VO Kernenergie und Umwelt TU Graz. Eileen Langegger,

|

|

|

- Beverly Burns

- 5 years ago

- Views:

Transcription

1 VO Kernenergie und Umwelt TU Graz Eileen Langegger,

2 Biblis A Biblis B Brokdorf Brunsbüttel Emsland, Lingen Grafenrheinfeld Grohnde Gundremmingen B Gundremmingen C Isar I, Essenbach Isar II Krümmel, Geesthacht Neckarwestheim I Neckarwestheim II Philippsburg I Philippsburg II Unterweser, Esensham Module 12 Europe six years after Fukushima

3 Situation in Europa after Fukushima Fukushima was a major nuclear accident (INES 7) No persons were killed due to overexposure No delayed radiation effects expected Large media coverage especially in German speaking countries The accident had a big international impact on nuclear power safety The role of the IAEA was rather disappointing In Europe only Germany, Switzerland and Italy reconsidered their nuclear power program

4 Europe after Fukushima Red: Phase out of NPP s Green: Continue with NPP s Yellow: No major changes

5 Updated State of NPPs Worldwide NPP in operation : 451 in 31 countries Net power: 395 GWe Net energy production: 2628 TWh NPP under construction: 58 NPPs with total capacity of 60 GWe net in 17 countries (such as Argentina (1), Belarus (2), Brasil (1), China (16), Finland (1), France (1), India (7), Japan (2), Korea (4), Pakistan (2), Russia (6), Slovakia (2), Taiwan (2), USA (2), UAE (4)) NPP under planning worldwide: 125 units in various planning stages in 25 countries such as China (>30), Russia (>30), India (>6), Turkey (5)

6 Belgium 7 nuclear power plants in operation licensed up to units in Doel, 3 units in Tihange Pressurized Water type (PWR) first unit operational since 1974 total capacity 5900 MWe 58% of the population favours nuclear energy NPP s cover 55% of the electricity needs of Belgium 45% mostly gas-fired and some coal plants Phase out decision after Fukushima by 2025, this decision might be reversed depending on the energy situation

7 Bulgaria During EU accession negotiations Bulgaria committed to close Kozloduy 1 & 2 by the end of 2002 and units 3 & 4 by the end of All four units are VVER-440/230 reactors (1st generation) Two VVER 1000/320 at Kozloduy continue to operate producing 1/3 of the country s electricity needs Plans for two VVER 1000/320 at Belene officially started in September 2008, however after several years of negotiations with Rosatom the two projects were cancelled Another Westinghouse AP-1200 is now under discussion at the same site The main problem is finding investors for this project China & Russia will invest No major influence from Fukushima on future nuclear plans

8 Czech Republic Czech Republic operates four VVER 440/213 at the Dukovany site and two VVER 1000/320 at the Temelin site producing appr. 1/3 of the country s electricity needs Dukovany 1-4 has been upgraded to 500 MWe each and Temelin 1 & 2 to 1050 MWe by Skoda by replacing the high pressure turbines and refurbishing the generators In July 2008 Czech Republic announced a plan to build two more reactors at Temelin totalling up to 3400 MWe and two units at the Dukovany site to be operational between 2035 to Three nuclear vendors have qualified to submit formal offers for the construction of units 3 and 4 at Temelin (NUCNET 197/ /2011) Westinghouse with its AP1000, Korea Electric Power Company KEPCO, and a consortium comprising of Skoda, Atomstroyexport and Gidropress with the MIR (Modernised International) (->NucNet Insider / No. 15 / 16th July 2015) Dukovany extension will start in 2035, several bids received

9 CEZ conditions for NPP tender PWR type 3+ generation existing NPP sites will be used output MWe turn key delivery compliance with the Czech legislation and IAEA, EUR (European Utility Requirements), WENRA conditions (Western European Nuclear Regulators Association) design of NPP is licensed in country of origin high participation of the Czech industry final decision of tender postponed NPP operation 2035 (NucNet Insider / No. 15 / 16th July 2015) No major influence from Fukushima on future nuclear plans, 2 NPP s at the Temelin site and 1 NPP at the Dukovany site under planning

10 Finlands nuclear program

11 Olkiluoto 3 scheduled to become operational by end of 2018 Parliament ratified on July 1, 2010 the Decisions-in-Principle (DiP), regarding Olkiluoto 4 by TVO and Fennovoima for one unit at the Hanhikvi site north of Olkiluoto Construction at Hanhikvi will start in 2018 with a Russian AES 2006 DiP was also approved for Olkiluoto 4 Finland New NPP projects DiP also approved for expanding the capacity of the spent fuel repository to be constructed in Olkiluoto. No influence from Fukushima on future nuclear plans, moreover 2 new NPP in concrete planning stage

EPR start of construction: 2017 commissioning:? politics?")

12 Cost developments Autumn 2017 Paks (Hungary) Olkiluoto (Finland) Flamanville (France) Hinkley Point (UK) 2 x WWER1200 start of construction:? 1 x EPR (derzeit) start of construction: 2005 comissioning: 2018 (planned) EPR start of construction: 2007 commissioning: 2018 (planned) EPR start of construction: 2017 commissioning:? politics? costs/construction time? costs/construction time? costs? planning and construction costs per MW reactor capacity (inflation-adjusted): : 1.07 million /MW (Fessenheim) : 1.37 million /MW (Chooz 1 and 2) : 3.70 million /MW (Flamanville expected) source: general accounting office (France, 2012)

13 French nuclear program

14

15 France France invests 1 billion for nuclear R&D especially for Gen IV NPP (Sarkozy ) France continues to rely on safe, independent and economic electricity supply based on NPP Further 1.3 billion will be invested in the development of regenerative energy sources (ATW July, 435) No major influence from Fukushima on future nuclear plans

16 installed power mean power lowest guaranteed wind power (March 2011)

17 Germany In June 2000 a compromise was announced which saved face for the government and secured the uninterrupted operation of the nuclear plants for many years ahead. The agreement, while limiting plant lifetime to some degree, averted the risk of any enforced plant closures during the term of the present government. The agreement put a cap of 2623 billion kwh on lifetime production by all 19 operating reactors, equivalent to an average lifetime of 32 years (less than the 35 years sought by industry). After Fukushima a political discussion started resulting in an immediate shut down of 9 older NPP s by end of 2015, further the government decided on May 29th to phase out all NPP s until 2022 German politicians state that there are enough other sources such hydro, wind, solar and biomass

18 Annual Nuclear Power Generation International Top Ten Bold: world record ,97 TWh ,04 TWh ,86 TWh ,34 TWh Grand Gulf 1 Philippsburg 2 Brokdorf Neckarwestheim 2 Isar 2 Source: DAtF, atw

19 Germany s Political System and the Nuclear Phase-out Regulatory and Political System Germany is a federal state, regarding nuclear issues, the regulator is on the federal level (Federal Ministry for the Environment, Nature Conservation, Building and Nuclear Safety) States are in charge of supervising and licensing the nuclear facilities in their respective area of responsibility on behalf of the federal regulator ( federal executive administration ) including matters of decommissioning and waste management Political Parties in the German Bundestag (National Parliament): Left (in parliament since 1990) Greens (in parliament since 1983) Social Democrats Christian Democrats Large Coalition under Angela Merkel socialistic conservative/ market oriented Courtesy of DAtF, 2016

20 Way to German Phase-out (1) 1961 First electricity generation from experimental reactor in Kahl 1973 Triggered among other things by the first oil crisis, Social Democrats launched a huge programme for nuclear power plants in Germany 1980 Foundation of the Green Party mainly out of anti-nuclear movement during government of Social Democrats and Free Democrats 1987 Social Democrats changed their programme to anti-nuclear after the Chernobyl accident and several years of alienation from nuclear power 1990 In the course of German reunification, all 6 reactors of German Democratic Republic were shut down and decommissioning was started Courtesy of DAtF, 2016

21 Way to German Phase-out (2) 1998 First Federal Government involving the Greens (in coalition with Social Democrats) decided on first phase-out (in 2000/2002 life time restriction to 32 years) as a consequence 17 plants to be shut down stepwise until 2020/2022 Liberalization of German Energy Market 2010 Government of Christian Democrats and Free Democrats enacted life time extension of plants either for 8 or 14 years for the first time the atomic law separates between older and newer plants. Until then plants just had to be safe, irrespective of their age. Support of public opinion for life-time extension back to near 50 % (in 2009). Courtesy of DAtF, 2016

22 Way to German Phase-out (3) 2011 Despite a national and (later) a European stress test after the Fukushima accident proving the outstanding safety levels of German NPPs, Christian Democrats and Free Democrats together with opposition in the German Bundestag and the states decided upon a second, accelerated phase-out: Immediately after the accident the older plants (7+1) are temporarily shut down and remain so for good Remaining 9 plants to be shut-down stepwise till 2022 Today All relevant political parties act anti-nuclear, as well as about 2/3 of German population Courtesy of DAtF, 2016

23 Schedule for Shutdown of NPPs in Germany Today * Quelle: Volker Noak, RWE and (*)

24 German nuclear program

25 Gross Electricity Generation in Germany 2015 Source: BDEW, Status

26 Searching for a Final Repository Site General criteria Area at least 9 km² Earthquake zone < 1 No volcanism Groundwater permeability < m/s No data or awareness which raise doubts about the safety ( What should that mean?) Source: Courtesy of DAtF, 2016

