Commercial Update Beth Hickey Director, Commercial Optimization. Development Update Coralie Sculley Director, Market Development

|

|

|

- Roderick Sutton

- 6 years ago

- Views:

Transcription

1

2 WELCOME TO NAPA

3 Agenda Energy Transfer Update/Overview Gregg Russell Vice President, Marketing Commercial Update Beth Hickey Director, Commercial Optimization Development Update Coralie Sculley Director, Market Development West End Supply Update Pat Anderson Director, Supply Development LNG Development Update Joey Colton Senior Optimization Rep

4 Important Disclosures This communication is based on information which Panhandle Eastern Pipe Line Company, LP, Sea Robin Pipeline Company, LLC, Trunkline Gas Company, LLC and Trunkline LNG Company, LLC (collectively, Company ) believes is reliable. However, Company does not represent or warrant its accuracy. The statements and opinions expressed in this communication represent the views of Company as of the date of this report. These statements and opinions may be subject to change without notice and Company will not be responsible for any consequences associated with reliance on any statement or opinion contained in this communication. Company disclaims any intention or obligation to update any statements or opinions contained in this communication. This communication is confidential and may not be reproduced in whole or in part without prior written permission from Company.

5 Energy Transfer Update/Overview GREGG RUSSELL Vice President, Marketing

6 ETE Organizational Structure Energy Transfer Equity, L.P. (NYSE: ETE) Ownership in RGP 100% RGP IDRs 1.8% General Partner Interest 26.3mm LP units (17% of total) Ownership in ETP 100% ETP IDRs 1.5% General Partner Interest 50.2mm LP units (22% of total) Ownership in SUG 100% SUG Shares Regency Energy Partners LP (NYSE: RGP) Energy Transfer Partners, L.P. (NYSE: ETP) Southern Union Co. Gathering & Processing Midstream SUGS Joint Ventures 30% Lone Star NGL 70% NGL Panhandle Companies LDCs Contract Treating Intrastate Transportation & Storage Contract Compression Interstate Transportation 50% FEP 50% Citrus

22.1 8.")

7 Combined Asset Footprint Natural Gas Assets Energy Transfer Southern Union Combined Miles of Pipeline 23,589 21,169 44,758 Throughput (Bcf/d) Storage (Bcf) Processing Capacity (Bcf/d)

8 Transwestern Pipeline 1.2 Bcf/d Capacity Bi-directional System Accesses Permian, San Juan and Anadarko Basins

9 Tiger Pipeline 2.4 Bcf/d Capacity Serves Haynesville Producers Interconnects with TETCO, TGT, TXG, ANR, CGT, SESH and Trunkline

10 Midcontinent Express Pipeline 1.2 / 1.8 Bcf/d Capacity Interconnects with NGPL, TGT, ANR, CGT, TETCO, SONAT, Destin and Transco 50/50 JV with KMP KMP operates

11 Fayetteville Express 2 Bcf/d Capacity Serves Fayetteville Producers Interconnects with NGPL, TXG, ANR and Trunkline 50/50 JV with KMP

12 Intrastate Assets ETE own/operates the largest intrastate pipeline system in the US 7,700+ miles of pipe moving upwards of 11 Bcf/d 74 Bcf Storage Serves Houston, Austin, Dallas/Ft. Worth & San Antonio Over 30 interconnects with interstate pipelines

13 NGL/Gathering & Processing

14 NGL Assets Hattiesburg Storage Refinery Services Pipeline Transportation 12 inch NGL pipeline 144,000 Bbls/d of capacity 12 pump stations with 21,500 hp Mont Belvieu Storage Sea Robin Plant Fractionation & Processing Two cryogenic processing plants 25,000 Bbl/d fractionator Sea Robin gas processing plant

15 The Future The Sunoco acquisition significantly diversifies ETE s existing infrastructure assets

16 Commercial Update BETH HICKEY Director, Commercial Optimization

17 Winter Record Warmth

18 March 2012 Record Weather

19 Customer Storage Comparison to 5 Year Average 100% 90% 80% 2012% 5 Year Average% 2011% 70% 60% 50% 40% 45.34% 56.69% End of April 2012 Customer Storage % by Segment: PEPL Field: 47.0% PEPL Mkt: 59.2% TGC: 20.8% 30% 20% 10% End of April 5 Year Average Customer Storage % by Segment: PEPL Field: 22.7% PEPL Mkt: 40.5% TGC: 27.5% End of April 2011 Customer Storage % by Segment PEPL Field: 12.9% PEPL Mkt: 44.6% TGC: 37.6% 0% 3/11/2012 4/11/2012 5/11/2012 6/11/2012 7/11/2012 8/11/2012 9/11/ /11/2012

20 Avg Peak Day - Houstonia 1,500,000 1,400,000 1,300,000 1,200,000 1,100,000 1,000, ,000 November December January February March

21 Winter Peak Days through Houstonia 1,600,000 1,500,000 1,400,000 1,300,000 1,200,000 1,100,000 1,000,000 November December January February March

22 Bcf/day (avg) Rockies Express Deliveries 2.0 REX Deliveries by Segment Jan-11 Feb Mar Apr May Jun Jul Aug Sep Oct Nov Dec Jan-12 Feb Mar Apr May* REX-West Upstream of Lebanon Lebanon Downstream of Lebanon * Through 5/17. Data derived from REX capacity postings.

23 Dt/day (avg) Rockies Express Deliveries REX (East) Deliveries - Upstream of Lebanon 180, , , , ,000 80,000 60,000 40,000 20,000 - Jan-12 Feb-12 Mar-12 Apr-12 May-12 Ameren Illinois ANR Citizens Midwestern PEPL Trunkline Vectren Indiana * Through 5/17. Data derived from REX capacity postings.

24 Winter Peak Days through Independence 1,400,000 1,200,000 1,000, , ,000 November December January February March

25 Winter Daily Avg of Zone 1A Receipts 1,400,000 1,200,000 1,000, , , , , November December January February March

26 Z1A Average Daily Receipt Quantities January 2012 April , , , , , , , ,000 0 Jan-12 Feb-12 Mar-12 Apr-12 Richland Parish Regency Tiger Interconnect Bobo Road Olla- Gulf South Acadian McNutt TGC Receipt

27 Summer Maintenance PEPL Major work Haven 400 line beginning June 2012 Trunkline Cypress outage June 2012 (see critical posting)

28 PEPL Operational Constraints Tuscola Haven Edgerton Houstonia

29 Johnsonville Trunkline Operational Constraints Joppa Dyersburg Texas Gas Greenville Lateral Cap 500,000 Independence Shaw Fayetteville Express Bobo Road Cap 900,000 Centerpoint - Perryville Cap 70,000 Centerpoint Richland Parish Cap 1,000,000 Pollock Epps ETC - Tiger Cap 566,000 Gulf South - Olla Cap 700,000 Regency Cap 1,000,000 Crosstex - Mcnutt Cap 380,000 Longville Acadian Cap 500,000

30 Total Consumption MCF Panhandle Powerplant Consumption 6,000,000 $8.00 $7.55 5,000,000 $6.08 $7.00 $6.00 4,000,000 $5.00 3,000,000 $3.88 $3.96 $4.00 2,000,000 $3.08 $3.00 $2.00 1,000,000 $ Summer 2008 Summer 2009 Summer 2010 Summer 2011 Summer $0.00

31 Total Consumption MCF Trunkline Powerplant Consumption 6,000,000 5,000,000 $9.69 $10.00 $8.00 4,000,000 $6.84 3,000,000 $6.00 2,000,000 $3.53 $4.18 $4.15 $4.00 1,000,000 $ Summer 2008 Summer 2009 Summer 2010 Summer 2011 Summer $0.00

32 What could the summer bring

33 PEPL Mid Season Fuel Filing Due to Record winter weather Historically high storage inventory Lower fuel consumption PEPL fuel tracker is highly over recovered Possible midcycle fuel filing to lower fuel rates

34 Tropical Activity Forecast Named Storms Hurricanes Major Hurricanes MDA CSU WSI Accuweather TSR TWC AVG NOAA AVG 0 6 0

