Denie S Tampubolon Senior VP Upstream Business Development

|

|

|

- Merry Maxwell

- 6 years ago

- Views:

Transcription

1 Denie S Tampubolon Senior VP Upstream Business Development

2 Pertamina : Scope of Business PT Pertamina EP PT Pertamina EP Cepu PT Pertamina Hulu Indonesia PT Pertamina EP Cepu ADK PT Elnusa Tbk. PT Pertamina Hulu Energi PT Pertamina Geothermal Energy PT Pertamina Internasional EP PT Pertamina Drilling Services Indonesia PT Pertamina Gas PT Pertamina Trans Kontinental PT Pertamina Retail PT Pertamina Lubricants PT Pertamina Patra Niaga Pertamina International Timor SA Non Core Business: Patra Jasa, Pelita Air Service, Pertamina Trans Kontinental, Pertamina Bina Medika, Tugu Pratama Indonesia, Pertamina Dana Ventura, Pertamina Training & Consulting.

3 Indonesia Economic Forecast in

500 Oil Production 2")

4 Indonesia Oil & Gas Reserves and Production The oil supply - demand balance is projected to reach a deficit of up to 1.5 million bpd by 2025 BOPD 2,000 Oil Production & Consumption Oil Consumption BCFD 9 Gas Production & Consumption 8 Gas Production 1, , Gas Production (domestic) 500 Oil Production Indonesia's oil reserves is at 3.6 Billion bbl (0.2% of the world's total reserves) 2025 SOURCE: BP Statistical Review 2016, SKKMigas Projection Indonesia's gas reserves is at 100 TCF (1.5% of total world reserves)

5 NOC Comparison: Domestic Production Portion 2015 Oil & Gas Production Thousand barrel equivalent per day Saudi Arabia 11,978 NOC Portion Percentage (%) 99 China 6, Algeria 2, Brazil 2, Norway 3, Nigeria 3, Malaysia 1, Indonesia 1, NOC Production Non NOC Production 5 SOURCE: Woodmackenzie, 2015

6 40 CONVENTIONAL 16 UNCONVENTIONAL 14 GEOTHERMAL MANAGED BY 6 SUBSIDIARIES

7 Aspiring Supply Growth to 2 Million BOEPD Increased oil and gas production from existing assets (exploration, EOR) as well as from business development (including transfer of post-expiry blocks in Indonesia). MBOEPD 2500 ASPIRATION ACTUAL ASET EXISTING EKSISTING ASSETS ASET POST EXPIRY EX-TERMINASI ASSETS ACQUISITION AKUISISI 7 SOURCE: Pertamina

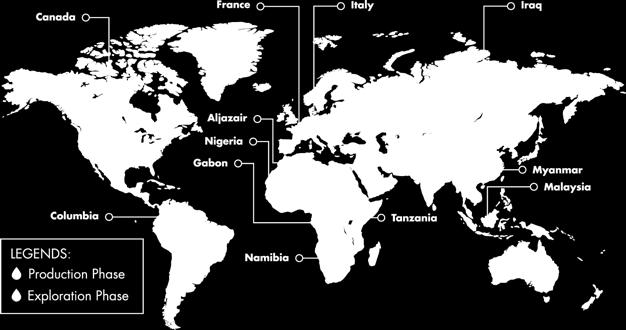

8 Upstream Business Development Strategies 1. Exploration : - Existing Assets - New Assets : Joint Study / Bid Round / PI 15% on new awarded block 2. Mature Fields : - Existing Assets : EOR - Post-Expiry Blocks in Indonesia : e.g. Mahakam, Sanga-sanga, OSES 3. Acquisition Overseas, production assets or discovered reserves 8 SOURCE: Pertamina

, while parts of South America are in turmoil (Brazil, Venezuela).")

9 Geopolitics and Petroleum Industry Despite the strengthening of oil prices is not expected to happen anytime soon, there remains a chance for the upstream oil and gas investment in the short and long term. Geopolitics Improved geopolitics and security of Africa and the Middle East (Iraq, Uganda, Sudan, Libya), while parts of South America are in turmoil (Brazil, Venezuela). OPEC countries reached a production-cutting deal in December 2016 and backed by non-opec major producers (Russia, Norway) Economics World economic growth has not fully recovered hence weaker demand growth in developing countries (China, India) Policy of several countries in opening up opportunities for foreign investment (Mexico, Iran, UAE, Saudi Arabia). US policy allows oil and gas exports from late of Oil & Gas Industry E&P companies and services adapt to lower oil prices with more focused and prudent investment efficiency (e.g. shale oil in North America). Substitution policy to more environmentally friendly and sustainable energy (solar power in the Middle East) or more competitive energy. => The world's oil supplies are to the point of equilibrium at lower oil prices. 9

10 Pertamina Exploration Way 10 SOURCE: Pertamina

, Pertamina EP, PHE/subsidiaries, UTC ~ 40 personnel, 24 months")

11 Integrated Tarakan Basin Regional Study Background After several new discoveries, there is a need to develop comprehensive and integrated exploration concept throughout Pertamina working areas e.g Bunyu, Tarakan, Nunukan, Simenggaris, Bukat, E. Ambalat) Purpose Integrate existing play concept and identify/develop New Play concept throughout Tarakan Basin. Execution Team : Exploration team in Pertamina Upstream (holding), Pertamina EP, PHE/subsidiaries, UTC ~ 40 personnel, 24 months 11 Lokasi Studi Study Area

12 12 TERIMA KASIH

13 Upstream Business Development Strategies and Stages Investment Selection and Approval Stages Initiation ~90 ~45 Stages Evaluated opportunity Recommended opportunities for further evaluation DG 1 DG 2 Selection Stages Further Execution ~35 ~20 Evaluation ~10 Stages 6 Stages DIRECTORATE CORPORATE DG 3 DG 4 DG 5 Operation Stages 2016 Track Record 13 SOURCE: Pertamina

14 Priority for Upstream Business Development Priority on oil fields with production or development assets stages with potentially substantial reserves for Pertamina. Middle East & Africa Southeast Asia 14 SOURCE: Pertamina

Upstream /15/2009. Industry Outlook - Oil & Gas Demand/Supply. Required New Production. Production MOEBD. Frédéric Guinot.