27 Germany Shut down procedure 8 (+1 in stand by) of the oldest reactors shut-down immediately after Fukushima will not go back in operation One of them shall be kept as cold back-up reserve until elder reactors shall be shut-down in of the newest reactors to be shut down in 2022 (Isar 2, Emsland, Neckarwestheim 2) In the year 2018, a commission shall verify if the 3 newest reactors will still be needed in 2022 or can also be shut down in 2021 Existing fossil back-up power plants shall replace the nuclear reactors No nuclear produced electricity shall be imported! (Whatever this means?) A monitoring commission shall constantly watch the development of the renewable replacement energy and report to the government on a yearly basis. Major influence from Fukushima on future nuclear plans

28 Germany before and after (ATW July p.448)

29 Germany after Fukushima

30 Effects Energy scenarios 2011 Prognois AG Higher electricity costs influence overall industry prices negativ Importe replace national production, unemployment negativ? More fossil plants, more imports negativ Costs for CO 2 certificates negativ? Investments of electricity companies positiv About 3800 km of new north-south tansmission lines are necessary by 2020 with investment of 28 billion Termination on nuclear research of HTR and LMFBR => => Willy Marth : Energiewende und Atomausstieg, 2015 ISBN

31 German electricity generating costs

32 Hungary Present 4 NPP s uprated from 440 MW to 500 MW Without open tender Hungary signed a contract with Rosatom for two 1200 MWe, the EC announced an investigation on this deal With the need to build about 6000 MWe of new generating capacity by 2030, four new nuclear plants are under consideration. Construction of the first 1200 MWe units at the Paks site will start in 2018 to be operating at 2023, the second about 2025 In 2014 Hungary signed a contract with Rosatom for two 1200 MWe 80% (or 10 billion) being financed by Russia No major influence from Fukushima on future nuclear plans

33 Italy Italy shut down four operating nuclear power reactors between 1987 and 1990 following the Chernobyl accident (Capacity 1423 MWe) However 10% of its electricity is imported nuclear power from France and Switzerland After Fukushima Italy reversed all plans for to built new NPP s On June 13, 2011 Italian population voted 94,05% vs 5,95% against nuclear power (ATW July 436) In 2005 ENEL invested in Electricité de France In 2004 ENEL bought 66% of Slovenske Electrarne (SE) with its four VVER 440/213 Bohunice and Mochovce reactors in ENEL's subsequent investment plan aimed for the completion of Mochovce units 3 & MWe gross - by being delayed to 2017/2018 In 2015 this share was resold to SE Major influence from Fukushima on future nuclear plans

34 Netherlands Nuclear energy is seen as an important cornerstone in an affordable, low carbon energy mix. The government encourages the market to build nuclear power plants, of course within crisp and clear requirements for safety, management and disposal of radioactive waste. This vision is in line with the approach in the UK, France, Sweden and Finland. The phase-out of nuclear in Germany can give impetus to more capacity in the Netherlands. In September 2008 Delta (50% owner of Borssele) announced plans to build a second unit at Borssele, of MWe. In June 2009 it embarked upon seeking preliminary approvals.

35 Netherlands In 2009 German utility RWE agreed to buy shares for EUR 8.35 billion and announced to build new nuclear capacity in Netherlands. Delta, one of the owners of the Borssele nuclear power plant, started the licensing procedure for a new built NPP of 1600 MWe at the Borssele site. The new government is positive about nuclear energy for near and the long term. Plans have been established to build one or two AP-1000 but presently this project is on hold. No major influence from Fukushima on future nuclear plans

36 Poland Poland's largest power group announced in January 2009 plans to build two nuclear power plants by 2020, with a total capacity of 3000 MWe. First site will be at Zarnowiec about 40 km north of Gdanks, two more sites under consideration In November 2015 five companies had expressed interest in bidding: GE Hitachi, Kepco, SNC-Lavalin,Westinghouse and EdF/Areva. The tender qualification phase has been delayed, selection of an investor scheduled until No major influence from Fukushima on future nuclear plans

37 Baltic States In July 2008 the Lithuanian government decided together with several energy companies from Latvia, Estonia and Poland two new MWe nuclear power plant. In May 2011 competitive proposals from potential strategic investors were received, from Westinghouse and Hitachi GE. In July the government selected Hitachi as strategic investor. Lithuania's partners in the project, Estonia, Latvia and Poland participated in the evaluation to determine which of the two proposals was most economically advantageous. GE Hitachi plans to build a single 1350 MWe Advanced Boiling Water Reactor, several of which are operating and under construction in Japan and Taiwan. That NPP was expected to operate from The cost of the project was estimated at 4.92 billion. No major influence from Fukushima on future nuclear plans, but delays due to political problems between the Baltic States, Poland and Russia

38 Russia-Kaliningrad (Baltic Enclave) Russia* is building two nuclear plants in the Neman district of the Kaliningrad exclave, close to the border with Lithuania. This project consisted orignially of twovver-1200 units. Full construction of unit 1 began early in 2012 but was stopped in 2013; the current state of the project is unclear. Russia invited Lithuania to participate in the project but the invitation was declined. One NPP would supply the private sector and industry in KG The second NPP should export electricy to the Baltic States, Belarus as well as to Poland *Rosatom presently is involved in 10 national and 21 international projects: 4 NPPs in India, 4 NPP s in Turkey, 2 NPP s in Bulgaria,2 NPP s in Ukraina 1 NPP in Armenia, 2 NPP s in Bjelorussia, 2 NPP s in Vietnam, 2 NPP s in China, 2 NPP s in Bangladesh (ATW11/2011 p.626) No major influence from Fukushima on future nuclear plans

39 Romania Romania operates two CANDU reactors (units 1&2) with a total capacity of 1310 MWe. In July 2014 the China General Nuclear Power Group (CNPEC) signed a "binding and exclusive" cooperation agreement with CANDU Energy Inc for the construction of two more reactors (unit 3&4) at Cernavoda. In November 2015 the two companies signed a further agreement for the development, construction, operation and decommissioning of Cernavoda 3&4. The largely-new reactors will be updated versions of the CANDU 6, but not the full EC6 version, since the concrete structures are already built. They will have an operating life of 30 years with the possibility of 25-year extension. Plans exist for up to 4 more NPP in the next decade at other sites. No major influence from Fukushima on future nuclear plans

40 Slovakia

41 Slovak Republic Slovakia has four nuclear reactors generating half of its electricity and two more under construction. Government commitment to the future of nuclear energy is strong. In October 2014 Mochovce unit 3 was 80% complete and unit 4 60%. In October 2016 SE said that first power from unit 3 was expected in summer 2018, with unit 4 a year later. Plans for Bohunice 5 (V3) announced in April 2008: a MWe, using Western technology to enable MOX use. Rosatom has been exploring the prospect of being both technology provider and investor building a 1200 MWe reactor from about No major influence from Fukushima on future nuclear plans

42 Slovenia Slovenia operates a 696 MWe Westinghouse NPP Krsko jointly owned by Croatia. Entering commercial operation in In 2001 its steam generators were replaced and the plant was uprated 6% then and 3% subsequently. Its operational life was designed to be 40 years, but a 20-year extension is being sought. A further Krsko unit is under consideration, of up to 1600 MWe. An application towards a second reactor at the Krsko nuclear power plant was submitted to the country's Ministry of Economy by GEN Energija in January It would be built from , with cost estimated at up to EUR 5 billion, and fully owned by Slovenia. Postponement for future nuclear plans due to Fukushima

43 Spain Spain operates 7 NPPs with a total capacity of 7000 MWe licensed presently to 2020 and 2024 Spain is notable for power plant uprates. It has a program to add 810 MWe (11%) to its nuclear capacity through upgrading its seven reactors by up to 13%. In 2011 the responsible minister said that nuclear plants are "essential for the supply of electricity in Spain" and that almost all nuclear power units "will be open, operating and even repowering" until 2021 or beyond. Presently no plans for new NPP s, but power uprates and life extension for existing NPP s

44 Sweden Sweden operates 9 NPPs with a total capacity of 8850 MWe Utilities expand nuclear capacity to replace the 1200 MWe lost in closure of Barsebäck 1 & 2. By the end of 2008, some 1050 MWe had been added to the nine surviving reactors. The total uprate for Ringhals plant over is about 400 MWe. The three Forsmark units were uprated for about 300 MWe. Oskarshamn 2 uprate from 613 to 840 MWe (38%) and extend its life to 60 years, but further operation is presently under negotiations. Oskarshamn 3 reactor, +250 MWe to 1450 MWe net as well as a plant's life extension to 60 years. No major influence from Fukushima on future nuclear plans, Sweden does presently not consider a nuclear phase-out

1165 MW e KKB-I Beznau (1969) 365 MW e")

373 MW e 1-2 new NPP could replace the old")

45 Nuclear Power in Switzerland 5 Nuclear Power Plants (3220 MWe) KKL Leibstadt (1984) 1165 MW e KKB-I Beznau (1969) 365 MW e KKB-II Beznau (1971) 365 MW e KKG Gösgen (1979) 970 MW e KKM Mühleberg (1971) 373 MW e 1-2 new NPP could replace the old reactors

