US LNG Supply into Europe. Baltic Energy Summit, Vilnius November 25 th, 2015 Helena Wisden, Cheniere Marketing International

|

|

|

- Malcolm Harry McCoy

- 5 years ago

- Views:

Transcription

1 US LNG Supply into Europe Baltic Energy Summit, Vilnius November 25 th, 2015 Helena Wisden, Cheniere Marketing International

2 Forward Looking Statements This presentation contains certain statements that are, or may be deemed to be, forward looking statements within the meaning of Section 27A of the Securities Act and Section 21E of the Securities Exchange Act of 1933, as amended. All statements, other than statements of historical facts, included herein are forward looking statements. Included among forward looking statements are, among other things: Statements that we expect to commence or complete construction of a liquefaction facility by certain dates, or at all; Statements that we expect to receive authorization from the Federal Energy Regulatory Commission, or FERC, or the Department of Energy, or DOE to construct and operate a proposed liquefaction facility by a certain date, or at all; Statements regarding future levels of domestic or foreign natural gas production and consumption, or the future level of LNG imports into North America or exports from the U.S., or regarding projected future capacity of liquefaction or regasification facilities worldwide; Statements regarding any financing transactions or arrangements, whether on the part of Cheniere or at the project level; Statements regarding any commercial arrangements marketed or potential arrangements to be performed in the future, including any cash distributions and revenues anticipated to be received; Statements regarding the commercial terms and potential revenues from activities described in this presentation; Statements that our proposed liquefaction facility, when completed, will have certain characteristics, including a number of trains; Statements regarding our business strategy, our business plan or any other plans, forecasts, examples, models, forecasts or objectives: any or all of which are subject to change; Statements regarding estimated corporate overhead expenses; and Any other statements that relate to non historical information. These forward looking statements are often identified by the use of terms and phrases such as achieve, anticipate, believe, estimate, example, expect, forecast, opportunities, plan, potential, project, propose, subject to, and similar terms and phrases. Although we believe that the expectations reflected in these forward looking statements are reasonable, they do involve assumptions, risks and uncertainties, and these expectations may prove to be incorrect. You should not place undue reliance on these forward looking statements, which speak only as of the date of this presentation. Our actual results could differ materially from those anticipated in these forward looking statements as a result of a variety of factors, including those discussed in Risk Factors in the Cheniere Energy, Inc. and Cheniere Energy Partners, L.P. Current Reports on Form 8 K filed with the Securities and Exchange Commission, which are incorporated by reference into this presentation. All forward looking statements attributable to us or persons acting on our behalf are expressly qualified in their entirety by these Risk Factors. These forward looking statements are made as of the date of this presentation, and we undertake no obligation to publicly update or revise any forward looking statements. 2

3 Agenda Introduction to Cheniere US Unconventional Gas US LNG Exports Evolving Global LNG Trade Impact on Europe 3

Trains")

First LNG targeted in late")

Trains")

4 Cheniere LNG Platform 30 MT under Construction 60 MT total under development Sabine Pass Liquefaction 6 train development 27 mtpa (~3.8 Bcf/d in export capacity) Trains 1 5 are under construction; First LNG expected in late 2015 Train 6 under development, FID expected 2015 Live Oak LNG 2 train development 5.2 mtpa (~0.7Bcf/d) First LNG targeted in late 2021 Live Oak LNG TX Corpus Christi Liquefaction Sabine Pass Liquefaction Creole Trail PL Corpus Christi Liquefaction 5train development 22.5 mtpa (~3.2 Bcf/d in export capacity) Trains 1 2 are under construction; First LNG expected 2018 Train 3 under development; FID expected 2015 Trains 4 5 under development; Permitting process initiated June 2015 LA Louisiana LNG Louisiana LNG 2 train development 5.2 mtpa (~0.7Bcf/d) First LNG targeted in late 2021 Under Construction Proposed 4

5 U.S. Shale Plays 5 Source: EIA

6 Shale Revolution Reversed Trend in U.S. Gas Supply U.S. Dry Gas Production Bcf/d : + 50 % Conventional Production Shale Production Source: EIA 6

Total Shale Wells Drilled as of June 2014 U.S. 1,161 >100,000 China 1,115 >200 Argentina 802 >200 Algeria 707 0 Canada 573 >20,000 Mexico 545 <20 Australia 437 ~40 S.")

7 U.S. Stands Alone as Unconventional Hydrocarbon Producer Abundant Reserves Are Necessary But Insufficient For U.S. Style Revolution Europe 2011: At least 7 IOCs in Poland, 120 test wells planned per year 2014: COP only remaining major in Poland Argentina 2011: Halliburton completes first Argentine shale well for Apache 2014: YPF/Chevron producing 20 kbd of tight oil China 2011: NDRC targets 10 Bcf/d production by : China produces 0.25 Bcf/d in 2014 NDRC halves shale gas target Shell shifts focus from shale to offshore United States of America 2011: 23% of wells are shale wells 2014: 90% of new wells are unc. wells World s #1 natural gas producer World s #1 liquids producer Technically Recoverable Shale Gas Resources (Tcf) Total Shale Wells Drilled as of June 2014 U.S. 1,161 >100,000 China 1,115 >200 Argentina 802 >200 Algeria Canada 573 >20,000 Mexico 545 <20 Australia 437 ~40 S. Africa Russia Brazil Enabling Factors: Mineral Rights Innovation Supply Chain/Services Capital Formation Pipeline Infrastructure Water Resources Public Perception Regulatory Framework U.S. China x X x x x X Argentina x X X x x Europe x x X x x x 7 Source: ARI, Accenture, CAPP, Baker Hughes, API, Cheniere Research

8 U.S. LNG Export Projects Company Quantity (Bcf/d) DOE FERC * Contracts Cheniere Sabine Pass T1 T4 2.2 Fully permitted Fully Subscribed Oregon LNG Freeport 1.8 Fully permitted Fully Subscribed Jordan Cove Dominion Cove Point Lake Charles 2.0 Dominion Cove Point FTA + NonFTA 1.0 Fully permitted Fully Subscribed Fully Subscribed Cameron LNG 1.7 Fully permitted Fully Subscribed Freeport LNG Corpus Christi Golden Pass Southern LNG Gulf LNG Lake Charles Magnolia Cameron LNG Sabine Pass Jordan Cove 1.2/0.8 Oregon LNG 1.25 Cheniere Corpus Christi T1 T3 Cheniere Sabine Pass T5 T6 FTA + NonFTA FTA + NonFTA 2.1 Fully permitted 1.3 Fully permitted Southern LNG 0.5 FTA Partially Subscribed T5 Subscribed Fully Subscribed Under Construction Magnolia LNG 0.5 FTA Partially Subscribed Filed FERC Application Golden Pass LNG 2 FTA Fully Subscribed Gulf LNG 1.3 FTA 8 Source: Office of Oil and Gas Global Security and Supply, Office of Fossil Energy, U.S. Department of Energy; U.S. Federal Energy Regulatory Commission; Company releases Plus other proposed LNG export projects that have not filed a FERC application. Excelerate has requested that FERC put on hold the review its application. Application filing = FERC scheduling notice issued =

9 U.S. To Become One of the Top Three LNG Suppliers Projected LNG Capacity 2014 Global LNG Capacity: ~37 Bcf/d 94 mtpa 60 mtpa mtpa 68 mtpa mtpa under 31.5 mtpa 1.4 const. mtpa mtpa under 26 const. mtpa AP AP United States Source: Wood Mackenzie Q Cheniere Cheniere Sabine Pass T1 6 Corpus Christi T1 5 Parallax MEG MEG Rest of World Includes Existing and AB AB Under Construction Projects 2014: 171 mtpa 2025: 189 mtpa Qatar Australia

10 Projected Global LNG Demand 436 mtpa by 2025 Demand forecasted to increase by 193 mtpa to 2025, a 6% CAGR Average of 23 mtpa of new liquefaction capacity needed each year (1) Europe Americas Middle East/N. Africa Asia Source: Wood Mackenzie Q LNG Tool (1) Assumes 85% utilization of nameplate capacity

11 LNG Trade Today A Snapshot 50 years old 240 mt (32 bcf/d) 19 exporting countries 31 importing countries ~400 ships 10% of all gas consumed worldwide 30% of internationally traded gas 11 Source: BP Statistical Review of World Energy 2015, Cheniere interpretation of Wood Mackenzie data (Q3 2015)