Oil and Gas Industry Upstream 29 Frédéric Guinot Swiss Section The Challenge MOEBD Industry Outlook - Oil & Gas Demand/Supply 2 World Demand 16 175 12 8 9 12 Required New Production Equal to Today s Production

Oil and Gas Industry Upstream 29 Frédéric Guinot Swiss Section The Challenge MOEBD Industry Outlook - Oil & Gas Demand/Supply 2 World Demand 16 175 12 8 9 12 Required New Production Equal to Today s Production

ZHOU Peng. College of Economics and Management & Research Center for Soft Energy Science Nanjing University of Aeronautics and Astronautics, China

China s Energy Import Dependency: Status and Strategies ZHOU Peng College of Economics and Management & Research Center for Soft Energy Science Nanjing University of Aeronautics and Astronautics, China

China s Energy Import Dependency: Status and Strategies ZHOU Peng College of Economics and Management & Research Center for Soft Energy Science Nanjing University of Aeronautics and Astronautics, China

International Energy Outlook 2011

International Energy Outlook 211 Center for Strategic and International Studies, Acting Administrator September 19, 211 Washington, DC U.S. Energy Information Administration Independent Statistics & Analysis

International Energy Outlook 211 Center for Strategic and International Studies, Acting Administrator September 19, 211 Washington, DC U.S. Energy Information Administration Independent Statistics & Analysis

CHAPTER 4: A REVIEW OF THE ENERGY ECONOMY IN IRAN AND OTHER COUNTRIES

CHAPTER 4: A REVIEW OF THE ENERGY ECONOMY IN IRAN AND OTHER COUNTRIES 60 Nowadays, energy is the lifeblood of modern civilization. The shortage of energy that can be one of the issues related to the economy

CHAPTER 4: A REVIEW OF THE ENERGY ECONOMY IN IRAN AND OTHER COUNTRIES 60 Nowadays, energy is the lifeblood of modern civilization. The shortage of energy that can be one of the issues related to the economy

Challenges of Fracking for the MENA Region Martin Bachmann, Member of the Board

Challenges of Fracking for the MENA Region Martin Bachmann, Member of the Board NUMOV German MENA Conference Berlin, 26 January 2017 Simplified Model of Hydrocarbon Deposits Conventional versus Unconventional

Challenges of Fracking for the MENA Region Martin Bachmann, Member of the Board NUMOV German MENA Conference Berlin, 26 January 2017 Simplified Model of Hydrocarbon Deposits Conventional versus Unconventional

Overview of global crude oil reserve estimates and supply patterns. Professor Wumi Iledare LSU Center for Energy studies Baton Rouge, LA 70803

Overview of global crude oil reserve estimates and supply patterns Professor Wumi Iledare LSU Center for Energy studies Baton Rouge, LA 70803 Presentation at Audubon Kiwanis Weekly Meeting Baton Rouge,

Overview of global crude oil reserve estimates and supply patterns Professor Wumi Iledare LSU Center for Energy studies Baton Rouge, LA 70803 Presentation at Audubon Kiwanis Weekly Meeting Baton Rouge,

Production: Industry view. World Oil Reserves and. World Oil Reserves and. Kuwait Energy Company. Ray Leonard. ASPO 2007 Cork Ireland

World Oil Reserves and World Oil Reserves and Production: Industry view ASPO 2007 Cork Ireland Ray Leonard Kuwait Energy Company November 2006 Hedberg Conference November 2006 Hedberg Conference Gathering

World Oil Reserves and World Oil Reserves and Production: Industry view ASPO 2007 Cork Ireland Ray Leonard Kuwait Energy Company November 2006 Hedberg Conference November 2006 Hedberg Conference Gathering

B O USINESS VER VIEW. FY 2012 Financial Results Briefing. May 13 th, Keisuke Takeuchi Chairman and Representative Director

Translation This presentation is English-language translation of the original Japanese-language document for your convenience. In the case that there is any discrepancy between the Japanese and English

Translation This presentation is English-language translation of the original Japanese-language document for your convenience. In the case that there is any discrepancy between the Japanese and English

Recent Developments in Global Crude Oil and Natural Gas Markets

Recent Developments in Global Crude Oil and Natural Gas Markets Kenneth B Medlock III, PhD James A Baker III and Susan G Baker Fellow in Energy and Resource Economics, and Senior Director, Center for Energy

Recent Developments in Global Crude Oil and Natural Gas Markets Kenneth B Medlock III, PhD James A Baker III and Susan G Baker Fellow in Energy and Resource Economics, and Senior Director, Center for Energy

Energy Statistics: Making the Numbers Count

Energy Statistics: Making the Numbers Count IFEG Autumn Seminar, 5 th November 29 Paul Appleby, BP Group Economics Team Working with Energy Statistics The key challenges. Finding relevant & reliable data

Energy Statistics: Making the Numbers Count IFEG Autumn Seminar, 5 th November 29 Paul Appleby, BP Group Economics Team Working with Energy Statistics The key challenges. Finding relevant & reliable data

Argus Ethylene Annual 2017

Argus Ethylene Annual 2017 Market Reporting Petrochemicals illuminating the markets Consulting Events Argus Ethylene Annual 2017 Summary Progress to the next peak of the economic cycle, now expected by

Argus Ethylene Annual 2017 Market Reporting Petrochemicals illuminating the markets Consulting Events Argus Ethylene Annual 2017 Summary Progress to the next peak of the economic cycle, now expected by

An Analysis of Major Countries Energy Security Policies and Conditions

An Analysis of Major Countries Energy Security Policies and Conditions Summary Quantitative Assessment of Energy Security Policies Tomoko Murakami * Mitsuru Motokura ** Ichiro Kutani *** In this research,

An Analysis of Major Countries Energy Security Policies and Conditions Summary Quantitative Assessment of Energy Security Policies Tomoko Murakami * Mitsuru Motokura ** Ichiro Kutani *** In this research,

HUBBERT REVISTED---1: Imbalances Among Oil Demand, Reserves, Alternatives Define Energy Dilemma Today

Oil & Gas Journal Volume 102.26 (July 12, 2004) HUBBERT REVISTED---1: Imbalances Among Oil Demand, Reserves, Alternatives Define Energy Dilemma Today Rafael Sandrea, PhD Background A sizzling world economy

Oil & Gas Journal Volume 102.26 (July 12, 2004) HUBBERT REVISTED---1: Imbalances Among Oil Demand, Reserves, Alternatives Define Energy Dilemma Today Rafael Sandrea, PhD Background A sizzling world economy

The Energy Challenge

The Energy Challenge Joan F. Brennecke Dept. of Chemical and Biomolecular Engineering Director, Notre Dame Energy Center Siemens Westinghouse Science and Technology Competition November 12, 2005 ENERGY

The Energy Challenge Joan F. Brennecke Dept. of Chemical and Biomolecular Engineering Director, Notre Dame Energy Center Siemens Westinghouse Science and Technology Competition November 12, 2005 ENERGY

TRINIDAD AND TOBAGO ENERGY CONFERENCE JANUARY 2017

BY TRINIDAD AND TOBAGO ENERGY CONFERENCE JANUARY 2017 *No. of unique client sites Independent and neutral insight. The Rystad Energy business data solution is global. 400 350 300 250 200 150 100 50 0 2010

BY TRINIDAD AND TOBAGO ENERGY CONFERENCE JANUARY 2017 *No. of unique client sites Independent and neutral insight. The Rystad Energy business data solution is global. 400 350 300 250 200 150 100 50 0 2010

BP Energy Outlook 2017 edition

BP Energy Outlook 217 edition Margaret Chen Head of China Economist bp.com/energyoutlook #BPstats Economic backdrop Contributions to GDP growth by factor Contributions to GDP growth by region % per annum

BP Energy Outlook 217 edition Margaret Chen Head of China Economist bp.com/energyoutlook #BPstats Economic backdrop Contributions to GDP growth by factor Contributions to GDP growth by region % per annum

2017 oil price forecast: who predicts best? Information document

2017 oil price forecast: who predicts best? Information document March 2017 Since 2007, Roland Berger has published a yearly overview of available oil price forecasts Roland Berger study of oil price forecasts,

2017 oil price forecast: who predicts best? Information document March 2017 Since 2007, Roland Berger has published a yearly overview of available oil price forecasts Roland Berger study of oil price forecasts,

Gulf Coast Energy Outlook: Addendum.

