Unconventional Resources Technology Creating Opportunities and Challenges. Alberta Government Workshop

|

|

|

- Nicholas Allison

- 6 years ago

- Views:

Transcription

1 Unconventional Resources Technology Creating Opportunities and Challenges Alberta Government Workshop

2 Alberta Government Technology Workshop Welcome The goal of this workshop is to provide an overview of key exploration and development technologies that have enabled the development of the unconventional resource potential in Alberta. In the last decade, E&P companies have recognized the unconventional resource potential including shale gas, tight gas, natural gas from coal and tight oil. The development and deployment of key technologies such as horizontal drilling, multi-stage fracturing and more recently fracture modeling and visualization have enabled an unparalleled growth of energy supply as these resources are developed. Understanding the various aspects of unconventional resources including geological setting, technologies, challenges and opportunities will form a foundation upon which analogues and opportunities in Mexico can be identified and a strong E&P strategy can be created

3 Canadian Society for Unconventional Resources CSUR is a not for profit industry association, formed in 2002, to support the responsible exploration and development of unconventional resources in Canada Mission To facilitate the factual and collaborative exchange of knowledge and challenges of unconventional resources among government, regulators, industry and public stakeholders for the exploration and production of the resource in an environmentally sensitive and economical manner

4 Canadian Society for Unconventional Resources Advisory Forward-Looking Information This presentation may contain information that constitutes forward-looking information or forward-looking statements (collectively forward-looking information ) provided by the association relating to the exploration and development of unconventional hydrocarbon resources in Canada, North America and possibly worldwide. The opinions expressed by the presenter should not necessarily be considered to be those of the association or its board of directors. Forward-looking information is based on current expectations, estimates and projections that involve a number of risks which could cause actual results to vary and in some instances to differ materially from those anticipated by the unconventional resource industry. The material risk factors include, but are not limited to: the risks of the oil and gas industry, such as operational risks in exploring for, developing and producing crude oil and natural gas, market demand; risks and uncertainties involving geology of oil and gas deposits; uncertainty related to securing sufficient egress and markets to meet hydrocarbon production; the uncertainty of reserves and resources estimates, reserves life and underlying reservoir risk; the uncertainty of estimates and projections relating to production, costs and expenses; potential delays or changes in plans with respect to exploration or development projects or capital expenditures by individual companies; fluctuations in oil and gas prices, health, safety and environmental risks; changes in general economic and business conditions and the possibility that government policies or laws may change or governmental approvals may be delayed or withheld. The foregoing list of risk factors is not exhaustive.

5 Short Course Outline Introduction Module 1 (0.5 hour) What are Unconventional Resources? Module 2 (0.5 hour) Drilling and Completion Technologies Module 3 ( 0.5 hour) North American Natural Gas Market and its Impact on Western Canada Oil and Gas Exploration and Development Module 4 The Shift to Tight Oil ( 0.5 hour) Questions and Discussion

6 Module 1 What Are Unconventional Resources Alberta Government Workshop

7 Outline Module 1 What are Unconventional Resources? Main Types of Unconventional Resources Differences between Unconventional and Conventional Reservoirs Trapping Mechanisms for Gas Storage Exploration and Development Strategies for Unconventional Gas Risk Profile What Risks Do Exploration Companies Face Resources versus Reserves

8 Outline - Module 1 Reservoir Porosity Permeability Resources Reserves Source Rock Glossary of Terms The rock that contains potentially economic amounts of natural gas The free space within the fine grained rock that can store natural gas The ability of the rock to pass fluids or gas through it. The higher the permeability number, the greater ease in which the fluid or gas that can flow through the rock over a fixed time period The amount of gas or oil that is thought to lie within a reservoir (lower degree of confidence) but does not account for how much is actually recoverable The amount of gas or oil that is actually proven to be recoverable from a reservoir (high degree of confidence) The rock material which contains organic material from which the natural gas is formed. In the case of shale gas and coal, the reservoir is also the source rock. In tight gas reservoirs, natural gas or oil is sourced elsewhere and migrated to the reservoir rock

9 What is an Unconventional Reservoir? CSUR Definition Unconventional Resources are very simply oil or gas that is produced from what industry would call Unconventional Reservoirs Often these reservoirs are of a lower quality and require enhanced technology types of completions to yield commercially successful wells Over time the technology to produce from these reservoirs will become mainstream and may not be considered unconventional Resource play types of exploration and development projects are usually successful through lower cost operational efficiency and economy of scale type operations Oil or gas reservoir is usually distributed over a large geographic area and will host local regions of improved productivity (sweet spots)

10 What are Unconventional Resources? Natural Resources Triangle Larger Reservoirs More Difficult to Develop Smaller Reservoirs Easier to Develop 1000 md High Quality 100 md Gas Shales Tight Gas Tight Oil Medium Quality Lower Quality Coalbed Methane 1 md 0.1 md Gas Hydrates md Increased Cost to Develop md Increased Technology Requirements modified from Schmezl, 2009

11 Differences Between Conventional and Unconventional Reservoirs Conventional Reservoirs Storage tank Gas or Oil is generated elsewhere (source rock) and then migrates to the potential reservoir Need a trap for the gas or oil accumulation: structural, stratigraphic Usually constrained geographically by trap boundaries Unconventional Reservoirs Can be both source and reservoir as in the case of shale gas or CBM Gas or oil is generated in situ, (some migration) Do not necessarily need a trap but generally need a seal Gas and oil is held in reservoir by either pressure or low permeability Usually laterally pervasive with local sweet spots

12 Differences Between Conventional and Unconventional Reservoirs Conventional vs Continuous or Unconventional Type Accumulations from Midnight Oil and Gas, 2009

13 Unconventional Resource Risk Profiles Conventional Reservoirs Unconventional Reservoirs Engineering Geoscience Geoscience Engineering Much of the risk is concentrated in the front end geoscience exploration and the ability to locate natural gas or oil reservoirs of economic size Risk is concentrated in the ability to produce economic volumes from laterally pervasive deposits of natural gas and oil where the risk of finding hydrocarbons is low

14 Types of Unconventional Reservoirs Tight Gas and Oil Sands and Carbonates Natural gas or oil has migrated into the microporosity of the rock matrix Commonly found in basin centered gas deposits Natural Gas from Coal (Coalbed Methane) Host rock is both source and reservoir for natural gas Reservoir rock is highly compressible and subject to changes in permeability Shale Gas Very high natural gas resource base per volume of reservoir rock due to high micro-porosity Requires extensive fracture stimulation

15 Types of Unconventional Reservoirs Unconventional Reservoirs Tight Gas or Oil Sandstone Conventional Reservoirs Conventional Oil or Gas Reservoirs Shale Tight Oil in Limestone Natural Gas from Coal Extremely Tight Very Tight Tight Low Moderate High Permeability (md) Poor Quality of Reservoir Good Granite Sidewalk Cement Volcanic Pumice Note: Natural Gas from Coal reservoirs are classified as unconventional due to type of gas storage modified from US DOE

16 Types of Unconventional Gas Reservoirs Unconventional Reservoir Continuum Conventional Gas Reservoirs Tight Gas and Oil Reservoirs Hybrid Reservoirs Shale Gas Shale Oil Coalbed Methane Reservoirs The shift from conventional to unconventional reservoirs reflects a change in grain size from higher permeability, coarser grained rocks towards very fine grained rocks with low permeability Reservoir variability both vertical and geographically can lead to the development of sweet spots of higher permeability in the finer grained reservoir rocks Core photos courtesy of Canadian Discovery

17 Types of Unconventional Gas Reservoirs Organic-rich Black Shale High TOC & high adsorbed gas Low matrix Sw High matrix Sg Gas or Oil stored as free & adsorbed Silt - Laminated Shale or Hybrid Gas or Oil stored in shale and silt Low to moderate TOC Higher permeabilities in silty layers Highly Fractured Shale Low TOC & low adsorbed gas High matrix Sw Low matrix Sg Gas stored in fractures Shale is the source rock Mature Source Rock From Hall, 2008

18 Key Aspects of Unconventional Resource Play Development Two Major Resource Play Types in Canada Deep HIGH RISK Shallow LOWER RISK Horizontal BIG PRIZE Co-Mingled SMALLER PRIZE High costs due to horizontal drilling and multi-stage fracing Well costs $6-10 MM High productivity wells with sharp decline rates Initial well production >2 MMcf/d High entry costs Lower costs due to depth and drilling and fracing equipment such as coiled tubing drilling and use of nitrogen with proppant fracing technology Well costs $250,000 to D&C and Stimulate Low productivity wells with flatter decline rates Economic wells due to co-mingled zones Initial Well production mcf/d Lower entry costs

19 Key Aspects of Unconventional Resource Play Development Each basin is unique requiring capital intensive exploration and experimentation to optimize productive sweet spots as well as stimulation and production methodologies Creates a two tier approach by industry players: Early Explorers - large capital expenditures required - advantage in land acquisition position and cost - higher risk due to uncertainty of the science - generally associated with resource play development Early Adopters - apply learnings of the early explorers to optimize capital costs and completion techniques - do not have the opportunity to acquire prime land position other than perhaps by serendipity - lower risk of technology but higher risk associated with resource base size Most shale and tight sandstone wells have very high decline rates need to plan for a large acreage position to allow for continued drilling to offset declines

