IFC - ESMAP - RENEWABLE ENERGY TRAINING PROGRAM. Wind Module. I. Technology Overview, Market Analysis and Economics

|

|

|

- Ronald Fleming

- 6 years ago

- Views:

Transcription

1 IFC - ESMAP - RENEWABLE ENERGY TRAINING PROGRAM Wind Module I. Technology Overview, Market Analysis and Economics Washington DC, June 16th

2 Index Wind Technology Overview, Market Analysis and Economics Introduction and Technology Overview Market Analysis and Perspectives Support Schemes and Price Forecasting Grid Integration and System Flexibility Challenges and Competitiveness 2 2

3 Wind Power Generation Wind power generation: Conversion of wind energy into electricity using wind turbines Max Power output for a wind speed: W m 1 3 A v 2 C p (, ) = 1,225 kg/m 3 density of the air A= swept Area V= wind Speed Cp= Power Coefficient 3 3

4 Wind - Power Coefficient Power Coefficient: Efficiency of a wind turbine transforming wind power into electricity Betz Limit: Maximum Power Coefficient of an ideal wind turbine For commercial turbines, Cp is typically between 40-50% 4

5 Wind - Weibull Distribution Wind speeds can be modeled using the Weibull Distribution. This function represents how often winds of different speeds will be observed at a location with a certain average wind speed. The shape of the Weibull Distribution depends on a parameter called Shape. In Northern Europe and most other locations around the world the value of Shape is approximately 2, then the distribution is named Rayleigh Distribution. 5 5

6 Wind - Capacity factor Weibull Distribution of Wind Speeds for a site with an average wind speed of 7m/s. It demonstrates visually how low and moderate winds are very common, and that strong gales are relatively rare. It is used to work out the number of hours that a certain wind speeds are likely to be recorded and the likely total energy output of a WT a year. Capacity factor is the ratio of the actual energy produced in a given period, to the hypothetical maximum possible, i.e. running full time at rated power. i.e. Spain Wind sector c.f % 6 6

7 Wind - Resource maps (1) Europe Onshore Europe Offshore Source: Risø National Laboratory, Roskilde, Denmark 7 7

8 Wind - Resource maps (2) China Onshore & Offshore 8 8

9 Wind - Resource maps (3) US Onshore & Offshore 9 9

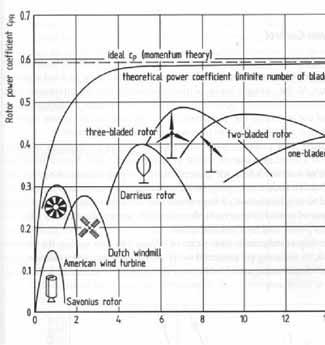

10 Wind - Turbine types Darrieus Savonius-Rotor H-Type One, two and three blades turbines Horizontal Axis Vertical Axis

11 Wind - Turbine size evolution Land-based supply is now dominated by turbines in the 1.5 and 3 MW range REpower, exploiting reserve capacity in design margins, has up-rated its 5 MW wind turbine to 6 MW BARD Engineering has launched a similar up-rating of its 5 MW design to 6 MW and later 7 MW Clipper Windpower is working in two new sizes: 7.5 MW and 10 MW Enercon is currently working on a 7.5 MW turbine 11 11

12 Wind - Power curve (1) Source: Vestas V90 3 MW Source: Vestas V112 3MW Source: GE Energy 2.5 MW Source: Vestas E

Source: Gamesa 13")

13 Wind - Power curve (2) Typical generation for a WTG depends on average speed and rotor diameter and not only on WTG nameplate capacity Generation output Average speed (m/s) Source: Gamesa 13 13

14 Wind - Power curve (3) Power curve: WT output power characteristic Partial Load Full load P (kw) Starting Vn Stop Vs Vp Speed (m/s) 14 14

")

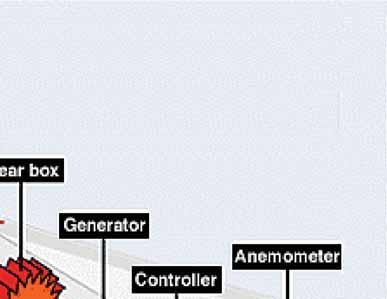

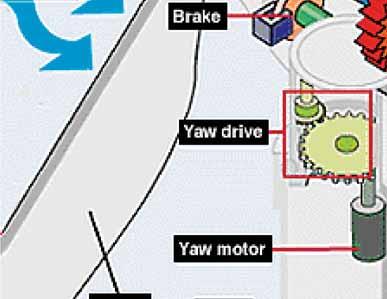

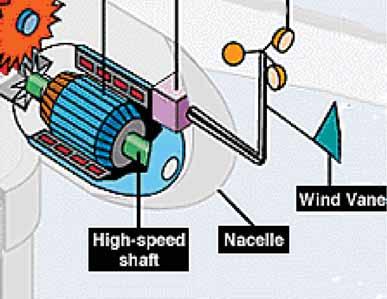

15 Wind turbine components (1) 15 15

16 Wind turbine components (2) 16 16

17 Blades manufacturing Diseño y Tecnología Departamento de Eólica Offshore 17 17

18 Tower manufacturing and installation Diseño y Tecnología Departamento de Eólica Offshore 18 18

5. Distance to point of connection 6. Technical constraints of the grid (voltage dips, reactive power) 7.")

19 Wind farm flowchart 1. Wind resource assessment 2. WT Selection: restriction of wind turbine type 3. Micrositting: output (MWh/year) 4. Maximum installed capacity (due to grid connection capability) 5. Distance to point of connection 6. Technical constraints of the grid (voltage dips, reactive power) 7. Environmental constrains 8. Factors affecting turbine location 19 19

20 Wind - Factors affecting turbine location 1. Maximum installed capacity (due to grid connection or Power Purchase Agreement terms); 2. Site boundary; 3. 'Set back - distances from roads, dwellings, electric lines, ownership boundaries and so on; 4. Environmental constraints; 5. Location of noise-sensitive dwellings, if any, and assessment criteria; 6. Location of visually-sensitive viewpoints, if any, and assessment criteria; 7. Location of dwellings that may be affected by shadow flicker (flickering shadows cast by rotating blades) when the sun is in particular directions, and assessment criteria; 8. Turbine minimum spacing, as defined by the turbine supplier (these are affected by turbulence, in particular); and 9. Constraints associated with communications signals, for example, radar. Optimize process inimize risks 20 20

; and Buildings housing electrical switchgear, SCADA central equipment, and")

21 Wind farm cost breakdown 1. Civil works: Roads and drainage; Wind turbine foundations; Met mast foundations (and occasionally also the met masts); and Buildings housing electrical switchgear, SCADA central equipment, and possibly spares and maintenance facilities. 2. Electrical works 3. Supervisory Control and Data Acquisition (SCADA) system The civil and electrical works are often referred to as the Balance of Plant (BOP) 21 21

22 Wind Onshore vs Offshore (1) Onshore Offshore Influence of local topographical effects Constant roughness on surface Limited influence of topographical effects Surface roughness varies with sea conditions Hub always at same height Hub height varies with tidal More natural turbulence Laminar regimen but with more dissipation difficulty Capacity factor 20%-30% Capacity factor >30% 22 22

23 Wind Onshore vs Offshore (2) Turbines are very similar to onshore wind turbines, but there are important differences: Installation Phase Protection and specific isolation required O&M: access is key Bigger turbines Wind resource Construction & logistics Foundations Specific studies Laminar wind profiles Specialized vessel fleet Monopiles Gravity Jacket O & M Turbines Marine environment brings larger risks and costs 23 23

24 Index Wind Technology Overview, Market Analysis and Economics Introduction and Technology Overview Market Analysis and Perspectives Support Schemes and Price Forecasting Grid Integration and System Flexibility Challenges and Competitiveness 24 24

25 Wind Global current situation 350 Global cumulative installed capacity GW GW/year Source: GWEC 25 25

26 Wind Current situation per country Countries MW (end of 13) % China 91, USA 61, Others Germany 34, Spain 22, India 20, UK 10, Italy 8, France 8, Canada 7, Denmark 4, Denmark Canada France Italy UK India Spain USA China Others 48, TOTAL 318,105 Germany Source: GWEC 26 26

27 Wind Onshore WTG manufacturers Global wind turbine market share evolution: % 29.3% 3.5% 2.1% 3.5% 4.7% 4.1% 23.7% 7.3% 5.4% 6.0% 5.6% 13.3% 13.9% 10.6% 6.3% 8.1% 10.0% 9.4% 15.0% 8.1% 6.7% Vestas Goldwind Enercon Siemens GE Energy Gamesa Suzlon Guodian Mingyang Nordex Others 2013 was a challenging year for the global wind turbine market. A severe drop in US deliveries and increased demand in China shaped last year s market for wind turbine equipment manufacturers. Down from 43.6 GW in 2012, about 36.7 GW of wind turbines were shipped globally in Source: IHS 27 27

28 Wind Global offshore capacity Countries MW (end of 13) UK 3, Denmark 1, Belgium Germany China Netherlands Sweden Japan Finland Ireland Others TOTAL 7,046 % Germany Belgium Ireland Others Finland Japan Sweden Netherlands China Denmark UK Source: GWEC 28 28