46 Switzerland Work on projects for new NPPs stopped after Fukushima accident. Swiss Federal government proposed phase-out of nuclear for the long-term, keeping existing NPP running as long as safe operation is assured. 64% of the population considers that the country s five nuclear reactors were essential in meeting the electricity demand and reduce dependence on foreign energy sources. The Council of States (cantons) voted on the matter in September 2015, and agreed to avoid putting legal limits on the operating lives of reactors Open question also: What are the alternatives to replace 40 % nuclear electricity in CH, Imports, Gas, Renewables? Postponement for future nuclear plans due to Fukushima, November 2016 referendum with 55% pro-nuclear, 2017 phase out referendum

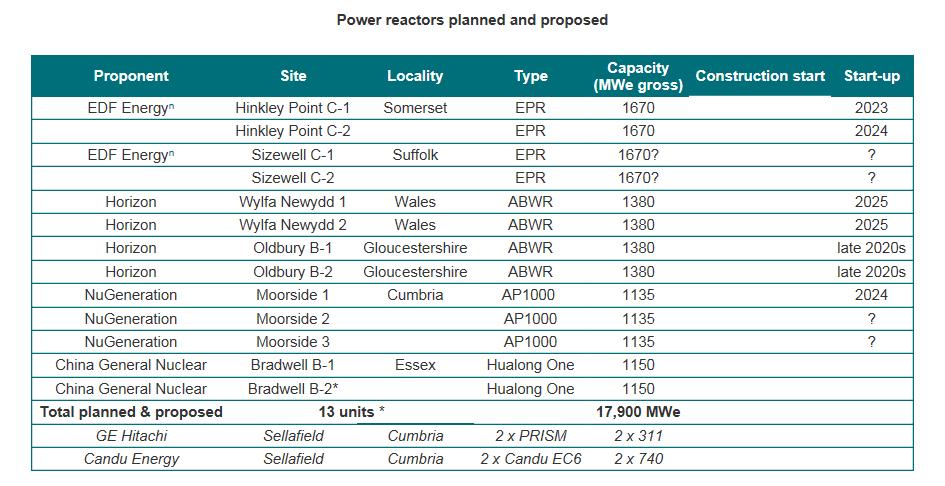

47 UK In 2008 announced that construction of new nuclear plants could start in mid Four of six NPPs could be in operation by First EPR site a Hinkley Point/Somerset, application on July 29, (NUCNET 177). On June 23, 2011 the national energy plan defines 8 NPP sites at Bradwell, Hartlepool, Heysham, Hinkley Point, Oldbury, Sellafield, Sizewell and Wylfa, all already existing sites of GCR NPP. The first new NPP will be located at Hinkley Point, followed by Wylfa and at the Oldbury site, at each site capacity of 3000 MWe planned. Westinghouse announced that six major European utilities were providing resources and sharing the costs of taking the AP-1000 reactor design through the pre-licensing process. In summary UK plans 12 NPP s on those 8 sites up to 2025 with investments of 100 Mrd.. (ATW July p.435) No major influence from Fukushima on future nuclear plans, 6 to 10 new NPP s planned.

48

49 Emerging Nuclear Countries Nuclear power is under serious consideration in over 45 countries which do not currently have it (in a few, consideration is not necessarily at government level). These range from sophisticated economies to developing nations. The front runners after Iran are UAE, Turkey, Vietnam, Belarus, Poland and possibly Jordan.

50 Emerging Nuclear Countries In Europe: Albania, Serbia, Croatia, Portugal, Norway, Poland, Belarus, Estonia, Latvia, Ireland,Turkey. In the Middle East and North Africa: Iran (reactor now operating), Gulf states including UAE, Saudi Arabia, Qatar & Kuwait, Yemen, Israel, Syria, Jordan, Egypt,Tunisia, Libya,Algeria, Morocco, Sudan. In West-, Central- and Southern Africa: Nigeria, Ghana, Senegal, Kenya, Uganda,Tanzania, Namibia. In Central and South America: Cuba, Chile, Ecuador, Venezuela, Bolivia, Peru, Paraguay. In central and southern Asia: Azerbaijan, Georgia, Kazakhstan, Mongolia, Bangladesh, Sri Lanka. In South East Asia: Indonesia, Philippines, Vietnam, Thailand, Laos, Cambodia, Malaysia, Singapore, Myanmar,Australia, New Zealand.

51 Conclusions Europe was in a renaissance situation before Fukushima, in several countries (i.e. Germany) this had a strong effect on the future energy policy. However in most of the NPP countries this accident had little impact on the long term energy plans except Germany, Italy and Switzerland. There may be delays due to the financial situation, lack of heavy industry, loss of knowledge and qualified nuclear experts. Hydro and nuclear are the only choice for base-load electricty in Europe, if the CO 2 targets are kept in mind, however all energy sources must be developed in parallel under the same legal, political, economic and environmental conditions.

52 References Updated country data from: country profiles

Module 17 Europe after Fukushima Status

Biblis A Biblis B Brokdorf Brunsbüttel Emsland, Lingen Grafenrheinfeld Grohnde Gundremmingen B Gundremmingen C Isar I, Essenbach Isar II Krümmel, Geesthacht Neckarwestheim I Neckarwestheim II Philippsburg

Biblis A Biblis B Brokdorf Brunsbüttel Emsland, Lingen Grafenrheinfeld Grohnde Gundremmingen B Gundremmingen C Isar I, Essenbach Isar II Krümmel, Geesthacht Neckarwestheim I Neckarwestheim II Philippsburg

Nuclear Power Development in Europe: Rosatom perspective

ROSATOM Nuclear Power Development in Europe: Rosatom perspective Alexey Kalinin Head, International Business, Rosatom CEO, Rusatom Overseas Platts 7 th Annual European Nuclear Conference June 25-26, 2012

ROSATOM Nuclear Power Development in Europe: Rosatom perspective Alexey Kalinin Head, International Business, Rosatom CEO, Rusatom Overseas Platts 7 th Annual European Nuclear Conference June 25-26, 2012

Prospects for a Global Nuclear Revival: Challenges and Risks. Prof. Wil Kohl Johns Hopkins SAIS October 2011

Prospects for a Global Nuclear Revival: Challenges and Risks Prof. Wil Kohl Johns Hopkins SAIS October 2011 Source: IAEA Source: IAEA NUCLEAR REVIVAL? Before Fukushima, the United States and a number

Prospects for a Global Nuclear Revival: Challenges and Risks Prof. Wil Kohl Johns Hopkins SAIS October 2011 Source: IAEA Source: IAEA NUCLEAR REVIVAL? Before Fukushima, the United States and a number

Rosatom Global Development, International Cooperation Perspective

ROSATOM STATE ATOMIC ENERGY CORPORATION ROSATOM Rosatom Global Development, International Cooperation Perspective Atomex-Europe 013 Forum Nikolay Drozdov Director, International Business State Corporation

ROSATOM STATE ATOMIC ENERGY CORPORATION ROSATOM Rosatom Global Development, International Cooperation Perspective Atomex-Europe 013 Forum Nikolay Drozdov Director, International Business State Corporation

FSC Facts & Figures. September 6, 2018

FSC Facts & Figures September 6, 2018 Global FSC-certified forest area North America 34.5% of total FSC-certified area ( 69,584,479 ha ) 253 certificates Europe 49.4% of total FSC-certified area ( 99,747,108

FSC Facts & Figures September 6, 2018 Global FSC-certified forest area North America 34.5% of total FSC-certified area ( 69,584,479 ha ) 253 certificates Europe 49.4% of total FSC-certified area ( 99,747,108

FSC Facts & Figures. August 1, 2018

FSC Facts & Figures August 1, 2018 Global FSC-certified forest area North America 34.6% of total FSC-certified area ( 69,481,877 ha ) 253 certificates Europe 49.4% of total FSC-certified area ( 99,104,573

FSC Facts & Figures August 1, 2018 Global FSC-certified forest area North America 34.6% of total FSC-certified area ( 69,481,877 ha ) 253 certificates Europe 49.4% of total FSC-certified area ( 99,104,573

Le eccellenze italiane nello scenario internazionale

Le eccellenze italiane nello scenario internazionale Giornata di studio AIN 2012 Roma, 10 maggio 2012 Enel/ATN The Enel Group Nuclear Assets Nuclear Policy ATN Area Tecnica Nucleare The Slovak Project

Le eccellenze italiane nello scenario internazionale Giornata di studio AIN 2012 Roma, 10 maggio 2012 Enel/ATN The Enel Group Nuclear Assets Nuclear Policy ATN Area Tecnica Nucleare The Slovak Project

Analysis of Load Factors at Nuclear Power Plants

Clemson University From the SelectedWorks of Michael T. Maloney June, 2003 Analysis of Load Factors at Nuclear Power Plants Michael T. Maloney, Clemson University Available at: https://works.bepress.com/michael_t_maloney/10/

Clemson University From the SelectedWorks of Michael T. Maloney June, 2003 Analysis of Load Factors at Nuclear Power Plants Michael T. Maloney, Clemson University Available at: https://works.bepress.com/michael_t_maloney/10/

FSC Facts & Figures. June 1, 2018

FSC Facts & Figures June 1, 2018 Global FSC-certified forest area North America 34.6% of total FSC-certified area ( 69,460,004 ha ) 242 certificates Europe 49.4% of total FSC-certified area ( 99,068,686

FSC Facts & Figures June 1, 2018 Global FSC-certified forest area North America 34.6% of total FSC-certified area ( 69,460,004 ha ) 242 certificates Europe 49.4% of total FSC-certified area ( 99,068,686