12 LNG: Changing Trade Characteristics Over the past decade; LNG trade by contract length Spot and short term trade* 29% Significant growth in flexible volumes Supply tenders Back stop markets Re loads mtpa Mid & long term contract trade 71% Portfolio players / aggregators Traders Growing cargo diversions Increasing competition between markets Source: Poten and Partners (2001), GIIGNL (2015) * Contract duration of 4 years or less (GIIGNL)

13 Non Long Term LNG Trade Increasing MTPA U.S. Supplies to Create More Market Liquidity Flexible destination clauses New pricing index Henry Hub Option to purchase lifting not required Spot and Short Term LNG Trade % of Total LNG Trade (right axis) % SHARE 35% 30% 25% 20% 15% 10% 5% 0% 13 Source: GIIGNL 2015

14 LNG Exporters (2020) mtpa LNG exporters by rank (2020) Top 15 exporters (2020) shown Other exporters (2014) = 5 (14 mt) Other exporters (2020) = 6 (19 mt) Source: Cheniere interpretation of Wood Mackenzie data (Q3 2015)

15 Gas and LNG Prices ( ) $/mmbtu Asia spot Oil parity Asia LT proxy 5 NBP HH Source: Platts, Heren, Petroleum Association of Japan and Bloomberg (May 2015) Note: Asia long term proxy = 14.85% JCC( 3) Oil parity = JCC = Japanese average crude price

16 U.S. Can Deliver Gas Profitably Delivered Price To: Europe Asia (MMBtu) Gas $3.00 $3.00 Transportation Regasification Total Cost $4.40 $5.50 Landed Price $6.00 (TTF) $7.40 (JKM) Margin $1.60 $1.90 Construction costs in the U.S. are between $600 $800/tonne At $600/tonne of construction cost, $2.00 is a 16% return on capital US prices market oriented High flexibility (no TOP, no destination clause) 16

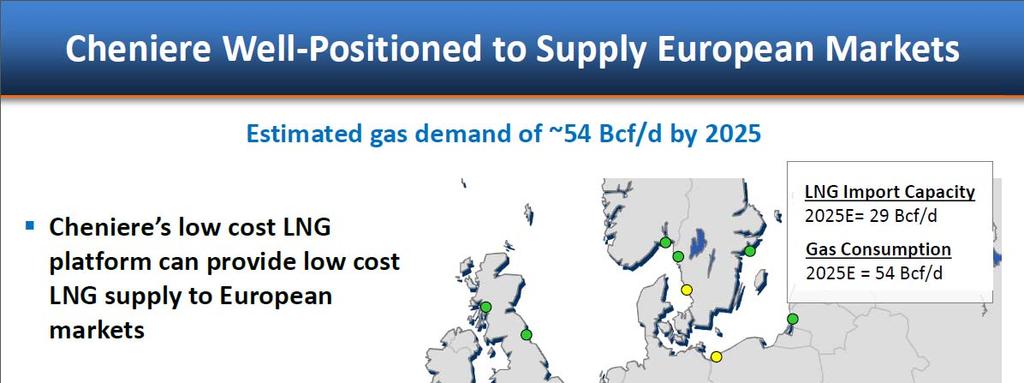

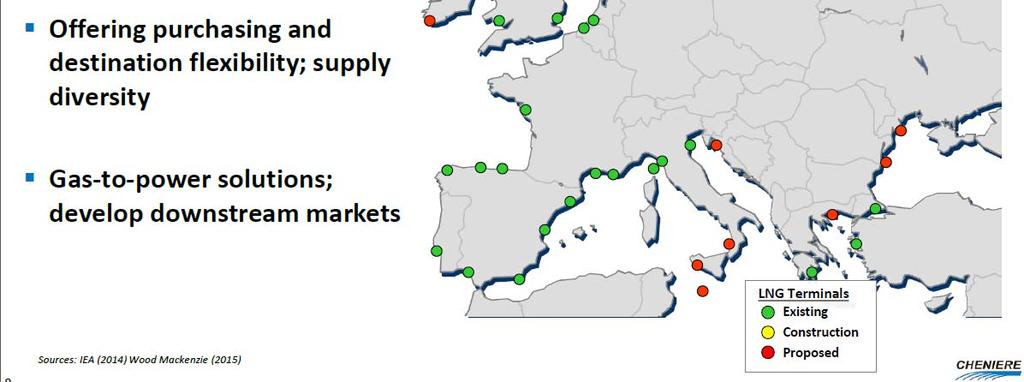

17 European LNG Import Capacity European LNG import capacity* versus LNG imports (2014) 50 mtpa imports 10 0 Spain UK France Italy Netherlands Belgium Turkey Portugal Greece Poland Lithuania 17 Source: Regas capacity : Wood Mackenzie (Q3 2015) (Existing and Under construction) 2014 imports IHS Waterborne data (2015), delivered volumes *Turkey included as regional importer

18 Cheniere Energy Global Customers U.K. BG Centrica Spain Gas Natural Fenosa Endesa Iberdrola France Total EDF Portugal EDP 8.6 South Korea Kogas India GAIL Indonesia Pertamina Australia Woodside Supply Purchase Agreements 18

19 19

20 Cheniere: A Key LNG Supplier to Europe With its LT contracts with Gas Natural Fenosa, Iberdrola, Endesa, Cheniere will supply 30% of the Spanish Market Cheniere LT contracts in Europe 16 MT/year 5% of total European Gas Market 20

21 Key Points The U.S. is a low cost natural gas producer even in a depressed commodity price environment, enabling it to become a competitive global LNG supplier for decades Plentiful, low cost natural gas supply in the USA is not in question The U.S. can build LNG infrastructure cheaper than competitors and is poised to become one of the top global LNG suppliers U.S. LNG is competitive with alternative energy sources Existing regas infrastructure in Europe, but still additional investments needed Cheniere is well positioned tosupplyeuropewithmore LNG 21

22 Aerial View of SPL Construction August 2015 Train 6 Under Development T5 Soil Stabilization Train 5 Train 3 T3 Ethylene Cold Box T3 Methane Cold Box Train 4 T1 Methane Cold Box T1 Ethylene Cold Box Air Coolers Propane Condenser Area Train 1 T2 Methane Cold Box T2 Ethylene Cold Box Train 2

23

CHENIERE ENERGY, INC. Louisiana Energy Conference. June 2016

CHENIERE ENERGY, INC. Louisiana Energy Conference June 2016 Forward Looking Statements This presentation contains certain statements that are, or may be deemed to be, forward-looking statements within

CHENIERE ENERGY, INC. Louisiana Energy Conference June 2016 Forward Looking Statements This presentation contains certain statements that are, or may be deemed to be, forward-looking statements within

Cheniere Energy Partners, L.P. / Cheniere Energy, Inc. Proposed Sabine Pass LNG Facility Expansion Adding Liquefaction Capabilities.

Cheniere Energy Partners, L.P. / Cheniere Energy, Inc. Proposed Sabine Pass LNG Facility Expansion Adding Liquefaction Capabilities June 4, 2010 Forward Looking Statements This presentation contains certain

Cheniere Energy Partners, L.P. / Cheniere Energy, Inc. Proposed Sabine Pass LNG Facility Expansion Adding Liquefaction Capabilities June 4, 2010 Forward Looking Statements This presentation contains certain

CHENIERE ENERGY, INC. How is the Rest of the World s LNG Interfacing With Europe?

CHENIERE ENERGY, INC. How is the Rest of the World s LNG Interfacing With Europe? European Gas Conference - Vienna Andrew Walker VP LNG Strategy January 23, 18 2 Safe Harbor Statements Forward-Looking

CHENIERE ENERGY, INC. How is the Rest of the World s LNG Interfacing With Europe? European Gas Conference - Vienna Andrew Walker VP LNG Strategy January 23, 18 2 Safe Harbor Statements Forward-Looking

CHENIERE ENERGY, INC.