29 Wind Offshore capacity evolution Offshore capacity growth drivers: : offshore market impulse caused by Denmark take off : UK (Round 1) contributes to market growth : UK + new EU countries (Sweden (Lillgrund), Germany (Alpha Ventus), Denmark (Horns Rev II) and The Netherlands (Egmond aan Zee)) support offshore development : first relevant offshore projects in Asia (China and Japan) : UK (Round 2) drives worldwide offshore growth. China speeding up growth 29 29

30 Wind Offshore WTG manufacturers YE 2013 Offshore WTG Market Share 0.8% 0.5% Siemens 8% 6% 1.3% Vestas Senvion (REpower) 23% 60% BARD WinWind GE Others Note: Figures for Europe Siemens is the lead offshore wind turbine supplier in Europe with 60% of total installed capacity Together with Vestas (23%) they accrue the majority of the installed offshore capacity Siemens secured the most offshore wind deals, accounting for 1.7 GW (62%) of all announced orders in Europe accounted for almost 80% of announced deals, underlining the relative maturity of the region Source: EWEA Offshore Statistics,

31 Wind Perspectives The market diversification trend which has emerged over the past several years and intensified during 2013 is expected to continue to do so over the next several years. New markets outside the OECD continue to appear, and some of them will begin to make a significant difference to overall market figures. Inside the OECD, as wind power approaches double digit penetration levels in an increasing number of markets, and as demand growth either stalls or goes backwards, incumbents feel increasingly threatened. The fight for market share and policy support in these markets is becoming more and more intense. As a result, most of the growth in the coming years will be in markets outside the OECD looks to be a record year, with annual market growth of about 33%, to bring the annual market to about 47 GW, with strong installations in North America and Asia, and the Brazilian market really beginning to come into its own. Brazil, Mexico and South Africa will figure increasingly strongly in the annual market figures in the years to come. After 2014, the market is expected to return to a more normal annual market growth of 6-10% out to Cumulative growth will rise to nearly 15% in 2014, but average 12-14% from 2015 to Total installations should nearly double from today s numbers by the end of the period, going from just over 300 GW today to just about 600 GW by the end of

32 Wind Short-term market forecast In 2018, global wind generating capacity will stand at nearly 600 GW, up from 318 GW at the end of During 2018, 64 GW of new capacity will be added to the global total, almost the double of 2008 market. Source: GWEC 32 32

33 Wind Short-term market forecast The IEA predicts a sustained over 40 GW annual growth. Driven mainly by developments in China and the Americas. Source: IEA,

34 Wind Global market outlook Global wind additions by region: The Asia Pacific region continues to drive future demand for wind capacity, accounting for 485 GW, or over half of all global wind additions through 2030 Source: IHS 34 34

35 Wind Offshore capacity forecast Global offshore wind additions by market: Despite an 8.6 GW forecast cut for Germany, global offshore wind additions through 2030 are expected to exceed 153 GW; China, the UK, and Germany together make up 106 GW, or 69% of this capacity Source: IHS 35 35

36 Index Wind Technology Overview, Market Analysis and Economics Introduction and Technology Overview Market Analysis and Perspectives Support Schemes and Price Forecasting Grid Integration and System Flexibility Challenges and Competitiveness 36 36

37 Determining factors for renewable growth Economical sustainability Supporting policies to allow competitiveness of Renewables in the electric system and to protect consumers Regulatory framework to promote the most competitive technologies, taking into account the added value these represent in terms of benefits and costs Technical sustainability Reaching a high level of renewable penetration with sufficient security and reliability conditions for the electric systems Optimizing the integration and management of renewable generation 37 37

38 Economical sustainability TYPES OF SUPPORTING SCHEMES Feed-In Tariff Market + Premium Green Certificates Tenders Generation-based Price-driven Fixed income Tax Incentives Generation-based Price-driven Variable income Carbon Credits Generation-based Quantity-driven Variable income Subsidies Generation-based Quantity-driven Fixed income 38 38

39 Technical sustainability Dispatch priority Reactive and active power control Voltage control Balancing services among others 39 39

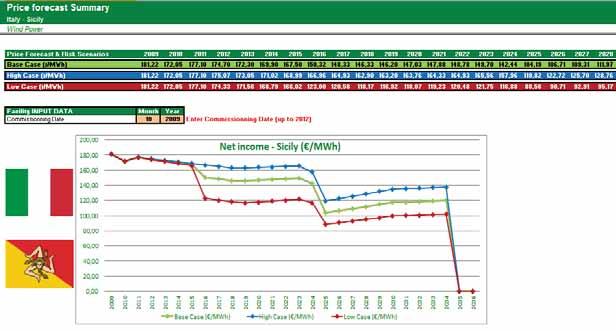

40 Keys to price forecasting Investments are based in a thorough analysis of regulation and current support schemes Price analysis are one of the most relevant inputs for the investment decision making Clear and simple revenues forecasting are a key to attract investment and to match targets Schemes are composed of different variables that may impact pricing in diverse ways. No one-fit-all solution Each wind farm is subject to specific variables that may affect potential revenues Regulation and support schemes are the key driver for providing certainty in terms of future revenues 40 40

41 Price forecasting examples 41 41

42 Wind contribution to sustainability Environment Emissions free Contributes to emission reduction targets: Kyoto Protocol (1997), Bali Agreements (2007), EU Directives Benefits Energy Dependency Local endless energy Energy dependency reduction Volatility and growth scenarios for fossil fuels Competitiveness Industrial and socio-economic driver More competitive generation costs in the longer run Wind and renewables are ready to face the challenges of the current and future energy context 42 42

43 What makes life easier for developers? Theoretically ideal scenario Clear rules, high legal level: a Law is better than a Decree Long term visibility: the forecast is for the whole life time of the asset (20-25 years) Country stability, political & social support to RES. Regulatory tradition Can full certainty be guaranteed? NO Sources of uncertainty Reasonability Political stability Macroeconomics Support mechanism 43 43

44 The effectiveness of support frameworks An effective support framework for renewables must be based on four indispensable factors Profitability Economic Predictability Stability Technical Adequate Integration 44 44

45 Index Wind Technology Overview, Market Analysis and Economics Introduction and Technology Overview Market Analysis and Perspectives Support Schemes and Price Forecasting Grid Integration and System Flexibility Challenges and Competitiveness 45 45

46 Wind generation control capabilities o Start-up and Stop Controls o Yaw Control o Pitching-Speed Control o Over-speed Control o Grid Integration: Power Control Voltage Control 46 46

47 WTG Control WTG stop under control 47 47

48 WTG Start-up and Stop Controls WTG out of control 48 48

49 General concepts: Electrical Grid Electrical Grid: bundle of interconnected elements (cables, lines, transformers ), with the purpose of providing electricity flowing from generators to consumers, with a certain voltage and frequency. The Electrical Grid is the largest infrastructure ever designed, built and controlled by men. NETWORK=CONTROL AC Grid. Since DC Grid. Offshore Wind Farms

50 General concepts: Electrical Grid DC Generator Thomas Alva Edison Nikola Tesla AC Generator Voltage amplitude Main barrier: transmission of electricity across long distances Light-bulb, phonograph, microphone, telegraph, GE founder. Motor / AC Generator, radio, remote control, wireless. Voltage amplitude Frequency In 1890 voltage rising was complex In 1890 voltage rising was simple using Transformers In 2014, offshore wind farms connected with DC links 50 50

51 General concepts: Electrical Grid Nikola Tesla s challenge: first electricity network ever in Niagara Falls Buffalo City 51 51

52 General concepts: Electrical Grid Hydro, coal, fuel and nuclear plants 93 years First hydro plant Wind Farm installation ti 52 52

53 Generation: Dispatchable vs. Variable Conventional Generation Wind Generation 53 53

")

54 General concepts: Electrical Grid Electricity Networks are complex systems by definition, due to this, sophisticated Control tools must be implemented by TSOs in order to hold grid stability: Keep voltage within certain boundaries Keep frequency within certain boundaries CONTROL CENTERS TSO Wind asset operators (CORE IBERDROLA) 54 54

55 Wind energy grid integration In order to facilitate wind integration in the electric systems and, therefore, maximize variable generation penetration, competing with conventional plants, it is necessary to improve WTG functioning in regards to: 1. Power control Dispatchable generation Ancillary services to the TSO 2. Voltage control TSO to improve voltage manageability Increase wind penetration 55 55

56 The balance between Demand and Generation SYSTEM OPERATOR GENERATION DEMAND Frequency (Hz) 56 56

57 The balance between Demand and Generation SYSTEM OPERATOR GENERATION DEMAND Frequency (Hz) 57 57

58 Real-Time generation balancing Demand (MW) :00 22:00 23:00 0:00 1:00 2:00 3:00 4:00 5:00 6:00 7:00 8:00 9:00 10:00 11:00 12:00 13:00 14:00 15:00 16:00 17:00 18:00 19:00 20:00 21:00 22:00 23:00 0:00 1:00 2:00 3:00 Time Balancing Mechanisms are required to adjust real-time generation

59 Power Control In order to keep demand continuously balanced with generation, three levels of capacity reserves are utilized: Primary Reserve: very quick response (2 to 15 seconds). Secondary Reserve: quick response (15 seconds to 15 min). Tertiary Reserve: slower response (over min). Due to the quick variability of wind, wind energy needs to be backed-up with secondary reserve

60 Voltage Control S 2 = P 2 + Q 2 S = apparent power (VA) P = real or active power (W) useful work Q = reactive power (VAr) electromagnetic fields Power factor (cos ) ratio of P to Q 60 60

