FEASIBILITY STUDY ON ACCESS TO FINANCING FOR RE APPLIANCE FOR RURAL POOR IN CAMBODIA

|

|

|

- Rosamund Hart

- 6 years ago

- Views:

Transcription

1 FEASIBILITY STUDY ON ACCESS TO FINANCING FOR RE APPLIANCE FOR RURAL POOR IN CAMBODIA

2 ACKNOWLEDGEMENTS This report was commissioned by VisionFund Cambodia under the frame of the UNEP Climate Finance Innovation Facility (CFIF). CONCEPT AND CONTRIBUTORS Jan G. Andreas Alicia Rondón-Krummheuer Indrani Hettiarachchy Tobias Panofen SURVEY TEAM COORDINATORS Pheng Raksa Sokmei Prav

3 TABLE OF CONTENTS EXECUTIVE SUMMARY INTRODUCTION COUNTRY PROFILE Geographical location and climate Geographical location Climate Demographics Economy Energy situation Legal and regulatory framework Energy prices overview CONCEPTUAL APPROACH AND METHODOLOGY Objectives of the study Essential concepts and termonology Identification of the methodology Location of the study, sample, data collection Data analysis Encountered difficulties MARKET ANALYSIS Financial sector in cambodia Vision Fund Cambodia Supply of RE Loans in Cambodia Potencial demand for RE microfinance loans in CAmbodia Determinants of potential demand Results of the Questionnaire Estimates of potential demand Market Available Products and Services LOAN PRODUCT FORMATION RECOMMENDATIONS Analysis of best practices RE Loan Product Sample

4 5.3. RE Loan Product Component Parts RE Loan Product Sales Efforts Evaluation and Monitoring of disbursed Loans FINAL CONSIDERATIONS AND RECOMENDATIONS POTENTIAL PARTNER SUPPLIERS INSTITUTIONS POTENTIAL DONOR INSTITUTIONS...25 ANNEXES ANNEX 1 QUESTIONNAIRE ANNEX 2 CURRENT OPERATIONAL AREAS ANNEX 3 ADDITIONAL MARKET INFORMATION ANNEX 5 POTENTIAL PARTNER SUPPLIERS INSTITUTION 2

5 EXECUTIVE SUMMARY VisionFund Cambodia, under the frame of the UNEP Climate Finance Innovation Facility, commissioned Frankfurt School of Finance & Management to conduct a detailed feasibility study on access to financing for RE appliance for rural poor in Cambodia. The purpose of this feasibility study was to assess the target market characteristics in terms of market potential and client/future client preferences, and help VisionFund Cambodia to understand how its abilities can be synchronised with market requirements. Additionally, the study aimed to assess the feasibility of RE lending products and more closely estimate the renewable energy in particular solar energy- lending potential. The scope of the study focused all 12 branches and its 17 operating provinces of VisionFund Cambodia. In order to reach these goals, direct market study estimation methods were employed: demand and supply analysis, and was based on the information gathered from the client/potential client, from the supplier or vendor side, and from other microfinance institutions and programs. Furthermore, a comprehensive secondary research via a desk study was performed. FINACIAL SECTOR IN CAMBODIA The banking and microfinance sector is one of the most developed sectors with 27 commercial banks, 6 specialized banks and 20 licensed microfinance institutions. The National Bank of Cambodia is responsible of supervising the banking sector. As of end-2009, there were 20 licensed MFIs operating plus additional 26 registered rural credit NGOs providing microfinance services. Furthermore, around 60 NGO-MFIs, not licensed nor registered, provided informal financial services. According to the NBC, the number of MFI borrowers grew from 230,114 in 2008 to 262,952 (by 14%) in SUPPLY OF RE LOANS IN CAMBODIA The overview of Cambodia s financial market certainly presents evidence of underserved niche for RE finance products and services. The assessment reveals the existence of a potential to target and create new segmented financing of RE investments. The main reason for low performance in building renewable energy investment pipeline still lays in general lack of awareness and lack of knowledge of the advantages of alternative energy forms for rural households. Currently the MFI which provides loans for RE are: AMRET and PRASAC MFIs offer credit/loans for RE products for bio-digesters. SNV supports this initiative together with ACLEDA Bank through the National Biodigester Programme (NBP). CMK gives credit for solar already but has no specific loan product for this. They have a MoU with the supplier Kamworks. Up to this period of time1, apart from VisionFund (MFI), CMK (Cooperative), Yejj Solar (NGO), International Solar Solutions (Enterprise/Supplier), Khmer Solar (Enterprise/Supplier), and Kamworks (Enterprise/Supplier) there are no other institutions intending to enter (or already on the business) the solar finance market, i.e. that will commence specialized solar financing. POTENTIAL DEMAND FOR RE MICROFINANCE LOANS IN CAMBODIA General experience in developing countries entails tight correlation between projected potential number of future clients and a combination of demographic characteristics, national/local policy & regulations and even climate characteristics. Detail analysis is presented in the document. 1 June

6 As mentioned before, a detail survey to 401 clients/potential clients was conducted in different provinces of Cambodia. As main results, it was found out that: Income is to some extend available for more than half of the interviewed people on a regular basis. Crops seasonality is a major issue for the rural population in Cambodia. Significant regional differences in income for food and clothes are measurable. Basic living conditions of rural households are significantly dependent on seasonal availability of income. Access to electricity is a key issue for rural households in Cambodia. The awareness of renewable energy is still on a low level. A third of total interviewed know solar energy. Despite the lack of awareness of RE in general, almost 70% of the interviewed are willing to take a credit for solar. The monthly repayment should match the amount households spent so far for energy sources. MARKET AVAILABLE PRODUCTS AND SERVICES In Cambodia there are several suitable solar products available for rural households. Financial services are however, a major gap. It is essential to mention that these technologies are mainly provided on a cash basis with too high upfront costs for rural poor, or sometimes they are donated (but in a small scale), or subsidised and there is no external assistance to follow up on the equipment. Although there are several suppliers companies for solar technology systems in Cambodia, the consultant has identified that there are seven main suppliers: Comin Khmere, Kamworks Ltd., Khmer Solar Ltd., Solar Energy Cambodia Ltd., International Solar Solutions, KC Solar, and Yejj Solar. The lessons learned are that people s expectations and the capacity of the solar technology system need to be matched. Education and awareness raising are the key issues. Furthermore, replacement parts should be standardized. The regular warranty is one year and after that customers need to maintain the system (change bulbs, batteries etc) on their own. Small monetary incentives to train customers on solar technology system potentially increases acceptance and trust and might be considered by VisionFund in cooperation with the yet to be identified supplier. FINAL CONSIDERATIONS AND RECOMMENDATIONS The Kingdom of Cambodia is undoubtedly an interest market for RE financing, especially for solar technology financing. Considering the present and booming situation of solar technology utilisation compared to neighbouring countries in the region, there is a good indication that any effort to introduce and reinforce solar technology financing operation would be successful, given the existing rural poor households needs and substantial lack of competitors in the FI sector. Results from the market analysis show that there is a positive potential demand of solar technology in the poor rural households of Cambodia, although there was a high indication for lack of awareness which is the key issue for VisionFund. The rural poor household s income is less important. Important is the amount of money people spend for electricity. Furthermore, the supply for solar technology financing is almost is its early stage compared to supply of solar technology lending in neighbouring countries. 3

7 The final recommendation is to set up a partnership with no more than 2 or 3 of them according to the criteria given in the especial chapter. With this partnership, the technical risk is somehow reduced if product specifications are fixed by VisionFund and solar technology product warrantees are made available. 4

8 1. INTRODUCTION VisionFund Cambodia is a licensed medium-sized microfinance institution with a clear social mission to provide financial services to help the poor liberate themselves from poverty. It offers three types of lending methodologies to its clients, namely community bank, solidarity group and individual loan. In January 2011, VisionFund had 105,574 active borrowers, of which about 88% were women. Total assets amount USD 36,658,687, compared to USD 26,531,016 at year-end The MFI has been growing at fast pace and managed to keep its portfolio at risk (> 30 days) well below 1%. VisionFund Cambodia, aiming to facilitate better access to qualitatively appropriate financial services for rural poor households in a social responsible manner, is now planning to introduce renewable energy financing. Therefore, within the framework of the Climate Finance Innovation Facility (CFIF), VisionFund approached Frankfurt School of Finance & Management to execute a detailed feasibility study. In close cooperation with VisionFund, a survey was conducted in seventeen operating provinces to determine the potential for financing renewable energy technologies for rural poor households. In addition to this demand survey, Frankfurt School also focussed on demand and supply of different kinds of energy from the supplier side as well as from the MFI side. The data was complemented with secondary sources of information (secondary research) and from information exchange with local experts. Based on the project proposal, Frankfurt School and VisionFund Cambodia agreed on the following objectives: 1. To assess the level of demand on solar energy; 2. To identify alternative renewable energy solutions to meet the demand; 3. To obtain information on the development of suitable products; 4. To be able to define criteria for selecting renewable energy suppliers. The consultant team prepared this feasibility study employing a tailor-made approach and methodology that is based on employing internationally adopted practices, systematic assessment of respective business segments and surrounding market conditions. Particularly, the research was performed by means of on-site visits, desk study and employed mixed methods including statistical review and structured surveys with a questionnaire and with interviews. The preliminary desk activity was employed to determine relevant local conditions, key market players in terms of product and financial services supply, demographic data and a rough estimation of potential demand. Fieldwork consisted of meeting with market players to estimate the supply. Undertaken market analysis has, in combination with demographic data and best practices in RE lending, led to recommendations for forming the RE loan product(s) and relevant operational guidelines. The results and recommendations are suited and directed to VisionFund Cambodia s future decisions about extending its operations to potentially underserved and immature financial market for financing RE products and services. 5