35 Reservation Charge Crediting (RCC) - PEPL March 1, 2012 fuel rate filing for fuel rates effective April 1, 2012 March 14, 2012 customer protest that PEPL s tariff did not include RCC March 30, 2012 Fuel rates approved and show cause order issued by FERC April 30, 2012 filed explanation to show cause order and request for rehearing Currently waiting on Commissions response

36 Development Update CORALIE SCULLEY Director, Market Development

37 Proposed Offshore Asset Consolidation Combined Asset Map

38 Proposed Offshore Asset Consolidation Summary and Expected Timeline Sea Robin to acquire Trunkline s offshore assets, including Terrebonne System Vermilion System Partial ownership interest in the Brazos A-47 system Offshore Terrebonne & Vermilion Systems remain FERC regulated Maintains rate & service protection for shippers on these systems Shipper access to offshore supplies will be maintained at three onshore receipt points: Terrebonne System - just upstream of the Patterson Compressor Station at both the Neptune and Patterson II processing plants Vermilion System - just upstream of the Kaplan Compressor Station at the Cow Island Meter Station Joint FERC filing by Trunkline and Sea Robin occurred on Oct. 7, 2011 Receipt of FERC approvals expected mid-2012 Initiation of Sea Robin s Terrebonne and Vermilion offshore service to commence upon receipt of FERC approval

39 Northeast Gas Supply Utica Shale Overview The Utica Shale formation lies 3,000 to 7,000 feet below the Marcellus Shale Estimated recoverable potential: 1.3 to 5.5 billion barrels of oil 3.8 to 5.7 Tcf of natural gas Major producers active in the play include Anadarko, Chesapeake, Devon, Enervest, Hess

40 Jan-11 Feb-11 Mar-11 Apr-11 May-11 Jun-11 Jul-11 Aug-11 Sep-11 Oct-11 Nov-11 Dec-11 Jan-12 Feb-12 Mar-12 Apr-12 Utica Shale Activity in Ohio Horizontal Well Activity Horizontal Well Permits Issued Jan Apr 12 = Total 2011 = Ohio Dept of Natural Resources

41 Northeast Gas Supply Where is it Going? Most new pipeline projects out of the Northeast are designed to serve historically premium markets: Boston/New England New Jersey/NewYork Other project destinations: Eastern Canada via Niagara Mid-Atlantic Southeast

42 Northeast Gas Supply Where Else Can It Go? Michigan Storage Marcellus and Utica supply Gas City Perryville, Henry Hub, LNG Exports, Gulf Coast Industrials Lebanon Hub: Columbia Dominion REX TETCO TX Gas

43 West End Supply Update PAT ANDERSON Director, Supply Development

44 Shale Plays Near Panhandle Mississippian Lime Core Mississippian Excello- Mulky Granite Wash Woodford/Cana Fayetteville Woodford Caney Bend Woodford Barnett

45 Mississippian Lime Encompasses ~17 million prospective acres across Oklahoma and Kansas Relatively shallow depth of 4,000-6,000 ft Quickly becoming one of the hottest onshore oil plays in the country Typical wells producing roughly 50% gas and 50% oil Lower well costs and better rates of return than Bakken wells

46 Mississippian Lime Activity

47 NGP Straddle Plant Located adjacent to the Haven Compressor station Capable of processing 1.4 Bcf/d Projected in-service date 4Q 2013 Existing gas stream processing but capable of handling richer gas streams

48 National Helium Upgrade DCP Midstream, LP is upgrading its National Helium Plant (NH) in Liberal Kansas NH is the largest plant in the Midcontinent, capable of processing more than 600 MMcf per day Connect NH to its Southern Hills NGL pipeline Southern Hills will have over 150,000 barrels per day of capacity and be operational in mid-2013

49 New Interconnections NGP Plant 3Q MM 3Q MM 4Q MM 3Q MM 1Q MM 1Q MM 3Q 13

50 LNG Development Update JOEY COLTON Senior Optimization Rep

- 37 Capacity -")

51 U.S. LNG Exports LNG Reference Material Production Pipeline Liquefaction Shipping Regasification Natural Gas/LNG Conversion Volume Reduction - 620:1 LNG Temperature Minus F 1 mtpa = 142,900 Mcf/d Typical LNG Shipping/Tankers Length Width Draft (Underwater) - 37 Capacity - 160,000 cm 3 (2.7 Bcf) Cost - ~$200 MM

52 U.S. LNG Exports Trunkline LNG Terminal Lake Charles, LA Year Milestone 1978 Construction begins 1982 Construction complete 6.3 Bcf of storage in 3 LNG storage tanks 630,000 Mcf/d of sendout capacity 1984 Terminal put in standby mode 1989 Terminal re-activated 2001 BG Group signs firm capacity agreement 2002 Phase I Expansion agreement signed Cargoes Received Phase II Expansion agreement signed Phase I & II Expansion placed in-service Storage capacity increased to 9 Bcf (1 additional tank) Sendout capacity increased to 1.8 Bcf/d (2.1 Bcf/d peak) Addition of second unloading dock Infrastructure Enhancement Project (IEP) agreement executed 2010 IEP placed in-service Ambient Air Vaporization of sendout Liquids extraction capacity of 1.1 Bcf/d

53 Cargoes Received Trunkline LNG Lake Charles Total Cargoes Received =

54 U.S. LNG Exports The Import Phenomenon Re-visited (2008)

55 U.S. LNG Exports North American Import Terminals (2012)

1.40 Approved Under Review Freeport LNG (Phase II) 1.")

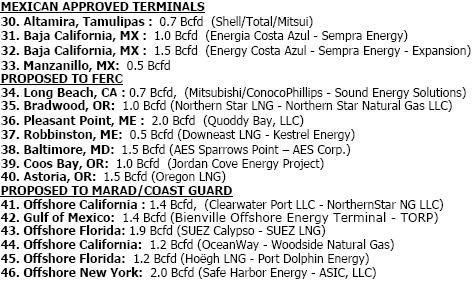

56 U.S. LNG Exports DOE Applications & Approvals Applications Received by DOE to Export Domestically Produced LNG from the Lower-48 States (as of May 7, 2012) Total Quantity (Bcf/d) FTA Applications Non-FTA Applications Cheniere Sabine Pass 2.20 Approved Approved Freeport LNG (Phase I) 1.40 Approved Under Review Freeport LNG (Phase II) 1.40 Approved Under Review Lake Charles Exports (Trunkline LNG) 2.00 Approved Under Review Carib Energy 0.03 Approved Under Review Dominion Cove Point 1.00 Approved Under Review Jordan Cove 1.20 Approved Under Review Sempra Cameron LNG 1.70 Approved Under Review Gulf Coast LNG 2.80 Under Review Under Review Cambridge Energy 0.27 Pending Approval N/A Gulf LNG Liquefaction Company, LLC 1.50 Pending Approval N/A LNG Development Comp. (Oregon LNG) 1.25 Pending Approval N/A SB Power Solutions Inc Pending Approval N/A Total Applications 16.82

57 U.S. LNG Exports Current FERC Proposals

58 U.S. LNG Exports Proximity to Trunkline Gas Pipeline Trunkline LNG Kountze Longville Cypress Centerville Patterson Edna Sabine Pass LNG Cameron LNG Beeville Freeport LNG Sea Robin Terrebonne Creole Trail Pipeline KM Louisiana Pipeline Cameron/LA STG Pipeline Trunkline

59 Thank You WE HOPE YOU ENJOY THE REST OF YOUR STAY

Spectra Energy: Moving Ahead, Gaining Momentum

8 th ANNUAL PLATTS PIPELINE EXPANSION & DEVELOPMENT CONFERENCE HOUSTON, TX SEPTEMBER 17, 2013 Spectra Energy: Greg Crisp Director, Business Development Safe Harbor Statement Some of the statements in this

8 th ANNUAL PLATTS PIPELINE EXPANSION & DEVELOPMENT CONFERENCE HOUSTON, TX SEPTEMBER 17, 2013 Spectra Energy: Greg Crisp Director, Business Development Safe Harbor Statement Some of the statements in this

ENERGY TRANSFER ROVER PIPELINE. Beth Hickey - Sr. Vice President, Interstate

ENERGY TRANSFER ROVER PIPELINE Beth Hickey - Sr. Vice President, Interstate ENERGY TRANSFER ASSET OVERVIEW Excludes retail locations ETP Assets Marcus Hook SXL Assets Eagle Point Nederland 2 ENERGY TRANSFER