Gulf Coast Energy Outlook: Addendum. Addendum accompanying whitepaper. See full whitepaper here. David E. Dismukes, Ph.D. Gregory B. Upton, Jr., Ph.D. Center for Energy Studies Louisiana State University

Gulf Coast Energy Outlook: Addendum. Addendum accompanying whitepaper. See full whitepaper here. David E. Dismukes, Ph.D. Gregory B. Upton, Jr., Ph.D. Center for Energy Studies Louisiana State University

Iran and China: Dialogue on Energy

Iran and China: Dialogue on Energy Abbas Maleki Research Seminar Repsol YPF-Harvard KSG Fellows Harvard University March 15, 2006 What is the crux of Iran-China relations? the exchange of Chinese capital

Iran and China: Dialogue on Energy Abbas Maleki Research Seminar Repsol YPF-Harvard KSG Fellows Harvard University March 15, 2006 What is the crux of Iran-China relations? the exchange of Chinese capital

World and U.S. Fossil Fuel Supplies

World and U.S. Fossil Fuel Supplies Daniel O Brien and Mike Woolverton, Extension Agricultural Economists K State Research and Extension Supplies of fossil fuel resources used for energy production vary

World and U.S. Fossil Fuel Supplies Daniel O Brien and Mike Woolverton, Extension Agricultural Economists K State Research and Extension Supplies of fossil fuel resources used for energy production vary

Asia s s National Oil Companies

Asia s s National Oil Companies International Expansion and Competitive Implications Mikkal Herberg The National Bureau of Asian Research The Institute of Energy Economics, Japan Tokyo April 5, 2007 Agenda

Asia s s National Oil Companies International Expansion and Competitive Implications Mikkal Herberg The National Bureau of Asian Research The Institute of Energy Economics, Japan Tokyo April 5, 2007 Agenda

Natural Gas Facts & Figures. New Approach & Proposal

Natural Gas Facts & Figures New Approach & Proposal 1. Production and reserves Sources : Total G&P, WOC1, IEA, IHS Cera, Resources- Reserves o Conventional o Unconventional : types and reserves Countries,

Natural Gas Facts & Figures New Approach & Proposal 1. Production and reserves Sources : Total G&P, WOC1, IEA, IHS Cera, Resources- Reserves o Conventional o Unconventional : types and reserves Countries,

Challenges and opportunities for an integrated oil and gas company

OMV Aktiengesellschaft Challenges and opportunities for an integrated oil and gas company ÖGEW Herbsttagung Vienna, 12 November 2010 Wolfgang Ruttenstorfer CEO and Chairman of the Executive Board OMV Aktiengesellschaft

OMV Aktiengesellschaft Challenges and opportunities for an integrated oil and gas company ÖGEW Herbsttagung Vienna, 12 November 2010 Wolfgang Ruttenstorfer CEO and Chairman of the Executive Board OMV Aktiengesellschaft

Indonesia s $120 Billion Oil and Gas Opportunity

Indonesia s $120 Billion Oil and Gas Opportunity By Alex Dolya, Asheesh Sastry, Eddy Tamboto, and Fadli Rahman It s a prize within reach: between $90 billion and $120 billion of additional GDP over the

Indonesia s $120 Billion Oil and Gas Opportunity By Alex Dolya, Asheesh Sastry, Eddy Tamboto, and Fadli Rahman It s a prize within reach: between $90 billion and $120 billion of additional GDP over the

TOWARDS GLOBAL RECOGNITION BUSINESS PROFILE

TOWARDS GLOBAL RECOGNITION BUSINESS PROFILE INTRODUCTION As Indonesia s flagship national company that is engaged in a broad spectrum of upstream and downstream energy operations, Pertamina has increased

TOWARDS GLOBAL RECOGNITION BUSINESS PROFILE INTRODUCTION As Indonesia s flagship national company that is engaged in a broad spectrum of upstream and downstream energy operations, Pertamina has increased

Gas in Power Generation Sector, the story as told by Jodi-Gas database.

1 GECF Gas in Power Generation Sector, the story as told by Jodi-Gas database. Mohamed Arafat Data Bank Analyst, GECF 14th Regional JODI Training Workshop 9-11 November 2016, Moscow, Russia 2 Agenda Why

1 GECF Gas in Power Generation Sector, the story as told by Jodi-Gas database. Mohamed Arafat Data Bank Analyst, GECF 14th Regional JODI Training Workshop 9-11 November 2016, Moscow, Russia 2 Agenda Why

Institut Français des Relations Internationales Energy Roundtable

Institut Français des Relations Internationales Energy Roundtable Brussels March 21 st, 2013 New Energy Resources in East Africa Pushing back the continent s last hydrocarbon frontier Roger CARVALHO CEO

Institut Français des Relations Internationales Energy Roundtable Brussels March 21 st, 2013 New Energy Resources in East Africa Pushing back the continent s last hydrocarbon frontier Roger CARVALHO CEO

Unconventional Oil & Gas: Reshaping Energy Markets

Unconventional Oil & Gas: Reshaping Energy Markets Guy Caruso Senior Advisor JOGMEC Seminar 7 February 2013 Landscape is Changing Even as We Sit Here Today - US Projected to reach 90% Energy Self-Sufficiency

Unconventional Oil & Gas: Reshaping Energy Markets Guy Caruso Senior Advisor JOGMEC Seminar 7 February 2013 Landscape is Changing Even as We Sit Here Today - US Projected to reach 90% Energy Self-Sufficiency

The GDP growth rate remains high in India and Indonesia, the major markets in the region.

1 2 The GDP growth rate remains high in India and Indonesia, the major markets in the region. Apart from Thailand where has been hit by devastating flood, the economic conditions in Asia remained strong.

1 2 The GDP growth rate remains high in India and Indonesia, the major markets in the region. Apart from Thailand where has been hit by devastating flood, the economic conditions in Asia remained strong.

Fracking Safety & Economics November 9, 2017 America 1 st Energy Conference, Houston Tx.

