Insights into the effectiveness of internal audit: a multi-method and multi-perspective study

|

|

|

- Anabel Perry

- 6 years ago

- Views:

Transcription

1 Version from: 30 January February 2013 Public defense Insights into the effectiveness of internal audit: a multi-method and multi-perspective study Rainer LENZ Doctoral Thesis Université catholique de Louvain (UCL) Louvain School of Management

2 Agenda Doctoral committee Night job Summary of my PhD dissertation... 5 Why? What? How? Results? New research opportunities Q&A

3 Doctoral committee Internal members (UCL) Prof. Philippe CHEVALIER External members Prof. Kenneth D SILVA London South Bank University, UK Prof. Yves DE RONGÉ Prof. Kim K. JEPPESEN Copenhagen Business School, Denmark Prof. Gerrit SARENS (Supervisor) Prof. Florian HOOS HEC Paris, France 3

4 4

5 Summary of my PhD dissertation

6 Why? 6

7 Most studies are based on selfassessments of internal auditors Source of cartoon: Independent Audit Limited, 7

8 The Little Prince Drawing No. 1 Research gaps identified: 1. Include the stakeholder s perspective on IA effectiveness; 2. Study factors that influence IA effectiveness and how IA effectiveness can be created and enhanced; 3. Provide definition of IA effectiveness. Source: de Saint-Exupéry (1943), LE PETIT PRINCE 8

9 Relevance of the topic The subject of IA effectiveness is topical in practice but under-examined in academic research; The Institute of Internal Auditors (IIA) claims Internal Auditing (IA) to be a pillar of Corporate Governance*; The value of IA is questioned by some of its key stakeholders. *) According to Huse (2007, 15), Corporate governance is seen as the interactions between various internal and external actors and the board members in directing a firm for value creation. 9

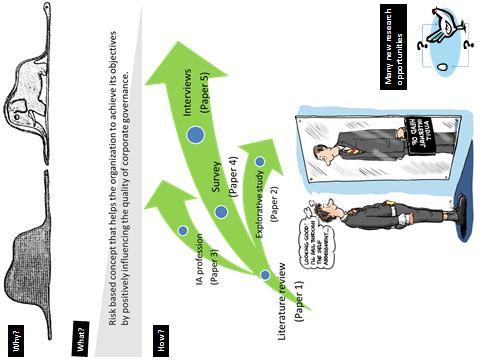

10 Motivation of research 1. Search for a path to effectiveness in IAFs Since my appointment as a Head of Internal Audit (CAE) in the summer of 2007, I have searched for a path to effectiveness in internal audit functions (IAFs). 2. Role and expectations of SM matter My first budget review as CAE in the autumn of 2007 clarified the importance of senior management s (SM s) expectations. Make the Internal Audit Function (IAF) effective in practice. 10

11 The Little Prince Drawing No. 1 Drawing No. 2 Source: de Saint-Exupéry (1943), LE PETIT PRINCE 11

12 What? 12

13 Auditing is a credence good (Causholli, 2009) Audit customers cannot discern the quality of the good even after purchasing and consuming it; Audit quality is not directly observable except in the event of an audit failure; It is relatively easy to see in hindsight when an audit was not effective (Bender, 2006). 13

14 Definition 1: IA effectiveness, definition 1 Risk based goal-attainment concept that helps the organization to achieve its objectives. 14

15 IA effectiveness, definition 2 Definition 1: Definition 2: Risk based goal-attainment concept that helps the organization to achieve its objectives. Positive influence on the quality of corporate governance (Sarens 2009). Source: Sarens, Gerrit (2009), Internal Auditing Research: Where are we going?, IJA, Vol. 13 No. 1, pp

16 IA effectiveness, definition 3 Definition 1: Definition 2: Risk based goal-attainment concept that helps the organization to achieve its objectives. Positive influence on the quality of corporate governance (Sarens 2009). Definition 3: Risk based concept that helps the organization to achieve its objectives by positively influencing the quality of corporate governance. 16

17 How? 17

18 Structure of my doctoral thesis 18

19 A multi-method and multi-perspective study Paper Method/type Perspective/theory 1 Literature review New-institutional theory and entrepreneurship (DiMaggio and Powell 1983; DiMaggio 1988) 2 Explorative work CBOK (2006) data from 782 U.S. CAEs 3 Conceptual paper Critical reflections on the IA profession 4 Empirical survey Questionnaire data from 46 German CAEs 5 Qualitative research 16 semi-structured interviews with CAEs and Senior Management in the same organization. Applied role theory (Kahn et al. 1964) in combination with the theory of relational coordination (Gittell 2006) 19

20 Five related papers 1. In Search of a Measure of Effectiveness for Internal Audit Functions: An Institutional Perspective Abacus, 2nd round 2. Factors Associated with the Internal Audit Function's Role in Corporate Governance Journal of Applied Accounting Research (2012), Vol. 13 No. 2, pp Reflections on the Internal Auditing Profession: What might have gone wrong? Managerial Auditing Journal (2012), Vol. 27 No. 6, pp Testing the discriminatory power of factors of Internal Auditing Effectiveness: Sorting the wheat from the chaff International Journal of Auditing, 2nd round 5. Internal Auditing Effectiveness: Multiple Case Study Research in Germany That Applies Role Theory and the Relational Theory of Coordination Submission to Management Science in February

21 Learn from differences As there is no typical (generic) Internal Audit Function or organization, my research seeks to study extreme cases in practice and learn from differences Review both ends of the continuum Comparatively strong and effective and poor and ineffective cases 21

: The Adventures of Tintin, The Black Island")

22 Tintin and Snowy are very effective Source: Hergé (1956): The Adventures of Tintin, The Black Island 22

23 An example of in-effectiveness 23

24 Results / key findings? 24

25 Internal Audit Effectiveness Black box 25

26 Internal Audit Effectiveness Black box Insights 26

27

28 Main contributions to academia -1 1) This dissertation uses the perspective of new institutional theory and entrepreneurship as a framework when providing a review of the existing empirical literature on IA effectiveness. 2) This dissertation offers an explanation why IA did not have a significant role in the financial crisis, neither as part of the problem nor as part of the solution. 3) This dissertation defines IA effectiveness as a risk based concept that helps the organization to achieve its objectives by positively influencing the quality of corporate governance. 28

29 Main contributions to academia -2 4) This research includes the first study that explores the variables that are associated with the IAF s role in corporate governance. 5) This dissertation is one of only a few studies and the first one in the German context, in which CAEs and SM in the same organization are interviewed. 6) Micro level forces largely determine the type of IAFs that organizations have. 7) Supply of a fresh agenda for future research on IA effectiveness. 29

30 Main contributions to practitioners 1) This study suggests what CAEs should focus on in order to increase the effectiveness of their IAF, and/or to increase its role in corporate governance. 2) The CAE should clarify the customer dimension and the purpose and mandate of its IAF in the respective organizational context. 3) This study introduces metaphors to characterize the effective internal auditor: Fingerspitzengefühl and Swimming in the organization are metaphors, evocative of an effective internal auditor who represents an effective IAF. 30

31 Metaphor Swimming in the organization : Associated with the more effective internal auditor, but that may not come risk-free Source of image: ACL (2012), Don t navigate risky waters without internal auditors: Guidance on leveraging audit analytics for risk assessment 31

32 Main contributions to the IIA 1) The dissertation shows the normative forces that demand compliance with the IA s common body of knowledge to be comparatively weak at this time. 2) The study encourages the IIA to clarify its core remit and determine a chief stakeholder. 3) The IIA should review its curricula and consider ways to increase the relevance and practical usefulness of IIA degrees, especially for CAEs. 32