ENERGY TRANSFER ROVER PIPELINE Beth Hickey - Sr. Vice President, Interstate ENERGY TRANSFER ASSET OVERVIEW Excludes retail locations ETP Assets Marcus Hook SXL Assets Eagle Point Nederland 2 ENERGY TRANSFER

NEXUS Gas Transmission

NEXUS Gas Transmission Bringing New Supplies to Market Ohio Manufacturers Association - October 2012 Agenda Project Introduction Utica and Marcellus Gas Supply Michigan and Ontario Markets Conclusion &

NEXUS Gas Transmission Bringing New Supplies to Market Ohio Manufacturers Association - October 2012 Agenda Project Introduction Utica and Marcellus Gas Supply Michigan and Ontario Markets Conclusion &

TransCanada U.S. Pipelines Central ANR Pipeline, ANR Storage, and Great Lakes Gas

TransCanada U.S. Pipelines Central ANR Pipeline, ANR Storage, and Great Lakes Gas SNAME Conference Great Lakes-Great Rivers Section February 13-14, 2013 Natural Gas Basics Players and Functions 1. Exploration

TransCanada U.S. Pipelines Central ANR Pipeline, ANR Storage, and Great Lakes Gas SNAME Conference Great Lakes-Great Rivers Section February 13-14, 2013 Natural Gas Basics Players and Functions 1. Exploration

Tennessee Gas Pipeline Co, L.L.C. Northeast Energy and Commerce Association September 27, 2012

Tennessee Gas Pipeline Co, L.L.C. Northeast Energy and Commerce Association September 27, 2012 The Kinder Morgan System 4 th largest energy company in North America Enterprise value ~ $95 billion Largest

Tennessee Gas Pipeline Co, L.L.C. Northeast Energy and Commerce Association September 27, 2012 The Kinder Morgan System 4 th largest energy company in North America Enterprise value ~ $95 billion Largest

CBIA Energy Conference Natural Gas- Coming to Your Neighborhood Soon October 10, 2013 Cromwell, Connecticut Michael Dirrane Director, Northeast

CBIA Energy Conference Natural Gas- Coming to Your Neighborhood Soon October 10, 2013 Cromwell, Connecticut Michael Dirrane Director, Northeast Marketing Spectra Energy U.S. Transmission Map Miles of Pipe

CBIA Energy Conference Natural Gas- Coming to Your Neighborhood Soon October 10, 2013 Cromwell, Connecticut Michael Dirrane Director, Northeast Marketing Spectra Energy U.S. Transmission Map Miles of Pipe

Major Changes in Natural Gas Transportation Capacity,

Major Changes in Natural Gas Transportation, The following presentation was prepared to illustrate graphically the areas of major growth on the national natural gas pipeline transmission network between

Major Changes in Natural Gas Transportation, The following presentation was prepared to illustrate graphically the areas of major growth on the national natural gas pipeline transmission network between

Building Pipelines Continuous Improvement (QA/QC) Business Environment

Business Environment") Building Pipelines Continuous Improvement (QA/QC) Business Environment The INGAA Foundation Inc. Building Interstate Natural Gas Pipelines Continuous Improvement (QA/QC) Workshop Houston, Texas March 25

Building Pipelines Continuous Improvement (QA/QC) Business Environment The INGAA Foundation Inc. Building Interstate Natural Gas Pipelines Continuous Improvement (QA/QC) Workshop Houston, Texas March 25

Natural Gas Outlook and Drivers

Natural Gas Outlook and Drivers November 2012 33% BENTEK Energy 5% 40% Who We Are Based in Evergreen, CO 120 People 400+ Customers Subsidiary of McGraw-Hill/Platts 22% What We Do Collect, Analyze and Distribute

Natural Gas Outlook and Drivers November 2012 33% BENTEK Energy 5% 40% Who We Are Based in Evergreen, CO 120 People 400+ Customers Subsidiary of McGraw-Hill/Platts 22% What We Do Collect, Analyze and Distribute

Natural Gas Market Update

Natural Gas Market Update John Jicha - MGE Director - Energy Supply and Trading Madison Gas and Electric Company Agenda What a difference ten years can make Low prices Fundamental factors impacting the

Natural Gas Market Update John Jicha - MGE Director - Energy Supply and Trading Madison Gas and Electric Company Agenda What a difference ten years can make Low prices Fundamental factors impacting the

The Energy Consortium Recent Developments and the Outlook for Natural Gas in the Northeast. John R. Bitler October 20, 2010

The Energy Consortium Recent Developments and the Outlook for Natural Gas in the Northeast John R. Bitler October 20, 2010 Northeast Overview Traditional Sources of Supply Gulf Coast Western Canada (WCSB)

The Energy Consortium Recent Developments and the Outlook for Natural Gas in the Northeast John R. Bitler October 20, 2010 Northeast Overview Traditional Sources of Supply Gulf Coast Western Canada (WCSB)

Background, Issues, and Trends in Underground Hydrocarbon Storage

Background, Issues, and Trends in Underground Hydrocarbon Storage David E. Dismukes Center for Energy Studies Louisiana State University Environmental Permitting Class January 29, 2009 Description of the

Background, Issues, and Trends in Underground Hydrocarbon Storage David E. Dismukes Center for Energy Studies Louisiana State University Environmental Permitting Class January 29, 2009 Description of the

Business Development Outlook. Paul Smith Director, Business Development

Business Development Outlook Paul Smith Director, Business Development 1 Development Trends TGP projects nearing in-service Supply Push: Susquehanna West: 145k In Service (9/1) Orion: 135k 11/1/2017 Broad

Business Development Outlook Paul Smith Director, Business Development 1 Development Trends TGP projects nearing in-service Supply Push: Susquehanna West: 145k In Service (9/1) Orion: 135k 11/1/2017 Broad

National Association of Publicly Traded Partnerships MLP Conference Presentation New York, New York May 21, 2008

National Association of Publicly Traded Partnerships MLP Conference Presentation New York, New York May 21, 2008 Safe Harbor Statement Some of the statements in this document concerning future company

National Association of Publicly Traded Partnerships MLP Conference Presentation New York, New York May 21, 2008 Safe Harbor Statement Some of the statements in this document concerning future company

Winter U.S. Natural Gas Production and Supply Outlook

Winter 2010-11 U.S. Natural Gas Production and Supply Outlook Prepared for Natural Gas Supply Association by: ICF International Fairfax, Virginia September, 2010 Introduction This report presents ICF s

Winter 2010-11 U.S. Natural Gas Production and Supply Outlook Prepared for Natural Gas Supply Association by: ICF International Fairfax, Virginia September, 2010 Introduction This report presents ICF s

Enable Midstream Partners Transportation & Storage

Enable Midstream Partners Transportation & Storage Natural Gas Society of East Texas Roundtable March 19, 2015 Carol Burchfield EMP Corporate Structure 2 Enable Midstream Partners Diverse Set of Interconnected

Enable Midstream Partners Transportation & Storage Natural Gas Society of East Texas Roundtable March 19, 2015 Carol Burchfield EMP Corporate Structure 2 Enable Midstream Partners Diverse Set of Interconnected

Platts NGLs Conference. September 24, 2013

Platts NGLs Conference September 24, 2013 Agenda 2013 - Executing the Plan 2014 Responding to Delineation Results 2015 Major Ramp Up 2016 Utica to Reach 50% of Marcellus Wet Conclusions 1 Executing the

Platts NGLs Conference September 24, 2013 Agenda 2013 - Executing the Plan 2014 Responding to Delineation Results 2015 Major Ramp Up 2016 Utica to Reach 50% of Marcellus Wet Conclusions 1 Executing the

Natural Gas Market Update

Natural Gas Market Update Bob Yu, Senior Analyst Quantitative Modeling September 2017 Restrictions on Use: You may use the prices, indexes, assessments and other related information (collectively, Data

Natural Gas Market Update Bob Yu, Senior Analyst Quantitative Modeling September 2017 Restrictions on Use: You may use the prices, indexes, assessments and other related information (collectively, Data

CERI Commodity Report Natural Gas

CERI Commodity Report Natural Gas November-December 15 The Energy Information Administration s New Storage Classifications Paul Kralovic November 19, 15 was an important date for the Energy Information

CERI Commodity Report Natural Gas November-December 15 The Energy Information Administration s New Storage Classifications Paul Kralovic November 19, 15 was an important date for the Energy Information

ENERGY TRANSFER PARTNERS, L.P. Bakken Pipeline System Overview & Quality Update February 22, 2018

ENERGY TRANSFER PARTNERS, L.P. Bakken Pipeline System Overview & Quality Update February 22, 2018 ETP S INTEGRATED HYDROCARBON BUSINESS Asset Overview Recently In-service & Announced Growth Projects ETP

ENERGY TRANSFER PARTNERS, L.P. Bakken Pipeline System Overview & Quality Update February 22, 2018 ETP S INTEGRATED HYDROCARBON BUSINESS Asset Overview Recently In-service & Announced Growth Projects ETP

The Shale Invasion: Will U.S. LNG Cross the Pond? New terminals ramp up exports.