20 Key Aspects of Resource Play Development UNCONVENTIONAL RESOURCE PLAY STRATEGY AN INTEGRATED APPROACH TO WELL DESIGN Completion Strategy Reservoir Characterization Unlocking the Resource Play Wellbore Architecture from E. Schmelzel, 2008

21 Key Aspects of Resource Play Development The Key Questions Reservoir Characterization Reservoir modeling Sweet Spot identification Wellbore placement THE GOAL MAXIMIZED RESERVOIR EXPOSURE Wellbore completion from E. Schmelzel, 2008

22 Resources versus Reserves Primary goals of initial exploration programs for unconventional plays are: Define rock properties of the target zones to determine how much hydrocarbon may be present Define reservoir properties to guide in the development of the fracture stimulation program Undertake initial stimulation testing of primary zones to quantify initial productivity Conduct extended reservoir testing to determine decline rates and changes in reservoir pressure Reserves Resources Exploration Activities Initial Drilling OGIP Initial Well Testing IP Initial Well Stimulation and Testing Extended Well Testing Multiple Wells And Reproducibility Of Results P10 P50 P90 Probability of Success

23 Completion and Stimulation Techniques Horizontal Wellbore and Multi-Lateral Wellbore Completions Commonly multi-stage fracture stimulations are conducted to optimize the amount of fracture energy entering into the wellbore The horizontal leg is broken into stages where fracture stimulation for each stage is isolated from the rest of the wellbore Fracture design for each stage within the horizontal leg is dependent on borehole logging indicators of gas concentration as well as natural fracture density

24 How Do We Measure Success in Reservoir Stimulation Run horizontal well video

25 How Do We Measure Success in Reservoir Stimulation Run vertical stimulation video

26 Completion and Stimulation Techniques From Fairborne Energy, 2009

27 How Do We Measure Success in Reservoir Stimulation Micro-Seismic to Determine Effectiveness of Stimulation Measures micro seismic events related to the propagation of fractures within the reservoir Requires one or more observation wells to allow proper mapping of location geographically and vertically of microseismic events Can be run independently or as permanent seismic arrays in field to be developed Provides a 3D image of fracture propagation that can be measured in real time during the fracture stages Allows fracture propagation trends to be identified and adjusted for additional stages so fractures can be contained within zone Identifies areas of poor fracture generation or geological barriers to effective stimulation

28 How Do We Measure Success in Reservoir Stimulation Run microseismic video

29 How Do We Measure Success in Reservoir Stimulation Micro-seismic monitoring of fracture events for each staged stimulation allows the lateral and vertical envelope of the fracture stimulated rock to be determined Dots represent individual micro-seismic events that occur during the fracturing of the reservoir Track of the horizontal wellbore Courtesy of Nexen, 2011

Multi-stage fracture stimulations are costly and should be undertaken only after reservoir properties have been tested from vertical wellbores and core data Courtesy Fairborne")

30 Completion and Stimulation Techniques Multi-stage fracture stimulations are labor and equipment intensive that requires planning for wellsite activities as well as supply of frac materials (sand and water primarily) Multi-stage fracture stimulations are costly and should be undertaken only after reservoir properties have been tested from vertical wellbores and core data Courtesy Fairborne Energy, 2009 Courtesy Fairborne Energy, 2009

31 Manufacturing Style Ideology In order to be economically successful most unconventional resource play projects require the adoption of a manufacturing style of operations. This is to ensure that the project achieves: Optimization of Reservoir Production Employs Economies of Scale and Economic Benefits Continuous Improvement of Productivity while at the same time reduction in production costs Sufficient land base to support ongoing drilling and development plans that account for steep decline of initial production rates Service sector alliances that will allow continuous operations and economies of scale

32 Optimization of Reservoir Production Understanding the Reservoir is Key to Optimizing Production and Reserve Recovery This is achieved through continuous improvements and experimentation in drilling, completion and production techniques From Southwestern Energy, 2009

33 Optimization of Reservoir Production Resource play development is a statistical play Recognition that within the oil or gas field there are going to be both high volume and low volume producers Rely on statistical average to achieve project economic return on investment Understanding reservoir properties will decrease the risk of completing low volume producing wells From Southwestern Energy, 2009

34 Key Aspects of Unconventional Play Development Unconventional Resource Play Strategy is Critical to Success Understanding the Play Reservoir Characterization Resource Assessment Formation Properties & Analogs Address The Resource Play Challenges Which technologies, services or products are most appropriate Operational Risk / Cost Assessment Field Trials / Pilot Build in Efficiency Scale of operations is usually large Remote areas may add significant cost Bundling of Services, Concurrent / Continuous Operations

35 Stages of Exploration and Development Stage 1: Identification of UCG Resource Stage 2: Early Evaluation Drilling Time (years) Preliminary geological assessment to determine potential for hydrocarbons Stage 3: Pilot Project Drilling Pace of development is largely dependent on technical success and market conditions Exploration Tasks Vertical drilling to obtain core samples for reservoir properties along with estimation of resource potential and geographic limits of potential field Early horizontal drilling to evaluate well performance with varying hydraulic fracturing technologies along with continued reservoir testing to determine engineering properties Stage 4: Pilot Production Testing Advanced hydraulic fracturing testing and improvements of productivity with reduced expenditure Stage 5: Commercial Development Project Reclamation

36 Economies of Scale and Economic Benefits Resource Play Success is achieved through the adoption of a Manufacturing Style approach to commercial development Cost savings can be realized through a number of business models that achieve economies of scale, bundling of services, continuous operations, service sector alliances and in some case vertical integration Fracture stimulation costs now account for more than half of the total well costs from E. Schmelzel, 2008

37 Economies of Scale and Economic Benefits Key Elements of Manufacturing Ideology Minimize completion time Mitigate operational risk Define synergies and economies of scale Maximize EUR - completion methods which are adaptable to future recompletion capabilities reserves Minimize Logistics Costs: Re-using water from flowback and production, innovative fluid handling & storage Minimize Surface Impact & Costs: Pad drilling and completions, multi-lateral capability

38 Module 21 Drilling What Are andunconventional Completion Technologies Resources Alberta Government Workshop

39 Outline Module 2 Accessing the Reservoir - Why and How Drilling and Completion Technologies Coiled Tubing Drilling Horizontal Drilling Multi-Lateral Drilling Completion and Stimulation Techniques Vertical Fracture Stimulations and Co-Mingling Multi-Stage Fracture Stimulation Techniques Micro-Seismic Monitoring to Determine Effectiveness of Stimulation Gas Factory Ideology Optimization of Reservoir Production Key Aspects of Unconventional Gas Development Stages of Exploration and Development Economies of Scale and Economic Benefits

40 Outline Module 2 EUR OGIP IP Hydraulic Fracturing Multi-Stage Fracturing Microseismic Glossary of Terms Estimated Ultimate Recoverable reserves from a well Original Gas in Place before production (usually quoted in billions or trillions of cubic feet) Initial production rate of a gas well often much higher than the sustained production rate usually quoted as millions or thousands of cubic feet per day (Mmcf/d or mcf/d) Commonly referred to as fracing, this is the process where the reservoir rock is cracked using pressure and fluids to create a series of fractures in the rock through which the natural gas will flow to the wellbore The process of undertaking multiple fracture stimulations in the reservoir section where selected parts of the reservoir are isolated and fractured separately The methods by which fracturing of the reservoir can be observed by geophysical methods to determine where the fractures occurred within the reservoir

41 Accessing the Reservoir The fundamental purpose of drilling a oil or gas wellbore is to intersect the maximum amount of pay zone within the reservoir and optimize the productivity from the wellbore In unconventional reservoirs the ability of the hydrocarbons to flow to the well is hindered due to lower permeability To counter this lower productivity, drilling and stimulation techniques are used to maximize the amount of the reservoir exposed to the wellbore Techniques include: Vertical well multi-zone stimulation Horizontal wells Multistage fracturing Essentially all unconventional gas reservoirs require some form of improved access either through drilling or hydraulic fracturing

42 Drilling and Completion Technologies Different types of drilling equipment and methodology are available dependent on reservoir depth, thickness and expected flow properties Some choices include: Coiled Tubing Drilling and multi-zone completions Horizontal Drilling with mono reservoir completion Multi-Lateral Drilling with multiple completions

Multiple drill string assemblies that reduce tripping time Geosteering in real time in horizontal and multilateral wells Automation")

43 Drilling and Completion Technologies Drilling Efficiencies and Savings have been achieved through: Speed of drilling using new bit technology (PDC bits achieve penetration rates of up to 80 m/hr) Multiple drill string assemblies that reduce tripping time Geosteering in real time in horizontal and multilateral wells Automation of rig floor equipment eliminating additional manpower Fit for purpose rigs that can move on site without teardown Eg. Range Resources operates two fit for purpose drilling rigs that can move to the next well location on a common pad with over 3000 m of drill pipe stacked on the derrick rig move reduced from days to hours From Range Resources, 2010

44 Drilling and Completion Technologies Geosteering of horizontal wells in real time allows optimal reservoir penetration Multiple well orientations either vertical or horizontal from single surface well pads minimizes footprint courtesy Halliburton