TRACTEBEL ENGINEERING

PUBLIC TRACTEBEL ENGINEERING M. AUGLAIRE March 17-18, 2015 CHOOSE EXPERTS, FIND PARTNERS 7th EMUG meeting 2015 2 PUBLIC TRACTEBEL ENGINEERING within Energy Europe Energy International Global Gas & LNG

PUBLIC TRACTEBEL ENGINEERING M. AUGLAIRE March 17-18, 2015 CHOOSE EXPERTS, FIND PARTNERS 7th EMUG meeting 2015 2 PUBLIC TRACTEBEL ENGINEERING within Energy Europe Energy International Global Gas & LNG

UNIVERSITY OF KANSAS Office of Institutional Research and Planning

10/13 TABLE 4-170 FALL - TOTAL 1,624 1,740 1,926 2,135 2,134 2,138 2,246 Male 927 968 1,076 1,191 1,188 1,179 1,262 Female 697 772 850 944 946 959 984 Undergraduate 685 791 974 1,181 1,189 1,217 1,281

10/13 TABLE 4-170 FALL - TOTAL 1,624 1,740 1,926 2,135 2,134 2,138 2,246 Male 927 968 1,076 1,191 1,188 1,179 1,262 Female 697 772 850 944 946 959 984 Undergraduate 685 791 974 1,181 1,189 1,217 1,281

FSC Facts & Figures. November 2, 2018

FSC Facts & Figures November 2, 2018 Global FSC-certified forest area North America 34.6% of total FSC-certified area ( 69,322,145 ha ) 256 certificates Europe 49.9% of total FSC-certified area ( 100,198,871

FSC Facts & Figures November 2, 2018 Global FSC-certified forest area North America 34.6% of total FSC-certified area ( 69,322,145 ha ) 256 certificates Europe 49.9% of total FSC-certified area ( 100,198,871

FSC Facts & Figures. December 3, 2018

FSC Facts & Figures December 3, 2018 Global FSC-certified forest area North America 34.5% of total FSC-certified area ( 69,285,190 ha ) 253 certificates Europe 50% of total FSC-certified area ( 100,482,414

FSC Facts & Figures December 3, 2018 Global FSC-certified forest area North America 34.5% of total FSC-certified area ( 69,285,190 ha ) 253 certificates Europe 50% of total FSC-certified area ( 100,482,414

FSC Facts & Figures. January 3, FSC F FSC A.C. All rights reserved

FSC Facts & Figures January 3, 2018 FSC F0001000 FSC A.C. All rights reserved Global FSC-certified forest area North America 34.7% of total FSC-certified area ( 69,082,443 ha ) 245 certificates Europe

FSC Facts & Figures January 3, 2018 FSC F0001000 FSC A.C. All rights reserved Global FSC-certified forest area North America 34.7% of total FSC-certified area ( 69,082,443 ha ) 245 certificates Europe

FSC Facts & Figures. February 9, FSC F FSC A.C. All rights reserved

FSC Facts & Figures February 9, 2018 FSC F0001000 FSC A.C. All rights reserved Global FSC-certified forest area North America 34.5% of total FSC-certified area ( 68,976,317 ha ) 243 certificates Europe

FSC Facts & Figures February 9, 2018 FSC F0001000 FSC A.C. All rights reserved Global FSC-certified forest area North America 34.5% of total FSC-certified area ( 68,976,317 ha ) 243 certificates Europe

FSC Facts & Figures. April 3, FSC F FSC A.C. All rights reserved

FSC Facts & Figures April 3, 2018 FSC F0001000 FSC A.C. All rights reserved Global FSC-certified forest area North America 34.7% of total FSC-certified area ( 69,167,742 ha ) 242 certificates Europe 49.3%

FSC Facts & Figures April 3, 2018 FSC F0001000 FSC A.C. All rights reserved Global FSC-certified forest area North America 34.7% of total FSC-certified area ( 69,167,742 ha ) 242 certificates Europe 49.3%

The future of nuclear energy in Central and Eastern Europe from ROSATOM perspective

ROSATOM STATE ATOMIC ENERGY CORPORATION ROSATOM Rusatom Overseas The future of nuclear energy in Central and Eastern Europe from ROSATOM perspective Ivo Kouklik Vice-president Rusatom Overseas Budapest.05.01

ROSATOM STATE ATOMIC ENERGY CORPORATION ROSATOM Rusatom Overseas The future of nuclear energy in Central and Eastern Europe from ROSATOM perspective Ivo Kouklik Vice-president Rusatom Overseas Budapest.05.01

FSC Facts & Figures. September 1, FSC F FSC A.C. All rights reserved

FSC Facts & Figures September 1, 2017 FSC F0001000 FSC A.C. All rights reserved Global FSC-certified forest area North America 34.9% of total FSC-certified area ( 69,014,953 ha ) 246 certificates Europe

FSC Facts & Figures September 1, 2017 FSC F0001000 FSC A.C. All rights reserved Global FSC-certified forest area North America 34.9% of total FSC-certified area ( 69,014,953 ha ) 246 certificates Europe

FSC Facts & Figures. October 4, FSC F FSC A.C. All rights reserved

FSC Facts & Figures October 4, 2017 FSC F0001000 FSC A.C. All rights reserved Global FSC-certified forest area North America 35.2% of total FSC-certified area ( 68,947,375 ha ) 246 certificates Europe

FSC Facts & Figures October 4, 2017 FSC F0001000 FSC A.C. All rights reserved Global FSC-certified forest area North America 35.2% of total FSC-certified area ( 68,947,375 ha ) 246 certificates Europe

FSC Facts & Figures. December 1, FSC F FSC A.C. All rights reserved

FSC Facts & Figures December 1, 2017 FSC F0001000 FSC A.C. All rights reserved Global FSC-certified forest area North America 35.7% of total FSC-certified area ( 69,695,913 ha ) 248 certificates Europe

FSC Facts & Figures December 1, 2017 FSC F0001000 FSC A.C. All rights reserved Global FSC-certified forest area North America 35.7% of total FSC-certified area ( 69,695,913 ha ) 248 certificates Europe

Forest Stewardship Council

Global FSC certified area*: by region Africa CAMEROON CONGO, THE REPUBLIC OF GABON GHANA MOZAMBIQUE NAMIBIA SOUTH AFRICA SWAZILAND TANZANIA, UNITED UGANDA Asia CAMBODIA CHINA INDIA INDONESIA JAPAN KOREA,

Global FSC certified area*: by region Africa CAMEROON CONGO, THE REPUBLIC OF GABON GHANA MOZAMBIQUE NAMIBIA SOUTH AFRICA SWAZILAND TANZANIA, UNITED UGANDA Asia CAMBODIA CHINA INDIA INDONESIA JAPAN KOREA,

Dentsu Inc. Investor Day Developing our global footprint

Dentsu Inc. Investor Day Developing our global footprint September 4, 2015 Tim Andree EVP, Member of the Board, Dentsu Inc. Executive Chairman Dentsu Aegis Network Innovating The Way Brands Are Built Dentsu

Dentsu Inc. Investor Day Developing our global footprint September 4, 2015 Tim Andree EVP, Member of the Board, Dentsu Inc. Executive Chairman Dentsu Aegis Network Innovating The Way Brands Are Built Dentsu

CSM-PD. pre-heating, degassing and storage system for clean steam generators

CSM-PD pre-heating, degassing and storage system for clean steam generators Clean steam generator feedwater treatment system To enable clean steam generators to provide the highest quality clean steam

CSM-PD pre-heating, degassing and storage system for clean steam generators Clean steam generator feedwater treatment system To enable clean steam generators to provide the highest quality clean steam

Population Distribution by Income Tiers, 2001 and 2011

1 Updated August 13, 2015: This new edition includes corrected estimates for Iceland, Luxembourg, Netherlands and Taiwan, and some related aggregated data. TABLE A1 Distribution by Income Tiers, 2001 and

1 Updated August 13, 2015: This new edition includes corrected estimates for Iceland, Luxembourg, Netherlands and Taiwan, and some related aggregated data. TABLE A1 Distribution by Income Tiers, 2001 and

Forest Stewardship Council

Global FSC Certified Businesses: by country PUERTO RICO 4 FINLAND 83 BAHRAIN GUATEMALA 29 MACEDONIA 3 VIETNAM 004 CONGO, THE REPUBLIC OF 5 NEW ZEALAND 287 KOREA, REPUBLIC OF 243 UGANDA 3 MONACO 4 EGYPT

Global FSC Certified Businesses: by country PUERTO RICO 4 FINLAND 83 BAHRAIN GUATEMALA 29 MACEDONIA 3 VIETNAM 004 CONGO, THE REPUBLIC OF 5 NEW ZEALAND 287 KOREA, REPUBLIC OF 243 UGANDA 3 MONACO 4 EGYPT

enhance your automation thinking

enhance your automation thinking PLCnext Technology The platform for limitless automation PLCnext Technology Designed by PHOENIX CONTACT In a rapidly changing world, in which more things are now networked

enhance your automation thinking PLCnext Technology The platform for limitless automation PLCnext Technology Designed by PHOENIX CONTACT In a rapidly changing world, in which more things are now networked

FSC Facts & Figures. January 6, FSC F FSC A.C. All rights reserved

FSC Facts & Figures January 6, 2017 FSC F000100 0 FSC A.C. All rights reserved Global FSC-certified forest area North America 35.3% of total FSC-certified area ( 69,212,841 ha ) 248 certificates Europe