9 Solar radiation (kwh/m2/d) FEASIBILITY STUDY ON ACCESS TO FINANCING FOR RE APPLIANCE FOR RURAL POOR IN CAMBODIA 2. COUNTRY PROFILE In 1991, a comprehensive peace treaty was signed which officially ended the Cambodian civil war. The following years were still characterized by several skirmishes and conflicts, especially with supporters of the old Khmer Rouge regime. In 1997, most of them accepted an amnesty assured by the government and fighting came to an end. Today, Cambodia is a stable, multiparty democracy under a constitutional monarchy. However, with about USD 783 gross national income (GNI) per capita, the country is classified as a low-income country by the World Bank. About 30% of the population lives below the national poverty line and 20% is illiterate. Moreover, in Cambodia there are significant differences regarding living conditions between urban and rural households GEOGRAPHICAL LOCATION AND CLIMATE GEOGRAPHICAL LOCATION Cambodia shares borders with Thailand to the west and northwest, Laos PDR to the northeast, and Vietnam to the east in south-eastern Asia. The country holds approx. 443 km coastline to the Gulf of Thailand and its area totals in 181,035 sq km of which 4,520 sq km is water. Most dominant is the Mekong River, one of the largest rivers in the world. The terrain is low with some mountains in the south-west and north. The highest elevation is the Phnom Aural (~1800 m.a.s.l.), which is northwest of the capital city, Phnom Penh. About 21% of the land in Cambodia is arable; the rest is mostly covered by forests, woodlands, build-on areas, roads and barren land CLIMATE Cambodia is located in the tropical climate zone at approximately degrees north of the equator. Therefore, Cambodia s climate is typically hot tropical with limited variation in temperature between seasons. The average year-round temperature is 27.5 ºC, with maximum monthly mean temperature of 35 ºC and minimum 21 ºC. The average sunshine duration during the year is 6-9 hours per day. The hot dry season usually is between December and April. During these months river and lake levels are very low. Therefore river transport is much more difficult and time consuming. Road travel however, increases significantly due to the lack of flooding caused by the monsoons. The following graph shows the monthly average solar radiation in kwh/m²/d in Cambodia. Graph 1: Annual Solar radiation in Cambodia January February March April May Month June July August September October November December Source: Surface meteorology and Solar energy; Atmospheric Science Data Centre, NASA; 6

10 2.2. DEMOGRAPHICS In 2009 about 14.8 million people lived in Cambodia, of which 22% in urban areas. The overall population density is about 75 persons per square kilometre. The highest population density is in the regions in and around Kampong Cham, Phnom Penh in the southeast and Battambang and Siem Reap in the northwest of Cambodia. The average growth rate over the last five years has been 1.6%. As shown in the following graph 2, more than 75% of the population is less than 50 years old. Especially in the post-war period, the birth rate increased significantly. Between the 1998 census and the 2008 census the population expanded by 17%. UNCDF estimates that between 2009 and 2013 annually 300,000 Cambodians will reach the age of 15 and seek employment. Graph 2: Population Pyramid in Cambodia Source: International Data Base U.S. Census Bureau 2.3. ECONOMY Between 2003 and 2007 the country s GDP grew with an average of 10.6 % annually. Although at lower rates than its neighbouring countries, Cambodia s GDP per capita has been increasing as well, reaching USD in This growth was mainly attributed to garment export expansion, growth in the construction sector and rise in tourism. Hence, this growth has been mainly urban-focused with limits to the rural population, which still makes up about 78% of total population. This has led to an increasing inequality in income during the last decade. GDP contracted 1.5% in 2009 as a result of the global economic slowdown, but climbed more than 4% in 2010, driven by renewed exports. Approximately 5% of Cambodia s work force more than people is employed by the garment industry, which currently accounts for more than 70% of Cambodia's exports. The tourism industry has been growing constantly during the past decade, with tourist arrivals exceeding 2 million per year in However, the global financial crisis has led to a decrease in growth in In 2011 the economy of Cambodia is expected to show further growth, but not in the levels succeeding the crisis. The recent global downturn has also impacted demand for Cambodian exports. Furthermore, construction is declining because of the 7

11 negative effects of the crisis on the banking sector. The long-term development of the economy still remains a great challenge. More than 50% of the population is less than 25 years old. Therefore one of the major challenges facing the economy is to promote private sector development to absorb this amount of work force. Still, the country is characterized by limited access to basic infrastructure, an environment where the population lacks education and 90% of rural population living beneath the poverty line ENERGY SITUATION In 2010 only 29% of households had access to the electricity grid in Cambodia. Almost 100% of urban households are electrified (73% of these households are situated in Phnom Penh), but only about 12.3% have access to services in rural areas. The main domestic suppliers of electricity are Independent Power Suppliers (IPP) accounting for 31% of energy production, Electricité du Cambodia (state-owned electricity provider; EDC) with 15%, Rural Electricity Enterprises (REE) with about 8% and Private Electricity Companies (PEC) producing 4% of total supply in % of the Cambodian electricity is generated from diesel (1.294,4 GWh). The two EDC Hydropower Plants (49,7 GWh), one at Kirirom connected to Phnom Penh power system and the other one at Ratanakiri connected to Ratanakiri power system, produce 3,6 % and the 3 biomass gasifiers (5,3 GWh) in Battambang and Phnom Penh produce the remaining 0,4%. 84,58% of the electricity is distributedby independent power producers, 12,74 % by EDC and the remaining 2,68% by consolidated licensees2. Currently six provinces are not yet connected to the transmission grid3. The annual electricity demand growth rate was 19% in 2009 with peak supply capacity increasing only from 472 MW in 2009 to 528 MW in Hence, Cambodia is highly dependent on its neighbours: 42% of total electricity demand is met via imports from Laos PDR, Vietnam and Thailand. In order to cope with the increasing demand and to decrease dependency on foreign energy imports, the Power Development Plan (PDP) targets the development of more hydro power plants, which is expected to contribute to 50% of energy supply by Currently about 1 GW is under construction and MoUs for approximately 2.2 GW have already been signed LEGAL AND REGULATORY FRAMEWORK There are three main entities which are responsible for the electricity supply in Cambodia. The Ministry of Industry, Mines and Energy (MIME) is in charge of setting and administrating government policies, strategies and planning. The Electricity Authority of Cambodia (EAC) is responsible for the regulation to ensure the qualitative and efficient use of electricity and monitoring as well as guiding suppliers and consumers to follow the policies set by MIME. The public electricity provider EDC is attached to the Ministry of Economic and Finance (MEF) and the MIME. The hierarchy is as follows: 2 Taken from Antje Klauß-Vorreiter (2009) at the International Solar Energy Society (

12 Graph 3: Structure of Electricity Organization Government of Cambodia Electricity Authority of Cambodia (EAC) Ministry of Industry, Mines and Energy (MIME) Ministry of Economic and Finance (MEF) Regulation Policy Maker Owner REE IPP PEC EDC REE IPP PEC EDC Rural Electricity Enterprise Independent Power Producer Private Electricity Company Electricité du Cambodge Source: Cambodia Outlook Conference, Victor Jona, Cambodia Development Resource Institute (CDRI), 2011 With the Power Sector Policy of (1994) the Government is aiming to extend good quality electricity access to 70% of households by 2030 and electrify 90% of villages in the same time period5. This is to be achieved by pursuing a number of strategies: First, grid extension is one of the highest priorities for EDC. The Ministry of Industry, Mines and Energy (MIME)plans to have all of Cambodia s 23 provinces connected to the grid by Second, the government tries to obtain cross-border power supplies from neighbouring countries. Based on the National Grid Development Plan , approximately 200 MW of power would be imported from Vietnam each year from 2010 to From Thailand import would amount to approximately 60 MW. Third, government policy aims to create and rehabilitate isolated grid systems in provincial towns. Fourth strategy is to intensify the application of renewable energy sources, such as mini-hydro, solar and biogas and to provide battery-based stand-alone systems for remote areas6. The Renewable Energy Action Plan was formulated in The four targets of the plan are: 1. Increase electricity supply from renewable energy sources up to 6 MW. 2. Give 100,000 households access to RE electricity. 3. Install 10,000 PV systems. 4. Establish a conducive environment for RE markets. 5 A village counts as electrified when most community facilities and more than 50% of households have electricity. 6 Status and Potential fort he Development of Biofuels and rural renewable energy in Cambodia ADB, Greater Mekong Sub region Development Programme, 9

