 1.2 Bcf/d 2016 - PG&E Baja Path: 36% 1.")

28 Traditional Constraints PG&E Redwood Path: 88.5% 2.1 Bcf/d PG&E Redwood Path: 89.5% 2.1 Bcf/d Utilization Capacity (summer to date) 2016 Ruby (West): 26% 2.4 Bcf/d 2017 Ruby (West): 26% 2.4 Bcf/d Kern River (Veyo): 93% 2.4 Bcf/d Kern River (Veyo): 86% 2.4 Bcf/d Transwestern (W. Thoreau): 77% 1.2 Bcf/d PG&E Baja Path: 36% 1.1 Bcf/d PG&E Baja Path: 31% 1.1 Bcf/d Transwestern (W. Thoreau): 76% 1.2 Bcf/d El Paso South ML at Cornudas: 75% 2.4 Bcf/d El Paso South ML at Cornudas: 82% 2.4 Bcf/d

29 Rockies & West Basis Widen $0.50 $0.40 $0.30 $0.20 $0.10 $0.00 -$0.10 -$0.20 -$0.30 -$0.40 -$0.50 Rockies and West Basis Opal S. California Border Malin PG&E CG Opal2 S. California Border3 Malin4 PG&E CG5 Above-average Rockies storage inventories, along with cheap supply from western Canada and the Permian Basin, will continue to limit Rockies outflows, keeping basis discounts wider than last year North and South California basis remains wider than the five-year average in both regions because of weak power sector gas demand and large discounts in California s supply regions. Source: IHS

30 Rockies and the West: Conclusions As Northeast supply spills over into neighboring regions, it will put downward pressure on traditional supply basis because it is closer and cheaper to premium markets. Competition in the Midwest forces Rockies supply to shift to the West. Pipeline constraints to the Southwest play an important role in dictating how Rockies gas will find a home in the West.

31 Appendix

32 Rockies Gets Slightly Less Long Summer 2016 vs Dry Prod Supply Canadian Imports Total Supply Power Demand Industrial Res/Com Total Demand Source: PointLogic Energy

33 West Gets Slightly Longer Summer 2016 vs Supply Demand Dry Prod Canadian Imports Total Supply Power Industrial Res/Com Mexican Exports Total Demand Power demand collapses summer-on-summer Source: PointLogic Energy

34 Pricing: California Hub Basis $/MMBtu Malin Basis PG&E-Citygate Basis SoCal Border Basis SoCal-Citygate Basis Note: Negative numbers indicate a price discount to Henry Hub.

35 Competition from Canada Canadian Flows into Rocky Mountains Canadian production nearly doubles Rockies quantities to ship. Bcf/d

36 Change in Flows Demand: Winter = 10.7 Summer = 9.2 Demand: Winter = 4 Summer = 2.2 Rockies to Mid-Continent: 5.8 Winter, 6.2 Summer All data: Average of last 5 years, Bcf/d

37 Big-Picture Flows: Summer 2017 Demand = 9.0 Demand= 2.1 Rockies to Mid-Continent: 6.6 All data: Summer 2017 (April-September), Bcf/d

38 West Production: Small and Steady Bcf/d Other Monterey Shale Suan Juan-NM Permian-NM Forecast Production in Western Region dominated by Permian-NM and San Juan-NM. Source: PointLogic Energy We expect production for the Western region to remain relatively flat at 3.6 Bcf/d through the forecast period as increasing production from Permian-NM is offset by losses in the rest of the region.

39 West Demand Bcf/d * * Winter Summer Industrial Res/Comm Power

40 Power Burn Per Temp: Rockies 1 Jan.-Sept. Power Burn per Degree in the Rockies, Rockies Power Burn in Bcf/d YTD 2017 Power YTD 2016 Power YTD 2015 Power YTD 2014 Power YTD 2017 Power Trendline YTD 2016 Power Trendline YTD 2015 Power Trendline YTD 2014 Power Trendline Rockies Temperatures in Population Weighted Degrees

Jim Cleary President, El Paso Western Pipelines. Platts Conference, Rockies Gas & Oil April 25, 2008

Jim Cleary President, El Paso Western Pipelines Platts Conference, Rockies Gas & Oil April 25, 2008 Cautionary Statement Regarding Forward-looking Statements This presentation includes forward-looking

Jim Cleary President, El Paso Western Pipelines Platts Conference, Rockies Gas & Oil April 25, 2008 Cautionary Statement Regarding Forward-looking Statements This presentation includes forward-looking

Outlook for Western U.S. Natural Gas Markets

Outlook for Western U.S. Natural Gas Markets Summer Energy Outlook Conference April, Contact: Kevin R. Petak Vice President, Gas Market Modeling ICF International 73-1 1-753753 kpetak@icfi.com ICF International.

Outlook for Western U.S. Natural Gas Markets Summer Energy Outlook Conference April, Contact: Kevin R. Petak Vice President, Gas Market Modeling ICF International 73-1 1-753753 kpetak@icfi.com ICF International.

Major Changes in Natural Gas Transportation Capacity,

Major Changes in Natural Gas Transportation, The following presentation was prepared to illustrate graphically the areas of major growth on the national natural gas pipeline transmission network between

Major Changes in Natural Gas Transportation, The following presentation was prepared to illustrate graphically the areas of major growth on the national natural gas pipeline transmission network between

Wyoming Pipelines - The Territory Ahead October 31, 2008 October 15, 2013

Wyoming Pipelines - The Territory Ahead October 31, 2008 October 15, 2013 1 $ per MMBtu Representative Wyoming Natural Gas Price by Month 10.00 9.00 8.00 7.00 6.00 5.00 4.00 3.00 2.00 1.00 0.00 Jan Feb

Wyoming Pipelines - The Territory Ahead October 31, 2008 October 15, 2013 1 $ per MMBtu Representative Wyoming Natural Gas Price by Month 10.00 9.00 8.00 7.00 6.00 5.00 4.00 3.00 2.00 1.00 0.00 Jan Feb

Ruby Pipeline Project

Ruby Pipeline Project Ed Miller Ruby Project Manager October 21, 2008 El Paso Pipeline System Ruby Pipeline CIG & WIC Tennessee Gas Pipeline Mojave Pipeline El Paso Natural Gas Cheyenne Plains Pipeline

Ruby Pipeline Project Ed Miller Ruby Project Manager October 21, 2008 El Paso Pipeline System Ruby Pipeline CIG & WIC Tennessee Gas Pipeline Mojave Pipeline El Paso Natural Gas Cheyenne Plains Pipeline

Broad market presence: Growing demand regions, key supply basins, LNG terminals. Excellent connections to markets and supply

Pipeline Group Strong and Growing Broad market presence: Growing demand regions, key supply basins, LNG terminals Excellent connections to markets and supply Almost $4 billion of committed growth projects

Pipeline Group Strong and Growing Broad market presence: Growing demand regions, key supply basins, LNG terminals Excellent connections to markets and supply Almost $4 billion of committed growth projects

Wyoming Pipeline Authority Public Meeting. Anne Swedberg, Manager, North American Power and Gas Content