CHENIERE ENERGY, INC. U.S. LNG in the new energy price environment January 2016 Forward Looking Statements This presentation contains certain statements that are, or may be deemed to be, forward-looking

CHENIERE ENERGY, INC. U.S. LNG in the new energy price environment January 2016 Forward Looking Statements This presentation contains certain statements that are, or may be deemed to be, forward-looking

Forward Looking Statements This presentation contains certain statements that are, or may be deemed to be, forward looking statements within the meani

Outlook for U.S. LNG Exports METI, Japan LNG Producer Consumer Conference Charif Souki CEO, Cheniere Energy Inc. Forward Looking Statements This presentation contains certain statements that are, or may

Outlook for U.S. LNG Exports METI, Japan LNG Producer Consumer Conference Charif Souki CEO, Cheniere Energy Inc. Forward Looking Statements This presentation contains certain statements that are, or may

CHENIERE ENERGY, INC.

CHENIERE ENERGY, INC. THE GAS PACKAGE - THE ROLE OF US LNG European Parliament Public Hearing Andrew Walker Vice-President, Strategy, Cheniere Marketing May 23, 2016 Forward Looking Statements This presentation

CHENIERE ENERGY, INC. THE GAS PACKAGE - THE ROLE OF US LNG European Parliament Public Hearing Andrew Walker Vice-President, Strategy, Cheniere Marketing May 23, 2016 Forward Looking Statements This presentation

CHENIERE ENERGY, INC.

CHENIERE ENERGY, INC. Factors Affecting Global Coal-Gas Competition NGI Workshop - Global Competition Between Coal and Natural Gas October 15th 218 Najla Jamoussi Director, Market Fundamentals & Corporate

CHENIERE ENERGY, INC. Factors Affecting Global Coal-Gas Competition NGI Workshop - Global Competition Between Coal and Natural Gas October 15th 218 Najla Jamoussi Director, Market Fundamentals & Corporate

Global LNG Market dynamics, key trends and market outlook

REUTERS / Anne Kat Brevik Global LNG Market dynamics, key trends and market outlook December 14, 217 What to address Market dynamics, key trends and market outlook The role and outlook for U.S. LNG China

REUTERS / Anne Kat Brevik Global LNG Market dynamics, key trends and market outlook December 14, 217 What to address Market dynamics, key trends and market outlook The role and outlook for U.S. LNG China

LNG strategy and the outlook for global gas markets

LNG strategy and the outlook for global gas markets October 16 th, 2012 Jean-Marie Dauger Executive Vice-president GDF SUEZ The LNG market Strong growth particularly in Asia An LNG market of ~550 Mt in

LNG strategy and the outlook for global gas markets October 16 th, 2012 Jean-Marie Dauger Executive Vice-president GDF SUEZ The LNG market Strong growth particularly in Asia An LNG market of ~550 Mt in

Trends in International LNG

Trends in International LNG Anthony Patten, Partner, Allens Presentation to AMPLA State Conference Fremantle, Western Australia 18 May 2012 Allens is an independent partnership operating in alliance with

Trends in International LNG Anthony Patten, Partner, Allens Presentation to AMPLA State Conference Fremantle, Western Australia 18 May 2012 Allens is an independent partnership operating in alliance with

Rice Global E&C Forum

Rice Global E&C Forum "Will Shale revolution trigger game changes in Asian Energy Market and LNG?" Tevin Vongvanich President and Chief Executive Officer PTT Exploration and Production Public Company Limited

Rice Global E&C Forum "Will Shale revolution trigger game changes in Asian Energy Market and LNG?" Tevin Vongvanich President and Chief Executive Officer PTT Exploration and Production Public Company Limited

ROYAL DUTCH SHELL PLC LEADER IN GLOBAL GAS

ROYAL DUTCH SHELL PLC LEADER IN GLOBAL GAS DEFINITIONS AND CAUTIONARY NOTE Resources: Our use of the term resources in this announcement includes quantities of oil and gas not yet classified as Securities

ROYAL DUTCH SHELL PLC LEADER IN GLOBAL GAS DEFINITIONS AND CAUTIONARY NOTE Resources: Our use of the term resources in this announcement includes quantities of oil and gas not yet classified as Securities

Safe Harbor Statements. CHENIERE ENERGY, INC. NYSE American: LNG CHENIERE ENERGY, INC. The LNG market: new opportunities and challenges

IEEJ:December 18 IEEJ18 CHENIERE ENERGY, INC. The LNG market: new opportunities and challenges 23 rd International Gas and Power Summit, Paris. November 22, 18 Eric Bensaude Managing Director Commercial

IEEJ:December 18 IEEJ18 CHENIERE ENERGY, INC. The LNG market: new opportunities and challenges 23 rd International Gas and Power Summit, Paris. November 22, 18 Eric Bensaude Managing Director Commercial

Natural Gas: Challenges for the Industry, the LNG Chain, and Implications for Market Structure

27 September 216 Algiers Natural Gas: Challenges for the Industry, the LNG Chain, and Implications for Market Structure Plenary Session 2 Introduction Market context Session objectives Low gas prices across

27 September 216 Algiers Natural Gas: Challenges for the Industry, the LNG Chain, and Implications for Market Structure Plenary Session 2 Introduction Market context Session objectives Low gas prices across

Natural Gas Supply, Demand, and the Prospects for North American LNG Exports

Natural Gas Supply, Demand, and the Prospects for North American LNG Exports December 3 rd, 2014 Robert D. Stibolt Senior Managing Director Observations on natural gas prices and project returns Price

Natural Gas Supply, Demand, and the Prospects for North American LNG Exports December 3 rd, 2014 Robert D. Stibolt Senior Managing Director Observations on natural gas prices and project returns Price

Cheniere Energy, Inc. July 2015

Cheniere Energy, Inc. July 2015 Forward Looking Statements 2 This presentation contains certain statements that are, or may be deemed to be, forward-looking statements within the meaning of Section 27A

Cheniere Energy, Inc. July 2015 Forward Looking Statements 2 This presentation contains certain statements that are, or may be deemed to be, forward-looking statements within the meaning of Section 27A

Shale Gas and U.S. LNG Exports. Vienna, January 29, 2013 Jean Abiteboul President, Cheniere Supply & Marketing

Shale Gas and U.S. LNG Exports Vienna, January 29, 2013 Jean Abiteboul President, Cheniere Supply & Marketing Forward Looking Statements This presentation contains certain statements that are, or may be

Shale Gas and U.S. LNG Exports Vienna, January 29, 2013 Jean Abiteboul President, Cheniere Supply & Marketing Forward Looking Statements This presentation contains certain statements that are, or may be

The Shale Invasion: Will U.S. LNG Cross the Pond? New terminals ramp up exports.

? The Shale Invasion: Will U.S. LNG Cross the Pond? New terminals ramp up exports. Morningstar Commodities Research 6 December 2016 Sandy Fielden Director, Oil and Products Research +1 512 431-8044 sandy.fielden@morningstar.com

? The Shale Invasion: Will U.S. LNG Cross the Pond? New terminals ramp up exports. Morningstar Commodities Research 6 December 2016 Sandy Fielden Director, Oil and Products Research +1 512 431-8044 sandy.fielden@morningstar.com

The Case for Investing in LNG Export Terminals in the US. Marine Money 2017 Meg Gentle, CEO

The Case for Investing in LNG Export Terminals in the US Marine Money 2017 Meg Gentle, CEO June 19, 2017 Cautionary statement Forward looking statement Non-GAAP Financial Measures The information in this

The Case for Investing in LNG Export Terminals in the US Marine Money 2017 Meg Gentle, CEO June 19, 2017 Cautionary statement Forward looking statement Non-GAAP Financial Measures The information in this

Summary LNG, an increasingly important energy option in Asia and the rest of the world But challenges remain for LNG to play an expected bigger role S

Prospect and Challenges in the World and Asian LNG Market LNG Producer Consumer Conference September 19, 2012 The Institute of Energy Economics Japan Ken Koyama 0 Summary LNG, an increasingly important

Prospect and Challenges in the World and Asian LNG Market LNG Producer Consumer Conference September 19, 2012 The Institute of Energy Economics Japan Ken Koyama 0 Summary LNG, an increasingly important

CHENIERE ENERGY, INC.

CHENIERE ENERGY, INC. * Sabine Pass LNG, L.P. Cheniere Energy Partners, L.P. Cheniere Energy, Inc. 91% *Corpus Christi LNG, LLC Cheniere Energy, Inc. 100% *Creole Trail LNG, L.P. Cheniere Energy, Inc.