FSC Facts & Figures January 6, 2017 FSC F000100 0 FSC A.C. All rights reserved Global FSC-certified forest area North America 35.3% of total FSC-certified area ( 69,212,841 ha ) 248 certificates Europe

FSC Facts & Figures. February 1, FSC F FSC A.C. All rights reserved

FSC Facts & Figures February 1, 2017 FSC F000100 0 FSC A.C. All rights reserved Global FSC-certified forest area North America 35.8% of total FSC-certified area ( 69,590,919 ha ) 249 certificates Europe

FSC Facts & Figures February 1, 2017 FSC F000100 0 FSC A.C. All rights reserved Global FSC-certified forest area North America 35.8% of total FSC-certified area ( 69,590,919 ha ) 249 certificates Europe

FSC Facts & Figures. March 13, FSC F FSC A.C. All rights reserved

FSC Facts & Figures March 13, 2017 FSC F000100 0 FSC A.C. All rights reserved Global FSC-certified forest area North America 35.6% of total FSC-certified area ( 69,049,912 ha ) 248 certificates Europe

FSC Facts & Figures March 13, 2017 FSC F000100 0 FSC A.C. All rights reserved Global FSC-certified forest area North America 35.6% of total FSC-certified area ( 69,049,912 ha ) 248 certificates Europe

FSC Facts & Figures. August 4, FSC F FSC A.C. All rights reserved

FSC Facts & Figures August 4, 2016 FSC F0001000 FSC A.C. All rights reserved Global FSC-certified forest area North America 35.9% of total FSC-certified area ( 68,725,419 ha ) 249 certificates Europe 47.7%

FSC Facts & Figures August 4, 2016 FSC F0001000 FSC A.C. All rights reserved Global FSC-certified forest area North America 35.9% of total FSC-certified area ( 68,725,419 ha ) 249 certificates Europe 47.7%

FSC Facts & Figures. September 12, FSC F FSC A.C. All rights reserved

FSC Facts & Figures September 12, 2016 FSC F0001000 FSC A.C. All rights reserved Global FSC-certified forest area North America 35.8% of total FSC-certified area ( 68,217,276 ha ) 243 certificates Europe

FSC Facts & Figures September 12, 2016 FSC F0001000 FSC A.C. All rights reserved Global FSC-certified forest area North America 35.8% of total FSC-certified area ( 68,217,276 ha ) 243 certificates Europe

FSC Facts & Figures. November 15. FSC F FSC A.C. All rights reserved

FSC Facts & Figures November FSC F00000 FSC A.C. All rights reserved Global FSC certified forest area North America.u of total FSC certified area / 6.8.89 ha D 6 certificates Europe 8u of total FSC certified

FSC Facts & Figures November FSC F00000 FSC A.C. All rights reserved Global FSC certified forest area North America.u of total FSC certified area / 6.8.89 ha D 6 certificates Europe 8u of total FSC certified

Global Gas Deregulation Ed

Global Gas Deregulation Ed 1 2012 What s in this report and analysis? Overview of the state of the gas sector World Survey of Gas Privatisation and Deregulation Coverage of Gas privatisation and deregulation

Global Gas Deregulation Ed 1 2012 What s in this report and analysis? Overview of the state of the gas sector World Survey of Gas Privatisation and Deregulation Coverage of Gas privatisation and deregulation

Rosatom Global Expertise in NPP Construction

ROSATOM STATE ATOMIC ENERGY CORPORATION ROSATOM Rosatom Global Expertise in NPP Construction Nuclear Industry Localization Conference Cape Town, June 1-3, 2011 Fully Integrated Nuclear Technology Company

ROSATOM STATE ATOMIC ENERGY CORPORATION ROSATOM Rosatom Global Expertise in NPP Construction Nuclear Industry Localization Conference Cape Town, June 1-3, 2011 Fully Integrated Nuclear Technology Company

The Future of Nuclear Power after Fukushima

The Future of Nuclear Power after Fukushima Thomas Jonter Professor of International Relations Stockholm University Trends Energy consumption map 1 Before Fukushima: Nuclear Renaissance Reasons: The increasingly

The Future of Nuclear Power after Fukushima Thomas Jonter Professor of International Relations Stockholm University Trends Energy consumption map 1 Before Fukushima: Nuclear Renaissance Reasons: The increasingly

FSC Facts & Figures. December 1, FSC F FSC A.C. All rights reserved

FSC Facts & Figures December, 0 FSC F00000 FSC A.C. All rights reserved Global FSC certified forest area North America.9v of total FSC certified area m 67::08 ha I 47 certificates Europe 47.v of total

FSC Facts & Figures December, 0 FSC F00000 FSC A.C. All rights reserved Global FSC certified forest area North America.9v of total FSC certified area m 67::08 ha I 47 certificates Europe 47.v of total

Nuclear Power Outlook

Q1 2019 A PUBLICATION OF UXC.COM Nuclear Power Outlook 1501 MACY DRIVE ROSWELL, GA 30076 PH +1 770 642-7745 FX +1 770 643-2954 NOTICE UxC, LLC ( UxC ) shall have title to, ownership of, and all proprietary

Q1 2019 A PUBLICATION OF UXC.COM Nuclear Power Outlook 1501 MACY DRIVE ROSWELL, GA 30076 PH +1 770 642-7745 FX +1 770 643-2954 NOTICE UxC, LLC ( UxC ) shall have title to, ownership of, and all proprietary

Press Release. Wind turbines generate more than 1 % of the global electricity. Worldwide Capacity at 93,8 GW 19,7 GW added in 2007

1 Press Release Wind turbines generate more than 1 % of the global electricity Worldwide at 93,8 GW 19,7 GW added in Head Office: Charles-de-Gaulle-Str. 5 53113 Bonn Germany Tel. +49-228-369 40-80 Fax

1 Press Release Wind turbines generate more than 1 % of the global electricity Worldwide at 93,8 GW 19,7 GW added in Head Office: Charles-de-Gaulle-Str. 5 53113 Bonn Germany Tel. +49-228-369 40-80 Fax

Cambridge International Examinations Cambridge International Advanced Subsidiary and Advanced Level

Cambridge International Examinations Cambridge International Advanced Subsidiary and Advanced Level *2029778719-I* GEOGRAPHY 9696/32 Paper 3 Advanced Human Options October/November 2015 INSERT 1 hour 30

Cambridge International Examinations Cambridge International Advanced Subsidiary and Advanced Level *2029778719-I* GEOGRAPHY 9696/32 Paper 3 Advanced Human Options October/November 2015 INSERT 1 hour 30

Cotton: World Markets and Trade

United States Department of Agriculture Foreign Agricultural Service Circular Series FOP - December Cotton: World Markets and Trade Unprecedented Daily Price Volatility Rules the Market Now Daily NY Nearby

United States Department of Agriculture Foreign Agricultural Service Circular Series FOP - December Cotton: World Markets and Trade Unprecedented Daily Price Volatility Rules the Market Now Daily NY Nearby

Oil and Petrochemical overview. solutions for your steam and condensate system

o i l a n d p e t r o c h e m i c a l o v e r v i e w Oil and Petrochemical overview solutions for your steam and condensate system Understanding your steam and condensate system At Spirax Sarco we understand

o i l a n d p e t r o c h e m i c a l o v e r v i e w Oil and Petrochemical overview solutions for your steam and condensate system Understanding your steam and condensate system At Spirax Sarco we understand

OTS. FEEL GOODS. COMPANY PROFILE

OTS. FEEL GOODS. COMPANY PROFILE CONTENTS 4 ABOUT US 6 TRANSPORT 8 MISSION 10 VISION 12 SERVICES 14 SALES AND CUSTOMER SERVICE 16 IMPORT / EXPORT AND CROSSTRADE 18 LOGISTICS 20 CUSTOMS 22 PROJECT DIVISION

OTS. FEEL GOODS. COMPANY PROFILE CONTENTS 4 ABOUT US 6 TRANSPORT 8 MISSION 10 VISION 12 SERVICES 14 SALES AND CUSTOMER SERVICE 16 IMPORT / EXPORT AND CROSSTRADE 18 LOGISTICS 20 CUSTOMS 22 PROJECT DIVISION

INPRO Dialogue Forum on Opportunities and Issues in Non-Electric Applications of Nuclear Energy

INPRO Dialogue Forum on Opportunities and Issues in Non-Electric Applications of Nuclear Energy (16th INPRO Dialogue Forum) Meliá Vienna Hotel (DC Tower) Vienna, Austria 12-14 December 2018 Ref. No.: EVT1702017

INPRO Dialogue Forum on Opportunities and Issues in Non-Electric Applications of Nuclear Energy (16th INPRO Dialogue Forum) Meliá Vienna Hotel (DC Tower) Vienna, Austria 12-14 December 2018 Ref. No.: EVT1702017

Energy, Electricity and Nuclear Power Estimates for the Period up to 2050

REFERENCE DATA SERIES No. 1 2018 Edition Energy, Electricity and Nuclear Power Estimates for the Period up to 2050 @ ENERGY, ELECTRICITY AND NUCLEAR POWER ESTIMATES FOR THE PERIOD UP TO 2050 REFERENCE

REFERENCE DATA SERIES No. 1 2018 Edition Energy, Electricity and Nuclear Power Estimates for the Period up to 2050 @ ENERGY, ELECTRICITY AND NUCLEAR POWER ESTIMATES FOR THE PERIOD UP TO 2050 REFERENCE