33 Summary of my PhD dissertation

34 New research opportunities 34

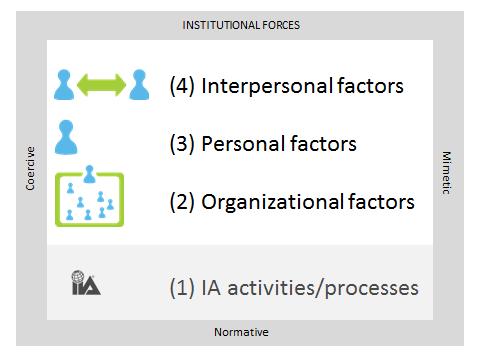

can lead to (perceived) IA")

35 Fresh agenda for IA research 40+ research questions What do we know about the causality of effective IA? Successful interpersonal interaction between the CAE and SM (and the board/ac) can lead to (perceived) IA effectiveness; In turn, rendering an IA service that is perceived as effective may also lead to improved interpersonal relations. Experimental research is encouraged to learn more about causalities between factors that influence IA effectiveness. 35

36 Q&A 36

37 Appendices 37

38 What You Know vs. How much you know about it 38

39 What? Literature review ( supply- and demand-side ) through an effectiveness lens. Paper 1 Why? Clarify the enigmatic phenomenon of IA effectiveness. Provide suggestions for future academic research on IA effectiveness. *) How? Institutional theory and institutional entrepreneurship (DiMaggio and Powell, 1983; DiMaggio, 1988) as framework. Results/key findings: Institutional forces affect IA effectiveness but cannot fully explain the plurality in practice. Organizational hypocrisy and agency are two theoretical outcomes when isomorphic forces point in different directions and/or are in conflict with organizational demands. Implication/key contribution: CAE agency is suggested as a new field for empirical research. The CAE who typically seeks to meet others expectations may become an agent who drives change. *) Q1: What characterizes the comparatively more effective, and value-adding, IAF? 39

40 What? Investigate variables that are associated with IAF s role in corporate governance. Paper 2 Why? Many IAFs do not play an active role in corporate governance. Provide guidance to strengthening the role of IAF s in corporate governance. How? Use responses from 782 U.S. CAEs in the CBOK (2006) database. Results/key findings: IAF having an active role in corporate governance is significantly and positively associated with the use of a risk-based audit plan, existence of a quality assurance and improvement program, and audit committee input to the audit plan. Implication/key contribution: For CAEs who wish to increase their IAF s role in corporate governance. The effectiveness of an IAF depends on its interactions with other corporate governance stakeholders. 40

41 Paper 3 Why? Investigate why the IA profession has been marginalized in the governance debate on solutions after the financial crisis that started in What? Conceptual discussion that offers an explanation for the IA profession s marginalization. How? Based on an objective review of relevant literature, both practitioner and academic. Results/key findings: Serve the chief stakeholder best and first (it is suggested that to be ideally the board/audit committee), and narrow but deepen the value proposition in the arena of assurance service at the expense of consulting services is the suggested path forward. Implication/key contribution: For practitioner: Clarify the ultimate customer and the core IA service. For IIA: May help when seeking universal recognition for IA as a profession. 41

42 Paper 4 Why? Identify differentiating characteristics of IAFs considering organizational factors, IA resources, IA processes, and the pattern of relationships between the CAE and key governance stakeholders. What? Rough tool for pointing to levels of IA effectiveness at both ends of the range. How? Empirical survey based on 46 CAEs in private organizations in Germany. Results/key findings: We find IAF characteristics that differentiate between IAFs that could be seen as determinants ( seeds for a theory ) of IA effectiveness: IA charter, possible career progression after a tenure in IA, some degree of co-sourcing, the level of training and professional qualification of IA staff and CAEs, the use of IA technology and risk-based IA, whether IA rates individual findings and grades the overall report, whether the CAE has appropriate access to the board/ac and senior management s (SM). Implication/key contribution: Micro-level: Get the basics in place; Rate individual findings and/or grade the overall IA report; Benefit from co-sourced services to complement the IAF s skill; Aim to improve through qualification and continuous learning; Exploit technology; Right level of informal communication with SM; Improve (and benefit from) the level of access to the board/ac. Macro-level: Upgrade the value of IA designations for CAEs; Strengthen quality assurance and improvement programs; Emphasize the link between the CAE and the oversight body. 42

43 Paper 5 Why? Improve the understanding of IA effectiveness by studying the relationship between the CAE and SM working in the same organization. What? Multiple-case-study that introduces and hardens new theories. How? 16 semi-structured interviews of CAEs and SM in private organizations in Germany. Results/key findings: Role theory (Kahn et al. 1964) when combined with the theory of relational coordination (Gittell 2006) provides a promising theoretical framework that is well tailored to the research subject of IA effectiveness. Implication/key contribution: Organizational factors: Hidden champions demand and benefit from effective IA practices. Personality factors: Swimming in the organization and Fingerspitzengefühl are suggested metaphors for effective internal auditors. Interpersonal factors: Frequent, timely and problem-solving communication nurture IA effectiveness especially when such communication is supported by shared goals, shared knowledge, and mutual respect. 43

External Quality Assessment Are You Ready? Institute of Internal Auditors

External Quality Assessment Are You Ready? Institute of Internal Auditors Objectives Describe frameworks used to assess the quality of an IA activity Discuss benefits, challenges, and success factors related

External Quality Assessment Are You Ready? Institute of Internal Auditors Objectives Describe frameworks used to assess the quality of an IA activity Discuss benefits, challenges, and success factors related

The Impact of an Organization s Governance Maturity on Its Internal Audit Activity INTRODUCTION AND INSTRUCTIONS

The Impact of an Organization s Governance Maturity on Its Internal Audit Activity INTRODUCTION AND INSTRUCTIONS The Institute of Internal Auditors Research Foundation (IIARF) is the global leader in providing

The Impact of an Organization s Governance Maturity on Its Internal Audit Activity INTRODUCTION AND INSTRUCTIONS The Institute of Internal Auditors Research Foundation (IIARF) is the global leader in providing

2012 IIA Standards Update

2012 IIA Standards Update International Internal Audit Standards Board (IIASB) October 2012 1 Session Overview Why the Standards matter Standards-setting due process The key changes in 2012 Best practices

2012 IIA Standards Update International Internal Audit Standards Board (IIASB) October 2012 1 Session Overview Why the Standards matter Standards-setting due process The key changes in 2012 Best practices

Caribbean Association of Audit Committee Members Inc. Independent Quality Assurance Assessment of the Internal Audit function

www.pwc.com/bb Caribbean Association of Audit Committee Members Inc. Independent Quality Assurance Assessment of the Internal Audit function Strengthening the Performance and Influence of the Audit Committee

www.pwc.com/bb Caribbean Association of Audit Committee Members Inc. Independent Quality Assurance Assessment of the Internal Audit function Strengthening the Performance and Influence of the Audit Committee

SIAAB Guidance #02 Internal Audit Independence- Interaction with Agency Head, Senior Staff and Placement Within the Organizational Structure

SIAAB Guidance #02 Internal Audit Independence- Interaction with Agency Head, Senior Staff and Placement Within the Organizational Structure SIAAB Interpretation Adopted July 9, 2013 Revised In Accordance

SIAAB Guidance #02 Internal Audit Independence- Interaction with Agency Head, Senior Staff and Placement Within the Organizational Structure SIAAB Interpretation Adopted July 9, 2013 Revised In Accordance

IIA 2015 Worldwide survey of 15,000 internal auditors

IIA 2015 Worldwide survey of 15,000 internal auditors Michael P. Cangemi CPA, retired CISA, CGMA retired Former CFO, CEO & Director; Audit Com Chair Senior Fellow Rutgers CA Lab Senior Advisor/Investor

IIA 2015 Worldwide survey of 15,000 internal auditors Michael P. Cangemi CPA, retired CISA, CGMA retired Former CFO, CEO & Director; Audit Com Chair Senior Fellow Rutgers CA Lab Senior Advisor/Investor

STOP ACTING LIKE AUDITORS!

