An INDEPENDENT energy consulting company since 1996 No affiliation with any marketer, broker, agent, utility, pipeline or producer.

|

|

|

- Johnathan Owen

- 5 years ago

- Views:

Transcription

1

2 An INDEPENDENT energy consulting company since 1996 No affiliation with any marketer, broker, agent, utility, pipeline or producer. More than two decades of experience in the natural gas and electric industries Specialize in natural gas and electricity buying advice for businesses and the development and implementation of proactive purchasing plans. Publications, Seminars, & Consulting Services

3 Cost Categories for Business Customers Utility 7% P/L 8% DEREGULATED Commodity 85% Based on the Henry Hub, located in Louisiana The most volatile price component

4 06/90 01/91 08/91 03/92 10/92 05/93 12/93 07/94 02/95 09/95 04/96 11/96 06/97 01/98 08/98 03/99 10/99 05/00 12/00 07/01 02/02 09/02 04/03 11/03 06/04 01/05 08/05 03/06 10/06 05/07 12/07 07/08 02/09 09/09 04/10 11/10 06/11 01/12 Natural Gas Monthly NYMEX Expirations $ $ $ $ What has changed The long-term price trend change for natural gas is going to be more heavily driven by the cost of other commodities crude oil, NGLs, and coal. $8.000 $6.000 $4.000 $2.000 $-

5 Fundamentals Supply & Demand Weather Competing Fuels Technicals Support/Resistance Charts Financial Economy Psychology Bull/Bear Markets

6 Trillion cubic feet per year Source: Early Release: EIA Annual Energy Outlook 2012 NOTE: Imports have disappeared Since 2000, shale gas production has increased 17-fold and is now about 30% of U.S. production. Shale gas production increases from 5 Tcf in 2010 to 13.6 Tcf in 2035.

7 Estimates will continue to change as new wells provide additional data and technologies change Long-term productivity remains untested Only portions of plays are tested Unknowns of stacked plays

8

9 Ongoing advancements in technologies Multi-stage fracturing process increases productivity No fears over a supply shortfall Source: Wood Mackenzie Long Term View April 2011 From ExxonMobil LDC Forum Presentation: Fall 2011 Chicago

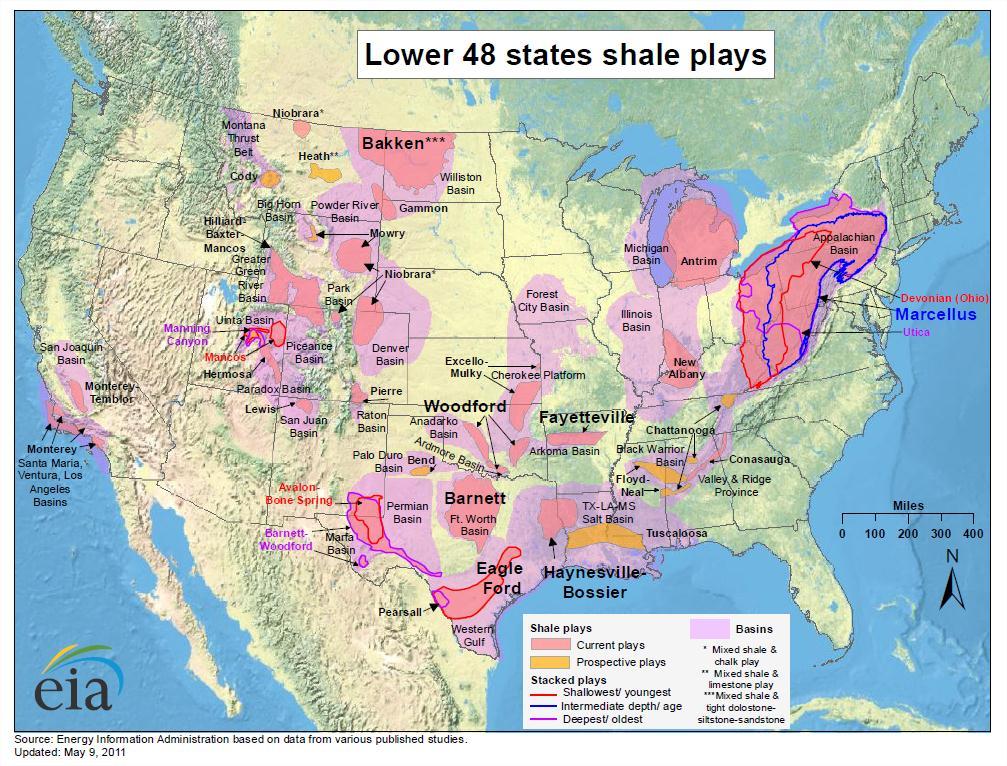

: 5,000 square miles")

10 Productive portion comparisons Marcellus Shale: 95,000 square miles Barnett Shale (Texas): 5,000 square miles

11 Lies beneath the Marcellus Shale Stacked plays Still many unknowns Estimated to hold as much as 25 billion barrels of oil May be the largest domestic discovery of oil in 50 years

12 Associated Natural Gas: Gas that is produced as a byproduct of crude oil production Producers have moved drilling rigs from natural gas to crude oil plays due to economics Drilling for crude oil has increased natural gas supply levels through the production of associated gas The amount of associated gas being produced has been greatly underestimated

13 6/1/1990 6/1/1991 6/1/1992 6/1/1993 6/1/1994 6/1/1995 6/1/1996 6/1/1997 6/1/1998 6/1/1999 6/1/2000 6/1/2001 6/1/2002 6/1/2003 6/1/2004 6/1/2005 6/1/2006 6/1/2007 6/1/2008 6/1/2009 6/1/2010 6/1/2011 6/1/2012 1,800 Drilling Rig Counts 1,600 Crude Oil Drilling Rig Count Natural Gas Drilling Rig Count 1,400 1,200 Oct 2008: Price of natural gas: $7.50 per MMBtu Apr 2012: Price of natural gas: $2.50 per MMBtu Crude $103/barrel = $17.76 per MMBtu 1, Source: Baker Hughes

Wet natural gas contains impurities and hydrocarbons NGLs are stripped away and sold separately based on crude oil prices NGLs include ethane, propane, normal")

14 Dry gas vs. wet gas Natural Gas Liquids (NGLs) Wet natural gas contains impurities and hydrocarbons NGLs are stripped away and sold separately based on crude oil prices NGLs include ethane, propane, normal butane, isobutane, pentane, and natural gasoline Natural gas production curtailments are taking place in the most inefficient and drier natural gas plays, which contain little or no NGLs

15 Revenue supplements NGLs Associated natural gas production Break-even prices have fallen Expenses have fallen (lower rig rental rates, less labor needed, falling real estate prices) Higher well productivity levels (more gas from single rig, higher reserve finds) Improved efficiencies (average time to drill to total depth has fallen by more than 25% in past two years)

16 Disconnection between rig count, production levels and price Investors want active companies Backlog of wells ready to come on-line Supply exists and will be produced at the right price New attitudes toward the market Producers say they will increase spending at $5 and cut spending at $3.50 per MMBtu One year ago, they said they would increase spending at $6 and cut spending at $4 per MMBtu Producers are hedging 2013 supplies Supply is positive for consumers

17 U.S. Natural Gas Production and Imports billion cubic feet per day (bcf/d) annual change (bcf/d) Federal Gulf of Mexico production (right axis) U.S. net imports (right axis) U.S. non-gulf of Mexico production (right axis) Total marketed production (left axis) Marketed production forecast (left axis) Source: Short-Term Energy Outlook, September 2012

18 Weekly injections/withdrawals are a measurement of supply and demand Expectations vs. reality create a volatile market environment on Thursdays

19 U.S. Working Natural Gas in Storage billion cubic feet 5,000 4,000 deviation from average Forecast 210% 180% 3, % 2, % 1,000 90% 0 60% -1,000 30% -2,000 0% -3,000 Jan 2008 Jan 2009 Jan 2010 Jan 2011 Jan 2012 Jan % Note: Colored band around storage levels represents the range between the minimum and maximum from Jan Dec Source: Short-Term Energy Outlook, September 2012