Summary for Policymakers

Summary for Policymakers Yale Center for Environmental Law and Policy, Yale University Center for International Earth Science Information Network, Columbia University In collaboration with World Economic

Summary for Policymakers Yale Center for Environmental Law and Policy, Yale University Center for International Earth Science Information Network, Columbia University In collaboration with World Economic

Payroll Across Borders

Payroll Across Borders 2 Question: Are you planning to expand your Does Global Payroll truly exist? business into new global markets? Question: Based on your experience, do you believe that there is a

Payroll Across Borders 2 Question: Are you planning to expand your Does Global Payroll truly exist? business into new global markets? Question: Based on your experience, do you believe that there is a

A National Energy Perspective

Olkiluoto-3, Finland (Source: TVO) Olkiluoto-3, Finland (Source: Google) A National Energy Perspective Prof. Dr. Attila ASZÓDI Director Budapest University of Technology and Economics Institute of Nuclear

Olkiluoto-3, Finland (Source: TVO) Olkiluoto-3, Finland (Source: Google) A National Energy Perspective Prof. Dr. Attila ASZÓDI Director Budapest University of Technology and Economics Institute of Nuclear

The Future of Nuclear Market Challenges and Solutions: New Projects, New Products, New Business-Models

The Future of Nuclear Market Challenges and Solutions: New Projects, New Products, New Business-Models Dzhomart Aliev Director General Rusatom Overseas 26.06.2013 Rosatom s Global Perspective For Nuclear

The Future of Nuclear Market Challenges and Solutions: New Projects, New Products, New Business-Models Dzhomart Aliev Director General Rusatom Overseas 26.06.2013 Rosatom s Global Perspective For Nuclear

Spirax Sarco. Clean steam overview

Spirax Sarco Clean steam overview Spirax Sarco - investing in solutions for clean systems Clean steam has been an important part of Spirax Sarco s business since pioneering the development of the BT6,

Spirax Sarco Clean steam overview Spirax Sarco - investing in solutions for clean systems Clean steam has been an important part of Spirax Sarco s business since pioneering the development of the BT6,

Spirax SafeBloc TM. double block and bleed bellows sealed stop valve

Spirax SafeBloc TM double block and bleed bellows sealed stop Spirax SafeBloc TM a single solution for safe double isolation The Spirax SafeBloc TM is a safe isolation solution, with a unique space-saving

Spirax SafeBloc TM double block and bleed bellows sealed stop Spirax SafeBloc TM a single solution for safe double isolation The Spirax SafeBloc TM is a safe isolation solution, with a unique space-saving

Nuclear in the national and international framework. Dr. Pompiliu Budulan Director General

Nuclear in the national and international framework Dr. Pompiliu Budulan Director General CEI Summit Economic Forum 12 November 2009 - Bucharest 1 Content Energy - a global issue Nuclearelectrica general

Nuclear in the national and international framework Dr. Pompiliu Budulan Director General CEI Summit Economic Forum 12 November 2009 - Bucharest 1 Content Energy - a global issue Nuclearelectrica general

AREVA Forward-looking Nuclear Energy. Karl-Heinz Poets AREVA South America

AREVA Forward-looking Nuclear Energy Karl-Heinz Poets AREVA South America Energy market: continued growth announced tep Macroeconomics Energy demand multiplied by 2 by 2050 1990 2010 2030 BUSINESS AS USUAL

AREVA Forward-looking Nuclear Energy Karl-Heinz Poets AREVA South America Energy market: continued growth announced tep Macroeconomics Energy demand multiplied by 2 by 2050 1990 2010 2030 BUSINESS AS USUAL

CONVENTION FOR THE UNIFICATION OF CERTAIN RULES FOR INTERNATIONAL CARRIAGE BY AIR DONE AT MONTREAL ON 28 MAY 1999

State CONVENTION FOR THE UNIFICATION OF CERTAIN RULES FOR INTERNATIONAL CARRIAGE BY AIR DONE AT MONTREAL ON 28 MAY 1999 Entry into force: The Convention entered into force on 4 November 2003. Status: 91

State CONVENTION FOR THE UNIFICATION OF CERTAIN RULES FOR INTERNATIONAL CARRIAGE BY AIR DONE AT MONTREAL ON 28 MAY 1999 Entry into force: The Convention entered into force on 4 November 2003. Status: 91

Nuclear Power Profile of Germany

Nuclear Power Profile of Germany Technical Meeting on CNPP, Vienna, 10 13 May 2016 Dr. Claudia Link Federal Office for Radiation Protection, Salzgitter Content Electricity Production Nuclear Power Plants

Nuclear Power Profile of Germany Technical Meeting on CNPP, Vienna, 10 13 May 2016 Dr. Claudia Link Federal Office for Radiation Protection, Salzgitter Content Electricity Production Nuclear Power Plants

HEALTH WEALTH CAREER MERCER LIFE SCIENCES REMUNERATION SURVEY

HEALTH WEALTH CAREER MERCER LIFE SCIENCES REMUNERATION SURVEY MAKE SMART COMPENSATION DECISIONS BY JOINING THE 2016 MERCER TOTAL REMUNERATION SURVEY FOR THE LIFE SCIENCES SECTOR THE LIFE SCIENCES REMUNERATION

HEALTH WEALTH CAREER MERCER LIFE SCIENCES REMUNERATION SURVEY MAKE SMART COMPENSATION DECISIONS BY JOINING THE 2016 MERCER TOTAL REMUNERATION SURVEY FOR THE LIFE SCIENCES SECTOR THE LIFE SCIENCES REMUNERATION

NUCLEAR OPERATOR LIABILITY AMOUNTS AND FINANCIAL SECURITY LIMITS. (Last updated: July 2015)

") NUCLEAR OPERATOR LIABILITY AMOUNTS AND FINANCIAL SECURITY LIMITS (: July 2015) The OECD Nuclear Energy Agency attempts to maintain the information contained in the attached table in as current a state

NUCLEAR OPERATOR LIABILITY AMOUNTS AND FINANCIAL SECURITY LIMITS (: July 2015) The OECD Nuclear Energy Agency attempts to maintain the information contained in the attached table in as current a state

Argus Benzene Annual 2017

Argus Benzene Annual 2017 Petrochemicals illuminating the markets Market Reporting Consulting Events Argus Benzene Annual 2017 Summary The Argus (formerly DeWitt) Benzene Annual has provided an accurate

Argus Benzene Annual 2017 Petrochemicals illuminating the markets Market Reporting Consulting Events Argus Benzene Annual 2017 Summary The Argus (formerly DeWitt) Benzene Annual has provided an accurate

International Nuclear Fuel Centers in the Global Infrastructure of Nuclear Power (Technological Aspects of the Problem)

") International Conference on Fast Reactors and Related Fuel Cycles: Challenges and Opportunities FR09 Kyoto, Japan, 7-11 December, 2009 International Nuclear Fuel Centers in the Global Infrastructure of

International Conference on Fast Reactors and Related Fuel Cycles: Challenges and Opportunities FR09 Kyoto, Japan, 7-11 December, 2009 International Nuclear Fuel Centers in the Global Infrastructure of

Siemens Partner Program

Siemens Partner Program Factory Automation Partner Strategy for Factory Automation End Customer Focus on core competencies Demand on efficient solutions Certified Partner Added value in solutions and services

Siemens Partner Program Factory Automation Partner Strategy for Factory Automation End Customer Focus on core competencies Demand on efficient solutions Certified Partner Added value in solutions and services

SAMPLE. Reference Code: GDAE6529IDB. Publication Date: April 2015

Hydropower in Indonesia, Market Outlook to 2025, Update 2015 Capacity, Generation, Levelized Cost of Energy (LCOE), Investment Trends, Regulations and Company Profiles Reference Code: GDAE6529IDB Publication

Hydropower in Indonesia, Market Outlook to 2025, Update 2015 Capacity, Generation, Levelized Cost of Energy (LCOE), Investment Trends, Regulations and Company Profiles Reference Code: GDAE6529IDB Publication

2015 MERCER LIFE SCIENCES REMUNERATION SURVEY

2015 MERCER LIFE SCIENCES REMUNERATION SURVEY MAKE SMART COMPENSATION DECISIONS BY JOINING THE 2015 MERCER TOTAL REMUNERATION SURVEY FOR THE LIFE SCIENCES SECTOR THE LIFE SCIENCES REMUNERATION SURVEY PROVIDES

2015 MERCER LIFE SCIENCES REMUNERATION SURVEY MAKE SMART COMPENSATION DECISIONS BY JOINING THE 2015 MERCER TOTAL REMUNERATION SURVEY FOR THE LIFE SCIENCES SECTOR THE LIFE SCIENCES REMUNERATION SURVEY PROVIDES

GLOBAL VIDEO-ON- DEMAND (VOD)

") GLOBAL VIDEO-ON- DEMAND (VOD) HOW WORLDWIDE VIEWING HABITS ARE CHANGING IN THE EVOLVING MEDIA LANDSCAPE MARCH 2016 A CHANGING VIDEO-VIEWING LANDSCAPE Nearly two-thirds of global respondents say they watch

GLOBAL VIDEO-ON- DEMAND (VOD) HOW WORLDWIDE VIEWING HABITS ARE CHANGING IN THE EVOLVING MEDIA LANDSCAPE MARCH 2016 A CHANGING VIDEO-VIEWING LANDSCAPE Nearly two-thirds of global respondents say they watch

Energiewende. Germany s energy system and the status of the energy transition. Dr Falk Bömeke, LL.M.