CHENIERE ENERGY, INC. * Sabine Pass LNG, L.P. Cheniere Energy Partners, L.P. Cheniere Energy, Inc. 91% *Corpus Christi LNG, LLC Cheniere Energy, Inc. 100% *Creole Trail LNG, L.P. Cheniere Energy, Inc.

Outlook for Gas Markets

IEEJ IEEJ:Published 2015 年 7 in 月 August 禁無断転載 2015 All rights reserved The 420th Forum on Research Work July 10, 2015 Outlook for Gas Markets The Institute of Energy Economics, Japan Tetsuo Morikawa Manager,

IEEJ IEEJ:Published 2015 年 7 in 月 August 禁無断転載 2015 All rights reserved The 420th Forum on Research Work July 10, 2015 Outlook for Gas Markets The Institute of Energy Economics, Japan Tetsuo Morikawa Manager,

World LNG Report industry trends-

World LNG Report-218 -industry trends- Satoshi Yoshida General Manager, International Section, Policy and Planning Department Japan Gas Association International Gas Union (IGU) Who we are Founded in 1931,

World LNG Report-218 -industry trends- Satoshi Yoshida General Manager, International Section, Policy and Planning Department Japan Gas Association International Gas Union (IGU) Who we are Founded in 1931,

LNG Exports: A Brief Introduction

LNG Exports: A Brief Introduction Natural gas one of the world s most useful substances is burned to heat homes and run highly-efficient electrical powerplants. It is used as a feedstock in the manufacture

LNG Exports: A Brief Introduction Natural gas one of the world s most useful substances is burned to heat homes and run highly-efficient electrical powerplants. It is used as a feedstock in the manufacture

Cheniere Energy and the LNG Market. NARUC LNG Working Group November 8, 2015 Patricia Outtrim, Vice President, Government and Regulatory Affairs

Cheniere Energy and the LNG Market NARUC LNG Working Group November 8, 2015 Patricia Outtrim, Vice President, Government and Regulatory Affairs Forward Looking Statements 2 This presentation contains certain

Cheniere Energy and the LNG Market NARUC LNG Working Group November 8, 2015 Patricia Outtrim, Vice President, Government and Regulatory Affairs Forward Looking Statements 2 This presentation contains certain

An Overview of U.S. Liquefied Natural Gas Exports

Executive Brief An Overview of U.S. Liquefied Natural Gas Exports Executive Summary The world is competing for the tremendous advantage offered by affordable U.S. natural gas. Relative to globally expensive

Executive Brief An Overview of U.S. Liquefied Natural Gas Exports Executive Summary The world is competing for the tremendous advantage offered by affordable U.S. natural gas. Relative to globally expensive

Gas Markets in 2015: Outlook and Challenges

The 418th Forum on Research Work Gas Markets in 2015: Outlook and Challenges December 19, 2014 Tetsuo Morikawa The Institute of Energy Economics, Japan Natural Gas Demand in Major Regions Natural Gas Demand

The 418th Forum on Research Work Gas Markets in 2015: Outlook and Challenges December 19, 2014 Tetsuo Morikawa The Institute of Energy Economics, Japan Natural Gas Demand in Major Regions Natural Gas Demand

The impact of US LNG on European gas prices

January 2018 The impact of US LNG on European gas prices Increasing US exports of LNG will change how gas prices are determined in Europe Import dependency for the European Union, pushed higher as a result

January 2018 The impact of US LNG on European gas prices Increasing US exports of LNG will change how gas prices are determined in Europe Import dependency for the European Union, pushed higher as a result

BC Gas Exports and LNG Shipping: Unlocking the Export Potential

BC Gas Exports and LNG Shipping: Unlocking the Export Potential Christian Waldegrave Manager, Research, Strategic Development Tony Bingham Director, Business Development & Technology, Strategic Development

BC Gas Exports and LNG Shipping: Unlocking the Export Potential Christian Waldegrave Manager, Research, Strategic Development Tony Bingham Director, Business Development & Technology, Strategic Development

Today s Presentation Update on US LNG projects U.S. Gas Market Overview Impact of U.S. LNG on Global LNG Dynamics Sabine Pass First Cargo: 24 th Feb 2

CHENIERE ENERGY, INC. LNG Market Outlook and US LNG s Function - The Perspective from Cheniere IEEJ 2 October 217 Andrew Walker VP Strategy and Communication Today s Presentation Update on US LNG projects

CHENIERE ENERGY, INC. LNG Market Outlook and US LNG s Function - The Perspective from Cheniere IEEJ 2 October 217 Andrew Walker VP Strategy and Communication Today s Presentation Update on US LNG projects

216 IEEJ216 Key points of this report Oversupply in the international LNG market will expand further in the coming years. Upstream industry is cutting

216 IEEJ216 423 rd Forum on Research Works on July 26, 216 Outlook for Gas Market The Institute of Energy Economics, Japan Yoshikazu Kobayashi Senior Economist, Manager, Gas Group, Fossil Fuels & Electric

216 IEEJ216 423 rd Forum on Research Works on July 26, 216 Outlook for Gas Market The Institute of Energy Economics, Japan Yoshikazu Kobayashi Senior Economist, Manager, Gas Group, Fossil Fuels & Electric

The Global Context for Alaskan LNG

The Global Context for Alaskan LNG PRESENTED TO LSI Energy in Alaska Conference PRESENTED BY Dr. Paul R. Carpenter December 7, 2015 Copyright 2015 The Brattle Group, Inc. Agenda 12-18 months into the oil

The Global Context for Alaskan LNG PRESENTED TO LSI Energy in Alaska Conference PRESENTED BY Dr. Paul R. Carpenter December 7, 2015 Copyright 2015 The Brattle Group, Inc. Agenda 12-18 months into the oil

Comparison of Netbacks from Potential LNG Project with ALCAN Pipeline Project

Comparison of Netbacks from Potential LNG Project with ALCAN Pipeline Project June 20, 2008 Barry Pulliam Senior Economist Econ One Research 5th Floor 601 W 5th Street Los Angeles, California 90071 213

Comparison of Netbacks from Potential LNG Project with ALCAN Pipeline Project June 20, 2008 Barry Pulliam Senior Economist Econ One Research 5th Floor 601 W 5th Street Los Angeles, California 90071 213

Corporate Presentation. March 2008

Corporate Presentation March 2008 Safe Harbor Act This presentation contains certain statements that are, or may be deemed to be, forward-looking statements within the meaning of Section 27A of the Securities

Corporate Presentation March 2008 Safe Harbor Act This presentation contains certain statements that are, or may be deemed to be, forward-looking statements within the meaning of Section 27A of the Securities

International gas markets: recent developments and prospects

International gas markets: recent developments and prospects Christopher Allsopp New College Oxford Director, Oxford Institute for Energy Studies December 2012 International gas markets are changing rapidly

International gas markets: recent developments and prospects Christopher Allsopp New College Oxford Director, Oxford Institute for Energy Studies December 2012 International gas markets are changing rapidly

The Impact of US LNG Exports on India s Gas Market Jason Bordoff

The Impact of US LNG Exports on India s Gas Market Jason Bordoff November 30, 2016 Delhi, India US Natural Gas Outlook 2 US Shale: There Will Be Gas US Dry Gas Production Under the EIA s Reference Case

The Impact of US LNG Exports on India s Gas Market Jason Bordoff November 30, 2016 Delhi, India US Natural Gas Outlook 2 US Shale: There Will Be Gas US Dry Gas Production Under the EIA s Reference Case

Global Energy Assessment: Shale Gas and Oil

Global Energy Assessment: Shale Gas and Oil KEEI September, 2014 Yonghun Jung Shale Gas: a new source of energy Shale gas deposits around the world vs. 2009 natural gas consumption (tcf) U.S. 862 22.8

Global Energy Assessment: Shale Gas and Oil KEEI September, 2014 Yonghun Jung Shale Gas: a new source of energy Shale gas deposits around the world vs. 2009 natural gas consumption (tcf) U.S. 862 22.8

CHENIERE ENERGY, INC. CLARKSONS PLATOU ENERGY & SHIPPING CONFERENCE. January 2016

CHENIERE ENERGY, INC. CLARKSONS PLATOU ENERGY & SHIPPING CONFERENCE January 2016 Forward Looking Statements This presentation contains certain statements that are, or may be deemed to be, forward-looking