20 Storage Inventories Currently 3,402 Bcf (395 Bcf higher than last year) Ending inventories are projected to exceed 4,000 Bcf. Maximum practical storage capacity is estimated to be 4,340 Bcf. It will be the smallest summer build since 1991 Limits on storage capacity will limit overall injections Physical system constraints occur when storage gets too full

21 Most growth from the electric power sector Near-term: Increased coal-to-natural gas fuel switching because of price Long-term: Coal-fired plant retirements could drive a 4-6 Bcf/day rise in demand from the electric power sector through 2018 Unknowns: Compliance timing and requirements with new EPA rules Additional demand growth from LNG and pipeline exports

22 Source: Goldman Sachs Equity Research

23 Natural gas has become a competitive fuel choice for electric generation Gas peaking units in the Southeast outcompete most base load coal units Central Appalachian (CAPP) $57/ton = $2.85/MMBtu Long-term: Coal-fired plant retirements could drive a 4-6 Bcf/day rise in demand from the electric power sector between

24 Source: Dominick Chirichella

Japan: Henry Hub Price + $5.30 ($2.60 in liquefaction costs + $2.")

25 LNG Exports LNG exports should begin in 2015 By 2020, 2-4 Bcf/day is projected to be exported LNG export costs from Gulf of Mexico Europe: Henry Hub Price + $3.80 ($2.60 in liquefaction costs + $1.20 for shipping) Japan: Henry Hub Price + $5.30 ($2.60 in liquefaction costs + $2.70 for shipping) $12-$18 per MMBtu overseas due to price link to crude oil

26 U.S. becomes an LNG exporter in 2015.

27 Weather: Flip a coin! Summer heat Winter cold Hurricanes Economic recovery and industrial demand Natural Gas Vehicles: Lack of infrastructure Anticipated political actions

28 U.S. Natural Gas Consumption billion cubic feet per day (bcf/d) Production still expected to outpace year-over-year increases in demand annual change (bcf/d) Electric power (right axis) Residential and comm. (right axis) Industrial (right axis) Other (right axis) Total consumption (left axis) Consumption forecast (left axis) Source: Short-Term Energy Outlook, September 2012

29 Price downside limited due to fuel switching A lack of storage capacity could depress near-term spot market prices No concerns over supply meeting demand

30 A change in the perception of the future balance between supply and demand Structural permanent shifts in demand Electric generation Coal plant retirements / Coal displacement LNG exports Speculators will likely decide when the bottom is in (watch for herd mentality)

31 EIA 2010: $4.39 per MMBtu (Actual) 2011: $4.04 per MMBtu (Actual) 2012: $2.58 per MMBtu 2013: $3.22 per MMBtu Long-term projections 2013: $2.75-$4.00/MMBtu 2014: $3.50-$4.25/MMBtu 2015: $4.00-$4.50/MMBtu After 2015: $5-$6/MMBtu

32 Changes in the outlook for crude oil prices Economic data becomes increasingly positive Non-OPEC countries experience large and persistent supply disruptions Changes in the outlook for coal commodities Coal prices tumble causing natural gas demand to significantly decline Restrictive EPA policies that support a faster transition to natural gas-fired electric generation Changes in the outlook for NGLs Economics of NGL supplements declines

33 Natural Gas Fracking issues (earthquakes, water supply) Technologies of waterless fracking implemented Economics of accessing stacked plays declines Draft EPA Fracturing Study to determine the potential impact of fracking fluids on drinking water, human health and the environment to be released at end of 2012 Legislation which dramatically alters the number of players participating in futures market trading LNG export market doesn t evolve as anticipated

34 Valerie Wood Verona, WI Tel: (608) Industry info at

Technologies to recover it were refined as natural gas prices rose to $10 per MMBtu Locations of shale gas were known for decades

Technologies to recover it were refined as natural gas prices rose to $10 per MMBtu Locations of shale gas were known for decades Discovery rates are very high Reduces producer expenses Volume was greatly

Technologies to recover it were refined as natural gas prices rose to $10 per MMBtu Locations of shale gas were known for decades Discovery rates are very high Reduces producer expenses Volume was greatly

Gas s Pipeline to Sustainability:

Gas s Pipeline to Sustainability: An Update on Gas Markets September 28, 2017 An INDEPENDENT energy consulting company since 1996 No affiliation with any marketer, broker, agent, utility, pipeline or producer

Gas s Pipeline to Sustainability: An Update on Gas Markets September 28, 2017 An INDEPENDENT energy consulting company since 1996 No affiliation with any marketer, broker, agent, utility, pipeline or producer

UNDERSTANDING NATURAL GAS MARKETS. Mohammad Naserifard MSc student of Oil & Gas Economics at PUT Fall 2015

UNDERSTANDING NATURAL GAS MARKETS Mohammad Naserifard MSc student of Oil & Gas Economics at PUT Fall 2015 Table of Contents 3 Overview Natural Gas is an Important Source of Energy for the United States.

UNDERSTANDING NATURAL GAS MARKETS Mohammad Naserifard MSc student of Oil & Gas Economics at PUT Fall 2015 Table of Contents 3 Overview Natural Gas is an Important Source of Energy for the United States.

Natural Gas Price Dynamics. Insight to Emerging Trends

Natural Gas Price Dynamics Insight to Emerging Trends January 13, 2011 Natural Gas Price Dynamics Insight to Emerging Trends o o o o Who is Gavilon? History of Natural Gas What Drives Pricing? a. Weather

Natural Gas Price Dynamics Insight to Emerging Trends January 13, 2011 Natural Gas Price Dynamics Insight to Emerging Trends o o o o Who is Gavilon? History of Natural Gas What Drives Pricing? a. Weather

CenterPoint Energy Services. Current Market Fundamentals June 27, 2013

CenterPoint Energy Services Current Market Fundamentals June 27, 2013 CenterPoint Energy is one of the largest combined electric and natural gas delivery companies in the U.S. Asset portfolio CNP Footprint

CenterPoint Energy Services Current Market Fundamentals June 27, 2013 CenterPoint Energy is one of the largest combined electric and natural gas delivery companies in the U.S. Asset portfolio CNP Footprint

Short Term Energy Outlook March 2011 March 8, 2011 Release

Short Term Energy Outlook March 2011 March 8, 2011 Release Highlights West Texas Intermediate (WTI) and other crude oil spot prices have risen about $15 per barrel since mid February partly in response

Short Term Energy Outlook March 2011 March 8, 2011 Release Highlights West Texas Intermediate (WTI) and other crude oil spot prices have risen about $15 per barrel since mid February partly in response

MARKET COMMENTARY. Energy and Sustainability Solutions Energy Market Roundup. North America. November 20, 2014 MARKET FUNDAMENTALS OIL PRICE UPDATE

PRICING As unseasonably cold weather and early season snowstorms have blanketed much of the Midwest and Northeast, and natural gas market volatility has reacted predictably. Volatility in the prompt month

PRICING As unseasonably cold weather and early season snowstorms have blanketed much of the Midwest and Northeast, and natural gas market volatility has reacted predictably. Volatility in the prompt month

October U.S. Energy Information Administration Winter Fuels Outlook October

October 2017 Winter Fuels Outlook EIA forecasts that average household expenditures for all major home heating fuels will rise this winter because of expected colder weather and higher energy costs. Average

October 2017 Winter Fuels Outlook EIA forecasts that average household expenditures for all major home heating fuels will rise this winter because of expected colder weather and higher energy costs. Average

Greg Hathaway Energy Source Holdings, LLC

Greg Hathaway Energy Source Holdings, LLC WEATHER THE PICTURE TO THE RIGHT SHOWS THE 2015-16 WINTER HAS BEEN MUCH ABOVE NORMAL. SINCE 2008 THE NATIONAL TEMPERATURE HAS BEEN BELOW NORMAL SIX TIMES 2013-14