61 Reactive Power Active Power Reactive Active Apparent 61 61

absorb and/or generate reactive")

62 Reactive Power / Voltage Ratio Reactive Power in the grid is directly related to voltage. Reactive energy flows from nodes with higher voltage to those with lower voltage. Capacitors and alternators By setting grid voltage, reactive energy can be controlled Low load lines and cables Max Grid infrastructure elements (lines, transformers ) absorb and/or generate reactive power, changing the voltage within the node where they are connected. Voltage Resistors and alternators Min High load lines and cables, motors, transformers 62 62

63 Main short-term challenges Generally, little challenges across systems at <10% annual shares apart from local hot-spots. When variable renewables are added to a capacity adequate system: Situations of low load and high wind generation Wind curtailment if flexibility is insufficient Negative market prices due to inflexible generation and renewables support mechanisms Grid bottlenecks in regions with high variable density Limitations feeding production from the distribution to the transmission grid Insufficient evacuation capacity in regions with rapid build out of new wind capacity 63 63

64 Wind Forecasting Wind forecasting accuracy above 85% Forecasting tools have improved continuously during the last years, and are meant to keep improving in the future 64 64

65 Long-term flexibility challenges Grid infrastructure Dispatchable generation Storage Demand side integration 65 65

66 Flexibility resources Flexible generation: Conventional plants and firm renewables adjustable in wide range, very durable, more or less rampable, different lead time and state dependency (nuclear to OCGT) Adjustability and durability of wind limited by resource, but within these bounds they are very rampable, little response time, almost no state dependency Demand Side Integration Adjustable (consumption), varying durability, varying rampable, lead time, possibly high state dependency Storage Perfect adjustability, determined durability Interconnection Can reduce demand and increase supply along all dimensions 66 66

67 Index Wind Technology Overview, Market Analysis and Economics Introduction and Technology Overview Market Analysis and Perspectives Support Schemes and Price Forecasting Grid Integration and System Flexibility Challenges and Competitiveness 67 67

68 Offshore wind: make or break The industry will have to prove it is capable to reduce costs, or face decline as a non-competitive technology /MWh Levelised cost of electricity ( /MWh) Offshore wind Europe wind cumulative capacity E (GW) 3 GW 13 GW 5 GW 0,9 GW 10 GW 0,4 GW Wholesale power price 120 /MWh? 0,2 GW 6 GW 0,3 GW GW UE 2020 High pressure to deliver capacity on large scale Source: IHS, BNEF, Own Estimates 68 68

69 Attracting billions of dollars US $150 bn of average annual investment over the next decade Renewable power investments by technology E $ 150 bn/year Wind will receive 55% of total expected investment; Solar 30% Source: IHS

70 The effect of the economic crisis In a context of economic difficulties Need to alleviate budget deficits Weak electricity demand leading to low electricity prices Reductions in bank lending and increased financing costs for projects pressure is building up to reduce costs Governments are reconsidering their priorities Some countries have announced or already carried out reviews of their renewable support 70 70

71 leading to regulatory instability High pressure to limit support for renewables Reviews of renewables support schemes have been carried out in many markets Spain: Italy: Greece: Bulgaria: Regulatory moratorium. Elimination of market+premium option and 7% tax to all power generation. Switch to tender scheme starting on 2013 and adjustments to solar PV incentives. Unexpected introduction of balancing costs. Introduction of new tax on incomes Introduction of grid access fees for all installed capacity since FIT reductions Germany: Government proposed measures that would reduce incomes both for existing and future installations Poland: Government proposed measures that would reduce income of existing installations challenging renewables growth / whole system stability 71 71

72 Renewables industry facing a turning point ? Early technology deployment of RES Government support driving RES investments Constant evolution of technology RES technologies maturing fast. Wind most mature renewable technology RES generation costs going down High penetration levels in many markets Massive RES deployment Will support mechanisms still be there in the future? Economic crisis. Pressure to limit support for RES High costs from solar bubble 72 72

73 Meeting the challenge of competitiveness Diverse technology solutions 2,0 1,8 1,6 1, Solar thermoelectric Renewable technologies On-shore wind Off-shore wind Solar photovoltaic Solar thermoelectric Different in terms of.. Natural resource availability and growth potential Energy index /KWh 1,2 1,0 0,8 0,6 0,4 0, Off-shore wind Solar photovoltaic On-shore wind 2020 Efficiency and level of technological maturity Cost-effectiveness Integration into the grid and into the system 0, GW 73 73

74 Wind Levelised Cost of Electricity ($/MWh) Offshore Onshore 0 Q3 Q4 Q1 Q2 Q3 Q4 Q1 Q2 Q3 Q4 Q1 Q2 Q3 Q4 Q1 Q2 Q3 Q Note: Prices are in nominal dollars. Onshore prices are for international turbines as opposed to Chinese-sourced turbines Onshore turbine prices inched up this quarter, resulting in a corresponding increase in our global onshore wind LCOE scenario from $78/MWh to $82/MWh Offshore wind LCOEs remain stable at $212/MWh, reflecting a scenario for a German offshore farm costing $5.9m/MW and producing at a capacity factor of 42% Source: Bloomberg New Energy Finance 74 74

75 Levelised Cost Of Electricity Q ($/MWh) Conventional technologies Note: LOCEs for coal and CCGTs in Europe and Australia assume a carbon price of $20/MWh. No carbon prices are assumed for China and US. Onshore wind is close to competitiveness Source: Bloomberg New Energy Finance 75 75

76 Classic approach Large renewable developers have typically followed simple business growth approaches: Organic and inorganic wind/renewable assets growth Greenfield development Tendering processes Build-to-sell Operation and maintenance 76 76

77 Iberdrola s renewable assets worldwide Present in 14 countries with 14 GW of operating wind assets USA USA MW UK UK MW Ireland 15 MW France Germany Hungary Mexico 231 MW Portugal 92 MW 158 MW Spain Spain MW Romania 80 MW Accumulated YE 2013 Brazil 194 MW Italy 132MW Cyprus 20 MW Greece 255 MW Projects/activities under development As of YE

78 Renewable business growth There are positive expectations for the growth of renewables worldwide in the following years Competitiveness of renewables, specially onshore wind and PV (Grid/Market parity) Replacement of old capacity for developed countries Renewable energies will grow during the next decade New capacity required for emerging markets Growing interest from institutional investors in renewables The expected growth will require expertise to allow an efficient and sustainable development 78 78

79 Renewable solutions provider A new perspective is addressed by traditional renewables developers, providing technical support as a consultancy firm, as a developer or as an asset manager Regulatory issues Support of the development of pieces of regulation for renewables Development of new assets Support of the development of new assets Assets management Applying the tools developed in-house and the expertise coming from vast experience in managing own assets 79 79

80 IFC - ESMAP - RENEWABLE ENERGY TRAINING PROGRAM Q & A aportellano@iberdrola.es Washington DC, June 16th

Medium Term Renewable Energy Market Report Michael Waldron Senior Energy Market Analyst Renewable Energy Division International Energy Agency

Medium Term Renewable Energy Market Report 13 Michael Waldron Senior Energy Market Analyst Renewable Energy Division International Energy Agency OECD/IEA 13 Methodology and Scope OECD/IEA 13 Analysis of

Medium Term Renewable Energy Market Report 13 Michael Waldron Senior Energy Market Analyst Renewable Energy Division International Energy Agency OECD/IEA 13 Methodology and Scope OECD/IEA 13 Analysis of

Energy Resources and Policy Handout: Wind power

Energy Resources and Policy Handout: Wind power 1. The Resource Wind energy is very widespread, with mean wind speeds in excess of 5 m/s being quite common. It is not in general a predictable or dependable

Energy Resources and Policy Handout: Wind power 1. The Resource Wind energy is very widespread, with mean wind speeds in excess of 5 m/s being quite common. It is not in general a predictable or dependable

Wind Energy: Overall Potential and Opportunities

Wind Energy: Overall Potential and Opportunities Prepared by: Jens Peter Molly, DEWI GmbH on behalf of UNIDO Global Renewable Energy Forum Foz do Iguaçu, Brazil 18 21 MAY 2008 SITE ASSESSMENT. WIND TURBINE

Wind Energy: Overall Potential and Opportunities Prepared by: Jens Peter Molly, DEWI GmbH on behalf of UNIDO Global Renewable Energy Forum Foz do Iguaçu, Brazil 18 21 MAY 2008 SITE ASSESSMENT. WIND TURBINE

Innovation Paths in Wind Power: Insights from Denmark and Germany

Innovation Paths in Wind Power: Insights from Denmark and Germany Rasmus Lema and Frauke Urban Paper with Johan Nordensvärd and Wilfried Lütkenhorst Technological pathways to low carbon: Competition and

Innovation Paths in Wind Power: Insights from Denmark and Germany Rasmus Lema and Frauke Urban Paper with Johan Nordensvärd and Wilfried Lütkenhorst Technological pathways to low carbon: Competition and

Roadmap for Solar PV. Michael Waldron Renewable Energy Division International Energy Agency

Roadmap for Solar PV Michael Waldron Renewable Energy Division International Energy Agency OECD/IEA 2014 IEA work on renewables IEA renewables website: http://www.iea.org/topics/renewables/ Renewable Policies

Roadmap for Solar PV Michael Waldron Renewable Energy Division International Energy Agency OECD/IEA 2014 IEA work on renewables IEA renewables website: http://www.iea.org/topics/renewables/ Renewable Policies