Fracking Safety & Economics November 9, 2017 America 1 st Energy Conference, Houston Tx. J.M. Leimkuhler, Vice President Drilling LLOG Exploration L.L.C. Fracking Fears, Perceptions Vs Reality Simplistic

Fracking Safety & Economics November 9, 2017 America 1 st Energy Conference, Houston Tx. J.M. Leimkuhler, Vice President Drilling LLOG Exploration L.L.C. Fracking Fears, Perceptions Vs Reality Simplistic

Short Term Energy Outlook March 2011 March 8, 2011 Release

Short Term Energy Outlook March 2011 March 8, 2011 Release Highlights West Texas Intermediate (WTI) and other crude oil spot prices have risen about $15 per barrel since mid February partly in response

Short Term Energy Outlook March 2011 March 8, 2011 Release Highlights West Texas Intermediate (WTI) and other crude oil spot prices have risen about $15 per barrel since mid February partly in response

17 th February 2015 BP Energy Outlook bp.com/energyoutlook #BPstats BP p.l.c. 2015

17 th February 215 BP bp.com/energyoutlook #BPstats Economic backdrop GDP Trillion, $211 PPP 24 Other Non-OECD Asia 18 OECD Contribution to GDP growth Trillion $211 PPP, 213-35 9 Population Income per

17 th February 215 BP bp.com/energyoutlook #BPstats Economic backdrop GDP Trillion, $211 PPP 24 Other Non-OECD Asia 18 OECD Contribution to GDP growth Trillion $211 PPP, 213-35 9 Population Income per

The Unconventional Oil and Gas Market Outlook

The Unconventional Oil and Gas Market Outlook The future of oil sands, shale gas, oil shale and coalbed methane Report Price: $2875 Publication Date: July 2010 E N E R G Y The Unconventional Oil and Gas

The Unconventional Oil and Gas Market Outlook The future of oil sands, shale gas, oil shale and coalbed methane Report Price: $2875 Publication Date: July 2010 E N E R G Y The Unconventional Oil and Gas

Global Energy Reserves

CH2356 Energy Engineering Unit I Global Energy Reserves Dr. M. Subramanian Associate Professor Department of Chemical Engineering Sri Sivasubramaniya Nadar College of Engineering Kalavakkam 603 110, Kanchipuram

CH2356 Energy Engineering Unit I Global Energy Reserves Dr. M. Subramanian Associate Professor Department of Chemical Engineering Sri Sivasubramaniya Nadar College of Engineering Kalavakkam 603 110, Kanchipuram

Rice Outlook and Baseline Projections. University of Arkansas Webinar Series February 13, 2015 Nathan Childs, Economic Research Service, USDA

Rice Outlook and Baseline Projections University of Arkansas Webinar Series February 13, 2015 Nathan Childs, Economic Research Service, USDA THE GLOBAL RICE MARKET PART 1 The 2014/15 Global Rice Market:

Rice Outlook and Baseline Projections University of Arkansas Webinar Series February 13, 2015 Nathan Childs, Economic Research Service, USDA THE GLOBAL RICE MARKET PART 1 The 2014/15 Global Rice Market:

World Energy Outlook 2035: A focus on LNG supply and demand dynamics

World Energy Outlook 2035: A focus on LNG supply and demand dynamics M.H. Siddiqui, Prescience, USA 1 Agenda The Energy Outlook in 2035 involving major landscape changes in supply, demand, fossil fuels,

World Energy Outlook 2035: A focus on LNG supply and demand dynamics M.H. Siddiqui, Prescience, USA 1 Agenda The Energy Outlook in 2035 involving major landscape changes in supply, demand, fossil fuels,

Global Energy Outlook. Offshore Center Danmark Esbjerg Jon Fløgstad, Manager Nordic Oil & Gas Ernst & Young September 13 th, 2012

Global Energy Outlook Offshore Center Danmark Esbjerg Jon Fløgstad, Manager Nordic Oil & Gas Ernst & Young September 13 th, 2012 Agenda Introduction Short-term perspectives Longer-term perspectives Concluding

Global Energy Outlook Offshore Center Danmark Esbjerg Jon Fløgstad, Manager Nordic Oil & Gas Ernst & Young September 13 th, 2012 Agenda Introduction Short-term perspectives Longer-term perspectives Concluding

Global Gasoline, Global Condensate and Global Petrochemical Markets to 2020 and How much naphtha will end up in gasoline blending?

Study Prospectus Nexus - The Interaction Between: Global Gasoline, Global Condensate and Global Petrochemical Markets to 2020 and 2025 Can I export more naphtha? Should I build a splitter? Should I build

Study Prospectus Nexus - The Interaction Between: Global Gasoline, Global Condensate and Global Petrochemical Markets to 2020 and 2025 Can I export more naphtha? Should I build a splitter? Should I build

The Outlook for Energy:

The Outlook for Energy: A View to 2040 Ken Golden February 3, 2016 The Outlook for Energy includes Exxon Mobil Corporation s internal estimates and forecasts of energy demand, supply, and trends through

The Outlook for Energy: A View to 2040 Ken Golden February 3, 2016 The Outlook for Energy includes Exxon Mobil Corporation s internal estimates and forecasts of energy demand, supply, and trends through

BP Energy Outlook 2016 edition

BP Energy Outlook 216 edition Mark Finley 14th February 216 Outlook to 235 bp.com/energyoutlook #BPstats Economic backdrop Trillion, $21 25 Other 2 India Africa 15 China 1 OECD 5 OECD 1965 2 235 GDP 2

BP Energy Outlook 216 edition Mark Finley 14th February 216 Outlook to 235 bp.com/energyoutlook #BPstats Economic backdrop Trillion, $21 25 Other 2 India Africa 15 China 1 OECD 5 OECD 1965 2 235 GDP 2

Russian Oil Supply: Uncertainties and Incentives

Russian Oil Supply: Uncertainties and Incentives Yuri Yegorov 1 January 2016 Task (FWF). Oil peak now attracts more attention of energy economists (see, for example, Semmler and Greiner, 2011). An uncertainty

Russian Oil Supply: Uncertainties and Incentives Yuri Yegorov 1 January 2016 Task (FWF). Oil peak now attracts more attention of energy economists (see, for example, Semmler and Greiner, 2011). An uncertainty

BBC Learning English Talk about English Insight Plus Part 6 Oil

BBC Learning English Insight Plus Part 6 Oil Jackie: Oil makes our world go round they call it black gold. It fuels our cars, runs our industries, it makes our countries work. So when oil prices go up,

BBC Learning English Insight Plus Part 6 Oil Jackie: Oil makes our world go round they call it black gold. It fuels our cars, runs our industries, it makes our countries work. So when oil prices go up,

The Constant Pursuit of Petroleum Self Sufficiency

The Constant Pursuit of Petroleum Self Sufficiency Presentation to the FIESP 14th International Energy Meeting August 5th & 6th, 2013 Pennsylvania, 1859 Total Depth: 21.2m or 69ft Renato T Bertani President