45 Drilling and Completion Technologies Drilling of horizontal wells with the horizontal legs being up to 3500 m in length Multi stage fracture stimulations using slick water and sand to essentially create reservoir in rock that would not have been considered reservoir quality previously Zonal isolation packer systems in horizontal and multi-lateral wells allow for selective stimulation as well as production courtesy Halliburton

46 Drilling and Completion Technologies Horizontal Drilling/ Multi-Lateral Drilling Side Laterals Main Lateral The Pinnate Drainage Pattern

47 Completion and Stimulation Techniques Fracture stimulations are required for most unconventional resource plays due to low permeabilities of the reservoirs Type of fracture stimulation used is defined by: Depth and number of reservoirs to be stimulated Reservoir quality Type of wellbore (vertical versus horizontal) Fluid sensitivity Geomechanical properties of the reservoir Availability of equipment and materials Economic assessment of wellbore deliverability

48 Completion and Stimulation Techniques Fracture Stimulation Parameters The main purpose of fracture stimulation is to create open pathways for fluid flow within the reservoir either by creation of fractures or intersection of existing fracture systems Ideally the reservoir rock should be brittle so that it fractures easily Mineral content of the shale component will determine fracability of reservoir ideally a silica rich shale is preferred Sheared and slickensided fractures Open vertical fractures From Hall, 2008

49 Completion and Stimulation Techniques Typical coil tubing unit used for multizone fracture stimulation Completion techniques as well as size and amount of equipment will be dependent on the depth of the reservoir, size of fracture stimulation and number of fracs designed for the well Courtesy of Halliburton, 2009

50 Module 13 Unconventional What Are Unconventional Resource Development Resources and Risk Alberta Government Workshop

51 Outline Module 3 Risk variables that may impact success Well productivity and decline rates Reservoir heterogeneity Achievement of Economies of Scale Role of government and regulatory framework Attraction of Foreign investment and Technology

52 Outline Module 3 Glossary of Terms OGIP Marketable Resources IP F&D Costs Royalties Original Gas in Place before production (usually quoted in billions or trillions of cubic feet) The estimated amount of natural gas that can be recovered from the OGIP values using existing technology Initial production rate of an oil or gas well often much higher than the sustained production rate usually quoted as millions or thousands of cubic feet per day (Mmcf/d or mcf/d) or BOE/day The finding and development costs that a company spends to develop the oil or natural gas well or field The amount of $$ that companies pay to the owner of the oil and gas resources (usually the government)

53 Unconventional Resource Development and Risk

54 Unconventional Resource Development and Risk

55 Unconventional Resource Development and Risk Current Dry Production Levels Pushing All Time Highs Hurricanes Gustav and Ike Hurricane Katrina Emergence of Giant Shale Plays Barnett Woodford Fayetteville Haynesville Marcellus Eagle Ford Advanced Drilling and Well Completion Technology Horizontal Well Drilling Higher Prices Source: BENTEK Pipeline Flow Data From --- Daily Supply and Demand Report

56 Unconventional Resource Development and Risk Major pipeline corridors in United States are being built to eliminate local bottlenecking in delivery of natural gas to the northeast market ANTRIM MARCELLUS NEW ALBANY BARNETT WOODFORD HAYNESVILLE FAYETTEVILLE

57 Impact of Oversupply of Natural Gas in the North American Modified from Government of Nebraska website, 2011

58 Projected Supplies of Natural Gas in United States Trillion cubic feet/year modified from EIA, 2012

59 Unconventional Resource Development and Risk Unconventional resources, particularly natural gas developments are capital intensive with return on investment over a much longer time frame Hydraulic fracturing now account for as much as 60% of total well costs The science part of the exploration projects can take as much as 2 to 3 years prior to commercial development decisions being made and can lead to many millions of $$ of sunk costs with little or no revenue generated Companies that are active in resource play development must have access to long term capital in the hundreds of million of $$ to be able to develop the project and realize a return on investment

60 Life Cycle of an Unconventional Natural Gas Resource Development The slower rate at which the EUR is captured in unconventional reservoirs extends the economic break- even point, but the long-term ultimate recovery due to the size of the OGIP remains attractive compared to conventional reservoirs To achieve economic production of unconventional resources you need: high commodity prices; preferably existing infrastructure, new and existing technologies, availability of equipment and materials in sufficient quantity; and a competitive / incented environment in which to work < $ million annual cash flow > Investor Cash Flow Tax Paid Production Cumulative Cash Flow Operating Expenditure 0 Capital Expenditure Each bar = 1 year From Shell E&P Technology, 2009

61 Unconventional Resource Development and Risk The Treadmill of Unconventional Resource Development Shale gas and tight gas reservoirs typically have steep decline curves in the early months of production In order for companies to grow and maintain production volumes they must continue to drill to offset the declines in single well production rates Successful resource play companies will have large land holdings with an inventory of well locations from Encana, 2011

62 Unconventional Resource Development and Risk Resource play development is statistical in terms of productivity The reservoirs will tend to be heterogenetic with variable production rates and EUR Within the laterally pervasive large reservoir area, there will be areas of enhanced production (sweet spots) that will balance the areas of lower productivity In order to achieve the statistical balance for economic success, the projects must be able to have multiple wells drilled hence the requirement for large tracts of oil and gas tenure held by individual companies

63 Unconventional Resource Development and Risk Challenge: Improve overall productivity and/or economics for the entire play not just the sweet spot high productivity areas Recognition that within the gas field there are going to be both high volume and low volume producers - Barnett shale completions Rely on statistical average to achieve project economic return on investment Understanding reservoir properties will decrease the risk of completing low volume producing wells Improved productivity will allow marginal wells to achieve economic thresholds Modified from Southwestern Energy, 2009

64 Unconventional Resource Development and Risk Well Cost Evolution ($C) Production Evolution Deep Basin (vertical wells) Montney - Per Interval $MM $MM/Frac Horn River MMcfe/d F NGC Well costs $MM F F Horn River Per Interval $MM/Frac F F Montney MMcfe/d * F Modified from Encana, 2010

65 Unconventional Resource Development and Risk Role of Government and Regulatory Framework Government must establish a regulatory framework that recognizes the exploration risk and the time to develop unconventional resource projects Royalty structure must recognize the extensive front end capital costs relative to the return of capital over the time frame of the entire project The application of technology will be critical to the success of unconventional resource development and government must ensure that these technologies can be deployed easily There may be a requirement for incentives to attract investment into new emerging play regions such as royalty holidays or tax credits

66 Unconventional Resource Development and Risk Attraction of Foreign Capital Large exploration companies will look at new exploration plays from a perspective of a global hydrocarbon portfolio they have choices as to where they will invest their capital Operatorship is a critical aspect of any new venture, particularly in regions where NOC s are involved Production sharing agreements require an understanding of the risk/reward that the projects encompass Foreign investment will also be highly dependent on other variables beyond the resource play opportunity such as: Availability of equipment, materials and manpower Local stakeholder relations Infrastructure and transportation costs/burdens Government and regulatory stability (looking for established regulatory environment where the investing companies understand all of the rule sna regulations prior to investing

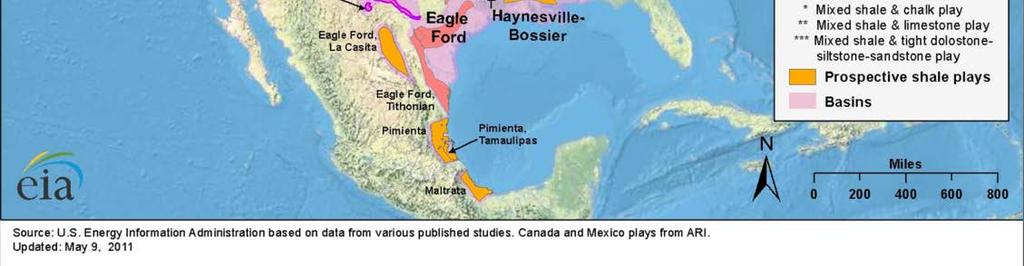

67 Emerging Opportunities for Unconventional Resources in Mexico There are a number of unconventional resource basins in Mexico that have significant potential but require: Grass roots exploration to identify the scale of the opportunities and at the same time some element of risk reduction to attract foreign investment Foreign Investment to provide the capital necessary for development Government incentives/encouragement for foreign investment into the new opportunities Strong commitment by Mexico for the attraction and deployment of technology

68 Emerging Opportunities for Unconventional Resources in Mexico

69 Emerging Opportunities for Unconventional Resources in Mexico

70 Emerging Opportunities for Unconventional Resources in Mexico

71 Summary and Conclusions Unconventional resource development is a technology play The application of horizontal drilling coupled with multi-stage hydraulic fracture stimulation has been the technological breakthrough that has unlocked most resource play opportunities Resource play development is capital intensive with return on investment spread out over a longer time period that perhaps conventional resource targets Longer investment time but the prize is bigger Large amounts of capital suggest that only the larger oil and gas companies have the financial capability to develop unconventional resource fields with any high potential for economic success Attraction of foreign capital may be critical for the successful development of the unconventional resource potential in Mexico