? The Shale Invasion: Will U.S. LNG Cross the Pond? New terminals ramp up exports. Morningstar Commodities Research 6 December 2016 Sandy Fielden Director, Oil and Products Research +1 512 431-8044 sandy.fielden@morningstar.com

? The Shale Invasion: Will U.S. LNG Cross the Pond? New terminals ramp up exports. Morningstar Commodities Research 6 December 2016 Sandy Fielden Director, Oil and Products Research +1 512 431-8044 sandy.fielden@morningstar.com

New Jersey Natural Gas Market Update

March 25, 2015 Mullica Hill, NJ New Jersey Natural Gas Market Update Presentation to: SNJDC Natural Gas Seminar Tom Kiley Northeast Gas Association Issues Regional Market Developments New Jersey Gas Market

March 25, 2015 Mullica Hill, NJ New Jersey Natural Gas Market Update Presentation to: SNJDC Natural Gas Seminar Tom Kiley Northeast Gas Association Issues Regional Market Developments New Jersey Gas Market

Expanding Existing Pipeline Capacity to Meet New England s Energy Needs. Mike Dirrane Director, Marketing

Expanding Existing Pipeline Capacity to Meet New England s Energy Needs Mike Dirrane Director, Marketing January 27, 2015 Spectra Energy s Portfolio of Assets Based in Houston, TX with operations in 30

Expanding Existing Pipeline Capacity to Meet New England s Energy Needs Mike Dirrane Director, Marketing January 27, 2015 Spectra Energy s Portfolio of Assets Based in Houston, TX with operations in 30

Ten Years After Gas & Power in Perspective

Regional Market Trends Forum Ten Years After Gas & Power in Perspective Richard Levitan, rll@levitan.com May 1, 2014 Agenda 2014 Polar Vortex v. 2004 Cold Snap Northeast Gas & Power 10 Years After Gas

Regional Market Trends Forum Ten Years After Gas & Power in Perspective Richard Levitan, rll@levitan.com May 1, 2014 Agenda 2014 Polar Vortex v. 2004 Cold Snap Northeast Gas & Power 10 Years After Gas

SUEZ LNG NA: A Leading Player in the U.S. LNG Market. Clay Harris, CEO of SUEZ LNG NA LLC May 30,2007

SUEZ LNG NA: A Leading Player in the U.S. LNG Market Clay Harris, CEO of SUEZ LNG NA LLC May 30,2007 Disclaimer Important Information This communication does not constitute an offer to sell or the solicitation

SUEZ LNG NA: A Leading Player in the U.S. LNG Market Clay Harris, CEO of SUEZ LNG NA LLC May 30,2007 Disclaimer Important Information This communication does not constitute an offer to sell or the solicitation

LNG Impact on U.S. Domestic Natural Gas Markets

LNG Impact on U.S. Domestic Natural Gas Markets Disclaimer This presentation contains statements about future events and expectations that can be characterized as forward-looking statements, including,

LNG Impact on U.S. Domestic Natural Gas Markets Disclaimer This presentation contains statements about future events and expectations that can be characterized as forward-looking statements, including,

AES CORPORATION. LNG Review. Aaron Samson Director, LNG Projects

AES CORPORATION LNG Review Aaron Samson Director, LNG Projects December 11, 2006 Safe Harbor Disclosure Certain statements in the following presentation regarding AES s business operations may constitute

AES CORPORATION LNG Review Aaron Samson Director, LNG Projects December 11, 2006 Safe Harbor Disclosure Certain statements in the following presentation regarding AES s business operations may constitute

Appendix A. Project Description

Appendix A Project Description I. Project Summary 1. The proposed Jordan Cove LNG export terminal ( Jordan Cove ) is a facility designed to produce and export liquefied natural gas ( LNG ). Jordan Cove

Appendix A Project Description I. Project Summary 1. The proposed Jordan Cove LNG export terminal ( Jordan Cove ) is a facility designed to produce and export liquefied natural gas ( LNG ). Jordan Cove

EIA Winter Fuels Outlook

EIA Winter Fuels Outlook For Washington, D.C. By Adam Sieminski, Administrator, U.S. Energy Information Administration U.S. Energy Information Administration Independent Statistics & Analysis www.eia.gov

EIA Winter Fuels Outlook For Washington, D.C. By Adam Sieminski, Administrator, U.S. Energy Information Administration U.S. Energy Information Administration Independent Statistics & Analysis www.eia.gov

Investor Chat Series December 17, Tom O Connor. President & CEO Duke Energy Gas Transmission

Investor Chat Series December 17, 2004 Tom O Connor President & CEO Duke Energy Gas Transmission Safe Harbor Statement Under the Private Securities Litigation Act of 1995 This document contains forward

Investor Chat Series December 17, 2004 Tom O Connor President & CEO Duke Energy Gas Transmission Safe Harbor Statement Under the Private Securities Litigation Act of 1995 This document contains forward

Natural Gas Next: Texas and Southeast Gulf Outlook. Charles Nevle Vice President. September 25, 2017

Natural Gas Next: Texas and Southeast Gulf Outlook Charles Nevle Vice President September 25, 2017 Texas and Southeast Overview Irma and Harvey impact. Production: Permian, Eagle Ford and Haynesville.

Natural Gas Next: Texas and Southeast Gulf Outlook Charles Nevle Vice President September 25, 2017 Texas and Southeast Overview Irma and Harvey impact. Production: Permian, Eagle Ford and Haynesville.

Natural Gas Pipelines

Natural Gas Pipelines Steve Kean and Tom Martin President Natural Gas Pipeline Group Overview Market Environment Transport spreads have flattened Storage spreads remain strong Processing margins expected

Natural Gas Pipelines Steve Kean and Tom Martin President Natural Gas Pipeline Group Overview Market Environment Transport spreads have flattened Storage spreads remain strong Processing margins expected

Infrastructure Fundamentals in Shale Rich Ohio

Infrastructure Fundamentals in Shale Rich Ohio Tony Blando Vice President - Marketing NiSource Midstream OGA 2014 Market Conditions Conference July 15, 2014 Columbus, Ohio A New and Dynamic Industry A

Infrastructure Fundamentals in Shale Rich Ohio Tony Blando Vice President - Marketing NiSource Midstream OGA 2014 Market Conditions Conference July 15, 2014 Columbus, Ohio A New and Dynamic Industry A

Albany, NY December 1, Natural Gas Outlook. Presentation to: Northeast Power Coordinating Council (NPCC) General Meeting

General Meeting") Albany, NY December 1, 2010 Natural Gas Outlook Presentation to: Northeast Power Coordinating Council (NPCC) General Meeting Stephen Leahy Northeast Gas Association Topics Gas Market Conditions Gas Supply

Albany, NY December 1, 2010 Natural Gas Outlook Presentation to: Northeast Power Coordinating Council (NPCC) General Meeting Stephen Leahy Northeast Gas Association Topics Gas Market Conditions Gas Supply

2005 North American Natural Gas Outlook Client Presentation

2005 North American Natural Gas Outlook Client Presentation January 17, 2005 Ron Denhardt Vice President, Natural Gas Services Strategic Energy & Economic Research Inc. 781 756 0550 (Tel) Copyright 2004