The Constant Pursuit of Petroleum Self Sufficiency Presentation to the FIESP 14th International Energy Meeting August 5th & 6th, 2013 Pennsylvania, 1859 Total Depth: 21.2m or 69ft Renato T Bertani President

North American Natural Gas Exports and Future U.S. Supply: Sound and Fury

North American Natural Gas Exports and Future U.S. Supply: Sound and Fury Arthur E. Berman Labyrinth Consulting Services, Inc. Corpus Christi SIPES Corpus Christi, Texas August 26, 2014 Slide 1 The Future

North American Natural Gas Exports and Future U.S. Supply: Sound and Fury Arthur E. Berman Labyrinth Consulting Services, Inc. Corpus Christi SIPES Corpus Christi, Texas August 26, 2014 Slide 1 The Future

Delivering Energy. Upstream Stranded Domestic Gas Potential to meet Energy Demand through LNG Value Chain: Lessons Learned from Senoro-DSLNG

Delivering Energy Upstream Stranded Domestic Gas Potential to meet Energy Demand through LNG Value Chain: Lessons Learned from Senoro-DSLNG Eka Satria, Development Director - PT Medco Energi International

Delivering Energy Upstream Stranded Domestic Gas Potential to meet Energy Demand through LNG Value Chain: Lessons Learned from Senoro-DSLNG Eka Satria, Development Director - PT Medco Energi International

U.S. EIA s Liquid Fuels Outlook

U.S. EIA s Liquid Fuels Outlook NCSL 2011 Energy Policy Summit: Fueling Tomorrow s Transportation John Staub, Team Lead August 8, 2011 San Antonio, Texas U.S. Energy Information Administration Independent

U.S. EIA s Liquid Fuels Outlook NCSL 2011 Energy Policy Summit: Fueling Tomorrow s Transportation John Staub, Team Lead August 8, 2011 San Antonio, Texas U.S. Energy Information Administration Independent

NOMADS Peak Oil Presentation Houston, Texas April 10, 2008

NOMADS Peak Oil Presentation Houston, Texas April 10, 2008 Presented by Steve Crower Energy Investment Banker Denver, Colorado 832.771.3888 Starlight Investments, LLC Agenda What is Peak Oil? My Conclusions

NOMADS Peak Oil Presentation Houston, Texas April 10, 2008 Presented by Steve Crower Energy Investment Banker Denver, Colorado 832.771.3888 Starlight Investments, LLC Agenda What is Peak Oil? My Conclusions

New energy realities

New energy realities Navigating the triple transition World Energy Council 2016 wwwworldenergyorg @WECouncil Christoph Frei Secretary General World Energy Council November 2016 @chwfrei Billions of People

New energy realities Navigating the triple transition World Energy Council 2016 wwwworldenergyorg @WECouncil Christoph Frei Secretary General World Energy Council November 2016 @chwfrei Billions of People

The price of oil. The disruption caused by the American shale oil industry. Martin Hvidt

News Analysis January 2018 The price of oil. The disruption caused by the American shale oil industry Martin Hvidt News Following the OPEC meeting decision 30 November 2017 to continue the restriction

News Analysis January 2018 The price of oil. The disruption caused by the American shale oil industry Martin Hvidt News Following the OPEC meeting decision 30 November 2017 to continue the restriction

Oil and natural gas: market outlook and drivers

Oil and natural gas: market outlook and drivers for American Foundry Society May 18, 216 Washington, DC by Howard Gruenspecht, Deputy Administrator U.S. Energy Information Administration Independent Statistics

Oil and natural gas: market outlook and drivers for American Foundry Society May 18, 216 Washington, DC by Howard Gruenspecht, Deputy Administrator U.S. Energy Information Administration Independent Statistics

Africa 2013: New roles for Oilfield Service companies in an emerging market. Gavin Graham EVP Business Development

Africa 2013: New roles for Oilfield Service companies in an emerging market Gavin Graham EVP Business Development Oil Council: 2013 Africa O&G Assembly Paris, 11 th June 2013 Oil and gas industry is not

Africa 2013: New roles for Oilfield Service companies in an emerging market Gavin Graham EVP Business Development Oil Council: 2013 Africa O&G Assembly Paris, 11 th June 2013 Oil and gas industry is not

Introduction. Reducing Gas Flaring and Venting: How a Partnership can help achieve success

Reducing Gas Flaring and Venting: How a Partnership can help achieve success Sascha T. Djumena 1 Energy Specialist, Global Gas Flaring Reduction Partnership (GGFR) World Bank/IFC Oil, Gas, Mining and Chemicals

Reducing Gas Flaring and Venting: How a Partnership can help achieve success Sascha T. Djumena 1 Energy Specialist, Global Gas Flaring Reduction Partnership (GGFR) World Bank/IFC Oil, Gas, Mining and Chemicals

Why Would An Investor Be Afraid Of Stranded Oil Assets?

Why Would An Investor Be Afraid Of Stranded Oil Assets? - Even if global oil demand peaks around 2030 why would you worry as an investor? - 85% of the valuation relates to the cash flow the oil producer

Why Would An Investor Be Afraid Of Stranded Oil Assets? - Even if global oil demand peaks around 2030 why would you worry as an investor? - 85% of the valuation relates to the cash flow the oil producer

Global and U.S. Rice Markets Face Tighter Supplies in 2015/16

Global and U.S. Rice Markets Face Tighter Supplies in 2015/16 University of Arkansas Webinar Series November 19, 2015 Nathan Childs, Economic Research Service, USDA 11.20.15 PART 1 THE 2015/16 GLOBAL RICE

Global and U.S. Rice Markets Face Tighter Supplies in 2015/16 University of Arkansas Webinar Series November 19, 2015 Nathan Childs, Economic Research Service, USDA 11.20.15 PART 1 THE 2015/16 GLOBAL RICE

US Oil and Gas Import Dependence: Department of Energy Projections in 2011

1800 K Street, NW Suite 400 Washington, DC 20006 Phone: 1.202.775.3270 Fax: 1.202.775.3199 Email: acordesman@gmail.com Web: www.csis.org/burke/reports US Oil and Gas Import Dependence: Department of Energy

1800 K Street, NW Suite 400 Washington, DC 20006 Phone: 1.202.775.3270 Fax: 1.202.775.3199 Email: acordesman@gmail.com Web: www.csis.org/burke/reports US Oil and Gas Import Dependence: Department of Energy

BP Energy Outlook 2016 edition

BP Energy Outlook 216 edition Spencer Dale, group chief economist Outlook to 235 bp.com/energyoutlook #BPstats Disclaimer This presentation contains forward-looking statements, particularly those regarding

BP Energy Outlook 216 edition Spencer Dale, group chief economist Outlook to 235 bp.com/energyoutlook #BPstats Disclaimer This presentation contains forward-looking statements, particularly those regarding

Conventional Energies (Oil & Gas)

") 13 Conventional Energies (Oil & Gas) 162 Conventional Energies (Oil & Gas) Conventional Energies (Oil & Gas) I. History and Background The first documented systematic oil exploration and drilling in Iran