72 Module 4 Tight Oil Unconventional But Different Alberta Government Workshop

73 Tight Oil Opportunities and Challenges What is Tight Oil? The Shift to Tight Oil Economic Balance Relationship and Sensitivity to World Oil Prices Critical Elements for Success Emerging Opportunities in Southern Alberta What does it mean to the business owner and stakeholder? January 27, 2012

74 Tight Oil Opportunities and Challenges Unconventional Reservoirs Conventional Reservoirs Tight Oil in Sandstone Conventional Sandstone Oil Reservoirs Shale Oil Oil in Limestone Conventional Limestone Oil Reservoirs Extremely Tight Very Tight Tight Low Moderate High Permeability (md) Poor Quality of Reservoir Good Granite Sidewalk Cement Volcanic Pumice modified from US DOE January 27, 2012

75 Tight Oil Opportunities and Challenges Modified from Canadian Discovery, 2011 and EOG Investor Presentation January 27, 2012

76 What is Driving the Industry Towards Tight Oil Strong Commodity Prices Creates Foundation for Technology Development and Deployment into Unconventional Gas Resource Plays Higher Demand Cycle Supply Glut - Lower Demand Cycle Modified from Government of Nebraska website, 2011 January 27, 2012

77 Tight Oil Opportunities and Challenges Modified from Macquarie Research, 2010 January 27, 2012

78 Tight Oil Opportunities and Challenges Technological Development Driven by Price $5 - $20 / bb/vertical wells Reservoir Quality Higher Quality Reservoirs Discreet Pool Size $20 - $60 / bbl Vertical wells with Fracture Stimulation $20 - $60 / bbl Horizontal wells $60 - $120 / bbl Horizontal wells with Staged Fracture Stimulation $120 / bbl+ Vertical Vertical with Frac Horizontal Key technologies of horizontal drilling and multi-stage fracturing Horizontal with Multi-Stage Frac Low Quality Reservoir Larger Geographic Distribution of Resources modified from Penn West, 2011 January 27, 2012

79 Tight Oil Opportunities and Challenges Modified from Macquarie Research, 2010 January 27, 2012

80 Tight Oil Opportunities and Challenges Drilling for Tight Oil is not a License to Print Money Challenges still exist and not all regions within a resource play are going to achieve economic success Current oil prices are driving the exploration activity but a sustained high price deck will be necessary for ongoing development Significant growth of tight oil opportunities in United States may create a number of issues: Pipeline infrastructure may create backlog for oil transport, particularly if the Niobrara potential continues to grow Downward pressure on West Texas pricing due to oversupply in Cushing Availability of equipment and materials for fracture stimulations Continued downward pressure on natural gas prices due to additional gas production from oil or liquids rich resource plays January 27, 2012

81 Tight Oil Opportunities and Challenges Critical Elements for Success Most tight oil prospects that are current exploration and development targets are in existing or the margins of field that have a large volume of oil still within the reservoir Economics of development need to take into account full cycle including land costs Evolving technology towards lower cost stimulations rather than more expensive frac fluids such as oil Need to be very aware of fracture propagation trends to ensure staying within zone and optimal reservoir stimulation Decline rates tend to be steep and the EUR for each well requires careful analysis based upon actual observed recovery factors January 27, 2012

82 Tight Oil Opportunities and Challenges from Petrobakken 2011 January 27, 2012

83 Tight Oil Opportunities in Southern Alberta The New Alberta Bakken Play The industry shift to more oilier prospects and the application of technology has created a new opportunity for hydrocarbon exploration in Southern Alberta Alberta Bakken This resource play consists of a number of tight hydrocarbon targets that contain light tight oil with minor gas accumulations Companies are looking to extend the prolific Bakken play in southern Saskatchewan into Alberta and Montana into a roughly north northwest trending play that extends from south of Vulcan down into into northern Montana The Alberta Bakken play is about 300 km long by about 80 km wide bounded on the west by subsurface faulting associated with the Rocky Mountains and to the east by a geological pressure boundary January 27, 2012

which is the")

84 Tight Oil Opportunities and Challenges The Alberta Bakken play consists of a number of oil bearing zones in the subsurface that are bounding the Exshaw Fm (Bakken equivalent in Sask) which is the source rock for the oil and gas Source BMO Capital Markets technical report, April, 2011 January 27, 2012

85 Tight Oil Opportunities and Challenges Companies have spent over $520 MM in the past 3-4 years establishing a land position both in Southern Alberta and Montana More than 60 wells have been drilled or licensed in this area with an estimated expenditure of over $250 MM A strong financial commitment by industry to conduct exploration Expect to see continued exploration and development where understanding the reservoir(s) will be critical in the early stages and then will potentially lead to commercial development Source BMO Capital Markets technical report, April, 2011 January 27, 2012

86 Tight Oil Opportunities and Challenges Early exploration tests designed to determine wellbore productivity and pressure responses Pace of development will be controlled by the results of these early test wells Argosy W4 Activity and types of equipment on site will be dependent on the types and volumes of hydrocarbons that are being recovered this is controlled to a large extent by the reservoir properties Crescent Point W4 Source BMO Capital Markets technical report, April, 2011 January 27, 2012

87 Tight Oil Opportunities and Challenges Wellbore production tends to improve over time as technologies are adapted and modified to reflect better understanding of reservoir properties Modified from Bowood Energy Inc. Investor Presentation, 2011 January 27, 2012

88 The Final Comment So what have we learned this morning? One thing for sure --- INFORMATION OVERLOAD But here are some things to think about: Canada and Alberta has enough natural gas to supply our needs as well as our export levels for over 100 years This abundance of natural gas in North America will continue to keep prices at the lower level for the near future due to oversupply into the market Companies exploring and producing natural gas in Western Canada will need to become the low cost operator if they are to compete in the North American market January 27, 2012

89 The Final Comment Economies of scale, manufacturing ideology and partnerships will be critical to achieve this goal Development of unconventional resources is a technology play. Industry continues to make advances in technology development and deployment that allows improvement in productivity and EUR as well as opening up opportunities in new basins (ie. Alberta Bakken) Companies will continue to look towards more oily type plays where the return on investment is more attractive in the short term Early drilling results for the Alberta Bakken look promising but it is still in the early days and widespread commercial success has yet to be proven January 27, 2012

90 Thank You for your Attention Questions????? Alberta Government Workshop

P R E PA R E D B Y C O L I N J O R D A N R E V I E W E D B Y G E O F F B A R K E R A N D B R U C E G U N N

Evaluating Australian unconventional gas use and misuse of north American analogues P R E PA R E D B Y C O L I N J O R D A N R E V I E W E D B Y G E O F F B A R K E R A N D B R U C E G U N N RISC ADVISORY

Evaluating Australian unconventional gas use and misuse of north American analogues P R E PA R E D B Y C O L I N J O R D A N R E V I E W E D B Y G E O F F B A R K E R A N D B R U C E G U N N RISC ADVISORY

Shale Plays. Baker Hughes. Adam Anderson, VP, US Land Operations Completions Fred Toney, VP, Pressure Pumping Services.

Shale Plays Baker Hughes Houston, Texas Adam Anderson, VP, US Land Operations Completions Fred Toney, VP, Pressure Pumping Services 2010 Baker Hughes Incorporated. All Rights Reserved. Forward Looking

Shale Plays Baker Hughes Houston, Texas Adam Anderson, VP, US Land Operations Completions Fred Toney, VP, Pressure Pumping Services 2010 Baker Hughes Incorporated. All Rights Reserved. Forward Looking

Natural Gas Abundance: The Development of Shale Resource in North America

Natural Gas Abundance: The Development of Shale Resource in North America EBA Brown Bag Luncheon Bracewell & Giuliani Washington, D.C. February 6, 2013 Bruce B. Henning Vice President, Energy Regulatory

Natural Gas Abundance: The Development of Shale Resource in North America EBA Brown Bag Luncheon Bracewell & Giuliani Washington, D.C. February 6, 2013 Bruce B. Henning Vice President, Energy Regulatory

RESOURCE PLAYS: UNDEVELOPED RESERVES THE LEARNING CURVE

RESOURCE PLAYS: UNDEVELOPED RESERVES THE LEARNING CURVE Tennessee Oil and Gas Association Nashville, TN May 12, 2011 D. Randall Wright (615) 370 0755 randy@wrightandcompany.com wrightandcompany.com Our

RESOURCE PLAYS: UNDEVELOPED RESERVES THE LEARNING CURVE Tennessee Oil and Gas Association Nashville, TN May 12, 2011 D. Randall Wright (615) 370 0755 randy@wrightandcompany.com wrightandcompany.com Our

Enabling Unconventional Resources

Enabling Unconventional Resources 8 th U.S. - China Oil and Gas Industry Forum San Francisco, California U.S.A. September 9-11, 2007 ROLE OF UNCONVENTIONAL Increasing contribution by unconventional resources

Enabling Unconventional Resources 8 th U.S. - China Oil and Gas Industry Forum San Francisco, California U.S.A. September 9-11, 2007 ROLE OF UNCONVENTIONAL Increasing contribution by unconventional resources

Conventional and Unconventional Oil and Gas

Conventional and Unconventional Oil and Gas What is changing in the world? Iain Bartholomew, Subsurface Director Siccar Point Energy Discussion outline 1. Conventional oil and gas - E&P life-cycle - How