Wyoming Pipeline Authority Public Meeting Anne Swedberg, Manager, North American Power and Gas Content 2015 2014 Platts, McGraw Hill Financial. All rights reserved. Benposium 2015. Key Take-Aways US production

Wyoming Pipeline Authority Public Meeting Anne Swedberg, Manager, North American Power and Gas Content 2015 2014 Platts, McGraw Hill Financial. All rights reserved. Benposium 2015. Key Take-Aways US production

Western US Natural Gas Supply & Demand Outlook

Western US Natural Gas Supply & Demand Outlook Rick Margolin, Senior Analyst WSPP Operating Committee Spring Conference Sonoma, CA March 11, 2015 info@genscape.com US: +1 502 583 3435 EU: +31 20 524 4089

Western US Natural Gas Supply & Demand Outlook Rick Margolin, Senior Analyst WSPP Operating Committee Spring Conference Sonoma, CA March 11, 2015 info@genscape.com US: +1 502 583 3435 EU: +31 20 524 4089

University of Wyoming The 2008 Conference The Wyoming Pipelines: The Territory Ahead

FERC CERTIFICATION University of Wyoming The 2008 Conference The Wyoming Pipelines: The Territory Ahead 1 Robert Cupina, Principal Deputy Director Federal Energy Regulatory Commission Cheyenne, Wyoming

FERC CERTIFICATION University of Wyoming The 2008 Conference The Wyoming Pipelines: The Territory Ahead 1 Robert Cupina, Principal Deputy Director Federal Energy Regulatory Commission Cheyenne, Wyoming

2005 North American Natural Gas Outlook Client Presentation

2005 North American Natural Gas Outlook Client Presentation January 17, 2005 Ron Denhardt Vice President, Natural Gas Services Strategic Energy & Economic Research Inc. 781 756 0550 (Tel) Copyright 2004

2005 North American Natural Gas Outlook Client Presentation January 17, 2005 Ron Denhardt Vice President, Natural Gas Services Strategic Energy & Economic Research Inc. 781 756 0550 (Tel) Copyright 2004

Midcontinent, Canada, and West

Midcontinent, Canada, and West How will western markets fare as eastern supply tries to find a home? John Hilfiker May 17, 217 Energy Analyst Restrictions on Use: You may use the prices, indexes, assessments

Midcontinent, Canada, and West How will western markets fare as eastern supply tries to find a home? John Hilfiker May 17, 217 Energy Analyst Restrictions on Use: You may use the prices, indexes, assessments

Northeast Drives US Basis Trends

Northeast Drives US Basis Trends Rocco Canonica, Director Energy Analysis September 2014 2014 Platts, McGraw Hill Financial. All rights reserved. Benposium 2014. Agenda 2014 Year of Extremes; Review Record

Northeast Drives US Basis Trends Rocco Canonica, Director Energy Analysis September 2014 2014 Platts, McGraw Hill Financial. All rights reserved. Benposium 2014. Agenda 2014 Year of Extremes; Review Record

Analysis of California Natural Gas Market, Supply Infrastructure, Regulatory Implications, and Future Market Conditions. CIEE Subcontract No.

Analysis of California Natural Gas Market, Supply Infrastructure, Regulatory Implications, and Future Market Conditions CIEE Subcontract No. MNG-07 07-0101 Natural Gas Storage Forum: Modeling of Natural

Analysis of California Natural Gas Market, Supply Infrastructure, Regulatory Implications, and Future Market Conditions CIEE Subcontract No. MNG-07 07-0101 Natural Gas Storage Forum: Modeling of Natural

Western Oklahoma Residue Takeaway Impact of Growing SCOOP/STACK Supply

Western Oklahoma Residue Takeaway Impact of Growing SCOOP/STACK Supply Craig Harris Executive Vice President & Chief Commercial Officer October 28, 2016 Forward-looking Statements This presentation and

Western Oklahoma Residue Takeaway Impact of Growing SCOOP/STACK Supply Craig Harris Executive Vice President & Chief Commercial Officer October 28, 2016 Forward-looking Statements This presentation and

Accessing New Markets for Rockies Natural Gas

Accessing New Markets for Rockies Natural Gas Presentation to: 2018 Uinta Basin Energy Summit By: John Harpole August 30, 2018 It is not a scarce resource anymore 2 Hydraulic Fracturing Pumping fluid under

Accessing New Markets for Rockies Natural Gas Presentation to: 2018 Uinta Basin Energy Summit By: John Harpole August 30, 2018 It is not a scarce resource anymore 2 Hydraulic Fracturing Pumping fluid under

Wyoming Pipelines The Territory Ahead Cheyenne, Wyoming October 31, Brian Jeffries Executive Director Wyoming Pipeline Authority

Wyoming Pipelines The Territory Ahead Cheyenne, Wyoming October 31, 2008 Brian Jeffries Executive Director Wyoming Pipeline Authority 1 Wyoming imports, produces, refines and exports crude 2 Wyoming imports,

Wyoming Pipelines The Territory Ahead Cheyenne, Wyoming October 31, 2008 Brian Jeffries Executive Director Wyoming Pipeline Authority 1 Wyoming imports, produces, refines and exports crude 2 Wyoming imports,

U.S. Natural Gas Markets Where Is It All Going to Go?

U.S. Natural Gas Markets Where Is It All Going to Go? October 19, 217 Today s Agenda» Current Natural Gas Market Production Shifting gas flows Demand LNG, Power and Mexico Evolving values basis and price»

U.S. Natural Gas Markets Where Is It All Going to Go? October 19, 217 Today s Agenda» Current Natural Gas Market Production Shifting gas flows Demand LNG, Power and Mexico Evolving values basis and price»

Natural Gas, Liquids and Crude Oil Market Outlook North America 2012 and Beyond

Natural Gas, Liquids and Crude Oil Market Outlook North America 2012 and Beyond August 14th, 2012 On behalf of: for: 1 BENTEK Energy Market Information Agenda: U.S. Supply, Demand and Storage Outlook Macro

Natural Gas, Liquids and Crude Oil Market Outlook North America 2012 and Beyond August 14th, 2012 On behalf of: for: 1 BENTEK Energy Market Information Agenda: U.S. Supply, Demand and Storage Outlook Macro

Connecting Supply Options GasMart May 21, 2008, Chicago

Connecting Supply Options GasMart May 21, 2008, Chicago Dean Ferguson, VP Marketing, Business Development & Regulatory Affairs, U.S. Pipeline Central Forward-Looking Information 2 This presentation may

Connecting Supply Options GasMart May 21, 2008, Chicago Dean Ferguson, VP Marketing, Business Development & Regulatory Affairs, U.S. Pipeline Central Forward-Looking Information 2 This presentation may

Natural Gas Markets and Regulation

Natural Gas Markets and Regulation Donald F. Santa President INGAA 33 rd Annual PURC Conference Gainesville, Florida February 24, 2006 Presentation Overview How did we get here? Natural Gas Restructuring

Natural Gas Markets and Regulation Donald F. Santa President INGAA 33 rd Annual PURC Conference Gainesville, Florida February 24, 2006 Presentation Overview How did we get here? Natural Gas Restructuring

Rockies Alliance Pipeline. Presentation to the Wyoming Pipeline Authority. May 20, 2008