2005 North American Natural Gas Outlook Client Presentation January 17, 2005 Ron Denhardt Vice President, Natural Gas Services Strategic Energy & Economic Research Inc. 781 756 0550 (Tel) Copyright 2004

CERI Commodity Report Natural Gas

September 1 CERI Commodity Report Natural Gas Natural Gas Prices Paul Kralovic The Commodity Report Natural Gas article, Turm-oil in the Natural Gas Markets, released in February 1, explored the low natural

September 1 CERI Commodity Report Natural Gas Natural Gas Prices Paul Kralovic The Commodity Report Natural Gas article, Turm-oil in the Natural Gas Markets, released in February 1, explored the low natural

East Tennessee Natural Gas. Shipper Meeting. Fox Den Country Club Knoxville, TN April 20, 2017

East Tennessee Natural Gas Shipper Meeting Fox Den Country Club Knoxville, TN April 20, 2017 Safe Harbor Statement Some of what we ll discuss today concerning future company performance will be forward-looking

East Tennessee Natural Gas Shipper Meeting Fox Den Country Club Knoxville, TN April 20, 2017 Safe Harbor Statement Some of what we ll discuss today concerning future company performance will be forward-looking

CenterPoint Energy Services. Current Market Fundamentals June 27, 2013

CenterPoint Energy Services Current Market Fundamentals June 27, 2013 CenterPoint Energy is one of the largest combined electric and natural gas delivery companies in the U.S. Asset portfolio CNP Footprint

CenterPoint Energy Services Current Market Fundamentals June 27, 2013 CenterPoint Energy is one of the largest combined electric and natural gas delivery companies in the U.S. Asset portfolio CNP Footprint

North America Midstream Infrastructure through 2035: Capitalizing on Our Energy Abundance

North America Midstream Infrastructure through 2035: Capitalizing on Our Energy Abundance Prepared by ICF International for The INGAA Foundation, Inc. Support provided by America s Natural Gas Alliance

North America Midstream Infrastructure through 2035: Capitalizing on Our Energy Abundance Prepared by ICF International for The INGAA Foundation, Inc. Support provided by America s Natural Gas Alliance

Platts 8 th Annual Pipeline Development & Expansion Conference. Gas-Electric Coordination Update

Platts 8 th Annual Pipeline Development & Expansion Conference Gas-Electric Coordination Update Anders Johnson, Director System Design KinderMorgan Pipelines September 17, 2013 Hilton Houston Post Oak,

Platts 8 th Annual Pipeline Development & Expansion Conference Gas-Electric Coordination Update Anders Johnson, Director System Design KinderMorgan Pipelines September 17, 2013 Hilton Houston Post Oak,

Director TGP Facility Planning and Gas Control June 3, Prepared for the Harvard Electricity Policy Group

www.elpaso.com NYSE:EP Anders Johnson Director TGP Facility Planning and Gas Control June 3, 2011 Prepared for the Harvard Electricity Policy Group D E P E N D A B L E N A T U R A L G A S El Paso Corporation

www.elpaso.com NYSE:EP Anders Johnson Director TGP Facility Planning and Gas Control June 3, 2011 Prepared for the Harvard Electricity Policy Group D E P E N D A B L E N A T U R A L G A S El Paso Corporation

ENERGY. Responding to the Upstream Boom

ENERGY Responding to the Upstream Boom CURRENT OPPORTUNITIES AND CHALLENGES IN MIDSTREAM/LNG 1 GROWTH Responding to demand for new and expanded oil and gas processing, transportation and storage following

ENERGY Responding to the Upstream Boom CURRENT OPPORTUNITIES AND CHALLENGES IN MIDSTREAM/LNG 1 GROWTH Responding to demand for new and expanded oil and gas processing, transportation and storage following

Permian to Katy Pipeline. Non-Binding Open Season

August - September 2017 TABLE OF CONTENTS Notice of Open Season and Project Overview...3 P2K Katy Hub...4 Anchor Shipper Status...6 Length of Open Season...6 Participation in the...6 Bid Evaluation Criteria...7

August - September 2017 TABLE OF CONTENTS Notice of Open Season and Project Overview...3 P2K Katy Hub...4 Anchor Shipper Status...6 Length of Open Season...6 Participation in the...6 Bid Evaluation Criteria...7

Increasing Industrial Demand As Easy (or not) as 1, 2, 3

as 1, 2, 3") Increasing Industrial Demand As Easy (or not) as 1, 2, 3 Marcellus & Manufacturing Conference Charleston, WV March 23, 2016 API s Market Development Group API is the only national trade association representing

Increasing Industrial Demand As Easy (or not) as 1, 2, 3 Marcellus & Manufacturing Conference Charleston, WV March 23, 2016 API s Market Development Group API is the only national trade association representing

Regasification N. Atlantic

North Atlantic Basin LNG Week in Review 1 The report is for the week ending December 13. Table 1 to the right tracks 2013 LNG consumption in the Atlantic Basin through December 13 versus the same time

North Atlantic Basin LNG Week in Review 1 The report is for the week ending December 13. Table 1 to the right tracks 2013 LNG consumption in the Atlantic Basin through December 13 versus the same time

Review of Pipeline Regions

Review of Pipeline Regions 76 Eastern Pipelines 77 Eastern Pipeline Group Overview Strategic Initiatives Project Development New Business Platforms Summary 78 Eastern Pipelines Great Lakes Gas Transmission

Review of Pipeline Regions 76 Eastern Pipelines 77 Eastern Pipeline Group Overview Strategic Initiatives Project Development New Business Platforms Summary 78 Eastern Pipelines Great Lakes Gas Transmission

What s next for Alaska gas

What s next for Alaska gas Will markets, competition, politics and federal laws get in the way of a pipeline Larry Persily, Alaska North Slope Gas Line Federal Coordinator Nov. 9, 2012 Commonwealth North

What s next for Alaska gas Will markets, competition, politics and federal laws get in the way of a pipeline Larry Persily, Alaska North Slope Gas Line Federal Coordinator Nov. 9, 2012 Commonwealth North

PBF Energy. State College, PA. North East Association of Rail Shippers Fall Conference. October 1, 2014

PBF Energy North East Association of Rail Shippers Fall Conference State College, PA October 1, 2014 Safe Harbor Statements This presentation contains forward-looking statements made by PBF Energy Inc.

PBF Energy North East Association of Rail Shippers Fall Conference State College, PA October 1, 2014 Safe Harbor Statements This presentation contains forward-looking statements made by PBF Energy Inc.

AEE New England New England Energy Update 1/6/2016. Tim Bigler Senior Market Strategist

AEE New England New England Energy Update 1/6/2016 Tim Bigler Senior Market Strategist Agenda NYMEX NG/Oil Prices New England NG/Electric Prices Future Gas Produc:on Influences New England NG Pipeline

AEE New England New England Energy Update 1/6/2016 Tim Bigler Senior Market Strategist Agenda NYMEX NG/Oil Prices New England NG/Electric Prices Future Gas Produc:on Influences New England NG Pipeline

Vector Pipeline TM. Vector Pipeline. Customer Meeting Nashville, Tennessee September 21, 2017

Vector Pipeline Customer Meeting Nashville, Tennessee September 21, 2017 Amy Bruhn Sr Manager, Transportation Services Mastio Customer Survey Baseline Requirements Items a company is expected to be competent

Vector Pipeline Customer Meeting Nashville, Tennessee September 21, 2017 Amy Bruhn Sr Manager, Transportation Services Mastio Customer Survey Baseline Requirements Items a company is expected to be competent

Trends, Issues and Market Changes for Crude Oil and Natural Gas

Trends, Issues and Market Changes for Crude Oil and Natural Gas East Iberville Community Advisory Panel Meeting Syngenta September 26, 2012 Center for Energy Studies David E. Dismukes, Ph.D. Center for

Trends, Issues and Market Changes for Crude Oil and Natural Gas East Iberville Community Advisory Panel Meeting Syngenta September 26, 2012 Center for Energy Studies David E. Dismukes, Ph.D. Center for

Pipeline Experts. Pipelines are back in business was the consensus of top industry. Expect Major Construction Boom. by Rita Tubb Managing Editor

by Rita Tubb Managing Editor Pipeline Experts Expect Major Construction Boom UC Home Permission to Copy Order Reprints Pipelines are back in business was the consensus of top industry executives at the

by Rita Tubb Managing Editor Pipeline Experts Expect Major Construction Boom UC Home Permission to Copy Order Reprints Pipelines are back in business was the consensus of top industry executives at the

The impact of US LNG on European gas prices

January 2018 The impact of US LNG on European gas prices Increasing US exports of LNG will change how gas prices are determined in Europe Import dependency for the European Union, pushed higher as a result

January 2018 The impact of US LNG on European gas prices Increasing US exports of LNG will change how gas prices are determined in Europe Import dependency for the European Union, pushed higher as a result

Performance of Industry Shale Plays. Rob Sutton February 23, 2010

Performance of Industry Shale Plays Rob Sutton February 23, 21 U.S. Shale Plays Swift Bakken Antrim Nortonville Paradox Gallup New Albany Brown Coffee Devonian Marcellus Ohio Queenston Abo Waddell Barnett

Performance of Industry Shale Plays Rob Sutton February 23, 21 U.S. Shale Plays Swift Bakken Antrim Nortonville Paradox Gallup New Albany Brown Coffee Devonian Marcellus Ohio Queenston Abo Waddell Barnett

OIL AND GAS OUTLOOK: HOW ARE THE ENERGY MARKET AFFECTING METALS? Nicole Leonard, Project Manager, Oil & Gas Consulting Services November 2015

OIL AND GAS OUTLOOK: HOW ARE THE ENERGY MARKET AFFECTING METALS? Nicole Leonard, Project Manager, Oil & Gas Consulting Services November 2015 KEY TAKEAWAYS Macroeconomic outlook: Prices have collapsed

OIL AND GAS OUTLOOK: HOW ARE THE ENERGY MARKET AFFECTING METALS? Nicole Leonard, Project Manager, Oil & Gas Consulting Services November 2015 KEY TAKEAWAYS Macroeconomic outlook: Prices have collapsed

Evaluating the Impacts of Market Shifts on Local Markets and Assets. Ron Norman May 20, 2009

Evaluating the Impacts of Market Shifts on Local Markets and Assets Ron Norman May 20, 2009 Gas market outlooks are only one component of an effective marketing or procurement strategy Agenda Gas Market

Evaluating the Impacts of Market Shifts on Local Markets and Assets Ron Norman May 20, 2009 Gas market outlooks are only one component of an effective marketing or procurement strategy Agenda Gas Market

Algonquin Gas Quality Technical Conference August 21, 2007 Weaver s Cove Energy

Algonquin Gas Quality Technical Conference August 21, 2007 Weaver s Cove Energy FERC approval in July 2005 Project proposes to utilize Air Injection Facilities LNG Marine Import Terminal 400 MMCF/day sendout

Algonquin Gas Quality Technical Conference August 21, 2007 Weaver s Cove Energy FERC approval in July 2005 Project proposes to utilize Air Injection Facilities LNG Marine Import Terminal 400 MMCF/day sendout

The project consisted of 7 miles of 36-inch pipeline and associated facilities. UPI provide EPCM

Haynesville Shale EXCO / TGGT Haynesville Development 36-inch Jebel Spine North The project consisted of five (5) miles of 36-inch pipeline and associated facilities. UPI provided EPCM services including,

Haynesville Shale EXCO / TGGT Haynesville Development 36-inch Jebel Spine North The project consisted of five (5) miles of 36-inch pipeline and associated facilities. UPI provided EPCM services including,

Broad market presence: Growing demand regions, key supply basins, LNG terminals. Excellent connections to markets and supply

Pipeline Group Strong and Growing Broad market presence: Growing demand regions, key supply basins, LNG terminals Excellent connections to markets and supply Almost $4 billion of committed growth projects

Pipeline Group Strong and Growing Broad market presence: Growing demand regions, key supply basins, LNG terminals Excellent connections to markets and supply Almost $4 billion of committed growth projects

24 September 2015 NORTH AMERICAN GAS OUTLOOK

NORTH AMERICAN GAS OUTLOOK WORKING GAS STORAGE FORECAST (BCF) 4,5 4, 3,996 3,5 3, 2,5 2, 1,5 1, 5 1,93 Jan Feb Mar Apr May Jun Jul Aug Sep Oct Nov Dec 21-14 range 215 216 Source: Bloomberg New Energy Finance

NORTH AMERICAN GAS OUTLOOK WORKING GAS STORAGE FORECAST (BCF) 4,5 4, 3,996 3,5 3, 2,5 2, 1,5 1, 5 1,93 Jan Feb Mar Apr May Jun Jul Aug Sep Oct Nov Dec 21-14 range 215 216 Source: Bloomberg New Energy Finance

Marcellus Shale Advisory Commission Infrastructure Work Group Meeting El Paso Corporation Tennessee Gas Pipeline Company April 11, 2011

Interstate Pipelines Exploration & Production Marcellus Shale Advisory Commission Infrastructure Work Group Meeting El Paso Corporation Tennessee Gas Pipeline Company April 11, 2011 El Paso Corporation

Interstate Pipelines Exploration & Production Marcellus Shale Advisory Commission Infrastructure Work Group Meeting El Paso Corporation Tennessee Gas Pipeline Company April 11, 2011 El Paso Corporation

Excelerate Energy: Efficient And Cost-Effective Solutions for the Global Gas Market

Excelerate Energy: Efficient And Cost-Effective Solutions for the Global Gas Market 14 January 2014 Copyright Excelerate Energy L.P. Who We Are: Pioneer and world leader in innovative LNG midstream solutions.

Excelerate Energy: Efficient And Cost-Effective Solutions for the Global Gas Market 14 January 2014 Copyright Excelerate Energy L.P. Who We Are: Pioneer and world leader in innovative LNG midstream solutions.

Outlook for Natural Gas Supply and Demand for Winter

Outlook for Natural Gas Supply and Demand for 2017-2018 Winter Energy Ventures Analysis, Inc. (EVA) Executive Summary While the forthcoming winter weather is expected to be close to normal, total consumption,

Outlook for Natural Gas Supply and Demand for 2017-2018 Winter Energy Ventures Analysis, Inc. (EVA) Executive Summary While the forthcoming winter weather is expected to be close to normal, total consumption,

ENERGY SLIDESHOW. Federal Reserve Bank of Dallas

ENERGY SLIDESHOW Updated: February 14, 2018 ENERGY PRICES www.dallasfed.org/research/energy Brent & WTI & Crude Brent Oil Crude Oil Dollars per barrel 140 Brent (Feb 9 = $65.50) WTI (Feb 9 = $62.01) 120

ENERGY SLIDESHOW Updated: February 14, 2018 ENERGY PRICES www.dallasfed.org/research/energy Brent & WTI & Crude Brent Oil Crude Oil Dollars per barrel 140 Brent (Feb 9 = $65.50) WTI (Feb 9 = $62.01) 120

Al Garcia Business Manager-Americas C4U Trade USA, Inc.

Revealing Global Trade Flows For Propane And Implications For Supply- Future export markets for North American propane and what this means for PDH feedstock security Al Garcia Business Manager-Americas

Revealing Global Trade Flows For Propane And Implications For Supply- Future export markets for North American propane and what this means for PDH feedstock security Al Garcia Business Manager-Americas

U.S. Shale Gas in Context

U.S. Shale Gas in Context Overview of U.S. Natural Gas production and trends For National Conference of State Legislatures Natural Gas Policy Institute September 9, 215 Pittsburgh, Pennsylvania By Grant

U.S. Shale Gas in Context Overview of U.S. Natural Gas production and trends For National Conference of State Legislatures Natural Gas Policy Institute September 9, 215 Pittsburgh, Pennsylvania By Grant

Crestwood Midstream Partners LP

Crestwood Midstream Partners LP Tracy Halleck Director, Northeast Marketing AGENDA Current Crestwood Asset Overview Competition correlation with many industries. Market Flows and Liquidity New Crestwood

Crestwood Midstream Partners LP Tracy Halleck Director, Northeast Marketing AGENDA Current Crestwood Asset Overview Competition correlation with many industries. Market Flows and Liquidity New Crestwood