13 The government tries to foster conducive environments by contributing up to 25% of start-up capital, tax incentives, and investment facilitation for private participants in the energy sector. Another key incentive for the development of the energy sector is the Rural Electrification Fund (REF) established by Royal Decree of the Government of Cambodia. The fund was established to offer grants for private rural operators or Rural Electricity Enterprises (REE). Main funders are the World Bank, the Global Environment Facility (GEF) and the Government of Cambodia. The fund consists of a grant element to sub-projects and a technical assistance element. The grant program targets mainly new stand alone connections, micro hydro, solar and biomass systems ENERGY PRICES OVERVIEW Cambodia s electricity prices are one of the highest in the world and especially in the region. EDC s average tariff is USD 0.16 per kwh8. Prices usually range between USD 0.09 per kwh and USD 0.23 per kwh. Energy in rural areas is most expensive. The tariffs of REEs, for example, 9 range from USD 0.30 per kwh to almost USD 0.90 per kwh. Due to the high prices for fuel and other energy sources, traditional biomass accounts for 90% of the cooking energy, resulting in one of the world s highest deforestation rate of 0.8% per year. These high energy prices are caused by multiple factors, some of which are10: Limited grid outreach resulting in higher generation costs for small scale sources; High dependency on imported, dollar denominated, expensive fuel due to the lack of local energy sources; Inefficiencies and heavy losses, especially in remote areas; High risk premium in small scale IPP contracts due to the lack of effective incentives and guarantees by the government.; Limited access to finance to alternative forms of energy; and Remoteness of villages causes high transaction costs for very small generators. According to the Cambodia Development Resource Institute (CDRI), almost 90% of the population living in rural areas has no access to electricity grid and does not own individual generating units. 55% of these households use automobile batteries for limited use at a cost of USD per kwh Electricity prices in Indonesia in average was USD/KWh for 2004; 0.06 for 2005; for 2006; for 2007 (Source: Ministry of Energy and Mineral Resources of the Republic of Indonesia (2008): Key Indicator 2008) 9 Due to the present system and the strong reliance on diesel the electricity prices in Cambodia is with about 0,25 USD in Phnom Penh to up to 1,0 USD in the provinces the highest in the region. 10 World Bank Energy and Mining in East Asia and Pacific; URL: ~menuPK:574024~pagePK: ~piPK: ~theSitePK:574015~isCURL:Y,00.html 10

14 3. CONCEPTUAL APPROACH AND METHODOLOGY During the past three years VisionFund Cambodia, together with Yejj Solar Tech, conducted a pilot market demand study for solar energy in two operating provinces.11 They discovered that the demand for energy is relatively high while the costs for electricity due to the usage of rechargeable batteries severely impacts households budget. Based on the above results, VisionFund Cambodia has been encourage to launch a product concept on renewable energy, especially for solar energy, in order to benefit the rural poor in Cambodia by improving living standards. However, the pilot market study results were not accurate enough to broaden its portfolio and provide the necessary financial services for solar lending OBJECTIVES OF THE STUDY The main objective of this study is to assess the target market characteristics in terms of market potential and client/future client preferences, and help VisionFund Cambodia understand how its abilities can be synchronised with market requirements. Additionally, the study aims to assess the feasibility of RE lending products and more closely estimate the renewable energy in particular solar energy lending potential. Furthermore, tailor-made recommendations in line with international best practices are to be incorporated. In order to build on the findings of the pilot study, and in accordance with the project proposal, Frankfurt School and VisionFund Cambodia agreed to focus on the following detailed-objectives: 1. To assess the level of demand on solar energy; 2. To identify alternative renewable energy solutions to meet the demand; 3. To obtain information on the development of suitable products; and 4. To be able to define criteria for selecting renewable energy suppliers. The recommendations of the study are will be used for the design, planning, and operational set-up of the RE lending product. This includes remarks and suggestions for the product development, business roll-out plan, and a professional marketing campaign ESSENTIAL CONCEPTS AND TERMONOLOGY The following list of main concepts and terminology are more closely defined as to supplement perceived contextual meaning with internationally adopted denotations: Target market Under the target market we understand all the eligible households in VisionFund Cambodia s 17 operating provinces: Prey Veng, Phnom Penh, Kandal, Takeo, Kampot, Kampong Speu, Koh Kong, Kampong Chhnang, Pursat, Battambang, Pailin, Banteay Meanchey, Oddar Meanchey, Siem Reap, Preah Vihear, Kampong Thom, and Kampong Cham. Renewable Energy (RE) Renewable energy is derived from resources that are naturally regenerative or are practically inexhaustible, such as biomass, heat (solar, geothermal, thermal gradient), moving water (hydro, tidal, and wave power), and wind energy. Municipal solid waste may also be considered a source of renewable (electrical and thermal) energy. 11 VisionFund. March 2008 Residential energy demand in rural Cambodia: an empirical study for Kampong Speu and Svay Rieng 11

15 Environmental Protection Environmental protection refers to any activity to maintain or restore the quality of environmental media through preventing the emission of pollutants or reducing the presence of polluting substances in environment media. It may consist of: o Changes in characteristics of goods and services; o Changes in consumption patterns; o Changes in production techniques; o Treatment or disposal of residuals in separate environmental protection facilities; o Recycling; and o Prevention of degradation of the landscape and ecosystems Sustainable Energy Sustainable energy is the provision of energy that meets the needs of the present without compromising the ability of future generations to meet their energy needs. With that in mind, sustainable energy development encompasses employment of two key components: renewable energy sources, such as hydroelectricity, solar energy, wind energy, wave power, geothermal energy, bioenergy, and tidal power. It typically also includes technologies that improve energy efficiency IDENTIFICATION OF THE METHODOLOGY The main objective of the study essentially involves qualitative assessment of two units, that is, (1) of the potential clients living in the target market region as well as (2) of the supply and demand of products. Appropriately, the approach and methodology employed in executing of constituent objectives differ to a moderate extent. The assessment of the target market characteristics in st terms of market potential and clients needs and preferences (1 main objective) employed direct market study estimation methods, and was based on the information gathered from the client surveying and the comprehensive secondary research via a desk study. The estimation of renewable energy lending potential with references to loan product design (2nd main objective) was based on information gathered from client surveying and a focused secondary research of rural household client data for target market regions. Identification of target market potential was performed through analysing demand and supply of RE loans in target market regions from both inside the organisation, and external evaluation including valuable customer feedback. Data analysis, including all market metric statistics, correlations, and future trends are based on the analysis through the statistical programme tool SPSS. THE DEMAND Within the scope of the study, the demand was understood as the effective desire of rural household clients for RE loans offered by VisionFund Cambodia. Additionally, RE loans were understood as to be used for investments made deliberately into renewable energy products and services. In order to identify the demand for RE products and services among rural household clients, the research included an overview of the market to obtain a general perspective using available published data (secondary research). To gain a better understanding of the potential clients, primary research on potential demand was performed using focus group questionnaire-type data collection 12

16 THE SUPPLY In order to identify the supply, Frankfurt School focused the study on the availability and usage of loans in general explicitly not on RE loans in particular. As preliminary research indicated, the supply of RE loans for rural households in Cambodia is still in its infancy. However, it is crucial to assess potential customers experience with financial services. Therefore, we strongly relied on information provided by VisionFund Cambodia and on information gained through the survey, as well as from some other secondary sources. THE SURVEY To collect relevant data the survey was divided into interviews and a questionnaire- which sought to find both quantitative aspects of the target population, such as demographic data, income and expenditures, and qualitative information such as perceptions and opinions. The survey data collection, besides its primary role to assess client s potential demand, served also as a catalyst in determining social patterns and demographic norms regarding both the supply and the demand for investments into renewable energy solutions. The questions that guided the study were organised in sections as follows12: General Information: This section included variables to characterize the age, level of literacy, personal status, number of household members, and way of obtaining and amount of income. Furthermore, it included variables on the basic conditions of living, employment situation, on the household expenditure, personal assets, and on credit experiences. Business Situation: These questions were about the personal business situation, the availability of supplies, and the seasonality of (the most successful) business. Questions on credit and savings for the business were also included. Agriculture: This section aims to gather more detailed information on agriculture, if applicable. Questions on land holdings and cultivation, on harvest, and expenditure of respective earnings were included. Livestock: Questions in this section focused on a more detailed overview on livestock, if applicable. It was asked for specific species of animals and additional income derived from livestock. Energy Consumption: This section, the core of the survey, was aimed at gaining factual information (e.g. what kinds of energy do you / your village use?), information on energy expenditure and energy suppliers. Furthermore, the section entails variables on knowledge and awareness of RE in particular. Rural Households Credit Interest: The last section of the questionnaire focuses on hypothetical questions to get an impression on the potential clients expectations and willingness to invest in RE solutions (open-end questions) LOCATION OF THE STUDY, SAMPLE, DATA COLLECTION LOCATION OF THE STUDY Frankfurt School and VisionFund agreed to conduct the study on a broad scale; i.e. in all 12 branches and its 17 operating provinces of VisionFund. This decision was made to allow significant outreach 12 A copy of the questionnaire can be found in annex 1 at the end of the document. 13

17 relevant for determination of supply and demand of the RE products and services. The complete list of the branches and its operating provinces are presented in the following table: Table 1: Branches and Operating Provinces NO NAME OF BRANCH ABBREVIATION NAME OF OPERATING PROVICE 1 Phnom Penh PP Phnom Penh 2 Kandal KDL Kandal 3 Takeo TKO 4 Kampong Speu KSC Takeo Kampot Kampong Speu Koh Kong 5 Kampong Chnang KCC Kampong Chnang 6 Pursat PUS Pursat 7 Battambong BTB 8 Banteay Meanchey BTM Battambong Pailin Bantey Meanchey Odor Meanchey 9 Siem Reap SRP Siem Reap 10 Preah Vihea PVH Preah Vihea 11 Kampong Thom KPT Kampong Thom 12 Kampong Cham KCM Kampong Cham Prey Veng The research method that involved individual/household surveying was performed in cooperation with VisionFund s Business Development Department, who at the same time, received support from a team of 13 accordingly-trained university students (1 surveyors and 2 team leaders, 5 of whom were female) to conduct the guided questionnaires/interviews. SAMPLE AND DATA COLLECTION The sample was designed to obtain statistically significant indicators to assess the demand for RE products and services. According to VisionFund s experience, in order to have confidential level of 95% and significant error of 5%, a sample size of 400 interviews was the minimum amount required. Therefore, it was agreed to distribute the sample for clients and no-clients according to the following criteria: Less developed region in terms of access to electricity High need of energy access 14

18 Less sample size in regions next to the country-borders due to the fact that they have easily and more access to energy High population index crossed with high level of agriculture, livestock, and or business As mentioned, data collection was carried out and organised by VisionFund and took place between March 21 to 26, The final sample size distribution per Branches is shown in the next table: Table 2: Sample Size Distribution per Brach BRANCH DISTRICT INTERVIEW DATE NUMBER OF RESPONDENTS CLIENTS NON- CLIENTS TOTAL PUS Kravanh 21-Mar SRP Srey Snorm 21-Mar KCC Samki Meanchey 22 to 23-Mar PVH Rovieng 21 to 22-Mar KCM Dambe 24 to 25-Mar TKO Koh Andeth 21 to 25-Mar KSC Thpong 21 to 25-Mar BTB Ratanak Mondul 21 to 25-Mar BTM Mongkol Borei 21 to 25-Mar KPT Prasat Balang 21 to 25-Mar KDL Ksach Kandal 21 to 25-Mar Total With assistance from VisionFund s staff - Client Service Officers (CSO), the random clients as well as non-clients were informed of interview appointment. If the appointed clients or non-clients missed the interview, the surveyor would randomly select other respondents to hit the target number of data. To incentivize respondent s participation, they were given a bar of soap as gift. And to support the process of data collection, 2 cars were rented in the target provinces having bigger size while in non-target province; staff motorbike of each province was used to assist surveyors to complete activities DATA ANALYSIS The questionnaire data analysis was completed through the SPSS statistical-analysis software13. The questionnaire was initially pre-coded to facilitate easier application and subsequent data analysis. A pre-coded excel sheet was sent to VisionFund Cambodia in order to fill-in the information found from the questionnaires. 13 SPSS is leading IBM-owned statistical software for descriptive and bivariate statistics. 15

19 3.6. ENCOUNTERED DIFFICULTIES In general, there were no major difficulties encountered. During data analysis stage, open questions presented minor problems in terms of summarising and clustering them. However, these difficulties only refer to time management and did not affect the quality of data. In addition, some inconsistencies within the answers could be identified and were eluded or excluded from further analysis. 4. MARKET ANALYSIS 4.1. FINANCIAL SECTOR IN CAMBODIA The banking and microfinance sector is one of the most developed sectors in Cambodia with 27 commercial banks, 6 specialized banks and 20 licensed microfinance institutions (MFIs). As end of 2009, the total assets in the banking system grew by 20% down from 24% in The loans to deposit ratio on average is 74.3% for commercial banks. The great success in the development of the sector is achieved through strict regulations imposed by the National Bank of Cambodia (NBC) which has the sole responsibility of supervising the Cambodian banking sector. NBC divides financial institutions into three categories: commercial banks, specialized banks, and MFIs. Graph 4: The Banking System in Cambodia NATIONAL BANK OF CAMBODIA 27 Commercial Banks 6 Specialized Banks Micro Finance Institutions 21 NBC Provincial Branches 5 Foreign Branch Banks 22 Locally incorporated 1 state owned 20 Licensed First Commercial Bank Krung Thai Bank May Bank Bank of India Phnom Penh Branch Saigon Thuong Tin Commercial Joint Stock Bank Foreign Trade Bank of Cambodia Advanced Bank of Asia Cambodia Asia Bank Canadia Bank Plc. Cambodian Commercial Bank Cambodia Mekong Bank Cambodian Public Bank Singapore Banking Corporation Union Commercial Bank Vattanac Bank ACLEDA Bank Plc ANZ Royal Bank Cambodia Camko Bank Shinhan Khmer Bank Bank for Investment and Development of Cambodia Plc Maruhan Japan Bank Khmer Union Bank Booyoung Khmer Bank Phnom Penh Commercial Bank OSK Indochina Bank Angkor Capital Bank Hwang DBS Commercial Bank Rural Development Bank 5 Privately owned PHSME Specialized Bank Best Specialized Bank First Investment Specialized Bank ANCO Specialized Bank Cambodian Development Specialized Bank 2 Representative Offices Standard Chartered Vietnam Bank for agriculture and rural development AMRET Co Ltd. Hatthakaksekar Tong Fang Microfinance Thaneakea Phum Cambodia SATHAPANA Seilanithih Angkor Microheranhvatho Kampuchea Vision Fund Cambodia CREDIT Co. Ltd. Prasac Micro Finance Institution Farmer Union Dev. Fund Cambodia Business Integrate in rural Development Maxima Mikroheranhvatho Intean Poalroath Rongroeurng First Finance Farmer Finance Ltd. Entean Akpevath Pracheachun Green Central Microfinance SAMIC Y C P Micro Finance Money Changer NGOs 26 Registered Unregistered about 60 NGOs Source: National Bank of Cambodia (2009): Annual Report Banking and Supervision Department As of end-2009, there were 20 licensed MFIs operating plus additional 26 registered rural credit NGOs providing microfinance services. Furthermore, around 60 NGO-MFIs, not licensed nor registered, provided informal financial services. According to the NBC, the number of MFI borrowers grew from 230,114 in 2008 to 262,952 (by 14%) in Compared to 2008, the portfolio and number of MFI-borrowers increased by 9% and 8%, respectively. 16

20 Table 3: Performance of the microfinance sector (20 registered MFIs) Total Assets (Mio KHR) 727,995 1,362,372 1,525,818 Assets growth in % Total Loans (Mio KHR) 617,271 1,130,585 1,244,970 Number of borrowers 624, , ,412 Total Deposits (Mio KHR) 21,210 22,281 39,628 Number of Depositors 147, , ,959 Number of staff 3,504 5,148 6,330 Number of branches 882 1,105 1,315 Source: National Bank of Cambodia, Supervision Reports VISION FUND CAMBODIA VisionFund Cambodia14 is a licensed medium-sized MFI operating in Cambodia with a mission to provide financial services to help the poor liberate themselves from poverty. It provides financial (loan and savings, insurance, mobile banking) and non-financial (client education and reinforcement) services. As of end-2009, it served 98,777 families with a portfolio of approx. USD 21,314,258 with loans compared to a portfolio of USD 17,052,891 at year-end-2008 and USD 10,700,478 at year-end Despite this sharp increase in portfolio, VisionFund managed to maintain a low portfolio at risk (PAR > 30 days). With the exception of the year 2009 with 3.4% it PAR remained well below 1%. The average loan size is USD 284. VisionFund offers three lending methodologies: Table 4: VisionFund Cambodia Loan Methodology COMMUNITY BANK SOLIDARITY GROUP INDIVIDUAL LOAN Loan size (USD) ,000 1,001-10,000 Term (months) Interest rate p.m. (%) Poverty level poorest/poor not so poor vulnerable non-poor Source: VisionFund Cambodia Annual Reports 14 The information on VisionFund Cambodia is derived from the Annual Report 2009 and a presentation at VisionFund Cambodia in February

21 Graph 5: Methodology by Portfolio Size Graph 6: Methodology by Client Number Solidarity Group; 12% Individual Lending; 36% Solidarity Group; Individual Lending; 7% 5% S Community Bank; 52% Source: VisionFund Cambodia Annual Reports Community Bank; 88% Table 5: VisionFund Cambodia Key Financial Data 12/ / / /2011 Number of active borrowers % of women borrowers 78,092 98, , , Number of provinces Number of districts Total staff Loan portfolio (USD) 17,052,891 21,314,258 30,017,044 30,035,538 Average portfolio per borrower (USD) PAR > 30 days (%) Total assets (USD) 23,073,394 26,531,016 36,681,968 36,658,687 Total equities 4,619,380 7,074,927 9,310,378 9,391,905 OSS (%) FSS (%) RoA (%) Source: VisionFund Cambodia Annual Reports 4.2. SUPPLY OF RE LOANS IN CAMBODIA The overview of Cambodia s financial market certainly presents evidence of underserved niche for RE finance products anud services. The assessment reveals the existence of a potential to target and create new segmented financing of RE investments. Market penetration is very low because of a lack of competition and general reluctance to disburse RE designated loans. However, the main reason for low performance in building renewable energy investment pipeline still lays in general lack of 18

22 awareness and lack of knowledge of the advantages of alternative energy forms for rural households. According to the secondary information, we found out that there are two relevant MFIs worth mentioning (AMRET and PRASAC) because offer credit/loans for RE products, especially for biodigesters. These are loans designed for individuals intending to improve their living standard through building bio-digester plants which can reduce expenses within household (produce gas to cook and light) and improving better environment (reduce cutting trees for firewood or charcoal). Both MFIs received funding from the European Union. The features of these loan characteristics are presented in the next table: Table 6: RE loans supply AMRET PRASAC Loan Terms: Loan Terms: o A very low interest rate (1,2%) o Interest rate is 1.2% per month o Loan size from USD o Loan size from USD o Collateral: Loan term: 3 24 months o Loan term from 4-24 months o Real state: House or land title Repayment: Collateral: o Real estate: House or land title o o Receive 150 USD free from the National Biodigester Programme (NBP) to repay loan Borrow and repay funds at the nearest Amret branch or at the clients house Repayment: o o Receive 150 USD free from the National Biodigester Programme (NBP) to repay loan Flexible repayment method o Fees: o Flexible repayment method and loan term that suit clients business requirements No loan fees charged Pre-conditions: Fees: o No loan fees charged Pre-conditions: o o Have a legal business with real profitability Be able to collect 20 kg of the animal dung per day o o Meet condition from NBP officer: have livestock and proper place Age from 18 to 70 years old o o Have proper place for making a biogas pant Be a permanent resident in the village o o Have a business If customer do not fulfil agreements, then change of contract to consumption loan 2,5 to 3% interest Customers benefits: o o Age from 18 to 65 years old If customer do not fulfil agreements, then change of contract to consumption loan 2,7% 19

23 o Save money in average 12 USD/m o Help to protect the environment interest Customers benefits: o Spare time instead of collecting firewood o Opportunity to increase social activities. Source: Own source There are other projects or programs which are related to the RE activities through particular NGOs, cooperatives, international organisation, among others, which are important to mention in the sense of analysing external factors to start a RE credit/loan products. Some of them who performed feasibility studies or are performing (pilot) projects or initiatives are: CMK (Crédit Mutuel Kampuchea), funded by the French Development Agency, gives credit for solar already but has no specific loan product for this. It has a MoU with the supplier Kamworks. UNDP-Cambodia manages the GEF Small Grants Programme, which gives grants to communitybased organisations and NGOs up to 50,000 USD. The Swedish International Development Cooperation Agency (SIDA) works at policy level about climate change topics in Cambodia. The World Bank Group is also present in Cambodia and gathering information about shortages of reliable power and reducing electricity, improving rural electricity access, heavy use of biomass energy particularly wood fuel. Moreover, WB has signed a contract with Kamworks and a Chinese Enterprise to supervise installation, to collect payments and to maintain 12,000 SHS for 500 villages in 7 regions of Cambodia (MIME/REF Project). It will start end of July for 1.5 years. The Netherlands Development Organisation (SNV) has been present since 2005 when the National Biodigester Programme (NBP) commenced and now operates in eight southeast provinces, which consists in giving subsidy to farmers through ACLEDA Bank, with whom the NBP has set up a subsidy fund distribution system. Up to this period of time15, apart from VisionFund (MFI), CMK (Cooperative), Yejj Solar (NGO), International Solar Solutions (Enterprise/Supplier), Khmer Solar (Enterprise/Supplier), and Kamworks (Enterprise/Supplier) there are no other institutions intending to enter (or already on the business) the solar finance market, i.e. that will commence specialized solar financing POTENCIAL DEMAND FOR RE MICROFINANCE LOANS IN CAMBODIA DETERMINANTS OF POTENTIAL DEMAND General experience in developing countries entails tight correlation between projected potential number of future clients and a combination of demographic characteristics, national/local policy & regulations and even climate characteristics. Chapter 2 of this report give detailed information about each of these influencing factors. DEMOGRAPHIC CHARACTERISTICS Chapter 2.2 describes important demographic data and their influence on the potential demand. According to the last official estimates from 2009, Cambodia has a population of approximately 14,8 15 June

24 million inhabitants, with and average density of 75 people per square kilometre. The highest population density is in the regions in and around Kampong Cham, Phnom Penh in the southeast and Battanbang and Siem Reap in the northwest. The average growth rate over the last five years has been 1.6%. As presented in Graph 2, more than 75% of the population is less than 50 years, which also gives information about working population development. Even the UNCDF estimates that between 2009 and 2013 annually 300,000 Cambodians will reach the age of 15 and seek for employment. This trend in the long run has positive influences on demand, and can at present be leveraged by higher household solar equipment purchase due to the economic and development impact and the need of energy access. The World Bank classifies Cambodia as a low-income economy (GNI of 995 USD or less), which have an estimated annual per capita of about 666,8 USD in GDP has been growing since the last years due to garment export expansion, growth in the construction sector and rise in tourism, which gives a positive influence on demand. However, this growth has been mainly urban-focused with limits to the rural population, giving us a negative impact on the potential demand for RE microfinance loans. ENERGY PRICES AND PUBLIC INCENTIVES Energy prices and energy regulatory instruments are of highest importance in deciding the potential for RE MFI lending. The primary rationale for investments into RE products and services are deduced from associated monetary savings. Electricity and other energy prices are given in section , however accordingly to the information found, Cambodia s electricity prices are one of the highest in the world. Not only that, but due to the high prices for fuel and other energy sources, traditional biomass accounts for 90% of the cooking energy, resulting in one of the world s highest deforestation rate per year. Moreover, since more than 90% of the population living in rural areas has no access to electricity grid and does not own individual generating units. Most of these households use automobile batteries for a high cost. On the other hand, public incentives may have a negative impact on the potential demand for RE microfinance loans in the sense that such public programs offer grants to private rural operators or rural electricity enterprises in order to assist rural population to get access to electricity, like the example from the World Bank through its GEF. The incentive, however, does not go directly to the end user and this might take a long process until the actual use of the benefit. Therefore, it might have a positive impact on the potential demand for RE microfinance loans. However, The World Bank and the Ministry of Energy (MIME/REF project) is giving funds to a supplier (Kamworks and a Chinese Enterprise) in order to supply, deliver and install 12,000 SHS to 7 provinces in Cambodia. This public incentive have of course a negative impact on the potential demand for solar loans, nonetheless it might play a positive role when the non-benefit household or the non-benefit village might be eager to obtain a mentioned solar technology, and they may go for a loan. As a result, energy prices and public incentives do play a very important role and although in the long run the investment into RE equipment (like SHS) into energy lighting pays off, the immediate time value of money has higher importance than future light benefits. This important result must be calculated into decisions about RE loan product. CLIMATE / SOLAR INTENSITY In general, Cambodian climate including solar intensity- should be ideal for the RE equipment proposed, that is the solar technology system. According to the information provided in section 2.1.2, the average sunshine duration during the year is 6-9 hours per day. However, the appropriate position of the equipment is very important because where there is not enough direct sunlight, the battery will not be charged and the usable time will be reduced. Another important point to be taken into consideration is the seasonality between dry and rainy seasons. On cloudy days, for 21

25 instance, power requirement is high and the cost of solar technology system might be higher and the equipment may not be affordable to the low income segment. As a result, the determination of climate conditions is essential when looking on the potential demand for RE microfinance loans, especially for those areas with limited sun light RESULTS OF THE QUESTIONNAIRE The survey team conducted 401 interviews in different provinces of Cambodia, ensuring a 95% significance with 5% error. Among the survey population sample, 327 were women and 74 men. (see Fehler! Verweisquelle konnte nicht gefunden werden.). It was observed that 31.92% of total rural poor interviewed are illiterate, which is interesting in comparison with the country-wide average statistics of 20% Table 7: Gender and Education from the interviews EDUCATION (FROM THE INTERVIEWEE) TOTAL ILLITERATE PRIMARY SCHOOL SECONDARY SCHOOL UNIVERSITY GENDER MALE FEMALE Total Graph 7: Age of Interviewees Graph 8: Houshold Status 2,2% 1% 23,7% 73,1% Chief of the House Wife/Husband Daughter Mother 22

26 On average, interviewees are years old (stand. devt: , one invalid answer). Almost a quarter of them consider themselves as chief of the household and almost three quarters as wife or husband. Therefore, we can assume that 96.8% of interviewees have a high enough status within their respective household to be involved in decision making processes. Only 9.5% declared that they do not have regular employment (5 out of 401 answered that they are unemployed or live from subsistence economy). Fehler! Verweisquelle konnte nicht gefunden werden. indicates that also the vast majority of the 96.0% self-employed interviewed poor in rural Cambodia works on a regular basis. Table 8: (Regular) Employment IRREGULAR EMPLOYMENT TOTAL YES NO EMPLOYMENT EMPLOYED SELF EMPLOYED UNEMPLOYED SUBSISTENCE Total Graph 9: Sectors of Employment (in %) The survey shows that it is common for Cambodia s rural population to be involved in 4,5 20 different kind of economic sectors to obtain income. Agriculture is with 89% by far the most frequent answer, followed by trade and services. This result matches the statement in chapter 3.3 on 23,2 economy which says that GDP growth is mainly due to garment industry, 89 construction and tourism and therefore mainly affects the urban and not rural areas. That is the main reason why 85.2% of interviewees obtain A griculture T rade Services Others their income on a seasonal basis and strongly depend on their crops. However, 51.1% complement their seasonal income: 23.9% of total gain additional income on a daily, 2.7% on a weekly and 11.7% on a monthly basis. A total of 32.2% gain income on a daily, 5.2% on a weekly and 16.9% on a monthly basis (only 3 answered that they neither receive income on a daily, weekly, monthly nor seasonal basis). A further 29.2% have income from animal production. This indicates that income is to some extend available for more than half of the interviewed people on a regular basis. Of the 48.6% interviewed rural households with only seasonal income 90.2% earn more than USD 10 (KHR 40,100) on a monthly basis. Altogether, 85.3% of total interviewed households declared that they obtain seasonal income, of which 38.9% do not have enough money for food for their families. This percentage is significantly higher compared to 23

27 income on a daily (27.9%), weekly (28.6%) or monthly (25.0%) basis (see Fehler! Verweisquelle konnte nicht gefunden werden.). 24

28 Table 9: ENOUGH FOOD Income and Access to Food SEASONAL INCOME YES NO TOTAL YES NO ENOUGH FOOD DAILY INCOME YES NO TOTAL YES NO Total Total ENOUGH FOOD WEEKLY INCOME YES NO TOTAL YES NO Total ENOUGH FOOD MONTHLY INCOME YES NO TOTAL YES NO Total Thus, seasonality is a major issue for the rural population in Cambodia. That partly explains why 36.9% of total interviewees do not get enough food and 35.2% have not enough money for cloths for their families. Though as the Table 10 and 1

29 indicate, significant regional differences are measurable: Especially in the provinces of Kampong Chnang and Preah Vihea only about 30% of interviewed households has enough money to get food for their families. The same provinces rank with 43.4% and 35.2%, respectively, least in availability of money for clothes. On the contrary, in the provinces of Kandal (100%), Battambong (94.1%), Kampong Thom (94.1%) and Kampong Speu (94.1%) the population seems to have relatively good access to food. Therefore, it is possible to speculate that the survey shows no correlation between geographic direction or landscape and basic living conditions. 2

30 Table 10 Basic Living Conditions per Province NAME OF PROVINCE BTB BTM KCC KCM KDL KPT KSC PUS PVH SRP TKO TOTAL ENOUGH FOOD YES NO N % 94,1 87,5 30,2 56,8 100,0 94,1 94,1 83,0 29,6 63,5 88,2 63,1 N % 5,9 12,5 69,8 43,2 0,0 5,9 5,9 17,0 70,4 36,5 11,8 36,9 Total N % NAME OF PROVINCE BTB BTM KCC KCM KDL KPT KSC PUS PVH SRP TKO TOTAL SUFFICIEN T MONEY FOR CLOTHES YES NO N % ,5 43,4 59,1 94,1 82,4 94,1 81,1 35, ,8 N % 0 12,5 56,6 40,9 5,9 17,6 5,9 18,9 64,8 44,2 0 35,2 Total N % Graph 10 Position of family income during last six months The basic living conditions of rural households are, as shown above, significantly dependent on seasonal availability of income. However, almost half of interviewees answered that during the last six months their income stayed the same. The other half is split almost equally between an increase and a decrease in income. The 3

31 Table 11 Position of family income during last six months illustrates the regional differences in development of family income. Especially the province of Preah Vihea experienced a considerable decrease in average income, whereas in the province of Kampong Thom 41.2% of households income increased 27% 1% 25% 47% increased stayed the same decreased worsened 4

32 Table 11 Position of family income during last six months NAME OF PROVINCE BTB BTM KCC KCM KDL KPT KSC PUS PVH SRP TKO TOTAL INCREASED N % 17,6 37,5 11,3 23,9 23,5 41,2 35,3 39,6 13,0 28,8 17,6 24,7 STAYED THE SAME N ,9 56,3 58,5 45,5 76,5 47,1 35,3 39,6 42,6 34,6 70,6 47,4 DECREASED ,4 6,3 22,6 30,7,0 11,8 29,4 20,8 44,4 34,6 11,8 26,7 WORSENED % 0 0 7, ,9 0 1,2 Total N % % 23% 9% up to USD 100 USD % USD m ore than USD 500 Graph 11 Amount of Total Credit per Household Of total interviewed households 71.6% have ever applied for credit and 34.9% have at least one credit at the moment (of which 80.7% currently have one, 17.5% two and 4.4% three credits). Almost half of them (45%; see Graph 11 Amount of Total Credit per Household; for detailed figures see annex 3) have total credit ranging between USD 100 and USD 300 that is 15.7% of total interviewed households. Only three interviewees answered that they have problems to pay it back16. With 62.6% the majority of people indicated that the winter months17 (November to February) are best and 59.1% answered that the summer (June to October) is worst for their business. Accordingly, 54.9% are able to save some money in the winter time. 16 The total number of households with credit at the moment is of limited value due to the sample selection of roughly 50% VisionFund clients. Nevertheless, the amount of total credit per households allows drawing conclusions. 17 Winter=cool/dry (Nov.-Feb), Spring=hot/dry (Mar.-May), Summer=hot/rainy (Jun.-Aug.), Autumn=cool/rainy 5

33 Frequency Frequency FEASIBILITY STUDY ON ACCESS TO FINANCING FOR RE APPLIANCE FOR RURAL POOR IN CAMBODIA Graph 12 Seasonal Distribution of Business Activity B est fo r B usiness Wo rst fo r B usiness Able to Save Money W int er Spring Summer Aut umn Graph 13 Hectares of land (holdings and cultivated) Mean value: 2.54 Stand.-devt.: N=401 Mean value: 1.97 Stand.-devt.: 1.92 N=401 Hectares of land holdings Hectares of land cultivated Land holding amount on average 2.54 hectares of which 1.97 hectares are cultivated (see Graph 13 Hectares of land (holdings and cultivated). Most cultivated crop is rice; furthermore, soy beans, cashews, potatoes and other vegetables are grown. 90.3% own their property for agriculture. Seasonal differences are expressed by the result that 63.1% experienced a change in production compared to the last season 20% of total interviewees answered that production decreased and 38.9% that it increased (about 4% did not specify). Though corresponding with the change in production, mixed results were also achieved with regard to market price development in recent years for agricultural products. Cross-checking with the provinces shows that both change in production (Table 12) and market price development (Fehler! Verweisquelle konnte nicht gefunden werden.) can be attributed to geographical location: 6

34 Table 12: Change in Agricultural Production per Province NAME OF PROVINCE BTB BTM KCC KCM KDL KPT KSC PUS PVH SRP TKO TOTAL CHANGE IN PRODUCTI ON YES NO N % 82,4 57,1 41,2 73,8 64,7 64,7 70,6 74,4 45,8 96,0 88,2 68,2 N % 17,6 42,9 58,8 26,3 35,3 35,3 29,4 25,6 54,2 4,0 11,8 31,8 TOTAL N % Table 13: Market Price Changes for Agricultural Products in the last 2 years per Province NAME OF PROVINCE BTB BTM KCC KCM KDL KPT KSC PUS PVH SRP TKO TOTAL N INCREAS ED % 94,1 6,3 11,3 64,8 29,4 64,7 17,6 24,5 22,2 30,8 41,2 36,7 MARKET PRICE CHANGE D LAST TWO YEARS STAYED THE SAME DECREA SED N ,9 12,5 28,3 1,1 64,7 17,6 41,2 32,1 22,2 9,6 58,8 20, ,8 28,3 5,7 5,9 11,8 35,3 18,9 31,5 51,9 0 23,4 WORSEN ED % 0 12,5 32,1 28,4 0 5,9 5,9 24,5 24,1 7,7 0 19,0 TOTAL N % Access to electricity is a key issue for rural households in Cambodia. According to the information analysed in Table 1418, 121 households are spending money for electricity but do not have enough food for their families. 27% of them even spend more than USD 5 per month compared to the average of more than USD10 monthly income. Furthermore, the frequency distribution of the amount paid for electricity in relation to availability of food for the families shows only a low correlation. This means that electricity is of high importance for rural Cambodians. Even though people cannot afford enough food, they still spend money on electricity. 18 For detailed figures per provinces, see annex 3. 7

35 Table 14 Availability of Enough Food and Amount paid for Electricity/Month AMOUNT FOR ELECTRICITY/MONTH DO NOT SPEND MONEY FOR ENERGY LESS THAN USD 2 USD 2-5 USD 5-10 MORE THAN USD 10 TOTAL ENOUGH FOOD YES NO N % 19 24,9 36,4 13 6,7 100 N % 18,2 37, ,2 4,7 100 TOTAL N % 18,7 29,7 32,9 12, Graph 14 Amount spend for Electricity/month per Province19 The provinces are arranged in ascending order according to where people spend most for electricity with the province of BTM being the highest. 19 For detailed figures on the amount spent for electricity per month per province refer to the table in annex 3. 8

36 Candles Generator Batteries Kerosene RE Other FEASIBILITY STUDY ON ACCESS TO FINANCING FOR RE APPLIANCE FOR RURAL POOR IN CAMBODIA Graph 15 Kinds of Energy Offered 100% 90% 80% 70% 60% 50% 40% 30% 20% 10% 0% no yes Over 50% of the interviewees answered that candles, batteries and kerosene are available by their energy providers/suppliers and only 0.5% answered that RE appliances are available (Graph 15). Also in terms of actual usage of energy generating systems, RE appliances are not common. The prevailing usage of batteries and kerosene (as Graph 16 indicates) explains the relatively high costs for electricity. However, prices for these kinds are subject to fluctuations in recent years they steadily increased. In addition, agricultural productivity and income (main sector of employment; see above) strongly depend on the seasons. Funding gaps for fossil energies are therewith likely. Graph 16 Energy Generating Systems in Use (in %, total and per Province) yes no D ung C o al Fire wood ( bio ) Diesel generator B io g as LPG D end ro g asif ier M icro - hydro Solar Cooking SHS C and les B at t ery Kero sene village - total yes no D ung C o al Fire wood ( bio ) Diesel generator B io g as LPG D end ro g asif ier M icro - hydro Solar Cooking SHS C and les B at t ery Kero sene own household - total Firewood is used in every single village close to 100% (see graphs in Annex 3). People collect it and use it as a source for heating and cooking. Since they do not pay for firewood, people s awareness of RE in comparison to other frequently used sources like batteries and kerosene is a key issue. Households need to be confident that their needs are sufficiently met. Therefore, they need to know the benefits of RE. Though, the survey showed that of total interviewed households only 38.4% heard about renewable energies. Fehler! Verweisquelle konnte nicht gefunden werden. illustrates their awareness of different kinds of RE: 9

37 Graph 17 Awareness of Renewable Energie Known types of RE Known types of RE 100% 80% 60% 40% 20% no yes 100% 80% 60% 40% 20% 0% Solar Wind Hydro Biogas 0% Solar Wind Hydro Biogas The awareness of renewable energy is still on a low level. Only about a third of total interviewed people know solar energy (36.2% heard of it) and 18.0% know somebody who is using it. The types of RE appliances which people think are most suitable for their own village corresponds almost equally with the type they know. Another indicator of a general lack of awareness is the fact that out of the people who claim to know solar energy, only 53.4% explicitly attributed its eligibility to sunshine. Accordingly, only 15.2% of households which heard about RE ever tried to get access to these kinds of alternative energy (equals 5.7% of total interviewed households). Despite the lack of awareness of RE in general, 68.3% of total interviewed households answered that they would make use of a credit for solar energy (though only 36.2% heard of solar and only 38.4% of RE; see Table 15: Heard about RE and willing to take a credit for solar. Table 15: Heard about RE and willing to take a credit for solar HEARD ABOUT RE TOTAL YES NO WOULD MAKE USE OF CREDIT FOR SOLAR YES NO TOTAL Remarkably, the highest percentage of people willing to make use of credit for solar can be found among those who do not spend money for energy (85.3%, see Table 16: Amount spent for electricity per month and willingness to take a credit for solar energy). Furthermore, 78.8% answered that they prefer solar if offered as household lighting on a loan payment. Table 16: Amount spent for electricity per month and willingness to take a credit for solar energy WOULD MAKE USE OF CREDIT FOR SOLAR TOTAL YES NO 10

38 AMOUNT FOR ELECTRICITY /MONTH DO NOT SPEND MONEY FOR ENERGY LESS THAN USD USD USD MORE THAN USD TOTAL 274 (68,3%) 127 (31,7%) 401 (100%) Out of the 140 (34.9%) households who have at least one credit at the moment, only 15.7% pay more than USD 5 for electricity per month. In total only 18.7% pay more than USD 5 for electricity (see Graph 18, for detailed figures see table in annex 3). Graph 18 shows a detailed distribution of the amount spent: Graph 18 Amount Spend for Electricity and Open Credit credit at the moment 10% 31% 6% no credit at the moment 14% 34% 19% total 30% 6% 6% 21% 32% 35% 11% 13% 32% no money <USD 2 USD 2-5 USD 5-10 >USD 10 no money <USD 2 USD 2-5 USD 5-10 >USD 10 no money <USD 2 USD 2-5 USD 5-10 >USD 10 In order to provide RE appliances on a loan basis in Cambodia, the monthly repayment should match the amount households spent so far for energy sources. It is assumed that people awareness of RE ultimately decide regarding its affordability. Concerning up-front payment and as shown in Graph 19, Graph 20, and Graph 21, of total interviewees, 58.85% answered that they could pay USD 100 or more up front (37.16% USD 200 or more). Only 37.40% answered that they could pay USD 50 or less up front (including nonrespondents). Only 59.10% (including non-respondents) indicated that they could pay less than USD 10 per month for RE appliances % of total interviewees envisions more than one year to pay back the RE loan (7.23% did not answer this question). With 79.55% the vast majority of respondents envisions less than one year for repayments: 2.99% three months or less; 15.96% four to six months; 2.00% seven to nine months; 58.60% ten to twelve months, matching the current payment term of VisionFund Cambodia. Graph 19 Affordable up front payment for RE appliances (in USD) 11

39 months affordable monthly payment Affordable up front payment FEASIBILITY STUDY ON ACCESS TO FINANCING FOR RE APPLIANCE FOR RURAL POOR IN CAMBODIA No of Respondents Average: USD 188 Graph 20 Affordable Monthly Repayment for RE appliances (in USD) 50,00 40,00 30,00 20,00 10,00 0, No of respondents Average: USD 16 Graph 21 Envisioned Duration of Repayment for RE loan (in months) No of respondents Average: 11 months 12

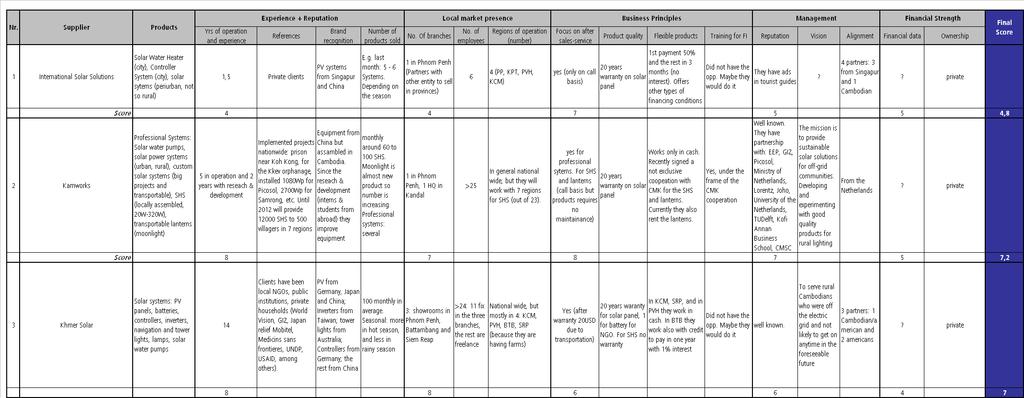

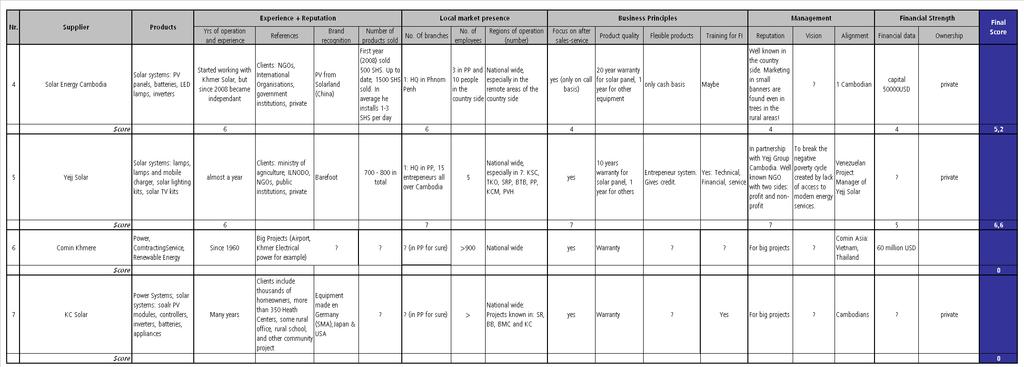

40 ESTIMATES OF POTENTIAL DEMAND From the data provided by VisionFund Cambodia and data on the microfinance sector the following position can be revealed that: Registered MFIs 20 Total MFI branches 1,315 Total lending USD million Number of borrowers VisionFund portfolio VisionFund borrowers 871,412 (5.88% of population) USD 2,131,424 (69.7% of total MFI lending) 98,777 (11.33% of total MFI borrowers) This reveals that the average borrowings of VisionFund s customers are of higher value compared to other MFIs. This might be an indication that these borrowers are of higher income levels. According to theory and praxis, several methods can be applied to estimate the potential demand for RE microfinance products and services, making use of the information outlined above. For the purpose of this study, the consultant will use some qualitative assessment of potential demand. From the information obtained, the consultant found out that from December 2009 until February 2010 (in three months) one MFI who is providing Biodigester Loans gained 2840 clients with 1 606,130 USD disbursed. Giving a conservative estimation (in comparison with the biodigesters) and crosschecking with the products sold by the suppliers, the consultant is assuming that in three months VisionFund after successful implementation will provide 1000 solar technology systems loans. Using this result, if we multiply an average of USD per credit (for example), we obtain a roughly loan portfolio of USD 200, ,000 in three months, giving an excellent argument to start the new RE product MARKET AVAILABLE PRODUCTS AND SERVICES In Cambodia there are several suitable solar products available for rural households. Financial services are however, a major gap. Since the recommendation is going into the direction of the RE: solar, it is essential to mention that these technologies are mainly provided on a cash basis with too high upfront costs for rural poor, or sometimes they are donated (but in a small scale), or subsidised and there is no external assistance to follow up on the equipment. Although there are several suppliers companies for solar technology systems in Cambodia, the consultant has identified that there are seven main suppliers: Comin Khmere, Kamworks Ltd., Khmer Solar Ltd., Solar Energy Cambodia Ltd., International Solar Solutions, KC Solar, and Yejj Solar. For the purpose of this study, Frankfurt School will briefly describe the solar products of Kamworks Ltd. and Yejj Solar20: 20 Note: This selection is not meant to be a recommendation on suppliers. It was rather due to the availability of data and should be regarded as examples. 13

41 The solar technology provided by Kamworks Ltd. is developed as a complete product of solar technology system, i.e. all components are included in one box21. For the end-user it is therewith an easy-to-use appliance. Initially, the solar technology systems were sold (incl. installation, battery and a one year warranty) for: I. medium SHS (DC, 40Wp-48Ah): USD 465, II. large SHS (DC, 78Wp-96Ah): USD 870; III. large + SHS (AC, 78Wp-96Ah): USD 990. Kamworks chose an innovative approach with offering USD 15 cash back for those people participating in one day solar technology system training. However, there were problems in the pilot phase with matching the energy consumption of families with the ability of the system. Often families appliances needed far more electricity than the SHS could provide. Moreover, it is worth to mention that Kamworks has recently signed a non-exclusive MoU with CMK (cooperative with gives microcredit), which means that this specific supplier has already experience dealing with such MoUs. Yejj Solar provides solar desk lamps and home lighting kits. Their prices range from USD 22 to USD 29 and USD 99 to USD 289, respectively (batteries not included). The lighting kits or SHS are plug&play systems which do not require any major installation. Five SHS are offered: I. 2.5W panel feeding 12V 2.8Ah battery, 2XLED matrix II. 5W panel feeding 12V 5Ah battery, 4XLED matrix III. 10W panel feeding 12V 17Ah battery, 2X LED matrix and 2 fluorescent tubes IV. 15W panel feeding 12V 26Ah battery, 2XLED matrix and 2 fluorescent tubes V. 15W panel feeding 12V 26 Ah battery, 4XLED tubes Yejj is already working on microfinancing for solar systems. Together with VisionFund Cambodia Yejj they conducted the pilot study mentioned previously. Furthermore, they are developing an approach for Solar Energy Micro-Entrepreneurs, i.e. to create a network of microentrepreneurs able to sell and maintain solar lighting solutions to rural areas. For that reason, they are aiming to partner with NGOs and MFIs. The lessons learned are that people s expectations and the capacity of the solar technology system need to be matched. Education and awareness raising are the key issues. Furthermore, replacement parts should be standardized. The regular warranty is one year and after that customers need to maintain the system (change bulbs, batteries etc) on their own. Small monetary incentives to train customers on solar technology system potentially increases acceptance and trust and might be considered by VisionFund in cooperation with the yet to be identified supplier. 5. LOAN PRODUCT FORMATION RECOMMENDATIONS As initially mentioned, one of the detailed-objectives of this study is to obtain information on the development of suitable products. Besides aiming to improve the client s access to innovative and market-tailored RE financial services, VisionFund further seeks to position itself as an institution socially responsible towards community and the environment. However, in order to maintain a sustainable RE lending portfolio Frankfurt School recommends that VisionFund keeps on taking the 21 The information on Kamworks SHSs are derived from: van Diessen, Tom (2008): Design of a Solar Home System for Rural Cambodia. Graduation Report. 14

42 operational self-sufficiency (OSS)22 into account. Furthermore, VisionFund should keep record of the financial self-sufficiency (FSS)23 in the long-term as well. Since RE lending (for SOLAR TECHNOLOGY SYSTEM) would increasingly focus on higher credits, the costs of capital (included in the adjusted operating expenses) are to be considered. In line with VisionFund s objective, Frankfurt School will make some suggestions regarding loan structure based on general knowledge of VisionFund s business policy and structure, and based on internationally best practices in RE lending. The individual determinants of loan product recommendation are furthermore the product of demographic (economic), climate and solar intensity, and legal (energy policies and regulations) characteristics of the market, carefully analysed existing market supply and demand of financial services, and market available RE products and services ANALYSIS OF BEST PRACTICES International development cooperation has in recent year increasingly focused on diffusion of sustainable energy solutions and clean energy technology. In most cases green house gas mitigation is the main environmental objective, further expanded to poverty alleviation and improvement of life-quality. However, economic objectives like cost-benefit relations play a determining role and sometimes even above the environmental and social objectives. As best practice can be considered a middle point of a combination of these three objectives: Environmental objectives Social objectives Economic objectives Most international financial institutions have set up facilities for financing renewable energy and energy efficiency investment measures. As a result, local intermediate banks and microfinance institutions worldwide increasingly offer loan products to individual/group private clients and to MSME for small RE/EE machinery/equipment. Hence, the finance of RE/EE systems has become an integrated part of many financial institutions daily lending business, also in the developing world and in the emerging markets. Experiences from our own and from similar projects will be the basis for best practices analysis. For example, in the context of our UNEP Collaboration Centre on Climate & Sustainable Energy Finance Frankfurt School manages the FACET programme which will implement three country programmes (in Southeast Asia) aimed at mobilizing end-user financing for small scale technologies such as solar systems and high efficiency appliances. The strategy will be to first identify technology/market opportunities, and for the best three to undertake consultation processes to identify support schemes for initiating bank lending. Each scheme will combine technical assistance with temporary financial support mechanisms, which will incentive banks to build up initial loan portfolios. 22 OSS=Operating Income/ Total Operating Costs 23 FSS=Operating Income/ Adjusted Operating Expenses 15