Rockies Alliance Pipeline Presentation to the Wyoming Pipeline Authority May 20, 2008 Slide 2 Rockies Alliance Pipeline Route RAP New Facilities New Hampto n Proposed Pipeline Facilities Wamsutter to Ventura:

Rockies Alliance Pipeline Presentation to the Wyoming Pipeline Authority May 20, 2008 Slide 2 Rockies Alliance Pipeline Route RAP New Facilities New Hampto n Proposed Pipeline Facilities Wamsutter to Ventura:

Rockies Alliance Pipeline. Presentation to the Wyoming Pipeline Authority. May 20, 2008

Rockies Alliance Pipeline Presentation to the Wyoming Pipeline Authority May 20, 2008 Slide 2 Rockies Alliance Pipeline Route RAP New Facilities New Hamp ton Proposed Pipeline Facilities Wamsutter to Ventura:

Rockies Alliance Pipeline Presentation to the Wyoming Pipeline Authority May 20, 2008 Slide 2 Rockies Alliance Pipeline Route RAP New Facilities New Hamp ton Proposed Pipeline Facilities Wamsutter to Ventura:

Questar Pipeline Current Capacity and Development

Questar Pipeline Current Capacity and Development Gary A. Schmitt Manager, Marketing and Business Development April 27, 2007 Platts Rockies Gas and Oil Conference 1 Agenda Questar Pipeline Overview Basin

Questar Pipeline Current Capacity and Development Gary A. Schmitt Manager, Marketing and Business Development April 27, 2007 Platts Rockies Gas and Oil Conference 1 Agenda Questar Pipeline Overview Basin

Modeling and Analysis of Oil & Gas Emissions Data University of North Carolina (UNC IE) ENVIRON International Corporation (ENVIRON)

ENVIRON International Corporation (ENVIRON)") Western States Air Quality Study Intermountain West Data Warehouse Western States Air Quality Study Modeling and Analysis of Oil & Gas Emissions Data University of North Carolina (UNC IE) ENVIRON International

Western States Air Quality Study Intermountain West Data Warehouse Western States Air Quality Study Modeling and Analysis of Oil & Gas Emissions Data University of North Carolina (UNC IE) ENVIRON International

Delivering Supply Options LDC Forum June 1, 2008, Boston. Tim Stringer Manager, U.S. Northeast Markets

Delivering Supply Options LDC Forum June 1, 2008, Boston Tim Stringer Manager, U.S. Northeast Markets Forward-Looking Information 2 This presentation may contain certain information that is forward looking

Delivering Supply Options LDC Forum June 1, 2008, Boston Tim Stringer Manager, U.S. Northeast Markets Forward-Looking Information 2 This presentation may contain certain information that is forward looking

C9-19. Slide 1. markets later in the presentation.

C9-19 Slide 1 Mr. Chairman, Commissioners. Today I am pleased to present the Office of Enforcement's Winter 2011-2012 Energy Market Assessment. The Winter Energy Assessment is staff's opportunity to share

C9-19 Slide 1 Mr. Chairman, Commissioners. Today I am pleased to present the Office of Enforcement's Winter 2011-2012 Energy Market Assessment. The Winter Energy Assessment is staff's opportunity to share

Review of Pipeline Regions

Review of Pipeline Regions 76 Eastern Pipelines 77 Eastern Pipeline Group Overview Strategic Initiatives Project Development New Business Platforms Summary 78 Eastern Pipelines Great Lakes Gas Transmission

Review of Pipeline Regions 76 Eastern Pipelines 77 Eastern Pipeline Group Overview Strategic Initiatives Project Development New Business Platforms Summary 78 Eastern Pipelines Great Lakes Gas Transmission

Measuring the Effects of Natural Gas Pipeline Constraints on Regional Pricing and Market Integration

Measuring the Effects of Natural Gas Pipeline Constraints on Regional Pricing and Market Integration Roger Avalos, Timothy Fitzgerald, and Randal Rucker Montana State University 6 November 2012 USAEE/IAEE

Measuring the Effects of Natural Gas Pipeline Constraints on Regional Pricing and Market Integration Roger Avalos, Timothy Fitzgerald, and Randal Rucker Montana State University 6 November 2012 USAEE/IAEE

NATURAL GAS MARKETS, STRUCTURES, AND MECHANISMS

NATURAL GAS MARKETS, STRUCTURES, AND MECHANISMS Mitchell DeRubis, Senior Energy Analyst Bob Yu, Senior Energy Analyst Restrictions on Use: You may use the prices, indexes, assessments and other related

NATURAL GAS MARKETS, STRUCTURES, AND MECHANISMS Mitchell DeRubis, Senior Energy Analyst Bob Yu, Senior Energy Analyst Restrictions on Use: You may use the prices, indexes, assessments and other related

A Tale of Two Fuels - Crude Oil and Natural Gas Supply. Private Capital Conference February 24, 2011 Houston, TX

A Tale of Two Fuels - Crude Oil and Natural Gas Supply Private Capital Conference February 24, 2011 Houston, TX Henry Hub Natural Gas vs. WTI Crude $/MMBTU $14 $12 $10 $8 $6 $4 $2 Henry Hub WTI 160 140

A Tale of Two Fuels - Crude Oil and Natural Gas Supply Private Capital Conference February 24, 2011 Houston, TX Henry Hub Natural Gas vs. WTI Crude $/MMBTU $14 $12 $10 $8 $6 $4 $2 Henry Hub WTI 160 140

Forecasts and Assumptions for IRP. Prepared for PNM September 2016

Forecasts and Assumptions for IRP Prepared for PNM September 2016 Answers for infrastructure and cities. Pace Global Disclaimer This Report was produced by Pace Global, a Siemens business ( Pace Global

Forecasts and Assumptions for IRP Prepared for PNM September 2016 Answers for infrastructure and cities. Pace Global Disclaimer This Report was produced by Pace Global, a Siemens business ( Pace Global

North American Natural Gas: A Crisis Ahead Or Is Chicken Little Running Around Again?

North American Natural Gas: A Crisis Ahead Or Is Chicken Little Running Around Again? Ron Denhardt Vice President, Natural Gas Services February 2003 Strategic Energy & Economic Research Inc. 781 756 0550

North American Natural Gas: A Crisis Ahead Or Is Chicken Little Running Around Again? Ron Denhardt Vice President, Natural Gas Services February 2003 Strategic Energy & Economic Research Inc. 781 756 0550

Overview. Market Alert. Back in the Black: Coal Makes Comeback. Figure 1 - Coal Stockpiles at Power Plants Key Takeaways

May 21, 2014 Market Alert Back in the Black: Coal Makes Comeback Contact: Michael Bennett, mbennett@bentekenergy.com Rocco Canonica, rcanonica@bentekenergy.com Figure 1 - Coal Stockpiles at Power Plants

May 21, 2014 Market Alert Back in the Black: Coal Makes Comeback Contact: Michael Bennett, mbennett@bentekenergy.com Rocco Canonica, rcanonica@bentekenergy.com Figure 1 - Coal Stockpiles at Power Plants

Rocky Mountain High? A Report on the Niobrara Production Rising, Infrastructure Expansions Under Way