Texas Eastern Appalachiaa to Market Expansion Project (TEAM

Texas Eastern Appalachiaa to Market Expansion Project (TEAM 2014) Moving emerging natural gas supplies from the Appalachian region to diverse market destinations along the existing Texas Eastern footprint

Texas Eastern Appalachiaa to Market Expansion Project (TEAM 2014) Moving emerging natural gas supplies from the Appalachian region to diverse market destinations along the existing Texas Eastern footprint

LSU Natural Gas Conference

LSU Natural Gas Conference Presented by: Bob Purgason VP Gulfcoast Region Williams Companies Introduction Structural shift in natural gas pricing The crude to gas ratio: A critical relationship for NGL

LSU Natural Gas Conference Presented by: Bob Purgason VP Gulfcoast Region Williams Companies Introduction Structural shift in natural gas pricing The crude to gas ratio: A critical relationship for NGL

UNDERSTANDING NATURAL GAS MARKETS

UNDERSTANDING NATURAL GAS MARKETS Table of Contents PREVIEW Overview... 2 The North American Natural Gas Marketplace... 4 Natural Gas Supply... 8 Natural Gas Demand... 12 Natural Gas Exports... 15 How

UNDERSTANDING NATURAL GAS MARKETS Table of Contents PREVIEW Overview... 2 The North American Natural Gas Marketplace... 4 Natural Gas Supply... 8 Natural Gas Demand... 12 Natural Gas Exports... 15 How

April 9, 2015 The LNG Export Review Process: A Projectby-Project

April 9, 2015 The LNG Export Review Process: A Projectby-Project Analysis for April What's Happening: Royal Dutch Shell announced a deal yesterday to buy BG Group, a move that will make Shell a major competitor

April 9, 2015 The LNG Export Review Process: A Projectby-Project Analysis for April What's Happening: Royal Dutch Shell announced a deal yesterday to buy BG Group, a move that will make Shell a major competitor

LNG Facts A Primer. Presentation before US Department of Energy, Office of Fossil Energy, LNG Forums. March 10, Kristi A. R.

LNG Facts A Primer Presentation before US Department of Energy, Office of Fossil Energy, LNG Forums March 10, 2006 Kristi A. R. Darby Center for Louisiana State University Overview What is Natural Gas?

LNG Facts A Primer Presentation before US Department of Energy, Office of Fossil Energy, LNG Forums March 10, 2006 Kristi A. R. Darby Center for Louisiana State University Overview What is Natural Gas?

Natural Gas Pipeline and Storage Infrastructure Projections Through 2030

Natural Gas Pipeline and Storage Infrastructure Projections Through 2030 October 20, 2009 Submitted to: The INGAA Foundation, Inc. 10 G Street NE Suite 700 Washington, DC 20002 Submitted by: ICF International

Natural Gas Pipeline and Storage Infrastructure Projections Through 2030 October 20, 2009 Submitted to: The INGAA Foundation, Inc. 10 G Street NE Suite 700 Washington, DC 20002 Submitted by: ICF International

NATURAL GAS MARKETS, STRUCTURES, AND MECHANISMS

NATURAL GAS MARKETS, STRUCTURES, AND MECHANISMS Mitchell DeRubis, Senior Energy Analyst Bob Yu, Senior Energy Analyst Restrictions on Use: You may use the prices, indexes, assessments and other related

NATURAL GAS MARKETS, STRUCTURES, AND MECHANISMS Mitchell DeRubis, Senior Energy Analyst Bob Yu, Senior Energy Analyst Restrictions on Use: You may use the prices, indexes, assessments and other related

Natural Gas The North American market. Trevor Sikorski, September 2014

Natural Gas The North American market Trevor Sikorski, September 2014 Overview Gas pricing contrasting fortunes Global gas pricing $/mmbtu 20 18 16 14 12 10 8 6 4 Japan India UK US Global gas market: Still

Natural Gas The North American market Trevor Sikorski, September 2014 Overview Gas pricing contrasting fortunes Global gas pricing $/mmbtu 20 18 16 14 12 10 8 6 4 Japan India UK US Global gas market: Still

Global energy markets

For Woodrow Wilson Center Global Energy Forum September 21, 215 Washington, DC by Adam Sieminski, Administrator U.S. Energy Information Administration U.S. Energy Information Administration Independent

For Woodrow Wilson Center Global Energy Forum September 21, 215 Washington, DC by Adam Sieminski, Administrator U.S. Energy Information Administration U.S. Energy Information Administration Independent

Alliance Pipeline Monetizing Gas & NGLs. Jason Feit Business Development Manager Platt's 6 th Annual Rockies Oil & Gas Conference

Alliance Pipeline Monetizing Gas & NGLs Jason Feit Business Development Manager Platt's 6 th Annual Rockies Oil & Gas Conference Forward looking statements and information Certain information contained

Alliance Pipeline Monetizing Gas & NGLs Jason Feit Business Development Manager Platt's 6 th Annual Rockies Oil & Gas Conference Forward looking statements and information Certain information contained

US NATURAL GAS & CRUDE OIL MARKET ANALYSIS: PRESENT & FUTURE STUDY. Drillinginfo Market Intelligence December 2017

US NATURAL GAS & CRUDE OIL MARKET ANALYSIS: PRESENT & FUTURE STUDY Drillinginfo Market Intelligence December 2017 AGENDA Three key parts to this presentation: 1. Crude Oil Market Analysis 2. Natural Gas

US NATURAL GAS & CRUDE OIL MARKET ANALYSIS: PRESENT & FUTURE STUDY Drillinginfo Market Intelligence December 2017 AGENDA Three key parts to this presentation: 1. Crude Oil Market Analysis 2. Natural Gas

Oil and natural gas: market outlook and drivers

Oil and natural gas: market outlook and drivers for American Foundry Society May 18, 216 Washington, DC by Howard Gruenspecht, Deputy Administrator U.S. Energy Information Administration Independent Statistics

Oil and natural gas: market outlook and drivers for American Foundry Society May 18, 216 Washington, DC by Howard Gruenspecht, Deputy Administrator U.S. Energy Information Administration Independent Statistics

CERI Commodity Report Natural Gas

July-August 1 CERI Commodity Report Natural Gas Ethane Availability for Proposed Western Canadian LNG Facilities Dinara Millington In the Canadian context, the main sources of petrochemical feedstock include

July-August 1 CERI Commodity Report Natural Gas Ethane Availability for Proposed Western Canadian LNG Facilities Dinara Millington In the Canadian context, the main sources of petrochemical feedstock include

Gas and Crude Oil Production Outlook

Gas and Crude Oil Production Outlook COQA/CCQTA Joint meeting October 3-31, 214 San Francisco, California By John Powell Office of Petroleum, Natural Gas, and Biofuels Analysis U.S. Energy Information

Gas and Crude Oil Production Outlook COQA/CCQTA Joint meeting October 3-31, 214 San Francisco, California By John Powell Office of Petroleum, Natural Gas, and Biofuels Analysis U.S. Energy Information

Leveraging Domestic Shale Gas Production Through Exports. Pat Outtrim, Vice President, Governmental Affairs Cheniere Energy, Inc.