13 Conventional Energies (Oil & Gas) 162 Conventional Energies (Oil & Gas) Conventional Energies (Oil & Gas) I. History and Background The first documented systematic oil exploration and drilling in Iran

An overview of global cement sector trends

An overview of global cement sector trends Insights from the Global Cement Report 1 th Edition XXX Technical Congress FICEM-APCAC 2 September, 213 Lima, Peru Thomas Armstrong International Cement Review

An overview of global cement sector trends Insights from the Global Cement Report 1 th Edition XXX Technical Congress FICEM-APCAC 2 September, 213 Lima, Peru Thomas Armstrong International Cement Review

Middle East Refining Technology Conference (MERTC) January 2017

January 2017") _ Middle East Refining Technology Conference (MERTC) 23-24 January 2017 Ladies & Gentlemen, KNPC Projects, Current Priorities and Growth Plans Good Morning It is indeed a great pleasure to participate

_ Middle East Refining Technology Conference (MERTC) 23-24 January 2017 Ladies & Gentlemen, KNPC Projects, Current Priorities and Growth Plans Good Morning It is indeed a great pleasure to participate

Davy Global Transportation & Logistics Conference

Davy Global Transportation & Logistics Conference John Manners-Bell FCILT CEO, Transport Intelligence 27 th June 2012, London 1. About Ti Established in 2002 to fill a gap in the market for high quality,

Davy Global Transportation & Logistics Conference John Manners-Bell FCILT CEO, Transport Intelligence 27 th June 2012, London 1. About Ti Established in 2002 to fill a gap in the market for high quality,

Dana Gas Presentation to ADX Brokers. 26 June

Dana Gas Presentation to ADX Brokers 26 June 2013 www.danagas.com 1 Disclaimer This presentation contains forward-looking statements which may be identified by their use of words like plans, expects, will,

Dana Gas Presentation to ADX Brokers 26 June 2013 www.danagas.com 1 Disclaimer This presentation contains forward-looking statements which may be identified by their use of words like plans, expects, will,

Global Scan of World Energy Trends

Global Scan of World Energy Trends Why Conduct a Global Scan? Importance of questioning, understanding our assumptions for energy outlooks implications for energy security First rule of scenario analysis,

Global Scan of World Energy Trends Why Conduct a Global Scan? Importance of questioning, understanding our assumptions for energy outlooks implications for energy security First rule of scenario analysis,

ENERGY TOMORROW: Canada in the World s Energy Future. Presented by Jeff Gaulin Queen s Global Energy Conference

ENERGY TOMORROW: Canada in the World s Energy Future Presented by Jeff Gaulin Queen s Global Energy Conference January 27, 2018 Good evening everyone. Thank you for that kind introduction. Thanks to Queen

ENERGY TOMORROW: Canada in the World s Energy Future Presented by Jeff Gaulin Queen s Global Energy Conference January 27, 2018 Good evening everyone. Thank you for that kind introduction. Thanks to Queen

Chevron Corporation (CVX) Analyst: Ryan Henderson Spring 2015

Analyst: Ryan Henderson Spring 2015") Recommendation: HOLD Target Price until (12/31/2016): $118.00 1. Reasons for Recommendation The driving factor behind my hold recommendation for Chevron is due to the state of the oil production industry

Recommendation: HOLD Target Price until (12/31/2016): $118.00 1. Reasons for Recommendation The driving factor behind my hold recommendation for Chevron is due to the state of the oil production industry

Professor Wumi Iledare, Ph.D. Senior Fellow, U.S. Association for Energy Economics Associate Editor, SPE Economics & Management Journal Professor,

Global Petroleum Supply and Pricing: Is the World Really Running Out of Oil? Professor Wumi Iledare, Ph.D. Senior Fellow, U.S. Association for Energy Economics Associate Editor, SPE Economics & Management

Global Petroleum Supply and Pricing: Is the World Really Running Out of Oil? Professor Wumi Iledare, Ph.D. Senior Fellow, U.S. Association for Energy Economics Associate Editor, SPE Economics & Management

VISION IAS. Slide in Oil Prices

VISION IAS www.visionias.in Slide in Oil Prices 1. Introduction One of the most unexpected stories since the start of 2015 has been the continuous decline in worldwide oil prices. In June 2014, oil prices

VISION IAS www.visionias.in Slide in Oil Prices 1. Introduction One of the most unexpected stories since the start of 2015 has been the continuous decline in worldwide oil prices. In June 2014, oil prices

CHAPTER III DISCUSSION

CHAPTER III DISCUSSION 3.1 Overview of PT. Pertamina 3.1.1 Background of PT. Pertamina PT.Pertamina (Persero) is a biggest state-owned oil, gas and renewable energy company in Indonesia that established

CHAPTER III DISCUSSION 3.1 Overview of PT. Pertamina 3.1.1 Background of PT. Pertamina PT.Pertamina (Persero) is a biggest state-owned oil, gas and renewable energy company in Indonesia that established

Grade 7 Practice Test for State Geography CRT 2007

Grade 7 Practice Test for State Geography CRT 2007 PASS 1.2 Sample Test Items: Depth of Knowledge: 2 Correct Answer: C Compared to the rest of Australia, the climate of Tasmania is A warmer. B drier. C

Grade 7 Practice Test for State Geography CRT 2007 PASS 1.2 Sample Test Items: Depth of Knowledge: 2 Correct Answer: C Compared to the rest of Australia, the climate of Tasmania is A warmer. B drier. C

American Strategy and US Energy Independence

Cordesman: Strategy and Energy Independence 10/21/13 1 American Strategy and US Energy Independence By Anthony H. Cordesman October 21, 2013 Changes in energy technology, and in the way oil and gas reserves

Cordesman: Strategy and Energy Independence 10/21/13 1 American Strategy and US Energy Independence By Anthony H. Cordesman October 21, 2013 Changes in energy technology, and in the way oil and gas reserves

The Oil Market Context 2006 Out of Step with Past and Future David Knapp Energy Intelligence Group

The Oil Market Context 2006 Out of Step with Past and Future David Knapp Energy Intelligence Group Presentation to Houston Chapter International Association for Energy Economics Houston, Texas - Mar. 9,

The Oil Market Context 2006 Out of Step with Past and Future David Knapp Energy Intelligence Group Presentation to Houston Chapter International Association for Energy Economics Houston, Texas - Mar. 9,

Are There Limits to Green Growth?

Are There Limits to Green Growth? Edward B. Barbier Key Points Introduction 1 1 http://www.greengrowthknowledge.org/ Green stimulus during the Great Recession 2 3 3 Table 1: Green stimulus during the Great

Are There Limits to Green Growth? Edward B. Barbier Key Points Introduction 1 1 http://www.greengrowthknowledge.org/ Green stimulus during the Great Recession 2 3 3 Table 1: Green stimulus during the Great

Unit 4. The secondary sector 1. The secondary sector - Industry is the activity that transforms raw materials into manufactured products.