Energiewende Germany s energy system and the status of the energy transition Dr Falk Bömeke, LL.M. Federal Ministry for Economic Affairs and Energy 25 June 2018 18-06-27 Referent 1 Source: Edelman.ergo

Energiewende Germany s energy system and the status of the energy transition Dr Falk Bömeke, LL.M. Federal Ministry for Economic Affairs and Energy 25 June 2018 18-06-27 Referent 1 Source: Edelman.ergo

Global Perspectives on SMRs Developing Countries Expectations

Global Perspectives on SMRs Developing Countries Expectations Dr Atam Rao Head Nuclear Power Technology Development Jun 18, 2010 The 4 th Annual Asia-Pacific Nuclear Energy Forum on Small and Medium Reactors

Global Perspectives on SMRs Developing Countries Expectations Dr Atam Rao Head Nuclear Power Technology Development Jun 18, 2010 The 4 th Annual Asia-Pacific Nuclear Energy Forum on Small and Medium Reactors

1 Controlling for non-linearities

1 Controlling for non-linearities Since previous studies have found significant evidence for deaths from natural catastrophes to be non-linearly related to different measures of development (Brooks et

1 Controlling for non-linearities Since previous studies have found significant evidence for deaths from natural catastrophes to be non-linearly related to different measures of development (Brooks et

APPLIED NUCLEAR KNOWLEDGE MANAGEMENT IN AUSTRIA

APPLIED NUCLEAR KNOWLEDGE MANAGEMENT IN AUSTRIA H.BOECK, M.VILLA, R.BERGMANN, THIRD INTERNATIONAL CONFERENCE ON NUCLEAR KNOWLEDGE MANAGEMENT CHALLENGES AND APPROACHES VIENNA, AUSTRIA 7 11 NOVEMBER 2016

APPLIED NUCLEAR KNOWLEDGE MANAGEMENT IN AUSTRIA H.BOECK, M.VILLA, R.BERGMANN, THIRD INTERNATIONAL CONFERENCE ON NUCLEAR KNOWLEDGE MANAGEMENT CHALLENGES AND APPROACHES VIENNA, AUSTRIA 7 11 NOVEMBER 2016

Cotton: World Markets and Trade

United States Department of Agriculture Foreign Agricultural Service Cotton: World Markets and Trade May Global Consumption Rises Above Production, Fall USDA s initial forecast for / shows world consumption

United States Department of Agriculture Foreign Agricultural Service Cotton: World Markets and Trade May Global Consumption Rises Above Production, Fall USDA s initial forecast for / shows world consumption

Reference Code: GDAE6521IDB. Publication Date: March 2015

Hydro Power in France, Market Outlook to 2025, Update 2015 Capacity, Generation, Levelized Cost of Energy (LCOE), Investment Trends, Regulations and Company Profiles Reference Code: GDAE6521IDB Publication

Hydro Power in France, Market Outlook to 2025, Update 2015 Capacity, Generation, Levelized Cost of Energy (LCOE), Investment Trends, Regulations and Company Profiles Reference Code: GDAE6521IDB Publication

Strategy of State Atomic Energy Corporation Rosatom till 2030

Strategy of State Atomic Energy Corporation Rosatom till Karavaev I.A. Chief Strategy and Investments Officer June, 2012 By, nuclear power generation is expected to keep pace with global energy demand

Strategy of State Atomic Energy Corporation Rosatom till Karavaev I.A. Chief Strategy and Investments Officer June, 2012 By, nuclear power generation is expected to keep pace with global energy demand

International management system: ISO on environmental management

International management system: ISO 14000 on environmental management Introduction In response to the growing interest from businesses in environmental standards, the International Standardization Institute,

International management system: ISO 14000 on environmental management Introduction In response to the growing interest from businesses in environmental standards, the International Standardization Institute,

Findings from FAOSTAT user questionnaire surveys

Joint FAO/UNECE Working party On Forest Economics and Statistics 28 th session, Geneva, 2-4 May 2006 Agenda Item 6 Dissemination of outputs During the last decade FAO has carried out two FAO forest product

Joint FAO/UNECE Working party On Forest Economics and Statistics 28 th session, Geneva, 2-4 May 2006 Agenda Item 6 Dissemination of outputs During the last decade FAO has carried out two FAO forest product

Solution Partner Program Global Perspective

Solution Partner Program Global Perspective SPACe 2012 Siemens Process Automation Conference Business Development Solution Partner Program Copyright Siemens AG 2012. All rights reserved Solution Partner

Solution Partner Program Global Perspective SPACe 2012 Siemens Process Automation Conference Business Development Solution Partner Program Copyright Siemens AG 2012. All rights reserved Solution Partner

SAMPLE. Reference Code: GDAE6535IDB. Publication Date: May 2015

Hydropower in Austria, Market Outlook to 2025, Update 2015 Capacity, Generation, Levelized Cost of Energy (LCOE), Investment Trends, Regulations and Company Profiles Reference Code: GDAE6535IDB Publication

Hydropower in Austria, Market Outlook to 2025, Update 2015 Capacity, Generation, Levelized Cost of Energy (LCOE), Investment Trends, Regulations and Company Profiles Reference Code: GDAE6535IDB Publication

PEFC Global Statistics: SFM & CoC Certification.

PEFC Global Statistics: SFM & CoC Certification Data: Sep 2017 www.pefc.org Members, Endorsed Systems; Distribution of Certificates North America 164.4 million ha 54.1% TCA 451 CoC Europe 95.9 million

PEFC Global Statistics: SFM & CoC Certification Data: Sep 2017 www.pefc.org Members, Endorsed Systems; Distribution of Certificates North America 164.4 million ha 54.1% TCA 451 CoC Europe 95.9 million

Rosatom Global Development, International Cooperation Perspective

ROSATOM STATE ATOMIC ENERGY CORPORATION ROSATOM Rosatom Global Development, International Cooperation Perspective Rosatom Seminar on Russian Nuclear Energy Technologies and Solutions Alexey Kalinin Head,

ROSATOM STATE ATOMIC ENERGY CORPORATION ROSATOM Rosatom Global Development, International Cooperation Perspective Rosatom Seminar on Russian Nuclear Energy Technologies and Solutions Alexey Kalinin Head,

Seizing E-Government Opportunities: Assessment, Prioritization, & Action. June 12, 2001

Seizing E-Government Opportunities: Assessment, Prioritization, & Action June 12, 2001 Today s Topics Understanding E-Readiness Assessing Readiness for E-Government Learning from Successes Prioritizing

Seizing E-Government Opportunities: Assessment, Prioritization, & Action June 12, 2001 Today s Topics Understanding E-Readiness Assessing Readiness for E-Government Learning from Successes Prioritizing

SMALL MODULAR REACTORS: CONTOURS OF PROLIFERATION/SECURIT Y RISKS

SMALL MODULAR REACTORS: CONTOURS OF PROLIFERATION/SECURIT Y RISKS Sharon Squassoni Director, Proliferation Prevention Program Center for Strategic & International Studies Platts 4 th Annual Small Modular

SMALL MODULAR REACTORS: CONTOURS OF PROLIFERATION/SECURIT Y RISKS Sharon Squassoni Director, Proliferation Prevention Program Center for Strategic & International Studies Platts 4 th Annual Small Modular

CONVERSION FACTORS. Standard conversion factors for liquid fuels are determined on the basis of the net calorific value for each product.

CONVERSION FACTORS The data which have been supplied by the countries in original units are converted to the common unit, terajoules (TJ), by using standard conversion factors or, in the case of solids,

CONVERSION FACTORS The data which have been supplied by the countries in original units are converted to the common unit, terajoules (TJ), by using standard conversion factors or, in the case of solids,

Argus Ethylene Annual 2017

Argus Ethylene Annual 2017 Market Reporting Petrochemicals illuminating the markets Consulting Events Argus Ethylene Annual 2017 Summary Progress to the next peak of the economic cycle, now expected by

Argus Ethylene Annual 2017 Market Reporting Petrochemicals illuminating the markets Consulting Events Argus Ethylene Annual 2017 Summary Progress to the next peak of the economic cycle, now expected by

Nuclear Energy & Economic Competitiveness in Various Regulatory Systems

Nuclear Energy & Economic Competitiveness in Various Regulatory Systems Presentation at: The re-emergence of nuclear energy: An option for climate change & emerging countries? UNAM, Mexico City, April

Nuclear Energy & Economic Competitiveness in Various Regulatory Systems Presentation at: The re-emergence of nuclear energy: An option for climate change & emerging countries? UNAM, Mexico City, April

Overview of FSC-certified forests January Maps of extend of FSC-certified forest globally and country specific

Overview of FSCcertified forests Maps of extend of FSCcertified forest globally and country specific Global certified forest area: 120.052.350 ha ( = 4,3%) + 1% Hectare FSCcertified forest 10.000.000 and

Overview of FSCcertified forests Maps of extend of FSCcertified forest globally and country specific Global certified forest area: 120.052.350 ha ( = 4,3%) + 1% Hectare FSCcertified forest 10.000.000 and

INTERNATIONAL ENERGY CHARTER

ENERGY CHARTER SECRETARIAT INTERNATIONAL ENERGY CHARTER Frequently Asked Questions What is the International Energy Charter? Brussels, 21 November 2014 In May 2015, states representing up to one half of