Leveraging Domestic Shale Gas Production Through Exports Pat Outtrim, Vice President, Governmental Affairs Cheniere Energy, Inc. Extensive Broad-Based Shale Resource Base Lower 48 Recoverable Unconventional

Leveraging Domestic Shale Gas Production Through Exports Pat Outtrim, Vice President, Governmental Affairs Cheniere Energy, Inc. Extensive Broad-Based Shale Resource Base Lower 48 Recoverable Unconventional

The Woodford Shale. Presenter Name: Sam Langford

The Woodford Shale Presenter Name: Sam Langford Woodford Agenda Background & History Development Plan Summary Pilots Results Reserves CAPEX Type Well Economics NAV Model Results Looking Forward Background

The Woodford Shale Presenter Name: Sam Langford Woodford Agenda Background & History Development Plan Summary Pilots Results Reserves CAPEX Type Well Economics NAV Model Results Looking Forward Background

Winter 2015 Cold Weather Operations

Winter 2015 Cold Weather Operations Wes Yeomans Vice President - Operations New York Independent System Operator Management Committee March 31, 2015 Rensselaer, NY 2015 New York Independent System Operator,

Winter 2015 Cold Weather Operations Wes Yeomans Vice President - Operations New York Independent System Operator Management Committee March 31, 2015 Rensselaer, NY 2015 New York Independent System Operator,

The Impact of Recent Hurricanes on U.S. Gas Markets for the Upcoming Winter

The Impact of Recent Hurricanes on U.S. Gas Markets for the Upcoming Winter A Study Performed For INGAA by Energy and Environmental Analysis, Inc. Background In early October 2005, INGAA contracted with

The Impact of Recent Hurricanes on U.S. Gas Markets for the Upcoming Winter A Study Performed For INGAA by Energy and Environmental Analysis, Inc. Background In early October 2005, INGAA contracted with

LNG Market through. Serving the Asia Pacific. Jordan Cove LNG. Vern A. Wadey. Vice President

Serving the Asia Pacific LNG Market through Jordan Cove LNG Vern A. Wadey Vice President Pacific North West Economic Region 25th Annual Summit Big Sky, Montana Monday, July 13, 2015 Veresen Inc.: A strong,

Serving the Asia Pacific LNG Market through Jordan Cove LNG Vern A. Wadey Vice President Pacific North West Economic Region 25th Annual Summit Big Sky, Montana Monday, July 13, 2015 Veresen Inc.: A strong,

World and U.S. Oil and Gas Production and Price Outlook: To Infinity (or at least 2050) and Beyond

and Beyond") World and U.S. Oil and Gas Production and Price Outlook: To Infinity (or at least 25) and Beyond Energy and Environment Symposium April 18, 218 Rifle, Colorado by Troy Cook, Senior Global Upstream Analyst,

World and U.S. Oil and Gas Production and Price Outlook: To Infinity (or at least 25) and Beyond Energy and Environment Symposium April 18, 218 Rifle, Colorado by Troy Cook, Senior Global Upstream Analyst,

Cheniere Energy and the LNG Market. NARUC LNG Working Group November 8, 2015 Patricia Outtrim, Vice President, Government and Regulatory Affairs

Cheniere Energy and the LNG Market NARUC LNG Working Group November 8, 2015 Patricia Outtrim, Vice President, Government and Regulatory Affairs Forward Looking Statements 2 This presentation contains certain

Cheniere Energy and the LNG Market NARUC LNG Working Group November 8, 2015 Patricia Outtrim, Vice President, Government and Regulatory Affairs Forward Looking Statements 2 This presentation contains certain

2017 MPEH LLC. Overview Main Pass Energy Hub LNG Export Project January 31, 2017

2017 MPEH LLC Overview Main Pass Energy Hub LNG Export Project January 31, 2017 THE COMPANY Global LNG Services AS (GLS), established in 2013, is an LNG project developer that will build, own, and operate

2017 MPEH LLC Overview Main Pass Energy Hub LNG Export Project January 31, 2017 THE COMPANY Global LNG Services AS (GLS), established in 2013, is an LNG project developer that will build, own, and operate

Alliance Pipeline. BMO Western Canadian Tour

Alliance Pipeline BMO Western Canadian Tour September 16, 2014 Forward-Looking Information Certain information contained in this presentation constitutes forwardlooking statements. The words anticipate,

Alliance Pipeline BMO Western Canadian Tour September 16, 2014 Forward-Looking Information Certain information contained in this presentation constitutes forwardlooking statements. The words anticipate,

Pricing, markets and investments. SPM 9541 December 2010 Aad Correljé

Pricing, markets and investments SPM 9541 December 2010 Aad Correljé Programme Visions on gas prices Gasmarkets Market prices? Pricing systems June 29, 2011 2 Dutch gas price to domestic households 10,2%

Pricing, markets and investments SPM 9541 December 2010 Aad Correljé Programme Visions on gas prices Gasmarkets Market prices? Pricing systems June 29, 2011 2 Dutch gas price to domestic households 10,2%

OUR CONVERSATION TODAY

OUR CONVERSATION TODAY Our goal is to raise the level of awareness around the natural gas supply chain among key stakeholders in order to facilitate positive working relationships and more informed decision

OUR CONVERSATION TODAY Our goal is to raise the level of awareness around the natural gas supply chain among key stakeholders in order to facilitate positive working relationships and more informed decision

2017 Annual Seaview Customer Meeting. SEAVIEW RESORT, Galloway, NJ May 4, 2017

2017 Annual Seaview Customer Meeting SEAVIEW RESORT, Galloway, NJ May 4, 2017 1 Agenda 2017 Seaview Customer Event Welcome/Enbridge Update Winter Operations Pipeline Postings New Pipeline Development Regulatory

2017 Annual Seaview Customer Meeting SEAVIEW RESORT, Galloway, NJ May 4, 2017 1 Agenda 2017 Seaview Customer Event Welcome/Enbridge Update Winter Operations Pipeline Postings New Pipeline Development Regulatory

Cheniere Energy October 2013

Cheniere Energy October 2013 Forward Looking Statements 2 This presentation contains certain statements that are, or may be deemed to be, forward-looking statements within the meaning of Section 27A of

Cheniere Energy October 2013 Forward Looking Statements 2 This presentation contains certain statements that are, or may be deemed to be, forward-looking statements within the meaning of Section 27A of

2016 Propane Market Outlook: Driving Change in Consumer Propane Markets

0 2016 Propane Market Outlook: Driving Change in Consumer Propane Markets NPGA Southeastern Convention & International Propane Expo April 8, 2016 Presented by: Michael Sloan ICF International 9300 Lee

0 2016 Propane Market Outlook: Driving Change in Consumer Propane Markets NPGA Southeastern Convention & International Propane Expo April 8, 2016 Presented by: Michael Sloan ICF International 9300 Lee

Natural Gas. Dr. Fred Beach Energy Institute The University of Texas at Austin. Infrastructure as Momentum. Dr. Fred C. Beach.

Infrastructure as Momentum Dr. Fred Beach Energy Institute The University of Texas at Austin 1 Fossil Fuels Supply 87% of All Energy Consumption in the World 2 Global Consumption Trends 2011 Energy Consumption,

Infrastructure as Momentum Dr. Fred Beach Energy Institute The University of Texas at Austin 1 Fossil Fuels Supply 87% of All Energy Consumption in the World 2 Global Consumption Trends 2011 Energy Consumption,

LNG strategy and the outlook for global gas markets

LNG strategy and the outlook for global gas markets October 16 th, 2012 Jean-Marie Dauger Executive Vice-president GDF SUEZ The LNG market Strong growth particularly in Asia An LNG market of ~550 Mt in

LNG strategy and the outlook for global gas markets October 16 th, 2012 Jean-Marie Dauger Executive Vice-president GDF SUEZ The LNG market Strong growth particularly in Asia An LNG market of ~550 Mt in

East Tennessee Natural Gas Customer Meeting. Hilton Head, South Carolina September 24, 2015

East Tennessee Natural Gas Customer Meeting Hilton Head, South Carolina September 24, 2015 Agenda Welcome Spectra Energy Poised for Growth Where does ETNG go from here? LINK System Review Break FERC Certificate

East Tennessee Natural Gas Customer Meeting Hilton Head, South Carolina September 24, 2015 Agenda Welcome Spectra Energy Poised for Growth Where does ETNG go from here? LINK System Review Break FERC Certificate

CHENIERE ENERGY, INC. CLARKSONS PLATOU ENERGY & SHIPPING CONFERENCE. January 2016

CHENIERE ENERGY, INC. CLARKSONS PLATOU ENERGY & SHIPPING CONFERENCE January 2016 Forward Looking Statements This presentation contains certain statements that are, or may be deemed to be, forward-looking

CHENIERE ENERGY, INC. CLARKSONS PLATOU ENERGY & SHIPPING CONFERENCE January 2016 Forward Looking Statements This presentation contains certain statements that are, or may be deemed to be, forward-looking

Infrastructure Update

Infrastructure Update Office of Energy Projects February 23, 2017 Agency Overview Independent regulatory agency Quasi-judicial agency Regulates the rates for interstate transmission of electricity, natural

Infrastructure Update Office of Energy Projects February 23, 2017 Agency Overview Independent regulatory agency Quasi-judicial agency Regulates the rates for interstate transmission of electricity, natural