Greg Hathaway Energy Source Holdings, LLC WEATHER THE PICTURE TO THE RIGHT SHOWS THE 2015-16 WINTER HAS BEEN MUCH ABOVE NORMAL. SINCE 2008 THE NATIONAL TEMPERATURE HAS BEEN BELOW NORMAL SIX TIMES 2013-14

AIChE: Natural Gas Utilization Workshop Overcoming Hurdles of Technology Implementation

AIChE: Natural Gas Utilization Workshop Overcoming Hurdles of Technology Implementation Natural Gas in the United States: An Overview of Resources and Factors Affecting the Market November 2, 216 Justin

AIChE: Natural Gas Utilization Workshop Overcoming Hurdles of Technology Implementation Natural Gas in the United States: An Overview of Resources and Factors Affecting the Market November 2, 216 Justin

EIA Short-Term Energy and Winter Fuels Outlook

EIA Short-Term Energy and Winter Fuels Outlook NASEO 2015 Winter Energy Outlook Conference Washington, DC by Howard Gruenspecht, Deputy Administrator U.S. Energy Information Administration Independent

EIA Short-Term Energy and Winter Fuels Outlook NASEO 2015 Winter Energy Outlook Conference Washington, DC by Howard Gruenspecht, Deputy Administrator U.S. Energy Information Administration Independent

SPECIAL MONTHLY REPORT ON. ENERGY (Aug 2016)

") SPECIAL MONTHLY REPORT ON () PERFORMANCE (July 2016) (% change) NYMEX -13.93-1.37 Natural Gas Crude oil MCX -15.80-2.23-18.00-16.00-14.00-12.00-10.00-8.00-6.00-4.00-2.00 0.00 Source: Reuters & SMC PERFORMANCE

SPECIAL MONTHLY REPORT ON () PERFORMANCE (July 2016) (% change) NYMEX -13.93-1.37 Natural Gas Crude oil MCX -15.80-2.23-18.00-16.00-14.00-12.00-10.00-8.00-6.00-4.00-2.00 0.00 Source: Reuters & SMC PERFORMANCE

October 23, 2018 Harrisburg, PA

Pennsylvania Public Utility Commission Annual Winter Reliability Assessment Terrance J. Fitzpatrick President & Chief Executive Officer Energy Association of Pennsylvania October 23, 2018 Harrisburg, PA

Pennsylvania Public Utility Commission Annual Winter Reliability Assessment Terrance J. Fitzpatrick President & Chief Executive Officer Energy Association of Pennsylvania October 23, 2018 Harrisburg, PA

The Energy Consortium Recent Developments and the Outlook for Natural Gas in the Northeast. John R. Bitler October 20, 2010

The Energy Consortium Recent Developments and the Outlook for Natural Gas in the Northeast John R. Bitler October 20, 2010 Northeast Overview Traditional Sources of Supply Gulf Coast Western Canada (WCSB)

The Energy Consortium Recent Developments and the Outlook for Natural Gas in the Northeast John R. Bitler October 20, 2010 Northeast Overview Traditional Sources of Supply Gulf Coast Western Canada (WCSB)

ENERGY SLIDESHOW. Federal Reserve Bank of Dallas

ENERGY SLIDESHOW Updated: July 5, 2018 ENERGY PRICES www.dallasfed.org/research/energy Brent & WTI & Crude Brent Oil Crude Oil Dollars per barrel 140 120 Brent (Jun 29 = $75.24) WTI (Jun 29 = $74.03) 95%

ENERGY SLIDESHOW Updated: July 5, 2018 ENERGY PRICES www.dallasfed.org/research/energy Brent & WTI & Crude Brent Oil Crude Oil Dollars per barrel 140 120 Brent (Jun 29 = $75.24) WTI (Jun 29 = $74.03) 95%

ENERGY SLIDESHOW. Federal Reserve Bank of Dallas

ENERGY SLIDESHOW Updated: February 14, 2018 ENERGY PRICES www.dallasfed.org/research/energy Brent & WTI & Crude Brent Oil Crude Oil Dollars per barrel 140 Brent (Feb 9 = $65.50) WTI (Feb 9 = $62.01) 120

ENERGY SLIDESHOW Updated: February 14, 2018 ENERGY PRICES www.dallasfed.org/research/energy Brent & WTI & Crude Brent Oil Crude Oil Dollars per barrel 140 Brent (Feb 9 = $65.50) WTI (Feb 9 = $62.01) 120

2012 NATURAL GAS MARKET OUTLOOK

2012 NATURAL GAS MARKET OUTLOOK Marjorie Schmidt-Pines, Principal Regulatory Economic Advisor Southern California Gas Company and SDG&E Regulatory Affairs January, 2012 This information is provided solely

2012 NATURAL GAS MARKET OUTLOOK Marjorie Schmidt-Pines, Principal Regulatory Economic Advisor Southern California Gas Company and SDG&E Regulatory Affairs January, 2012 This information is provided solely

North American Midstream Infrastructure Through 2035 A Secure Energy Future. Press Briefing June 28, 2011

North American Midstream Infrastructure Through 2035 A Secure Energy Future Press Briefing June 28, 2011 Disclaimer This presentation presents views of ICF International and the INGAA Foundation. The presentation

North American Midstream Infrastructure Through 2035 A Secure Energy Future Press Briefing June 28, 2011 Disclaimer This presentation presents views of ICF International and the INGAA Foundation. The presentation

Ponzi Scheme Keeps US Market Well Supplied

www.poten.com June 30, 2011 Ponzi Scheme Keeps US Market Well Supplied Conjuring up images of the dot-com bubble of the late-1990s, the industry leveled charges of unprofessional journalism against a story

www.poten.com June 30, 2011 Ponzi Scheme Keeps US Market Well Supplied Conjuring up images of the dot-com bubble of the late-1990s, the industry leveled charges of unprofessional journalism against a story

Overview of Florida s s Regulatory Environment

Overview of Florida s s Regulatory Environment October 21 st, 2011 Eduardo Balbis, P.E. Commissioner Florida Public Service Commission Florida Public Service Commission Gubernatorial Appointees Confirmed

Overview of Florida s s Regulatory Environment October 21 st, 2011 Eduardo Balbis, P.E. Commissioner Florida Public Service Commission Florida Public Service Commission Gubernatorial Appointees Confirmed

Shale Gas as an Alternative Petrochemical Feedstock

Shale Gas as an Alternative Petrochemical Feedstock Tecnon OrbiChem Seminar at KICHEM 2012 Seoul - 2 November, 2012 Roger Lee SHALE GAS WHERE DOES IT COME FROM? Source: EIA SHALE GAS EXPLOITATION Commercial

Shale Gas as an Alternative Petrochemical Feedstock Tecnon OrbiChem Seminar at KICHEM 2012 Seoul - 2 November, 2012 Roger Lee SHALE GAS WHERE DOES IT COME FROM? Source: EIA SHALE GAS EXPLOITATION Commercial

ENERGY OUTLOOK 2017 FALL/WINTER

ENERGY OUTLOOK 2017 FALL/WINTER With more than 105 years in the energy industry, BOK Financial is committed to helping you succeed. In this issue of the Energy Outlook, you ll learn more about the current

ENERGY OUTLOOK 2017 FALL/WINTER With more than 105 years in the energy industry, BOK Financial is committed to helping you succeed. In this issue of the Energy Outlook, you ll learn more about the current

Trends, Issues and Market Changes for Crude Oil and Natural Gas

Trends, Issues and Market Changes for Crude Oil and Natural Gas East Iberville Community Advisory Panel Meeting Syngenta September 26, 2012 Center for Energy Studies David E. Dismukes, Ph.D. Center for

Trends, Issues and Market Changes for Crude Oil and Natural Gas East Iberville Community Advisory Panel Meeting Syngenta September 26, 2012 Center for Energy Studies David E. Dismukes, Ph.D. Center for

Markets and Opportunities. Paul Burgener March 2015

Markets and Opportunities Paul Burgener March 2015 Disclaimer Copyright BP Energy Company. All rights reserved. Contents of this presentation do not necessarily reflect the Company s views. This presentation

Markets and Opportunities Paul Burgener March 2015 Disclaimer Copyright BP Energy Company. All rights reserved. Contents of this presentation do not necessarily reflect the Company s views. This presentation

Winter U.S. Natural Gas Production and Supply Outlook

Winter 2010-11 U.S. Natural Gas Production and Supply Outlook Prepared for Natural Gas Supply Association by: ICF International Fairfax, Virginia September, 2010 Introduction This report presents ICF s

Winter 2010-11 U.S. Natural Gas Production and Supply Outlook Prepared for Natural Gas Supply Association by: ICF International Fairfax, Virginia September, 2010 Introduction This report presents ICF s

The Shifting Sands of Natural Gas Abundance

August 17, 2016 The Shifting Sands of Natural Gas Abundance Richard Meyer Manager, Energy Analysis & Standards Here s how global energy changed between 2014 and 2015. Winners were oil, natural gas, renewables.