A RBN Energy Drill Down Report Copyright 2019 RBN Energy Rocky Mountain High? Production Rising, Infrastructure Expansions Under Way Crude oil, natural gas and NGL production in the Niobrara have risen

A RBN Energy Drill Down Report Copyright 2019 RBN Energy Rocky Mountain High? Production Rising, Infrastructure Expansions Under Way Crude oil, natural gas and NGL production in the Niobrara have risen

U.S. Natural Gas and the Potential for LNG Export Growth

U.S. Natural Gas and the Potential for LNG Export Growth Presentation to: 2018 Wyoming Oil & Gas Fair By: John Harpole September 12, 2018 It is not a scarce resource anymore 2 US RIG COUNTS: Aug 2018

U.S. Natural Gas and the Potential for LNG Export Growth Presentation to: 2018 Wyoming Oil & Gas Fair By: John Harpole September 12, 2018 It is not a scarce resource anymore 2 US RIG COUNTS: Aug 2018

OIL AND GAS OUTLOOK: HOW ARE THE ENERGY MARKET AFFECTING METALS? Nicole Leonard, Project Manager, Oil & Gas Consulting Services November 2015

OIL AND GAS OUTLOOK: HOW ARE THE ENERGY MARKET AFFECTING METALS? Nicole Leonard, Project Manager, Oil & Gas Consulting Services November 2015 KEY TAKEAWAYS Macroeconomic outlook: Prices have collapsed

OIL AND GAS OUTLOOK: HOW ARE THE ENERGY MARKET AFFECTING METALS? Nicole Leonard, Project Manager, Oil & Gas Consulting Services November 2015 KEY TAKEAWAYS Macroeconomic outlook: Prices have collapsed

WEEKLY MARKET UPDATE

WEEKLY MARKET UPDATE Weekly Summary: The U.S. Energy Information Administration reported last week that natural gas storage decreased by 183 Bcf. The withdrawal for the same week last year was 230 Bcf

WEEKLY MARKET UPDATE Weekly Summary: The U.S. Energy Information Administration reported last week that natural gas storage decreased by 183 Bcf. The withdrawal for the same week last year was 230 Bcf

Why Is Natural Gas Demand Growing? James Osten Principal, Global Insight

Why Is Natural Gas Demand Growing? James Osten Principal, Global Insight The U.S. Gas Market Survives Recession High natural gas prices, but much higher oil prices Interfuel substitution: Industry is still

Why Is Natural Gas Demand Growing? James Osten Principal, Global Insight The U.S. Gas Market Survives Recession High natural gas prices, but much higher oil prices Interfuel substitution: Industry is still

Building Pipelines Continuous Improvement (QA/QC) Business Environment

Business Environment") Building Pipelines Continuous Improvement (QA/QC) Business Environment The INGAA Foundation Inc. Building Interstate Natural Gas Pipelines Continuous Improvement (QA/QC) Workshop Houston, Texas March 25

Building Pipelines Continuous Improvement (QA/QC) Business Environment The INGAA Foundation Inc. Building Interstate Natural Gas Pipelines Continuous Improvement (QA/QC) Workshop Houston, Texas March 25

U.S. Natural Gas and the Poten3al for LNG Export Growth

U.S. Natural Gas and the Poten3al for LNG Export Growth Presentation to: 2018 Wyoming Oil & Gas Fair By: John Harpole September 12, 2018 It is not a scarce resource anymore 2 US RIG COUNTS: Aug 2018 vs

U.S. Natural Gas and the Poten3al for LNG Export Growth Presentation to: 2018 Wyoming Oil & Gas Fair By: John Harpole September 12, 2018 It is not a scarce resource anymore 2 US RIG COUNTS: Aug 2018 vs

Natural Gas Next 2017: Natural Gas Storage

Natural Gas Next 2017: Natural Gas Storage Callie Kolbe Manager, Energy Analysis September 26, 2017 Natural Gas Storage Introduction to Storage Why it is the market s balancer Where it exists and who owns

Natural Gas Next 2017: Natural Gas Storage Callie Kolbe Manager, Energy Analysis September 26, 2017 Natural Gas Storage Introduction to Storage Why it is the market s balancer Where it exists and who owns

201 CALIFORNIA GAS REPORT. Prepared by the California Gas and Electric Utilities

201 CALIFORNIA GAS REPORT Prepared by the California Gas and Electric Utilities 2016 C A L I F O R N I A G A S R E P O R T PREPARED BY THE CALIFORNIA GAS AND ELECTRIC UTILITIES Southern California Gas

201 CALIFORNIA GAS REPORT Prepared by the California Gas and Electric Utilities 2016 C A L I F O R N I A G A S R E P O R T PREPARED BY THE CALIFORNIA GAS AND ELECTRIC UTILITIES Southern California Gas

Midwest Supply Update: Alliance Pipeline and Rockies Alliance Pipeline

Midwest Supply Update: Alliance Pipeline and Rockies Alliance Pipeline Tony Straquadine Government Affairs Manager Forward looking statements and information o Certain information contained in this [presentation],

Midwest Supply Update: Alliance Pipeline and Rockies Alliance Pipeline Tony Straquadine Government Affairs Manager Forward looking statements and information o Certain information contained in this [presentation],

Winter U.S. Natural Gas Production and Supply Outlook

Winter 2010-11 U.S. Natural Gas Production and Supply Outlook Prepared for Natural Gas Supply Association by: ICF International Fairfax, Virginia September, 2010 Introduction This report presents ICF s

Winter 2010-11 U.S. Natural Gas Production and Supply Outlook Prepared for Natural Gas Supply Association by: ICF International Fairfax, Virginia September, 2010 Introduction This report presents ICF s

U.S. Shale Gas in Context

U.S. Shale Gas in Context Overview of U.S. Natural Gas production and trends For National Conference of State Legislatures Natural Gas Policy Institute September 9, 215 Pittsburgh, Pennsylvania By Grant

U.S. Shale Gas in Context Overview of U.S. Natural Gas production and trends For National Conference of State Legislatures Natural Gas Policy Institute September 9, 215 Pittsburgh, Pennsylvania By Grant

Natural Gas Outlook and Drivers

Natural Gas Outlook and Drivers November 2012 33% BENTEK Energy 5% 40% Who We Are Based in Evergreen, CO 120 People 400+ Customers Subsidiary of McGraw-Hill/Platts 22% What We Do Collect, Analyze and Distribute

Natural Gas Outlook and Drivers November 2012 33% BENTEK Energy 5% 40% Who We Are Based in Evergreen, CO 120 People 400+ Customers Subsidiary of McGraw-Hill/Platts 22% What We Do Collect, Analyze and Distribute

2017 Study Program PC02: High Wind

2017 Study Program PC02: High Wind Bhavana Katyal 2 PC02: Modeling Logic Production Cost Model Scope Scope Key Questions Assumptions Increased Wind Generation Results Generation Mix/ Curtailment Dump Energy

2017 Study Program PC02: High Wind Bhavana Katyal 2 PC02: Modeling Logic Production Cost Model Scope Scope Key Questions Assumptions Increased Wind Generation Results Generation Mix/ Curtailment Dump Energy