Conventional and Unconventional Oil and Gas What is changing in the world? Iain Bartholomew, Subsurface Director Siccar Point Energy Discussion outline 1. Conventional oil and gas - E&P life-cycle - How

Shale Gas - From the Source Rock to the Market: An Uneven pathway. Tristan Euzen

Shale Gas - From the Source Rock to the Market: An Uneven pathway Tristan Euzen Shale Gas Definition Seal Conventional Oil & Gas Tight Gas Source Rock Reservoir (Shale Gas) Modified from Williams 2013

Shale Gas - From the Source Rock to the Market: An Uneven pathway Tristan Euzen Shale Gas Definition Seal Conventional Oil & Gas Tight Gas Source Rock Reservoir (Shale Gas) Modified from Williams 2013

Gas Shales Drive the Unconventional Gas Revolution

Gas Shales Drive the Unconventional Gas Revolution Prepared By: Vello A. Kuuskraa, President ADVANCED RESOURCES INTERNATIONAL, INC. Arlington, VA Prepared for: Washington Energy Policy Conference The Unconventional

Gas Shales Drive the Unconventional Gas Revolution Prepared By: Vello A. Kuuskraa, President ADVANCED RESOURCES INTERNATIONAL, INC. Arlington, VA Prepared for: Washington Energy Policy Conference The Unconventional

EnerCom's London Oil & Gas Conference 16 June 2011 London, England Danny D. Simmons

Overview of Shale Plays EnerCom's London Oil & Gas Conference 16 June 2011 London, England Danny D. Simmons Daily Gas Production (BCFD) Barnett Shale Historical Gas Production Rig Count 6.0 300 5.0 Gas

Overview of Shale Plays EnerCom's London Oil & Gas Conference 16 June 2011 London, England Danny D. Simmons Daily Gas Production (BCFD) Barnett Shale Historical Gas Production Rig Count 6.0 300 5.0 Gas

GAIL s experience Shale Gas activities in US" 17th May 2013 Manas Das

GAIL s experience on Shale Gas activities in US" Manas Das 17 th May 2013 Outline About GAIL GAIL s Presence in USA Story of Shale Gas Revolution Cause & Effect Impact on Economy, Environment & Employment

GAIL s experience on Shale Gas activities in US" Manas Das 17 th May 2013 Outline About GAIL GAIL s Presence in USA Story of Shale Gas Revolution Cause & Effect Impact on Economy, Environment & Employment

Shale Projects Becoming Globally Important U.S. Shale Oil & Gas Experience Extrapolates Globally

Shale Projects Becoming Globally Important U.S. Shale Oil & Gas Experience Extrapolates Globally Global Shale Gas Estimated Reserves Shale Projects are Going Global Source: EIA Potential projects are developing

Shale Projects Becoming Globally Important U.S. Shale Oil & Gas Experience Extrapolates Globally Global Shale Gas Estimated Reserves Shale Projects are Going Global Source: EIA Potential projects are developing

Unconventional Gas Market Appraisal

Unconventional Gas Market Appraisal Chris Bryceland June 2013 Agenda Headline facts Fundamentals of unconventional gas Global resources Selected markets Economic impacts Supply chain opportunities Conclusions

Unconventional Gas Market Appraisal Chris Bryceland June 2013 Agenda Headline facts Fundamentals of unconventional gas Global resources Selected markets Economic impacts Supply chain opportunities Conclusions

Utica Point Pleasant Play - Range s View on a Key Appalachian Basin Unconventional Target & Plans for Future Development

Utica Point Pleasant Play - Range s View on a Key Appalachian Basin Unconventional Target & Plans for Future Development STRH 5 th Utica Shale Mini Conference November 14, 2013 Forward-Looking Statements

Utica Point Pleasant Play - Range s View on a Key Appalachian Basin Unconventional Target & Plans for Future Development STRH 5 th Utica Shale Mini Conference November 14, 2013 Forward-Looking Statements

Shale Gas - Transforming Natural Gas Flows and Opportunities. Doug Bloom President, Spectra Energy Transmission West October 18, 2011

Fort Nelson Gas Plant, British Columbia Shale Gas - Transforming Natural Gas Flows and Opportunities Doug Bloom President, Spectra Energy Transmission West October 18, 2011 Natural Gas Golden Age Natural

Fort Nelson Gas Plant, British Columbia Shale Gas - Transforming Natural Gas Flows and Opportunities Doug Bloom President, Spectra Energy Transmission West October 18, 2011 Natural Gas Golden Age Natural

The Impact of U.S. Shale Resources: A Global Perspective

The Impact of U.S. Shale Resources: A Global Perspective by Svetlana Ikonnikova Scott Tinker March 3, 2017 Outline Global Perspective U.S. Shale Resource Studies Implications Affordable Available Reliable

The Impact of U.S. Shale Resources: A Global Perspective by Svetlana Ikonnikova Scott Tinker March 3, 2017 Outline Global Perspective U.S. Shale Resource Studies Implications Affordable Available Reliable

UNCONVENTIONAL GAS RESOURCES

UNCONVENTIONAL GAS RESOURCES Exploration, Development and Planning Support Services RPS is an international consultancy providing world-class local solutions in energy and resources, infrastructure, environment

UNCONVENTIONAL GAS RESOURCES Exploration, Development and Planning Support Services RPS is an international consultancy providing world-class local solutions in energy and resources, infrastructure, environment

Dan Kelly. June 14, 2013

Dan Kelly June 14, 2013 2 Forward-looking Statements and Non-GAAP Measures This presentation contains certain forward-looking statements within the meaning of the federal securities law. Words such as

Dan Kelly June 14, 2013 2 Forward-looking Statements and Non-GAAP Measures This presentation contains certain forward-looking statements within the meaning of the federal securities law. Words such as

DTE Energy Barnett Shale Overview. April 6, 2006

DTE Energy Barnett Shale Overview April 6, 2006 Safe Harbor Statement The information contained herein is as of the date of this presentation. DTE Energy expressly disclaims any current intention to update

DTE Energy Barnett Shale Overview April 6, 2006 Safe Harbor Statement The information contained herein is as of the date of this presentation. DTE Energy expressly disclaims any current intention to update

SONATRACH ALGERIA SONATRACH. Vision & Perspectives. ALGERIA - Energy Day 04th May, 2016 HOUSTON - TEXAS - USA

SONATRACH ALGERIA SONATRACH Vision & Perspectives ALGERIA - Energy Day 04th May, 2016 HOUSTON - TEXAS - USA Sonatrach Corporate Profile : 2015 key figures E&P Midstream Downstream Marketing Discoveries

SONATRACH ALGERIA SONATRACH Vision & Perspectives ALGERIA - Energy Day 04th May, 2016 HOUSTON - TEXAS - USA Sonatrach Corporate Profile : 2015 key figures E&P Midstream Downstream Marketing Discoveries

AIChE: Natural Gas Utilization Workshop Overcoming Hurdles of Technology Implementation

AIChE: Natural Gas Utilization Workshop Overcoming Hurdles of Technology Implementation Natural Gas in the United States: An Overview of Resources and Factors Affecting the Market November 2, 216 Justin

AIChE: Natural Gas Utilization Workshop Overcoming Hurdles of Technology Implementation Natural Gas in the United States: An Overview of Resources and Factors Affecting the Market November 2, 216 Justin

The Shale Gas Revolution: Global Implications in a Changing Energy Landscape

The Shale Gas Revolution: Global Implications in a Changing Energy Landscape Shale Gas World Europe 2013 Expo XXI Centre, Warsaw, Poland November 26-28, 2013 Dr Basim Faraj VP New Ventures Tamboran Resources

The Shale Gas Revolution: Global Implications in a Changing Energy Landscape Shale Gas World Europe 2013 Expo XXI Centre, Warsaw, Poland November 26-28, 2013 Dr Basim Faraj VP New Ventures Tamboran Resources

Bakken Shale: Evolution of a Giant Oil Field

Continental Resources Inc. Bakken Shale: Evolution of a Giant Oil Field Jack Stark Sr. VP Exploration Feb.16, 2011 Continental Resources Highlights #3 largest oil producer in the Rockies 310MM boe proved

Continental Resources Inc. Bakken Shale: Evolution of a Giant Oil Field Jack Stark Sr. VP Exploration Feb.16, 2011 Continental Resources Highlights #3 largest oil producer in the Rockies 310MM boe proved

The Unconventional Reservoirs Revolution and the Rebirth of the U.S. Onshore Oil & Gas Industry

The Unconventional Reservoirs Revolution and the Rebirth of the U.S. Onshore Oil & Gas Industry Feb. 19, 2013 Cautionary Statement The following presentation includes forward-looking statements. These

The Unconventional Reservoirs Revolution and the Rebirth of the U.S. Onshore Oil & Gas Industry Feb. 19, 2013 Cautionary Statement The following presentation includes forward-looking statements. These

U.S. Crude Oil, Natural Gas, and NG Liquids Proved Reserves

1 of 5 3/14/2013 11:37 PM U.S. Crude Oil, Natural Gas, and NG Liquids Proved Reserves With Data for Release Date: August 1, 2012 Next Release Date: March 2013 Previous Issues: Year: Summary Proved reserves

1 of 5 3/14/2013 11:37 PM U.S. Crude Oil, Natural Gas, and NG Liquids Proved Reserves With Data for Release Date: August 1, 2012 Next Release Date: March 2013 Previous Issues: Year: Summary Proved reserves

A Global Perspective for IOR and Primary in Unconventional Tight Oil and Gas Reservoirs. Richard Baker May-13

A Global Perspective for IOR and Primary in Unconventional Tight Oil and Gas Reservoirs Richard Baker May-13 1 Conclusions 1. There has been tremendous growth in tight oil and gas rates and reserves. 2.