August 17, 2016 The Shifting Sands of Natural Gas Abundance Richard Meyer Manager, Energy Analysis & Standards Here s how global energy changed between 2014 and 2015. Winners were oil, natural gas, renewables.

Five Things You Should Know

Bureau of Economic Geology, Jackson School of Geosciences, The University of Texas at Austin Five Things You Should Know Tx Industries of the Future, March 7, 2013 M.M. Foss, 9/25/2012, BEG/CEE-UT, 1 #1

Bureau of Economic Geology, Jackson School of Geosciences, The University of Texas at Austin Five Things You Should Know Tx Industries of the Future, March 7, 2013 M.M. Foss, 9/25/2012, BEG/CEE-UT, 1 #1

Wood Mackenzie Gas Market Outlook

Wood Mackenzie Gas Market Outlook Southern Gas Association April 20, 2009 Amber McCullagh Short-Term Outlook 2008 markets were volatile as underlying fundamentals shifted rapidly Three primary phases:

Wood Mackenzie Gas Market Outlook Southern Gas Association April 20, 2009 Amber McCullagh Short-Term Outlook 2008 markets were volatile as underlying fundamentals shifted rapidly Three primary phases:

The Top Natural Gas Players In ExxonMobil restarts second PNG LNG train; resumes export

Apr-17 May-17 Jun-17 Jul-17 Aug-17 Sep-17 Oct-17 Nov-17 Dec-17 Jan-18 Feb-18 Mar-18 Apr-18 8: 8:45 9:3 1:15 11: 11:45 12:3 13:15 14: Prior Day s NYMEX May-18 Contract (CT) 2.82 2.81 2.8 2.79 2.78 2.77

Apr-17 May-17 Jun-17 Jul-17 Aug-17 Sep-17 Oct-17 Nov-17 Dec-17 Jan-18 Feb-18 Mar-18 Apr-18 8: 8:45 9:3 1:15 11: 11:45 12:3 13:15 14: Prior Day s NYMEX May-18 Contract (CT) 2.82 2.81 2.8 2.79 2.78 2.77

Natural Gas Issues and Emerging Trends for the Upcoming Winter and Beyond

Natural Gas Issues and Emerging Trends for the Upcoming Winter and Beyond 2013 NASEO WINTER ENERGY OUTLOOK CONFERENCE November 1, 2013 Kevin Petak Vice President, ICF International Kevin.Petak@icfi.com

Natural Gas Issues and Emerging Trends for the Upcoming Winter and Beyond 2013 NASEO WINTER ENERGY OUTLOOK CONFERENCE November 1, 2013 Kevin Petak Vice President, ICF International Kevin.Petak@icfi.com

The New Superpower : Emerging Supplies of Gas Liquids from the United States

The New Superpower : Emerging Supplies of Gas Liquids from the United States Lucian Pugliaresi President Energy Policy Research Foundation, Inc. Washington, DC Energy Policy Research Foundation, Inc. 1031

The New Superpower : Emerging Supplies of Gas Liquids from the United States Lucian Pugliaresi President Energy Policy Research Foundation, Inc. Washington, DC Energy Policy Research Foundation, Inc. 1031

Energy Market Outlook

Kyle Cooper, (713) 248-3009, Kyle.Cooper@iafadvisors.com Week Ending August 3, 2018 Please contact me to review a joint RBN Energy daily publication detailing natural gas fundamentals. Price Action: The

Kyle Cooper, (713) 248-3009, Kyle.Cooper@iafadvisors.com Week Ending August 3, 2018 Please contact me to review a joint RBN Energy daily publication detailing natural gas fundamentals. Price Action: The

Platts Natural Gas Storage Conference. January 2012

Platts Natural Gas Storage Conference January 2012 Changing Storage Landscape Tremendous development and expansion in last 10 years has created excess capacity in the Natural Gas Storage Sector Majority

Platts Natural Gas Storage Conference January 2012 Changing Storage Landscape Tremendous development and expansion in last 10 years has created excess capacity in the Natural Gas Storage Sector Majority

[LNG MARKET ANALYSIS ] 1. LNG Market Analysis

![[LNG MARKET ANALYSIS ] 1. LNG Market Analysis](/thumbs/82/85327793.jpg "[LNG MARKET ANALYSIS ] 1. LNG Market Analysis") [LNG MARKET ANALYSIS ] 1 LNG Market Analysis LNG Market Analysis Volume: 6 th April 2018 [LNG MARKET ANALYSIS ] 2 LNG and Natural Gas Price Assessment 26 th March 6 th April 2018 LNG Analysis Global LNG

[LNG MARKET ANALYSIS ] 1 LNG Market Analysis LNG Market Analysis Volume: 6 th April 2018 [LNG MARKET ANALYSIS ] 2 LNG and Natural Gas Price Assessment 26 th March 6 th April 2018 LNG Analysis Global LNG

ExxonMobil Resumes Liquefied Natural Gas Production in Papua New Guinea Commodities - Natural Gas Futures Turn Higher After Storage

Apr-17 May-17 Jun-17 Jul-17 Aug-17 Sep-17 Oct-17 Nov-17 Dec-17 Jan-18 Feb-18 Mar-18 Apr-18 8: 8:45 9:3 1:15 11: 11:45 12:3 13:15 14: Prior Day s NYMEX Jan-18 Contract (CT) 2.71 2.7 2.69 2.68 2.67 2.66

Apr-17 May-17 Jun-17 Jul-17 Aug-17 Sep-17 Oct-17 Nov-17 Dec-17 Jan-18 Feb-18 Mar-18 Apr-18 8: 8:45 9:3 1:15 11: 11:45 12:3 13:15 14: Prior Day s NYMEX Jan-18 Contract (CT) 2.71 2.7 2.69 2.68 2.67 2.66

The Really Big Game Changer: Crude Oil Production from Shale Resources and the Tuscaloosa Marine Shale

The Really Big Game Changer: Crude Oil Production from Shale Resources and the Tuscaloosa Marine Shale Baton Rouge Chamber of Commerce Regional Stakeholders Breakfast June 27, 2012 Center for Energy Studies

The Really Big Game Changer: Crude Oil Production from Shale Resources and the Tuscaloosa Marine Shale Baton Rouge Chamber of Commerce Regional Stakeholders Breakfast June 27, 2012 Center for Energy Studies

2005 North American Natural Gas Outlook Client Presentation

2005 North American Natural Gas Outlook Client Presentation January 17, 2005 Ron Denhardt Vice President, Natural Gas Services Strategic Energy & Economic Research Inc. 781 756 0550 (Tel) Copyright 2004

2005 North American Natural Gas Outlook Client Presentation January 17, 2005 Ron Denhardt Vice President, Natural Gas Services Strategic Energy & Economic Research Inc. 781 756 0550 (Tel) Copyright 2004

Winter U.S. Natural Gas Production and Supply Outlook

Winter 2012-13 U.S. Natural Gas Production and Supply Outlook Prepared for Natural Gas Supply Association by: ICF International Fairfax, Virginia September, 2012 Introduction This report presents ICF s

Winter 2012-13 U.S. Natural Gas Production and Supply Outlook Prepared for Natural Gas Supply Association by: ICF International Fairfax, Virginia September, 2012 Introduction This report presents ICF s

Acceptance Natural Gas Demand to Stay High on Cold Weather Forecast

Mar-17 Apr-17 May-17 Jun-17 Jul-17 Aug-17 Sep-17 Oct-17 Nov-17 Dec-17 Jan-18 Feb-18 Mar-18 8: 8:45 9:3 1:15 11: 11:45 12:3 13:15 14: Prior Day s NYMEX Jan-18 Contract (CT) 2.68 2.67 2.66 2.65 2.64 2.63

Mar-17 Apr-17 May-17 Jun-17 Jul-17 Aug-17 Sep-17 Oct-17 Nov-17 Dec-17 Jan-18 Feb-18 Mar-18 8: 8:45 9:3 1:15 11: 11:45 12:3 13:15 14: Prior Day s NYMEX Jan-18 Contract (CT) 2.68 2.67 2.66 2.65 2.64 2.63

Energy Markets. U.S. Energy Information Administration. for Center on Global Energy Policy, Columbia University November 20, 2015 New York, New York

Energy Markets for Center on Global Energy Policy, Columbia University New York, New York by Adam Sieminski, Administrator U.S. Energy Information Administration U.S. Energy Information Administration

Energy Markets for Center on Global Energy Policy, Columbia University New York, New York by Adam Sieminski, Administrator U.S. Energy Information Administration U.S. Energy Information Administration

Industrial Energy Consumers of America The Voice of the Industrial Energy Consumers WHY MANUFACTURERS ARE CONCERNED ABOUT UNFETTERED LNG EXPORTS

The Voice of the Industrial Energy Consumers 1776 K Street, NW, Suite 720 Washington, D.C. 20006 Telephone (202) 223-1420 www.ieca-us.org June 19, 2014 WHY MANUFACTURERS ARE CONCERNED ABOUT UNFETTERED

The Voice of the Industrial Energy Consumers 1776 K Street, NW, Suite 720 Washington, D.C. 20006 Telephone (202) 223-1420 www.ieca-us.org June 19, 2014 WHY MANUFACTURERS ARE CONCERNED ABOUT UNFETTERED

Background, Issues, and Trends in Underground Hydrocarbon Storage

Background, Issues, and Trends in Underground Hydrocarbon Storage David E. Dismukes Center for Energy Studies Louisiana State University Environmental Permitting Class January 29, 2009 Description of the

Background, Issues, and Trends in Underground Hydrocarbon Storage David E. Dismukes Center for Energy Studies Louisiana State University Environmental Permitting Class January 29, 2009 Description of the

Outlook for Natural Gas Demand for Winter

Outlook for Natural Gas Demand for 2010-2011 Winter Energy Ventures Analysis, Inc. (EVA) Overview Natural gas demand this winter is projected to be about 295 BCF, or 2.5 percent, above demand levels recorded

Outlook for Natural Gas Demand for 2010-2011 Winter Energy Ventures Analysis, Inc. (EVA) Overview Natural gas demand this winter is projected to be about 295 BCF, or 2.5 percent, above demand levels recorded

NATURAL GAS 101 THE BASICS OF NATURAL GAS

NATURAL GAS 101 THE BASICS OF NATURAL GAS April 25, 2014 Natural Gas Basics What is natural gas? Natural gas is a fossil fuel composed primarily of methane, and other hydrocarbons such as ethane, butane

NATURAL GAS 101 THE BASICS OF NATURAL GAS April 25, 2014 Natural Gas Basics What is natural gas? Natural gas is a fossil fuel composed primarily of methane, and other hydrocarbons such as ethane, butane

Short-Term Energy Outlook (STEO)

") May 2013 Short-Term Energy Outlook (STEO) Highlights Falling crude oil prices contributed to a decline in the U.S. regular gasoline retail price from a year to date high of $3.78 per gallon on February

May 2013 Short-Term Energy Outlook (STEO) Highlights Falling crude oil prices contributed to a decline in the U.S. regular gasoline retail price from a year to date high of $3.78 per gallon on February

Energy Markets. U.S. Energy Information Administration. for. October 29, 2015 Golden, Colorado. by Adam Sieminski, Administrator

Energy Markets for The Payne Institute for Earth Resources at the Colorado School of Mines Golden, Colorado by Adam Sieminski, Administrator U.S. Energy Information Administration U.S. Energy Information

Energy Markets for The Payne Institute for Earth Resources at the Colorado School of Mines Golden, Colorado by Adam Sieminski, Administrator U.S. Energy Information Administration U.S. Energy Information

EIA Winter Fuels Outlook

EIA 2018 19 Winter Fuels Outlook U.S. Energy Information Administration Independent Statistics & Analysis www.eia.gov The main determinants of winter heating fuels expenditures are temperatures and prices

EIA 2018 19 Winter Fuels Outlook U.S. Energy Information Administration Independent Statistics & Analysis www.eia.gov The main determinants of winter heating fuels expenditures are temperatures and prices

Oil and gas outlook. For New York Energy Forum October 15, 2015 New York, NY. By Adam Sieminski, Administrator. U.S. Energy Information Administration

Oil and gas outlook For New York Energy Forum New York, NY By Adam Sieminski, Administrator U.S. Energy Information Administration U.S. Energy Information Administration Independent Statistics & Analysis

Oil and gas outlook For New York Energy Forum New York, NY By Adam Sieminski, Administrator U.S. Energy Information Administration U.S. Energy Information Administration Independent Statistics & Analysis

EIA Short-Term Energy and

EIA Short-Term Energy and Winter Fuels Outlook Washington, DC U.S. Energy Information Administration Independent Statistics & Analysis www.eia.gov Overview EIA expects higher average fuel bills this winter

EIA Short-Term Energy and Winter Fuels Outlook Washington, DC U.S. Energy Information Administration Independent Statistics & Analysis www.eia.gov Overview EIA expects higher average fuel bills this winter

Global energy markets

For Woodrow Wilson Center Global Energy Forum September 21, 215 Washington, DC by Adam Sieminski, Administrator U.S. Energy Information Administration U.S. Energy Information Administration Independent

For Woodrow Wilson Center Global Energy Forum September 21, 215 Washington, DC by Adam Sieminski, Administrator U.S. Energy Information Administration U.S. Energy Information Administration Independent

The Impact of Developing Energy and Environmental Policy on the Gas Industry Plus Impacts of the Current Economic State

The Impact of Developing Energy and Environmental Policy on the Gas Industry Plus Impacts of the Current Economic State Gas / Electric Partnership Conference XVII Gas Compression from Production thru Transmission

The Impact of Developing Energy and Environmental Policy on the Gas Industry Plus Impacts of the Current Economic State Gas / Electric Partnership Conference XVII Gas Compression from Production thru Transmission

Navigating through the energy landscape.

Navigating through the energy landscape. Baton Rouge Rotary Club Luncheon, May 24, 2017. David E. Dismukes, Ph.D. Executive Director & Professor Center for Energy Studies Louisiana State University Professor

Navigating through the energy landscape. Baton Rouge Rotary Club Luncheon, May 24, 2017. David E. Dismukes, Ph.D. Executive Director & Professor Center for Energy Studies Louisiana State University Professor

EIA Short-Term and Winter Fuels Outlook

EIA Short-Term and Winter Fuels Outlook New York Energy Forum October 18, 21 New York, NY Richard Newell, Administrator U.S. Energy Information Administration Richard Newell, New York Energy Forum, October

EIA Short-Term and Winter Fuels Outlook New York Energy Forum October 18, 21 New York, NY Richard Newell, Administrator U.S. Energy Information Administration Richard Newell, New York Energy Forum, October

Energy Market Outlook

Kyle Cooper, (713) 248-3009, Kyle.Cooper@iafadvisors.com Week Ending September 7, 2018 Please contact me to review a joint RBN Energy daily publication detailing natural gas fundamentals. Price Action:

Kyle Cooper, (713) 248-3009, Kyle.Cooper@iafadvisors.com Week Ending September 7, 2018 Please contact me to review a joint RBN Energy daily publication detailing natural gas fundamentals. Price Action:

Energy Market Outlook

Kyle Cooper, (713) 248-3009, Kyle.Cooper@iafadvisors.com Week Ending November 23, 2018 Please contact me to review a joint RBN Energy daily publication detailing natural gas fundamentals. Price Action:

Kyle Cooper, (713) 248-3009, Kyle.Cooper@iafadvisors.com Week Ending November 23, 2018 Please contact me to review a joint RBN Energy daily publication detailing natural gas fundamentals. Price Action:

2010 Annual Winter Reliability Assessment Meeting November 4, Carlos Thillet Manager Gas Supply and Transportation PECO Energy Company

Pennsylvania Public Utility Commission 2010 Annual Winter Reliability Assessment Meeting November 4, 2010 Carlos Thillet Manager Gas Supply and Transportation PECO Energy Company 2010-11 Reliability Overview

Pennsylvania Public Utility Commission 2010 Annual Winter Reliability Assessment Meeting November 4, 2010 Carlos Thillet Manager Gas Supply and Transportation PECO Energy Company 2010-11 Reliability Overview

U.S. Crude Oil and Natural Gas Proved Reserves, Year-end 2016

U.S. Crude Oil and Natural Gas Proved Reserves, Year-end 2016 February 2018 Independent Statistics & Analysis www.eia.gov U.S. Department of Energy Washington, DC 20585 This report was prepared by the

U.S. Crude Oil and Natural Gas Proved Reserves, Year-end 2016 February 2018 Independent Statistics & Analysis www.eia.gov U.S. Department of Energy Washington, DC 20585 This report was prepared by the

EIA Winter Fuels Outlook

EIA Winter Fuels Outlook For Washington, D.C. By Adam Sieminski, Administrator, U.S. Energy Information Administration U.S. Energy Information Administration Independent Statistics & Analysis www.eia.gov

EIA Winter Fuels Outlook For Washington, D.C. By Adam Sieminski, Administrator, U.S. Energy Information Administration U.S. Energy Information Administration Independent Statistics & Analysis www.eia.gov

Energy Market Outlook

Kyle Cooper, (713) 248-3009, Kyle.Cooper@iafadvisors.com Week Ending August 31, 2018 Please contact me to review a joint RBN Energy daily publication detailing natural gas fundamentals. Price Action: The

Kyle Cooper, (713) 248-3009, Kyle.Cooper@iafadvisors.com Week Ending August 31, 2018 Please contact me to review a joint RBN Energy daily publication detailing natural gas fundamentals. Price Action: The

Natural Gas Market Update

Natural Gas Market Update John Jicha - MGE Director - Energy Supply and Trading Madison Gas and Electric Company Agenda What a difference ten years can make Low prices Fundamental factors impacting the

Natural Gas Market Update John Jicha - MGE Director - Energy Supply and Trading Madison Gas and Electric Company Agenda What a difference ten years can make Low prices Fundamental factors impacting the

Energy Market Outlook

Kyle Cooper, (713) 248-3009, Kyle.Cooper@iafadvisors.com Week Ending December 28, 2018 Please contact me to review a joint RBN Energy daily publication detailing natural gas fundamentals. Price Action:

Kyle Cooper, (713) 248-3009, Kyle.Cooper@iafadvisors.com Week Ending December 28, 2018 Please contact me to review a joint RBN Energy daily publication detailing natural gas fundamentals. Price Action:

Energy Availability and the Future of the Fertilizer Industry. Rayola Dougher API Senior Economic Advisor

Energy Availability and the Future of the Fertilizer Industry Rayola Dougher API Senior Economic Advisor dougherr@api.org Energy: the engine of our economic growth 1974 1980 1986 1992 1998 2004 2010 2016

Energy Availability and the Future of the Fertilizer Industry Rayola Dougher API Senior Economic Advisor dougherr@api.org Energy: the engine of our economic growth 1974 1980 1986 1992 1998 2004 2010 2016

Short-Term Energy and Summer Fuels Outlook (STEO)

") April 2013 Short-Term Energy and Summer Fuels Outlook (STEO) Highlights During the April through September summer driving season this year, regular gasoline retail prices are forecast to average $3.63

April 2013 Short-Term Energy and Summer Fuels Outlook (STEO) Highlights During the April through September summer driving season this year, regular gasoline retail prices are forecast to average $3.63

UNDERSTANDING NATURAL GAS MARKETS

UNDERSTANDING NATURAL GAS MARKETS Table of Contents PREVIEW Overview... 2 The North American Natural Gas Marketplace... 4 Natural Gas Supply... 8 Natural Gas Demand... 12 Natural Gas Exports... 15 How

UNDERSTANDING NATURAL GAS MARKETS Table of Contents PREVIEW Overview... 2 The North American Natural Gas Marketplace... 4 Natural Gas Supply... 8 Natural Gas Demand... 12 Natural Gas Exports... 15 How

Energy Market Outlook

Kyle Cooper, (713) 248-3009, Kyle.Cooper@iafadvisors.com Week Ending September 21, 2018 Please contact me to review a joint RBN Energy daily publication detailing natural gas fundamentals. Price Action:

Kyle Cooper, (713) 248-3009, Kyle.Cooper@iafadvisors.com Week Ending September 21, 2018 Please contact me to review a joint RBN Energy daily publication detailing natural gas fundamentals. Price Action:

Energy Market Outlook

Kyle Cooper, (713) 248-3009, Kyle.Cooper@iafadvisors.com Week Ending September 14, 2018 Please contact me to review a joint RBN Energy daily publication detailing natural gas fundamentals. Price Action:

Kyle Cooper, (713) 248-3009, Kyle.Cooper@iafadvisors.com Week Ending September 14, 2018 Please contact me to review a joint RBN Energy daily publication detailing natural gas fundamentals. Price Action:

Energy Market Outlook

Kyle Cooper, (713) 248-3009, Kyle.Cooper@iafadvisors.com Week Ending April 12, 2019 Please contact me to review a joint RBN Energy daily publication detailing natural gas fundamentals. Price Action: The

Kyle Cooper, (713) 248-3009, Kyle.Cooper@iafadvisors.com Week Ending April 12, 2019 Please contact me to review a joint RBN Energy daily publication detailing natural gas fundamentals. Price Action: The

Short-Term Energy Outlook and Winter Fuels Outlook

Short-Term Energy Outlook and Winter Fuels Outlook For NASEO Winter Fuels Outlook Conference Washington, DC By Adam Sieminski, Administrator U.S. Energy Information Administration Independent Statistics

Short-Term Energy Outlook and Winter Fuels Outlook For NASEO Winter Fuels Outlook Conference Washington, DC By Adam Sieminski, Administrator U.S. Energy Information Administration Independent Statistics

Energy Market Outlook

Kyle Cooper, (713) 248-3009, Kyle.Cooper@iafadvisors.com Week Ending November 24, 2017 Please contact me to review a joint RBN Energy daily publication detailing natural gas fundamentals. Price Action:

Kyle Cooper, (713) 248-3009, Kyle.Cooper@iafadvisors.com Week Ending November 24, 2017 Please contact me to review a joint RBN Energy daily publication detailing natural gas fundamentals. Price Action:

$40 Billion Ichthys LNG Project Begins Gas Exports US' Range Resources to fill Rover gas pipeline volumes by yearend; processing ramps up

Oct-17 Nov-17 Dec-17 Jan-18 Feb-18 Mar-18 Apr-18 May-18 Jun-18 Jul-18 Aug-18 Sep-18 Oct-18 8: 8:45 9:3 1:15 11: 11:45 12:3 13:15 14: O C T O B E R 2 5, 2 1 8 3.26 3.24 3.22 3.2 3.18 3.16 3.14 3.12 3.1

Oct-17 Nov-17 Dec-17 Jan-18 Feb-18 Mar-18 Apr-18 May-18 Jun-18 Jul-18 Aug-18 Sep-18 Oct-18 8: 8:45 9:3 1:15 11: 11:45 12:3 13:15 14: O C T O B E R 2 5, 2 1 8 3.26 3.24 3.22 3.2 3.18 3.16 3.14 3.12 3.1

Energy Market Update. April 8, Kevin Krcil Chris Dubay

Energy Market Update April 8, 2014 Kevin Krcil Chris Dubay Winter 2013-14 Review and Brief Look at Summer 2014 Kevin Krcil, Head of Weather Trading Agenda Winter 2013-14 Review Outcome Polar Vortex Specific

Energy Market Update April 8, 2014 Kevin Krcil Chris Dubay Winter 2013-14 Review and Brief Look at Summer 2014 Kevin Krcil, Head of Weather Trading Agenda Winter 2013-14 Review Outcome Polar Vortex Specific

WEEKLY MARKET UPDATE

WEEKLY MARKET UPDATE Weekly Summary: The U.S. Energy Information Administration reported last week that natural gas storage decreased by 183 Bcf. The withdrawal for the same week last year was 230 Bcf

WEEKLY MARKET UPDATE Weekly Summary: The U.S. Energy Information Administration reported last week that natural gas storage decreased by 183 Bcf. The withdrawal for the same week last year was 230 Bcf

Natural Gas. Tuesday, May 1, 2012; 4:00 PM 5:15 PM

Natural Gas Tuesday, May 1, 2012; 4:00 PM 5:15 PM Moderator: Joel Kurtzman, Senior Fellow and Executive Director of the Center for Accelerating Energy Solutions, Milken Institute Speakers: Ralph Eads,

Natural Gas Tuesday, May 1, 2012; 4:00 PM 5:15 PM Moderator: Joel Kurtzman, Senior Fellow and Executive Director of the Center for Accelerating Energy Solutions, Milken Institute Speakers: Ralph Eads,

Short-Term Energy Outlook

May 2012 Short-Term Energy Outlook Highlights EIA s current forecast of the average U.S. refiner acquisition cost of crude oil in 2012 is $110 per barrel, which is $2.50 per barrel lower than in last month

May 2012 Short-Term Energy Outlook Highlights EIA s current forecast of the average U.S. refiner acquisition cost of crude oil in 2012 is $110 per barrel, which is $2.50 per barrel lower than in last month

Electricity Price Outlook for December By John Howley Senior Economist

Jan-18 Feb-18 Mar-18 Apr-18 May-18 Jun-18 Jul-18 Aug-18 Sep-18 Oct-18 Nov-18 Dec-18 Electricity Price Outlook for December 2017 By John Howley Senior Economist Office of Technical and Regulatory Analysis

Jan-18 Feb-18 Mar-18 Apr-18 May-18 Jun-18 Jul-18 Aug-18 Sep-18 Oct-18 Nov-18 Dec-18 Electricity Price Outlook for December 2017 By John Howley Senior Economist Office of Technical and Regulatory Analysis

IMGA Annual Meeting- NG Fundamentals Update. March 28, 2017

IMGA Annual Meeting- NG Fundamentals Update Presenter Trevor Cooper Name / Date March 28, 2017 Disclaimer Copyright. All rights reserved. Contents of this presentation do not necessarily reflect the Company

IMGA Annual Meeting- NG Fundamentals Update Presenter Trevor Cooper Name / Date March 28, 2017 Disclaimer Copyright. All rights reserved. Contents of this presentation do not necessarily reflect the Company

NYMEX UPDATE BULLS & BEARS REPORT

June 30, 2016 NYMEX UPDATE BULLS & BEARS REPORT Author MATTHEW MATTINGLY Energy Analyst / Louisville Ph: 502-895-7882 Author JASON SCARBROUGH VP Risk Management / Houston Ph: 713-899-3639 INTRODUCTION

June 30, 2016 NYMEX UPDATE BULLS & BEARS REPORT Author MATTHEW MATTINGLY Energy Analyst / Louisville Ph: 502-895-7882 Author JASON SCARBROUGH VP Risk Management / Houston Ph: 713-899-3639 INTRODUCTION

What s Going on With Energy? How Unconventional Oil & Gas Development is Impacting Renewables, Efficiency, Power Markets and All That Other Stuff

What s Going on With Energy? How Unconventional Oil & Gas Development is Impacting Renewables, Efficiency, Power Markets and All That Other Stuff Atlanta Economics Club Monthly Meeting December 10, 2012

What s Going on With Energy? How Unconventional Oil & Gas Development is Impacting Renewables, Efficiency, Power Markets and All That Other Stuff Atlanta Economics Club Monthly Meeting December 10, 2012

Energy Market Outlook

Kyle Cooper, (713) 248-3009, Kyle.Cooper@iafadvisors.com Week Ending January 25, 2019 Please contact me to review a joint RBN Energy daily publication detailing natural gas fundamentals. Price Action:

Kyle Cooper, (713) 248-3009, Kyle.Cooper@iafadvisors.com Week Ending January 25, 2019 Please contact me to review a joint RBN Energy daily publication detailing natural gas fundamentals. Price Action:

STATE OF MICHIGAN BEFORE THE MICHIGAN PUBLIC SERVICE COMMISSION

STATE OF MICHIGAN BEFORE THE MICHIGAN PUBLIC SERVICE COMMISSION In the matter of the Application of ) DTE ELECTRIC COMPANY for ) approval of Certificates of Necessity ) pursuant to MCL 460.6s, as amended,

STATE OF MICHIGAN BEFORE THE MICHIGAN PUBLIC SERVICE COMMISSION In the matter of the Application of ) DTE ELECTRIC COMPANY for ) approval of Certificates of Necessity ) pursuant to MCL 460.6s, as amended,

Forward Looking Statements This presentation contains certain statements that are, or may be deemed to be, forward looking statements within the meani

Outlook for U.S. LNG Exports METI, Japan LNG Producer Consumer Conference Charif Souki CEO, Cheniere Energy Inc. Forward Looking Statements This presentation contains certain statements that are, or may

Outlook for U.S. LNG Exports METI, Japan LNG Producer Consumer Conference Charif Souki CEO, Cheniere Energy Inc. Forward Looking Statements This presentation contains certain statements that are, or may

U.S. Crude Oil, Natural Gas, and NG Liquids Proved Reserves

1 of 5 3/14/2013 11:37 PM U.S. Crude Oil, Natural Gas, and NG Liquids Proved Reserves With Data for Release Date: August 1, 2012 Next Release Date: March 2013 Previous Issues: Year: Summary Proved reserves

1 of 5 3/14/2013 11:37 PM U.S. Crude Oil, Natural Gas, and NG Liquids Proved Reserves With Data for Release Date: August 1, 2012 Next Release Date: March 2013 Previous Issues: Year: Summary Proved reserves

Quarterly Energy Comment

Quarterly Energy Comment By Bill O Grady December 15, 2017 The Market Oil prices have recovered strongly from the mid-summer lows. It appears we are establishing a new trading range between $55 and $60

Quarterly Energy Comment By Bill O Grady December 15, 2017 The Market Oil prices have recovered strongly from the mid-summer lows. It appears we are establishing a new trading range between $55 and $60

Texas Natural Gas Prices Plunge To All-Time Low Column: U.S. natural gas prices unmoved by colder winter, low

2.69 2.69 2.68 2.68 2.67 2.67 2.66 2.66 2.65 2.65 2.64 Prior Day s NYMEX MAY-19 Contract (CT) 8: 8:45 9:3 1:15 11: 11:45 12:3 13:15 Apr-18 May-18 Jun-18 Jul-18 Aug-18 Sep-18 Oct-18 Nov-18 Dec-18 Jan-19

2.69 2.69 2.68 2.68 2.67 2.67 2.66 2.66 2.65 2.65 2.64 Prior Day s NYMEX MAY-19 Contract (CT) 8: 8:45 9:3 1:15 11: 11:45 12:3 13:15 Apr-18 May-18 Jun-18 Jul-18 Aug-18 Sep-18 Oct-18 Nov-18 Dec-18 Jan-19

Fortress America. A Resource Rich Island of Stability in a Sea of Turmoil. Presented by Jason Willan Director, Risk Management & Research

Fortress America A Resource Rich Island of Stability in a Sea of Turmoil Presented by Jason Willan Director, Risk Management & Research Disclaimer The data and information contained in this presentation

Fortress America A Resource Rich Island of Stability in a Sea of Turmoil Presented by Jason Willan Director, Risk Management & Research Disclaimer The data and information contained in this presentation

The Outlook for Energy

The Outlook for Energy A View to 23 Flexible Packaging Association March 1 th, 26 Jesse Tyson President, ExxonMobil Inter-America Inc. This presentation includes forward-looking statements. Actual future

The Outlook for Energy A View to 23 Flexible Packaging Association March 1 th, 26 Jesse Tyson President, ExxonMobil Inter-America Inc. This presentation includes forward-looking statements. Actual future

The US shale revolution and its economic impact

The US shale revolution and its economic impact Sylvie Cornot-Gandolphe Groupe Idées, Rueil Malmaison, 16 mars 2015 1 The US shale revolution and its economic impact 1. Shale gas Coal-to-gas switching

The US shale revolution and its economic impact Sylvie Cornot-Gandolphe Groupe Idées, Rueil Malmaison, 16 mars 2015 1 The US shale revolution and its economic impact 1. Shale gas Coal-to-gas switching

IAF Advisors Energy Market Outlook Kyle Cooper, (713) , October 31, 2014

, October 31, 2014") IAF Advisors Energy Market Outlook Kyle Cooper, (713) 722 7171, Kyle.Cooper@IAFAdvisors.com October 31, 2014 Price Action: The December contract rose 17.5 cents (4.7%) to $3.873 on a 33.3 cent range. Price

IAF Advisors Energy Market Outlook Kyle Cooper, (713) 722 7171, Kyle.Cooper@IAFAdvisors.com October 31, 2014 Price Action: The December contract rose 17.5 cents (4.7%) to $3.873 on a 33.3 cent range. Price

Outlook for the Oil and Gas Industry

Outlook for the Oil and Gas Industry VMA Market Outlook Workshop Boston, MA Spears& Associates Tulsa, OK August 2017 1 Outlook for the Oil and Gas Industry: Market Drivers Global oil consumption is forecast

Outlook for the Oil and Gas Industry VMA Market Outlook Workshop Boston, MA Spears& Associates Tulsa, OK August 2017 1 Outlook for the Oil and Gas Industry: Market Drivers Global oil consumption is forecast

ST98: 2018 ALBERTA S ENERGY RESERVES & SUPPLY/DEMAND OUTLOOK. Executive Summary.

ST98: 2018 ALBERTA S ENERGY RESERVES & SUPPLY/DEMAND OUTLOOK Executive Summary ST98 www.aer.ca EXECUTIVE SUMMARY The Alberta Energy Regulator (AER) ensures the safe, efficient, orderly, and environmentally

ST98: 2018 ALBERTA S ENERGY RESERVES & SUPPLY/DEMAND OUTLOOK Executive Summary ST98 www.aer.ca EXECUTIVE SUMMARY The Alberta Energy Regulator (AER) ensures the safe, efficient, orderly, and environmentally

ST98: 2018 ALBERTA S ENERGY RESERVES & SUPPLY/DEMAND OUTLOOK. Executive Summary.

ST98: 2018 ALBERTA S ENERGY RESERVES & SUPPLY/DEMAND OUTLOOK Executive Summary ST98 www.aer.ca EXECUTIVE SUMMARY The Alberta Energy Regulator (AER) ensures the safe, efficient, orderly, and environmentally

ST98: 2018 ALBERTA S ENERGY RESERVES & SUPPLY/DEMAND OUTLOOK Executive Summary ST98 www.aer.ca EXECUTIVE SUMMARY The Alberta Energy Regulator (AER) ensures the safe, efficient, orderly, and environmentally

Regional Gas Market Update

April 26, 2018 Milford, MA Regional Gas Market Update Presentation to: ISO-NE Planning Advisory Committee Tom Kiley Northeast Gas Association 1 Topic Areas Natural gas safety message. Recent market growth,

April 26, 2018 Milford, MA Regional Gas Market Update Presentation to: ISO-NE Planning Advisory Committee Tom Kiley Northeast Gas Association 1 Topic Areas Natural gas safety message. Recent market growth,

U.S. Natural Gas Market Dynamics

U.S. Natural Gas Market Dynamics University of Houston Global Energy Management Institute The Future of the Gulf Coast Petrochemical Industry Michael Speltz April 29, 2005 ChevronTexaco 2002 Legal Disclaimer

U.S. Natural Gas Market Dynamics University of Houston Global Energy Management Institute The Future of the Gulf Coast Petrochemical Industry Michael Speltz April 29, 2005 ChevronTexaco 2002 Legal Disclaimer

Energy Prospectus Group

Energy Prospectus Group Founded in 2001 Current Membership is 530 We have members in 38 states and eight countries ~ 60% of our members live in Texas Mission is to help our members make money Luncheons

Energy Prospectus Group Founded in 2001 Current Membership is 530 We have members in 38 states and eight countries ~ 60% of our members live in Texas Mission is to help our members make money Luncheons

U.S. Historical and Projected Shale Gas Production

U.S. Historical and Projected Shale Gas Production Phyllis Martin Phyllis Martin, Senior Energy Analyst Office of Petroleum, Gas and Biofuels Analysis U.S. Energy Information Administration phyllis.martin@eia.doe.gov

U.S. Historical and Projected Shale Gas Production Phyllis Martin Phyllis Martin, Senior Energy Analyst Office of Petroleum, Gas and Biofuels Analysis U.S. Energy Information Administration phyllis.martin@eia.doe.gov

Power & Politics Navigating the Changing Vision of Our Energy Future. Rayola Dougher, API Senior Economic Advisor,

Power & Politics Navigating the Changing Vision of Our Energy Future Rayola Dougher, API Senior Economic Advisor, dougherr@api.org U.S. oil and natural gas production is increasing as a result of technological

Power & Politics Navigating the Changing Vision of Our Energy Future Rayola Dougher, API Senior Economic Advisor, dougherr@api.org U.S. oil and natural gas production is increasing as a result of technological

North American Natural Gas Market Outlook

North American Natural Gas Market Outlook Energy Trends & Impacts On Gas Infrastructure Prepared For: Gas/Electric Partnership, Conference XVIII Darryl Rogers February 10, 2010 Agenda Introduction to Purvin

North American Natural Gas Market Outlook Energy Trends & Impacts On Gas Infrastructure Prepared For: Gas/Electric Partnership, Conference XVIII Darryl Rogers February 10, 2010 Agenda Introduction to Purvin

Natural Gas, Liquids and Crude Oil Market Outlook North America 2012 and Beyond

Natural Gas, Liquids and Crude Oil Market Outlook North America 2012 and Beyond August 14th, 2012 On behalf of: for: 1 BENTEK Energy Market Information Agenda: U.S. Supply, Demand and Storage Outlook Macro

Natural Gas, Liquids and Crude Oil Market Outlook North America 2012 and Beyond August 14th, 2012 On behalf of: for: 1 BENTEK Energy Market Information Agenda: U.S. Supply, Demand and Storage Outlook Macro

OUR CONVERSATION TODAY

OUR CONVERSATION TODAY Our goal is to raise the level of awareness around the natural gas supply chain among key stakeholders in order to facilitate positive working relationships and more informed decision

OUR CONVERSATION TODAY Our goal is to raise the level of awareness around the natural gas supply chain among key stakeholders in order to facilitate positive working relationships and more informed decision

Contemplations about the future of natural gas: the good, the bad and the ugly

Contemplations about the future of natural gas: the good, the bad and the ugly Charles F. Mason H.A. True Chair in Petroleum and Natural Gas Economics Department of Economics Associate Dean, College of

Contemplations about the future of natural gas: the good, the bad and the ugly Charles F. Mason H.A. True Chair in Petroleum and Natural Gas Economics Department of Economics Associate Dean, College of