STATE OF MICHIGAN BEFORE THE MICHIGAN PUBLIC SERVICE COMMISSION

STATE OF MICHIGAN BEFORE THE MICHIGAN PUBLIC SERVICE COMMISSION In the matter of the Application of ) DTE ELECTRIC COMPANY for ) approval of Certificates of Necessity ) pursuant to MCL 460.6s, as amended,

STATE OF MICHIGAN BEFORE THE MICHIGAN PUBLIC SERVICE COMMISSION In the matter of the Application of ) DTE ELECTRIC COMPANY for ) approval of Certificates of Necessity ) pursuant to MCL 460.6s, as amended,

Colorado Energy & Environmental Issues. Chris Hansen, PhD Senior Advisor, Janys Analytics Candidate, Colorado House of Representatives

Colorado Energy & Environmental Issues Chris Hansen, PhD Senior Advisor, Janys Analytics Candidate, Colorado House of Representatives Oil 2 Thousand Barrels per Day U.S. Crude Oil Production & Consumption,

Colorado Energy & Environmental Issues Chris Hansen, PhD Senior Advisor, Janys Analytics Candidate, Colorado House of Representatives Oil 2 Thousand Barrels per Day U.S. Crude Oil Production & Consumption,

MACRO OVERVIEW OF DESERT SOUTHWEST POWER MARKET - CHALLENGES AND OPPORTUNITIES

Power Task Force Agenda Number 4. MACRO OVERVIEW OF DESERT SOUTHWEST POWER MARKET - CHALLENGES AND OPPORTUNITIES CENTRAL ARIZONA PROJECT POWER TASK FORCE MEETING MAY 18, 2017 DALE PROBASCO MANAGING DIRECTOR

Power Task Force Agenda Number 4. MACRO OVERVIEW OF DESERT SOUTHWEST POWER MARKET - CHALLENGES AND OPPORTUNITIES CENTRAL ARIZONA PROJECT POWER TASK FORCE MEETING MAY 18, 2017 DALE PROBASCO MANAGING DIRECTOR

2000 California Gas Report P R E PA R E D B Y THE C A L I F O R N I A G A S U T I L I TIES

2000 California Gas Report P R E PA R E D B Y THE C A L I F O R N I A G A S U T I L I TIES 2000 CALIFORNIA GAS REPORT Table of Contents Page No. FOREWORD...3 EXECUTIVE SUMMARY...7 Demand Outlook...7 Gas

2000 California Gas Report P R E PA R E D B Y THE C A L I F O R N I A G A S U T I L I TIES 2000 CALIFORNIA GAS REPORT Table of Contents Page No. FOREWORD...3 EXECUTIVE SUMMARY...7 Demand Outlook...7 Gas

ENERGY OUTLOOK 2017 FALL/WINTER

ENERGY OUTLOOK 2017 FALL/WINTER With more than 105 years in the energy industry, BOK Financial is committed to helping you succeed. In this issue of the Energy Outlook, you ll learn more about the current

ENERGY OUTLOOK 2017 FALL/WINTER With more than 105 years in the energy industry, BOK Financial is committed to helping you succeed. In this issue of the Energy Outlook, you ll learn more about the current

************ Day 2 ************ ************ Session 2, Session 3 11:45 and 1:45 ************

Natural Gas Value Chain: Discussion Questions ************ Day 2 ************ ************ Session 2, Session 3 11:45 and 1:45 ************ Electric Generation What other generation fuels are in the mix?

Natural Gas Value Chain: Discussion Questions ************ Day 2 ************ ************ Session 2, Session 3 11:45 and 1:45 ************ Electric Generation What other generation fuels are in the mix?

North America Midstream Infrastructure through 2035: Capitalizing on Our Energy Abundance

North America Midstream Infrastructure through 2035: Capitalizing on Our Energy Abundance Prepared by ICF International for The INGAA Foundation, Inc. Support provided by America s Natural Gas Alliance

North America Midstream Infrastructure through 2035: Capitalizing on Our Energy Abundance Prepared by ICF International for The INGAA Foundation, Inc. Support provided by America s Natural Gas Alliance

NATURAL GAS MARKET ASSESSMENT PRELIMINARY RESULTS

CALIFORNIA ENERGY COMMISSION NATURAL GAS MARKET ASSESSMENT PRELIMINARY RESULTS In Support of the 2007 Integrated Energy Policy Report STAFF DRAFT REPORT MAY 2007 CEC-200-2007-009-SD Arnold Schwarzenegger,

CALIFORNIA ENERGY COMMISSION NATURAL GAS MARKET ASSESSMENT PRELIMINARY RESULTS In Support of the 2007 Integrated Energy Policy Report STAFF DRAFT REPORT MAY 2007 CEC-200-2007-009-SD Arnold Schwarzenegger,

Market Diversification & Infrastructure Oilmen s Executive Business Forum Banff, August 21, 2012 Dave Collyer, CAPP

Market Diversification & Infrastructure Oilmen s Executive Business Forum Banff, August 21, 2012 Dave Collyer, CAPP The Canadian Oil and Natural Gas Industry - A Key Driving Force in the Canadian Economy

Market Diversification & Infrastructure Oilmen s Executive Business Forum Banff, August 21, 2012 Dave Collyer, CAPP The Canadian Oil and Natural Gas Industry - A Key Driving Force in the Canadian Economy

We ve Seen This Movie Before

The Dynamic Energy Landscape: Natural Gas in the U.S. We ve Seen This Movie Before October 26, 2015 Production of Natural Gas, NGLs & Crude Oil Bcf/d 75 70 65 60 55 50 U.S. Lower 48 Dry Gas Production

The Dynamic Energy Landscape: Natural Gas in the U.S. We ve Seen This Movie Before October 26, 2015 Production of Natural Gas, NGLs & Crude Oil Bcf/d 75 70 65 60 55 50 U.S. Lower 48 Dry Gas Production

Kern River Gas Transmission Company. Customer Meetings 2018

Kern River Gas Transmission Company Customer Meetings 2018 1 Exceptional Businesses and Assets 11.6 million customers worldwide Top-rated service provider within the industry 22,700 employees worldwide

Kern River Gas Transmission Company Customer Meetings 2018 1 Exceptional Businesses and Assets 11.6 million customers worldwide Top-rated service provider within the industry 22,700 employees worldwide

OVERVIEW OF DESERT SOUTHWEST POWER MARKET AND ECONOMIC ASSESSMENT OF THE NAVAJO GENERATING STATION

OVERVIEW OF DESERT SOUTHWEST POWER MARKET AND ECONOMIC ASSESSMENT OF THE NAVAJO GENERATING STATION ARIZONA CORPORATION COMMISSION APRIL 6, 2017 DALE PROBASCO MANAGING DIRECTOR ROGER SCHIFFMAN DIRECTOR

OVERVIEW OF DESERT SOUTHWEST POWER MARKET AND ECONOMIC ASSESSMENT OF THE NAVAJO GENERATING STATION ARIZONA CORPORATION COMMISSION APRIL 6, 2017 DALE PROBASCO MANAGING DIRECTOR ROGER SCHIFFMAN DIRECTOR

EXPORT DEPENDENCE: THE U.S. NATURAL GAS STORY

Platts Analytics EXPORT DEPENDENCE: THE U.S. NATURAL GAS STORY Supply and Demand; Exports and Economics Rick Allen, Director, Consulting Services CoBank Energy Directors Conference June 28, 2017 Disclaimer

Platts Analytics EXPORT DEPENDENCE: THE U.S. NATURAL GAS STORY Supply and Demand; Exports and Economics Rick Allen, Director, Consulting Services CoBank Energy Directors Conference June 28, 2017 Disclaimer

NORTHEAST GAS MIDSTREAM

NORTHEAST GAS MIDSTREAM PREVIEW FundamentalEdge February 2018 learn more at drillinginfo.com Contents This is a PREVIEW of a 15+ Page Report Introduction and Key Takeaways 3 Northeast Gas Midstream 4 Production

NORTHEAST GAS MIDSTREAM PREVIEW FundamentalEdge February 2018 learn more at drillinginfo.com Contents This is a PREVIEW of a 15+ Page Report Introduction and Key Takeaways 3 Northeast Gas Midstream 4 Production

Copyright 2018 RBN Energy. Permian Global Access Pipeline (PGAP) Natural Gas Market Analysis

Natural Gas Market Analysis") Permian Global Access Pipeline (PGAP) Natural Gas Market Analysis Permian Global Access Pipeline (PGAP)» Natural gas production growth in the Permian will continue to accelerate, resulting in outbound

Permian Global Access Pipeline (PGAP) Natural Gas Market Analysis Permian Global Access Pipeline (PGAP)» Natural gas production growth in the Permian will continue to accelerate, resulting in outbound

North American Midstream Infrastructure Through 2035 A Secure Energy Future. Press Briefing June 28, 2011

North American Midstream Infrastructure Through 2035 A Secure Energy Future Press Briefing June 28, 2011 Disclaimer This presentation presents views of ICF International and the INGAA Foundation. The presentation

North American Midstream Infrastructure Through 2035 A Secure Energy Future Press Briefing June 28, 2011 Disclaimer This presentation presents views of ICF International and the INGAA Foundation. The presentation

USEA Briefing on Capitol Hill June 25, 2012 Deloitte Center for Energy Solutions and Deloitte MarketPoint LLC

Analysis of the Impact of U.S. LNG Exports on U.S. Consumers USEA Briefing on Capitol Hill June 25, 2012 Deloitte Center for Energy Solutions and Deloitte MarketPoint LLC Study analyzed key questions and

Analysis of the Impact of U.S. LNG Exports on U.S. Consumers USEA Briefing on Capitol Hill June 25, 2012 Deloitte Center for Energy Solutions and Deloitte MarketPoint LLC Study analyzed key questions and

Impacts of. Canada s Cleaner Energy Exports. Global Greenhouse Gas Emissions. Whistler, B.C. Canada. May 2002

Impacts of Canada s Cleaner Energy Exports on Global Greenhouse Gas Emissions Whistler, B.C. Canada May 2002 1. Introduction The North American economy is highly integrated. Canada and the United States

Impacts of Canada s Cleaner Energy Exports on Global Greenhouse Gas Emissions Whistler, B.C. Canada May 2002 1. Introduction The North American economy is highly integrated. Canada and the United States

The Impact of Developing Energy and Environmental Policy on the Gas Industry Plus Impacts of the Current Economic State

The Impact of Developing Energy and Environmental Policy on the Gas Industry Plus Impacts of the Current Economic State Gas / Electric Partnership Conference XVII Gas Compression from Production thru Transmission

The Impact of Developing Energy and Environmental Policy on the Gas Industry Plus Impacts of the Current Economic State Gas / Electric Partnership Conference XVII Gas Compression from Production thru Transmission

Overview of Florida s s Regulatory Environment

Overview of Florida s s Regulatory Environment October 21 st, 2011 Eduardo Balbis, P.E. Commissioner Florida Public Service Commission Florida Public Service Commission Gubernatorial Appointees Confirmed

Overview of Florida s s Regulatory Environment October 21 st, 2011 Eduardo Balbis, P.E. Commissioner Florida Public Service Commission Florida Public Service Commission Gubernatorial Appointees Confirmed

Agenda. Natural gas and power markets overview. Generation retirements and in developments. Future resource mix including large hydro

Agenda Natural gas and power markets overview Generation retirements and in developments Future resource mix including large hydro Balancing environmental, reliability and cost impacts 1 Northeast Utilities

Agenda Natural gas and power markets overview Generation retirements and in developments Future resource mix including large hydro Balancing environmental, reliability and cost impacts 1 Northeast Utilities

QUESTAR PIPELINE CUSTOMER MEETING MARCH 2017 PARK CITY, UTAH

QUESTAR PIPELINE CUSTOMER MEETING MARCH 2017 PARK CITY, UTAH Ron Jorgensen Vice President Operations & Gas Control, Questar Pipeline 2 Merger Related Update February 1, 2016 Dominion/Questar merger announced

QUESTAR PIPELINE CUSTOMER MEETING MARCH 2017 PARK CITY, UTAH Ron Jorgensen Vice President Operations & Gas Control, Questar Pipeline 2 Merger Related Update February 1, 2016 Dominion/Questar merger announced

Assessment of California Natural Gas and Electricity Markets

Assessment of California Natural Gas and Electricity Markets Prepared for: Valley Center Municipal Water District 29300 Valley Center Rd Valley Center, CA 921082-0067 By: Lon W. House, Ph.D. Water and

Assessment of California Natural Gas and Electricity Markets Prepared for: Valley Center Municipal Water District 29300 Valley Center Rd Valley Center, CA 921082-0067 By: Lon W. House, Ph.D. Water and

Recent Regulatory Developments in Gas Storage

Michael J. McGehee, Director Division of Pipeline Certificates Federal Energy Regulatory Commission Recent Regulatory Developments in Gas Storage Platt s 10 th Annual Gas Storage Outlook Houston, TX January

Michael J. McGehee, Director Division of Pipeline Certificates Federal Energy Regulatory Commission Recent Regulatory Developments in Gas Storage Platt s 10 th Annual Gas Storage Outlook Houston, TX January

October U.S. Energy Information Administration Winter Fuels Outlook October

October 2017 Winter Fuels Outlook EIA forecasts that average household expenditures for all major home heating fuels will rise this winter because of expected colder weather and higher energy costs. Average

October 2017 Winter Fuels Outlook EIA forecasts that average household expenditures for all major home heating fuels will rise this winter because of expected colder weather and higher energy costs. Average

1998 California Gas Report PREPARED BY THE CALIFORNIA GAS AND ELECTRIC UTILITIES

1998 California Gas Report PREPARED BY THE CALIFORNIA GAS AND ELECTRIC UTILITIES i ii 1998 CALIFORNIA GAS REPORT Table of Contents Page No. FOREWORD... 1 EXECUTIVE SUMMARY... 5 Demand Outlook... 7 Gas

1998 California Gas Report PREPARED BY THE CALIFORNIA GAS AND ELECTRIC UTILITIES i ii 1998 CALIFORNIA GAS REPORT Table of Contents Page No. FOREWORD... 1 EXECUTIVE SUMMARY... 5 Demand Outlook... 7 Gas

Annual Energy Outlook 2017

Annual Energy Outlook 217 Valve Manufacturers Association of America VMA Technical Seminar 217 March 2, 217 Nashville, TN By, Director, Office of Integrated and International Energy Analysis U.S. Energy

Annual Energy Outlook 217 Valve Manufacturers Association of America VMA Technical Seminar 217 March 2, 217 Nashville, TN By, Director, Office of Integrated and International Energy Analysis U.S. Energy

North American Crude Oil and Natural Gas Too Much Too Soon!

North American Crude Oil and Natural Gas Too Much Too Soon! Energy and Water Executive Forum August 9, 2018 Crude Oil, Natural Gas and Product Prices $105 250 2017 $18 $/Bbl $84 $63 $42 $21 c/gal 200 150

North American Crude Oil and Natural Gas Too Much Too Soon! Energy and Water Executive Forum August 9, 2018 Crude Oil, Natural Gas and Product Prices $105 250 2017 $18 $/Bbl $84 $63 $42 $21 c/gal 200 150

Energy Costs for Water Suppliers: Prospects and Options

Energy Costs for Water Suppliers: Prospects and Options Bill Kemp Vice President, Business Strategy & Planning Services AMWA Annual Meeting October 20, 2008 BUILDING A WORLD OF DIFFERENCE Agenda Energy

Energy Costs for Water Suppliers: Prospects and Options Bill Kemp Vice President, Business Strategy & Planning Services AMWA Annual Meeting October 20, 2008 BUILDING A WORLD OF DIFFERENCE Agenda Energy

TransCanada Natural Gas Pipelines As at December 31, 2017

TransCanada Natural Gas Pipelines As at December 31, 2017 Natural Gas Pipeline In Development/Construction Regulated Natural Gas Storage Unregulated Natural Gas Storage Liard Conventional Basins Montney

TransCanada Natural Gas Pipelines As at December 31, 2017 Natural Gas Pipeline In Development/Construction Regulated Natural Gas Storage Unregulated Natural Gas Storage Liard Conventional Basins Montney

API Industry Outlook. Third Quarter R. Dean Foreman, Ph.D. Great Plains and EmPower ND Energy Conference October 8, 2018.

API Industry Outlook Third Quarter 2018 R. Dean Foreman, Ph.D. Chief Economist American Petroleum Institute Great Plains and EmPower ND Energy Conference October 8, 2018 American Updated Petroleum September

API Industry Outlook Third Quarter 2018 R. Dean Foreman, Ph.D. Chief Economist American Petroleum Institute Great Plains and EmPower ND Energy Conference October 8, 2018 American Updated Petroleum September

OREGON PUBLIC UTILITY COMMISSION 2011 NATURAL GAS OUTLOOK WORKSHOP. August 3, :30 AM Main Hearing Room

OREGON PUBLIC UTILITY COMMISSION 2011 NATURAL GAS OUTLOOK WORKSHOP August 3, 2011 9:30 AM Main Hearing Room Agenda Overview of expected PNW natural gas prices for 2011-2012 Staff Top natural gas issues

OREGON PUBLIC UTILITY COMMISSION 2011 NATURAL GAS OUTLOOK WORKSHOP August 3, 2011 9:30 AM Main Hearing Room Agenda Overview of expected PNW natural gas prices for 2011-2012 Staff Top natural gas issues

Regional energy challenges in New England and Eastern Canada

Regional energy challenges in New England and Eastern Canada For 39 th Annual Conference of New England Governors and Eastern Canadian Premiers () August 31, 2015 St. John s By Adam Sieminski Energy Information

Regional energy challenges in New England and Eastern Canada For 39 th Annual Conference of New England Governors and Eastern Canadian Premiers () August 31, 2015 St. John s By Adam Sieminski Energy Information

FLM ISSUES AROUND THE COUNTRY EPA, STATE, LOCAL AIR QUALITY MODELERS WORKSHOP 2016

FLM ISSUES AROUND THE COUNTRY EPA, STATE, LOCAL AIR QUALITY MODELERS WORKSHOP 2016 Disclaimer The following presentation represents the current views and ideas of the federal land management agencies staff

FLM ISSUES AROUND THE COUNTRY EPA, STATE, LOCAL AIR QUALITY MODELERS WORKSHOP 2016 Disclaimer The following presentation represents the current views and ideas of the federal land management agencies staff

2008 California Gas Report. Prepared by the California Gas and Electric Utilities

2008 California Gas Report Prepared by the California Gas and Electric Utilities 2008 CALIFORNIA GAS REPORT PREPARED BY THE CALIFORNIA GAS AND ELECTRIC UTILITIES Southern California Gas Company Pacific

2008 California Gas Report Prepared by the California Gas and Electric Utilities 2008 CALIFORNIA GAS REPORT PREPARED BY THE CALIFORNIA GAS AND ELECTRIC UTILITIES Southern California Gas Company Pacific

Natural Gas Issues and Emerging Trends for the Upcoming Winter and Beyond

Natural Gas Issues and Emerging Trends for the Upcoming Winter and Beyond 2013 NASEO WINTER ENERGY OUTLOOK CONFERENCE November 1, 2013 Kevin Petak Vice President, ICF International Kevin.Petak@icfi.com

Natural Gas Issues and Emerging Trends for the Upcoming Winter and Beyond 2013 NASEO WINTER ENERGY OUTLOOK CONFERENCE November 1, 2013 Kevin Petak Vice President, ICF International Kevin.Petak@icfi.com

NYMEX - Annual Strips

Weekly Summary: The U.S. Energy Information Administration reported that natural gas storage fell by 48 billion cubic feet this week, higher than the expected reduction of 39 Bcf but considerably lower

Weekly Summary: The U.S. Energy Information Administration reported that natural gas storage fell by 48 billion cubic feet this week, higher than the expected reduction of 39 Bcf but considerably lower

Greg Hathaway Energy Source Holdings, LLC

Greg Hathaway Energy Source Holdings, LLC WEATHER THE PICTURE TO THE RIGHT SHOWS THE 2015-16 WINTER HAS BEEN MUCH ABOVE NORMAL. SINCE 2008 THE NATIONAL TEMPERATURE HAS BEEN BELOW NORMAL SIX TIMES 2013-14

Greg Hathaway Energy Source Holdings, LLC WEATHER THE PICTURE TO THE RIGHT SHOWS THE 2015-16 WINTER HAS BEEN MUCH ABOVE NORMAL. SINCE 2008 THE NATIONAL TEMPERATURE HAS BEEN BELOW NORMAL SIX TIMES 2013-14

ISO New England Gambling with Natural Gas U.S. Power and Gas Weekly.

? ISO New England Gambling with Natural Gas U.S. Power and Gas Weekly. Morningstar Commodities Research 25 January 2018 Dan Grunwald Associate, Power and Gas +1 312 244-7135 daniel.grunwald@morningstar.com

? ISO New England Gambling with Natural Gas U.S. Power and Gas Weekly. Morningstar Commodities Research 25 January 2018 Dan Grunwald Associate, Power and Gas +1 312 244-7135 daniel.grunwald@morningstar.com

Natural Gas Producer to Consumer

Natural Gas Producer to Consumer Cy Esphahanian CCOP Beijing - June 25 Scope of this Presentation History and Overview The Physical Flow of Natural Gas Infrastructure The Financial/Business Structure Pricing

Natural Gas Producer to Consumer Cy Esphahanian CCOP Beijing - June 25 Scope of this Presentation History and Overview The Physical Flow of Natural Gas Infrastructure The Financial/Business Structure Pricing

CERI Commodity Report Natural Gas

September 1 CERI Commodity Report Natural Gas Natural Gas Prices Paul Kralovic The Commodity Report Natural Gas article, Turm-oil in the Natural Gas Markets, released in February 1, explored the low natural

September 1 CERI Commodity Report Natural Gas Natural Gas Prices Paul Kralovic The Commodity Report Natural Gas article, Turm-oil in the Natural Gas Markets, released in February 1, explored the low natural

Power Sector Transition: GHG Policy and Other Key Drivers

Power Sector Transition: GHG Policy and Other Key Drivers JENNIFER MACEDONIA ARKANSAS 111(D) STAKEHOLDER MEETING MAY 28, 214 5/23/14 POWER SECTOR TRANSITION: GHG POLICY AND OTHER KEY DRIVERS 2 Purpose

Power Sector Transition: GHG Policy and Other Key Drivers JENNIFER MACEDONIA ARKANSAS 111(D) STAKEHOLDER MEETING MAY 28, 214 5/23/14 POWER SECTOR TRANSITION: GHG POLICY AND OTHER KEY DRIVERS 2 Purpose

LNG Market through. Serving the Asia Pacific. Jordan Cove LNG. Vern A. Wadey. Vice President

Serving the Asia Pacific LNG Market through Jordan Cove LNG Vern A. Wadey Vice President Pacific North West Economic Region 25th Annual Summit Big Sky, Montana Monday, July 13, 2015 Veresen Inc.: A strong,

Serving the Asia Pacific LNG Market through Jordan Cove LNG Vern A. Wadey Vice President Pacific North West Economic Region 25th Annual Summit Big Sky, Montana Monday, July 13, 2015 Veresen Inc.: A strong,

Platts Natural Gas Storage Conference. January 2012

Platts Natural Gas Storage Conference January 2012 Changing Storage Landscape Tremendous development and expansion in last 10 years has created excess capacity in the Natural Gas Storage Sector Majority

Platts Natural Gas Storage Conference January 2012 Changing Storage Landscape Tremendous development and expansion in last 10 years has created excess capacity in the Natural Gas Storage Sector Majority

Shale Gas, Drilling Access Restrictions, and the Future of US LNG Imports

Shale Gas, Drilling Access Restrictions, and the Future of US LNG Imports Peter Hartley George & Cynthia Mitchell Professor, Economics Department Academic Director, Shell Center for Sustainability Rice

Shale Gas, Drilling Access Restrictions, and the Future of US LNG Imports Peter Hartley George & Cynthia Mitchell Professor, Economics Department Academic Director, Shell Center for Sustainability Rice

Natural Gas Supply, Demand, and the Prospects for North American LNG Exports

Natural Gas Supply, Demand, and the Prospects for North American LNG Exports December 3 rd, 2014 Robert D. Stibolt Senior Managing Director Observations on natural gas prices and project returns Price

Natural Gas Supply, Demand, and the Prospects for North American LNG Exports December 3 rd, 2014 Robert D. Stibolt Senior Managing Director Observations on natural gas prices and project returns Price

The Impacts of Natural Gas Prices on the California Economy: Final Report

The Impacts of Natural Gas Prices on the California Economy: Final Report PREPARED FOR: The California Natural Gas Advisory Group PREPARED BY: Global Insight, Inc. Global Energy Services, United States

The Impacts of Natural Gas Prices on the California Economy: Final Report PREPARED FOR: The California Natural Gas Advisory Group PREPARED BY: Global Insight, Inc. Global Energy Services, United States

TESORO CREATES FULL-SERVICE LOGISTICS COMPANY TLLP ACQUIRES QEP FIELD SERVICES ASSETS

TESORO CREATES FULL-SERVICE LOGISTICS COMPANY TLLP ACQUIRES QEP FIELD SERVICES ASSETS October 20, 2014 FORWARD LOOKING STATEMENTS This Presentation includes forward-looking statements. These statements

TESORO CREATES FULL-SERVICE LOGISTICS COMPANY TLLP ACQUIRES QEP FIELD SERVICES ASSETS October 20, 2014 FORWARD LOOKING STATEMENTS This Presentation includes forward-looking statements. These statements

Insights into the future of the

Navigating a fractured future Insights into the future of the North American natural gas market A report by the Deloitte Center for Energy Solutions and Deloitte MarketPoint LLC Deloitte Center for Energy

Navigating a fractured future Insights into the future of the North American natural gas market A report by the Deloitte Center for Energy Solutions and Deloitte MarketPoint LLC Deloitte Center for Energy

Shelley Wright Kendrick General Manager, Marketing & Business Development. April 13, 2012 Platt s 6 th Annual Rockies Oil & Gas Conference

Shelley Wright Kendrick General Manager, Marketing & Business Development April 13, 2012 Platt s 6 th Annual Rockies Oil & Gas Conference 1 Questar Pipeline System Overview Overthrust Pipeline Company

Shelley Wright Kendrick General Manager, Marketing & Business Development April 13, 2012 Platt s 6 th Annual Rockies Oil & Gas Conference 1 Questar Pipeline System Overview Overthrust Pipeline Company

North American Gas Supply Outlook

Hart Energy s Commercializing Methane Hydrates Conference Houston, Texas December 5, 2006 North American Gas Supply Outlook Richard M. Tucker Vice President Ziff Energy Group Houston Calgary www.ziffenergy.com

Hart Energy s Commercializing Methane Hydrates Conference Houston, Texas December 5, 2006 North American Gas Supply Outlook Richard M. Tucker Vice President Ziff Energy Group Houston Calgary www.ziffenergy.com

Natural Gas Abundance: The Development of Shale Resource in North America

Natural Gas Abundance: The Development of Shale Resource in North America EBA Brown Bag Luncheon Bracewell & Giuliani Washington, D.C. February 6, 2013 Bruce B. Henning Vice President, Energy Regulatory

Natural Gas Abundance: The Development of Shale Resource in North America EBA Brown Bag Luncheon Bracewell & Giuliani Washington, D.C. February 6, 2013 Bruce B. Henning Vice President, Energy Regulatory

IMPACT OF CLOSING NAVAJO GENERATING STATION ON ARIZONA POWER MARKETS

IMPACT OF CLOSING NAVAJO GENERATING STATION ON ARIZONA POWER MARKETS Prepared for: Arizona Corporation Commission Mr. Seth Schwartz President schwartz@evainc.com August 2018 Energy Ventures Analysis 1901

IMPACT OF CLOSING NAVAJO GENERATING STATION ON ARIZONA POWER MARKETS Prepared for: Arizona Corporation Commission Mr. Seth Schwartz President schwartz@evainc.com August 2018 Energy Ventures Analysis 1901