STOP ACTING LIKE AUDITORS! THE HUMAN SIDE OF AUDITING Steve Goodson, Lecturer The University of Texas, McCombs School of Business CIA, CGAP, CCSA, CISA, CRMA, CLEA May 6, 2016 What would you say you do

STOP ACTING LIKE AUDITORS! THE HUMAN SIDE OF AUDITING Steve Goodson, Lecturer The University of Texas, McCombs School of Business CIA, CGAP, CCSA, CISA, CRMA, CLEA May 6, 2016 What would you say you do

The IPPF in How changes to The IIA s guidance framework can benefit internal auditors and SAIs

The IPPF in 2017 How changes to The IIA s guidance framework can benefit internal auditors and SAIs From the Previous IPPF To the New IPPF International Professional Practices Framework Launched July 2015

The IPPF in 2017 How changes to The IIA s guidance framework can benefit internal auditors and SAIs From the Previous IPPF To the New IPPF International Professional Practices Framework Launched July 2015

10/5/2016. Quality Assessment Review. Agenda. What s the purpose of a QAR? Internal Audit Manager Training October 3-4, 2016

Quality Assessment Review Internal Audit Manager Training October 3-4, 2016 Lori Clark CIGA, CCEP, CGAP Compliance & Audit Specialist State University System of Florida Agenda What s the purpose of a QAR?

Quality Assessment Review Internal Audit Manager Training October 3-4, 2016 Lori Clark CIGA, CCEP, CGAP Compliance & Audit Specialist State University System of Florida Agenda What s the purpose of a QAR?

Quality Assurance in Internal Audit. Standard on Internal Audit (SIA) 7

7") Quality Assurance in Internal Audit Standard on Internal Audit (SIA) 7 1 Agenda Introduction Expectations from Internal Audit Quality Assurance Framework Internal Quality Review External Quality Review

Quality Assurance in Internal Audit Standard on Internal Audit (SIA) 7 1 Agenda Introduction Expectations from Internal Audit Quality Assurance Framework Internal Quality Review External Quality Review

Implementation Guide 1312

Implementation Guide 1312 Standard 1312 External Assessments External assessments must be conducted at least once every five years by a qualified, independent assessor or assessment team from outside the

Implementation Guide 1312 Standard 1312 External Assessments External assessments must be conducted at least once every five years by a qualified, independent assessor or assessment team from outside the

Quality Assurance and Improvement Program

Internal Audit Foundations Standards 1000, 1010, 1100, 1110, 1111, 1120, 1130, 1300, 1310, 1320, 1321, 1322, 2000, 2040 There is an Internal Audit Charter in place Internal Audit Charter is in place The

Internal Audit Foundations Standards 1000, 1010, 1100, 1110, 1111, 1120, 1130, 1300, 1310, 1320, 1321, 1322, 2000, 2040 There is an Internal Audit Charter in place Internal Audit Charter is in place The

Good Practices of the Audit Committee

Good Practices of the Audit Committee Richard F. Chambers, CIA, QIAL, CGAP, CCSA, CRMA President and Chief Executive Officer The Institute of Internal Auditors Overview Audit Committee s Core responsibilities

Good Practices of the Audit Committee Richard F. Chambers, CIA, QIAL, CGAP, CCSA, CRMA President and Chief Executive Officer The Institute of Internal Auditors Overview Audit Committee s Core responsibilities

Internal Audit Quality Analysis Evaluation against the Standards International Standards for the Professional Practice of Internal Auditing (2017)

") Internal Audit Quality Analysis Evaluation against the Standards International Standards for the Professional Practice of Internal Auditing (2017) Assessor 1: Assessor 2: Date: Date: Legend: Generally

Internal Audit Quality Analysis Evaluation against the Standards International Standards for the Professional Practice of Internal Auditing (2017) Assessor 1: Assessor 2: Date: Date: Legend: Generally

INFORMATION SECURITY MANAGEMENT MATURITY: A STUDY OF SELECT ORGANIZATIONS

INFORMATION SECURITY MANAGEMENT MATURITY: A STUDY OF SELECT ORGANIZATIONS ABHISHEK NARAIN SINGH DEPARTMENT OF MANAGEMENT STUDIES INDIAN INSTITUTE OF TECHNOLOGY DELHI MARCH, 2014 Indian Institute of Technology

INFORMATION SECURITY MANAGEMENT MATURITY: A STUDY OF SELECT ORGANIZATIONS ABHISHEK NARAIN SINGH DEPARTMENT OF MANAGEMENT STUDIES INDIAN INSTITUTE OF TECHNOLOGY DELHI MARCH, 2014 Indian Institute of Technology

Implementation Guide 2050

Implementation Guide 2050 Standard 2050 Coordination and Reliance The chief audit executive should share information, coordinate activities, and consider relying upon the work of other internal and external

Implementation Guide 2050 Standard 2050 Coordination and Reliance The chief audit executive should share information, coordinate activities, and consider relying upon the work of other internal and external

Integrated Reporting: What Is Internal Audit s Role? INTRODUCTION AND INSTRUCTIONS

Integrated Reporting: What Is Internal Audit s Role? INTRODUCTION AND INSTRUCTIONS The Institute of Internal Auditors Research Foundation (IIARF) is the global leader in providing research and knowledge

Integrated Reporting: What Is Internal Audit s Role? INTRODUCTION AND INSTRUCTIONS The Institute of Internal Auditors Research Foundation (IIARF) is the global leader in providing research and knowledge

Meeting Stakeholder Expectations for Assurance: Internal Audit s Role in a Group Effort

Meeting Stakeholder Expectations for Assurance: Internal Audit s Role in a Group Effort Urton Anderson The University of Texas at Austin 1 2 Agenda The IA Value Proposition The Demand for Assurance Assurance

Meeting Stakeholder Expectations for Assurance: Internal Audit s Role in a Group Effort Urton Anderson The University of Texas at Austin 1 2 Agenda The IA Value Proposition The Demand for Assurance Assurance

Changes in the IIA Standards: New Requirements for Internal Audit Functions

Changes in the IIA Standards: New Requirements for Internal Audit Functions Summary of Changes Effective January 1, 2009, the IIA made changes to the IIA Standards: Changed from should to must throughout

Changes in the IIA Standards: New Requirements for Internal Audit Functions Summary of Changes Effective January 1, 2009, the IIA made changes to the IIA Standards: Changed from should to must throughout

JOB DESCRIPTION. You will need to be able to travel to London and other parts of the UK, with occasional nights away from home.