PES ESSENTIAL. PES: Europe

PES ESSENTIAL 96 PES: Europe The cost of wind Like other renewable energy technologies, wind is capital intensive, but has no fuel costs. The key parameters governing wind power economics are the investment

PES ESSENTIAL 96 PES: Europe The cost of wind Like other renewable energy technologies, wind is capital intensive, but has no fuel costs. The key parameters governing wind power economics are the investment

Making the Electricity System Work

Making the Electricity System Work Variable Renewables Electricity Systems Integration get it right Alessandro Clerici July 24/2017 Varenna Variable Renewables Electricity Systems Integration: how to get

Making the Electricity System Work Variable Renewables Electricity Systems Integration get it right Alessandro Clerici July 24/2017 Varenna Variable Renewables Electricity Systems Integration: how to get

Politique et sécurité énergétique dans le contexte des nouvelles énergies

Politique et sécurité énergétique dans le contexte des nouvelles énergies Didier Houssin Director, Energy Markets and Security International Energy Agency Colloque L Energie : enjeux socio-économiques

Politique et sécurité énergétique dans le contexte des nouvelles énergies Didier Houssin Director, Energy Markets and Security International Energy Agency Colloque L Energie : enjeux socio-économiques

WIND POWER TARGETS FOR EUROPE: 75,000 MW by 2010

About EWEA EWEA is the voice of the wind industry actively promoting the utilisation of wind power in Europe and worldwide. EWEA members from over 4 countries include 2 companies, organisations, and research

About EWEA EWEA is the voice of the wind industry actively promoting the utilisation of wind power in Europe and worldwide. EWEA members from over 4 countries include 2 companies, organisations, and research

Gamesa Global technology, everlasting energy. September 2012

Gamesa Global technology, everlasting energy September 2012 Technological global leader o Global presence o Built-in operator o Sustainable company 2 Technological global leader Extensive experience in

Gamesa Global technology, everlasting energy September 2012 Technological global leader o Global presence o Built-in operator o Sustainable company 2 Technological global leader Extensive experience in

China Drives Global Wind Growth

Megawatts China Drives Global Wind Growth Mark Konold and Samantha Bresler May 30, 2012 I n 2011, global wind power capacity topped out at 238,000 megawatts (MW) after adding just over 41,000 MW. 1 (See

Megawatts China Drives Global Wind Growth Mark Konold and Samantha Bresler May 30, 2012 I n 2011, global wind power capacity topped out at 238,000 megawatts (MW) after adding just over 41,000 MW. 1 (See

SAMPLE. Reference Code: GDAE6214IDB. Publication Date: September GDAE6214IDB / Published SEP 2012

Solar PV in Spain, Market Outlook to 2025 - Capacity, Generation, Levelized Cost of Energy (LCOE), Investment Trends, Regulations and Reference Code: GDAE6214IDB Publication Date: September 2012 GlobalData.

Solar PV in Spain, Market Outlook to 2025 - Capacity, Generation, Levelized Cost of Energy (LCOE), Investment Trends, Regulations and Reference Code: GDAE6214IDB Publication Date: September 2012 GlobalData.

WIND ENERGY - THE FACTS PART VI SCENARIOS AND TARGETS

WIND ENERGY - THE FACTS PART VI SCENARIOS AND TARGETS Acknowledgements Part VI was compiled by Arthouros Zervos of the National Technical University of Athens, Greece (www. ntua.gr), and Christian Kjaer

WIND ENERGY - THE FACTS PART VI SCENARIOS AND TARGETS Acknowledgements Part VI was compiled by Arthouros Zervos of the National Technical University of Athens, Greece (www. ntua.gr), and Christian Kjaer

An Imagination Breakthrough: Offshore Wind Energy

An Imagination Breakthrough: Offshore Wind Energy Alternative Energy Technology Innovations: Savannah, Georgia Benjamin Bell GE Energy Overview Why Wind? Why Offshore? The Technology Wind Energy Economics

An Imagination Breakthrough: Offshore Wind Energy Alternative Energy Technology Innovations: Savannah, Georgia Benjamin Bell GE Energy Overview Why Wind? Why Offshore? The Technology Wind Energy Economics

1 New Energy Outlook 2017

1 New Energy Outlook 217 Leveraging the power of Bloomberg Since 1981 Over 15, employees in 192 locations Generating 5, news stories a day from 15 bureaus 32, global clients Since 24 2+ employees in 15

1 New Energy Outlook 217 Leveraging the power of Bloomberg Since 1981 Over 15, employees in 192 locations Generating 5, news stories a day from 15 bureaus 32, global clients Since 24 2+ employees in 15

H APAC LCOE UPDATE

12 August 2014 H2 2014 APAC LCOE UPDATE A race between renewable penetration and fuel prices Maggie Kuang A NOTE ON BNEF S EXPANDING LCOE UNIVERSE BNEF introduces a new, expanded and more regional approach

12 August 2014 H2 2014 APAC LCOE UPDATE A race between renewable penetration and fuel prices Maggie Kuang A NOTE ON BNEF S EXPANDING LCOE UNIVERSE BNEF introduces a new, expanded and more regional approach

Medium Term Renewable Energy Market Report 2016

Medium Term Renewable Energy Market Report 2016 Clean Energy Investment and Trends IETA Pavilion COP22, Marrakech November 10, 2016 Liwayway Adkins Environment and Climate Change Unit International Energy

Medium Term Renewable Energy Market Report 2016 Clean Energy Investment and Trends IETA Pavilion COP22, Marrakech November 10, 2016 Liwayway Adkins Environment and Climate Change Unit International Energy

Renewable Energy and other Sustainable Energy Sources. Paul Simons Deputy Executive Director International Energy Agency

Renewable Energy and other Sustainable Energy Sources Paul Simons Deputy Executive Director International Energy Agency G20 ESWG meeting Munich, 14 December 2016 Renewables and efficiency lead the transition

Renewable Energy and other Sustainable Energy Sources Paul Simons Deputy Executive Director International Energy Agency G20 ESWG meeting Munich, 14 December 2016 Renewables and efficiency lead the transition

U.S electricity flow, 2005

Wind Energy Systems Prof. Surya Santoso Department of Electrical and Computer Engineering The University of Texas at Austin ssantoso@ece.utexas.edu U.S electricity flow, 2005 Unit is in quadrillion BTU

Wind Energy Systems Prof. Surya Santoso Department of Electrical and Computer Engineering The University of Texas at Austin ssantoso@ece.utexas.edu U.S electricity flow, 2005 Unit is in quadrillion BTU

Methodology for calculating subsidies to renewables

1 Introduction Each of the World Energy Outlook scenarios envisages growth in the use of renewable energy sources over the Outlook period. World Energy Outlook 2012 includes estimates of the subsidies

1 Introduction Each of the World Energy Outlook scenarios envisages growth in the use of renewable energy sources over the Outlook period. World Energy Outlook 2012 includes estimates of the subsidies

Roadmap for Small Wind Turbines

Roadmap for Small Wind Turbines Deepak Valagam, Technical Director, Vaata Infra Limited, Chennai Introduction With depletion of fossil fuel and ever growing electricity demand, the focus has shifted to

Roadmap for Small Wind Turbines Deepak Valagam, Technical Director, Vaata Infra Limited, Chennai Introduction With depletion of fossil fuel and ever growing electricity demand, the focus has shifted to

Integrating variable renewables: Implications for energy resilience

Integrating variable renewables: Implications for energy resilience Peerapat Vithaya, Energy Analyst System Integration of Renewables Enhancing Energy Sector Climate Resilience in Asia Asia Clean Energy

Integrating variable renewables: Implications for energy resilience Peerapat Vithaya, Energy Analyst System Integration of Renewables Enhancing Energy Sector Climate Resilience in Asia Asia Clean Energy

How to secure Europe s competitiveness in terms of energy and raw materials? The answer, my friend, is blowing in the wind

How to secure Europe s competitiveness in terms of energy and raw materials? The answer, my friend, is blowing in the wind Iván Pineda Head of Policy Analysis, EWEA PolyTalk 2014, Brussels Around 600 members

How to secure Europe s competitiveness in terms of energy and raw materials? The answer, my friend, is blowing in the wind Iván Pineda Head of Policy Analysis, EWEA PolyTalk 2014, Brussels Around 600 members

Competitive energy landscape in Europe

President of Energy Sector, South West Europe, Siemens Competitive energy landscape in Europe Brussels, siemens.com/answers Agenda Europe s competitiveness depends on an affordable and reliable energy

President of Energy Sector, South West Europe, Siemens Competitive energy landscape in Europe Brussels, siemens.com/answers Agenda Europe s competitiveness depends on an affordable and reliable energy

Photo: Thinkstock. Wind in power 2010 European statistics. February The European Wind energy association

Photo: Thinkstock Wind in power 21 European statistics February 211 1 WIND IN POWER: 21 EUROPEAN STATISTICS Contents Executive summary 21 annual installations Wind map 21 Wind power capacity installations

Photo: Thinkstock Wind in power 21 European statistics February 211 1 WIND IN POWER: 21 EUROPEAN STATISTICS Contents Executive summary 21 annual installations Wind map 21 Wind power capacity installations

18 Informe Anual 2012 Aerogeneradores

18 Informe Anual 2012 Aerogeneradores 19 Annual Report 2012 08 wind turbines 26,625 MW installed (cumulative) 42 countries worldwide 2,119 MWe sold in 2012 2,625 MW installed in 2012 Nineteen years experience,