Unit 4. The secondary sector 1. The secondary sector - Industry is the activity that transforms raw materials into manufactured products. Industry requires raw materials, energy sources (provide the force)

Unit 4. The secondary sector 1. The secondary sector - Industry is the activity that transforms raw materials into manufactured products. Industry requires raw materials, energy sources (provide the force)

Welcome to the Revolution: Why Shale Is the Next Shale

1 of 5 7/24/2014 7:52 PM Back to previous page document 1 of 1 Welcome to the Revolution: Why Shale Is the Next Shale Morse, Edward L. Foreign Affairs 93.3 (May/Jun 2014): 3-7. Find a copy http://sfxhosted.exlibrisgroup.com/nps?url_ver=z39.88-2004&rft_val_fmt=info:ofi/fmt:kev:mtx:journal&

1 of 5 7/24/2014 7:52 PM Back to previous page document 1 of 1 Welcome to the Revolution: Why Shale Is the Next Shale Morse, Edward L. Foreign Affairs 93.3 (May/Jun 2014): 3-7. Find a copy http://sfxhosted.exlibrisgroup.com/nps?url_ver=z39.88-2004&rft_val_fmt=info:ofi/fmt:kev:mtx:journal&

LNG TRADE FLOWS. Hans Stinis Shell Upstream International

LNG TRADE FLOWS Hans Stinis Shell Upstream International ABSTRACT The LNG industry has witnessed a great deal of change recently, and indications are that this will only continue. Global gas demand is

LNG TRADE FLOWS Hans Stinis Shell Upstream International ABSTRACT The LNG industry has witnessed a great deal of change recently, and indications are that this will only continue. Global gas demand is

BP Energy Outlook 2017 edition

BP Energy Outlook 2017 edition Bob Dudley Group chief executive bp.com/energyoutlook #BPstats BP Energy Outlook 2017 edition Spencer Dale Group chief economist bp.com/energyoutlook #BPstats Economic backdrop

BP Energy Outlook 2017 edition Bob Dudley Group chief executive bp.com/energyoutlook #BPstats BP Energy Outlook 2017 edition Spencer Dale Group chief economist bp.com/energyoutlook #BPstats Economic backdrop

Twilight of Big Energy

Volume XXXIV, No. 7 July 2017 Twilight of Big Energy HHI for Global Crude Oil Exports: History and Possible Future under Middle Eastern Dominant Control HHI 3,500 3,000 2,500 HHI possible if low-cost Middle

Volume XXXIV, No. 7 July 2017 Twilight of Big Energy HHI for Global Crude Oil Exports: History and Possible Future under Middle Eastern Dominant Control HHI 3,500 3,000 2,500 HHI possible if low-cost Middle

Geopolitical Implications of Shale Gas

Geopolitical Implications of Shale Gas Amy Myers Jaffe Dr. Kenneth Medlock February 8, 202 James A Baker III Institute for Public Policy Rice University From Tunisia to Egypt and beyond, Tail Risk Issues

Geopolitical Implications of Shale Gas Amy Myers Jaffe Dr. Kenneth Medlock February 8, 202 James A Baker III Institute for Public Policy Rice University From Tunisia to Egypt and beyond, Tail Risk Issues

Canadian Oil and Gas Industry: What lies ahead

Canadian Oil and Gas Industry: What lies ahead Presented by Dinara Millington Vice President, Research Canadian Energy Research Institute June 10, 2015 1 Canadian Energy Research Institute Overview Founded

Canadian Oil and Gas Industry: What lies ahead Presented by Dinara Millington Vice President, Research Canadian Energy Research Institute June 10, 2015 1 Canadian Energy Research Institute Overview Founded

The sheep and sheep meat trade market. Second EU Sheep Meat Forum Brussels, February 25, 2016

The sheep and sheep meat trade market Second EU Sheep Meat Forum Brussels, February 25, 2016 Partnering your agribusiness development Market research 45 years Focused on agribusiness Worldwide coverage

The sheep and sheep meat trade market Second EU Sheep Meat Forum Brussels, February 25, 2016 Partnering your agribusiness development Market research 45 years Focused on agribusiness Worldwide coverage

Integrating Renewable Fuel Heating Systems

Integrating Renewable Fuel Heating Systems An Overview of Wood Heating Systems Better Buildings by Design 2009 February 12th, 2009 Adam Sherman, Program Manager Biomass Energy Resource Center Biomass Energy

Integrating Renewable Fuel Heating Systems An Overview of Wood Heating Systems Better Buildings by Design 2009 February 12th, 2009 Adam Sherman, Program Manager Biomass Energy Resource Center Biomass Energy

Pyramid Research. Publisher Sample

Pyramid Research http://www.marketresearch.com/pyamidresearch-v4002/ Publisher Sample Phone: 800.298.5699 (US) or +1.240.747.3093 or +1.240.747.3093 (Int'l) Hours: Monday - Thursday: 5:30am - 6:30pm EST

Pyramid Research http://www.marketresearch.com/pyamidresearch-v4002/ Publisher Sample Phone: 800.298.5699 (US) or +1.240.747.3093 or +1.240.747.3093 (Int'l) Hours: Monday - Thursday: 5:30am - 6:30pm EST

OPEC World Oil Outlook edition

Organization of the Petroleum Exporting Countries OPEC World Oil Outlook 2040 2017 edition Presented at presented at Riyadh, 15 November 2017 WOO2017 1 Disclaimer The data, analysis and any other information

Organization of the Petroleum Exporting Countries OPEC World Oil Outlook 2040 2017 edition Presented at presented at Riyadh, 15 November 2017 WOO2017 1 Disclaimer The data, analysis and any other information

Summary - The Challenge to European Refining Posed by the Rise of US Unconventionals Scottish Oil Club

Summary - The Challenge to European Refining Posed by the Rise of US Unconventionals Scottish Oil Club November 2014 About us We are a global leader in commercial intelligence for the energy, metals and

Summary - The Challenge to European Refining Posed by the Rise of US Unconventionals Scottish Oil Club November 2014 About us We are a global leader in commercial intelligence for the energy, metals and

Iran Energy Database. Address: 1629 K St NW, Suite 300, Washington, DC Tel: Fax:

Iran Energy Database Email: info@svbenergy.com Address: 1629 K St NW, Suite 300, Washington, DC 20006 Tel: +1 202 600 7831 Fax: +1 202 331 3759 About US SVB Energy International LLC (SVBEI) is a Washington

Iran Energy Database Email: info@svbenergy.com Address: 1629 K St NW, Suite 300, Washington, DC 20006 Tel: +1 202 600 7831 Fax: +1 202 331 3759 About US SVB Energy International LLC (SVBEI) is a Washington

Short-Term Energy Outlook (STEO)