JOB DESCRIPTION Job title: Location: Reports to: Job level: Head of Primary Care Contracting Leeds Assistant Director - Primary Care Contracting Grade B Date prepared: May 2017 PURPOSE The Primary Care

JOB DESCRIPTION Job title: Location: Reports to: Job level: Head of Primary Care Contracting Leeds Assistant Director - Primary Care Contracting Grade B Date prepared: May 2017 PURPOSE The Primary Care

Bachelor of Science (Honours)

") Bachelor of Science (Honours) Business Management Business Management with Communications Business Management with Communications and Year in Industry Business Management with Industrial Placement International

Bachelor of Science (Honours) Business Management Business Management with Communications Business Management with Communications and Year in Industry Business Management with Industrial Placement International

Public Sector Internal Auditors Body of Knowledge (BoK) T&C workshop October 18-19, 2010

T&C workshop October 18-19, 2010") Public Sector Internal Auditors Body of Knowledge (BoK) T&C workshop October 18-19, 2010 14/12/2006 Yalta conclusion Members want more information and data about the content of the modules for public sector

Public Sector Internal Auditors Body of Knowledge (BoK) T&C workshop October 18-19, 2010 14/12/2006 Yalta conclusion Members want more information and data about the content of the modules for public sector

Leadership and Rising Stakeholder Expectations

Leadership and Rising Stakeholder Expectations Larry Harrington VP, Internal Audit Raytheon Company December 16, 2014 Copyright 2014 Raytheon Company. All rights reserved. Customer Success Is Our Mission

Leadership and Rising Stakeholder Expectations Larry Harrington VP, Internal Audit Raytheon Company December 16, 2014 Copyright 2014 Raytheon Company. All rights reserved. Customer Success Is Our Mission

Developing an Integrated Anti-Fraud, Compliance, and Ethics Program

Developing an Integrated Anti-Fraud, Compliance, and Ethics Program Establishing an Effective Anti-Fraud, Compliance, and Ethics Function 2018 Association of Certified Fraud Examiners, Inc. Discussion

Developing an Integrated Anti-Fraud, Compliance, and Ethics Program Establishing an Effective Anti-Fraud, Compliance, and Ethics Function 2018 Association of Certified Fraud Examiners, Inc. Discussion

The European Charter for Researchers and The Code of Conduct for the Recruitment of Researchers (C&C)

") THE CYPRUS INSTITUTE OF NEUROLOGY AND GENETICS THE HUMAN RESOURCES STRATEGY FOR RESEARCHERS INCORPORATING The European Charter for Researchers and The Code of Conduct for the Recruitment of Researchers

THE CYPRUS INSTITUTE OF NEUROLOGY AND GENETICS THE HUMAN RESOURCES STRATEGY FOR RESEARCHERS INCORPORATING The European Charter for Researchers and The Code of Conduct for the Recruitment of Researchers

Value-Added Internal Audit: Myth or Reality?

Value-Added Internal Audit: Myth or Reality? Istanbul 12 November 2013 Jean-Pierre Garitte, CIA, CCSA, CISA, CFE, RFA Past Chairman of the Board IIA Past President ECIIA Polling question #1 For how long

Value-Added Internal Audit: Myth or Reality? Istanbul 12 November 2013 Jean-Pierre Garitte, CIA, CCSA, CISA, CFE, RFA Past Chairman of the Board IIA Past President ECIIA Polling question #1 For how long

Practice Advisory : Quality Assurance and Improvement Program

Practice Advisory 1300-1: Quality Assurance and Improvement Program Primary Related Standard 1300: Quality Assurance and Improvement Program The chief audit executive must develop and maintain a quality

Practice Advisory 1300-1: Quality Assurance and Improvement Program Primary Related Standard 1300: Quality Assurance and Improvement Program The chief audit executive must develop and maintain a quality

#PurposeServiceImpact IIA Global Chairman s Theme

#PurposeServiceImpact 2017-18 IIA Global Chairman s Theme J. Michael Peppers, CIA, QIAL, CRMA 2017-18 Chairman of The IIA Global Board Chief Audit Executive, University of Texas System @jmpeppers Retweeted

#PurposeServiceImpact 2017-18 IIA Global Chairman s Theme J. Michael Peppers, CIA, QIAL, CRMA 2017-18 Chairman of The IIA Global Board Chief Audit Executive, University of Texas System @jmpeppers Retweeted

World Anti Corruption Forum

World Anti Corruption Forum Anti Corruption in Public and Private Sectors 24-25 September 2012, Amman Jordan THE EFFECTIVE ROLE OF ACADEMIA AND PROFESSIONAL INSTITUTIONS IN CORRUPTION DETECTION Hossam

World Anti Corruption Forum Anti Corruption in Public and Private Sectors 24-25 September 2012, Amman Jordan THE EFFECTIVE ROLE OF ACADEMIA AND PROFESSIONAL INSTITUTIONS IN CORRUPTION DETECTION Hossam

Implementation Guides

Implementation Guides Implementation Guides assist internal auditors in applying the Definition of Internal Auditing, the Code of Ethics, and the Standards and promoting good practices. Implementation

Implementation Guides Implementation Guides assist internal auditors in applying the Definition of Internal Auditing, the Code of Ethics, and the Standards and promoting good practices. Implementation

Requisite competencies for government Chief Information Officer in Sri Lanka

Page1 ISSN: 2302-4593 Vol. 2 (7): 1-11 Requisite competencies for government Chief Information Officer in Sri Lanka Kanchana Thudugala Information and Communication Technology Agency, Sri Lanka kanchanat75@gmail.com

Page1 ISSN: 2302-4593 Vol. 2 (7): 1-11 Requisite competencies for government Chief Information Officer in Sri Lanka Kanchana Thudugala Information and Communication Technology Agency, Sri Lanka kanchanat75@gmail.com

PULSE OF INTERNAL AUDIT Navigating an Increasingly Volatile Risk Environment.

PULSE OF INTERNAL AUDIT Navigating an Increasingly Volatile Risk Environment www.theiia.org/cae Overview Pulse of Internal Auditing: Assessing Emerging and Evolving Risks is a Key Priority Linking Risks

PULSE OF INTERNAL AUDIT Navigating an Increasingly Volatile Risk Environment www.theiia.org/cae Overview Pulse of Internal Auditing: Assessing Emerging and Evolving Risks is a Key Priority Linking Risks

Implementation Guide 1000

Implementation Guide 1000 Standard 1000 Purpose, Authority, and Responsibility The purpose, authority, and responsibility of the internal audit activity must be formally defined in an internal audit charter,

Implementation Guide 1000 Standard 1000 Purpose, Authority, and Responsibility The purpose, authority, and responsibility of the internal audit activity must be formally defined in an internal audit charter,

Quality Assessments what you need to know

Quality Assessments what you need to know Patty Miller, Partner Deloitte & Touche LLP Cavell Alexander, VP-Internal Audit Intermountain Healthcare Overview of requirements Scope of assessment Approaches

Quality Assessments what you need to know Patty Miller, Partner Deloitte & Touche LLP Cavell Alexander, VP-Internal Audit Intermountain Healthcare Overview of requirements Scope of assessment Approaches

International Finance Corporation

International Finance Corporation Corporate Governance and Internal Audit Overview Bob Lamm Independent Senior Advisor Center for Corporate Governance Deloitte LLP Neil White Global IA Analytics Leader

International Finance Corporation Corporate Governance and Internal Audit Overview Bob Lamm Independent Senior Advisor Center for Corporate Governance Deloitte LLP Neil White Global IA Analytics Leader

CORPORATE GOVERNANCE THEORY, SCOPE AND IMPORTANCE

CORPORATE GOVERNANCE THEORY, SCOPE AND IMPORTANCE What is on the agenda Corporate Governance: In Theory Brief history The concept Principles Corporate Governance: In Practice Corporate governance elements

CORPORATE GOVERNANCE THEORY, SCOPE AND IMPORTANCE What is on the agenda Corporate Governance: In Theory Brief history The concept Principles Corporate Governance: In Practice Corporate governance elements

(NAME) BACCALAUREATE SOCIAL WORK PROGRAM. ASSESSMENT OF STUDENT LEARNING OUTCOMES ( Academic Year) LAST COMPLETED ON July

BACCALAUREATE SOCIAL WORK PROGRAM. ASSESSMENT OF STUDENT LEARNING OUTCOMES ( Academic Year) LAST COMPLETED ON July") (NAME) BACCALAUREATE SOCIAL WORK PROGRAM ASSESSMENT OF STUDENT LEARNING OUTCOMES (2015-16 Academic Year) LAST COMPLETED ON July 20 2016 Form AS4 (B) Duplicate and expand as needed. Provide table(s) to

(NAME) BACCALAUREATE SOCIAL WORK PROGRAM ASSESSMENT OF STUDENT LEARNING OUTCOMES (2015-16 Academic Year) LAST COMPLETED ON July 20 2016 Form AS4 (B) Duplicate and expand as needed. Provide table(s) to

EFFECTIVENESS OF AUDIT COMMITTEES IN THE PUBLIC SECTOR

INSTITUTE OF CERTIFIED PUBLIC ACCOUNTANTS OF KENYA EFFECTIVENESS OF AUDIT COMMITTEES IN THE PUBLIC SECTOR WEDNESDAY, 12 TH OCTOBER 2016 @ Sarova Whitesands Hotel, Mombasa Credibility. Professionalism.