ENERGY CHARTER SECRETARIAT INTERNATIONAL ENERGY CHARTER Frequently Asked Questions What is the International Energy Charter? Brussels, 21 November 2014 In May 2015, states representing up to one half of

New German Energy Policy - Achievements and Challenges

New German Energy Policy - Achievements and Challenges Dr. Stefan NIESSEN Vice-President Research & Development AREVA NP GmbH Comparison of German NPP lifetime before and post March 2011 (1/2) 2005 2010

New German Energy Policy - Achievements and Challenges Dr. Stefan NIESSEN Vice-President Research & Development AREVA NP GmbH Comparison of German NPP lifetime before and post March 2011 (1/2) 2005 2010

CONVENTION FOR THE UNIFICATION OF CERTAIN RULES FOR INTERNATIONAL CARRIAGE BY AIR DONE AT MONTREAL ON 28 MAY 1999

State CONVENTION FOR THE UNIFICATION OF CERTAIN RULES FOR INTERNATIONAL CARRIAGE BY AIR DONE AT MONTREAL ON 28 MAY 1999 Entry into force: The Convention entered into force on 4 November 2003*. Status:

State CONVENTION FOR THE UNIFICATION OF CERTAIN RULES FOR INTERNATIONAL CARRIAGE BY AIR DONE AT MONTREAL ON 28 MAY 1999 Entry into force: The Convention entered into force on 4 November 2003*. Status:

Global Food Security Index

Global Food Security Index Sponsored by 26 September 2012 Agenda Overview Methodology Overall results Results for India Website 2 Overview The Economist Intelligence Unit was commissioned by DuPont to

Global Food Security Index Sponsored by 26 September 2012 Agenda Overview Methodology Overall results Results for India Website 2 Overview The Economist Intelligence Unit was commissioned by DuPont to

The nuclear scene in Europe: current reality and future trends

The nuclear scene in Europe: current reality and future trends Santiago San Antonio Director General of FORATOM UPM Summer Courses Madrid, 6 July 2009 FORATOM who we are? Brussels-based trade association

The nuclear scene in Europe: current reality and future trends Santiago San Antonio Director General of FORATOM UPM Summer Courses Madrid, 6 July 2009 FORATOM who we are? Brussels-based trade association

Management of Spent Fuel from the Perspective of the German Industry

Management of Spent Fuel from the Perspective of the German Industry Dipl.-Ing. W. Graf GNS Gesellschaft für Nuklear- Service mbh IAEA Vienna International Conference on Management of Spent Fuel from Nuclear

Management of Spent Fuel from the Perspective of the German Industry Dipl.-Ing. W. Graf GNS Gesellschaft für Nuklear- Service mbh IAEA Vienna International Conference on Management of Spent Fuel from Nuclear

Nuclear Power Economics and Markets

Nuclear Power Economics and Markets IBC - Decommissioning of Nuclear Reactors & Materials 29 30 September 2014; Miami, Florida Edward Kee Disclaimer The NECG slides that follow are not a complete record

Nuclear Power Economics and Markets IBC - Decommissioning of Nuclear Reactors & Materials 29 30 September 2014; Miami, Florida Edward Kee Disclaimer The NECG slides that follow are not a complete record

A d i l N a j a m Pardee Center for the study of the Longer-Term Future B o s t o n U n i v e r s i t y

A d i l N a j a m The Fredrick S. Pardee Chair for Global Public Policy Pardee Center for the study of the Longer-Term Future B o s t o n U n i v e r s i t y How can ECOSOC and AMR foster integration of

A d i l N a j a m The Fredrick S. Pardee Chair for Global Public Policy Pardee Center for the study of the Longer-Term Future B o s t o n U n i v e r s i t y How can ECOSOC and AMR foster integration of

PEFC Global Statistics: SFM & CoC Certification. November 2013

PEFC Global Statistics: SFM & CoC Certification 1 November 2013 Members; Endorsed Systems; Distribution of Certificates North America 151 million ha 60% TCA 503 CoC Europe 81 million ha 32% TCA 8,389 CoC

PEFC Global Statistics: SFM & CoC Certification 1 November 2013 Members; Endorsed Systems; Distribution of Certificates North America 151 million ha 60% TCA 503 CoC Europe 81 million ha 32% TCA 8,389 CoC

NUCLEAR OPERATORS THIRD PARTY LIABILITY AMOUNTS AND FINANCIAL SECURITY LIMITS

NUCLEAR OPERATORS THIRD PARTY LIABILITY AMOUNTS AND FINANCIAL SECURITY LIMITS (: April 2018) The OECD Nuclear Energy Agency attempts to maintain the information contained in the attached table in as current

NUCLEAR OPERATORS THIRD PARTY LIABILITY AMOUNTS AND FINANCIAL SECURITY LIMITS (: April 2018) The OECD Nuclear Energy Agency attempts to maintain the information contained in the attached table in as current

MERCER TRS TOTAL REMUNERATION SURVEY THE KEY TO DESIGNING COMPETITIVE PAY PACKAGES WORLDWIDE

MERCER TRS THE KEY TO DESIGNING COMPETITIVE PAY PACKAGES WORLDWIDE MERCER TRS THE KEY TO DESIGNING COMPETITIVE PAY PACKAGES WORLDWIDE CONSIDER THESE QUESTIONS... Do you have an easy-to-use source for comparing

MERCER TRS THE KEY TO DESIGNING COMPETITIVE PAY PACKAGES WORLDWIDE MERCER TRS THE KEY TO DESIGNING COMPETITIVE PAY PACKAGES WORLDWIDE CONSIDER THESE QUESTIONS... Do you have an easy-to-use source for comparing

Appendix F. Electricity Emission Factors

Appendix F. Electricity Emission Factors F.1 Domestic Electricity Emission Factors, 1999-2002 Region / MWh) Methane Nitrous Oxide (1) New York, Connecticut, Rhode Island, Massachusetts, Vermont, New Hampshire

Appendix F. Electricity Emission Factors F.1 Domestic Electricity Emission Factors, 1999-2002 Region / MWh) Methane Nitrous Oxide (1) New York, Connecticut, Rhode Island, Massachusetts, Vermont, New Hampshire

Global Guide to Natural Gas Utilities Report Edition 1, 2012

Global Guide to Natural Gas Utilities Report Edition 1, 2012 Market Intelligence Carbon reduction commitments and low gas prices relative to other fossil fuels have made natural gas more attractive for

Global Guide to Natural Gas Utilities Report Edition 1, 2012 Market Intelligence Carbon reduction commitments and low gas prices relative to other fossil fuels have made natural gas more attractive for

Germany s energy system and the status of the energy transition

Energiewende Germany s energy system and the status of the energy transition Dr Falk Bömeke, LL.M. (Sydney) Federal Ministry for Economic Affairs and Energy Drivers, challenges and opportunities of the

Energiewende Germany s energy system and the status of the energy transition Dr Falk Bömeke, LL.M. (Sydney) Federal Ministry for Economic Affairs and Energy Drivers, challenges and opportunities of the

Cancer survival trends and inequalities: what is the role for Europe?

Cancer survival trends and inequalities: what is the role for Europe? European Joint Action on Comprehensive Cancer Control 2014-2017 Brussels, Belgium, 13 May 2015 Measures of cancer burden definition

Cancer survival trends and inequalities: what is the role for Europe? European Joint Action on Comprehensive Cancer Control 2014-2017 Brussels, Belgium, 13 May 2015 Measures of cancer burden definition

RENEWABLES IN GLOBAL ENERGY SUPPLY. An IEA Fact Sheet

I N T E R N AT I O N A L E N E R G Y A G E N C Y RENEWABLES IN GLOBAL ENERGY SUPPLY An IEA Fact Sheet November 2002 INTERNATIONAL ENERGY AGENCY 9 rue de la Fédération 75739 Paris Cedex 15 - France Tel:

I N T E R N AT I O N A L E N E R G Y A G E N C Y RENEWABLES IN GLOBAL ENERGY SUPPLY An IEA Fact Sheet November 2002 INTERNATIONAL ENERGY AGENCY 9 rue de la Fédération 75739 Paris Cedex 15 - France Tel:

Hao Jia (Dr.), Researcher, APERC Takashi Otsuki (Mr.), Researcher, APERC* Kazutomo Irie (Dr.), General Manager, APERC. *Corresponding author

, Researcher, APERC Takashi Otsuki (Mr.), Researcher, APERC* Kazutomo Irie (Dr.), General Manager, APERC. *Corresponding author") Hao Jia (Dr.), Researcher, APERC Takashi Otsuki (Mr.), Researcher, APERC* Kazutomo Irie (Dr.), General Manager, APERC *Corresponding author Contents Introduction / project overview Nuclear power in the

Hao Jia (Dr.), Researcher, APERC Takashi Otsuki (Mr.), Researcher, APERC* Kazutomo Irie (Dr.), General Manager, APERC *Corresponding author Contents Introduction / project overview Nuclear power in the

CONVERSION FACTORS. Standard conversion factors for liquid fuels are determined on the basis of the net calorific value for each product.

CONVERSION FACTORS The data which have been supplied by the countries in original units are converted to the common unit, terajoules (TJ), by using standard conversion factors or, in the case of solids,

CONVERSION FACTORS The data which have been supplied by the countries in original units are converted to the common unit, terajoules (TJ), by using standard conversion factors or, in the case of solids,