CHENIERE ENERGY, INC. CLARKSONS PLATOU ENERGY & SHIPPING CONFERENCE January 2016 Forward Looking Statements This presentation contains certain statements that are, or may be deemed to be, forward-looking

US LNG Export Growth and the Benefits to Midstream

US LNG Export Growth and the Benefits to Midstream July 2018 The US is on the brink of adding significant LNG export capacity in 2019 and becoming a sizable player in the global LNG market. In 2017, the

US LNG Export Growth and the Benefits to Midstream July 2018 The US is on the brink of adding significant LNG export capacity in 2019 and becoming a sizable player in the global LNG market. In 2017, the

LNG Markets GDF SUEZ and its LNG activities

LNG Markets GDF SUEZ and its LNG activities Paris 22 April 2013 Denis Bonhomme Executive VP Strategy GDF SUEZ LNG This presentation is not intended to provide the basis for any evaluation of GDF SUEZ or

LNG Markets GDF SUEZ and its LNG activities Paris 22 April 2013 Denis Bonhomme Executive VP Strategy GDF SUEZ LNG This presentation is not intended to provide the basis for any evaluation of GDF SUEZ or

Markets and Opportunities. Paul Burgener March 2015

Markets and Opportunities Paul Burgener March 2015 Disclaimer Copyright BP Energy Company. All rights reserved. Contents of this presentation do not necessarily reflect the Company s views. This presentation

Markets and Opportunities Paul Burgener March 2015 Disclaimer Copyright BP Energy Company. All rights reserved. Contents of this presentation do not necessarily reflect the Company s views. This presentation

LNG Shipping: How Long Will The Good Times Last?

LNG Shipping: How Long Will The Good Times Last? Poten & Partners November 1 HOUSTON NEW YORK LONDON ATHENS SINGAPORE GUANGZHOU PERTH A GLOBAL BROKER AND COMMERCIAL ADVISOR FOR THE ENERGY AND OCEAN TRANSPORTATION

LNG Shipping: How Long Will The Good Times Last? Poten & Partners November 1 HOUSTON NEW YORK LONDON ATHENS SINGAPORE GUANGZHOU PERTH A GLOBAL BROKER AND COMMERCIAL ADVISOR FOR THE ENERGY AND OCEAN TRANSPORTATION

LNG Market in Asia. - A Japanese Perspective on the LNG Industry - October 14 th, Industry Research Department

LNG Market in Asia - A on the LNG Industry - October 14 th, 216 Industry Research Department Copyright (c) Mizuho Bank, Ltd. All Rights Reserved. Contents 1 Energy Policies in Japan P. 2 2 P. 9 3 P. 15

LNG Market in Asia - A on the LNG Industry - October 14 th, 216 Industry Research Department Copyright (c) Mizuho Bank, Ltd. All Rights Reserved. Contents 1 Energy Policies in Japan P. 2 2 P. 9 3 P. 15

The Evolving Global LNG Industry South Africa Gas Options, Cape Town, 3 rd 5 th October 2016

The Evolving Global LNG Industry South Africa Gas Options, Cape Town, 3 rd 5 th October 2016 John Mauel Head of Energy Transactions, United States Norton Rose Fulbright US LLP An industry in transformation

The Evolving Global LNG Industry South Africa Gas Options, Cape Town, 3 rd 5 th October 2016 John Mauel Head of Energy Transactions, United States Norton Rose Fulbright US LLP An industry in transformation

Brian A. Habacivch Constellation, Commodities Management Group October 20, 2018

North American Energy Outlook The Transformative Role of Shale in the Global Hydrocarbons Market Why It Matters to Commercial, Institutional, and Industrial End Users Brian A. Habacivch Constellation,

North American Energy Outlook The Transformative Role of Shale in the Global Hydrocarbons Market Why It Matters to Commercial, Institutional, and Industrial End Users Brian A. Habacivch Constellation,

Developments in global gas markets & the impact on Asia LNG - my flexible friend in the face of uncertainty Neil Semple Singapore Round Table October

Developments in global gas markets & the impact on Asia LNG - my flexible friend in the face of uncertainty Neil Semple Singapore Round Table October 2013 Key takeaways Post Fukushima Japan has been a

Developments in global gas markets & the impact on Asia LNG - my flexible friend in the face of uncertainty Neil Semple Singapore Round Table October 2013 Key takeaways Post Fukushima Japan has been a

TIGHT OIL/ SHALE GAS REVOLUTION. RICE Global E&C Forum - March 19, 2013

TIGHT OIL/ SHALE GAS REVOLUTION RICE Global E&C Forum - March 19, 213 GLOBAL OIL & GAS RESOURCES SOURCE: TOTAL Global resources Liquids Gas ~3,5 Gb ~2,5 Gboe 1 Oil shale Unconventional resources ** 8 35

TIGHT OIL/ SHALE GAS REVOLUTION RICE Global E&C Forum - March 19, 213 GLOBAL OIL & GAS RESOURCES SOURCE: TOTAL Global resources Liquids Gas ~3,5 Gb ~2,5 Gboe 1 Oil shale Unconventional resources ** 8 35

Natural Gas Opportunities

Natural Gas Opportunities NAFTANEXT Summit Chicago, IL Erica Bowman, Chief Economist April 25, 2014 U.S. Natural Gas Reserves Source: Potential Gas Committee Abundant Supply Estimates of U.S. Recoverable

Natural Gas Opportunities NAFTANEXT Summit Chicago, IL Erica Bowman, Chief Economist April 25, 2014 U.S. Natural Gas Reserves Source: Potential Gas Committee Abundant Supply Estimates of U.S. Recoverable

The Evolving Landscape of the LNG Sector.

The Evolving Landscape of the LNG Sector Four Divisions One Team One integrated full-service team for your project to serve you from concept to commercial operations Ship Broking Logistics Braemar ACM

The Evolving Landscape of the LNG Sector Four Divisions One Team One integrated full-service team for your project to serve you from concept to commercial operations Ship Broking Logistics Braemar ACM

Gas Markets Globalization: Perspectives and Limits

Gas Markets Globalization: Perspectives and Limits By: Sid Ahmed Hamdani, Senior Business Analyst, Sonatrach, Algeria Date:04 June 2012 Venue: Kuala Lumpur Towards Gas Market Globalization? Increasing

Gas Markets Globalization: Perspectives and Limits By: Sid Ahmed Hamdani, Senior Business Analyst, Sonatrach, Algeria Date:04 June 2012 Venue: Kuala Lumpur Towards Gas Market Globalization? Increasing

Höegh LNG The floating LNG services provider. Company and Market Update May 2012

Höegh LNG The floating LNG services provider Company and Market Update May 2012 Forward looking statements This presentation contains forward-looking statements which reflects management s current expectations,

Höegh LNG The floating LNG services provider Company and Market Update May 2012 Forward looking statements This presentation contains forward-looking statements which reflects management s current expectations,

The IEA s Gas 2017 Report - LNG moves to the front

The IEA s Gas 2017 Report - LNG moves to the front Peter Fraser, Head of the Gas, Coal and Power Division EMART Energy, Amsterdam, 5 October 2017 IEA Gas in today s world The contribution of gas Versatile

The IEA s Gas 2017 Report - LNG moves to the front Peter Fraser, Head of the Gas, Coal and Power Division EMART Energy, Amsterdam, 5 October 2017 IEA Gas in today s world The contribution of gas Versatile

World LNG Trade 2014 & Outlook 2015

World LNG Trade 2014 & Outlook 2015 By: Global LNG Info (GLNGI) May 2015 www.globallnginfo.com LNG Trades 2014 (1) 239.2 MMT of LNG traded in 2014, effectively flat for the third year running as reduced

World LNG Trade 2014 & Outlook 2015 By: Global LNG Info (GLNGI) May 2015 www.globallnginfo.com LNG Trades 2014 (1) 239.2 MMT of LNG traded in 2014, effectively flat for the third year running as reduced

RIM LNG Trade Annual 2010 Edition

RIM LNG Trade Annual 2010 Edition -Contents Volume 1 = Liquefacation Terminals in the world 1. Liquefacation Terminals in Asian Pacific Region 1 United states of America(Alaska) 2 Brunei 3 Indonesia 4