A Global Perspective for IOR and Primary in Unconventional Tight Oil and Gas Reservoirs Richard Baker May-13 1 Conclusions 1. There has been tremendous growth in tight oil and gas rates and reserves. 2.

White Paper: Shale Gas Technology. September Shale Gas Technology 2011 NRGExpert Page 1 of 8

White Paper: Shale Gas Technology September 2011 Shale Gas Technology 2011 NRGExpert www.nrgexpert.com Page 1 of 8 Table of Contents An Introduction to Shale Gas Technology... 3 Horizontal drilling...

White Paper: Shale Gas Technology September 2011 Shale Gas Technology 2011 NRGExpert www.nrgexpert.com Page 1 of 8 Table of Contents An Introduction to Shale Gas Technology... 3 Horizontal drilling...

SAMPLE. US Shale. Insight Report

US Shale Insight Report 2013 www.eic-consult.com Contents Page Outlook and Executive Summary 8-15 Shale Operations and Technology 16-24 Shale Economics and International LNG Markets 25-37 Major Shale Plays

US Shale Insight Report 2013 www.eic-consult.com Contents Page Outlook and Executive Summary 8-15 Shale Operations and Technology 16-24 Shale Economics and International LNG Markets 25-37 Major Shale Plays

Unconventional Gas: Efficient and Effective Appraisal and Development. Jeff Meisenhelder VP Unconventional Resources

Unconventional Gas: Efficient and Effective Appraisal and Development Jeff Meisenhelder VP Unconventional Resources Million Cubic Feet The Barnett Story Perserverence and Technology Make the Difference

Unconventional Gas: Efficient and Effective Appraisal and Development Jeff Meisenhelder VP Unconventional Resources Million Cubic Feet The Barnett Story Perserverence and Technology Make the Difference

THIRTY YEARS OF LESSONS LEARNED. Coal

THIRTY YEARS OF LESSONS LEARNED TIPS AND TRICKS FOR FINDING, DEVELOPING AND OPERATING A COALBED METHANE FIELD Philip Loftin BP America Coal Lesson #1 Coal is different than conventional reservoir rock

THIRTY YEARS OF LESSONS LEARNED TIPS AND TRICKS FOR FINDING, DEVELOPING AND OPERATING A COALBED METHANE FIELD Philip Loftin BP America Coal Lesson #1 Coal is different than conventional reservoir rock

For personal use only. AWE Limited. Asian Roadshow Presentation. June 2012

AWE Limited Asian Roadshow Presentation June 2012 Disclaimer This presentation may contain forward looking statements that are subject to risk factors associated with the oil and gas businesses. It is

AWE Limited Asian Roadshow Presentation June 2012 Disclaimer This presentation may contain forward looking statements that are subject to risk factors associated with the oil and gas businesses. It is

The SPE Foundation through member donations and a contribution from Offshore Europe

Primary funding is provided by The SPE Foundation through member donations and a contribution from Offshore Europe The Society is grateful to those companies that allow their professionals to serve as

Primary funding is provided by The SPE Foundation through member donations and a contribution from Offshore Europe The Society is grateful to those companies that allow their professionals to serve as

The Better Business Publication Serving the Exploration / Drilling / Production Industry AOGR

JANUARY 2014 The Better Business Publication Serving the Exploration / Drilling / Production Industry Refracturing Extends Lives Of Unconventional Reservoirs The ability to refracture source rock reservoirs

JANUARY 2014 The Better Business Publication Serving the Exploration / Drilling / Production Industry Refracturing Extends Lives Of Unconventional Reservoirs The ability to refracture source rock reservoirs

Carbon Dioxide Capture and Storage in Deep Geological Formations. Carbon Dioxide Capture and Geologic Storage

Stanford University Global Climate & Energy Project Public Workshops on Carbon Capture and Sequestration Sacramento Sheraton & University of Southern California February 13 & 14, 2008 Carbon Dioxide Capture

Stanford University Global Climate & Energy Project Public Workshops on Carbon Capture and Sequestration Sacramento Sheraton & University of Southern California February 13 & 14, 2008 Carbon Dioxide Capture

Benchmarking Reserve Estimation by Comparing EUR Variability Across the BC Montney May 28, 2014

Benchmarking Reserve Estimation by Comparing EUR Variability Across the BC Montney May 28, 2014 Jake Thompson, Development Engineer jthompson@blackswanenergy.com Presented at: Reserve Estimation Unconventionals

Benchmarking Reserve Estimation by Comparing EUR Variability Across the BC Montney May 28, 2014 Jake Thompson, Development Engineer jthompson@blackswanenergy.com Presented at: Reserve Estimation Unconventionals

Successful Completion Optimization of the Eagle Ford Shale

Successful Completion Optimization of the Eagle Ford Shale Supplement to SPE Paper 170764 Presented at the Society of Petroleum Engineers Annual Technical Conference and Exhibition Amsterdam, The Netherlands

Successful Completion Optimization of the Eagle Ford Shale Supplement to SPE Paper 170764 Presented at the Society of Petroleum Engineers Annual Technical Conference and Exhibition Amsterdam, The Netherlands

Status of Shale Gas Development in New Brunswick. Habitation 2012

Status of Shale Gas Development in New Brunswick Angie Leonard, Senior Advisor, CAPP Habitation 2012 St. Andrews, New Brunswick February 9, 2012 What Is CAPP? CAPP s mission is to enhance the economic

Status of Shale Gas Development in New Brunswick Angie Leonard, Senior Advisor, CAPP Habitation 2012 St. Andrews, New Brunswick February 9, 2012 What Is CAPP? CAPP s mission is to enhance the economic

ENCANA CORPORATION. Operational Excellence. Michael McAllister. Executive Vice President & Chief Operating Officer

ENCANA CORPORATION Operational Excellence Michael McAllister Executive Vice President & Chief Operating Officer ENCANA Delivering Quality Corporate Returns North American leader in: Generating free cash

ENCANA CORPORATION Operational Excellence Michael McAllister Executive Vice President & Chief Operating Officer ENCANA Delivering Quality Corporate Returns North American leader in: Generating free cash

THE U.S. OIL AND NATURAL GAS INDUSTRY: MARKET DYNAMICS AND INDUSTRY RESPONSES

THE U.S. OIL AND NATURAL GAS INDUSTRY: MARKET DYNAMICS AND INDUSTRY RESPONSES 1 OVERVIEW Market Overview Cost Reduction Actions Best Management/Recommended Practices Technology and Industry Advances Summary

THE U.S. OIL AND NATURAL GAS INDUSTRY: MARKET DYNAMICS AND INDUSTRY RESPONSES 1 OVERVIEW Market Overview Cost Reduction Actions Best Management/Recommended Practices Technology and Industry Advances Summary

Global Unconventional Potential at $50 Oil What are you missing? August 2017 Ian Cockerill

Global Unconventional Potential at $50 Oil What are you missing? August 2017 Ian Cockerill Presentation Outline GLOBAL PERSPECTIVE NORTH AMERICAN PERSPECTIVE PLAY PERSPECTIVE PLAY MAPPING QUANTIFICATION

Global Unconventional Potential at $50 Oil What are you missing? August 2017 Ian Cockerill Presentation Outline GLOBAL PERSPECTIVE NORTH AMERICAN PERSPECTIVE PLAY PERSPECTIVE PLAY MAPPING QUANTIFICATION

Proppant Surface Treatment and Well Stimulation for Tight Oil and Shale Gas Development

Proppant Surface Treatment and Well Stimulation for Tight Oil and Shale Gas Development Final Report March 31, 2016 \ Disclaimer PTAC Petroleum Technology Alliance Canada and 3M Canada do not warrant or

Proppant Surface Treatment and Well Stimulation for Tight Oil and Shale Gas Development Final Report March 31, 2016 \ Disclaimer PTAC Petroleum Technology Alliance Canada and 3M Canada do not warrant or

Jerzy M. Rajtar* SHALE GAS HOW IS IT DEVELOPED?