18 Informe Anual 2012 Aerogeneradores 19 Annual Report 2012 08 wind turbines 26,625 MW installed (cumulative) 42 countries worldwide 2,119 MWe sold in 2012 2,625 MW installed in 2012 Nineteen years experience,

The German Wind Energy Market

Energy The German Wind Energy Market Current developements and perspectives April 14 th 2010, Austin Lars Velser, German Wind Energy Association (BWE) www.exportinitiative.bmwi.de Content About the German

Energy The German Wind Energy Market Current developements and perspectives April 14 th 2010, Austin Lars Velser, German Wind Energy Association (BWE) www.exportinitiative.bmwi.de Content About the German

Plenary session 2: Sustainable and Inclusive Growth: Energy Access and Affordability. Background Paper

India Plenary session 2: Sustainable and Inclusive Growth: Energy Access and Affordability New Delhi Background Paper Disclaimer The observations presented herein are meant as background for the dialogue

India Plenary session 2: Sustainable and Inclusive Growth: Energy Access and Affordability New Delhi Background Paper Disclaimer The observations presented herein are meant as background for the dialogue

GE OIL & GAS ANNUAL MEETING 2016 Florence, Italy, 1-2 February

Navigating energy transition Keisuke Sadamori Director for Energy Markets and Security IEA GE OIL & GAS ANNUAL MEETING 2016 Florence, Italy, 1-2 February 2016 General Electric Company - All rights reserved

Navigating energy transition Keisuke Sadamori Director for Energy Markets and Security IEA GE OIL & GAS ANNUAL MEETING 2016 Florence, Italy, 1-2 February 2016 General Electric Company - All rights reserved

DIRECTORATE FOR FUEL AND ENERGY SECTOR. Development of Wind Energy Technology in the World

DIRECTORATE FOR FUEL AND ENERGY SECTOR Development of Wind Energy Technology in the World INFORMATION REFERENCE October 2013 I N F O R M A T I O N R E F E R E N C E General Information on Wind Energy Wind

DIRECTORATE FOR FUEL AND ENERGY SECTOR Development of Wind Energy Technology in the World INFORMATION REFERENCE October 2013 I N F O R M A T I O N R E F E R E N C E General Information on Wind Energy Wind

RENEWABLE POWER GENERATION COSTS IN 2014

RENEWABLE POWER GENERATION COSTS IN Executive Summary The competiveness of renewable power generation technologies continued improving in 2013 and. The cost-competitiveness of renewable power generation

RENEWABLE POWER GENERATION COSTS IN Executive Summary The competiveness of renewable power generation technologies continued improving in 2013 and. The cost-competitiveness of renewable power generation

Outlook for Renewable Energy Market

216 IEEJ216 423 rd Forum on Research Works on July 26, 216 Outlook for Renewable Energy Market The Institute of Energy Economics, Japan Yoshiaki Shibata Senior Economist, Manager, New and Renewable Energy

216 IEEJ216 423 rd Forum on Research Works on July 26, 216 Outlook for Renewable Energy Market The Institute of Energy Economics, Japan Yoshiaki Shibata Senior Economist, Manager, New and Renewable Energy

Global technology, everlasting energy. Camaçari, 8 June 2011

Global technology, everlasting energy Camaçari, 8 June 2011 Gamesa Technological global leader More than 15 years of experience in technological sector and wind industry Listed company, member of the Ibex-35

Global technology, everlasting energy Camaçari, 8 June 2011 Gamesa Technological global leader More than 15 years of experience in technological sector and wind industry Listed company, member of the Ibex-35

European Commission. Communication on Support Schemes for electricity from renewable energy sources

European Commission Communication on Support Schemes for electricity from renewable energy sources External Costs of energy and their internalisation in Europe Beatriz Yordi DG Energy and Transport External

European Commission Communication on Support Schemes for electricity from renewable energy sources External Costs of energy and their internalisation in Europe Beatriz Yordi DG Energy and Transport External

EU 2020 Targets: Managing integration of wind in the Hungarian grid. Tari Gábor CEO. Wind Energy the Facts Tari G. 12 June 2009 Workshop,

EU 2020 Targets: Managing integration of wind in the Hungarian grid Tari Gábor CEO Wind Energy the Facts Workshop, 12.06.2009 Contents 2 Hungarian Electric Power System the facts Generation mix Consumption

EU 2020 Targets: Managing integration of wind in the Hungarian grid Tari Gábor CEO Wind Energy the Facts Workshop, 12.06.2009 Contents 2 Hungarian Electric Power System the facts Generation mix Consumption

Advanced Renewable Incentive Schemes. Simon Müller Senior Analyst System Integration of Renewables International Energy Agency

Advanced Renewable Incentive Schemes Simon Müller Senior Analyst System Integration of Renewables International Energy Agency Berlin Energy Transition Dialogue, 17 March 2016 The start of a new energy

Advanced Renewable Incentive Schemes Simon Müller Senior Analyst System Integration of Renewables International Energy Agency Berlin Energy Transition Dialogue, 17 March 2016 The start of a new energy

Conditions for accelerating the deployment of offshore wind power in the BSR - Seminar 27 April 2012, Wind Power in the Nordic and Baltic Region

Conditions for accelerating the deployment of offshore wind power in the BSR - Seminar 27 April 2012, Wind Power in the Nordic and Baltic Region BASREC - Wind Contents: 1. Objectives & Implementation Framework

Conditions for accelerating the deployment of offshore wind power in the BSR - Seminar 27 April 2012, Wind Power in the Nordic and Baltic Region BASREC - Wind Contents: 1. Objectives & Implementation Framework

Vestas Presentation. Javier Ojanguren Sales Manager Central America & Caribbean

Vestas Presentation Javier Ojanguren Sales Manager Central America & Caribbean jaosa@vestas.com About Vestas 2 Dominican Republic Energy Roundtable - February 2011 About Vestas Vestas at a glance Today,

Vestas Presentation Javier Ojanguren Sales Manager Central America & Caribbean jaosa@vestas.com About Vestas 2 Dominican Republic Energy Roundtable - February 2011 About Vestas Vestas at a glance Today,

RENEWABLE ENERGY IN AUSTRALIA

RENEWABLE ENERGY IN AUSTRALIA How do we really compare? FACT SHEET Increasing electricity generation from renewable energy sources is one of the main strategies to reduce greenhouse emissions from the

RENEWABLE ENERGY IN AUSTRALIA How do we really compare? FACT SHEET Increasing electricity generation from renewable energy sources is one of the main strategies to reduce greenhouse emissions from the

SUSTAINABLE USE OF OCEANS IN THE CONTEXT OF THE GREEN ECONOMY AND THE ERADICATION OF POVERTY, PRINCIPALITY OF MONACO, NOVEMBER, 2011

SUSTAINABLE USE OF OCEANS IN THE CONTEXT OF THE GREEN ECONOMY AND THE ERADICATION OF POVERTY, PRINCIPALITY OF MONACO, 28 30 NOVEMBER, 2011 Implementation of Offshore Wind Power & Potential of Tidal, Wave

SUSTAINABLE USE OF OCEANS IN THE CONTEXT OF THE GREEN ECONOMY AND THE ERADICATION OF POVERTY, PRINCIPALITY OF MONACO, 28 30 NOVEMBER, 2011 Implementation of Offshore Wind Power & Potential of Tidal, Wave

Introduction: Wind Power and Renewable Energy industry in China. Hugo Yu

Introduction: Wind Power and Renewable Energy industry in China Hugo Yu June 04, 2012 YU Huajun (Hugo) 2005 Awarded with Electrical Engineering Doctoral Degree in Shanghai Jiaotong University. Research

Introduction: Wind Power and Renewable Energy industry in China Hugo Yu June 04, 2012 YU Huajun (Hugo) 2005 Awarded with Electrical Engineering Doctoral Degree in Shanghai Jiaotong University. Research

Trends in renewable energy and storage

Trends in renewable energy and storage Energy and Mines World Congress, 2017 Rachel Jiang November 27, 2017 Key trends Solar, wind may make up one-third of global electricity generation by 2040 and a growing

Trends in renewable energy and storage Energy and Mines World Congress, 2017 Rachel Jiang November 27, 2017 Key trends Solar, wind may make up one-third of global electricity generation by 2040 and a growing

ENERGY PRIORITIES FOR EUROPE

ENERGY PRIORITIES FOR EUROPE Presentation of J.M. Barroso, President of the European Commission, to the European Council of 4 February 2011 Contents 1 I. Why energy policy matters II. Why we need to act

ENERGY PRIORITIES FOR EUROPE Presentation of J.M. Barroso, President of the European Commission, to the European Council of 4 February 2011 Contents 1 I. Why energy policy matters II. Why we need to act

Renewable energy in Europe. E-turn 21 workshop Cologne, 10 May 2006

Renewable energy in Europe E-turn 21 workshop Cologne, 10 May 2006 Content 1. Introduction to Essent 2. EU policy 3. Support for renewable energy 4. Success factors 5. Outlook and recommendations Content

Renewable energy in Europe E-turn 21 workshop Cologne, 10 May 2006 Content 1. Introduction to Essent 2. EU policy 3. Support for renewable energy 4. Success factors 5. Outlook and recommendations Content

Core projects and scientific studies as background for the NREAPs. 9th Inter-Parliamentary Meeting on Renewable Energy and Energy Efficiency

Core projects and scientific studies as background for the NREAPs 9th Inter-Parliamentary Meeting on Renewable Energy and Energy Efficiency Brussels, 18.11.2009 Mario Ragwitz Fraunhofer Institute Systems

Core projects and scientific studies as background for the NREAPs 9th Inter-Parliamentary Meeting on Renewable Energy and Energy Efficiency Brussels, 18.11.2009 Mario Ragwitz Fraunhofer Institute Systems

European Offshore Wind Overview. February C Offshore - OrbisEnergy Centre, Lowestoft, NR32 1XH T: +44 (0) E:

E:") European Offshore Wind Overview February 2015 4C Offshore - OrbisEnergy Centre, Lowestoft, NR32 1XH T: +44 (0)1502 307 037 E: info@4coffshore.com European Overview 2 Table of Contents Capacity Overview

European Offshore Wind Overview February 2015 4C Offshore - OrbisEnergy Centre, Lowestoft, NR32 1XH T: +44 (0)1502 307 037 E: info@4coffshore.com European Overview 2 Table of Contents Capacity Overview

Wind Power in Romania: Potential, Benefits, Barriers

Wind Power in Romania: Potential, Benefits, Barriers Jannik Termansen, Vestas Wind Systems A/S, 2 June 2009 vestas.com Agenda 1. Romania s wind potential 2. Wind benefits for Romania 3. Barriers and recommendations

Wind Power in Romania: Potential, Benefits, Barriers Jannik Termansen, Vestas Wind Systems A/S, 2 June 2009 vestas.com Agenda 1. Romania s wind potential 2. Wind benefits for Romania 3. Barriers and recommendations

Wind Power in Denmark. Steffen Nielsen Head of Section Danish Energy Authority Ministry of Climate and Energy

Wind Power in Denmark Steffen Nielsen Head of Section Danish Energy Authority Ministry of Climate and Energy Outline Status on wind power deployment and large scale integration Support system and consent

Wind Power in Denmark Steffen Nielsen Head of Section Danish Energy Authority Ministry of Climate and Energy Outline Status on wind power deployment and large scale integration Support system and consent

Realizing the Flexibility Potential of Industrial Electricity Demand: Overview of the H2020 Project IndustRE

EMART Energy 2017: Commercial and Industrial Energy Users Amsterdam, 4 th October 2017 Realizing the Flexibility Potential of Industrial Electricity Demand: Overview of the H2020 Project IndustRE Dimitrios

EMART Energy 2017: Commercial and Industrial Energy Users Amsterdam, 4 th October 2017 Realizing the Flexibility Potential of Industrial Electricity Demand: Overview of the H2020 Project IndustRE Dimitrios

INTERNATIONAL ENERGY AGENCY. In support of the G8 Plan of Action TOWARD A CLEAN, CLEVER & COMPETITIVE ENERGY FUTURE

INTERNATIONAL ENERGY AGENCY In support of the G8 Plan of Action TOWARD A CLEAN, CLEVER & COMPETITIVE ENERGY FUTURE 2007 REPORT TO THE G8 SUMMIT in Heiligendamm, Germany The International Energy Agency,

INTERNATIONAL ENERGY AGENCY In support of the G8 Plan of Action TOWARD A CLEAN, CLEVER & COMPETITIVE ENERGY FUTURE 2007 REPORT TO THE G8 SUMMIT in Heiligendamm, Germany The International Energy Agency,

Building a Profitable Wind Business

GE Energy Building a Profitable Wind Business Vic Abate July 26, 2006 This document contains "forward-looking statements" - that is, statements related to future, not past, events. In this context, forward-looking

GE Energy Building a Profitable Wind Business Vic Abate July 26, 2006 This document contains "forward-looking statements" - that is, statements related to future, not past, events. In this context, forward-looking

Offshore Wind Technology

Offshore Wind Technology Jason Jonkman Senior Engineer National Renewable Energy Laboratory Golden, Colorado Webinar: Offshore Wind Potential for the Great Lakes January 30, 2009 Why Offshore Wind? 28

Offshore Wind Technology Jason Jonkman Senior Engineer National Renewable Energy Laboratory Golden, Colorado Webinar: Offshore Wind Potential for the Great Lakes January 30, 2009 Why Offshore Wind? 28

Energy Perspectives for Asia

Energy Perspectives for Asia By Rajiv Ranjan Mishra Nov 21, 2017 Energy Asia Population Asia 4.06 billion 55% of World 8X of EU Expected to be 8.5 billion by 2030 Source: World Bank, 2016; UN GDP Per Capita

Energy Perspectives for Asia By Rajiv Ranjan Mishra Nov 21, 2017 Energy Asia Population Asia 4.06 billion 55% of World 8X of EU Expected to be 8.5 billion by 2030 Source: World Bank, 2016; UN GDP Per Capita

The Future of the Ocean Economy - Offshore Wind

The Future of the Ocean Economy - Offshore Wind Workshop on Shipping and the Offshore Industry Monday 24 th November, 2014 OECD, Paris Key data sources EWEA Background Projections Technology Finance IEA

The Future of the Ocean Economy - Offshore Wind Workshop on Shipping and the Offshore Industry Monday 24 th November, 2014 OECD, Paris Key data sources EWEA Background Projections Technology Finance IEA

Why does a wind turbine have three blades?

Why does a wind turbine have three blades? 1980 Monopteros 1983 Growian 1982 Darrieus Page 1 Why does a wind turbine have three blades? 1. It is because they look nicer? 2. Or because three blades are

Why does a wind turbine have three blades? 1980 Monopteros 1983 Growian 1982 Darrieus Page 1 Why does a wind turbine have three blades? 1. It is because they look nicer? 2. Or because three blades are

Execution according to plan More to come. Markus Tacke, CEO Wind Power and Renewables Capital Market Day Energy and Oil & Gas Houston, June 29, 2016

Execution according to plan More to come Markus Tacke, CEO Wind Power and Renewables Capital Market Day Energy and Oil & Gas siemens.com/investor Notes and forward-looking statements This document contains

Execution according to plan More to come Markus Tacke, CEO Wind Power and Renewables Capital Market Day Energy and Oil & Gas siemens.com/investor Notes and forward-looking statements This document contains

EDF and Integration of Distributed Energy Resources

IEEE Power Engineering Society Tuesday, June 20, 2006. Montreal EDF and Integration of Distributed Energy Resources Bruno Meyer (presenter) Director Power Systems Technology and Economics Yves Bamberger,

IEEE Power Engineering Society Tuesday, June 20, 2006. Montreal EDF and Integration of Distributed Energy Resources Bruno Meyer (presenter) Director Power Systems Technology and Economics Yves Bamberger,

Towards mega size wind turbines

TECHNOLOGY PAPER 1 Towards mega size wind turbines The development and application of the wind energy technology is one of the genuine success stories in modern history of technology. The most impressive

TECHNOLOGY PAPER 1 Towards mega size wind turbines The development and application of the wind energy technology is one of the genuine success stories in modern history of technology. The most impressive

Nordex SE 10 th WEED Focus Ghana. Berlin 15 Oct 2015

Nordex SE 10 th WEED Focus Ghana Berlin 15 Oct 2015 COMPANY PROFILE NORDEX SE Nordex at a glance Installed capacity (12.1 GW) Global manufacturer of wind energy systems with a focus on turbines in the

Nordex SE 10 th WEED Focus Ghana Berlin 15 Oct 2015 COMPANY PROFILE NORDEX SE Nordex at a glance Installed capacity (12.1 GW) Global manufacturer of wind energy systems with a focus on turbines in the

EU Climate and Energy Policy Framework: EU Renewable Energy Policies

EU Climate and Energy Policy Framework: EU Renewable Energy Policies Buenos Aires 26-27 May 2015 Dr Stefan Agne European Commission DG Climate Action Energy 1 EU Climate and Energy Policy Framework 2 Agreed

EU Climate and Energy Policy Framework: EU Renewable Energy Policies Buenos Aires 26-27 May 2015 Dr Stefan Agne European Commission DG Climate Action Energy 1 EU Climate and Energy Policy Framework 2 Agreed

Renewable sources of energy, dispatching priority and balancing the system, facts and options: Part I

Renewable sources of energy, dispatching priority and balancing the system, facts and options: Part I Matteo Leonardi 22 May 2013 Liberalized markets versus monopolies Production Transmission distribution

Renewable sources of energy, dispatching priority and balancing the system, facts and options: Part I Matteo Leonardi 22 May 2013 Liberalized markets versus monopolies Production Transmission distribution

Panel #2 - Wind logistics: Onshore towards offshore 2 nd Annual DHL Global Wind Conference

Panel #2 - Wind logistics: Onshore towards offshore Hamburg, September 26, 2016 Renewable Energy Solutions Presented by Thomas Poulsen, Managing Partner Wind logistics: Onshore towards offshore Key Definitions

Panel #2 - Wind logistics: Onshore towards offshore Hamburg, September 26, 2016 Renewable Energy Solutions Presented by Thomas Poulsen, Managing Partner Wind logistics: Onshore towards offshore Key Definitions

Analyses market and policy trends for electricity, heat and transport Investigates the strategic drivers for RE deployment Benchmarks the impact and c

Paolo Frankl Head Renewable Energy Division International Energy Agency Institute of Energy Economics, Japan (IEEJ) Energy Seminar Tokyo, 7 March 2012 OECD/IEA 2011 Analyses market and policy trends for

Paolo Frankl Head Renewable Energy Division International Energy Agency Institute of Energy Economics, Japan (IEEJ) Energy Seminar Tokyo, 7 March 2012 OECD/IEA 2011 Analyses market and policy trends for

GE Power & Water Renewable Energy. GE s A brilliant wind turbine for India. ge-energy.com/wind

GE Power & Water Renewable Energy GE s 1.7-103 A brilliant wind turbine for India ge-energy.com/wind GE s 1.7-103 Wind Turbine Since entering the wind industry in 2002, GE Power & Water s Renewable Energy

GE Power & Water Renewable Energy GE s 1.7-103 A brilliant wind turbine for India ge-energy.com/wind GE s 1.7-103 Wind Turbine Since entering the wind industry in 2002, GE Power & Water s Renewable Energy

Engaging consumers in a decarbonized world with the right pricing

Engaging consumers in a decarbonized world with the right pricing BEHAVE 2016 Coimbra, 9 th of September of 2016 Ana Quelhas Director of Energy Planning Department ana.quelhas@edp.pt Agenda Achieving decarbonization

Engaging consumers in a decarbonized world with the right pricing BEHAVE 2016 Coimbra, 9 th of September of 2016 Ana Quelhas Director of Energy Planning Department ana.quelhas@edp.pt Agenda Achieving decarbonization

The Global Grid. Prof. Damien Ernst University of Liège December 2013

The Global Grid Prof. Damien Ernst University of Liège December 2013 1 The Global Grid: what is it? Global Grid: Refers to an electrical grid spanning the whole planet and connecting most of the large

The Global Grid Prof. Damien Ernst University of Liège December 2013 1 The Global Grid: what is it? Global Grid: Refers to an electrical grid spanning the whole planet and connecting most of the large

Global Wind Turbine Technology Trends

Analyst PRESENTATION Global Wind Turbine Technology Trends 26 April 2017 Andy Li lb@consultmake.com Introduction A few words about MAKE Summary MAKE is one of the global wind industry's premier strategic

Analyst PRESENTATION Global Wind Turbine Technology Trends 26 April 2017 Andy Li lb@consultmake.com Introduction A few words about MAKE Summary MAKE is one of the global wind industry's premier strategic

Why China Is Acting on Clean Energy: Successes, Challenges, and Implications

Why China Is Acting on Clean Energy: Successes, Challenges, and Implications Joanna Lewis, Ph.D. Georgetown University Presented at the EESI/WRI Senate Briefing October 12, 2012 China s Clean Energy Achievements

Why China Is Acting on Clean Energy: Successes, Challenges, and Implications Joanna Lewis, Ph.D. Georgetown University Presented at the EESI/WRI Senate Briefing October 12, 2012 China s Clean Energy Achievements

Distributed Generation Technologies A Global Perspective

Distributed Generation Technologies A Global Perspective NSF Workshop on Sustainable Energy Systems Professor Saifur Rahman Director Alexandria Research Institute Virginia Tech November 2000 Nuclear Power

Distributed Generation Technologies A Global Perspective NSF Workshop on Sustainable Energy Systems Professor Saifur Rahman Director Alexandria Research Institute Virginia Tech November 2000 Nuclear Power

Wind energy. Stefan Karlsson Global Segment Manager, Renewable Energy

Wind energy Stefan Karlsson Global Segment Manager, Renewable Energy Capital Markets Day 2009 The dynamic wind energy market Wind energy business development snapshot 70,000 60,000 50,000 40,000 30,000

Wind energy Stefan Karlsson Global Segment Manager, Renewable Energy Capital Markets Day 2009 The dynamic wind energy market Wind energy business development snapshot 70,000 60,000 50,000 40,000 30,000

UE 1.65 DirectDrive Turbine Technology

UE 1.65 DirectDrive Turbine Technology A World full of Energy. The right choice for the maximum return on your investment in wind energy. UE 1.65 DirectDrive With its simplicity and modularity the UE 1.65

UE 1.65 DirectDrive Turbine Technology A World full of Energy. The right choice for the maximum return on your investment in wind energy. UE 1.65 DirectDrive With its simplicity and modularity the UE 1.65

Summary. Ad Hoc Group Report

PRELIMINARY Long term R&D needs for wind energy For the time frame 2000 2020 Ad Hoc Group Report Summary The dawn of R&D was technologically driven whereas, when it later became more mature other topics

PRELIMINARY Long term R&D needs for wind energy For the time frame 2000 2020 Ad Hoc Group Report Summary The dawn of R&D was technologically driven whereas, when it later became more mature other topics

Where is moving the electricity sector and how are Electric. Industry Investment Decisions Influenced by Potential

Where is moving the electricity sector and how are Electric Industry Investment Decisions Influenced by Potential Instability in the Regulatory Environment by : G. Dodero I.P.G. Industrial Project Group

Where is moving the electricity sector and how are Electric Industry Investment Decisions Influenced by Potential Instability in the Regulatory Environment by : G. Dodero I.P.G. Industrial Project Group

Steady as she goes By Alasdair Cameron

RENEWABLE ENERGY WORLD, July-August 2005, Volume 8, Number 4 Steady as she goes By Alasdair Cameron BTM's world market update Total wind capacity grew by around 20% in 2004, despite a temporary slump in

RENEWABLE ENERGY WORLD, July-August 2005, Volume 8, Number 4 Steady as she goes By Alasdair Cameron BTM's world market update Total wind capacity grew by around 20% in 2004, despite a temporary slump in

Local impact, global leadership. The impact of wind energy on jobs and the EU economy

Local impact, global leadership The impact of wind energy on jobs and the EU economy Local impact, global leadership The impact of wind energy on jobs and the EU economy November 2017 The socio-economic

Local impact, global leadership The impact of wind energy on jobs and the EU economy Local impact, global leadership The impact of wind energy on jobs and the EU economy November 2017 The socio-economic

Demand Response as Flexibility Provider: what are the challenges to achieve its full potential?

Demand Response as Flexibility Provider: what are the challenges to achieve its full potential? Dr. Kristof De Vos, KU Leuven - EnergyVille Febeliec Workshop on Demand Response June 15, 2015 Diamant Building,

Demand Response as Flexibility Provider: what are the challenges to achieve its full potential? Dr. Kristof De Vos, KU Leuven - EnergyVille Febeliec Workshop on Demand Response June 15, 2015 Diamant Building,

Status Quo - Storage systems and PV in a global context

Status Quo - Storage systems and PV in a global context 2. October 2013 Stuttgart Martin Ammon Senior Research Manager EuPD Research Economic Parameters of Photovoltaics and Storage 2 Evaluation approaches

Status Quo - Storage systems and PV in a global context 2. October 2013 Stuttgart Martin Ammon Senior Research Manager EuPD Research Economic Parameters of Photovoltaics and Storage 2 Evaluation approaches

China National Renewable Energy Centre

China National Renewable Energy Centre Content A B C D E F G H I China s energy and power generation mix China Renewable Energy Development Hydropower Wind energy Solar energy Biomass energy China's investment

China National Renewable Energy Centre Content A B C D E F G H I China s energy and power generation mix China Renewable Energy Development Hydropower Wind energy Solar energy Biomass energy China's investment

Retail Choice in Electricity: What Have We Learned in 20 Years?

Retail Choice in Electricity: What Have We Learned in 20 Years? Mathew Morey & Laurence Kirsch Christensen Associates Energy Consulting www.caenergy.com March 7, 2016 Presentation Outline Summary Status

Retail Choice in Electricity: What Have We Learned in 20 Years? Mathew Morey & Laurence Kirsch Christensen Associates Energy Consulting www.caenergy.com March 7, 2016 Presentation Outline Summary Status

WIND ENERGY GROUP 3 MEMBERS: ALEJANDRO ESPINOLA JUAN C. ENRIQUEZ LINDA ALAMILLO THOMAS BROWN BRUCE SAENZ

WIND ENERGY GROUP 3 MEMBERS: ALEJANDRO ESPINOLA JUAN C. ENRIQUEZ LINDA ALAMILLO THOMAS BROWN BRUCE SAENZ Overview Problem statement Wind EnergyTechnologies Technical development Status in Renewable Energy

WIND ENERGY GROUP 3 MEMBERS: ALEJANDRO ESPINOLA JUAN C. ENRIQUEZ LINDA ALAMILLO THOMAS BROWN BRUCE SAENZ Overview Problem statement Wind EnergyTechnologies Technical development Status in Renewable Energy

Climate Change and Energy Sector Transformation: Implications for Asia-Pacific Including Japan

Climate Change and Energy Sector Transformation: Implications for Asia-Pacific Including Japan Aligning Policies for the Transition to a Low-carbon Economy: OECD Recommendations and Implications for Asia-Pacific

Climate Change and Energy Sector Transformation: Implications for Asia-Pacific Including Japan Aligning Policies for the Transition to a Low-carbon Economy: OECD Recommendations and Implications for Asia-Pacific

PROVIDER A Case Study for EPC Projects in Pakistan. Jun. 4th, 2012

NORDEX A SOLUTION PROVIDER A Case Study for EPC Projects in Pakistan Jun. 4th, 2012 CONTENT 1. Project background Pakistan wind market environment 2. Wind resources assessment 3. Financial model 4. Project

NORDEX A SOLUTION PROVIDER A Case Study for EPC Projects in Pakistan Jun. 4th, 2012 CONTENT 1. Project background Pakistan wind market environment 2. Wind resources assessment 3. Financial model 4. Project

Physics and engineering of wind power systems

Physics and engineering of wind power systems Hermann-Josef Wagner Institute for Energy Systems and Energy Economy Ruhr-University Bochum, Germany lee@lee.rub.de International School on Energy, Varenna/Lombardy,

Physics and engineering of wind power systems Hermann-Josef Wagner Institute for Energy Systems and Energy Economy Ruhr-University Bochum, Germany lee@lee.rub.de International School on Energy, Varenna/Lombardy,

The challenges of a changing energy landscape

The challenges of a changing energy landscape October 26 th 2016 Maria Pedroso Ferreira EDP Energy Planning maria.pedrosoferreira@edp.pt Agenda 1 A changing energy landscape 2 Challenges and opportunities

The challenges of a changing energy landscape October 26 th 2016 Maria Pedroso Ferreira EDP Energy Planning maria.pedrosoferreira@edp.pt Agenda 1 A changing energy landscape 2 Challenges and opportunities

CONTENTS TABLE OF PART A GLOBAL ENERGY TRENDS PART B SPECIAL FOCUS ON RENEWABLE ENERGY OECD/IEA, 2016 ANNEXES

TABLE OF CONTENTS PART A GLOBAL ENERGY TRENDS PART B SPECIAL FOCUS ON RENEWABLE ENERGY ANNEXES INTRODUCTION AND SCOPE 1 OVERVIEW 2 OIL MARKET OUTLOOK 3 NATURAL GAS MARKET OUTLOOK 4 COAL MARKET OUTLOOK

TABLE OF CONTENTS PART A GLOBAL ENERGY TRENDS PART B SPECIAL FOCUS ON RENEWABLE ENERGY ANNEXES INTRODUCTION AND SCOPE 1 OVERVIEW 2 OIL MARKET OUTLOOK 3 NATURAL GAS MARKET OUTLOOK 4 COAL MARKET OUTLOOK

Click to edit Master title style

Overview of the status of renewable energy policy Click Third and level to market edit development Master title worldwide style Christine Lins Executive Secretary of REN21 Click to edit Master subtitle

Overview of the status of renewable energy policy Click Third and level to market edit development Master title worldwide style Christine Lins Executive Secretary of REN21 Click to edit Master subtitle

Green Engineering Technology Day , Scandic Hotel Kolding. Siemens Wind Power. Hardware In Loop Software Test System

Green Engineering Technology Day 24-03-2010, Scandic Hotel Kolding Siemens Wind Power Hardware In Loop Software Test System Agenda About Siemens Siemens Energy Sector Siemens Wind Power Hardware In Loop

Green Engineering Technology Day 24-03-2010, Scandic Hotel Kolding Siemens Wind Power Hardware In Loop Software Test System Agenda About Siemens Siemens Energy Sector Siemens Wind Power Hardware In Loop

PRICE SETTING IN THE ELECTRICITY MARKETS WITHIN THE EU SINGLE MARKET

PRICE SETTING IN THE ELECTRICITY MARKETS WITHIN THE EU SINGLE MARKET A report to the Committee on Industry, Research and Energy of the European Parliament February, 2006 Outline Characteristics of the

PRICE SETTING IN THE ELECTRICITY MARKETS WITHIN THE EU SINGLE MARKET A report to the Committee on Industry, Research and Energy of the European Parliament February, 2006 Outline Characteristics of the

Wind Power at a Distance: A Voyage around the Globe, the US and Africa

Wind Power at a Distance: A Voyage around the Globe, the US and Africa Jeremy Firestone, Director UD Center for Carbon-free Power Integration April 26, 2016 UD-Africa Energy 2016 1 UD Wind Power Program

Wind Power at a Distance: A Voyage around the Globe, the US and Africa Jeremy Firestone, Director UD Center for Carbon-free Power Integration April 26, 2016 UD-Africa Energy 2016 1 UD Wind Power Program

2 ENERGY TECHNOLOGY RD&D BUDGETS: OVERVIEW (2017 edition) Released in October 2017. The IEA energy RD&D data collection and the analysis presented in this paper were performed by Remi Gigoux under the

2 ENERGY TECHNOLOGY RD&D BUDGETS: OVERVIEW (2017 edition) Released in October 2017. The IEA energy RD&D data collection and the analysis presented in this paper were performed by Remi Gigoux under the

RES forecasting from a TSO perspective

Dr. Alejandro J. Gesino Market Design Renewable Energy TenneT TSO EWEA Technology Workshop: Wind Power Forecasting Rotterdam, The Netherlands. December 4 th 2013 Agenda 1. Role of the German TSOs. 2. TenneT

Dr. Alejandro J. Gesino Market Design Renewable Energy TenneT TSO EWEA Technology Workshop: Wind Power Forecasting Rotterdam, The Netherlands. December 4 th 2013 Agenda 1. Role of the German TSOs. 2. TenneT

Solar Heat Worldwide

Solar Heat Worldwide Markets and Contribution to the Energy Supply 2013 EDITION 2015 Franz Mauthner, Werner Weiss, Monika Spörk-Dür AEE INTEC AEE - Institute for Sustainable Technologies A-8200 Gleisdorf,

Solar Heat Worldwide Markets and Contribution to the Energy Supply 2013 EDITION 2015 Franz Mauthner, Werner Weiss, Monika Spörk-Dür AEE INTEC AEE - Institute for Sustainable Technologies A-8200 Gleisdorf,

Support Schemes for PV in Europe

Support Schemes for PV in Europe EPIA Denis Thomas 1 Presentation overview 1. Main PV support schemes in Europe 2. Support policy vs. Market development: case studies 1. Germany 2. Spain 3. Italy 3. Conclusions

Support Schemes for PV in Europe EPIA Denis Thomas 1 Presentation overview 1. Main PV support schemes in Europe 2. Support policy vs. Market development: case studies 1. Germany 2. Spain 3. Italy 3. Conclusions

China's Green Growth Strategy: Industry Policy or Green Environment Policy?

China's Green Growth Strategy: Industry Policy or Green Environment Policy? Conférence internationale Débattre de l innovation responsable dans les énergies renouvelables et l architecture» 16 novembre

China's Green Growth Strategy: Industry Policy or Green Environment Policy? Conférence internationale Débattre de l innovation responsable dans les énergies renouvelables et l architecture» 16 novembre

Changing the Scale of Offshore Wind: Examining Mega-Projects in the United Kingdom

Changing the Scale of Offshore Wind: Examining Mega-Projects in the United Kingdom SESSION: Wind Energy and the current international situation, Madrid, June 12, 2012 More than 50% of mega-projects are

Changing the Scale of Offshore Wind: Examining Mega-Projects in the United Kingdom SESSION: Wind Energy and the current international situation, Madrid, June 12, 2012 More than 50% of mega-projects are

Medium voltage products. Technical Application Papers No. 17 Smart grids 1. Introduction

Medium voltage products Technical Application Papers No. 17 Smart grids 1. Introduction Contents 2 1. Introduction 8 2 The different components and functions of a smart grid 8 2.1 Integration of distributed

Medium voltage products Technical Application Papers No. 17 Smart grids 1. Introduction Contents 2 1. Introduction 8 2 The different components and functions of a smart grid 8 2.1 Integration of distributed

GE Renewable Energy CAPACITY FACTOR LEADERSHIP IN HIGH WIND REGIMES. GE s

GE Renewable Energy CAPACITY FACTOR LEADERSHIP IN HIGH WIND REGIMES GE s 1.85-82.5 www.ge.com/wind GE S 1.85-82.5 PITCH Since entering the wind industry in 2002, GE Renewable Energy has invested more than

GE Renewable Energy CAPACITY FACTOR LEADERSHIP IN HIGH WIND REGIMES GE s 1.85-82.5 www.ge.com/wind GE S 1.85-82.5 PITCH Since entering the wind industry in 2002, GE Renewable Energy has invested more than

Strategy Profitable Growth for Vestas

Strategy Profitable Growth for Vestas 011 Industry dynamics 013 The strategic direction remains unchanged 013 The four key pillars in Vestas strategy 015 Financial and capital structure targets and priorities

Strategy Profitable Growth for Vestas 011 Industry dynamics 013 The strategic direction remains unchanged 013 The four key pillars in Vestas strategy 015 Financial and capital structure targets and priorities

Siemens Solar Energy. Buenos Aires, November 2011 By Rolf Schumacher R2 Siemens AG All rights reserved

Siemens Solar Energy Buenos Aires, November 2011 By Rolf Schumacher 2010-03-04-R2 Siemens has the answers to your burning questions 1 Why Solar / Renewable Energy? 2 What are the different technologies?

Siemens Solar Energy Buenos Aires, November 2011 By Rolf Schumacher 2010-03-04-R2 Siemens has the answers to your burning questions 1 Why Solar / Renewable Energy? 2 What are the different technologies?

Wind Farms. December Stjepan Čerkez

Wind Farms December 2017 Stjepan Čerkez 2 Contents 1. Introduction 2. Wind Farm Life Cycle 3. Examples of different Technologies 4. Manufacturing and Assembly Process 5. Movie, WF Glunca in Croatia 6.

Wind Farms December 2017 Stjepan Čerkez 2 Contents 1. Introduction 2. Wind Farm Life Cycle 3. Examples of different Technologies 4. Manufacturing and Assembly Process 5. Movie, WF Glunca in Croatia 6.