RIM LNG Trade Annual 2010 Edition -Contents Volume 1 = Liquefacation Terminals in the world 1. Liquefacation Terminals in Asian Pacific Region 1 United states of America(Alaska) 2 Brunei 3 Indonesia 4

Changes in Dynamics and Pricing of LNG in the Atlantic Basin

Changes in Dynamics and Pricing of LNG in the Atlantic Basin Andrew Williamson Head of LNG Supply, Commercial Operations & Trading Vienna, 29 January 2018 OMV Gas & Power Agenda Changes in Dynamics and

Changes in Dynamics and Pricing of LNG in the Atlantic Basin Andrew Williamson Head of LNG Supply, Commercial Operations & Trading Vienna, 29 January 2018 OMV Gas & Power Agenda Changes in Dynamics and

IHS LATIN AMERICA LPG SEMINAR

ENTERPRISE PRODUCTS PARTNERS L.P. IHS LATIN AMERICA LPG SEMINAR November 8, 2016 Joseph Fasullo Manager, International NGLs ALL RIGHTS RESERVED. ENTERPRISE PRODUCTS PARTNERS L.P. enterpriseproducts.com

ENTERPRISE PRODUCTS PARTNERS L.P. IHS LATIN AMERICA LPG SEMINAR November 8, 2016 Joseph Fasullo Manager, International NGLs ALL RIGHTS RESERVED. ENTERPRISE PRODUCTS PARTNERS L.P. enterpriseproducts.com

LNG Facts A Primer. Presentation before US Department of Energy, Office of Fossil Energy, LNG Forums. March 10, Kristi A. R.

LNG Facts A Primer Presentation before US Department of Energy, Office of Fossil Energy, LNG Forums March 10, 2006 Kristi A. R. Darby Center for Louisiana State University Overview What is Natural Gas?

LNG Facts A Primer Presentation before US Department of Energy, Office of Fossil Energy, LNG Forums March 10, 2006 Kristi A. R. Darby Center for Louisiana State University Overview What is Natural Gas?

LNG TRADE FLOWS. Hans Stinis Shell Upstream International

LNG TRADE FLOWS Hans Stinis Shell Upstream International ABSTRACT The LNG industry has witnessed a great deal of change recently, and indications are that this will only continue. Global gas demand is

LNG TRADE FLOWS Hans Stinis Shell Upstream International ABSTRACT The LNG industry has witnessed a great deal of change recently, and indications are that this will only continue. Global gas demand is

LNG: DEVELOPMENTS GLOBALLY AND IN EUROPE. Roger Bounds Vice President Global Gas at Shell 17 th March 2016

LNG: DEVELOPMENTS GLOBALLY AND IN EUROPE Roger Bounds Vice President Global Gas at Shell 17 th March 2016 Copyright of Copyright Royal Dutch of COMPANY Shell plc NAME 1 DEFINITIONS AND CAUTIONARY NOTE

LNG: DEVELOPMENTS GLOBALLY AND IN EUROPE Roger Bounds Vice President Global Gas at Shell 17 th March 2016 Copyright of Copyright Royal Dutch of COMPANY Shell plc NAME 1 DEFINITIONS AND CAUTIONARY NOTE

Corporate Presentation

Corporate Presentation Enercom Conference Denver, Colorado August 2018 John Howie, President Tellurian Production Company Cautionary statements Forward-looking statements The information in this presentation

Corporate Presentation Enercom Conference Denver, Colorado August 2018 John Howie, President Tellurian Production Company Cautionary statements Forward-looking statements The information in this presentation

Marine Technology Society Houston, Texas April 28, Energy Bridge. Bringing Continents of Energy Together

Marine Technology Society Houston, Texas April 28, 5 Energy Bridge Bringing Continents of Energy Together Agenda The economics of Challenges to building regasification facilities in the United States Growth

Marine Technology Society Houston, Texas April 28, 5 Energy Bridge Bringing Continents of Energy Together Agenda The economics of Challenges to building regasification facilities in the United States Growth

CHENIERE ENERGY, INC J.P. MORGAN GLOBAL HIGH YIELD & LEVERAGED FINANCE CONFERENCE. March 2016

CHENIERE ENERGY, INC. 2016 J.P. MORGAN GLOBAL HIGH YIELD & LEVERAGED FINANCE CONFERENCE March 2016 Forward Looking Statements This presentation contains certain statements that are, or may be deemed to

CHENIERE ENERGY, INC. 2016 J.P. MORGAN GLOBAL HIGH YIELD & LEVERAGED FINANCE CONFERENCE March 2016 Forward Looking Statements This presentation contains certain statements that are, or may be deemed to

Russia s Changing Role in the Global Gas Market

Russia s Changing Role in the Global Gas Market Dr. Tatiana Mitrova Head of Oil and Gas Department Energy Research Institute of the Russian Academy of Sciences Daegu June 18, 2013 1 1 CHANGING GLOBAL GAS

Russia s Changing Role in the Global Gas Market Dr. Tatiana Mitrova Head of Oil and Gas Department Energy Research Institute of the Russian Academy of Sciences Daegu June 18, 2013 1 1 CHANGING GLOBAL GAS

CHENIERE ENERGY, INC.

CHENIERE ENERGY, INC. J.P. MORGAN WEST COAST ENERGY INFRASTRUCTURE/MLP 1x1 FORUM March 2016 Forward Looking Statements This presentation contains certain statements that are, or may be deemed to be, forward-looking

CHENIERE ENERGY, INC. J.P. MORGAN WEST COAST ENERGY INFRASTRUCTURE/MLP 1x1 FORUM March 2016 Forward Looking Statements This presentation contains certain statements that are, or may be deemed to be, forward-looking

The Global Context for Alaskan Oil and LNG

The Global Context for Alaskan Oil and LNG PRESENTED TO LSI Energy in Alaska Conference PRESENTED BY Paul R. Carpenter Steven H. Levine Anul Thapa December 12, 2016 Copyright 2015 The Brattle Group, Inc.

The Global Context for Alaskan Oil and LNG PRESENTED TO LSI Energy in Alaska Conference PRESENTED BY Paul R. Carpenter Steven H. Levine Anul Thapa December 12, 2016 Copyright 2015 The Brattle Group, Inc.

The Impact of the Recession on Gas Markets

The Impact of the Recession on Gas Markets What has changed in our Brave New World Gas demand dropped by 2% Bigger drops in OECD region, FSU, Latin America But some notable exceptions: China, India Some

The Impact of the Recession on Gas Markets What has changed in our Brave New World Gas demand dropped by 2% Bigger drops in OECD region, FSU, Latin America But some notable exceptions: China, India Some

June North American LNG Projects and Outlook

June 2014 North American LNG Projects and Outlook About your presenter: Geoffrey Cann National Director, Oil and Gas, Deloitte Brisbane 25 years with Deloitte Canada, Korea, Japan, China, Hong Kong, Australia,

June 2014 North American LNG Projects and Outlook About your presenter: Geoffrey Cann National Director, Oil and Gas, Deloitte Brisbane 25 years with Deloitte Canada, Korea, Japan, China, Hong Kong, Australia,

An Exporter s Perspective

An Exporter s Perspective Kathleen Eisbrenner CEO, Pangea LNG B.V. May 2013 Mayer Brown is a global legal services provider comprising legal practices that are separate entities (the "Mayer Brown Practices").

An Exporter s Perspective Kathleen Eisbrenner CEO, Pangea LNG B.V. May 2013 Mayer Brown is a global legal services provider comprising legal practices that are separate entities (the "Mayer Brown Practices").