") May 2013 Short-Term Energy Outlook (STEO) Highlights Falling crude oil prices contributed to a decline in the U.S. regular gasoline retail price from a year to date high of $3.78 per gallon on February

May 2013 Short-Term Energy Outlook (STEO) Highlights Falling crude oil prices contributed to a decline in the U.S. regular gasoline retail price from a year to date high of $3.78 per gallon on February

Progressing CBM Development in Indonesia - An Industry Perspective -

Progressing CBM Development in Indonesia - An Industry Perspective - Mohd. Radzif Mohamad VICO CBM Commercial Manager IndoGAS Conference 27 th 29 th January 2015 1 VICO Overview VICO is a 50:50 JV between

Progressing CBM Development in Indonesia - An Industry Perspective - Mohd. Radzif Mohamad VICO CBM Commercial Manager IndoGAS Conference 27 th 29 th January 2015 1 VICO Overview VICO is a 50:50 JV between

LNG supply chain analysis and optimisation of Turkey's natural gas need with LNG import

World Maritime University The Maritime Commons: Digital Repository of the World Maritime University World Maritime University Dissertations Dissertations 2011 LNG supply chain analysis and optimisation

World Maritime University The Maritime Commons: Digital Repository of the World Maritime University World Maritime University Dissertations Dissertations 2011 LNG supply chain analysis and optimisation

Anadarko LNG and China

Anadarko LNG and China Scott Moore Vice President Worldwide Marketing US-China Oil and Gas Industry Forum September 26, 2014 Regarding Forward-Looking Statements and Other Matters This presentation contains

Anadarko LNG and China Scott Moore Vice President Worldwide Marketing US-China Oil and Gas Industry Forum September 26, 2014 Regarding Forward-Looking Statements and Other Matters This presentation contains

RYSTAD ENERGY GAS PERSPECTIVES. Jakarta, November 20 th 2017

RYSTAD ENERGY GAS PERSPECTIVES Jakarta, November 2 th 217 Agenda 1. Global LNG market outlook Oversupply and new Asian demand 2. Japan LNG Market outlook LNG demand in a nuclear restart 2 Longer distances

RYSTAD ENERGY GAS PERSPECTIVES Jakarta, November 2 th 217 Agenda 1. Global LNG market outlook Oversupply and new Asian demand 2. Japan LNG Market outlook LNG demand in a nuclear restart 2 Longer distances

Brunei s Energy Future: a Global Perspective Yves Grosjean General Manager Total E&P Borneo

Brunei s Energy Future: a Global Perspective Yves Grosjean General Manager Total E&P Borneo National Environment Conference, 01 July 2010, The Empire Hotel and Country Club DISCLAIMER and COPYRIGHT RESERVATION

Brunei s Energy Future: a Global Perspective Yves Grosjean General Manager Total E&P Borneo National Environment Conference, 01 July 2010, The Empire Hotel and Country Club DISCLAIMER and COPYRIGHT RESERVATION

James F. Van Ness. Domestic vs. International Projects Unique Challenges and Best Practices. Project Director - SERP Syncrude Canada Limited

Domestic vs. International Projects Unique Challenges and Best Practices Panel Participant James F. Van Ness Project Director - SERP Syncrude Canada Limited Jim Van Ness Project Director for Syncrude s

Domestic vs. International Projects Unique Challenges and Best Practices Panel Participant James F. Van Ness Project Director - SERP Syncrude Canada Limited Jim Van Ness Project Director for Syncrude s

Global CAM Software Detailed Analysis Report

Report Information More information from: https://www.reportsandmarkets.com/reports/1530934 Global CAM Software Detailed Analysis Report 2018-2023 Report / Search Code: RnM1530934 Publish Date: 7 February,

Report Information More information from: https://www.reportsandmarkets.com/reports/1530934 Global CAM Software Detailed Analysis Report 2018-2023 Report / Search Code: RnM1530934 Publish Date: 7 February,

World Economic Dynamics (WED) Model: Oil consumption modeling and forecasting

Model: Oil consumption modeling and forecasting") World Economic Dynamics (WED) Model: Oil consumption modeling and forecasting Inforum World Conference Alexandria, USA Tatiana Fokina, Rosneft 02.09.2014 WED Content Economics modeling and forecasting

World Economic Dynamics (WED) Model: Oil consumption modeling and forecasting Inforum World Conference Alexandria, USA Tatiana Fokina, Rosneft 02.09.2014 WED Content Economics modeling and forecasting

Fossil Fuels: Natural Gas. Outline: Formation Global supply and Distribution NGCC Carbon management Biological Artificial

Fossil Fuels: Natural Gas Outline: Formation Global supply and Distribution NGCC Carbon management Biological Artificial Formation of Natural Gas Migration Phases separate according to density, with the

Fossil Fuels: Natural Gas Outline: Formation Global supply and Distribution NGCC Carbon management Biological Artificial Formation of Natural Gas Migration Phases separate according to density, with the

A Regional Oil Extraction and Consumption Model. Part II: Predicting the declines in regional oil consumption

A Regional Oil Extraction and Consumption Model. Part II: Predicting the declines in regional oil consumption Michael Dittmar, Institute of Particle Physics, ETH, 8093 Zurich, Switzerland arxiv:1708.03150v1

A Regional Oil Extraction and Consumption Model. Part II: Predicting the declines in regional oil consumption Michael Dittmar, Institute of Particle Physics, ETH, 8093 Zurich, Switzerland arxiv:1708.03150v1

Gas perspectives. Houston/Paris, 3-4 December Ministère de l'écologie, du Développement durable et de l Énergie

Gas perspectives Houston/Paris, 3-4 December 2014 Ministère de l'écologie, du Développement durable et de l Énergie www.developpement-durable.gouv.fr Historic perspective Security of supply and gas Storage

Gas perspectives Houston/Paris, 3-4 December 2014 Ministère de l'écologie, du Développement durable et de l Énergie www.developpement-durable.gouv.fr Historic perspective Security of supply and gas Storage

The Geopolitics and Geoeconomics of Global Energy, Spring 2007 Prof. Flynt Leverett Lecture 9: Resource mercantilism China, India, and Japan

17.906 The Geopolitics and Geoeconomics of Global Energy, Spring 2007 Prof. Flynt Leverett Lecture 9: Resource mercantilism China, India, and Japan Resource mercantilism is not Not demand side management-

17.906 The Geopolitics and Geoeconomics of Global Energy, Spring 2007 Prof. Flynt Leverett Lecture 9: Resource mercantilism China, India, and Japan Resource mercantilism is not Not demand side management-

Energy where are we heading?

Energy where are we heading? Morningstar Investment Conference Nordic Oslo, Oct. 9, 2013 Øystein Noreng Professor Emeritus BI Norwegian Business School The Setting the World Economy Imbalances slow growth

Energy where are we heading? Morningstar Investment Conference Nordic Oslo, Oct. 9, 2013 Øystein Noreng Professor Emeritus BI Norwegian Business School The Setting the World Economy Imbalances slow growth