WIERTNICTWO NAFTA GAZ TOM 27 ZESZYT 1 2 2010 Jerzy M. Rajtar* SHALE GAS HOW IS IT DEVELOPED? 1. INTRODUCTION XTO Energy, Inc. has been engaged in development of major gas shale plays in the continental

WIERTNICTWO NAFTA GAZ TOM 27 ZESZYT 1 2 2010 Jerzy M. Rajtar* SHALE GAS HOW IS IT DEVELOPED? 1. INTRODUCTION XTO Energy, Inc. has been engaged in development of major gas shale plays in the continental

Fracture Stimulation Just the Facts, Ma am

Fracture Stimulation Just the Facts, Ma am 1 Picture of a frac treatment in a coalbed methane well that was mined out in a NM coal mine at 600 depth. Fluid containing sand pumped at high pressures to crack

Fracture Stimulation Just the Facts, Ma am 1 Picture of a frac treatment in a coalbed methane well that was mined out in a NM coal mine at 600 depth. Fluid containing sand pumped at high pressures to crack

Petrotechnical Expert Services. Multidisciplinary expertise, technology integration, and collaboration to improve operations

Petrotechnical Expert Services Multidisciplinary expertise, technology integration, and collaboration to improve operations From reservoir characterization and comprehensive development planning to production

Petrotechnical Expert Services Multidisciplinary expertise, technology integration, and collaboration to improve operations From reservoir characterization and comprehensive development planning to production

AADE Symposium 2011 Haynesville Shale. Presented by James R. Redfearn Vice President Drilling & Completions Mid Continent Region January 19, 2011

AADE Symposium 211 Haynesville Shale Presented by James R. Redfearn Vice President Drilling & Completions Mid Continent Region January 19, 211 1 Forward Looking Statements This communication contains forward-looking

AADE Symposium 211 Haynesville Shale Presented by James R. Redfearn Vice President Drilling & Completions Mid Continent Region January 19, 211 1 Forward Looking Statements This communication contains forward-looking

Carbon Dioxide Capture and Sequestration in Deep Geological Formations

Stanford University Global Climate & Energy Project Public Workshops on Carbon Capture and Sequestration Bloomberg National Headquarters, NY and Rayburn House Office Bldg., Washington, DC March 5&6, 2009

Stanford University Global Climate & Energy Project Public Workshops on Carbon Capture and Sequestration Bloomberg National Headquarters, NY and Rayburn House Office Bldg., Washington, DC March 5&6, 2009

North American Midstream Infrastructure Through 2035 A Secure Energy Future. Press Briefing June 28, 2011

North American Midstream Infrastructure Through 2035 A Secure Energy Future Press Briefing June 28, 2011 Disclaimer This presentation presents views of ICF International and the INGAA Foundation. The presentation

North American Midstream Infrastructure Through 2035 A Secure Energy Future Press Briefing June 28, 2011 Disclaimer This presentation presents views of ICF International and the INGAA Foundation. The presentation

Marcellus Shale Water Group

Marcellus Shale Water Group Targeting unconventional oil & gas reservoirs with better ideas, better solutions Our technique of calculating actual production increases the value of your reservoir 1 Predictive

Marcellus Shale Water Group Targeting unconventional oil & gas reservoirs with better ideas, better solutions Our technique of calculating actual production increases the value of your reservoir 1 Predictive

U.S. Natural Gas A Decade of Change and the Emergence of the Gas-Centric Future

AIChE Alternative Natural Gas Applications Workshop U.S. Natural Gas A Decade of Change and the Emergence of the Gas-Centric Future Francis O Sullivan October 8 th, 214 1 Natural gas The new unconventional

AIChE Alternative Natural Gas Applications Workshop U.S. Natural Gas A Decade of Change and the Emergence of the Gas-Centric Future Francis O Sullivan October 8 th, 214 1 Natural gas The new unconventional

WORKSHOP ON GOVERNANCE OF RISKS OF UNCONVENTIONAL SHALE GAS. Governance Considerations from a Technical Perspective

WORKSHOP ON GOVERNANCE OF RISKS OF UNCONVENTIONAL SHALE GAS National Research Council August 15, 2013 Governance Considerations from a Technical Perspective Mark D. Zoback Professor of Geophysics Shale

WORKSHOP ON GOVERNANCE OF RISKS OF UNCONVENTIONAL SHALE GAS National Research Council August 15, 2013 Governance Considerations from a Technical Perspective Mark D. Zoback Professor of Geophysics Shale

Winter U.S. Natural Gas Production and Supply Outlook

Winter 2010-11 U.S. Natural Gas Production and Supply Outlook Prepared for Natural Gas Supply Association by: ICF International Fairfax, Virginia September, 2010 Introduction This report presents ICF s

Winter 2010-11 U.S. Natural Gas Production and Supply Outlook Prepared for Natural Gas Supply Association by: ICF International Fairfax, Virginia September, 2010 Introduction This report presents ICF s

1951 Clarence Iverson #1

THE BAKKEN Where It All Began... On April 4, 95, the first successful well in North Dakota was drilled outside the community of Tioga. Since the success of the first well, named Clarence Iverson #, the

THE BAKKEN Where It All Began... On April 4, 95, the first successful well in North Dakota was drilled outside the community of Tioga. Since the success of the first well, named Clarence Iverson #, the

Benelux Conference Pan European Days

Benelux Conference Pan European Days 3-5 June 2013 Waldorf Astoria New York, New York Slide 1 Benelux Conference Pan European Days 3-5 June 2013 Waldorf Astoria New York, New York Slide 2 Three principal

Benelux Conference Pan European Days 3-5 June 2013 Waldorf Astoria New York, New York Slide 1 Benelux Conference Pan European Days 3-5 June 2013 Waldorf Astoria New York, New York Slide 2 Three principal

By Bob Hugman and Harry Vidas

WHITE PAPER Oklahoma: A Major Player for Future Hydrocarbon Production By Bob Hugman and Harry Vidas Bottom Line 1. Despite sharp drilling activity declines over the past year in most areas of the country,

WHITE PAPER Oklahoma: A Major Player for Future Hydrocarbon Production By Bob Hugman and Harry Vidas Bottom Line 1. Despite sharp drilling activity declines over the past year in most areas of the country,

Unconventional Gas Resources

Unconventional Gas Resources Methane to Markets Partnership Expo Beijing, China Well Completion and Production Challenges October 31, 2007 James A. Slutz Deputy Assistant Secretary Office of Oil and Natural

Unconventional Gas Resources Methane to Markets Partnership Expo Beijing, China Well Completion and Production Challenges October 31, 2007 James A. Slutz Deputy Assistant Secretary Office of Oil and Natural

DJ Basin. Dan Kelly Vice President Wattenberg

DJ Basin Dan Kelly Vice President Wattenberg NBL Leading the Way Wattenberg and Northern Colorado Premier Oil Play that Compares Favorably to Other Plays Net Resources Dramatically Increased to 2.1 BBoe

DJ Basin Dan Kelly Vice President Wattenberg NBL Leading the Way Wattenberg and Northern Colorado Premier Oil Play that Compares Favorably to Other Plays Net Resources Dramatically Increased to 2.1 BBoe

In Part 1 I explained how Argentina s Vaca Muerta shale is the only international play so far that looks like it could be bigger than the Bakken.

In Part 1 I explained how Argentina s Vaca Muerta shale is the only international play so far that looks like it could be bigger than the Bakken. For investors, the challenge is that most of the activity

In Part 1 I explained how Argentina s Vaca Muerta shale is the only international play so far that looks like it could be bigger than the Bakken. For investors, the challenge is that most of the activity

Injection Wells for Liquid-Waste Disposal. Long-term reliability and environmental protection

Injection Wells for Liquid-Waste Disposal Long-term reliability and environmental protection ACHIEVE MULTIPLE GOALS FOR LIQUID-WASTE DISPOSAL INJECTION WELLS Expertly located, designed, constructed, and

Injection Wells for Liquid-Waste Disposal Long-term reliability and environmental protection ACHIEVE MULTIPLE GOALS FOR LIQUID-WASTE DISPOSAL INJECTION WELLS Expertly located, designed, constructed, and

SHALE FACTS. Production cycle. Ensuring safe and responsible operations

SHALE FACTS Production cycle Ensuring safe and responsible operations Statoil is committed to developing our shale projects in a safe, responsible and open manner. Statoil takes a long term perspective

SHALE FACTS Production cycle Ensuring safe and responsible operations Statoil is committed to developing our shale projects in a safe, responsible and open manner. Statoil takes a long term perspective

Shouyang CBM Project Design for Production

Far East Energy Corporation U.S. - China Oil and Gas Industry Forum Chengdu, China Shouyang CBM Project Design for Production David J. Minor, P.E. Executive Director of Operations September 24-26, 2011

Far East Energy Corporation U.S. - China Oil and Gas Industry Forum Chengdu, China Shouyang CBM Project Design for Production David J. Minor, P.E. Executive Director of Operations September 24-26, 2011

Forward Looking Statements

is the world s largest supplier of ceramic proppant, the provider of the world s most popular fracture simulation software, and a leading provider of fracture design, engineering and consulting services.

is the world s largest supplier of ceramic proppant, the provider of the world s most popular fracture simulation software, and a leading provider of fracture design, engineering and consulting services.

SHALE GAS DEVELOPMENT IN ARGENTINA. A CHANGE TO THE TRADITIONAL E&P BUSINESS STRATEGY.