Japan s LNG Policies and Japan-Argentina Cooperation. December 2014

Japan s LNG Policies and Japan-Argentina Cooperation December 2014 High Dependency On Fossil Fuels For Power Generation The nuclear power ratio in domestic power generation has decreased after the Great

Japan s LNG Policies and Japan-Argentina Cooperation December 2014 High Dependency On Fossil Fuels For Power Generation The nuclear power ratio in domestic power generation has decreased after the Great

Milken Institute: Center for Accelerating Energy Solutions

Milken Institute: Center for Accelerating Energy Solutions Center for Accelerating Energy Solutions Promotes policy and market mechanisms to build a more stable and sustainable energy future Identifies

Milken Institute: Center for Accelerating Energy Solutions Center for Accelerating Energy Solutions Promotes policy and market mechanisms to build a more stable and sustainable energy future Identifies

NARUC. Global Liquefied Natural Gas Supply: An Introduction for Public Utility Commissioners

2009 Global Liquefied Natural Gas Supply: An Introduction for Public Utility Commissioners NARUC October 2009 The National Association of Regulatory Utility Commissioners Funded by the U.S. Department

2009 Global Liquefied Natural Gas Supply: An Introduction for Public Utility Commissioners NARUC October 2009 The National Association of Regulatory Utility Commissioners Funded by the U.S. Department

RYSTAD ENERGY GAS PERSPECTIVES. Jakarta, November 20 th 2017

RYSTAD ENERGY GAS PERSPECTIVES Jakarta, November 2 th 217 Agenda 1. Global LNG market outlook Oversupply and new Asian demand 2. Japan LNG Market outlook LNG demand in a nuclear restart 2 Longer distances

RYSTAD ENERGY GAS PERSPECTIVES Jakarta, November 2 th 217 Agenda 1. Global LNG market outlook Oversupply and new Asian demand 2. Japan LNG Market outlook LNG demand in a nuclear restart 2 Longer distances

7. Liquefied Natural Gas (LNG)

") 7. Liquefied Natural Gas (LNG) Figure 7-1: LNG supply chain Source; Total Liquid natural gas (LNG) is a good alternative to natural gas in remote locations or when the distance between the producer and

7. Liquefied Natural Gas (LNG) Figure 7-1: LNG supply chain Source; Total Liquid natural gas (LNG) is a good alternative to natural gas in remote locations or when the distance between the producer and

Gas Market Report 2017

Gas Market Report 2017 Peter Fraser, Head of the Gas Coal and Power Markets Division Norwegian Ministry of Petroleum and Energy, Oslo, 5 th September 2017 IEA Gas in today s world The contribution of gas

Gas Market Report 2017 Peter Fraser, Head of the Gas Coal and Power Markets Division Norwegian Ministry of Petroleum and Energy, Oslo, 5 th September 2017 IEA Gas in today s world The contribution of gas

[LNG MARKET ANALYSIS ] 1. LNG Market Analysis

![[LNG MARKET ANALYSIS ] 1. LNG Market Analysis](/thumbs/83/87599942.jpg "[LNG MARKET ANALYSIS ] 1. LNG Market Analysis") [LNG MARKET ANALYSIS ] 1 LNG Market Analysis LNG Market Analysis Volume: 20 th April 2018 LNG and Natural Gas Price Assessment 14 th 20 th April 2018 [LNG MARKET ANALYSIS ] 2 LNG Analysis Global LNG prices

[LNG MARKET ANALYSIS ] 1 LNG Market Analysis LNG Market Analysis Volume: 20 th April 2018 LNG and Natural Gas Price Assessment 14 th 20 th April 2018 [LNG MARKET ANALYSIS ] 2 LNG Analysis Global LNG prices

Bcma Global LNG Liqufaction capacity existing & FID d/under construction

OXFORD INSTITUTE FOR ENERGY STUDIES Natural Gas Research Programme Asian LNG Market Development to 2025: pricing and contractual challenges Professor Jonathan Stern Chairman and Senior Research Fellow

OXFORD INSTITUTE FOR ENERGY STUDIES Natural Gas Research Programme Asian LNG Market Development to 2025: pricing and contractual challenges Professor Jonathan Stern Chairman and Senior Research Fellow

The Economics of LNG Export Contract Flexibility: a quantitative approach

The Economics of LNG Export Contract Flexibility: a quantitative approach By Yichi Zhang, 29 October 2012, EPRG weekly seminar Supervisors: Pierre Noel, Chi Kong Chyong shebazhang@gmail.com Introduction

The Economics of LNG Export Contract Flexibility: a quantitative approach By Yichi Zhang, 29 October 2012, EPRG weekly seminar Supervisors: Pierre Noel, Chi Kong Chyong shebazhang@gmail.com Introduction

COMPETITIVE ANALYSIS OF CANADIAN LNG. CERI Breakfast Overview Allan Fogwill, President & CEO Sept 19, 2018

COMPETITIVE ANALYSIS OF CANADIAN LNG CERI Breakfast Overview Allan Fogwill, President & CEO Sept 19, 2018 Overview Canadian Energy Research Institute Founded in 1975, the Canadian Energy Research Institute

COMPETITIVE ANALYSIS OF CANADIAN LNG CERI Breakfast Overview Allan Fogwill, President & CEO Sept 19, 2018 Overview Canadian Energy Research Institute Founded in 1975, the Canadian Energy Research Institute

[LNG MARKET ANALYSIS ] 1. LNG Market Analysis

![[LNG MARKET ANALYSIS ] 1. LNG Market Analysis](/thumbs/83/87599992.jpg "[LNG MARKET ANALYSIS ] 1. LNG Market Analysis") [LNG MARKET ANALYSIS ] 1 LNG Market Analysis LNG Market Analysis Volume: 8 th June 2018 LNG and Natural Gas Price Assessment 28 th May 8 th June 2018 [LNG MARKET ANALYSIS ] 2 LNG Analysis Stable to bullish

[LNG MARKET ANALYSIS ] 1 LNG Market Analysis LNG Market Analysis Volume: 8 th June 2018 LNG and Natural Gas Price Assessment 28 th May 8 th June 2018 [LNG MARKET ANALYSIS ] 2 LNG Analysis Stable to bullish

Natural Gas. Dr. Fred Beach Energy Institute The University of Texas at Austin. Infrastructure as Momentum. Dr. Fred C. Beach.

Infrastructure as Momentum Dr. Fred Beach Energy Institute The University of Texas at Austin 1 Fossil Fuels Supply 87% of All Energy Consumption in the World 2 Global Consumption Trends 2011 Energy Consumption,

Infrastructure as Momentum Dr. Fred Beach Energy Institute The University of Texas at Austin 1 Fossil Fuels Supply 87% of All Energy Consumption in the World 2 Global Consumption Trends 2011 Energy Consumption,

The US shale revolution and its economic impact

The US shale revolution and its economic impact Sylvie Cornot-Gandolphe Groupe Idées, Rueil Malmaison, 16 mars 2015 1 The US shale revolution and its economic impact 1. Shale gas Coal-to-gas switching

The US shale revolution and its economic impact Sylvie Cornot-Gandolphe Groupe Idées, Rueil Malmaison, 16 mars 2015 1 The US shale revolution and its economic impact 1. Shale gas Coal-to-gas switching

DUAL PLENARY SESSION: Energy Market Integration - Developments in LNG

DUAL PLENARY SESSION: Energy Market Integration - Developments in LNG Effects of recent and future developments in LNG markets on the interconnectedness of regional gas markets Fisoye Delano Poten & Partners

DUAL PLENARY SESSION: Energy Market Integration - Developments in LNG Effects of recent and future developments in LNG markets on the interconnectedness of regional gas markets Fisoye Delano Poten & Partners

Edgardo Curcio President AIEE

Edgardo Curcio President AIEE The First National Conference on Liquefied Natural Gas for Transports - Italy and the Mediterranean Sea April 11, 2013 What is LNG? The LNG (Liquefied Natural Gas) is a fluid

Edgardo Curcio President AIEE The First National Conference on Liquefied Natural Gas for Transports - Italy and the Mediterranean Sea April 11, 2013 What is LNG? The LNG (Liquefied Natural Gas) is a fluid

Lecture 12. LNG Markets

Lecture 12 LNG Markets Data from BP Statistical Review of World Energy 1991 to 2016 Slide 1 LNG Demand LNG demand is expected to grow from China, India and Europe in particular. Currently biggest importer

Lecture 12 LNG Markets Data from BP Statistical Review of World Energy 1991 to 2016 Slide 1 LNG Demand LNG demand is expected to grow from China, India and Europe in particular. Currently biggest importer

Fundamentals. Summer 2018

Fundamentals Summer 2018 Cautionary statements Forward-looking statements The information in this presentation includes forward-looking statements within the meaning of Section 27A of the Securities Act

Fundamentals Summer 2018 Cautionary statements Forward-looking statements The information in this presentation includes forward-looking statements within the meaning of Section 27A of the Securities Act