INSTITUTE OF CERTIFIED PUBLIC ACCOUNTANTS OF KENYA EFFECTIVENESS OF AUDIT COMMITTEES IN THE PUBLIC SECTOR WEDNESDAY, 12 TH OCTOBER 2016 @ Sarova Whitesands Hotel, Mombasa Credibility. Professionalism.

Copyright 2016 The William Averette Anderson Fund 501(c)(3)

(3)") Mentee Guide Table of Contents BAF Background... 2 BAF Mentoring Program... 2 Defining Mentoring... 3 Being an Effective Mentee... 4 Key Considerations for Prospective Mentees... 5 Next Steps... 8 The

Mentee Guide Table of Contents BAF Background... 2 BAF Mentoring Program... 2 Defining Mentoring... 3 Being an Effective Mentee... 4 Key Considerations for Prospective Mentees... 5 Next Steps... 8 The

Strategy-related auditing explored

1 Strategy-related auditing explored 2 3 A recent news article 4 Agenda Introduction The research project What do internal auditors do with strategy? What is strategy? Results of research Discussion Way

1 Strategy-related auditing explored 2 3 A recent news article 4 Agenda Introduction The research project What do internal auditors do with strategy? What is strategy? Results of research Discussion Way

Agenda. How the strategy was developed. Update from your feedback in the first Informal Consultation. Implementation plan and progress so far

People Strategy Agenda How the strategy was developed Update from your feedback in the first Informal Consultation Implementation plan and progress so far How we developed the People Strategy Views from

People Strategy Agenda How the strategy was developed Update from your feedback in the first Informal Consultation Implementation plan and progress so far How we developed the People Strategy Views from

Please see the website for further information:

Foundation for Auditing Research: Call for Research Project Proposals 2018 December 2017 What is FAR? The Dutch Foundation for Auditing Research (FAR) was launched in Amsterdam on October 20, 2015. While

Foundation for Auditing Research: Call for Research Project Proposals 2018 December 2017 What is FAR? The Dutch Foundation for Auditing Research (FAR) was launched in Amsterdam on October 20, 2015. While

MBA Curriculum Program Schedule

MBA Curriculum Program Schedule Click on Course Title to see Course Description Accounting ACCT 600 1 st Semester Finance FIN 620 Leadership & Ethics BUAD 625 Information Technology & Supply Chain INSS

MBA Curriculum Program Schedule Click on Course Title to see Course Description Accounting ACCT 600 1 st Semester Finance FIN 620 Leadership & Ethics BUAD 625 Information Technology & Supply Chain INSS

WORKING PAPER 2014/02. The Champion Role of the Internal Audit Function in Combined Assurance. Loïc Decaux, Louvain School of Management

WORKING PAPER 2014/02 The Champion Role of the Internal Audit Function in Combined Assurance Loïc Decaux, Louvain School of Management Gerrit Sarens, Louvain School of Management LOUVAIN SCHOOL O F MA

WORKING PAPER 2014/02 The Champion Role of the Internal Audit Function in Combined Assurance Loïc Decaux, Louvain School of Management Gerrit Sarens, Louvain School of Management LOUVAIN SCHOOL O F MA

Quality Assurance and Improvement Program (QAIP)

") Quality Assurance and Improvement Program (QAIP) Presenters: Lori Carmichael, CPA Rafael Guijarro, CPA Florida Michigan North Carolina Texas Insight. Oversight. Foresight. Class Overview Overview- QAIP

Quality Assurance and Improvement Program (QAIP) Presenters: Lori Carmichael, CPA Rafael Guijarro, CPA Florida Michigan North Carolina Texas Insight. Oversight. Foresight. Class Overview Overview- QAIP

Auditor General s Office APPENDIX 1 REVIEW OF INFORMATION TECHNOLOGY TRAINING. October 30, 2009

APPENDIX 1 REVIEW OF INFORMATION TECHNOLOGY TRAINING October 30, 2009 Auditor General s Office Jeffrey Griffiths, C.A., C.F.E. Auditor General City of Toronto TABLE OF CONTENTS EXECUTIVE SUMMARY...1 BACKGROUND...3

APPENDIX 1 REVIEW OF INFORMATION TECHNOLOGY TRAINING October 30, 2009 Auditor General s Office Jeffrey Griffiths, C.A., C.F.E. Auditor General City of Toronto TABLE OF CONTENTS EXECUTIVE SUMMARY...1 BACKGROUND...3

Implementation Guide 1200

Implementation Guide 1200 Standard 1200 Proficiency and Due Professional Care Engagements must be performed with proficiency and due professional care. Revised Standards Effective 1 January 2017 Getting

Implementation Guide 1200 Standard 1200 Proficiency and Due Professional Care Engagements must be performed with proficiency and due professional care. Revised Standards Effective 1 January 2017 Getting

Agenda item XV The WCO PICARD Programme a PICARD 2020 strategy

Agenda item XV The WCO PICARD Programme a PICARD 2020 strategy Partnership In Customs Academic Research and Development Doc. HC0033 Contents 1. Introduction and Background 2. Management of the PICARD Programme

Agenda item XV The WCO PICARD Programme a PICARD 2020 strategy Partnership In Customs Academic Research and Development Doc. HC0033 Contents 1. Introduction and Background 2. Management of the PICARD Programme

Internal Audit Best Practices for Community Banks. A CSH White Paper

Internal Audit Best Practices for Community Banks A CSH White Paper Internal audit is not an option; examiners expect your bank to have an effective internal audit program in place. However, in today s

Internal Audit Best Practices for Community Banks A CSH White Paper Internal audit is not an option; examiners expect your bank to have an effective internal audit program in place. However, in today s

Practical Experience Requirements

International Accounting Education Standards Board AGENDA ITEM 3-2 RE-DRAFTED IES 5 October 2008 International Education Standard 5 Practical Experience Requirements International Accounting Education

International Accounting Education Standards Board AGENDA ITEM 3-2 RE-DRAFTED IES 5 October 2008 International Education Standard 5 Practical Experience Requirements International Accounting Education

Internal Audit Department

O C B o a r d o f S u p e r v i s o r s 1 st District Janet Nguyen 2 nd District John M.W. Moorlach, Vice Chairman 3 rd District Bill Campbell, Chairman 4 th District Shawn Nelson 5 th District Patricia

O C B o a r d o f S u p e r v i s o r s 1 st District Janet Nguyen 2 nd District John M.W. Moorlach, Vice Chairman 3 rd District Bill Campbell, Chairman 4 th District Shawn Nelson 5 th District Patricia

AUDIT COMMITTEE REPORTING: TRENDS & BEST PRACTICES Timothy Etoori Head of Internal Audit UGAFODE Microfinance

AUDIT COMMITTEE REPORTING: TRENDS & BEST PRACTICES Timothy Etoori Head of Internal Audit UGAFODE Microfinance The Internal Auditors Workshop Institute of Certified Public Accountants of Uganda 1 2 February,

AUDIT COMMITTEE REPORTING: TRENDS & BEST PRACTICES Timothy Etoori Head of Internal Audit UGAFODE Microfinance The Internal Auditors Workshop Institute of Certified Public Accountants of Uganda 1 2 February,

Internal Audit Challenges & Opportunities Speaker: Laurie Shen, Director, Grant Thornton LLP

Internal Audit Challenges & Opportunities Speaker: Laurie Shen, Director, Grant Thornton LLP March 28, 2012-1 - Speaker Introduction Laurie Shen is a Director at Grant Thornton's Northeast Internal Audit

Internal Audit Challenges & Opportunities Speaker: Laurie Shen, Director, Grant Thornton LLP March 28, 2012-1 - Speaker Introduction Laurie Shen is a Director at Grant Thornton's Northeast Internal Audit

From Dubai to Beijing

From Dubai to Beijing (How we use your GC input) Anton van Wyk, Chairman of the Board What Happens After GC? Global Council plays a key role in the governance process of The IIA. Discussion results are

From Dubai to Beijing (How we use your GC input) Anton van Wyk, Chairman of the Board What Happens After GC? Global Council plays a key role in the governance process of The IIA. Discussion results are

Agenda. Enterprise Risk Management Defined. The Intersection of Enterprise-wide Risk Management (ERM) and Business Continuity Management (BCM)

and Business Continuity Management (BCM)") The Intersection of Enterprise-wide Risk (ERM) and Business Continuity (BCM) Marc Dominus 2005 Protiviti Inc. EOE Agenda Terminology and Process Introductions ERM Process Overview BCM Process Overview

The Intersection of Enterprise-wide Risk (ERM) and Business Continuity (BCM) Marc Dominus 2005 Protiviti Inc. EOE Agenda Terminology and Process Introductions ERM Process Overview BCM Process Overview

GLOBAL ADVOCACY PLATFORM

GLOBAL ADVOCACY PLATFORM 2 INTRODUCTION The Global Advocacy Platform has been developed to support the advocacy efforts of IIA institutes, chapters, volunteers, members, and other practitioners and stakeholders

GLOBAL ADVOCACY PLATFORM 2 INTRODUCTION The Global Advocacy Platform has been developed to support the advocacy efforts of IIA institutes, chapters, volunteers, members, and other practitioners and stakeholders

Maneuvering the Politics of Internal Auditing to Make Positive Change. Richard F. Chambers, CIA, QIAL, CGAP, CCSA, CRMA IIA President and CEO

Maneuvering the Politics of Internal Auditing to Make Positive Change Richard F. Chambers, CIA, QIAL, CGAP, CCSA, CRMA IIA President and CEO Discussion Topics Politics of Internal Auditing Approach/Research/Results

Maneuvering the Politics of Internal Auditing to Make Positive Change Richard F. Chambers, CIA, QIAL, CGAP, CCSA, CRMA IIA President and CEO Discussion Topics Politics of Internal Auditing Approach/Research/Results

CHARTER OF THE SONOMA COUNTY INTERNAL AUDIT FUNCTION JANUARY 15, 2013

I. Introduction CHARTER OF THE JANUARY 15, 2013 ATTACHMENT B Fiscal Policy IA-1 A. The Institute of Internal Auditors (IIA) defines internal auditing as "an independent objective assurance and consulting

I. Introduction CHARTER OF THE JANUARY 15, 2013 ATTACHMENT B Fiscal Policy IA-1 A. The Institute of Internal Auditors (IIA) defines internal auditing as "an independent objective assurance and consulting

REVISED CORPORATE GOVERNANCE PRINCIPLES FOR BANKS (CONSULTATION PAPER) ISSUED BY THE BASEL COMMITTEE ON BANKING SUPERVISION

ISSUED BY THE BASEL COMMITTEE ON BANKING SUPERVISION") January 9, 2015 Secretariat of the Basel Committee on Banking Supervision Bank for International Settlements CH-4002 Basel, Switzerland Submitted via http://www.bis.org/bcbs/commentupload.htm REVISED CORPORATE

January 9, 2015 Secretariat of the Basel Committee on Banking Supervision Bank for International Settlements CH-4002 Basel, Switzerland Submitted via http://www.bis.org/bcbs/commentupload.htm REVISED CORPORATE

Session 6C Internal audit value Developing metrics to present IA value

Session 6C Internal audit value Developing metrics to present IA value Lawrence J. Harrington CIA QIAL CRMA, Vice President, Internal Audit, Raytheon Company, USA and Chairman of the Board, IIA-Global

Session 6C Internal audit value Developing metrics to present IA value Lawrence J. Harrington CIA QIAL CRMA, Vice President, Internal Audit, Raytheon Company, USA and Chairman of the Board, IIA-Global

BEST PRACTICES FOR AUDIT COMMITTEES

BEST PRACTICES FOR AUDIT COMMITTEES Introduction This document summarises key international best practices with respect to Audit Committees. In particular it presents the principles governing: the purpose

BEST PRACTICES FOR AUDIT COMMITTEES Introduction This document summarises key international best practices with respect to Audit Committees. In particular it presents the principles governing: the purpose

June 2016 Issue 05/2016

CBOK 2015: THE TOP 7 SKILLS CAEs WANT Building the right mix of talent for your organisation This report is part of the 2015 Global Internal Audit Common Body of Knowledge (CBOK) Practitioner Study series.

CBOK 2015: THE TOP 7 SKILLS CAEs WANT Building the right mix of talent for your organisation This report is part of the 2015 Global Internal Audit Common Body of Knowledge (CBOK) Practitioner Study series.

IAESB GLOSSARY OF TERMS

AGENDA ITEM 9-2 CLEAN Version 1. This glossary comprises a collection of defined terms, many of which have been specifically defined within existing IAESB pronouncements. Some of the existing terms may

AGENDA ITEM 9-2 CLEAN Version 1. This glossary comprises a collection of defined terms, many of which have been specifically defined within existing IAESB pronouncements. Some of the existing terms may

Corporate Social Responsibility (CSR)

") Heads of Internal Audit Service Benchmarking Report Corporate Social Responsibility (CSR) Introduction The aim of this survey is to gauge the level of development that organisations have achieved with

Heads of Internal Audit Service Benchmarking Report Corporate Social Responsibility (CSR) Introduction The aim of this survey is to gauge the level of development that organisations have achieved with

Dexia Group Audit Charter

January 2013 Dexia Group Audit Charter The present Charter states the fundamental principles governing the internal audit function in the Dexia Group, describing its objectives, its role, responsibilities

January 2013 Dexia Group Audit Charter The present Charter states the fundamental principles governing the internal audit function in the Dexia Group, describing its objectives, its role, responsibilities

Implementation Guide 1300

Implementation Guide 1300 Standard 1300 Quality Assurance and Improvement Program The chief audit executive must develop and maintain a quality assurance and improvement program that covers all aspects

Implementation Guide 1300 Standard 1300 Quality Assurance and Improvement Program The chief audit executive must develop and maintain a quality assurance and improvement program that covers all aspects

Tools & Techniques II: Lead Auditor

About This Course Tools & Techniques II: Lead Auditor Course Description Learn the skills necessary to lead an audit team with confidence. This course provides an overview of the life cycle of an audit

About This Course Tools & Techniques II: Lead Auditor Course Description Learn the skills necessary to lead an audit team with confidence. This course provides an overview of the life cycle of an audit

University of Greenwich

JOB DESCRIPTION Job Title: Head, Research and Enterprise Training Institute Grade: SG10 Directorate: Role reports to: Direct Reports Indirect Reports: Other Key contacts: Greenwich Research & Enterprise

JOB DESCRIPTION Job Title: Head, Research and Enterprise Training Institute Grade: SG10 Directorate: Role reports to: Direct Reports Indirect Reports: Other Key contacts: Greenwich Research & Enterprise

2017 Global Council Global Council Background Papers

2017 Global Council 2017 Global Council Background Papers A. Agenda... Page 3 B. Global Council Overview Pages 4 6 C. Background Paper #1: Strategic Planning.. Pages 7 10 D. Background Paper #2: Stakeholder

2017 Global Council 2017 Global Council Background Papers A. Agenda... Page 3 B. Global Council Overview Pages 4 6 C. Background Paper #1: Strategic Planning.. Pages 7 10 D. Background Paper #2: Stakeholder

External Quality Assessment of the Internal Audit Activity at. County of Orange. April County of Orange Final Report: June 13,

Eternal Quality Assessment of the Internal Audit Activity at County of Orange April 2017 County of Orange Final Report: June 13, 2017 1 EXECUTIVE SUMMARY... 3 OPINION AS TO CONFORMANCE... 3 PART I MATTERS

Eternal Quality Assessment of the Internal Audit Activity at County of Orange April 2017 County of Orange Final Report: June 13, 2017 1 EXECUTIVE SUMMARY... 3 OPINION AS TO CONFORMANCE... 3 PART I MATTERS

Program Evaluation and Performance Measurement An Introduction to Practice

SECOND EDITION Program Evaluation and Performance Measurement An Introduction to Practice JAMES C. McDAVID University of Victoria, Canada IRENE HUSE LAURA R.L. HAWTHORN (DSAGE Los Angeles London New Delhi

SECOND EDITION Program Evaluation and Performance Measurement An Introduction to Practice JAMES C. McDAVID University of Victoria, Canada IRENE HUSE LAURA R.L. HAWTHORN (DSAGE Los Angeles London New Delhi

Managerial Auditing Journal Emerald Article: Usage of Internal Auditing Standards by companies in the United States and select European countries

Managerial Auditing Journal Emerald Article: Usage of Internal Auditing by companies in the United States and select European countries Priscilla A. Burnaby, Mohammad Abdolmohammadi, Susan Hass, Gerrit

Managerial Auditing Journal Emerald Article: Usage of Internal Auditing by companies in the United States and select European countries Priscilla A. Burnaby, Mohammad Abdolmohammadi, Susan Hass, Gerrit

Continuing Professional Development (CPD) Requirements for New Zealand Licensed Auditors

Requirements for New Zealand Licensed Auditors") Policy and guidance Continuing Professional Development (CPD) Requirements for New Zealand Licensed Auditors (Effective 1 July 2016) CONTENTS 1 CPD Policy for New Zealand licensed auditors... 3 1.1 Introduction...

Policy and guidance Continuing Professional Development (CPD) Requirements for New Zealand Licensed Auditors (Effective 1 July 2016) CONTENTS 1 CPD Policy for New Zealand licensed auditors... 3 1.1 Introduction...

Report. Quality Assessment of Internal Audit at <Organisation> Draft Report / Final Report

Report Quality Assessment of Internal Audit at Draft Report / Final Report Quality Self-Assessment by Independent Validation by Table of Contents 1.

Report Quality Assessment of Internal Audit at Draft Report / Final Report Quality Self-Assessment by Independent Validation by Table of Contents 1.

The Future of Internal Auditing:

Internal Audit The Future of Internal Auditing: Changing Internal Audit s Value Proposition October 12, 2010 Istanbul, Turkey Presented by: Naman Parekh Partner, Agenda Background of the 2012 Study Key

Internal Audit The Future of Internal Auditing: Changing Internal Audit s Value Proposition October 12, 2010 Istanbul, Turkey Presented by: Naman Parekh Partner, Agenda Background of the 2012 Study Key

Mobility of researchers

Mobility of researchers Results from the MORE2 study KoWi Annual Conference Berlin 18 June 2015 Miriam Van Hoed, IDEA Consult, Belgium MORE2 Continued data collection and analysis concerning mobility patterns

Mobility of researchers Results from the MORE2 study KoWi Annual Conference Berlin 18 June 2015 Miriam Van Hoed, IDEA Consult, Belgium MORE2 Continued data collection and analysis concerning mobility patterns

Mr. Paul Druckman Chief Executive Officer, International Integrated Reporting Council

Philip D. Tarling, CIA, CRMA, CMIIA Global Chairman of the Board The Institute of Internal Auditors 247 Maitland Avenue Altamonte Springs, FL 32701 July 12, 2013 Professor Mervyn King Chairman, International

Philip D. Tarling, CIA, CRMA, CMIIA Global Chairman of the Board The Institute of Internal Auditors 247 Maitland Avenue Altamonte Springs, FL 32701 July 12, 2013 Professor Mervyn King Chairman, International

MEHNATY CAREER SERVICE STUDENTS GUIDE

MEHNATY CAREER SERVICE STUDENTS GUIDE Given below are three important steps for your successful job search. 1. Create a CV and Cover Letter 2. Setup email alerts 3. Apply to jobs regularly on your career

MEHNATY CAREER SERVICE STUDENTS GUIDE Given below are three important steps for your successful job search. 1. Create a CV and Cover Letter 2. Setup email alerts 3. Apply to jobs regularly on your career

Karlstad Business School

Karlstad Business School Paper On Conceptual framework: objective and Qualitative characteristics Presented to Berndt Andersson Dept. of Business Administration Prepared By: Mohammed Toufiq Rizwan 830105

Karlstad Business School Paper On Conceptual framework: objective and Qualitative characteristics Presented to Berndt Andersson Dept. of Business Administration Prepared By: Mohammed Toufiq Rizwan 830105

Advisory Services Governance, Risk & Compliance

Advisory Services Governance, Risk & Compliance Caribbean Association of Audit Committee Members Inc. 2010 Conference Caretakers of Integrity and Accountability: The Role of Internal Audit in Corporate

Advisory Services Governance, Risk & Compliance Caribbean Association of Audit Committee Members Inc. 2010 Conference Caretakers of Integrity and Accountability: The Role of Internal Audit in Corporate

Leading the Global. Next Decade Doing More with Less The Lean Internal Audit Model. Larry Rieger

Leading the Global Profession into the Next Decade Doing More with Less The Lean Internal Audit Model Larry Rieger 1 Agenda How chief audit executives and internal audit functions remain relevant Market

Leading the Global Profession into the Next Decade Doing More with Less The Lean Internal Audit Model Larry Rieger 1 Agenda How chief audit executives and internal audit functions remain relevant Market

2014 Global Council. Dubai, UAE 6-9 March 2014 DAY 2. globaliia.org

2014 Global Council Dubai, UAE 6-9 March 2014 DAY 2 Opening Remarks Paul J. Sobel, Chairman of the Board Agenda - Tuesday Opening Remarks P. Sobel Expanding the Umbrella of the IIA D. Beran Tuesday Discussion

2014 Global Council Dubai, UAE 6-9 March 2014 DAY 2 Opening Remarks Paul J. Sobel, Chairman of the Board Agenda - Tuesday Opening Remarks P. Sobel Expanding the Umbrella of the IIA D. Beran Tuesday Discussion

SEMINAR FOR SENIOR BANK SUPERVISORS

SEMINAR FOR SENIOR BANK SUPERVISORS World Bank/IMF/Federal Reserve Risk Governance & the Role of the Board Progression Through International Standards Laura Ard (Lard@worldbank.org) Lead Financial Sector

SEMINAR FOR SENIOR BANK SUPERVISORS World Bank/IMF/Federal Reserve Risk Governance & the Role of the Board Progression Through International Standards Laura Ard (Lard@worldbank.org) Lead Financial Sector

WCO Framework of Principles and Practices on Customs Professionalism

WCO Framework of Principles and Practices on Customs Professionalism WCO Framework of Principles and Practices on Customs Professionalism WCO Framework of Principles and Practices on Customs Professionalism

WCO Framework of Principles and Practices on Customs Professionalism WCO Framework of Principles and Practices on Customs Professionalism WCO Framework of Principles and Practices on Customs Professionalism

Patty Miller, CIA, QIAL, CPA, CRMA, CISA PKMiller Risk Consulting, LLC

Patty Miller, CIA, QIAL, CPA, CRMA, CISA PKMiller Risk Consulting, LLC pkmiller100@gmail.com Background Approach Results of Interviews/Survey Aggravating Factors for Political Pressure Implications for

Patty Miller, CIA, QIAL, CPA, CRMA, CISA PKMiller Risk Consulting, LLC pkmiller100@gmail.com Background Approach Results of Interviews/Survey Aggravating Factors for Political Pressure Implications for

Measuring the Performance of Internal Audit Function in Saudi Listed Companies: An Empirical Study

International Business Research; Vol. 7, No. 7; 2014 ISSN 1913-9004 E-ISSN 1913-9012 Published by Canadian Center of Science and Education Measuring the Performance of Internal Audit Function in Saudi

International Business Research; Vol. 7, No. 7; 2014 ISSN 1913-9004 E-ISSN 1913-9012 Published by Canadian Center of Science and Education Measuring the Performance of Internal Audit Function in Saudi

Audit Committee Member Roles and Responsibilities

PURPOSE OF THIS TOOL: The following information illustrates how the audit committee might be structured and assigns roles and responsibilities between the audit committee and finance committee. Not-for-profits

PURPOSE OF THIS TOOL: The following information illustrates how the audit committee might be structured and assigns roles and responsibilities between the audit committee and finance committee. Not-for-profits

Mr Philippe Maystadt Special Advisor European Commission Rue de la Loi 200 B-1049 Bruxelles. 30 September Dear Mr Maystadt

Mr Philippe Maystadt Special Advisor European Commission Rue de la Loi 200 B-1049 Bruxelles 30 September 2013 602/550 Dear Mr Maystadt Re: Draft Report Should IFRS Standards be more European? Mission to

Mr Philippe Maystadt Special Advisor European Commission Rue de la Loi 200 B-1049 Bruxelles 30 September 2013 602/550 Dear Mr Maystadt Re: Draft Report Should IFRS Standards be more European? Mission to

CESAER Mutual Learning Workshop. Euraxess. «The Human Resource Excellence Logo»

CESAER Mutual Learning Workshop Euraxess «The Human Resource Excellence Logo» ZOOM Facts & figures ZOOM Facts & figures ZOOM Facts & figures Louvain-la-Neuve, Bruxelles Woluwe, Mons, Tournai, Bruxelles

CESAER Mutual Learning Workshop Euraxess «The Human Resource Excellence Logo» ZOOM Facts & figures ZOOM Facts & figures ZOOM Facts & figures Louvain-la-Neuve, Bruxelles Woluwe, Mons, Tournai, Bruxelles

JOB DESCRIPTION. Manager Department: Finance Length of contract: Permanent. Role type: National Grade: 11

JOB DESCRIPTION Job title: Internal Audit Location: London Manager Department: Finance Length of contract: Permanent Role type: National Grade: 11 Travel involved: Up to 40% Child safeguarding level: TBC

JOB DESCRIPTION Job title: Internal Audit Location: London Manager Department: Finance Length of contract: Permanent Role type: National Grade: 11 Travel involved: Up to 40% Child safeguarding level: TBC

REPORT 2014/148 INTERNAL AUDIT DIVISION. Audit of the recruitment process at the Office of the High Commissioner for Human Rights

INTERNAL AUDIT DIVISION REPORT 2014/148 Audit of the recruitment process at the Office of the High Commissioner for Human Rights Overall results relating to the efficient and effective management of the

INTERNAL AUDIT DIVISION REPORT 2014/148 Audit of the recruitment process at the Office of the High Commissioner for Human Rights Overall results relating to the efficient and effective management of the

THREE-YEAR STRATEGIC PLAN UPDATE v1

THREE-YEAR STRATEGIC PLAN UPDATE v1 FY2017-FY2019 OUR STRATEGY To develop future professionals through relevant and accessible credentialing programs 100% Member Market Penetration To deliver member value

THREE-YEAR STRATEGIC PLAN UPDATE v1 FY2017-FY2019 OUR STRATEGY To develop future professionals through relevant and accessible credentialing programs 100% Member Market Penetration To deliver member value

The Continuing Competence Program for Psychologists Practicing in Nova Scotia. A Guide for Participants

The Continuing Competence Program for Psychologists Practicing in Nova Scotia A Guide for Participants Guide Revised April 2017 1 Table of Contents Introduction to the Continuing Competence Program.3 1.

The Continuing Competence Program for Psychologists Practicing in Nova Scotia A Guide for Participants Guide Revised April 2017 1 Table of Contents Introduction to the Continuing Competence Program.3 1.

National Action Plan on Energy Efficiency (NAPE)

") National Action Plan on Energy Efficiency (NAPE) CO2-Modernisation Program 5 th Meeting of the Concerted Action for the Energy Efficiency Directive March 24 th 2015, Riga Johannes Thomas Federal Ministry

National Action Plan on Energy Efficiency (NAPE) CO2-Modernisation Program 5 th Meeting of the Concerted Action for the Energy Efficiency Directive March 24 th 2015, Riga Johannes Thomas Federal Ministry

An analysis of the differences between Corporate Governance Structure in Germany and UK. Claudiu Ghiuzan. Claudiu Ghiuzan

An analysis of the differences between Corporate Governance Structure in Germany and UK 1 German Corporate Governance Structure German Corporate Governance principles and procedures are mainly established

An analysis of the differences between Corporate Governance Structure in Germany and UK 1 German Corporate Governance Structure German Corporate Governance principles and procedures are mainly established

UC Core Competency Model

UC Core Competency Model Developed and Endorsed by: UC Learning and Development Consortium Chief Human Resources Officers Date: May 2011 University of California Staff Employees Core Competencies Communication

UC Core Competency Model Developed and Endorsed by: UC Learning and Development Consortium Chief Human Resources Officers Date: May 2011 University of California Staff Employees Core Competencies Communication

Joining The IIA is an investment in your career and the profession.

Joining The IIA is an investment in your career and the profession. Connected. Knowledgeable. Confident. The IIA is the internal audit profession s global voice, recognized authority, acknowledged leader,

Joining The IIA is an investment in your career and the profession. Connected. Knowledgeable. Confident. The IIA is the internal audit profession s global voice, recognized authority, acknowledged leader,

Best Practices for Establishing a Cost-Effective Internal Audit Function. Article by Heidi Wier June 2016

Best Practices for Establishing a Cost-Effective Internal Audit Function Article by Heidi Wier June 2016 Best Practices for Establishing a COST-EFFECTIVE INTERNAL AUDIT FUNCTION BY HEIDI WIER The heightened

Best Practices for Establishing a Cost-Effective Internal Audit Function Article by Heidi Wier June 2016 Best Practices for Establishing a COST-EFFECTIVE INTERNAL AUDIT FUNCTION BY HEIDI WIER The heightened

DIRECTOR TRAINING AND QUALIFICATIONS: SAMPLE SELF-ASSESSMENT TOOL February 2015

DIRECTOR TRAINING AND QUALIFICATIONS: SAMPLE SELF-ASSESSMENT TOOL February 2015 DIRECTOR TRAINING AND QUALIFICATIONS SAMPLE SELF-ASSESSMENT TOOL INTRODUCTION The purpose of this tool is to help determine

DIRECTOR TRAINING AND QUALIFICATIONS: SAMPLE SELF-ASSESSMENT TOOL February 2015 DIRECTOR TRAINING AND QUALIFICATIONS SAMPLE SELF-ASSESSMENT TOOL INTRODUCTION The purpose of this tool is to help determine