SHALE GAS DEVELOPMENT IN ARGENTINA. A CHANGE TO THE TRADITIONAL E&P BUSINESS STRATEGY. Author: Noelia Denisse Chimale, Instituto Tecnológico de Buenos Aires, Nicolas de Vedia 1682, 3 A, Buenos Aires, Argentina,

SHALE GAS DEVELOPMENT IN ARGENTINA. A CHANGE TO THE TRADITIONAL E&P BUSINESS STRATEGY. Author: Noelia Denisse Chimale, Instituto Tecnológico de Buenos Aires, Nicolas de Vedia 1682, 3 A, Buenos Aires, Argentina,

Woodford Shale Development in the Ardmore Basin, Oklahoma

Woodford Shale Development in the Ardmore Basin, Oklahoma Initial thoughts on beginning an infill drilling program Sam Henderson Merit Energy Company Merit Energy Company Founded in 1989 Primarily focused

Woodford Shale Development in the Ardmore Basin, Oklahoma Initial thoughts on beginning an infill drilling program Sam Henderson Merit Energy Company Merit Energy Company Founded in 1989 Primarily focused

Oil and gas companies are pushing for improved performance and better efficiency from service providers

RIGMINDER TECHNICAL PRESENTATION December 7, 2017 Industry Trends Oil and gas companies are pushing for improved performance and better efficiency from service providers Drillers are responding with integrated

RIGMINDER TECHNICAL PRESENTATION December 7, 2017 Industry Trends Oil and gas companies are pushing for improved performance and better efficiency from service providers Drillers are responding with integrated

Bank of America Merrill Lynch 2012 Global Energy Conference

Bank of America Merrill Lynch 2012 Global Energy Conference November 14-16, 2012 Fontainebleau Hotel Miami, Florida Slide 1 2012 Global Energy Conference November 14 16, 2012 Fontainebleau Hotel, Miami,

Bank of America Merrill Lynch 2012 Global Energy Conference November 14-16, 2012 Fontainebleau Hotel Miami, Florida Slide 1 2012 Global Energy Conference November 14 16, 2012 Fontainebleau Hotel, Miami,

Approach Optimizes Frac Treatments

JULY 2011 The Better Business Publication Serving the Exploration / Drilling / Production Industry Approach Optimizes Frac Treatments By Jamel Belhadi, Hariharan Ramakrishnan and Rioka Yuyan HOUSTON Geologic,

JULY 2011 The Better Business Publication Serving the Exploration / Drilling / Production Industry Approach Optimizes Frac Treatments By Jamel Belhadi, Hariharan Ramakrishnan and Rioka Yuyan HOUSTON Geologic,

Integrated Sensor Diagnostics (ISD) Subsurface Insight for Unconventional Reservoirs

Subsurface Insight for Unconventional Reservoirs") HALLIBURTON WHITE PAPER Integrated Sensor Diagnostics (ISD) Subsurface Insight for Unconventional Reservoirs Solving challenges. Integrated Sensor Diagnostics (ISD) Subsurface Insight for Unconventional

HALLIBURTON WHITE PAPER Integrated Sensor Diagnostics (ISD) Subsurface Insight for Unconventional Reservoirs Solving challenges. Integrated Sensor Diagnostics (ISD) Subsurface Insight for Unconventional

TSX-V: YO. September. Duvernay Shale Peters & Co. Energy Conference

TSX-V: YO September Duvernay Shale Peters & Co. Energy Conference Yoho Quick Facts SYMBOL YO TSX.V BASIC SHARES (Insiders 14.8%) DILUTED SHARES (WA Exercise Price of options $2.90) MARKET CAP 46.4 MM *

TSX-V: YO September Duvernay Shale Peters & Co. Energy Conference Yoho Quick Facts SYMBOL YO TSX.V BASIC SHARES (Insiders 14.8%) DILUTED SHARES (WA Exercise Price of options $2.90) MARKET CAP 46.4 MM *

Unconventional Oil and Gas Reservoirs

Energy from the Earth Briefing Series, Part 4 May, 2014 Unconventional Oil and Gas Reservoirs Scott W. Tinker Bureau of Economic Geology Jackson School of Geosciences, The University of Texas at Austin

Energy from the Earth Briefing Series, Part 4 May, 2014 Unconventional Oil and Gas Reservoirs Scott W. Tinker Bureau of Economic Geology Jackson School of Geosciences, The University of Texas at Austin

Drilling Deeper: A Reality Check on U.S. Government Forecasts for a Lasting Tight Oil & Shale Gas Boom. Web Briefing December 9, 2014

Drilling Deeper: A Reality Check on U.S. Government Forecasts for a Lasting Tight Oil & Shale Gas Boom Web Briefing December 9, 214 J. David Hughes Post Carbon Institute Global Sustainability Research

Drilling Deeper: A Reality Check on U.S. Government Forecasts for a Lasting Tight Oil & Shale Gas Boom Web Briefing December 9, 214 J. David Hughes Post Carbon Institute Global Sustainability Research

NEVADA EXPLORATION PROJECT

Energizing the World, Bettering People s Lives NEVADA EXPLORATION PROJECT Legislative Committee on Public Lands June 12, 2014 Kevin Vorhaben, Rockies/Frontier Business Unit Manager Forward-looking Statements

Energizing the World, Bettering People s Lives NEVADA EXPLORATION PROJECT Legislative Committee on Public Lands June 12, 2014 Kevin Vorhaben, Rockies/Frontier Business Unit Manager Forward-looking Statements

Bakken Pad Drilling Greater Resource Potential with a Reduced Environmental Footprint

Bakken Pad Drilling Greater Resource Potential with a Reduced Environmental Footprint Multi-Well Pad Drilling Congress 2014 Houston, Texas October 1, 2014 John Harju Associate Director for Research 2014

Bakken Pad Drilling Greater Resource Potential with a Reduced Environmental Footprint Multi-Well Pad Drilling Congress 2014 Houston, Texas October 1, 2014 John Harju Associate Director for Research 2014

Technology Enhancements in the Hydraulic Fracturing of Horizontal Wells

Technology Enhancements in the Hydraulic Fracturing of Horizontal Wells Brian Clark Senior Production and Completions Engineer Unconventional Resources Group Topics Environmental Horizontal Completion

Technology Enhancements in the Hydraulic Fracturing of Horizontal Wells Brian Clark Senior Production and Completions Engineer Unconventional Resources Group Topics Environmental Horizontal Completion

Southeast Regional Carbon Sequestration Partnership

Southeast Regional Carbon Sequestration Partnership The, encompasses an 11 state region including the states of Alabama, Arkansas, Florida, Georgia, Louisiana, Mississippi, North Carolina, South Carolina,

Southeast Regional Carbon Sequestration Partnership The, encompasses an 11 state region including the states of Alabama, Arkansas, Florida, Georgia, Louisiana, Mississippi, North Carolina, South Carolina,

Latest insights in shale gas technology and environmental impacts

Latest insights in shale gas technology and environmental impacts Jan ter Heege TNO Petroleum Geosciences, the Netherlands EERA Shale Gas JP Knowledge Sharing Event, Krakow, 03.12.2015 Part of this presentation

Latest insights in shale gas technology and environmental impacts Jan ter Heege TNO Petroleum Geosciences, the Netherlands EERA Shale Gas JP Knowledge Sharing Event, Krakow, 03.12.2015 Part of this presentation

ShaleGas:- Opportunities and Barriers: A UK Perspective. Professor Peter Styles, Applied and Environmental Geophysics Research Group

ShaleGas:- Opportunities and Barriers: A UK Perspective Professor Peter Styles, Applied and Environmental Geophysics Research Group 1 Stop Press! SHEER 2.7 Million Euros HORIZON2020 Research Grant for

ShaleGas:- Opportunities and Barriers: A UK Perspective Professor Peter Styles, Applied and Environmental Geophysics Research Group 1 Stop Press! SHEER 2.7 Million Euros HORIZON2020 Research Grant for

Horizontal Well Spacing and Hydraulic Fracturing Design Optimization: A Case Study on Utica-Point Pleasant Shale Play

URTeC: 2459851 Horizontal Well Spacing and Hydraulic Fracturing Design Optimization: A Case Study on Utica-Point Pleasant Shale Play Alireza Shahkarami*, Saint Francis University; Guochang Wang*, Saint

URTeC: 2459851 Horizontal Well Spacing and Hydraulic Fracturing Design Optimization: A Case Study on Utica-Point Pleasant Shale Play Alireza Shahkarami*, Saint Francis University; Guochang Wang*, Saint

Trends, Issues and Market Changes for Crude Oil and Natural Gas

Trends, Issues and Market Changes for Crude Oil and Natural Gas East Iberville Community Advisory Panel Meeting Syngenta September 26, 2012 Center for Energy Studies David E. Dismukes, Ph.D. Center for

Trends, Issues and Market Changes for Crude Oil and Natural Gas East Iberville Community Advisory Panel Meeting Syngenta September 26, 2012 Center for Energy Studies David E. Dismukes, Ph.D. Center for

Unconventional Oil & Gas: Reshaping Energy Markets

Unconventional Oil & Gas: Reshaping Energy Markets Guy Caruso Senior Advisor JOGMEC Seminar 7 February 2013 Landscape is Changing Even as We Sit Here Today - US Projected to reach 90% Energy Self-Sufficiency

Unconventional Oil & Gas: Reshaping Energy Markets Guy Caruso Senior Advisor JOGMEC Seminar 7 February 2013 Landscape is Changing Even as We Sit Here Today - US Projected to reach 90% Energy Self-Sufficiency

New Technologies, Innovations

New Technologies, Innovations Drilling New Technologies, Innovations Advances in technologies used for well drilling and completion have enabled the energy industry to reach new sources of oil and natural