Global LNG-based natural gas trade: The role of the US and Louisiana

Global LNG-based natural gas trade: The role of the US and Louisiana Energy Summit 2018 Louisiana s Place in the Global Energy Economy LSU Center for Energy Studies Baton Rouge, Louisiana October 24, 2018

Global LNG-based natural gas trade: The role of the US and Louisiana Energy Summit 2018 Louisiana s Place in the Global Energy Economy LSU Center for Energy Studies Baton Rouge, Louisiana October 24, 2018

[LNG MARKET ANALYSIS ] 1. LNG Market Analysis

![[LNG MARKET ANALYSIS ] 1. LNG Market Analysis](/thumbs/82/85327793.jpg "[LNG MARKET ANALYSIS ] 1. LNG Market Analysis") [LNG MARKET ANALYSIS ] 1 LNG Market Analysis LNG Market Analysis Volume: 6 th April 2018 [LNG MARKET ANALYSIS ] 2 LNG and Natural Gas Price Assessment 26 th March 6 th April 2018 LNG Analysis Global LNG

[LNG MARKET ANALYSIS ] 1 LNG Market Analysis LNG Market Analysis Volume: 6 th April 2018 [LNG MARKET ANALYSIS ] 2 LNG and Natural Gas Price Assessment 26 th March 6 th April 2018 LNG Analysis Global LNG

ASIAN OFFSHORE ENERGY CONFERENCE DISPUTES IN LNG CONTRACTS

ASIAN OFFSHORE ENERGY CONFERENCE 28 SEPTEMBER 2017 DISPUTES IN LNG CONTRACTS Bob Broxson BDO USA, LLP, a Delaware limited liability partnership, is the U.S. member of BDO International Limited, a UK company

ASIAN OFFSHORE ENERGY CONFERENCE 28 SEPTEMBER 2017 DISPUTES IN LNG CONTRACTS Bob Broxson BDO USA, LLP, a Delaware limited liability partnership, is the U.S. member of BDO International Limited, a UK company

Why it Makes Sense for Europe to Embrace Nord Stream 2?

Why it Makes Sense for Europe to Embrace Nord Stream 2? Sergei Komlev Head of Contract Structuring and Price Formation Directorate Gazprom Export Global Gas Centre Meeting Brussels, December 10 th, 2015

Why it Makes Sense for Europe to Embrace Nord Stream 2? Sergei Komlev Head of Contract Structuring and Price Formation Directorate Gazprom Export Global Gas Centre Meeting Brussels, December 10 th, 2015

Asia-Pacific Gas Market Developments Long Term and Short Term Predictions Sarah Fairhurst - O&M and Lifecycle Management Strategies for CCGT Power

Asia-Pacific Gas Market Developments Long Term and Short Term Predictions Sarah Fairhurst - O&M and Lifecycle Management Strategies for CCGT Power Plants, 29 November 2013 The long title of this talk is:

Asia-Pacific Gas Market Developments Long Term and Short Term Predictions Sarah Fairhurst - O&M and Lifecycle Management Strategies for CCGT Power Plants, 29 November 2013 The long title of this talk is:

The Role of GCC s Natural Gas in the World s Gas Markets

World Review of Business Research Vol. 1. No. 2. May 2011 Pp. 168-178 The Role of GCC s Natural Gas in the World s Gas Markets Abdulkarim Ali Dahan* The objective of this research is to analyze the growth

World Review of Business Research Vol. 1. No. 2. May 2011 Pp. 168-178 The Role of GCC s Natural Gas in the World s Gas Markets Abdulkarim Ali Dahan* The objective of this research is to analyze the growth

The Uncertain Future For ANS LNG Exports

The Uncertain Future For ANS LNG Exports Presented to: LSI Energy in Alaska Conference Anchorage, AK Presented by: Paul R. Carpenter Steven H. Levine Anul Thapa The Brattle Group 44 Brattle Street Cambridge,

The Uncertain Future For ANS LNG Exports Presented to: LSI Energy in Alaska Conference Anchorage, AK Presented by: Paul R. Carpenter Steven H. Levine Anul Thapa The Brattle Group 44 Brattle Street Cambridge,

[LNG MARKET ANALYSIS ] 1. LNG Market Analysis

![[LNG MARKET ANALYSIS ] 1. LNG Market Analysis](/thumbs/82/85327769.jpg "[LNG MARKET ANALYSIS ] 1. LNG Market Analysis") [LNG MARKET ANALYSIS ] 1 LNG Market Analysis LNG Market Analysis Volume: 13 th April 2018 LNG and Natural Gas Price Assessment 3 rd 13 th April 2018 [LNG MARKET ANALYSIS ] 2 LNG Analysis Global LNG prices

[LNG MARKET ANALYSIS ] 1 LNG Market Analysis LNG Market Analysis Volume: 13 th April 2018 LNG and Natural Gas Price Assessment 3 rd 13 th April 2018 [LNG MARKET ANALYSIS ] 2 LNG Analysis Global LNG prices

Energy Trade Flows. U.S. LNG-based natural gas exports

Energy Trade Flows U.S. LNG-based natural gas exports Energy and the Economy: Charting the Course Ahead A joint conference hosted by the Federal Reserve Bank of Dallas and Federal Reserve Bank of Kansas

Energy Trade Flows U.S. LNG-based natural gas exports Energy and the Economy: Charting the Course Ahead A joint conference hosted by the Federal Reserve Bank of Dallas and Federal Reserve Bank of Kansas

Shale Gas as an Alternative Petrochemical Feedstock

Shale Gas as an Alternative Petrochemical Feedstock Tecnon OrbiChem Seminar at KICHEM 2012 Seoul - 2 November, 2012 Roger Lee SHALE GAS WHERE DOES IT COME FROM? Source: EIA SHALE GAS EXPLOITATION Commercial

Shale Gas as an Alternative Petrochemical Feedstock Tecnon OrbiChem Seminar at KICHEM 2012 Seoul - 2 November, 2012 Roger Lee SHALE GAS WHERE DOES IT COME FROM? Source: EIA SHALE GAS EXPLOITATION Commercial

LNG as a global market ESCP London School London, September 22nd, 2015 GUY BROGGI SENIOR ADVISOR, LNG DIVISON

LNG as a global market ESCP London School London, September 22nd, 2015 GUY BROGGI SENIOR ADVISOR, LNG DIVISON Today s Menu (and take-aways ) Latest changes in the LNG landscape 2014 was a continuation

LNG as a global market ESCP London School London, September 22nd, 2015 GUY BROGGI SENIOR ADVISOR, LNG DIVISON Today s Menu (and take-aways ) Latest changes in the LNG landscape 2014 was a continuation

[LNG MARKET ANALYSIS ] 1. LNG Market Analysis

![[LNG MARKET ANALYSIS ] 1. LNG Market Analysis](/thumbs/89/100997948.jpg "[LNG MARKET ANALYSIS ] 1. LNG Market Analysis") [LNG MARKET ANALYSIS ] 1 LNG Market Analysis LNG Market Analysis Volume: 23 rd March 2018 [LNG MARKET ANALYSIS ] 2 LNG Price Assessment and Natural Gas 12 th 23 rd March 2018 LNG Analysis Global LNG prices

[LNG MARKET ANALYSIS ] 1 LNG Market Analysis LNG Market Analysis Volume: 23 rd March 2018 [LNG MARKET ANALYSIS ] 2 LNG Price Assessment and Natural Gas 12 th 23 rd March 2018 LNG Analysis Global LNG prices

Does LNG Threaten Russian Supplies to Europe?

Does LNG Threaten Russian Supplies to Europe? Sergei Komlev Head of Contract Structuring and Price Formation Directorate Gazprom Export IEA workshop on Eurasian gas markets Paris, April15 th, 2016 2010

Does LNG Threaten Russian Supplies to Europe? Sergei Komlev Head of Contract Structuring and Price Formation Directorate Gazprom Export IEA workshop on Eurasian gas markets Paris, April15 th, 2016 2010

Impact of American Unconventional Oil and Gas Revolution

National University of Singapore Energy Studies Institute 18 May 215 Impact of American Unconventional Oil and Gas Revolution Edward C. Chow Senior Fellow Revenge of the Oil Price Cycle American Innovation:

National University of Singapore Energy Studies Institute 18 May 215 Impact of American Unconventional Oil and Gas Revolution Edward C. Chow Senior Fellow Revenge of the Oil Price Cycle American Innovation: